UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2016

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____________ to _____________

Commission File No.001-35561

WECAST NETWORK, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 20-1778374 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

Building B4, Tai Ming International Business Court,

Tai Hu Town, Tongzhou District, Beijing, China 101116

(Address of principal executive offices)

(212) 206-1216

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered |

| Common Stock, par value $0.001 per share | Nasdaq Capital Market |

Securities registered pursuant to Section 12(g) of the Exchange Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act

| Large Accelerated Filer ¨ | Accelerated Filer ¨ |

| Non-Accelerated Filer ¨ | Smaller reporting company x |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes ¨ No x

As of June 30, 2016 (the last business day of the registrant’s most recently completed second fiscal quarter), the market value of the shares of the registrant’s common stock held by non-affiliates (based upon the closing price of shares as reported by Nasdaq) was approximately $29,555,315 Shares of the registrant’s common stock held by each executive officer and director and each by each person who owns 10% or more of the outstanding common stock have excluded from the calculation in that such persons may be deemed to be affiliates of the registrant. This determination affiliate status is not necessarily a conclusive determination for other purposes.

There were a total of 59,891,201 shares of the registrant’s common stock outstanding as of March 28, 2017.

DOCUMENTS INCORPORATED BY REFERENCE

None.

Annual Report on FORM 10-K

For the Fiscal Year Ended December 31, 2016

TABLE OF CONTENTS

| 2 |

Special Note Regarding Forward Looking Statements

In addition to historical information, this report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We use words such as “believe,” “expect,” “anticipate,” “project,” “target,” “plan,” “optimistic,” “intend,” “aim,” “will” or similar expressions which are intended to identify forward-looking statements. Such statements include, among others, those concerning market and industry segment growth and demand and acceptance of our new and existing products or services; any projections of sales, earnings, revenue, margins or other financial items; any statements regarding the plans, strategies and objectives of management for future operations; any statements regarding future economic conditions or performance; uncertainties related to conducting business in China; and all assumptions, expectations, predictions, intentions or beliefs about future events. You are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, including, and without limitation, those identified in Item 1A, “Risk Factors” included herein, as well as assumptions, which, if they were to ever materialize or prove incorrect, could cause the results of the Company to differ materially from those expressed or implied by such forward-looking statements.

Although we believe the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, level of activity, performance, or achievements. Moreover, neither we nor any other person assumes responsibility for the accuracy or completeness of any of these forward-looking statements. You should not rely upon forward-looking statements as predictions of future events. The forward-looking statements included herein are made as of the date of this report. We undertake no obligation to update any of these forward-looking statements, whether written or oral, that may be made, from time to time, after the date of this report to conform our prior statements to actual results or revised expectations.

Use of Terms

Except as otherwise indicated by the context, references in this report to “we,” “us,” “our,” “our Company,” “the Company,” or “Wecast Network,” are to the business of Wecast Network, Inc. (formerly known as YOU On Demand Holdings, Inc.), a Nevada corporation, and its consolidated subsidiaries and variable interest entities.

In addition, unless the context otherwise requires and for the purposes of this report only:

| . | “CB Cayman” refers to our wholly-owned subsidiary China Broadband, Ltd., a Cayman Islands company; |

| . | “Exchange Act” refers to the Securities Exchange Act of 1934, as amended; |

| . | “Hong Kong” refers to the Hong Kong Special Administrative Region of the People’s Republic of China; |

| . | “Hua Cheng” refers to Hua Cheng Hu Dong (Beijing) Film and Television Communication Co., Ltd., a PRC company 39% owned by Sinotop Beijing and 20% owner of Zhong Hai Media; |

| . | “PRC,” “China,” and “Chinese,” refer to the People’s Republic of China; |

| . | “Renminbi” and “RMB” refer to the legal currency of China; |

| . | “SAPPRFT” refers to the State Administration of Press, Publication, Radio, Film & Television, an executive branch under the State Council of the People’s Republic of China; |

| . | “SEC” refers to the United States Securities and Exchange Commission; |

| . | “Securities Act” refers to the Securities Act of 1933, as amended; |

| . | “Shandong Broadcast” refers to Shandong Broadcast & TV Weekly Press, a PRC company; |

| . | “Shandong Media” refers to our previously owned 50% joint venture, Shandong Lushi Media Co., Ltd., a PRC company; effective July 1, 2012, Shandong Media became a 30% owned company by Sinotop Beijing; |

| . | “Shandong Newspaper Entities” refers to Shandong Broadcast and Modern Movie; |

| . | “Sinotop Beijing” refers to Beijing Sino Top Scope Technology Co., Ltd., a PRC company controlled by YOD Hong Kong through contractual arrangements; |

| . | “U.S. dollars,” “dollars,” “USD,” “US$,” and “$” refer to the legal currency of the United States; |

| . | “VIEs” refers to our current variable interest entities Sinotop Beijing, and SSF; |

| . | “VOD” refers to video on demand, which includes near video on demand (“NVOD”), subscription video on demand (“SVOD”), and transactional video on demand (“TVOD”); |

| . | “WFOE” refers to our wholly-owned subsidiary Beijing China Broadband Network Technology Co., Ltd., a PRC company which was sold during the quarter ended March 31, 2014; |

| “YOD Hong Kong” refers to YOU On Demand (Asia) Limited, formerly Sinotop Group Limited, a Hong Kong company wholly- owned by CB Cayman; |

| . | “SSF” refers to Tianjin Sevenstarflix Network Technology Limited, a PRC company controlled by YOD Hong Kong through contractual arrangements; |

| . | “YOD WFOE” refers to YOU On Demand (Beijing) Technology Co., Ltd., a PRC company wholly-owned by YOD Hong Kong; and |

| . | “Zhong Hai Media” refers to Zhong Hai Shi Xun Media Co., Ltd., a PRC company 80% owned by Sinotop Beijing. |

In this report we are relying on and we refer to information and statistics regarding the media industry in China that we have obtained from various public sources. Any such information is publicly available for free and has not been specifically prepared for us for use or incorporation in this report or otherwise.

| 3 |

| ITEM 1. | BUSINESS. |

Overview

Wecast Network is a premium content Video On Demand (“VOD”) service provider with primary operations in the People’s Republic of China. Wecast Network, Inc. was incorporated in the State of Nevada on October 19, 2004.

Wecast Network, through its subsidiaries and variable interest entities, provides premium content and integrated value-added service solutions for the delivery of VOD and paid video programming to digital cable providers, Internet Protocol Television (“IPTV”) providers, Over-the-Top (“OTT”) streaming providers, mobile manufacturers and operators, as well as direct customers. By leveraging and optimizing its existing operations, we have positioned ourselves to evolve into a mobile-driven, “new media” platform for both enterprises and consumers.

We launched our VOD service through acquisition of YOD Hong Kong, formerly Sinotop Group Limited, in July 30, 2010. Through a series of contractual arrangements, YOD WFOE, the subsidiary of YOD Hong Kong, controls Sinotop Beijing, a corporation established in the PRC. Sinotop Beijing is the 80% owner of Zhong Hai Media, the entity though which we provide: 1) integrated value-added business-to-business (“B2B”) service solutions for the delivery of VOD and enhanced premium content for digital cable; 2) integrated value-added business-to-business-to-customer (“B2B2C”) service solutions for the delivery of VOD and enhanced premium content for IPTV and OTT providers and; 3) direct to user, or B2C, mobile video service apps. As a result of the contractual arrangements with Sinotop Beijing, we have the right to control management decisions and direct the economic activities that most significantly impact Sinotop Beijing and Zhong Hai Media, and, accordingly, under generally accepted accounting principles in the United States (“U.S. GAAP”), we consolidate these operating entities in our consolidated financial statements.

