Use these links to rapidly review the document

ImmunoGen, Inc. Form 10-K TABLE OF CONTENTS

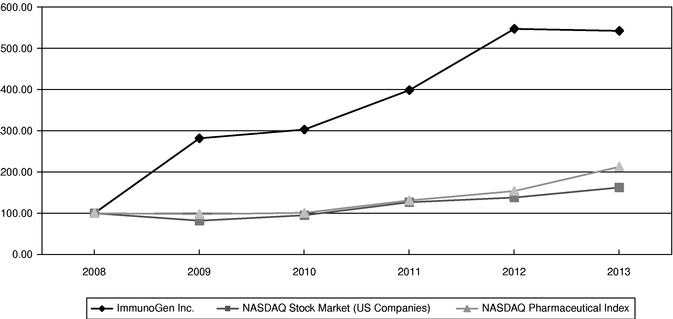

Item 8. Financial Statements and Supplementary Data

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended June 30, 2013 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission file number 0-17999

ImmunoGen, Inc.

| Massachusetts (State or other jurisdiction of incorporation or organization) |

04-2726691 (I.R.S. Employer Identification No.) |

|

830 Winter Street, Waltham, MA 02451 (Address of principal executive offices, including zip code) |

||

(781) 895-0600 (Registrant's telephone number, including area code) |

||

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

|---|---|---|

| Common Stock, $.01 par value | NASDAQ Global Select Market |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ý Yes o No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes ý No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ý Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ý Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes ý No

Aggregate market value, based upon the closing sale price of the shares as reported by the NASDAQ Global Select Market, of voting stock held by non-affiliates at December 31, 2012: $1,070,664,433 (excludes shares held by executive officers and directors). Exclusion of shares held by any person should not be construed to indicate that such person possesses the power, direct or indirect, to direct or cause the direction of management or policies of the registrant, or that such person is controlled by or under common control with the registrant. Common Stock outstanding at August 20, 2013: 85,109,108 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement to be delivered to shareholders in connection with the Annual Meeting of Shareholders to be held on November 12, 2013 are incorporated by reference into Part III.

ImmunoGen, Inc.

Form 10-K

TABLE OF CONTENTS

2

In this Annual Report on Form 10-K, ImmunoGen, Inc. (ImmunoGen, Inc., together with its subsidiaries, is referred to in this document as "we", "us", "ImmunoGen", or the "Company"), incorporates by reference certain information from parts of other documents filed with the Securities and Exchange Commission. The Securities and Exchange Commission allows us to disclose important information by referring to it in that manner. Please refer to all such information when reading this Annual Report on Form 10-K. All information is as of June 30, 2013 unless otherwise indicated. For a description of the risk factors affecting or applicable to our business, see "Risk Factors," below.

Overview

We are a biotechnology company that develops targeted anticancer therapeutics. All of our wholly owned clinical and preclinical product candidates are antibody-drug conjugates, or ADCs, which use a monoclonal antibody to deliver a small molecule to targeted cells.

We developed our Targeted Antibody Payload, or TAP, ADC technology to enable the creation of highly effective, well-tolerated anticancer products. A TAP compound consists of an antibody that binds specifically to an antigen found on the targeted cancer cells with one of our potent cancer-cell killing agents attached using one of our engineered linkers. The antibody component enables a TAP compound to target cancer cells expressing its antigen, and the highly potent cell-killing agent serves to kill these cells. Our linkers are engineered to keep the cell-killing agent securely attached to the antibody while traveling through the bloodstream, and then control its release and activation once inside a cancer cell. Depending on the target, the antibody component of the TAP compound may serve only as a targeting vehicle or it may also have anticancer activity.

We develop our own product candidates using our TAP technology with antibodies from our research programs. We now have four wholly owned, clinical-stage anticancer compounds—IMGN901, IMGN853, IMGN289, and IMGN529. We also license to other companies limited rights to use our technology with their antibodies to create products. The most advanced compound with our TAP technology is Kadcyla® (ado-trastuzumab emtansine), which was launched in the U.S.and Switzerland earlier this year by Genentech, a member of the Roche Group. Kadcyla comprises Roche's trastuzumab antibody, which is the active ingredient of their Herceptin® product, with our DM1 cell-killing agent attached using our thioether engineered linker. Six other TAP compounds and one unconjugated, or "naked," antibody product candidate are in clinical testing through our partnerships. Our partnership agreements entitle us to earn royalties on product sales, if any, and milestone payments with agreed upon achievements. Our current partners are: Amgen Inc., Bayer HealthCare (a subgroup of Bayer AG), Biotest AG, Eli Lilly and Company, or Lilly, Novartis Institutes for BioMedical Research, Inc., or Novartis, the Roche Group and Sanofi. We began receiving royalties on Kadcyla sales in the fourth quarter of our 2013 fiscal year.

We were organized as a Massachusetts corporation in 1981. Our principal offices are located at 830 Winter Street, Waltham, Massachusetts (MA) 02451, and our telephone number is (781) 895-0600. We maintain a website at www.immunogen.com, where certain information about us is available. Please note that information contained on the website is not a part of this document. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and any amendments to those reports are available free of charge through the "Investor Information" section of our website as soon as reasonably practicable after those materials have been electronically filed with, or furnished to, the Securities and Exchange Commission. We have adopted a Code of Corporate Conduct that applies to all our directors, officers and employees and a Senior Officer and Financial Personnel Code of Ethics that applies to our senior officers and financial personnel. Our Code of Corporate Conduct and Senior Officer and Financial Personnel Code of Ethics are available free of charge through the "Investor Information" section of our website.

3

Pipeline: Kadcyla and Earlier-Stage Product Candidates

Listed in the tables below are the compounds in the clinic through our own programs and our collaborations with other companies. Additional earlier-stage compounds are in development by us and our partners. The results in early clinical trials may not be predictive of results obtained in subsequent clinical trials and there can be no assurance that all of our or our collaborators' product candidates will advance or will demonstrate the level of safety and efficacy necessary to obtain regulatory approval.

Compounds Wholly Owned by ImmunoGen

Compound

|

Lead Indication(s) | Target | Most Advanced Status | |||||

|---|---|---|---|---|---|---|---|---|

IMGN901 |

Small-cell lung cancer | CD56 | Phase II | |||||

IMGN853 |

Ovarian cancer, non-small cell lung cancer | Folate receptor a | Phase I | |||||

IMGN289 |

Head and neck cancer, non-small cell lung cancer | EGFR | Active IND* | |||||

IMGN529 |

Non-Hodgkin lymphoma | CD37 | Phase I | |||||

Collaborative Partner Compounds**

Compound

|

Lead Indication(s) | Target | Partner | Most Advanced Status |

||||||

|---|---|---|---|---|---|---|---|---|---|---|

Kadcyla |

Previously treated HER2-positive metastatic breast cancer | HER2 | Roche | Marketed | ||||||

SAR3419 |

DLBCL, B-ALL*** | CD19 | Sanofi | Phase II | ||||||

SAR566658 |

Solid tumors | CA6 | Sanofi | Phase I | ||||||

SAR650984 |

Multiple myeloma | CD38 | Sanofi | Phase I | ||||||

AMG 172 |

Kidney cancer | CD70 | Amgen | Phase I | ||||||

AMG 595 |

Glioblastoma | EGFRvIII | Amgen | Phase I | ||||||

BAY 94-9343 |

Mesothelioma, ovarian cancer | Mesothelin | Bayer | Phase I | ||||||

BT-062 |

Multiple myeloma | CD138 | Biotest | Phase I | ||||||

- *

- IND: Investigational New Drug Application

- **

- All are ADCs, except for SAR650984, which is a "naked" antibody therapeutic

- ***

- DLBCL: diffuse large B-cell lymphoma; B-ALL: B-cell acute lymphoblastic leukemia

Kadcyla (previously referred to as T-DM1)

Kadcyla is an ADC that consists of trastuzumab, which is the active component of Roche's antibody therapeutic, Herceptin (trastuzumab), with our DM1 cell-killing agent attached using our thioether engineered linker. Kadcyla is in global development by Roche, under a license from us.

