UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

For the quarterly period ended

For the transition period from ____________ to ____________

Commission File Number

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of | (IRS Employer | |

| incorporation or organization) | Identification No.) |

(Address of principal executive offices) (Zip Code)

(Issuer’s telephone number, including area code)

Indicate by check mark whether

the issuer (1) filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding

12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days.

Indicate by check mark whether

the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted

and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter

period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | ||

| ☒ | Smaller reporting company | ||||

| Emerging growth company | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether

the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

APPLICABLE ONLY TO CORPORATE ISSUERS:

Indicate the number of shares

outstanding of each of the issuer’s classes of common stock, as of the latest practicable date:

TABLE OF CONTENTS

i

INFORMATION RELATING TO FORWARD-LOOKING STATEMENTS

In addition to historical information, this report contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. You can identify such forward-looking statements by terms such as “anticipates,” “believes,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “would” and similar expressions intended to identify forward-looking statements. Forward-looking statements reflect our current views with respect to future events and are based on assumptions and subject to risks and uncertainties. Given these uncertainties, you should not place undue reliance on these forward-looking statements. These forward-looking statements may include, among other things, statements relating to:

| ● | our expectations regarding the market for our products and services; |

| ● | our expectations regarding the continued growth of our industry; |

| ● | our beliefs regarding the competitiveness of our products; |

| ● | our expectations regarding the expansion of our manufacturing capacity; |

| ● | our expectations with respect to increased revenue growth and our ability to maintain profitability resulting from increases in our production volumes; |

| ● | our future business development, results of operations and financial condition; |

| ● | competition from other fertilizer and plant producers; |

| ● | the loss of any member of our management team; |

| ● | our ability to integrate acquired subsidiaries and operations into existing operations; |

| ● | market conditions affecting our equity capital; |

| ● | our ability to successfully implement our selective acquisition strategy; |

| ● | changes in general economic conditions; |

| ● | changes in accounting rules or the application of such rules; |

| ● | any failure to comply with the periodic filing and other requirements of The New York Stock Exchange, or NYSE, for continued listing, |

| ● | any failure to identify and remediate the material weaknesses or other deficiencies in our internal control and disclosure control over financial reporting; |

Also, forward-looking statements represent our estimates and assumptions only as of the date of this report. You should read this report and the documents that we reference in this report, or that we filed as exhibits to this report, in their entirety and with the understanding that our actual future results may be materially different from what we expect.

Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, even if new information becomes available in the future.

ii

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements

CHINA GREEN AGRICULTURE, INC. AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS

(UNAUDITED)

| September 30, 2023 | June 30, 2023 | |||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Digital assets | ||||||||

| Accounts receivable, net | ||||||||

| Inventories, net | ||||||||

| Prepaid expenses and other current assets | ||||||||

| Amount due from related parties | ||||||||

| Advances to suppliers, net | ||||||||

| Total Current Assets | ||||||||

| Plant, property and equipment, net | ||||||||

| Other assets | ||||||||

| Other non-current assets | ||||||||

| Intangible assets, net | ||||||||

| Deferred Tax Asset | ||||||||

| Total Assets | $ | $ | ||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current Liabilities | ||||||||

| Accounts payable | $ | $ | ||||||

| Customer deposits | ||||||||

| Accrued expenses and other payables | ||||||||

| Amount due to related parties | ||||||||

| Taxes payable | ||||||||

| Short term loans | ||||||||

| Total Current Liabilities | ||||||||

| Long-term Liabilities | ||||||||

| Long-term loans | ||||||||

| Total Liabilities | $ | |||||||

| Commitments and Contingencies | ||||||||

| Stockholders’ Equity | ||||||||

| Preferred Stock, $ | ||||||||

| Common stock, $ | ||||||||

| Additional paid-in capital | ||||||||

| Statutory reserve | ||||||||

| Retained earnings | ( | ) | ( | ) | ||||

| Accumulated other comprehensive loss | ( | ) | ( | ) | ||||

| Total Stockholders’ Equity | ||||||||

| Total Liabilities and Stockholders’ Equity | $ | $ | ||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

1

CHINA GREEN AGRICULTURE, INC. AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND

COMPREHENSIVE LOSS

(UNAUDITED)

| Three Months Ended September 30, | ||||||||

| 2023 | 2022 | |||||||

| Sales | ||||||||

| Jinong | $ | $ | ||||||

| Gufeng | ||||||||

| Yuxing | ||||||||

| Antaeus | ||||||||

| Net sales | ||||||||

| Cost of goods sold | ||||||||

| Jinong | ||||||||

| Gufeng | ||||||||

| Yuxing | ||||||||

| Antaeus | ||||||||

| Cost of goods sold | ||||||||

| Gross profit | ||||||||

| Operating expenses | ||||||||

| Selling expenses | ||||||||

| General and administrative expenses | ||||||||

| Total operating expenses | ||||||||

| Loss from operations | ( | ) | ( | ) | ||||

| Other income (expense) | ||||||||

| Other (expense) | ||||||||

| Interest income | ||||||||

| Interest expense | ( | ) | ( | ) | ||||

| Total other (expense) | ( | ) | ||||||

| Loss before income taxes | ( | ) | ( | ) | ||||

| Provision for income taxes | ( | ) | ||||||

| Net loss | $ | ( | ) | ( | ) | |||

| Other comprehensive loss | ||||||||

| Foreign currency translation loss | ( | ) | ( | ) | ||||

| Comprehensive loss | $ | ( | ) | $ | ( | ) | ||

| Basic weighted average shares outstanding | ||||||||

| Basic net loss per share | $ | ( | ) | $ | ( | ) | ||

| Diluted weighted average shares outstanding | ||||||||

| Diluted net loss per share | $ | ( | ) | $ | ( | ) | ||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

2

CHINA GREEN AGRICULTURE, INC. AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

FOR THE THREE MONTHS ENDED SEPTEMBER 30, 2023 AND 2022

(UNAUDITED)

| Number Of | Common | Additional Paid In | Statutory | Retained | Accumulated Other Comprehensive | Total Stockholders’ | ||||||||||||||||||||||

| Shares | Stock | Capital | Reserve | Earnings | Loss | Equity | ||||||||||||||||||||||

| BALANCE, JUNE 30, 2023 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ||||||||||||||||||

| Net loss | ( | ) | ( | ) | ||||||||||||||||||||||||

| Issuance of stock | ||||||||||||||||||||||||||||

| Transfer to statutory reserve | ( | ) | ||||||||||||||||||||||||||

| Other comprehensive loss | ( | ) | ( | ) | ||||||||||||||||||||||||

| BALANCE, SEPTEMBER 30, 2023 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ||||||||||||||||||

| Number Of | Common | Additional Paid In | Statutory | Retained | Accumulated Other Comprehensive | Total Stockholders’ | ||||||||||||||||||||||

| Shares | Stock | Capital | Reserve | Earnings | Loss | Equity | ||||||||||||||||||||||

| BALANCE, JUNE 30, 2022 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ||||||||||||||||||

| Net loss | ( | ) | ( | ) | ||||||||||||||||||||||||

| Issuance of stock | ||||||||||||||||||||||||||||

| Transfer to statutory reserve | ( | ) | ||||||||||||||||||||||||||

| Other comprehensive loss | ( | ) | ( | ) | ||||||||||||||||||||||||

| BALANCE, SEPTEMBER 30, 2022 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ||||||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

