UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the fiscal year ended

or

For the transition period from _______________ to ____________________

Commission file number:

(Exact Name of Registrant as Specified in Its Charter)

| ||

(State or Other Jurisdiction of | (I.R.S. Employer Identification No.) | |

Incorporation or Organization) | ||

(Address of Principal Executive Offices) | (Zip Code) |

Registrant’s telephone number, including area code (

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ◻

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ◻

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Accelerated filer ◻ | |

Non-accelerated filer ◻ | Smaller reporting company |

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ◻

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

The aggregate market value of the 255,723 shares of Seaboard common stock held by nonaffiliates was approximately $

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates information by reference to the registrant’s definitive proxy statement, to be filed with the Securities and Exchange Commission within 120 days after the close of the fiscal year ended December 31, 2019.

SEABOARD CORPORATION

FORM 10-K

YEAR ENDED DECEMBER 31, 2019

TABLE OF CONTENTS

Part I | Page | |

Item 1 | 2 | |

Item 1A | 6 | |

Item 1B | 12 | |

Item 2 | 12 | |

Item 3 | 13 | |

Item 4 | 13 | |

Part II | ||

Item 5 | 14 | |

Item 6 | 15 | |

Item 7 | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 16 |

Item 7A | 25 | |

Item 8 | 27 | |

27 | ||

29 | ||

30 | ||

31 | ||

32 | ||

33 | ||

Item 9 | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 63 |

Item 9A | 63 | |

Item 9B | 65 | |

Part III | ||

Item 10 | 65 | |

Item 11 | 65 | |

Item 12 | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 65 |

Item 13 | Certain Relationships and Related Transactions, and Director Independence | 65 |

Item 14 | 65 | |

Part IV | ||

Item 15 | 65 | |

Item 16 | 68 | |

69 | ||

PART I

Forward-looking Statements

This report, including information included or incorporated by reference in this report, contains certain forward-looking statements with respect to the financial condition, results of operations, plans, objectives, future performance and business of Seaboard Corporation and its subsidiaries (“Seaboard”). Forward-looking statements generally may be identified as statements that are not historical in nature and statements preceded by, followed by or that include the words “believes,” “expects,” “may,” “will,” “should,” “could,” “anticipates,” “estimates,” “intends” or similar expressions.

In more specific terms, forward-looking statements include, without limitation:

| ● | statements concerning the projection of revenues, income or loss, capital expenditures, capital structure or other financial items; |

| ● | statements regarding the plans and objectives of management for future operations; |

| ● | statements of future economic performance; |

| ● | statements regarding the intent, belief or current expectations of Seaboard and its management with respect to: |

| (i) | Seaboard’s ability to obtain adequate financing and liquidity; |

| (ii) | the price of feed stocks and other materials used by Seaboard; |

| (iii) | the sale price or market conditions for pork, agricultural commodities, sugar, alcohol, turkey and other products and services; |

| (iv) | the recorded tax effects under certain circumstances and changes in tax laws; |

| (v) | the volume of business and working capital requirements associated with the competitive trading environment for the Commodity Trading and Milling (CT&M) segment; |

| (vi) | the charter hire rates and fuel prices for vessels; |

| (vii) | the fuel costs and related spot market prices in the Dominican Republic; |

| (viii) | the effect of the fluctuation in foreign currency exchange rates; |

| (ix) | the profitability or sales volume of any of Seaboard’s segments; |

| (x) | the anticipated costs and completion timetables for Seaboard’s scheduled capital improvements, acquisitions and dispositions; |

| (xi) | the productive capacity of facilities that are planned or under construction, and the timing of the commencement of operations at such facilities; or |

| (xii) | other trends affecting Seaboard’s financial condition or results of operations, and statements of the assumptions underlying or relating to any of the foregoing statements. |

This list of forward-looking statements is not exclusive. Seaboard undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events, changes in assumptions or otherwise, except as required by law. Forward-looking statements are not guarantees of future performance or results. They involve risks, uncertainties and assumptions. Actual results may differ materially from those contemplated by the forward-looking statements due to a variety of factors. The information contained in this Form 10-K and in other filings Seaboard makes with the Securities and Exchange Commission (the “SEC”), including without limitation, the information under the items “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Form 10-K, identifies important factors which could cause such differences.

1

Item 1. Business

General Development of Business

Seaboard Corporation was originally founded in 1918 as a flour brokerage business and was organized as a Delaware corporation in 1946. Seaboard Corporation and its subsidiaries (collectively, “Seaboard”) together comprise a diverse global agribusiness and transportation company. In the United States (“U.S.”), Seaboard is primarily engaged in hog production, pork processing and ocean transportation. Overseas, Seaboard is primarily engaged in commodity merchandising, grain processing, sugar and alcohol production and electric power generation. Seaboard also has an equity method investment in Butterball, LLC (“Butterball”), a producer and processor of branded and non-branded turkey products. See Note 15 to the consolidated financial statements for specific developments for each segment.

Approximately 77% of the outstanding common stock of Seaboard is collectively owned by Seaboard Flour LLC and SFC Preferred, LLC. Mr. Steven J. Bresky, President and Chief Executive Officer of Seaboard, and other members of the Bresky family, including trusts created for their benefit, own the equity interests of Seaboard Flour LLC and SFC Preferred, LLC, which are Delaware limited liability companies.

Description of Business

Principal Products and Services

Pork Segment – Seaboard, through its subsidiary Seaboard Foods LLC, engages in the business of hog production and pork processing in the U.S. Seaboard’s Pork segment is a vertically integrated pork producer that primarily produces and sells fresh and frozen pork products to further processors, foodservice operators, distributors and grocery stores. This segment sells to U.S. customers and exports to Japan, Mexico, China and numerous other foreign markets. Pork products include fresh pork, such as loins, tenderloins and ribs which are primarily sold to distributors and grocery stores and fresh and frozen pork products sold in bulk to further processors who produce products, such as lunchmeat, ham, bacon and sausage.

This segment’s pork processing plant, located in Guymon, Oklahoma, generally operates at a double-shift processing capacity of approximately six million hogs annually. Seaboard also has a ham boning and processing plant in Mexico. In 2019, Seaboard raised approximately 88% of the hogs processed at its processing plant, with the remaining hog requirements purchased primarily under contracts from independent producers. Seaboard’s hog production facilities consist of genetic and commercial breeding, farrowing, nursery and finishing buildings located in the Central U.S. These facilities have capacity to produce approximately eight million hogs annually.

The Pork segment also produces biodiesel at facilities in Oklahoma and Missouri. Biodiesel is produced from pork fat supplied by the Oklahoma pork processing plant and from other animal fats and vegetable oils purchased from third parties. The biodiesel is sold to fuel blenders for distribution. In 2019, the Pork segment purchased and began modifying an idle ethanol plant in Hugoton, Kansas, that it plans to use to produce renewable diesel in the future. The Kansas plant is expected to produce 85 million gallons of renewable diesel annually when operating at full capacity.

Seaboard has a 50% noncontrolling interest in Seaboard Triumph Foods, LLC (“STF”), which operates a pork processing plant located in Sioux City, Iowa. STF began single-shift operations in September 2017 and a second shift commenced in October 2018. STF’s plant is designed to process approximately six million market hogs annually when operating at full capacity. Seaboard has agreements with STF and Triumph Foods, LLC (“Triumph”), an independent pork processor, to market substantially all pork products produced at STF’s and Triumph’s pork processing plants. Seaboard and Triumph supply a portion of the hogs processed at the STF plant. Seaboard’s revenues for its pork products are primarily based on a margin sharing arrangement that considers the average sales price, standard costs and the mix of products sold from the Seaboard and Triumph pork processing plants. The Pork segment also has a 50% noncontrolling interest in Daily’s Premium Meats, LLC (“Daily’s”). Daily’s produces and markets raw and pre-cooked bacon using pork bellies sourced from Seaboard, Triumph and STF.

