Use these links to rapidly review the document

TABLE OF CONTENTS

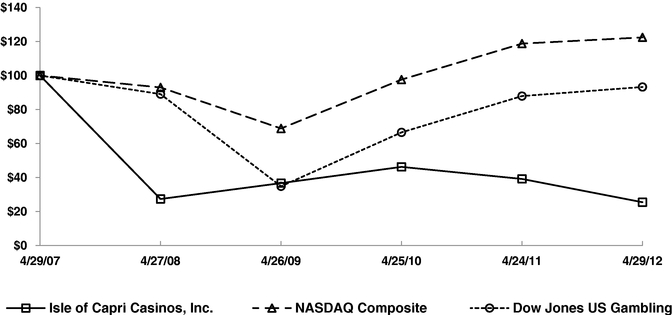

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | ||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended April 29, 2012 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission File Number 0-20538

ISLE OF CAPRI CASINOS, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

41-1659606 (I.R.S. Employer Identification Number) |

|

600 Emerson Road, Suite 300, St. Louis, Missouri (Address of principal executive offices) |

63141 (Zip Code) |

Registrant's telephone number, including area code: (314) 813-9200

Securities Registered Pursuant to Section 12(b) of the Act:

Common Stock, $.01 Par Value Per Share

(Title of Class)

Securities Registered Pursuant to Section 12(g) of the Act:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of the voting and non-voting stock held by non-affiliates(1) of the Company is $117,115,786, based on the last reported sale price of $5.19 per share on October 24, 2011 on the NASDAQ Stock Market; multiplied by 22,565,662 shares of Common Stock outstanding and held by non-affiliates of the Company on such date.

As of June 8, 2012, the Company had a total of 38,982,281 shares of Common Stock outstanding (which excludes 3,083,867 shares held by us in treasury).

Part III incorporates information by reference to the Registrant's definitive proxy statement to be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year.

- (1)

- Affiliates for the purpose of this item refer to the directors, named executive officers and/or persons owning 10% or more of the Company's common stock, both of record and beneficially; however, this determination does not constitute an admission of affiliate status for any of the individual stockholders.

ISLE OF CAPRI CASINOS, INC.

FORM 10-K

INDEX

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains statements that we believe are, or may be considered to be, "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact included in this Annual Report regarding the prospects of our industry or our prospects, plans, financial position or business strategy, may constitute forward-looking statements. In addition, forward-looking statements generally can be identified by the use of forward-looking words such as "may," "will," "expect," "intend," "estimate," "foresee," "project," "anticipate," "believe," "plans," "forecasts," "continue" or "could" or the negatives of these terms or variations of them or similar terms. Furthermore, such forward-looking statements may be included in various filings that we make with the SEC or press releases or oral statements made by or with the approval of one of our authorized executive officers. Although we believe that the expectations reflected in these forward-looking statements are reasonable, we cannot assure you that these expectations will prove to be correct. These forward-looking statements are subject to certain known and unknown risks and uncertainties, as well as assumptions that could cause actual results to differ materially from those reflected in these forward-looking statements. Factors that might cause actual results to differ include, but are not limited to, those discussed in the section entitled "Risk Factors" beginning on page 11 of this report. Readers are cautioned not to place undue reliance on any forward-looking statements contained herein, which reflect management's opinions only as of the date hereof. Except as required by law, we undertake no obligation to revise or publicly release the results of any revision to any forward-looking statements. You are advised, however, to consult any additional disclosures we make in our reports to the SEC. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained in this Annual Report.

1

Overview

We are a leading developer, owner and operator of regional gaming facilities and related dining, lodging and entertainment facilities in the United States. We currently own and operate 15 gaming and entertainment facilities in Louisiana, Mississippi, Missouri, Iowa, Colorado and Florida. Collectively, these properties feature approximately 14,000 slot machines and over 330 table games (including approximately 90 poker tables) over 3,000 hotel rooms and more than 45 restaurants. We also operate a harness racing track at our casino in Florida. Our portfolio of properties provides us with a diverse geographic footprint that minimizes geographically concentrated risks caused by weather, regional economic difficulties, gaming tax rates and regulations imposed by local gaming authorities.

We operate primarily under two brands, Isle and Lady Luck. Isle-branded facilities are generally in larger markets with a larger regional draw and offer expanded amenities, whereas Lady Luck-branded facilities are typically in smaller markets drawing primarily from a local customer base. Our senior management team has over 200 collective years of experience spanning 20 states, and multiple foreign jurisdictions. This team has established and executed against a strategic plan for growth focusing on three core principles, (1) refined fiscal discipline, (2) restyled customer experiences, and (3) a renewed asset base.

1. Refined Fiscal Discipline—We believe that our business benefits from a cost-effective approach to creating valuable customer experiences and a stronger balance sheet. We focus on fiscal discipline by utilizing technology and our customer research platform, responsibly reducing our cost structure and identifying opportunities for operating efficiencies at our properties.

Over the past four fiscal years, since current management joined the Company, we have reduced our debt by approximately $350 million, or 23%, and reduced our leverage ratio through the disciplined application of our free cash flow and a series of financing transactions including retiring approximately $143 million of debt through a tender offer for approximately $83 million, a $51 million equity offering, a senior notes offering and an extension of our senior secured credit facility. We plan to maintain this discipline through continued efforts to further reduce our overhead costs, achieving operating efficiencies by realigning our casino floors, and applying cost discipline in the evaluation and execution of future capital projects.

2. Restyled Customer Experiences—We focus on customer satisfaction and delivering superior guest experiences by providing popular gaming, dining and entertainment experiences that are designed to exceed customer expectations in a clean, safe, friendly and fun environment. We have introduced initiatives to increase customer time on device, refreshed several of our casino floors, and introduced an improved loyalty program, and have introduced several targeted non-gaming amenities.

These non-gaming amenities have included the development of several custom food, beverage and entertainment offerings, including the introduction of Lone Wolf bars and Otis and Henry's restaurants, a new buffet concept called Farmer's Pick, focused on locally-sourced, fresh food and a live entertainment series, Jester's Jam. In fiscal 2013, we expect to add additional Farmer's Pick Buffets, new Otis and Henry's restaurants and Lone Wolf bars across several of our properties, and to complete the introduction of our enhanced customer loyalty program, the Fan Club, at our remaining properties aimed to attract new customers and increase visitation.

3. Renewed Asset Base—We believe our long-term success will depend substantially upon increasing the quality, reach and scope of our operating portfolio, including new-build developments, acquisitions, rebranding projects and, where appropriate, asset sales. Recently we have renovated the

2

gaming floors at our Lake Charles, Louisiana and Black Hawk, Colorado properties. Currently we are in the process of renovating hotel rooms at each of these locations.

We have completed the Lady Luck rebranding of our facilities in Marquette, Iowa, Caruthersville, Missouri and one of our two facilities in Black Hawk, Colorado. We currently are rebranding Rainbow Casino in Vicksburg, Mississippi to a Lady Luck and expect to be completed by the end of the second quarter of fiscal 2013. We anticipate rebranding additional facilities in the future.

We were selected by regulatory agencies to develop an Isle-branded $135 million gaming and entertainment facility in Cape Girardeau, Missouri, as well as a Lady Luck-branded facility at Nemacolin Woodlands Resort in Fayette County, Pennsylvania. Subject to regulatory approval we anticipate opening our facility in Cape Girardeau by November 1, 2012. An appeal has been filed by one of the other applicants regarding the selection by the Pennsylvania Gaming Board to award a casino to the facility at Nemacolin Woodlands Resort. The appeal is under consideration by the Pennsylvania Supreme Court. No date has been determined for an expected ruling or the ultimate resolution of the matter. Following a successful resolution to the appeal and the receipt of any necessary regulatory or other approvals, we anticipate construction on the facility would take approximately nine months.

