UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

FORM N-CSR

Investment Company Act file number: 811-05767

DWS Strategic Municipal Income Trust

(Exact Name of Registrant as Specified in Charter)

875 Third Avenue

New York, NY 10022-6225

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: (212) 454-4500

Diane Kenneally

One International Place

Boston, MA 02110

(Name and Address of Agent for Service)

| Date of fiscal year end: | 11/30 |

| Date of reporting period: | 11/30/19 |

| ITEM 1. | REPORT TO STOCKHOLDERS |

Table of Contents

Table of Contents

The Fund’s investment objective is to provide a high level of current income exempt from federal income tax.

Closed-end funds, unlike open-end funds, are not continuously offered. There is a one time public offering and once issued, shares of closed-end funds are sold in the open market through a stock exchange. Shares of closed-end funds frequently trade at a discount to net asset value. The price of the Fund’s shares is determined by a number of factors, several of which are beyond the control of the Fund. Therefore, the Fund cannot predict whether its shares will trade at, below or above net asset value.

Bond investments are subject to interest-rate, credit, liquidity and market risks to varying degrees. When interest rates rise, bond prices generally fall. Credit risk refers to the ability of an issuer to make timely payments of principal and interest. Investing in derivatives entails special risks relating to liquidity, leverage and credit that may reduce returns and/or increase volatility. Leverage results in additional risks and can magnify the effect of any gains or losses. Although the Fund seeks income that is exempt from federal income taxes, a portion of the Fund’s distributions may be subject to federal, state and local taxes, including the alternative minimum tax.

The brand DWS represents DWS Group GmbH & Co. KGaA and any of its subsidiaries such as DWS Distributors, Inc. which offers investment products or DWS Investment Management Americas, Inc. and RREEF America L.L.C. which offer advisory services.

NOT FDIC/NCUA INSURED NO BANK GUARANTEE MAY LOSE VALUE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY

| 2 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| Portfolio Management Review | (Unaudited) |

Market Overview and Fund Performance

All performance information below is historical and does not guarantee future results. Investment return and principal fluctuate, so your shares may be worth more or less when sold. Current performance may differ from performance data shown. Please visit dws.com for the Fund’s most recent month-end performance. Fund performance includes reinvestment of all distributions. Please refer to pages 8 through 9 for more complete performance information.

Investment Guidelines

The Fund’s investment objective is to provide a high level of current income exempt from federal income tax. The Fund will seek to achieve its investment objective by investing in a portfolio of tax-exempt municipal securities. The Fund will invest at least 50% of its assets in investment-grade or unrated municipal securities of comparable quality and may invest up to 50% of its assets in high-yield municipal securities that are below investment grade.

The lowest-quality municipal securities in which the Fund will invest are those rated B by Moody’s Investors Service, Inc. or B- by Standard & Poor’s Corporation, or unrated municipal securities, which, in the opinion of the Fund’s investment advisor, have credit characteristics equivalent to, and will be of comparable quality to, such B or B- rated municipal securities.

DWS Strategic Municipal Income Trust returned 13.68% based on net asset value for the annual period ended November 30, 2019, while the Fund’s benchmark, the unmanaged, unleveraged Bloomberg Barclays Municipal Bond Index, returned 8.49% for the 12-month period. The broad taxable bond market, as measured by the Bloomberg Barclays Aggregate Bond Index, returned 10.79% for the same period. The Fund’s return based on market price was 26.01%. Over the period, the Fund’s traded shares went from a discount of 12.41% to a discount of 2.92%. The Fund’s monthly dividend was reduced from 5 cents per share to 4.25 cents per share during the fiscal period.

Performance for the broader fixed income markets was supported over the 12-month period by a decline in U.S. Treasury yields. December of 2018 saw Treasury yields drop sharply as investors sought a safe haven in the face of uncertainty around global growth and concerns that the U.S. Federal Reserve would overshoot on normalizing interest rates. Municipal bond market performance was constrained to a degree in late

| DWS Strategic Municipal Income Trust | | | 3 |

Table of Contents

2018 by outflows from tax-free mutual funds, although the impact was largely offset by moderate new issue supply.

Entering 2019, the Fed signaled patience with respect to future increases in its benchmark overnight lending rate, sparking a rebound in sentiment. After having raised rates in December of 2018, the Fed’s Open Market Committee implemented a quarter-point decrease in its benchmark overnight lending rate at each of its late-July, mid-August and late-October 2019 meetings. The result was to leave the fed funds target at 1.50%–1.75%, somewhat below the low end of its historically normal range.

Tax-free funds would see record inflows of $84.1 billion over the first eleven months of 2019. Longer-maturity and lower quality municipal funds experienced the largest inflows as investors sought incremental income in a low interest rate environment. The level of demand was more than sufficient to absorb an increase in municipal issuance relative to the same period in 2018.

“Performance for the broader fixed income markets was supported over the 12-month period by a decline in U.S. Treasury yields.”

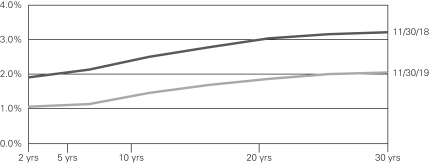

The yield curve for AAA-rated municipal bonds finished the 12 months ended November 30, 2019 lower along its length. In addition, the curve flattened as longer maturities experienced the most significant yield declines. Specifically, the yield on two-year issues declined by 85 basis points from 1.92% to 1.07%, while the 10-year yield declined 104 basis points from 2.51% to 1.47%, and the 30-year yield declined 116 basis point from 3.22% to 2.06% for a flattening of 31 basis points between two and 30 years. (100 basis points equals one percentage point. See the accompanying graph for a depiction of municipal bond yield changes between the beginning and end of the period.)

For the 12 months ending November 30, 2019, municipal market credit spreads — the incremental yield offered by lower-quality issues vs. AAA-rated issues — generally narrowed, as investors continued to seek sources of higher yield in a low rate environment.

| 4 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| AAA Municipal Bond Yield Curve (as of 11/30/19 and 11/30/18) |

Source: Thomson Reuters as of 11/30/19.

Chart is for illustrative purposes only and does not represent any DWS product.

Positive and Negative Contributors to Performance

Given less attractive yields relative to Treasuries on the front end of the municipal curve, we looked for opportunities to gain incremental income by maintaining a tilt toward issues in the 20-30-year maturity range, while underweighting the 5-year part of the curve. This positioning aided performance vs. the benchmark, as longer-term issues benefited the most from falling yields as the curve flattened over the period.

In a period when investors were generally rewarded for lower credit quality exposure, the Fund’s overall stance with respect to credit quality added to performance vs. the benchmark. Specifically, the Fund carried overweights relative to the benchmark in issues rated A and BBB, and also had out-of benchmark exposure to bonds rated below investment grade or that were unrated. This positioning added to performance as credit spreads narrowed over the 12 months ended November 30, 2019. In sector terms, exposure to tobacco-related issues led positive contributions, followed by hospital issues.

Relative to its Morningstar peer group, the Fund had a higher-quality bias and less exposure to below-investment-grade issues, which acted as a constraint on returns.

| DWS Strategic Municipal Income Trust | | | 5 |

Table of Contents

Outlook and Positioning

At the end of November 2019, municipal yields on an absolute basis were low by historical standards. Yields for longer-maturity municipals remained reasonably attractive vs. taxable alternatives. As of November 30, 2019, the 10-year municipal yield of 1.47% was 82.5% of the 1.78% yield on comparable-maturity U.S. Treasuries, as compared to a ratio of 83.4% twelve months earlier. The 30-year municipal yield of 2.06% was 93.2% of the 2.21% yield on comparable-maturity U.S. Treasuries, as compared to a ratio of 97.6% twelve months earlier.

The municipal curve is flat by historical standards, particularly between two and 10 years. However, the municipal curve has maintained more slope than the Treasury curve and we view the 20-30-year maturity range as offering attractive incremental income.

We believe credit spreads to currently be relatively fully valued. Consequently, we are being selective as we seek to add exposure to lower quality paper. We continue to perform careful analysis of each issue’s risk/reward profile given the environment of relatively tight spreads.

Portfolio Management Team

Ashton P. Goodfield, CFA, Managing Director

Portfolio Manager of the Fund. Began managing the Fund in 2014.

| – | Joined DWS in 1986. |

| – | Head of Municipal Bonds. |

| – | BA, Duke University. |

Chad Farrington, CFA, Managing Director

Portfolio Manager of the Fund. Began managing the Fund in 2018.

| – | Joined DWS in 2018 with 20 years of industry experience; previously, worked as Portfolio Manager, Head of Municipal Research, and Senior Credit Analyst at Columbia Threadneedle. |

| – | BS, Montana State University. |

Michael J. Generazo, Director

Portfolio Manager of the Fund. Began managing the Fund in 2018.

| – | Joined DWS in 1999. |

| – | BS, Bryant College; MBA, Suffolk University. |

The views expressed reflect those of the portfolio management team only through the end of the period of the report as stated on the cover. The management team’s views are subject to change at any time based on market and other conditions and should not be construed as a recommendation. Past performance is no guarantee of future results. Current and future portfolio holdings are subject to risk.

| 6 | | | DWS Strategic Municipal Income Trust |

Table of Contents

Terms to Know

The unmanaged, unleveraged Bloomberg Barclays Municipal Bond Index covers the U.S.-dollar-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and pre-refunded bonds.

The Bloomberg Barclays Aggregate Bond Index is an unmanaged, unleveraged index representing domestic taxable investment-grade bonds, with index components for government and corporate securities, mortgage pass-through securities, and asset- backed securities with average maturities of one year or more.

Index returns do not reflect any fees or expenses and it is not possible to invest directly into an index.

The yield curve is a graphical representation of how yields on bonds of different maturities compare. Normally, yield curves slant up, as bonds with longer maturities typically offer higher yields than short-term bonds.

Spread refers to the excess yield various bond sectors offer over financial instruments with similar maturities. When spreads widen, yield differences are increasing between bonds in the two sectors being compared. When spreads narrow, the opposite is true.

Credit quality measures a bond issuer’s ability to repay interest and principal in a timely manner. Rating agencies assign letter designations, such as AAA, AA and so forth. The lower the rating, the higher the probability of default. Credit quality does not remove market risk and is subject to change.

