UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

———————

FORM

———————

For the quarterly period ended:

or

For the transition period from: _____________ to _____________

(Exact name of registrant as specified in its charter) |

———————

|

| |||

(State or Other Jurisdiction |

| (Commission |

| (I.R.S. Employer |

of Incorporation) |

| File Number) |

| Identification No.) |

(Address of Principal Executive Office) (Zip Code)

(

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

———————

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☐ (Do not check if a smaller reporting company) | Smaller reporting company | ||

|

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

|

|

TABLE OF CONTENTS

PART I - FINANCIAL INFORMATION

3 | ||

| Consolidated Balance Sheets as of September 30, 2022 (Unaudited) and December 31, 2021 | 3 |

| 4 | |

| 5 | |

| 6 | |

| 7 | |

| 8 | |

Management’s Discussion and Analysis of Financial Condition and Results of Operations. | 16 | |

23 | ||

23 |

| ||

24 | ||

24 | ||

Unregistered Sales of Equity Securities and Use of Proceeds. | 24 | |

24 | ||

24 | ||

24 | ||

25 | ||

| 26 | |

| 2 |

| Table of Contents |

PART I – FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

ISSUER DIRECT CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(in thousands, except share and per share amounts)

|

| September 30, |

|

| December 31, |

| ||

|

| 2022 |

|

| 2021 |

| ||

ASSETS |

| (unaudited) |

|

|

| |||

Current assets: |

|

|

|

|

|

| ||

Cash and cash equivalents |

| $ |

|

| $ |

| ||

Accounts receivable (net of allowance for doubtful accounts of $ |

|

|

|

|

|

| ||

Income tax receivable |

|

|

|

|

|

| ||

Other current assets |

|

|

|

|

|

| ||

Total current assets |

|

|

|

|

|

| ||

Capitalized software (net of accumulated amortization of $ |

|

|

|

|

|

| ||

Fixed assets (net of accumulated depreciation of $ |

|

|

|

|

|

| ||

Right-of-use asset – leases |

|

|

|

|

|

| ||

Other long-term assets |

|

|

|

|

|

| ||

Goodwill |

|

|

|

|

|

| ||

Intangible assets (net of accumulated amortization of $ |

|

|

|

|

|

| ||

Total assets |

| $ |

|

| $ |

| ||

|

|

|

|

|

|

|

|

|

LIABILITIES AND STOCKHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

|

|

|

|

Accounts payable |

| $ |

|

| $ |

| ||

Accrued expenses |

|

|

|

|

|

| ||

Income taxes payable |

|

|

|

|

|

| ||

Deferred revenue |

|

|

|

|

|

| ||

Total current liabilities |

|

|

|

|

|

| ||

Deferred income tax liability |

|

|

|

|

|

| ||

Lease liabilities – long-term |

|

|

|

|

|

| ||

Total liabilities |

|

|

|

|

|

| ||

Commitments and contingencies |

|

|

|

|

|

|

|

|

Stockholders' equity: |

|

|

|

|

|

|

|

|

Preferred stock, $ |

|

|

|

|

|

| ||

Common stock $ |

|

|

|

|

|

| ||

Additional paid-in capital |

|

|

|

|

|

| ||

Other accumulated comprehensive loss |

|

| ( | ) |

|

| ( | ) |

Retained earnings |

|

|

|

|

|

| ||

Total stockholders' equity |

|

|

|

|

|

| ||

Total liabilities and stockholders’ equity |

| $ |

|

| $ |

| ||

The accompanying notes are an integral part of these unaudited financial statements.

| 3 |

| Table of Contents |

ISSUER DIRECT CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(UNAUDITED)

(in thousands, except share and per share amounts)

|

| For the Three Months Ended |

|

| For the Nine Months Ended |

| ||||||||||

|

| September 30, |

|

| September 30, |

|

| September 30, |

|

| September 30, |

| ||||

|

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||

Revenues |

| $ |

|

| $ |

|

| $ |

|

| $ |

| ||||

Cost of revenues |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Gross profit |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Operating costs and expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

General and administrative |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Sales and marketing expenses |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Product development |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Depreciation and amortization |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Total operating costs and expenses |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Operating income |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Other income |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Interest income |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Income before taxes |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Income tax expense |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Net income |

| $ |

|

| $ |

|

| $ |

|

| $ |

| ||||

Income per share – basic |

| $ |

|

| $ |

|

| $ |

|

| $ |

| ||||

Income per share – fully diluted |

| $ |

|

| $ |

|

| $ |

|

| $ |

| ||||

Weighted average number of common shares outstanding – basic |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Weighted average number of common shares outstanding – fully diluted |

|

|

|

|

|

|

|

|

|

|

|

| ||||

The accompanying notes are an integral part of these unaudited financial statements.

| 4 |

| Table of Contents |

ISSUER DIRECT CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(UNAUDITED)

(in thousands)

|

| For the Three Months Ended |

|

| For the Nine Months Ended |

| ||||||||||

|

| September 30, |

|

| September 30, |

|

| September 30, |

|

| September 30, |

| ||||

|

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||

Net income |

| $ |

|

| $ |

|

| $ |

|

| $ |

| ||||

Foreign currency translation adjustment |

|

| ( | ) |

|

|

|

|

| ( | ) |

|

|

| ||

Comprehensive income |

| $ |

|

| $ |

|

| $ |

|

| $ |

| ||||

The accompanying notes are an integral part of these unaudited financial statements.

| 5 |

| Table of Contents |

ISSUER DIRECT CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

(UNAUDITED)

