As filed with the Securities and Exchange Commission on October 10, 2018

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM SF-3

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933

FORD CREDIT FLOORPLAN MASTER OWNER TRUST A

(Name of issuing entity)

|

FORD CREDIT FLOORPLAN CORPORATION |

|

FORD CREDIT FLOORPLAN LLC |

(Depositors for the issuing entity)

(Exact names of co-registrants as specified in their respective charters)

|

Delaware |

|

38-2973806 |

|

Delaware |

|

38-3372243 |

|

(State of incorporation) |

|

(I.R.S. Employer Identification No.) |

|

(State of organization) |

|

(I.R.S. Employer Identification No.) |

|

One American Road |

|

48126 |

|

One American Road |

|

48126 |

|

(Address of principal executive office of co-registrant) |

|

ZIP Code |

|

(Address of principal executive office of co-registrant) |

|

ZIP Code |

FORD MOTOR CREDIT COMPANY LLC

(Sponsor for the issuing entity)

(Exact name of sponsor as specified in its charter)

A Delaware Limited Liability Company

Central Index Key Number of sponsor: 0000038009

One American Road

Dearborn, Michigan 48126

(313) 322-3000

NATHAN A. HERBERT

Ford Motor Credit Company LLC

One American Road

Dearborn, Michigan 48126

(313) 390-1907

(Name and Address of Agent for Service)

Copy to:

JOSEPH P. TOPOLSKI

Katten Muchin Rosenman LLP

575 Madison Avenue

New York, New York 10022

(212) 940-8800

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this registration statement as determined by market conditions.

If any of the securities being registered on this Form SF-3 are to be offered pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form SF-3 is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form SF-3 is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities to be Registered |

|

|

Amount to be |

|

|

Proposed Maximum |

|

|

Proposed Maximum |

|

|

Amount of |

|

Asset Backed Securities |

|

|

(2)(3) |

|

|

(2)(3) |

|

|

(2)(3) |

|

|

(2)(3) |

(1) Calculated in accordance with Rule 457(s) of the Securities Act of 1933.

(2) The Depositors as registrants previously registered $2,000,000,000.00 of securities on March 8, 2018 under registration statement Nos. 333-206773, 333-206773-01 and 333-206773-02 filed on November 20, 2015, $718,954,000.00 of which remain unsold. Pursuant to Rule 415(a)(6) of the Securities Act of 1933, the registrants are including such unsold securities and the $89,509.77 of registration fees previously paid in connection with such unsold securities.

(3) An unspecified additional amount of securities of each identified class is being registered as may from time to time be offered at unspecified prices. The registrants are deferring payment of all of the registration fees for such additional securities in accordance with Rules 456(c) and 457(s) of the Securities Act of 1933.

The registrants hereby amend this registration statement on such date or dates as may be necessary to delay its effective date until the registrants file a further amendment that specifically states that this registration statement will thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement becomes effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

[Form of Prospectus]

This prospectus is not complete and may be changed. This prospectus is not an offer to sell these securities and we are not seeking an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED ________, 20__

$_______________

Series 20__-__ Asset Backed Notes

Ford Credit Floorplan Master Owner Trust A

Issuing Entity or Trust

(CIK: 0001159408)

|

Ford Credit Floorplan Corporation Ford Credit Floorplan LLC |

|

Ford Motor Credit Company LLC Sponsor and Servicer (CIK: 0000038009) |

|

Before you purchase any notes, be sure you understand the structure and the risks. You should read carefully the risk factors beginning on page __ of this prospectus. |

|

|

|

The notes will be obligations of the issuing entity only and will not be obligations of or interests in the sponsor, either depositor or any of their affiliates. |

|

|

The trust will issue:

|

|

|

Principal |

|

Interest Rate |

|

Expected Final |

|

Final |

|

|

Class A[-1] notes[(2)(3)(5)] |

|

} $ |

|

[One-month LIBOR +] __% |

|

|

|

|

|

|

[Class A-2 notes(2)(3)(5) |

|

|

One-month LIBOR + __%] |

|

|

|

|

| |

|

Class B notes[(3)(4)(5)] |

|

|

|

[One-month LIBOR +] __% |

|

|

|

|

|

|

Class C notes[(3)(4)(5)] |

|

|

|

[One-month LIBOR +] __% |

|

|

|

|

|

|

Class D notes[(3)(4)(5)] |

|

|

|

[One-month LIBOR +] % |

|

|

|

|

|

|

Total |

|

$ |

|

|

|

|

|

|

|

(1) The aggregate principal amount of each class of notes may be increased or decreased, pro rata, on or before the day of pricing. Any dollar amounts in this prospectus that are calculated based on the principal amount of the notes will be similarly increased or decreased, pro rata.

[(2) The allocation of the principal amount between the Class A-1 and Class A-2 notes will be determined on or before the day of pricing. The entire principal amount may be allocated to either the Class A 1 or Class A 2 notes, but neither class will be issued in an aggregate principal amount of less than $ .]

[(3) If one-month LIBOR plus the spread for the Class A[-1, A-2, Class B, Class C and Class D] notes is less than zero, the interest rate will be 0.00%.]

[(4) The [Class B, Class C and Class D] notes are not being offered by this prospectus.]

[(5) For more information on how one-month LIBOR is determined, you should read “Description of the Notes — Payments of Interest.”]

· The primary asset of the trust is a revolving pool of receivables originated in connection with the purchase and financing of new and used car, truck and utility vehicle inventory by motor vehicle dealers.

· The trust will pay interest on the notes on the 15th day of each month (or, if not a business day, the next business day). The first payment date will be , 20 .

· The trust expects to pay the principal of the notes on the expected final payment date. No principal will be paid on the notes before the expected final payment date, unless an amortization event occurs.

· The credit enhancement for the notes will be a reserve account, subordination, subordination of a portion of the depositor interest and excess spread.

The pricing terms of the offered notes are:

|

|

|

Price to Public |

|

Underwriting |

|

Proceeds to the |

| |||

|

Class A[-1] notes |

|

|

% |

|

% |

|

% | |||

|

[Class A-2 notes |

|

|

% |

|

% |

|

%] | |||

|

[Class B notes |

|

|

% |

|

% |

|

%] | |||

|

[Class C notes |

|

|

% |

|

% |

|

%] | |||

|

[Class D notes |

|

|

% |

|

% |

|

%] | |||

|

Total |

|

$ |

|

|

$ |

|

|

$ |

|

|

(1) Before deducting expenses estimated to be $_________ and any selling concessions rebated to the depositors by an underwriter due to sales to affiliates.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined that this prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

[NAMES OF UNDERWRITERS]

The date of this prospectus is _________, 20__

[To be included in Rule 424(h) filing of each pay-as-you-go takedown]

[CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities |

|

Amount to be |

|

Proposed Maximum |

|

Proposed Maximum |

|

Amount of |

|

|

Asset Backed Securities[(2)] |

|

$ [(3)] |

|

100% |

|

$ [(3)] |

|

$ [(3)] |

|

(1) Calculated according to Rule 457(s) of the Securities Act of 1933.]

[(2) Relates to the trust’s Series 20__-__ notes and Series 20__-__ notes. The trust expects to issue Series 20__-__ on the closing date. The Series 20__-__ notes are not being offered by this prospectus. Some expected characteristics of the Series 20__-__ notes are summarized in Annex A to this prospectus.]