3

CHINA GREEN AGRICULTURE, INC. AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| Three Months Ended September 30, | ||||||||

| 2023 | 2022 | |||||||

| Cash flows from operating activities | ||||||||

| Net loss | $ | ( | ) | $ | ( | ) | ||

| Adjustments to reconcile Net loss to net cash provided by (used in) operating activities | ||||||||

| Depreciation and amortization | ||||||||

| Provision for losses on accounts receivable | ( | ) | ||||||

| Inventories impairment | ||||||||

| Changes in operating assets | ||||||||

| Digital assets | ||||||||

| Accounts receivable | ( | ) | ( | ) | ||||

| Amount due from related parties | ( | ) | ||||||

| Other current assets | ( | ) | ( | ) | ||||

| Inventories | ( | ) | ||||||

| Advances to suppliers | ( | ) | ||||||

| Other assets | ||||||||

| Deferred tax assets | ( | ) | ||||||

| Changes in operating liabilities | ||||||||

| Accounts payable | ( | ) | ||||||

| Customer deposits | ( | ) | ||||||

| Amount due to related parties | ( | ) | ||||||

| Tax payables | ( | ) | ||||||

| Accrued expenses and other payables | ||||||||

| Interest payable | ( | ) | ||||||

| Net cash used in operating activities | ( | ) | ( | ) | ||||

| Cash flows from investing activities | ||||||||

| Purchase of plant, property, and equipment | ( | ) | ( | ) | ||||

| Sales of discontinued operations | ||||||||

| Net cash (used in) provided by investing activities | ( | ) | ||||||

| Cash flows from financing activities | ||||||||

| Proceeds from the sale of common stock | ||||||||

| Proceeds from loans | ||||||||

| Repayment of loans | ( | ) | ||||||

| Advance from related party | ||||||||

| Net cash (used in) provided by financing activities | ( | ) | ||||||

| Effect of exchange rate change on cash and cash equivalents | ( | ) | ( | ) | ||||

| Net (decrease) increase in cash and cash equivalents | ( | ) | ||||||

| Cash and cash equivalents, beginning balance | ||||||||

| Cash and cash equivalents, ending balance | $ | $ | ||||||

| Supplement disclosure of cash flow information | ||||||||

| Interest expense paid | $ | $ | ||||||

| Income taxes paid | $ | $ | ||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

4

CHINA GREEN AGRICULTURE, INC. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1 – ORGANIZATION AND DESCRIPTION OF BUSINESS

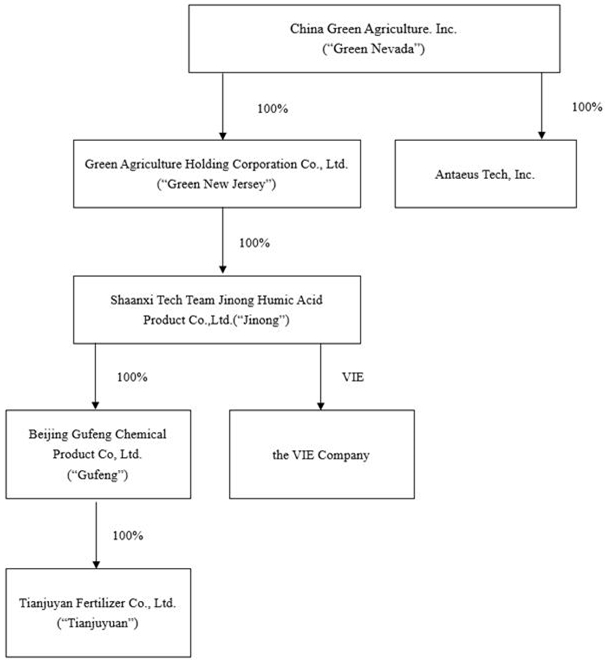

China Green Agriculture, Inc. (the “Company”, “Parent Company” or “Green Nevada”), through its subsidiaries, is engaged in the research, development, production, distribution and sale of humic acid-based compound fertilizer, compound fertilizer, blended fertilizer, organic compound fertilizer, slow-release fertilizers, highly concentrated water-soluble fertilizers and mixed organic-inorganic compound fertilizer and the development, production, and distribution of agricultural products.

Unless the context indicates otherwise, as used in this Report, the following are the references herein of all the subsidiaries of the Company (i) Green Agriculture Holding Corporation (“Green New Jersey”), a wholly-owned subsidiary of Green Nevada, incorporated in the State of New Jersey; (ii) Shaanxi TechTeam Jinong Humic Acid Product Co., Ltd. (“Jinong”), a wholly-owned subsidiary of Green New Jersey organized under the laws of the PRC; (iii) Xi’an Hu County Yuxing Agriculture Technology Development Co., Ltd. (“Yuxing”), a Variable Interest Entity (“VIE”) in the in the PRC controlled by Jinong through a series of contractual agreements; (iv) Beijing Gufeng Chemical Products Co., Ltd., a wholly-owned subsidiary of Jinong in the PRC (“Gufeng”), (v) Beijing Tianjuyuan Fertilizer Co., Ltd., Gufeng’s wholly-owned subsidiary in the PRC (“Tianjuyuan”), and (vi)Antaeus Tech, Inc. (“Antaeus”), a wholly-owned subsidiary of Green Nevada incorporated in the State of Delaware.

On June 30, 2016 the Company, through its wholly-owned subsidiary Jinong, entered into strategic acquisition agreements and a series of contractual agreements with the shareholders of the following six companies that are organized under the laws of the PRC and would be deemed VIEs: Shaanxi Lishijie Agrochemical Co., Ltd. (“Lishijie”), Songyuan Jinyangguang Sannong Service Co., Ltd. (“Jinyangguang”), Shenqiu County Zhenbai Agriculture Co., Ltd. (“Zhenbai”), Weinan City Linwei District Wangtian Agricultural Materials Co., Ltd. (“Wangtian”), Aksu Xindeguo Agricultural Materials Co., Ltd. (“Xindeguo”), and Xinjiang Xinyulei Eco-agriculture Science and Technology co., Ltd. (“Xinyulei”). On January 1, 2017, the Company, through its wholly owned subsidiary Jinong, entered into strategic acquisition agreements and a series of contractual agreements with the shareholders of the following two companies that are organized under the laws of the PRC and would be deemed VIEs, Sunwu County Xiangrong Agricultural Materials Co., Ltd. (“Xiangrong”), and Anhui Fengnong Seed Co., Ltd. (“Fengnong”).

On November 30, 2017, the Company, through its wholly owned subsidiary Jinong, discontinued the strategic acquisition agreements and the series of contractual agreements with the shareholders of Zhenbai.

On June 2, 2021, the Company, through its wholly owned subsidiary Jinong, discontinued the strategic acquisition agreements and the series of contractual agreements with the shareholders of Xindeguo, Xinyulei and Xiangrong.

On December 1, 2021, the Company, through its wholly owned subsidiary Jinong, discontinued the strategic acquisition agreements and the series of contractual agreements with the shareholders of Lishijie.

On December 31, 2021, the Company, through its wholly owned subsidiary Jinong, discontinued the strategic acquisition agreements and the series of contractual agreements with the shareholders of Fengnong.

On March 31, 2022, the Company, through its wholly owned subsidiary Jinong, discontinued the strategic acquisition agreements and the series of contractual agreements with the shareholders of Jinyangguang and Wangtian.

On March 13, 2023, the Company established Antaeus Tech Inc. (“Antaeus”) in the State of Delaware. In April 2023, Antaeus started to purchase digital assets mining machines and to mine Bitcoin in West Texas.

5

Our current corporate structure is set forth in the following diagram:

Yuxing may also collectively be referred to as “the VIE Company”.

6

NOTE 2 – BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Principle of consolidation

The accompanying consolidated financial statements include the accounts of the Company and its wholly owned subsidiaries, Green New Jersey, Jinong, Gufeng, Tianjuyuan, Yuxing and Antaeus. All significant inter-company accounts and transactions have been eliminated in consolidation.

For purposes of comparability, certain prior period amounts have been reclassified to conform to the current year presentation in accordance with accounting principles generally accepted in the United States of America (“GAAP”).

Effective June 16, 2013, Yuxing was converted from being a wholly owned foreign enterprise 100% owned by Jinong to a domestic enterprise 100% owned one natural person, who is not affiliated to the Company (“Yuxing’s Owner”). Effective the same day, Yuxing’s Owner entered into a series of contractual agreements with Jinong pursuant to which Yuxing became the VIE of Jinong.

VIE assessment

A VIE is an entity (1) that has total equity at risk that is not sufficient to finance its activities without additional subordinated financial support from other entities, (2) where the group of equity holders does not have the power to direct the activities of the entity that most significantly impact the entity’s economic performance, or the obligation to absorb the entity’s expected losses or the right to receive the entity’s expected residual returns, or both, or (3) where the voting rights of some investors are not proportional to their obligations to absorb the expected losses of the entity, their rights to receive the expected residual returns of the entity, or both, and substantially all of the entity’s activities either involve or are conducted on behalf of an investor that has disproportionately few voting rights. In order to determine if an entity is considered a VIE, the Company first performs a qualitative analysis, which requires certain subjective decisions regarding its assessments, including, but not limited to, the design of the entity, the variability that the entity was designed to create and pass along to its interest holders, the rights of the parties, and the purpose of the arrangement. If the Company cannot conclude after a qualitative analysis whether an entity is a VIE, it performs a quantitative analysis. The qualitative analysis considered the design of the entity, the risks that cause variability, the purpose for which the entity was created, and the variability that the entity was designed to pass along to its variable interest holders. When the primary beneficiary could not be identified through a qualitative analysis, we used internal cash flow models to compute and allocate expected losses or expected residual returns to each variable interest holder based upon the relative contractual rights and preferences of each interest holder in the VIE’s capital structure.

