UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended March 31, 2024

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

Commission File Number 0-19311

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(617 ) 679-2000

(Address, including zip code, and telephone number, including

area code, of registrant’s principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | |||||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files): Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act:

| x | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

The number of shares of the issuer’s Common Stock, $0.0005 par value, outstanding as of April 23, 2024, was 145,596,895 shares.

BIOGEN INC.

FORM 10-Q — Quarterly Report

For the Quarterly Period Ended March 31, 2024

TABLE OF CONTENTS

| Page | ||||||||

PART I — FINANCIAL INFORMATION | ||||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

PART II — OTHER INFORMATION | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

2

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements that are being made pursuant to the provisions of the Private Securities Litigation Reform Act of 1995 (the Act) with the intention of obtaining the benefits of the “Safe Harbor” provisions of the Act. These forward-looking statements may be accompanied by such words as “aim,” “anticipate,” “believe,” “could,” "contemplate," "continue," “estimate,” “expect,” “forecast,” "goal," “intend,” “may,” “plan,” “potential,” “possible,” "predict," "project", "should," "target," “will,” “would” or the negative of these words or other words and terms of similar meaning. Reference is made in particular to forward-looking statements regarding:

•the anticipated amount, timing and accounting of revenue; contingent, milestone, royalty and other payments under licensing, collaboration, acquisition or divestiture agreements; tax positions and contingencies; collectability of receivables; pre-approval inventory; cost of sales; research and development costs; compensation and other selling, general and administrative expense; amortization of intangible assets; foreign currency exchange risk; estimated fair value of assets and liabilities; and impairment assessments;

•expectations, plans and prospects relating to product approvals, sales, pricing, growth, reimbursement and launch of our marketed and pipeline products;

•the potential impact of increased product competition in the markets in which we compete, including increased competition from new originator therapies, generics, prodrugs and biosimilars of existing products and products approved under abbreviated regulatory pathways, including generic or biosimilar versions of our products or competing products;

•patent terms, patent term extensions, patent office actions and expected availability and periods of regulatory exclusivity;

•our plans and investments in our portfolio as well as implementation of our corporate strategy;

•the execution of our strategic and growth initiatives, including the ultimate success of our acquisition of Reata and our ability to realize the anticipated benefits from the acquisition, including future performance of the SKYCLARYS product and anticipated synergies, as well as the exploration of strategic options for our biosimilars business;

•the drivers for growing our business, including our plans and intention to commit resources relating to discovery, research and development programs and business development opportunities as well as the potential benefits and results of, and the anticipated completion of, certain business development transactions and cost-reduction measures, including our Fit for Growth program;

•the expectations, development plans and anticipated timelines, including costs and timing of potential clinical trials, regulatory filings and approvals, of our products, drug candidates and pipeline programs, including collaborations with third-parties, as well as the potential therapeutic scope of the development and commercialization of our and our collaborators’ pipeline products;

•the timing, outcome and impact of administrative, regulatory, legal and other proceedings related to our patents and other proprietary and intellectual property rights, tax audits, assessments and settlements, pricing matters, sales and promotional practices, product liability, investigations and other matters;

•our ability to finance our operations and business initiatives and obtain funding for such activities;

•adverse safety events involving our marketed or pipeline products, generic or biosimilar versions of our marketed products or any other products from the same class as one of our products;

•the current and potential impacts of geopolitical tensions, acts of war and other large-scale crises, including impacts to our operations, sales and the possible disruptions or delay in our plans to conduct clinical trial activities in areas of geopolitical tension, including regions affected by Russia's invasion of Ukraine and the military conflict in the Middle East;

•the direct and indirect impact of global health outbreaks on our business and operations, including sales, expense, reserves and allowances, the supply chain, manufacturing, research and development costs, clinical trials and employees;

•our use of information systems and data and the potential impacts of any breakdowns, invasions, corruptions, destructions and/or breaches of such systems or those of our business partners;

3

•the potential impact of healthcare reform in the U.S., including the IRA, and measures being taken worldwide designed to reduce healthcare costs and limit the overall level of government expenditures, including the impact of pricing actions and reduced reimbursement for our products;

•our manufacturing capacity, use of third-party contract manufacturing organizations, plans and timing relating to changes in our manufacturing capabilities, activities in new or existing manufacturing facilities and the expected timeline for the gene therapy manufacturing facility in RTP, North Carolina to be operational;

•the impact of the continued uncertainty of the credit and economic conditions in certain countries and our collection of accounts receivable in such countries;

•lease commitments, purchase obligations and the timing and satisfaction of other contractual obligations; and

•the impact of new laws (including tax), regulatory requirements, judicial decisions and accounting standards.

These forward-looking statements involve risks and uncertainties, including those that are described in Item 1A. Risk Factors included in this report and elsewhere in this report, that could cause actual results to differ materially from those reflected in such statements. Because some of these risks and uncertainties cannot be predicted or quantified and some are beyond our control, you should not rely on our forward-looking statements as predictions of future events and you should not place undue reliance on these statements. Moreover, we operate in a very competitive and rapidly changing environment, new risks and uncertainties may emerge from time to time and it is not possible for us to predict all risks nor identify all uncertainties. Forward-looking statements speak only as of the date of this report and are based on information and estimates available to us at this time. Except as required by law, we do not undertake any obligation to publicly update any forward-looking statements, whether as a result of new information, future developments or otherwise. You should read this report with the understanding that our actual future results, performance, events and circumstances might be materially different from what we expect.

NOTE REGARDING COMPANY AND PRODUCT REFERENCES

References in this report to:

•“Biogen,” the “company,” “we,” “us” and “our” refer to Biogen Inc. and its consolidated subsidiaries; and

•“RITUXAN” refers to both RITUXAN (the trade name for rituximab in the U.S., Canada and Japan) and MabThera (the trade name for rituximab outside the U.S., Canada and Japan).

NOTE REGARDING TRADEMARKS

ADUHELM®, AVONEX®, BYOOVIZ®, PLEGRIDY®, QALSODY®, RITUXAN®, RITUXAN HYCELA®, SKYCLARYS®, SPINRAZA®, TECFIDERA®, TYSABRI® and VUMERITY® are registered trademarks of Biogen.

BENEPALI™, FLIXABI™, FUMADERM™, IMRALDI™ and TOFIDENCE™ are trademarks of Biogen.

ACTEMRA®, COLUMVI®, ENBREL®, EYLEA®, FAMPYRA™, GAZYVA®, LEQEMBI®, HUMIRA®, LUCENTIS®, LUNSUMIO®, OCREVUS®, REMICADE®, ZURZUVAE™ and other trademarks referenced in this report are the property of their respective owners.

4

DEFINED TERMS

| 2023 Form 10-K | Annual Report on Form 10-K for the year ended December 31, 2023 | ||||

| 2020 Share Repurchase Program | Board of Directors authorized program to repurchase up to $5.0 billion of our common stock | ||||

AbbVie | AbbVie Inc. | ||||

| Acorda | Acorda Therapeutics, Inc. | ||||

| AI | Artificial Intelligence | ||||

| Alkermes | Alkermes plc | ||||

| ALS | Amyotrophic Lateral Sclerosis | ||||

| AOCI | Accumulated Other Comprehensive Income (Loss) | ||||

| ASU | Accounting Standards Update | ||||

| ATV | Antibody Transport Vehicle | ||||

| BLA | Biologics License Application | ||||

| Blackstone | Blackstone Life Sciences | ||||

| CCPA | California Consumer Privacy Act | ||||

| CHMP | Committee for Medicinal Products for Human Use | ||||

CISA | Cybersecurity and Infrastructure Security Agency | ||||

| CJEU | Court of Justice of the European Union | ||||

| CLE | Cutaneous Lupus Erythematosus | ||||

| CLL | Chronic Lymphocytic Leukemia | ||||

| CLO | Chief Legal Officer | ||||

CODM | Chief Operating Decision Maker | ||||

| Convergence | Convergence Pharmaceuticals Ltd. | ||||

| CRL | Complete Response Letter | ||||

| CROs | Contract Research Organizations | ||||

DEA | Drug Enforcement Agency | ||||

| Denali | Denali Therapeutics Inc. | ||||

District Court | U.S. District Court for the District of Massachusetts | ||||

| DOJ | U.S. Department of Justice | ||||

| EC | European Commission | ||||

| Eisai | Eisai Co., Ltd. | ||||

| EMA | European Medicines Agency | ||||

| EPO | European Patent Office | ||||

| ERM | Enterprise Risk Management | ||||

| E.U. | European Union | ||||

| FA | Friedreich's Ataxia | ||||

| FASB | Financial Accounting Standards Board | ||||

| FCPA | Foreign Corrupt Practices Act | ||||

| FDA | U.S. Food and Drug Administration | ||||

| FDIC | Federal Deposit Insurance Corporation | ||||

| Fit for Growth | Cost saving program initiated in 2023 | ||||

FSS | Federal Supply Schedule | ||||

| Genentech | Genentech, Inc. | ||||

| GILTI | Global Intangible Low Tax Income | ||||

| GloBE | Global Anti-Base Erosion | ||||

| GMP | Good Manufacturing Practices | ||||

5

DEFINED TERMS (continued)