Overweight means the fund holds a higher weighting in a given sector or security than the benchmark. Underweight means the fund holds a lower weighting.

| DWS Strategic Municipal Income Trust | | | 7 |

Table of Contents

| Performance Summary | November 30, 2019 (Unaudited) |

Performance is historical, assumes reinvestment of all dividend and capital gain distributions, and does not guarantee future results. Investment return and principal value fluctuate with changing market conditions so that, when sold, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please visit dws.com for the Fund’s most recent month-end performance.

Fund specific data and performance are provided for informational purposes only and are not intended for trading purposes.

| Average Annual Total Returns as of 11/30/19 | ||||||||||||

| DWS Strategic Municipal Income Trust | 1-Year | 5-Year | 10-Year | |||||||||

| Based on Net Asset Value(a) | 13.68% | 5.08% | 7.35% | |||||||||

| Based on Market Price(a) | 26.01% | 4.41% | 6.75% | |||||||||

| Bloomberg Barclays Municipal Bond Index(b) | 8.49% | 3.57% | 4.34% | |||||||||

| Morningstar Closed-End High-Yield Municipal Funds Category(c) |

10.63% | 5.44% | 7.64% | |||||||||

| (a) | Total return based on net asset value reflects changes in the Fund’s net asset value during each period. Total return based on market price reflects changes in market price. Each figure assumes that dividend and capital gain distributions, if any, were reinvested. These figures will differ depending upon the level of any discount from or premium to net asset value at which the Fund’s shares traded during the period. Expenses of the Fund include management fee, interest expense and other fund expenses. Total returns shown take into account these fees and expenses. The expense ratio of the Fund for the year ended November 30, 2019 was 2.89% (1.12% excluding interest expense). |

| (b) | The unmanaged, unleveraged Bloomberg Barclays Municipal Bond Index covers the U.S. dollar-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and pre-refunded bonds. Index returns do not reflect any fees or expenses and it is not possible to invest directly into an index. |

| (c) | Morningstar’s Closed-End High-Yield Municipal Funds category represents high-yield muni portfolios that typically invest at least 50% of assets in high-income municipal securities that are not rated or that are rated by a major agency such as Standard & Poor’s or Moody’s at the level of BBB and below (considered part of the high-yield universe within the municipal industry). Morningstar figures represent the average of the total returns based on net asset value reported by all of the closed-end funds designated by Morningstar, Inc. as falling into the Closed-End High-Yield Municipal Funds category. Category returns assume reinvestment of all distributions. It is not possible to invest directly in a Morningstar category. |

| 8 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| Net Asset Value and Market Price | ||||||||

| As of 11/30/19 | As of 11/30/18 | |||||||

| Net Asset Value | $ | 12.69 | $ | 11.76 | ||||

| Market Price | $ | 12.32 | $ | 10.30 | ||||

| Premium (discount) | (2.92 | %) | (12.41 | %) | ||||

Prices and net asset value fluctuate and are not guaranteed.

| Distribution Information | ||||

| Twelve Months as of 11/30/19: |

||||

| Income Dividends (common shareholders) |

$ | .57 | ||

| Capital Gains Dividend (common shareholders) | $ | .0346 | ||

| November Income Dividend (common shareholders) | $ | .0425 | ||

| Current Annualized Distribution Rate (Based on Net Asset Value) as of 11/30/19† |

4.02 | % | ||

| Current Annualized Distribution Rate (Based on Market Price) as of 11/30/19† |

4.14 | % | ||

| Tax Equivalent Distribution Rate (Based on Net Asset Value) as of 11/30/19† |

6.79 | % | ||

| Tax Equivalent Distribution Rate (Based on Market Price) as of 11/30/19† |

6.99 | % | ||

| DWS Strategic Municipal Income Trust | | | 9 |

Table of Contents

The quality ratings represent the higher of Moody’s Investors Service, Inc. (“Moody’s”), Fitch Ratings, Inc. (“Fitch”) or Standard & Poor’s Corporation (“S&P”) credit ratings. The ratings of Moody’s, Fitch and S&P represent their opinions as to the quality of the securities they rate. Credit quality measures a bond issuer’s ability to repay interest and principal in a timely manner. Ratings are relative and subjective and are not absolute standards of quality. Credit quality does not remove market risk and is subject to change.

| Top Five State/Territory Allocations (As a % of Investment Portfolio excluding Open-End Investment Companies) |

11/30/19 | 11/30/18 | ||||||

| Texas | 14% | 14% | ||||||

| Florida | 9% | 9% | ||||||

| New York |

8% | 8% | ||||||

| Illinois |

8% | 7% | ||||||

| California |

7% | 10% | ||||||

| Interest Rate Sensitivity | 11/30/19 | 11/30/18 | ||||||

| Effective Maturity | 6.1 years | 6.2 years | ||||||

| Modified Duration | 5.8 years | 5.6 years | ||||||

| Leverage (As a % of Total Assets) | 11/30/19 | 11/30/18 | ||||||

| 40% | 42% | |||||||

Effective maturity is the weighted average of the maturity date of bonds held by the Fund taking into consideration any available maturity shortening features.

Modified duration is an approximate measure of a fund’s sensitivity to movements in interest rates based on the current interest rate environment.

Leverage results in additional risks and can magnify the effect of any gains or losses to a greater extent than if leverage were not used.

Portfolio holdings and characteristics are subject to change.

For more complete details about the Fund’s investment portfolio, see page 11. A fact sheet is available on dws.com or upon request. Please see the Additional Information section on page 63 for contact information.

| 10 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| Investment Portfolio | as of November 30, 2019 |

| Principal Amount ($) |

Value ($) | |||||||

| Municipal Bonds and Notes 135.6% |

| |||||||

| Alabama 0.3% |

| |||||||

| Alabama, UAB Medicine Finance Authority Revenue, Series B2, 5.0%, 9/1/2041 |

325,000 | 383,032 | ||||||

| Alaska 1.5% |

| |||||||

| Alaska, Industrial Development & Export Authority Revenue, Tanana Chiefs Conference Project, Series A, 4.0%, 10/1/2049 |

2,000,000 | 2,164,280 | ||||||

| Arizona 3.9% |

| |||||||

| Arizona, State Industrial Development Authority, 3rd Tier Great Lakes Senior Living Revenue Communities Project: |

||||||||

| Series C, 144A, 5.0%, 1/1/2049 |

200,000 | 214,296 | ||||||

| Series C, 144A, 5.5%, 1/1/2054 |

300,000 | 330,732 | ||||||

| Arizona, State Industrial Development Authority, Education Revenue, Odyssey Preparatory Academy Project, 144A, 5.0%, 7/1/2054 |

175,000 | 182,961 | ||||||

| Arizona, State Industrial Development Authority, Senior Living Revenue, Great Lakes Senior Living Communities, Series A, 5.0%, 1/1/2054 |

500,000 | 557,545 | ||||||

| Arizona, State University, Green Bond, Series A, 5.0%, 7/1/2043 |

2,000,000 | 2,495,720 | ||||||

| Glendale, AZ, Industrial Development Authority, Terrace of Phoenix Project, 5.0%, 7/1/2048 |

60,000 | 64,685 | ||||||

| Maricopa County, AZ, Industrial Development Authority, Education Revenue, Legacy Traditional School Project: |

||||||||

| Series B, 144A, 5.0%, 7/1/2049 (a) |

85,000 | 93,945 | ||||||

| Series B, 144A, 5.0%, 7/1/2054 (a) |

60,000 | 65,807 | ||||||

| Phoenix, AZ, Industrial Development Authority, Education Facility Revenue, Leman Academy of Excellence, ORO Valley Project: |

||||||||

| Series A, 144A, 5.0%, 7/1/2038 |

195,000 | 201,002 | ||||||

| Series A, 144A, 5.25%, 7/1/2048 |

250,000 | 258,153 | ||||||

| Tempe, AZ, Industrial Development Authority Revenue, Mirabella at ASU Project, Series A, 144A, 6.125%, 10/1/2047 |

255,000 | 290,909 | ||||||

| Yavapai County, AZ, Industrial Development Authority, Hospital Facility, Regional Medical Center, 4.0%, 8/1/2043 |

675,000 | 740,846 | ||||||

|

|

|

|||||||

| 5,496,601 | ||||||||

| California 10.9% |

| |||||||

| California, Golden State Tobacco Securitization Corp., Tobacco Settlement Revenue: |

||||||||

| Series A-1, 5.0%, 6/1/2047 |

300,000 | 308,673 | ||||||

| Series A-1, 5.25%, 6/1/2047 |

200,000 | 207,014 | ||||||

The accompanying notes are an integral part of the financial statements.

| DWS Strategic Municipal Income Trust | | | 11 |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| California, M-S-R Energy Authority, Series B, 7.0%, 11/1/2034 |

1,310,000 | 1,991,855 | ||||||

| California, Morongo Band of Mission Indians Revenue, Series B, 144A, 5.0%, 10/1/2042 |

115,000 | 132,140 | ||||||

| California, State General Obligation: |

||||||||

| 5.0%, 11/1/2043 |

1,300,000 | 1,471,444 | ||||||

| 5.25%, 4/1/2035 |

1,230,000 | 1,345,386 | ||||||

| 5.5%, 3/1/2040 |

1,000,000 | 1,010,590 | ||||||

| California, State Municipal Finance Authority Revenue, LINXS Apartment Project: |

||||||||

| Series A, AMT, 5.0%, 12/31/2043 |

300,000 | 351,546 | ||||||

| Series A, AMT, 5.0%, 12/31/2047 |

160,000 | 186,650 | ||||||

| Series A, AMT, 5.0%, 6/1/2048 |

60,000 | 69,880 | ||||||

| California, State Pollution Control Financing Authority, Solid Waste Disposal Revenue, Rialto Bioenergy Facility LLC Project, Green Bonds Revenue, AMT, 144A, 7.5%, 12/1/2040 |