During fiscal 2012, we sold one of our two riverboat licenses in Lake Charles, Louisiana and entered into an agreement to sell our facility in Biloxi, Mississippi for approximately $45 million. We expect the sale of the Biloxi facility to close by the end of Summer 2012.

In addition to the items discussed above, we plan to continue to refresh our hotel room product, pursue third-party development partners for additional hotel and restaurant concepts, consider opportunistic monetization of non-core operating assets and renovate select facilities to improve our product offerings.

3

Casino Properties

The following is an overview of our existing casino properties as of April 29, 2012:

Property

|

Date Acquired or Opened |

Slot Machines |

Table Games |

Hotel Rooms |

Parking Spaces |

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Louisiana |

|||||||||||||||

Lake Charles |

July 1995 | 1,275 | 48 | 493 | 2,335 | ||||||||||

Mississippi |

|||||||||||||||

Lula |

March 2000 | 1,024 | 23 | 485 | 1,611 | ||||||||||

Natchez |

March 2000 | 583 | 9 | 141 | 645 | ||||||||||

Vicksburg |

June 2010 | 695 | 8 | — | 977 | ||||||||||

Missouri |

|||||||||||||||

Kansas City |

June 2000 | 1,081 | 20 | — | 1,715 | ||||||||||

Boonville |

December 2001 | 940 | 19 | 140 | 1,101 | ||||||||||

Caruthersville |

June 2007 | 595 | 16 | — | 1,000 | ||||||||||

Iowa |

|||||||||||||||

Bettendorf |

March 2000 | 988 | 22 | 514 | 2,057 | ||||||||||

Rhythm City—Davenport |

October 2000 | 931 | 14 | — | 911 | ||||||||||

Marquette |

March 2000 | 590 | 7 | — | 480 | ||||||||||

Waterloo |

June 2007 | 1,013 | 27 | 195 | 1,500 | ||||||||||

Colorado |

|||||||||||||||

Isle Casino Hotel-Black Hawk |

December 1998 | 957 | 31 | 238 | 1,100 | ||||||||||

Lady Luck Casino-Black Hawk |

April 2003 | 522 | 16 | 164 | 1,200 | ||||||||||

Florida |

|||||||||||||||

Pompano Park |

July 1995/April 2007 | 1,454 | 38 | — | 3,800 | ||||||||||

|

12,648 | 298 | 2,370 | 20,432 | |||||||||||

Assets Held for Sale |

|||||||||||||||

Biloxi, Mississippi |

August 1992 | 1,136 | 38 | 709 | 1,512 | ||||||||||

|

13,784 | 336 | 3,079 | 21,944 | |||||||||||

Louisiana

Lake Charles

Our Lake Charles property commenced operations in July 1995 and is located on a 19-acre site along Interstate 10, the main thoroughfare connecting Houston, Texas to Lake Charles, Louisiana. In February 2012 we consolidated our gaming operations onto one gaming vessel offering 1,275 slot machines, 48 table games, 8 poker tables, two hotels offering 493 rooms, a 105,000 square foot land-based pavilion and entertainment center, and 2,335 parking spaces, including approximately 1,400 spaces in an attached parking garage. The pavilion and entertainment center offer customers a wide variety of non-gaming amenities, including a 109-seat Otis & Henry's restaurant, a 290-seat Calypso's buffet, a 64-seat Lucky Wins Asian-inspired restaurant, which also includes a grab and go deli, and Caribbean Cove featuring free live entertainment and can accommodate 180 guests. The pavilion also has a 14,750 square foot entertainment center comprised of a 1,100-seat special events center designed for concerts, banquets and other events, meeting facilities and administrative offices.

The Lake Charles market currently consists of two dockside gaming facilities, a Native American casino and a pari-mutuel facility/racino. The current number of slot machines in the market is approximately 7,800 machines and table games are approximately 240 tables. In calendar year 2011, the two gaming facilities and one racino, in the aggregate, generated gaming revenues of approximately $673 million. Revenues for the Native American property are not published. Gaming revenues for our

4

Lake Charles property for calendar year 2011 were approximately $142 million. Lake Charles is the closest gaming market to the Houston metropolitan area, which has a population of approximately 5.5 million and is located approximately 140 miles west of Lake Charles. We believe that our Lake Charles property attracts customers primarily from southeast Texas, including Houston, Beaumont, Galveston, Orange and Port Arthur and from local area residents. Approximately 500,000 and 1.6 million people reside within 50 and 100 miles, respectively, of the Lake Charles property.

Mississippi

Lula

Our Lula property, which we acquired in March 2000, is strategically located off of Highway 49, the only road crossing the Mississippi River between Mississippi and Arkansas for more than 50 miles in either direction. The property consists of two dockside casinos containing 1,024 slot machines and 23 table games, two on-site hotels with a total of 485 rooms, a land-based pavilion and entertainment center, 1,611 parking spaces, and a 28-space RV Park. The pavilion and entertainment center offer a wide variety of non-gaming amenities, including a 122-seat Farraddays' restaurant, a 283-seat Calypso's buffet and a 35-seat Tradewinds Marketplace, and a gift shop.

Our Lula property is the only gaming facility in Coahoma County, Mississippi and generated net gaming revenues of approximately $56 million in calendar year 2011. Lula draws a significant amount of business from the Little Rock, Arkansas metropolitan area, which has a population of approximately 710,000 and is located approximately 120 miles west of the property. Coahoma County is also located approximately 60 miles southwest of Memphis, Tennessee, which is primarily served by nine casinos in Tunica County, Mississippi. Approximately 1.1 million people reside within 60 miles of the property. Lula also competes with Native American casinos in Oklahoma and a racino in West Memphis, Arkansas.

Natchez

Our Natchez property, which we acquired in March 2000, is located off of Highways 84 and 61 in western Mississippi. The property consists of a dockside casino offering 583 slot machines and 9 table games, a 141-room off-site hotel located approximately one mile from the casino, a 150-seat Calypso's buffet and 645 parking spaces.

Our Natchez property is currently the only gaming facility in the Natchez market and generated total gaming revenues of approximately $29 million in calendar year 2011. We believe that the Natchez property attracts customers primarily from among the approximately 350,000 people residing within 60 miles of the Natchez property.

Vicksburg

Our Vicksburg property, which we acquired in June 2010, is located off Interstate 20 and Highway 61 in western Mississippi, approximately 50 miles west of Jackson, Mississippi. The property consists of a dockside casino offering 695 slot machines and eight table games, a 224-seat Riverview Buffet, a 26-seat Crossroads Deli and 977 parking spaces.

The Vicksburg market consists of five dockside casinos which generated total gaming revenues of approximately $261 million in calendar year 2011. Our Vicksburg property generated gaming revenues of approximately $40 million in calendar year 2011. Approximately 700,000 people reside within 60 miles of the property.

5

Missouri

Kansas City

Our Kansas City property, which we acquired in June 2000, is the closest gaming facility to downtown Kansas City and consists of a dockside casino offering 1,081 slot machines and 20 table games, a 202-seat Calypso's buffet, a 176-seat Lone Wolf restaurant, a 32-seat Tradewinds Marketplace and 1,715 parking spaces.