Commodity Trading and Milling Segment – Seaboard’s CT&M segment, which is managed under the name of Seaboard Overseas and Trading Group, is an integrated agricultural commodity trading, processing and logistics company. Overall, the CT&M segment has facilities in 29 countries, primarily in Africa, South America and the Caribbean. This segment sources, transports and markets approximately 13 million metric tons per year of wheat, corn, soybeans, soybean meal and other commodities. Also, Seaboard and its affiliates produce approximately six million metric tons of wheat flour, maize meal, manufactured feed and oilseed crush commodities per year in addition to other related grain-based products. This segment owns three vessels, but the majority of the trading business is transacted with chartered ships.

2

Marine Segment – Seaboard, through its subsidiary, Seaboard Marine Ltd., and various foreign affiliated companies and third-party agents, provides cargo shipping services in the U.S. and 26 countries in the Caribbean and Central and South America. The Marine segment’s primary operations are at PortMiami and include a terminal and an off-port warehouse for cargo consolidation and temporary storage. At the Port of Houston, this segment operates a cargo terminal facility that includes on-dock warehouse space for temporary storage of bagged grains, resins and other cargoes. Seaboard also makes scheduled vessel calls to Brooklyn, New Orleans, Philadelphia, Savannah and various ports in the Caribbean and Central and South America. The Marine segment uses a network of offices and agents throughout the U.S., Canada, the Caribbean and Central and South America to sell freight services. Seaboard’s capabilities allow transport by truck or rail of import and export cargo to and from various U.S. ports and foreign ports. This segment’s fleet consists of 22 chartered and 3 owned vessels, and includes dry, refrigerated and specialized containers and other cargo related equipment.

Sugar and Alcohol Segment – Seaboard, through its subsidiary, Seaboard Energías Renovables y Alimentos S.R.L., operates a vertically integrated sugar and alcohol production facility in Argentina. Sugarcane grown on owned land supplies most of the raw material processed in its plant. The sugar is primarily marketed locally, with some exports to the U.S. and other countries. The alcohol is primarily marketed to industrial users or sold as dehydrated alcohol to certain oil companies under the Argentine governmental bioethanol program, which requires alcohol to be blended with gasoline. This segment also owns a 51 megawatt cogeneration power plant, which is fueled by the burning of sugarcane by-products, natural gas and other biomass when available.

Power Segment – Seaboard, through its subsidiary, Transcontinental Capital Corp. (Bermuda) Ltd., is an independent power producer generating electricity for the Dominican Republic power grid. Seaboard’s Power segment owns and operates a power generating barge, located on the Ozama River, that contains a system of engines capable of using natural gas or heavy fuel oil to produce up to 108 megawatts of electricity. Seaboard’s Power segment sells the electricity it generates primarily on the spot market to government-owned distribution companies. It is not directly involved in the transmission or distribution of electricity and is exempt from regulations under the Public Utility Holding Company Act of 1938, as amended. Seaboard’s Power segment is currently constructing a new floating power barge with capacity to generate approximately 146 megawatts of electricity using gaseous fuels, including natural gas. Operations are anticipated to begin in mid-2021. Seaboard is exploring strategic alternatives for the existing barge, including selling, relocating or operating in conjunction with the new barge at the current site. The estimated total cost of the project ranges from approximately $185 million to $210 million depending upon the alternative selected.

Turkey Segment – Seaboard has a 50% noncontrolling interest in Butterball, LLC (“Butterball”), a vertically integrated producer and processor of branded and non-branded conventional, antibiotic-free and organic turkey products. Butterball is a national supplier to retail stores, foodservice outlets and industrial entities, and to a lesser extent, exports products to Mexico and other foreign markets.

Other Businesses – Seaboard, through its subsidiary, Mount Dora Farms Inc., processes jalapeño peppers at its plant in Honduras, which are primarily shipped to and sold in the U.S.

The information required by this item with respect to the amount or percentage of total revenue contributed by any class of similar products or services, which account for 10% or more of consolidated revenue in any of the last three fiscal years, is set forth in Note 15 to the consolidated financial statements.

Sources and Availability of Raw Materials

The Power segment and Turkey segment utilize material amounts of raw materials that are dependent on purchases from one supplier or a small group of dominant suppliers. The Power segment has one primary supplier of natural gas, but the barge can run on other types of fuel. The Turkey segment purchases a significant portion of its feed and grain used in the manufacturing of feed for its turkeys in North Carolina from Seaboard’s 50% partner in Butterball.

Patents, Trademarks, Licenses, Franchises and Concessions

Seaboard believes there is significant recognition of the trademarks identified below in the various industries Seaboard serves and by many of its customers. Seaboard uses the trademark of Seaboard™.

The Pork segment uses registered trademarks including, but not limited to, Seaboard Foods®, Seaboard Farms®, Seaboard EnergyTM, Prairie Fresh®, Our Farms, Our Commitment®, St. Joe Pork®, and Cook-in Bag®. Daily’s uses the trademarks Daily’s®, Daily’s Premium Meats Since 1893®, Belly Up to the Best®, Buffet Brand® and Del Pueblo®. Seaboard considers the use of these trademarks important to the marketing and promotion of its pork products.

3

The CT&M segment uses registered trademarks including, but not limited to, Mothers Pride® and Zambia’s Pride® in Zambia, Thunderbolt Flour® and Maid Marian® in Guyana, GMA® and Top Pain® in Ivory Coast, and GMD® and Jarga® in Senegal.

The Marine segment uses the registered trademarks of Seaboard Marine® and Seaboard Solutions®.

The Sugar and Alcohol segment markets sugar under the Chango® brand.

The Turkey segment uses registered trademarks including, but not limited to, Butterball®, Carolina Turkey® and Farm to Family Butterball®. Seaboard considers the use of these trademarks important to marketing and promotion of its turkey products.

Seasonal Business

The Turkey business is seasonal for whole birds and related products with the Thanksgiving and Christmas holiday demands driving the majority of those sales. Seaboard’s other segments are not seasonally dependent to any material extent.

Dependence on a Single Customer or Few Customers

Seaboard does not have sales to any one customer equal to 10% or more of consolidated revenues. The CT&M segment derived 11% and 12% of its sales from a former non-consolidated affiliate for the years ended December 31, 2018 and 2017, respectively. Additional equity interests were obtained in 2019 and as a result, this entity became consolidated in 2019. The Sugar and Alcohol segment derived 25%, 29% and 39% of its sales from one customer for the years ended December 31, 2019, 2018 and 2017, respectively, and another customer represented 23%, 19% and 10% of its sales for the years ended December 31, 2019, 2018 and 2017, respectively. The Power segment sells power in the Dominican Republic on the spot market accessed primarily by three wholly government-owned distribution companies. The Turkey segment had one customer that represented 16%, 15% and 13% of its sales for the years ended December 31, 2019, 2018 and 2017, respectively, and another customer that represented 12%, 11% and 11% of its sales for the years ended December 31, 2019, 2018 and 2017, respectively. No other segment has sales to a few customers that, if lost, would have a material adverse effect on any such segment or on Seaboard taken as a whole.

Competitive Conditions

Competition in Seaboard’s Pork segment comes from a variety of regional, national and international producers and processors and is based primarily on product quality, customer service and price. According to the trade publications Successful Farming and Informa Economics, Seaboard was ranked number three in hog production (based on sows in production) and number four in pork processing in the U.S. in 2019 (based on daily processing capacity, including Triumph’s and STF’s capacity).

Seaboard’s commodity trading business faces competition from numerous traders around the world. Most of the grain processing and related businesses face competition from either imported products or other local producers in the same industries.

Seaboard’s Marine segment faces competition based on price, reliable sailing frequencies and customer service. Seaboard believes it is among the top five ranking ocean liner services for cargoes in the Caribbean and Central America based on cargo volume.

Seaboard’s Sugar and Alcohol segment owns one of the largest sugar mills in Argentina and faces significant competition for sugar sales in the local Argentine market. Sugar prices in Argentina can fluctuate compared to world markets due to Argentine government price controls and protection policies.