Wecast Network is a next generation global brand licensing, IP sales and video commerce company driven by Artificial Intelligence (“AI”) and Big Data. With a firm focus on 4 strategy pillars which include: Brand, Content, Commerce and Licensing, the Company is leveraging and optimizing its legacy operations as a premium content VOD service provider in China to evolve into a global, vertical, and transactional B2B2C, mobile-driven, consumer and supply chain management platform. By aiming to establish the world’s premier multimedia, social networking and smart e-commerce-enabled network with the largest global effective connected user base, Wecast, through this expanded, cloud-based, ecosystem of connected screens combined with strong partnerships with leading global providers, will be capable of delivering a vast array of Wecast Network-branded products and services to enterprise customers and end-use consumers–anytime and anywhere, across multiple platforms and devices.

Our OTT, Mobile App, IPTV and Digital Cable VOD Businesses

Wecast Network is a leading multi-platform entertainment company delivering premium content, including leading Hollywood and China-produced movie titles as well as children’s programming, to customers’ mobile and TV screens across China via Subscription Video On Demand (“SVOD”) and Transactional Video On Demand (“TVOD”) paid content services. The Company’s current distribution partners include digital cable operators, IPTV operators, OTT streaming operators and mobile smartphone manufacturers and operators. Our subscribers can watch our content anytime, anywhere and have full DVD-like control as they can play, pause and resume watching, all without commercial and advertising interruptions. Our core revenues are being generated from both minimum guarantee payments and revenue sharing arrangements with our distribution partners as well as subscription or transactional fees from our subscribers.

We have distribution agreements with several OTT, IPTV and mobile distributors, manufacturers and operators. In 2016 and 2015, the YOU Cinema movie subscription service made its commercial debut on the Xiaomi OTT set-top box as part of Wecast Network’s previously announced distribution deal with China Network Television’s (“CNTV”) subsidiary, Future TV Co. Ltd. (the official online division of Chinese national public broadcaster China Central Television “CCTV”). Other distribution partners of ours include: Huawei, a leading global information and communications technology solutions provider and one of the largest global smartphone manufacturers; Dr. Peng Telecom and Media Group, Ltd and its OTT box, the Domy Box; Southern Media Corporation’s 3GTV mobile video platform which currently serves 6 million subscribers through China Mobile, China Unicom and China Telecom in Guangdong, a province which has the largest mobile service and movie box office in China.

Specifically, for digital cable, through the acquisition of YOD Hong Kong and its VIE, Sinotop Beijing, Wecast Network has an exclusive 20-year joint venture (approximately 15 years remaining) with CCTV-6’s China Home Cinema (“CHC”), making us the first national VOD platform in China. We operate under a national government license obtained by CHC to serve as their exclusive agent in the PRC for operating and marketing TVOD, SVOD, Near Video On Demand (“NVOD”) and related Value-Added Services (“VAS”).

In October 2016, we announced a partnership with Zhejiang Yanhua Culture Media Co., Ltd. (“Yanhua”), where Yanhua will act as the exclusive distribution operator (within the territory of the People’s Republic of China) of Wecast Network’s licensed library of major studio films. We still operate our Hollywood movie mobile/smartphone app independent of this partnership.

Yanhua will assume all sales and marketing costs and will pay us a minimum guarantee in exchange for a percentage of the total revenue share.

Wecast Network has and continues to license increasing amounts of entertainment and educational content that enables our subscribers to enjoy premium and diverse entertainment directly on their mobile and TV screens. We have content agreements with Disney Media Distribution, Paramount Pictures, Twentieth Century Fox Television Distribution, NBC Universal, Miramax Films, Lionsgate, Screen Media Ventures, among other independent studios.

| 4 |

Recent Developments

On January 30, 2017, based on the terms of a non-binding term sheet entered into on September 19, 2016, we entered into a Securities Purchase Agreement (the “Sun Video SPA”) with BT Capital Global Limited, a Hong Kong company (“BT”) and affiliate of the Company’s chairman Bruno Wu, for the purchase by us of all of the outstanding capital stock of Sun Video Group Hong Kong Limited, a Hong Kong corporation (“SVG”) for an aggregate purchase price of $800,000 and a $50 million Promissory Note (the “SVG Note”) with the principal and interest thereon convertible into shares of the Company’s common stock at a conversion rate of $1.50 per share. BT has guaranteed that SVG will achieve certain financial goals within 12 months of the closing. Until receipt of necessary Company’s shareholder approvals, the Note is not convertible into the Wecast Common Shares. Under the terms of the Sun Video SPA, BT has guaranteed that the business of the SVG and its subsidiaries (the “Sun Video Business”) shall achieve revenue of $250 million, and $15 million of gross profit (collectively the “Performance Guarantees”) within 12 months of the closing. If the Sun Video Business fails to meet either of the Performance Guarantees within such time, BT shall forfeit back to us the shares of our common stock, on a pro rata basis based on the Performance Guarantee for which the Sun Video Business achieves the lowest percentage of the respective amount guaranteed.

In addition, if the Sun Video Business achieves more than $50 million in cumulative net income within 3 years of closing, (the “Net Income Threshold”), we shall pay BT 50% of the amount of any cumulative net income above the Net Income Threshold. Profit share payments shall be made on an annual basis, in either cash or stock at the discretion of our Board of Directors. If the Board decides to make the payment in stock, the number of our shares of common stock to be awarded shall be calculated based on the market price of such shares.

The transaction was recommended by our Audit Committee and approved by our Board of Directors. Duff & Phelps, LLC served as an independent financial advisor to the Audit Committee and rendered a fairness opinion in connection with the transaction, which concluded that the transaction was fair from a financial point of view to the Company.

On January 31, 2017, we entered into a Securities Purchase Agreement (the “Wide Angle SPA”) with BT and Sun Seven Stars Media Group Limited, a Hong Kong company (“SSS”), one of the Company’s largest shareholders, controlled by our chairman Bruno Wu, as guarantor, for the purchase by us of 55% of the outstanding capital stock of Wide Angle Group Limited, a Hong Kong company (“Wide Angle”) for the sole consideration of the Company adding Wide Angle to the Sun Video Business acquired by the Company under the Sun Video SPA and thereby including the revenue and gross profit from Wide Angle in the calculation of the SVG Performance Guarantees set forth in the Sun Video SPA.

On March 14, 2017, the Company through its PRC subsidiary Shanghai Blue World Investment Management Consulting Limited (“SVG WFOE”), entered into a Capital Increase Agreement (the “Capital Increase Agreement”) with Guizhou Sun Seven Stars Technology Company Limited, a PRC company (“GZSSS”), which is an affiliate of Wecast Media Group Limited (formerly known as Sun Seven Stars Hong Kong Cultural Development Limited), a Hong Kong company controlled by Bruno Wu. Pursuant to the terms of the Capital Increase Agreement, GZSSS will invest RMB 80 million (approximately $11.6 million) to own 94.12% of Guizhou Sun Seven Stars Technology Trading Platform Limited (“GZ”), a PRC company formed in February 2017 100% owned by SVG WFOE and prior to this transaction. The Company and GZSSS will share the dividends and other profits of GZ at a ratio of 70% and 30%, respectively. In addition, the Company will have the right to appoint two of GZ’s three board members, and GZSSS will have the right to appoint one board member.

Additionally, the Company changed its corporate name from YOU On Demand Holdings, Inc. to Wecast Network, Inc. effective as of November 11, 2016.

