ANNUAL INFORMATION FORM

FOR THE YEAR ENDED DECEMBER 31, 2020

AS AT MARCH 29, 2021

TABLE OF CONTENTS

INTRODUCTORY NOTES

Forward-Looking Statements

This Annual Information Form ("AIF"), including the documents incorporated by reference, contains forward-looking statements and forward-looking information (collectively referred to as "forward-looking statements") which may not be based on historical fact, including without limitation statements regarding our expectations in respect of future financial position, business strategy, future production, reserve potential, feasibility of development projects, exploration drilling, exploitation activities, events or developments that we expect to take place in the future, projected costs and plans and objectives, financial capacity to complete anticipated development projects, and anticipated effects of changes in taxation levels on the value of development projects. Often, but not always, forward-looking statements can be identified by the use of the words "believes", "may", "plan", "will", "estimate", "scheduled", "continue", "anticipates", "intends", "expects", "aim" and similar expressions.

Such statements reflect our current views with respect to future events and are subject to risks and uncertainties. These statements are necessarily based upon a number of estimates and assumptions that are inherently subject to significant business, economic, competitive, political and social uncertainties and contingencies. Many factors could cause our actual results, performance or achievements to be materially different from any future results, performance, or achievements that may be expressed or implied by such forward-looking statements, including, among others:

-

uncertainties about the effect of the novel coronavirus ("COVID-19") and the response of local, provincial, state, federal and international governments to the threat of COVID-19, on our operations (including our suppliers, customers, supply chain, employees and contractors) and economic conditions generally and in particular with respect to the demand for copper and other metals we produce;

-

uncertainties about the future market price of copper and the other metals that we produce or may seek to produce;

-

changes in general economic conditions, the financial markets and in the demand and market price for our input costs, such as diesel fuel, reagents, steel, concrete, electricity and other forms of energy, mining equipment, and fluctuations in exchange rates, particularly with respect to the value of the U.S. dollar and Canadian dollar, and the continued availability of capital and financing;

-

inherent risks associated with mining operations, including our current mining operations at Gibraltar, and their potential impact on our ability to achieve our production estimates;

-

uncertainties as to our ability to control our operating costs at Gibraltar without impacting our planned copper production;

- 3 -

-

the risk of inadequate insurance or inability to obtain insurance to cover material mining risks;

-

uncertainties related to the feasibility study for Florence copper project (the "Florence Copper Project" or "Florence Copper") that provides estimates of expected or anticipated capital and operating costs, expenditures and economic returns from this mining project;

-

the risk that the results from our operations of the Florence Copper production test facility ("PTF") and ongoing engineering work including cost updates will negatively impact our estimates for current projected economics for commercial operations at Florence Copper;

-

uncertainties related to the accuracy of our estimates of Mineral Reserves (as defined below), Mineral Resources (as defined below), production rates and timing of production, future production and future cash and total costs of production and milling;

-

the risk that we may not be able to expand or replace reserves as our existing mineral reserves are mined;

-

the availability of, and uncertainties relating to the development of, additional financing and infrastructure necessary for the advancement of our projects, including with respect to our ability to obtain the required remaining construction financing to move forward with commercial operations at Florence Copper;

-

our ability to comply with the extensive governmental regulation to which our business is subject;

-

uncertainties related to our ability to obtain necessary title, licenses and permits for our development projects and project delays due to third party opposition, particularly in respect to Florence Copper that requires one key regulatory permit from the U.S. Environmental Protection Agency ("EPA") in order to advance to commercial operations;

-

uncertainties related to First Nations claims and consultation issues;

-

our reliance on rail transportation and port terminals for shipping our copper concentrate production from Gibraltar;

-

uncertainties related to unexpected judicial or regulatory proceedings;

-

changes in, and the effects of, the laws, regulations and government policies affecting our exploration and development activities and mining operations;

-

our dependence solely on our 75% interest in Gibraltar (as defined below) for revenues and operating cashflows;

-

our ability to extend existing concentrate off-take agreements or enter into new agreements;

- 4 -

-

environmental issues and liabilities associated with mining including processing and stock piling ore;

-

labour strikes, work stoppages, or other interruptions to, or difficulties in, the employment of labour in markets in which we operate our mine, industrial accidents, equipment failure or other events or occurrences, including third party interference that interrupt the production of minerals in our mine;

-

environmental hazards and risks associated with climate change, including the potential for damage to infrastructure and stoppages of operations due to forest fires, flooding, drought, or other natural events in the vicinity of our operations;

-

litigation risks and the inherent uncertainty of litigation, including litigation to which Florence Copper is subject;

-

our actual costs of reclamation and mine closure may exceed our current estimates of these liabilities;

-

our ability to renegotiate our existing union agreement for Gibraltar when it expires in June 2021;

-

the capital intensive nature of our business both to sustain current mining operations and to develop any new projects;

-

our reliance upon key management and operating personnel;

-

the competitive environment in which we operate;

-

the effects of forward selling instruments to protect against fluctuations in copper prices, foreign exchange or input costs such as fuel;

-

the risk of changes in accounting policies and methods we use to report our financial condition, including uncertainties associated with critical accounting assumptions and estimates; and Management Discussion and Analysis ("MD&A"), quarterly reports and material change reports filed with and furnished to securities regulators, and those risks which are discussed under the heading "Risk Factors".

Such information is included, among other places, in this AIF under the headings "Taseko's Business" and "Risk Factors".

Should one or more of these risks and uncertainties materialize, or should underlying factors or assumptions prove incorrect, actual results may vary materially from those described in forward-looking statements. Material factors or assumptions involved in developing forward-looking statements include, without limitation, that:

- 5 -

-

COVID-19, and the response of governments thereto, will not result in a material slow down or stoppage of our mining operations, disrupt our permitting activities or the timing of the response of government agencies to our permitting activities;

-

the price of copper and other metals will not decline significantly or for a protracted period of time;

-

our mining operations will not experience any significant production disruptions that would materially affect our production forecasts or our revenues;

-

our estimates regarding future capital and operating costs at Gibraltar will be accurate;

-

grades and recoveries at Gibraltar remain consistent with current mine plans;

-

we will be able to incorporate the Gibraltar pit into our operations as planned;

-

the results from our operations of the PTF at Florence Copper will continue to support that commercial operations at Florence Copper are technically and economically feasible;

-

we will be able to obtain the remaining construction financing necessary for us to advance Florence Copper to a positive construction decision and eventual commercial production;

-

we will be able to obtain the required permits necessary for us to proceed with construction and commercial operations at Florence;

-

litigation regarding Florence Copper will not materially impede or delay our ability to proceed with construction and commercial operations at Florence;

-

there are no changes to any existing agreements or relationships with affected First Nations groups which would materially and adversely impact our operations;

-

there are no adverse regulatory changes affecting any of our operations;

-

exchange rates, prices of key consumables, costs of power, labour, material costs, supplies and services, and other cost assumptions at our projects are not significantly higher than prices assumed in planning;

-

our mineral reserve and resource estimates and the assumptions on which they are based, are accurate;

-

our estimates of reclamation liabilities and mine closure costs are accurate; and

-

we will continue to generate positive cash flows from Gibraltar and be able to secure additional funding necessary for the development and continued advancement of our development projects.

These factors should be considered carefully and readers are cautioned not to place undue reliance on any forward-looking statements. Readers are also cautioned that the foregoing list of risk factors is not exhaustive and it is recommended that prospective investors carefully read the more complete discussion of risks and uncertainties facing the Company included under "Risk Factors" in this AIF.

- 6 -

Although the Company believes that the expectations conveyed by the forward-looking statements are reasonable based on the information available to it on the date such statements were made, no assurances can be given as to future results, approvals or achievements. The forward-looking statements contained in this AIF and the documents incorporated by reference herein are expressly qualified by this cautionary statement. The Company disclaims any duty to update any of the forward-looking statements after the date of the AIF to conform such statements to actual results or to changes in the Company's expectations except as otherwise required by applicable law.