Kadcyla was granted marketing approval in February 2013 by the U.S. Food and Drug Administration, or FDA. It is approved for the treatment of HER2-positive metastatic breast cancer in patients who previously received Herceptin and a taxane. In the EMILIA Phase III trial, Kadcyla was found to significantly improve both overall survival and progression-free survival compared to standard of care. These were the co-primary endpoints of the trial. Kadcyla was also associated with fewer Grade 3 or greater adverse events, which are more severe side effects.

Roche also has applied for marketing approval of Kadcyla in the European Union and in Japan, with decisions there expected in late 2013 and in 2014, respectively.

4

Roche is developing Kadcyla for a number of additional indications, including for patients with

- •

- Metastatic HER2-positive breast cancer that has not previously been treated—Roche is assessing Kadcyla for

this use in the Phase III trial, MARIANNE. Roche intends to use MARIANNE results, if favorable, to apply in 2015 for marketing approval of Kadcyla for this indication, both used alone and used

with Perjeta® (pertuzumab). Roche expects the data from this trial in 2014.

- •

- Early stage HER2-positive breast cancer—Roche plans to evaluate Kadcyla in several early stage HER2-positive

breast cancer settings. In early 2013, patient enrollment commenced in its KATHERINE Phase III trial, which evaluates Kadcyla for the treatment of patients with residual invasive disease

following pre-operative therapy. Roche has said it plans to initiate registration trials evaluating Kadcyla for use in the adjuvant and neoadjuvant settings.

- •

- Advanced HER2-positive gastric cancer—Roche is evaluating Kadcyla for the treatment of patients with this cancer in its GATSBY trial. Roche intends to use the results from GATSBY, if favorable, to apply in 2015 for marketing approval for this use.

IMGN901

Our most advanced wholly owned product candidate is IMGN901, or lorvotuzumab mertansine. We created IMGN901 for the treatment of CD56-positive cancers, which include small cell lung cancer, or SCLC, Merkel cell carcinoma, multiple myeloma, ovarian cancers, carcinoid tumors, and other cancers of neuroendocrine origin. IMGN901 consists of a CD56-targeting antibody with our DM1 cell-killing agent attached using one of our hindered disulfide linkers.

In early clinical testing, IMGN901 has been found to be generally well tolerated and to demonstrate evidence of activity when used as a single agent to treat CD56-positive solid tumors and multiple myeloma. IMGN901 also has been found to be generally well tolerated and to demonstrate evidence of activity when used in combination with Revlimid® (lenalidomide) and dexamethasone for treating CD56-positive multiple myeloma.

In preclinical models of SCLC, use of IMGN901 in combination with etoposide plus carboplatin, or E/C, was found to achieve markedly greater anticancer activity than either IMGN901 or E/C alone. E/C is a standard of care for the treatment of newly diagnosed SCLC. Based on the encouraging activity seen both preclinically and in early clinical testing, we are assessing IMGN901 for the treatment of patients with newly diagnosed extensive disease SCLC in our Phase II NORTH trial. Patients in the NORTH trial receive treatment with IMGN901 plus E/C or with E/C alone. We expect to make certain development-related decisions based on the results from this trial.

IMGN853

We created our IMGN853 product candidate to treat cancers that highly express folate receptor a, or FRa. FRa-positive cancers include many cases of ovarian cancer, endometrial cancer and adenocarcinoma non-small cell lung cancer, or NSCLC. IMGN853 consists of a FRa-targeting antibody with our potent DM4 cell-killing agent attached using one of our linkers engineered to counteract one drug resistance pathway that cancer cells can develop.

IMGN853 is currently in Phase I clinical testing. Once the maximum tolerated dose, or MTD, has been established in the dose-finding phase of the trial, we plan to evaluate IMGN853 used at that dose in the expansion phase of the trial. There, IMGN853 will be evaluated specifically in patients with either FRa-positive ovarian cancer, endometrial cancer or adenocarcinoma NSCLC. The first IMGN853 clinical data were reported at a medical conference in June 2013. The compound was found to be generally well tolerated and to demonstrate evidence of activity.

5

IMGN289

Our IMGN289 product candidate is a potential new treatment for cancers that highly express EGFR. EGFR-positive cancers include squamous cell carcinoma of the head and neck, or SCCHN, and types of NSCLC. IMGN289 consists of our EGFR-binding antibody with our DM1 cell-killing agent attached using our thioether linker. In preclinical testing, the antibody component of IMGN289 was found to have meaningful anticancer activity against EGFR-positive cancer cells sensitive to EGFR inhibition. The full product candidate, which includes DM1, demonstrates superior activity against these cancers, and also against EFGR-positive cancers not sensitive to EGFR inhibitors. The DM1 enables IMGN289 to kill EGFR-positive cancer cells by a second method that is independent of the sensitivity of these cells to EGFR inhibitors.

We submitted an IND for IMGN289 to the FDA in late June 2013; it became active in late July 2013. We are preparing to begin Phase I testing of the compound.

IMGN529

Our IMGN529 TAP compound targets CD37, which is expressed on B-cell malignancies such as non-Hodgkin lymphoma, or NHL, and on chronic lymphocytic leukemia. ImmunoGen scientists have found the expression profile of CD37 on NHL subtypes to be similar to that of CD20, the target of Rituxan®.

IMGN529 comprises an antibody that, in preclinical testing, has demonstrated meaningful anticancer activity, our DM1 cell-killing agent, and our thioether engineered linker. We believe IMGN529 is a highly differentiated product candidate for B-cell malignancies because it combines the anticancer activity of its antibody component with the actions of one of our potent cell-killing agents. IMGN529 is in Phase I clinical testing for the treatment of NHL.

Compounds in Development by Our Partners

In addition to Kadcyla, seven other compounds are in clinical testing through our collaborations with other companies. Additionally, several of our collaborative partners have TAP compounds in earlier stages of development.

Sanofi

Each of the three clinical-stage Sanofi compounds—SAR3419, SAR566658 and SAR650984—was created as part of a broader research collaboration between ImmunoGen and Sanofi. The antibodies in all three compounds were developed by ImmunoGen scientists. The two TAP compounds, SAR3419 and SAR566658, contain our DM4 cell-killing agent attached with one of our hindered disulfide linkers. Sanofi has additional compounds created under that agreement in earlier stages of development.

SAR3419 targets CD19 and is a potential treatment for CD19-expressing B-cell malignancies. Sanofi is evaluating SAR3419 in Phase II clinical testing for both a type of NHL called diffuse large B-cell lymphoma, or DLBCL, and in B-cell acute lymphoblastic leukemia, or B-ALL. In Phase I clinical testing, SAR3419 showed encouraging efficacy and tolerability in the treatment of NHL previously treated with approved anticancer agents.

SAR566658 is a TAP compound in development as a potential treatment for CA6-expressing solid tumors, including ovarian cancers. Sanofi is evaluating SAR566658 in Phase I clinical testing.