The purpose of changing the corporate name to Wecast Network, was to find a designation that could better encompass and further establish the Company’s unique identity in the industry and to more accurately represent the planned full portfolio of solutions and services that are in development and aimed at both a Chinese and global audience. This name change marks a new and expanded focus, and it underscores the Company’s firm commitment to offering innovative products and solutions that go well beyond the current offering. We are investing heavily in the future of our Company, as the Company’s industry requires an innovative approach and a fundamentally different way of operating. The Company’s transformation strategy is focused on understanding and capturing data on the Company’s consumer’s desires and habits and leveraging business partner’s technology and marketing to better monetize our Company’s world-class content in order to deliver personalized experiences to our Company’s contracted and addressable users and drive value for all of the stakeholders. The rebranding to Wecast Network represents the ecosystem our Company is trying to build, coupled with our Company’s intention to leverage the infrastructure and reach of some of our Company’s partners in order to execute on the Company’s strategy.

| 5 |

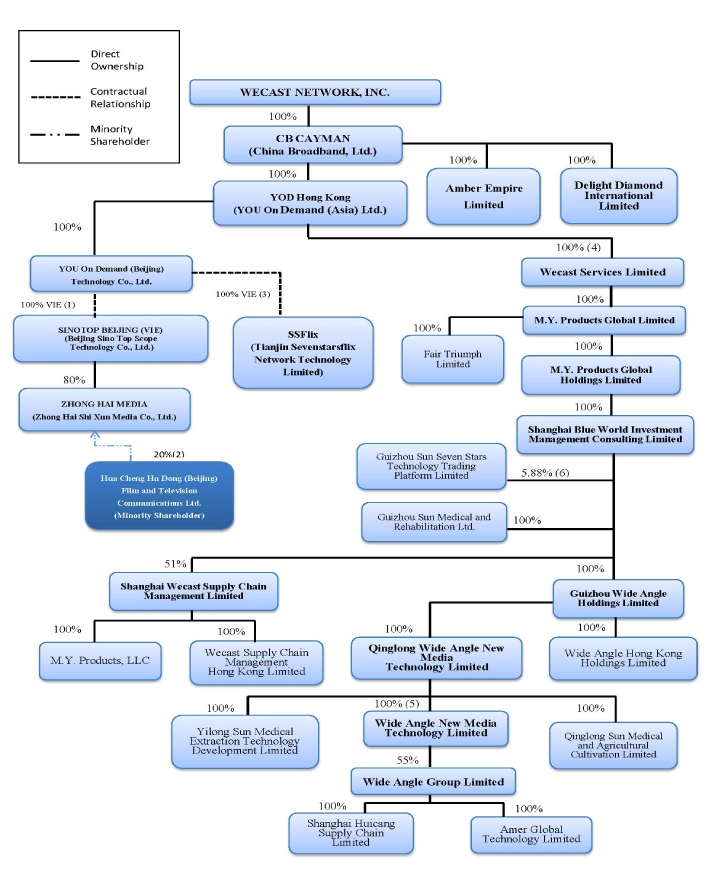

Corporate Structure

The following chart depicts our corporate structure as of March 31, 2017:

| (1). | Sinotop Beijing VIE Agreements, including with Mei Chen and Yun Zhu, the nominee shareholders of Sinotop Beijing Mei Chen, holder of 95% equity ownership in Sinotop Beijing and a party to certain VIE arrangements between YOD WFOE and Sinotop Beijing, is our former Chief Finance Officer. Yun Zhu, holder of 5% equity ownership in Sinotop Beijing and a party to certain VIE arrangements between YOD WFOE and Sinotop Beijing, is the Vice President of SSS, a significant shareholder of the Company. |

| (i) | Management Services Agreement between Sinotop Beijing and YOD Hong Kong, dated as of March 9, 2010. |

| (ii) | Call Option Agreement among YOD WFOE, Sinotop Beijing, Mei Chen and Yun Zhu, dated as of January 25, 2016; and Call Option Agreement among YOD WFOE, Sinotop Beijing and Mei Chen was dated as of November 4, 2016. |

| (iii) | Equity Pledge Agreement among YOD WFOE, Sinotop Beijing, Mei Chen and Yun Zhu, dated as of January 25, 2016, Mei Chen’s Equity Pledge Agreement was dated as of November 21, 2016. |

| (iv) | Power of Attorney agreements among YOD WFOE, Sinotop Beijing and Mei Chen was dated on November 4, 2016 and Power of Attorney agreements among YOD WFOE, Sinotop Beijing and Yun Zhu, dated as of January 25, 2016. |

| (iv) | Technical Services Agreement among YOD WFOE and Sinotop Beijing, dated as of January 25, 2016. |

| 6 |

| (2). | Cooperation Agreement, by and among, Sinotop Beijing, Hua Cheng Hu Dong (Beijing) Film and Television Communication Co., Ltd. (“Hua Cheng”) and Zhong Hai Shi Xun Media Co., Ltd. (“Zhong Hai Media”), dated September 30, 2010. The controlling party of Hua Cheng is Hua Cheng Film and Television Digital Programs Co. Ltd. (“Hua Cheng Digital”). Hua Cheng Digital is not related to us or our principles. |

| (3). | SSF VIE Agreements, including with Lan Yang and Yun Zhu, the nominee shareholders of SSF. Lan Yang, holder of 99% equity ownership in SSF and a party to certain of the SSF VIE Agreements, is the spouse of Bruno Zheng Wu, the Company’s Chairman. Yun Zhu, holder of 1% equity ownership in SSF and a party to certain of the SSF VIE Agreements, is the Vice President of SSS. |

| (i) | Management Services Agreement between SSF and YOD Hong Kong, dated as of April 6, 2016. |

| (ii) | Call Option Agreement among YOD WFOE, SSF and the Nominee Shareholders, dated April 5, 2016. |

| (iii) | Equity Pledge Agreement among YOD WFOE, Lan Yang and Yun Zhu (the “Nominee Shareholders”), dated April 5, 2016; Amended and Restated Equity Pledge Agreement among YOD WFOE and the Nominee Shareholders , dated May 23, 2016. |

| (iv) | Power of Attorney agreements among YOD WFOE, SSF and each of the respective Nominee Shareholders, dated April 5, 2016. |

| (v) | Technical Service Agreement between YOD WFOE and SSF, dated April 5, 2016. |

| (vi) | Spousal Consent, undersigned by the respective spouse of the Nominee Shareholders (collectively, the “Spouses”), dated April 5, 2016. |

| (vii) | Letter of Indemnification among YOD WFOE and Lan Yang and YOD WFOE and Yun Zhu, both dated as of April 5, 2016. |

| (viii) | Loan Agreement among YOD WFOE and the Nominee Shareholders, dated April 5, 2016; Supplemental Loan agreement among YOD WFOE and the Nominee Shareholders, dated May 31, 2016. |

| (4). |

On January 30, 2017, the Company entered into a Securities Purchase Agreement (the “SVG Purchase Agreement”) with BT Capital Global Limited, a Hong Kong company (“BT”) and affiliate of the Company’s chairman Bruno Wu, pursuant to which the Company agreed to purchase and BT agreed to sell all of the outstanding capital of SVG for an aggregate purchase price of (i) $800,000; and (ii) a Promissory Note with the principal and interest thereon convertible into shares of the Company’s Common Stock, par value $0.001 per share at a conversion rate of $1.50 per share of Company Common Stock. BT has guaranteed that SVG will achieve certain financial goals within 12 months of the closing. See “Business – Recent Developments” for more details. |

| (5). | On January 31, 2017, the Company entered into a Securities Purchase Agreement (the “WAG Purchase Agreement”) with BT and SSS, as guarantor, pursuant to which the Company agreed to purchase and BT agreed to sell 55% of the outstanding capital stock (the “Wide Angle Common Shares”) of Wide Angle Group Limited, a Hong Kong company (“Wide Angle”) for the sole consideration of the Company adding Wide Angle to the Sun Video Business acquired by the Company under SVG Purchase Agreement entered into with BT on January 30, 2017 and thereby including the revenue and gross profit from Wide Angle in the calculation of the SVG Performance Guarantees set forth in the SVG Purchase Agreement as described in Note 20(a) to the consolidated financial statements included in this report. |

| (6). | Shanghai Blue Investment Management limited Consulting Limited (“Shanghai Blue”) holds 5.88% common shares of Guizhou Sun Seven Stars Technology Trading Platform Limited (“Guizhou Trading Platform”) and will be entitled with 70% of profit and loss realized by Guizhou Trading Platform. The Board of Directors shall consist of three members, Shanghai Blue has the right to appoint two members of the board. |

VIE Structure and Arrangements

To comply with PRC laws and regulations that prohibit or restrict foreign ownership of companies that provide value-added telecommunication services, we provide services through Sinotop Beijing, Sinotop Beijing’s subsidiary Zhong Hai Media, and SSF, which hold the licenses and approvals to provide digital distribution and Internet content services in the PRC. We have the ability to control Sinotop Beijing and SSF through a series of contractual agreements, as described below, entered into among YOD WFOE, YOD Hong Kong, Sinotop Beijing, SSF and the respective legal shareholders of Sinotop Beijing and SSF.