(in thousands, except share and per share amounts)

|

| Common Stock |

|

| Additional Paid-in |

|

| Other Accumulated Comprehensive Income |

|

| Retained |

|

| Total Stockholders’ |

| |||||||||

|

| Shares |

|

| Amount |

|

| Capital |

|

| (Loss) |

|

| Earnings |

|

| Equity |

| ||||||

Balance at December 31, 2020 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

|

| $ |

| |||||

Stock-based compensation expense |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Exercise of stock awards, net of tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Stock repurchase and retirement |

|

| ( | ) |

|

|

|

|

| ( | ) |

|

|

|

|

|

|

|

| ( | ) | |||

Foreign currency translation |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Net income |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Balance at March 31, 2021 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

|

| $ |

| |||||

Stock-based compensation expense |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Exercise of stock awards, net of tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Foreign currency translation |

|

| — |

|

|

|

|

|

|

|

|

| ( | ) |

|

|

|

|

| ( | ) | |||

Net income |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Balance at June 30, 2021 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

|

| $ |

| |||||

Stock-based compensation expense |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Exercise of stock awards, net of tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Foreign currency translation |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Net income |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Balance at September 30, 2021 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

|

| $ |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance at December 31, 2021 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

|

| $ |

| |||||

Stock-based compensation expense |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Exercise of stock awards, net of tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Stock repurchase and retirement |

|

| ( | ) |

|

|

|

|

| ( | ) |

|

|

|

|

|

|

|

| ( | ) | |||

Foreign currency translation |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Net income |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Balance at March 31, 2022 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

|

| $ |

| |||||

Stock-based compensation expense |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Exercise of stock awards, net of tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Stock repurchase and retirement |

|

| ( | ) |

|

|

|

|

| ( | ) |

|

|

|

|

|

|

|

| ( | ) | |||

Foreign currency translation |

|

| — |

|

|

|

|

|

|

|

|

| ( | ) |

|

|

|

|

| ( | ) | |||

Net income |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Balance at June 30, 2022 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

|

| $ |

| |||||

Stock-based compensation expense |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Exercise of stock awards, net of tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Stock repurchase and retirement |

|

| ( | ) |

|

|

|

|

| ( | ) |

|

|

|

|

|

|

|

| ( | ) | |||

Foreign currency translation |

|

| — |

|

|

|

|

|

|

|

|

| ( | ) |

|

|

|

|

| ( | ) | |||

Net income |

|

| — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Balance at September 30, 2022 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

|

| $ |

| |||||

The accompanying notes are an integral part of these unaudited financial statements.

| 6 |

| Table of Contents |

ISSUER DIRECT CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

(in thousands)

|

| For the Nine Months Ended |

| |||||

|

| September 30, |

|

| September 30, |

| ||

|

| 2022 |

|

| 2021 |

| ||

Cash flows from operating activities: |

|

|

|

|

|

| ||

Net income |

| $ |

|

| $ |

| ||

Adjustments to reconcile net income to net cash provided by operating activities: |

|

|

|

|

|

|

|

|

Depreciation and amortization |

|

|

|

|

|

| ||

Bad debt expense |

|

|

|

|

|

| ||

Deferred income taxes |

|

| ( | ) |

|

| ( | ) |

Stock-based compensation expense |

|

|

|

|

|

| ||

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

Decrease (increase) in accounts receivable |

|

| ( | ) |

|

| ( | ) |

Decrease (increase) in other assets |

|

| ( | ) |

|

| ( | ) |

Increase (decrease) in accounts payable |

|

| ( | ) |

|

|

| |

Increase (decrease) in accrued expenses |

|

| ( | ) |

|

| ( | ) |

Increase (decrease) in deferred revenue |

|

|

|

|

|

| ||

Net cash provided by operating activities |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

Cash flows from investing activities: |

|

|

|

|

|

|

|

|

Capitalized software |

|

|

|

|

| ( | ) | |

Purchase of fixed assets |

|

| ( | ) |

|

| ( | ) |

Net cash used in investing activities |

|

| ( | ) |

|

| ( | ) |

|

|

|

|

|

|

|

|

|

Cash flows from financing activities: |

|

|

|

|

|

|

|

|

Exercise of stock options |

|

|

|

|

|

| ||

Payment for stock repurchase and retirement |

|

| ( | ) |

|

| ( | ) |

Net cash used in financing activities |

|

| ( | ) |

|

| ( | ) |

|

|

|

|

|

|

|

|

|

Net change in cash and cash equivalents |

|

| ( | ) |

|

|

| |

Cash – beginning |

|

|

|

|

|

| ||

Currency translation adjustment |

|

| ( | ) |

|

| ( | ) |

Cash and cash equivalents – ending |

| $ |

|

| $ |

| ||

|

|

|

|

|

|

|

|

|

Supplemental disclosures: |

|

|

|

|

|

|

|

|

Cash paid for income taxes |

| $ |

|

| $ |

| ||

The accompanying notes are an integral part of these unaudited financial statements.

| 7 |

| Table of Contents |

ISSUER DIRECT CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Note 1. Basis of Presentation

The unaudited interim consolidated balance sheet as of September 30, 2022 and consolidated statements of operations, comprehensive income, stockholders’ equity, and cash flows for the three and nine-month periods ended September 30, 2022 and 2021 included herein, have been prepared in accordance with the instructions for Form 10-Q under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and Article 10 of Regulation S-X under the Exchange Act. In the opinion of management, they include all normal recurring adjustments necessary for a fair presentation of the financial statements. Results of operations reported for the interim periods are not necessarily indicative of results for the entire year. Certain information and footnote disclosures normally included in financial statements prepared in accordance with accounting principles generally accepted in the United States ("US GAAP") have been condensed or omitted pursuant to such rules and regulations relating to interim financial statements. The interim financial information should be read in conjunction with the 2021 audited financial statements of Issuer Direct Corporation (the “Company”, “We”, or “Our”) filed on our Form 10-K.

Note 2. Summary of Significant Accounting Policies

The consolidated financial statements include the accounts of the Company and its wholly-owned subsidiaries. Significant intercompany accounts and transactions are eliminated in consolidation.

Earnings Per Share (EPS)

Earnings per share accounting guidance requires that basic net income per common share be computed by dividing net income for the period by the weighted average number of common shares outstanding during the period. Diluted net income per share is computed by dividing the net income for the period by the weighted average number of common and dilutive common equivalent shares outstanding during the period. Shares issuable upon the exercise of stock options totaling

Revenue Recognition

Substantially all the Company’s revenue comes from contracts with customers for subscriptions to its cloud-based products or contracts for Communications and Compliance products and services. Customers consist of public corporate issuers and professional firms, such as investor and public relations firms. In the case of our news distribution and webcasting offerings, our customers also include private companies. The Company accounts for a contract with a customer when there is an enforceable contract between the Company and the customer, the rights of the parties are identified, the contract has economic substance, and collectability of the contract consideration is probable. The Company's revenues are measured based on consideration specified in the contract with each customer.