SAR650984 is a CD38-targeting therapeutic, or "naked", antibody created by ImmunoGen for the treatment of hematological malignancies. It is in Phase I clinical testing for the treatment of blood cancers including multiple myeloma.

6

Amgen

Pursuant to the terms of a separate right-to-test agreement entered into in 2000, Amgen took licenses in 2009 for rights to use our TAP technology to develop therapeutics targeting CD70 and EGFRvIII and has since advanced product candidates AMG 172 and AMG 595 into clinical testing. In late 2012 and in early 2013, Amgen took licenses under the same right-to-test agreement for rights to use our TAP technology to develop therapeutics to two additional targets, which are undisclosed. Amgen has no remaining rights under the right-to-test agreement to take licenses to additional targets.

AMG 172 is a potential treatment for CD70-expressing cancers, and is in Phase I clinical testing for the treatment of patients with clear cell renal cell carcinoma. AMG 595 is a potential treatment for EGFRvIII-expressing cancers. It is in Phase I clinical testing for the treatment of patients with glioblastoma.

Bayer

BAY 94-9343 was created by Bayer under a single-target license agreement that granted Bayer rights to use our technology to develop TAP compounds to the target, mesothelin, and is currently in Phase I clinical testing.

The first clinical data for BAY 94-9343 were reported at a scientific conference in early 2013. These data were from the dose-escalation part of its Phase I trial and showed that the compound was generally well tolerated and demonstrated evidence of activity among patients with mesothelin-expressing solid tumors treated at higher dose levels. The compound is now being evaluated in the expansion phase of the trial specifically in patients with mesothelioma and in patients with ovarian cancer. It has been granted orphan drug status for the treatment of mesothelioma.

Biotest

BT-062 was created by Biotest under a single-target license agreement that granted Biotest rights to use our TAP technology with antibodies that target CD138, an antigen found on multiple myeloma and certain solid tumors. We have opt-in rights with respect to BT-062 in the U.S.

Encouraging Phase I clinical data have been reported with BT-062 used as a single agent to treat patients with multiple myeloma. Biotest is assessing BT-062 used as part of a combination regimen for this cancer. In preclinical testing, BT-062 demonstrated activity against several types of aggressive solid tumors. It is expected to advance into clinical testing for the treatment of one or more types of solid tumors.

Lilly and Novartis

Our most recent partnerships are with Lilly and Novartis. Compounds are in preclinical development under these agreements.

Incidence of Relevant Cancers

Cancer remains a leading cause of death worldwide, and is the second leading cause of death in the U.S. The American Cancer Society, or ACS, estimates that in 2013 approximately 1.7 million new cases of cancer will be diagnosed in the U.S. and that approximately 580,000 people will die from the disease. The total number of people living with cancer significantly exceeds the number of patients diagnosed with cancer in a given year as patients can live with cancer for a year or longer. Additionally, the potential market for anticancer drugs exceeds the number of patients treated as many types of cancer typically are treated with multiple compounds at the same time and because patients often receive a number of drug regimens sequentially.

7

Below is information about incidence of cancers we are seeking to treat with our wholly owned compounds. For the approved product, Kadcyla, information about the incidence of HER2-positive breast cancer is available from Roche, the marketer of the product.

IMGN901—The lead indication for IMGN901is for the treatment of extensive disease SCLC. Based on our own studies and scientific literature, we believe that CD56 is expressed on almost all cases of SCLC. Based on ACS estimates and other sources, we believe that at least 22,800 new cases of SCLC will be diagnosed in the U.S. in 2013. SCLC tends to spread broadly through the body quite early in the course of the disease, and—according to the ACS—approximately two-thirds of patients with SCLC have extensive disease at the time of diagnosis.

IMGN853—Our IMGN853 compound is a potential treatment for many cases of epithelial ovarian cancer, endometrial cancer and adenocarcinoma NSCLC. Based on published sources, we believe approximately 22,000 new cases of ovarian cancer will be diagnosed in the US in 2013 and epithelial ovarian cancer accounts for approximately 85% to 90% of these ovarian cancer cases. We believe that approximately 49,600 cases of endometrial cancers will be diagnosed in the US in 2013. Additionally, based on published sources, we believe that approximately 194,000 new cases of NSCLC will be diagnosed in the US in 2013, and that approximately 40% of these cases are the adenocarcinoma subtype.

IMGN289—Our IMGN289 compound is a potential treatment for many cases of head and neck cancer and types of NSCLC. The ACS estimates that approximately 53,600 new cases of head and neck cancers will be diagnosed in 2013. Research conducted at ImmunoGen found that over 90% of these types of cancer strongly express EGFR. Based on ACS estimates, we believe approximately 194,000 new cases of NSCLC will be diagnosed in the U.S. in 2013. This figure comprises three main subtypes—adenocarcinoma, squamous cell carcinoma, and large cell carcinoma. These subtypes account for approximately 40%, 25-30%, and 10-15% of NSCLC diagnoses, respectively. Research with tumor samples conducted at ImmunoGen found that approximately 20% of adenocarcinoma cases and about half of squamous and of large cell carcinoma cases strongly express EGFR.

IMGN529—We are assessing our IMGN529 compound for the treatment of NHL. Based on ACS estimates, we believe approximately 69,700 new cases of NHL will be diagnosed in the U.S. in 2013.

Out-licenses and Collaborations

We selectively out-license restricted access to our TAP technology to other companies to provide us with cash to fund our own product programs and to expand the utilization of our technology. These agreements typically provide the licensee with rights to use our TAP technology with antibodies to a defined target to develop products. The licensee is generally responsible for the development, clinical testing, manufacturing, registration and commercialization of any resulting product candidate. As part of these agreements, we are generally entitled to receive upfront fees, potential milestone payments, royalties on the sales of any resulting products and research and development funding based on activities performed at our collaborative partner's request. We are also compensated for preclinical and clinical materials supplied to our partners.

We only receive royalty payments from our out-licenses after a product candidate developed under the license has been approved for marketing and commercialized. Additionally, the largest milestone payments under our existing collaborations usually are on later-stage events, such as commencement of pivotal clinical trials and product approval. Achievement of product approval requires, at a minimum, favorable completion of preclinical development and evaluation, assessment of early-stage clinical trials, advancement into pivotal Phase II and/or Phase III clinical testing, completion of this later-stage clinical testing with favorable results, and completion of regulatory submissions and a positive regulatory decision. Currently, we have a license with Roche relating to Kadcyla that provides us with royalty revenue and may provide us with significant milestone payments in the foreseeable future.

8

Below is a table setting forth our active agreements, the number of targets licensed and current status of the product candidates being developed thereunder:

Partner

|

Agreement Type | Effective Date(s) | Development Status(1) | |||

|---|---|---|---|---|---|---|

| Roche(2) | Multiple single-targets | 2000 | US Marketing Approval | |||

| Amgen(3) | Multiple single-targets | 2000 | Phase I | |||

| Sanofi | Multiple single-targets | 2003 | Phase II | |||

| Sanofi(4) | Right-to-test | 2006 | Research/Preclinical | |||

| Biotest | Single-target | 2006 | Phase I | |||

| Bayer HealthCare | Single-target | 2008 | Phase I | |||

| Novartis(4) | Right-to-test | 2010 | Research/Preclinical | |||

| Lilly(4) | Right-to-test | 2011 | Research/Preclinical |

- (1)

- For

agreements involving multiple targets, development status denotes the most advanced program under the collaboration.