Documents Incorporated by Reference

Incorporated by reference into this AIF are the audited consolidated financial statements, together with the auditors' report thereon, and MD&A for Taseko Mines Limited for the year ended December 31, 2020. The financial statements are available for review on the SEDAR website at www.sedar.com. All financial information in this AIF is prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board and expressed in Canadian dollars.

Non-GAAP Performance Measures

This AIF, including the documents incorporated by reference, includes the following non-GAAP performance measures: (i) total operating costs and site operating costs, net of by-product credits; (ii) adjusted net income (loss); (iii) Adjusted EBITDA; (iv) earnings from mining operations before depletion and amortization. These measures may differ from those used by, and may not be comparable to such measures as reported by, other issuers. The Company believes that these measures are commonly used by certain investors, in conjunction with conventional IFRS measures, to enhance their understanding of the Company's performance. These measures have been derived from the Company's financial statements and applied on a consistent basis. See "Non-GAAP Performance Measures" in our MD&A for the year ended December 31, 2020 for a reconciliation of these measures to the most directly comparable IFRS measure.

Currency and Metric Equivalents

The Company's accounts are maintained in Canadian dollars and all dollar amounts herein are expressed in Canadian dollars unless otherwise indicated.

The following factors for converting Imperial measurements into metric equivalents are provided:

- 7 -

|

To Convert from Imperial |

To Metric |

Multiply by |

|

acres |

hectares |

0.405 |

|

feet |

metres |

0.305 |

|

miles |

kilometres |

1.609 |

|

tons (2,000 pounds) |

tonnes |

0.907 |

|

ounces (troy)/ton |

grams/tonne |

34.286 |

In this AIF, the following capitalized terms have the defined meanings set forth below:

|

ASCu |

The weight percentage of copper per unit weight of rock that is acid soluble, including native copper. |

|

ADEQ |

Arizona Department of Environmental Quality. |

|

APP and TAPP |

Aquifer Protection Permit and Temporary Aquifer Protection Permit. |

|

Common Shares |

The Company's common shares without par value, being the only class or kind of the Company's authorized capital. |

|

Carbonatite Deposit |

Carbonatite deposits are igneous rocks largely consisting of the carbonate minerals calcite and dolomite, which contain the niobium mineral pyrochlore, rare earth minerals or copper sulphide minerals. |

|

Concentrator |

A type of mineral processing facility that converts raw ore from the mine into a metal concentrate that can then be sold to a smelter for further processing. |

|

EPA |

U.S. Environmental Protection Agency. |

|

Epithermal Deposit |

A mineral deposit formed at low temperature (50 to 200°C), usually within one kilometre of the earth's surface, often as structurally controlled veins. |

|

Flotation |

Flotation is a method of mineral separation whereby, after crushing and grinding ore, froth created in a slurry by a variety of reagents causes some finely crushed minerals to float to the surface where they are skimmed off. |

|

ISCR |

In-situ copper recovery. |

|

LSE |

The London Stock Exchange being one of the three stock exchanges (together with the NYSE American and TSX) on which the Common Shares are listed. |

|

NSR |

Net smelter return, a general proxy for the gross value of metals derived from concentrates delivered to a smelter for refining. |

- 8 -

|

Mineral Deposit |

A deposit of mineralization, which may or may not be ore. |

|

Mineral Symbols |

Ag - silver; Au - gold; Cu - copper; Pb - lead; Zn - Zinc; Mo - molybdenum; and Nb - niobium. |

|

NYSE American |

The NYSE American, being one of the three stock exchanges (together with the LSE and TSX) on which the Common Shares are listed. |

|

PLS |

Pregnant leach solutions containing copper. |

|

PTF |

The production test facility, a 24-well ISCR operation designed to prove the feasibility of extracting copper at Florence Copper using in-situ mining methods. |

|

Porphyry Deposit |

A type of mineral deposit in which ore minerals are widely disseminated, generally of low grade but large tonnage. |

|

Semi-autogenous Grinding ("SAG") |

SAG mills are essentially autogenous mills, but utilize grinding balls to aid in grinding like in a ball mill. A SAG mill is generally used as a primary or first stage grinding solution. |

|

Solvent Extraction/ |

Solvent extraction is the technique of transferring a solute from one solution to another; for example when copper oxide is dissolved into solution, copper becomes the solute. Electrowinning is the process in which an electric current flows between a pair of electrodes (anode & cathode) in a solution containing metal ions (electrolyte). Metal is deposited on the cathode in accordance with the metal's ability to gain or lose electrons. Since ion deposition is selective, the cathode product is generally high grade and requires little further refining. |

|

Taseko or the Company |

Taseko Mines Limited, including its subsidiaries, unless the context requires otherwise. |

|

TSX |

The Toronto Stock Exchange, being one of the three stock exchanges (together with the LSE and NYSE American) on which the Company's Common Shares are listed. |

|

UIC |

Underground Injection Control permit. |

Resource and Reserve Categories (Classifications) Used in this AIF

The discussion of mineral deposit classifications in this AIF adheres to the resource/reserve definitions and classification criteria developed by the Canadian Institute of Mining, Metallurgy and Petroleum (the "CIM Council") as required reporting standards in Canada and in accordance with Canadian National Instrument 43-101 Standards of Disclosure for Mineral Projects ("NI 43-101"). Estimated mineral resources fall into two broad categories dependent on whether their economic viability has been established and these are namely "resources" (economic viability not established) and "reserves" (viable economic production is feasible). Resources are sub-divided into categories depending on the confidence level of the estimate based on level of detail of sampling and geological understanding of the deposit. The categories, from lowest confidence to highest confidence, are inferred resource, indicated resource and measured resource. Similarly reserves are sub-divided by order of confidence into probable (lowest) and proven (highest). These classifications can be more particularly described as follows in accordance with the CIM Definition Standards on Mineral Resources and Reserves (the "2014 CIM Standards") adopted by the CIM Council on May 10, 2014:

- 9 -

A "feasibility study" is a comprehensive technical and economic study of the selected development option for a mineral project that includes appropriately detailed assessments of applicable modifying factors together with any other relevant operational factors and detailed financial analysis that are necessary to demonstrate, at the time of reporting, that extraction is reasonably justified (economically mineable). The results of the study may reasonably serve as the basis for a final decision by a proponent or financial institution to proceed with, or finance, the development of the project. The confidence level of the study will be higher than that of a pre-feasibility study.

A "Mineral Resource" is a concentration or occurrence of solid material of economic interest in or on the Earth's crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade or quality, continuity and other geological characteristics of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling.

An "Inferred Mineral Resource" is that part of a Mineral Resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. Geological evidence is sufficient to imply, but not verify geological, and grade or quality continuity. An Inferred Mineral Resource has a lower level of confidence than that applying to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of Inferred Mineral Resources could be upgraded to Indicated Mineral Resources with continued exploration.

An "Indicated Mineral Resource" is that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics are estimated with sufficient confidence to allow the application of Modifying Factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Geological evidence is derived from adequately detailed and reliable exploration, sampling and testing and is sufficient to assume geological and grade or quality continuity between points of observation. An Indicated Mineral Resource has a lower level of confidence than that applying to a Measured Mineral Resource and may only be converted to a Probable Mineral Reserve.

A "Measured Mineral Resource" is that part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are estimated with confidence sufficient to allow the application of Modifying Factors to support detailed mine planning and final evaluation of the economic viability of the deposit. Geological evidence is derived from detailed and reliable exploration, sampling and testing and is sufficient to confirm geological and grade or quality continuity between points of observation. A Measured Mineral Resource has a higher level of confidence than that applying to either an Indicated Mineral Resource or an Inferred Mineral Resource. It may be converted to a Proven Mineral Reserve or to a Probable Mineral Reserve.