500,000 | 521,895 | ||||||

| California, Statewide Communities Development Authority Revenue, Loma Linda University Medical Center: |

||||||||

| Series A, 5.25%, 12/1/2044 |

195,000 | 215,650 | ||||||

| Series A, 144A, 5.25%, 12/1/2056 |

735,000 | 827,801 | ||||||

| Series A, 5.5%, 12/1/2054 |

195,000 | 216,887 | ||||||

| Series A, 144A, 5.5%, 12/1/2058 |

105,000 | 122,929 | ||||||

| California, Statewide Communities Development Authority, College Housing Revenue, NCCD-Hooper Street LLC, College of the Arts Project, 144A, 5.25%, 7/1/2049 |

825,000 | 951,043 | ||||||

| California, Tobacco Settlement Revenue, San Diego, Tobacco Securitization Corp., “2” Series B-1, 5.0%, 6/1/2048 |

835,000 | 960,384 | ||||||

| Riverside County, CA, Transportation Commission Toll Revenue Senior Lien, Series A, 5.75%, 6/1/2048 |

1,000,000 | 1,116,710 | ||||||

| San Buenaventura, CA, Community Memorial Health Systems, 7.5%, 12/1/2041 |

500,000 | 550,535 | ||||||

| San Francisco, CA, City & County Airports Commission, International Airport Revenue: |

||||||||

| Series A, 5.0%, 5/1/2044 |

1,000,000 | 1,126,210 | ||||||

| Series A, AMT, 5.0%, 5/1/2049 |

1,110,000 | 1,340,247 | ||||||

| San Joaquin Hills, CA, Transportation Corridor Agency, Toll Road Revenue, Series A, 5.0%, 1/15/2050 |

445,000 | 500,371 | ||||||

|

|

|

|||||||

| 15,525,840 | ||||||||

| Colorado 4.1% |

| |||||||

| Colorado, High Performance Transportation Enterprise Revenue, C-470 Express Lanes, 5.0%, 12/31/2056 |

225,000 | 245,502 | ||||||

| Colorado, Park Creek Metropolitan District Revenue, Senior Ltd. Property Tax Supported, Series A, 5.0%, 12/1/2045 |

235,000 | 264,410 | ||||||

The accompanying notes are an integral part of the financial statements.

| 12 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Colorado, Public Energy Authority, Natural Gas Purchased Revenue, 6.25%, 11/15/2028 |

635,000 | 811,200 | ||||||

| Colorado, State Health Facilities Authority Revenue, Covenant Retirement Communities: |

||||||||

| Series A, 5.0%, 12/1/2033 |

440,000 | 475,671 | ||||||

| Series A, 5.0%, 12/1/2035 |

250,000 | 283,017 | ||||||

| Colorado, State Health Facilities Authority Revenue, School Health Systems, Series A, 5.5%, 1/1/2035 |

1,000,000 | 1,145,530 | ||||||

| Colorado, State Health Facilities Authority, Hospital Revenue, Covenant Retirement Communities Obligated Group: |

||||||||

| Series A, 5.0%, 12/1/2043 |

165,000 | 192,047 | ||||||

| Series A, 5.0%, 12/1/2048 |

260,000 | 301,733 | ||||||

| Denver City & County, CO, Special Facilities Airport Revenue, United Airlines, Inc. Project, AMT, 5.0%, 10/1/2032 |

200,000 | 218,342 | ||||||

| Denver, CO, City & County Airport Revenue: |

||||||||

| Series A, AMT, 5.0%, 12/1/2048 |

585,000 | 691,025 | ||||||

| Series A, AMT, 5.25%, 11/15/2043 |

600,000 | 674,052 | ||||||

| Denver, CO, Health & Hospital Authority, Certificates of Participation, 5.0%, 12/1/2048 |

140,000 | 164,884 | ||||||

| Denver, CO, Health & Hospital Authority, Healthcare Revenue, Series A, 4.0%, 12/1/2040 |

300,000 | 329,991 | ||||||

|

|

|

|||||||

| 5,797,404 | ||||||||

| Connecticut 0.1% |

| |||||||

| Connecticut, Mashantucket Western Pequot Tribe Bond, 6.05%, PIK, 7/1/2031* |

2,983,189 | 111,869 | ||||||

| Connecticut, State Health & Educational Facilities Authority Revenue, Covenant Home, Inc., Series B, 5.0%, 12/1/2040 |

85,000 | 99,486 | ||||||

|

|

|

|||||||

| 211,355 | ||||||||

| District of Columbia 1.1% |

| |||||||

| District of Columbia, Ingleside Rock Creek Project: |

||||||||

| Series A, 5.0%, 7/1/2042 |

130,000 | 139,434 | ||||||

| Series A, 5.0%, 7/1/2052 |

195,000 | 208,159 | ||||||

| District of Columbia, Metropolitan Airport Authority Systems Revenue: |

||||||||

| Series A, AMT, 5.0%, 10/1/2038 |

200,000 | 222,456 | ||||||

| Series A, AMT, 5.0%, 10/1/2043 |

850,000 | 940,797 | ||||||

|

|

|

|||||||

| 1,510,846 | ||||||||

| Florida 10.7% |

| |||||||

| Alachua County, FL, Health Facilities Authority Revenue, Shands Teaching Hospital & Clinics, Inc., Series A, 4.0%, 12/1/2049 |

210,000 | 228,028 | ||||||

The accompanying notes are an integral part of the financial statements.

| DWS Strategic Municipal Income Trust | | | 13 |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Broward County, FL, Airport System Revenue: |

||||||||

| Series A, AMT, 4.0%, 10/1/2044 |

145,000 | 160,499 | ||||||

| Series A, AMT, 4.0%, 10/1/2049 |

230,000 | 253,414 | ||||||

| Collier County, FL, Industrial Development Authority, Continuing Care Community Revenue, Arlington of Naples Project, Series A, 144A, 8.125%, 5/15/2044* |

290,000 | 275,886 | ||||||

| Davie, FL, Educational Facilities Revenue, Nova Southeastern University Project, 5.0%, 4/1/2048 |

335,000 | 389,257 | ||||||

| Florida, Capital Trust Agency, Educational Facilities Authority, Charter Educational Foundation Project, Series A, 144A, 5.375%, 6/15/2048 |

230,000 | 253,368 | ||||||

| Florida, Capital Trust Agency, Senior Living Revenue, American Eagle Portfolio Project, Series A-1, 5.875%, 7/1/2054 |

1,000,000 | 1,076,020 | ||||||

| Florida, Development Finance Corp., Surface Transportation Facilities Revenue, Virgin Trains USA Passenger Rail Project, Series A, 144A, AMT, 6.5%**, 1/1/2049 |

355,000 | 335,912 | ||||||

| Florida, State Atlantic University Finance Corp., Capital Improvements Revenue, Student Housing Project, Series B, 4.0%, 7/1/2044 |

1,685,000 | 1,852,826 | ||||||

| Florida, Tolomato Community Development District, Special Assessment: |

||||||||

| Series 2015-1, Step-up Coupon, 0% to 11/1/2021, 6.61% to 5/1/2040 |

250,000 | 215,575 | ||||||

| Series 2015-2, Step-up Coupon, 0% to 11/1/2024, 6.61% to 5/1/2040 |

150,000 | 106,037 | ||||||

| Series A-4, Step-up Coupon, 0% to 5/1/2022, 6.61% to 5/1/2040 |

55,000 | 47,660 | ||||||

| Series 3, 6.55%, 5/1/2027* |

130,000 | 1 | ||||||

| Series 2015-3, 6.61%, 5/1/2040* |

165,000 | 2 | ||||||

| Florida, Village Community Development District No. 9, Special Assessment Revenue, 5.5%, 5/1/2042 |

145,000 | 153,471 | ||||||

| Florida, Village Community Development District No. 12, Special Assessment Revenue: |

||||||||

| 144A, 4.25%, 5/1/2043 |

400,000 | 426,680 | ||||||

| 144A, 4.375%, 5/1/2050 |

300,000 | 320,781 | ||||||

| Greater Orlando, FL, Aviation Authority Airport Facilities Revenue, Series A, AMT, 5.0%, 10/1/2047 |

400,000 | 468,228 | ||||||

| Hillsborough County, FL, Aviation Authority, Tampa International Airport, Series A, AMT, 5.0%, 10/1/2048 |

500,000 | 593,540 | ||||||

| Lake County, FL, Senior Living Revenue, Village Veranda at Lady Lake Project, Series A-1, 144A, 7.125%, 1/1/2052 |

300,000 | 309,264 | ||||||

| Martin County, FL, Health Facilities Authority, Martin Memorial Medical Center, Prerefunded, 5.5%, 11/15/2042 |

335,000 | 362,544 | ||||||

| Miami Beach, FL, Health Facilities Authority, Mount Sinai Medical Center, 5.0%, 11/15/2044 |

500,000 | 555,070 | ||||||

The accompanying notes are an integral part of the financial statements.

| 14 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Miami-Dade County, FL, Aviation Revenue, Series B, AMT, 5.0%, 10/1/2040 |

470,000 | 554,576 | ||||||

| Miami-Dade County, FL, Health Facilities Authority Hospital Revenue, Nicklaus Children’s Hospital, 5.0%, 8/1/2047 |

665,000 | 779,313 | ||||||

| Orlando & Orange County, FL, Expressway Authority Revenue, Series C, Prerefunded, 5.0%, 7/1/2035 |

830,000 | 848,633 | ||||||

| Tallahassee, FL, Health Facilities Revenue, Memorial Healthcare, Inc. Project, Series A, 5.0%, 12/1/2055 |

1,150,000 | 1,284,722 | ||||||

| Tampa-Hillsborough County, FL, Expressway Authority: |

||||||||

| Series A, 5.0%, 7/1/2031 |

1,500,000 | 1,629,585 | ||||||

| Series A, 5.0%, 7/1/2037 |

1,590,000 | 1,724,498 | ||||||

|

|

|

|||||||

| 15,205,390 | ||||||||

| Georgia 3.4% |

| |||||||

| Americus-Sumter County, GA, Hospital Authority, Magnolia Manor Obligated Group, Series A, 6.25%, 5/15/2033 |

1,000,000 | 1,111,190 | ||||||

| Atlanta, GA, Airport Revenue, Series C, AMT, 5.0%, 1/1/2037 |

375,000 | 399,761 | ||||||

| Cobb County, GA, Kennestone Hospital Authority, Revenue Anticipation Certificates, Wellstar Health System, Series A, 5.0%, 4/1/2047 |