- (2)

- Roche

has five single-target licenses. Pursuant to the license covering the target HER2, which was entered into in 2000, a product candidate,

Kadcyla, has received marketing approval in the US and Switzerland and Roche has submitted a marketing application for the compound in the EU and Japan. The remaining four licenses were entered into

between 2005 and 2008, and the development status of product candidates under each of those licenses is research/preclinical.

- (3)

- Amgen

has three exclusive, single-target licenses and one non-exclusive, single-target license.

- (4)

- Sanofi, Novartis and Lilly each have the right to take a defined number of exclusive, single-target options that provide the right to take single-target licenses, on pre-negotiated terms, to specified targets during the respective option periods. As of June 30, 2013, Novartis has taken one license to two related targets, one on an exclusive basis and one on a non-exclusive basis. In August 2013, Lilly took an exclusive license to a single target.

Roche

In May 2000, we granted Roche, through its Genentech unit, an exclusive development and commercialization license to our maytansinoid TAP technology for use with antibodies or other proteins that target HER2, such as trastuzumab. In February 2013, the US FDA granted marketing approval to the anti-HER2 TAP compound, Kadcyla. We received a $2 million upfront payment from Roche upon execution of the agreement. We are also entitled to receive up to a total of $44 million in milestone payments, plus tiered royalties on the commercial sales of Kadcyla or any other resulting products as described below.

The royalty term is determined on a country-by-country basis, and is initially 10 years from the date of first commercial sale of Kadcyla in the country. If, on such 10th anniversary, Kadcyla is covered by a valid claim under any patents controlled by us (excluding patents jointly owned by us and Genentech), then royalties remain payable on sales of Kadcyla in that country for an additional 2 years and no more.

The following two territories are used in our agreement with Genentech to determine the Kadcyla sales levels for the calculation of the applicable tiered royalty levels: (1) the U.S. and (2) the rest of the world. Royalties on sales of Kadcyla are determined based on annual calendar year net sales in each

9

territory in accordance with a tiered structure calculated separately in each of the two territories as follows:

- •

- 3% of net sales up to $250 million;

- •

- 3.5% of net sales above $250 million and up to $400 million;

- •

- 4% of net sales above $400 million and up to $700 million; and

- •

- 5% of net sales above $700 million.

The sales in the country count towards the annual sales in that territory for purposes of calculation of sales tiers.

Royalties will be reduced to a flat 2% of net sales in any country at any time during the royalty term in which Kadcyla is not covered by a valid claim under any patents controlled by us (excluding patents jointly owned by us and Genentech or solely owned by Genentech) in such country.

The license agreement also provides for certain adjustments to the royalties payable to us if:

- •

- Genentech makes certain third party license payments in order to exploit the TAP technology components of Kadcyla,

although such adjustments would in no event reduce the royalties payable for any country below the greater of 50% of the royalties otherwise payable with respect to sales of Kadcyla in such country,

or 2% of net sales in such country; or

- •

- a third party obtains regulatory approval in a country to market and sell a product containing a conjugate of an anti-HER2 antibody with a maytansinoid, in which case royalties will be reduced to a flat 1% of net sales of Kadcyla in such country during the royalty term as long as such competing product has not been withdrawn from the market in such country.

As of the date of this annual report on Form 10-K, we are unaware of any facts or circumstances that would give rise to the adjustments described in either of the above two circumstances.

Roche may terminate this agreement for convenience at any time upon 90 days' prior written notice to us. The agreement may also be terminated by either party for a material breach by the other, subject to notice and cure provisions. Unless earlier terminated, the agreement will continue in effect until the expiration of Roche's royalty obligations.

The US marketing approval of Kadcyla in February 2013 triggered a $10.5 million milestone payment to us. Through June 30, 2013, we have received and recognized a total of $24.0 million in milestone payments under this agreement. The next potential milestone we will be entitled to receive will be either a $5 million regulatory milestone for marketing approval of Kadcyla in Europe or a $5 million regulatory milestone for marketing approval of Kadcyla in Japan, depending on which occurs first.

Roche, through its Genentech unit, also has licenses for the exclusive right to use our maytansinoid TAP technology with antibodies to four undisclosed targets, which were granted under the terms of a separate May 2000 right-to-test agreement with Genentech. For each of these licenses we received a $1 million license fee and are entitled to receive up to a total of $38 million in milestone payments and also royalties on the sales of any resulting products. We have not received any milestone payments from these agreements through June 30, 2013. Roche is responsible for the development, manufacturing, and marketing of any products resulting from these licenses. Roche no longer has the right to take additional licenses under the right-to-test agreement.

Amgen

In September 2000, we entered into a ten-year right-to-test agreement with Abgenix, Inc. which was later acquired by Amgen. The agreement provided Amgen with the right to (a) test our maytansinoid TAP technology with Amgen's antibodies under a right-to-test, or research, license,

10

(b) take options, with certain restrictions, to individual targets selected by Amgen on either an exclusive or non-exclusive basis for specified option periods and (c) upon exercise of those options, take exclusive or non-exclusive licenses to use our maytansinoid TAP technology to develop and commercialize products directed to the specified targets on previously agreed-upon terms. Amgen no longer has the right to take additional options under the right-to-test agreement and there are no unexercised options outstanding.

Under the right-to-test agreement, in September 2009, November 2009 and December 2012, Amgen took three exclusive development and commercialization licenses, for which we received an exercise fee of $1 million for each license taken. In May 2013, Amgen took one non-exclusive development and commercialization license, for which we received an exercise fee of $500,000. We are entitled to receive up to a total of $34 million in milestone payments for each exclusive license and up to a total of $17 million in milestone payments for the non-exclusive license, plus in each case, royalties on the commercial sales of any resulting products.

In November 2011, the IND applications to the FDA for two compounds developed under two of the exclusive development and commercialization licenses became active, which triggered two $1 million milestone payments to us. The next potential milestone we will be entitled to receive under either of these two development and commercialization licenses will be a development milestone for the first dosing of a patient in a Phase II clinical trial, which will result in a $3 million payment being due. The next potential milestone we will be entitled to receive under the December 2012 development and commercialization license will be a development milestone for IND approval which will result in a $1 million payment being due to us. The next potential milestone we will be entitled to receive under the May 2013 development and commercialization license will be a development milestone for IND approval which will result in a $500,000 payment being due to us.

Amgen may terminate each development and commercialization license for convenience upon prior notice to us. Each license may also be terminated by either party for a material breach by the other, subject to notice and cure provisions. Unless earlier terminated, each license will continue in effect until the expiration of Amgen's royalty obligations, which are determined on a product-by-product and country-by-country basis. For each product and country, Amgen's royalty obligations commence with the first commercial sale of that product in that country, and extend until the later of either the expiration of the last-to-expire ImmunoGen patent covering that product in that country or the expiration for that country of the minimum royalty period specified in each development and commercialization license.

Sanofi

Collaboration Agreement

In July 2003, we entered into a broad collaboration agreement with Sanofi (formerly Aventis) to discover, develop and commercialize antibody-based products. The collaboration agreement provides Sanofi with worldwide development and commercialization rights to new antibody-based products directed to targets that are included in the collaboration, including the exclusive right to use our maytansinoid TAP technology in the creation of products directed to these targets. The product candidates (targets) currently in development under the collaboration include SAR3419 (CD19), SAR650984 (CD38), SAR566658 (DS6, also known as CA6) and two earlier-stage compounds that have yet to be disclosed. For each of the targets included in the collaboration at this time, we are entitled to receive up to a total of $21.5 million in milestone payments, plus royalties on the commercial sales of any resulting products.