The Kansas City market consists of four dockside gaming facilities, a land-based facility which opened in February 2012 and a Native American casino. Operating statistics for the Native American casino are not published. The four dockside gaming facilities generated gaming revenues of approximately $710 million in calendar year 2011. Our Kansas City property generated gaming revenues of approximately $85 million during calendar year 2011. We believe that our Kansas City casino attracts customers primarily from the Kansas City metropolitan area, which has approximately 1.9 million residents

Boonville

Our Boonville property, which opened in December 2001, is located three miles off Interstate 70, approximately halfway between Kansas City and St. Louis. The property consists of a single level dockside casino offering 940 slot machines, 19 table games, a 140-room hotel, a 32,400 square foot pavilion and entertainment center and 1,101 parking spaces. In February 2012 the Company launched a new branded restaurant within the Boonville property pavilion, The Farmer's Pick buffet. The newly renovated 201-seat restaurant features locally sourced food products that are prepared at action stations in view of the guests. In addition, the pavilion and entertainment center also offers customers a wide variety of other non-gaming amenities, including an 83-seat Farraddays' restaurant, a 36-seat Tradewinds Marketplace, an 800 seat event center, and a historic display area. Our Boonville property is the only gaming facility in central Missouri and generated gaming revenues of approximately $82 million in calendar year 2011. We believe that our Boonville casino attracts customers primarily from the approximately 580,000 people who reside within 60 miles of the property which includes the Columbia and Jefferson City areas.

Caruthersville

Our Caruthersville property was acquired in June 2007 and is a riverboat casino located along the Mississippi River in Southeast Missouri. The dockside casino offers 595 slot machines, 11 table games and 5 poker tables. The property offers a 40,000 square foot pavilion, which includes a 130-seat Lone Wolf restaurant, bar and lounge and a 270-seat Otis & Henry's restaurant. The property also operates a 10,000 square foot exposition center with seating for up to 1,100 patrons and has 1,000 parking spaces. Our Caruthersville facility is the only casino located in Southeast Missouri and generated gaming revenues of approximately $33 million in calendar year 2011. Approximately 650,000 people reside within 60 miles of the property.

Iowa

Bettendorf

Our Bettendorf property was acquired in March 2000 and is located off of Interstate 74, an interstate highway serving the Quad Cities metropolitan area, which consists of Bettendorf and Davenport, Iowa and Moline and Rock Island, Illinois. The property consists of a dockside casino offering 988 slot machines, 18 table games, 4 poker tables, 514 hotel rooms, 40,000 square feet of flexible convention/banquet space, a 120-seat Farraddays' restaurant, a 260-seat Calypso's buffet, a 24-seat Tradewinds Marketplace and 2,057 parking spaces. We have entered into agreements with the

6

City of Bettendorf, Iowa under which we manage and provide financial and operating support for the QC Waterfront Convention Center that is adjacent to our hotel. The QC Waterfront Convention Center opened in January 2009.

Davenport

Our Davenport property, which we acquired in October 2000, is located at the intersection of River Drive and Highway 61, a state highway serving the Quad Cities metropolitan area. The property consists of a dockside gaming facility offering 931 slot machines, 14 table games, a 209-seat Hit Parade buffet, a Grab-n-Go food outlet and 911 parking spaces.

The Quad Cities metropolitan area currently has three gaming operations—our two gaming facilities in Bettendorf and Davenport, and a larger land-based facility, including a hotel, which opened in December 2008. The three operations in the Quad Cities generated total gaming revenues of approximately $212 million in calendar year 2011. Our Bettendorf and Davenport properties generated casino revenues for calendar year 2011 of approximately $77 million and $49 million, respectively. Our operations in the Quad Cities also compete with other gaming operations in Illinois and Iowa. Approximately 923,000 people reside within 60 miles of our Bettendorf and Davenport properties.

Marquette

Our Marquette property, which we acquired in March 2000, is located in Marquette, Iowa, approximately 60 miles north of Dubuque, Iowa. The property consists of a dockside casino offering 590 slot machines and 7 table games, a marina and 480 parking spaces. The facility was rebranded as a Lady Luck casino in fiscal 2010 and includes a 142-seat buffet restaurant, a 15-seat Otis and Henry's Express food outlet and a 155-seat Lone Wolf restaurant and bar.

Our Marquette property is the only gaming facility in the Marquette, Iowa market and generated gaming revenues of approximately $30 million in calendar year 2011. We believe most of our Marquette customers are from northeast Iowa and Wisconsin, which includes approximately 490,000 people within 60 miles of our property, and we compete for those customers with other gaming facilities in Dubuque, Iowa and Native American casinos in southwestern Wisconsin.

Waterloo

Our Waterloo property opened on June 30, 2007 and is located adjacent to Highway 218 and US 20 in Waterloo, Iowa. The property consists of a single-level casino offering 1,013 slot machines, 23 table games and 4 poker tables. The property also offers a wide variety of non-gaming amenities, including a 118-seat Otis & Henry's restaurant, a 205-seat buffet, a 44-seat Tradewinds marketplace, Club Capri Lounge, Fling feature bar, 5,000 square feet of meeting space, 1,500 parking spaces and a 195-room hotel, which includes 27 suites, as well as an indoor pool and hot tub area.

Our Waterloo property is the only gaming facility in the Waterloo, Iowa market and approximately 640,000 people live within 60 miles of the property. We compete with other casinos in eastern Iowa. We generated gaming revenues of approximately $82 million in calendar year 2011.

Colorado

Isle Casino Hotel-Black Hawk

Isle Casino Hotel-Black Hawk commenced operations in December 1998, is located on an approximately 10-acre site and is one of the first gaming facilities reached by customers arriving from Denver via Highway 119, the main thoroughfare connecting Denver to Black Hawk. The property includes a land-based casino with 957 slot machines, 24 standard table games, a 7 table poker room, a 238-room hotel and 1,100 parking spaces in an attached parking garage. Isle Casino Hotel-Black Hawk

7

also offers customers three restaurants, including a 128-seat Farraddays' restaurant, a 270-seat Calypso's buffet and a 42-seat Tradewinds Marketplace.

Lady Luck Casino-Black Hawk

Lady Luck Casino-Black Hawk, which we acquired in April 2003 and rebranded in June 2009, is located across the intersection of Main Street and Mill Street from the Isle Casino Hotel-Black Hawk. The property consists of a land-based casino with 522 slot machines, 10 standard table games, 6 poker tables, a 164-room hotel that opened in December 2005 and 1,200 parking spaces in our parking structure connecting Isle Casino Hotel-Black Hawk and Lady Luck Casino-Black Hawk. The property also offers guests dining in a 93-seat Otis & Henry's restaurant as well as a grab-and-go fast serve food cart that is located in the main level of the facility. The property has also recently converted approximately 2,250 square feet of space to flex space that can be used for meetings and special events. Our Black Hawk sites are connected via sky bridges.

When casinos having multiple gaming licenses in the same building are combined, the Black Hawk/Central City market consists of 24 gaming facilities (seven of which have more than 600 slot machines), which in aggregate, generated gaming revenues of approximately $619 million in calendar year 2011. Our Black Hawk properties generated casino revenues for calendar year 2011 of approximately $127 million. Black Hawk is the closest gaming market to the Denver, Colorado metropolitan area, which has a population of approximately 2.9 million and is located approximately 40 miles east of Black Hawk and serves as the primary feeder market for Black Hawk.