175,000 | 203,147 | ||||||

| DeKalb County, GA, Water & Sewer Revenue, Series A, 5.25%, 10/1/2036 |

1,000,000 | 1,070,790 | ||||||

| Fulton County, GA, Development Authority Hospital Revenue, Revenue Anticipation Certificates, Wellstar Health System, Series A, 5.0%, 4/1/2042 |

210,000 | 245,332 | ||||||

| Gainesville & Hall County, GA, Hospital Authority, Northeast Georgia Health System, Inc. Project: |

||||||||

| Series A, 5.25%, 8/15/2049 |

100,000 | 116,158 | ||||||

| Series A, 5.5%, 8/15/2054 |

180,000 | 210,028 | ||||||

| Georgia, Main Street Natural Gas, Inc., Gas Project Revenue, Series A, 5.5%, 9/15/2024 |

1,220,000 | 1,429,328 | ||||||

|

|

|

|||||||

| 4,785,734 | ||||||||

| Guam 1.0% |

| |||||||

| Guam, International Airport Authority Revenue, Series C, AMT, 6.375%, 10/1/2043 |

215,000 | 248,093 | ||||||

| Guam, Port Authority Revenue, Series A, 5.0%, 7/1/2048 |

65,000 | 76,492 | ||||||

| Guam, Power Authority Revenue, Series A, Prerefunded, 5.5%, 10/1/2030 |

1,000,000 | 1,035,800 | ||||||

|

|

|

|||||||

| 1,360,385 | ||||||||

| Hawaii 1.2% |

| |||||||

| Hawaii, State Airports Systems Revenue, Series A, AMT, 5.0%, 7/1/2041 |

695,000 | 793,745 | ||||||

| Hawaii, State Department of Budget & Finance Special Purpose Revenue, 3.2%, 7/1/2039 |

855,000 | 870,698 | ||||||

|

|

|

|||||||

| 1,664,443 | ||||||||

The accompanying notes are an integral part of the financial statements.

| DWS Strategic Municipal Income Trust | | | 15 |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Illinois 13.6% |

| |||||||

| Chicago, IL, Board of Education: |

||||||||

| Series A, 5.0%, 12/1/2030 |

100,000 | 116,890 | ||||||

| Series A, 5.0%, 12/1/2032 |

105,000 | 121,953 | ||||||

| Series A, 5.0%, 12/1/2033 |

100,000 | 115,882 | ||||||

| Series H, 5.0%, 12/1/2036 |

245,000 | 278,712 | ||||||

| Series H, 5.0%, 12/1/2046 |

140,000 | 156,303 | ||||||

| Chicago, IL, General Obligation: |

||||||||

| Series A, 5.0%, 1/1/2044 |

200,000 | 225,308 | ||||||

| Series A, 5.5%, 1/1/2049 |

215,000 | 254,057 | ||||||

| Series A, 6.0%, 1/1/2038 |

455,000 | 547,097 | ||||||

| Chicago, IL, O’Hare International Airport Revenue: |

||||||||

| Series A, AMT, 5.0%, 1/1/2037 |

1,500,000 | 1,813,920 | ||||||

| Series C, AMT, 5.0%, 1/1/2046 |

1,000,000 | 1,116,230 | ||||||

| Series B, Prerefunded, 6.0%, 1/1/2041 |

2,000,000 | 2,104,020 | ||||||

| Chicago, IL, O’Hare International Airport Revenue, Senior Lien: |

||||||||

| Series D, AMT, 5.0%, 1/1/2047 |

415,000 | 477,391 | ||||||

| Series A, AMT, 5.0%, 1/1/2053 |

500,000 | 587,615 | ||||||

| Chicago, IL, O’Hare International Airport, Special Facility Revenue, AMT, 5.0%, 7/1/2048 |

130,000 | 151,145 | ||||||

| Illinois, Finance Authority Revenue, The Admiral at Lake Project, Series A, Prerefunded, 8.0%, 5/15/2040 |

1,000,000 | 1,030,040 | ||||||

| Illinois, Metropolitan Pier & Exposition Authority Revenue, McCormick Place Expansion Project: |

||||||||

| Series B, 5.0%, 6/15/2052 |

520,000 | 543,733 | ||||||

| Series A, 5.0%, 6/15/2057 |

390,000 | 431,804 | ||||||

| Illinois, Metropolitan Pier & Exposition Authority, Dedicated State Tax Revenue, Capital Appreciation-McCormick, Series A, Zero Coupon, 6/15/2036, INS: NATL |

3,000,000 | 1,744,080 | ||||||

| Illinois, Railsplitter Tobacco Settlement Authority, Prerefunded, 6.0%, 6/1/2028 |

365,000 | 390,984 | ||||||

| Illinois, State Finance Authority Revenue, Nursing Homes, 5.0%, 2/15/2037 |

1,000,000 | 980,710 | ||||||

| Illinois, State Finance Authority Revenue, Lutheran Communities: |

||||||||

| Series A, 5.0%, 11/1/2040 (a) |

30,000 | 32,075 | ||||||

| Series A, 5.0%, 11/1/2049 (a) |

40,000 | 42,102 | ||||||

| Illinois, State Finance Authority Revenue, OSF Healthcare Systems, Series A, 5.0%, 11/15/2045 |

525,000 | 587,212 | ||||||

| Illinois, State Finance Authority Revenue, Park Place of Elmhurst Project, Series C, 2.0%, 5/15/2055* |

150,000 | 4,523 | ||||||

| Illinois, State Finance Authority Revenue, Three Crowns Park Obligated Group, 5.25%, 2/15/2047 |

205,000 | 221,010 | ||||||

| Illinois, State Finance Authority Revenue, Trinity Health Corp., Series L, Prerefunded, 5.0%, 12/1/2030 |

1,000,000 | 1,074,260 | ||||||

The accompanying notes are an integral part of the financial statements.

| 16 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Illinois, State General Obligation: |

||||||||

| 5.0%, 2/1/2027 |

500,000 | 574,495 | ||||||

| Series D, 5.0%, 11/1/2027 |

500,000 | 575,810 | ||||||

| 5.0%, 2/1/2029 |

225,000 | 256,120 | ||||||

| Series A, 5.0%, 10/1/2033 |

620,000 | 710,160 | ||||||

| Series B, 5.0%, 10/1/2033 |

395,000 | 452,441 | ||||||

| Series A, 5.0%, 12/1/2038 |

350,000 | 392,833 | ||||||

| Series A, 5.0%, 12/1/2039 |

750,000 | 839,992 | ||||||

| Springfield, IL, Electric Revenue, Senior Lien, 5.0%, 3/1/2040, INS: AGMC |

385,000 | 436,282 | ||||||

|

|

|

|||||||

| 19,387,189 | ||||||||

| Indiana 3.3% |

| |||||||

| Indiana, State Finance Authority Revenue, BHI Senior Living Obligated Group, Series A, 5.25%, 11/15/2046 |

365,000 | 414,593 | ||||||

| Indiana, State Finance Authority Revenue, Community Foundation of Northwest Indiana, 5.0%, 3/1/2041 |

1,000,000 | 1,084,350 | ||||||

| Indiana, State Finance Authority Revenue, Greencroft Obligation Group, Series A, 7.0%, 11/15/2043 |

460,000 | 521,990 | ||||||

| Indiana, State Finance Authority, Health Facilities Revenue, Baptist Healthcare System, Series A, 5.0%, 8/15/2051 |

1,560,000 | 1,782,643 | ||||||

| Valparaiso, IN, Exempt Facilities Revenue, Pratt Paper LLC Project, AMT, 7.0%, 1/1/2044, GTY: Pratt Industries (U.S.A.), Inc. |

780,000 | 909,386 | ||||||

|

|

|

|||||||

| 4,712,962 | ||||||||

| Iowa 1.3% |

| |||||||

| Iowa, State Finance Authority Revenue, Lifespace Communities, Inc.: |

||||||||

| Series A, 5.0%, 5/15/2043 |

290,000 | 325,728 | ||||||

| Series A, 5.0%, 5/15/2047 |

1,000,000 | 1,108,600 | ||||||

| Series A, 5.0%, 5/15/2048 |

425,000 | 475,732 | ||||||

|

|

|

|||||||

| 1,910,060 | ||||||||

| Kansas 0.6% |

| |||||||

| Kansas, State Development Finance Authority Revenue, Village Shalom Project, Series A, 5.25%, 11/15/2053 |

500,000 | 531,030 | ||||||

| Wyandotte County, KS, Unified Government, Legends Apartments Garage & West Lawn Project, 4.5%, 6/1/2040 |

295,000 | 308,685 | ||||||

|

|

|

|||||||

| 839,715 | ||||||||

| Kentucky 3.2% |

| |||||||

| Columbia, KY, Educational Development Revenue, Lindsey Wilson College Project, 5.0%, 12/1/2033 |

440,000 | 490,222 | ||||||

| Kentucky, Economic Development Finance Authority, Hospital Facilities Revenue, Owensboro Medical Health Systems, Series A, Prerefunded, 6.5%, 3/1/2045 |

2,000,000 | 2,052,500 | ||||||

The accompanying notes are an integral part of the financial statements.

| DWS Strategic Municipal Income Trust | | | 17 |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Kentucky, Public Transportation Infrastructure Authority Toll Revenue, 1st Tier-Downtown Crossing, Series A, 6.0%, 7/1/2053 |

1,440,000 | 1,636,301 | ||||||

| Kentucky, State Economic Development Finance Authority, Owensboro Health, Inc., Obligated Group: |

||||||||

| Series A, 5.0%, 6/1/2045 |

130,000 | 146,373 | ||||||

| Series A, 5.25%, 6/1/2041 |

190,000 | 220,294 | ||||||

|

|

|

|||||||

| 4,545,690 | ||||||||

| Louisiana 2.2% |

| |||||||

| Calcasieu Parish, LA, Memorial Hospital Service, District Hospital Revenue, 5.0%, 12/1/2039 |

500,000 | 588,095 | ||||||

| Louisiana, New Orleans Aviation Board, General Airport North Terminal, Series B, AMT, 5.0%, 1/1/2048 |

140,000 | 160,313 | ||||||

| Louisiana, Public Facilities Authority Revenue, Ochsner Clinic Foundation Project, 5.0%, 5/15/2046 |