[(3) The Depositors as registrants previously registered [on _______, 20__,] $__________ of securities under the registration statement originally filed on _______, 20__, of which this prospectus is a part, $__________ of which remain unsold. Pursuant to Rule 456(c) of the Securities Act of 1933, the registrants are hereby registering an additional $__________ of securities (and paying the $__________ registration fee in connection with those additional securities) for a proposed maximum aggregate offering of $__________.]

|

4 | |

|

4 | |

|

4 | |

|

4 | |

|

6 | |

|

7 | |

|

8 | |

|

10 | |

|

11 | |

|

19 | |

|

32 | |

|

32 | |

|

33 | |

|

33 | |

|

34 | |

|

34 | |

|

Material Changes to Origination and Underwriting Policies and Procedures |

38 |

|

38 | |

|

39 | |

|

42 | |

|

44 | |

|

44 | |

|

44 | |

|

45 | |

|

45 | |

|

46 | |

|

46 | |

|

47 | |

|

48 | |

|

49 | |

|

54 | |

|

56 | |

|

57 | |

|

57 | |

|

60 | |

|

61 | |

|

61 |

|

62 | |

|

62 | |

|

63 | |

|

Defaulted Receivables and Principal Collections Used to Pay Interest |

65 |

|

65 | |

|

66 | |

|

66 | |

|

66 | |

|

67 | |

|

69 | |

|

69 | |

|

71 | |

|

Defaulted Receivables and Principal Collections Used to Pay Interest |

78 |

|

78 | |

|

80 | |

|

80 | |

|

81 | |

|

82 | |

|

84 | |

|

84 | |

|

85 | |

|

86 | |

|

86 | |

|

87 | |

|

88 | |

|

88 | |

|

88 | |

|

88 | |

|

89 | |

|

89 | |

|

91 | |

|

92 | |

|

92 | |

|

92 | |

|

92 | |

|

93 | |

|

94 |

|

94 | |

|

95 | |

|

95 | |

|

95 | |

|

Amendments to Sale and Servicing Agreements and Receivables Purchase Agreements |

95 |

|

96 | |

|

97 | |

|

98 | |

|

98 | |

|

100 | |

|

100 | |

|

100 | |

|

101 | |

|

102 | |

|

103 | |

|

104 | |

|

106 | |

|

106 | |

|

107 | |

|

107 | |

|

108 | |

|

108 |

|

109 | |

|

109 | |

|

110 | |

|

112 | |

|

113 | |

|

113 | |

|

114 | |

|

114 | |

|

117 | |

|

117 | |

|

117 | |

|

118 | |

|

119 | |

|

119 | |

|

121 | |

|

121 | |

|

121 | |

|

122 | |

|

122 | |

|

123 | |

|

A-1 |

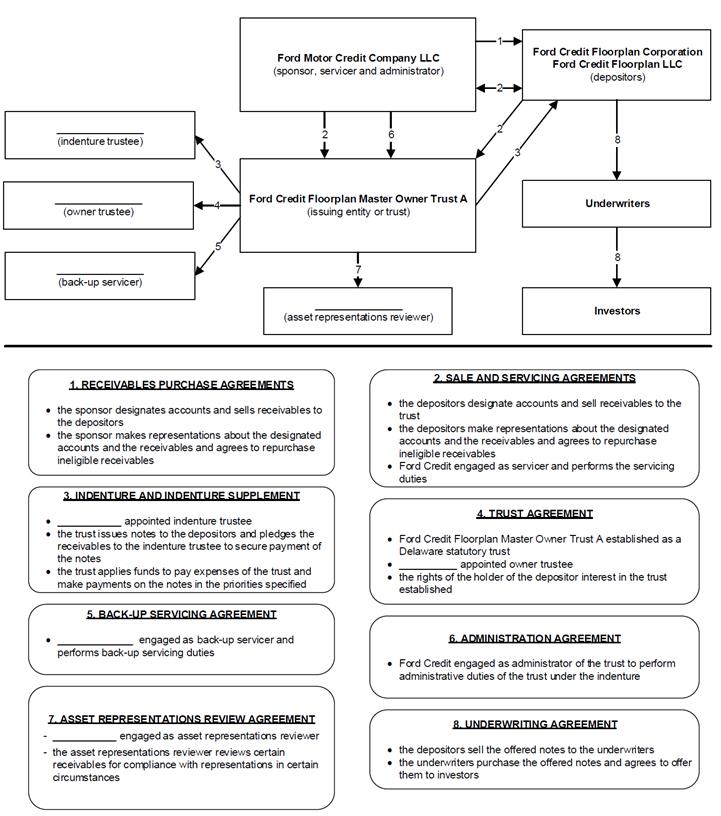

This prospectus contains information about Ford Credit Floorplan Master Owner Trust A and the terms of the Series 20__-__ notes to be issued by the trust. You should only rely on information in or referenced in this prospectus and any information incorporated by reference into the registration statement for this securitization transaction filed with the Securities and Exchange Commission, or “SEC,” that includes this prospectus. Ford Credit has not authorized anyone to provide you with different information.

This prospectus starts with the following introductory sections:

· Transaction Diagrams — separate diagrams show the structure of this securitization transaction, the credit enhancement available for the notes, transaction payments and the role of each transaction party and transaction document in this securitization transaction,

· Summary — provides an overview of the series, the assets of the trust, the cash flows of the series and the credit enhancement available for the series, and

· Risk Factors — describes the most significant risks of investing in the notes.

The other sections of this prospectus contain more details about the series and the structure of the series. Cross-references refer you to more details about a particular topic or related information elsewhere in this prospectus. The Table of Contents contains references to key topics.

An index of defined terms is at the end of this prospectus.

Any projections, expectations and estimates in this prospectus are not historical in nature but are forward-looking statements based on information and assumptions Ford Credit and the depositors consider reasonable. Forward-looking statements are about circumstances and events that have not yet taken place, so they are uncertain and may vary materially from actual events. Neither Ford Credit nor either depositor is obligated to update or revise any forward-looking statements, including changes in economic conditions, portfolio or asset pool performance or other circumstances or developments, after the date of this prospectus.

[NOTICE TO UNITED KINGDOM RESIDENTS

THIS PROSPECTUS IS DIRECTED IN THE UNITED KINGDOM ONLY AT PERSONS WHO (I) HAVE PROFESSIONAL EXPERIENCE IN MATTERS RELATING TO INVESTMENTS AND WHO QUALIFY AS INVESTMENT PROFESSIONALS UNDER ARTICLE 19(5) OF THE UNITED KINGDOM FINANCIAL SERVICES AND MARKETS ACT 2000 (FINANCIAL PROMOTION) ORDER 2005 (THE “FSMA”), OR (II) ARE HIGH NET WORTH COMPANIES, UNINCORPORATED ASSOCIATIONS, PARTNERSHIPS OR TRUSTEES UNDER ARTICLE 49(2) OF THE FSMA (TOGETHER, “RELEVANT PERSONS”). THIS PROSPECTUS MUST NOT BE ACTED ON OR RELIED ON BY PERSONS WHO ARE NOT RELEVANT PERSONS AND ONLY RELEVANT PERSONS MAY INVEST IN THE NOTES. ANY INVESTMENT ACTIVITY RELATING TO THIS PROSPECTUS OR THE NOTES WILL BE ENGAGED IN ONLY WITH RELEVANT PERSONS.]

[NOTICE TO EUROPEAN ECONOMIC AREA RESIDENTS

THIS PROSPECTUS IS NOT A PROSPECTUS FOR THE PURPOSE OF THE PROSPECTUS DIRECTIVE (AS DEFINED BELOW). THIS PROSPECTUS HAS BEEN PREPARED ON THE BASIS THAT ANY OFFERS OF THE NOTES IN ANY MEMBER STATE OF THE EUROPEAN ECONOMIC AREA (“EEA”), WHICH HAS IMPLEMENTED THE PROSPECTUS DIRECTIVE (EACH, A “RELEVANT MEMBER STATE”) WILL ONLY BE MADE TO A LEGAL ENTITY THAT IS A QUALIFIED INVESTOR

UNDER THE PROSPECTUS DIRECTIVE (“QUALIFIED INVESTOR”). ACCORDINGLY, ANY PERSON OFFERING OR INTENDING TO OFFER IN A RELEVANT MEMBER STATE THE NOTES DESCRIBED IN THIS PROSPECTUS MAY ONLY DO SO WITH RESPECT TO QUALIFIED INVESTORS. NONE OF THE TRUST, EITHER DEPOSITOR NOR ANY UNDERWRITER HAS AUTHORIZED, NOR DO THEY AUTHORIZE, THE OFFERING OF THE NOTES OTHER THAN TO QUALIFIED INVESTORS. “PROSPECTUS DIRECTIVE” MEANS DIRECTIVE 2003/71/EC (AS AMENDED, INCLUDING BY DIRECTIVE 2010/73/EU), AND INCLUDES ANY IMPLEMENTING MEASURE IN THE RELEVANT MEMBER STATE.

THE NOTES ARE NOT INTENDED TO BE OFFERED, SOLD OR OTHERWISE MADE AVAILABLE TO AND SHOULD NOT BE OFFERED, SOLD OR OTHERWISE MADE AVAILABLE TO ANY RETAIL INVESTOR IN THE EEA. FOR THESE PURPOSES, A RETAIL INVESTOR MEANS A PERSON WHO IS ONE (OR MORE) OF: (I) A RETAIL CLIENT AS DEFINED IN POINT (11) OF ARTICLE 4(1) OF DIRECTIVE 2014/65/EU (AS AMENDED, “MIFID II”); (II) A CUSTOMER WITHIN THE MEANING OF DIRECTIVE 2002/92/EC (KNOWN AS THE “INSURANCE MEDIATION DIRECTIVE”) AS AMENDED, WHERE THAT CUSTOMER WOULD NOT QUALIFY AS A PROFESSIONAL CLIENT AS DEFINED IN POINT (10) OF ARTICLE 4(1) OF MIFID II; OR (III) NOT A QUALIFIED INVESTOR AS DEFINED IN THE PROSPECTUS DIRECTIVE.