| Humana | Humana Inc. | ||||

| IPR&D | In-process Research and Development | ||||

| Ionis | Ionis Pharmaceuticals Inc. | ||||

| IRA | Inflation Reduction Act of 2022 | ||||

| IT | Information Technology | ||||

| IV | Intravenous | ||||

| LRRK2 | Leucine-Rich Repeat Kinase 2 | ||||

| MAA | Marketing Authorization Application | ||||

| MDD | Major Depressive Disorder | ||||

| MS | Multiple Sclerosis | ||||

| Mylan Ireland | Mylan Ireland Ltd. | ||||

| NCD | National Coverage Decision | ||||

| NDA | New Drug Application | ||||

| Neurimmune | Neurimmune SubOne AG | ||||

| NMPA | National Medicinal Products Administration | ||||

| OECD | Organization for Economic Co-operation and Development | ||||

| OIE | Other (Income) Expense, Net | ||||

| Polpharma | Polpharma Biologics S.A. | ||||

| PPACA | Patient Protection and Affordable Care Act | ||||

| PPD | Postpartum Depression | ||||

| PPMS | Primary Progressive MS | ||||

| PRV | Priority Review Voucher | ||||

| R&D | Research and Development | ||||

| Reata | Reata Pharmaceuticals, Inc. | ||||

| RMS | Relapsing MS | ||||

| RRMS | Relapsing-Remitting MS | ||||

| RTP | Research Triangle Park | ||||

| Sage | Sage Therapeutics, Inc. | ||||

| Samsung Bioepis | Samsung Bioepis Co., Ltd. | ||||

| Samsung BioLogics | Samsung BioLogics Co., Ltd. | ||||

| Sangamo | Sangamo Therapeutics, Inc. | ||||

SEC | U.S. Securities and Exchange Commission | ||||

| SG&A | Selling, General and Administrative | ||||

| SLE | Systemic Lupus Erythematosus | ||||

| SMA | Spinal Muscular Atrophy | ||||

| SMN | Survival Motor Neuron | ||||

| SOD1 | Superoxide Dismutase 1 | ||||

| SWISSMEDIC | Swiss Agency for Therapeutic Products | ||||

| TBA | Technical Boards of Appeal | ||||

| Transition Toll Tax | A one-time mandatory deemed repatriation tax on accumulated foreign subsidiaries' previously untaxed foreign earnings | ||||

| U.K. | United Kingdom | ||||

| U.S. | United States | ||||

| U.S. GAAP | Accounting Principles Generally Accepted in the U.S. | ||||

VA | Veterans Administration | ||||

6

PART I FINANCIAL INFORMATION

BIOGEN INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME

(unaudited, in millions, except per share amounts)

| For the Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Revenue: | |||||||||||

| Product, net | $ | $ | |||||||||

| Revenue from anti-CD20 therapeutic programs | |||||||||||

| Contract manufacturing, royalty and other revenue | |||||||||||

| Total revenue | |||||||||||

| Cost and expense: | |||||||||||

| Cost of sales, excluding amortization and impairment of acquired intangible assets | |||||||||||

| Research and development | |||||||||||

| Selling, general and administrative | |||||||||||

| Amortization and impairment of acquired intangible assets | |||||||||||

| Collaboration profit sharing/(loss reimbursement) | |||||||||||

| Restructuring charges | |||||||||||

| Other (income) expense, net | |||||||||||

| Total cost and expense | |||||||||||

| Income before income tax (benefit) expense | |||||||||||

| Income tax (benefit) expense | |||||||||||

| Net income | |||||||||||

| Net income (loss) attributable to noncontrolling interests, net of tax | ( | ||||||||||

| Net income attributable to Biogen Inc. | $ | $ | |||||||||

| Net income per share: | |||||||||||

| Basic earnings per share attributable to Biogen Inc. | $ | $ | |||||||||

| Diluted earnings per share attributable to Biogen Inc. | $ | $ | |||||||||

| Weighted-average shares used in calculating: | |||||||||||

| Basic earnings per share attributable to Biogen Inc. | |||||||||||

| Diluted earnings per share attributable to Biogen Inc. | |||||||||||

See accompanying notes to these unaudited condensed consolidated financial statements.

7

BIOGEN INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(unaudited, in millions)

| For the Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Net income (loss) attributable to Biogen Inc. | $ | $ | |||||||||

| Other comprehensive income: | |||||||||||

Unrealized gains (losses) on securities available for sale, net of tax | |||||||||||

Unrealized gains (losses) on cash flow hedges, net of tax | ( | ||||||||||

Unrealized gains (losses) on pension benefit obligation, net of tax | ( | ||||||||||

Currency translation adjustment | ( | ||||||||||

| Total other comprehensive income (loss), net of tax | ( | ( | |||||||||

| Comprehensive income (loss) attributable to Biogen Inc. | |||||||||||

| Comprehensive income (loss) attributable to noncontrolling interests, net of tax | ( | ||||||||||

| Comprehensive income (loss) | $ | $ | |||||||||

See accompanying notes to these unaudited condensed consolidated financial statements.

8

BIOGEN INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(unaudited, in millions, except per share amounts)

| As of March 31, 2024 | As of December 31, 2023 | ||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

Accounts receivable, net of allowance for doubtful accounts of $ | |||||||||||

| Due from anti-CD20 therapeutic programs | |||||||||||

| Inventory | |||||||||||

| Other current assets | |||||||||||

| Total current assets | |||||||||||

| Property, plant and equipment, net | |||||||||||

| Operating lease assets | |||||||||||

| Intangible assets, net | |||||||||||

| Goodwill | |||||||||||

| Deferred tax asset | |||||||||||

| Investments and other assets | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES AND EQUITY | |||||||||||

| Current liabilities: | |||||||||||

| Current portion of term loan | $ | $ | |||||||||

| Taxes payable | |||||||||||

| Accounts payable | |||||||||||

| Accrued expense and other | |||||||||||

| Total current liabilities | |||||||||||

| Notes payable and term loan | |||||||||||

| Deferred tax liability | |||||||||||

| Long-term operating lease liabilities | |||||||||||

| Other long-term liabilities | |||||||||||

| Total liabilities | |||||||||||

| Commitments, contingencies and guarantees | |||||||||||

| Equity: | |||||||||||

| Biogen Inc. shareholders’ equity: | |||||||||||

Preferred stock, par value $ | |||||||||||

Common stock, par value $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated other comprehensive income (loss) | ( | ( | |||||||||

| Retained earnings | |||||||||||

| Treasury stock, at cost | ( | ( | |||||||||

| Total equity | |||||||||||

| Total liabilities and equity | $ | $ | |||||||||

See accompanying notes to these unaudited condensed consolidated financial statements.