Through these contractual arrangements, we have acquired both control over and rights to, 100% of the economic benefit of Sinotop Beijing and SSF. Accordingly, Sinotop Beijing and SSF are each considered a variable interest entity, or VIE, and are therefore consolidated in our financial statements. Pursuant to the below contractual agreements, YOD WFOE can have the assets transferred freely out of each VIE without any restrictions. Therefore, YOD WFOE considers that there is no asset of the respective VIE that can be used only to settle obligation of such VIE, except for the registered capital of each respective VIE, amounting to RMB 21.8 million (or approximately $3.1 million) for Sinotop Beijing (and Zhong Hai Media) as of December 31, 2016, and RMB 50.0 million (approximately $7.5 million) for SSF, among which RMB 27.6 million (approximately $4.2 million) has been injected as of December 31, 2016. As Sinotop Beijing, Zhong Hai Media and SSF are incorporated as limited liability companies under PRC Company Law, creditors of these three entities do not have recourse to the general credit of other entities of the Company.

The following is a summary of the common contractual arrangements that provide us with effective control our VIEs and that enable us to receive substantially all of the economic benefits from their operations:

Equity Pledge Agreement

Pursuant to the Equity Pledge Agreement among YOD WFOE and the respective nominee shareholders, the nominee shareholders pledge all of their capital contribution rights in the VIEs to YOD WFOE as security for the performance of the obligations of the VIEs to make all the required technical service fee payments pursuant to the Technical Services Agreement and for performance of the nominee shareholders’ obligation under the Call Option Agreement. The terms of the Equity Pledge Agreement expire upon satisfaction of all obligations under the Technical Services Agreement and Call Option Agreement.

Call Option Agreement

Pursuant to the Call Option Agreement among YOD WFOE, the VIEs and the respective nominee shareholders, the nominee shareholders grant an exclusive option to YOD WFOE, or its designee, to purchase, at any time and from time to time, to the extent permitted under PRC law, all or any portion of the nominee shareholders’ equity in the VIEs. The exercise price of the option shall be determined by YOD WFOE at its sole discretion, subject to any restrictions imposed by PRC law. The term of the agreement is until all of the equity interest in the VIEs held by the nominee shareholders is transferred to YOD WFOE, or its designee and may not be terminated by any party to the agreement without consent of the other parties.

Power of Attorney

Pursuant to the Power of Attorney agreements among YOD WFOE, each VIE and each of the respective nominee shareholders, each nominee shareholder grants YOD WFOE the irrevocable right, for the maximum period permitted by law, to all of its voting rights as shareholder of the VIE. The nominee shareholders may not transfer any of their equity interest in the VIE to any party other than YOD WFOE. The Power of Attorney agreements may not be terminated except until all of the equity in the VIE has been transferred to YOD WFOE or its designee.

| 7 |

Technical Service Agreement

Pursuant to the Technical Service Agreement, between YOD WFOE and each VIE, YOD WFOE has the exclusive right to provide technical service, marketing and management consulting service, financial support service and human resource support services to VIE, and VIE is required to take all commercially reasonable efforts to permit and facilitate the provision of the services by YOD WFOE. As compensation for providing the services, YOD WFOE is entitled to receive service fees from VIE equivalent to YOD WFOE’s cost plus 20-30% of such costs as calculated on accounting policies generally accepted in the PRC. YOD WFOE and VIE agree to periodically review the service fee and make adjustments as deemed appropriate. The term of the Technical Services Agreement is perpetual, and may only be terminated upon written consent of both parties.

Spousal Consent

Pursuant to the Spousal Consent, undersigned by the respective spouse of the nominee shareholders, the spouses unconditionally and irrevocably agree to the execution of the Equity Pledge Agreement, Call Option Agreement and Power of Attorney agreement. The spouses agree to not make any assertions in connection with the equity interest of VIE and to waive consent on further amendment or termination of the Equity Pledge Agreement, Call Option Agreement and Power of Attorney agreement. The spouses further pledge to execute all necessary documents and take all necessary actions to ensure appropriate performance under these agreements upon YOD WFOE’s request. In the event the spouses obtain any equity interests of VIE which are held by the nominee shareholders, the spouses agreed to be bound by the VIE agreements, including the Technical Services Agreement, and comply with the obligations thereunder, including sign a series of written documents in substantially the same format and content as the VIE agreements.

Letter of Indemnification

Pursuant to the Letter of Indemnification among YOD WFOE and each nominee shareholder, YOD WFOE agrees to indemnify such nominee shareholder against any personal, tax or other liabilities incurred in connection with their role in equity transfer to the greatest extent permitted under PRC law. YOD WFOE further waives and releases the nominee shareholders from any claims arising from, or related to, their role as the legal shareholder of the VIE, provided that their actions as a nominee shareholder are taken in good faith and are not opposed to YOD WFOE’s best interests. The nominee shareholders will not be entitled to dividends or other benefits generated therefrom, or receive any compensation in connection with this arrangement. The Letter of Indemnification will remain valid until either the nominee shareholder or YOD WFOE terminates the agreement by giving the other party hereto sixty (60) days’ prior written notice.

Management Services Agreement

In addition to VIE agreements described above, the Company’s subsidiary and the parent company of YOD WFOE, YOU On Demand (Asia) Limited, a company incorporated under the laws of Hong Kong (“YOD Hong Kong”) has entered into a Management Services Agreement with each VIE.

Pursuant to such Management Services Agreement, YOD Hong Kong has the exclusive right to provide to the VIE management, financial and other services related to the operation of the VIE’s business, and the VIE is required to take all commercially reasonable efforts to permit and facilitate the provision of the services by YOD Hong Kong. As compensation for providing the services, YOD Hong Kong is entitled to receive a fee from the VIE, upon demand, equal to 100% of the annual net profits as calculated on accounting policies generally accepted in the PRC of the VIE during the term of the Management Services Agreement. YOD Hong Kong may also request ad hoc quarterly payments of the aggregate fee, which payments will be credited against the VIE’s future payment obligations.

In addition, at the sole discretion of YOD Hong Kong, the VIE is obligated to transfer to YOD Hong Kong, or its designee, any part or all of the business, personnel, assets and operations of the VIE which may be lawfully conducted, employed, owned or operated by YOD Hong Kong, including:

(a) business opportunities presented to, or available to the VIE may be pursued and contracted for in the name of YOD Hong Kong rather than the VIE, and at its discretion, YOD Hong Kong may employ the resources of the VIE to secure such opportunities;

| 8 |

(b) any tangible or intangible property of the VIE, any contractual rights, any personnel, and any other items or things of value held by the VIE may be transferred to YOD Hong Kong at book value;

(c) real property, personal or intangible property, personnel, services, equipment, supplies and any other items useful for the conduct of the business may be obtained by YOD Hong Kong by acquisition, lease, license or otherwise, and made available to the VIE on terms to be determined by agreement between YOD Hong Kong and the VIE;

(d) contracts entered into in the name of the VIE may be transferred to YOD Hong Kong, or the work under such contracts may be subcontracted, in whole or in part, to YOD Hong Kong, on terms to be determined by agreement between YOD Hong Kong and the VIE; and

(e) any changes to, or any expansion or contraction of, the business may be carried out in the exercise of the sole discretion of YOD Hong Kong, and in the name of and at the expense of, YOD Hong Kong;

provided, however, that none of the foregoing may cause or have the effect of terminating (without being substantially replaced under the name of YOD Hong Kong) or adversely affecting any license, permit or regulatory status of the VIE.

