UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the Fiscal Year Ended September 30 , 2020

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the transition period from to

Commission File No. 0-19424

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||||||||

Registrant’s telephone number, including area code: (512 ) 314-3400

Securities Registered Pursuant to Section 12(b) of the Act:

Securities Registered Pursuant to Section 12(g) of the Act: None

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | ||||||||||||

| (NASDAQ Global Select Market) | ||||||||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☑ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☑ No ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

The only class of voting securities of the registrant issued and outstanding is the Class B Voting Common Stock, par value $.01 per share, all of which is owned by an affiliate of the registrant. There is no trading market for the Class B Voting Common Stock. The aggregate market value of the Class A Non-Voting Common Stock held by non-affiliates of the registrant was $212 million, based on the closing price on the NASDAQ Stock Market on March 31, 2020.

As of November 30, 2020, 52332848 shares of the registrant’s Class A Non-Voting Common Stock, par value $.01 per share, and 2,970,171 shares of the registrant’s Class B Voting Common Stock, par value $.01 per share, were outstanding.

Documents incorporated by reference: None

EZCORP, INC.

YEAR ENDED SEPTEMBER 30, 2020

INDEX TO FORM 10-K

| Item | Page | ||||

| No. | No. | ||||

PART I

This report contains forward-looking statements that reflect our future plans, estimates, beliefs and expected performance. Our actual results may differ materially from those currently anticipated and expressed or implied by those forward-looking statements because of a number of risks and uncertainties, including those discussed under “Part I, Item 1A — Risk Factors.” We caution that assumptions, expectations, projections, intentions or beliefs about future events may, and often do, vary from actual results, and the differences can be material. See also “Part II, Item 7 — Management's Discussion and Analysis of Financial Condition and Results of Operations — Cautionary Statement Regarding Risks and Uncertainties That May Affect Future Results.”

Unless otherwise specified, references to the “company,” “we,” “our,” “us” and “EZCORP” refer to EZCORP, Inc. and its consolidated subsidiaries, collectively. References to a “fiscal” year refer to our fiscal year ended September 30 of the specified year. For example, “fiscal 2020” refers to the fiscal year ended September 30, 2020. All currency amounts preceded with “$” are stated in U.S. dollars, except as otherwise indicated.

ITEM 1 — BUSINESS

Overview

EZCORP, Inc. is a Delaware corporation headquartered in Austin, Texas. We are a leading provider of pawn loans in the United States and Latin America with over 1,000 locations and approximately 5,900 team members.

Our vision is to be our customers’ first and best choice for their short-term cash needs. This vision is supported by a customer-centric strategy that includes the following:

•Providing fast, easy and simple access to cash;

•Serving our customers in a friendly and respectful way;

•Always being competitive and fair;

•Passionately solving customer needs;

•Building enduring relationships; and

•Recognizing and rewarding customer loyalty.

At September 30, 2020, we operated a total of 1,005 locations, consisting of:

•505 U.S. pawn stores (operating primarily as EZPAWN or Value Pawn & Jewelry);

•368 Mexico pawn stores (operating primarily as Empeño Fácil); and

•132 pawn stores in Guatemala, El Salvador, Honduras and Peru (operating as GuatePrenda and MaxiEfectivo).

At our pawn stores, we offer non-recourse pawn loans collateralized by tangible personal property, and sell merchandise to customers looking for good value. The merchandise we sell primarily consists of second-hand collateral forfeited from our pawn lending activities or merchandise purchased from customers. By store count, we are the second largest pawn store owner and operator in the U.S. and one of the largest in Latin America. We also offer a web-based application called Lana that allows customers to manage their pawn loans in one place.

In addition to our core pawn business in the U.S. and Latin America, we own 34.75% of Cash Converters International Limited (“Cash Converters International”), a publicly traded company (ASX: CCV) headquartered in Perth, Western Australia. Cash Converters International and its controlled companies comprise a diverse group generating revenues from franchising, store operations, personal finance and vehicle finance, controlling over 700 stores across 16 countries.

We also own approximately 13% of Rich Data Corporation (RDC), a Singapore-based software-as-a-service company that utilizes global financial services expertise, advanced artificial intelligence and non-traditional data to deliver a next-generation credit scoring and decisioning platform.

3

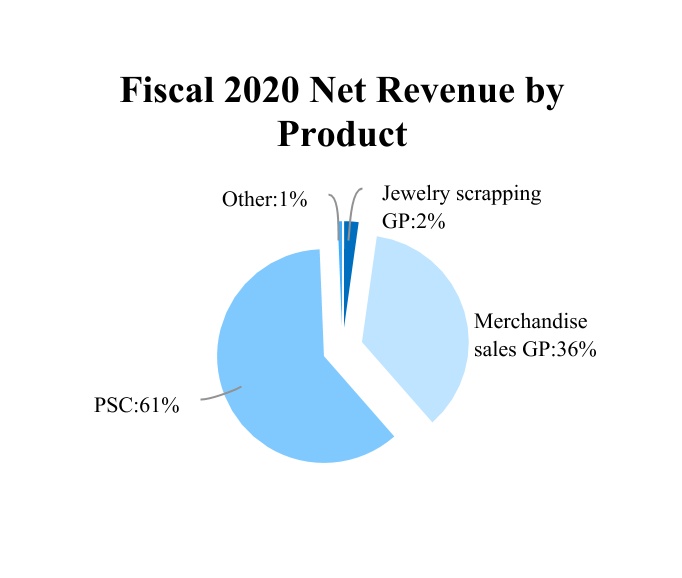

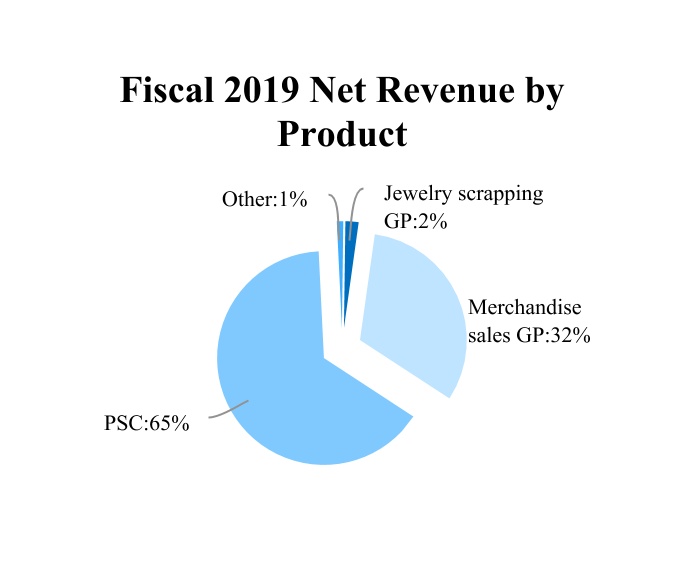

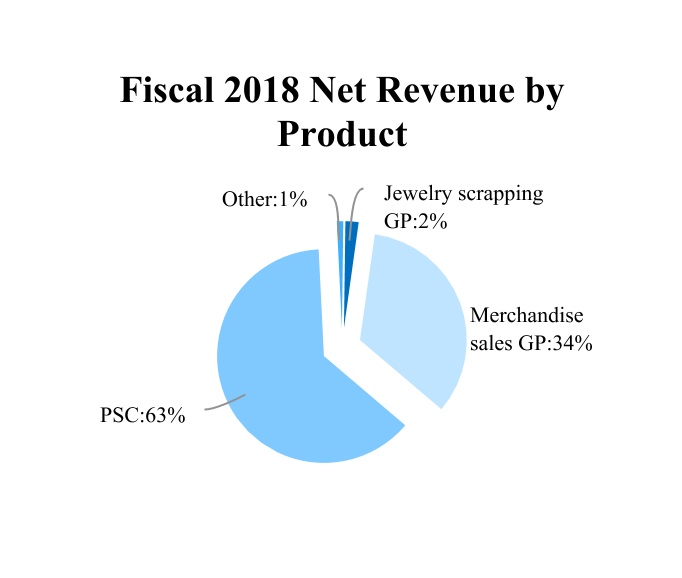

We generate revenues primarily from pawn services charges (“PSC”) on pawn loans outstanding (“PLO”), merchandise sales and jewelry scrapping. We remain focused on optimizing our balance of PLO and the resulting higher pawn service charges (“PSC”). The following charts present sources of net revenues, including PSC, merchandise sales gross profit (“Merchandise sales GP”) and jewelry scrapping gross profit (“Jewelry scrapping GP”):

