UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2023

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

Commission file number: 0-19311

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(617 ) 679-2000

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | |||||||||||||||

| The | |||||||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| x | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No x

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant (without admitting that any person whose shares are not included in such calculation is an affiliate) computed by reference to the price at which the common stock was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter was $41,190,868,800 .

As of February 12, 2024, the registrant had 145,360,798 shares of common stock, $0.0005 par value, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for our 2024 Annual Meeting of Stockholders are incorporated by reference into Part III of this report.

BIOGEN INC.

ANNUAL REPORT ON FORM 10-K

For the Year Ended December 31, 2023

TABLE OF CONTENTS

| Page | ||||||||

F- 1 | ||||||||

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements that are being made pursuant to the provisions of the Private Securities Litigation Reform Act of 1995 (the Act) with the intention of obtaining the benefits of the “Safe Harbor” provisions of the Act. These forward-looking statements may be accompanied by such words as “aim,” “anticipate,” “believe,” “could,” "contemplate," "continue," “estimate,” “expect,” “forecast,” "goal," “intend,” “may,” “plan,” “potential,” “possible,” "predict," "project", "should," "target," “will,” “would” or the negative of these words or other words and terms of similar meaning. Reference is made in particular to forward-looking statements regarding:

•the anticipated amount, timing and accounting of revenue; contingent, milestone, royalty and other payments under licensing, collaboration, acquisition or divestiture agreements; tax positions and contingencies; collectability of receivables; pre-approval inventory; cost of sales; research and development costs; compensation and other selling, general and administrative expense; amortization of intangible assets; foreign currency exchange risk; estimated fair value of assets and liabilities; and impairment assessments;

•expectations, plans and prospects relating to product approvals, sales, pricing, growth, reimbursement and launch of our marketed and pipeline products;

•the potential impact of increased product competition in the markets in which we compete, including increased competition from new originator therapies, generics, prodrugs and biosimilars of existing products and products approved under abbreviated regulatory pathways, including generic or biosimilar versions of our products or competing products;

•patent terms, patent term extensions, patent office actions and expected availability and periods of regulatory exclusivity;

•our plans and investments in our portfolio as well as implementation of our corporate strategy;

•the execution of our strategic and growth initiatives, including the ultimate success of our acquisition of Reata and our ability to realize the anticipated benefits from the acquisition, including future performance of the SKYCLARYS product and anticipated synergies, as well as the exploration of strategic options for our biosimilars business;

•the drivers for growing our business, including our plans and intention to commit resources relating to discovery, research and development programs and business development opportunities as well as the potential benefits and results of, and the anticipated completion of, certain business development transactions and cost-reduction measures, including our Fit for Growth program;

•the expectations, development plans and anticipated timelines, including costs and timing of potential clinical trials, regulatory filings and approvals, of our products, drug candidates and pipeline programs, including collaborations with third-parties, as well as the potential therapeutic scope of the development and commercialization of our and our collaborators’ pipeline products;

•the timing, outcome and impact of administrative, regulatory, legal and other proceedings related to our patents and other proprietary and intellectual property rights, tax audits, assessments and settlements, pricing matters, sales and promotional practices, product liability, investigations and other matters;

•our ability to finance our operations and business initiatives and obtain funding for such activities;

•adverse safety events involving our marketed or pipeline products, generic or biosimilar versions of our marketed products or any other products from the same class as one of our products;

•the current and potential impacts of geopolitical tensions, acts of war and other large-scale crises, including impacts to our operations, sales and the possible disruptions or delay in our plans to conduct clinical trial activities in areas of geopolitical tension, including regions affected by Russia's invasion of Ukraine and the military conflict in the Middle East;

•the direct and indirect impact of global health outbreaks on our business and operations, including sales, expense, reserves and allowances, the supply chain, manufacturing, research and development costs, clinical trials and employees;

•our use of information systems and data and the potential impacts of any breakdowns, invasions, corruptions, destructions and/or breaches of such systems or those of our business partners;

•the potential impact of healthcare reform in the U.S., including the IRA, and measures being taken worldwide designed to reduce healthcare costs and limit the overall level of government expenditures, including the impact of pricing actions and reduced reimbursement for our products;

•our manufacturing capacity, use of third-party contract manufacturing organizations, plans and timing relating to changes in our manufacturing capabilities, activities in new or existing manufacturing facilities and the expected timeline for the gene therapy manufacturing facility in RTP, North Carolina to be operational;

•the impact of the continued uncertainty of the credit and economic conditions in certain countries and our collection of accounts receivable in such countries;

•lease commitments, purchase obligations and the timing and satisfaction of other contractual obligations; and

•the impact of new laws (including tax), regulatory requirements, judicial decisions and accounting standards.

These forward-looking statements involve risks and uncertainties, including those that are described in Item 1A. Risk Factors included in this report and elsewhere in this report, that could cause actual results to differ materially from those reflected in such statements. Because some of these risks and uncertainties cannot be predicted or quantified and some are beyond our control, you should not rely on our forward-looking statements as predictions of future events and you should not place undue reliance on these statements. Moreover, we operate in a very competitive and rapidly changing environment, new risks and uncertainties may emerge from time to time and it is not possible for us to predict all risks nor identify all uncertainties. Forward-looking statements speak only as of the date of this report and are based on information and estimates available to us at this time. Except as required by law, we do not undertake any obligation to publicly update any forward-looking statements, whether as a result of new information, future developments or otherwise. You should read this report with the understanding that our actual future results, performance, events and circumstances might be materially different from what we expect.

NOTE REGARDING COMPANY AND PRODUCT REFERENCES

References in this report to:

•“Biogen,” the “company,” “we,” “us” and “our” refer to Biogen Inc. and its consolidated subsidiaries; and

•“RITUXAN” refers to both RITUXAN (the trade name for rituximab in the U.S., Canada and Japan) and MabThera (the trade name for rituximab outside the U.S., Canada and Japan).

NOTE REGARDING TRADEMARKS

ADUHELM®, AVONEX®, BYOOVIZ®, PLEGRIDY®, QALSODY®, RITUXAN®, RITUXAN HYCELA®, SKYCLARYS®, SPINRAZA®, TECFIDERA®, TYSABRI® and VUMERITY® are registered trademarks of Biogen.

BENEPALI™, FLIXABI™, FUMADERM™, IMRALDI™ and TOFIDENCE™ are trademarks of Biogen.

ACTEMRA®, COLUMVI®, ENBREL®, EYLEA®, FAMPYRA™, GAZYVA®, LEQEMBI®, HUMIRA®, LUCENTIS®, LUNSUMIO®, OCREVUS®, REMICADE®, ZURZUVAE™ and other trademarks referenced in this report are the property of their respective owners.

DEFINED TERMS

| 2022 Form 10-K | Annual Report on Form 10-K for the year ended December 31, 2022 | ||||

| 2020 Share Repurchase Program | Board of Directors authorized program to repurchase up to $5.0 billion of our common stock | ||||

| 125 Broadway | 125 Broadway, Cambridge, MA | ||||

| 300 Binney Street | 300 Binney Street, Cambridge, MA | ||||

| AAIC | Alzheimer's Association International Conference | ||||

AbbVie | AbbVie Inc. | ||||

| Acorda | Acorda Therapeutics, Inc. | ||||

| AI | Artificial Intelligence | ||||

| Alkermes | Alkermes plc | ||||

| ALS | Amyotrophic Lateral Sclerosis | ||||

AMP | Average Manufacturer Price | ||||

| AOCI | Accumulated Other Comprehensive Income (Loss) | ||||

ASO | Antisense Oligonucleotide | ||||

| ASU | Accounting Standards Update | ||||

| ATV | Antibody Transport Vehicle | ||||

| BLA | Biologics License Application | ||||

| Blackstone | Blackstone Life Sciences | ||||

CCDAA | Climate Corporate Data Accountability Act | ||||

| CCPA | California Consumer Privacy Act | ||||

| CEO | Chief Executive Officer | ||||

| CHMP | Committee for Medicinal Products for Human Use | ||||

| CISO | Chief Information Security Officer | ||||

| CJEU | Court of Justice of the European Union | ||||

| CLE | Cutaneous Lupus Erythematosus | ||||

| CLL | Chronic Lymphocytic Leukemia | ||||

| CMS | Centers for Medicare & Medicaid Services | ||||

CODM | Chief Operating Decision Maker | ||||

| Convergence | Convergence Pharmaceuticals Ltd. | ||||

CRFRA | Climate-Related Financial Risk Act | ||||

| CRL | Complete Response Letter | ||||

| CROs | Contract Research Organizations | ||||

| CTAD | Clinical Trials on Alzheimer's Disease | ||||

DEA | Drug Enforcement Agency | ||||

| DE&I | Diversity, Equity and Inclusion | ||||

| Denali | Denali Therapeutics Inc. | ||||

DOJ | U.S. Department of Justice | ||||

| DPN | Diabetic Painful Neuropathy | ||||

| EC | European Commission | ||||

| Eisai | Eisai Co., Ltd. | ||||

| EMA | European Medicines Agency | ||||

| EPO | European Patent Office | ||||

| ERISA | Employee Retirement Income Security Act of 1974 | ||||

| ERM | Enterprise Risk Management | ||||

DEFINED TERMS (continued)