The term of each Management Services Agreement is 20 years, and may not be terminated by the VIE, except with the consent of, or a material breach by, YOD Hong Kong.

In addition, for SSF, we have also entered into a Loan Agreement with the following terms:

Loan Agreement

Pursuant to the Loan Agreement among YOD WFOE and the nominee shareholders, YOD WFOE agrees to lend RMB 19.8 million and RMB 0.2 million, respectively, to the nominee shareholders of SSF for the purpose of establishing SSF and for development of its business. As of December 31, 2016, RMB 27.6 million (US $4.2 million) and RMB nil have been lent to Lan Yang and Yun Zhu, respectively. Lan Yang has contributed all of the RMB 27.6 million (US $4.2 million) in the form of capital contribution and accordingly the loan is eliminated with the capital of SSF upon consolidation. The loan can only be repaid by a transfer by the nominee shareholders of their equity interests in SSF to YOD WFOE or YOD WFOE’s designated persons, through (i) YOD WFOE having the right, but not the obligation to at any time purchase, or authorize a designated person to purchase, all or part of the Nominee Shareholders’ equity interests in SSF at such price as YOD WFOE shall determine (the “Transfer Price”), (ii) all monies received by the nominee shareholders through the payment of the Transfer Price being used solely to repay YOD WFOE for the loans, and (iii) if the Transfer Price exceeds the principal amount of the loans, the amount in excess of the principal amount of the loans being deemed as interest payable on the loans, and to be payable to YOD WFOE in cash. Otherwise, the loans shall be deemed to be interest-free. The term of the Loan Agreement is perpetual, and may only be terminated upon the nominee shareholders receiving repayment notice, or upon the occurrence of an event of default under the terms of the agreement.

Our Unconsolidated Equity Investment

We hold 30% ownership interest in Shandong Media, our print-based media business, and account for our investment in Shandong Media under the equity method. The business of Shandong Media includes a television programming guide publication, the distribution of periodicals, the publication of advertising, the organization of public relations events, the provision of information related services, copyright transactions, the production of audio and video products, and the provision of audio value added communication services.

We hold 39% ownership interest in Hua Cheng, and account for our investment in Hua Cheng under the equity method. The business of Hua Cheng mainly includes distribution of content and video on demand business on television terminal.

We hold 50% ownership interest in Wecast Internet Limited (“Wecast Internet”), and account for our investment in Wecast Internet under the equity method. The business of Wecast Internet mainly includes computer network technology development, integrated circuit of software and hardware technology development, technical consultation.

Investments in Shandong Media, Hua Cheng and Wecast Internet where the Company can exercise significant influence, but not control, is classified as a long-term equity investment and accounted for using the equity method. Under the equity method, the investment is initially recorded at cost and adjusted for the Company’s share of undistributed earnings or losses of the investee. Investment losses are recognized until the investment is written down to nil provided the Company does not guarantee the investee’s obligations nor it is committed to provide additional funding.

Our Industry (For the OTT, Mobile App, IPTV and Digital Cable VOD Businesses)

Mobile

China’s smartphone market is now the world’s largest. According to the International Data Corporation (IDC), the smartphones shipped to China in 2016 represented 8.7% Year-to-Year growth comparing to the 434.1 million smartphones being shipped to China in 2015. In addition, China’s three mobile telecom carriers have created a new company, China Tower, which has taken over ownership of the three firms’ telecom infrastructure while ambitiously. China Tower has invested RMB3.37 billion in 2015 and RMB 6.11 billion in 2016 in telecom tower construction projections. China Tower’s accumulated construction in the past two year has reached 82% of the 140 million towers of the total industry, which are accumulated in the past 30 years. The increasing physical improvements to the network are meant to accommodate the expansion of 4G mobile services.

| 9 |

OTT & IPTV

China plans to invest 2 trillion yuan ($323 billion) to improve its broadband infrastructure by 2020 with the aim of taking the nearly entire population online, according to the Ministry of Information and Industry on the government’s official website www.gov.cn. The government is trying to improve fixed-line and wireless connectivity throughout China, where only 45 percent of the population have Internet access. China’s broadband strategy will ensure that the number of 3G and LTE users will increase to 1.2 billion by 2020, four times of the current figure.

Cable

Until 2005, there were over 3,000 independent cable operators in the PRC. While the State Administration of Press, Publication, Radio, Film and Television (“SAPPRFT”), an executive branch under the State Council of the PRC, has advocated for national consolidation of the country’s sprawling cable networks, the consolidation has primarily occurred at the provincial level. The 30 provinces are highly variable in their consolidation efforts and processes. To expedite consolidation, SAPPRFT announced in 2010 that it would permit and encourage state-owned cable operators to expand and consolidate through mergers and acquisitions. We believe that as consolidation proceeds it will smooth the way to two-way digitization through common technical standards.

We believe that SAPPRFT and its broadcasters are currently focusing on increasing subscription revenues by converting Chinese television viewers from “analog” service to “digital” (pay TV) service. The digitalization efforts include providing upgraded digital set-top-boxes free of charge that will provide the bandwidth to deliver pay channels and services beyond the basic tier as part of a digital television service bundling initiative.

Our Competition (For the OTT, Mobile App, IPTV and Digital Cable VOD Businesses)

The market for video entertainment is subject to continuous change and aggressive competition. Our primary competitors include Internet-based content providers and the DVD market, both of which include those that provide legal and pirated (illegal) content. Specifically, our primary competitors include companies that operate online video websites in China where we compete with these entities for customers and users. Some of these competitors include iQiyi.com, Youku, Tencent and Sohu. As far as digital cable distribution, although we can provide no assurances that other companies will not enter the market of providing such services, we believe that we will have a competitive advantage over any new market entrant because of our exclusive joint venture partnership with CCTV-6’s pay channel, CHC, and first to market advantage. We also have some indirect competition from the pirated DVD market.

Intellectual Property

We are not a party to any royalty agreements, labor contracts or franchise agreements. We own the trademark “YOU On Demand” and “(优点互动)” which are both registered in the PRC. The duration of our trademarks is ten years and trademarks are generally subject to an indefinite number of renewals upon appropriate application.

Our Employees

As of December 31, 2016, we had a total of 48 full-time employees including one located in the United States. The following table sets forth the number of our employees by function at December 31, 2016.

| Function | Number of Employees | |

| Business Development | 7 | |

| Service Operations | 7 | |

| Technology | 13 | |

| Content Production | 4 | |

| Financial and Legal | 11 | |

| Human Resource | 2 | |

| Administrative | 4 | |

| TOTAL | 48 |

Our employees are not represented by a labor organization or covered by a collective bargaining agreement. We have not experienced any work stoppages.

| 10 |

We are required under PRC law to make contributions to employee benefit plans at specified percentages of employee salary. In addition, we are required by the PRC law to cover employees in China with various types of social insurance. We believe that we are in compliance with the relevant PRC laws.

Seasonality

Our operating results and operating cash flows historically have not been subject to seasonal variations. This pattern may change, however, as a result of new market opportunities or new product introductions.

Regulation

General Regulation of Businesses

Our PRC-based operating subsidiaries and VIEs are regulated by the national and local laws of the PRC. The radio and television broadcasting industries are highly regulated in China. Local broadcasters including national, provincial and municipal radio and television broadcasters are 100% state-owned assets. SAPPRFT regulates the radio and television broadcasting industry in China. In China, the radio and television broadcasting industries are designed to serve the needs of government programming first, and to make profits second. The SAPPRFT and the upper level government bodies control broadcasting assets and broadcasting content in China.