Seaboard’s Power segment sells the power it generates to the spot market or to contract customers at prices based on market conditions and cost-based rates.

Competition for the Turkey segment comes from a variety of regional and national producers and processors and is based primarily on product quality, customer service and price. Butterball ranks as one of the nation’s top three turkey producers based on live production.

Environmental Compliance

Seaboard’s Pork segment and Turkey segment are subject to numerous federal, state and local laws and regulations relating to the environment that require the expenditure of funds in the ordinary course of business. Seaboard’s Pork segment and Turkey segment do not anticipate making expenditures for these purposes that, in the aggregate, would have a material effect on Seaboard’s financial condition or results of operations.

4

Number of Persons Employed by Registrant

At the time of this report, Seaboard, excluding non-consolidated affiliates, had approximately 13,100 employees, of whom approximately 6,600 were employed in the U.S.

Available Information

Seaboard electronically files with the SEC annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports pursuant to Section 13(a) or 15(d) of the Exchange Act. The SEC maintains an internet website that contains reports, proxy and information statements, and other information regarding electronic filers at http://www.sec.gov. Seaboard provides access to its most recent Form 10-K, 10-Q and 8-K reports, and any amendments to these reports, on its internet website, www.seaboardcorp.com, free of charge, as soon as reasonably practicable after those reports are electronically filed with the SEC. Please note that any internet addresses provided in this report are for information purposes only and are not intended to be hyperlinks. Accordingly, no information provided at such internet addresses is intended or deemed to be incorporated herein by reference.

Executive Officers of the Registrant

The following table lists the executive officers of Seaboard. Generally, executive officers are elected at the annual meeting of the Board of Directors following the Annual Meeting of Stockholders and hold office until the next such annual meeting or until their respective successors are duly chosen and qualified. There are no arrangements or understandings pursuant to which any executive officer was elected.

Name (Age) |

| Positions and Offices with Registrant and Affiliates |

Steven J. Bresky (66) | President and Chief Executive Officer | |

Robert L. Steer (60) | Executive Vice President, Chief Financial Officer | |

David M. Becker (58) | Senior Vice President, General Counsel and Secretary | |

James L. Gutsch (66) | Senior Vice President, Engineering | |

Ralph L. Moss (74) | Senior Vice President, Governmental Affairs | |

David S. Oswalt (52) | Senior Vice President, Finance and Treasurer | |

David H. Rankin (48) | Senior Vice President, Tax and Business Development | |

Michael D. Trollinger (51) | Vice President, Corporate Controller and Chief Accounting Officer | |

Ty A. Tywater (50) | Vice President, Audit Services | |

Ivan J. Winfield, Jr (55) | Vice President, Information Technology | |

David M. Dannov (58) | President, Seaboard Overseas and Trading Group | |

Edward A. Gonzalez (54) | President, Seaboard Marine Ltd. | |

Darwin E. Sand (55) | President, Seaboard Foods LLC |

Mr. Bresky has served as President and Chief Executive Officer of Seaboard since July 2006.

Mr. Steer has served as Executive Vice President, Chief Financial Officer of Seaboard since April 2011.

Mr. Becker has served as Senior Vice President, General Counsel and Secretary of Seaboard since April 2011.

Mr. Gutsch has served as Senior Vice President, Engineering of Seaboard since April 2011.

Mr. Moss has served as Senior Vice President, Governmental Affairs of Seaboard since April 2011.

Mr. Oswalt has served as Senior Vice President, Finance and Treasurer since April 2013.

Mr. Rankin has served as Senior Vice President, Taxation and Business Development since April 2015 and previously as Vice President, Taxation and Business Development since April 2013.

Mr. Trollinger has served as Vice President, Corporate Controller and Chief Accounting Officer of Seaboard since March 2015. Prior to that, he served as Vice President, Finance and Operational Reporting for Jack Cooper Enterprises, Inc. from 2011 to 2015.

Mr. Tywater has served as Vice President, Audit Services of Seaboard since November 2008.

Mr. Winfield has served as Vice President, Information Technology since February 2018 and previously as Director of Information Technology from 2009 to 2018.

Mr. Dannov has served as President of Seaboard Overseas and Trading Group since August 2006.

Mr. Gonzalez has served as President of Seaboard Marine Ltd. since January 2005.

Mr. Sand has served as President of Seaboard Foods LLC since March 2018 and previously as Senior Vice President of Sales since 2011.

5

Item 1A. Risk Factors

Seaboard has identified important risks and uncertainties that could affect the results of operations, financial condition or business and that could cause them to differ materially from Seaboard’s historical results of operations, financial condition or business, or those contemplated by forward-looking statements made herein or elsewhere, by, or on behalf of, Seaboard. Factors that could cause or contribute to such differences include those factors described below.

| (a) | General |

| (1) | Seaboard’s Operations Are Subject to the General Risks of the Food Industry. The food products manufacturing industry is subject to the risks posed by: |

| ● | food spoilage; |

| ● | food contamination, including contamination caused by disease-producing organisms or pathogens, such as Listeria monocytogenes, Salmonella, pathogenic E coli and aflatoxin; |

| ● | food allergens; |

| ● | evolving consumer preferences and nutritional and health-related concerns; |

| ● | international, foreign, federal, state and local food processing regulations; |

| ● | consumer product liability claims; |

| ● | product recall; |

| ● | product tampering; and |

| ● | public perception of food production practices, including handling of production and live animals. |

Pathogens which may cause food contamination are found generally in livestock and in the environment and therefore may be present in Seaboard’s products. These pathogens also can be introduced to its products as a result of improper handling by customers or consumers. Seaboard does not have control over handling procedures once products have been shipped for distribution. If one or more of these risks were to materialize, Seaboard’s revenues could decrease, costs of doing business could increase, and Seaboard’s operating results could be adversely affected.

| (2) | International Operations Subject Seaboard to Risks That Could Have a Significant Impact on Seaboard’s Business. Seaboard is a diverse agribusiness and transportation company with global operations in several industries. Most of the sales and costs of Seaboard’s segments are significantly influenced by worldwide fluctuations in commodity prices or changes in foreign political and economic conditions. Accordingly, revenues, operating income and cash flows could fluctuate significantly from year to year. In addition, Seaboard’s international activities pose risks not faced by companies that limit themselves to U.S. markets. These risks include: |

| ● | changes in foreign currency exchange rates; |

| ● | foreign currency exchange controls; |

| ● | changes in a specific country’s or region’s political or economic conditions, particularly in emerging markets; |

| ● | hyperinflation; |

| ● | heightened customer credit and execution risk; |

| ● | tariffs, other trade protection measures and import or export licensing requirements; |

| ● | closing of borders by foreign countries to the import of meat products due to animal disease or other perceived health or safety issues; |

| ● | potentially negative consequences from changes in tax laws; |

| ● | legal and regulatory structures and unexpected changes in legal and regulatory requirements and any lawsuits that may arise; |

| ● | negative perception within a foreign country of a U.S. company doing business in that foreign country; |

| ● | compliance with laws and regulations for conducting international business such as Foreign Account Tax Compliance Act, Foreign Corrupt Practices Act and Office of Foreign Assets Control regulations; |

| ● | expropriation, civil unrest and government instability; and |

| ● | inconsistent application or enforcement of local laws, including tax laws. |

| (3) | Deterioration of Economic Conditions Could Negatively Impact Seaboard’s Business. Seaboard’s business may be adversely affected by changes in national or global economic conditions, including inflation, interest rates, including LIBOR phase-out risks, availability of capital markets, consumer spending rates, energy availability and costs, and the effects of governmental initiatives to manage economic conditions. Any such changes could adversely affect the demand for Seaboard’s meat products, grains, shipping services and other products, or the cost and availability of needed raw materials and packaging materials, thereby negatively affecting Seaboard’s financial results. The current national and global economic conditions, could, among other things: |

| ● | impair the financial condition of some of Seaboard’s customers and suppliers, thereby increasing customer bad debts or non-performance by customers and suppliers; |

