Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

(Mark One)

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2018

or

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 001-10932

WisdomTree Investments, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 13-3487784 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

| 245 Park Avenue, 35th Floor New York, New York |

10167 | |

| (Address of principal executive officers) | (Zip Code) |

212-801-2080

(Registrant’s Telephone Number, Including Area Code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☒ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of November 2, 2018, there were 153,036,126 shares of the registrant’s Common Stock, $0.01 par value per share, outstanding.

Table of Contents

WISDOMTREE INVESTMENTS, INC.

Form 10-Q

For the Quarterly Period Ended September 30, 2018

2

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains forward-looking statements that are based on our management’s beliefs and assumptions and on information currently available to our management. Although we believe that the expectations reflected in these forward-looking statements are reasonable, these statements relate to future events or our future financial performance, and involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continue” or the negative of these terms or other comparable terminology. These statements are only predictions. You should not place undue reliance on forward-looking statements because they involve known and unknown risks, uncertainties and other factors, which are, in some cases, beyond our control and which could materially affect results. Factors that may cause actual results to differ materially from current expectations include, among other things, those listed in the section entitled “Risk Factors” included in our Annual Report on Form 10-K for the fiscal year ended December 31, 2017 and Quarterly Report on Form 10-Q for the quarter ended March 31, 2018. If one or more of these or other risks or uncertainties occur, or if our underlying assumptions prove to be incorrect, actual events or results may vary significantly from those implied or projected by the forward-looking statements. No forward-looking statement is a guarantee of future performance. You should read this Report and the documents that we reference in this Report and have filed with the Securities and Exchange Commission, or the SEC, as exhibits to this Report, completely and with the understanding that our actual future results may be materially different from any future results expressed or implied by these forward-looking statements.

In particular, forward-looking statements in this Report may include statements about:

| • | anticipated trends, conditions and investor sentiment in the global markets and exchange traded products, or ETPs; |

| • | anticipated levels of inflows into and outflows out of our ETPs; |

| • | our ability to deliver favorable rates of return to investors; |

| • | our ability to develop new products and services; |

| • | our ability to maintain current vendors or find new vendors to provide services to us at favorable costs; |

| • | our ability to successfully expand our business into non-U.S. markets; |

| • | competition in our business; and |

| • | the effect of laws and regulations that apply to our business. |

The forward-looking statements in this Report represent our views as of the date of this Report. We anticipate that subsequent events and developments may cause our views to change. However, while we may elect to update these forward-looking statements at some point in the future, we have no current intention of doing so except to the extent required by applicable law. Therefore, these forward-looking statements do not represent our views as of any date other than the date of this Report.

3

Table of Contents

| ITEM 1. | FINANCIAL STATEMENTS |

WisdomTree Investments, Inc. and Subsidiaries

Consolidated Balance Sheets

(In Thousands, Except Per Share Amounts)

| September 30, 2018 |

December 31, 2017 |

|||||||

| (Unaudited) | ||||||||

| Assets |

||||||||

| Current assets: |

||||||||

| Cash and cash equivalents |

$ | 77,125 | $ | 54,193 | ||||

| Securities owned, at fair value |

4,426 | 66,294 | ||||||

| Securities held-to-maturity |

— | 1,000 | ||||||

| Accounts receivable |

25,528 | 21,309 | ||||||

| Income taxes receivable |

— | 6,978 | ||||||

| Prepaid expenses |

5,505 | 3,550 | ||||||

| Other current assets |

303 | 1,007 | ||||||

|

|

|

|

|

|||||

| Total current assets |

112,887 | 154,331 | ||||||

| Fixed assets, net |

9,723 | 10,693 | ||||||

| Note receivable, net (Note 8) |

28,121 | 18,748 | ||||||

| Indemnification receivable (Note 20) |

35,654 | — | ||||||

| Securities held-to-maturity |

20,199 | 20,299 | ||||||

| Deferred tax assets, net |

2,213 | 1,050 | ||||||

| Investments, carried at cost (Note 9) |

35,187 | 35,187 | ||||||

| Goodwill (Note 22) |

85,856 | 1,799 | ||||||

| Intangible assets (Note 22) |

613,274 | 12,085 | ||||||

| Other noncurrent assets |

2,304 | 793 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 945,418 | $ | 254,985 | ||||

|

|

|

|

|

|||||

| Liabilities and stockholders’ equity |

||||||||

| Liabilities |

||||||||

| Current liabilities: |

||||||||

| Fund management and administration payable |

$ | 24,383 | $ | 20,099 | ||||

| Compensation and benefits payable |

13,728 | 28,053 | ||||||

| Deferred consideration – gold payments (Note 11) |

11,788 | — | ||||||

| Income taxes payable |

799 | — | ||||||

| Securities sold, but not yet purchased, at fair value |

2,018 | 950 | ||||||

| Accounts payable and other liabilities |

8,668 | 8,246 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

61,384 | 57,348 | ||||||

| Long-term debt (Note 12) |

193,999 | — | ||||||

| Deferred consideration – gold payments (Note 11) |

144,267 | — | ||||||

| Deferred rent payable |

4,462 | 4,686 | ||||||

| Other noncurrent liabilities (Note 20) |

35,654 | — | ||||||

|

|

|

|

|

|||||

| Total liabilities |

439,766 | 62,034 | ||||||

|

|

|

|

|

|||||

| Preferred stock – Series A Non-Voting Convertible, par value $0.01; 14.750 shares authorized, issued and outstanding (Note 13) |

132,569 | — | ||||||

|

|

|

|

|

|||||

| Commitments and Contingencies (Note 14) |

||||||||

| Stockholders’ equity |

||||||||

| Preferred stock, par value $0.01; 2,000 shares authorized (Note 13): |

— | — | ||||||

| Common stock, par value $0.01; 250,000 shares authorized; issued and outstanding: 153,083 and 136,996 at September 30, 2018 and December 31, 2017, respectively |

1,531 | 1,370 | ||||||

| Additional paid-in capital |

361,900 | 216,006 | ||||||

| Accumulated other comprehensive income |

373 | 291 | ||||||

| Retained earnings/(Accumulated deficit) |

9,279 | (24,716 | ) | |||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

373,083 | 192,951 | ||||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ equity |

$ | 945,418 | $ | 254,985 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of these consolidated financial statements

4

Table of Contents

WisdomTree Investments, Inc. and Subsidiaries

Consolidated Statements of Operations

(In Thousands, Except Per Share Amounts)

(Unaudited)

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Operating Revenues: |

||||||||||||||||

| Advisory fees |

$ | 71,679 | $ | 57,293 | $ | 203,913 | $ | 166,177 | ||||||||

| Other income |

891 | 421 | 2,336 | 1,145 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

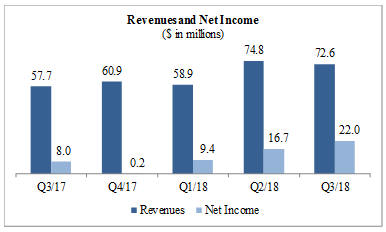

| Total revenues |

72,570 | 57,714 | 206,249 | 167,322 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating Expenses: |

||||||||||||||||

| Compensation and benefits |

17,544 | 19,492 | 55,677 | 55,787 | ||||||||||||

| Fund management and administration |

15,292 | 10,862 | 40,825 | 30,574 | ||||||||||||

| Marketing and advertising |

3,239 | 3,314 | 10,212 | 10,676 | ||||||||||||

| Sales and business development |

3,801 | 3,617 | 12,117 | 9,968 | ||||||||||||

| Contractual gold payments (Note 11) |

2,880 | — | 5,595 | — | ||||||||||||

| Professional and consulting fees |

1,934 | 1,035 | 5,130 | 3,814 | ||||||||||||

| Occupancy, communications and equipment |

1,722 | 1,378 | 4,659 | 4,102 | ||||||||||||

| Depreciation and amortization |

306 | 353 | 998 | 1,042 | ||||||||||||

| Third-party distribution fees |

1,407 | 710 | 4,798 | 2,312 | ||||||||||||

| Acquisition-related costs (Note 3) |

456 | — | 10,446 | — | ||||||||||||

| Other |

2,281 | 1,729 | 6,332 | 5,195 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total expenses |