The Ministry of Industry and Information Technology (“MIIT”) plays a similar role to SAPPRFT in the telecom industry in China. China’s telecom industry is comparatively more deregulated than the broadcasting industry. While China’s telecom industry has substantial financial backing, SAPPRFT, and its regulator, the Propaganda Ministry under China’s Communist Party Central Committee, never relinquished ultimate regulatory control over content and broadcasting control.

The major internet regulatory barrier for cable operators to migrate into multiple-system operators and to be able to offer telecom services is the license barrier. Few independent cable operators in China are able to acquire full and proper broadband connection licenses from MIIT. The licenses, while awarded by MIIT, are given on very-fragmented regional market levels. With cable operators holding the last mile to access end users, cable operators are believed to pose a competitive threat to local telecom carriers. While internet connection licenses are deregulated to even the local private sector, MIIT still tries to utilize the relevant licenses as a barrier to entry from cable operators that fall under the administration of SAPPRFT.

We are required to obtain government approval from the Ministry of Commerce of the People’s Republic of China (“MOFCOM”), and other government agencies in China for transactions such as our acquisition or disposition of business entities in China. Additionally, foreign ownership of business and assets in China is not permitted without specific government approval. For this reason, Sinotop Beijing was acquired through our acquisition of YOD Hong Kong, which controls Sinotop Beijing through a series of contractual agreements with YOD Hong Kong and YOD WFOE. We use voting control agreements among the parties so as to obtain equitable and legal ownership or control of our subsidiaries and VIEs.

The PRC market in which the Company operates poses certain macro-economic and regulatory risks and uncertainties. These uncertainties extend to the ability of the Company to conduct wireless telecommunication services through contractual arrangements in the PRC since the industry remains highly regulated. The Company conducts all of its operations in China through Zhong Hai Media and SSF, which the Company controls as a result of a series of contractual arrangements entered among YOD WFOE, Sinotop Beijing as the parent company of Zhong Hai Media, SSF and the respective legal shareholders of Sinotop Beijing and SSF. The Company believes that these contractual arrangements are in compliance with PRC law and are legally enforceable. If Sinotop Beijing, SSF or their respective legal shareholders fail to perform the obligations under the contractual arrangements or any dispute relating to these contracts remains unresolved, YOD WFOE or YOD HK can enforce its rights under the VIE contracts through PRC law and courts. However, uncertainties in the PRC legal system could limit the Company’s ability to enforce these contractual arrangements. In particular, the interpretation and enforcement of these laws, rules and regulations involve uncertainties. If YOD WFOE had direct ownership of Sinotop Beijing and SSF, it would be able to exercise its rights as a shareholder to effect changes in the board of directors of Sinotop Beijing or SSF, which in turn could effect changes at the management level, subject to any applicable fiduciary obligations. However, under the current contractual arrangements, the Company relies on Sinotop Beijing, SSF and their respective legal shareholders to perform their contractual obligations to exercise effective control. The Company also gives no assurance that PRC government authorities will not take a view in the future that is contrary to the opinion of the Company. If the current ownership structure of the Company and its contractual arrangements with the VIEs and their equity holders were found to be in violation of any existing or future PRC laws or regulations, the Company’s ability to conduct its business could be impacted and the Company may be required to restructure its ownership structure and operations in the PRC to comply with the changes in the PRC laws which may result in deconsolidation of the VIEs.

In particular, the interpretation and enforcement of these laws, rules and regulations involve uncertainties. If YOD WFOE had direct ownership of Sinotop Beijing and SSF, it would be able to exercise its rights as a shareholder to effect changes in the board of directors of Sinotop Beijing or SSF, which in turn could effect changes at the management level, subject to any applicable fiduciary obligations. However, under the current contractual arrangements, the Company relies on Sinotop Beijing, SSF and their respective legal shareholders to perform their contractual obligations to exercise effective control. The Company also gives no assurance that PRC government authorities will not take a view in the future that is contrary to the opinion of the Company. If the current ownership structure of the Company and its contractual arrangements with the VIEs and their equity holders were found to be in violation of any existing or future PRC laws or regulations, the Company’s ability to conduct its business could be impacted and the Company may be required to restructure its ownership structure and operations in the PRC to comply with the changes in the PRC laws which may result in deconsolidation of the VIEs.

In addition, the telecommunications, information and media industries remain highly regulated. Restrictions are currently in place and are unclear with respect to which segments of these industries foreign owned entities, like YOD WFOE, may operate. The PRC government may issue from time to time new laws or new interpretations on existing laws to regulate areas such as telecommunications, information and media, some of which are not published on a timely basis or may have retroactive effect. For example, there is substantial uncertainty regarding the Draft Foreign Investment Law, including, among others, what the actual content of the law will be as well as the adoption and effective date of the final form of the law. Administrative and court proceedings in China may also be protracted, resulting in substantial costs and diversion of resources and management attention. While such uncertainty exists, the Company cannot assure that the new laws, when it is adopted and becomes effective, and potential related administrative proceedings will not have a material and adverse effect on the Company’s ability to control the affiliated entities through the contractual arrangements. Regulatory risk also encompasses the interpretation by the tax authorities of current tax laws, and the Company’s legal structure and scope of operations in the PRC, which could be subject to further restrictions resulting in limitations on the Company’s ability to conduct business in the PRC.

| 11 |

Licenses and Permits

Video on Demand

Zhong Hai Media holds the following licenses:

| Description | License/Permit | |

| Cable Television & Operations Permit | Beijing No. 1413 | |

| Internet Content Provider | Beijing No. 140351 | |

| Video Production Permit | Beijing No. 0080 | |

| Internet Publication Permit | Beijing No. 213 |

Shandong Media

Shandong Media holds the following licenses:

| Description | License/Permit | |

| PRC Newspaper Publication License for Shandong Broadcast & TV Weekly | National Unified Publication CN 37-0014 | |

| PRC Magazine Publication License for View Weekly | Ruqichu No:1384 | |

| PRC Magazine Publication License for Modern Movie & TV Biweekly | Ruqichu No:1318 | |

| Advertising License for Shandong Broadcast & TV Weekly | 3700004000093 | |

| Advertising License for View Weekly | 3700004000186 | |

| Advertising License for Modern Movie & TV Biweekly | 3700004000124 |

Taxation

On March 16, 2007, the National People’s Congress of China passed the EIT Law, and on November 28, 2007, the State Council of China passed its implementing rules which took effect on January 1, 2008. The EIT Law and its implementing rules impose a unified earned income tax (“EIT”) rate of 25.0% on all domestic-invested enterprises and foreign invested enterprises (“FIEs”) unless they qualify under certain limited exceptions. In addition, under the EIT Law, an enterprise established outside of China with “de facto management bodies” within China is considered a resident enterprise and will normally be subject to an EIT of 25% on its global income. The implementing rules define the term “de facto management bodies” as “an establishment that exercises, in substance, overall management and control over the production, business, personnel, accounting, etc., of a Chinese enterprise.” If the PRC tax authorities subsequently determine that we should be classified as a resident enterprise, then our organization’s global income will be subject to PRC income tax of 25%. For detailed discussion of PRC tax issues related to resident enterprise status, see “Risk Factors – Risks Related to Doing Business in China – Under the New Enterprise Income Tax Law, we may be classified as a “resident enterprise” of China.” Such classification will likely result in unfavorable tax consequences to us and our non-PRC shareholders.”

Foreign Currency Exchange

All of our sales revenue and significant expenses are denominated in RMB. Under the PRC foreign currency exchange regulations applicable to us, RMB is convertible for current account items, including the distribution of dividends, interest payments, trade and service-related foreign exchange transactions. Currently, our PRC operating entities may purchase foreign currencies for settlement of current account transactions, including payments of dividends to us, without the approval of the PRC State Administration of Foreign Exchange (“SAFE”), by complying with certain procedural requirements. Conversion of RMB for capital account items, such as direct investment, loan, security investment and repatriation of investment, however, is still subject to the approval of SAFE. In particular, if our PRC operating entities borrow foreign currency through loans from us or other foreign lenders, these loans must be registered with SAFE, and if we finance the subsidiaries by means of additional capital contributions, these capital contributions must be approved by certain government authorities, including the MOFCOM, or their respective local branches. These limitations could affect our PRC operating entities’ ability to obtain foreign exchange through debt or equity financing.