| ERN | Employee Resource Network | ||||

| ESG | Environmental, Social and Governance | ||||

| E.U. | European Union | ||||

| FA | Friedreich's Ataxia | ||||

| FASB | Financial Accounting Standards Board | ||||

| FCPA | Foreign Corrupt Practices Act | ||||

| FDA | U.S. Food and Drug Administration | ||||

| FDIC | Federal Deposit Insurance Corporation | ||||

| Fit for Growth | Cost saving program initiated in 2023 | ||||

FSS | Federal Supply Schedule | ||||

| GCP | Good Clinical Practices | ||||

GDPR | General Data Privacy Regulation | ||||

| Genentech | Genentech, Inc. | ||||

| GILTI | Global Intangible Low Tax Income | ||||

| GloBE | Global Anti-Base Erosion | ||||

| GMP | Good Manufacturing Practices | ||||

| Humana | Humana Inc. | ||||

| IPR&D | In-process Research and Development | ||||

| Ionis | Ionis Pharmaceuticals Inc. | ||||

| IRA | Inflation Reduction Act of 2022 | ||||

| IT | Information Technology | ||||

| LHI | Large Hemispheric Infarction | ||||

| LRRK2 | Leucine-Rich Repeat Kinase 2 | ||||

| MAA | Marketing Authorization Application | ||||

| MDD | Major Depressive Disorder | ||||

| MHRA | Medicines and Healthcare products Regulatory Agency | ||||

| MS | Multiple Sclerosis | ||||

| Mylan Ireland | Mylan Ireland Ltd. | ||||

| NCD | National Coverage Decision | ||||

| NDA | New Drug Application | ||||

| NDS | New Drug Submission | ||||

| Neurimmune | Neurimmune SubOne AG | ||||

NIST | National Institute of Standards and Technology | ||||

| NMPA | National Medicinal Products Administration | ||||

| OECD | Organization for Economic Co-operation and Development | ||||

| OIE | Other (Income) Expense, Net | ||||

| PDUFA | Prescription Drug User Fee Act | ||||

| PFAS | Per- and Polyfluoroalkyl Substances | ||||

PHS | Public Health Service | ||||

| PMDA | Pharmaceuticals and Medical Devices Agency | ||||

| Polpharma | Polpharma Biologics S.A. | ||||

| PPACA | Patient Protection and Affordable Care Act | ||||

| PPD | Postpartum Depression | ||||

| PPMS | Primary Progressive MS | ||||

DEFINED TERMS (continued)

| R&D | Research and Development | ||||

| Reata | Reata Pharmaceuticals, Inc. | ||||

| REMS | Risk Evaluation and Mitigation Strategies | ||||

| RMS | Relapsing MS | ||||

| RRMS | Relapsing-Remitting MS | ||||

| RTP | Research Triangle Park | ||||

| SAG | Scientific Advisory Group | ||||

| Sage | Sage Therapeutics, Inc. | ||||

| Samsung Bioepis | Samsung Bioepis Co., Ltd. | ||||

| Samsung BioLogics | Samsung BioLogics Co., Ltd. | ||||

| Sangamo | Sangamo Therapeutics, Inc. | ||||

SEC | U.S. Securities and Exchange Commission | ||||

| SG&A | Selling, General and Administrative | ||||

| SLE | Systemic Lupus Erythematosus | ||||

| SMA | Spinal Muscular Atrophy | ||||

| SMN | Survival Motor Neuron | ||||

| SOD1 | Superoxide Dismutase 1 | ||||

SPC | Supplementary Protection Certificate | ||||

| SSP | Supplemental Savings Plan | ||||

| SWISSMEDIC | Swiss Agency for Therapeutic Products | ||||

| TBA | Technical Boards of Appeal | ||||

| TGN | Trigeminal Neuralgia | ||||

| TNF | Anti-tumor Necrosis Factor | ||||

| Transition Toll Tax | A one-time mandatory deemed repatriation tax on accumulated foreign subsidiaries' previously untaxed foreign earnings | ||||

| U.K. | United Kingdom | ||||

| U.S. | United States | ||||

| U.S. GAAP | Accounting Principles Generally Accepted in the U.S. | ||||

VA | Veterans Administration | ||||

PART I

ITEM 1. BUSINESS

OVERVIEW

Biogen is a global biopharmaceutical company focused on discovering, developing and delivering innovative therapies for people living with serious and complex diseases worldwide. We have a broad portfolio of medicines to treat MS, have introduced the first approved treatment for SMA, co-developed treatments to address a defining pathology of Alzheimer’s disease and launched the first approved treatment to target a genetic cause of ALS. Through our 2023 acquisition of Reata we market the first and only drug approved in the U.S. and the E.U. for the treatment of Friedreich's Ataxia in adults and adolescents aged 16 years and older. We are focused on advancing our pipeline in neurology, specialized immunology and rare diseases. We support our drug discovery and development efforts through internal research and development programs and external collaborations.

Our marketed products include TECFIDERA, VUMERITY, AVONEX, PLEGRIDY, TYSABRI and FAMPYRA for the treatment of MS; SPINRAZA for the treatment of SMA; SKYCLARYS for the treatment of Friedreich's Ataxia; QALSODY for the treatment of ALS; and FUMADERM for the treatment of severe plaque psoriasis.

We also have collaborations with Eisai on the commercialization of LEQEMBI for the treatment of Alzheimer's disease and Sage on the commercialization of ZURZUVAE for the treatment of PPD and we have certain business and financial rights with respect to RITUXAN for the treatment of non-Hodgkin's lymphoma, CLL and other conditions; RITUXAN HYCELA for the treatment of non-Hodgkin's lymphoma and CLL; GAZYVA for the treatment of CLL and follicular lymphoma; OCREVUS for the treatment of PPMS and RMS; LUNSUMIO for the treatment of relapsed or refractory follicular lymphoma; COLUMVI, a bispecific antibody for the treatment of non-Hodgkin's lymphoma; and have the option to add other potential anti-CD20 therapies, pursuant to our collaboration arrangements with Genentech, a wholly-owned member of the Roche Group.

We commercialize a portfolio of biosimilars of advanced biologics including BENEPALI, an etanercept biosimilar referencing ENBREL, IMRALDI, an adalimumab biosimilar referencing HUMIRA, and FLIXABI, an infliximab biosimilar referencing REMICADE, in certain countries in Europe, as well as BYOOVIZ, a ranibizumab biosimilar referencing LUCENTIS, in the U.S. and certain international markets. We also have exclusive rights to commercialize TOFIDENCE, a tocilizumab biosimilar referencing ACTEMRA. We continue to develop potential biosimilar product SB15, a proposed aflibercept biosimilar referencing EYLEA. In February 2023 we announced that we are exploring strategic options for our biosimilars business.

KEY BUSINESS DEVELOPMENTS

The following is a summary of key developments affecting our business since the beginning of 2023.

For additional information on our collaborative and other relationships discussed below, please read Note 19, Collaborative and Other Relationships, to our consolidated financial statements included in this report.

DEVELOPMENTS IN KEY COLLABORATIVE RELATIONSHIPS

LEQEMBI (lecanemab)

United States

In July 2023 the FDA granted traditional approval of LEQEMBI, an anti-amyloid antibody for the treatment of Alzheimer's disease, which was previously granted accelerated approval by the FDA in January 2023. Following the FDA's traditional approval of LEQEMBI, CMS confirmed broader coverage of LEQEMBI.

Additionally, in March 2023 Eisai announced that the U.S. Veteran's Health Administration will be providing coverage of LEQEMBI to veterans living with early stages of Alzheimer's disease.