The agreement may be terminated by either party for a material breach by the other, subject to notice and cure provisions. Unless earlier terminated, the agreement will continue in effect until the expiration of Sanofi's royalty obligations, which are determined on a product-by-product and country-by-country basis. For each product and country, Sanofi's royalty obligations commence upon

11

first commercial sale of that product in that country, and extend until the later of either the expiration of the last-to-expire ImmunoGen patent covering that product in that country or the expiration for that country of the minimum royalty period specified in the agreement.

The collaboration agreement also provides us an option to certain co-promotion rights in the U.S. on a product-by-product basis. The terms of the collaboration agreement allow Sanofi to terminate our co-promotion rights if there is a change in control of our company.

Through June 30, 2013, we have received and recognized a total of $16.5 million in milestone payments related to compounds covered under this agreement now and in the past, including a total of $8 million in milestone payments related to two product candidates previously in the collaboration that have been returned to us along with the rights to the respective targets.

The next potential milestone we will be entitled to receive with respect to SAR3419 will be for initiation of a Phase III clinical trial, which will result in a $3 million payment being due. The next potential milestone we will be entitled to receive with respect to each of SAR566658 and for SAR650984 will be a development milestone for initiation of a Phase IIb clinical trial (as defined in the agreement), which will result in each case in a $3 million payment being due. The next potential milestone we will be entitled to receive for each of the unidentified targets will be a development milestone for commencement of a Phase I clinical trial, which will result in a $1 million payment being due.

Right-to-Test Agreement

In December 2006, we entered into a separate right-to-test agreement with Sanofi. The agreement provides Sanofi with the right to (a) test our maytansinoid TAP technology with Sanofi's antibodies to targets that were not included in the collaboration agreement described above under a right-to-test, or research, license, (b) take exclusive options, with certain restrictions, to individual targets selected by Sanofi for specified time periods and (c) upon exercise of those options, take exclusive licenses to use our maytansinoid TAP technology to develop and commercialize products directed to the specified targets on terms agreed upon at the inception of the right-to-test agreement. The right-to-test agreement had a three-year original term from the activation date that was renewed by Sanofi in August 2011for its final three-year term by payment of a $2 million extension fee. No additional extensions are included in this agreement.

For each development and commercialization license taken, we are entitled to receive an exercise fee of $2 million and up to a total of $30 million in milestone payments, plus royalties on the commercial sales of any resulting products.

Each development and commercialization license may be terminated by either party for a material breach by the other, subject to notice and cure provisions. Unless earlier terminated, each license will continue in effect until the expiration of Sanofi's royalty obligations, which are determined on a product-by-product and country-by-country basis. For each product and country, Sanofi's royalty obligations commence with the first commercial sale of that product in that country, and extend until the later of either the expiration of the last-to-expire ImmunoGen patent covering that product in that country or the expiration for that country of the minimum royalty period specified in each development and commercialization license. No development and commercialization license has yet been taken under the right-to-test agreement.

Biotest

In July 2006, we granted Biotest an exclusive development and commercialization license to our maytansinoid TAP technology for use with antibodies that target CD138. The product candidate BT-062 is in development under this agreement. We received a $1 million upfront payment from Biotest upon

12

execution of the agreement. We are also entitled to receive up to a total of $35.5 million in milestone payments, plus royalties on the commercial sales of any resulting products.

The agreement also provides us with the right to elect, at specific stages during the clinical evaluation of any compound created under the agreement, to participate in the U.S. development and commercialization of that compound in lieu of receiving the milestone payments not yet earned and royalties on sales in the U.S. We can exercise this right during an exercise period specified in the agreement by notice and payment to Biotest of an agreed upon opt-in fee of $15 million. Upon exercise of this right, we would share equally with Biotest the associated costs of product development and commercialization in the U.S. along with the profit, if any, from product sales in the U.S.

Biotest may terminate the agreement for convenience at any time prior to our election to participate in the U.S. development and commercialization of a compound created under this agreement upon prior notice to us. The agreement may also be terminated by either party for a material breach by the other, subject to notice and cure provisions. Unless earlier terminated, the agreement will continue in effect until the expiration of Biotest's royalty obligations, which are determined on a product-by-product and country-by-country basis. For each product and country, Biotest's royalty obligations commence upon first commercial sale of that product in that country, and extend until the later of either the expiration of the last-to-expire ImmunoGen patent covering that product in that country or the expiration for that country of the minimum royalty period specified in the agreement.

Through June 30, 2013, we have received and recognized a total of $500,000 in milestone payments under this agreement. The next potential milestone we will be entitled to receive will be a development milestone for commencement of a Phase IIb clinical trial (as defined in the agreement) which will result in a $2 million payment being due.

Bayer HealthCare

In October 2008, we granted Bayer HealthCare an exclusive development and commercialization license to our maytansinoid TAP technology for use with antibodies or other proteins that target mesothelin. The product candidate BAY 94-9343 is currently in development under this agreement. We received a $4 million upfront payment upon execution of the agreement. We are also entitled to receive, for each product developed and marketed by Bayer HealthCare under this agreement, up to a total of $170.5 million in milestone payments, plus royalties on the commercial sales of any resulting products.

Bayer HealthCare may terminate the agreement for convenience at any time upon prior written notice to us. The agreement may also be terminated by either party for a material breach by the other, subject to notice and cure provisions. We may also terminate the agreement upon the occurrence of specified events. Unless earlier terminated, the agreement will continue in effect until the expiration of Bayer HealthCare's royalty obligations, which are determined on a product-by-product and country-by-country basis. For each product and country, Bayer HealthCare's royalty obligations commence upon first commercial sale of that product in that country, and extend until the later of either the expiration of the last-to-expire ImmunoGen patent covering that product in that country or the expiration for that country of the minimum royalty period specified in the agreement.

Through June 30, 2013, we have received and recognized a total of $3 million in milestone payments under this agreement. The next potential milestone we will be entitled to receive will be a development milestone for commencement of a non-pivotal Phase II clinical trial, which will result in a $4 million payment being due.

13

Novartis

In October 2010, we entered into a right-to-test agreement with Novartis. The agreement provides Novartis with a right to (a) test our TAP technology with Novartis' antibodies directed to individual targets selected by Novartis under a right-to-test, or research, license, (b) take exclusive options, with certain restrictions, to individual targets selected by Novartis for specified option periods, and (c) upon exercise of those options take exclusive licenses to use our TAP technology to develop and commercialize products for a specified number of individual targets on terms agreed upon at the inception of the right-to-test agreement. The initial term of the right-to-test agreement is three years, which may be extended by Novartis for up to two additional one-year periods by the payment of additional consideration. Novartis must exercise its options for the development and commercialization licenses by the end of the term of the right-to-test agreement, after which any then outstanding options will lapse.

We received a $45 million upfront payment in connection with the execution of the right-to-test agreement, and we are also entitled to receive additional payments under the agreement for research and development activities performed on behalf of Novartis during the term of the agreement. For each development and commercialization license taken, we are entitled to receive an exercise fee of $1 million and up to a total of $199.5 million in milestone payments, plus royalties on the commercial sales of any resulting products.

Effective March 29, 2013, we and Novartis amended the right-to-test agreement so that Novartis can take a license to develop and commercialize products directed at two pre-defined and related undisclosed targets, one target licensed on an exclusive basis and the other target initially licensed on a non-exclusive basis. The target licensed on a non-exclusive basis may be converted to an exclusive target by notice and payment to us of an agreed upon fee of at least $5 million, depending on specific circumstances. We received a $3.5 million fee in connection with the execution of the amendment to the agreement. We may be required to credit this fee against future milestone payments if Novartis discontinues the development of a specified product under certain circumstances.