4

Segment and Geographic Information

We conduct our business globally and manage our business by geography. Our business is organized into the following reportable segments:

•U.S. Pawn, which includes our EZPAWN, Value Pawn & Jewelry and other branded pawn operations in the United States;

•Latin America Pawn, which includes our Empeño Fácil and other branded pawn operations in Mexico, as well as our GuatePrenda and MaxiEfectivo pawn operations in Guatemala, El Salvador, Honduras and Peru;

•Lana, which is our customer-centric web-based engagement platform; and

•Other International, which includes the consumer finance activities in Canada that we closed in the fourth quarter and our equity interests in Cash Converters International and RDC.

We began reporting separate financial results for our Lana business in the first quarter of fiscal 2020, and our historical segment results have been recast to conform to current presentation.

The following table presents store data by segment (excluding Lana, which has no separate physical store locations), included in our continuing operations:

| Company-owned Stores | |||||||||||||||||||||||

| U.S. Pawn | Latin America Pawn | Other International | Consolidated | ||||||||||||||||||||

As of September 30, 2017 | 513 | 246 | 27 | 786 | |||||||||||||||||||

| New locations opened | — | 12 | — | 12 | |||||||||||||||||||

| Locations acquired | — | 196 | — | 196 | |||||||||||||||||||

| Locations sold, combined or closed | (5) | (1) | — | (6) | |||||||||||||||||||

As of September 30, 2018 | 508 | 453 | 27 | 988 | |||||||||||||||||||

| New locations opened | — | 22 | — | 22 | |||||||||||||||||||

| Locations acquired | 7 | 5 | — | 12 | |||||||||||||||||||

| Locations sold, combined or closed | (3) | — | (5) | (8) | |||||||||||||||||||

As of September 30, 2019 | 512 | 480 | 22 | 1,014 | |||||||||||||||||||

| New locations opened | — | 23 | — | 23 | |||||||||||||||||||

| Locations acquired | — | — | — | — | |||||||||||||||||||

| Locations sold, combined or closed | (7) | (3) | (22) | (32) | |||||||||||||||||||

As of September 30, 2020 | 505 | 500 | — | 1,005 | |||||||||||||||||||

For additional information about our segments and geographic areas, see Note 14 of Notes to Consolidated Financial Statements included in “Part II, Item 8 — Financial Statements and Supplementary Data.”

Pawn Activities

At our pawn stores, we offer pawn loans, which are typically small, non-recourse loans collateralized by tangible personal property. We earn pawn service charges on our pawn loans, which varies by state and loan size. Collateral for our pawn loans consists of tangible personal property, generally jewelry, consumer electronics, tools, sporting goods and musical instruments. Security for our pawn loans is provided via the estimated resale value of the collateralized personal property and the perceived probability of the loans' redemption.

As of September 30, 2020, we had a closing pawn loan principal balance of $131.3 million, from which we earn pawn service charges. In fiscal 2020, pawn service charges accounted for approximately 33% of our total revenues and 61% of our net revenues.

U.S. pawn loans primarily earn 13% to 25% per month as permitted by applicable law, excluding forfeitures. The U.S. pawn loan term generally ranges between 30 and 90 days. While individual loans vary depending on the valuation of each item pawned, our U.S. pawn loans typically average between $100 and $120.

5

In Mexico, pawn loans earn 15% to 21% per month as permitted by applicable law, excluding forfeitures. The Mexico pawn loan primary term is 30 days. Individual loans are made in Mexican pesos and vary depending on the valuation of each item pawned. Mexico pawn loans typically average between 1,100 and 1,300 Mexican pesos, or approximately $50 to $60 on average using the average exchange rate for fiscal 2020.

In Guatemala, El Salvador, Honduras and Peru, pawn loans earn 12% to 18% per month as permitted by applicable law, excluding forfeitures. The pawn loan primary term in these countries is 30 days. Individual loans are made in the local currency of the country and vary depending on the valuation of each item pawned. Our pawn loans in these countries typically average between $100 and $120 using the average exchange rates for fiscal 2020. The average loan amounts tend to be higher in these countries than in Mexico due to the higher concentration of jewelry loans.

If a customer chooses not to repay, renew or extend a pawn loan, the collateral is forfeited and becomes inventory available for sale. We do not record loan losses or charge-offs of pawn loans because the principal amount of an unpaid loan becomes the inventory carrying cost of the forfeited collateral. The difference between the subsequent sale of the forfeited collateral and the loan value is reflected in merchandise sales gross margin.

The redemption rate represents the percentage of loans made that are repaid, renewed or extended, including loans that may extend multiple times in a given time period. The following table presents our pawn loan redemption rates by segment:

| Fiscal Year Ended September 30, | ||||||||||||||||||||

| Redemption Rate | 2020 | 2019 | 2018 | |||||||||||||||||

| U.S. Pawn | 88 | % | 84 | % | 84 | % | ||||||||||||||

| Latin America Pawn | 78 | % | 78 | % | 79 | % | ||||||||||||||

Our ability to offer quality second-hand goods at prices significantly lower than original retail prices attracts value-conscious customers. The gross profit on sales of inventory depends primarily on our assessment of the loan or purchase value at the time the property is either accepted as loan collateral or purchased and our ability to sell that merchandise in a timely manner. As a significant portion of our inventory and sales involve gold and jewelry, our results can be influenced by the market price of gold and diamonds.

Customers in the United States and the majority of our Latin America stores may purchase a product protection plan that allows them to exchange certain general merchandise (non-jewelry) sold through our retail pawn operations within six months of purchase. We also offer a jewelry VIP package, which guarantees customers a minimum future pawn loan amount on the item sold, allows them full credit if they trade in the item to purchase a more expensive piece of jewelry, and provides minor repair service on the item sold. Customers may also purchase an item on layaway by paying a minimum layaway deposit of typically 10% of the item’s sale price, in addition to an upfront fee. We hold items on layaway for a 90 to 180-day period, during which the customer is required to pay the balance of the sales price through a series of installment payments. If a payment is missed, we hold the item for a maximum of 30 days, after which it is returned to active inventory for sale.

Closure of CASHMAX

We operated 22 financial services stores in Canada under the CASHMAX brand during the fiscal year. All of the stores were located in the Ontario province, in and around Toronto. During the fourth quarter, as part of a review of our growth strategies and cost optimization initiatives, we closed our CASHMAX business.

Operations and Risk Management

Our pawn operations are designed to provide the optimum level of support to the store teams, providing coaching, mentoring and problem solving to identify opportunities to better serve our customers and position us to be the leader in customer service and satisfaction.