9

BIOGEN INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOW

(unaudited, in millions)

| For the Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Cash flow from operating activities: | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash flow from operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Excess and obsolescence charges related to inventory | |||||||||||

| Amortization of inventory step-up | |||||||||||

| Share-based compensation | |||||||||||

| Deferred income taxes | ( | ||||||||||

| (Gain) loss on strategic investments | |||||||||||

| Other | |||||||||||

| Changes in operating assets and liabilities, net of effects of business acquired: | |||||||||||

| Accounts receivable | |||||||||||

| Due from anti-CD20 therapeutic programs | |||||||||||

| Inventory | ( | ||||||||||

| Accrued expense and other current liabilities | ( | ( | |||||||||

| Income tax assets and liabilities | ( | ||||||||||

| Other changes in operating assets and liabilities, net | ( | ( | |||||||||

| Net cash flow provided by (used in) operating activities | |||||||||||

| Cash flow from investing activities: | |||||||||||

| Purchases of property, plant and equipment | ( | ( | |||||||||

| Proceeds from sales and maturities of marketable securities | |||||||||||

| Purchases of marketable securities | ( | ||||||||||

| Acquisitions of intangible assets | ( | ( | |||||||||

| Proceeds from sales of strategic investments | |||||||||||

| Other | ( | ( | |||||||||

| Net cash flow provided by (used in) investing activities | ( | ( | |||||||||

| Cash flow from financing activities: | |||||||||||

| Payments related to issuance of stock for share-based compensation arrangements, net | ( | ( | |||||||||

| Repayment of borrowings and premiums paid | ( | ||||||||||

| Net (distribution) contribution to noncontrolling interest | |||||||||||

| Other | |||||||||||

| Net cash flow provided by (used in) financing activities | ( | ( | |||||||||

| Net increase (decrease) in cash and cash equivalents | ( | ||||||||||

| Effect of exchange rate changes on cash and cash equivalents | ( | ||||||||||

| Cash and cash equivalents, beginning of the period | |||||||||||

| Cash and cash equivalents, end of the period | $ | $ | |||||||||

See accompanying notes to these unaudited condensed consolidated financial statements.

10

BIOGEN INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF EQUITY

(unaudited, in millions)

| March 31, 2024 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Preferred stock | Common stock | Additional paid-in capital | Accumulated other comprehensive loss | Retained earnings | Treasury stock | Total equity | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance, December 31, 2023 | $ | $ | $ | $ | ( | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss), net of tax | — | — | — | — | — | ( | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock under stock option and stock purchase plans | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock under stock award plan | — | — | — | ( | — | — | — | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Compensation related to share-based payments | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Other | — | — | — | — | ( | — | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||

| Balance, March 31, 2024 | $ | $ | $ | $ | ( | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2023 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Preferred stock | Common stock | Additional paid-in capital | Accumulated other comprehensive loss | Retained earnings | Treasury stock | Total Biogen Inc. shareholders’ equity | Noncontrolling interests | Total equity | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance, December 31, 2022 | $ | $ | $ | $ | ( | $ | ( | $ | ( | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | — | — | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss), net of tax | — | — | — | — | — | ( | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Capital contribution from noncontrolling interest | — | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock under stock option and stock purchase plans | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock under stock award plan | — | — | — | ( | — | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Compensation related to share-based payments | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other | — | — | — | — | ( | — | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance, March 31, 2023 | $ | $ | $ | $ | ( | $ | ( | $ | ( | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

See accompanying notes to these unaudited condensed consolidated financial statements.

11

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Note 1: | Summary of Significant Accounting Policies | ||||

References in these notes to "Biogen," the "company," "we," "us" and "our" refer to Biogen Inc. and its consolidated subsidiaries.

Business Overview

Biogen is a global biopharmaceutical company focused on discovering, developing and delivering innovative therapies for people living with serious and complex diseases worldwide. We have a broad portfolio of medicines to treat MS, have introduced the first approved treatment for SMA, co-developed treatments to address a defining pathology of Alzheimer’s disease and launched the first approved treatment to target a genetic cause of ALS. Through our 2023 acquisition of Reata we market the first and only drug approved in the U.S. and the E.U. for the treatment of Friedreich's Ataxia in adults and adolescents aged 16 years and older. We are focused on advancing our pipeline in neurology, specialized immunology and rare diseases. We support our drug discovery and development efforts through internal research and development programs and external collaborations.

Our marketed products include TECFIDERA, VUMERITY, AVONEX, PLEGRIDY, TYSABRI and FAMPYRA for the treatment of MS; SPINRAZA for the treatment of SMA; SKYCLARYS for the treatment of Friedreich's Ataxia; QALSODY for the treatment of ALS; and FUMADERM for the treatment of severe plaque psoriasis.

We also have collaborations with Eisai on the commercialization of LEQEMBI for the treatment of Alzheimer's disease and Sage on the commercialization of ZURZUVAE for the treatment of PPD and we have certain business and financial rights with respect to RITUXAN for the treatment of non-Hodgkin's lymphoma, CLL and other conditions; RITUXAN HYCELA for the treatment of non-Hodgkin's lymphoma and CLL; GAZYVA for the treatment of CLL and follicular lymphoma; OCREVUS for the treatment of PPMS and RMS; LUNSUMIO for the treatment of relapsed or refractory follicular lymphoma; COLUMVI, a bispecific antibody for the treatment of non-Hodgkin's lymphoma; and have the option to add other potential anti-CD20 therapies, pursuant to our collaboration arrangements with Genentech, a wholly-owned member of the Roche Group.

We commercialize a portfolio of biosimilars of advanced biologics including BENEPALI, an etanercept biosimilar referencing ENBREL, IMRALDI, an adalimumab biosimilar referencing HUMIRA, and FLIXABI, an infliximab biosimilar referencing REMICADE, in certain countries in Europe, as well as BYOOVIZ, a ranibizumab biosimilar referencing LUCENTIS, in the U.S. and certain international markets. We also have exclusive rights to commercialize TOFIDENCE, a tocilizumab biosimilar referencing ACTEMRA. We continue to develop potential biosimilar product SB15, a proposed aflibercept biosimilar referencing EYLEA.

For additional information on our collaboration arrangements, please read Note 19, Collaborative and Other Relationships, to these unaudited condensed consolidated financial statements (condensed consolidated financial statements).

Basis of Presentation

In the opinion of management, our condensed consolidated financial statements include all adjustments, consisting of normal recurring accruals, necessary for a fair statement of our financial statements for interim periods in accordance with U.S. GAAP. The information included in this quarterly report on Form 10-Q should be read in conjunction with our audited consolidated financial statements and the accompanying notes included in our 2023 Form 10-K. Our accounting policies are described in the Notes to Consolidated Financial Statements in our 2023 Form 10-K and updated, as necessary, in this report. The year-end condensed consolidated balance sheet data presented for comparative purposes was derived from our audited financial statements, but does not include all disclosures required by U.S. GAAP. The results of operations for the three months ended March 31, 2024, are not necessarily indicative of the operating results for the full year or for any other subsequent interim period.

We operate as one operating segment, focused on discovering, developing and delivering worldwide innovative therapies for people living with serious neurological and neurodegenerative diseases as well as related therapeutic adjacencies.

12

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

Consolidation

Our condensed consolidated financial statements reflect our financial statements, those of our wholly-owned subsidiaries and certain variable interest entities where we are the primary beneficiary. For consolidated entities where we own or are exposed to less than 100.0 % of the economics, we record net income (loss) attributable to noncontrolling interests, net of tax in our condensed consolidated statements of income equal to the percentage of the economic or ownership interest retained in such entities by the respective noncontrolling parties. Intercompany balances and transactions are eliminated in consolidation.

In determining whether we are the primary beneficiary of a variable interest entity, we apply a qualitative approach that determines whether we have both (1) the power to direct the economically significant activities of the entity and (2) the obligation to absorb losses of, or the right to receive benefits from, the entity that could potentially be significant to that entity. We continuously assess whether we are the primary beneficiary of a variable interest entity as changes to existing relationships or future transactions may result in us consolidating or deconsolidating one or more of our collaborators or partners. In November 2023 we terminated the Neurimmune Agreement, which resulted in the deconsolidation of our variable interest entity, Neurimmune. For additional information on the deconsolidation of Neurimmune, please read Note 20, Investments in Variable Interest Entities, to these condensed consolidated financial statements.

Use of Estimates

The preparation of our condensed consolidated financial statements requires us to make estimates, judgments and assumptions that may affect the reported amounts of assets, liabilities, equity, revenue and expense and related disclosure of contingent assets and liabilities. On an ongoing basis we evaluate our estimates, judgments and assumptions. We base our estimates on historical experience and on various other assumptions that we believe are reasonable, the results of which form the basis for making judgments about the carrying values of assets, liabilities and equity and the amount of revenue and expense. Actual results may differ from these estimates.