CONSEQUENTLY NO KEY INFORMATION DOCUMENT REQUIRED BY REGULATION (EU) NO 1286/2014 (THE “PRIIPS REGULATION”) FOR OFFERING OR SELLING THE NOTES OR OTHERWISE MAKING THEM AVAILABLE TO RETAIL INVESTORS IN THE EEA HAS BEEN PREPARED AND THEREFORE OFFERING OR SELLING THE NOTES OR OTHERWISE MAKING THEM AVAILABLE TO ANY RETAIL INVESTOR IN THE EEA MAY BE UNLAWFUL UNDER THE PRIIPS REGULATION.]

This diagram is a simplified overview of the structure of Series 20__-__ and the credit enhancement available for the series. You should read this prospectus completely for more details about the series.

(1) Excess spread for this series is the excess of interest collections allocated to the series over the interest payments on the notes and the senior fees and expenses of the trust that are allocated to the series.

(2) The depositor interest will be held by the depositors and represents the interest in the trust property not allocated to a series. A portion of the depositor interest equal to the available subordinated amount is subordinated to the notes.

(3) The depositors will deposit $_________ in the reserve account on the closing date. The amount that is required to be in the reserve account is ___% of the initial note balance of the Series 20__-__ notes, unless the depositors elect to increase the amount in the reserve account during a subordination step-up period or an amortization event occurs in which case the reserve account required amount will increase.

(4) All notes other than the Class D notes will benefit from subordination of more junior classes to more senior classes. The subordination varies depending on whether interest or principal is being paid, whether an amortization event that results in monthly payments of principal has occurred and whether an event of default that results in acceleration has occurred. For more details about subordination, you should read “Description of the Notes — Application of Investor Collections — Payment of Interest, Fees and Other Items” and “Description of the Notes — Application of Investor Collections — Payment of Principal” and “Credit Enhancement — Subordination.”

(5) The aggregate principal amount of each class of notes may be increased or decreased, pro rata, on or before the day of pricing. Any dollar amounts in this prospectus that are calculated based on the principal amount of the notes will be similarly increased or decreased, pro rata.

TRANSACTION CREDIT ENHANCEMENT DIAGRAM

This diagram is a simplified overview of the credit enhancement available for the series on the closing date and how credit enhancement is used to offset losses on the receivables. You should read this prospectus completely, including “Credit Enhancement,” for more details about the credit enhancement available for the series.

(1) All notes other than the Class D notes benefit from subordination of more junior classes to more senior classes. The subordination varies depending on whether interest or principal is being paid, whether an amortization event that results in monthly payments of principal has occurred and whether an event of default that results in acceleration has occurred. For more details about subordination, you should read “Description of the Notes — Application of Investor Collections — Payment of Interest, Fees and Other Items” and “Description of the Notes — Application of Investor Collections — Payment of Principal” and “Credit Enhancement — Subordination.”

(2) A portion of the depositor interest, or the “available subordinated amount,” is subordinated to the series. The amount subordinated will initially equal $_____________, which is approximately __% of the initial note balance, plus any incremental subordinated amount for the first determination date. The available subordinated amount will increase during a subordination step-up period, unless the depositors elect to increase the amount required to be in the reserve account during that period, and is subject to other reductions and increases from time to time.

(3) The depositors will deposit $_________ in the reserve account on the closing date. The amount that is required to be in the reserve account is ___% of the initial note balance of the Series 20__-__ notes, unless the depositors elect to increase the amount in the reserve account during a subordination step-up period or an amortization event occurs in which case the reserve account required amount will increase.

(4) Excess spread for this series is the excess of interest collections allocated to the series over the interest payments on the notes and the senior fees and expenses of the trust that are allocated to the series.

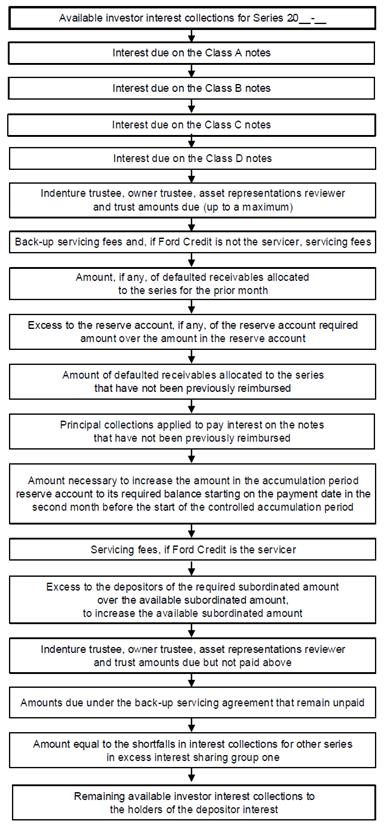

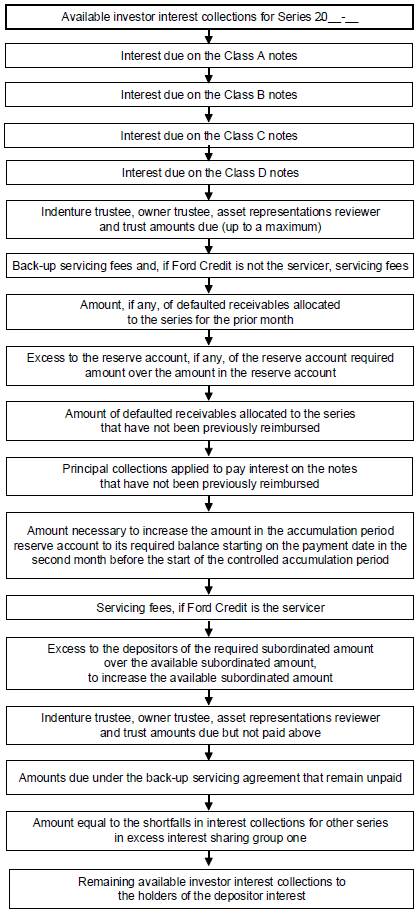

This diagram shows how available investor interest collections are paid on each payment date. You should read this prospectus completely, including “Description of the Notes — Application of Investor Collections,” for more details about the payments of available investor interest collections for this series.