1,000,000 | 1,147,490 | ||||||

| Louisiana, State Local Government Environmental Facilities & Community Development Authority Revenue, Westlake Chemical Corp. Project, 3.5%, 11/1/2032 |

1,010,000 | 1,064,479 | ||||||

| Louisiana, Tobacco Settlement Financing Corp. Revenue, Series A, 5.25%, 5/15/2035 |

180,000 | 198,110 | ||||||

|

|

|

|||||||

| 3,158,487 | ||||||||

| Maine 0.8% |

| |||||||

| Maine, Health & Higher Educational Facilities Authority Revenue, Maine General Medical Center, 6.75%, 7/1/2036 |

1,000,000 | 1,070,980 | ||||||

| Maryland 1.1% |

| |||||||

| Maryland, State Health & Higher Educational Facilities Authority Revenue, Adventist Healthcare, Series A, 5.5%, 1/1/2046 |

375,000 | 437,888 | ||||||

| Maryland, State Health & Higher Educational Facilities Authority Revenue, Meritus Medical Center Obligated Group, 5.0%, 7/1/2040 |

1,000,000 | 1,143,930 | ||||||

|

|

|

|||||||

| 1,581,818 | ||||||||

| Massachusetts 0.8% |

| |||||||

| Massachusetts, State Development Finance Agency Revenue, Linden Ponds, Inc. Facility, Series B, 11/15/2056* |

505,485 | 143,927 | ||||||

| Massachusetts, State Development Finance Agency Revenue, NewBridge Charles, Inc., 144A, 5.0%, 10/1/2057 |

100,000 | 109,685 | ||||||

| Massachusetts, State Health & Educational Facilities Authority Revenue, Milford Regional Medical Center, Series E, 5.0%, 7/15/2037 |

950,000 | 957,106 | ||||||

|

|

|

|||||||

| 1,210,718 | ||||||||

The accompanying notes are an integral part of the financial statements.

| 18 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Michigan 3.4% |

| |||||||

| Dearborn, MI, Economic Development Corp. Revenue, Limited Obligation, Henry Ford Village, 144A, 7.5%, 11/15/2044 |

490,000 | 478,642 | ||||||

| Detroit, MI, Water & Sewerage Department, Sewerage Disposal System Revenue, Series A, 5.25%, 7/1/2039 |

280,000 | 303,131 | ||||||

| Detroit, MI, Water Supply Systems Revenue, Series A, 5.75%, 7/1/2037 |

1,000,000 | 1,064,960 | ||||||

| Michigan, State Building Authority Revenue, Facilities Program, Series I-A, 5.5%, 10/15/2045 |

2,000,000 | 2,138,220 | ||||||

| Michigan, State Finance Authority Revenue, Detroit Water & Sewer, Series C-3, 5.0%, 7/1/2033, INS: AGMC |

180,000 | 205,313 | ||||||

| Michigan, State Finance Authority Revenue, Detroit Water & Sewer Department, Series C, 5.0%, 7/1/2035 |

90,000 | 104,014 | ||||||

| Tawas City, MI, Hospital Finance Authority, St. Joseph Health Services, Series A, ETM, 5.75%, 2/15/2023 |

605,000 | 606,990 | ||||||

|

|

|

|||||||

| 4,901,270 | ||||||||

| Minnesota 1.0% |

| |||||||

| Bethel, MN, Senior Housing Revenue, Lodge at Stillwater LLC Project: |

||||||||

| 5.0%, 6/1/2048 |

80,000 | 84,274 | ||||||

| 5.0%, 6/1/2053 |

50,000 | 52,469 | ||||||

| 5.25%, 6/1/2058 |

130,000 | 137,558 | ||||||

| Duluth, MN, Economic Development Authority, Health Care Facilities Revenue, Essentia Health Obligated Group: |

||||||||

| Series A, 5.0%, 2/15/2048 |

200,000 | 237,456 | ||||||

| Series A, 5.0%, 2/15/2053 |

565,000 | 666,293 | ||||||

| Minneapolis, MN, Health Care Systems Revenue, Fairview Health Services, Series A, 5.0%, 11/15/2049 |

205,000 | 244,440 | ||||||

|

|

|

|||||||

| 1,422,490 | ||||||||

| Mississippi 0.7% |

| |||||||

| Lowndes County, MS, Solid Waste Disposal & Pollution Control Revenue, Weyerhaeuser Co. Project, Series A, 6.8%, 4/1/2022 |

250,000 | 274,907 | ||||||

| Mississippi, State Business Finance Corp., Solid Waste Disposal Revenue, Waste Pro U.S.A., Inc. Project, AMT, 144A, 5.0%**, 2/1/2036 |

145,000 | 153,503 | ||||||

| West Rankin, MS, Utility Authority Revenue, 5.0%, 1/1/2048, INS: AGMC |

500,000 | 582,115 | ||||||

|

|

|

|||||||

| 1,010,525 | ||||||||

The accompanying notes are an integral part of the financial statements.

| DWS Strategic Municipal Income Trust | | | 19 |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Missouri 2.1% |

| |||||||

| Kansas City, MO, Industrial Development Authority, Airport Special Obligation, International Airport Terminal Modernization Project, Series B, AMT, 5.0%, 3/1/2049, INS: AGMC |

1,000,000 | 1,193,430 | ||||||

| Kansas City, MO, Land Clearance Redevelopment Authority Project Revenue, Convention Center Hotel Project: |

||||||||

| Series B, 144A, 5.0%, 2/1/2040 |

200,000 | 220,680 | ||||||

| Series B, 144A, 5.0%, 2/1/2050 |

220,000 | 239,004 | ||||||

| Lee’s Summit, MO, Industrial Development Authority, Senior Living Facilities Revenue, John Knox Village Project, Series A, 5.0%, 8/15/2042 |

500,000 | 549,365 | ||||||

| Missouri, State Health & Educational Facilities Authority Revenue, Medical Research, Lutheran Senior Services, Series A, 5.0%, 2/1/2046 |

65,000 | 72,934 | ||||||

| Missouri, State Health & Educational Facilities Authority, Health Facilities Revenue, Lester E Cox Medical Centers, Series A, 5.0%, 11/15/2048 |

150,000 | 163,338 | ||||||

| St. Louis County, MO, Industrial Development Authority, Senior Living Facilities, Friendship Village, 5.0%, 9/1/2048 |

245,000 | 274,314 | ||||||

| St. Louis, MO, Industrial Development Authority Financing Revenue, Ballpark Village Development Project, Series A, 4.75%, 11/15/2047 |

225,000 | 245,257 | ||||||

|

|

|

|||||||

| 2,958,322 | ||||||||

| Nebraska 0.6% |

| |||||||

| Douglas County, NE, Hospital Authority No. 2, Health Facilities, Children’s Hospital Obligated Group, 5.0%, 11/15/2047 |

535,000 | 620,279 | ||||||

| Nebraska, Central Plains Energy Project, Gas Project Revenue: |

||||||||

| Series A, 5.0%, 9/1/2029 |

70,000 | 86,542 | ||||||

| Series A, 5.0%, 9/1/2033 |

155,000 | 199,809 | ||||||

|

|

|

|||||||

| 906,630 | ||||||||

| Nevada 1.2% |

| |||||||

| Las Vegas Valley, NV, Water District, Series B, 5.0%, 6/1/2037 |

1,565,000 | 1,696,382 | ||||||

| Reno, NV, Sales Tax Revenue, Transportation Rail Access, Series C, 144A, Zero Coupon, 7/1/2058 |

500,000 | 72,330 | ||||||

|

|

|

|||||||

| 1,768,712 | ||||||||

| New Hampshire 0.4% |

| |||||||

| New Hampshire, State Health & Educational Facilities Authority Revenue, Hillside Village: |

||||||||

| Series A, 144A, 6.125%, 7/1/2037 |

100,000 | 108,445 | ||||||

The accompanying notes are an integral part of the financial statements.

| 20 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Series A, 144A, 6.125%, 7/1/2052 |

300,000 | 323,910 | ||||||

| Series A, 144A, 6.25%, 7/1/2042 |

125,000 | 135,869 | ||||||

|

|

|

|||||||

| 568,224 | ||||||||

| New Jersey 5.4% |

| |||||||

| New Jersey, State Economic Development Authority Revenue: |

||||||||

| Series DDD, 5.0%, 6/15/2042 |

140,000 | 156,751 | ||||||

| Series BBB, 5.5%, 6/15/2030 |

895,000 | 1,066,697 | ||||||

| New Jersey, State Economic Development Authority Revenue, Black Horse EHT Urban Renewal LLC Project, Series A, 144A, 5.0%, 10/1/2039 |

605,000 | 606,821 | ||||||

| New Jersey, State Economic Development Authority, Motor Vehicle Surcharge Revenue, Series A, 5.0%, 7/1/2033 |

115,000 | 132,448 | ||||||

| New Jersey, State Economic Development Authority, Special Facilities Revenue, Continental Airlines, Inc. Project, Series B, AMT, 5.625%, 11/15/2030 |

500,000 | 572,700 | ||||||

| New Jersey, State Economic Development Authority, State Government Buildings Project: |

||||||||

| Series A, 5.0%, 6/15/2042 |

115,000 | 129,475 | ||||||

| Series A, 5.0%, 6/15/2047 |

130,000 | 145,699 | ||||||

| New Jersey, State Health Care Facilities Financing Authority Revenue, University Hospital, Series A, 5.0%, 7/1/2046, INS: AGMC |

180,000 | 202,829 | ||||||

| New Jersey, State Transportation Trust Fund Authority, Series B, 5.5%, 6/15/2031 |

1,500,000 | 1,581,675 | ||||||

| New Jersey, State Transportation Trust Fund Authority, Transportation Program Bonds, Series AA, 5.0%, 6/15/2046 |

1,400,000 | 1,588,678 | ||||||

| New Jersey, Tobacco Settlement Financing Corp.: |

| |||||||

| Series A, 5.0%, 6/1/2046 |

350,000 | 397,645 | ||||||

| Series B, 5.0%, 6/1/2046 |

750,000 | 829,215 | ||||||

| Series A, 5.25%, 6/1/2046 |

175,000 | 203,042 | ||||||

|

|

|

|||||||

| 7,613,675 | ||||||||

| New Mexico 0.3% |

| |||||||

| New Mexico, State Mortgage Finance Authority, “I”, Series D, 3.25%, 7/1/2044 |

485,000 | 501,335 | ||||||

| New York 5.5% |

| |||||||

| New York, Brooklyn Arena Local Development Corp., Pilot Revenue, Barclays Center Project, Series A, 4.0%, 7/15/2035, INS: AGMC |