6

| ● | negatively impact global demand for protein and grain-based products, which could result in a reduction of revenues, operating income and cash flows; |

| ● | decrease the value of Seaboard’s investments in equity and debt securities, including pension plan assets, causing losses that would adversely impact Seaboard’s net earnings; and |

| ● | impair the financial viability of Seaboard’s insurers. |

| (4) | Decentralization May Present Certain Risks. Seaboard’s operations are relatively decentralized in comparison with its peers. While Seaboard management believes this practice enables it to remain responsive to risks, opportunities and to customers’ needs, it necessarily places significant control and decision-making powers in the hands of local management. This presents various risks, including the risk that management may be slower or less able to identify or react to problems affecting a key business than in a more centralized environment. In addition, it means that Seaboard may be slower to detect compliance related problems (e.g., a rogue employee undertaking activities that are prohibited by applicable law or Seaboard’s internal policies) and that “company-wide” business initiatives, such as the integration of disparate information technology systems, are often more challenging and costly to implement, and their risk of failure higher, than they would be in a more centralized environment. Depending on the nature of the problem or initiative in question, such failure could materially adversely affect Seaboard’s business, financial condition or results of operations. |

| (5) | Ocean Transportation Has Inherent Risks. Seaboard’s owned and chartered vessels along with related cargoes are at risk of being damaged or lost because of events such as: |

| ● | bad weather; |

| ● | mechanical failures; |

| ● | grounding, fire, explosions and collisions; |

| ● | human error; and |

| ● | war, piracy and terrorism. |

Any of these hazards could result in death or injury to persons, loss of property, environmental damages, delays or rerouting. If one of Seaboard’s vessels were involved in an incident, the resulting negative public perception could have a material adverse effect on Seaboard’s business, financial condition and results of operations. Also, many aspects of the shipping industry are subject to extensive governmental regulations. Compliance with applicable laws, regulations and standards may require installation of costly equipment or operational changes, while the failure to comply may result in administrative and civil penalties, criminal sanctions, the suspension or termination of Seaboard’s operations or detention of its vessels.

| (6) | Fluctuations in Fuel Costs Could Adversely Affect Operating Margins. Fuel expenses are a large expense for the Marine segment and impacts the CT&M segment’s results. Fuel prices can vary greatly from year to year. While such fluctuations may be offset through fuel surcharges or other mechanisms, such mechanisms do not act with precision in terms of timing and amount and may not adjust revenues enough to offset the increase in costs. The reduced global sulfur emissions cap from 3.5% to 0.5%, effective January 1, 2020, increased fuel costs or required equipment to clean emissions. Seaboard does not know the long-term effects of this new emissions requirement. |

| (7) | Seaboard’s Common Stock Is Thinly Traded and Subject to Daily Price Fluctuations. The common stock of Seaboard is closely held and thinly traded on a daily basis on the NYSE American. Seaboard Flour LLC and SFC Preferred, LLC, which are beneficially owned by Mr. Steven Bresky, President and Chief Executive Officer of Seaboard, and other members of the Bresky family, hold approximately 77% of Seaboard’s outstanding common stock. Accordingly, the price of a share of common stock could fluctuate more significantly from day-to-day than that of a share of more widely held stock that is actively traded on a daily basis. |

| (8) | Seaboard Has Investments in Non-Consolidated Affiliates That Are Managed by Third Parties. Seaboard has several equity method investments in which it owns 50% or less, with various third-party business partners owning the remaining equity. Due to the ownership structure of these affiliates, Seaboard does not control all of the decision making processes and could be exposed to various business risks if the business partners’ business decisions do not align with Seaboard’s best interests, which could adversely impact the results for Seaboard’s income (loss) from affiliates. |

| (9) | Seaboard Is Increasingly Dependent on Information Technology Systems to Manage and Support a Variety of Business Processes and Activities. Seaboard may be adversely impacted if it is unable to protect its information technology systems against, or effectively respond to, cyber-attacks or cybersecurity breaches. Attempted cyber-attacks and other cyber incidents are occurring more frequently and are being made by groups and individuals with a wide range of motives and expertise. Any significant penetration, invasion, destruction, or interruption of these systems could negatively impact operations and there is a risk of business interruption and reputational damage from the unauthorized disclosure of confidential information and a risk of loss to financial assets related to manipulated electronic communications. This includes additional costs for increased security, system remediation and breach detection. If Seaboard is unable to prevent such breaches or failures, its operations could be disrupted or it could negatively impact its financial condition, results of operations, and the market price of its |

7

| common stock. |

| (b) | Pork Segment |

| (1) | Fluctuations in Commodity Pork Prices Could Adversely Affect the Results of Operations. Sales prices for this segment’s products are directly affected by both domestic and worldwide supply and demand for pork products and other proteins, all of which are determined by constantly changing market forces of supply and demand as well as other factors over which Seaboard has little to no control. Commodity pork prices demonstrate a cyclical nature over periods of years, reflecting changes in the supply of fresh pork and competing proteins on the market, especially beef and chicken. This segment’s results of operations could be adversely affected by fluctuations in pork commodity prices. |

| (2) | Increases in Costs of This Segment’s Feed Components and Third-Party Hog Purchases Could Adversely Affect Costs and Operating Margins. Feed costs are the most significant single component of the cost of raising hogs and could be materially affected by commodity price fluctuations for corn and soybean meal. The results of this segment could be negatively affected by increased costs of its feed components. The continued operation of ethanol plants has elevated this risk as it has increased the competing demand for feed ingredients, primarily corn. Approximately 12% of this segment’s slaughtered hogs are purchased from third parties, and commodity price fluctuations for hogs could have an impact on this segment’s total costs. The cost and supply of feed components and the third-party hogs that this segment purchases are determined by constantly changing market forces of supply and demand, which are driven by matters over which Seaboard has no control, including weather, current and projected worldwide grain stocks and prices, grain export prices and supports, and governmental agricultural policies. This segment attempts to manage certain of these risks through the use of financial instruments; however, this may also limit its ability to participate in gains from favorable commodity fluctuations. Unless wholesale pork prices correspondingly increase, increases in the prices of this segment’s feed components or in the cost of third-party hogs purchased would adversely affect Seaboard’s operating margins. |

| (3) | Seaboard May Be Unable to Obtain and Retain Appropriate Personnel. The remote locations of the pork processing plant and live hog operations and a more restrictive national policy on immigration could negatively affect the availability and cost of labor. This segment is dependent on having a sufficient number of properly trained operations personnel. Attracting and retaining qualified personnel is important to this segment’s success. The inability to acquire and retain the services of such personnel could have a material adverse effect on Seaboard’s operations. |

| (4) | The Loss of This Segment’s Oklahoma Pork Processing Plant Could Adversely Affect the Business. This segment is largely dependent on the continued operation of its Oklahoma pork processing plant. The loss of or damage to this plant for any reason, including fire, tornado or earthquake, or the occurrence of adverse governmental action could adversely affect the business of this segment. |

| (5) | Environmental Regulation and Related Litigation Could Have a Material Adverse Effect on the Business. This segment’s operations and properties are subject to extensive and increasingly stringent laws and regulations pertaining to, among other things, odors, the discharge of materials into the environment and the handling and disposition of wastes (including solid and hazardous wastes) or otherwise relating to protection of the environment. Failure to comply with these laws and regulations and any future changes to them could result in significant consequences to Seaboard, including civil and criminal penalties, liability for damages and negative publicity. Some requirements applicable to this segment may also be enforced by citizen groups. Seaboard has incurred, and will continue to incur, operating expenditures to comply with these laws and regulations. |