Our risk management structure consists of asset protection, compliance and internal audit departments, which monitor the inventory system, lending practices, regulatory compliance and compliance with our policies and procedures. We perform full physical audits of inventory at each store at least annually, and more often in higher risk stores or those experiencing higher shrinkage. Inventory counts are completed daily for jewelry and firearms, and other inventory categories more susceptible to theft are cycle counted multiple times annually. We record shrink adjustments for known losses at the conclusion of each inventory count. These adjustments are recorded as estimates during interim periods and as discovered during cycle counts.

6

Human Capital Management

We employ 5,900 Team Members in the U.S., Mexico, Guatemala, El Salvador, Honduras, Peru and Canada, all of whom are expected to be guided by our vision and values and by an underlying set of ethical principles. Incorporated into our Code of Conduct, our vision, values and principles define our culture and strengthen the workforce. We strive to demonstrate to our customers, shareholders, business partners, communities and Team Members that we are worthy of their trust and continually strive to enhance and differentiate our brand reputation as the best in our industry. Globally, we invest in Team Members at all levels who are expected to integrate our vision and values in all that we do.

We employ 5,900 Team Members in the U.S., Mexico, Guatemala, El Salvador, Honduras, Peru and Canada, all of whom are expected to be guided by our vision and values and by an underlying set of ethical principles. Incorporated into our Code of Conduct, our vision, values and principles define our culture and strengthen the workforce. We strive to demonstrate to our customers, shareholders, business partners, communities and Team Members that we are worthy of their trust and continually strive to enhance and differentiate our brand reputation as the best in our industry. Globally, we invest in Team Members at all levels who are expected to integrate our vision and values in all that we do.

While the People and Compensation Committee of the Board of Directors has the primary responsibility of overseeing our human capital management activities (including assessing the effectiveness of employee programs and advising management with regard to the quality of the workforce to carry out our strategic goals and overall human resource strategies), other Board committees also have responsibilities that impact our human capital management as outlined in their respective Charters. Within management, our Human Resources function has global management responsibility for advising and assisting the business on human resource matters and executing our overall human capital management strategies.

We are committed to fostering work environments that value diversity and inclusion. This commitment includes providing equal access to, and participation in, equal employment opportunities, programs and services without regard to race, creed, religion, color, national origin, disability, sex (including pregnancy), sexual orientation, gender identity, veteran status, age or stereotypes or assumptions based thereon. We welcome and celebrate our Team Members’ differences, experiences and beliefs, and we are investing in a more productive, engaged, diverse and inclusive workforce.

During fiscal 2020, we appointed a Senior Manager of Diversity and Inclusion, who is responsible for strategic management and planning for diversity and inclusion within the Company, as well as enhancing our understanding, providing training and development, and partnering with and assisting all of us to be accountable. During the year, our new Diversity and Inclusion function drove a number of initiatives to enhance our focus on diversity and inclusion and raise our awareness, including mandatory compliance training on unconscious bias, introduction of the Diversity Word of the Month (a recurring program to raise awareness and promote constructive conversations about various diversity and inclusion issues), and conducting a series of surveys and group feedback sessions, the results of which are shared with senior management and help guide our ongoing Diversity and Inclusion activities.

We strive to engage and retain our Team Members throughout the employment life-cycle with effective recruiting and onboarding; competitive pay, benefits and other total rewards; mandatory and optional programs for professional development and career advancement; compliance training; succession planning; and a safe, healthy and respectful workplace. Our EZCORP University includes mandatory global compliance training at hire and periodically thereafter, career advancement training requirements and thousands of self-directed developmental courses.

In response to the COVID-19 pandemic, we quickly implemented safety and health standards and protocols for our Team Members while continuing to offer a safe environment as an essential service to our customers. Team Members in our Corporate Support Centers have been working from home since March. Our pawn locations are provided with PPE, other equipment and enhanced cleaning supplies, and are required to adhere to appropriate protocols for social distancing, limiting density, taking temperatures, reporting and documenting exposures and wearing masks at all times, all as recommended by the Centers for Disease Control or mandated by local regulations.

We maintain an Ethics Hotline that is available to all of our Team Members to report (anonymously if desired) any matter of concern. Communications to the hotline (which is facilitated by an independent third party) are routed to appropriate functions (whether Human Resources, Legal or Compliance) for investigation and resolution. In addition, any shareholder or other interested party may send communications to the Board of Directors, either individually or as a group, through a process that is outlined in the Investor Relations section of our website.

Growth and Expansion

Part of our strategy is to grow the number of locations we operate through opening new (“de novo”) locations and through acquisitions in both Latin America and the U.S. and potential new markets. Our ability to add new stores is dependent on several variables, such as projected achievement of internal investment hurdles, the availability of acceptable sites or acquisition candidates, the alignment of acquirer/seller price expectations, the regulatory environment, local zoning ordinances, access to capital and availability of qualified personnel.

During fiscal 2020, we continued our expansion in Latin America with the opening of 23 de novo stores (14 in Mexico, 7 in Guatemala, 1 in Honduras and 1 in Peru). We now own a total of 500 stores in Latin America, representing 50% of our total pawn stores. In fiscal 2020, these stores represented 19% of our consolidated net revenues as the average scale of Latin

7

America pawn stores is smaller than in the U.S. We see opportunity for further expansion in Latin America through both acquisitions and de novo openings.

For further information about our acquisitions, see Note 3 of Notes to Consolidated Financial Statements included in “Part II, Item 8 — Financial Statements and Supplementary Data.”

Seasonality and Quarterly Results

In the United States, pawn service charges are historically highest in our fourth fiscal quarter (July through September) due to a higher average loan balance during the summer lending season and lowest in our third fiscal quarter (April through June) following the tax refund season, and merchandise sales are highest in our first and second fiscal quarters (October through March) due to the holiday season, jewelry sales surrounding Valentine’s Day and the availability of tax refunds. In Latin America, most of our customers receive additional compensation from their employers in December, and many receive additional compensation in June or July, applying downward pressure on loan balances and fueling some merchandise sales in those periods. As a net effect of these and other factors and excluding discrete charges, our consolidated profit before tax is generally highest in our first fiscal quarter (October through December) and lowest in our third fiscal quarter (April through June). These historical trends have been impacted by COVID-19, but we expect them to return in the future.

Competition

We encounter significant competition in connection with all of our activities. These competitive conditions may have an impact on our revenues, profitability and ability to expand. We compete with other pawn stores, credit service organizations, banks, credit unions and other financial institutions, such as consumer finance companies. We believe the primary elements of competition are the quality of customer service and relationship management, including understanding our customers’ needs better than anyone else, convenience, store location and a customer-friendly environment. In addition, we believe the ability to compete effectively will be based increasingly on strong general management, regional focus, automated management information systems, access to capital and superior customer service.

Our competitors for merchandise sales include numerous retail and wholesale stores such as jewelry stores, discount retail stores, consumer electronics stores, other pawn stores, other resale stores, electronic commerce retailers and auction sites. Competitive factors in our retail operations include the ability to provide the customer with a variety of merchandise at an exceptional value coupled with exceptional customer service and convenient locations.

The pawn industry in the United States is large, relatively mature and highly fragmented. The industry consists of a few large operators (of which we are the second largest) and then independent operators who primarily own one to three locations.

The pawn industry in Latin America is also fragmented, but less so than in the United States. The industry consists of pawn stores owned by independent operators and chains, including some not-for-profit organizations. We are the second largest for-profit operator in Mexico. The pawn industry, particularly full-line stores offering general merchandise and jewelry loans and resale, remains in an expansion stage in Latin America.