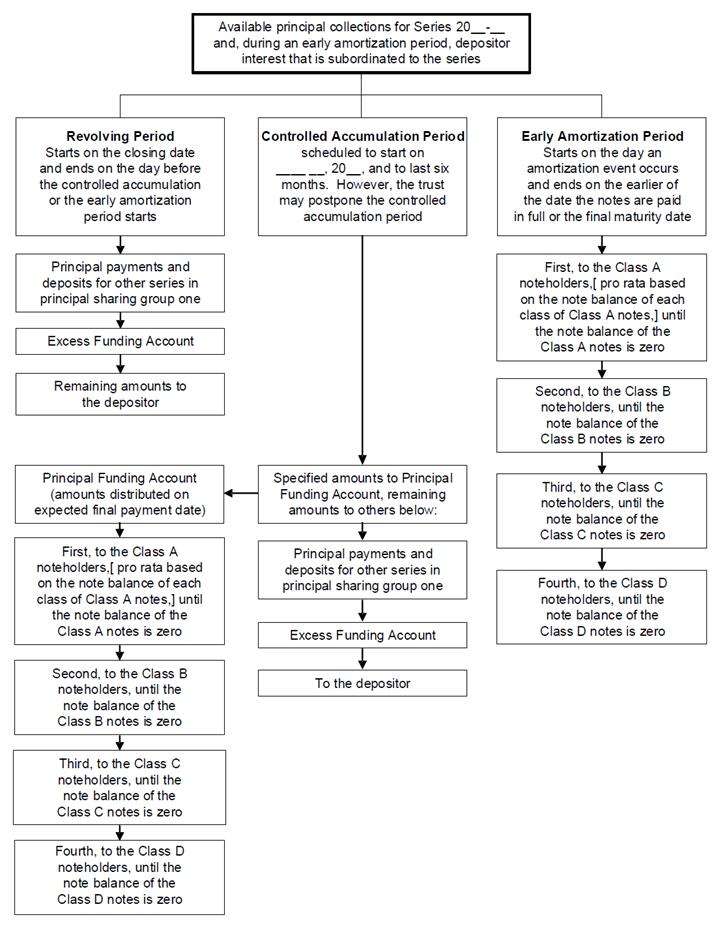

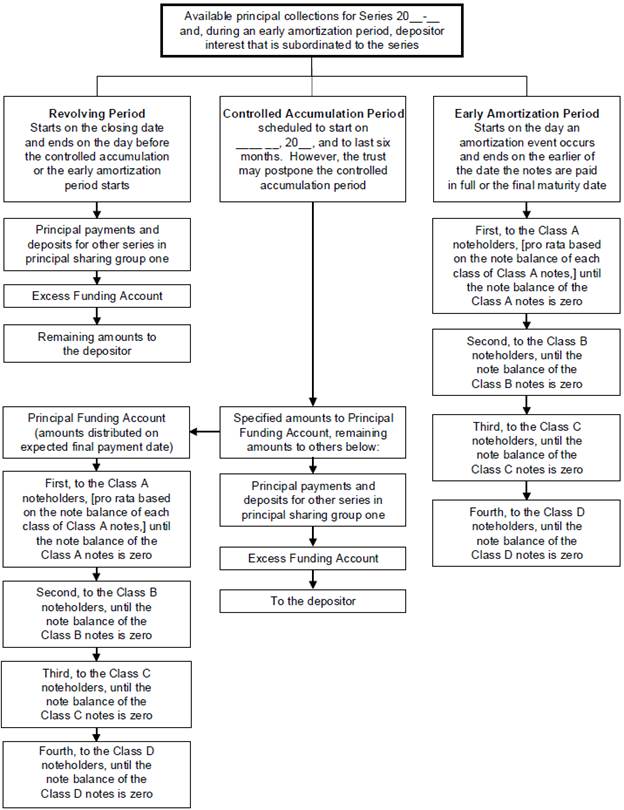

This diagram shows how available investor principal collections are paid on each payment date. You should read this prospectus completely, including “Description of the Notes — Application of Investor Collections,” for more details about the payments of available investor principal collections for this series.

TRANSACTION PARTIES AND DOCUMENTS DIAGRAM

This diagram shows the role of each transaction party and each transaction document in this securitization transaction. You should read this prospectus completely, including “Transaction Parties,” “Trust Property,” “Description of the Notes” and “Servicing,” for more details about the roles of each transaction party and each transaction document in this securitization transaction.

This summary describes the main terms of the issuance of and payments on the Series 20__-__ notes, the assets of the trust, the cash flows of the series and the credit enhancement available for the series. It does not contain all of the information that you should consider in making your decision to purchase any notes. To understand fully the terms of the notes and the transaction structure, you should read this prospectus completely, especially “Risk Factors” starting on page __.

Transaction Overview

The trust is a master trust that owns a revolving pool of receivables originated in connection with the purchase and financing of new and used car, truck and utility vehicle inventory by motor vehicle dealers. The trust will issue the Series 20__-__ notes backed by this revolving pool of receivables to the depositors on the closing date. The depositors will sell the offered notes to the underwriters who will offer them to investors.

Transaction Parties

Sponsor, Servicer and Administrator of the Trust

Ford Motor Credit Company LLC, or “Ford Credit,” is a Delaware limited liability company and a wholly-owned subsidiary of Ford Motor Company, or “Ford.”

Depositors

Ford Credit Floorplan Corporation, or “FCF Corp,” a Delaware corporation, and Ford Credit Floorplan LLC, or “FCF LLC,” a Delaware limited liability company, are special-purpose companies wholly owned by Ford Credit.

Issuing Entity or Trust

Ford Credit Floorplan Master Owner Trust A, or the “trust,” is a Delaware statutory trust established under a trust agreement between the depositors and the owner trustee.

Owner Trustee

_______________________

Indenture Trustee

_______________________

Back-up Servicer

_______________________

Asset Representations Reviewer

_______________________

For more information about the transaction parties and their roles in this securitization transaction, you should read “Sponsor and Servicer” and “Transaction Parties.”

Closing Date

The trust expects to issue the Series 20__-__ notes on or about _______, 20__, or the “closing date.”

Notes

The trust will issue the following notes in Series 20__-__:

|

|

|

Principal |

|

Interest Rate |

|

Class A-1[(2)(3)] |

|

} $ |

|

[One-month LIBOR +] __% |

|

[Class A-2(2)(3) |

|

|

One-month LIBOR + __%] | |

|

Class B[(3)(4)] |

|

$ |

|

[One-month LIBOR +] __% |

|

Class C[(3)(4)] |

|

$ |

|

[One-month LIBOR +] __% |

|

Class D[(3)(4)] |

|

$ |

|

[One-month LIBOR +] __% |

(1) The aggregate principal amount of each class of notes may be increased or decreased, pro rata, on or before the day of pricing.

[(2) The allocation of the principal amount between the Class A-1 and Class A-2 notes will be determined on or before the day of pricing.]

(3) If one-month LIBOR plus the spread for the Class A[-1, A-2, Class B, Class C and Class D] notes is less than zero, the interest rate will be 0.00%.

[(4) The [Class B, Class C and Class D] notes are not being offered by this prospectus.]

[The Class A-1 and Class A-2 notes are together referred to as the “Class A notes.”] [The Class A [and Class B] notes are being offered by this prospectus and are collectively referred to as the “offered notes” and, together with the [Class B, Class C and Class D notes], the “Series 20__-__

notes,” the “notes.”] [The Class A[-1, Class A-2 Class B, Class C and Class D] notes are sometimes referred to as the “fixed rate notes.”] [The Class A[-1, A-2, Class B, Class C and Class D] notes are sometimes referred to as the “floating rate notes.”] [The Class A-1 and Class A-2 notes have equal rights to interest and principal payments and, unless stated in this prospectus, will be treated as a single class in relation to the other classes.]

The depositors [may retain some or all of the offered notes and] will initially retain the [Class C and Class D notes] and the depositor interest in the trust.

The Series 20__-__notes will be issued under the indenture and an indenture supplement to be entered into between the trust and the indenture trustee, or the “indenture supplement.”

Form and Minimum Denomination

The notes will be issued in book-entry form. The offered notes will be available in minimum denominations of $1,000 and in multiples of $1,000.

Payment Dates

The trust will pay interest and principal, if any, on the notes on “payment dates,” which will be the 15th day of each month (or, if not a business day, the next business day). The first payment date will be ________, 20__.

[The fixed rate notes will accrue interest on a “30/360” basis from the 15th day of the prior month to the 15th day of the current month (or the closing date to ________, 20__, for the first period).] [The floating rate notes will accrue interest on an “actual/360” basis from the prior payment date (or from the closing date, for the first period) to the current payment date.]

The trust expects to pay the principal of the Series 20__-__ notes in full on the expected final payment date shown below:

|

|

|

Expected Final |

|

Final |

|

Class A[-1] |

|

|

|

|

|

[Class A-2] |

|

|

|

|

|

Class B |

|

|

|

|

|

Class C |

|

|

|

|

|

Class D |

|

|

|

|

No principal will be paid on the notes before the expected final payment date, unless an amortization event occurs, after which principal will be paid monthly on each payment date. Principal may be paid on the notes after the expected final payment date.

For more details about the payment of interest and principal on each payment date, you should read “Description of the Notes — Payments of Interest” and “Description of the Notes — Payments of Principal.”

[Calculation Agent

The “calculation agent” will be the indenture trustee. The calculation agent will determine LIBOR, which is used to calculate the interest rate for the floating rate notes.]

Trust Property

The primary asset of the trust is a revolving pool of receivables and related assets originated in accounts designated to the trust. On ________, 20__, the total principal balance of the receivables was $___________. The number of designated accounts was _____.

For more information about the accounts and receivables in the trust, you should read “Trust Property.”

Servicing

Ford Credit will be the “servicer” of the receivables and this securitization transaction. The servicer is responsible for collecting and recording payments, making required adjustments to the receivables, monitoring dealer payments and maintaining books and records relating to the accounts and the receivables. The servicer will prepare monthly reports on the accounts and the receivables,

payments on the Series 20__-__ notes and the status of credit enhancements.

The trust will pay the servicer a fee each month equal to 1/12 of ___% of the portion of the receivables allocated to the Series 20__-__ notes.

For more information about the servicer, you should read “Sponsor and Servicer.”

[__________ is the back-up servicer. The back-up servicer will review the servicer’s operations annually, receive monthly receivables data and confirm certain information on the monthly investor reports. If the servicer resigns or is terminated, the back-up servicer will be the successor servicer.

The trust will pay the back-up servicer a fee each month equal to 1/12 of ___% of the portion of the receivables allocated to the Series 20__-__ notes.

For more information about the back-up servicer, you should read “Transaction Parties — Back-up Servicer.”]