- 10 -

A "Mineral Reserve" is the economically mineable part of a Measured and/or Indicated Mineral Resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or extracted and is defined by studies at Pre-Feasibility or Feasibility level as appropriate that include application of Modifying Factors. Such studies demonstrate that, at the time of reporting, extraction could reasonably be justified. The U.S. Securities and Exchange Commission require permits in hand or their issuance imminent to classify mineralized material as reserves.

A "pre-feasibility study" is a comprehensive study of a range of options for the technical and economic viability of a mineral project that has advanced to a stage where a preferred mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, is established and an effective method of mineral processing is determined. It includes a financial analysis based on reasonable assumptions on the modifying factors and the evaluation of any other relevant factors which are sufficient for a Qualified Person, acting reasonably, to determine if all or part of the mineral resource may be converted to a mineral reserve at the time of reporting. A pre-feasibility is at a lower confidence level than a feasibility study.

A "Probable Mineral Reserve" is the economically mineable part of an Indicated Mineral Resource, and in some circumstances, a Measured Mineral Resource. The confidence in the Modifying Factors applying to a Probable Mineral Reserve is lower than that applying to a Proven Mineral Reserve.

A "Proven Mineral Reserve" is the economically mineable part of a Measured Mineral Resource. A Proven Mineral Reserve implies a high degree of confidence in the Modifying Factors.

"Modifying Factors" are considerations used to convert Mineral Resources to Mineral Reserves. These include, but are not restricted to, mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social and governmental factors.

CAUTIONARY NOTE TO UNITED STATES INVESTORS CONCERNING ESTIMATES OF RESERVES AND MEASURED, INDICATED AND INFERRED RESOURCES

The disclosure in this AIF, including the documents incorporated by reference herein, uses terms that comply with reporting standards in Canada in accordance with NI 43-101 and the 2014 CIM Standards. NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Unless otherwise indicated, all reserve and resource estimates contained in or incorporated by reference in this AIF have been prepared in accordance with NI 43-101 and the 2014 CIM Standards.

- 11 -

The SEC has adopted amendments to its disclosure rules to modernize the mineral property disclosure requirements for issuers whose securities are registered with the SEC under the U.S. Exchange Act, effective February 25, 2019 (the "SEC Modernization Rules"). The SEC Modernization Rules replace the historical property disclosure requirements for mining registrants that were included in SEC Industry Guide 7.

The SEC Modernization Rules include the adoption of definitions of terms, which are "substantially similar" to the corresponding terms under the 2014 CIM Standards that are presented above under "Resource and Reserve Categories (Classifications) Used in this AIF".

We will not be required to provide disclosure on our mineral properties under the SEC Modernization Rules as we are presently a "foreign issuer" under the U.S. Exchange Act and entitled to file continuous disclosure reports with the SEC under the Multijurisdictional Disclosure System ("MJDS") between Canada and the United States. Accordingly, we anticipate that we will be entitled to continue to provide disclosure on our mineral properties in accordance with NI 43-101 disclosure standards and CIM Definition Standards. However, if we either cease to be a "foreign issuer" or cease to be able to or entitled to file reports under the MJDS, then we will be required to provide disclosure on our mineral properties under the SEC Modernization Rules. Accordingly, United States investors are cautioned that the disclosure that we provide on our mineral properties in the AIF and under our continuous disclosure obligations under the U.S. Exchange Act may be different from the disclosure that we would otherwise be required to provide as a U.S. domestic issuer or a non-MJDS foreign issuer under the SEC Modernization Rules.

United States investors are cautioned that while the above terms under the SEC Modernization Rules are "substantially similar" to CIM Definitions, there are differences in the definitions under the SEC Modernization Rules and the CIM Definition Standards. Accordingly, there is no assurance any resources and reserves that we may report as "measured mineral resources", "indicated mineral resources" and "inferred mineral resources" and "proven mineral reserves" and "probable mineral reserves" under NI 43-101 would be the same had we prepared these estimates under the standards adopted under the SEC Modernization Rules.

United States investors are also cautioned that while the SEC now recognizes "measured mineral resources", "indicated mineral resources" and "inferred mineral resources", investors should not assume that any part or all of the mineral deposits in these categories will ever be converted into a higher category of mineral resources or into mineral reserves. Mineralization described by these terms has a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. Accordingly, investors are cautioned not to assume that any "measured mineral resources", "indicated mineral resources", or "inferred mineral resources" that we report in this AIF are or will be economically or legally mineable.

Further, "inferred resources" have a great amount of uncertainty as to their existence and as to whether they can be mined legally or economically. Therefore, United States investors are also cautioned not to assume that all or any part of the inferred resources exist. In accordance with Canadian rules, estimates of "inferred mineral resources" cannot form the basis of feasibility or other economic studies, except in limited circumstances where permitted under NI 43-101.

- 12 -

For the above reasons, information contained in this AIF and the documents incorporated by reference herein containing descriptions of our mineral deposits may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

CORPORATE STRUCTURE

Taseko Mines Limited was incorporated on April 15, 1966, pursuant to the Company Act (British Columbia). This corporate legislation was superseded in 2004 by the British Columbia Business Corporations Act which is now the corporate law statute that governs us. Our registered office is located at Suite 1500, 1055 West Georgia Street, Vancouver, British Columbia, V6E 4N7, and our head office is located at Suite 1200, 1040 West Georgia Street, Vancouver, British Columbia, V6E 4H1.

The following is a list of the Company's principal subsidiaries:

|

Subsidiary |

Jurisdiction of |

Ownership |

|

Gibraltar Mines Ltd. 1 |

British Columbia |

100% |

|

Curis Holdings (Canada) Ltd. 2 |

British Columbia |

100% |

|

Florence Holdings Inc. 2 |

Nevada, USA |

100% |

|

Florence Copper Inc. 2 |

Nevada, USA |

100% |

|

Yellowhead Mining Inc. |

British Columbia |

100% |

|

Aley Corporation |

British Columbia |

100% |

|

Taseko Holdings Ltd. |

British Columbia |

100% |

|

1280860 BC Ltd. |

British Columbia |

100% |

1. Taseko owns 100% of Gibraltar Mines Ltd., which owns 75% of the Gibraltar Joint Venture.

2. Taseko owns 100% of Curis Holdings (Canada) Ltd., which owns 100% of Florence Holdings Inc., which owns 100% of Florence Copper Inc.

Gibraltar Joint Venture

On March 31, 2010, we established an unincorporated joint venture ("JV") between Gibraltar Mines Ltd., and Cariboo Copper Corp. ("Cariboo") over the Gibraltar copper and molybdenum mine (the "Gibraltar Mine" or "Gibraltar"), whereby Cariboo acquired a 25% interest in the Gibraltar Mine and we retained a 75% interest with Gibraltar Mines Ltd. operating the mine for the two JV participants. Under the related Joint Venture Formation Agreement ("JVFA"), the Company contributed to the Joint Venture substantially all assets and obligations pertaining to the Gibraltar Mine, and Cariboo paid the Company $187 million to obtain its 25% interest in the JV. Gibraltar Mines Ltd. continues to be the operator of the Gibraltar Mine under the Joint Venture Operating Agreement (the "JVOA") which is filed at www.sedar.com. Cariboo is a Japanese consortium jointly owned by Sojitz Corporation (50%), Dowa Metals & Mining Co., Ltd. (25%) and Furukawa Co., Ltd. (25%).

- 13 -

TASEKO's BUSINESS

Taseko is a Vancouver, B.C. headquartered mining company that seeks to create long-term shareholder value by acquiring, developing, and operating large tonnage mineral deposits which are capable of supporting a mine for ten years or longer. The Company's principal operating asset is the 75% owned Gibraltar Mine, which is located in central British Columbia and is one of the largest copper mines in North America. Taseko also owns Florence Copper, an advanced stage project which is nearing a construction decision, as well as the Yellowhead copper, New Prosperity copper-gold, Aley niobium and Harmony gold projects.