50,862 | 42,490 | 156,789 | 123,470 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income |

21,708 | 15,224 | 49,460 | 43,852 | ||||||||||||

| Other Income/(Expenses): |

||||||||||||||||

| Interest expense |

(2,747 | ) | — | (5,103 | ) | — | ||||||||||

| Gain on revaluation of deferred consideration – gold payments (Note 11) |

7,732 | — | 17,630 | — | ||||||||||||

| Interest income |

719 | 772 | 2,293 | 1,999 | ||||||||||||

| Settlement gain |

— | — | — | 6,909 | ||||||||||||

| Other gains and losses, net |

118 | (500 | ) | (644 | ) | (217 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income before taxes |

27,530 | 15,496 | 63,636 | 52,543 | ||||||||||||

| Income tax expense |

5,481 | 7,520 | 15,439 | 25,582 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

$ | 22,049 | $ | 7,976 | $ | 48,197 | $ | 26,961 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings per share—basic |

$ | 0.13 | $ | 0.06 | $ | 0.31 | $ | 0.20 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings per share—diluted |

$ | 0.13 | $ | 0.06 | $ | 0.31 | $ | 0.20 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted-average common shares—basic |

150,892 | 134,709 | 145,149 | 134,552 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted-average common shares—diluted |

166,622 | 135,933 | 155,584 | 135,768 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Cash dividends declared per common share |

$ | 0.03 | $ | 0.08 | $ | 0.09 | $ | 0.24 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The accompanying notes are an integral part of these consolidated financial statements

5

Table of Contents

WisdomTree Investments, Inc. and Subsidiaries

Consolidated Statements of Comprehensive Income

(In Thousands)

(Unaudited)

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Net income |

$ | 22,049 | $ | 7,976 | $ | 48,197 | $ | 26,961 | ||||||||

| Other comprehensive (loss)/income |

||||||||||||||||

| Change in unrealized gains/(losses) on available-for-sale debt securities, net of tax |

— | (96 | ) | 477 | (230 | ) | ||||||||||

| Foreign currency translation adjustment |

(88 | ) | 363 | (395 | ) | 802 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Other comprehensive (loss)/income |

(88 | ) | 267 | 82 | 572 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Comprehensive income |

$ | 21,961 | $ | 8,243 | $ | 48,279 | $ | 27,533 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The accompanying notes are an integral part of these consolidated financial statements

6

Table of Contents

WisdomTree Investments, Inc. and Subsidiaries

Consolidated Statements of Cash Flows

(In Thousands)

(Unaudited)

| Nine Months Ended September 30, |

||||||||

| 2018 | 2017 | |||||||

| Cash flows from operating activities: |

||||||||

| Net income |

$ | 48,197 | $ | 26,961 | ||||

| Adjustments to reconcile net income to net cash provided by operating activities: |

||||||||

| Advisory fees paid in gold and other precious metals |

(21,998 | ) | — | |||||

| Contractual gold payments (Note 11) |

5,595 | — | ||||||

| Gain on revaluation of deferred consideration – gold payments (Note 11) |

(17,630 | ) | — | |||||

| Stock-based compensation |

10,078 | 10,558 | ||||||

| Deferred income taxes |

(1,251 | ) | 3,823 | |||||

| Paid-in-kind interest income (Note 8) |

(1,373 | ) | — | |||||

| Settlement gain |

— | (6,909 | ) | |||||

| Amortization of credit facility issuance costs |

1,360 | — | ||||||

| Depreciation and amortization |

998 | 1,042 | ||||||

| Other |

810 | 524 | ||||||

| Changes in operating assets and liabilities, net of the effects of the ETFS Acquisition: |

||||||||

| Securities owned, at fair value |

(2,735 | ) | 1,146 | |||||

| Accounts receivable |

3,771 | (1,969 | ) | |||||

| Income taxes receivable/payable |

7,654 | (628 | ) | |||||

| Prepaid expenses |

(621 | ) | (361 | ) | ||||

| Gold and other precious metals |

18,472 | — | ||||||

| Other assets |

954 | (31 | ) | |||||

| Acquisition payable |

— | (3,545 | ) | |||||

| Fund management and administration payable |

1,998 | 561 | ||||||

| Compensation and benefits payable |

(21,025 | ) | 115 | |||||

| Securities sold, but not yet purchased, at fair value |

1,068 | (1,249 | ) | |||||

| Accounts payable and other liabilities |

(4,122 | ) | 1,041 | |||||

|

|

|

|

|

|||||

| Net cash provided by operating activities |

30,200 | 31,079 | ||||||

|

|

|

|

|

|||||

| Cash flows from investing activities: |

||||||||

| Purchase of fixed assets |

(45 | ) | (253 | ) | ||||

| Purchase of securities held-to-maturity |

— | (3,009 | ) | |||||

| Purchase of debt securities available-for-sale |

— | (76,776 | ) | |||||

| Purchase of investments |

— | (5,000 | ) | |||||

| Funding of AdvisorEngine note receivable (Note 8) |

(8,000 | ) | — | |||||

| Proceeds from held-to-maturity securities maturing or called prior to maturity |

1,096 | 2,162 | ||||||

| Proceeds from sales and maturities of debt securities available-for-sale |

64,498 | 65,067 | ||||||

| Cash paid – ETFS Acquisition, net of cash acquired (Note 3) |

(239,313 | ) | — | |||||

|

|

|

|

|

|||||

| Net cash used in investing activities |

(181,764 | ) | (17,809 | ) | ||||

|

|

|

|

|

|||||

| Cash flows from financing activities: |

||||||||

| Dividends paid |

(14,202 | ) | (32,825 | ) | ||||

| Shares repurchased |

(1,430 | ) | (4,178 | ) | ||||

| Credit facility issuance costs |

(8,690 | ) | — | |||||

| Preferred stock issuance costs |

(181 | ) | — | |||||

| Proceeds from the issuance of long-term debt (Note 12) |

200,000 | — | ||||||

| Proceeds from exercise of stock options |

157 | 53 | ||||||

|

|

|

|

|

|||||

| Net cash provided by/(used in) financing activities |

175,654 | (36,950 | ) | |||||

|

|

|

|

|

|||||

| (Decrease)/increase in cash flow due to changes in foreign exchange rate |

(1,158 | ) | 1,179 | |||||

|

|

|

|

|

|||||

| Net increase/(decrease) in cash and cash equivalents |

22,932 | (22,501 | ) | |||||

| Cash and cash equivalents—beginning of period |

54,193 | 92,722 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents—end of period |

$ | 77,125 | $ | 70,221 | ||||

|

|

|

|

|

|||||

| Supplemental disclosure of cash flow information: |

||||||||

| Cash paid for taxes |

$ | 8,759 | $ | 22,130 | ||||

|

|

|

|

|

|||||

| Cash paid for interest |

$ | 3,351 | $ | — | ||||

|

|

|

|

|

|||||

Refer to Note 3 for information regarding the non-cash effects of the ETFS Acquisition, including non-cash consideration paid.