45,000 | 49,826 | ||||||

| New York, Buffalo & Fort Erie Public Bridge Authority, 5.0%, 1/1/2047 |

1,000,000 | 1,167,190 | ||||||

| New York, Metropolitan Transportation Authority Revenue: |

||||||||

| Series D, 5.0%, 11/15/2038 |

275,000 | 307,871 | ||||||

The accompanying notes are an integral part of the financial statements.

| DWS Strategic Municipal Income Trust | | | 21 |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Series E-1, 5.0%, 11/15/2042 |

70,000 | 76,259 | ||||||

| Series E-1, Prerefunded, 5.0%, 11/15/2042 |

235,000 | 262,768 | ||||||

| New York, State Dormitory Authority Revenues, Non-State Supported Debt, Montefiore Obligated Group: |

||||||||

| Series A, 5.0%, 8/1/2034 |

75,000 | 90,754 | ||||||

| Series A, 5.0%, 8/1/2035 |

105,000 | 126,543 | ||||||

| New York, State Liberty Development Corp. Revenue, World Trade Center Project, Class 1-3, 144A, 5.0%, 11/15/2044 |

915,000 | 1,010,993 | ||||||

| New York, State Transportation Development Corp., Special Facilities Revenue, American Airlines, Inc., John F. Kennedy International Airport Project, AMT, 5.0%, 8/1/2031, GTY: American Airlines Group |

445,000 | 465,167 | ||||||

| New York, State Transportation Development Corp., Special Facilities Revenue, Delta Air Lines, Inc., LaGuardia Airport C&D Redevelopment: |

||||||||

| AMT, 5.0%, 1/1/2033 |

100,000 | 118,965 | ||||||

| AMT, 5.0%, 1/1/2034 |

100,000 | 118,738 | ||||||

| AMT, 5.0%, 1/1/2036 |

100,000 | 118,170 | ||||||

| New York, State Transportation Development Corp., Special Facilities Revenue, Laguardia Gateway Partners LLC, Redevelopment Project, Series A, AMT, 5.0%, 7/1/2041 |

1,200,000 | 1,330,464 | ||||||

| New York, TSASC, Inc.: |

||||||||

| Series A, 5.0%, 6/1/2041 |

60,000 | 67,272 | ||||||

| Series B, 5.0%, 6/1/2045 |

730,000 | 726,664 | ||||||

| Series B, 5.0%, 6/1/2048 |

310,000 | 307,672 | ||||||

| New York & New Jersey Port Authority, Series 207, AMT, 5.0%, 9/15/2048 |

625,000 | 739,581 | ||||||

| New York & New Jersey Port Authority, Special Obligation Revenue, JFK International Air Terminal LLC, 6.0%, 12/1/2042 |

680,000 | 709,947 | ||||||

|

|

|

|||||||

| 7,794,844 | ||||||||

| North Carolina 0.4% |

| |||||||

| New Hanover County, NC, Hospital Revenue, New Hanover Regional Medical Centre: |

||||||||

| 5.0%, 10/1/2042 |

260,000 | 298,040 | ||||||

| 5.0%, 10/1/2047 |

240,000 | 273,454 | ||||||

|

|

|

|||||||

| 571,494 | ||||||||

| Ohio 3.9% |

| |||||||

| Buckeye, OH, Tobacco Settlement Financing Authority, Series A-2, 5.875%, 6/1/2047 |

1,175,000 | 1,181,051 | ||||||

| Centerville, OH, Health Care Revenue, Graceworks Lutheran Services, 5.25%, 11/1/2047 |

220,000 | 240,669 | ||||||

| Chillicothe, OH, Hospital Facilities Revenue, Adena Health System Obligated Group Project, 5.0%, 12/1/2047 |

445,000 | 523,049 | ||||||

The accompanying notes are an integral part of the financial statements.

| 22 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Cleveland-Cuyahoga County, OH, Port Authority Cultural Facility Revenue, Playhouse Square Foundation Project, 5.5%, 12/1/2053 |

270,000 | 311,361 | ||||||

| Ohio, Akron, Bath & Copley Joint Township Hospital District Revenue, 5.25%, 11/15/2046 |

615,000 | 718,671 | ||||||

| Ohio, American Municipal Power, Inc. Revenue, Fremont Energy Center Project, Series B, 5.0%, 2/15/2037 |

1,575,000 | 1,685,628 | ||||||

| Ohio, State Air Quality Development Authority, Exempt Facilities Revenue, Pratt Paper LLC Project: |

||||||||

| AMT, 144A, 4.25%, 1/15/2038, GTY: Pratt Industries, Inc. |

70,000 | 75,527 | ||||||

| AMT, 144A, 4.5%, 1/15/2048, GTY: Pratt Industries, Inc. |

225,000 | 243,247 | ||||||

| Ohio, State Hospital Revenue, Aultman Health Foundation, 144A, 5.0%, 12/1/2048 |

500,000 | 535,690 | ||||||

|

|

|

|||||||

| 5,514,893 | ||||||||

| Oklahoma 0.9% |

| |||||||

| Oklahoma, State Development Finance Authority, Health System Revenue, OU Medicine Project: |

||||||||

| Series B, 5.5%, 8/15/2052 |

180,000 | 215,498 | ||||||

| Series B, 5.5%, 8/15/2057 |

880,000 | 1,046,839 | ||||||

|

|

|

|||||||

| 1,262,337 | ||||||||

| Oregon 0.6% |

| |||||||

| Clackamas County, OR, Hospital Facilities Authority Revenue, Mary’s Woods at Marylhurst, Inc. Project, Series A, 5.0%, 5/15/2038 |

25,000 | 27,787 | ||||||

| Oregon, Portland Airport Revenue, Series 25B, AMT, 5.0%, 7/1/2049 |

665,000 | 798,685 | ||||||

|

|

|

|||||||

| 826,472 | ||||||||

| Pennsylvania 6.5% |

| |||||||

| Cumberland County, PA, Municipal Authority, Asbury Pennsylvania Obligated Group, 5.0%, 1/1/2045 (a) |

50,000 | 54,327 | ||||||

| Doylestown, PA, Hospital Authority Revenue, Series A, 5.0%, 7/1/2049 |

140,000 | 160,849 | ||||||

| Franklin County, PA, Industrial Development Authority Revenue, Menno Haven, Inc. Project: |

||||||||

| 5.0%, 12/1/2043 |

60,000 | 65,536 | ||||||

| 5.0%, 12/1/2048 |

65,000 | 70,813 | ||||||

| 5.0%, 12/1/2053 |

95,000 | 103,120 | ||||||

| Lancaster County, PA, Hospital Authority, Brethren Village Project: |

||||||||

| 5.125%, 7/1/2037 |

100,000 | 109,132 | ||||||

| 5.25%, 7/1/2041 |

100,000 | 109,605 | ||||||

The accompanying notes are an integral part of the financial statements.

| DWS Strategic Municipal Income Trust | | | 23 |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Montgomery County, PA, Industrial Development Authority, Meadowood Senior Living Project: |

||||||||

| Series A, 5.0%, 12/1/2038 |

85,000 | 96,342 | ||||||

| Series A, 5.0%, 12/1/2048 |

215,000 | 240,323 | ||||||

| Pennsylvania, Certificate of Participations, Series A, 5.0%, 7/1/2043 |

155,000 | 183,861 | ||||||

| Pennsylvania, Commonwealth Financing Authority, Series A, 5.0%, 6/1/2035 |

315,000 | 362,181 | ||||||

| Pennsylvania, Commonwealth Financing Authority, Tobacco Master Settlement Payment Revenue Bonds: |

||||||||

| 5.0%, 6/1/2034 |

250,000 | 304,305 | ||||||

| 5.0%, 6/1/2035 |

125,000 | 151,342 | ||||||

| Pennsylvania, Geisinger Authority Health System Revenue, Series A-1, 5.0%, 2/15/2045 |

740,000 | 868,212 | ||||||

| Pennsylvania, State Economic Development Financing Authority Revenue, Bridges Finco LP: |

||||||||

| AMT, 5.0%, 12/31/2034 |

1,000,000 | 1,154,390 | ||||||

| AMT, 5.0%, 12/31/2038 |

1,000,000 | 1,144,690 | ||||||

| Pennsylvania, State Turnpike Commission Revenue: |

| |||||||

| Series A-1, 5.0%, 12/1/2040 |

2,500,000 | 2,872,450 | ||||||

| Series C, 5.0%, 12/1/2044 |

240,000 | 272,059 | ||||||

| Philadelphia, PA, Authority for Individual Development Senior Living Revenue, Wesley Enhanced Living Obligated Group: |

||||||||

| Series A, 5.0%, 7/1/2042 |

135,000 | 149,604 | ||||||

| Series A, 5.0%, 7/1/2049 |

160,000 | 176,074 | ||||||

| Philadelphia, PA, School District, Series B, 5.0%, 9/1/2043 |

500,000 | 592,865 | ||||||

|

|

|

|||||||

| 9,242,080 | ||||||||

| Puerto Rico 0.7% |

| |||||||

| Puerto Rico, Sales Tax Financing Corp., Sales Tax Revenue, Series A-1, 5.0%, 7/1/2058 |

997,000 | 1,047,598 | ||||||

| Rhode Island 0.1% |

| |||||||

| Rhode Island, Tobacco Settlement Financing Corp., Series A, 5.0%, 6/1/2040 |

155,000 | 172,262 | ||||||

| South Carolina 4.0% |

| |||||||

| Hardeeville, SC, Assessment Revenue, Anderson Tract Municipal Improvement District, Series A, 7.75%, 11/1/2039 |

815,000 | 816,027 | ||||||

| South Carolina, State Jobs-Economic Development Authority, Residential Facilities Revenue, Episcopal Home Still Hopes: |

||||||||

| 5.0%, 4/1/2047 |

200,000 | 216,966 | ||||||

| 5.0%, 4/1/2052 |

175,000 | 189,401 | ||||||

| South Carolina, State Ports Authority Revenue, Series B, AMT, 4.0%, 7/1/2049 |

2,000,000 | 2,187,420 | ||||||

The accompanying notes are an integral part of the financial statements.