Use of estimates

The preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the amount of revenues and expenses during the reporting periods. Management makes these estimates using the best information available at the time the estimates are made. However, actual results and outcomes may differ from management’s estimates and assumptions due to risks and uncertainties.

Leases

The Company determines if an arrangement is a lease or contains a lease at inception. Operating lease right-of-use assets and lease liabilities are recognized at commencement based on the present value of lease payments over the lease term. As the implicit rate is typically not readily determinable in the Company’s lease agreements, the Company uses its incremental borrowing rate as of the lease commencement date to determine the present value of the lease payments. The incremental borrowing rate is based on the Company’s specific rate of interest to borrow on a collateralized basis, over a similar term and in a similar economic environment as the lease. Lease expense is recognized on a straight-line basis over the lease term. Leases with an initial term of 12 months or less are not recognized on the balance sheet; the Company recognizes lease expense for these leases on a straight-line basis over the lease term. Additionally, the Company accounts for lease and non-lease components as a single lease component for its identified asset classes. As of September 30, 2023, the Company does not have any material leases for the implementation of ASC 842.

7

Cash and cash equivalents and concentration of cash

For statement of cash flows purposes, the Company

considers all cash on hand and in banks, certificates of deposit with state owned banks in the PRC and banks in the United States, and

other highly-liquid investments with maturities of three months or less, when purchased, to be cash and cash equivalents. The Company

maintains large sums of cash in three major banks in China. The aggregate cash in such accounts and on hand as of September 30, 2023 and

June 30, 2023 were $

Digital Assets

Digital assets are included in current assets in the condensed consolidated balance sheets. Digital assets are accounted for as indefinite-lived intangible assets, and are initially measured in accordance with FASB Accounting Standards Codification (“ASC”) Topic 350 – Intangibles-Goodwill and Other. The Company measures gains or losses on the disposition of digital assets in accordance with the first-in-first-out (“FIFO”) method of accounting.

Digital assets are not amortized, but are assessed for impairment annually, or more frequently, when events or changes in circumstances occur indicating that it is more likely than not that the indefinite-lived intangible asset is impaired. Whenever the exchange-traded price of digital assets declines below its carrying value, the Company has determined that an impairment exists and records an impairment equal to the amount by which the carrying value exceeds the fair value.

As of September

30, 2023, the Company held Bitcoin as digital assets with amount of $

Accounts receivable

Management regularly reviews the composition of

accounts receivable and analyzes customer credit worthiness, current economic trends and changes in customer payment patterns to evaluate

the adequacy of these reserves at each year-end. Accounts considered uncollectible are provisioned for /written off based upon management’s

assessment. As of September 30, 2023, and June 30, 2023, the Company had accounts receivable of $

Inventories

Inventory is valued at the lower of cost (determined

on a weighted average basis) or market. Inventories consist of raw materials, work in process, finished goods and packaging materials.

The Company reviews its inventories regularly for possible obsolete goods and establishes reserves when determined necessary. As of September

30, 2023, and 2022, the Company had no reserve for obsolete goods. The company confirmed the loss of $

Intangible Assets

The Company records intangible assets acquired individually or as part of a group at fair value. Intangible assets with definitive lives are amortized over the useful life of the intangible asset, which is the period over which the asset is expected to contribute directly or indirectly to the entity’s future cash flows. The Company evaluates intangible assets for impairment at least annually and more often whenever events or changes in circumstances indicate that the carrying value may not be recoverable. Whenever any such impairment exists, an impairment loss will be recognized for the amount by which the carrying value exceeds the fair value. The Company has not recorded impairment of intangible assets as of September 30, 2023 and 2022, respectively.

Customer deposits

Payments received before all the relevant criteria

for revenue recognition are satisfied are recorded as customer deposits. When all revenue recognition criteria are met, the customer deposits

are recognized as revenue. As of September 30, 2023, and June 30, 2023, the Company had customer deposits of $

8

Earnings per share

Basic earnings per share is computed based on the weighted average number of shares of common stock outstanding during the period. Diluted earnings per share is computed based on the weighted average number of shares of common stock plus the effect of dilutive potential common shares outstanding during the period using the treasury stock method. Dilutive potential common shares include outstanding stock options and stock awards.

| Three Months Ended | ||||||||

| September 30, | ||||||||

| 2023 | 2022 | |||||||

| Net loss for Basic Earnings Per Share | $ | ( | ) | $ | ( | ) | ||

| Basic Weighted Average Number of Shares | ||||||||

| Net loss Per Share – Basic | $ | ( | ) | $ | ( | ) | ||

| Net loss for Diluted Earnings Per Share | $ | ( | ) | $ | ( | ) | ||

| Diluted Weighted Average Number of Shares | ||||||||

| Net loss Per Share – Diluted | $ | ( | ) | $ | ( | ) | ||

Recent accounting pronouncements

The Company has evaluated all recently issued accounting pronouncements and does not believe any such pronouncements currently have, and does not expect such pronouncements to have, a material impact on the Condensed Consolidated Financial Statements on a prospective basis.

NOTE 3 – GOING CERCERN

The Company’s financial statements are prepared assuming that the Company will continue as a going concern. The Company has incurred operating losses and had negative operating cash flows during the reporting period from July 1, 2023 through September 30, 2023 and may continue to incur operating losses and generate negative cash flows as the Company implements its future business plan. If the situation exists, there could be substantial doubt about the Company’s ability to continue as going concern.

To meet its working capital needs through the next twelve months and to fund the growth of the Company, the Company may consider plans to raise additional funds through the issuance of equity or borrow loan from local bank. The ability of the Company to continue as a going concern is dependent upon its ability to successfully execute its new business strategy and eventually attain profitable operations.

The accompanying financial statements do not include any adjustments to reflect the recoverability and classification of recorded asset amounts and classification of liabilities that might be necessary should the Company be unable to continue as going concern.

9

NOTE 4 – INVENTORIES

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| Raw materials | $ | $ | ||||||

| Supplies and packing materials | $ | $ | ||||||

| Work in progress | $ | $ | ||||||

| Finished goods | $ | $ | ||||||

| Total | $ | $ | ||||||

The company confirmed the loss of $

NOTE 5 – PROPERTY, PLANT AND EQUIPMENT

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| Building and improvements | $ | $ | ||||||

| Auto | ||||||||

| Machinery and equipment | ||||||||

| Others | ||||||||

| Total property, plant and equipment | ||||||||

| Less: accumulated depreciation | ( | ) | ( | ) | ||||

| Total | $ | $ | ||||||

For the three months ended September 30, 2023,

total depreciation expense was $

NOTE 6 – INTANGIBLE ASSETS AND DIGITAL ASSETS

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| Land use rights, net | $ | $ | ||||||

| Technology patent, net | ||||||||

| Customer relationships, net | ||||||||

| Non-compete agreement | ||||||||

| Trademarks | ||||||||

| Total | $ | $ | ||||||

LAND USE RIGHT

On September 25, 2009, Yuxing was granted a land

use right for approximately 88 acres (

On August 13, 2003, Tianjuyuan was granted a certificate

of Land Use Right for a parcel of land of approximately 11 acres (

On August 16, 2001, Jinong received a land use

right as a contribution from a shareholder, which was granted by the People’s Government and Land & Resources Bureau of Yangling

District, Shaanxi Province. The fair value of the related intangible asset at the time of the contribution was determined to be RMB

10

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| Land use rights | $ | |||||||

| Less: accumulated amortization | ( | ) | ( | ) | ||||

| Total land use rights, net | $ | |||||||

TECHNOLOGY PATENT

On August 16, 2001, Jinong was issued a technology

patent related to a proprietary formula used in the production of humic acid. The fair value of the related intangible asset was determined

to be the respective cost of RMB

On July 2, 2010, the Company acquired Gufeng and

its wholly-owned subsidiary Tianjuyuan. The fair value of the acquired technology patent was estimated to be RMB

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| Technology know-how | $ | $ | ||||||

| Less: accumulated amortization | ( | ) | ( | ) | ||||

| Total technology know-how, net | $ | $ | ||||||

CUSTOMER RELATIONSHIPS

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| Customer relationships | $ | $ | ||||||

| Less: accumulated amortization | ( | ) | ( | ) | ||||

| Total customer relationships, net | $ | $ | ||||||

NON-COMPETE AGREEMENT

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| Non-compete agreement | $ | $ | ||||||

| Less: accumulated amortization | ( | ) | ( | ) | ||||

| Total non-compete agreement, net | $ | $ | ||||||

TRADEMARKS

On July 2, 2010, the Company acquired Gufeng and

its wholly-owned subsidiary Tianjuyuan. The preliminary fair value of the acquired trademarks was estimated to be RMB (or $