| (6) | Health Risk to Livestock Could Adversely Affect Production, the Supply of Raw Materials and the Business. Seaboard is subject to risks relating to its ability to maintain animal health and control diseases. The general health of the hogs and the reproductive performance of the sows could have an adverse impact on production and production costs, the supply of raw material to this segment’s pork processing operations and consumer confidence. If this segment’s hogs are affected by disease, Seaboard could be required to destroy infected livestock, which could adversely affect this segment’s production or ability to sell or export its products. Moreover, the herd health of third-party suppliers could adversely affect the supply and cost of hogs available for purchase. Adverse publicity concerning any disease or health concern could also cause customers to lose confidence in the safety and quality of this segment’s food products. |

| (7) | International Trade Barriers Could Adversely Affect This Segment’s Operations. This segment realizes revenues from international markets, particularly Japan, Mexico and China. International sales are subject to risks related to general economic conditions, imposition of tariffs, quotas, trade barriers and other restrictions, enforcement of remedies in foreign jurisdictions and compliance with applicable foreign laws, and other economic and political uncertainties. These and other risks have resulted in, and in the future may result in, border closings or other international trade barriers that could have an adverse effect on Seaboard’s earnings. |

| (8) | The Operating Profit of the Biodiesel Production Facilities Could Be Adversely Impacted by Various Factors. The profitability of this segment’s biodiesel plants could be adversely affected by various factors, including the market price of pork fat, other animal fats and vegetable oils, all of which are utilized to produce biodiesel, and the market price for biodiesel, which is influenced by world oil prices and U.S. government mandates and incentives to use biofuels. Unfavorable changes in these prices over extended periods of time or adverse changes in U.S. government mandates |

| and incentives to use biofuels could adversely affect this segment’s results of operations and could result in the potential impairment of the recorded value of the property, plant and equipment related to these facilities. Also, the federal blender’s credits are not permanent and may not be renewed beyond 2022. |

| (9) | Difficulties Could Be Experienced in the Conversion of the New Renewable Diesel Production Facility. In February 2019, the Pork segment purchased an idle ethanol plant in Kansas. Projected costs to convert the existing plant’s infrastructure to support the new renewable diesel production facility and the costs to construct the new portions of the renewable diesel plant are variable and could be higher than initially projected by the time the plant is operational. Also, significant construction delays could delay the expected timing of operations. |

| (c) | Commodity Trading and Milling Segment |

| (1) | This Segment Is Subject to Risks Associated with Foreign Operations. This segment principally operates in Africa, South America and the Caribbean and, in most cases, in what are generally regarded to be lesser-developed countries. Many of these foreign operations are subject to risks of doing business in lesser-developed countries, which are subject to potential civil unrest and government instability, increasing the exposure to potential expropriation, confiscation, war, insurrection, civil strife and revolution, corruption, currency inconvertibility and devaluation, and currency exchange controls. In addition, foreign government policies and regulations could restrict the purchase of various agricultural commodities and commodity products, reducing or limiting this segment’s ability to access materials or to limit this segment’s sales prices for products sold in local markets. |

| (2) | Fluctuations in Commodity Prices Could Adversely Affect the Business of This Segment. This segment’s sales are significantly affected by fluctuating worldwide prices for various commodities, such as wheat, corn, soybeans, soybean meal and, to a lesser degree, various other agricultural commodity products. These prices are determined by constantly changing market forces of supply and demand, as well as other factors over which Seaboard has little or no control. European flour exports, donated food aid, flour dumping practices and worldwide and local crop production could contribute to these fluctuating market conditions and could have a significant impact on the trading and milling businesses’ sales, value of commodities held in inventory and operating income. |

| (3) | This Segment Uses a Material Amount of Derivative Products to Manage Certain Market Risks. The commodity trading portion of this segment enters into various commodity derivative and foreign exchange derivative transactions to create what management believes is an economic hedge for commodity trades it executes or intends to execute with its customers. This portion of the segment also enters into speculative derivative transactions related to its market risks. Failure to execute or improper execution of a derivative position or a firmly committed sale or purchase contract or a speculative transaction that closes without the desired result or exposure to counter party risk could have an adverse impact on the results of operations and liquidity. |

| (4) | This Segment Is Subject to Higher Than Normal Risks for Attracting and Retaining Key Personnel. In the commodity trading environment, loss of a key employee such as a commodity trader could have a negative impact resulting from the loss of revenues as personal customer relationships can be vital to obtaining and retaining business with various foreign customers. In the milling portion of this segment, employing and retaining qualified expatriate personnel are key elements to success given the difficult living conditions, the unique operating environments and the reliance on a relatively small number of executives to manage each individual location. |

| (5) | This Segment Faces Increasing Competition. This segment is experiencing increasing competition in certain foreign markets by well-capitalized originators, traders of commodities making sales directly to end-use customers and industrial-asset owners that compete in the same markets as this segment. If various raw-material originators refuse to sell commodities to Seaboard for sale in these foreign markets, it could be more challenging for this segment to purchase commodities for sale to its customers at competitive prices. This segment’s sales volume and sale prices for commodities to customers, as well as results of operations, could be adversely impacted by such increased competition. |

| (d) | Marine Segment |

| (1) | The Demand for This Segment’s Services Are Affected by International Trade and Fluctuating Freight Rates. This segment provides cargo shipping services primarily from the U.S. to many different countries in the Caribbean and Central and South America. In addition to the risks of overseas operations, fluctuations in economic conditions and unstable or hostile local political situations in the countries in which this segment operates could affect trade volumes and cargo freight rates, as well as adversely affect this segment’s results of operations. |

| (2) | Chartered Ships Are Subject to Fluctuating Rates. Time-charter expenses are one of this segment’s largest expenses. Certain ships are under charters longer than one year while others are less than one year. These costs can vary greatly due to a number of factors including the worldwide supply and demand for shipping. It is not possible to determine in advance whether a charter contract for more or less than one year will be favorable to this segment’s business. Accordingly, entering into either long-term charter hire contracts during periods of decreasing charter hire costs or short-term charter hire contracts during periods of increasing charter hire costs could have an adverse effect on this segment’s results of operations. In an effort to improve cargo services on higher frequency routes and use more capacity, this segment purchases space, also known as slots, on certain third-party operated vessels. It is expected that this |

9

| segment will continue purchasing slots in the future, but these ship providers may not be reliable and cause shipment delays, damaged goods or other challenges. |

| (3) | Hurricanes May Disrupt Operations. This segment’s port operations can be subject to disruption due to hurricanes, especially at this segment’s major ports in Miami, Florida and Houston, Texas, which could have an adverse effect on this segment’s results of operations. |

| (4) | This Segment Is Subject to Complex Laws and Regulations That May Adversely Affect the Revenues, Costs, Manner or Feasibility of Doing Business. Federal, state and local laws and domestic and international regulations governing worker health and safety, environmental protection, port and terminal security, and the operation of vessels, including fuel regulations, significantly affect this segment’s operations, including rate discussions and other related arrangements. Many aspects of the shipping industry, including rate agreements and vessel cost sharing agreements, are subject to extensive governmental regulation by the Federal Maritime Commission, the U.S. Coast Guard, and U.S. Customs and Border Protection, as well as regulation by private industry organizations. Compliance with applicable laws, regulations and standards may require installation of costly equipment or operational changes, while the failure to comply may result in administrative and civil penalties, criminal sanctions, the suspension or termination of Seaboard’s operations or detention of its vessels. In addition, future changes in laws, regulations and standards, including allowed freight rate discussions and other related arrangements, may result in additional costs or a reduction in revenues. |