Taseko's mineral properties are summarized in the table below.

|

Project/Mine |

Ownership Interest |

Location |

Principal Mineralization |

|

Gibraltar Mine |

75% |

British Columbia |

Copper/ Molybdenum/ Silver |

|

Florence Copper |

100% |

Arizona, USA |

Copper |

|

Yellowhead |

100% |

British Columbia |

Copper/ Gold/ Silver |

|

New Prosperity |

100% |

British Columbia |

Copper/ Gold |

|

Aley |

100% |

British Columbia |

Niobium |

|

Harmony |

100% |

British Columbia |

Gold |

The map below highlights the location of our mineral properties:

- 14 -

Figure 1: Location of Taseko's Properties

Gibraltar

Taseko's principal operating asset is its 75% joint venture interest in the Gibraltar Mine in British Columbia, Canada. Gibraltar is the second largest open pit copper mine in Canada, having produced 123 million pounds of copper and 2.3 million pounds of molybdenum (on a 100% basis) in 2020. Gibraltar also produces silver and has an expected mine life of at least 17 years based on Proven and Probable Sulphide Mineral Reserves of 538 million tons at a grade of 0.25% copper as of December 31, 2020.

Between 2006 and 2013, the Company expanded and modernized the Gibraltar Mine ore concentrator, added a second ore concentrator, increased the mining fleet and made other production improvements at the mine. Following this period of mine expansion and capital expenditure, Gibraltar has achieved a stable level of operations and the Company's focus is on further improvements to operating practices to reduce unit costs.

Florence Copper

Taseko is proceeding with the development of Florence Copper in Arizona in two phases. For the first phase, Taseko completed construction of the PTF for Florence Copper in 2018 and PTF wellfield operations commenced in the fourth quarter of 2018. Operation of the PTF has continued as planned since that time with the wellfield performing to its design, and the small-scale SX-EW plant producing cathode copper. The PTF completed the leach testing phase in June 2020 and the operation subsequently transitioned into a demonstration of rinsing the ore zone.

- 15 -

The second phase of Florence Copper will consist of the permitting, construction and operation of the commercial ISCR facility. On December 8, 2020 Taseko received the Aquifer Protection Permit ("APP") from Arizona Department of Environmental Quality ("ADEQ") which is one of two key permits required to commence certain construction and operation of the commercial-scale wellfield. Completion of the ISCR production facility has an estimated capital cost of US$230 million (including reclamation bonding and working capital). At a long-term copper price of US$3.00 per pound, Florence Copper is expected to generate an after-tax internal rate of return of 37%, an after-tax net present value of US$680 million at a 7.5% discount rate, and an after-tax payback period of 2.5 years.

With the recently concluded equity and bond financings, the Company now has the majority of the required construction funding for Florence Copper in hand. Discussions with potential joint venture partners continue to advance, but with the improved cash position and stronger expected operating cash flows from Gibraltar due to higher prevailing copper prices, the Company has numerous options available to obtain the remaining funding.

The Company is moving forward with final design engineering for the commercial production facility as well as procurement of certain critical components.

Other Development Projects

Taseko has a diverse pipeline of wholly-owned development projects at various stages of technical and economic feasibility studies, including the Yellowhead copper project, the Aley niobium project, and the New Prosperity gold and copper project (collectively as the "Other Development Projects"). Taseko also owns the Harmony gold project, an exploration stage gold property.

Business Strategy

Taseko's strategy has been to grow the Company by utilizing the cash flow from Gibraltar to acquire and develop a pipeline of projects. We continue to believe this will generate long-term returns for shareholders. Our development projects are located in British Columbia and Arizona and represent a diverse range of metals, including copper, molybdenum, gold, silver and niobium. Our project focus is currently on the development of Florence Copper.

Development of Taseko's Business over the Past Three Years

The following is a summary of the development of Taseko's business over the last three financial years:

- 16 -

2018

Construction of the Florence Copper PTF was completed on time and on budget and wellfield operations commenced in the fourth quarter. The main focus of the PTF phase was to demonstrate to regulators and key stakeholders the regulatory compliance aspects of the process and the ability to maintain hydraulic control of underground leach solutions.

In December 2018, the Company entered into an agreement to acquire all of the outstanding common shares of Yellowhead that it did not already own, in exchange for approximately 17.3 million Taseko common shares. Yellowhead holds a 100% interest in a copper-gold-silver development project located in south-central British Columbia.

2019

Commissioning of the PTF SX/EW plant for Florence Copper was completed in the first quarter of 2019 and first copper was produced in April. The PTF achieved steady state operation and the focus turned to testing different wellfield operating strategies, including adjusting pumping rates, solution strength, flow direction, and the use of packers in recovery and injection wells to isolate different zones of the orebody. PTF operations of the wellfield performed to design and the SX-EW plant produced copper cathode.

The Company submitted a permit amendment application for the commercial production facilities at Florence Copper. The APP amendment application was submitted to the ADEQ in June. The Underground Injection Control ("UIC") Permit application was submitted to the EPA in August.

In October 2019, the Company announced its intention to seek a listing of the Company's common shares on the LSE Main Market. Admission became effective and unconditional dealings in the common shares commenced on November 22, 2019. The Company did not raise capital in conjunction with the LSE admission.

In December 2019, the Tŝilhqot'in Nation, as represented by Tŝilhqot'in National Government, and Taseko entered into a dialogue, with the Province of British Columbia, to try to obtain a long-term solution to the conflict regarding Taseko's proposed gold-copper mine currently known as New Prosperity, acknowledging Taseko's commercial interests and the Tŝilhqot'in Nation's opposition to the project. The dialogue was supported by the parties' agreement on December 7, 2019, to a one year standstill on certain outstanding litigation and regulatory matters that relate to Taseko's tenures and the area in the vicinity of Teẑtan Biny (Fish Lake). The COVID-19 pandemic delayed the commencement of the dialogue for several months in 2020, but the Tŝilhqot'in Nation and Taseko have made progress in establishing a constructive dialogue. In December 2020, the parties agreed to extend the standstill for an additional one year period.

2020

In January 2020, the Company announced the results of an updated technical study on Yellowhead which resulted in a 22% increase in recoverable copper reserves and significantly improved project economics. The Company filed a new NI 43-101 technical report entitled "Technical Report on the Mineral Reserve Update at the Yellowhead Copper Project" dated January 16, 2020 on SEDAR.

- 17 -

In March 2020, the World Health Organization declared COVID-19 outbreak a pandemic creating an unprecedented global health and economic crisis. Copper prices dropped significantly in March to a low of US$2.04 per pound before recovering in the latter half of the year and ended the year at US$3.70 per pound. The Company adopted a revised mining plan in April of 2020 in response to COVID-19 which resulted in reduced site costs over the second and third quarter while maintaining copper production. Gibraltar produced a total of 123 million pounds for the year ended 2020. As of the date of this annual report, there has not been any direct impact on the Company's operations as a result of COVID-19.

In May 2020, Taseko published its first Environmental, Social, and Governance report, which includes an examination of the Company's sustainable performance, with specific details for 2017, 2018 and 2019. The report is available on the Company's website at www.tasekomines.com/esg.

By mid-2020, Taseko had successfully operated the Florence PTF for 18 months, demonstrating that the ISCR process can produce high quality cathode while operating within permit conditions. In June of 2020, the Company ceased injection of solution and by November, the last cathode was produced from the SX/EW and with total production from the PTF wellfield being approximately 1.1 million pounds. The Company is currently in the rinsing phase of the PTF operation which activities will continue in 2021.

In December 2020, the Company received the APP from the ADEQ. The APP permit was issued following a public comment period and public hearing in August 2020 where the project received strong support from local community members, business owners and elected officials. The other required key permit is the UIC from the EPA. The EPA's technical review for the UIC permit has identified no significant issues and the Company expects to receive this permit in the coming months.