Significant Accounting Policies

New Accounting Pronouncements

From time to time, new accounting pronouncements are issued by the FASB or other standard setting bodies that we adopt as of the specified effective date. Unless otherwise discussed below, we do not believe that the adoption of recently issued standards have had or may have a material impact on our condensed consolidated financial statements or disclosures.

Climate-Related Disclosures

In March 2024 the SEC issued a final rule under SEC Release No. 33-11275, The Enhancement and Standardization of Climate-Related Disclosures for Investors. This new rule will require large accelerated filers to disclose material climate-related risks that are reasonably likely to have a material impact on its business, results of operations or financial condition. The required information about climate-related risks will also include disclosure of material direct greenhouse gas emissions from operations owned or controlled (Scope 1) and/or material indirect greenhouse gas emissions from purchased energy consumed in owned or controlled operations (Scope 2). Additionally, the new rules will require disclosure within the notes to the financial statements of the effects of severe weather events and other natural conditions and information on any climate-related targets or goals, subject to certain materiality thresholds. The final rule, if adopted, includes a phased-in compliance period which will begin phasing in with our annual report for the year ending December 31, 2025.

In April 2024 the SEC voluntarily stayed implementation of the new climate-related disclosure requirements pending judicial review. We are currently evaluating the potential impact that this new rule will have on our company's disclosures.

13

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

Segment Reporting

In November 2023 the FASB issued ASU No. 2023-07, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosure. This standard requires disclosure of significant segment expenses that are regularly provided to the CODM and included within each reported measure of segment profit or loss, an amount and description of its composition for other segment items to reconcile to segment profit or loss and the title and position of the entity's CODM. The amendments in this update also expand the interim segment disclosure requirements. All disclosure requirements under this standard are also required for public entities with a single reportable segment. This standard is effective for fiscal years beginning after December 15, 2023, and interim periods within fiscal years beginning after December 15, 2024. Early adoption is permitted and the amendments in this update are required to be applied on a retrospective basis. We are currently evaluating the potential impact that this new standard will have on our condensed consolidated financial statements and related disclosures.

Note 2: | Acquisitions | ||||

Reata Pharmaceuticals, Inc.

On September 26, 2023, we completed the acquisition of all of the issued and outstanding shares of Reata, a biopharmaceutical company focused on developing therapeutics that regulate cellular metabolism and inflammation in serious neurologic diseases. As a result of this transaction we acquired SKYCLARYS (omaveloxolone), the first and only drug approved in the U.S. and the E.U. for the treatment of Friedreich's Ataxia in adults and adolescents aged 16 years and older, as well as other clinical and preclinical pipeline programs. The acquisition of Reata is expected to complement our global portfolio of neuromuscular and rare disease therapies. The addition of SKYCLARYS is anticipated to provide potential operating synergies with SPINRAZA and QALSODY.

Under the terms of this acquisition, we paid Reata shareholders $172.50 in cash for each issued and outstanding Reata share, which totaled approximately $6.6 billion. In addition, we agreed to pay approximately $983.9 million in cash for Reata's outstanding equity awards, inclusive of employer taxes, of which approximately $590.5 million was attributable to pre-acquisition services and is therefore reflected as a component of total purchase price paid. Of the $983.9 million paid to Reata's equity award holders, we recognized approximately $393.4 million as compensation attributable to the post-acquisition service period, of which $196.4 million was recognized as a charge to selling, general and administrative expense with the remaining $197.0 million as a charge to research and development expense within our condensed consolidated statements of income for the year ended December 31, 2023. These amounts were associated with the accelerated vesting of stock options and RSUs previously granted to Reata employees and required no future services to vest.

We funded this acquisition through available cash, cash equivalents and marketable securities, supplemented by the issuance of a $1.0 billion term loan under our term loan credit agreement. For additional information on our term loan credit agreement, please read Note 13, Indebtedness, to these condensed consolidated financial statements.

We accounted for this acquisition as a business combination using the acquisition method of accounting in accordance with ASC Topic 805, Business Combinations, and recorded assets acquired and liabilities assumed at their respective fair values as of the acquisition date.

Purchase Price Consideration

Total consideration transferred for the acquisition of Reata is summarized as follows:

| (In millions) | As of September 26, 2023 | |||||||

Cash consideration paid to Reata shareholders(1) | $ | |||||||

Fair value of Reata equity compensation pre-acquisition services and related taxes(2) | ||||||||

| Total consideration | $ | |||||||

(1) Represents cash consideration transferred of $172.50 per outstanding Reata ordinary share based on 38.3 million Reata shares outstanding at closing.

(2) Represents the fair value of Reata stock options and stock units issued to Reata equity award holders and the related taxes attributable to pre-acquisition vesting services.

14

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

Preliminary Purchase Price Allocation

The following table summarizes the provisional amounts recognized for assets acquired and liabilities assumed as of the acquisition date, as well as measurement period adjustments made year-to-date to the amounts initially recorded as of the acquisition date on September 26, 2023. The measurement period adjustments summarized below resulted from updates to our valuation assumptions related to the estimated amounts and timing of future cash flows associated with certain intangible assets, updates of our assumptions related to the quantities, selling location and remaining manufacturing and selling costs of acquired inventory, and other assets and liabilities. The related impact to our condensed consolidated statements of income that would have been recognized in previous periods if the adjustments were recognized as of the acquisition date is immaterial.

| (In millions) | Amounts Recognized as of Acquisition Date (as adjusted) March 31, 2024 | |||||||

| Cash and cash equivalents | $ | |||||||

| Accounts receivable | ||||||||

| Inventory | ||||||||

| Other current assets | ||||||||

| Intangible assets: | ||||||||

| Completed technology for SKYCLARYS (U.S.) | ||||||||

| In-process research and development (omaveloxolone) | ||||||||

| Priority review voucher | ||||||||

| Other clinical programs | ||||||||

| Operating lease assets | ||||||||

Accrued expense and other(1) | ( | |||||||

| Debt payable | ( | |||||||

| Contingent payable to Blackstone | ( | |||||||

Deferred tax liability(1) | ( | |||||||

| Operating lease liabilities | ( | |||||||

| Other assets and liabilities, net | ( | |||||||

| Total identifiable net assets | ||||||||

Goodwill(1) | ||||||||

| Total assets acquired and liabilities assumed | $ | |||||||

(1) Includes measurement period adjustments recorded in the first quarter of 2024 that increased accrued expense and other by $4.9 million, deferred tax liability by $4.1 million and goodwill by $9.0 million.

Inventory: Total inventory acquired was approximately $1.3 billion, which reflects a step-up in the fair value of finished goods and work-in-process inventory for SKYCLARYS. The fair value was determined based on the estimated selling price of the inventory, less the remaining manufacturing and selling costs and a normal profit margin on those manufacturing and selling efforts. This fair value step-up adjustment is being amortized to cost of sales within our condensed consolidated statements of income as the inventory is sold, which is expected to be within approximately 3 years from the acquisition date. For the three months ended March 31, 2024, amortization from the fair value step-up adjustment as a result of inventory sold was approximately $44.1 million.

Intangible assets: Intangible assets are comprised of $4.2 billion related to SKYCLARYS commercialization rights in the U.S., $2.3 billion of IPR&D related to the omaveloxolone program outside the U.S., which had not yet received regulatory approval in the E.U. as of the acquisition date, $100.0 million related to a rare pediatric disease priority voucher which may be used to obtain priority review by the FDA for a future regulatory submission or sold to a third party and $40.0 million related to other clinical programs. The estimated fair values of the program related intangible assets were determined using a multi-period excess earnings method, a form of the income approach, utilizing a discount rate of 14.3 % and the estimated fair value of the priority review voucher was based on recent external purchase and sale transactions of similar vouchers.

15

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

Our valuation of the SKYCLARYS commercialization rights reflects the assumption that, using an economic consumption model, the related $4.2 billion intangible asset will be amortized over its expected economic life.

Upon SKYCLARYS receiving E.U. regulatory approval in February 2024, we began selling the product in certain countries in Europe, and began amortizing the $2.3 billion IPR&D asset related to the program outside the U.S. over its expected economic life using an economic consumption model.