In connection with the amendment, on March 29, 2013, Novartis took the license referenced above under the right-to-test agreement, as amended, enabling it to develop and commercialize products directed at the two targets. We received a $1 million upfront fee with the execution of this license. Additionally, the execution of this license provides us the opportunity to receive milestone payments totaling $199.5 million or $238 million, depending on the composition of any resulting products. The first potential milestone we will be entitled to receive will be a $5.0 million development milestone for commencement of a Phase I clinical trial.

Novartis may terminate any development and commercialization license for convenience upon prior notice to us. Each license may also be terminated by either party for a material breach by the other, subject to notice and cure provisions. Unless earlier terminated, each development and commercialization license will continue in effect until the expiration of Novartis' royalty obligations, which are determined on a product-by-product and country-by-country basis. For each product and country, Novartis' royalty obligations commence upon first commercial sale of that product in that country, and extend until the later of either the expiration of the last-to-expire ImmunoGen patent covering that product in that country or the expiration for that country of the minimum royalty period specified in each license.

Lilly

In December 2011, we entered into a three-year right-to-test agreement with Lilly. The agreement provides Lilly with the right to (a) take exclusive options, with certain restrictions, to individual targets selected by Lilly for specified option periods, (b) test our maytansinoid TAP technology with Lilly's antibodies directed to the optioned targets under a right-to-test, or research, license, and (c) upon exercise of those options take exclusive licenses to use our maytansinoid TAP technology to develop

14

and commercialize products for a specified number of individual targets on terms agreed upon at the inception of the right-to-test agreement. Lilly must exercise its options for the development and commercialization licenses by the end of the term of the right-to-test agreement, after which any then outstanding options will lapse. Under the terms of the agreement, Lilly took an exclusive development and commercialization license to a single target in August 2013.

We received a $20 million upfront payment in connection with the execution of the agreement, and we are also entitled to receive additional payments under the agreement for research and development activities performed under the agreement on behalf of Lilly during the term of the research license. For the first development and commercialization license taken, which occurred in August 2013, we are entitled to receive up to a total of $200.5 million in milestone payments, plus tiered royalties in the mid-single to low-double digits on the commercial sales of any resulting products. For each subsequent development and commercialization license taken, we are entitled to receive an exercise fee of $2 million and up to a total of $199 million in milestone payments, plus royalties on the commercial sales of any resulting products.

Lilly may terminate any development and commercialization license for convenience upon prior notice to us. Each license may also be terminated by either party for a material breach by the other, subject to notice and cure provisions. We may also terminate the agreement upon the occurrence of specified events. Unless earlier terminated, each development and commercialization license will continue in effect until the expiration of Lilly's royalty obligations, which are determined on a product-by-product and country-by-country basis. For each product and country, Lilly's royalty obligations commence upon first commercial sale of that product in that country, and extend until the later of either the expiration of the last-to-expire ImmunoGen patent covering that product in that country or the expiration for that country of the minimum royalty period specified in each license.

In-Licenses

From time to time we may in-license certain rights to targets or technologies for use in conjunction with our internal efforts to develop TAP compounds and related technologies. These licenses include rights to certain antibodies. In exchange, we may be obligated to pay upfront fees, potential milestone payments and royalties on any product sales.

Patents, Trademarks and Trade Secrets

Our intellectual property strategy centers on obtaining patent protection for our proprietary technologies and product candidates. As of June 30, 2013, our patent portfolio had a total of 459 issued patents worldwide and 477 pending patent applications worldwide that we own or license from third parties. We seek to protect our TAP technology and our product candidates through a multi-pronged approach. In this regard, we have patents and patent applications covering antibodies and other cell-binding agents, linkers, maytansinoid and other cell-killing agents, and complete antibody-drug conjugates, or immunoconjugates, comprising these components and methods of making and using each of the above. Typically, multiple issued patents and pending patent applications cover various aspects of each product candidate.

We consider our maytansinoid technology to be a key component of our overall corporate strategy. We currently own 42 issued U.S. patents covering various embodiments of our maytansinoid technology including claims directed to certain maytansinoids, antibody-maytansinoid conjugates and other cell-binding agents used with maytansinoids, and methods of making and using the same. In all cases, we have received or are applying for comparable patents in other jurisdictions including Europe and Japan. We have issued patents that cover numerous aspects of the manufacture of both our DM1 and DM4 cell-killing agents. These issued patents remain in force until various times between 2020 and 2026. We also have several composition of matter patents covering various aspects of our DM4

15

cell-killing agent and antibody-maytansinoid conjugates incorporating DM4 that are expected to remain in force until 2024-2025.

Our intellectual property strategy also includes pursuing patents directed to linkers, antibodies, conjugation methods, immunoconjugate formulations and the use of specific antibodies and immunoconjugates to treat certain diseases. In this regard, we have issued patents and pending patent applications related to many of our linker technologies. These issued patents, expiring in 2021-2029, and any patents which may issue from the patent applications, cover antibody-maytansinoid conjugates using these linkers. We also have issued U.S. patents and pending patent applications covering methods of assembling immunoconjugates from their constituent antibody, linker and cell-killing agent moieties. These issued patents will expire in 2021-2027, while any patents that may issue from pending patent applications also covering various aspects of these technologies will, if issued, expire between 2021 and 2034. We also have issued patents and pending patent applications related to monoclonal antibodies that may be a component of a TAP compound or may be developed as a therapeutic, or "naked," antibody anticancer compound. Among these patents is an issued U.S. patent claiming a method of humanizing murine antibodies to avoid their detection by the human immune system. We have received patents in other jurisdictions, including Europe and Japan, that correspond to our antibody humanization U.S. patent. These patents will expire between 2013 and 2014.

We expect our continued work in each of these areas will lead to other patent applications. In all such cases, we will either be the assignee or owner of such patents or have an exclusive license to the technology covered by the patents. For example, we also own issued patents covering proprietary derivatives of non-maytansinoid cell-killing molecules. However, we do not currently consider these additional patent families to be material to our business.

The rates at which we are entitled to receive royalties based on sales of Kadcyla in any particular country depend in part on whether the manufacture, use or sale of Kadcyla is covered by ImmunoGen patent rights in that country. In this regard, we own patents in the U.S. and Europe covering the composition of matter of Kadcyla that expire at the earliest in 2023 and 2024, respectively, and may be eligible for extension of those terms under applicable patent laws in those jurisdictions. We also own patents in the U.S. and Europe that cover various elements of the manufacture of Kadcyla, with expiration dates extending to at least 2027 and 2026, respectively. Notwithstanding these patent terms, the period during which we are entitled to receive royalties based on sales of Kadcyla in any country does not extend beyond the 12th anniversary of the date of the first commercial sale of Kadcyla in such country.

We have in-licensed intellectual property relating to our IMGN901 product candidate from Dana-Farber Cancer Institute. We do not believe that the terms of this license are material to our business or prospects.

We cannot provide assurance that the patent applications will issue as patents or that any patents, if issued, will provide us with adequate protection against competitors with respect to the covered products, technologies or processes. Defining the scope and term of patent protection involves complex legal and factual analyses and, at any given time, the result of such analyses may be uncertain. In addition, other parties may challenge our patents in litigation or administrative proceedings resulting in a partial or complete loss of certain patent rights owned or controlled by ImmunoGen, Inc. Furthermore, as a patent does not confer any specific freedom to operate, other parties may have patents that may block or otherwise hinder the development and commercialization of our technology.