Dividend Distributions

All of our revenues are earned by our PRC entities. However, PRC regulations restrict the ability of our PRC entities to make dividends and other payments to their offshore parent company. PRC legal restrictions permit payments of dividends by our PRC entities only out of their accumulated after-tax profits, if any, determined in accordance with PRC accounting standards and regulations. Each of our PRC subsidiaries is also required under PRC laws and regulations to allocate at least 10% of our annual after-tax profits determined in accordance with PRC GAAP to a statutory general reserve fund until the amounts in such fund reaches 50% of its registered capital. These reserves are not distributable as cash dividends. Our PRC subsidiaries have the discretion to allocate a portion of their after-tax profits to staff welfare and bonus funds, which may not be distributed to equity owners except in the event of liquidation.

| 12 |

In addition, under the new EIT law, the Notice of the State Administration of Taxation on Negotiated Reduction of Dividends and Interest Rates (“Notice 112”), which was issued on January 29, 2008, and the Notice of the State Administration of Taxation Regarding Interpretation and Recognition of Beneficial Owners under Tax Treaties (“Notice 601”), which became effective on October 27, 2009, dividends from our PRC operating subsidiaries paid to us through our entities will be subject to a withholding tax at a rate of 10%. Furthermore, the ultimate tax rate will be determined by treaty between the PRC and the tax residence of the holder of the PRC subsidiary. Dividends declared and paid from before January 1, 2008 on distributable profits are grandfathered under the EIT Law and are not subject to withholding tax.

The Company intends on reinvesting profits, if any, and does not intend on making cash distributions of dividends in the near future.

| ITEM 1A. | RISK FACTORS. |

The business, financial condition and operating results of the Company may be affected by a number of factors, whether currently known or unknown, including but not limited to those described below. Any one or more of such factors could directly or indirectly cause the Company’s actual results of operations and financial condition to vary materially from past or anticipated future results of operations and financial condition. Any of these factors, in whole or in part, could materially and adversely affect the Company’s business, financial condition, results of operations and stock price. The following information should be read in conjunction with Part II, Item 7 – “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes in Part II, Item 8, “Financial Statements and Supplementary Data” of this Annual Report.

RISKS RELATED TO OUR BUSINESS

Substantial doubt about our ability to continue as a going concern.

As discussed in Note 3 to the consolidated financial statements included in this report, the Company has incurred significant losses during 2016 and 2015 and has relied on debt and equity financings to fund our operations. As of December 31, 2016, the Company had net current liabilities (current assets less current liabilities) of $4,084,000. Management’s plans regarding these matters are also described in Note 3.

The Company must continue to rely on proceeds from debt and equity issuances to pay for ongoing operating expenses in order to execute its business plan. On March 28, 2016, the Company completed a common stock financing with SSS for $10.0 million. In addition, the Company completed two common stock financing with Seven Star Works Co. Ltd. (“SSW”) for $4.0 million, and with Harvest Alternative Investment Opportunities SPC (“Harvest”) for $4.0 million on July 19, 2016 and August 12, 2016, respectively. On November 17, 2016, the Company completed on additional common stock financing with Wecast Media Group Limited (formerly known as Sun Seven Star Hong Kong Cultural Development Limited) for $2.0 million. Although the Company believes it has the ability to raise funds by issuing debt or equity instruments, additional financing may not be available to the Company on terms acceptable to the Company or at all or such resources may not be received in a timely manner.

These conditions raise substantial doubt about the Company’s ability to continue as a going concern. The consolidated financial statements have been prepared assuming that the Company will continue as a going concern and, accordingly, do not include any adjustments that might result from the outcome of this uncertainty. If we are in fact unable to continue as a going concern, our shareholders may lose their entire investment in our Company.

The Company is in the process of transforming its business model and this transformation may not be successful.

The Company is in the process of transforming its business model, by leveraging and optimizing its current operations as a premium content Video On Demand service provider in China to evolve into a global, B2B2C, mobile-driven, consumer management platform for both enterprises and consumers. By aiming to establish the world’s premier multimedia, social networking and e-commerce- enabled network with the largest global effective connected user base, Wecast Network, through this expanded, cloud-based, ecosystem of connected screens combined with strong partnerships with leading global providers, will be capable of delivering a vast array of Wecast Network–branded products and services to enterprise customers and end-use consumers - anytime and anywhere, across multiple platforms and devices. In connection with this transformation, the Company has recently assembled a new experienced management team, stabilized the foundation, capitalized and rebranded the Company, reconfigured the business structure, expanded the Company’s mission and business lines, made several key investments and finally, injected several privately held and revenue producing assets into the corporation. It is uncertain whether these efforts will prove beneficial or whether we will be able to develop the necessary business models, infrastructure and systems to support the business. This includes having or hiring the right talent to execute our business strategy. Market acceptance of new product and service offerings will be dependent in part on our ability to include functionality and usability that address customer requirements, and optimally price our products and services to meet customer demand and cover our costs.

Any failure to implement this plan in accordance with our expectations could have a material adverse effect on our financial results. Even if the anticipated benefits and savings are substantially realized, there may be consequences, internal control issues, or business impacts that were not expected. Additionally, as a result of our restructuring efforts in connection with our business transformation plan, we may experience a loss of continuity, loss of accumulated knowledge or loss of efficiency during transitional periods. Reorganization and restructuring can require a significant amount of management and other employees' time and focus, which may divert attention from operating activities and growing our business. If we fail to achieve some or all of the expected benefits of these activities, it could have a material adverse effect on our competitive position, business, financial condition, results of operations and cash flows.

Our operating results are likely to fluctuate significantly and may differ from market expectations.

Our annual and quarterly operating results have varied significantly in the past, and may vary significantly in the future, due to a number of factors which could have an adverse impact on our business. Our revenue may fluctuate as our channel partners make changes to their business model and we rely on third-party payment platforms to produce billing based on payment collection from end-users across all platforms. In recent years, video content costs escalated sharply in the industry which affected our ability to procure new content at the same cost as prior years. In addition, we incurred certain impairment losses of intangible assets and earn-out share award expenses as discussed in Note 7 and 12 to the consolidated financial statements included in this report.

Expansion of our business may put added pressure on our management and operational infrastructure, impeding our ability to meet any potential increased demand for our services and possibly hurting our future operating results.

Our business plan is to significantly grow our operations to meet anticipated growth in demand for the services that we offer, and by the introduction of new goods or services. Growth in our businesses may place a significant strain on our personnel, management, financial systems and other resources. The evolution of our business also presents numerous risks and challenges, including:

| 13 |

| . | our ability to successfully and rapidly expand sales to potential new distributors in response to potentially increasing demand; |

| . | the costs associated with such growth, which are difficult to quantify, but could be significant; and |

| . | rapid technological change. |

To accommodate any such growth and compete effectively, we may need to obtain additional funding to improve information systems, procedures and controls and expand, train, motivate and manage our employees, and such funding may not be available in sufficient quantities, if at all. If we are not able to manage these activities and implement these strategies successfully to expand to meet any increased demand, our operating results could suffer.

In order to comply with PRC regulatory requirements, we operate our businesses through companies with which we have contractual relationships. By virtue of these contractual relationships, we control the economic interests and have the power to direct the activities of these entities, and are therefore determined to be the primary beneficiary of these entities, but we do not have any equity ownership interest in these entities. If the PRC government determines that our contractual agreements with these entities are not in compliance with applicable regulations, our business in the PRC could be materially adversely affected.