The accompanying notes are an integral part of these consolidated financial statements

7

Table of Contents

WisdomTree Investments, Inc. and Subsidiaries

Notes to Consolidated Financial Statements

(In Thousands, Except Share and Per Share Amounts)

1. Organization and Description of Business

WisdomTree Investments, Inc., through its global subsidiaries (collectively, “WisdomTree” or the “Company”), is an exchange traded product (“ETP”) sponsor and asset manager headquartered in New York. WisdomTree offers ETPs covering equity, fixed income, currencies, commodities and alternative strategies. The Company has the following wholly-owned operating subsidiaries:

| • | WisdomTree Asset Management, Inc. is a New York based investment adviser registered with the SEC providing investment advisory and other management services to the WisdomTree Trust (“WTT”) and WisdomTree exchange traded funds (“ETFs”). The WisdomTree ETFs are issued in the U.S. by WTT. WTT, a non-consolidated third party, is a Delaware statutory trust registered with the SEC as an open-end management investment company. The Company has licensed to WTT the use of certain of its own indexes on an exclusive basis for the WisdomTree ETFs in the U.S. |

| • | ETFS Management Company (Jersey) Limited (“ManJer”) is a Jersey based management company providing investment and other management services to nine issuers (the “ETFS Issuers”) and the ETPs issued and listed by the ETFS Issuers covering commodity, currency and short-and-leveraged strategies. |

| • | Boost Management Limited (“BML”) is a Jersey based management company providing investment and other management services to Boost Issuer PLC (“BI”) and Boost ETPs. The Boost ETPs are issued by BI. BI, a non-consolidated third party, is a public limited company domiciled in Ireland. |

| • | WisdomTree Management Limited (“WML”) is an Ireland based management company providing investment and other management services to WisdomTree Issuer plc (“WTI”) and WisdomTree UCITS ETFs. The WisdomTree UCITS ETFs are issued by WTI. WTI, a non-consolidated third party, is a public limited company domiciled in Ireland. |

| • | WisdomTree UK Limited is a U.K. based company registered with the Financial Conduct Authority currently providing management and other services to ManJer, BML and WML. |

| • | WisdomTree Europe Limited is a U.K. based company registered with the Financial Conduct Authority currently providing management and other services to WisdomTree UK Limited, BML and WML. |

| • | WisdomTree Asset Management Canada, Inc. (“WTAMC”) is a Canada based investment fund manager registered with the Ontario Securities Commission providing fund management services to locally-listed WisdomTree Canadian ETFs. |

| • | WisdomTree Commodity Services, LLC (“WTCS”) is a New York based company that serves as the managing owner and commodity pool operator of the WisdomTree Continuous Commodity Index Fund. WTCS is registered with the Commodity Futures Trading Commission and is a member of the National Futures Association. |

| • | WisdomTree Ireland Limited is an Ireland based company authorized by the Central Bank of Ireland to provide distribution services. It is intended that WisdomTree Ireland Limited will provide EU distribution services to ManJer, BML and WTML post-Brexit. |

Acquisition of ETFS

On April 11, 2018, the Company acquired the European exchange-traded commodity, currency and short-and-leveraged business (“ETFS”) of ETFS Capital Limited (“ETFS Capital”, formerly known as ETF Securities Limited). This acquisition is referred to throughout the consolidated financial statements as the ETFS Acquisition. See Note 3 for additional information.

Restructuring of Distribution Strategy in Japan

In July 2018, the Company determined to restructure its distribution strategy in Japan and has expanded its existing relationship with a third party to manage distribution of WisdomTree ETFs in Japan. As a result, the Company will close WisdomTree Japan Inc. (“WTJ”). During the three months ended September 30, 2018 and 2017, WTJ reported an operating loss of $1,342 and $1,085, respectively. During the nine months ended September 30, 2018 and 2017, WTJ reported an operating loss of $3,698 and $3,447, respectively.

2. Significant Accounting Policies

Basis of Presentation

These consolidated financial statements have been prepared in conformity with U.S. generally accepted accounting principles (“GAAP”) and in the opinion of management reflect all adjustments, consisting of only normal recurring adjustments, necessary for a fair statement of financial condition, results of operations, and cash flows for the periods presented. The consolidated financial statements include the accounts of the Company’s wholly owned subsidiaries. All intercompany accounts and transactions have been eliminated in consolidation.

8

Table of Contents

The financial results of ETFS are included in our consolidated financial statements since the acquisition date, April 11, 2018 (See Note 3).

Certain accounts in the prior years’ consolidated financial statements have been reclassified to conform to the current year’s consolidated financial statement presentation. The following table summarizes these reclassifications for the three and nine months ended September 30, 2017, which had no effect on previously reported net income.

| Operating Revenues: | Three Months Ended September 30, 2017 |

Nine Months Ended September 30, 2017 |

||||||

| Advisory fees (previously reported) |

$ | 57,574 | $ | 166,950 | ||||

| Other ETP fees reclassified to Other income |

(281 | ) | (773 | ) | ||||

|

|

|

|

|

|||||

| Advisory fees (currently reported) |

$ | 57,293 | $ | 166,177 | ||||

|

|

|

|

|

|||||

| Settlement gain (previously reported) |

$ | — | $ | 6,909 | ||||

| Reclassify to Other Income/(Expenses) |

— | (6,909 | ) | |||||

|

|

|

|

|

|||||

| Settlement gain (currently reported) |

$ | — | $ | — | ||||

|

|

|

|

|

|||||

| Other income (previously reported) |

$ | 412 | $ | 2,154 | ||||

| Other ETP fees reclassified from Advisory fees |

281 | 773 | ||||||

| Interest income reclassified to Other Income/(Expenses) |

(772 | ) | (1,999 | ) | ||||

| Realized and unrealized losses reclassified to Other gains and losses, net |

535 | 1,054 | ||||||

| Miscellaneous other income reclassified to Other gains and losses, net |

(35 | ) | (837 | ) | ||||

|

|

|

|

|

|||||

| Other income (currently reported) |

$ | 421 | $ | 1,145 | ||||

|

|

|

|

|

|||||

| Total revenues (currently reported) |

$ | 57,714 | $ | 167,322 | ||||

|

|

|

|

|

|||||

| Other Income/(Expenses): |

||||||||

| Interest income reclassified from operating revenues |

$ | 772 | $ | 1,999 | ||||

|

|

|

|

|

|||||

| Settlement gain reclassified from operating revenues |

$ | — | $ | 6,909 | ||||

|

|

|

|

|

|||||

| Other gains and losses, net (previously reported) |

$ | — | $ | — | ||||

| Realized and unrealized losses reclassified from operating revenues |

(535 | ) | (1,054 | ) | ||||

| Miscellaneous other income reclassified from operating revenues |

35 | 837 | ||||||

|

|

|

|

|

|||||

| Other gains and losses, net (currently reported) |

$ | (500 | ) | $ | (217 | ) | ||

|

|

|

|

|

|||||

Consolidation

The Company consolidates entities in which it has a controlling financial interest. The Company determines whether it has a controlling financial interest in an entity by first evaluating whether the entity is a voting interest entity (“VOE”) or a variable interest entity (“VIE”). The usual condition for a controlling financial interest in a VOE is ownership of a majority voting interest. If the Company has a majority voting interest in a VOE, the entity is consolidated. The Company has a controlling financial interest in a VIE when the Company has a variable interest that provides it with (i) the power to direct the activities of the VIE that most significantly impact the VIE’s economic performance and (ii) the obligation to absorb losses of the VIE or the right to receive benefits from the VIE that could potentially be significant to the VIE.