In November 2020, Taseko closed an offering of 34,322,138 common shares of the Company for net proceeds of $34.3 million. The proceeds of the offering are expected to be used to fund ongoing operating, engineering and project costs in connection with the advancement of Florence Copper and for general corporate purposes and working capital.

Subsequent to December 31, 2020, the Company completed an offering of US$400 million aggregate principal amount of 7.0% Senior Secured Notes due February 15, 2026. A majority of the proceeds were used to redeem the outstanding US$250 million 8.75% Senior Secured Notes due on June 15, 2022. The remaining proceeds, net of transaction costs, call premium and accrued interest, of approximately $167 million (US$131 million) are available for capital expenditures, including at Florence Copper and the Gibraltar mine, working capital and for general corporate purposes.

Competitive Conditions

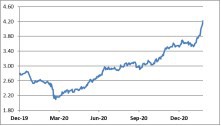

After a significant but short-lived drop in copper prices with the onset of COVID-19 in March of 2020, copper prices have recovered to over US$4.00 per pound and are now at record levels in Canadian dollar terms. Disruptions to mining operations caused by the COVID-19 pandemic, particularly in Peru and Chile where the largest copper mines in the world are located, led to supply challenges in 2020 and are expected to continue to impact supply in 2021. At the same time, Chinese demand recovered swiftly in the second half of 2020 resulting in an estimated deficit of copper of over 500,000 tonnes, the highest in more than a decade. Focus in 2021 is now turning to strong demand growth, inflation and the weaker US dollar arising from the expected economic recovery in North America and Europe. The rollout of vaccine programs will also improve the global demand outlook, further pressuring the copper supply deficit. The longer-term outlook for copper is also favorable with the focus on government investment in construction and infrastructure including initiatives focused on green sources of power and the electrification of transportation which are inherently copper intensive. This increased demand for copper after years of under investment by the industry in new mine supply is expected to support incentive copper prices in the years ahead.

- 18 -

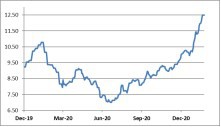

Molybdenum prices have also experienced volatility in 2020 due to the combination of a COVID-19 induced global economic slowdown and a decrease in molybdenum usage which has a particularly high dependence on demand from the oil and gas and transportation sectors. The average molybdenum price was US$8.68 per pound during 2020, compared to US$11.36 per pound in 2019. The Company's sales agreements specify molybdenum pricing based on the published Platts Metals reports.

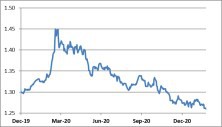

Approximately 80% of the Gibraltar Mine's costs are Canadian dollar denominated and therefore, fluctuations in the Canadian/US dollar exchange rate can have a significant effect on the Company's operating results and unit production costs, which are earned and in some cases reported in US dollars. Overall, the Canadian dollar modestly strengthened by approximately 2% during 2020 although decreased sharply in the second quarter to a low of C$1.45 per US dollar before recovering in the second half of the year.

Environmental Protection Requirements

Taseko's mining, exploration and development activities in Canada are subject to various levels of Canadian Federal and British Columbia Provincial laws and regulations relating to the protection of the environment. Similarly, Florence Copper is subject to various levels of US Federal and Arizona State laws and regulations relating to protection of the environment. All of the jurisdictions include requirements for closure and reclamation of mining properties as part of their regulatory framework.

The total liability for reclamation and closure cost obligations for the Company's share of the Gibraltar Mine and its other projects, as calculated in accordance with IFRS at December 31, 2020 was $79.0 million. This amount represents the present value of the estimated future costs of planned and anticipated closure and remediation activities, assuming a long-term nominal risk free rate of up to 2.86% and an inflation rate of 1.49%.

- 19 -

Employees

The Company had the following employees and contractors as at December 31, 2020:

|

Location |

Full-time Salaried |

Hourly |

Contractors |

|

Vancouver, BC, Canada |

25 |

- |

- |

|

McLeese Lake, BC, Canada |

171 |

538 |

17 |

|

Florence, Arizona, USA |

23 |

15 |

1 |

|

Total |

219 |

553 |

18 |

Environment, Social and Governance

In May 2020, Taseko published its first Environmental, Social, and Governance report, which includes an examination of the Company's sustainable performance, with specific details for 2017, 2018 and 2019. The report is available on the Company's website at www.tasekomines.com/esg.

Nothing is more important to Taseko than the safety, health and well-being of our workers and their families. Taseko is committed to operational practices that result in improved efficiencies, safety performance and occupational health.

Taseko places a high priority on the continuous improvement of performance in the areas of employee health and safety at the workplace and protection of the environment. In 2020, Gibraltar's days lost, loss time incidents, lost time frequency, and loss time severity were all zero. The British Columbia mining industry averages for 2020 were 0.68 for loss time frequency (per 200,000 hours worked) and 105.7 for loss time severity.

Taseko recognizes that responsible environmental management is critical to our success and has committed that it will:

-

Consider the environmental impacts of its operations and take appropriate steps to prevent environmental pollution;

-

Comply with relevant environmental legislation, regulations and corporate requirements;

-

Integrate environmental policies, programs and practices into all activities;

-

Ensure that all employees and service providers understand their environmental responsibilities and encourage dialogue on environmental issues;

-

Develop, maintain and test emergency preparedness plans to ensure protection of the environment, employees and the public;

-

Work with government and the public to develop effective and efficient measures to improve protection of the environment, based on sound science; and

-

Maintain an environmental committee to review environmental performance, objectives and targets, and to ensure continued recognition of environmental issues as a high priority.

- 20 -

The same priority on health, safety, and environmental performance, as well as the methods and culture at Gibraltar are being implemented at Florence Copper as it prepares for construction.

MINERAL PROPERTIES

Our material properties are the Gibraltar Mine and Florence Copper. Information regarding the Gibraltar Mine, Florence Copper and Yellowhead Copper Project is based on current technical reports available on SEDAR, as updated by the Company's Chief Engineer, Richard Weymark, P. Eng., MBA, (in respect of the Gibraltar Mine and Yellowhead Copper Project) and Vice President Capital Projects, Rob Rotzinger, P. Eng. (in respect of Florence Copper). Information regarding our other projects, New Prosperity and Aley, has been prepared by Richard Weymark.

Gibraltar Mine

Unless stated otherwise, information of a technical or scientific nature related to the Gibraltar Mine contained in this AIF (including documents incorporated by reference herein) is summarized or extracted from a technical report entitled "Technical Report on the Mineral Reserve Update at the Gibraltar Mine" dated November 6, 2019 (the "Gibraltar Technical Report"), prepared under the supervision of Richard Weymark, P. Eng., MBA, filed on Taseko's profile at www.sedar.com and updated with production and development results since that time. Mr. Weymark is employed by the Company as Chief Engineer and is a "Qualified Person" as defined by Canadian securities regulatory instrument NI 43-101.

Project Description, Location, and Access

The Gibraltar open pit mine and related facilities are located 65 kms north of the town of Williams Lake and are centered at latitude 52o 30'N and longitude 122o 16'W in the Cariboo Mining Division. Williams Lake is approximately 590 kms north of Vancouver, British Columbia.

Access to the Gibraltar Mine from Williams Lake is 45 kms via Highway 97 to McLeese Lake, and then 20 kilometres by paved road to the mine site.

The Gibraltar Mine property consists of 245 tenures held as summarized in Table 1 below.