Florida

Pompano

In 1995, we acquired Pompano Park, a harness racing track located in Pompano Beach, Florida. Pompano Park is located off of Interstate 95 and the Florida Turnpike on a 223-acre owned site, near Fort Lauderdale, midway between Miami and West Palm Beach. Pompano Park is the only racetrack licensed to conduct harness racing in Florida.

Our Pompano facility includes 1,454 slot machines, a 38-table poker room, a 120-seat Farradday's restaurant, a 110-seat Bragozzo's Italian restaurant, a 250-seat buffet, a 100-seat deli, a 60-seat casual restaurant, an express grab and go food outlet, a feature bar and 3,800 parking spaces.

Approximately 2.6 million people reside within a 25-mile radius of our Pompano facility, which competes with four other racinos and three Native American gaming facilities in the market. While casino revenues are not available for all market competitors, we estimate that we operate approximately 10% of the slot machines in the market and generated approximately $142 million in casino revenues for calendar year 2011.

Assets Held for Sale

Biloxi

Our Biloxi property, which commenced operations in August 1992, is located on a 17-acre site at the eastern end of a cluster of facilities formerly known as "Casino Row" in Biloxi, Mississippi, and is the first property reached by visitors coming from Alabama, Florida and Georgia via Highway 90.

Our Biloxi property offers approximately 1,200 slot machines, 27 table games, a nine-table poker room, a 709-room hotel including 200 whirlpool suites, a 120-seat banquet room called "Paradise Room," 138-seat Farraddays' restaurant, a 200-seat Calypso's buffet, a 128-seat Café at the Point restaurant, a 94-seat Tradewinds marketplace, a multi-story feature bar, a full service Starbucks and over 1,300 parking spaces.

8

The Mississippi Gulf Coast market (which includes Biloxi, Gulfport and Bay St. Louis) consists of 11 dockside gaming facilities, which in the aggregate, generated net gaming revenues of approximately $1.1 billion during calendar year 2011. Our Biloxi property generated net gaming revenues of approximately $57 million during calendar year 2011. Approximately one million people reside within 60 miles of the property.

In March 2012 we entered into an agreement to sell our Biloxi operation for approximately $45 million. The transaction is expected to close in fiscal 2013.

Marketing

Our marketing programs are designed to promote our overall business strategy of providing customers with a safe, clean, friendly and fun gaming experience at each of our properties. We have developed an extensive proprietary database of customers that allows us to create effective targeted marketing and promotional programs that are designed to reward customer loyalty, attract new customers to our properties and maintain high recognition of our brands.

Specifically, our marketing programs and initiatives are tailored to support this corporate strategic plan and are generally focused on the following areas:

- •

- Customer Research: Our marketing strategies have been

developed and implemented to meet the needs and desires of our casino customers in each of our locations. In order to assess these needs and desires, we engage in significant customer research in each

of our markets by conducting periodic surveys. Upon receipt of these surveys, we assess the attitudes of our customers and the customers of our competitors' properties towards the most important

attributes of their experience in a regional and/or local gaming facility. We use the extensive information gathered from these research initiatives to make marketing, operating and development

decisions that, we believe, will optimize the position of our properties relative to our competition.

- •

- Branding Initiatives: Our strategic plan is designed to

consolidate our property portfolio from four brands into two brands as the economy improves and we undertake significant new capital improvement programs. To date, our Lady Luck

re-branding initiative includes our properties in Caruthersville, Missouri and Marquette, Iowa. Additionally, we have converted Colorado Central Station in Black Hawk, Colorado to Lady

Luck-Black Hawk. In addition, we are currently rebranding our casino in Vicksburg, Mississippi to Lady Luck Casino Vicksburg, with expected completion by the end of the second quarter of

fiscal 2013. As a component of these re-branding programs, we have also implemented newly-branded customer outlets, including custom restaurants and lounges that we are expanding through

our portfolio to other properties. We believe, over time, this approach will allow us to more effectively align and promote our properties based upon customer needs and desires and market our

properties on a consolidated basis. Furthermore, we expect our approach will streamline the costs associated with marketing our portfolio.

- •

- Database Marketing: We have streamlined our database marketing initiatives across the Company in order to focus our marketing efforts on profitable customers who have demonstrated a willingness to regularly visit our properties. Specifically, we have focused on eliminating from our database customers who have historically been included in significant marketing efforts but have proven costly either as a result of excessive marketing expenditures on the part of the Company, or because these customers have become relatively dormant in terms of customer activity.

9

- •

- Fan Club: During fiscal 2012, we began implementation of a

new customer loyalty program, Fan Club, which allows customers greater choice in how to use their points for cash, free play or food. The five-tier program provides for clear customer understanding of

how points are earned, how points can be utilized and the benefits offered at each tier. Fan Club has been implemented at four of our properties to date and our goal is to have full implementation by

the end of fiscal 2013.

- •

- Segmentation: We have compiled an extensive database of

customer information over time. Among our most important marketing initiatives, we have introduced database segmentation to our properties and at the corporate level in order to adjust investment

rates to a level at which we expect to meet a reasonable level of customer profit contribution.

- •

- Retail Development: We believe that we must more effectively attract new, non-database customers to our properties in order to increase profitability and free cash flow. These customers are generally less expensive to attract and retain and, therefore, currently represent a significant opportunity for our operations.

Employees

As of April 29, 2012, we employed approximately 7,700 full and part-time people. We have a collective bargaining agreement with UNITE HERE covering approximately 450 employees at our Pompano property which was renewed in May 2012 and expires in May 2015. We believe that our relationship with our employees is satisfactory.

Governmental Regulations

The gaming and racing industries are highly regulated, and we must maintain our licenses and pay gaming taxes to continue our operations. Each of our facilities is subject to extensive regulation under the laws, rules and regulations of the jurisdiction where it is located. These laws, rules and regulations generally relate to the responsibility, financial stability and character of the owners, managers and persons with financial interests in the gaming operations. Violations of laws in one jurisdiction could result in disciplinary action in other jurisdictions. A more detailed description of the regulations to which we are subject is contained in Exhibit 99.1 to this Annual Report on Form 10-K.

Our businesses are subject to various federal, state and local laws and regulations in addition to gaming regulations. These laws and regulations include, but are not limited to, restrictions and conditions concerning alcoholic beverages, food service, smoking, environmental matters, employees and employment practices, currency transactions, taxation, zoning and building codes, and marketing and advertising. Such laws and regulations could change or could be interpreted differently in the future, or new laws and regulations could be enacted. Material changes, new laws or regulations, or material differences in interpretations by courts or governmental authorities could adversely affect our operating results.

Available Information

For more information about us, visit our web site at www.isleofcapricasinos.com. Our electronic filings with the U.S. Securities and Exchange Commission (including all annual reports on Form 10-K, quarter reports on Form 10-Q, and current reports on Form 8-K, and any amendments to these reports), including the exhibits, are available free of charge through our web site as soon as reasonably practicable after we electronically file them with or furnish them to the U.S. Securities and Exchange Commission.

10

We face significant competition from other gaming operations, including Native American gaming facilities, that could have a material adverse effect on our future operations.

The gaming industry is intensely competitive, and we face a high degree of competition in the markets in which we operate. We have numerous competitors, including land-based casinos, dockside casinos, riverboat casinos, casinos located on racing, pari-mutuel operations or Native American-owned lands and video lottery and poker machines not located in casinos. Some of our competitors may have better name recognition, marketing and financial resources than we do; competitors with more financial resources may therefore be able to improve the quality of, or expand, their gaming facilities in a way that we may be unable to match.