| (e) | Sugar and Alcohol Segment |

| (1) | The Success of This Segment Depends on the Condition of the Argentine Economy, Currency and Political Climate. This segment operates a sugar mill, alcohol production and power generation facility in Argentina. Fluctuations in economic conditions or changes in the Argentine political climate could have an impact on the costs of operations, the sales prices of products, export opportunities and the exchange rate of the Argentine peso to the U.S. dollar. In this regard, local sales prices for bioethanol are affected by government price controls and domestic prices for sugar are affected by import duties imposed by the Argentine government, impacting local volume sold, as well as imported and exported volumes to and from international markets. If import duties are changed, this could have a negative impact on the sales prices of this segment’s products. In addition, the majority of this segment’s sales are within Argentina, and any Argentine government attempts to control inflation through retail price controls on mass consumption products, including sugar, could adversely impact the local sales prices of this segment’s products and the results of operations for this segment. In the second quarter of 2018, Argentina was determined to be a highly inflationary economy. A devaluation of the Argentine peso would have a negative impact on this segment’s financial position and results of operations. |

| (2) | This Segment Is Subject to the Risks That Are Inherent in any Agricultural Business. Seaboard’s results of operations for this segment may be adversely affected by numerous factors over which Seaboard has little or no control and that are inherent in any agricultural business, including reductions in the market prices for this segment’s products, adverse weather and growing conditions, pest and disease problems, and new government regulations regarding agriculture and the marketing of agricultural products. Of these risks, weather particularly could adversely affect the amount and quality of the sugarcane produced by this segment and its competitors located in other regions of Argentina. |

| (3) | The Loss of This Segment’s Sole Processing Facility Would Adversely Affect the Business. This segment is largely dependent on the continued operation of a single sugar mill. The loss of or damage to this mill for any reason, including fire, tornado or earthquake, or the occurrence of adverse governmental action or labor unrest resulting in labor strikes could adversely affect the business of this segment. |

| (4) | Labor Relations Challenges Could Adversely Affect Operations. This segment is dependent on unionized labor at its single sugar mill in Argentina. The political and economic environment in Argentina makes normal labor relations very challenging. Contributing to the situation are the historical policies of Argentina’s government and the failure of the Argentine courts to enforce contractual obligations with unions and basic property rights. Interruptions in production as a result of labor unrest could adversely impact the quantity of sugarcane harvested and the amount of sugar, alcohol and power produced and could interfere with the distribution of products stored at the facility. |

| (5) | The Operating Profit of the Alcohol Production Facility Could Be Adversely Impacted by Government Regulations. The profitability of this segment’s alcohol production facility could be adversely affected by Argentine government regulations regarding production quotas, fuel blends and sales prices in the bioethanol market. In addition, corn alcohol producers in Argentina have increased competition in the bioethanol market. Adverse changes in the Argentine government’s regulations regarding bioethanol production quotas and fuel blends could adversely affect this segment’s results of operations. |

| (6) | The Operating Profit of the Cogeneration Power Plant Could Be Adversely Impacted by Contract for the Sale of Energy. The sale price for energy produced and sold by this segment’s cogeneration power plant is based on a biomass cogeneration contract with the Argentine government. The profitability of the cogeneration power plant could be adversely affected by this segment’s failure to enforce the terms of the contract, which could adversely affect this |

| segment’s results of operations and could result in the potential impairment of the recorded value of the property, plant and equipment related to this facility. |

| (f) | Power Segment |

| (1) | The Success of This Segment Depends on the Condition of the Dominican Republic Economy, Currency and Political Climate. Fluctuations in economic conditions or changes in the Dominican Republic political climate could have an impact on the costs of operations, the sales prices of products and the exchange rate of the Dominican peso to the U.S. dollar. In addition to significant currency fluctuations and the other risks of overseas operations, this segment could experience difficulty in obtaining timely collections of trade receivables from the government owned distribution companies or other companies that must also collect from the government in order to make payments on their accounts. Currently, the Dominican Republic does not allow a free market to enable prices to rise with demand, which could limit this segment’s profitability. The government has the ability to arbitrarily decide which power units will be able to operate, which can ultimately determine spot market prices for electricity generated and sold into the power grid and, therefore, could have adverse effects on results of operations. |

| (2) | Supply of Natural Gas Is Limited in the Dominican Republic. Supply of natural gas in the Dominican Republic is limited to one primary supplier. Although the barge can run on other types of fuel, supply disruptions of natural gas could have a negative impact on this segment’s operating income. |

| (3) | The Loss of This Segment’s Sole Facility Would Adversely Affect the Business. This segment is dependent on the continued operation of a single facility. The loss of or damage to this facility for any reason, including fire, hurricane, tornado or earthquake, or the occurrence of adverse governmental actions or labor unrest resulting in labor strikes would adversely affect the business of this segment. |

| (4) | Difficulties Could Be Experienced in the Construction and Installation of the New Power Generating Barge. The new power generating barge is being constructed in Singapore, with delivery to the Dominican Republic expected in late 2020. Installation and commissioning are anticipated to take several months, with commercial operations expected in mid-2021. Significant operational delays, plans for the existing barge or other difficulties encountered in the start-up of operations could have adverse effects on results of operations. |

| (g) | Turkey Segment |

| (1) | Fluctuations in Commodity Turkey Prices Could Adversely Affect the Results of Operations. Sales prices for turkey products are directly affected by both domestic and worldwide supply and demand for turkey products and other proteins, which are determined by constantly changing market forces of supply and demand as well as other factors over which Butterball has little or no control. Butterball’s results of operations and the value of Seaboard’s investment in Butterball could be adversely affected by fluctuations in turkey commodity prices. |

| (2) | Increases in Costs of Butterball’s Feed Components and Turkey Purchases Could Adversely Affect Costs and Operating Margins. Feed costs are the most significant single component of the cost of raising turkeys and could be materially affected by commodity price fluctuations for corn, soybean meal and other commodity grain inputs. Butterball’s results may be negatively affected by increased costs of the feed components. Butterball attempts to manage some of these risks through the use of financial instruments; however, this may also limit its ability to participate in gains from favorable commodity fluctuations. Unless wholesale turkey prices correspondingly increase, increases in the prices of Butterball’s feed components would adversely affect Butterball’s results of operations and the value of Seaboard’s investment in Butterball. |

| (3) | Adverse Operating Results Could Result in Need for Additional Investment. Butterball has third-party bank loan facilities that are secured by substantially all of the assets of Butterball. Adverse operating results could cause Butterball to default on such loan facilities, which could result in a significant adverse impact on Butterball’s financial position or result in Seaboard needing to increase its investment or provide financing to Butterball. |

| (4) | Decreased Perception of Value in the Butterball Brand and Changes in Consumer Preferences Could Adversely Affect Sales Quantity and Price of Butterball Products. Butterball is a premium brand name, built on a long history of offering a quality product that has been differentiated in the market. The value of the Butterball brand allows for sales of a higher unit price than other turkey products. In order to maintain this advantage, Butterball must continue to support the brand with successful marketing efforts and develop new products. Consumer product preferences continue to evolve as a result of, among other things, shifting consumer demographics; changes in consumer lifestyles; digital shopping patterns; and competitive product and pricing pressures. If Butterball’s products fail to meet consumer preferences, or Butterball fails to introduce new products or product extensions on a timely basis, the brand value could diminish significantly. In addition, negative news reports for any reason related to Butterball or the turkey/poultry industry could negatively impact this brand perception, Butterball’s results of operations and the value of Seaboard’s investment in Butterball. |

11

| (5) | The Loss of Butterball’s Primary Further Processing Facility Could Adversely Affect Butterball’s Business. Although Butterball has four processing plants and two further processing plants, Butterball is disproportionately dependent on the continued operation of the processing plant in Mt. Olive, North Carolina, that handles a significant volume of the production of further processed turkey products. The loss of or damage to this plant for any reason, including fire, hurricane, tornado or the occurrence of an adverse governmental action could adversely affect the results of operations for Butterball and the value of Seaboard’s investment in Butterball. |

| (6) | Health Risk to Poultry Could Adversely Affect Production, the Supply of Raw Materials and Butterball’s Business. Butterball is subject to risks relating to its ability to maintain animal health and control diseases, such as avian influenza. The general health of the turkeys and reproductive performance could have an adverse impact on production and production costs, the supply of raw material to Butterball’s processing operations and consumer confidence. If Butterball’s turkeys are affected by disease, Butterball may be required to destroy infected birds, which could adversely affect Butterball’s production or ability to sell or export its products. Adverse publicity concerning any disease or health concern could also cause customers to lose confidence in the safety and quality of Butterball products, resulting in an adverse effect on Butterball’s results of operations and the value of Seaboard’s investment in Butterball. |

| (7) | Butterball May Be Unable to Obtain and Retain Appropriate Personnel. The remote locations of some of Butterball’s processing plants and live turkey operations, along with a more restrictive national policy on immigration, could negatively affect the availability and cost of labor. Butterball is dependent on having sufficient properly trained operations personnel. Attracting and retaining qualified personnel is important to Butterball’s success. The inability to acquire and retain the services of such personnel could have a material adverse effect on Butterball’s operations and the value of Seaboard’s investment in Butterball. |