Rest of World

Key developments related to LEQEMBI (lecanemab) in rest of world markets during 2023 consisted of the following:

•In January 2024 we and Eisai announced that the SAG will convene at the request of the CHMP to discuss the MAA of lecanemab that is currently under review by the EMA. The meeting of the SAG is expected to take place during the first quarter of 2024 and the EC decision for the MAA of lecanemab is expected during the first half of 2024.

•In January 2024 the NMPA approved LEQEMBI in China, with an expected launch date in 2024.

1

•In December 2023 we and Eisai announced that LEQEMBI intravenous infusion was launched in Japan.

•In September 2023 the Japanese Ministry of Health, Labor and Welfare approved LEQEMBI in Japan.

•In January 2023 the EMA accepted for review the MAA for lecanemab.

•In February 2023 the BLA for lecanemab was granted Priority Review by the NMPA of China.

•In May 2023 we and Eisai announced the submission of a MAA for lecanemab to the U.K. MHRA in Great Britain, which has been designated by the MHRA for the Innovative Licensing and Access Pathway. Additionally, in May 2023 Health Canada accepted for review the NDS for lecanemab.

•In June 2023 we and Eisai announced the submission of a MAA for lecanemab to the Ministry of Food and Drug Safety in South Korea.

ZURZUVAE (zuranolone)

In August 2023 the FDA approved ZURZUVAE for adults with PPD, pending DEA scheduling, which was completed in October 2023. Upon approval, ZURZUVAE for PPD became the first and only oral, once-daily, 14-day treatment that can provide rapid improvements in depressive symptoms by day 15 for women with PPD. ZURZUVAE for PPD became commercially available in the U.S. during the fourth quarter of 2023. Additionally, the FDA issued a CRL for the NDA for zuranolone in the treatment of adults with MDD. The CRL stated that the application did not provide substantial evidence of effectiveness to support the approval of zuranolone for the treatment of MDD and that an additional study or studies would be needed. We and Sage are continuing to seek feedback from the FDA and evaluating next steps.

For additional information on our collaboration arrangement with Sage, please read Note 19, Collaborative and Other Relationships, to our consolidated financial statements included in this report.

BUSINESS COMBINATIONS

REATA ACQUISITION

On September 26, 2023, we completed the acquisition of all of the issued and outstanding shares of Reata, a biopharmaceutical company focused on developing therapeutics that regulate cellular metabolism and inflammation in serious neurologic diseases. As a result of this transaction we acquired SKYCLARYS (omaveloxolone), the first and only drug approved in the U.S. and the E.U. for the treatment of Friedreich's Ataxia in adults and adolescents aged 16 years and older, as well as other clinical and preclinical pipeline programs.

Under the terms of this acquisition, we paid Reata shareholders $172.50 in cash for each issued and outstanding Reata share, which totaled approximately $6.6 billion. In addition, we agreed to pay approximately $983.9 million in cash for Reata's outstanding equity awards, inclusive of employer taxes, of which approximately $590.5 million was attributable to pre-acquisition services and is therefore reflected as a component of total purchase price paid. Of the $983.9 million paid to Reata's equity award holders, we recognized approximately $393.4 million as compensation attributable to the post-acquisition service period, of which $196.4 million was recognized as a charge to selling, general and administrative expense with the remaining $197.0 million as a charge to research and development expense within our consolidated statements of income for the year ended December 31, 2023. These amounts were associated with the accelerated vesting of stock options and RSUs previously granted to Reata employees that required no future services to vest.

For additional information on our acquisition of Reata, please read Note 2, Acquisitions, to our consolidated financial statements included in this report.

OTHER KEY DEVELOPMENTS

QALSODY (tofersen)

In April 2023 the FDA approved QALSODY for the treatment of ALS in adults who have a mutation in the SOD1 gene. This indication is approved under accelerated approval based on reduction in plasma neurofilament light chain observed in patients treated with QALSODY. Continued approval for this indication may be contingent upon verification of clinical benefit in confirmatory trial(s).

TECFIDERA

Following a favorable March 2023 decision of the CJEU affirming TECFIDERA's right to regulatory data and marketing protection and the EC determination in May 2023 that TECFIDERA is entitled to an additional year of market

2

protection for its pediatric indication, we believe that TECFIDERA is entitled to regulatory marketing protection in the E.U. until at least February 2, 2025, and are seeking to enforce this protection. In December 2023, the EC revoked all centralized marketing authorizations for generic versions of TECFIDERA. As of December 31, 2023, some of the TECFIDERA generics have not yet fully exited some E.U. markets and we expect removal of all generics from the market will take additional time. We are closely monitoring this situation and working to enforce our legal right to market protection. In addition, we will continue to enforce our EP 2 653 873 patent related to TECFIDERA, which expires in 2028.

CORPORATE MATTERS

FIT FOR GROWTH

In 2023 we initiated additional cost saving measures as part of our Fit for Growth program to reduce operating costs, while improving operating efficiency and effectiveness. The Fit for Growth program is expected to generate approximately $1.0 billion in gross operating expense savings and $800.0 million in net operating expense savings by 2025, some of which will be reinvested in various initiatives. The Fit for Growth program is currently estimated to include net headcount reductions of approximately 1,000 employees and we expect to incur restructuring charges ranging from approximately $260.0 million to $280.0 million.

For additional information on our Fit for Growth program, please read Note 4, Restructuring, to our consolidated financial statements included in this report.

MANAGEMENT CHANGES

•In September 2023 we announced the appointment of Jane Grogan, Ph.D., as Executive Vice President, Head of Research.

•In April 2023 we announced the appointment of Adam Keeney, as Executive Vice President, Head of Corporate Development.

BOARD OF DIRECTORS UPDATE

•In November 2023 we announced Monish Patolawala will be joining our Board of Directors, effective January 1, 2024.

•In June 2023 Susan Langer joined our Board of Directors.

•In June 2023 Caroline Dorsa succeeded Stelios Papadopoulos as Chair of our Board of Directors.

•In June 2023 Stelios Papadopoulos, Alexander J. Denner, Ph.D., William D. Jones and Richard C. Mulligan, Ph.D., departed from our Board of Directors.

For additional information on our executive officers, please read the subsection entitled "Information about our Executive Officers" included in this report.

PRODUCT AND PIPELINE DEVELOPMENTS

NEUROLOGY

ALZHEIMER'S DISEASE

LEQEMBI (lecanemab)

•In October 2023 Eisai presented new data for LEQEMBI 100 mg/mL injection for intravenous use at the 2023 CTAD conference. The new data suggests that there is continued benefit associated with LEQEMBI treatment as patients continued to show benefits at 24 months of treatment and after the removal of amyloid plaques.

•In September 2023 we and Eisai announced that the LEQEMBI intravenous infusion (200 mg, 500 mg, lecanemab) was approved in Japan as a treatment for slowing progression of mild cognitive impairment and mild dementia due to Alzheimer's disease.

3

•In July 2023 we and Eisai announced the results of a detailed analysis of the Phase 3 CLARITY Alzheimer's disease study of LEQEMBI at the 2023 AAIC conference. The study provided further Phase 3 analysis showing benefits of LEQEMBI on both amyloid-beta and tau, two underlying pathological hallmarks of Alzheimer's disease, as well as new data on subcutaneous formulation showing promising PK/PD data modeling on efficacy and safety, representing a potential new option for administering therapy.

•In March 2023 we and Eisai announced that three additional detailed analyses from the Phase 2b clinical study (Study 201) of lecanemab, evaluating the efficacy and safety of lecanemab for mild cognitive impairment due to Alzheimer's disease and mild Alzheimer's disease, were published in peer-reviewed journals.

BIIB080

•In October 2023 we announced new Phase 1b clinical data from the Phase 1b clinical study of BIIB080, an investigational ASO therapy targeting tau, in mild Alzheimer's disease, showing favorable trends on multiple exploratory endpoints of cognition and activities of daily living in Alzheimer's disease.

•In October 2023 JAMA Neurology published biomarker data from the placebo-controlled period and long-term extension phase of the BIIB080 Phase 1b study of the ASO which targets tau pre-mRNA in early-stage Alzheimer's disease. This publication includes preliminary data in 46 patients which showed that the investigational therapy substantially reduced soluble and aggregated pathologic tau in patients with mild Alzheimer's disease.

•In April 2023 Nature Medicine published a manuscript detailing promising results from Biogen's multiple ascending dose Phase 1b trial, which evaluated the safety, pharmacokinetics and target engagement of Biogen's BIIB080.