Trademarks and Trade Names

We operate our U.S. pawn stores principally under the names “EZPAWN” or “Value Pawn & Jewelry,” our Mexico pawn stores principally under the name “EMPEÑO FÁCIL,” our Guatemala pawn stores under the name “GuatePrenda,” and our El Salvador, Honduras and Peru pawn stores under the name “MaxiEfectivo.” We have registered the names EZPAWN and EZCORP, among others, with the United States Patent and Trademark Office. In Mexico, we have registered the names “EMPEÑO FÁCIL,” “Bazareño,” “Presta Dinero” and “Montepio San Patricio” with the Instituto Mexicano de la Propiedad Industrial. We have registered the name “GuatePrenda” in Guatemala and the name “MaxiEfectivo” in Guatemala, El Salvador, Honduras and Peru.

Regulation

Compliance with federal, state and local laws and regulations is an integral part of how we manage our business, and we conduct our business in material compliance with all of these rules. The following is a general description of significant regulations affecting our business.

U.S. Regulations

Pawn Regulations — Our pawn stores are regulated by the states in which they are located and, in some cases, by individual municipalities or other local authorities. The applicable statutes, ordinances and regulations vary from location to location and typically impose licensing requirements for pawn stores or individual pawn store team members. Licensing requirements

8

typically relate to financial responsibility and character and may establish restrictions on where pawn stores can operate. Additional rules regulate various aspects of the day-to-day pawn operations, including the pawn service charges that a pawn store may charge, the maximum amount of a pawn loan, the minimum or maximum term of a pawn loan, the content and format of the pawn ticket, and the length of time after a loan default that a pawn store must hold a pawned item before it can be offered for sale. Failure to observe applicable regulations could result in a revocation or suspension of pawn licenses, the imposition of fines or requirements to refund service charges and fees, and other civil or criminal penalties. We must also comply with various federal requirements regarding the disclosure of the annual percentage rate, finance charge, amount financed, total of payments and payment schedule related to each pawn loan transaction. Additional federal regulations applicable to our pawn lending business are described in “Other Regulations” below.

The majority of our pawn stores, voluntarily or pursuant to applicable laws, provide periodic (generally daily) reports to local law enforcement agencies. These reports provide local law enforcement with information about the items received from customers (whether through pawn or purchase), including a detailed description of the goods involved and the name and address of the customer. If we accept as collateral or purchase merchandise from a customer and it is determined that our customer was not the rightful owner, the merchandise is subject to recovery by the rightful owner and those losses are included in our shrinkage. Historically, we have not experienced a material number of claims of this nature.

Some of our pawn stores in the U.S. handle firearms and each of those stores maintains a federal firearms license as required by federal law. The federal Gun Control Act of 1968 and regulations issued by the Bureau of Alcohol, Tobacco, and Firearms also require each pawn store dealing in firearms to maintain a permanent written record of all receipts and dispositions of firearms. In addition, we must comply with the Brady Handgun Violence Prevention Act, which requires us to conduct a background check before releasing, selling or otherwise disposing of firearms.

Other Regulations — Our pawn lending activities are subject to other state and federal statutes and regulations, including the following:

•We are subject to the federal Gramm-Leach-Bliley Act and its underlying regulations, as well as various state laws and regulations relating to privacy and data security. Under these regulations, we are required to disclose to our customers our policies and practices relating to the protection and sharing of customers’ nonpublic personal information. These regulations also require us to ensure that our systems are designed to protect the confidentiality of customers’ nonpublic personal information, and many of these regulations dictate certain actions that we must take to notify customers if their personal information is disclosed in an unauthorized manner. We are subject to the Fair Credit Reporting Act, which was enacted, in part, to address privacy concerns associated with the sharing of consumers’ financial information and credit history contained in consumer credit reports and limits our ability to share certain consumer report information. We are subject to the Federal Fair and Accurate Credit Transactions Act, which amended the Fair Credit Reporting Act and requires us to adopt written guidance and procedures for detecting, preventing and mitigating identity theft, and to adopt various policies and procedures (including Team Member training) that address and aid in detecting and responding to suspicious activity or identity theft “red flags.”

•As a provider of consumer financial products, we are prohibited from engaging in any unfair, deceptive or abusive act or practice (UDAAP) under the Dodd-Frank Act, as they can cause significant financial injury to consumers, erode consumer confidence and undermine the financial marketplace.

•The Equal Credit Opportunity Act prohibits discrimination on the basis of race, color, religion, national origin, sex, marital status, age, receipt of public assistance or good faith exercise of any rights under the Consumer Credit Protection Act.

•Under the USA PATRIOT Act, we must maintain an anti-money laundering compliance program that includes the development of internal policies, procedures and controls; the designation of a compliance officer; an ongoing team member training program; and an independent audit function to test the program.

•We are subject to the Bank Secrecy Act and its underlying regulations, which require us to report and maintain records of certain high-dollar transactions. In addition, federal laws and regulations require us to report certain suspicious transactions to the Financial Crimes Enforcement Network of the Treasury Department (“FinCen”). Generally, a transaction is considered to be suspicious if we know, suspect or have reason to suspect that the transaction (a) involves funds derived from illegal activity or is intended to hide or disguise such funds, (b) is designed to evade the requirements of the Bank Secrecy Act or (c) appears to serve no legitimate business or lawful purpose.

•The Office of Foreign Assets Control (“OFAC”) of the Department of the Treasury administers and enforces economic and trade sanctions based on U.S. foreign policy and national security goals against targeted foreign countries and regimes, terrorists, international narcotics traffickers, those engaged in activities related to the proliferation of weapons

9

of mass destruction and other threats to the national security, foreign policy or economy of the United States. We are prohibited from doing business with named individuals, businesses and countries subject to sanctions and restrictions, and we are required to report any transactions involving those named by the US. Department of the Treasury.

•The Foreign Corrupt Practices Act ("FCPA") makes it unlawful for certain classes of persons and entities to make payments to foreign government officials to assist in obtaining or retaining business. Specifically, the anti-bribery provisions of the FCPA prohibit the willful use of mail or any means of instrumentality of interstate commerce corruptly in furtherance of any offer, payment, promise to pay, or authorization of the payment of money or anything of value to any person, while knowing that all or a portion of such money or thing of value will be offered, given or promised, directly or indirectly, to a foreign official to influence the foreign official in his or her official capacity, induce the foreign official to do or omit to do an act in violation of his or her lawful duty, or to secure any improper advantage in order to assist in obtaining or retaining business for or with, or directing business to, any person.

•The Department of Defense regulations promulgated under the Military Lending Act (the “MLA”) limit the annual percentage rate charged on certain consumer loans (including pawn loans) made to active military personnel or their dependents to 36%.

Under certain circumstances, the federal Consumer Financial Protection Bureau (“CFPB”) may be able to exercise regulatory authority over the U.S. pawn industry through its rule making authority. To date, the CFPB has not taken any steps to exercise such authority or indicated any intention to do so.

Mexico Regulations

Pawn Regulations — Federal law in Mexico provides for administrative regulation of the pawnshop industry by Procuraduría Federal del Consumidor (PROFECO), Mexico’s primary federal consumer protection agency. PROFECO regulates the form and terms of pawn loan contracts (but not interest or service charge rates) and defines certain operating standards and procedures for pawnshops, including retail operations, and establishes registration, disclosure, bonding and reporting requirements. There are significant fines and sanctions, including operating suspensions, for failure to comply with PROFECO’s rules and regulations.

PROFECO requires that we report certain transactions (or series of transactions) that exceed certain monetary limits. Anti-money laundering regulations restrict the use of cash in certain transactions. Relevant aspects of the law specifically affecting the pawn industry include monthly reporting on “vulnerable activities,” which includes certain high-value pawn and precious metal transactions.