The Company reassesses its evaluation of whether an entity is a VIE when certain reconsideration events occur.

Segment and Geographic Information

The Company operates as an ETP sponsor and asset manager providing investment advisory services globally. These activities are reported in the Company’s U.S. Business and International Business reportable segments. The International Business reportable segment includes the results of the Company’s European operations and Canadian operations.

The financial results of ETFS are included in the International Business reportable segment as of the acquisition date.

9

Table of Contents

Foreign Currency Translation

Assets and liabilities of subsidiaries whose functional currency is not the U.S. dollar are translated based on the end of period exchange rates from local currency to U.S. dollars. Results of operations are translated at the average exchange rates in effect during the period. The impact of the foreign currency translation adjustment is included in the Consolidated Statements of Comprehensive Income as a component of other comprehensive income.

Use of Estimates

The preparation of the Company’s consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities as of the balance sheet dates and the reported amounts of revenues and expenses for the periods presented. Actual results could differ materially from those estimates.

Revenue Recognition

The Company earns substantially all of its revenue in the form of advisory fees from its ETPs and recognizes this revenue over time, as the performance obligation is satisfied. ETP advisory fees are based on a percentage of the ETPs’ average daily net assets. Progress is measured using the practical expedient under the output method resulting in the recognition of revenue in the amount for which the Company has a right to invoice.

Contractual Gold Payments

Contractual gold payments are measured monthly based upon the average daily spot price of gold (See Note 11).

Marketing and Advertising

Advertising costs, including media advertising and production costs, are expensed when incurred.

Depreciation and Amortization

Depreciation is provided for using the straight-line method over the estimated useful lives of the related assets as follows:

| Equipment |

5 years | |||

| Furniture and fixtures |

15 years |

Leasehold improvements are amortized over the term of their respective leases or service lives of the improvements, whichever is shorter. Fixed assets are recorded at cost less accumulated depreciation and amortization.

Occupancy

The Company accounts for its office lease facilities as operating leases, which may include free rent periods and escalation clauses. The Company expenses the lease payments associated with operating leases on a straight-line basis over the lease term.

Stock-Based Awards

Accounting for stock-based compensation requires the measurement and recognition of compensation expense for all equity awards based on estimated fair values. Stock-based compensation is measured based on the grant-date fair value of the award and is amortized over the relevant service period. Forfeitures are recognized when they occur.

Third-Party Distribution Fees

The Company pays a percentage of its advisory fee revenues based on incremental growth in AUM, subject to caps or minimums, to marketing agents to sell WisdomTree ETFs and for including WisdomTree ETFs on third-party customer platforms.

Cash and Cash Equivalents

The Company considers all highly liquid investments with an original maturity of 90 days or less at the time of purchase to be classified as cash equivalents. The Company maintains deposits with financial institutions in an amount that is in excess of federally insured limits.

Accounts Receivable and Allowance for Doubtful Accounts

Accounts receivable are customer and other obligations due under normal trade terms. An allowance for doubtful accounts is not provided since, in the opinion of management, all accounts receivable recorded are deemed current and collectible.

10

Table of Contents

Impairment of Long-Lived Assets

The Company performs a review for the impairment of long-lived assets when events or changes in circumstances indicate that the estimated undiscounted future cash flows expected to be generated by the assets are less than their carrying amounts or when other events occur which may indicate that the carrying amount of an asset may not be recoverable.

Note Receivable

Note receivable is accounted for on an amortized cost basis, net of original issue discount. Interest income is accrued over the term of the note using the effective interest method. The Company performs a review for the impairment of the note receivable on a quarterly basis and provides for an allowance for credit losses if all or a portion of the note is determined to be uncollectible.

Securities Owned and Securities Sold, but not yet Purchased (at fair value)

Securities owned and securities sold, but not yet purchased are securities classified as either trading or available-for-sale. These securities are recorded on their trade date and are measured at fair value. All equity securities are classified by the Company as trading. Debt securities are classified based primarily on the Company’s intent to hold or sell the security. Changes in the fair value of securities classified as trading are reported in other income in the period the change occurs. Unrealized gains and losses of securities classified as available-for-sale are included in other comprehensive income. Once sold, amounts reclassified out of accumulated other comprehensive income and into earnings are determined using the specific identification method. Available-for-sale securities are assessed for impairment on a quarterly basis.

Securities Held-to-Maturity

The Company accounts for certain of its investments as held-to-maturity on a trade date basis, which are recorded at amortized cost. For held-to-maturity investments, the Company has the intent and ability to hold investments to maturity and it is not more-likely-than-not that the Company will be required to sell the investments before recovery of their amortized cost bases, which may be maturity. On a quarterly basis, the Company reviews its portfolio of investments for impairment. If a decline in fair value is deemed to be other-than-temporary, the security is written down to its fair value through earnings.

Investments, Carried at Cost

The Company accounts for equity investments that do not have a readily determinable fair value as cost method investments under the measurement alternative prescribed within Accounting Standards Update (“ASU”) 2016-01, Financial Instruments – Recognition and Measurement of Financial Assets and Financial Liabilities, to the extent such investments are not subject to consolidation or the equity method. Under the measurement alternative, these financial instruments are carried at cost, less any impairment (assessed quarterly), plus or minus changes resulting from observable price changes in orderly transactions for an identical or similar investment of the same issuer. In addition, income is recognized when dividends are received only to the extent they are distributed from net accumulated earnings of the investee. Otherwise, such distributions are considered returns of investment and are recorded as a reduction of the cost of the investment.

Goodwill

Goodwill is the excess of the fair value of the purchase price over the fair values of the identifiable net assets at the acquisition date. The Company tests its goodwill for impairment at least annually and at the time of a triggering event requiring re-evaluation, if one were to occur, in accordance with ASU 2017-04, Intangibles-Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment. The Company early adopted the revised guidance for the impairment tests performed after January 1, 2017. Under the revised guidance, goodwill is considered impaired when the estimated fair value of the reporting unit that was allocated the goodwill is less than its carrying value. If the estimated fair value of such reporting unit is less than its carrying value, goodwill impairment is recognized based on that difference, not to exceed the carrying amount of goodwill. A reporting unit is an operating segment or a component of an operating segment provided that the component constitutes a business for which discrete financial information is available and management regularly reviews the operating results of that component.

For impairment testing purposes, goodwill has been allocated to the Company’s U.S. Business reporting unit which is assessed annually for impairment on April 30th (See Note 22). In addition, goodwill arising from the ETFS Acquisition (See Note 3) has been allocated to the European Business reporting unit, included within the International Business reportable segment and assessed annually for impairment on November 30th. When performing its goodwill impairment test, the Company considers a qualitative assessment, when appropriate, and the income approach, market approach and its market capitalization when determining the fair value of its reporting units.

11

Table of Contents

Intangible Assets

Indefinite-lived intangible assets are tested for impairment at least annually and are also reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Indefinite-lived intangible assets are impaired if their estimated fair values are less than their carrying values.