Legalized gaming is currently permitted in various forms throughout the United States. Certain states have recently legalized, and other states are currently considering legalizing gaming. Our existing gaming facilities compete directly with other gaming properties in the states in which we operate. Our existing casinos attract a significant number of their customers from Houston, Texas; Mobile, Alabama; Kansas City, Kansas; Southern Florida; Little Rock, Arkansas; and Denver, Colorado. Legalization of gaming in jurisdictions closer to these geographic markets other than the jurisdictions in which our facilities are located would have a material adverse effect on our operating results. Other jurisdictions, including states in close proximity to jurisdictions where we currently have operations, have considered and may consider legalizing casino gaming and other forms of competition. In addition, there is no limit on the number of gaming licenses that may be granted in several of the markets in which we operate. As a result, new gaming licenses could be awarded in these markets, which could allow new gaming operators to enter our markets that could have an adverse effect on our operating results. For example, on February 17, 2011, a project was awarded a gaming license in Lake Charles, Louisiana which, if completed, will compete with our existing Lake Charles property. A casino property, which could compete with our Natchez, Mississippi property, is currently under development.

Our continued success depends upon drawing customers from each of these geographic markets. We expect competition to increase as new gaming operators enter our markets, existing competitors expand their operations, gaming activities expand in existing jurisdictions and gaming is legalized in new jurisdictions. We cannot predict with any certainty the effects of existing and future competition on our operating results.

We also compete with other forms of legalized gaming and entertainment such as online computer gambling, bingo, pull tab games, card parlors, sports books, "cruise-to-nowhere" operations, pari-mutuel or telephonic betting on horse racing and dog racing, state-sponsored lotteries, jai-alai, and, in the future, may compete with gaming at other venues. In addition, we compete more generally with other forms of entertainment for the discretionary spending of our customers.

We are subject to extensive regulation from gaming and other regulatory authorities that could adversely affect us.

Licensing requirements. As owners and operators of gaming and pari-mutuel wagering facilities, we are subject to extensive state and local regulation. State and local authorities require us and our subsidiaries to demonstrate suitability to obtain and retain various licenses and require that we have registrations, permits and approvals to conduct gaming operations. The regulatory authorities in the jurisdictions in which we operate have very broad discretion with regard to their regulation of gaming operators, and may for a broad variety of reasons and in accordance with applicable laws, rules and regulations, limit, condition, suspend, fail to renew or revoke a license to conduct gaming operations or prevent us from owning the securities of any of our gaming subsidiaries, or prevent other persons from owning an interest in us or doing business with us. We may also be deemed responsible for the acts and conduct of our employees. Substantial fines or forfeiture of assets for violations of gaming laws or

11

regulations may be levied against us, our subsidiaries and the persons involved, and some regulatory authorities have the ability to require us to suspend our operations. The suspension or revocation of any of our licenses or our operations or the levy on us or our subsidiaries of a substantial fine would have a material adverse effect on our business.

To date, we have demonstrated suitability to obtain and have obtained all governmental licenses, registrations, permits and approvals necessary for us to operate our existing gaming facilities. We cannot assure you that we will be able to retain these licenses, registrations, permits and approvals or that we will be able to obtain any new ones in order to expand our business, or that our attempts to do so will be timely. Like all gaming operators in the jurisdictions in which we operate, we must periodically apply to renew our gaming licenses and have the suitability of certain of our directors, officers and employees approved. We cannot assure you that we will be able to obtain such renewals or approvals.

In addition, regulatory authorities in certain jurisdictions must approve, in advance, any restrictions on transfers of, agreements not to encumber or pledges of equity securities issued by a corporation that is registered as an intermediary company with such state, or that holds a gaming license. If these restrictions are not approved in advance, they will be invalid.

Compliance with other laws. We are also subject to a variety of other federal, state and local laws, rules, regulations and ordinances that apply to non-gaming businesses, including zoning, environmental, construction and land-use laws and regulations governing the serving of alcoholic beverages. Under various federal, state and local laws and regulations, an owner or operator of real property may be held liable for the costs of removal or remediation of certain hazardous or toxic substances or wastes located on its property, regardless of whether or not the present owner or operator knows of, or is responsible for, the presence of such substances or wastes. We have not identified any issues associated with our properties that could reasonably be expected to have a material adverse effect on us or the results of our operations. However, several of our properties are located in industrial areas or were used for industrial purposes for many years. As a consequence, it is possible that historical or neighboring activities have affected one or more of our properties and that, as a result, environmental issues could arise in the future, the precise nature of which we cannot now predict. The coverage and attendant compliance costs associated with these laws, regulations and ordinances may result in future additional costs.

Regulations adopted by the Financial Crimes Enforcement Network of the U.S. Treasury Department require us to report currency transactions in excess of $10,000 occurring within a gaming day, including identification of the patron by name and social security number. U.S. Treasury Department regulations also require us to report certain suspicious activity, including any transaction that exceeds $5,000 if we know, suspect or have reason to believe that the transaction involves funds from illegal activity or is designed to evade federal regulations or reporting requirements. Substantial penalties can be imposed against us if we fail to comply with these regulations.

Several of our riverboats must comply with U.S. Coast Guard requirements as to boat design, on-board facilities, equipment, personnel and safety and must hold U.S. Coast Guard Certificates of Documentation and Inspection. The U.S. Coast Guard requirements also set limits on the operation of the riverboats and mandate licensing of certain personnel involved with the operation of the riverboats. Loss of a riverboat's Certificate of Documentation and Inspection could preclude its use as a riverboat casino. The U.S. Coast Guard has shifted inspection duties related to permanently moored casino vessels to the individual states. Louisiana and Missouri have elected to utilize the services of the American Bureau of Shipping to undertake the inspections. Iowa has elected to handle the inspections through the Iowa Department of Natural Resources. The states will continue the same inspection criteria as the U.S. Coast Guard in regard to annual and five year inspections. Depending on the

12

outcome of these inspections a vessel could become subject to dry-docking for inspection of its hull, which could result in a temporary loss of service.

We are required to have third parties periodically inspect and certify all of our casino barges for stability and single compartment flooding integrity. Our casino barges and other facilities must also meet local fire safety standards. We would incur additional costs if any of our gaming facilities were not in compliance with one or more of these regulations.

Potential changes in legislation and regulation of our operations. From time to time, legislators and special interest groups have proposed legislation that would expand, restrict or prevent gaming operations in the jurisdictions in which we operate. In addition, from time to time, certain anti-gaming groups have challenged constitutional amendments or legislation that would limit our ability to continue to operate in those jurisdictions in which these constitutional amendments or legislation have been adopted.

Taxation and fees. State and local authorities raise a significant amount of revenue through taxes and fees on gaming activities. We believe that the prospect of significant revenue is one of the primary reasons that jurisdictions permit legalized gaming. As a result, gaming companies are typically subject to significant taxes and fees in addition to normal federal, state, local and provincial income taxes, and such taxes and fees are subject to increase at any time. We pay substantial taxes and fees with respect to our operations. From time to time, federal, state, local and provincial legislators and officials have proposed changes in tax laws, or in the administration of such laws, affecting the gaming industry. Any material increase, or the adoption of additional taxes or fees, could have a material adverse effect on our future financial results.

Effective July 1, 2011, the Colorado Limited Gaming Control Commission reduced all gaming tax tiers by 5%, which resulted in a reduction of the top rate tier from 20% to 19%. The Commission has announced that it plans to restore the rates to their previous levels effective July 1, 2012.