These fair value measurements were based on significant inputs not observable in the market and thus represent Level 3 fair value measurements.

Leases: We assumed responsibility for a single-tenant, build-to-suit building of approximately 327,400 square feet of office and laboratory space located in Plano, Texas, with an initial lease term of 16 years. We recorded a lease liability of approximately $151.8 million, which represents the net present value of rental expense over the remaining lease term of approximately 15 years, with a corresponding right-of-use asset of approximately $121.2 million, which represents our estimate of the fair value for a market participant of the current rental market in the Dallas, Texas area. Included in our estimate of the market rental rate is the value of any leasehold improvements or tenant allowances related to the building. We do not intend to occupy this building and are evaluating opportunities to sublease the property.

Goodwill: Goodwill was calculated as the excess of the consideration transferred over the net assets recognized and represents the future economic benefits arising from the other assets acquired that could not be individually identified and separately recognized. We recognized goodwill of approximately $473.5 million, which is not deductible for tax purposes. The goodwill recognized from our acquisition of Reata is primarily the result of the deferred tax consequences from the transaction recorded for financial statement purposes.

Acquisition-related expenses: Acquisition-related expense, primarily comprised of regulatory, advisory and legal fees, and other transaction costs, totaled approximately $28.4 million and were recorded within selling, general and administrative expense within our condensed consolidated statements of income for the year ended December 31, 2023.

Assumptions in the Allocations of Purchase Price

The results of operations of Reata, along with the estimated fair values of the assets acquired and liabilities assumed in the Reata acquisition, have been included in our condensed consolidated financial statements since the closing of the Reata acquisition on September 26, 2023.

Our preliminary estimate of the fair value of the specifically identifiable assets acquired and liabilities assumed as of the date of acquisition is subject to the finalization of management's analysis related to certain matters, such as finalizing our assessment of income taxes. The final determination of these fair values will be completed as additional information becomes available but no later than one year from the acquisition date. The final determination may result in asset and liability fair values that are different than the preliminary estimates.

Note 3: | Dispositions | ||||

Sale of Joint Venture Equity Interest in Samsung Bioepis

In April 2022 we completed the sale of our 49.9 % equity interest in Samsung Bioepis to Samsung BioLogics in exchange for total consideration of approximately $2.3 billion. Under the terms of this transaction, we received approximately $1.0 billion in cash at closing, with approximately $1.3 billion in cash to be deferred over two payments. The first deferred payment of $812.5 million was received in April 2023 and the second deferred payment of $437.5 million was received in April 2024.

We elected the fair value option and measured the payments due to us from Samsung BioLogics at fair value. As of March 31, 2024, the estimated fair value of the second deferred payment using a risk-adjusted discount rate of 6.0 % was approximately $436.1 million. This payment has been classified as a Level 3 measurement and is reflected in other current assets within our condensed consolidated balance sheets as of March 31, 2024.

For the three months ended March 31, 2024, we recognized a gain of approximately $6.1 million to reflect the change in fair value related to the second deferred payment due to us. For the three months ended March 31, 2023, we recognized gains of approximately $11.1 million and $6.2 million to reflect the changes in fair value related to

16

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

the first and second deferred payments due to us, respectively. These changes were recorded in other (income) expense, net in our condensed consolidated statements of income.

For additional information on the sale of our equity interest in Samsung Bioepis, please read Note 3, Dispositions, to our consolidated financial statements included in our 2023 Form 10-K.

Note 4: | Restructuring | ||||

2023 Fit for Growth Restructuring Program

In July 2023 we initiated additional cost saving measures as part of our Fit for Growth program to reduce operating costs, while improving operating efficiency and effectiveness. The Fit for Growth program is expected to generate approximately $1.0 billion in gross operating expense savings by the end of 2025, some of which will be reinvested in various initiatives. The Fit for Growth program is currently estimated to include net headcount reductions of approximately 1,000 employees and we expect to incur restructuring charges ranging from approximately $260.0 million to $280.0 million.

Total charges incurred from our 2023 cost saving initiatives are summarized as follows:

| For the Three Months Ended March 31, | |||||||||||||||||||||||

| 2024 | |||||||||||||||||||||||

| (In millions) | Severance Costs | Accelerated Depreciation and Other Costs | Total | ||||||||||||||||||||

| Selling, general and administrative | $ | $ | $ | ||||||||||||||||||||

| Research and development | |||||||||||||||||||||||

| Restructuring charges | |||||||||||||||||||||||

| Total charges | $ | $ | $ | ||||||||||||||||||||

Other Costs: includes costs associated with items such as asset abandonment and write-offs, facility closure costs, pretax gains and losses resulting from the termination of certain leases, employee non-severance expense, consulting fees and other costs.

Reata Integration

Following the close of our Reata acquisition in September 2023, we implemented an integration plan designed to realize operating synergies through cost savings and avoidance. Under this initiative, we estimate we will incur total integration charges ranging from approximately $35.0 million to $40.0 million, related to severance and employment costs, which are expected to be paid by the end of 2024. These amounts were substantially incurred during 2023.

Total charges incurred from our Reata integration are summarized as follows:

| For the Three Months Ended March 31, | |||||||||||||||||||||||

| 2024 | |||||||||||||||||||||||

| (In millions) | Severance Costs | Accelerated Depreciation and Other Costs | Total | ||||||||||||||||||||

| Selling, general and administrative | $ | $ | $ | ||||||||||||||||||||

| Research and development | |||||||||||||||||||||||

| Restructuring charges | |||||||||||||||||||||||

| Total charges | $ | $ | $ | ||||||||||||||||||||

In connection with our acquisition of Reata we assumed responsibility for a single-tenant, build-to-suit building of approximately 327,400 square feet of office and laboratory space located in Plano, Texas, with an initial lease term of 16 years. We do not intend to occupy this building and are evaluating opportunities to sublease the property.

Charges and spending related to workforce reductions from our 2023 Fit for Growth program and Reata Integration are summarized as follows:

17

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

| For the Three Months Ended March 31, | ||||||||||||||

| (In millions) | 2024 | 2023 | ||||||||||||

| Restructuring reserve as of December 31 | $ | $ | ||||||||||||

| Expense | ||||||||||||||

| Payment | ( | ( | ||||||||||||

| Foreign currency and other adjustments | ||||||||||||||

| Restructuring reserve as of March 31 | $ | $ | ||||||||||||

18

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

Note 5: | Revenue | ||||

Product Revenue

Revenue by product is summarized as follows:

| For the Three Months Ended March 31, | ||||||||||||||||||||||||||||||||||||||

| 2024 | 2023 | |||||||||||||||||||||||||||||||||||||

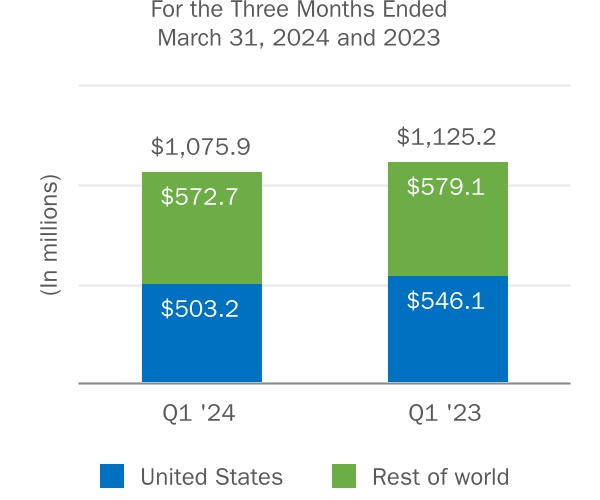

| (In millions) | United States | Rest of World | Total | United States | Rest of World | Total | ||||||||||||||||||||||||||||||||

| Multiple Sclerosis: | ||||||||||||||||||||||||||||||||||||||

| TECFIDERA | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| VUMERITY | ||||||||||||||||||||||||||||||||||||||