The Federal Law on the Protection of Personal Data Held by Private Parties requires us to protect our customers’ personal information. This law requires us to inform customers if we share customer personal information with third parties and to post (both online and in-store) our Data Privacy Policy.

Our pawn business in Mexico is also subject to regulation at the state and local level through state laws and local zoning and permitting ordinances. For example, some states require permits for pawn stores to operate, certification of team members as trained in the valuation of merchandise, and strict customer identification controls. State and local agencies often have authority to suspend store operations pending resolution of actual or alleged regulatory, licensing and permitting issues.

Other Regulations — Our pawn business in Mexico is subject to the General Law of Administrative Responsibility (“GLAR”), effective July 2017. GLAR establishes administrative penalties for improper payments to government officials, influence peddling (including the hiring of public officials and the use of undue influence) and other corrupt acts in public procurement processes.

We are also subject to The Federal Law for the Prevention and Identification of Transactions with Funds from Illegal Sources, which requires reporting of certain transactions exceeding certain monetary limits, maintenance of customer identification records and controls, and reporting of all non-Mexican customer transactions. This law affects all industries in Mexico and is intended to detect commercial activities arising from illicit or ill-gotten means through bilateral cooperation between Mexico’s Ministry of Finance and Public Credit and Mexico’s Attorney General’s Office. The law also restricts the use of cash in certain transactions associated with high-value assets and limits, and to the extent possible, money laundering activities protected by the anonymity that such cash transactions provide. Relevant aspects of the law specifically affecting the pawn industry include monthly reporting on “vulnerable activities,” which include pawn transactions exceeding 139,442 Mexican pesos and retail transactions of precious metals exceeding 139,442 Mexican pesos. Retail transactions of precious metals in cash exceeding 271,213 Mexican pesos are prohibited. There are significant fines and sanctions for failure to comply with these rules.

10

In addition to the above, our pawn business in Mexico is subject to various general business regulations in the areas of tax compliance, customs, consumer protections, money laundering, civil protection regulations, municipal regulations, trade code (federal), public safety and employment matters, among others, by various federal, state and local governmental agencies.

Other Latin American Regulations

Local governmental entities in Guatemala, El Salvador, Honduras and Peru also regulate lending and retail businesses. Certain laws and local zoning and permitting ordinances require basic commercial business licenses and signage permits. Operating in these countries also subjects us to other types of regulations, including regulations related to financial reporting, data protection and privacy, tax compliance, labor and employment practices, real estate transactions, anti-money laundering, commercial and electronic banking restrictions, credit card transactions, usury law, consumer protection, marketing, advertising and other general business activities. As the scope of our international operations increases, we may face additional administrative and regulatory costs in managing our business. In addition, unexpected changes in laws and regulations, administrative interpretations of local requirements or legislation, or public remarks by elected officials could negatively affect our operations and profitability.

Available Information

We file annual, quarterly and current reports and other documents with the Securities and Exchange Commission (“SEC”) under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The SEC maintains an Internet website that contains reports and other information regarding issuers that file electronically with the SEC. The public can obtain any documents that we file with the SEC at www.sec.gov.

We maintain a website at www.ezcorp.com. Our filings with the SEC, including our Annual Reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and Section 16 filings, are available free of charge through links maintained on our website under the heading “Investor Relations — SEC Filings.” Information contained on our website is not incorporated by reference into this report.

ITEM 1A — RISK FACTORS

There are many risks and uncertainties that may affect our operations, performance, development and results. Many of these risks are beyond our control. The following is a description of the important risk factors that may affect our business. If any of these risks were to occur, our business, financial condition or results of operations could be materially adversely affected. Additional risks and uncertainties not currently known to us or that we currently consider to be immaterial may also materially adversely affect our business, financial condition or results of operations.

Company Specific Risks

As a result of the current COVID-19 pandemic, we incurred operating losses in the fourth quarter of fiscal 2020 and expect those operating losses to continue into fiscal 2021.

The outbreak of COVID-19 began affecting our operations in March 2020. Governmental fiscal stimulus response, stay-at-home orders and business restrictions, health agency guidance regarding social distancing and public perceptions of the risks associated with the COVID-19 pandemic have resulted in a reduction in the demand for pawn loans with a resulting significant decline in pawn loan balances. See “Part II, Item 7 — Management’s Discussion and Analysis of Results of Operations and Financial Condition — Impact of COVID-19.” The decline in pawn loan balances negatively impacted our financial performance during the third and fourth quarters of fiscal 2020. We expect the impact of the pandemic, and the recovery therefrom, will continue to adversely affect our net revenues and earnings in fiscal 2021. A prolonged pandemic and recovery may impact our financial condition, results of operations and liquidity in future periods. The extent of the impact is dependent upon a number of factors, including the longevity and severity of the pandemic, the pace of business reopenings and rebound, the impact of government responses and the degree to which customer behaviors return to historical norms.

Failure to sustain focus on internal controls could adversely affect our business, results of operations and financial condition.

As described in "Part II, Item 9A — Controls and Procedures," we identified and evaluated certain deficiencies in our IT general controls in the second quarter of fiscal 2019, and concluded those deficiencies, collectively, represented a material weakness in our internal control over financial reporting. During the fourth quarter of fiscal 2020, we completed our efforts to remediate the underlying deficiencies, and have concluded that our disclosure controls and procedures and our internal control over financial reporting are effective as of September 30, 2020. If we do not sustain our focus on internal controls, our consolidated financial statements may contain material misstatements and we could be required to restate our financial results,

11

which could materially and adversely affect our business, results of operations and financial condition, restrict our ability to access the capital markets, require us to expend significant resources to correct the deficiencies, subject us to fines, penalties or judgments, harm our reputation or otherwise cause a decline in investor confidence and the market value of our publicly traded Class A Non-Voting Common Stock (“Class A Common Stock”).

Changes in, or failure to comply with, laws and regulations affecting our products and services could have a material adverse effect on our operations and financial performance.

Our products and services are subject to regulation under various laws and regulations in each country and jurisdiction in which we operate (see “Part I, Item 1 — Business — Regulation”), and adverse legislation or regulations could be adopted in any such country or jurisdiction. If such legislation or regulation is adopted in any particular jurisdiction, we generally evaluate our business in the context of the new rules and determine whether we can continue to operate in that jurisdiction with new or modified products or whether it is feasible to enhance our business with additional product offerings. In any case, if we are unable to continue to operate profitably under the new rules, we may decide to close or consolidate stores, resulting in decreased revenues, earnings and assets. Further, our failure to comply with applicable laws and regulations could result in fines, penalties or orders to cease or suspend operations, which could have a material adverse effect on our results of operations.

Negative characterizations of the pawn industry by consumer advocates, media or others could result in increased legislative or regulatory activity, could adversely affect the market value of our publicly traded stock, or could make it harder to operate our business successfully.

Many of the legislative and regulatory efforts that are adverse to the pawn industry are the result of negative characterization of the pawn industry by consumer advocacy groups, members of the media or others that focus on the cost of pawn loans or instances of pawn operators purchasing stolen property or accepting it as pawn collateral. We can give no assurance that there will not be further negative characterizations of our industry or that legislative or regulatory efforts to restrict the availability of pawn loans or otherwise regulate pawn operations will not be successful despite significant customer demand for such services. Such efforts, if successful, could have a material adverse effect on our operations or financial performance.

Furthermore, negative characterizations of our industry could limit the number of investors who are willing to hold our Class A Common Stock, which may adversely affect its market value; limit sources of the debt or equity financing that we need in order to conduct our operations and achieve our strategic growth objectives; or make it harder for us to attract, hire and retain talented executives and other key team members.