The Company's contracts include either a subscription to our entire platform or certain modules within our platform, or an agreement to perform services, or any combination thereof, and often contain multiple subscriptions and services. For these bundled contracts, the Company accounts for individual subscriptions and services as separate performance obligations if they are distinct, which is when a product or service is separately identifiable from other items in the bundled package, and a customer can benefit from it on its own or with other resources that are readily available to the customer. The Company separates revenue from its contracts into two revenue streams: i) Communications and ii) Compliance. Performance obligations of Communications contracts include providing subscriptions to certain modules or the entire Platform id. Communications module, distributing press releases on a per release basis or conducting webcasts, virtual annual meetings or other events on a per event basis. Performance obligations of Compliance contracts include providing subscriptions to our cloud-based Platform id. Compliance module, Whistleblower module or other stand-ready obligations to deliver services and annual report printing and distribution. Additionally, services are provided on a per project basis. Set up fees for disclosure services are considered a separate performance obligation and are satisfied upfront. Set up fees for our transfer agent module and investor relations content management module are immaterial. The Company’s subscription and service contracts are generally for one year, with automatic renewal clauses included in the contract until the contract is cancelled. The contracts do not contain any rights of returns, guarantees or warranties. Since contracts are generally for one year, all the revenue is expected to be recognized within one year from the contract start date. As such, the Company has elected the optional exemption that allows the Company not to disclose the transaction price allocated to performance obligations that are unsatisfied or partially satisfied at the end of each reporting period.

The Company recognizes revenue for subscriptions evenly over the contract period, upon distribution for per release contracts and upon event completion for webcasting and virtual annual meeting events. For service contracts that include stand ready obligations, revenue is recognized evenly over the contract period. For all other services delivered on a per project or event basis, the revenue is recognized at the completion of the event. The Company believes recognizing revenue for subscriptions and stand ready obligations using a time-based measure of progress, best reflects the Company’s performance in satisfying the obligations.

| 8 |

| Table of Contents |

For bundled contracts, revenue is allocated to each performance obligation based on its relative standalone selling price. Standalone selling prices are based on observable prices at which the Company separately sells the subscription or service. If a standalone selling price is not directly observable, the Company uses the residual method to allocate any remaining price to that subscription or service. The Company reviews standalone selling prices, at least annually, and updates these estimates if necessary.

The Company invoices its customers based on the billing schedules designated in its contracts, typically upfront on either a monthly, quarterly or annual basis or per transaction at the completion of the performance obligation. Deferred revenue for the periods presented was primarily press release packages which have been prepaid, however the releases have not yet been disseminated, as well as, subscription and service contracts, which are billed upfront, quarterly or annually, however the revenue has not yet been recognized. The associated deferred revenue is generally recognized as releases are disseminated for press release packages and ratably over the billing period for subscriptions. Deferred revenue as of September 30, 2022, and December 31, 2021, was $

Costs to obtain contracts with customers consist primarily of sales commissions. As of September 30, 2022 and December 31, 2021, the Company has capitalized $

Cash Equivalents

For purposes of the Company’s financial statements, the Company considers all highly liquid investments purchased with an original maturity date of three months or less to be cash equivalents.

Accounts Receivable and Allowance for Doubtful Accounts

The Company monitors outstanding receivables based on factors surrounding the credit risk of specific customers, historical trends, and other information. Credit is granted on an unsecured basis. The allowance for doubtful accounts is estimated based on an assessment of the Company’s ability to collect on customer accounts receivable. There is judgment involved with estimating the allowance for doubtful accounts and if the financial condition of the Company’s customers were to deteriorate, resulting in their inability to make the required payments, the Company may be required to record additional allowances or charges against revenues. Given the ongoing environment of the COVID-19 pandemic and recent economic downturn, additional attention has been paid to the financial viability of our customers. The Company generally writes off accounts receivable against the allowance when it determines a balance is uncollectible and no longer actively pursues its collection.

Concentration of Credit Risk

Financial instruments and related items which potentially subject the Company to concentrations of credit risk consist primarily of cash, cash equivalents and accounts receivable. The Company places its cash and temporary cash investments with credit quality institutions. Such cash balances are currently in excess of the FDIC insurance limit of $

The Company believes it did not have any financial instruments that could have potentially subjected us to significant concentrations of credit risk for any relevant period.

Use of Estimates

The preparation of financial statements in conformity with US GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Significant estimates include the allowance for doubtful accounts and the valuation of goodwill, intangible assets, deferred tax assets, and stock-based compensation. Actual results could differ from those estimates.

| 9 |

| Table of Contents |

Income Taxes

Deferred income tax assets and liabilities are computed for differences between the financial statement and tax bases of assets and liabilities that will result in future taxable or deductible amounts based on enacted tax laws and rates applicable to the periods in which the differences are expected to affect taxable income. Valuation allowances are established, when necessary, to reduce deferred income tax assets to the amounts expected to be realized. For any uncertain tax positions, we recognize the impact of a tax position, only if it is more likely than not of being sustained upon examination, based on the technical merits of the position. Our policy regarding the classification of interest and penalties is to classify them as income tax expense in our financial statements, if applicable.

Capitalized Software

Costs incurred to develop our cloud-based platform products are capitalized when the preliminary project phase is complete, management commits to fund the project and it is probable the project will be completed and used for its intended purposes. Once the software is substantially complete and ready for its intended use, the software is amortized over its estimated useful life, which is typically four years. Costs related to design or maintenance of the software are expensed as incurred. Capitalized costs and amortization for the three and nine-month periods ended September 30, 2022 and 2021, are as follows (in thousands):

|

| For the Three Months Ended |

|

| For the Nine Months Ended |

| ||||||||||

|

| September 30, |

|

| September 30, |

|

| September 30, |

|

| September 30, |

| ||||

|

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Capitalized software development costs |

| $ |

|

| $ |

|

| $ |

|

| $ |

| ||||

Amortization included in cost of revenues |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Impairment of Long-lived Assets

In accordance with the authoritative guidance for accounting for long-lived assets, assets such as property and equipment, trademarks, and intangible assets subject to amortization, are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset group may not be recoverable. Recoverability of asset groups to be held and used is measured by a comparison of the carrying amount of an asset group to estimated undiscounted future cash flows expected to be generated by the asset group. If the carrying amount of an asset group exceeds its estimated future cash flows, an impairment charge is recognized by the amount by which the carrying amount of an asset group exceeds fair value of the asset group.

Lease Accounting

The Company determines if an arrangement is a lease at inception. Operating lease agreements are primarily for office space and are included within lease right-of-use (“ROU”) assets and lease liabilities on the consolidated balance sheet.