Table 1: Mineral Tenures - Gibraltar Mine

|

Tenure Type |

Number |

Area (ha) |

|

Claims |

213 |

20,424 |

|

Leases |

32 |

2,275 |

|

Total |

245 |

22,699 |

There are 32 mining leases at the Gibraltar Mine which are valid until at least July 2023 as long as renewal fees, which are due on an annual basis, are paid. Rights to use the surface accompany each mining lease. There are 213 claims included in the Gibraltar property tenure package all of which are due to expire in March 2022 or later. It is intended that all leases and claims will be renewed prior to their renewal fees being due (in the case of the leases) and prior to their expiry (in the case of the claims).

- 21 -

There are several land parcels for which surface rights were purchased outright. There is one fee simple lot at the Gibraltar Mine on which the plant site is located and annual taxes are paid. In addition, the Gibraltar Mine holds three other land parcels.

In December 2020, Gibraltar Mines Ltd. entered into an option agreement granting Gibraltar the exclusive right and option to acquire a 100% title and interest in five mineral claims which are located near the Gibraltar Mine.

In March 2017, Taseko entered into an agreement to sell its 75% share of payable silver production from the Gibraltar Mine to Osisko Gold Royalties Ltd. ("Osisko"). In April 2020, Taseko entered into an amendment to the Osisko Silver Sale Agreement and received $8.5 million in exchange for reducing the delivery price of silver from US$2.75 per ounce to nil. There are no other royalties, overrides, back-in rights, payments or other agreements to which the project is subject.

There are no significant factors or risks that might affect access, title or ability to perform work on the property.

History

In 1964, Gibraltar acquired a group of claims in the McLeese Lake area from Malabar Mining Co. Ltd.

Canadian Exploration Limited ("Canex"), at that time a wholly-owned subsidiary of Placer Development ("Placer"), and Duval Corporation ("Duval") had also been exploring on claims known as the Pollyanna Group which they had acquired adjacent to Gibraltar's claims. In 1969 Canex and Duval optioned the Gibraltar property. In 1970 Canex acquired Duval's remaining interest to hold both properties.

Placer began construction of the mine in October 1970. The concentrator commenced production in March 1972 and was fully operational by April 1972. A cathode copper plant with an annual capacity of 10 million pounds of market-ready copper metal began operation in October 1986.

In October 1996, Westmin Resources Limited ("Westmin") acquired 100% control of Gibraltar and in December 1997, Boliden Westmin (Canada) Limited ("Boliden") acquired Westmin. In March 1998, Boliden announced that it would cease mining operations at the Gibraltar Mine at the end of 1998.

In July 1999, Taseko's subsidiary, Gibraltar Mines Ltd., purchased the Gibraltar Mine assets from Boliden and certain of its affiliates, including all mineral interests, mining and processing equipment and facilities, and assumed responsibility for reclamation obligations.

- 22 -

From 1999 to 2004, Taseko geologists and engineers sought to better define known resources and explored for additional mineralized material. The on-site staff completed on-going reclamation work and maintained the Gibraltar Mine for re-start. Operating and environmental permits were kept in good standing. The mine re-opened in October 2004.

Gibraltar has been owned and operated as an unincorporated joint venture between Taseko and Cariboo since March 31, 2010. The Company's wholly-owned subsidiary, Gibraltar Mines Ltd. and Cariboo hold 75% and 25% beneficial interests in the Joint Venture, respectively.

Gibraltar increased design mill capacity to 55,000 tons per day in 2011. Gibraltar further increased design mill capacity to 85,000 tons per day in 2013 through installation of a complete independent second concentrator and a stand-alone molybdenum separation plant.

Total production since 1972 is 676 million tons of ore producing 3.5 billion pounds of copper in concentrate, 102 million pounds of cathode copper and 42 million pounds of molybdenum.

Geological Setting, Mineralization, and Deposit Types

The Gibraltar deposits are hosted by the upper Triassic Granite Mountain batholith, located within a wedge of Mesozoic and Palaeozoic rocks bounded on the west by the Fraser Fault system and on the east by the Pinchi Fault system. The Granite Mountain batholith is a composite body consisting of three major phases; Border Phase diorite, Mine Phase tonalite, and Granite Mountain trondjhemite. Contacts between the major phases are gradational over widths ranging from two metres to several hundred metres. The regional deformation was accompanied by localized metasomatic alteration and associated sulphide deposition that led to the concentration of copper mineralization in specific areas of the batholith.

There are currently five defined mineralized zones on the Gibraltar Mine property. They are the Granite, Pollyanna, Connector, Gibraltar, and Extension zones. They occur in a broad zone of shearing and alteration.

Two major ore structure orientations have been recognized; the Sunset and Granite Creek systems. Ore host structures of the Sunset system are mainly shear zones, with minor development of stockworks and associated foliation lamellae whereas oriented stockworks with associated pervasive foliation lamellae predominate in the Granite Creek system.

Pyrite and chalcopyrite are the principal primary sulphide minerals. Small concentrations of other sulphides are present in the Gibraltar ores with molybdenite being a minor but economically important associate of chalcopyrite in the Pollyanna, Granite, and Connector deposits.

Exploration

A property-scale Induced Polarization ("IP") geophysical survey was designed and initiated in August 2000. Field activities included 237 kms of line cutting and some 220 kms of IP survey. Several deposit scale anomalies external to current reserves were identified and drill tested in 2003.

- 23 -

In 2011, Gibraltar Mines Ltd. had an airborne Z-Axis Tipper electromagnetic and magnetic ("ZTEM") survey flown over its then existing claims surrounding the Gibraltar mine. A total of some 690 line kms of ZTEM data was collected.

In 2015, a ground magnetometer survey was performed over 36.6 line kms on four mineral claims.

In 2017, two geophysical surveys were conducted over the Gibraltar NW area by Walcott & Associates. The first consisted of an airborne magnetics survey flown over the property. The survey covered a total of 346 line-km flown along northeast orientated lines at 100 m spacings. The second survey consisted of a ground IP survey that covered a total of 41.5 line-km along 11 northeasterly orientated lines with spacing between 200 and 400 metres. The collected data was used to target a diamond drill program which consisted of two exploration diamond drill holes totaling 3,941 feet (1,201.4m) in the area northwest of the current Extension Resource.

Drilling

From 1999 to 2004, Taseko geologists and engineers sought to better define known resources and explored for additional mineralized material. A core drilling program for pit definition for the Granite Lake and PGE Connector deposits and property exploration at the 98 Oxide Zone was carried out between September and November 2005. A further drilling program carried out in 2006 was designed to define the mineral resources between the existing pits by tying together the extensive mineralization zones, and to test for additional mineralization at depth.

The 2007 program tested a number of targets to define further mineralization, provided definition drilling in the Pollyanna-Granite saddle zone and Granite West areas and included condemnation drilling for the proposed extensions of both the #5 and #6 Dump footprints. The targets for further mineralization were Gibraltar South, Pollyanna North IP anomaly, Granite South and the Gunn Zone.

The 2008 exploration program was conducted on the southern and eastern margins of the Gibraltar pit and northwest of the Gibraltar West pit. The objective was to upgrade identified inferred resources to indicated or measured categories through "in-fill" drilling. Holes drilled in the Gibraltar West pit area were incorporated into the 2008 reserve estimate for the new Gibraltar Extension Pit.

The 2010 program was conducted on the northern and western margins of the Gibraltar Pit, and one hole on the southwest margin. The objective was to define the ultimate limit of the Gibraltar Pit to the north and west. The 2010 drilling program met the objective of delineating mineralization to the north and west of the Gibraltar Pit. A total of 28,129 feet was drilled in 34 drill holes in 2010.

The 2011 program was aimed at identifying mineralization down-dip of the Gibraltar and Granite deposits. A total of 12,229 feet were drilled in 5 holes. A deep zone of anomalous copper and molybdenum mineralization encountered in drill-hole 2011-003 extends from approximately 2,600 to 3,700 feet and consists of intermittent intercepts grading up to 1.3% total copper ("TCu") and 0.4% molybdenum.