Our business may be adversely affected by legislation prohibiting tobacco smoking.

Legislation in various forms to ban indoor tobacco smoking has recently been enacted or introduced in many states and local jurisdictions, including several of the jurisdictions in which we operate. If additional restrictions on smoking are enacted in jurisdictions in which we operate, we could experience a significant decrease in gaming revenue and particularly, if such restrictions are not applicable to all competitive facilities in that gaming market, our business could be materially adversely affected.

Our substantial indebtedness could adversely affect our financial health and restrict our operations.

We have a significant amount of indebtedness. As of April 29, 2012, we had approximately $1.2 billion of total debt outstanding.

Our significant indebtedness could have important consequences to our financial health, such as:

- •

- limiting our ability to use operating cash flow or obtain additional financing to fund working capital, capital

expenditures, expansion and other important areas of our business because we must dedicate a significant portion of our cash flow to make principal and interest payments on our indebtedness;

- •

- causing an event of default if we fail to satisfy the financial and restrictive covenants contained in the indentures and agreements governing our senior secured credit facility, our 7.75% senior notes, our 7% senior subordinated notes and our other indebtedness, which could result in all of our debt becoming immediately due and payable, could permit our secured lenders to foreclose

13

- •

- if the indebtedness under our 7.75% senior notes, our 7% senior subordinated notes, our senior secured credit facility, or

our other indebtedness were to be accelerated, there can be no assurance that our assets would be sufficient to repay such indebtedness in full;

- •

- placing us at a competitive disadvantage to our competitors who are not as highly leveraged;

- •

- increasing our vulnerability to and limiting our ability to react to changing market conditions, changes in our industry

and economic downturns or downturns in our business; and

- •

- our agreements governing our indebtedness, among other things, require us to maintain certain specified financial ratios and to meet certain financial tests. Our debt agreements also limit our ability to:

on the assets securing our secured debt and have other adverse consequences, any of which, if not cured or waived, could have a material adverse effect on us;

i. borrow money;

ii. make capital expenditures;

iii. use assets as security in other transactions;

iv. make restricted payments or restricted investments;

v. incur contingent obligations; and

vi. sell assets and enter into leases and transactions with affiliates.

A substantial portion of our outstanding debt bears interest at variable rates, although we have entered into interest rate protection agreements expiring through fiscal 2014 with counterparty banks with respect to $150 million of our term loans under our senior secured credit facility. If short-term interest rates rise, our interest cost will increase on the unhedged portion of our variable rate indebtedness, which will adversely affect our results of operations and available cash.

Any of the factors listed above could have a material adverse effect on our business, financial condition and results of operations. We cannot assure you that our business will continue to generate sufficient cash flow, or that future available draws under our senior secured credit facility will be sufficient, to enable us to meet our liquidity needs, including those needed to service our indebtedness.

Despite our significant indebtedness, we may still be able to incur significantly more debt. This could intensify the risks described above.

The terms of the indentures and agreements governing our senior secured credit facility, our 7.75% senior notes, our 7% senior subordinated notes and our other indebtedness limit, but do not prohibit, us or our subsidiaries from incurring significant additional indebtedness in the future.

As of April 29, 2012, we had the capacity to incur additional indebtedness, including the ability to incur additional indebtedness under our line of credit, of approximately $258 million. Approximately $29 million of capacity of our senior secured credit facility was used to support letters of credit and surety bonds. Our capacity to issue additional indebtedness is subject to the limitations imposed by the covenants in our senior secured credit facility, the indenture governing our 7.75% senior notes and the indenture governing our 7% senior subordinated notes. The indenture governing our 7% senior subordinated notes, the indenture governing our 7.75% senior notes and our senior secured credit facility contain financial and other restrictive covenants, but will not fully prohibit us from incurring additional debt. If new debt is added to our current level of indebtedness, the related risks that we now face could intensify.

14

If we cannot refinance our 7% senior subordinated notes on or prior to November 1, 2013, then our senior secured credit facility matures on that date and we may not be able to renew or extend our senior secured credit facility or enter into a new credit facility in today's difficult markets. In addition, our ability to renew or extend our senior secured credit facility or to enter into a new credit facility may be impaired further if market conditions worsen. If we are able to refinance our 7% senior subordinated notes or, in the alternative, renew or extend our senior secured credit facility, it may be on terms substantially less favorable than the 7% senior subordinated notes or senior secured credit facility.

Our senior secured credit facility matures on November 1, 2013 if we have not refinanced or otherwise retired the 7% senior subordinated notes on or prior to such date. Our cash flow from operations is unlikely to be sufficient to retire all of such notes at or prior to November 1, 2013.We may therefore be forced to refinance the 7% senior subordinated notes on substantially less favorable terms than we have currently. Failure to obtain new debt on favorable or reasonable terms to replace existing debt could affect our liquidity and the value of our other securities, including our equity. Our ability to refinance or otherwise retire our 7% senior subordinated notes prior to November 1, 2013, or in the alternative to renew or extend our existing senior secured credit facility or to enter into a new credit facility to replace the existing senior secured credit facility could be impaired if market conditions worsen. In the current environment, lenders may seek more restrictive lending provisions and higher interest rates that may reduce our borrowing capacity and increase our costs. We can make no assurances that we will be able to refinance or otherwise retire our 7% senior subordinated notes prior to November 1, 2013, and if we are unable to do so, that we will be able to enter into a new credit facility or renew or extend our existing senior secured credit facility, or whether any such credit facility will be available under acceptable terms. Failure to obtain sufficient financing or financing on acceptable terms would constrain our ability to operate our business and to continue our development and expansion projects. Any of these circumstances could have a material adverse effect on our business, financial condition and results of operations.

We may not be able to successfully expand to new locations or recover our investment in new properties which would adversely affect our operations and available resources.

We regularly evaluate opportunities for growth through development of gaming operations in existing or new markets, through acquiring or managing other gaming entertainment facilities or through redeveloping our existing facilities. The expansion of our operations, whether through acquisitions, development, management contracts or internal growth, could divert management's attention and could also cause us to incur substantial costs, including legal, professional and consulting fees. To the extent that we elect to pursue any new gaming acquisition, management or development opportunity, our ability to benefit from our investment will depend on many factors, including:

- •

- our ability to successfully identify attractive acquisition and development opportunities;

- •

- our ability to successfully operate any developed, managed or acquired properties;

- •

- our ability to attract and retain competent management and employees for the new locations;

- •

- our ability to secure required federal, state and local licenses, permits and approvals, which in some jurisdictions are

limited in number and subject to intense competition; and

- •

- the availability of adequate financing on acceptable terms.

Many of these factors are beyond our control. There have been significant disruptions in the global capital markets that have adversely impacted the ability of borrowers to access capital. Accordingly, it is likely that we are dependent on free cash flow from operations and remaining borrowing capacity under our senior secured credit facility to implement our near-term expansion plans and fund our planned capital expenditures. As a result of these and other considerations, we cannot be sure that we

15

will be able to recover our investments in any new gaming development or management opportunities or acquired facilities, or successfully expand to additional locations.

We may experience construction delays during our expansion or development projects that could adversely affect our operations.