We do not have direct or indirect equity ownership of our VIEs, which collectively operate all our businesses in China, but instead have entered into contractual arrangements with our VIEs and each of its individual legal shareholder(s) pursuant to which we received an economic interest in, and have the power to direct the activities of the VIEs, in a manner substantially similar to a controlling equity interest. Although we believe that our business operations are in compliance with the current laws in China, we cannot be sure that the PRC government would view our operating arrangements to be in compliance with PRC regulations that may be adopted in the future. If we are determined not to be in compliance, the PRC government could levy fines, revoke our business and operating licenses, require us to restrict or discontinue our operations, restrict our right to collect revenues, require us to restructure our business, corporate structure or operations, impose additional conditions or requirements with which we may not be able to comply, impose restrictions on our business operations or on our customers, or take other regulatory or enforcement actions against us that could be harmful to our business. As a result, our business in the PRC could be materially adversely affected.

We rely on contractual arrangements with our VIEs for our operations, which may not be as effective for providing control over these entities as direct ownership.

Our operations and financial results are dependent on our VIEs in which we have no equity ownership interest and must rely on contractual arrangements to control and operate the businesses of our VIEs. These contractual arrangements may not be as effective for providing control over the VIEs as direct ownership. For example, the VIEs may be unwilling or unable to perform its contractual obligations under our commercial agreements. Consequently, we may not be able to conduct our operations in the manner currently planned. In addition, the VIEs may seek to renew their agreements on terms that are disadvantageous to us. Although we have entered into a series of agreements that provide us with the ability to control the VIEs, we may not succeed in enforcing our rights under them insofar as our contractual rights and legal remedies under PRC law are inadequate. In addition, if we are unable to renew these agreements on favorable terms when these agreements expire or to enter into similar agreements with other parties, our business may not be able to operate or expand, and our operating expenses may significantly increase.

Our arrangements with our VIEs and its respective shareholders may be subject to a transfer pricing adjustment by the PRC tax authorities which could have an adverse effect on our income and expenses.

We could face material and adverse tax consequences if the PRC tax authorities determine that our contracts with our VIEs and their respective shareholders were not entered into based on arm’s length negotiations. Although our contractual arrangements are similar to those of other companies conducting similar operations in China, if the PRC tax authorities determine that these contracts were not entered into on an arm’s length basis, they may adjust our income and expenses for PRC tax purposes in the form of a transfer pricing adjustment. Such an adjustment may require that we pay additional PRC taxes plus applicable penalties and interest, if any.

If we do not obtain shareholder approval of certain potential common stock issuances to BT Capital Global Limited, or BT Capital, a promissory note held by BT Capital will be due, and we may not have the resources to repay such note.

Under the rules of the NASDAQ Capital Market, we generally may not issue more than 4.99% of our outstanding shares in connection with an acquisition where a related party has an interest in the target, unless we obtain shareholder approval. On January 30, 2017, we entered into an Securities Purchase Agreement (the “Securities Purchase Agreement”) with BT Capital for the purchase by us of all of the outstanding capital stock of Sun Video Group Hong Kong Limited (“SVG”), an affiliate of the Company’s chairman Bruno Wu, for an aggregate purchase price of (i) $800,000; and (ii) a convertible promissory note (the “SVG Note”) with the principal and interest thereon convertible into shares of the Company’s common stock at a conversion rate of $1.50 per share. BT has guaranteed that SVG will achieve certain financial goals within 12 months of the closing. The SVG Note has a stated principal amount of $50 million, bears interest at the rate of 0.56% per annum and matures on December 31, 2017. In the event of default, the SVG Note will become immediately due and payable, subject to certain limitations set forth in the Securities Purchase Agreement.

Under the terms of the Securities Purchase Agreement, until receipt of necessary Company’s shareholder approvals, the SVG Note is not convertible into shares of Company common stock.

| 14 |

Although we will put this proposal to our shareholders for their approval, no assurances can be given that we will obtain such shareholder approval. If we fail to obtain such shareholder approval by December 31, 2017 (unless such maturity date for the SVG Note is extended), BT Capital may require us to satisfy all of our obligations under the SVG Note, including the payment in full of all principal and interest, and may pursue other legal or equitable remedies against us. Our ability to make such cash payments will depend on available cash resources at that time, and there can be no assurance that we will have the cash necessary to make such payments. Early payment of the SVG Note could therefore have a significantly adverse effect on our liquidity and financial condition.

The success of our business is dependent on our ability to retain our existing key employees and to add and retain senior officers to our management.

We depend on the services of our key employees, in particular, Mr. Bing Yang, our Chief Executive Officer. Our success will largely depend on our ability to retain these key employees and to attract and retain qualified senior and middle level managers to our management team. We have recruited executives and management in China to assist in our ability to manage the business and to recruit and oversee employees. While we believe we offer compensation packages that are consistent with market practice, we cannot be certain that we will be able to hire and retain sufficient personnel to support our business. In addition, severe capital constraints have limited our ability to attract specialized personnel. Moreover, our budget limitations will restrict our ability to hire qualified personnel. The loss of any of our key employees would significantly harm our business. We do not maintain key person life insurance on any of our employees.

We may be unable to compete successfully against new entrants and established film and media industry competitors.

The Chinese market for film and media content and services is intensely competitive and rapidly changing. Barriers to entry may be relatively minimal, and current and new competitors may be able to provide film and media content at a lower cost. Although the Chinese government continues to improve its efforts to enforce intellectual property protection, pirated film and media content continues to be prevalent in China, which may reduce our potential profits. In addition, other companies offer competitive products or services including Chinese language content. Furthermore, as many of our existing competitors, as well as a number of potential competitors, have longer operating histories in the entertainment, film, media or Internet service markets, greater name and brand recognition, better relationships with key players, larger customer bases and libraries and significantly greater financial, technical and marketing resources than we have, we cannot assure you that we will be able to compete successfully against our current or future competitors. Any increased competition could reduce our subscribers, make it difficult for us to attract and retain subscribers, reduce or eliminate our market share, lower our profit margins and reduce our revenues.

Videos and other types of content displayed on Internet platforms may be found objectionable by PRC regulatory authorities, which may result in penalties and other administrative actions against us.

The PRC government has adopted regulations governing Internet access and the distribution of videos over the Internet. Although we have adopted internal procedures to obtain the appropriate PRC censorship and regulatory approval for content licensed to us, new regulations and implementation guidance may require us to limit or eliminate the dissemination of certain content through Internet channels. Moreover, the costs of compliance with these regulations may continue to increase as we procure more content to support our business growth. In addition, we may also face litigation or administrative action for defamation, negligence, or other purported injuries resulting from content programming operated by us. Such litigation and administrative actions, with or without merit, may be expensive and time-consuming and may result in significant diversion of resources and management attention from our business operations. Furthermore, such litigation or administrative actions may adversely affect our brand image and reputation.

We derived a substantial portion of our revenue from several major customers. If we lose any of these customers, or if the volume of business with these distribution partners decline, our revenues may be significantly affected.

Revenue from four of our distribution partners accounted for about 59% of our revenues for the year ended December 31, 2016 and revenue from three of our distribution partners accounted for over 41% of our revenues for the year ended December 31, 2015. Due to our reliance on a limited number of distribution partners, any of the following events may cause a material decline in our revenue and have a material adverse effect on our results of operations:

| . | reductions, delays or cessation of purchases from one or more significant distribution partner; |

| . | loss of one or more distribution partner and our inability to find new distribution partners that can generate the same volume of business; and |

| . | failure of any distribution partner to make timely payment of our products and services. |

We cannot be certain whether these relationships will continue to develop or if these distribution partners will continue to generate significant revenue for us in the future.

| 15 |

If we fail to develop and maintain an effective system of internal control over financial reporting, our ability to accurately and timely report our financial results or prevent fraud may be adversely affected, and investor confidence and market price of our shares may be adversely impacted.