•In March 2023 we presented new data from the Phase 1b clinical study of BIIB080 at the 2023 International Conference on Alzheimer's and Parkinson's Diseases, showing that BIIB080 substantially reduced tau protein levels in patients with early-stage Alzheimer's disease.

RARE DISEASE

SPINRAZA (nusinersen)

•In June 2023 we announced new data from the Phase 4 RESPOND study, which is designed to evaluate the clinical outcomes and safety following treatment with SPINRAZA in infants and toddlers with SMA who have unmet clinical needs after treatment with ZOLGENSMA (onasemnogene abeparvovec-xioi). Interim results from the Phase 4 RESPOND study showed improved motor function in most participants treated with SPINRAZA after ZOLGENSMA.

SKYCLARYS (omaveloxolone)

•In February 2024 the EC approved SKYCLARYS in the E.U. for the treatment of FA in adults and adolescents aged 16 years and older. SKYCLARYS is the first treatment approved within the E.U. for this rare, genetic, progressive neurodegenerative disease.

•In December 2023 the CHMP of the EMA issued a positive opinion recommending marketing authorization for omaveloxolone for the treatment of FA in people aged 16 years and older.

QALSODY (tofersen)

•In August 2023 the first Veteran was dosed with QALSODY following the VA's coverage for QALSODY.

•In July 2023 the European Academy of Neurology guideline recommendations on the management of ALS provided updated guidelines recommending that tofersen be offered as first-line treatment for patients with progressive ALS caused by pathogenic mutations in SOD1.

•In June 2023 the first patient with SOD1-ALS, outside of a clinical trial or early access program, was dosed with QALSODY.

•In April 2023 the FDA approved QALSODY for the treatment of ALS in adults who have a mutation in the SOD1 gene.

4

BIOSIMILARS

BYOOVIZ (referencing LUCENTIS)

•In October 2023 BYOOVIZ was granted an interchangeability designation by the FDA and was deemed interchangeable to Genentech's LUCENTIS.

•In March 2023 we announced that BYOOVIZ, a ranibizumab biosimilar referencing LUCENTIS, launched in Canada.

•In February 2023 Samsung Bioepis announced that BYOOVIZ launched in Germany.

TOFIDENCE (referencing ACTEMRA)

•In September 2023 the FDA approved TOFIDENCE, a tocilizumab biosimilar referencing ACTEMRA, for the treatment of severe, active and progressive rheumatoid arthritis.

DISCONTINUED PROGRAMS AND STUDIES

ENVISION STUDY

In November 2023 we notified Neurimmune of our decision to terminate our collaboration and license agreement with Neurimmune, to discontinue the development and commercialization of ADUHELM and to terminate the ENVISION clinical study. In connection with this termination, we recorded close-out costs of approximately $60.0 million in research and development expense within our consolidated statements of income for the year ended December 31, 2023.

EMBARK STUDY

In September 2023 we discontinued our EMBARK study for aducanumab. In connection with this discontinuation we recorded termination costs of approximately $43.0 million in research and development expense within our consolidated statements of income for the year ended December 31, 2023.

ACORDA COLLABORATION

In January 2024 we notified Acorda of our decision to terminate our collaboration and license agreement, effective January 1, 2025. As a result of this termination, Acorda will regain global commercialization rights to FAMPYRA.

BIIB122

In June 2023 we and Denali announced plans to terminate the Phase 3 LIGHTHOUSE study for BIIB122, a small molecule inhibitor of LRRK2 in Parkinson's disease. The protocol for the Phase 2b LUMA study for BIIB122 in patients with early-stage Parkinson’s disease was amended to now include eligible patients with a LRRK2 genetic mutation in addition to continuing to enroll eligible patients with early-stage idiopathic Parkinson’s disease.

BIIB093

In April 2023 we announced that we would terminate the development of BIIB093 (glibenclamide IV), currently in a Phase 3 study for LHI and a Phase 2 study for brain contusion, due to operational challenges and other strategic considerations. In connection with this termination, we recorded close-out costs of approximately $13.2 million in research and development expense within our consolidated statements of income for the year ended December 31, 2023.

BIIB131

In April 2023 we announced that we will be pausing the initiation of a Phase 2b study for BIIB131 (TMS-007) for acute ischemic stroke and will continue to assess whether to initiate this study. We sold the rights to BIIB131 to a third-party biopharmaceutical company in exchange for an upfront with potential milestones and future royalties on global sales.

BIIB132

In April 2023 we announced that we would discontinue further development of BIIB132 in spinocerebellar ataxia type 3, as part of our ongoing research and development prioritization initiative.

5

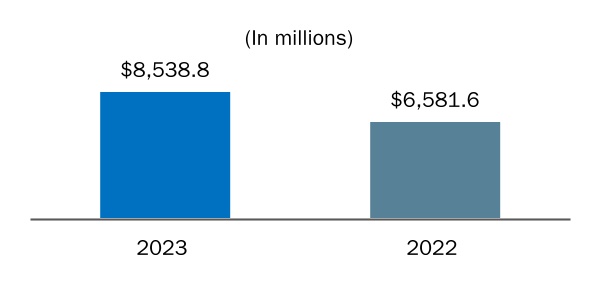

MARKETED PRODUCTS

The following graph shows our product revenue and revenue from anti-CD20 therapeutic programs for the years ended December 31, 2023, 2022 and 2021.

(1) MS includes TECFIDERA, VUMERITY, AVONEX, PLEGRIDY, TYSABRI and FAMPYRA. VUMERITY became commercially available in the E.U. during the fourth quarter of 2021.

(2) Rare disease includes SPINRAZA, QALSODY, which became commercially available in the U.S. during the second quarter of 2023, and SKYCLARYS, which was obtained as part of our acquisition of Reata in September 2023. SKYCLARYS became commercially available in the U.S. during the second quarter of 2023 and we began recognizing revenue from SKYCLARYS in the U.S. during the fourth quarter of 2023, subsequent to our acquisition.

(3) Biosimilars includes BENEPALI, IMRALDI, FLIXABI and BYOOVIZ. BYOOVIZ became commercially available in the U.S. during the third quarter of 2022 and commercially available in certain international markets in 2023.

(4) Anti-CD20 therapeutic programs include RITUXAN, RITUXAN HYCELA, GAZYVA, OCREVUS and LUNSUMIO. LUNSUMIO became commercially available in the U.S. during the first quarter of 2023.

(5) Other includes FUMADERM, ADUHELM and ZURZUVAE, which became commercially available in the U.S. during the fourth quarter of 2023.

6

Product sales for TECFIDERA, TYSABRI and SPINRAZA each accounted for more than 10.0% of our total revenue for the years ended December 31, 2023, 2022 and 2021. For additional financial information about our product and other revenue and geographic areas where we operate, please read Note 5, Revenue and Note 25, Segment Information, to our consolidated financial statements included in this report and Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations included in this report. A discussion of the risks attendant to our operations is set forth in Item 1A. Risk Factors included in this report.

NEUROLOGY

MULTIPLE SCLEROSIS

We develop, manufacture and market a number of products designed to treat patients with MS. MS is a progressive disease in which the body loses the ability to transmit messages along nerve cells, leading to a loss of muscle control, paralysis and, in some cases, death. Patients with active RMS experience an uneven pattern of disease progression characterized by periods of stability that are interrupted by flare-ups of the disease after which the patient may return to a lower baseline of functioning.

The MS products we market and our major markets are as follows:

| Product | Indication | Collaborator | Major Markets | |||||||||||||||||

| RMS in the U.S. RRMS in the E.U. | None | U.S. France Germany Italy Japan Spain U.K. | |||||||||||||||||

| RMS in the U.S. RRMS in the E.U. | Alkermes Pharma Ireland Limited, a subsidiary of Alkermes | U.S. Germany Israel Switzerland U.K. | |||||||||||||||||

| RMS | None | U.S. France Germany Italy Japan Spain | |||||||||||||||||

| RMS in the U.S. RRMS in the E.U. | None | U.S. France Germany Italy Spain U.K. | |||||||||||||||||

| RMS RRMS in the E.U. Crohn's disease in the U.S. | None | U.S. France Germany Italy Spain U.K. | |||||||||||||||||

| Walking ability for patients with MS | Acorda | France Germany | |||||||||||||||||

7

For additional information on our collaboration arrangements with Alkermes and Acorda, please read Note 19, Collaborative and Other Relationships, to our consolidated financial statements included in this report.

ALZHEIMER'S DISEASE

Alzheimer's disease is characterized by two abnormalities in the brain: amyloid plaques and neurofibrillary tangles. Amyloid plaques, which are found in the tissue between the nerve cells, are unusual clumps of a protein called beta amyloid along with degenerating bits of neurons and other cells.