In addition, many of the processes and much of the know-how that are important to us depend upon the skills, knowledge and experience of our key scientific and technical personnel, which skills, knowledge and experience are not patentable. To protect our rights in these areas, we require that all employees, consultants, advisors and collaborators enter into confidentiality agreements with us. Further, we require that all employees enter into assignment of invention agreements as a condition of

16

employment. We cannot provide assurance, however, that these agreements will provide adequate or any meaningful protection for our trade secrets, know-how or other proprietary information in the event of any unauthorized use or disclosure of such trade secrets, know-how or proprietary information. Further, in the absence of patent protection, we may be exposed to competitors who independently develop substantially equivalent technology or otherwise gain access to our trade secrets, know-how or other proprietary information.

Competition

We focus on highly competitive areas of product development. Our competitors include major pharmaceutical companies and other biotechnology firms. For example, Pfizer, Seattle Genetics, Rocheand Bristol-Myers Squibb have programs to attach a proprietary cell-killing small molecule to an antibody for targeted delivery to cancer cells. Pharmaceutical and biotechnology companies, as well as other institutions, also compete with us for promising targets for antibody-based therapeutics and in recruiting highly qualified scientific personnel. Many competitors and potential competitors have substantially greater scientific, research and product development capabilities, as well as greater financial, marketing and human resources than we do. In addition, many specialized biotechnology firms have formed collaborations with large, established companies to support the research, development and commercialization of products that may be competitive with ours.

In particular, competitive factors within the antibody and cancer therapeutic market include:

- •

- the safety and efficacy of products;

- •

- the timing of regulatory approval and commercial introduction;

- •

- special regulatory designation of products, such as Orphan Drug designation; and

- •

- the effectiveness of marketing, sales, and reimbursement efforts.

Our competitive position depends on our ability to develop effective proprietary products, implement clinical development programs, production plans and marketing plans, including collaborations with other companies with greater marketing resources than ours, and to obtain patent protection and secure sufficient capital resources.

Continuing development of conventional and targeted chemotherapeutics by large pharmaceutical companies and biotechnology companies may result in new compounds that may compete with our product candidates. Antibodies developed by certain of these companies have been approved for use as cancer therapeutics. In the future, new antibodies or other targeted therapies may compete with our product candidates. Other companies have created or have programs to create potent cell-killing agents for attachment to antibodies. These companies may compete with us for technology out-license arrangements.

Regulatory Matters

Government Regulation and Product Approval

Government authorities in the U.S., at the federal, state and local level, and other countries extensively regulate, among other things, the research, development, testing, manufacture, quality control, approval, labeling, packaging, storage, record-keeping, promotion, advertising, distribution, marketing and export and import of products such as those we are developing. A new drug must be approved by the FDA through the new drug application, or NDA, process and a new biologic must be approved by the FDA through the biologics license application, or BLA, process before it may be legally marketed in the U.S.

17

U.S. Drug Development Process

In the U.S., the FDA regulates drugs under the federal Food, Drug, and Cosmetic Act, or FDCA, and in the case of biologics, also under the Public Health Service Act, or PHSA, and implementing regulations. The process of obtaining regulatory approvals and the subsequent compliance with appropriate federal, state, local, and foreign statutes and regulations require the expenditure of substantial time and financial resources. Failure to comply with the applicable U.S. requirements at any time during the product development process, approval process or after approval, may subject an applicant to administrative or judicial sanctions. These sanctions could include the FDA's refusal to approve pending applications, withdrawal of an approval, a clinical hold, warning letters, product recalls, product seizures, total or partial suspension of production or distribution, injunctions, fines, refusals of government contracts, restitution, disgorgement, or civil or criminal penalties. Any agency or judicial enforcement action could have a material adverse effect on us. The process required by the FDA before a drug or biologic may be marketed in the U.S. generally involves the following:

- •

- completion of preclinical laboratory tests, animal studies and formulation studies according to current Good Laboratory

Practices (cGLP) or other applicable regulations;

- •

- submission to the FDA of an IND which must become effective before human clinical trials may begin;

- •

- performance of adequate and well-controlled human clinical trials according to Good Clinical Practices (cGCP) to establish

the safety and efficacy of the proposed drug for its intended use;

- •

- submission to the FDA of an NDA or BLA;

- •

- satisfactory completion of an FDA inspection of the manufacturing facility or facilities at which the drug is produced to

assess compliance with current Good Manufacturing Practice (cGMP) to assure that the facilities, methods and controls are adequate to preserve the drug's identity, strength, quality and purity; and

- •

- FDA review and approval of the NDA or BLA.

Once a pharmaceutical candidate is identified for development it enters the preclinical testing stage. Preclinical tests include laboratory evaluations of product chemistry, toxicity and formulation, as well as animal studies. An IND sponsor must submit the results of the preclinical tests, together with manufacturing information and analytical data, to the FDA as part of the IND. The sponsor will also include a protocol detailing, among other things, the objectives of the first phase of the clinical trial, the parameters to be used in monitoring safety, and the effectiveness criteria to be evaluated, if the first phase lends itself to an efficacy evaluation. Some preclinical testing may continue even after the IND is submitted. The IND automatically becomes effective 30 days after receipt by the FDA, unless the FDA, within the 30-day time period, places the clinical trial on a clinical hold. In such a case, the IND sponsor and the FDA must resolve any outstanding concerns before the clinical trial can begin. Clinical holds also may be imposed by the FDA at any time before or during studies due to safety concerns or non-compliance.

All clinical trials must be conducted under the supervision of one or more qualified investigators in accordance with cGCP regulations. They must be conducted under protocols detailing the objectives of the trial, dosing procedures, subject selection and exclusion criteria and the safety and effectiveness criteria to be evaluated. Each protocol must be submitted to the FDA as part of the IND, and progress reports detailing the results of the clinical trials must be submitted at least annually. In addition, timely safety reports must be submitted to the FDA and the investigators for serious and unexpected adverse events. An institutional review board, or IRB, at each institution participating in the clinical trial must review and approve each protocol before a clinical trial commences at that institution and must also approve the information regarding the trial and the consent form that must be provided to each trial

18

subject or his or her legal representative, monitor the study until completed and otherwise comply with IRB regulations.

Human clinical trials are typically conducted in three sequential phases that may overlap or be combined:

- •

- Phase I: The product candidate is initially introduced into healthy human

subjects and tested for safety, dosage tolerance, absorption, metabolism, distribution and excretion. In the case of some products for severe or life-threatening diseases, such as cancer, especially

when the product may be too inherently toxic to ethically administer to healthy volunteers, the initial human testing is often conducted in patients.

- •

- Phase II: This phase involves studies in a limited patient population to

identify possible adverse effects and safety risks, to preliminarily evaluate the efficacy of the product for specific targeted diseases and to determine dosage tolerance and optimal dosage.

- •

- Phase III: Clinical trials are undertaken to further evaluate dosage, clinical efficacy and safety in an expanded patient population at geographically dispersed clinical study sites. These studies are intended to establish the overall risk-benefit ratio of the product candidate and provide, if appropriate, an adequate basis for product labeling.

The FDA or the sponsor may suspend a clinical trial at any time on various grounds, including a finding that the research subjects or patients are being exposed to an unacceptable health risk. Similarly, an IRB can suspend or terminate approval of a clinical trial at its institution if the clinical trial is not being conducted in accordance with the IRB's requirements or if the drug has been associated with unexpected serious harm to patients. Phase I, Phase II, and Phase III testing may not be completed successfully within any specified period, if at all.