Allocation of Collections

The servicer will collect payments on the receivables and will deposit these collections, up to the amount required for payment to each series on the following payment date, in the collection account. Each month, the servicer will allocate interest collections, principal collections and the principal balance of defaulted receivables to:

· Series 20__-__,

· other series of notes issued by the trust, and

· the depositor interest.

The amounts allocated to Series 20__-__ will be based generally on the size of its invested amount compared with the adjusted pool balance of the trust. The initial invested amount of the series will be $_________, which is the initial note balance of the series.

For more details about these allocations, you should read “Description of the Notes — Investor Percentages” and “— Defaulted

Receivables and Principal Collections Used to Pay Interest.”

Application of Collections

Interest Collections

On each payment date, interest collections allocated to Series 20__-__ for the prior month will be applied in the order of priority listed below:

(1) Class A Interest — to pay interest due on the Class A notes,

(2) Class B Interest — to pay interest due on the Class B notes,

(3) Class C Interest — to pay interest due on the Class C notes,

(4) Class D Interest — to pay interest due on the Class D notes,

(5) Transaction Fees and Expenses — to the indenture trustee, the owner trustee and the asset representations reviewer, the fees, expenses and indemnities due for the series, and to or at the direction of the trust, any expenses of the trust for the series, up to a maximum of $_________ per year,

(6) Servicing Fees — (a) to the back-up servicer, the monthly back-up servicing fee for the series and (b) to the servicer, the monthly servicing fee for the series if Ford Credit is no longer the servicer,

(7) Defaulted Receivables — to reimburse the defaulted receivables allocated to the series for the prior month,

(8) Reserve Account — to the reserve account, to fund it up to the reserve account required amount,

(9) Reimbursement of Defaulted Receivables for Prior Periods — to reimburse the defaulted receivables allocated to the series for prior months that have not been previously reimbursed,

(10) Reimbursement of Principal Used to Pay Interest — to reimburse principal

collections allocated to the series that were used to pay interest on the notes,

(11) Accumulation Period Reserve Account — starting on the accumulation period reserve account funding date, to the accumulation period reserve account, to fund it up to $__________,

(12) Servicing Fees — to Ford Credit, if Ford Credit is the servicer, the monthly servicing fee for the series,

(13) Available Subordinated Amount — to increase the available subordinated amount up to the required subordinated amount,

(14) Additional Transaction Fees and Expenses – to the indenture trustee, the owner trustee, the asset representations reviewer and the trust, all amounts due for the series to the extent not paid under item (5) above,

(15) Additional Servicing Fees – to the back-up servicer, any remaining amounts due including any transition expenses incurred by the back-up servicer as the successor servicer, in excess of amounts in the back-up servicer reserve account,

(16) Excess Interest Sharing Group One — to cover any shortfalls for other series in excess interest sharing group one, and

(17) Depositor Interest — to the holders of the depositor interest in the trust.

For more details about the application of interest collections, you should read “Description of the Notes — Application of Investor Collections — Payment of Interest, Fees and Other Items.”

Principal Collections

The application of principal collections allocated to Series 20__-__ on each payment date will depend on whether it is in the revolving period, the controlled accumulation period or the early amortization period.

· Revolving Period. The revolving period for the series starts on the closing date and ends when the controlled accumulation

period or the early amortization period starts. During the revolving period, no principal will be paid to or accumulated for the series. Instead, principal collections allocated to the series will be (1) used to pay principal and make deposits for other series in principal sharing group one, (2) deposited in the excess funding account and (3) paid to the depositors.

· Controlled Accumulation Period. The controlled accumulation period for the series is scheduled to start _______, 20__, but may start at a later date. On each payment date during the controlled accumulation period, principal collections allocated to the series will be deposited in the principal funding account up to the controlled accumulation amount. Any remaining principal collections will be (1) used to pay principal and make deposits for other series in principal sharing group one, (2) deposited in the excess funding account and (3) paid to the depositors. On the expected final payment date, the amounts in the principal funding account will be paid to the Series 20__-__ noteholders sequentially by class.

An accumulation period reserve account will be established to provide additional funds to pay interest on the notes during the controlled accumulation period. The accumulation period reserve account will be funded before the start of the controlled accumulation period from interest collections allocated to the series. The amount required to be in the accumulation period reserve account will be $_________, which is __% of the initial note balance of the series.

· Early Amortization Period. If an amortization event occurs, the early amortization period will start. On each payment date during the early amortization period, (1) principal collections allocated to the series and (2) collections allocated to the portion of the depositor interest that is subordinated to the series (in the case of principal collections, in an amount not to exceed the available subordinated amount) will be paid to the Series 20__-__ noteholders sequentially by class.

For more details about the application of principal collections, you should read

“Description of the Notes — Application of Investor Collections — Payment of Principal.”

Amortization Events

If the events described below occur, an early amortization period will start.

The following “series amortization events” only apply to Series 20__-__:

· either depositor fails to make a payment or deposit required under the sale and servicing agreement within five business days,

· either depositor fails to observe or perform a covenant or agreement in a material respect or its representations are incorrect in a material respect, and the breach is not corrected within 60 days after the depositor receives notice of the breach, and the breach continues to adversely affect the amount or timing of payments to be made to the Series 20__-__ noteholders for that period,

· a servicer termination event occurs that adversely affects the amount or timing of payments to be made to the Series 20__-__ noteholders,

· the notes are not paid in full on their expected final payment date,

· the average monthly payment rate on the receivables for three consecutive months is less than __%,

· the available subordinated amount falls below the required subordinated amount for five business days,

· the amount in the excess funding account exceeds __% of the sum of the adjusted invested amounts of all series issued by the trust for three consecutive months, and

· the notes are accelerated after an event of default.

The following “trust amortization events” apply to all series:

· either depositor fails to designate additional eligible accounts to the trust to maintain the pool balance at required levels,

· a bankruptcy or dissolution of a depositor, Ford Credit or Ford, and

· the trust becomes subject to regulation as an “investment company” within the meaning of the Investment Company Act of 1940.

For more details about the amortization events, you should read “Description of the Notes — Amortization Events.”

Events of Default

Each of the following will be an “event of default” under the indenture:

· the trust fails to pay interest due on any note within 35 days after a payment date,

· the trust fails to pay the principal amount of any note in full by its final maturity date,

· the trust fails to observe or perform a material covenant or agreement or breaches a representation in any material respect that is not corrected within a 60-day cure period, and

· a bankruptcy or dissolution of the trust.

· If an event of default occurs, other than because of a bankruptcy or dissolution of the trust, the indenture trustee or a majority of Series 20__-__ may accelerate the Series 20__-__ notes and declare them immediately due and payable. If an event of default occurs because of a bankruptcy or dissolution of the trust, the Series 20__-__ notes will be accelerated automatically.

For more details about events of default, acceleration of the notes and other remedies available to noteholders after an event of default, you should read “Description of the Notes — Events of Default and Acceleration.”

Credit Enhancement

Credit enhancement provides protection for the Series 20__-__ notes against losses on the

receivables and potential shortfalls in the funds available to the trust to make required payments. If the credit enhancement is not sufficient to cover all amounts payable on the series, the losses will be allocated first, to the Class D notes, second, to the Class C notes, third, to the Class B notes, and fourth, to the Class A notes.

The enhancement described below is available only to Series 20__-__. The series is not entitled to enhancement available to another series.

Reserve Account

On the closing date, the trust will deposit $_________ in the reserve account, which is __% of the initial note balance of the series. If the depositors elect to increase the amount required to be in the reserve account during a subordination step-up period or an amortization event occurs, the amount required to be in the reserve account will increase. Funds in the reserve account will be available to pay interest on the notes, senior fees and expenses for the series and to cover defaulted receivables if interest collections allocated to the series are insufficient.

Subordination of Notes

The trust will pay interest to [all classes of] the Class A notes and then will pay interest sequentially to the remaining classes of notes in order of seniority. The trust will not pay interest on the Class B, Class C or Class D notes until all interest due on the Class A notes is paid in full.

The trust will pay principal sequentially to each class of notes in order of seniority. The trust will not pay the principal of any class of notes until the principal amounts of more senior classes of notes are paid in full.

Subordination of the Depositor Interest

A portion of the depositor interest, or the “available subordinated amount,” is subordinated to the series. The amount subordinated will initially equal $_____________, which is approximately __% of the initial note balance, plus any incremental subordinated amount for the first determination date. The available subordinated amount will

increase during a subordination step-up period, unless the depositors elect to increase the amount required to be in the reserve account during that period, and is subject to other reductions and increases from time to time.

Excess Spread

Excess spread for this series is the excess of interest collections allocated to the series over the interest payments on the notes and the senior fees and expenses of the trust that are allocated to the series. Any excess spread for this series will be available on each payment date to cover shortfalls in certain items in the priority of payments, including to offset losses on any defaulted receivables allocated to the series and to make required deposits in the reserve account.