Our Alzheimer's disease products and major markets are as follows:

| Product | Indication | Collaborator | Major Market | |||||||||||||||||

| Alzheimer's disease | Eisai | U.S. Japan | |||||||||||||||||

| Alzheimer's disease | None | U.S. | |||||||||||||||||

In November 2023 we notified Neurimmune of our decision to terminate our collaboration and license agreement with Neurimmune and to discontinue the development and commercialization of ADUHELM.

For additional information on our collaboration arrangements with Eisai, please read Note 19, Collaborative and Other Relationships, to our consolidated financial statements included in this report. For additional information on the discontinuation of ADUHELM, please read Note 20, Investments in Variable Interest Entities, to our consolidated financial statements included in this report.

NEUROPSYCHIATRY

Neuropsychiatry includes ZURZUVAE for PPD, which became commercially available in the U.S. during the fourth quarter of 2023.

Depression is a debilitating illness that is one of the leading contributors to disability worldwide and the second leading cause of disability in the U.S. PPD symptoms are estimated to affect approximately one in eight women who have given birth in the U.S. According to the Centers for Disease Control and Prevention, mental health conditions are the leading cause of maternal mortality with PPD among the most common complications during and after pregnancy.

| Product | Indication | Collaborator | Major Markets | |||||||||||||||||

| PPD in adults | Sage | U.S. | |||||||||||||||||

For additional information on our collaboration with Sage, please read Note 19, Collaborative and Other Relationships, to our consolidated financial statements included in this report.

RARE DISEASE

Rare disease includes SPINRAZA for SMA, SKYCLARYS for FA, which was obtained as part of our acquisition of Reata in September 2023 and QALSODY for ALS, which became commercially available in the U.S. during the second quarter of 2023.

8

SMA is characterized by loss of motor neurons in the spinal cord and lower brain stem, resulting in severe and progressive muscular atrophy and weakness. Ultimately, individuals with the most severe type of SMA can become paralyzed and have difficulty performing the basic functions of life, like breathing and swallowing. Due to a deletion or mutations in the SMN1 gene, people with SMA do not produce enough SMN protein, which is critical to the survival of the neurons that control muscles. The severity of SMA correlates with the amount of SMN protein. People with Type 1 SMA, the most severe life-threatening form, produce very little SMN protein and do not achieve the ability to sit without support, and typically do not live beyond two years of age without respiratory support and nutritional interventions. People with Type 2 and Type 3 SMA produce greater amounts of SMN protein and have less severe, but still life-altering, forms of SMA.

FA is an inherited, debilitating and degenerative neuromuscular disorder that is typically diagnosed during adolescence and can ultimately lead to premature death. Patients with FA experience progressive loss of coordination, muscle weakness and fatigue, which commonly progresses to motor incapacitation, wheelchair reliance and eventually death. Symptoms generally first occur in children, with patients requiring a wheelchair by their teens or early-20s and generally have a life expectancy of their mid-30s.

ALS is a rare, progressive and fatal neurodegenerative disease that results in the loss of motor neurons in the brain and the spinal cord that are responsible for controlling voluntary muscle movement. People with ALS experience muscle weakness and atrophy, causing them to lose independence as they steadily lose the ability to move, speak, eat and eventually breathe. Average life expectancy for people with ALS is three to five years from time of symptom onset. Multiple genes have been implicated in ALS. Genetic testing helps determine if a person's ALS is associated with a genetic mutation, even in individuals without a known family history of the disease. SOD1-ALS is diagnosed in approximately two percent of all ALS cases.

Our Rare disease products and major markets are as follows:

| Product | Indication | Collaborator | Major Markets | |||||||||||||||||

| SMA | Ionis | U.S. Brazil Canada China France Germany Italy Japan Spain Turkey | |||||||||||||||||

| ALS in adults with SOD1 gene | Ionis | U.S. | |||||||||||||||||

| FA in adults and adolescents aged 16 years and older | None | U.S. | |||||||||||||||||

For additional information on our collaboration arrangements with Ionis, please read Note 19, Collaborative and Other Relationships, to our consolidated financial statements included in this report.

9

BIOSIMILARS

Biosimilars are a group of biologic medicines that are highly similar to currently available biologic therapies developed by companies known as "originators". Under our agreements with Samsung Bioepis, we commercialize three anti-TNF biosimilars in certain countries in Europe: BENEPALI, an etanercept biosimilar referencing ENBREL, IMRALDI, an adalimumab biosimilar referencing HUMIRA, and FLIXABI, an infliximab biosimilar referencing REMICADE. We have also secured the exclusive rights to commercialize BYOOVIZ, a ranibizumab biosimilar referencing LUCENTIS, which is commercially available in the U.S. and certain international markets, and TOFIDENCE, a tocilizumab biosimilar referencing ACTEMRA, which was approved by the FDA during the third quarter of 2023.

Our current biosimilar products and major markets are as follows:

| Product | Indication | Major Markets | ||||||||||||

| Rheumatoid arthritis Juvenile idiopathic arthritis Psoriatic arthritis Axial spondyloarthritis Plaque psoriasis Paediatric plaque psoriasis | France Germany Italy Spain U.K. | ||||||||||||

| Rheumatoid arthritis Juvenile idiopathic arthritis Axial spondyloarthritis Psoriatic arthritis Psoriasis Paediatric plaque psoriasis Hidradenitis suppurativa Adolescent hidradenitis suppurativa Crohn’s disease Paediatric Crohn's disease Ulcerative colitis Uveitis Paediatric Uveitis | France Germany Sweden U.K. | ||||||||||||

| Rheumatoid arthritis Crohn’s disease Paediatric Crohn’s disease Ulcerative colitis Paediatric ulcerative colitis Ankylosing spondylitis Psoriatic arthritis Psoriasis | France Germany Italy | ||||||||||||

| Neovascular (wet) age-related macular degeneration Macular edema following retinal vein occlusion Myopic choroidal neovascularization | U.S. Canada Germany | ||||||||||||

For additional information on our collaboration arrangements with Samsung Bioepis, please read Note 19, Collaborative and Other Relationships, to our consolidated financial statements included in this report.

10

GENENTECH RELATIONSHIPS

We have agreements with Genentech that entitle us to certain business and financial rights with respect to RITUXAN, RITUXAN HYCELA, GAZYVA, OCREVUS, LUNSUMIO, COLUMVI, which was granted accelerated approval by the FDA during the second quarter of 2023, and have the option to add other potential anti-CD20 therapies.

Our current anti-CD20 therapeutic programs and major markets are as follows:

| Product | Indication | Major Markets | ||||||||||||

| Non-Hodgkin's lymphoma CLL Rheumatoid arthritis Two forms of ANCA-associated vasculitis Pemphigus vulgaris | U.S. Canada | ||||||||||||

| Non-Hodgkin's lymphoma CLL | U.S. | ||||||||||||

| In combination with chlorambucil for previously untreated CLL follicular lymphoma In combination with chemotherapy followed by GAZYVA alone for previously untreated follicular lymphoma | U.S. | ||||||||||||

| RMS PPMS | U.S. | ||||||||||||

| Relapsed or refractory follicular lymphoma | U.S. | ||||||||||||

| Relapsed or refractory diffuse large B-cell lymphoma Large B-cell lymphoma arising from follicular lymphoma | U.S. | ||||||||||||

For additional information on our collaboration arrangements with Genentech, please read Note 19, Collaborative and Other Relationships, to our consolidated financial statements included in this report.

OTHER

| Product | Indication | Collaborator | Major Markets | |||||||||||||||||

| Moderate to severe plaque psoriasis | None | Germany | |||||||||||||||||

PATIENT SUPPORT AND ACCESS

We interact with patients, advocacy organizations and healthcare societies in order to gain insights into unmet needs. The insights gained from these engagements help us support patients with services, programs and applications that are designed to help patients lead better lives. Among other things, we provide customer service and other related programs for our products, such as disease and product specific websites, insurance research services, financial assistance programs and the facilitation of the procurement of our marketed products.

11

We are dedicated to helping patients obtain access to our therapies. Our patient representatives have access to a suite of financial assistance tools. With those tools, we help patients understand their insurance coverage and, if needed, help patients compare insurance options and programs. In the U.S., we have established programs that provide co-pay assistance or free product for qualified uninsured or underinsured patients, based on specific eligibility criteria. We also provide charitable contributions to independent charitable organizations that assist patients with out-of-pocket expenses associated with their therapy.