From time to time we may commence construction projects at our properties. We also evaluate other expansion opportunities as they become available and we may in the future engage in additional construction projects. On December 1, 2010, the Missouri Gaming Commission selected our proposed Cape Girardeau Project for prioritization for the 13th and final gaming license in the State of Missouri. The Cape Girardeau Project is expected to include approximately 1,000 slot machines, 28 table games, 3 restaurants, a lounge and terrace overlooking the Mississippi River and a 750-seat event center at an estimated cost of $135 million. On April 14, 2011, our project at the Nemacolin Woodlands Resort ("Nemacolin") was selected by the Pennsylvania Gaming Control Board for the final Category 3 resort gaming license. We had previously entered into an agreement with Nemacolin to complete the build-out of the casino space and provide management services to the casino. The Nemacolin project is expected to include 600 slot machines, 28 table games, a casual dining restaurant and lounge. We currently estimate the project cost at approximately $50 million. Following a successful resolution of an appeal filed by another applicant and receipt of any necessary regulatory approvals, we expect to complete the project within nine months of the commencement of construction. The anticipated costs and construction periods for the Cape Girardeau project, the Nemacolin project and other projects are based upon budgets, conceptual design documents and construction schedule estimates prepared by us in consultation with our architects. Construction projects entail significant risks, which can substantially increase costs or delay completion of a project. Such risks include shortages of materials or skilled labor, unforeseen engineering, environmental or geological problems, work stoppages, weather interference and unanticipated cost increases. Most of these factors are beyond our control. In addition, difficulties or delays in obtaining any of the requisite licenses, permits or authorizations from regulatory authorities can increase the cost or delay the completion of an expansion or development. Significant budget overruns or delays with respect to expansion and development projects could adversely affect our results of operations.

If we construct the Cape Girardeau Project and we are not granted gaming licenses, our financial condition could be materially adversely affected.

On December 1, 2010, the Missouri Gaming Commission selected our proposed Cape Girardeau Project for prioritization for the 13th and final gaming license in the State of Missouri. As a participant in this process, our subsidiary IOC-Cape Girardeau LLC applied for a Class B Riverboat Gaming License in Missouri. The decision by the Missouri Gaming Commission to prioritize its casino development does not provide IOC-Cape Girardeau LLC with any license to open the casino once developed or any assurance that such a license will be granted. The Class B license required for IOC-Cape Girardeau LLC to operate its proposed gaming facility cannot be granted by the Missouri Gaming Commission until the gaming facility development is substantially complete and ready to accept patrons. The grant of this license would be subject to numerous conditions as described in "Description of Government Regulations—Missouri" in Exhibit 99.1 to this Annual Report on Form 10-K for the fiscal year ended April 29, 2012. If, as a result of these regulatory conditions or otherwise, we are unable to receive the gaming license after we construct the Cape Girardeau Project, our financial condition could be materially adversely affected.

16

If we are not licensed in Pennsylvania in connection with the proposed resort casino at Nemacolin Woodlands Resort or if our management agreement is not approved in its current form or if either of these matters are materially delayed, we may not manage the casino or the terms upon which we manage may be less favorable to us.

On April 14, 2011, Nemacolin Woodlands Resort ("Nemacolin") in Farmington, Pennsylvania was selected by the Pennsylvania Gaming Control Board for the final Category 3 resort gaming license. We had previously entered into an agreement with Nemacolin to complete the build-out of the casino space and provide management services of the casino. We currently estimate the project cost at approximately $50 million. The award of the Pennsylvania license to Nemacolin has been appealed to the Pennsylvania Supreme Court by one of the other applicants. Subject to a successful ruling in the appeal, and the receipt of all necessary regulatory and other approvals we expect to complete the facility within approximately nine months after commencing construction.

If our key personnel leave us, our business could be adversely affected.

Our continued success will depend, among other things, on the efforts and skills of a few key executive officers and the experience of our property managers. Our ability to retain key personnel is affected by the competitiveness of our compensation packages and the other terms and conditions of employment, our continued ability to compete effectively against other gaming companies and our growth prospects. The loss of the services of any of these key individuals could have a material adverse effect on our business, financial condition and results of operations. We do not maintain "key man" life insurance for any of our employees.

We are effectively controlled by members of the Goldstein Family and their decisions may differ from those that may be made by other stockholders.

Robert S. Goldstein, our Vice Chairman of the Board, and Jeffrey D. Goldstein and Richard A. Goldstein, two of our directors, and various family trusts associated with members of the Goldstein family and entities associated with certain members of the Goldstein family, (collectively the "Goldstein Parties") directly and indirectly collectively own and control approximately 42.1% of our common stock as of April 29, 2012.

The Goldstein Parties have substantial control over the election of our board of directors and the outcome of the vote on substantially all other matters, including amendment of our amended and restated certificate of incorporation, amendment of our by-laws and significant corporate transactions, such as the approval of a merger or other transactions involving a sale of the Company. Such substantial control may have the effect of discouraging transactions involving an actual or potential change of control, which in turn could have a material adverse effect on the market price of our common stock or prevent our stockholders from realizing a premium over the market price for their shares of common stock. The interests of the Goldstein Parties may differ from those of our other stockholders.

Our amended and restated certificate of incorporation contains provisions that could delay and discourage takeover attempts that stockholders may consider favorable.

Certain provisions of our amended and restated certificate of incorporation may make it more difficult or prevent a third party from acquiring control of us, including:

- •

- we may not, until the Supermajority Expiration Time (as defined below) without the affirmative vote of the holders of at least 662/3% of the Company's voting power, voting as a single class, authorize, adopt or approve certain extraordinary corporate transactions; and

17

- •

- the classification of our board of directors and staggered three-year terms of service for each class of directors.

"Supermajority Expiration Time" means the first to occur of (i) the Goldstein Group ceasing to hold common stock of the Company representing at least 22.5% of our outstanding common stock, not including any shares of Class B common stock or shares of common stock issued upon conversion of any preferred stock and (ii) April 8, 2021. The "Goldstein Group" means Robert S. Goldstein, our Vice Chairman, and Jeffrey D. Goldstein and Richard A. Goldstein, two of our directors, spouses, children and grandchildren of certain members of the Goldstein family and entities associated with certain members of the Goldstein family.

These provisions may make mergers, acquisitions, tender offers, the removal of management and certain other transactions more difficult or more costly and could discourage or limit stockholder participation in such types of transactions, whether or not such transactions are favored by the stockholders. The provisions also could limit the price that investors might be willing to pay in the future for shares of our common stock. Further, the existence of these anti-takeover measures may cause potential bidders to look elsewhere, rather than initiating acquisition discussions with us. Any of these factors could reduce the price of our common stock.

We have a history of fluctuations in our operating income (losses) from continuing operations, and we may incur additional operating losses from continuing operations in the future. Our operating results could fluctuate significantly on a periodic basis.

We sustained a (loss) from continuing operations of $(17.4) million in fiscal 2012, earned income from continuing operations of $3.7 million in fiscal 2011 and earned income from continuing operations of $5.0 million in fiscal 2010. Companies with fluctuations in income (loss) from continuing operations often find it more challenging to raise capital to finance improvements in their businesses and to undertake other activities that return value to their stockholders. In addition, companies with operating results that fluctuate significantly on a quarterly or annual basis experience increased volatility in their stock prices in addition to difficulties in raising capital. We cannot assure you that we will not have fluctuations in our income (losses) from continuing operations in the future, and should that occur, that we would not suffer adverse consequences to our business as a result, which could decrease the value of our common stock.

Inclement weather and other conditions could seriously disrupt our business and have a material, adverse effect on our financial condition and results of operations.