A significant portion of our U.S. business is concentrated in Texas and Florida.

As of September 30, 2020, more than 60% of our U.S. pawn stores were located in Texas (43%) and Florida (19%), and those stores account for a significant portion of our revenues and profitability. The legislative, regulatory and general business environment in Texas and Florida has been relatively favorable for our pawn business activities, but a negative legislative or regulatory change in either of those states could have a material adverse effect on our overall operations and financial performance. Further, as discussed below, areas in Texas and Florida where we have significant operations are particularly susceptible to hurricane and tropical storm activity.

A significant or sudden decrease in gold values or the volume of gold transactions may have a material impact on our earnings and financial position.

Gold jewelry comprises a large portion of the collateral security for our pawn loans and our inventory. Pawn service charges, sales proceeds and our ability to liquidate excess jewelry inventory at an acceptable margin are dependent upon gold values and the volume of gold transactions. A decline in the availability of gold or our customers’ willingness or ability to sell us gold or use gold as collateral for pawn loans could impact our business. The impact on our financial position and results of operations of decreases in gold values or volumes or a change in customer behavior cannot be reasonably estimated because the market and customer response to changes in gold values is not known; however, a significant decline in gold values or gold volumes could result in decreases in sales, sales margins, pawn loan balances and pawn service charges.

Fluctuations in our sales, pawn loan balances, sales margins and pawn redemption rates could have a material adverse impact on our operating results.

We regularly experience fluctuations in a variety of operating metrics. Changes in any of these metrics, as might be caused by changes in the economic environment, competitive pressures, changes in customers’ tastes and preferences or a significant decrease in gold prices could materially and adversely affect our profitability and ability to achieve our planned results of operations.

12

Achievement of our growth objectives is dependent upon our ability to open and acquire new stores.

Our expansion strategy includes acquiring existing stores and opening de novo store locations. Our acquisition strategy is dependent upon the availability of attractive acquisition candidates, while the success of our de novo store strategy is contingent upon numerous factors that cannot be predicted or controlled, such as the availability of acceptable locations with a desirable customer base, the negotiation of acceptable lease terms, the ability to obtain required government permits and licenses and the existence of a suitable competitive environment. The achievement of our growth objectives is also subject to our ability to attract, train and retain qualified team members. Failure to achieve our expansion goals could adversely affect our prospects, future results of operations and future cash flows.

Our development of a digital platform, and the commercialization of that platform, may not be successful.

We have invested in the design and development of a digital platform to enhance our relationships with customers and provide them access to a broader range of financial products and services. There can be no assurance that our efforts to develop and launch such a digital platform will be successful or that the platform will be accepted by existing customers or attract new customers. Consequently, we may not realize the expected return on our investment.

We continue to have limited indemnity obligations to AlphaCredit for pre-closing taxes.

Under the terms of the Purchase Agreement related to the sale of our 94%-owned subsidiary, Prestaciones Finmart, S.A.P.I. de C.V., SOFOM, E.N.R. ("Grupo Finmart") to Alpha Holding, S.A. de C.V. ( “AlphaCredit”) in September 2016, we remain obligated to indemnify AlphaCredit for any “pre-closing taxes” (i.e., tax obligations arising from the Grupo Finmart business that are attributable to periods prior to the completion of the sale in September 2016). Those obligations continue until the expiration of the statute of limitations applicable to the pre-closing periods. In August 2019, AlphaCredit notified us of a potential indemnity claim for certain pre-closing taxes, but the nature, extent and validity of such claim has yet to be determined. The last two payments from AlphaCredit totaling $8.0 million have been placed into escrow pending resolution of the potential indemnity claim.

One person beneficially owns all of our voting stock and generally controls the outcome of all matters requiring a vote of stockholders, which may influence the value of our publicly traded non-voting stock.

Phillip E. Cohen is the beneficial owner of all our Class B Voting Common Stock, and all our publicly traded stock is non-voting stock. Consequently, stockholders other than Mr. Cohen have no vote with respect to the election of directors or any other matter requiring a vote of stockholders except in limited circumstances as required by law. Further, our Bylaws currently provide that the voting stockholder may appoint or remove officers or take any other action that the Board of Directors may take with respect to officers under the Bylaws. The lack of voting rights may adversely affect the market value of our publicly traded Class A Common Stock.

In September 2019, Mr. Cohen joined the Board of Directors and was appointed Executive Chairman. As a member of the Board, Mr. Cohen is entitled to vote on all matters requiring approval of the Board. Our Bylaws currently provide that the presence of all directors shall constitute a quorum for the transaction of business, and that any act of the Board of Directors requires a unanimous approval of all directors. Consequently, Mr. Cohen, as is the case with each of the other directors, has the ability to block actions of the Board. Mr. Cohen has agreed that, as a member of the Board of Directors, he will not participate in any Board vote regarding his position as Executive Chairman.

We have a significant firearms business in the U.S., which exposes us to increased risks of regulatory fines and penalties, lawsuits and related liabilities.

As discussed under “Part I, Item 1 — Business — Regulation — U.S. Regulations — Pawn Regulations,” some of our stores in the U.S. conduct pawn and retail transactions involving firearms, which may be associated with an increased risk of injury and related lawsuits. We may be subject to lawsuits relating to the improper use of firearms that we sell, including actions by persons attempting to recover damages from firearms retailers relating to misuse of firearms. We may also incur fines, penalties or liabilities, or have our federal firearms licenses revoked or suspended, if we fail to properly perform required background checks for, and otherwise record and report, firearms transactions. Any such actions could have a material adverse effect on our business, prospects, results of operations, financial condition and reputation.

Our business is subject to Team Member and third-party robberies, burglaries and other crimes at the store level.

The nature of our business requires us to maintain significant cash on hand, loan collateral and inventories in our stores. Consequently, we are subject to loss of cash or merchandise as a result of robberies, burglaries, thefts, riots, looting and other criminal activity in our stores. Further, we could be subject to liability to customers or other third parties as a result of such activities. While we maintain asset protection and monitoring programs to mitigate these risks, as well as insurance programs to

13

protect against catastrophic loss or exposure, there can be no assurance that these crimes will not occur or that such losses will not have an adverse effect on our business or results of operations.

Changes in competition from various sources could have a material adverse impact on our ability to achieve our plans.

We encounter significant competition from other pawn stores, consumer lending companies, other retailers, online retailers and auction sites, many of which have significantly greater financial resources than we do. Increases in the number or size of competitors or other changes in competitive influences, such as aggressive marketing and pricing practices, could adversely affect our operations. In Mexico, we compete directly with certain pawn stores owned and operated by government affiliated or sponsored non-profit foundations, and the government could take actions that would harm our ability to compete in that market.

Our continued profitability and growth plans are dependent on our ability to successfully design or acquire, deploy and maintain information technology and other business systems to support our current business and our planned growth and expansion.

The success of our business depends on the efficiency and reliability of our information technology and business systems and related controls, including the point-of-sale system utilized in our store locations. If access to our technology infrastructure is impaired (as may occur with a computer virus, a cyber-attack or other intentional disruption by a third party, natural disaster, telecommunications system failure, electrical system failure or lost connectivity), or if there are flaws in the design or roll-out of new or refreshed technology systems (such as our point-of-sale system), we may be unable to process transactions or otherwise carry on our business in a timely and efficient manner. An infrastructure disruption could damage our reputation and cause us to lose customers and revenue. We consider security risks from multiple viewpoints, including physical security as well as security of infrastructure and databases. As our technology infrastructure continues to evolve from on premise to cloud service providers, we continue to assess the security of such infrastructure, including third party service providers.