We believe all healthcare stakeholders have a shared responsibility to ensure patients have equitable access to new, innovative medicines. We regularly review our pricing strategy and prioritize patient access to our therapies. We have a value-based contracting program designed to align the price of our therapies to the value our therapies deliver to patients. We also work with regulators, clinical researchers, ethicists, physicians and patient advocacy organizations and communities, among others, to determine how best to address requests for access to our investigational therapies in a manner that is consistent with our patient-focused values and compliant with regulatory standards and protocols. In appropriate situations, patients may have access to investigational therapies through Early Access Programs, single patient access or emergency use based on humanitarian or compassionate grounds.

MARKETING AND DISTRIBUTION

SALES FORCE AND MARKETING

We promote our marketed products worldwide, including in the U.S., Europe and Japan, primarily through our own sales forces and marketing groups. In some countries, particularly in areas where we continue to expand into new geographic areas, we partner with third parties.

RITUXAN, RITUXAN HYCELA, GAZYVA, OCREVUS and LUNSUMIO are marketed by the Roche Group and its sublicensees.

We commercialize BENEPALI, IMRALDI and FLIXABI pursuant to our agreement with Samsung Bioepis in certain countries in Europe, as well as BYOOVIZ in the U.S. and certain international markets.

We focus our sales and marketing efforts on physicians in private practice or at major medical centers. We use customary industry practices to market our products and to educate physicians. This includes our sales representatives calling on individual health care providers (in-person and virtually), advertisements, professional symposia, direct mail, digital marketing, point of care marketing, public relations and other methods. We focus on health care provider sales and marketing efforts on specialty providers in both private practice and at major medical centers.

DISTRIBUTION ARRANGEMENTS

We distribute our products in the U.S. principally through wholesale and specialty distributors of pharmaceutical products and specialty pharmacies, mail order specialty distributors or shipping service providers. In other countries, the distribution of our products varies from country to country, including through wholesale distributors of pharmaceutical products and third-party distribution partners who are responsible for most marketing and distribution activities.

RITUXAN, RITUXAN HYCELA, GAZYVA, OCREVUS and LUNSUMIO are distributed by the Roche Group and its sublicensees.

We distribute BENEPALI, IMRALDI and FLIXABI in certain countries in Europe and have an option to acquire exclusive rights to distribute these products in China, as well as BYOOVIZ in the U.S. and certain international markets.

Our product sales to two wholesale distributors each accounted for more than 10.0% of our total revenue for the years ended December 31, 2023, 2022 and 2021, and on a combined basis, accounted for approximately 36.9%, 37.9% and 38.9%, respectively, of our gross product revenue. For additional information, please read Note 5, Revenue, to our consolidated financial statements included in this report.

PATENTS AND OTHER PROPRIETARY RIGHTS

Patents are important for obtaining and protecting exclusive rights in our products and product candidates. We regularly seek patent protection in the U.S. and in selected countries outside the U.S. for inventions originating from our research and development efforts and those we license or acquire. In addition, we license rights to various patents and patent applications.

12

U.S. patents, as well as most foreign patents, are generally effective for 20 years from the date the earliest application was filed; however, U.S. patents on applications filed before June 8, 1995, may be effective until 17 years from the issue date, if that is later than the 20-year date. In some cases, the patent term may be extended to recapture a portion of the term lost during regulatory review of the claimed therapeutic or, in the case of the U.S., additional patent term may be awarded due to U.S. Patent and Trademark Office delays in prosecuting the application. In the U.S., under the Drug Price Competition and Patent Term Restoration Act of 1984, commonly known as the Hatch-Waxman Act, a patent that covers a drug approved by the FDA may be eligible for patent term extension (for up to 5 years, but not beyond a total of 14 years from the date of product approval) as compensation for patent term lost during the FDA regulatory review process. The duration and extension of the term of foreign patents vary, in accordance with local law. For example, in a number of European countries, SPCs can be granted to a product to compensate in part for delays in obtaining marketing approval.

Regulatory exclusivity, which may consist of regulatory data protection and market protection, can also provide meaningful protection for our products. Regulatory data protection provides to the holder of a drug or biologic marketing authorization, for a set period of time, the exclusive use of the proprietary pre-clinical and clinical data that it created at significant cost and submitted to the applicable regulatory authority to obtain approval of its product. After the period of exclusive use, third parties are permitted to reference such data in abbreviated applications for approval and to market (subject to any applicable market protection) their generic drugs and biosimilars. Market protection provides the holder of a drug or biologic marketing authorization the exclusive right to commercialize its product for a period of time, thereby preventing the commercialization of another product containing the same active ingredient(s) during that period. Although the World Trade Organization's agreement on trade-related aspects of intellectual property rights requires signatory countries to provide regulatory exclusivity to innovative pharmaceutical products, implementation and enforcement varies widely from country to country.

We also rely upon other forms of unpatented confidential information to remain competitive. We protect such information principally through refraining from public disclosure and utilizing confidentiality agreements with our employees, consultants, outside scientific collaborators, scientists whose research we sponsor and other advisers. In the case of our employees, these agreements also provide, in compliance with relevant law, that inventions and other intellectual property conceived by such employees during their employment are our exclusive property.

Our trademarks are important to us and are generally covered by trademark applications or registrations in the U.S. Patent and Trademark Office and the patent or trademark offices of other countries. We also use trademarks licensed from third parties. Trademark protection varies in accordance with local law, and continues in some countries as long as the trademark is used and in other countries as long as the trademark is registered. Trademark registrations generally are for fixed but renewable terms.

OUR PATENT PORTFOLIO

The following table describes certain patents in the U.S. and Europe that we currently consider of primary importance to our marketed products, including the territory, patent number, general subject matter and expected expiration dates. Except as otherwise noted, the expected expiration dates include any granted patent term extensions and issued SPCs. In some instances, there may be additional later-expiring patents relating to our products directed to, among other things, particular forms or compositions, methods of manufacturing or use of the drug in the treatment of particular diseases or conditions. We also continue to pursue additional patents and patent term extensions in the U.S. and other territories covering various aspects of our products that may, if issued, extend exclusivity beyond the expiration of the patents listed in the table.

13

| Product | Territory | Patent No. | General Subject Matter | Patent Expiration(1) | ||||||||||||||||||||||

| TECFIDERA | Europe | 1,131,065 | Formulations of dialkyl fumarates and their use for treating autoimmune diseases | 2024(2) | ||||||||||||||||||||||

| Europe | 2,653,873 | Methods of use | 2028 | |||||||||||||||||||||||

| PLEGRIDY | U.S. | 8,017,733 | Polymer conjugates of interferon beta-1a | 2027 | ||||||||||||||||||||||

| Europe | 1,656,952 | Polymer conjugates of interferon-beta-1a and uses thereof | 2024(3) | |||||||||||||||||||||||

| Europe | 1,476,181 | Polymer conjugates of interferon-beta-1a and uses thereof | 2023(4) | |||||||||||||||||||||||

| TYSABRI | U.S. | 8,124,350 | Methods of treatment | 2027 | ||||||||||||||||||||||

| U.S. | 8,349,321 | Formulation | 2024 | |||||||||||||||||||||||

| U.S. | 8,815,236 | Formulation | 2024 | |||||||||||||||||||||||

| U.S. | 8,871,449 | Methods of treatment | 2026 | |||||||||||||||||||||||

| U.S. | 8,900,577 | Formulation | 2024 | |||||||||||||||||||||||

| U.S. | 9,316,641 | Safety-related assay | 2032 | |||||||||||||||||||||||

| U.S. | 9,493,567 | Methods of treatment | 2027 | |||||||||||||||||||||||

| U.S. | 9,709,575 | Methods of treatment | 2026 | |||||||||||||||||||||||

| U.S. | 10,119,976 | Methods of evaluating patient risk | 2034 | |||||||||||||||||||||||