During the development of a new drug, sponsors are given opportunities to meet with the FDA at certain points. These points may be prior to submission of an IND, at the end of Phase II, and before an NDA or BLA is submitted. Meetings at other times may be requested. These meetings can provide an opportunity for the sponsor to share information about the data gathered to date, for the FDA to provide advice, and for the sponsor and FDA to reach agreement on the next phase of development. Sponsors typically use the End of Phase II meeting to discuss their Phase II clinical results and present their plans for the pivotal Phase III clinical trial that they believe will support approval of the new drug. If this type of discussion occurs, a sponsor may be able to request a Special Protocol Assessment, or SPA, the purpose of which is to reach agreement with the FDA on the design of the Phase III clinical trial protocol design and analysis that will form the primary basis of an efficacy claim.

According to FDA guidance for industry on the SPA process, a sponsor that meets the prerequisites may make a specific request for a special protocol assessment and provide information regarding the design and size of the proposed clinical trial. The FDA is required to evaluate the protocol within 45 days of the request to assess whether the proposed trial is adequate, and that evaluation may result in discussions and a request for additional information. A SPA request must be made before the proposed trial begins, and all open issues must be resolved before the trial begins. If a written agreement is reached, it will be documented and made part of the record. The agreement will be binding on the FDA and may not be changed by the sponsor or the FDA after the trial begins except with the written agreement of the sponsor and the FDA or if the FDA determines that a substantial scientific issue essential to determining the safety or efficacy of the drug was identified after the testing began. If the sponsor makes any unilateral changes to the approved protocol, the agreement will be invalidated.

Concurrent with clinical trials, companies usually complete additional animal studies and must also develop additional information about the chemistry and physical characteristics of the drug and finalize a process for manufacturing the product in commercial quantities in accordance with cGMP

19

requirements. The manufacturing process must be capable of consistently producing quality batches of the product candidate and, among other things, the manufacturer must develop methods for testing the identity, strength, quality and purity of the final drug. Additionally, appropriate packaging must be selected and tested and stability studies must be conducted to demonstrate that the product candidate does not undergo unacceptable deterioration over its shelf life.

U.S. Review and Approval Processes

The results of product development, preclinical studies and clinical trials, along with descriptions of the manufacturing process, analytical tests conducted on the chemistry of the drug, proposed labeling, and other relevant information are submitted to the FDA as part of an NDA or BLA requesting approval to market the product. The submission of an NDA or BLA is subject to the payment of user fees; a waiver of such fees may be obtained under certain limited circumstances. The FDA reviews all NDAs and BLAs submitted to ensure that they are sufficiently complete for substantive review before it accepts them for filing. The FDA may request additional information rather than accept an NDA or BLA for filing. In this event, the NDA or BLA must be resubmitted with the additional information. The resubmitted application also is subject to review before the FDA accepts it for filing. Once the submission is accepted for filing, the FDA begins an in-depth substantive review. FDA may refer the NDA or BLA to an advisory committee for review, evaluation and recommendation as to whether the application should be approved and under what conditions. The FDA is not bound by the recommendation of an advisory committee, but it generally follows such recommendations. The approval process is lengthy and often difficult, and the FDA may refuse to approve an NDA or BLA if the applicable regulatory criteria are not satisfied or may require additional clinical or other data and information. Even if such data and information is submitted, the FDA may ultimately decide that the NDA or BLA does not satisfy the criteria for approval. Data obtained from clinical trials are not always conclusive and the FDA may interpret data differently than we interpret the same data. The FDA may issue a complete response letter, which may require additional clinical or other data or impose other conditions that must be met in order to secure final approval of the NDA or BLA, or an approved letter following satisfactory completion of all aspects of the review process. The FDA reviews an NDA to determine, among other things, whether a product is safe and effective for its intended use and whether its manufacturing is cGMP-compliant to assure and preserve the product's identity, strength, quality and purity. The FDA reviews a BLA to determine, among other things whether the product is safe, pure and potent and the facility in which it is manufactured, processed, packed or held meets standards designed to assure the product's continued safety, purity and potency. Before approving an NDA or BLA, the FDA will inspect the facility or facilities where the product is manufactured.

NDAs or BLAs receive either standard or priority review. A drug representing a significant improvement in treatment, prevention or diagnosis of disease may receive priority review. Priority review for an NDA for a new molecular entity and original BLAs will be 6 months from the date that the NDA or BLA is filed. In addition, products studied for their safety and effectiveness in treating serious or life-threatening illnesses and that provide meaningful therapeutic benefit over existing treatments may receive accelerated approval and may be approved on the basis of adequate and well-controlled clinical trials establishing that the drug product has an effect on a surrogate endpoint that is reasonably likely to predict clinical benefit or on the basis of an effect on a clinical endpoint other than survival or irreversible morbidity. As a condition of approval, the FDA may require that a sponsor of a drug receiving accelerated approval perform adequate and well-controlled post-marketing clinical trials. Priority review and accelerated approval do not change the standards for approval, but may expedite the approval process.

If a product receives regulatory approval, the approval may be significantly limited to specific diseases and dosages or the indications for use may otherwise be limited, which could restrict the

20

commercial value of the product. In addition, the FDA may require us to conduct Phase IV testing which involves clinical trials designed to further assess a drug's safety and effectiveness after NDA or BLA approval, and may require testing and surveillance programs to monitor the safety of approved products which have been commercialized.

The recently enacted Food and Drug Administration Safety and Innovation Act, or FDASIA, made permanent the Pediatric Research Equity Act, or PREA, which requires a sponsor to conduct pediatric studies for most drugs and biologicals, for a new active ingredient, new indication, new dosage form, new dosing regimen or new route of administration. Under PREA, original NDAs, BLAs and supplements thereto, must contain a pediatric assessment unless the sponsor has received a deferral or waiver. The required assessment must evaluate the safety and effectiveness of the product for the claimed indications in all relevant pediatric subpopulations and support dosing and administration for each pediatric subpopulation for which the product is safe and effective. The sponsor or FDA may request a deferral of pediatric studies for some or all of the pediatric subpopulations. A deferral may be granted for several reasons, including a finding that the drug or biologic is ready for approval for use in adults before pediatric studies are complete or that additional safety or effectiveness data needs to be collected before the pediatric studies begin. After April 2013, the FDA must send a non-compliance letter to any sponsor that fails to submit the required assessment, keep a deferral current or fails to submit a request for approval of a pediatric formulation.

Patent Term Restoration and Marketing Exclusivity

Depending upon the timing, duration and specifics of FDA approval of our drugs, some of our U.S. patents may be eligible for limited patent term extension under the Drug Price Competition and Patent Term Restoration Act of 1984, referred to as the Hatch-Waxman Amendments. The Hatch-Waxman Amendments permit a patent restoration term of up to five years as compensation for patent term lost during product development and the FDA regulatory review process. However, patent term restoration cannot extend the remaining term of a patent beyond a total of 14 years from the product's approval date. The patent term restoration period is generally one-half the time between the effective date of an IND, and the submission date of an NDA or BLA, plus the time between the submission date of an NDA or BLA and the approval of that application. Only one patent applicable to an approved drug is eligible for the extension, and the extension must be applied for prior to expiration of the patent. The United States Patent and Trademark Office, in consultation with the FDA, reviews and approves the application for any patent term extension or restoration. In the future, we intend to apply for restorations of patent term for some of our currently owned or licensed patents to add patent life beyond their current expiration date, depending on the expected length of clinical trials and other factors involved in the filing of the relevant NDA.