Finite-lived intangible assets, if any, are amortized over their estimated useful life, which is the period over which the assets are expected to contribute directly or indirectly to the future cash flows of the Company. These intangible assets are tested for impairment at the time of a triggering event, if one were to occur. Finite-lived intangible assets may be impaired when the estimated undiscounted future cash flows generated from the assets are less than their carrying amounts.

The Company may rely on a qualitative assessment when performing its intangible asset impairment test. Otherwise, the impairment evaluation is performed at the lowest level of reasonably identifiable cash flows independent of other assets. The annual impairment testing date for all of the Company’s intangible assets is November 30th.

Deferred Consideration

Deferred consideration represents the present value of an obligation to pay gold to a third party into perpetuity and is measured using forward-looking gold prices and a selected discount rate (See Note 11). Changes in the fair value of this obligation are reported as gain/(loss) on revaluation of deferred consideration on the Company’s Consolidated Statements of Operations.

Long-Term Debt

Long-term debt is carried at amortized cost, net of debt issuance costs. Interest expense is recognized using the effective interest method and includes amortization of debt issuance costs over the life of the debt.

Earnings per Share

Basic earnings per share (“EPS”) is computed by dividing net income available to common stockholders by the weighted-average number of common shares outstanding for the period. Net income available to common stockholders represents net income of the Company reduced by an allocation of earnings to participating securities. The preferred stock issued in connection with the ETFS Acquisition (see Note 3) and unvested share-based payment awards that contain non-forfeitable rights to dividends or dividend equivalents (whether paid or unpaid) are participating securities and are included in the computation of EPS pursuant to the two-class method. Share-based payment awards that do not contain such rights are not deemed participating securities and are included in diluted shares outstanding (if dilutive) under the treasury stock method. Diluted EPS reflects the reduction in earnings per share assuming dilutive options or other dilutive contracts to issue common stock were exercised or converted into common stock. Diluted EPS is calculated under the treasury stock and if-converted method and the two-class method. The calculation that results in the most dilutive EPS amount for the common stock is reported in the Company’s consolidated financial statements.

Income Taxes

The Company accounts for income taxes using the liability method, which requires the determination of deferred tax assets and liabilities based on the differences between the financial and tax basis of assets and liabilities using the enacted tax rates in effect for the year in which differences are expected to reverse. Deferred tax assets are adjusted by a valuation allowance if, based on the weight of available evidence, it is more-likely-than-not that some portion or all the deferred tax assets will not be realized.

Tax positions are evaluated utilizing a two-step process. The Company first determines whether any of its tax positions are more-likely-than-not to be sustained upon examination, based solely on the technical merits of the position. Once it is determined that a position meets this recognition threshold, the position is measured as the largest amount of benefit that is greater than 50% likely of being realized upon ultimate settlement. The Company records interest expense and penalties related to tax expenses as income tax expense.

Non-income based taxes are recorded as part of other liabilities and other expenses.

Recently Issued Accounting Pronouncements

In May 2014, the Financial Accounting Standards Board, or FASB, issued ASU 2014-09, Revenue from Contracts with Customers (ASU 2014-09), a comprehensive revenue recognition standard on the financial reporting requirements for revenue from contracts entered into with customers. In July 2015, the FASB deferred this ASU’s effective date by one year, to interim and annual periods beginning after December 15, 2017. The deferral allows early adoption at the original effective date. During 2016, the FASB issued ASU 2016-08, which clarifies principal versus agent considerations, ASU 2016-10, which clarifies identifying performance obligations and the licensing implementation guidance, and ASU 2016-12, which amends certain aspects of the new revenue recognition standard pursuant to ASU 2014-09. ASU 2014-09 allows for the use of either the retrospective or modified retrospective adoption method. The guidance in ASU 2014-09, and the related amendments, became effective for the Company on January 1, 2018.

12

Table of Contents

The Company adopted this standard under the modified retrospective method and has determined the standard did not have a material impact on the Company’s historical pattern of recognizing revenue from its contracts with customers (See Note 16).

In January 2016, the FASB issued ASU 2016-01, Financial Instruments – Recognition and Measurement of Financial Assets and Financial Liabilities (ASU 2016-01). The main objective of the standard is to enhance the reporting model for financial instruments to provide users of financial statements with more decision-useful information. The amendments in the update make targeted improvements to generally accepted accounting principles. These include requiring equity investments (except those accounted for under the equity method of accounting or those that result in consolidation of the investee) to be measured at fair value with changes in fair value recognized in net income. Available-for-sale classification for equity investments with readily determinable fair values will no longer be permissible. However, an entity may choose a measurement alternative to measure equity investments that do not have readily determinable fair values by recognizing these financial instruments at cost minus impairment, if any, plus or minus changes resulting from observable price changes in orderly transactions for the identical or similar investment of the same issuer. The update also simplifies the impairment assessment of equity investments without readily determinable fair values by requiring a qualitative assessment to identify impairment. When a qualitative assessment indicates that impairment exists, an entity is required to measure the investment at fair value. ASU 2016-01 is effective for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years. The Company adopted this standard on January 1, 2018 and has elected to apply the measurement alternative to its equity investments that do not have readily determinable fair values. The adoption of this standard did not have a material impact on the Company’s consolidated financial statements.

In June 2016, the FASB issued ASU 2016-13, Financial Instruments-Credit Losses (Topic 326) – Measurement of Credit Losses on Financial Instruments (ASU 2016-13). The main objective of the standard is to provide financial statement users with more decision-useful information about the expected credit losses on financial instruments and other commitments to extend credit held by a reporting entity at each reporting date. In issuing this standard, the FASB is responding to criticism that today’s guidance delays recognition of credit losses. The standard will replace today’s “incurred loss” approach with an “expected loss” model. The new model, referred to as the current expected credit loss (“CECL”) model, will apply to: (1) financial assets subject to credit losses and measured at amortized cost, and (2) certain off-balance sheet credit exposures. The standard is applicable to loans, accounts receivable, trade receivables, and other financial assets measured at amortized cost, loan commitments and certain other off-balance sheet credit exposures, debt securities (including those held-to-maturity) and other financial assets measured at fair value through other comprehensive income, and beneficial interests in securitized financial assets. The CECL model does not apply to available-for-sale debt securities. For available-for-sale debt securities with unrealized losses, entities will measure credit losses in a manner similar to what they do today, except that the credit losses will be recognized as allowances rather than reductions in the amortized cost of the securities. Accordingly, the new methodology will be utilized when assessing the Company’s financial instruments for impairment. As a result, entities will recognize improvements to estimated credit losses immediately in earnings rather than as interest income over time, as they do today. The ASU also simplifies the accounting model for purchased credit-impaired debt securities and loans. ASU 2016-13 also expands the disclosure requirements regarding an entity’s assumptions, models, and methods for estimating the allowance for loan and lease losses. ASU 2016-13 is effective for years beginning after December 15, 2019, including interim periods within those fiscal years under a modified retrospective approach. Early adoption is permitted for periods beginning after December 15, 2018. The Company is currently evaluating the impact that the standard will have on its consolidated financial statements.

In February 2016, the FASB issued ASU 2016-02, Leases (ASU 2016-02), which requires lessees to include most leases on the balance sheet. ASU 2016-02 is effective for fiscal years (and interim reporting periods within those years) beginning after December 15, 2018 and early adoption is permitted. The Company is currently evaluating the impact that the standard will have on its consolidated financial statements and expects, at a minimum, that its implementation will result in a gross-up on the consolidated balance sheets upon recognition of right-of-use assets and lease liabilities associated with the future minimum payments required under operating leases as disclosed in Note 14.