| U.S. | 10,233,245 | Methods of treatment | 2027 | |||||||||||||||||||||||

| U.S. | 10,444,234 | Safety-related assay | 2031 | |||||||||||||||||||||||

| U.S. | 10,677,803 | Methods of treatment | 2034 | |||||||||||||||||||||||

| U.S. | 10,705,095 | Methods of treatment | 2026 | |||||||||||||||||||||||

| U.S. | 11,280,794 | Methods of treatment | 2034 | |||||||||||||||||||||||

| U.S. | 11,287,423 | Safety-related assay | 2031 | |||||||||||||||||||||||

| U.S. | 11,292,845 | Methods of treatment | 2027 | |||||||||||||||||||||||

| Europe | 2,170,390 | Formulation | 2028 | |||||||||||||||||||||||

| Europe | 2,236,154 | Formulation | 2024 | |||||||||||||||||||||||

| Europe | 3,339,865 | Safety-related assay | 2031 | |||||||||||||||||||||||

| Europe | 3,417,875 | Formulation | 2024 | |||||||||||||||||||||||

| Europe | 3,575,792 | Safety-related assay | 2032 | |||||||||||||||||||||||

| FAMPYRA | Europe | 1,732,548 | Sustained-release aminopyridine compositions for increasing walking speed in patients with MS | 2025(5) | ||||||||||||||||||||||

| Europe | 2,377,536 | Sustained-release aminopyridine compositions for treating MS | 2025(6) | |||||||||||||||||||||||

| VUMERITY | U.S. | 8,669,281 | Compounds and pharmaceutical compositions | 2033 | ||||||||||||||||||||||

| U.S. | 9,090,558 | Methods of treatment | 2033 | |||||||||||||||||||||||

| U.S. | 10,080,733 | Crystalline forms, pharmaceutical compositions and methods of treatment | 2033 | |||||||||||||||||||||||

| Europe | 2,970,101 | Crystalline forms, pharmaceutical compositions and methods of treatment Prodrugs of fumarates and their use in treating various diseases | 2034 | |||||||||||||||||||||||

| SPINRAZA | U.S. | 7,838,657 | SMA treatment via targeting of SMN2 splice site inhibitory sequences | 2027 | ||||||||||||||||||||||

| U.S. | 8,110,560 | SMA treatment via targeting of SMN2 splice site inhibitory sequences | 2025 | |||||||||||||||||||||||

| U.S. | 8,361,977 | Compositions and methods for modulation of SMN2 splicing | 2030 | |||||||||||||||||||||||

| U.S. | 8,980,853 | Compositions and methods for modulation of SMN2 splicing | 2030 | |||||||||||||||||||||||

| U.S. | 9,717,750 | Compositions and methods for modulation of SMN2 splicing | 2030 | |||||||||||||||||||||||

| U.S. | 9,926,559 | Compositions and methods for modulation of SMN2 splicing | 2034 | |||||||||||||||||||||||

| U.S. | 10,266,822 | SMA treatment via targeting of SMN2 splice site inhibitory sequences | 2025 | |||||||||||||||||||||||

| U.S. | 10,436,802 | Methods for Treating Spinal Muscular Atrophy | 2035 | |||||||||||||||||||||||

| Europe | 1,910,395 | Compositions and methods for modulation of SMN2 splicing | 2026(7) | |||||||||||||||||||||||

| Europe | 2,548,560 | Compositions and methods for modulation of SMN2 splicing | 2026(8) | |||||||||||||||||||||||

| Europe | 3,305,302 | Compositions and methods for modulation of SMN2 splicing | 2030 | |||||||||||||||||||||||

| Europe | 3,308,788 | Compositions and methods for modulation of SMN2 splicing | 2026 | |||||||||||||||||||||||

| Europe | 3,449,926 | Compositions and methods for modulation of SMN2 splicing | 2030(10) | |||||||||||||||||||||||

14

| Product | Territory | Patent No. | General Subject Matter | Patent Expiration(1) | ||||||||||||||||||||||

| ADUHELM | U.S. | 8,906,367 | Method of providing disease-specific binding molecules and targets | 2032(11) | ||||||||||||||||||||||

| U.S. | 10,131,708 | Methods of treating Alzheimer's disease | 2028 | |||||||||||||||||||||||

| LEQEMBI | U.S. | 8,025,878 | Protofibril selective antibodies and the use thereof | 2027(1)(11) | ||||||||||||||||||||||

| QALSODY | U.S. | 10,385,341 | Compositions for modulating SOD-1 expression | 2035(11) | ||||||||||||||||||||||

| U.S. | 10,669,546 | Compositions for modulating SOD-1 expression | 2035 | |||||||||||||||||||||||

| U.S. | 10,968,453 | Compositions for modulating SOD-1 expression | 2035 | |||||||||||||||||||||||

| ZURZUVAE | U.S. | 9,512,165 | 19-nor C3, 3-disubstituted C21-N-pyrazolyl steroids and methods of use thereof | 2034(9) | ||||||||||||||||||||||

| U.S. | 10,172,871 | 19-nor C3, 3-disubstituted C21-N-pyrazolyl steroids and methods of use thereof | 2034(9) | |||||||||||||||||||||||

| U.S. | 10,342,810 | 19-nor C3, 3-disubstituted C21-N-pyrazolyl steroids and methods of use thereof | 2034(9) | |||||||||||||||||||||||

| U.S. | 11,236,121 | Crystalline 19-nor C3, 3-disubstituted C21-N-pyrazolyl steroid | 2034(9) | |||||||||||||||||||||||

| SKYCLARYS | U.S. | 8,124,799 | Antioxidant Inflammation Modulators: Oleanolic Acid Derivatives with Amino and other Modifications at C-17 (Composition) | 2029(9) | ||||||||||||||||||||||

| U.S. | 8,440,854 | Antioxidant Inflammation Modulators: Oleanolic Acid Derivatives with Amino and other Modifications at C-17 (Composition) | 2029(9) | |||||||||||||||||||||||

| U.S. | 8,993,640 | 2,2-Difluoropropionamide Derivatives of Bardoxolone Methyl, Polymorphic Forms and Methods of Use Thereof (Composition) | 2033(9) | |||||||||||||||||||||||

| U.S. | 9,670,147 | Antioxidant Inflammation Modulators: Oleanolic Acid Derivatives with Amino and other Modifications at C-17 (Composition) | 2029(9) | |||||||||||||||||||||||

| U.S. | 9,701,709 | 2,2-Difluoropropionamide Derivatives of Bardoxolone Methyl, Polymorphic Forms and Methods of Use Thereof (Composition) | 2033(9) | |||||||||||||||||||||||

| U.S. | 11,091,430 | Antioxidant Inflammation Modulators: Oleanolic Acid Derivatives with Amino and other Modifications at C-17 (Treatment Method) | 2029(9) | |||||||||||||||||||||||

Footnotes follow on next page.

15

(1)In addition to patent protection, certain of our products are entitled to regulatory exclusivity in the U.S. and the E.U. expected until the dates set forth below:

| Product | Territory | Expected Expiration | ||||||||||||

| TECFIDERA | E.U. | 2025 | ||||||||||||

| PLEGRIDY | U.S. | 2026 | ||||||||||||

| E.U. | 2024 | |||||||||||||

| SPINRAZA | E.U. | 2029 | ||||||||||||

| ADUHELM | U.S. | 2033 | ||||||||||||

| LEQEMBI | U.S. | 2035 | ||||||||||||

| QALSODY | U.S. | 2030 | ||||||||||||

| ZURZUVAE | U.S. | 2028 | ||||||||||||

| SKYCLARYS | U.S. | 2030 | ||||||||||||

(2)This patent is subject to granted SPCs in certain European countries, which extended the patent term in those countries to 2024.

(3)This patent is subject to granted SPCs in certain European countries, which extended the patent term in those countries to 2024.

(4)This patent is subject to granted SPCs in certain European countries, which extended the patent term in those countries to 2028.

(5)This patent is subject to granted SPCs in certain European countries, which extended the patent term in those countries to 2026.

(6)This patent is subject to granted SPCs in certain European countries, which extended the patent term in those countries to 2026.

(7)This patent is subject to granted SPCs in certain European countries, which extended the patent term in those countries to 2031.

(8)This patent is subject to granted SPCs in certain European countries, which extended the patent term in those countries to 2031.

(9)A patent with this subject matter may be entitled to patent term extension in the U.S.

(10)This patent is subject to granted SPCs in certain European countries, which extended the patent term in those countries to 2032.

The existence of patents does not guarantee our right to practice the patented technology or commercialize the patented product. Patents relating to pharmaceutical, biopharmaceutical and biotechnology products, compounds and processes, such as those that cover our existing products, compounds and processes and those that we will likely file in the future, do not always provide complete or adequate protection. Litigation, interferences, oppositions, inter partes reviews, administrative challenges or other similar types of proceedings are, have been and may in the future be necessary in some instances to determine the validity and scope of certain of our patents, regulatory exclusivities or other proprietary rights, and in other instances to determine the validity, scope or non-infringement of certain patent rights claimed by third parties to be pertinent to the manufacture, use or sale of our products. We also face challenges to our patents, regulatory exclusivities or other proprietary rights covering our products by third-parties, such as manufacturers of generics, biosimilars, prodrugs and products approved under abbreviated regulatory pathways. A discussion of certain risks and uncertainties that may affect our patent position, regulatory exclusivities or other proprietary rights is set forth in Item 1A. Risk Factors included in this report, and the discussion of legal proceedings related to certain patents described above is set forth in Note 21, Litigation, to our consolidated financial statements included in this report.