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

Management believes that Seaboard’s present facilities are adequate and suitable for its current purposes. Seaboard’s principal properties by segment are described below:

(1) Pork — Seaboard’s Pork segment owns a pork processing plant in Guymon, Oklahoma. It has a double-shift capacity to process approximately six million hogs annually and generally operates at capacity with additional weekend shifts depending on market conditions. Seaboard’s hog production operations consist of the breeding and raising of approximately eight million hogs annually at facilities it primarily owns or at facilities owned and operated by third parties with whom it has grower contracts. This segment owns and operates seven centrally located feed mills, which have a combined capacity to produce approximately three million tons of formulated feed annually. These feed mills are used primarily to support Seaboard’s existing hog production and have the capability of supporting additional hog production in the future. These facilities are located in Iowa, Oklahoma, Texas, Kansas and Colorado. The Pork segment also operates a ham-boning and processing plant in Mexico that has the capacity to process 96 million pounds of ham annually. The Pork segment owns biodiesel plants in Oklahoma and Missouri, with the capacity to produce 46 million gallons and 30 million gallons, respectively, of biodiesel annually. In 2019, the Pork segment purchased and began modifying an idle ethanol plant in Hugoton, Kansas, that it plans to use to produce renewable diesel in the future. The Kansas plant is expected to produce 85 million gallons of renewable diesel annually when operating at full capacity.

(2) Commodity Trading and Milling — Seaboard’s CT&M grain-processing business, which includes 10 consolidated and 17 non-consolidated affiliates, operates facilities at 41 locations in 23 countries. Seaboard and its affiliates produce approximately six million metric tons of wheat flour, maize meal, manufactured feed and oilseed crush commodities per year in addition to other related grain-based products. The grain-processing and related agribusiness operations located in Botswana, Brazil, Colombia, the Democratic Republic of Congo, Ecuador, Gambia, Ghana, Guyana, Haiti, Jamaica, Kenya, Lesotho, Mauritania, Morocco, Mozambique, Nigeria, Peru, Republic of Congo, South Africa, Turkey, and Zambia own their facilities; and in Ivory Coast, Kenya, Lesotho, Morocco, Mozambique, Nigeria, Republic of Congo, Senegal and Zambia, the land on which certain facilities are located is leased under long-term agreements. Certain foreign milling operations may operate at less than full capacity due to low demand, poor consumer purchasing power, excess milling capacity in their competitive environment or imported flour. The commodity trading business has 13 offices in 12 countries, in addition to two non-consolidated affiliates in two other countries. Seaboard’s CT&M segment owns three 18,900 metric ton deadweight dry bulk vessels and charters between 30 and 59 bulk vessels with deadweights ranging from 5,000 to 64,000 metric tons under short-term agreements. Also, the CT&M segment charters four dry bulk vessels, each with a deadweight of 28,000 metric tons, which were originally purchased and then subsequently sold and leased-back.

(3) Marine — Seaboard’s Marine segment leases approximately 297,000 square feet of off-port warehouse space and approximately 86 acres of port terminal land and facilities in Miami, Florida, which are used in its containerized cargo

12

operations. Seaboard’s Marine segment also leases an approximately 62-acre cargo handling and terminal facility in Houston, Texas, which includes several on-dock warehouses totaling approximately 690,000 square feet for cargo storage. As of December 31, 2019, the Marine segment owned three ocean cargo vessels with deadweights ranging from 7,700 to 11,000 metric tons. In addition, this segment chartered 22 vessels under contracts ranging from less than one year to over two years with deadweights ranging from approximately 8,500 to 34,700 metric tons but has also entered into some contracts for longer-term charters that range up to 11 years. Seaboard’s Marine segment owns or leases dry, refrigerated and specialized containers and other related equipment.

(4) Sugar and Alcohol — Seaboard’s Sugar and Alcohol segment owns nearly 70,000 acres of planted sugarcane and a sugar mill with an annual capacity to crush approximately three million metric tons of sugar cane. The facility, including an alcohol distillery, has an annual production capacity of approximately 250,000 metric tons of sugar and approximately 33 million gallons of alcohol. This capacity is sufficient to process all of the cane harvested by this segment and additional quantities purchased from third-party farmers in the region. The sugarcane fields, processing mill, distillery and 51 megawatt cogeneration power plant are located in northern Argentina in the Salta Province. This area experiences seasonal rainfalls that may limit the harvest season, which then affects the duration of mill operations and quantities of sugar and alcohol produced.

(5) Power — Seaboard’s Power segment owns one power generating barge with capacity to generate approximately 108 megawatts of electricity that is secured on the Ozama River in Santo Domingo, Dominican Republic. Seaboard’s Power segment is currently constructing a new floating power barge with capacity to generate approximately 146 megawatts of electricity using gaseous fuels, including natural gas.

(6) Turkey — Seaboard’s Turkey segment has a total of four processing plants, two further processing plants and numerous company and third-party live production facilities and feed milling operations, located in North Carolina, Arkansas, Missouri and Kansas. These facilities produce over one billion pounds of turkey each year. Although capacity to meet core further processing demand is sufficient, Butterball uses third-party copack arrangements to supplement portions of its portfolio where it either does not maintain competencies, or to meet demand beyond its internal production capacity.

Item 3. Legal Proceedings

The information required by this item is included in Note 9 to the consolidated financial statements.

Item 4. Mine Safety Disclosures

Not Applicable.

13

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Seaboard’s common stock is traded on the NYSE American under the symbol SEB. Seaboard had 2,308 stockholders of record of its common stock as of January 31, 2020.

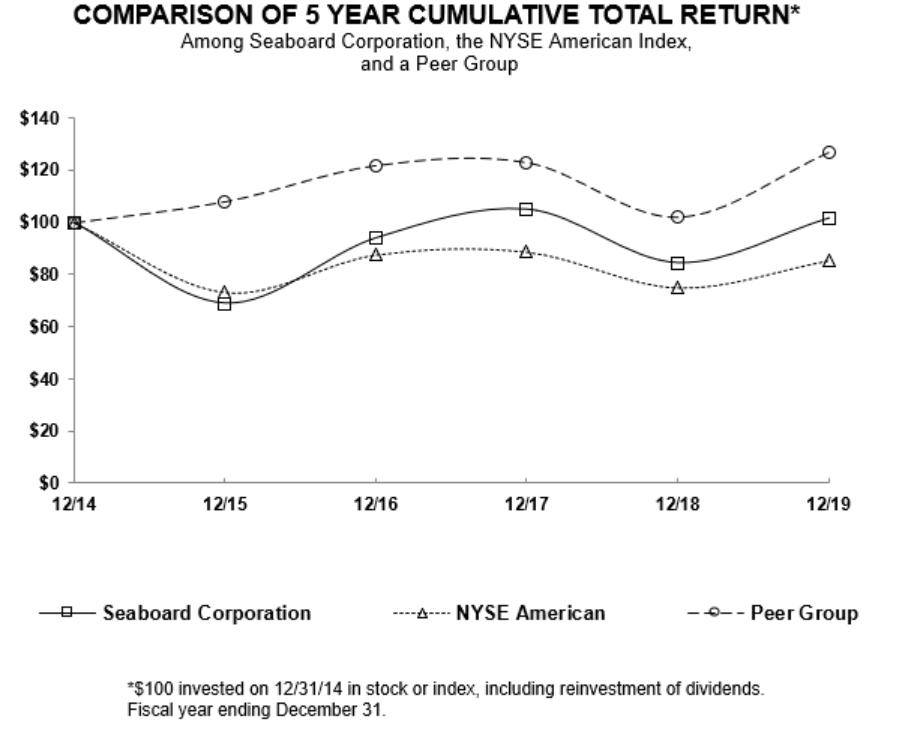

Stock Performance Chart

The SEC requires a five-year comparison of stock performance for Seaboard with that of an appropriate broad equity market index and similar industry index. Since there is no single industry index to compare stock performance, the companies comprising the Dow Jones U.S. Food Products and Dow Jones U.S. Marine Transportation Industry indices (the “Peer Group”) were chosen as the second comparison.