ROU assets represent the right to use an underlying asset for the lease term and lease liabilities represent the obligation to make lease payments arising from the lease. ROU assets and lease liabilities are recognized at the commencement date based on the present value of lease payments over the lease term. Variable lease payments consist of non-lease services related to the lease and payments under operating leases classified as short-term. Variable lease payments are excluded from the ROU assets and lease liabilities and are recognized in the period in which the obligation for those payments is incurred. As most of the leases do not provide an implicit rate, the Company uses its incremental borrowing rate based on the information available at commencement date in determining the present value of lease payments. ROU assets include any lease payments due and exclude lease incentives. Rental expense for lease payments related to operating leases is recognized on a straight-line basis over the lease term.

Fair Value Measurements

ASC Topic 820 establishes a fair value hierarchy that requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. Assets and liabilities recorded at fair value in the financial statements are categorized based upon the hierarchy of levels of judgment associated with the inputs used to measure their fair value. Hierarchical levels directly related to the amount of subjectivity associated with the inputs to fair valuation of these assets and liabilities, are as follows:

| · | Level 1 – Quoted prices are available in active markets for identical assets or liabilities at the reporting date. Generally, this includes debt and equity securities that are traded in an active market. Our cash and cash equivalents are quoted at Level 1. |

|

|

|

| · | Level 2 – Observable inputs other than Level 1 prices such as quoted prices for similar assets or liabilities; quoted prices in markets that are not active; or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets or liabilities. Generally, this includes debt and equity securities that are not traded in an active market. |

|

|

|

| · | Level 3 – Unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities. Level 3 assets and liabilities include financial instruments whose value is determined using pricing models, discounted cash flow methodologies, or other valuation techniques, as well as instruments for which the determination of fair value requires significant management judgment or estimation. |

| 10 |

| Table of Contents |

As of September 30, 2022 and December 31, 2021, the Company believes that the fair value of our financial instruments, such as, accounts receivable, our line of credit, and accounts payable approximate their carrying amounts.

Translation of Foreign Financial Statements

The financial statements of the foreign subsidiaries of the Company have been translated into U.S. dollars. All assets and liabilities have been translated at current rates of exchange in effect at the end of the period. Income and expense items have been translated at the average exchange rates for the year or the applicable interim period. The gains or losses that result from this process are recorded as a separate component of other accumulated comprehensive income until the entity is sold or substantially liquidated.

Business Combinations, Goodwill and Intangible Assets

The authoritative guidance for business combinations specifies the criteria for recognizing and reporting intangible assets apart from goodwill. The Company records the assets acquired and liabilities assumed in business combinations at their respective fair values at the date of acquisition, with any excess purchase price recorded as goodwill. Goodwill is an asset representing the future economic benefits arising from other assets acquired in a business combination that are not individually identified and separately recognized. Intangible assets consist of client relationships, customer lists, distribution partner relationships, software, technology, non-compete agreements and trademarks that are initially measured at fair value. At the time of the business combination, trademarks are considered an indefinite-lived asset and, as such, are not amortized as there is no foreseeable limit to cash flows generated from them. The goodwill and intangible assets are assessed annually for impairment, or whenever conditions indicate the asset may be impaired, and any such impairment will be recognized in the period identified. The client relationships (

Comprehensive Income

Comprehensive income consists of net income and other comprehensive income related to changes in the cumulative foreign currency translation adjustment.

Advertising

The Company expenses advertising as incurred. During the three and nine-month periods ended September 30, 2022, advertising expense was $

Stock-based Compensation

The authoritative guidance for stock compensation requires that companies estimate the fair value of share-based payment awards on the date of the grant using an option-pricing model. The associated cost is recognized over the period during which an employee or director is required to provide service in exchange for the award.

Employee Retention Credit

On March 27, 2020, the Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”) was signed into law providing numerous tax provisions and other stimulus measures, including an employee retention credit (“ERC”), which is a refundable tax credit against certain employment taxes. The Taxpayer Certainty and Disaster Tax Relief Act of 2020 and the American Rescue Plan Act of 2021 extended and expanded the availability of the ERC.

We are eligible under the CARES Act ERC as an employer that carried on a trade or business during calendar year 2020 and whose business operations were fully or partially suspended during any calendar quarter in 2020 due to orders from an appropriate governmental authority limiting commerce, travel, or group meetings (for commercial, social, religious, or other purposes) due to COVID-19.

ASC 105, Generally Accepted Accounting Principles, describes the decision-making framework when no guidance exists in US GAAP for a particular transaction. Specifically, ASC 105-10-05-2 instructs companies to look for guidance for a similar transaction within US GAAP and apply that guidance by analogy. As such, forms of government assistance, such as the ERC, provided to business entities would not be within the scope of ASC 958, but it may be applied by analogy under ASC 105-10-05-2. We accounted for the ERC as a government grant in accordance with Accounting Standards Update 2013-06, Not-for-Profit Entities (Topic 958) by analogy under ASC 105-10-05-2. Under this standard, government grants are recognized when the conditions or conditions on which they depend are substantially met. The conditions for recognition of the ERC include, but are not limited to:

| · | An entity has been adversely affected by the COVID-19 pandemic |

|

|

|

| · | We have not used qualifying payroll for both the Paycheck Protection Program and the ERC |

|

|

|

| · | We incurred payroll costs to retain employees |

During the three and nine months ended September 30, 2021, we recorded an ERC benefit of

| 11 |

| Table of Contents |

Note 3: Equity

2014 Equity Incentive Plan

On May 23, 2014, the shareholders of the Company approved the 2014 Equity Incentive Plan (the “2014 Plan”). Under the terms of the 2014 Plan, the Company is authorized to issue incentive awards for common stock up to

The following table summarizes information about stock options outstanding and exercisable at September 30, 2022:

|

|

|

| Options Outstanding |

|

| Options Exercisable |

| |||||||||||

| Exercise Price Range |

|

| Number |

|

| Weighted Average Remaining Contractual Life (in Years) |

|

| Weighted Average Exercise Price |

|

| Number |

| |||||

| $ |

|

|

|

|

|

| |

|

| $ |

|

|

|

| ||||

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

| ||||

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

| ||||

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

| ||||

| $ |

|

|

|

|

|

| |

|

|

|

|

|

|

| ||||

|

| Total |

|

|

|

|

|

| |

|

| $ |

|

|

|

| |||

As of September 30, 2022, the Company had unrecognized stock compensation related to the options of $