We invested in Cash Converters International Limited for strategic reasons. We may be required in future periods to impair our investment and recognize related investment losses, as we have done in the past, and we may not realize a positive return on the investment.

We currently own 34.75% of the outstanding ordinary shares of Cash Converters International, which is a publicly traded company based in Australia. We made the initial investment in November 2009 and have made incremental investments periodically since then. The success of this strategic investment is dependent on a variety of factors, including Cash Converters International’s business performance and the market’s assessment of that performance. We have recorded a number of impairments to the carrying value of our investment in Cash Converters International in the past. After an analysis of Cash Converters International’s stock price performance and other factors, we determined that the fair value of our investment in Cash Converters International at September 30, 2020 was greater than its carrying value. Accordingly, we did not record an impairment at that date. See Note 5 of Notes to Consolidated Financial Statements included in “Part II, Item 8 - Financial Statements and Supplemental Data.” If the fair value of our investment declines and we determine that such decline is other-than-temporary, we may be required to further impair our investment and recognize the related investment loss, which would adversely affect our results of operations and financial position in the period of impairment. Furthermore, there can be no assurance that we will be able to dispose of some or all of our investment in Cash Converters International on favorable terms, should we decide to do so in the future.

Our ability to recover our investment in RDC is heavily dependent on RDC's success and performance, including its ability to obtain further debt or equity financing.

We have an investment in Rich Data Corporation (“RDC”), a previously consolidated variable interest entity. See Note 6 of Notes to Consolidated Financial Statements included in “Part II, Item 8 — Financial Statements and Supplemental Data.” Our ability to recover our investment in RDC is heavily dependent on RDC's success and performance, potentially including its ability to obtain further debt or equity financing. To the extent that RDC is not successful, we may be required in future periods to impair our investment and recognize related investment losses.

We may incur property, casualty or other losses, including losses related to natural disasters such as hurricanes, earthquakes and volcanoes. Not all such losses will be covered by insurance.

We maintain a program of insurance coverage for various types of property, casualty and other risks. The types and amounts of insurance that we obtain vary from time to time, depending on availability, cost and our decisions with respect to risk retention. The policies are subject to deductibles and exclusions that result in our retention of a level of risk on a self-insurance basis. Losses not covered by insurance could be substantial and may increase our expenses, which could harm our results of operations and financial condition.

14

We have significant operations located in areas that are susceptible to hurricanes (notably the Atlantic and Gulf Coast regions of Florida, the Gulf Coast regions of Texas including Houston, as well as Mexico and Central America). Certain areas of our operations are also susceptible to other types of natural disasters such as earthquakes, volcanoes and tornadoes. As noted above, not all physical damage that we incur as a result of any such natural disaster will be covered by insurance due to policy deductibles and risk retentions. In addition, natural disasters could have a significant negative impact on our business beyond physical damage to property, including a reduction of our loan portfolio, inventory, pawn service charges and merchandise sales. Only limited portions, if any, of those negative impacts will be covered by applicable business interruption insurance policies. As a result, geographically isolated natural disasters could have a material adverse effect on our overall operations and financial performance.

Goodwill comprises a significant portion of our total assets. We assess goodwill for impairment at least annually, which could result in a material, non-cash write-down and could have a material adverse effect on our results of operations and financial conditions.

The carrying value of our goodwill was $257.6 million, or approximately 22% of our total assets, as of September 30, 2020. In accordance with Financial Accounting Standards Board Accounting Standards Codification 350-20-35, we test goodwill and intangible assets with an indefinite useful life for potential impairment annually, or more frequently if an event occurs or circumstances change that would more likely than not reduce the fair value of a reporting unit below its carrying value. These events or circumstances could include a significant change in the business climate, a change in strategic direction, legal factors, operating performance indicators, a change in the competitive environment, the sale or disposition of a significant portion of a reporting unit, or future economic factors such as unfavorable changes in the estimated future discounted cash flows of our reporting units. Our annual goodwill impairment test is performed in the fourth quarter utilizing the income approach. This approach uses future cash flows and estimated terminal values for each reporting unit (discounted using a market participant perspective) to determine the fair value of each reporting unit, which is then compared to the carrying value of the reporting unit to determine if an impairment exists. The income approach includes assumptions about revenue growth rates, operating margins and terminal growth rates discounted by an estimated weighted-average cost of capital derived from other publicly traded companies that are similar but not identical from an operational and economic standpoint.

During the second quarter of fiscal 2020, there was an indicator of impairment due to a decline in our market capitalization. We performed a quantitative analysis as of March 31, 2020 utilizing the income approach. As a result of our quantitative analysis, we determined the fair value of each of our reporting units was below its carrying value because of the impact of COVID-19, including a significant decline in pawn loan balances due to changes in typical customer behavior and mandated store closures in our GPMX countries. These factors impacted the forecast of future net revenues and earnings and resulted in lower present value of future cash flows. This led to a goodwill impairment charge of $41.3 million in the second quarter of fiscal 2020. These impairments were recorded under "Impairment of goodwill, intangible and other assets" in the Consolidated Statements of Operations

See Note 1 and Note 8 of Notes to Consolidated Financial Statements included in “Part II, Item 8 — Financial Statements and Supplementary Data” for a discussion of our annual impairment tests performed for goodwill and indefinite-lived intangible assets during fiscal 2020. We remain confident in our businesses, as all business units were performing well prior to the impact of COVID-19.

The conversion feature of our convertible notes, if triggered, may adversely affect our financial condition and operating results.

We have outstanding a total of $316.3 million of convertible notes. See Note 9 of Note to Consolidated Financial Statements included in “Part II, Item 8 — Financial Statements and Supplementary Data.” If the conversion feature of any of those convertible notes is triggered, holders will be entitled to convert the notes at their option at any time during specified periods. If one or more holders elect to convert their notes, we may be required, or may choose, to settle the obligation through the payment of cash, which could adversely affect our liquidity. In addition, even if holders do not elect to convert their notes, we could be required under applicable accounting rules to reclassify all or a portion of the outstanding principal of the convertible notes as a current rather than long-term liability, which would result in a material reduction of our net working capital.

Conversion of our convertible notes into stock may dilute the ownership interests of existing stockholders or may otherwise depress the price of our Class A Common Stock.

If it were to occur, the conversion of convertible notes would dilute the ownership interests of existing stockholders to the extent we deliver shares of Class A Common Stock upon conversion. Any sales in the public market of such shares could adversely affect prevailing market prices of our Class A Common Stock. In addition, the existence of the convertible notes may encourage short selling by market participants because the conversion of such notes could be used to satisfy short positions, or

15

anticipated conversion of the notes into shares of our Class A Common Stock could depress the price of our Class A Common Stock.

We have a limited number of unreserved shares available for future issuance, which may limit our ability to conduct future financings and other transactions and our ability to offer equity awards to management.

Our certificate of incorporation currently authorizes us to issue up to 100 million shares of Class A Common Stock. Taking into consideration the shares that are issued and outstanding, as well as the shares that have been reserved for issuance pursuant to convertible notes, warrants and outstanding equity incentive compensation awards and the conversion of the Class B Common Stock, we had approximately 10.4 million shares of authorized Class A Common Stock available for other uses as of September 30, 2020. Therefore, our ability to issue shares of Class A Common Stock (other than pursuant to the existing reserved-for commitments), or securities or instruments that are convertible into or exchangeable for shares of Class A Common Stock, may be limited until such time that additional authorized, unissued and unreserved shares become available or unless we determine that we are unlikely to issue all of the shares that are currently reserved. During this time, for example, our ability to complete equity or equity-linked financings or other transactions (including strategic acquisitions) that involve the issuance or potential issuance of Class A Common Stock may be limited. Further, our ability to offer equity-based compensation to our management team may also be limited, which could adversely affect our ability to align management’s incentives with stockholders or attract and retain key management personnel.