The following graph shows a five-year comparison of cumulative total return for Seaboard Corporation, the NYSE American Index and the companies comprising the Peer Group, weighted by market capitalization for the five fiscal years commencing December 31, 2014 and ending December 31, 2019.

The comparison of cumulative total returns presented in the above graph was plotted using the following index values and common stock price values:

| 12/31/14 |

| 12/31/15 |

| 12/31/16 |

| 12/31/17 |

| 12/31/18 |

| 12/31/19 |

| |||||||

Seaboard Corporation | $ | 100.00 | $ | 68.96 | $ | 94.14 | $ | 105.21 | $ | 84.54 | $ | 101.79 | |||||||

NYSE American | $ | 100.00 | $ | 73.17 | $ | 87.62 | $ | 88.68 | $ | 74.91 | $ | 85.42 | |||||||

Peer Group | $ | 100.00 | $ | 107.99 | $ | 121.71 | $ | 122.82 | $ | 102.13 | $ | 126.73 | |||||||

14

In each of the four quarters of 2019, Seaboard declared and paid quarterly dividends of $2.25 per share of common stock. In each of the four quarters of 2018 and 2017, Seaboard declared and paid quarterly dividends of $1.50 per share of common stock. Seaboard’s Board of Directors intends that Seaboard will continue to pay quarterly dividends for the reasonably foreseeable future, with the amount of any dividends being dependent upon such factors as Seaboard’s financial condition, results of operations and current and anticipated cash needs, including capital requirements. As discussed in Note 8 to the consolidated financial statements, Seaboard’s ability to declare and pay dividends is subject to limitations imposed by debt agreements.

Seaboard has not established any equity compensation plans or individual agreements for its employees under which Seaboard common stock, or options, rights or warrants with respect to Seaboard common stock, may be granted.

As of December 31, 2019, Seaboard may repurchase up to $78 million of its common stock at market value from time to time in open market or privately negotiated purchases under its share repurchase program. There were no purchases made by or on behalf of Seaboard or any “affiliated purchaser” (as defined by applicable rules of the SEC) of shares of Seaboard’s common stock during the fourth quarter of the fiscal year covered by this report. See Note 12 to the consolidated financial statements for discussion of share repurchase activity during 2019.

Item 6. Selected Financial Data

Years ended December 31, | ||||||||||||||||

(Millions of dollars except per share amounts) |

| 2019 |

| 2018 |

| 2017 |

| 2016 |

| 2015 | ||||||

Net sales | $ | 6,840 | $ | 6,583 | $ | 5,809 | $ | 5,379 | $ | 5,594 | ||||||

Operating income | $ | 104 | $ | 209 | $ | 240 | $ | 230 | $ | 126 | ||||||

Net earnings (loss) attributable to Seaboard | $ | 283 | (b) | $ | (17) | (b) | $ | 247 | (b)(c) | $ | 312 | (b) | $ | 171 | (d) | |

Basic earnings (loss) per common share | $ | 242.78 | (b) | $ | (14.61) | (b) | $ | 211.01 | (b)(c) | $ | 266.50 | (b) | $ | 146.44 | (d) | |

Total assets | $ | 6,285 | (a) | $ | 5,307 | $ | 5,161 | $ | 4,755 | $ | 4,431 | |||||

Long-term debt, less current maturities | $ | 730 | $ | 739 | $ | 482 | $ | 499 | $ | 518 | ||||||

Stockholders’ equity | $ | 3,554 | $ | 3,329 | $ | 3,408 | $ | 3,175 | $ | 2,882 | ||||||

Dividends declared per common share (e) | $ | 9.00 | $ | 6.00 | $ | 6.00 | $ | — | $ | — | ||||||

| (a) | Total assets increased $496 million with the adoption of the new leasing guidance. See Note 1 to the consolidated financial statements for further information. |

| (b) | In 2019, net earnings attributable to Seaboard included other investment income of $225 million, which included $176 million of non-cash unrealized mark-to-market gains on short-term investments. Net earnings (loss) attributable to Seaboard for 2018, 2017 and 2016 included other investment income (losses) of $(152) million, $177 million and $69 million, respectively. |

| (c) | In 2017, Seaboard recorded $65 million of additional income tax expense, or $55.31 per common share, as a result of the December 22, 2017 enactment of the Tax Cuts and Job Act (the “2017 Tax Act”). The additional income tax expense included a provisional $112 million of additional federal tax, payable over eight years, associated with the mandatory deemed repatriation of permanently invested foreign profits, offset by an estimated reduction in deferred taxes resulting from the rate decrease from 35% to 21%. See Note 14 to the consolidated financial statements for further information on the 2017 Tax Act. |

| (d) | In the fourth quarter of 2015, Seaboard recorded interest income of $23 million, net of taxes ($31 million before taxes), or $19.49 per common share, for interest recognized on certain outstanding customer receivable balances in its Power segment. This interest income related to amounts determined to be collectible as of December 31, 2015, but previously had been considered uncollectable in prior years. This amount was fully collected by Seaboard in January 2016. |

| (e) | In 2017, Seaboard resumed declaring quarterly dividends. In December 2012, Seaboard declared and paid a dividend of $12.00 per common share. The amount of the dividend represented a prepayment of the annual 2013, 2014, 2015 and 2016 dividends ($3.00 per common share per year). Basic and diluted earnings per common share are the same for all periods presented. |

15

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

OVERVIEW

Sales and costs of Seaboard’s segments are significantly influenced by worldwide fluctuations in commodity prices and changes in foreign political and economic conditions. Accordingly, sales, operating income and cash flows can fluctuate significantly from year to year. As each segment operates in a distinct industry and a different geographic location, management evaluates their operations separately. Seaboard’s reporting segments are based on information used by Seaboard’s Chief Executive Officer to determine allocation of resources and assess performance, in his capacity as chief operating decision maker.

Pork Segment

The Pork segment primarily produces hogs to process and sells fresh and frozen pork products to further processors, foodservice operators, distributors and grocery stores throughout the U.S. and to foreign markets. This segment also produces biodiesel from pork fats and other animal fat and vegetable oils for sale to third parties. Sales prices are directly affected by both domestic and worldwide supply and demand for pork products and other proteins. Feed accounts for the largest input cost in raising hogs and is materially affected by price changes for corn and soybean meal. Market prices for hogs purchased from third parties for processing at the plant also represent a major cost factor. Within the portfolio of Seaboard’s businesses, management believes profitability of the Pork segment is most susceptible to commodity price fluctuations. As a result, this segment’s operating income and cash flows can materially fluctuate from year to year, significantly affecting Seaboard’s consolidated operating income and cash flows. This segment is Seaboard’s most capital-intensive segment, representing approximately 53% of Seaboard’s total fixed assets, in addition to approximately 41% of total inventories. With the plant generally operating at capacity, Seaboard is continually looking for ways to enhance the plant’s operational efficiency, while also looking to increase margins by introducing new, higher value products.

CT&M Segment