| Total Fumarate | ||||||||||||||||||||||||||||||||||||||

| AVONEX | ||||||||||||||||||||||||||||||||||||||

| PLEGRIDY | ||||||||||||||||||||||||||||||||||||||

| Total Interferon | ||||||||||||||||||||||||||||||||||||||

| TYSABRI | ||||||||||||||||||||||||||||||||||||||

| FAMPYRA | ||||||||||||||||||||||||||||||||||||||

| Subtotal: Multiple Sclerosis | ||||||||||||||||||||||||||||||||||||||

| Rare Disease: | ||||||||||||||||||||||||||||||||||||||

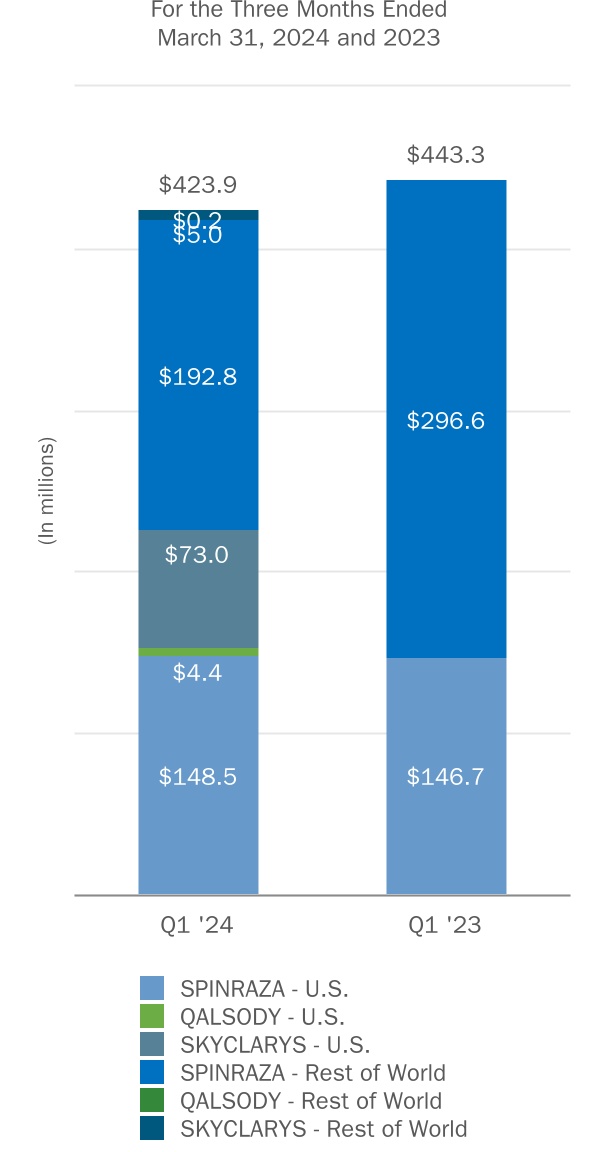

| SPINRAZA | ||||||||||||||||||||||||||||||||||||||

QALSODY(1) | ||||||||||||||||||||||||||||||||||||||

SKYCLARYS(2) | ||||||||||||||||||||||||||||||||||||||

| Subtotal: Rare Disease | ||||||||||||||||||||||||||||||||||||||

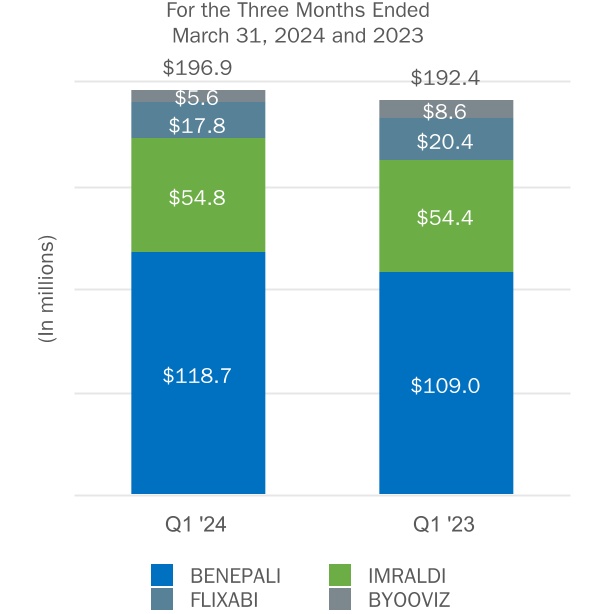

| Biosimilars: | ||||||||||||||||||||||||||||||||||||||

| BENEPALI | ||||||||||||||||||||||||||||||||||||||

| IMRALDI | ||||||||||||||||||||||||||||||||||||||

| FLIXABI | ||||||||||||||||||||||||||||||||||||||

BYOOVIZ(3) | ||||||||||||||||||||||||||||||||||||||

| Subtotal: Biosimilars | ||||||||||||||||||||||||||||||||||||||

Other(4) | ||||||||||||||||||||||||||||||||||||||

| Total product revenue | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

(1) QALSODY became commercially available in the U.S. during the second quarter of 2023.

(2) SKYCLARYS was obtained as part of our acquisition of Reata in September 2023. SKYCLARYS became commercially available in the U.S. during the second quarter of 2023 and we began recognizing revenue from SKYCLARYS in the U.S. during the fourth quarter of 2023, subsequent to our acquisition. SKYCLARYS was approved and became commercially available in the E.U. during the first quarter of 2024.

(3) BYOOVIZ became commercially available in certain international markets in 2023.

(4) Other includes FUMADERM, ADUHELM and ZURZUVAE, which became commercially available in the U.S. during the fourth quarter of 2023.

We recognized revenue from two 25.6 % and 11.7 % of gross product revenue for the three months ended March 31, 2024, and 27.3 % and 7.4 % of gross product revenue for the three months ended March 31, 2023.

19

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

An analysis of the change in reserves for discounts and allowances is summarized as follows:

| (In millions) | Discounts | Contractual Adjustments | Returns | Total | ||||||||||||||||||||||

| Balance, December 31, 2023 | $ | $ | $ | $ | ||||||||||||||||||||||

| Current provisions relating to sales in current year | ||||||||||||||||||||||||||

| Adjustments relating to prior years | ( | ( | ||||||||||||||||||||||||

| Payments/credits relating to sales in current year | ( | ( | ( | ( | ||||||||||||||||||||||

| Payments/credits relating to sales in prior years | ( | ( | ( | ( | ||||||||||||||||||||||

| Balance, March 31, 2024 | $ | $ | $ | $ | ||||||||||||||||||||||

The total reserves above, which are included in our condensed consolidated balance sheets, are summarized as follows:

| (In millions) | As of March 31, 2024 | As of December 31, 2023 | ||||||||||||

| Reduction of accounts receivable | $ | $ | ||||||||||||

| Component of accrued expense and other | ||||||||||||||

| Total revenue-related reserves | $ | $ | ||||||||||||

Revenue from Anti-CD20 Therapeutic Programs

Revenue from anti-CD20 therapeutic programs is summarized in the table below. For the purposes of this footnote, we refer to RITUXAN and RITUXAN HYCELA collectively as RITUXAN.

| For the Three Months Ended March 31, | ||||||||||||||

| (In millions) | 2024 | 2023 | ||||||||||||

| Royalty revenue on sales of OCREVUS | $ | $ | ||||||||||||

| Biogen’s share of pre-tax profits in the U.S. for RITUXAN, GAZYVA and LUNSUMIO | ||||||||||||||

| Other revenue from anti-CD20 therapeutic programs | ||||||||||||||

| Total revenue from anti-CD20 therapeutic programs | $ | $ | ||||||||||||

For additional information on our collaboration arrangements with Genentech, please read Note 19, Collaborative and Other Relationships, to our consolidated financial statements included in this report.

Contract Manufacturing, Royalty and Other Revenue

Contract manufacturing, royalty and other revenue is summarized in the table below.

| For the Three Months Ended March 31, | ||||||||||||||

| (In millions) | 2024 | 2023 | ||||||||||||

| Contract manufacturing revenue | $ | $ | ||||||||||||

Royalty and other revenue | ( | |||||||||||||

| Total contract manufacturing, royalty and other revenue | $ | $ | ||||||||||||

Contract Manufacturing Revenue

Contract manufacturing revenue primarily reflects amounts earned under contract manufacturing agreements with our strategic customers. During the first quarter of 2023 we began recognizing contract manufacturing revenue for LEQEMBI, upon accelerated approval of LEQEMBI in the U.S. Prior to accelerated approval, our share of contract manufacturing amounts related to LEQEMBI were recognized in research and development expense within our condensed consolidated statements of income.