During the nine months ended September 30, 2022, the Company granted

Stock repurchase and retirement

On August 7, 2019, the Company publicly announced a share repurchase program under which the Company was authorized to repurchase up to $

|

| Shares Repurchased |

| |||||||||||||

Period |

| Total Number of Shares Repurchased |

|

| Average Price Paid Per Share |

|

| Total Number of Shares Purchased as Part of Publicly Announced Program |

|

| Maximum Dollar Value of Shares that May Yet Be Purchased Under the Program |

| ||||

August 7-31, 2019 |

|

|

|

| $ |

|

|

|

|

| $ |

| ||||

September 1-30, 2019 |

|

|

|

|

|

|

|

|

|

| ||||||

October 1-31, 2019 |

|

|

|

|

|

|

|

|

|

| ||||||

November 1-30, 2019 |

|

|

|

|

|

|

|

|

|

| ||||||

December 1-31, 2019 |

|

|

|

|

|

|

|

|

|

|

| |||||

January 1-31, 2020 |

|

|

|

|

|

|

|

|

|

|

| |||||

February 1-29, 2020 |

|

|

|

|

|

|

|

|

|

|

| |||||

March 1-31, 2020 |

|

|

|

|

|

|

|

|

|

| ||||||

April 1-30, 2020 |

|

|

|

|

|

|

|

|

|

| ||||||

May 1-31, 2020 |

|

|

|

|

|

|

|

|

|

| ||||||

No shares repurchased between June 2020 and February 2021 | ||||||||||||||||

March 1-31, 2021 |

|

|

|

|

|

|

|

|

|

| ||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

|

| $ |

|

|

|

|

| $ |

| ||||

| 12 |

| Table of Contents |

On March 1, 2022, the Company’s board of directors authorized a stock repurchase program under which the Company was authorized to repurchase up to $

|

| Shares Repurchased |

| |||||||||||||

Period |

| Total Number of Shares Repurchased |

|

| Average Price Paid Per Share |

|

| Total Number of Shares Purchased as Part of Publicly Announced Program |

|

| Maximum Dollar Value of Shares that May Yet Be Purchased Under the Program |

| ||||

March 1-31, 2022 |

|

|

|

| $ |

|

|

|

|

| $ |

| ||||

April 1-30, 2022 |

|

|

|

|

|

|

|

|

|

|

|

| ||||

May 1-31, 2022 |

|

|

|

|

|

|

|

|

|

|

|

| ||||

June 1-30, 2022 |

|

|

|

|

|

|

|

|

|

|

|

| ||||

July 1-31, 2022 |

|

|

|

|

|

|

|

|

|

|

|

| ||||

August 1-31, 2022 |

|

|

|

|

|

|

|

|

|

|

|

| ||||

September 1-30, 2022 |

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

|

| $ |

|

|

|

|

| $ |

| ||||

Note 4: Income taxes

The company recognized income tax expense of $

Note 5: Leases

Leasing activity generally consists of office leases. In March 2019, a new lease was signed to move the corporate headquarters to Raleigh, North Carolina. The new lease, which had a lease commencement date of October 2, 2019, expires

Lease liabilities totaled $

| 13 |

| Table of Contents |

For the Three Months Ended For the Nine Months Ended September 30, September 30, September 30, September 30, 2022 2021 2022 2021 Lease expense Operating lease expense Variable lease expense Total lease expense $ $ $ $ $ $ $ $

The weighted-average remaining non-cancelable lease term for our operating leases was

Year Ended December 31: |

|

|

| |

2022 |

| $ |

| |

2023 |

|

|

| |

2024 |

|

|

| |

2025 |

|

|

| |

2026 |

|

|

| |

Thereafter |

|

|

| |

Total lease payments |

|

|

| |

Present value adjustment |

|

| ( | ) |

Lease liability |

| $ |

| |

We have performed an evaluation of our other contracts with customers and suppliers in accordance with Topic 842 and have determined that, except for the leases described above, none of our contracts contain a lease.

Note 6: Revenue

The Company considers itself to be a single reportable segment under the authoritative guidance for segment reporting, specifically a communications and compliance company for publicly traded and private companies. The following tables present revenue disaggregated by revenue stream in (000’s):

|

| Three months ended September 30, |

| |||||||||||||

Revenue Streams |

| 2022 |

|

| 2021 |

| ||||||||||

Communications |

| $ |

|

|

| % |

| $ |

|

|

| % | ||||

Compliance |

|

|

|

|

| % |

|

|

|

|

| % | ||||

Total |

| $ |

|

|

| % |

| $ |

|

|

| % | ||||

|

| Nine months ended September 30, |

| |||||||||||||

Revenue Streams |

| 2022 |

|

| 2021 |

| ||||||||||

Communications |

| $ |

|

|

| % |

| $ |

|

|

| % | ||||

Compliance |

|

|

|

|

| % |

|

|

|

|

| % | ||||

Total |

| $ |

|

|

| % |

| $ |

|

|

| % | ||||

The Company did not have any customers during the three and nine-month periods ended September 30, 2022 or 2021 that accounted for more than 10% of revenue.

Note 7: Line of Credit

Effective October 3, 2021, the Company renewed its unsecured Line of Credit, which changed the interest rate from LIBOR plus

| 14 |

| Table of Contents |

Note 8: Subsequent Event

Acquisition of iNewsWire.com LLC

On November 1, 2022 (the “Closing Date”), the Company entered into a Membership Interest Purchase Agreement (the “Purchase Agreement”) with Lead Capital, LLC, a Delaware limited liability company (the “Seller”), whereby the Company purchased all of the issued and outstanding membership interests of iNewsWire.com LLC, a Delaware limited liability company (“Newswire”). Newswire is a leading media and marketing communications technology company that provides press release distribution, media databases, media monitoring, and newsrooms through its Media Advantage Platform.