In August 2018, the FASB issued ASU 2018-13, Fair Value Measurement (Topic 820) – Disclosure Framework – Changes to the Disclosure Requirements for Fair Value Measurement (ASU 2018-13), which modifies the disclosure requirements on fair value measurements, including removing the requirement to disclose (1) the amount of and reasons for transfers between Level 1 and Level 2 of the fair value hierarchy, (2) the policy for timing of transfers between levels and (3) the valuation processes for Level 3 fair value measurements. ASU 2018-13 also added new disclosures including the requirement to disclose (A) the changes in unrealized gains and losses for the period included in other comprehensive income for recurring Level 3 fair value measurements held at the end of the reporting period and (B) the range and weighted average of significant unobservable inputs used to develop Level 3 fair value measurements. ASU 2018-13 is effective for fiscal years (and interim reporting periods within those years) beginning after December 15, 2019 and early adoption is permitted. This standard will only impact the disclosures pertaining to fair value measurements.

13

Table of Contents

3. Business Combination

Summary

On November 13, 2017, the Company entered into a Share Sale Agreement as amended by the Waiver and Variation Agreement, dated April 11, 2018 (collectively referred to as the “Share Sale Agreement”) with ETFS Capital and WisdomTree International Holdings Ltd, an indirect wholly owned subsidiary of the Company (“WisdomTree International”), pursuant to which the Company agreed to acquire ETFS. On April 11, 2018, the Company completed the acquisition by purchasing the entire issued share capital of a subsidiary of ETFS Capital into which ETFS Capital transferred ETFS prior to completion of the ETFS Acquisition.

Pursuant to the Share Sale Agreement, the Company acquired ETFS for a purchase price consisting of (a) $253,000 in cash (including $53,000 paid from proceeds arising from maturities of securities owned, at fair value), subject to customary adjustments for working capital, and (b) a fixed number of shares of the Company’s capital stock, consisting of (i) 15,250,000 shares of common stock (the “Common Shares”) and (ii) 14,750 shares of Series A Non-Voting Convertible Preferred Stock (the “Preferred Shares”), which are convertible, subject to certain restrictions, into an aggregate of 14,750,000 shares of common stock.

On April 11, 2018 and in connection with the ETFS Acquisition, the Company and WisdomTree International entered into a credit agreement (the “Credit Agreement”), by and among the Company, WisdomTree International, certain subsidiaries of the Company as guarantors, the lenders party thereto and Credit Suisse AG, Cayman Islands Branch, as administrative agent, collateral agent, L/C Issuer and lender. Under the Credit Agreement, the lenders extended a $200,000 term loan (the “Term Loan”) to WisdomTree International, the net cash proceeds of which were used by WisdomTree International, together with other cash on hand, to complete the acquisition and pay certain related fees, costs and expenses, and made a $50,000 revolving credit facility (the “Revolver” and, together with the Term Loan, the “Credit Facility”) available to the Company and WisdomTree International for revolving borrowings from time to time for working capital, capital expenditures and general corporate purposes (See Note 12).

On April 11, 2018 and in connection with the acquisition, the Company and ETFS Capital also entered into an Investor Rights Agreement, pursuant to which, among other things, ETFS Capital is subject to lock-up, standstill and voting restrictions. ETFS Capital also received certain registration rights with respect to the Common Shares and the shares of common stock issuable upon conversion of the Preferred Shares it received in the transaction.

Purchase Price Allocation

The ETFS Acquisition has been accounted for under the acquisition method of accounting in accordance with ASC Topic 805, Business Combinations, which requires an allocation of the consideration paid by the Company to the identifiable assets and liabilities of ETFS based on the estimated fair values as of the closing date of the acquisition. An allocation of the consideration transferred is presented below based on information currently available and includes the Company’s valuation of the fair value of tangible and intangible assets acquired and liabilities assumed.

The following table summarizes the allocation of the purchase price as of the acquisition date:

| Purchase price |

| |||

| Preferred Shares issued |

14,750 | |||

| Conversion ratio |

1,000 | |||

|

|

|

|||

| Common stock equivalents |

14,750,000 | |||

| Common Shares issued |

15,250,000 | |||

|

|

|

|||

| Total shares issued |

30,000,000 | |||

| WisdomTree stock price(1) |

$ | 9.00 | ||

|

|

|

|||

| Equity portion of purchase price |

$ | 270,000 | ||

| Cash portion of purchase price |

||||

| Term Loan (See Note 12) |

200,000 | |||

| Cash on hand |

53,000 | |||

|

|

|

|||

| Purchase price |

523,000 | |||

| Deferred consideration (See Note 11) |

172,746 | |||

|

|

|

|||

| Total |

$ | 695,746 | ||

| Allocation of consideration |

||||

| Cash and cash equivalents |

13,687 | |||

| Receivables and other current assets |

14,069 | |||

| Intangible assets(2) |

601,247 | |||

| Other current liabilities |

(17,314 | ) | ||

| Fair value of net assets acquired |

611,689 | |||

|

|

|

|||

| Goodwill resulting from the ETFS Acquisition (3) |

$ | 84,057 | ||

|

|

|

|||

14

Table of Contents

| (1) | The closing price of the Company’s common stock on April 10, 2018, the last trading day prior to the closing date of the acquisition. |

| (2) | Represents purchase price allocated to customary advisory agreements. The fair value of the intangible assets was determined using an income approach (discounted cash flow analysis) which relied upon significant unobservable inputs including a revenue growth multiple of 3% to 4% and a weighted average cost of capital of 11.6%. These intangible assets were determined to have an indefinite useful life and are not deductible for tax purposes. A deferred tax liability associated with these intangible assets was not recognized as the intangibles arose in Jersey, where the Company will be subject to a zero percent tax rate. |

| (3) | Goodwill arising from the ETFS Acquisition represents the value of expected synergies created from combining the operations of ETFS and the Company. The goodwill is not deductible for tax purposes as the transaction was structured as a stock acquisition occurring in the United Kingdom. |

Acquisition-Related Costs

During the three and nine months ended September 30, 2018, the Company incurred acquisition-related costs associated with the ETFS Acquisition of $456 and $10,446, respectively. Costs incurred during the three months ended September 30, 2018 were primarily related to the integration of ETFS. Costs incurred during the nine months ended September 30, 2018 included professional advisor fees, severance and other compensation costs, a write-off of the Company’s office lease and other integration costs.

Operating Results of ETFS

The Company’s Consolidated Statements of Operations include the following operating results of ETFS since the acquisition date of April 11, 2018 through September 30, 2018:

| Revenues: |

$37,137 | |

| Income before taxes: |

$33,496 (including a gain on revaluation of deferred consideration of $17,630) |

Supplemental Unaudited Pro Forma Financial Information

The following table presents unaudited pro forma financial information of the Company as if the ETFS Acquisition had been consummated on January 1, 2017. The information was derived from the historical financial results of the Company and ETFS for all periods presented and was adjusted to give effect to pro forma events that are directly attributable to the acquisition, factually supportable and expected to have a continuing impact on the combined results following the acquisition.