11

AMORTIZATION EXPENSE

| Twelve Months Ended on September 30, | Expense ($) | |||

| 2024 | ||||

| 2025 | ||||

| 2026 | ||||

| 2027 | ||||

| 2028 | ||||

DIGITAL ASSETS

On March 13, 2023, the Company established Antaeus

Tech Inc. (“Antaeus”) in the State of Delaware. In April 2023, Antaeus started to purchase digital assets mining machines

and to mine Bitcoin in West Texas. As of September 30, 2023, the company held digital assets with amount of $

NOTE 7 – OTHER NON-CURRENT ASSETS

Other non-current assets mainly include advance

payments related to leasing land for use by the Company. As of September 30, 2023, the balance of other non-current assets was $

| Twelve months ending September 30, | ||||

| 2024 | $ | |||

| 2025 | $ | |||

| 2026 | $ | |||

| 2027 | $ | |||

NOTE 8 – ACCRUED EXPENSES AND OTHER PAYABLES

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| Payroll and welfare payable | $ | $ | ||||||

| Accrued expenses | ||||||||

| Other payables | ||||||||

| Other levy payable | ||||||||

| Total | $ | $ | ||||||

12

NOTE 9 – AMOUNT DUE TO RELATED PARTIES

At the end of December 2015, Yuxing entered into

a sales agreement with the Company’s affiliate, 900LH.com Food Co., Ltd. (“900LH.com”, previously announced as Xi’an

Gem Grain Co., Ltd) pursuant to which Yuxing is to supply various vegetables to 900LH.com for its incoming seasonal sales at the holidays

and year ends (the “Sales Agreement”). The contingent contracted value of the Sales Agreement is RMB

The amount due from 900LH.com to Yuxing was $

As of September 30, 2023, and June 30, 2023, the

amount due to related parties was $

As of September 30, 2023, and June 30, 2023, the

Company’s subsidiary, Jinong, owed 900LH.com $

On July 1, 2022, Jinong signed an office lease

with Kingtone Information Technology Co., Ltd. (“Kingtone Information”), of which Mr. Zhuoyu Li, Chairman and CEO of the Company,

served as Chairman. Pursuant to the lease, Jinong rented

NOTE 10 – LOAN PAYABLES

| No. | Payee | Loan period per agreement | Interest Rate | September 30, 2023 | ||||||||

| 1 | Beijing Bank -Pinggu Branch | % | ||||||||||

| 2 | Huaxia Bank -HuaiRou Branch | % | ||||||||||

| 3 | Pinggu New Village Bank | % | ||||||||||

| 4 | Industrial Bank Co. Ltd | % | ||||||||||

| Total | $ | |||||||||||

The interest expense from loans was $

13

NOTE 11 – TAXES PAYABLE

Enterprise Income Tax

Effective January 1, 2008, the Enterprise Income

Tax (“EIT”) law of the PRC replaced the tax laws for Domestic Enterprises (“DEs”) and Foreign Invested Enterprises

(“FIEs”). The EIT rate of

Value-Added Tax

All the Company’s fertilizer products that

are produced and sold in the PRC were subject to a Chinese Value-Added Tax (VAT) of

On April 28, 2017, the PRC State of Administration

of Taxation (SAT) released Notice 2017 #37, “Notice on Policy of Reduced Value Added Tax Rate,” under which, effective

July 1, 2017, all the Company’s fertilizer products that are produced and sold in the PRC are subject to a Chinese Value-Added Tax

(VAT) of

On April 4, 2018, the PRC State of Administration

of Taxation (SAT) released Notice 2018 #32, “Notice on Adjustment of VAT Tax Rate,” under which, effective May 1, 2018,

all the Company’s fertilizer products that are produced and sold in the PRC are subject to a Chinese Value-Added Tax (VAT) of

On March 20, 2019, the PRC State of Administration

of Taxation (SAT) released Notice 2019 #39, “Announcement on Policies Concerning Deepening the Reform of Value Added Tax,”

under which, effective April 1, 2019, all the Company’s fertilizer products that are produced and sold in the PRC are subject to

a Chinese Value-Added Tax (VAT) of

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| VAT provision | $ | ( | ) | $ | ( | ) | ||

| Income tax payable | ( | ) | ( | ) | ||||

| Other levies | ||||||||

| Repatriation tax | ||||||||

| Total | $ | $ | ||||||

| September 30, | September 30, | |||||||

| 2023 | 2022 | |||||||

| Current tax - foreign | $ | ( | ) | $ | ||||

| Deferred tax | ||||||||

| Total | $ | ( | ) | $ | ||||

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| Deferred tax assets | ||||||||

| Deferred Tax Benefit | ||||||||

| Valuation allowance | ( | ) | ( | ) | ||||

| Total deferred tax assets | $ | |||||||

14

Tax Rate Reconciliation

Our effective tax rates were approximately

September 30, 2023

| China 15% - 25% | United States 21% | Total | ||||||||||||||||||||||

| Pretax loss | $ | ( | ) | ( | ) | $ | ( | ) | ||||||||||||||||

| Expected income tax expense (benefit) | ( | ) | % | ( | ) | % | ( | ) | ||||||||||||||||

| High-tech income benefits on Jinong | ||||||||||||||||||||||||

| Losses from subsidiaries in which no benefit is recognized | - | % | ||||||||||||||||||||||

| Change in valuation allowance on deferred tax asset from US tax benefit | ( | )% | ||||||||||||||||||||||

| Actual tax expense | $ | ( | ) | % | $ | $ | ( | ) | % | |||||||||||||||

September 30, 2022

| China 15% - 25% | United States 21% | Total | ||||||||||||||||||||||

| Pretax loss | $ | ( | ) | $ | ( | ) | ||||||||||||||||||

| Expected income tax expense (benefit) | % | ( | ) | % | ( | ) | ||||||||||||||||||

| High-tech income benefits on Jinong | ( | ) | ( | )% | ( | ) | ||||||||||||||||||

| Losses from subsidiaries in which no benefit is recognized | % | |||||||||||||||||||||||

| Change in valuation allowance on deferred tax asset from US tax benefit | ( | )% | ||||||||||||||||||||||

| Actual tax expense | $ | $ | $ | % | ||||||||||||||||||||

NOTE 12 – STOCKHOLDERS’ EQUITY

Common Stock

There were no shares of common stock issued during the quarter ended September 30, 2023.

On August 2, 2022, the Company completed the issuance

of

As of September 30, 2023, and June 30, 2023, there

were

15

Preferred Stock

Under the Company’s Articles of Incorporation,

the Board has the authority, without further action by stockholders, to designate up to

As of September 30, 2023, the Company has

NOTE 13 – CONCENTRATIONS AND LITIGATION

Market Concentration

The majority of the Company’s revenue-generating operations are conducted in the PRC. Accordingly, the Company’s business, financial condition and results of operations may be influenced by the political, economic and legal environments in the PRC, and by the general state of the PRC’s economy.

The Company’s operations in the PRC are subject to specific considerations and significant risks not typically associated with companies in North America and Western Europe. These include risks associated with, among other things, the political, economic and legal environment and foreign currency exchange. The Company’s results may be adversely affected by, among other things, changes in governmental policies with respect to laws and regulations, anti-inflationary measures, currency conversion and remittance abroad, and rates and methods of taxation.

Vendor and Customer Concentration

There are

No customer accounted for over

Litigation

On June 5, 2020, an individual filed suit pro se (as in, representing oneself without an attorney) in the Southern District of Florida federal court alleging violations of the Securities Exchange Act. The Company believes the action is without merit and vigorously opposed it. The company moved to dismiss the litigation and for attorney’s fees from the plaintiff. On November 2, 2020, the case was transferred to the United States District Court for The Southern District Of New York. On September 30, 2021, the Southern District of New York federal court presiding over the case dismissed all claims against the company, its executives, and its independent directors. The dismissal was without prejudice and the plaintiff can appeal or amend within 30 days, or by October 29, 2021. The plaintiff amended the complaint on Oct 30, 2021. On August 30, 2022, the Southern District of New York federal court presiding over the case issued an order granting motions to dismiss all claims in the amended complaint against the Company, its executives, and its independent directors. On September 6, 2022, the plaintiff filed a notice of civil appeal to the U.S. Court of Appeals, Second Circuit. The appeal has now been fully briefed and the Company expects a decision to issue sometime in the coming year.