16

COMPETITION

Competition in the biopharmaceutical industry and the markets in which we operate is intense. There are many companies, including biotechnology and pharmaceutical companies, engaged in developing products for the indications our approved products are approved to treat and the therapeutic areas we are targeting with our research and development activities. Some of our competitors may have substantially greater financial, marketing, research and development and other resources than we do.

We believe that competition and leadership in the industry is based on scientific, managerial and technological excellence and innovation as well as establishing patent and other proprietary positions through research and development. The achievement of a leadership position also depends largely upon our ability to maximize the approval, acceptance and use of our product candidates and the availability of adequate financial resources to fund facilities, equipment, personnel, clinical testing, manufacturing and marketing. Another key aspect of remaining competitive in the industry is recruiting and retaining leading scientists and technicians to conduct our research activities and advance our development programs, including with the regulatory and commercial expertise to effectively advance and market our products.

Competition among products approved for sale may be based, among other things, on patent position, product efficacy, safety, patient convenience, delivery devices, reliability, availability, reimbursement and price. In addition, early entry of a new pharmaceutical product into the market may have important advantages in gaining product acceptance and market share. Accordingly, the relative speed with which we can develop products, complete the testing and approval process and supply commercial quantities of products will have a significant impact on our competitive position.

The introduction of new products or technologies, including the development of new processes or technologies by competitors or new information about existing products or technologies, results in increased competition for our marketed products and pricing pressure on our marketed products. The development of new or improved treatment options or standards of care or cures for the diseases our products treat reduces and could eliminate the use of our products or may limit the utility and application of ongoing clinical trials for our product candidates.

In addition, the commercialization of certain of our own approved products, products of our collaborators and pipeline product candidates may negatively impact future sales of our existing products.

We believe our long-term competitive position depends upon our success in discovering and developing innovative, cost-effective products that serve unmet medical needs, along with our ability to manufacture products efficiently and to launch and market them effectively in a highly competitive environment.

Additional information about the competition that our marketed products face is set forth below and in Item 1A. Risk Factors included in this report.

NEUROLOGY

MULTIPLE SCLEROSIS

Our MS products and revenue streams continue to face increasing competition in many markets from the introduction of generic versions, prodrugs and biosimilars of existing products and products approved under abbreviated regulatory pathways. Such products are likely to be sold at substantially lower prices than branded products. Accordingly, the introduction of such products as well as other lower-priced competing products may significantly reduce both the price that we are able to charge for our products and the volume of products we sell, which will negatively impact our revenue. In some jurisdictions a decrease in reimbursed price is mandated by law. In addition, in some markets, when a generic or biosimilar version of one of our products is commercialized, it may be automatically substituted for our product and significantly reduce our revenue in a short period of time.

Competition in the MS market is intense. Along with us, a number of companies are working to develop additional treatments for MS that may in the future compete with our MS products. One such product that was approved in the U.S. in 2017 and in the E.U. in 2018 is OCREVUS, a treatment for RMS and PPMS that was developed by Genentech. While we have a financial interest in OCREVUS, future sales of our MS products may be adversely affected if OCREVUS continues to gain market share, or if other MS products that we or our competitors are developing are commercialized.

17

TECFIDERA, AVONEX, PLEGRIDY, TYSABRI and VUMERITY each compete with one or more of the following branded products as well as generic and biosimilar versions of some of these products:

| Competing Product | Competitor | |||||||

| AUBAGIO (teriflunomide) | Sanofi Genzyme | |||||||

| BAFIERTAM (monomethyl fumarate) | Banner Life Sciences | |||||||

| BETASERON/BETAFERON (interferon-beta-1b) | Bayer Group | |||||||

| BRIUMVI (ublituximab-xiiy) | TG Therapeutics, Inc. | |||||||

| COPAXONE (glatiramer acetate) | Teva Pharmaceuticals Industries Ltd. | |||||||

| EXTAVIA (interferon-beta-1b) | Novartis AG | |||||||

| GILENYA (fingolimod) | Novartis AG | |||||||

| GLATOPA (glatiramer acetate) | Sandoz, a division of Novartis AG | |||||||

| KESIMPTA (ofatumumab) | Novartis AG | |||||||

| LEMTRADA (alemtuzumab) | Sanofi Genzyme | |||||||

| MAVENCLAD (cladribine) | EMD Serono | |||||||

| MAYZENT (siponimod) | Novartis AG | |||||||

| OCREVUS (ocrelizumab) | Genentech | |||||||

| PONVORY (ponesimod) | Janssen Pharmaceutical Companies of Johnson & Johnson | |||||||

| REBIF (interferon-beta-1) | EMD Serono | |||||||

| TYRUKO (natalizumab-sztn) | Sandoz, a division of Novartis AG | |||||||

| ZEPOSIA (ozanimod) | Bristol Myers Squibb Company | |||||||

Multiple TECFIDERA generic entrants are now in North America, Brazil and certain E.U. countries and have deeply discounted prices compared to TECFIDERA.

Following a favorable March 2023 decision of the CJEU affirming TECFIDERA's right to regulatory data and marketing protection and the EC determination in May 2023 that TECFIDERA is entitled to an additional year of market protection for its pediatric indication, we believe that TECFIDERA is entitled to regulatory marketing protection in the E.U. until at least February 2, 2025, and are seeking to enforce this protection. In December 2023, the EC revoked all centralized marketing authorizations for generic versions of TECFIDERA. As of December 31, 2023, some of the TECFIDERA generics have not yet fully exited some E.U. markets and we expect removal of all generics from the market will take additional time. We are closely monitoring this situation and working to enforce our legal right to market protection. In addition, we will continue to enforce our EP 2 653 873 patent related to TECFIDERA, which expires in 2028.

The generic competition for TECFIDERA has significantly reduced our TECFIDERA revenue and we expect that TECFIDERA revenue will continue to decline in the future.

We are also aware of a biosimilar entrant of TYSABRI that was approved in the U.S. in August 2023 and the E.U. in September 2023. We believe that future sales of TYSABRI may be adversely affected by the entrance of this biosimilar.

For additional information on the U.S. patent litigation related to a TYSABRI biosimilar, please read Note 21, Litigation, to our consolidated financial statements included in this report.

ALZHEIMER'S DISEASE

The market for the treatment of Alzheimer's disease is undeveloped and could be subject to rapid change in the future. Most current treatments are symptomatic or intended to improve quality of life. Along with us, several companies are working to develop additional treatments. Most recently, we codeveloped LEQEMBI, a treatment to address a defining pathology of Alzheimer's disease and we and our collaborator Eisai are in the process of launching this product. We are aware of other products now in development that, if approved, may also compete with LEQEMBI.

18

RARE DISEASE

SPINAL MUSCULAR ATROPHY

We face competition from a gene therapy product ZOLGENSMA (onasemnogene abeparvovec-xioi) and an oral product EVRYSDI (risdiplam). We expect that we will experience competition from both products in additional jurisdictions in the future, which may adversely affect our sales of SPINRAZA.

Additionally, we are aware of other products now in development that, if launched, may also compete with SPINRAZA. Future sales of SPINRAZA may be adversely affected by the commercialization of competing products.

FRIEDREICH'S ATAXIA

SKYCLARYS is the first treatment on the market for this indication and could face future competition from pipeline programs under development.

BIOSIMILARS

BENEPALI, IMRALDI and FLIXABI, the three biosimilar products we currently commercialize in certain countries in Europe pursuant to an agreement with Samsung Bioepis, compete with their reference products, ENBREL, HUMIRA and REMICADE, respectively, as well as other biosimilars of those reference products.

BYOOVIZ, a biosimilar product we currently commercialize in the U.S. and certain international markets pursuant to an agreement with Samsung Bioepis, competes with its reference product LUCENTIS, as well as other biosimilars of this reference product.

GENENTECH RELATIONSHIPS IN OTHER INDICATIONS

RITUXAN, RITUXAN HYCELA, GAZYVA and LUNSUMIO in Oncology