Royalty and Other Revenue

Royalty and other revenue primarily reflects the royalties we receive from net sales on products related to patents that we have out-licensed, as well as royalty revenue on biosimilar products from our license arrangements with

20

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

Samsung Bioepis and our 50.0 % share of LEQEMBI product revenue, net and cost of sales, including royalties, as we are not the principal.

For additional information on our collaboration arrangements with Eisai and our license arrangements with Samsung Bioepis, please read Note 19, Collaborative and Other Relationships, to these condensed consolidated financial statements.

Note 6: | Inventory | ||||

The components of inventory are summarized as follows:

| (In millions) | As of March 31, 2024 | As of December 31, 2023 | ||||||||||||

| Raw materials | $ | $ | ||||||||||||

| Work in process | ||||||||||||||

| Finished goods | ||||||||||||||

| Total inventory | $ | $ | ||||||||||||

| Balance Sheet Classification: | ||||||||||||||

| Inventory | $ | $ | ||||||||||||

| Investments and other assets | ||||||||||||||

| Total inventory | $ | $ | ||||||||||||

Note 7: | Intangible Assets and Goodwill | ||||

Intangible Assets

Intangible assets, net of accumulated amortization, impairment charges and adjustments are summarized as follows:

| As of March 31, 2024 | As of December 31, 2023 | |||||||||||||||||||||||||||||||||||||||||||

| (In millions) | Estimated Life | Cost | Accumulated Amortization | Net | Cost | Accumulated Amortization | Net | |||||||||||||||||||||||||||||||||||||

| Completed technology: | ||||||||||||||||||||||||||||||||||||||||||||

| Acquired and in-licensed rights and patents | $ | $ | ( | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||

| Developed technology and other | ( | ( | ||||||||||||||||||||||||||||||||||||||||||

| Total completed technology | ( | ( | ||||||||||||||||||||||||||||||||||||||||||

| In-process research and development | Indefinite until commercialization | — | — | |||||||||||||||||||||||||||||||||||||||||

| Priority review voucher | Indefinite | — | — | |||||||||||||||||||||||||||||||||||||||||

| Trademarks and trade names | Indefinite | — | — | |||||||||||||||||||||||||||||||||||||||||

| Total intangible assets | $ | $ | ( | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||

Amortization and Impairments

For the three months ended March 31, 2024, amortization and impairment of acquired intangible assets totaled $78.3 million, compared to $50.2 million in the prior year comparative period. The increase was primarily due to

21

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

amortization for the Reata acquisition acquired intangible assets associated with SKYCLARYS. For the three months ended March 31, 2024 and 2023, we had no impairment charges.

Completed Technology

Completed technology primarily relates to our other marketed products and programs acquired through asset acquisitions, licenses and business combinations. Completed technology intangible assets are amortized over their estimated useful lives, which range between 2 to 31 years, with a remaining weighted average useful life of 12 years for acquired and in-licensed rights and patents and 10 years for developed technology and other. In connection with our acquisition of Reata in September 2023 we acquired SKYCLARYS, a commercially-approved product in the U.S., with an estimated fair value of approximately $4.2 billion, which includes measurement period adjustments. During the first quarter of 2024 SKYCLARYS was approved in the E.U. and became commercially available, which resulted in the reclassification of the related intangible asset, with an estimated fair value of approximately $2.3 billion, from IPR&D to completed technology.

IPR&D Related to Business Combinations

IPR&D represents the fair value assigned to research and development assets that we acquired as part of a business combination and had not yet reached technological feasibility at the date of acquisition. Included in IPR&D balances are adjustments related to foreign currency exchange rate fluctuations. The carrying value associated with our IPR&D assets as of December 31, 2023, related to the IPR&D programs we acquired in connection with our acquisition of Reata in September 2023, with an estimated fair value of approximately $2.3 billion, which includes measurement period adjustments. During the first quarter of 2024 SKYCLARYS was approved in the E.U. and became commercially available, which resulted in the reclassification of the related intangible asset from IPR&D to completed technology.

Priority Review Voucher

In connection with our acquisition of Reata in September 2023 we acquired a rare pediatric disease priority review voucher that may be used to obtain priority review by the FDA for a future regulatory submission or sold to a third party. We recorded the priority review voucher based on its estimated fair value of $100.0 million as an intangible asset. The estimated fair value was based on recent external purchase and sale transactions of similar vouchers.

For additional information on our acquisition of Reata, please read Note 2, Acquisitions, to these condensed consolidated financial statements.

Estimated Future Amortization of Intangible Assets

The estimated future amortization of finite-lived intangible assets for the next five years is expected to be as follows:

| (In millions) | As of March 31, 2024 | |||||||

| 2024 (remaining nine months) | $ | |||||||

| 2025 | ||||||||

| 2026 | ||||||||

| 2027 | ||||||||

| 2028 | ||||||||

| 2029 | ||||||||

Goodwill

The following table provides a roll forward of the changes in our goodwill balance:

| (In millions) | As of March 31, 2024 | |||||||

| Goodwill, December 31, 2023 | $ | |||||||

| Goodwill resulting from Reata acquisition | ||||||||

| Other | ( | |||||||

| Goodwill, March 31, 2024 | $ | |||||||

For additional information on our acquisition of Reata, please read Note 2, Acquisitions, to these condensed consolidated financial statements.

22

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

As of March 31, 2024, we had no accumulated impairment losses related to goodwill. Other includes adjustments related to foreign currency exchange rate fluctuations.

Note 8: | Fair Value Measurements | ||||

The tables below present information about our assets and liabilities that are regularly measured and carried at fair value and indicate the level within the fair value hierarchy of the valuation techniques we utilized to determine such fair value:

| Fair Value Measurements on a Recurring Basis | ||||||||||||||||||||||||||

| As of March 31, 2024 | ||||||||||||||||||||||||||

| (In millions) | Total | Quoted Prices in Active Markets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | ||||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||

| Cash equivalents | $ | $ | $ | $ | ||||||||||||||||||||||

| Marketable equity securities | ||||||||||||||||||||||||||

| Other current assets: | ||||||||||||||||||||||||||

Receivable from Samsung BioLogics(1) | ||||||||||||||||||||||||||

| Derivative contracts | ||||||||||||||||||||||||||

| Other non-current assets: | ||||||||||||||||||||||||||

| Plan assets for deferred compensation | ||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

| Liabilities: | ||||||||||||||||||||||||||

| Derivative contracts | $ | $ | $ | $ | ||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

(1) Represents the fair value of the current payment due from Samsung BioLogics as a result of the sale of our 49.9 % equity interest in Samsung Bioepis to Samsung BioLogics during the second quarter of 2022, for which we elected the fair value option. For additional information on the sale of our equity interest in Samsung Bioepis, please read Note 3, Dispositions, to these condensed consolidated financial statements.

During the third quarter of 2023 we sold all of our marketable debt securities and used the proceeds to partially fund our acquisition of Reata. For additional information on our acquisition of Reata, please read Note 2, Acquisitions, to these condensed consolidated financial statements.

23

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

| Fair Value Measurements on a Recurring Basis | ||||||||||||||||||||||||||

| As of December 31, 2023 | ||||||||||||||||||||||||||

| (In millions) | Total | Quoted Prices in Active Markets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | ||||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||

| Cash equivalents | $ | $ | $ | $ | ||||||||||||||||||||||

| Marketable equity securities | ||||||||||||||||||||||||||

| Other current assets: | ||||||||||||||||||||||||||

Receivable from Samsung BioLogics(1) | ||||||||||||||||||||||||||

| Derivative contracts | ||||||||||||||||||||||||||

Other non-current assets: | ||||||||||||||||||||||||||

| Plan assets for deferred compensation | ||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

| Liabilities: | ||||||||||||||||||||||||||

| Derivative contracts | $ | $ | $ | $ | ||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

(1) Represents the fair value of the current payment due from Samsung BioLogics as a result of the sale of our 49.9 % equity interest in Samsung Bioepis to Samsung BioLogics during the second quarter of 2022, for which we elected the fair value option. For additional information on the sale of our equity interest in Samsung Bioepis, please read Note 3, Dispositions, to these condensed consolidated financial statements.