There are no other actions, suits, proceedings, inquiries or investigations before or by any court, public board, government agency, self-regulatory organization or body pending or, to the knowledge of the executive officers of our company or any of our subsidiaries, threatened against or affecting our company, our common stock, any of our subsidiaries or of our companies or our subsidiaries’ officers or directors in their capacities as such, in which an adverse decision could have a material adverse effect.

NOTE 14 – SEGMENT REPORTING

As of September 30, 2023, the Company was organized

into

16

| Three Months Ended September 30, | ||||||||

| 2023 | 2022 | |||||||

| Revenues from unaffiliated customers: | ||||||||

| Jinong | $ | $ | ||||||

| Gufeng | ||||||||

| Yuxing | ||||||||

| Antaeus | ||||||||

| Consolidated | $ | |||||||

| Operating income (expense): | ||||||||

| Jinong | $ | ( | ) | $ | ||||

| Gufeng | ( | ) | ( | ) | ||||

| Yuxing | ||||||||

| Antaeus | ( | ) | ||||||

| Reconciling item (1) | ||||||||

| Reconciling item (2) | ( | ) | ( | ) | ||||

| Consolidated | $ | ( | ) | $ | ( | ) | ||

| Net income (loss): | ||||||||

| Jinong | $ | ( | ) | $ | ||||

| Gufeng | ( | ) | ( | ) | ||||

| Yuxing | ||||||||

| Antaeus | ( | ) | ||||||

| Reconciling item (1) | ||||||||

| Reconciling item (2) | ( | ) | ( | ) | ||||

| Consolidated | $ | ( | ) | $ | ( | ) | ||

| Depreciation and Amortization: | ||||||||

| Jinong | $ | $ | ||||||

| Gufeng | ||||||||

| Yuxing | ||||||||

| Antaeus | ||||||||

| Consolidated | $ | $ | ||||||

| Interest expense: | ||||||||

| Jinong | ||||||||

| Gufeng | ||||||||

| Yuxing | ||||||||

| Antaeus | ||||||||

| Consolidated | $ | $ | ||||||

| Capital Expenditure: | ||||||||

| Jinong | $ | $ | ||||||

| Gufeng | ||||||||

| Yuxing | ||||||||

| Antaeus | ||||||||

| Consolidated | $ | $ | ||||||

17

| As of | ||||||||

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| Identifiable assets: | ||||||||

| Jinong | $ | $ | ||||||

| Gufeng | ||||||||

| Yuxing | ||||||||

| Antaeus | ||||||||

| Reconciling item (1) | ||||||||

| Reconciling item (2) | ||||||||

| Consolidated | $ | $ | ||||||

| (1) |

| (2) |

NOTE 15 – COMMITMENTS AND CONTINGENCIES

We are subject to various claims and contingencies related to lawsuits, certain taxes and environmental matters, as wells commitments under contractual and other commercial obligations. We recognize liabilities for commitments and contingencies when a loss is probable and estimable.

On July 1, 2022, Jinong signed an office lease

with Kingtone Information Technology Co., Ltd. (“Kingtone Information”), of which Mr. Zhuoyu Li, Chairman and CEO of the Company,

served as Chairman. Pursuant to the lease, Jinong rented

In February 2004, Tianjuyuan signed a fifty-year rental agreement with the village committee of Dong Gao Village and Zhen Nan Zhang Dai Village in the Beijing Ping Gu District.

On April 2, 2023, Antaeus signed a one-year rental

agreement for an office in Austin, Texas for approximately

Accordingly, the Company recorded an aggregate

of $

| Years ending September 30, | ||||

| 2024 | $ | |||

| 2025 | ||||

| 2026 | ||||

| 2027 | ||||

| 2028 | ||||

NOTE 16 – VARIABLE INTEREST ENTITIES

In accordance with accounting standards regarding consolidation of variable interest entities, VIEs are generally entities that lack sufficient equity to finance their activities without additional financial support from other parties or whose equity holders lack adequate decision-making ability. All VIEs with which a company is involved must be evaluated to determine the primary beneficiary of the risks and rewards of the VIE. The primary beneficiary is required to consolidate the VIE for financial reporting purposes.

Green Nevada through one of its subsidiaries, Jinong, entered into a series of agreements (the “VIE Agreements”) with Yuxing for it to qualify as a VIE, effective June 16, 2013.

The Company has concluded, based on the contractual arrangements, that Yuxing is a VIE and that the Company’s wholly owned subsidiary, Jinong, absorbs most of the risk of loss from the activities of Yuxing, thereby enabling the Company, through Jinong, to receive a majority of Yuxing expected residual returns.

On June 30, 2016 and January 1, 2017, the Company, through its wholly owned subsidiary Jinong, entered into strategic acquisition agreements and into a series of contractual agreements to qualify as VIEs with the shareholders of the sales VIE Companies.

Jinong, the sales VIE Companies, and the shareholders of the sales VIE Companies also entered into a series of contractual agreements for the sales VIE Companies to qualify as VIEs (the “VIE Agreements”).

18

On November 30, 2017, the Company, through its wholly owned subsidiary Jinong, exited the VIE agreements with the shareholders of Zhenbai.

On June 2, 2021, the Company, through its wholly owned subsidiary Jinong, discontinued the strategic acquisition agreements and the series of contractual agreements with the shareholders of Xindeguo, Xinyulei and Xiangrong.

On December 1, 2021, the Company, through its wholly owned subsidiary Jinong, discontinued the strategic acquisition agreements and the series of contractual agreements with the shareholders of Lishijie.

On December 31, 2021, the Company, through its wholly owned subsidiary Jinong, discontinued the strategic acquisition agreements and the series of contractual agreements with the shareholders of Fengnong.

On March 31, 2022, the Company, through its wholly owned subsidiary Jinong, discontinued the strategic acquisition agreements and the series of contractual agreements with the shareholders of Jinyangguang and Wangtian.

As a result of these contractual arrangements,

with Yuxing and the sales VIE Companies the Company is entitled to substantially all the economic benefits of Yuxing and the VIE Companies.

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Accounts receivable, net | ||||||||

| Inventories | ||||||||

| Other current assets | ||||||||

| Related party receivable | ||||||||

| Total Current Assets | ||||||||

| Plant, Property and Equipment, Net | ||||||||

| Other assets | ||||||||

| Intangible Assets, Net | ||||||||

| Total Assets | $ | $ | ||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current Liabilities | ||||||||

| Accounts payable | $ | $ | ||||||

| Customer deposits | ||||||||

| Accrued expenses and other payables | ||||||||

| Amount due to related parties | ||||||||

| Total Current Liabilities | ||||||||

| Total Liabilities | $ | |||||||

| Stockholders’ equity | ( | ) | ( | ) | ||||

| Total Liabilities and Stockholders’ Equity | $ | $ | ||||||

| Three Months Ended September 30, | ||||||||

| 2023 | 2022 | |||||||

| Revenue | $ | $ | ||||||

| Expenses | ||||||||

| Net income | $ | $ | ||||||

NOTE 17 – SUBSEQUENT EVENTS

In accordance with ASC 855-10, the Company has analyzed its operations after September 30, 2023 to the date these unaudited condensed consolidated financial statements were available to be issued and has determined that there were no significant subsequent events or transactions that would require recognition or disclosure in the unaudited condensed consolidated financial statements.

19

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our consolidated financial statements and the notes to those financial statements appearing elsewhere in this report. This discussion and analysis contain forward-looking statements that involve significant risks and uncertainties. As a result of many factors, such as the slow-down of the macro-economic environment in China and its impact on economic growth in general, the competition in the fertilizer industry and the impact of such competition on pricing, revenues and margins, the weather conditions in the areas where our customers are based, the cost of attracting and retaining highly skilled personnel, the prospects for future acquisitions, and the factors set forth elsewhere in this report, our actual results may differ materially from those anticipated in these forward-looking statements. With these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this report will in fact occur. You should not place undue reliance on the forward-looking statements contained in this report.

The forward-looking statements speak only as of the date on which they are made, and, except to the extent required by U.S. federal securities laws, we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. Further, the information about our intentions contained in this report is a statement of our intention as of the date of this report and is based upon, among other things, the existing regulatory environment, industry conditions, market conditions and prices, and our assumptions as of such date. We may change our intentions, at any time and without notice, based upon any changes in such factors, in our assumptions or otherwise.