- 24 -

In 2013, there were two drill programs completed, one in the summer and the other in the fall. Both programs targeted the projected mineralization south of the current Granite Pit. A total of 38,093 feet in 33 holes were drilled between the two programs.

In early spring of 2014, a resource drill program commenced targeting the Connector pit and the area between Gibraltar East and Granite Pit. At the same time a geotechnical drill program was undertaken. Between the two programs a total of 38 holes were drilled with a cumulative length of 37,456 feet. The main goals of the drilling programs were (1) to collect high-quality geological, geotechnical and assay data, (2) to improve the geological understanding of the ore body, and (3) to increase the drill density within and confidence level of the resource model.

In late 2015, one exploration drill hole was drilled to expand the current known mineralization northwest of the Extension deposit. The total depth of the hole was 2,507 feet. A significant interval of copper was encountered at above reserve grade. The mineralization to the west, northwest and at depth is open. More drilling is needed to confirm if the Extension pit can be expanded to include this material.

In 2016, two drill programs were completed. The first program targeted the conversion of resource material from inferred to measured/indicated at the Granite and Pollyanna deposits. This reserve definition program totaled 35 holes with a cumulative length of 29,342 feet. The second program was an exploration program that targeted the extension of the mineralization discovered in the 2015 exploration hole. Drilling totaled 14,432 feet in 7 holes. The preliminary exploration results were positive with the best results received from the northwestern most hole.

In 2017, two drill programs were completed. The first program targeted the conversion of resource material from inferred to measured/indicated at the Granite, Pollyanna and Connector deposits. This reserve definition program totaled 38 holes with a cumulative length of 38,821 feet. The second program was an exploration program that targeted the extension of the mineralization discovered in the 2015/2016 exploration drilling with 4 holes with a cumulative length of 7,996 feet. This program had 2 phases: two holes (4,055 feet) drilled between January 4, 2017 and February 14, 2017 and two holes (3,941 feet) drilled between September 15, 2017 and October 3, 2017. The exploration results received have expanded the known mineralization to the west, northwest and at depth with the 2016 and 2017 drilling and remains open in these directions. More drilling is needed to prove up the extent of this mineralization.

In 2019, a single 1,327 foot drill hole was drilled targeting a deeper zone below the Granite Pit was completed with the purpose of upgrading and expanding inferred resources to measured/indicated below the Granite Pit. The results received confirmed the presence of mineralization which remains open to the southwest.

Sampling, Analysis, and Data Verification

Over 136,000 samples have been taken for total copper analysis from drilling at Gibraltar since 1965. About 93% of these samples were also assayed for molybdenum, 51% for acid soluble copper, 50% for acid soluble iron, 46% for multi-element inductively coupled plasma ("ICP") and 36% for gold. Essentially all rock drilled and recovered is sampled in 10 ft intervals. Unconsolidated overburden material, where it exists, is generally not recovered by core drilling and therefore not usually sampled.

- 25 -

From discovery in 1965 through mine start-up in 1971, and since mine re-start in 2004, 93% of the assays on exploration drill samples have been performed by reputable, independent third party analytical laboratories. Mine laboratory personnel performed all exploration drill sample analyses from 1979 to 2003.

Well-documented sample preparation, security and analytical procedures used on the Gibraltar drill programs since 1999 have been carried out in an appropriate manner consistent with common industry practice. The results are supported by many years of mine production. A significant amount of due diligence and analytical quality assurance and quality control ("QA/QC") for copper and molybdenum has been completed on the samples that were used in the current mineral resource/reserve estimate. The quality of the work performed on the digital database provides confidence that it is of good quality and acceptable for use in geological and resource modeling of the Gibraltar deposits.

Details of sample preparation, assay laboratories, security, and data verification used in the Gibraltar drill hole sampling and analytical programs is documented in the Gibraltar Technical Report. Sample preparation, security and data verification protocols since the Gibraltar Technical Report continue to apply these same procedures and standards.

Mineral Processing and Metallurgical Testing

Sulphide ore from the Gibraltar deposits has been processed on-site since 1972 and run of mine oxide ore has been leached since 1986. The current mineral reserves are contained within zones which have been significantly mined, with the exception of the Extension Zone. Metallurgical testing associated with the Extension Zone returned results consistent with the rest of the mineralized zones.

The basis for predictions of copper concentrate flotation recovery is plant performance data from both of the existing concentrators based on sulphide and oxide content. Copper recovery is expected to average 86% over the remaining operating period of the reserves.

Molybdenum recovery predictions are based on the average bulk flotation circuit molybdenum recovery, combined with locked cycle testing of molybdenum recovery from the bulk concentrate. The overall molybdenum recovery is predicted to be 50% for the remaining reserves. The basis of the predictions of copper cathode produced from heap leaching and subsequent solvent extraction is based upon historical recovery to cathode. Historical recovery to cathode is 50% of placed copper mass.

- 26 -

Mineral Resource and Mineral Reserve Estimates

The Gibraltar Mine mineral resources and reserves are based on the published reserves as of December 31, 2018, as documented in the Gibraltar Technical Report and reflect depletion due to mining in 2019 and 2020.

The reserve estimate uses long-term metal prices of US$2.75/lb for copper and US$8.00/lb for molybdenum and a foreign exchange rate of C$1.00=US$0.80.

The proven and probable sulphide reserves as of December 31, 2020, are tabulated in Table 2 below.

Table 2: Gibraltar Mine Sulphide Mineral Reserves at 0.15% Copper Cut-off

|

Pit |

Category |

Tons (millions)(1) |

Cu (%) |

Mo (%) |

|

Connector |

Proven |

156 |

0.25 |

0.010 |

|

|

Probable |

7 |

0.22 |

0.007 |

|

|

Subtotal |

163 |

0.25 |

0.010 |

|

Gibraltar |

Proven |

146 |

0.25 |

0.008 |

|

|

Probable |

112 |

0.23 |

0.008 |

|

|

Subtotal |

258 |

0.24 |

0.008 |

|

Extension |

Proven |

50 |

0.33 |

0.002 |

|

|

Probable |

1 |

0.26 |

0.001 |

|

|

Subtotal |

51 |

0.33 |

0.002 |

|

Pollyanna |

Proven |

61 |

0.24 |

0.007 |

|

|

Probable |

1 |

0.23 |

0.006 |

|

|

Subtotal |

61 |

0.24 |

0.007 |

|

Ore Stockpiles |

|

5 |

0.17 |

0.009 |

|

Total |

538 |

0.25 |

0.008 |

|

(1) Totals may not add due to rounding.

There are also oxide reserves as shown in Table 3 below. These oxide reserves as of December 31, 2020 are in addition to the sulphide reserves stated in Table 2.

- 27 -

Table 3: Gibraltar Mine - Oxide Mineral Reserves at 0.10% ASCu Cut-off

|

Pit |

Category |

Tons (millions)(1) |

ASCu (%) |

|

Connector |

Proven |

1 |

0.16 |

|

|

Probable |

14 |

0.15 |

|

|

Subtotal |

15 |

0.15 |

|

Gibraltar |

Proven |

- |

0.17 |

|

|

Probable |

1 |

0.19 |

|

|

Subtotal |

1 |

0.19 |

|

Pollyanna |

Proven |

- |

0.12 |

|

|

Probable |

- |

0.12 |

|

|

Subtotal |

- |

0.12 |

|

Ore Stockpiles |

- |

0.15 |

|

|

Total |

17 |

0.15 |

|

(1) Totals may not add due to rounding.

The resource estimate uses long-term metal prices of US$3.25/lb for copper and US$12.00/lb for molybdenum and a foreign exchange rate of C$1.00=US$0.80.