General Risks

Public health issues could adversely affect our financial condition, results of operations or liquidity.

Our business may be impacted by public health issues, including other pandemics and the spread of contagious diseases. Such public health issues, and the government and consumer responses thereto, may (i) limit our ability to supply products and services to our customers as a result of store closures, reduced access to or foot traffic in our stores, or labor shortages, (ii) adversely affect the demand for our products and services or (iii) cause other unforeseen negative developments. Any of these factors may adversely affect our financial condition, results of operations or liquidity.

We have significant operations in Latin America, and changes in the business, regulatory, political or social climate could impact our operations there, which could adversely affect our results of operations and growth plans.

We own and operate a significant number of pawn stores in Latin America (primarily Mexico, but also Guatemala, El Salvador, Honduras and Peru). Further, our growth plans include potential expansion in some of those countries as well as potentially other countries in Latin America. Doing business in those countries exposes us to risks related to political instability, corruption, economic volatility, drug cartel and gang-related violence, social unrest including riots and looting, tax and foreign investment policies, public safety and security concerns, and uncertain application of laws and regulations. Consequently, actions or events in any of those countries that are beyond our control could restrict our ability to operate there or otherwise adversely affect the profitability of those operations. Furthermore, changes in the business, regulatory or political climate in any of those countries, or significant fluctuations in currency exchange rates, could affect our ability to expand or continue our operations there, which could have a material adverse impact on our prospects, results of operations and cash flows. For a description of the current regulatory environment in the Latin American countries in which we operate, see “Mexico Regulations” and “Other Latin America Regulations” under “Part I, Item 1 — Business — Regulation.”

A significant change in foreign currency exchange rates could have a material adverse impact on our earnings and financial position.

We have foreign operations in Latin America (Mexico, Guatemala, Honduras, El Salvador and Peru) and an equity investment in Australia. Our assets and investments in, and earnings and dividends from each of these countries must be translated to U.S. dollars from their respective functional currencies. A significant weakening of any of these foreign currencies could result in lower assets and earnings in U.S. dollars, resulting in a potentially material adverse impact on our financial position, results of operations and cash flows.

Litigation and regulatory proceedings could have a material adverse impact on our business.

We are currently subject to various litigation and regulatory actions, and additional actions could arise in the future. Potential actions range from claims and assertions arising in the ordinary course of business (such as contract, customer or employment disputes) to more significant corporate-level matters or shareholder litigation. All of these matters are subject to inherent uncertainties, and unfavorable rulings could occur, which could include monetary damages, fines and penalties or other relief. Any unfavorable ruling or outcome could have a material adverse effect on our results of operations or could negatively affect our reputation.

16

Under our certificate of incorporation, we are generally obligated to indemnify our directors and officers for costs and liabilities they incur in their capacity as directors or officers of the Company. Consequently, if a proceeding names or involves any of our directors or officers, then (subject to certain exceptions) we are generally obligated to pay or reimburse the cost or liability such director or officer incurs as a result of such proceeding (including defense costs, judgments and amounts paid in settlement). We maintain management liability insurance that protects us from much of this potential indemnification exposure, as well as potential costs or liabilities that may be directly incurred by the Company in some cases. However, our insurance coverage is subject to deductibles and there may be elements of the costs or liabilities that are not covered under the insurance policies. In addition, to the extent that our ultimate liability in any such proceeding (or any combination of proceedings that are included in the same policy year) exceeds the management liability policy limits, our results of operations and financial condition could be adversely affected.

Our acquisitions, investments and other transactions could disrupt our ongoing business and harm our results of operations.

In pursuing our business strategy, we routinely conduct discussions, evaluate opportunities and enter into agreements regarding possible acquisitions, investments and other transactions. These transactions may involve significant challenges and risks, including risks that we may not realize the expected return on an acquisition or investment, that we may not be able to retain key personnel of an acquired business, or that we may experience difficulty in integrating acquired businesses into our business systems and processes. If we do enter into agreements with respect to acquisitions, investments or other transactions, we may fail to complete them due to inability to obtain required regulatory or other approvals or other factors. Furthermore, acquisitions, investments and other transactions require substantial management resources and have the potential to divert our attention from our existing business, and there are inherent risks in integrating and operating any acquired business. These factors could harm our business and results of operations.

We may be exposed to liabilities under applicable anti-bribery, anti-corruption, anti-money laundering and other general business laws and regulations, and any determination that we violated these laws or regulations could have a material adverse effect on our business.

We are subject to various anti-bribery and anti-corruption laws that prohibit improper payments or offers of payments to foreign governments and their officials for the purpose of obtaining or retaining business, including the Foreign Corrupt Practices Act in the U.S. and the General Law of Administrative Responsibility in Mexico. We are also subject to various laws and regulations designed to prevent money laundering or the financial support of terrorism or other illegal activity, including the USA PATRIOT Act and the Bank Secrecy Act in the U.S. and The Federal Law for the Prevention and Identification of Transactions with Funds From Illegal Sources in Mexico. See “Part I, Item 1 — Business — Regulation.” Further, our business is expanding in countries and regions that are less developed and are generally recognized as potentially more corrupt business and political environments.

While we maintain controls and policies to ensure compliance with applicable laws and regulations, these controls and policies may prove to be less than effective. If team members, agents or other persons for whose conduct we are held responsible violate our policies, we may be subject to severe criminal or civil sanctions and penalties, and we may be subject to other liabilities that could have a material adverse effect on our business, results of operations and financial condition.

Changes in our liquidity and capital requirements or in access to capital markets or other financing and transactional banking sources could limit our ability to achieve our plans.

A significant reduction in cash flows from operations or the availability of debt or equity financing could materially and adversely affect our ability to achieve our planned growth and operating results. Our ability to obtain debt or equity financing, including the possible refinancing of existing indebtedness, will depend upon market conditions, our financial condition and the willingness of financing sources to make capital available to us at acceptable rates and terms. The inability to access capital at acceptable rates and terms could restrict or limit our ability to achieve our growth objectives, which could adversely affect our financial condition and results of operations.

Our access to transactional banking services, as well as international wire services between certain countries, is an ongoing business requirement. Inability in accessing or maintaining transactional banking or wire services could lead to increased costs or the inability to efficiently manage our cash as we would be required to seek alternative banking services or obtain services from several regional or local retail banks.

17

We collect and store a variety of sensitive customer information, and breaches in data security or other cyber-attacks could harm our business operations and lead to reputational damage.

In the course of conducting our business, we collect and store on our information technology systems a variety of information about our customers, including sensitive personal identifying and financial information. We may not have the resources or technical expertise to anticipate or prevent rapidly evolving types of cyber-attacks. Attacks may be targeted at us, our service providers, our customers or others who have entrusted us with information. Actual or anticipated attacks may cause us to incur increased costs, including costs to hire additional personnel, purchase additional protection technologies, train team members and engage third-party experts and consultants. Advances in computer capabilities, new technological discoveries or other developments may result in the technology we use to protect data being breached or compromised. In addition, data and security breaches can occur as a result of non-technical issues, including breach by us or by persons with whom we have commercial relationships that result in the unauthorized release of personal or confidential information. We could be subject to fines, penalties and liabilities if any such information is misappropriated from our systems or we otherwise fail to maintain the security and confidentiality of such information. Further, any such data security breach could cause damage to our reputation and a loss of confidence in our data security measures, which could adversely affect our business and prospects.

We may face business interruptions or other adverse effects on our operations and growth.