Unless the context indicates otherwise, as used in the notes to the financial statements of the Company, the following are the references herein of all the subsidiaries of the Company (i) Green Agriculture Holding Corporation (“Green New Jersey”), a wholly-owned subsidiary of Green Nevada incorporated in the State of New Jersey; (ii) Shaanxi TechTeam Jinong Humic Acid Product Co., Ltd. (“Jinong”), a wholly-owned subsidiary of Green New Jersey organized under the laws of the PRC; (iii) Xi’an Hu County Yuxing Agriculture Technology Development Co., Ltd. (“Yuxing”), a Variable Interest Entity in the PRC (“VIE”) controlled by Jinong through contractual agreements; (iv) Beijing Gufeng Chemical Products Co., Ltd., a wholly-owned subsidiary of Jinong in the PRC (“Gufeng”); (v) Beijing Tianjuyuan Fertilizer Co., Ltd., Gufeng’s wholly-owned subsidiary in the PRC (“Tianjuyuan”). Yuxing may also collectively be referred to as the “the VIE Company”, and (vi)Antaeus Tech, Inc. (“Antaeus”), a wholly-owned subsidiary of Green Nevada incorporated in the State of Delaware.

Unless the context otherwise requires, all references to (i) “PRC” and “China” are to the People’s Republic of China; (ii) “U.S. dollar,” “$” and “US$” are to United States dollars; and (iii) “RMB”, “Yuan” and Renminbi are to the currency of the PRC or China.

Overview

We are engaged in the research, development, production, and sale of various types of fertilizers, agricultural products and Bitcoin in the PRC and United State through our wholly owned Chinese subsidiaries, Jinong and Gufeng (including Gufeng’s subsidiary Tianjuyuan), our VIE, Yuxing and our wholly owned U.S. subsidiary Antaeus. Our primary business is fertilizer products, specifically humic-acid based compound fertilizer produced by Jinong and compound fertilizer, blended fertilizer, organic compound fertilizer, slow-release fertilizer, highly concentrated water-soluble fertilizer, and mixed organic-inorganic compound fertilizer produced by Gufeng. In addition, through Yuxing, we develop and produce various agricultural products, such as top-grade fruits, vegetables, flowers and colored seedlings. Besides, we engaged in the mining of digital assets Bitcoin through Antaeus. For financial reporting purposes, our operations are organized into four business segments: fertilizer products (Jinong), fertilizer products (Gufeng), agricultural products (Yuxing), and Bitcoin (Antaeus).

The fertilizer business conducted by Jinong and Gufeng generated approximately 88.0% and 89.6% of our total revenues for the three months ended September 30, 2023 and 2022, respectively. Yuxing generated 10.5% and 10.4% of our revenues for the years ended September 30, 2023 and 2022, respectively. Yuxing serves as a research and development base for our fertilizer products. Antaeus generated 1.5% and 0% of our revenues for the years ended September 30, 2023 and 2022, respectively.

Fertilizer Products

As of September 30, 2023, we had developed and produced a total of 409 different fertilizer products in use, of which 73 were developed and produced by Jinong, 336 by Gufeng.

20

Below is a table that shows the metric tons of fertilizer sold by Jinong and Gufeng and the revenue per ton for the periods indicated:

| Three Months Ended | ||||||||||||||||

| September 30, | Change 2022 to 2023 | |||||||||||||||

| 2023 | 2022 | Amount | % | |||||||||||||

| (metric tons) | ||||||||||||||||

| Jinong | 8,036 | 9,385 | (1,349 | ) | -14.4 | % | ||||||||||

| Gufeng | 20,809 | 24,171 | (3,362 | ) | -13.9 | % | ||||||||||

| 28,845 | 33,556 | (4,711 | ) | -14.0 | % | |||||||||||

| Three Months Ended September 30, | ||||||||

| 2023 | 2022 | |||||||

| (revenue per tons) | ||||||||

| Jinong | $ | 1,157 | $ | 1,294 | ||||

| Gufeng | 501 | 520 | ||||||

For the three months ended September 30, 2023, we sold approximately 28,845 tons of fertilizer products, as compared to 33,556 metric tons for the three months ended September 30, 2022. For the three months ended September 30, 2023, Jinong sold approximately 8,036 metric tons of fertilizer products, as compared to 9,385 metric tons for the three months ended September 30, 2022. For the three months ended September 30, 2023, Gufeng sold approximately 20,809 metric tons of fertilizer products, as compared to 24,171 metric tons for the three months ended September 30, 2022.

Our sales of fertilizer products to customers in five provinces within China accounted for approximately 61.9% of our fertilizer revenue for the three months ended September 30, 2023. Specifically, the provinces and their respective percentage contributing to our fertilizer revenues were Hebei (26.2%), Heilongjiang (11.5%), Inner Mongolia (9.5%), Liaoning (9.4%), and Shaanxi (5.3%).

As of September 30, 2023, we had a total of 1,223 distributors covering 22 provinces, 4 autonomous regions and 4 central government-controlled municipalities in China. Jinong had 878 distributors in China. Jinong’s sales are not dependent on any single distributor or any group of distributors. Jinong’s top five distributors accounted for 18.2% of its fertilizer revenues for the three months ended September 30, 2023. Gufeng had 345 distributors, including some large state-owned enterprises. Gufeng’s top five distributors accounted for 80.9% of its revenues for the three months ended September 30, 2023.

Agricultural Products

Through Yuxing, we develop, produce and sell high-quality flowers, green vegetables and fruits to local marketplaces and various horticulture and planting companies. We also use certain of Yuxing’s greenhouse facilities to conduct research and development activities for our fertilizer products. The three PRC provinces and municipalities that accounted for 83.2% of our agricultural products revenue for the three months ended September 30, 2023 were Shaanxi (67.4%), Beijing (9.4%), and Shanghai (6.4%).

Digital Assets Bitcoin

In March 2023, we established Antaeus Tech Inc. (“Antaeus”) and purchased mining machines to mine digital assets Bitcoin in the State of Texas. Through Antaeus, we expanded our activities in the mining of digital assets Bitcoin.

Recent Developments

New Products

During the three months ended September 30, 2023, Jinong launched 3 new fertilizer products but eliminated 105 unqualified distributors. During the same period, Gufeng neither launched any new fertilizer products nor added any new distributors

21

Results of Operations

Three Months ended September 30, 2023 Compared to the Three Months ended September 30, 2022.

| 2023 | 2022 | Change $ | Change % | |||||||||||||

| Sales | ||||||||||||||||

| Jinong | $ | 9,288,758 | $ | 12,148,002 | (2,859,244 | ) | -23.5 | % | ||||||||

| Gufeng | 10,421,274 | 12,578,822 | (2,157,548 | ) | -17.2 | % | ||||||||||

| Yuxing | 2,342,716 | 2,870,501 | (527,785 | ) | -18.4 | % | ||||||||||

| Antaeus | 345,114 | - | 345,114 | - | ||||||||||||

| Net sales | 22,397,862 | 27,597,325 | (5,199,463 | ) | -18.8 | % | ||||||||||

| Cost of goods sold | ||||||||||||||||

| Jinong | 6,606,614 | 8,760,170 | (2,153,556 | ) | -24.6 | % | ||||||||||

| Gufeng | 8,995,321 | 11,254,877 | (2,259,556 | ) | -20.1 | % | ||||||||||

| Yuxing | 1,877,527 | 2,397,469 | (519,942 | ) | -21.7 | % | ||||||||||

| Antaeus | 268,546 | - | 268,546 | - | ||||||||||||

| Cost of goods sold | 17,748,008 | 22,412,516 | (4,664,508 | ) | -20.8 | % | ||||||||||

| Gross profit | 4,649,854 | 5,184,809 | (534,955 | ) | -10.3 | % | ||||||||||

| Operating expenses | ||||||||||||||||

| Selling expenses | 1,879,155 | 2,437,354 | (558,199 | ) | -22.9 | % | ||||||||||

| General and administrative expenses | 4,556,606 | 3,285,115 | 1,271,491 | 38.7 | % | |||||||||||

| Total operating expenses | 6,435,761 | 5,722,469 | 713,292 | 12.5 | % | |||||||||||

| Loss from operations | (1,785,907 | ) | (537,660 | ) | (1,248,247 | ) | 232.2 | % | ||||||||

| Other income (expense) | ||||||||||||||||

| Other income (expense) | 9,783 | 27,790 | (18,007 | ) | -64.8 | % | ||||||||||

| Interest income | 55,072 | 64,000 | (8,928 | ) | -13.9 | % | ||||||||||

| Interest expense | (67,554 | ) | (82,244 | ) | 14,690 | -17.9 | % | |||||||||

| Total other income (expense) | (2,699 | ) | 9,546 | (12,245 | ) | -128.3 | % | |||||||||

| Loss before income taxes | (1,788,606 | ) | (528,114 | ) | (1,260,492 | ) | 238.7 | % | ||||||||

| Provision for income taxes | (4,413 | ) | - | (4,413 | ) | - | ||||||||||

| Net loss | (1,784,193 | ) | (528,114 | ) | (1,256,078 | ) | 237.8 | % | ||||||||

| Other comprehensive loss | ||||||||||||||||

| Foreign currency translation loss | (836,377 | ) | (10,920,158 | ) | 10,083,781 | -92.3 | % | |||||||||

| Comprehensive loss | $ | (2,620,570 | ) | $ | (11,448,272 | ) | 8,827,703 | -77.1 | % | |||||||

22

Net Sales

Total net sales for the three months ended September 30, 2023 were $22,397,862, a decrease of $5,199,463 or 18.8%, from $27,597,325 for the three months ended September 30, 2022. This decrease was mainly due to the decrease for Jinong’s net sales.