For more information about the credit enhancement for the series, you should read “Credit Enhancement.”

Repurchases of Receivables

Ford Credit will make representations about the origination, characteristics and terms of each account and receivable. If a representation is later determined to be untrue, the receivable was not eligible to be sold to the depositor or the trust. If the breach of a representation has a material adverse effect on a receivable, the depositor must accept reassignment of the receivables from the trust and Ford Credit must repurchase the receivable from the depositor unless the breach is corrected before that date.

For more details about the representations made about the accounts and receivables and Ford Credit’s repurchase obligation if these representations are breached, you should read “Trust Property — Representations About Receivables” and “— Obligation to Repurchase Receivables”. For more information about when the asset representations reviewer may review certain accounts and receivables for compliance with the representations, you should read “Trust Property — Asset Representations Review.”

Sharing Groups

Series 20__-__ will be included in “excess interest sharing group one” and in “principal sharing group one.” As part of these groups, Series 20__-__ will be entitled in certain

situations to share in excess interest collections and shared principal collections from other series in the same group.

For more information about these groups, you should read “Description of the Notes — Groups.”

Other Series

The trust has issued other series of notes which are secured by the trust property. Annex A summarizes the main terms of each series issued by the trust.

Ratings

The depositors expect that the offered notes will receive credit ratings from two nationally recognized statistical rating organizations, or “rating agencies.” The sponsor has also hired nationally recognized statistical rating organizations to rate the notes of other series issued by the trust, who are also referred to as “rating agencies” when referring to ratings of other series.

The ratings of the offered notes reflect the likelihood of the timely payment of interest on, and the ultimate payment of principal of, the offered notes according to their terms. Each rating agency rating the offered notes will monitor the ratings under its normal surveillance process. Ford Credit has agreed to provide ongoing information about the offered notes and the receivables to each rating agency. A rating agency may change or withdraw an assigned rating at any time. A rating action taken by one rating agency may not necessarily be taken by another rating agency. No transaction party will be responsible for monitoring any changes to the ratings on the offered notes.

Tax Status

If you purchase a note, you agree by your purchase that you will treat your note as debt for U.S. federal, state and local income and franchise tax purposes.

Katten Muchin Rosenman LLP will deliver its opinion that, for U.S. federal income tax purposes:

· the offered notes will be treated as debt to the extent the offered notes are treated as beneficially owned by a person other than the sponsor or its affiliates for such purposes, and

· the trust will not be classified as an association or publicly traded partnership taxable as a corporation.

For more information about the application of U.S. federal, state and local tax laws, you should read “Tax Considerations.”

ERISA Considerations

The offered notes generally will be eligible for purchase by employee benefit plans.

For more information about the treatment of the notes under ERISA, you should read “ERISA Considerations.”

Credit Risk Retention

The risk retention regulations in Regulation RR of the Securities Exchange Act of 1934 applicable to revolving pool securitizations require the sponsor, either directly or through its wholly-owned affiliates, to retain an economic interest of at least 5% in the credit risk of the receivables. The sponsor will satisfy this requirement by causing the depositors to retain a “seller’s interest” of not less than 5% of the principal amount of the notes of each series, including this series.

For more information about the manner in which the risk retention requirements will be satisfied, you should read “Credit Risk Retention.”

[EEA Credit Risk Retention

Legislation in the European Economic Area, or “EEA,” permits some EEA-regulated entities to invest in securitizations only if a sponsor, originator or original lender for the securitization retains, on an ongoing basis, a material net economic interest of not less than 5% of the nominal amount of the securitized exposures. Ford Credit, as originator for this purpose, will retain, on a consolidated basis with the depositors, the depositor interest, which meets these requirements.

In addition, the legislation imposes due diligence and ongoing monitoring obligations on the affected investors for the securitization transaction and the securitized exposures. Affected investors are solely responsible for compliance with these additional obligations.

For more information about the risk retention requirements of the EEA, you should read “EEA Credit Risk Retention.”]

Investment Considerations

The trust is not registered or required to be registered as an “investment company” under the Investment Company Act of 1940 and, in making this determination, is relying on the exemption in [Rule 3a-7] of the Investment Company Act of 1940, although other exclusions or exemptions may also be available to the trust. The trust is structured not to be a “covered fund” under the regulations adopted to implement Section 619 of the Dodd-Frank Wall Street Reform and Consumer Protection Act, commonly known as the Volcker Rule.

Contact Information for the Depositors

Ford Credit Floorplan Corporation or

Ford Credit Floorplan LLC

c/o Ford Motor Credit Company LLC

c/o Ford Motor Company

World Headquarters, Suite 805-A4

One American Road

Dearborn, Michigan 48126

Attention: Ford Credit SPE Management Office

Telephone number: (313) 594-3495

Email address: FSPEMgt@ford.com

Contact Information for the Servicer

Ford Motor Credit Company LLC

c/o Ford Motor Company

World Headquarters, Suite 805-A4

One American Road

Dearborn, Michigan 48126

Attention: Securitization Operations Supervisor

Telephone number: (313) 594-1540

Email address: FDSecops@ford.com

Website: www.fordcredit.com

CUSIP Numbers

|

|

|

CUSIP |

|

Class A[-1] notes |

|

· |

|

[Class A-2 notes] |

|

· |

|

[Class B notes] |

|

· |

|

[Class C notes] |

|

· |

|

[Class D notes] |

|

· |

You should consider the following risk factors in deciding whether to purchase any notes.

|

The assets of the trust are limited and are the only source of payment for your notes |

|

The trust will not have assets or sources of funds other than the receivables and related property it owns. Credit enhancement is limited. Your notes will not be insured or guaranteed by Ford Credit or any of its affiliates or anyone else. If these assets or sources of funds are insufficient to pay your notes in full, you will incur losses on your notes. |

|

|

|

|

|

[The Class B, Class C and Class D notes will be subject to greater risk because of subordination |

|

The Class B notes will bear greater risk than the Class A notes because no interest will be paid on the Class B notes on any payment date until all interest on the Class A notes is paid in full on that payment date, and no principal will be paid on the Class B notes until the principal amount of the Class A notes is paid in full. The Class C and Class D notes will bear even greater risk because of similar subordination to more senior classes of notes.] |

|

|

|

|

|

A decline in the sale of dealer vehicle inventory or a decline in dealer vehicle inventory levels may result in accelerated, reduced or delayed payments on your notes |

|

The willingness of dealers to purchase new vehicle inventory depends to a large extent on their ability to sell their existing vehicle inventory. The ability of dealers to sell their vehicle inventory is directly affected by a variety of economic, market and social factors, including competition in the automobile industry, which factors will also ultimately affect the size of Ford Credit’s dealer floorplan portfolio. Examples of factors which may negatively impact the ability of dealers to sell vehicle inventory and vehicle inventory levels are: |

|

|

|

|

|

|

|

· a decline in the manufacture and sale of Ford vehicles due to an economic downturn, a labor disruption, competitive pressure, changes in the preferences of buyers of cars, trucks and utility vehicles, or production interruptions due to vehicle recalls, supply chain disruptions, natural disasters or other factors, |

|

|

|

|

|

|

|

· a change in (or a change in consumer perception of) the quality, safety, reliability or performance of Ford vehicles, |

|

|

|

|

|

|

|

· a change in Ford’s vehicle marketing or purchase incentive programs, |

|

|

|

|

|

|

|

· seasonal fluctuations in the sale of vehicles, |

|

|

|

|

|

|

|

· a change in the number of dealer franchises, |

|

|

|

|

|

|

|

· changes in the terms offered by Ford Credit to dealers to finance their vehicle inventory, including the interest rates charged or the sizes of the credit lines, |

|

|

|

|

|

|

|

· competition from banks or other financing sources available to dealers, |

|

|

|

|

|

|

|

· government or regulatory investigations or other actions relating to safety, emissions or fuel efficiency, including actions that encourage consumers to purchase certain types of vehicles, or |

|

|

|

· significant vehicle recalls, including recalls resulting from government or regulatory investigations or other actions, which will have a greater impact if they apply to vehicle models that represent a higher percentage of the pool balance. |

|

|

|

|

|

|

|

The rate of dealer vehicle sales, the level of dealer vehicle inventory and the size of Ford Credit’s dealer floorplan portfolio may change over time. A significant reduction in the rate of dealer vehicle sales or in the level of dealer vehicle inventory, and any resulting decline in the size of Ford Credit’s dealer floorplan portfolio, could lead to an amortization event and may also adversely impact the amount of principal collections on the receivables, which may result in accelerated, reduced or delayed payments on your notes. |