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Revenues |

n/a | $ | 78,594 | $ | 229,674 | $ | 228,004 | |||||||||

| Net income |

n/a | $ | 6,736 | $ | 48,088 | $ | 22,011 | |||||||||

Included within the pro forma financial information above is a gain/(loss) on revaluation of deferred consideration of ($4,869) for the three months ended September 30, 2017, and $4,670 and ($15,088) for the nine months ended September 30, 2018 and 2017, respectively. Significant adjustments to the unaudited pro forma financial information above include the recognition of interest expense associated with the Credit Facility for the periods presented, eliminating acquisition-related costs directly attributable to the acquisition and adjusting consolidated income tax expense based upon the Company’s anticipated normalized consolidated effective tax rate.

The unaudited pro forma financial information above is not necessarily indicative of what the combined results of the Company would have been had the acquisition been completed as of January 1, 2017 and does not purport to project the future results of the combined company. In addition, the unaudited pro forma financial information does not reflect any future planned cost savings initiatives following the completion of the acquisition.

15

Table of Contents

4. Cash and Cash Equivalents

Cash and cash equivalents of approximately $32,412 and $24,103 at September 30, 2018 and December 31, 2017, respectively, were held at one financial institution. At September 30, 2018 and December 31, 2017, cash equivalents were approximately $5,722 and $26,548, respectively.

5. Fair Value Measurements

Securities owned and securities sold, but not yet purchased are measured at fair value. The fair value of securities is defined as the price that would be received to sell an asset or paid to transfer a liability (i.e., “the exit price”) in an orderly transaction between market participants at the measurement date. Accounting Standards Codification (“ASC”) 820, Fair Value Measurements, establishes a hierarchy for inputs used in measuring fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs by requiring that the most observable inputs be used when available. Observable inputs are inputs that market participants would use in pricing the asset or liability developed based on market data obtained from independent sources. Unobservable inputs reflect assumptions that market participants would use in pricing the asset or liability developed based on the best information available in the circumstances. The hierarchy is broken down into three levels based on the transparency of inputs as follows:

| Level 1 | – | Quoted prices for identical instruments in active markets. | ||||

| Level 2 | – | Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations whose inputs are observable or whose significant value drivers are observable. | ||||

| Level 3 | – | Instruments whose significant drivers are unobservable. | ||||

The availability of observable inputs can vary from product to product and is affected by a wide variety of factors, including, for example, the type of product, whether the product is new and not yet established in the marketplace, and other characteristics particular to the transaction. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised by management in determining fair value is greatest for instruments categorized in Level 3. In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement in its entirety falls is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The tables below summarize the categorization of the Company’s assets and liabilities measured at fair value. During the three and nine months ended September 2018 and 2017 there were no transfers between Levels 1, 2 and 3.

| September 30, 2018 | ||||||||||||||||

| Total | Level 1 | Level 2 | Level 3 | |||||||||||||

| Assets: |

||||||||||||||||

| Recurring fair value measurements: |

||||||||||||||||

| Cash equivalents |

$ | 5,722 | $ | 5,722 | $ | — | $ | — | ||||||||

| Securities owned, at fair value |

4,426 | 4,426 | — | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 10,148 | $ | 10,148 | — | $ | — | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Non-recurring fair value measurements: |

||||||||||||||||

| AdvisorEngine Inc. – Option(1) |

$ | 3,278 | $ | — | $ | — | $ | 3,278 | ||||||||

| Thesys Group, Inc. – Series Y preferred stock(2) |

6,909 | — | — | 6,909 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 10,187 | $ | — | $ | — | $ | 10,187 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Liabilities: |

||||||||||||||||

| Recurring fair value measurements: |

||||||||||||||||

| Deferred consideration (Note 11) |

$ | 156,055 | $ | — | $ | — | $ | 156,055 | ||||||||

| Securities sold, but not yet purchased |

2,018 | 2,018 | — | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 158,073 | $ | 2,018 | $ | — | $ | 156,055 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

16

Table of Contents

| December 31, 2017 | ||||||||||||||||

| Total | Level 1 | Level 2 | Level 3 | |||||||||||||

| Assets: |

||||||||||||||||

| Recurring fair value measurements: |

||||||||||||||||

| Cash equivalents |

$ | 26,548 | $ | 26,548 | $ | — | $ | — | ||||||||

| Securities owned, at fair value |

66,294 | 1,691 | 64,603 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 92,842 | $ | 28,239 | $ | 64,603 | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Non-recurring fair value measurements: |

||||||||||||||||

| AdvisorEngine Inc. – Option(1) |

$ | 3,278 | — | — | $ | 3,278 | ||||||||||

| Thesys Group, Inc. – Series Y preferred stock(2) |

6,909 | — | — | 6,909 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 10,187 | $ | — | $ | — | $ | 10,187 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Liabilities: |

||||||||||||||||

| Recurring fair value measurements: |

||||||||||||||||

| Securities sold, but not yet purchased |

$ | 950 | $ | 950 | $ | — | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 950 | $ | 950 | $ | — | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | Fair value determined on December 29, 2017 (See Note 9). |

| (2) | Fair value determined on June 20, 2017 (See Note 9). |

Recurring Fair Value Measurements - Methodology

Cash and Cash Equivalents (Note 4) – These financial assets represent cash in banks or cash invested in highly liquid investments with original maturities less than 90 days. These investments are valued at par, which approximates fair value, and are considered Level 1.

Securities Owned/Sold but Not Yet Purchased (Note 6) – Securities owned and sold, but not yet purchased include investments in ETFs and short-term investment grade corporate bonds. ETFs are generally traded in active, quoted and highly liquid markets and are therefore classified as Level 1 in the fair value hierarchy. Investments in short-term investment grade corporate bonds are classified as Level 2 as fair value is generally derived from observable bids for these financial instruments.

Deferred Consideration – Deferred consideration represents the present value of an obligation to pay gold into perpetuity and was measured at September 30, 2018 using forward-looking gold prices ranging from $1,193 per ounce to $2,693 per ounce which are extrapolated from the last observable price (beyond 2024), discounted at a rate of 10%. This obligation is classified as Level 3 as the discount rate and extrapolated forward-looking gold prices are significant unobservable inputs. An increase in gold prices would result in an increase in deferred consideration, whereas, an increase in the discount rate would reduce the fair value. See Note 11 for additional information.

The following table presents a reconciliation of beginning and ending balances of recurring fair value measurements classified as Level 3:

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Deferred consideration (See Note 11) |

||||||||||||||||

| Beginning balance |

$ | 162,848 | $ | — | $ | 172,746 | (1) | $ | — | |||||||

| Net realized losses/(gains)(2) |

2,880 | — | 5,595 | — | ||||||||||||

| Net unrealized losses/(gains)(3) |

(7,732 | ) | — | (17,630 | ) | — | ||||||||||

| Settlements |

(1,941 | ) | — | (4,656 | ) | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Ending balance |

$ | 156,055 | $ | — | $ | 156,055 | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | Arose in connection with the completion of the ETFS Acquisition on April 11, 2018 (See Note 3). |

| (2) | Recorded as contractual gold payments expense on the Company’s Consolidated Statements of Operations. |

| (3) | Recorded as gain on revaluation of deferred consideration on the Company’s Consolidated Statements of Operations. |

17

Table of Contents

6. Securities Owned/Sold but Not Yet Purchased

These securities consist of securities classified as trading and available-for-sale, as follows:

| September 30, 2018 |

December 31, 2017 |

|||||||

| Securities Owned |

||||||||

| Trading securities |

$ | 4,426 | $ | 1,691 | ||||

| Available-for-sale debt securities |

— | 64,603 | ||||||

|

|

|

|

|

|||||

| Total |

$ | 4,426 | $ | 66,294 | ||||

|

|

|

|

|

|||||

| Securities Sold, but not yet Purchased |

||||||||

| Trading securities |

$ | 2,018 | $ | 950 | ||||

| Available-for-sale debt securities |

— | — | ||||||

|

|

|

|

|

|||||

| Total |

$ | 2,018 | $ | 950 | ||||

|

|

|

|

|

|||||

Available-for-Sale Debt Securities

The following table summarizes unrealized gains, losses and fair value of the available-for-sale debt securities:

| September 30, 2018 |

December 31, 2017 |

|||||||

| Cost |

$ | — | $ | 65,237 | ||||

| Gross unrealized gains in other comprehensive income |

— | — | ||||||

| Gross unrealized losses in other comprehensive income |

— | (634 | ) | |||||

|

|

|

|

|

|||||

| Fair value |

$ | — | $ | 64,603 | ||||

|

|

|

|

|

|||||

During the three and nine months ended September 30, 2018, the Company received $0 and $64,498, respectively, of proceeds from the sale and maturity of available-for-sale securities and recognized gross realized losses of $0 and $739, respectively.