| 24 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| South Carolina, State Public Service Authority Revenue, Series E, 5.25%, 12/1/2055 |

1,070,000 | 1,232,255 | ||||||

| South Carolina, State Public Service Authority Revenue, Santee Cooper, Series A, Prerefunded, 5.75%, 12/1/2043 |

890,000 | 1,047,476 | ||||||

|

|

|

|||||||

| 5,689,545 | ||||||||

| Tennessee 0.6% |

| |||||||

| Greeneville, TN, Health & Educational Facilities Board Hospital Revenue, Ballad Health Obligation Group: |

||||||||

| Series A, 5.0%, 7/1/2037 |

300,000 | 355,923 | ||||||

| Series A, 5.0%, 7/1/2044 |

400,000 | 468,460 | ||||||

|

|

|

|||||||

| 824,383 | ||||||||

| Texas 19.6% |

| |||||||

| Austin, TX, Airport Systems Revenue, Series B, AMT, 5.0%, 11/15/2048 |

1,000,000 | 1,210,700 | ||||||

| Central Texas, Regional Mobility Authority Revenue, Senior Lien: |

||||||||

| Series A, 5.0%, 1/1/2040 |

230,000 | 263,573 | ||||||

| Series A, 5.0%, 1/1/2043 |

1,500,000 | 1,624,620 | ||||||

| Prerefunded, 6.0%, 1/1/2041 |

545,000 | 573,046 | ||||||

| Dallas-Fort Worth, International Airport Revenue: |

||||||||

| Series F, AMT, Prerefunded, 5.0%, 11/1/2035 |

1,000,000 | 1,033,670 | ||||||

| Series D, AMT, 5.0%, 11/1/2038 |

2,000,000 | 2,118,220 | ||||||

| Houston, TX, Airport System Revenue, Series A, AMT, 5.0%, 7/1/2041 |

750,000 | 895,657 | ||||||

| Houston, TX, Airport System Revenue, Special Facilities United Airlines, Inc., Airport Improvement Projects, AMT, 5.0%, 7/15/2028 |

300,000 | 358,491 | ||||||

| Matagorda County, TX, Navigation District No. 1, Pollution Control Revenue, AEP Texas Central Co. Project, Series A, 4.4%, 5/1/2030, INS: AMBAC |

2,250,000 | 2,664,922 | ||||||

| Mission, TX, Economic Development Corp. Revenue, Senior Lien-Natgasoline Project, AMT, 144A, 4.625%, 10/1/2031 |

210,000 | 227,392 | ||||||

| Newark, TX, Higher Education Finance Corp., Education Revenue, Austin Achieve Public School, Inc., 5.0%, 6/15/2048 |

60,000 | 61,519 | ||||||

| North Texas, Tollway Authority Revenue: |

||||||||

| Series B, 5.0%, 1/1/2045 |

665,000 | 753,113 | ||||||

| 5.0%, 1/1/2048 |

1,355,000 | 1,603,399 | ||||||

| San Antonio, TX, Convention Center Hotel Finance Corp., Contract Revenue, Empowerment Zone, Series A, AMT, 5.0%, 7/15/2039, INS: AMBAC |

1,000,000 | 1,000,650 | ||||||

| Tarrant County, TX, Cultural Education Facilities Finance Corp. Revenue, Christus Health Obligated Group, Series B, 5.0%, 7/1/2048 |

1,000,000 | 1,189,470 | ||||||

The accompanying notes are an integral part of the financial statements.

| DWS Strategic Municipal Income Trust | | | 25 |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Tarrant County, TX, Cultural Education Facilities Finance Corp. Revenue, Trinity Terrace Project, The Cumberland Rest, Inc., Series A-1, 5.0%, 10/1/2044 |

175,000 | 189,625 | ||||||

| Tarrant County, TX, Cultural Education Facilities Finance Corp., Buckner Retirement Services Revenue, 5.0%, 11/15/2046 |

1,000,000 | 1,143,230 | ||||||

| Tarrant County, TX, Cultural Education Facilities Finance Corp., Hospital Revenue, Scott & White Healthcare, 5.0%, 8/15/2043 |

2,100,000 | 2,319,807 | ||||||

| Temple, TX, Tax Increment, Reinvestment Zone No. 1, Series A, 144A, 5.0%, 8/1/2038 |

300,000 | 328,095 | ||||||

| Texas, Grand Parkway Transportation Corp., System Toll Revenue, Series B, 5.0%, 4/1/2053 |

500,000 | 554,550 | ||||||

| Texas, Love Field Airport Modernization Corp., Special Facilities Revenue, Southwest Airlines Co. Project, 5.25%, 11/1/2040 |

1,055,000 | 1,088,686 | ||||||

| Texas, New Hope Cultural Education Facilities Finance Corp., Retirement Facilities Revenue, Legacy Midtown Park, Inc. Project, Series A, 5.5%, 7/1/2054 |

250,000 | 263,105 | ||||||

| Texas, New Hope Cultural Education Facilities Finance Corp., Retirement Facilities Revenue, Presbyterian Village North Project, 5.0%, 10/1/2039 |

180,000 | 197,620 | ||||||

| Texas, SA Energy Acquisition Public Facility Corp., Gas Supply Revenue, 5.5%, 8/1/2020 |

2,000,000 | 2,051,180 | ||||||

| Texas, State Municipal Gas Acquisition & Supply Corp. III Gas Supply Revenue: |

||||||||

| 5.0%, 12/15/2030 |

165,000 | 178,980 | ||||||

| 5.0%, 12/15/2031 |

1,000,000 | 1,083,600 | ||||||

| 5.0%, 12/15/2032 |

1,000,000 | 1,081,980 | ||||||

| Texas, State Private Activity Bond, Surface Transportation Corp. Revenue, Senior Lien, North Tarrant Express Mobility Partners Segments LLC, AMT, 6.75%, 6/30/2043 |

280,000 | 324,010 | ||||||

| Texas, State Transportation Commission, Turnpike Systems Revenue, Series C, 5.0%, 8/15/2034 |

825,000 | 942,208 | ||||||

| Travis County, TX, Health Facilities Development Corp. Revenue, Westminster Manor Health, Prerefunded, 7.125%, 11/1/2040 |

510,000 | 536,908 | ||||||

|

|

|

|||||||

| 27,862,026 | ||||||||

| Utah 1.5% |

| |||||||

| Salt Lake City, UT, Airport Revenue: |

||||||||

| Series A, AMT, 5.0%, 7/1/2043 |

190,000 | 226,206 | ||||||

| Series A, AMT, 5.0%, 7/1/2047 |

595,000 | 694,062 | ||||||

| Series A, AMT, 5.0%, 7/1/2048 |

115,000 | 136,106 | ||||||

| Utah, Infrastructure Agency Telecommunication Revenue, Series 2019, 4.0%, 10/15/2042 |

650,000 | 677,567 | ||||||

The accompanying notes are an integral part of the financial statements.

| 26 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Utah, State Charter School Financing Authority Revenue, Freedom Academy Foundation Project, 144A, 5.375%, 6/15/2048 |

320,000 | 334,595 | ||||||

|

|

|

|||||||

| 2,068,536 | ||||||||

| Virginia 1.2% |

| |||||||

| Roanoke County, VA, Economic Development Authority, RSDL Care Facilities Revenue, Series A, 5.375%, 9/1/2054 |

500,000 | 522,920 | ||||||

| Virginia, Peninsula Town Center, Community Development Authority Revenue, Special Obligation: |

||||||||

| 144A, 5.0%, 9/1/2037 |

100,000 | 112,249 | ||||||

| 144A, 5.0%, 9/1/2045 |

100,000 | 110,711 | ||||||

| Virginia, Small Business Financing Authority, Private Activity Revenue, Transform 66 P3 Project, AMT, 5.0%, 12/31/2052 |

865,000 | 988,349 | ||||||

|

|

|

|||||||

| 1,734,229 | ||||||||

| Washington 3.0% |

| |||||||

| Klickitat County, WA, Public Hospital District No. 2 Revenue, Skyline Hospital: |

||||||||

| 5.0%, 12/1/2037 |

100,000 | 101,004 | ||||||

| 5.0%, 12/1/2046 |

135,000 | 135,396 | ||||||

| Pierce County, WA, Bethel School District No. 403, 4.0%, 12/1/2037 |

1,000,000 | 1,148,210 | ||||||

| Washington, Port of Seattle Revenue, Series A, AMT, 5.0%, 5/1/2043 |

415,000 | 482,599 | ||||||

| Washington, State Health Care Facilities Authority, Catholic Health Initiatives, Series A, Prerefunded, 5.0%, 2/1/2041 |

595,000 | 620,841 | ||||||

| Washington, State Health Care Facilities Authority, Virginia Mason Medical Center: |

||||||||

| 5.0%, 8/15/2034 |

135,000 | 156,238 | ||||||

| 5.0%, 8/15/2035 |

120,000 | 138,551 | ||||||

| 5.0%, 8/15/2036 |

80,000 | 92,151 | ||||||

| Washington, State Housing Finance Commission, Reference Judson Park Project, 144A, 5.0%, 7/1/2048 |

50,000 | 53,905 | ||||||

| Washington, State Housing Finance Commission, Rockwood Retirement Communities Project, Series A, 144A, 7.375%, 1/1/2044 |

1,000,000 | 1,140,320 | ||||||

| Washington, State Housing Finance Commission, The Hearthstone Project: |

||||||||

| Series A, 144A, 5.0%, 7/1/2038 |

50,000 | 54,090 | ||||||

| Series A, 144A, 5.0%, 7/1/2048 |

115,000 | 122,846 | ||||||

| Series A, 144A, 5.0%, 7/1/2053 |

75,000 | 79,837 | ||||||

|

|

|

|||||||

| 4,325,988 | ||||||||

The accompanying notes are an integral part of the financial statements.

| DWS Strategic Municipal Income Trust | | | 27 |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| West Virginia 0.7% |

| |||||||

| West Virginia, State Hospital Finance Authority, State University Health System Obligated Group, Series A, 5.0%, 6/1/2047 |