Under the terms of the Purchase Agreement and on the Closing Date, the Company paid to the Seller aggregate consideration of approximately $

The Secured Note is due and payable on November 8, 2023 (the “Maturity Date”) and bears an annual interest rate of

| 15 |

| Table of Contents |

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

The discussion of the financial condition and results of operations of the Company set forth below should be read in conjunction with the consolidated financial statements and related notes thereto included elsewhere in this Form10-Q. This Form10-Q contains forward-looking statements that involve risks and uncertainties. The statements contained in this Form10-Q that are not purely historical are forward-looking statements within the meaning of Section 27a of the Securities Act and Section 21e of the Exchange Act. When used in this Form10-Q, or in the documents incorporated by reference into this Form 10-Q, the words “anticipate,” “believe,” “estimate,” “intend” and “expect” and similar expressions are intended to identify such forward-looking statements. Such forward-looking statements include, without limitation, the statements regarding the Company’s strategy, future sales, future expenses, future liquidity and capital resources. All forward-looking statements in this Form10-Q are based upon information available to the Company on the date of this Form10-Q, and the Company assumes no obligation to update any such forward-looking statements. The Company’s actual results could differ materially from those discussed in this Form10-Q for many reasons, including the impact of the COVID-19 pandemic. Factors that could cause or contribute to such differences (“Cautionary Statements”) include, but are not limited to, those discussed in Item 1. Business — “Risk Factors” and elsewhere in the Company’s Annual Report on Form10-K for the year ended December 31, 2021, which are incorporated by reference into this Form 10-Q. All subsequent written and oral forward-looking statements attributable to the Company, or persons acting on the Company’s behalf, are expressly qualified in their entirety by the Cautionary Statements.

Overview

Issuer Direct Corporation and its subsidiaries are hereinafter collectively referred to as “Issuer Direct”, the “Company”, “We” or “Our” unless otherwise noted. Our corporate headquarters are located at One Glenwood Ave., Suite 1001, Raleigh, North Carolina, 27603.

We announce material financial information to our investors using our investor relations website (www.issuerdirect.com), SEC filings, investor events, news and earnings releases, public conference calls, webcasts and social media. We use these channels to communicate with our investors and the public about our company, our products and services and other related matters. It is possible that information we post on some of these channels could be deemed to be material information. Therefore, we encourage investors, the media and others interested in Issuer Direct to review the information we post to all our channels, including our social media accounts.

We are a premier provider of communications and compliance technology solutions that are designed to help organizations tell their stories globally. Our principal platform, Platform id.™, empowers users by thoughtfully integrating the most relevant tools, technologies and products, thus eliminating the complexity associated with producing and distributing their business communications and financial information. Platform id. efficiently and effectively helps our customers manage their events when seeking to distribute their messaging to key constituents, investors, markets and regulatory systems around the globe. Platform id. consists of several related but distinct Communications and Compliance modules that our customers utilize every quarter.

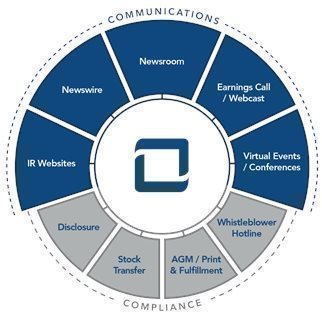

We disclose our revenues in the following two main categories: (i) Communications and (ii) Compliance. Set forth below is an infographic depicting the products included in each of these two main categories we provide today:

| 16 |

| Table of Contents |

Over the next several years, we expect the Communications portion of our business to increase, both in terms of overall revenue and as compared to the Compliance portion of our business. Therefore, we plan to continue to invest in offerings we intend to incorporate into our Communications product lineup. Within most of our target markets, customers require several individual services and/or software providers to meet their investor relations and communications needs. We believe Platform id. can address all these needs in a single, secure, cloud-based platform - one that offers a customer control, increases efficiencies, demonstrates clear value and, most importantly, delivers consistent and compliant messaging from one centralized platform.

We work with a diverse customer base, which includes not only corporate issuers and private companies, but also investment banks, professional firms, such as investor relations and public relations firms, as well as the accounting and legal communities. Our customers and their service providers utilize our platform and related solutions from document creation all the way to dissemination to regulatory bodies, news outlets, financial platforms, and our customers’ shareholders. Private companies primarily use our news distribution, newsroom and webcasting products and services to disseminate their message globally.

We also work with several select stock exchanges by making available certain parts of our platform under agreements to integrate our offerings within their products. We believe such partnerships will continue to yield increased exposure to a targeted customer base that could impact our revenue and overall brand in the market.

Communications

Our Communications platform consists of our ACCESSWIRE branded newswire, our webcasting and events business, professional conference and events software, as well as our investor relations website technology. These products are sold as the leading part of our Platform id. subscription, as well as individually to customers around the globe and are further described below.

ACCESSWIRE

Our press release offering, which is marketed under the brand ACCESSWIRE, is a news dissemination and media outreach service. The ACCESSWIRE product offering focuses on press release distribution for both private and public companies globally. We believe ACCESSWIRE is becoming a competitive alternative in the newswire industry because we have been able to use our technological advancements to allow customers to self-edit releases or use our editorial staff as desired to edit releases. We continue to expand our distribution points, improve our targeting and enhance our analytics reporting. We also offer an e-commerce element to our ACCESSWIRE product, whereby customers can self-select their distribution, register, and then upload their press release for editorial review in minutes. We believe these enhancements have helped lead to an increase in ACCESSWIRE revenues and customers each year compared to the prior year, a trend we expect to continue over the next several years. We have also been able to maintain high gross margins while providing our customers flexible pricing, with options to pay per release or enter longer-term agreements for a designated package of releases.

Like other newswires globally, ACCESSWIRE is dependent upon several key partners for its news distribution. Disruption in any of our partnerships could have a materially adverse impact on ACCESSWIRE and our overall business.

Newsroom

A natural expansion to our ACCESSWIRE and investor relations website business is our corporate Newsroom, which we brought to market during the middle of the third quarter of 2021. This product offering can be an add-on to any customer’s ACCESSWIRE or Platform id. account. The Newsroom suite includes a custom newsroom page builder, a brand asset manager and contact manager.

Our Newsroom suite addresses the needs of our customers looking to build connections with media, journalists, customers and, if applicable the investment community. According to a survey from TekGroup, a majority of journalists and media professionals indicated the importance of newsrooms that include digital media, press kits and video. We believe our Newsroom suite accomplishes this by including the following three components:

Newsroom page - a custom URL, self-publishing system for customers that automatically adds ACCESSWIRE news to their newsroom and allows them the ability to add any other mention, article or post from the internet to their newsroom. Customers can self-manage this platform to customize colors, font, logo, images, social integration, and contact and customer URLs.