During the three and nine months ended September 30, 2017, the Company received $19,003 and $65,067, respectively, of proceeds from the sale and maturity of available-for-sale securities and recognized gross realized losses of $277 and $687, respectively.

Realized losses have been reclassified out of accumulated other comprehensive income and into the Consolidated Statements of Operations.

7. Securities Held-to-Maturity

The following table is a summary of the Company’s securities held-to-maturity:

| September 30, 2018 |

December 31, 2017 |

|||||||

| Federal agency debt instruments (amortized cost) |

$ | 20,199 | $ | 21,299 | ||||

|

|

|

|

|

|||||

The following table summarizes unrealized gains, losses, and fair value of securities held-to-maturity:

| September 30, 2018 |

December 31, 2017 |

|||||||

| Cost/amortized cost |

$ | 20,199 | $ | 21,299 | ||||

| Gross unrealized gains |

4 | 9 | ||||||

| Gross unrealized losses |

(2,232 | ) | (1,257 | ) | ||||

|

|

|

|

|

|||||

| Fair value |

$ | 17,971 | $ | 20,051 | ||||

|

|

|

|

|

|||||

The Company assesses these securities for other-than-temporary impairment on a quarterly basis. No securities were determined to be other-than-temporarily impaired at September 30, 2018 or December 31, 2017. The Company does not intend to sell these securities and it is not more-likely-than-not that the Company will be required to sell the securities before recovery of their amortized cost bases, which may be maturity.

18

Table of Contents

The following table sets forth the maturity profile of the securities held-to-maturity; however, these securities may be called prior to maturity date:

| September 30, 2018 |

December 31, 2017 |

|||||||

| Due within one year |

$ | — | $ | 1,000 | ||||

| Due one year through five years |

4 | 11 | ||||||

| Due five years through ten years |

6,025 | 6,027 | ||||||

| Due over ten years |

14,170 | 14,261 | ||||||

|

|

|

|

|

|||||

| Total |

$ | 20,199 | $ | 21,299 | ||||

|

|

|

|

|

|||||

8. Note Receivable

On December 29, 2017, the Company committed to provide up to $30,000 in additional working capital to AdvisorEngine Inc. (“AdvisorEngine”) pursuant to an unsecured promissory note, all of which has been funded. The majority of the funds were used by AdvisorEngine to acquire CRM Software, Inc., known as Junxure, a comprehensive client relationship management software and technology provider for financial advisors.

All principal amounts under the note bear interest from the date such amounts are advanced until repaid at a rate of 5% per annum, provided that immediately upon the occurrence and during the continuance of an event of default (as defined), interest will be increased to 10% per annum. All accrued and unpaid interest is treated as paid-in-kind (“PIK”) by capitalizing such amount and adding it to the principal amount of the original note. AdvisorEngine has the option to prepay the note, in whole or in part, at any time without premium or penalty. All borrowings under the promissory note mature on December 29, 2021.

In connection with providing funding to AdvisorEngine for the acquisition of Junxure, the Company secured an option to purchase the remaining equity interests in AdvisorEngine. The option was ascribed a fair value of $3,278 (See Note 9) which gave rise to original issue discount reducing the carrying value of the note.

The following is a summary of the outstanding note receivable balance:

| September 30, 2018 |

December 31, 2017 |

|||||||

| Note receivable (face value) |

$ | 30,000 | $ | 22,000 | ||||

| Less: Original issue discount (“OID”), unamortized |

(2,788 | ) | (3,252 | ) | ||||

| Plus: PIK interest |

909 | — | ||||||

|

|

|

|

|

|||||

| Total note receivable, net |

$ | 28,121 | $ | 18,748 | ||||

|

|

|

|

|

|||||

| Commitment remaining |

n/a | $ | 8,000 | |||||

|

|

|

|

|

|||||

During the three and nine months ended September 30, 2018, the Company recognized interest income of $533 and $1,373, respectively, which included OID amortization and accrued PIK interest. The Company determined that an allowance for credit loss was not necessary at September 30, 2018 and December 31, 2017 as the note receivable was recently issued and no adverse events or circumstances have occurred which may indicate that its carrying amount may not be recoverable. The carrying value of the note receivable at September 30, 2018 and December 31, 2017 approximates fair value as the implied discount rate of the note is similar to observable high yield credit spreads.

9. Investments, Carried at Cost

The following table sets forth the Company’s investments, carried at cost:

| September 30, 2018 |

December 31, 2017 |

|||||||

| AdvisorEngine – Preferred stock |

$ | 25,000 | $ | 25,000 | ||||

| AdvisorEngine – Option |

3,278 | 3,278 | ||||||

| Thesys Group, Inc. (“Thesys”) |

6,909 | 6,909 | ||||||

|

|

|

|

|

|||||

| Total |

$ | 35,187 | $ | 35,187 | ||||

|

|

|

|

|

|||||

19

Table of Contents

AdvisorEngine

Preferred Stock

On November 18, 2016, the Company made a $20,000 strategic investment in AdvisorEngine, an end-to-end wealth management platform which enables individual customization of investment philosophies. The Company and AdvisorEngine also entered into an agreement whereby the Company’s asset allocation models are made available through AdvisorEngine’s open architecture platform and the Company actively introduces the platform to its distribution network. In consideration of its investment, the Company received 11,811,856 shares of Series A convertible preferred shares (“Series A Preferred”).

The Series A Preferred is convertible into common stock at the option of the Company and contains various rights and protections including a non-cumulative 6.0% dividend, payable if and when declared by the board of directors, and a liquidation preference that is senior to all other holders of capital stock of AdvisorEngine.

On April 27, 2017, the Company invested an additional $5,000 in AdvisorEngine to help facilitate AdvisorEngine’s acquisition of Kredible Technologies, Inc., a technology enabled, research-driven practice management firm designed to help advisors acquire new clients, and to continue to fuel AdvisorEngine’s growth, leadership and innovation in the advisor solutions space. The Company received 2,646,062 shares of Series A-1 convertible preferred stock which has substantially the same terms as the Series A Preferred.

The Company’s aggregate equity ownership interest in AdvisorEngine is approximately 47% (or 41% on a fully-diluted basis). The investment is accounted for under the cost method of accounting as it is not considered to be in-substance common stock. No impairment existed at September 30, 2018 or December 31, 2017 and there were no observable price changes during the three and nine months ended September 30, 2018.

Option