The operations of our facilities are subject to disruptions or reduced patronage as a result of severe weather conditions, natural disasters and other casualties. Because many of our gaming operations are located on or adjacent to bodies of water, these facilities are subject to risks in addition to those associated with other casinos, including loss of service due to casualty, forces of nature, mechanical failure, extended or extraordinary maintenance, flood, hurricane or other severe weather conditions and other disasters. For example, flooding along the Mississippi River resulted in five of our properties being closed for differing periods of time in fiscal 2012. In addition, severe weather such as high winds and blizzards occasionally limits access to our land-based facilities in Colorado. We cannot be sure that the proceeds from any future insurance claim will be sufficient to compensate us if one or more of our casinos experience a closure.

18

Reductions in discretionary consumer spending could have a material adverse effect on our business.

Our business has been and may continue to be adversely affected by economic fluctuations experienced in the United States, as we are highly dependent on discretionary spending by our patrons. Reductions in discretionary consumer spending or changes in consumer preferences brought about by factors such as increased unemployment, significant increases in energy prices, perceived or actual deterioration in general economic conditions, housing market instability, bank failures and the potential for additional bank failures, perceived or actual decline in disposable consumer income and wealth, the global economic recession and changes in consumer confidence in the economy could reduce customer demand for the leisure activities we offer and may adversely affect our revenues and operating cash flow. We are unable to predict the frequency, length or severity of economic circumstances.

The market price of our common stock may fluctuate significantly.

The market price of our common stock has historically been volatile and may continue to fluctuate substantially due to a number of factors, including actual or anticipated changes in our results of operations, the announcement of significant transactions or other agreements by our competitors, conditions or trends in the our industry or other entertainment industries with which we compete, general economic conditions including those affecting our customers' discretionary spending, changes in the cost of air travel or the cost of gasoline, changes in the gaming markets in which we operate and changes in the trading value of our common stock. The stock market in general, as well as stocks in the gaming sector have been subject to significant volatility and extreme price fluctuations that have sometimes been unrelated or disproportionate to individual companies' operating performances. Broad market or industry factors may harm the market price of our common stock, regardless of our operating performance.

Work stoppages, organizing drives and other labor problems could negatively impact our future profits.

Some of our employees are currently represented by a labor union or have begun organizing a drive for labor union representation. Labor unions are making a concerted effort to recruit more employees in the gaming industry. In addition, organized labor may benefit from new legislation or legal interpretations by the current presidential administration. We cannot provide any assurance that we will not experience additional or more successful union activity in the future.

Additionally, lengthy strikes or other work stoppages at any of our casino properties or construction projects could have an adverse effect on our business and result of operations.

We are or may become involved in legal proceedings that, if adversely adjudicated or settled, could impact our financial condition.

From time to time, we are defendants in various lawsuits and gaming regulatory proceedings relating to matters incidental to our business. As with all litigation, no assurance can be provided as to the outcome of these matters and, in general, litigation can be expensive and time consuming. We may not be successful in the defense or prosecution of our current or future legal proceedings, which could result in settlements or damages that could significantly impact our business, financial condition and results of operations.

Our insurance coverage may not be adequate to cover all possible losses that our properties could suffer. In addition, our insurance costs may increase and we may not be able to obtain the same insurance coverage in the future.

We may suffer damage to our property caused by a casualty loss (such as fire, natural disasters, acts of war or terrorism), that could severely disrupt our business or subject us to claims by third parties who are injured or harmed. Although we maintain insurance customary in our industry,

19

(including property, casualty, terrorism and business interruption insurance) that insurance may not be adequate or available to cover all the risks to which our business and assets may be subject. The lack of sufficient insurance for these types of acts could expose us to heavy losses if any damages occur, directly or indirectly, that could have a significant adverse impact on our operations.

We renew our insurance policies on an annual basis. The cost of coverage may become so high that we may need to further reduce our policy limits or agree to certain exclusions from our coverage. Among other factors, it is possible that regional political tensions, homeland security concerns, other catastrophic events or any change in government legislation governing insurance coverage for acts of terrorism could materially adversely affect available insurance coverage and result in increased premiums on available coverage (which may cause us to elect to reduce our policy limits), additional exclusions from coverage or higher deductibles. Among other potential future adverse changes, in the future we may elect to not, or may not be able to, obtain any coverage for losses due to acts of terrorism.

The concentration and evolution of the slot machine manufacturing industry could impose additional costs on us.

A large majority of our revenues are attributable to slot machines at our casinos. It is important, for competitive reasons, we offer the most popular and up-to-date slot machine games, with the latest technology to our customers.

In recent years, slot machine manufacturers have frequently refused to sell slot machines featuring the most popular games, instead requiring participating lease arrangements. Generally, a participating lease is substantially more expensive over the long-term than the cost to purchase a new slot machine.

For competitive reasons, we may be forced to purchase new slot machines, slot machine systems, or enter into participating lease arrangements that are more expensive than our current costs associated with the continued operation of our existing slot machines. If the newer slot machines do not result in sufficient incremental revenues to offset the increased investment and participating lease costs, it could adversely affect our profitability.

* * * * * * *

In addition to the foregoing, you should consider each of the factors set forth in this Annual Report in evaluating our business and our prospects. The factors described in our Part 1, Item 1A are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently consider immaterial may also impair our business operations. This Annual Report is qualified in its entirety by these risk factors. If any of the foregoing risks actually occur, our business, financial condition and results of operation could be materially harmed. In that case, the trading price of our securities, including our common stock, could decline significantly.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

Lake Charles

We own approximately 2.7 acres and lease approximately 16.2 acres of land in Calcasieu Parish, Louisiana for use in connection with our Lake Charles operations. This lease automatically renewed in March 2010 for five years and we have the option to renew it for 14 additional terms of five years each, subject to increases based on the Consumer Price Index ("CPI") with a minimum of 10% and

20

construction of hotel facilities on the property. We own two hotels in Lake Charles with a total of 493 rooms. Annual rent payments under the Lake Charles lease are approximately $2.1 million.

Lula

We lease approximately 1,000 acres of land in Coahoma County, Mississippi and utilize approximately 50 acres in connection with the operations in Lula, Mississippi. Unless terminated by us at an earlier date, the lease expires in 2033. Rent under the lease is currently 5.5% of gross gaming revenue as reported to the Mississippi Gaming Commission, plus $100,000 annually. We also own approximately 100 acres in Coahoma County, which may be utilized for future development.

Natchez

Through numerous lease agreements, we lease approximately 24 acres of land in Natchez, Mississippi that are used in connection with the operations of our Natchez property. Unless terminated by us at an earlier date, the leases have varying expiration dates through 2037. Annual rent under the leases total approximately $1.2 million. We also lease approximately 7.5 acres of land that is utilized for parking at the facility. We own approximately 6 additional acres of property in Natchez, Mississippi, as well as the property upon which our hotel is located.

Vicksburg

We own approximately 60 acres in Vicksburg, Mississippi which are used in connection with the operations of our Vicksburg property.

Kansas City

We lease approximately 28 acres of land from the Kansas City Port Authority in connection with the operation of our Kansas City property. The term of the original lease was ten years and was renewed in October 2006 and October 2011 for additional five-year terms. The lease includes six additional five-year renewal options. The minimum lease payments correspond to any rise or fall in the CPI, initially after the ten-year term of the lease or October 18, 2006 and thereafter, at each five year renewal date. Rent under the lease currently is the greater of $2.9 million (minimum rent) per year, or 3.25% of gross revenues, less complimentaries.

Boonville