|

|

|

|

|

Economic, market and social factors could lead to slower sales of the vehicles, which may result in accelerated, reduced or delayed payments on your notes |

|

Payment of the receivables depends primarily on the rate of financed vehicle sales by the dealers. The rate of financed vehicle sales may change because of a variety of economic, market and social factors. Economic factors include interest rates, unemployment levels, the rate of inflation, the price of gasoline, the price of commodities used in the production of vehicles and consumer perception of general economic conditions. Ford’s discretionary use of incentive programs, including manufacturers’ rebate programs and low-interest rate financing, may also affect the rate of financed vehicle sales. Various market factors, including the introduction or increased promotion by other manufacturers of competitive models offering perceived advantages in performance, quality, reliability and fuel economy, may reduce sales of Ford vehicles. Social factors include consumer perception of Ford-branded products in the marketplace, including the effects of any significant vehicle recalls, changes in consumer demand for certain vehicle segments, consumer demand for vehicles generally and government actions, including actions that encourage consumers to purchase certain types of vehicles. |

|

|

|

|

|

|

|

We cannot predict whether or to what extent economic, market or social factors will affect the level of sales. A prolonged decline in the level of sales could lead to an amortization event and may also adversely impact the amount of principal collections on the receivables, which may result in accelerated, reduced or delayed payments on your notes. |

|

|

|

|

|

High vehicle model or vehicle type concentrations may adversely affect the performance of the receivables and your notes |

|

If a specific vehicle model or vehicle type of the financed vehicles represents a significant percentage of the pool balance, any adverse change in the rate of sales for that specific vehicle model or vehicle type of the financed vehicles may adversely impact the performance of the receivables and could result in reductions and delayed payments on the receivables and cause accelerated, reduced or delayed payments on your notes.

For more information about the rate of vehicle sales, you should read “Risk Factors — A decline in the sale of dealer vehicle inventory or a decline in dealer vehicle inventory levels may result in accelerated, reduced or delayed payments on your notes” and “Risk Factors — Economic, market and social factors could lead to slower sales of the vehicles, which may result in accelerated, reduced or delayed payments on your notes.” |

|

|

|

On _______, 20__, the following vehicle models of the financed vehicles related to the receivables in the pool balance represented 5% or more of the pool balance: [___], [___], and [___] |

|

|

|

|

|

A decrease in the dealer payment rate may result in accelerated, reduced or delayed payments on your notes |

|

The payment of principal of your notes will depend primarily on dealer payments of the receivables. Dealers are generally required to pay a receivable on the sale of the financed vehicle. The timing of these sales is uncertain, and particular patterns of dealer payments may or may not occur. The actual amount of available investor principal collections will depend on factors such as the rate of payment and the rate of default by dealers. Any significant decline in the dealer payment rate on the receivables during the controlled accumulation period or the early amortization period for your notes may result in reduced or delayed payments on your notes. Alternatively, if the average monthly payment rate for three consecutive months is less than __%, an amortization event will occur, which may result in accelerated payments on your notes. |

|

|

|

|

|

An increase in the dealer payment rate and/or a decrease in the origination of new receivables may result in accelerated payments on your notes |

|

If the dealer payment rate during the revolving period significantly exceeds the rate at which new receivables are originated — which could occur as a result of an increase in the rate of sales of financed vehicles, including increases resulting from manufacturer incentive programs or government actions that encourage consumers to purchase vehicles, or a decrease in the origination of new receivables, or both — principal collections otherwise payable to the depositors may be accumulated in the excess funding account to maintain the net adjusted pool balance at a stated level. However, if the amount in the excess funding account exceeds __% of the sum of the adjusted invested amounts of all series issued by the trust for three consecutive months, an amortization event will occur, which may result in accelerated payments on your notes. |

|

|

|

|

|

A decline in the financial condition or business prospects of Ford, Ford Credit or Ford-franchised dealers may result in losses on your notes |

|

The receivables owned by the trust are originated primarily through the financing provided by Ford Credit to Ford-franchised dealers for their dealer vehicle inventory. The level of dealer vehicle inventory and the size of Ford Credit’s dealer floorplan portfolio depend on Ford’s continuing ability to manufacture vehicles and to maintain franchise dealer relationships, on Ford Credit’s ability to provide financing and on the amount of vehicle inventory that Ford-franchised dealers are willing to hold, and the amount of principal collections on these receivables will depend on the dealers’ ability to sell these vehicles. The ability of Ford, Ford Credit and Ford-franchised dealers to compete in their industry environments will affect the amount of new receivables that are originated and the dealers’ ability to sell vehicles, which ultimately will affect the amount of principal collections and the payment rates on the receivables. A decline in the financial condition or business prospects of Ford, Ford Credit or Ford-franchised dealers could have an adverse effect on these factors, which may result in losses on your notes. |

|

|

|

|

|

|

|

If an economic downturn occurs, the financial condition and business prospects of the participants in the U.S. auto industry, including Ford, Ford Credit and Ford-franchised dealers, could be adversely affected. A decline in the financial condition or business prospects of Ford could also have an adverse effect on Ford Credit and Ford-franchised dealers. |

|

|

|

An economic downturn or a decline in the financial condition or business prospects of Ford could adversely affect Ford-franchised dealers’ ability to sell vehicles, the level of consumer demand for Ford-vehicles, the market value of the vehicles securing the receivables, and the ability of Ford Credit, as servicer, to service the receivables or honor its commitment to repurchase receivables due to breaches of representations, which may result in losses on your notes. |

|

|

|

|

|

|

|

For additional sources of information about Ford and Ford Credit, you should read “Where You Can Find More Information.” |

|

|

|

|

|

Increased losses may result in accelerated, reduced or delayed payments on your notes |

|

Historical losses experienced by the trust or by Ford Credit on its dealer floorplan portfolio may not indicate future performance of the trust’s receivables. Losses could increase significantly for a variety of economic, market or social factors, including adverse changes in the local, regional or national economies, adverse changes in the business prospects of Ford or Ford Credit or decreases in the market value of the financed vehicles in the absence of manufacturer incentives, dealer fraud or due to other events, such as significant vehicle recalls. A significant increase in losses on the receivables may result in accelerated, reduced or delayed payments on your notes. |

|

|

|

|

|

|

|

For more information about the performance of Ford Credit’s dealer floorplan portfolio, you should read “Sponsor and Servicer — Dealer Floorplan Portfolio Performance.” |

|

|

|

|

|

Amortization events may result in accelerated payments on your notes |

|

If an amortization event occurs, principal of your notes may be paid earlier than expected. If interest rates at that time are lower than interest rates at the time principal would have been paid on your notes had an amortization event not occurred, you may not be able to reinvest the principal at a rate of return that is equal to or greater than the rate of return on your notes. |

|

|

|

|

|

|

|

For more information about amortization events, you should read “Description of the Notes — Amortization Events.” |

|

|

|

|

|

Bankruptcy of Ford Credit may result in delayed payments or losses on your notes |

|

If Ford Credit becomes subject to a bankruptcy proceeding, you may have delayed payments or losses on your notes. A bankruptcy court could conclude that Ford Credit effectively still owns the receivables because the transfer of the receivables to the depositors was viewed as a financing and not a “true sale” or that the assets and liabilities of either or both of the depositors should be consolidated with those of Ford Credit for bankruptcy purposes. If a court were to reach either conclusion, you may have delayed payments or losses on your notes due to: |

|

|

|

|

|

|

|

· the “automatic stay” of the U.S. federal bankruptcy laws that prevents secured creditors from exercising remedies against a debtor in bankruptcy without permission from the bankruptcy court and other U.S. federal bankruptcy laws that permit substitution of collateral in limited circumstances, |

|

|

|

· tax or government liens on Ford Credit’s property that were existing before the transfer of the receivables to the trust having a claim on collections that is senior to your notes, or |

|

|

|

|

|

|

|

· the trust not having a perfected security interest in the financed vehicles or any cash collections held by Ford Credit at the time the bankruptcy proceeding starts. |

|

|

|

|

|

|

|

If a court were to decide that the transfer was not a “true sale” or that either or both of the depositors should be consolidated with Ford Credit for bankruptcy purposes, the trust would have a security interest in the receivables but the receivables would be owned by Ford Credit and payments may be delayed, collateral substituted or other remedies may be imposed by the bankruptcy court that may cause delayed payments or losses on your notes. |

|

|

|

|

|

|

|

Any bankruptcy proceeding involving Ford Credit may also adversely affect the rights and remedies of the trust and payments on your notes in other ways, whether or not the transfer of the receivables is considered a “true sale” or either or both depositors are consolidated with Ford Credit for bankruptcy purposes. For example: |