Our marketable equity securities represent investments in publicly traded equity securities. Our ability to liquidate our investments in Denali, Sage and Sangamo may be limited by the size of our interest, the volume of market related activity, our concentrated level of ownership and potential restrictions resulting from our status as a collaborator. Therefore, we may realize significantly less than the current value of such investments.

For additional information on our investments in Denali, Sangamo and Sage common stock, please read Note 19, Collaborative and Other Relationships, to our consolidated financial statements included in our 2023 Form 10-K.

There have been no

For a description of our validation procedures related to prices provided by third-party pricing services and our option pricing valuation model, please read Note 1, Summary of Significant Accounting Policies - Fair Value Measurements, to our consolidated financial statements included in our 2023 Form 10-K.

Level 3 Assets and Liabilities Held at Fair Value

There were no transfers of assets or liabilities into or out of Level 3 as of March 31, 2024 and December 31, 2023.

Financial Instruments Not Carried at Fair Value

Other Financial Instruments

Due to the short-term nature of certain financial instruments, the carrying value reflected in our condensed consolidated balance sheets for current accounts receivable, due from anti-CD20 therapeutic programs, other current assets, accounts payable and accrued expense and other, approximates fair value.

24

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

Debt Instruments

The fair and carrying values of our debt instruments, which are Level 2 liabilities, are summarized as follows:

| As of March 31, 2024 | As of December 31, 2023 | |||||||||||||||||||||||||

| (In millions) | Fair Value | Carrying Value | Fair Value | Carrying Value | ||||||||||||||||||||||

| Current portion: | ||||||||||||||||||||||||||

2023 Term Loan 364-day tranche(1) | $ | $ | $ | $ | ||||||||||||||||||||||

2023 Term Loan three-year tranche(1) | ||||||||||||||||||||||||||

| Current portion of notes payable and term loan | ||||||||||||||||||||||||||

| Non-current portion: | ||||||||||||||||||||||||||

2023 Term Loan three-year tranche(1) | ||||||||||||||||||||||||||

| 4.050% Senior Notes due September 15, 2025 | ||||||||||||||||||||||||||

| 2.250% Senior Notes due May 1, 2030 | ||||||||||||||||||||||||||

| 5.200% Senior Notes due September 15, 2045 | ||||||||||||||||||||||||||

| 3.150% Senior Notes due May 1, 2050 | ||||||||||||||||||||||||||

| 3.250% Senior Notes due February 15, 2051 | ||||||||||||||||||||||||||

| Non-current portion of notes payable and term loan | ||||||||||||||||||||||||||

| Total notes payable and term loan | $ | $ | $ | $ | ||||||||||||||||||||||

(1) In connection with our acquisition of Reata we drew $1.0 billion from our 2023 Term Loan, comprised of a $500.0 million floating rate 364-day tranche and a $500.0 million floating rate three-year tranche. For additional information on our 2023 Term Loan, please read Note 13, Indebtedness, to these condensed consolidated financial statements.

The fair values of each of our series of Senior Notes were determined through market, observable and corroborated sources. The changes in the fair values of our Senior Notes as of March 31, 2024, compared to December 31, 2023, are primarily related to increases in U.S. treasury yields partially offset by a decrease in credit spreads used to value our Senior Notes since December 31, 2023. For additional information related to our Senior Notes, please read Note 13, Indebtedness, to our consolidated financial statements included in our 2023 Form 10-K.

Note 9: | Financial Instruments | ||||

The following table summarizes our financial assets with maturities of less than 90 days from the date of purchase included in cash and cash equivalents in our condensed consolidated balance sheets:

| (In millions) | As of March 31, 2024 | As of December 31, 2023 | ||||||||||||

| Money market funds | $ | $ | ||||||||||||

Total | $ | $ | ||||||||||||

The carrying value of our money market funds approximate fair value due to their short-term maturities.

We partially funded our Reata acquisition through available cash, cash equivalents and marketable securities. As of December 31, 2023, we have sold all of our marketable debt securities. For additional information on our acquisition of Reata, please read Note 2, Acquisitions, to these condensed consolidated financial statements.

25

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

Our marketable equity securities gains (losses) are recorded in other (income) expense, net in our condensed consolidated statements of income. The following tables summarize our marketable equity securities, classified as available-for-sale:

| As of March 31, 2024 | ||||||||||||||||||||||||||

| (In millions) | Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | ||||||||||||||||||||||

| Marketable equity securities | ||||||||||||||||||||||||||

| Marketable equity securities, current | $ | $ | $ | ( | $ | |||||||||||||||||||||

| Marketable equity securities, non-current | ( | |||||||||||||||||||||||||

| Total marketable equity securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

| As of December 31, 2023 | ||||||||||||||||||||||||||

| (In millions) | Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | ||||||||||||||||||||||

| Marketable equity securities | ||||||||||||||||||||||||||

| Marketable equity securities, current | $ | $ | $ | ( | $ | |||||||||||||||||||||

| Marketable equity securities, non-current | ( | |||||||||||||||||||||||||

| Total marketable equity securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

Proceeds from Marketable Debt Securities

The proceeds from maturities and sales of marketable debt securities and resulting realized gains and losses are summarized as follows:

| (In millions) | For the Three Months Ended March 31, 2023 | |||||||

| Proceeds from maturities and sales | $ | |||||||

| Realized gains | ||||||||

| Realized losses | ||||||||

Realized losses for the three months ended March 31, 2023, primarily relate to sales of U.S. treasuries and corporate bonds.

During the third quarter of 2023 we sold all of our marketable debt securities and used the proceeds to partially fund our acquisition of Reata. For additional information on our acquisition of Reata, please read Note 2, Acquisitions, to these condensed consolidated financial statements.

Strategic Investments

Our strategic investment portfolio includes investments in equity securities of certain biotechnology companies, which are reflected within our disclosures included in Note 8, Fair Value Measurements, to these condensed consolidated financial statements, as well as venture capital funds where the underlying investments are in equity securities of certain biotechnology companies and non-marketable equity securities.

As of March 31, 2024 and December 31, 2023, our strategic investment portfolio was comprised of investments totaling $382.0 million and $460.7 million, respectively, which are included in other current assets and investments and other assets within our condensed consolidated balance sheets.

The decrease in our strategic investment portfolio as of March 31, 2024, was primarily due to the decrease in the fair value of our investments in Sage and Denali common stock. Additionally, during the first quarter of 2024 we sold a portion of our Denali and Sangamo common stock.

For additional information on our strategic investments in Denali, Sangamo and Sage common stock, please read Note 19, Collaborative and Other Relationships, to our consolidated financial statements included in our 2023 Form 10-K.

26

BIOGEN INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited, continued)

Note 10: | Derivative Instruments | ||||

Foreign Currency Forward Contracts - Hedging Instruments

Due to the global nature of our operations, portions of our revenue and operating expense are recorded in currencies other than the U.S. dollar. The value of revenue and operating expense measured in U.S. dollars is therefore subject to changes in foreign currency exchange rates. We enter into foreign currency forward contracts and foreign currency options with financial institutions with the primary objective to mitigate the impact of foreign currency exchange rate fluctuations on our international revenue and operating expense.

Foreign currency forward contracts and foreign currency options in effect as of March 31, 2024 and December 31, 2023, had durations of 1 to 9 months and 1 to 12 months, respectively. These contracts have been designated as cash flow hedges and unrealized gains and losses on the portion of these foreign currency forward contracts and foreign currency options that are included in the effectiveness test are reported in AOCI. Realized gains and losses of such contracts and options are recognized in revenue when the sale of product in the currency being hedged is recognized and in operating expense when the expense in the currency being hedged is recorded. We recognize all cash flow hedge reclassifications from AOCI and fair value changes of excluded portions in the same line item in our condensed consolidated statements of income that have been impacted by the hedged item.

The notional amount of foreign currency forward contracts and foreign currency options that were entered into to hedge forecasted revenue and operating expense is summarized as follows:

| Notional Amount | ||||||||||||||

| (In millions) | As of March 31, 2024 | As of December 31, 2023 | ||||||||||||

| Euro | $ | $ | ||||||||||||