The mineral reserves stated in Table 2 and Table 3 above are contained within the mineral resources as of December 31, 2020 indicated in Table 4 below:

Table 4: Gibraltar Mine Mineral Resources at 0.15% Copper and 0.10% ASCu Cut-off

|

Category |

Tons (millions) |

Cu (%) |

Mo (%) |

|

Measured |

747 |

0.25 |

0.007 |

|

Indicated |

301 |

0.23 |

0.007 |

|

Total (M&I) |

1,048 |

0.25 |

0.007 |

The mineral resource and reserve estimations were completed by Taseko and Gibraltar Mine staff under the supervision of Richard Weymark, P.Eng., MBA, Chief Engineer, a Qualified Person under NI 43-101 and the author of the Gibraltar Technical Report. Mr. Weymark has verified the methods used to determine grade and tonnage in the geological model, reviewed the long-range mine plan, and directed the updated economic evaluation.

Mining Operations

The Gibraltar Mine is a typical open pit operation that utilizes drilling, blasting, cable shovel loading and large-scale truck hauling to excavate rock. The Gibraltar Mine is planned for excavation of sulphide mineralized material of sufficient grade that it can be economically mined, crushed, ground and processed to a saleable product by froth flotation.

Rock containing oxide mineralization can be leached with a highly diluted sulphuric acid, which is naturally assisted by bacterial action, and the resultant copper sulphate solution can be processed to cathode copper in the Gibraltar Mine's SX/EW plant.

- 28 -

The strip ratio over the remaining 17 year operating period of the reserve will average 2:1. Strip ratio refers to the ratio of the amount of waste material required to be mined in order to extract a unit of ore. For example, a 2:1 stripping ratio means that mining one ton of ore will require mining two tons of waste rock. While the annual strip ratio generally decreases with time, the strip ratio will vary and be managed over the course of the mine life based on exchange rates, commodity prices, and grade distribution during annual and mid-range mine planning process to optimize the economic performance of the operation.

Processing and Recovery Operations

The processing facilities at the Gibraltar Mine consist of two separate bulk sulphide concentrators, a dedicated molybdenum flotation plant, and a series of leach piles which feed a SX/EW facility.

Run of mine ore is fed to the two sulphide concentrators in parallel at a combined design rate of approximately 85,000 tons per day. These two bulk concentrators, while differing in size, follow the same process path. Ore is fed to primary crushing with the product reporting to a closed circuit SAG/Ball comminution stage. Ground ore is processed through a rougher flotation stage. Tailings from the rougher flotation stage are pumped to a storage facility, while the concentrate is reground and processed through two further cleaner flotation stages. Final bulk concentrate contains both copper and molybdenum values.

The bulk concentrate from both facilities is combined and processed through a single molybdenum flotation plant. The bulk concentrate is floated in a rougher stage which depresses the copper values and selectively recovers molybdenum. The underflow from this plant is the site's final copper concentrate. This copper concentrate is dewatered and shipped in bulk to market. The rougher concentrate is reground and processed through two further cleaner flotation stages. Molybdenum final concentrate from this plant is dewatered and bagged, and subsequently shipped to market. The molybdenum flotation plant was restarted in September 2016 after being idled in July 2015 during a decline in molybdenum prices.

Oxide ore from the mine is delivered to oxide leach dumps. The SX/EW plant is designed to extract copper from the pregnant leach solutions ("PLS") collected from the site's leach dumps. Acidic solution is passed through the leach pile and extracts copper in the form of copper ions in this PLS. This copper laden solution is delivered to the SX/EW plant via collection ditches, ponds and pumping where required. The process takes PLS and selectively extracts the copper ions in solvent extraction mixer-settlers. The copper is transferred from this acid solution to an organic phase and finally to a clean electrolyte. The electrolyte is filtered and heated before being passed through the electrowinning cells where the copper is plated out on stainless steel cathodes. The resultant high quality cathode copper is bundled and sold. The barren solution leaving the plant, raffinate, is pumped back to leach additional copper from the leach piles. The SX/EW facility has been placed in care and maintenance since 2015 due to depleted leach dumps and limited fresh oxide ore feed from the mining activity. The plant will be restarted when sufficient oxide ore is mined to justify its operation.

- 29 -

Gibraltar's copper concentrate has a nominal 28.5% copper grade and includes silver as a by-product with no significant deleterious elements. Gibraltar's molybdenum concentrate has a nominal grade of 48% molybdenum and 1.5% copper which is industry standard grade. Gibraltar copper cathode is nominally 99.9%+ pure copper.

Infrastructure, Permitting and Compliance Activities

The Canadian National Railway ("CN") has rail service to facilitate the shipping of copper concentrates to Vancouver Wharves, owned and operated by PKM Canada Marine Terminal LP (or "Pembina") in North Vancouver, British Columbia. The Company operates the concentrate rail load-out facility on the CN rail line at Macalister, 26 kms from the mine site. Gibraltar owns the buildings and a portion of the land upon which the siding is located and has an agreement in place for the use of CN-owned siding materials.

Electricity is obtained from BC Hydro. Natural gas is provided by Fortis BC. The communities of Williams Lake and Quesnel are sufficiently close to the site to supply goods, services, and personnel to the Gibraltar Mine. The Gibraltar Mine had over 700 active personnel at the end of December 2020. Make-up fresh water for the mine site is obtained from a set of wells on the Gibraltar Mine property. Process facilities operate using reclaimed water from the existing tailings storage facility.

Dewatering of Pollyanna Pit is ongoing in preparation for future mining. Water is being pumped to the mined-out Granite Pit for long term storage. Water currently stored in the Gibraltar Pit will be transferred to the completed Granite pit starting in 2021 with construction of a bulk pit dewatering system underway.

Relocation of the in-pit crusher feeding concentrator 1 will need to be completed by 2024 prior to starting phase 2 of the Connector Pit.

With the current design parameters and tailings deposition plan, the tailings facility footprint will accommodate tailings storage until at least 2033. Starting in 2034 tailings will be deposited in the mined out Granite Pit.

All material regulatory authorizations and permits are in place to extract the reserves described in this report with the exception of:

-

A small extension of lease boundary to include the Extension Pit by 2032; and.

-

Periodic amendments of PE-416 and M-40 for pit wall pushbacks, water discharge, and waste rock and tailings storage.

Other permit considerations include approvals required for route changes to the access road, hydro transmission line, natural gas line, and water discharge pipeline in order to complete development of the Extension Pit which is scheduled to start in 2032. Approvals will be sought as required.

- 30 -

There have been no material environmental non-compliance incidents since the mine reopened in 2004.

Capital and Operating Costs

As the majority of the mine's facilities are in place and operating, the only capital requirements are for the relocation of the in-pit crusher/conveyor system and electrical substation, bulk pit dewatering, realignment of the site access road and utility lines, specific tailings and water discharge related activities, and sustaining capital to maintain the integrity of the mining and processing equipment.

The total anticipated site capital requirements over the next 17 years are summarized in Table 5.

Table 5: Capital Cost Summary

|

Area |

Total Capital (in millions) |

|

Process Improvements |

2 |

|

Bulk Pit Dewatering |

7 |

|

Tailings and Water Treatment |

33 |

|

Crusher & Substation Relocation |

43 |

|

Road and Utility Realignment |

6 |

|

General Sustaining |

131 |

|

Total |

223 |

Average estimated unit site operating costs over the next 17 years are summarized in Table 6:

Table 6: Site Operating Cost Summary

|

Operating Category |

Life of Mine Cost |

|

Mine cost/ton milled |

$5.52 |

|

Processing cost/ton milled |

$4.30 |

|

General and Admin cost/ton milled |

$0.90 |

|

Total Operating cost/ton milled |

$10.72 |

The basis for capital and operating cost estimates is documented in the Gibraltar Technical Report.

Exploration, Development, and Production

Gibraltar is pursuing initiatives to improve recovery, concentrator throughput, and mine cost and productivity. Continued improvement in any or all of these areas will have not only positive economic implications but could increase the size of the reserve pits under current commodity assumptions and/or impact the optimum cut-off grade.

- 31 -

Florence Copper