|

|

|

|

|

|

|

· as noted above, the “automatic stay” may prevent the exercise by the trust and others of their rights and remedies against Ford Credit and others, including the right to replace Ford Credit as servicer or the right to require it to repurchase receivables based on a breach of a representation, and/or |

|

|

|

|

|

|

|

· Ford Credit may be permitted to reject some agreements to which it is a party, including the sale and servicing agreements, and not be required to perform its obligations under those agreements. |

|

|

|

|

|

|

|

For more information about the effects of a bankruptcy of Ford Credit on your notes, you should read “Important Legal Considerations — Bankruptcy Considerations.” |

|

|

|

|

|

Ford’s failure to pay adjustment fees or to pay amounts relating to third-party financed in-transit receivables may result in delayed payments or losses on your notes |

|

Ford is obligated to pay adjustment fees to the servicer for any in-transit receivables held by the trust and to pay to the servicer principal collections that it receives on behalf of the dealers from any third-party finance sources relating to in-transit receivables. Each adjustment fee will be calculated based on an agreed on rate and the number of days during the “in-transit period,” which is generally the period from shipment to delivery of the vehicle, and will be treated as interest collections. Failure by Ford to pay adjustment fees or to pay principal collections relating to third-party financed in-transit receivables for any reason may result in shortfalls in amounts available to pay your notes and may result in delayed payments or losses on your notes. |

|

The termination of dealer financial assistance or failure to honor repurchase obligations by Ford may result in losses on your notes |

|

Ford has on occasion in the past provided discretionary financial assistance to dealers and limited commitments to repurchase vehicles and parts from the dealer’s inventory in connection with the termination of that dealer’s franchise. This financial assistance includes incentive programs, marketing support programs, interest reimbursement programs and purchase of new, current model year vehicles in the dealer’s inventory for the termination of a dealership. If Ford were unable to provide, or elected to terminate, this financial assistance or failed to honor its repurchase commitment for any reason, losses on the receivables could increase and you may incur losses on your notes. |

|

|

|

|

|

|

|

For more information about the financial assistance provided by Ford, you should read “Sponsor and Servicer — Servicing and Dealer Relations — Manufacturer Financial Assistance Programs for Dealers.” |

|

|

|

|

|

[The interest rates on the receivables may fluctuate differently than the interest rates on the notes, which may result in accelerated, reduced or delayed payments on your notes |

|

The receivables bear interest at a variable rate based on the prime rate, which may be changed or reduced by Ford Credit. The fixed rate notes accrue interest at a fixed rate, so if the interest rate on the receivables declines the notes may be adversely affected. The floating rate notes accrue interest at a variable rate based on one-month LIBOR, so if LIBOR increases at a greater rate than the prime rate or the prime rate declines at a greater rate than LIBOR the notes may be adversely affected. If the interest rate on the receivables declines, interest collections allocated to the notes may be reduced without a corresponding reduction in the amounts payable as interest on the notes. If interest collections are insufficient to pay interest on the notes, an amortization event will occur, which may result in accelerated, reduced or delayed payments on your notes. The trust is not entering into interest rate hedge agreements to protect either the fixed rate notes or the floating rate notes against fluctuations in the interest rate on the receivables.] |

|

|

|

|

|

[Negative LIBOR rates will reduce the rate of interest on the Class A[-1, A-2, Class B, Class C and Class D] notes. |

|

The interest rate on the Class A[-1, A-2, Class B, Class C and Class D] notes will be one-month LIBOR plus a spread. Changes in LIBOR will affect the interest rate and the amount of interest paid on the Class A[-1, A-2, Class B, Class C and Class D] notes. If LIBOR decreases below 0.00% for any interest period, the interest rate for that period, including the spread, will be reduced by the amount LIBOR is negative, but not below 0.00%.] |

|

|

|

|

|

[Uncertainty about the future of LIBOR and the potential discontinuance of LIBOR could adversely affect the market value of the Class A[-1, A-2, Class B, Class C and Class D] notes and/or limit your ability to resell them |

|

The chief executive of the United Kingdom Financial Conduct Authority, or the “FCA”, which regulates LIBOR, announced in July 2017 that the FCA intends to stop compelling banks to submit rates for the calculation of LIBOR after 2021. It is unknown whether any banks will continue to voluntarily submit rates for the calculation of LIBOR after 2021 or whether LIBOR will continue to be published by its administrator based on these submissions or on any other basis. It is not possible to predict the effect of these changes, other reforms or the establishment of alternative reference rates in the United States, United Kingdom or elsewhere. The resulting uncertainty could adversely affect the market value of the Class A[-1, A-2, Class B, Class C and Class D] notes and/or limit your ability to resell them. |

|

|

|

The trust will issue Class A[-1, A-2, Class B, Class C and Class D] notes that will accrue interest based on one-month LIBOR plus a spread. If one-month LIBOR is still being published after 2021, that rate will be used as the benchmark rate for the Class A[-1, A-2, Class B, Class C and Class D] notes, although we cannot provide any assurances that that rate will be representative of market interest rates or consistent with previously published one-month LIBOR. If a published one-month LIBOR is unavailable after 2021, the rate of interest on the Class A[-1, A-2, Class B, Class C and Class D] notes will be determined using the alternative methods stated in “Description of the Notes — Payments of Interest.” These alternative methods may result in lower interest payments or interest payments that do not otherwise correlate over time with payments that would have been made if one-month LIBOR were available in its current form. The alternative methods may also be subject to factors that make one-month LIBOR impossible or impracticable to determine. If a published one-month LIBOR is unavailable and banks are unwilling to provide quotations, the rate of interest on each Class A[-1, A-2, Class B, Class C and Class D] note for an interest period will be the same as the immediately preceding interest period, and could remain the rate of interest for the life of the Class A[-1, A-2, Class B, Class C and Class D] notes.] |

|

|

|

|

|

Ford Credit’s ability to change the terms of the receivables may result in accelerated, reduced or delayed payments on your notes |

|

Ford Credit continues to own the accounts in which the receivables are originated. As the owner of the accounts, Ford Credit may change the terms of the receivables, including the interest rates or adjustment fees and the payment terms. Ford Credit’s ability to change the terms of the receivables may result in accelerated, reduced or delayed payments on your notes. |

|

|

|

|

|

The addition or removal of receivables may decrease the credit quality of the trust property securing your notes and may result in accelerated, reduced or delayed payments on your notes |

|

The receivables in the trust will change every day. The depositors may choose, or be obligated, to sell to the trust receivables originated in additional designated accounts. While each additional designated account must be an eligible account at the time of its designation to the trust, additional designated accounts may not be of the same credit quality as the accounts currently designated to the trust and may have different terms. The depositors may also choose to redesignate accounts from the trust and remove the related receivables. If the addition or removal of receivables reduces the credit quality of the trust property, it may increase the likelihood of accelerated, reduced or delayed payments on your notes. |

|

|

|

|

|

The depositors may change certain requirements for the trust and the notes without the consent of any noteholder or other person, which may result in reduced or delayed payments on your notes |

|

The depositors may change the overconcentration definitions and/or increase or reduce the reserve account required amount for your notes. The depositors can make these changes so long as the rating agency condition has been satisfied for each rating agency then rating your series. If the depositors make any of these changes, it may result in reduced or delayed payments on your notes. |

|

Issuance of additional series by the trust may affect the timing and amounts of the payments on your notes |

|

The trust may issue additional series from time to time without your consent. The terms of a new series may be different from your series, which may affect the timing and amounts of payments on other series. For instance, different expected final payment dates and series early amortization events may cause some series to amortize earlier than your series. In addition, because some actions require the consent of a majority of each series, additional series may dilute the voting rights of your notes. The interests of the holders of a new series may be different from your interests. |

|

|

|

|

|

You may not receive your principal on the expected final payment date because of other series being in or entering into an accumulation or amortization period |

|

If your series were to enter the controlled accumulation period or the early amortization period while another series in principal sharing group one is either in an accumulation or amortization period or entering an accumulation or amortization period, available investor principal collections from that series may not be available to make payments on your notes. Other series in principal sharing group one may have different terms, such as an earlier expected final payment date or different series early amortization events, that could cause the series to amortize earlier than your series. As a result, the principal payments on your notes may be reduced and final payment of the principal of your notes may be delayed. Also, the shorter the controlled accumulation period for the notes of your series, the greater the likelihood that payment in full of the notes of your series on the expected final payment date will depend on available investor principal collections from other series in principal sharing group one. |

|

|

|

|

|

Failure to pay principal of a note will not be an event of default until its final maturity date |

|