Brand Asset Manager - a customizable library of images, video and press kits, which can be shared both privately and publicly, as well as integrated into the ACCESSWIRE editor for easy access of customers’ high- resolution images. All assets are tagged to give our customers analytics for both views and downloads. Subsequent versions of this feature will allow for greater analytics as engagement occurs with our customers’ assets.

| 17 |

| Table of Contents |

Contact Manager - a technology that allows our customers to provide their audiences the ability to quickly subscribe to alerts or notifications of a particular brand. Customers will have the ability to deliver their stories automatically or time based. Engagement and delivery reports will also be available to customers directly from their dashboard.

Webcasting & Events

Our webcasting and events business is comprised of our earnings call webcasting solutions and our virtual meeting and events software (such as annual meetings, deal/non-deal road shows, analyst days and shareholder days). The demand for these products with a virtual component was at an all-time high for us in 2020, largely due to the COVID-19 pandemic. The industry overall has begun to see a reduction in the number of virtual events, specifically annual meetings and deal/non-deal roadshows, as customers are relying on internal enterprise solutions or are returning to pre-pandemic travel and in-person meetings, reducing the need for a virtual component. This has contributed to a decline in demand for our virtual components since the prior year.

Traditional earnings calls and webcasts are a highly competitive market with the majority of the business being driven from practitioners in investor relations and communications firms. We estimate there are approximately 5,000 companies in North America conducting earnings events each quarter that include a teleconference, webcast, or both as part of their events. Platform id. also incorporates other elements of the earnings event, including earnings date/call announcement, earnings press release and SEC Form 8-K filings. There are a handful of our competitors that can offer this integrated full-service solution today, however, we believe our real-time event setup and integrated approach offers a more effective way to manage the process.

Additionally, as a commitment to broadening the reach of our webcast platform, we broadcast live additional companies’ earnings events, whether they are conducted on our platform or not, within our shareholder outreach module, which helps drive new audiences and give companies the ability to view their analytics and engagement of each event. During the first half of 2021, we released the first version of this real-time engagement and analytics dashboard to our customers subscribing to Platform id.

Our VisualWebcaster Platform (“VWP”) is a cloud-based webcast, webinar and virtual meeting platform that delivers live and on-demand streaming of events to audiences of all sizes. VWP allows customers to create, produce and deliver events, which we feel has significantly strengthened our webcasting product and Platform id. offering. The VWP technology gives us the ability to host thousands of webcasts each year, expanding and diversifying our webcast business from our historical earnings-based events to include any type of virtual event. As we expand our platform, it is vital for us to have solutions that service both our core public companies but also a growing segment of private customers.

Professional Conference and Events Software

Our professional conference and events software is a subscription offering we currently license to investor conference organizers, which in the aggregate we believe held an estimated 1,000 plus events a year prior to 2020. This number significantly decreased in 2020 and is expected to remain at decreased levels in the near future and possibly long-term as a result of COVID-19. This software, which is also available as a native mobile app, offers organizers, issuers and investors the ability to register, request and approve one-on-one meetings, manage schedules, perform event promotion and sponsorship, print attendee badges and manage lodging. This cloud-based product can be used in a virtual or in person conference setting and is integrated within Platform id. to enhance our Communications module subscription offerings of newswire, newsrooms, webcasting and shareholder targeting. We believe this integration gives us a unique offering for professional conference organizers that is not available elsewhere in the market. We believe this software helps make Platform id. a platform of choice for investment banks, issuers and investors. However, similar to our virtual events business, the transition of conferences back to in-person events has had an impact on our conference events software subscription business, as in-person events have either been smaller or delayed due to pandemic concerns.

Investor Relations Websites

Our investor relations content network is another component of Platform id., which is used to create the investor relations tab of a company’s website. This investor relations content network is a robust series of data feeds including news feeds, stock feeds, fundamentals, regulatory filings, corporate governance and many other components which are aggregated from most of the major exchanges and news distribution outlets around the world. Customers can subscribe to one or more of these data feeds or as a component of a fully designed and hosted website for pre-IPO companies, SEC reporting companies and partners seeking to display our content on their corporate sites. The clear benefit to our investor relations content network is its integration into Platform id. As such, companies can produce content for public distribution and it is automatically linked to their corporate website, distributed to targeted groups and placed into our data feed partners.

| 18 |

| Table of Contents |

Compliance

Our Compliance offerings consist of our disclosure software for financial reporting, stock transfer services, and related annual meeting, print and shareholder distribution services. Some of these products are sold as part of a Platform id. subscription as well as individually to customers around the globe.

Disclosure Software and Services

Platform id.’s disclosure reporting module is a document conversion, editing and filing offering which is designed for reporting companies and professionals seeking to insource the document drafting, editing and filing processes to the SEC’s EDGAR system. Our disclosure business also offers companies the ability to use our in-house staff to assist in the conversion, tagging and filing of their documents. We generate revenues in disclosure from both software and services and, in most cases, customers have both components within their annual agreements, while others pay for services as they are completed.

Our Inline XBRL (Inline Extensible Business Reporting Language or “iXBRL”) product now includes upgrades that meet mandated SEC disclosure requirements which became effective last year. These requirements began impacting most of our customers on June 15, 2021, however, we had a number of customers previously file using our iXBRL product.

Whistleblower Hotline

Our Whistleblower hotline is an add-on product within Platform id. This system delivers secure notifications and basic incident workflow management processes that align with a company’s corporate governance whistleblower policy. As a supported and subsidized bundle product of the New York Stock Exchange (“NYSE”) offerings, we are introduced to new IPO customers and other larger cap customers listed on the NYSE. Since 2014, we have been a named NYSE subsidy provider of this Whistleblower solution. In 2020, NYSE renewed and extended the initial subsidy term to four years from two years, whereby the first two years are provided under subsidy and the added two years are at our standard subscription rates.

Stock Transfer Module

A valued subscription add-on in our Platform id. offering is the ability for our customers to gain access to real-time information about their shareholders, stock ledgers and reports and to issue new shares from our cloud-based stock transfer module. Managing the capitalization table of a public company or pre-IPO company is a cornerstone of corporate governance and transparency, and as such companies and community banks have chosen us to assist with their stock transfer needs, including bond offerings and dividend management. This is an industry which has experienced declining overall revenues as it was affected by the replacement of paper certificates with digital certificates. However, we have been focused on selling subscriptions of the stock transfer component of our platform, allowing customers to gain access to our cloud-based system in order to move shares or query shareholders, which we believe has resulted in a more efficient process for both our customers and us.