For the three months ended September 30, 2023, Jinong’s net sales decreased $2,859,244, or 23.5%, to $9,288,758 from $12,148,002 for the three months ended September 30, 2022. This decrease was mainly due to Jinong’s lower sales volume in the last three months. Jinong sold approximately 8,036 metric tons of fertilizer products for the three months ended September 30, 2023, decreased 1,349 tons or 14.4%, as compared to 9,385 metric tons for the three months ended September 30, 2022.

For the three months ended September 30, 2023, Gufeng’s net sales were $10,421,274, a decrease of $2,157,548 or 17.2%, from $12,578,822 for the three months ended September 30, 2022. This decrease was mainly due to Gufeng’s lower sales volume in the last three months. Gufeng sold approximately 20,809 metric tons of fertilizer products for the three months ended September 30, 2023, decreased 3,362 tons or 13.9%, as compared to 24,171 metric tons for the three months ended September 30, 2022.

For the three months ended September 30, 2023, Yuxing’s net sales were $2,342,716, a decrease of $527,785 or 18.4%, from $2,870,501 for the three months ended September 30, 2022. The decrease was mainly due to the decrease in market demand during the three months ended September 30, 2023.

For the three months ended September 30, 2023, Antaeus’s net sales were $345,114.

Cost of Goods Sold

Total cost of goods sold for the three months ended September 30, 2023 was $17,748,008, a decrease of $4,664,508, or 20.8%, from $22,412,516 for the three months ended September 30, 2022. The decrease was mainly due lower sales.

Cost of goods sold by Jinong for the three months ended September 30, 2023 was $6,606,614, a decrease of $2,153,556, or 24.6%, from $8,760,170 for the three months ended September 30, 2022. The decrease in cost of goods was primarily due to lower sales in last three months ended September 30, 2023.

Cost of goods sold by Gufeng for the three months ended September 30, 2023 was $8,995,321, a decrease of $2,259,556, or 20.1%, from $11,254,877 for the three months ended September 30, 2022. This decrease was primarily due to the 17.2% decrease in net sale in last three months ended September 30, 2023.

For three months ended September 30, 2023, cost of goods sold by Yuxing was $1,877,527, a decrease of $519,942, or 21.7%, from $2,397,469 for the three months ended September 30, 2022. This decrease was primarily due to the 18.4% decrease in net sale in last three months ended September 30, 2023.

For the three months ended September 30, 2023, cost of goods sold by Antaeus was $268,546.

23

Gross Profit

Total gross profit for the three months ended September 30, 2023 decreased by $534,955, or 10.3%, to $4,649,854, as compared to $5,184,809 for the three months ended September 30, 2022. Gross profit margin percentage was 20.8% and 18.8% for the three months Ended September 30, 2023 and 2022, respectively.

Gross profit generated by Jinong decreased by $705,688, or 20.8%, to $2,682,144 for the three months ended September 30, 2023 from $3,387,832 for the three months ended September 30, 2022. Gross profit margin percentage from Jinong’s sales was approximately 28.9% and 27.9% for the three months Ended September 30, 2023 and 2022, respectively.

For the three months ended September 30, 2023, gross profit generated by Gufeng was $1,425,953, an increase of $102,008, or 7.7%, from $1,323,945 for the three months ended September 30, 2022. Gross profit margin percentage from Gufeng’s sales was approximately 13.7% and 10.5% for the three months ended September 30, 2023 and 2022, respectively.

For the three months ended September 30, 2023, gross profit generated by Yuxing was $465,189, a slightly decrease of $7,843, or 1.7% from $473,032 for the three months ended September 30, 2022. The gross profit margin percentage was approximately 19.9% and 16.5% for the three months Ended September 30, 2023 and 2022, respectively. The increase in gross profit margin percentage was mainly due to the decrease in product costs.

For the three months ended September 30, 2023, gross profit generated by Antaeus was $76,568. The gross profit margin was approximately 22.2% for the three months ended September 30, 2023.

Selling Expenses

Our selling expenses consisted primarily of salaries of sales personnel, advertising and promotion expenses, freight-out costs and related compensation. Selling expenses were $1,879,155, or 8.4%, of net sales for the three months ended September 30, 2023, as compared to $2,437,354, or 8.8%, of net sales for the three months ended September 30, 2022, a decrease of $558,199, or 22.9%. The decrease in selling expense was caused by the decrease in marketing activities.

The selling expenses of Jinong for the three months ended September 30, 2023 were $1,795,441 or 19.3% of Jinong’s net sales, as compared to selling expenses of $2,351,821 or 19.4% of Jinong’s net sales for the three months ended September 30, 2022. The selling expenses of Yuxing were $19,837 or 0.8% of Yuxing’s net sales for the three months ended September 30, 2023, as compared to $19,046 or 0.7% of Yuxing’s net sales for the three months ended September 30, 2022. The selling expenses of Gufeng were $63,877 or 0.6% of Gufeng’s net sales for the three months ended September 30, 2023, as compared to $66,487 or 0.5% of Gufeng’s net sales for the three months ended September 30, 2022. There is no selling expenses for Antaeus for the three months ended September 30, 2023.

General and Administrative Expenses

General and administrative expenses consisted primarily of related salaries, rental expenses, business development, depreciation and travel expenses incurred by our general and administrative departments and legal and professional expenses including expenses incurred and accrued for certain litigation. General and administrative expenses were $4,556,606, or 20.3% of net sales for the three months ended September 30, 2023, as compared to $3,285,115, or 11.9% of net sales for the three months ended September 30, 2022, an increase of $1,271,491, or 38.7%. The increase in general and administrative expenses was mainly due to higher general and administrative expenses for Jinong and Gufeng. Jinong’s general and administrative expenses were $1,031,827 for the three months ended September 30, 2023, increased $915,460, or 786.7%, as compared to $116,367 for the three months ended September 30, 2022. Gufeng’s general and administrative expenses were $2,581,958 for the three months ended September 30, 2023, increased $660,770, or 34.4%, as compared to $1,921,188 for the three months ended September 30, 2022.

Total Other Income (Expenses)

Total other income (expenses) consisted of income from subsidies received from the PRC government, interest income, interest expenses and bank charges. Total other expense for the three months ended September 30, 2023 was $2,699, as compared to other income of $9,546 for the three months ended September 30, 2022. The difference was mainly due to the decrease in other income with amount of 18,007, or 64.8% from $27,790 for the three months ended September 30, 2022 to $9,783 for the three months ended September 30, 2023. There was $21,898 in subsidy income for the three months ended September 30, 2022, compared to no subsidy income for the three months ended September 30, 2023.

24

Income Taxes

Jinong is subject to a preferred tax rate of 15% because of its business being classified as a High-Tech project under the PRC Enterprise Income Tax Law (“EIT”) that became effective on January 1, 2008. Jinong incurred no income tax expenses for the three months ended September 30, 2023 and 2022.

Gufeng is subject to a tax rate of 25%, incurred no income tax expenses for the three months ended September 30, 2023 and 2022.

Yuxing inccured no income tax for the three months ended September 30, 2023 and 2022 because of being exempted from paying income tax due to its products fall into the tax exemption list set out in the EIT.

Antaeus is subject to a tax rate of 21% and had income tax expense of $(4,413) for the three months ended September 30, 2023.