805,000 | 935,933 | ||||||

| Wisconsin 6.2% |

| |||||||

| Wisconsin, Health Educational Facilities Authority, Covenant Communities, Inc. Project: |

||||||||

| Series A-1, 5.0%, 7/1/2043 |

500,000 | 550,665 | ||||||

| Series B, 5.0%, 7/1/2048 |

90,000 | 96,256 | ||||||

| Wisconsin, Public Finance Authority, Education Revenue, Mountain Island Charter School Ltd.: |

||||||||

| 5.0%, 7/1/2047 |

200,000 | 215,496 | ||||||

| 5.0%, 7/1/2052 |

90,000 | 96,547 | ||||||

| Wisconsin, Public Finance Authority, Hospital Revenue, Series A, 5.0%, 10/1/2044 |

730,000 | 874,868 | ||||||

| Wisconsin, Public Finance Authority, Senior Living Community First Mortgage Revenue, Cedars Obligated Group: |

||||||||

| 144A, 5.5%, 5/1/2039 |

70,000 | 71,127 | ||||||

| 144A, 5.75%, 5/1/2054 |

675,000 | 686,731 | ||||||

| Wisconsin, Public Finance Authority, Senior Living Revenue, Mary’s Woods at Marylhurst Project, Series A, 144A, 5.25%, 5/15/2052 |

1,000,000 | 1,112,720 | ||||||

| Wisconsin, Public Finance Authority, Student Housing Revenue, Nevada State College, 144A, 5.0%, 5/1/2055 |

1,750,000 | 1,883,210 | ||||||

| Wisconsin, Public Financing Authority, Retirement Facilities Revenue, Southminster, Inc.: |

||||||||

| 144A, 5.0%, 10/1/2043 |

65,000 | 72,019 | ||||||

| 144A, 5.0%, 10/1/2048 |

185,000 | 204,456 | ||||||

| 144A, 5.0%, 10/1/2053 |

350,000 | 385,826 | ||||||

| Wisconsin, State Health & Educational Facilities Authority Revenue, Agnesian Healthcare, Inc., Series B, Prerefunded, 5.0%, 7/1/2036 |

500,000 | 565,400 | ||||||

| Wisconsin, State Health & Educational Facilities Authority Revenue, ThedaCare, Inc., Series A, 5.5%, 12/15/2038 |

1,765,000 | 1,768,654 | ||||||

| Wisconsin, State Health & Educational Facilities Authority, St. John’s Communities, Inc. Project: |

||||||||

| Series A, 5.0%, 9/15/2040 |

25,000 | 26,308 | ||||||

| Series A, 5.0%, 9/15/2045 |

30,000 | 31,461 | ||||||

| Series A, 5.0%, 9/15/2050 |

125,000 | 130,861 | ||||||

|

|

|

|||||||

| 8,772,605 | ||||||||

| Total Municipal Bonds and Notes (Cost $180,262,957) |

|

192,819,337 | ||||||

The accompanying notes are an integral part of the financial statements.

| 28 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Underlying Municipal Bonds of Inverse Floaters (b) 29.2% |

| |||||||

| Florida 4.2% |

| |||||||

| Orange County, FL, School Board Certificates Participation, Series C, 5.0%, 8/1/2034 (c) |

5,000,000 | 5,967,688 | ||||||

| Trust: Orange County, FL, School Board, Series 2016-XM0183, 144A, 14.51%, 2/1/2024, Leverage Factor at purchase date: 4 to 1 |

||||||||

| Massachusetts 8.2% |

| |||||||

| Massachusetts, State Development Finance Agency Revenue, Partners Healthcare System, Inc., Series Q, 5.0%, 7/1/2035 (c) |

5,000,000 | 5,970,438 | ||||||

| Trust: Massachusetts, State Development Finance Agency Revenue, Series 2016-XM0136, 144A, 14.72%, 1/1/2024, Leverage Factor at purchase date: 4 to 1 |

||||||||

| Massachusetts, State Development Finance Agency Revenue, Harvard University, Series A, 4.0%, 7/15/2036 (c) |

5,000,000 | 5,715,063 | ||||||

| Trust: Massachusetts, State Development Finance Agency Revenue, Series 2016-XM0401, 144A, 10.72%, 7/15/2024, Leverage Factor at purchase date: 4 to 1 |

||||||||

|

|

|

|||||||

| 11,685,501 | ||||||||

| New York 8.4% |

| |||||||

| New York, State Urban Development Corp. Revenue, Personal Income Tax, Series C-3, 5.0%, 3/15/2040 (c) |

5,000,000 | 6,021,063 | ||||||

| Trust: New York, State Urban Development Corp. Revenue, Personal Income Tax, Series 2018-XM0581, 144A, 15.155%, 9/15/2025, Leverage Factor at purchase date: 4 to 1 |

||||||||

| New York City, NY, Transitional Finance Authority, Building AID Revenue, Series S-1, 5.0%, 7/15/2037 (c) |

5,000,000 | 5,882,288 | ||||||

| Trust: New York, Transitional Finance Authority Building AID Revenue, Series 2018-XM0619, 144A, 15.065%, 1/15/2024, Leverage Factor at purchase date: 4 to 1 |

||||||||

|

|

|

|||||||

| 11,903,351 | ||||||||

| Texas 4.2% |

| |||||||

| Texas, State Transportation Commission- Highway Improvement, Series A, 5.0%, 4/1/2038 (c) |

5,000,000 | 5,910,363 | ||||||

| Trust: Texas, State Transportation Commission, Series 2016-XM0405, 144A, 14.72%, 4/1/2024, Leverage Factor at purchase date: 4 to 1 |

||||||||

The accompanying notes are an integral part of the financial statements.

| DWS Strategic Municipal Income Trust | | | 29 |

Table of Contents

| Principal Amount ($) |

Value ($) | |||||||

| Washington 4.2% |

| |||||||

| Washington, State General Obligation, Series D, 5.0%, 2/1/2035 (c) |

5,000,000 | 6,045,225 | ||||||

| Trust: Washington, State General Obligation, Series 2017-XM0478, 144A, 14.72%, 8/1/2024, Leverage Factor at purchase date: 4 to 1 |

||||||||

|

|

||||||||

| Total Underlying Municipal Bonds of Inverse Floaters (Cost $39,312,351) |

|

41,512,128 | ||||||

| Other Municipal Related 0.0% |

| |||||||

| Tarrant County, TX, Cultural Education Facilities Finance Corp., Retirement Facilities Revenue, Mirador Project, Escrow, Series A, 5.0%, 11/15/2055* (Cost $0) |

570,000 | 5,700 | ||||||

| Open-End Investment Companies 0.7% |

| |||||||

| BlackRock Liquidity Funds MuniCash Portfolio, Institutional Shares, 0.939%*** (Cost $1,028,458) |

1,028,271 | 1,028,320 | ||||||

| % of Net Assets |

Value ($) | |||||||

| Total Investment Portfolio (Cost $220,603,766) | 165.5 | 235,365,485 | ||||||

| Floating Rate Notes (b) | (18.5 | ) | (26,250,000 | ) | ||||

| Series 2018 MTPS, net of deferred offering cost | (49.2 | ) | (69,994,382 | ) | ||||

| Other Assets and Liabilities, Net | 2.2 | 3,083,487 | ||||||

|

|

||||||||

| Net Assets Applicable to Common Shareholders | 100.0 | 142,204,590 | ||||||

The following table represents bonds that are in default:

| Security | Coupon | Maturity Date |

Principal Amount ($) |

Cost ($) | Value ($) | |||||||||||||||

| Collier County, FL, Authority, Continuing Care |

8.125 | % | 5/15/2044 | 290,000 | 285,934 | 275,886 | ||||||||||||||

| Connecticut, Mashantucket Western Pequot Tribe Bond* |

6.05 | % | 7/1/2031 | 2,983,189 | 1,909,657 | 111,869 | ||||||||||||||

| Florida, Tolomato Community Development District, Special Assessment, Series 2015-3* | 6.61 | % | 5/1/2040 | 165,000 | 0 | 2 | ||||||||||||||

| Florida, Tolomato Community Development District, Special Assessment, Series 3* | 6.55 | % | 5/1/2027 | 130,000 | 1 | 1 | ||||||||||||||

| 2,195,592 | 387,758 | |||||||||||||||||||

| * | Non-income producing security. |

The accompanying notes are an integral part of the financial statements.

| 30 | | | DWS Strategic Municipal Income Trust |

Table of Contents

| ** | Variable or floating rate security. These securities are shown at their current rate as of November 30, 2019. For securities based on a published reference rate and spread, the reference rate and spread are indicated within the description above. Certain variable rate securities are not based on a published reference rate and spread but adjust periodically based on current market conditions, prepayment of underlying positions and/or other variables. |

| *** | Current yield; not a coupon rate. |

| (a) | When-issued security. |

| (b) | Securities represent the underlying municipal obligations of inverse floating rate obligations held by the Fund. The Floating Rate Notes represents leverage to the Fund and is the amount owed to the floating rate note holders. |

| (c) | Security forms part of the below inverse floater. The Fund accounts for these inverse floaters as a form of secured borrowing, by reflecting the value of the underlying bond in the investments of the Fund and the amount owed to the floating rate note holder as a liability. |

144A: Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers.

AGMC: Assured Guaranty Municipal Corp.

AMBAC: Ambac Financial Group, Inc.

AMT: Subject to alternative minimum tax.

ETM: Bonds bearing the description ETM (escrow to maturity) are collateralized usually by U.S. Treasury securities which are held in escrow and used to pay principal and interest on bonds so designated.

GTY: Guaranty Agreement

INS: Insured

NATL: National Public Finance Guarantee Corp.

PIK: Denotes that all or a portion of the income is paid in-kind in the form of additional principal.

Prerefunded: Bonds which are prerefunded are collateralized usually by U.S. Treasury securities which are held in escrow and used to pay principal and interest on tax-exempt issues and to retire the bonds in full at the earliest refunding date.

Fair Value Measurements

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in three broad levels. Level 1 includes quoted prices in active markets for identical securities. Level 2 includes other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds and credit risk). Level 3 includes significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments). The level assigned to the securities valuations may not be an indication of the risk or liquidity associated with investing in those securities.