Annual Meeting / Proxy Voting Platform

Our proxy module is marketed as a fully integrated, real-time voting platform for our customers and their shareholders of record. This module is utilized for every annual meeting or special meeting we manage for our customers and offers both full-set mailing and notice of internet availability options.

This module has been incorporated within our webcasting offering to enable our customers the ability to conduct their annual meetings in-person or fully virtual, which has often been required since the COVID-19 pandemic. Our solution incorporates shareholder and guest registration, voting integration, real-time statistics on attendance, audio video and presentation features as well as fully managed meeting managers and inspector of elections. Although we believe a virtual component to an annual meeting is both a benefit to all shareholders and a corporate governance advantage, there can be no assurances this product has longevity in the market.

Shareholder Distribution

Over the past few years, we have worked on refining the model of digital distribution of our customers’ message to the investment community and beyond. This was accomplished by integrating our shareholder outreach module, Investor Network, into and with Platform id. Most of the customers subscribing to this module today are historical PrecisionIR - Annual Report Service (“ARS”) users, as well as new customers purchasing the entire Platform id. subscription. We migrated some of the customers from the traditional ARS business into this new digital subscription business, however, we continue to operate a portion of this legacy physical hard copy delivery of annual reports and prospectuses for customers who opt to take advantage of it. We continue to see customer attrition for customers who subscribe to both the electronic and physical distribution of reports as a stand-alone product.

| 19 |

| Table of Contents |

Results of Operations

Comparison of results of operations for the three and nine months ended September 30, 2022 and 2021:

|

| Three months ended |

|

| Nine months ended |

| ||||||||||

|

| September 30, |

|

| September 30, |

| ||||||||||

Revenue Streams |

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||

Communications |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Revenue |

| $ | 3,487 |

|

| $ | 3,686 |

|

| $ | 10,561 |

|

| $ | 10,383 |

|

Gross margin |

| $ | 2,680 |

|

| $ | 2,882 |

|

| $ | 8,246 |

|

| $ | 7,839 |

|

Gross margin % |

|

| 77 | % |

|

| 78 | % |

|

| 78 | % |

|

| 75 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Compliance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue |

| $ | 1,793 |

|

| $ | 1,779 |

|

| $ | 5,814 |

|

| $ | 5,782 |

|

Gross margin |

| $ | 1,388 |

|

| $ | 1,228 |

|

| $ | 4,321 |

|

| $ | 4,097 |

|

Gross margin % |

|

| 77 | % |

|

| 69 | % |

|

| 74 | % |

|

| 71 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue |

| $ | 5,280 |

|

| $ | 5,465 |

|

| $ | 16,375 |

|

| $ | 16,165 |

|

Gross margin |

| $ | 4,068 |

|

| $ | 4,110 |

|

| $ | 12,567 |

|

| $ | 11,936 |

|

Gross margin % |

|

| 77 | % |

|

| 75 | % |

|

| 77 | % |

|

| 74 | % |

Revenues

Total revenue decreased by $185,000, or 3%, to $5,280,000 during the three-month period ended September 30, 2022, as compared to $5,465,000 during the same period of 2021. Total revenue increased by $210,000, or 1%, to $16,375,000 during the nine-month period ended September 30, 2022, compared to $16,165,000 during the same period of 2021.

Communications revenue decreased $199,000, or 5%, and increased $178,000, or 2%, during the three and nine-month periods ended September 30, 2022, respectively, as compared to the same periods of 2021. The decrease in revenue for the three-month period ended September 30, 2022, is attributed to a decrease in revenue from our webcasting and events revenue stream, partially due to less demand for our virtual products as conferences and meetings began to move back to in-person events, as well as timing of some events being pushed into the fourth quarter of 2022. This decrease was partially offset by an increase in revenue from our ACCESSWIRE news brand. ACCESSWIRE revenue for the three-month period ended September 30, 2022, increased approximately 6%, compared to the same period of the prior year. We also generated increased revenue from our investor relations websites and news feed product lines. The increase in revenue for the nine months ended September 30, 2022 is due to a 13% increase in revenue from ACCESSWIRE as well as increased revenue from investor relations websites and news feed product lines. These increases were partially offset by a decrease in revenue from our events and webcasting business due to the aforementioned reasons. Communications revenue was 66% and 65% of total revenue during the three and nine months ended September 30, 2022, respectively, as compared to 67% and 64% during the same periods of the prior year.

Compliance revenue increased $14,000, or 1% and $32,000 or also 1% during the three and nine-month periods ended September 30, 2022, respectively, as compared to the same periods of 2021. The increase in revenue is due primarily to an increase in revenue from print and proxy fulfillment services due to larger transactions during the periods. Revenue from our transfer agent services also increased for the three month-period ended September 30, 2022 due to an increase in subscription fees, however, continues to remain lower on a year-to-date basis. The increase in revenue from proxy fulfillment services was also partially offset by declines in disclosure services and software revenue and our legacy ARS services due to customer attrition.

No customers accounted for more than 10% of the revenues during the three and nine-month periods ended September 30, 2022, or 2021.

Deferred Revenue

At September 30, 2022, our deferred revenue balance was $3,429,000, which we expect to recognize over the next twelve months, compared to $3,086,000 at December 31, 2021, an increase of 11%. Deferred revenue primarily consists of advance billings for subscriptions of our cloud-based products and pre-paid packages of our news distribution product, as well as advance billings for annual service contracts.

| 20 |

| Table of Contents |

Cost of Revenues

Communications cost of revenues consists primarily of direct labor costs, newswire distribution costs, teleconferencing costs and third-party licensing costs. Compliance cost of revenue consists primarily of direct labor costs, warehousing, logistics, print production materials, postage, and amortization of capitalized software costs related to our disclosure software. Overall cost of revenues decreased by $143,000, or 11%, and $421,000, or 10%, during the three and nine-month periods ended September 30, 2022, respectively, as compared to the same periods of 2021. Overall gross margin decreased $42,000, or 1%, and increased $631,000, or 5%, during the three and nine-month periods ended September 30, 2022, respectively, as compared to the same periods of the prior year. Overall gross margin percentages increased to 77% during both the three and nine months ended September 30, 2022, respectively, compared to 75% and 74% during the same periods of 2021.