Net loss

Net loss for the three months ended September 30, 2023 was $(1,784,193), an increase in loss of $1,256,078, or 237.8%, compared to net loss of $(528,114) for the three months ended September 30, 2022. Net loss as a percentage of total net sales was approximately -8.0% and -1.9% for the three months Ended September 30, 2023 and 2022, respectively.

Discussion of Segment Profitability Measures

As of September 30, 2023, we were engaged in the following businesses: the production and sale of fertilizers through Jinong and Gufeng, the production and sale of high-quality agricultural products by Yuxing and the production and sale of Bitcoin by Antaeus. For financial reporting purpose, our operations were organized into four main business segments based on locations and products: Jinong (fertilizer production), Gufeng (fertilizer production), Yuxing (agricultural products production) and Antaeus (Bitcoin). Each of the segments has its own annual budget about development, production and sales.

Each of the four operating segments referenced above has separate and distinct general ledgers. The chief operating decision maker (“CODM”) makes decisions with respect to resources allocation and performance assessment upon receiving financial information, including revenue, gross margin, operating income and net income produced from the various general ledger systems; however, net income by segment is the principal benchmark to measure profit or loss adopted by the CODM.

For Jinong, the net income (loss) decreased by $1,098,712, or 111.6%, to $(114,362) for the three months ended September 30, 2023, from $984,350 for the three months ended September 30, 2022. The decrease in net income was principally due to lower sales and higher general and administrative expenses.

For Gufeng, the net loss increased by $515,923, or 69.1%, to $(1,262,423) for the three months ended September 30, 2023, from $(746,500) for the three months ended September 30, 2022. The increase in net loss was principally due to the increase in general and administrative expenses.

For Yuxing, the net income decreased $57,315 or 27.1%, to $154,271 for the three months ended September 30, 2023 from $211,586 for the three months ended September 30, 2022. The decrease was mainly due to lower net sales.

For Antaeus, the net loss was $(16,603) for the three months ended September 30, 2023.

Liquidity and Capital Resources

Our principal sources of liquidity include cash from operations, borrowings from local commercial banks and net proceeds of offerings of our securities.

As of September 30, 2023, cash and cash equivalents were $67,285,823, a decrease of $3,856,365, or 5.4%, from $71,142,188 as of June 30, 2023.

We intend to use the net proceeds from our securities offerings, as well as other working capital if required, to acquire new businesses, upgrade production lines and complete Yuxing’s new greenhouse facilities for agriculture products located on 88 acres of land in Hu County, 18 kilometers southeast of Xi’an city. We believe that we have sufficient cash on hand and positive projected cash flow from operations to support our business growth for the next twelve months to the extent we do not have further significant acquisitions or expansions. However, if events or circumstances occur and we do not meet our operating plan as expected, we may be required to seek additional capital and/or to reduce certain discretionary spending, which could have a material adverse effect on our ability to achieve our business objectives. Notwithstanding the foregoing, we may seek additional financing as necessary for expansion purposes and when we believe market conditions are most advantageous, which may include additional debt and/or equity financings. There can be no assurance that any additional financing will be available on acceptable terms, if at all. Any equity financing may result in dilution to existing stockholders and any debt financing may include restrictive covenants.

25

The following table sets forth a summary of our cash flows for the periods indicated:

| Three Months Ended | ||||||||

| September 30, | ||||||||

| 2023 | 2022 | |||||||

| Net cash used in operating activities | $ | (626,510 | ) | $ | (2,995,510 | ) | ||

| Net cash (used in) provided by investing activities | (1,507,026 | ) | 683,884 | |||||

| Net cash (used in) provided by financing activities | (1,383,960 | ) | 18,025,034 | |||||

| Effect of exchange rate change on cash and cash equivalents | (338,869 | ) | (3,651,176 | ) | ||||

| Net (decrease) increase in cash and cash equivalents | (3,856,365 | ) | 12,062,232 | |||||

| Cash and cash equivalents, beginning balance | 71,142,188 | 57,770,303 | ||||||

| Cash and cash equivalents, ending balance | $ | 67,285,823 | $ | 69,832,535 | ||||

Operating Activities

Net cash used in operating activities was $626,510 for the three months ended September 30, 2023, a decrease of $2,369,000, or 79.1%, from cash used in operating activities of $2,995,510 for the three months ended September 30, 2022. The decrease in cash used in operating activities was mainly due to an increase in customer deposits during the three months ended September 30, 2023 as compared to the same period in 2022.

Investing Activities

Net cash used in investing activities for the three months ended September 30, 2023 was $1,507,026, compared to cash provided by investing activities of $683,884 for the three months ended September 30, 2022. The difference of $2,190,910 was mainly due to purchase of plant, property, and equipment with amount of $1,507,026 during the three months ended September 30, 2023, comparing with $228,541 during the three months ended September 30, 2022.

Financing Activities

Net cash used in financing activities for the three months ended September 30, 2023 was $1,383,960, a decrease of $19,408,994, or 107.7% compared to $18,025,034 net cash provided by financing activities for the three months ended September 30, 2022. The decrease was mainly due to the repayment of loans with amount of $1,574,960 during the three months ended September 30, 2023.

As of September 30, 2023, and June 30, 2023, our loans payable was as follows:

| September 30, | June 30, | |||||||

| 2023 | 2023 | |||||||

| Short term loans payable: | $ | 3,756,540 | $ | 5,346,640 | ||||

| Long term loans payable: | 932,280 | 937,040 | ||||||

| Total | $ | 4,688,820 | $ | 6,283,680 | ||||

Accounts Receivable

We had accounts receivable of $19,908,132 as of September 30, 2023, as compared to $16,455,734 as of June 30, 2023, an increase of $3,452,398, or 21.0%.

Allowance for doubtful accounts in accounts receivable as of September 30, 2023 was $50,913,569, a decrease of $3,794,917, or 6.9%, from $54,708,486 as of June 30, 2023. And the allowance for doubtful accounts as a percentage of accounts receivable was 71.9% as of September 30, 2023 and 76.9% as of June 30, 2023.

Deferred assets

We had no deferred assets as of September 30, 2023 and June 30, 2023. During the three months, we assisted the distributors in certain marketing efforts and developing standard stores to expand our competitive advantage and market shares. Based on the distributor agreements, the amount owed by the distributors in certain marketing efforts and store development will be expensed over three years if the distributors are actively selling our products. If a distributor defaults, breaches, or terminates the agreement with us earlier than the contractual terms, the unamortized portion of the amount owed by the distributor is payable to us immediately. The deferred assets had been fully amortized as of September 30, 2023.

26

Inventories

We had inventories of $42,595,553 as of September 30, 2023, as compared to $46,455,131 as of June 30, 2023, a decrease of $3,859,578, or 8.3%. The decrease was primarily due to Gufeng’s inventory. As of September 30, 2023, Gufeng’s inventory was $17,730,525, compared to $21,691,450 as of June 30, 2023, a decrease of $3,960,925, or 18.3%. The company confirmed the loss of $2.4 million and $1.7 million of inventories for the three months ended September 30, 2023 and 2022, respectively.

Advances to Suppliers

We had advances to suppliers of $14,685,085 as of September 30, 2023 as compared to $14,332,715 as of June 30, 2023, representing an increase of $352,370, or 2.5%. Our inventory level may fluctuate from time to time, depending how quickly the raw material is consumed and replenished during the production process, and how soon the finished goods are sold. The replenishment of raw material relies on management’s estimate of numerous factors, including but not limited to, the raw materials future price, and spot price along with its volatility, as well as the seasonal demand and future price of finished fertilizer products. Such estimate may not be accurate, and the purchase decision of raw materials based on the estimate can cause excessive inventories in times of slow sales and insufficient inventories in peak times.

Accounts Payable

We had accounts payable of $1,979,494 as of September 30, 2023 as compared to $2,100,449 as of June 30, 2023, representing a decrease of $120,955, or 5.8%.

Customer Deposits (Unearned Revenue)

We had customer deposits of $5,669,071 as of September 30, 2023 as compared to $5,489,781 as of June 30, 2023, representing an increase of $179,290, or 3.3%. The increase was mainly attributable to Jinong’ $1,232,751 unearned revenue as of September 30, 2023, compared to $1,152,204 unearned revenue as of June 30, 2023, increased $80,547, or 7.0%, caused by the advance deposits made by clients. This increase was due to seasonal fluctuation and we expect to deliver products to our customers during the next three months at which time we will recognize the revenue.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements.

Critical Accounting Policies and Estimates