Exhibit 10.1

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

QUARTERLY REPORT

PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE QUARTERLY PERIOD ENDED July 31, 2013

Commission File Number 1-7062

INNSUITES HOSPITALITY TRUST

(Exact name of registrant as specified in its charter)

|

Ohio |

34-6647590 |

|

(State or other jurisdiction of |

(I.R.S. Employer Identification Number) |

|

incorporation or organization) |

|

|

| |

|

InnSuites Hotels Centre | |

|

1625 E. Northern Avenue, Suite 105 | |

|

Phoenix, AZ 85020 | |

|

(Address of principal executive offices) | |

|

| |

|

Registrant’s telephone number, including area code: (602) 944-1500 | |

Indicate by check mark whether the registrant: (l) has filed all reports required to be filed by Section 13 or l5(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ☐ Accelerated filer ☐ Non-accelerated filer ☐ Smaller reporting company ☒

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

Number of outstanding Shares of Beneficial Interest, without par value, as of September 3, 2013: 9,211,814

PART I

FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

INNSUITES HOSPITALITY TRUST AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

|

July 31, 2013 |

January 31, 2013 |

|||||||

|

(UNAUDITED) |

||||||||

|

ASSETS |

||||||||

|

Current Assets: |

||||||||

|

Cash and Cash Equivalents |

$ | 307,627 | $ | 493,953 | ||||

|

Restricted Cash |

41,955 | 13,783 | ||||||

|

Accounts Receivable, including $45,086 and $81,176 from related parties and net of Allowance for Doubtful Accounts of $34,049 and $34,415, as of July 31, 2013 and January 31, 2013, respectively |

392,933 | 568,186 | ||||||

|

Prepaid Expenses and Other Current Assets |

301,433 | 268,399 | ||||||

|

Total Current Assets |

1,043,948 | 1,344,321 | ||||||

|

Hotel Properties, net |

24,044,524 | 24,686,780 | ||||||

|

Property, Plant and Equipment, net |

99,265 | 112,977 | ||||||

|

Deferred Finance Costs and Other Assets |

110,503 | 137,884 | ||||||

|

TOTAL ASSETS |

$ | 25,298,240 | $ | 26,281,962 | ||||

|

LIABILITIES AND EQUITY |

||||||||

|

LIABILITIES |

||||||||

|

Current Liabilities: |

||||||||

|

Accounts Payable and Accrued Expenses |

$ | 2,020,312 | $ | 2,298,497 | ||||

|

Current Portion of Mortgage Notes Payable |

1,229,963 | 1,208,365 | ||||||

|

Current Portion of Notes Payable to Banks |

600,000 | 450,000 | ||||||

|

Current Portion of Other Notes Payable |

130,398 | 189,799 | ||||||

|

Total Current Liabilities |

3,980,673 | 4,146,661 | ||||||

|

Mortgage Notes Payable |

18,122,211 | 18,746,559 | ||||||

|

Other Notes Payable |

130,660 | 162,457 | ||||||

|

TOTAL LIABILITIES |

22,233,544 | 23,055,677 | ||||||

|

Commitments and Contingencies (See Note 10) |

||||||||

|

SHAREHOLDERS' EQUITY |

||||||||

|

Shares of Beneficial Interest, without par value, unlimited authorization; 16,822,746 and 16,804,746 shares issued and 8,371,988 and 8,375,207 shares outstanding at July 31, 2013 and January 31, 2013, respectively |

14,760,660 | 14,940,048 | ||||||

|

Treasury Stock, 8,450,758 and 8,429,539 shares held at July 31, 2013 and January 31, 2013, respectively |

(11,918,290 | ) | (11,877,886 | ) | ||||

|

TOTAL TRUST SHAREHOLDERS' EQUITY |

2,842,370 | 3,062,162 | ||||||

|

NON-CONTROLLING INTEREST |

222,326 | 164,123 | ||||||

|

TOTAL EQUITY |

3,064,696 | 3,226,285 | ||||||

|

TOTAL LIABILITIES AND EQUITY |

$ | 25,298,240 | $ | 26,281,962 | ||||

See accompanying notes to unaudited

condensed consolidated financial statements

INNSUITES HOSPITALITY TRUST AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

FOR THE SIX MONTHS ENDED July 31, 2013 2012 REVENUE Room Food and Beverage Other Management and Trademark Fees TOTAL REVENUE OPERATING EXPENSES Room Food and Beverage Telecommunications General and Administrative Sales and Marketing Repairs and Maintenance Hospitality Utilities Hotel Property Depreciation Real Estate and Personal Property Taxes, Insurance and Ground Rent Other TOTAL OPERATING EXPENSES OPERATING INCOME Interest Income TOTAL OTHER INCOME Interest on Mortgage Notes Payable Interest on Notes Payable to Banks Interest on Other Notes Payable TOTAL INTEREST EXPENSE CONSOLIDATED NET INCOME (LOSS) LESS: NET INCOME (LOSS) ATTRIBUTABLE TO NON-CONTROLLING INTEREST NET LOSS ATTRIBUTABLE TO CONTROLLING INTERESTS NET LOSS PER SHARE – BASIC AND DILUTED WEIGHTED AVERAGE NUMBER OF SHARES OUTSTANDING - BASIC AND DILUTED

$

7,428,119

$

7,314,135

561,762

603,035

135,718

107,333

97,611

166,624

8,223,210

8,191,127

1,902,041

1,939,662

494,266

521,742

14,434

36,076

1,769,173

1,614,296

535,229

597,315

606,240

767,220

440,158

442,220

607,399

627,996

899,481

867,187

482,484

544,989

4,475

5,053

7,755,380

7,963,756

467,830

227,371

1,811

5,402

1,811

5,402

371,843

465,915

8,852

1,094

16,302

18,088

396,997

485,097

72,644

(252,324

)

303,693

(30,547

)

$

(231,049

)

$

(221,777

)

$

(0.03

)

$

(0.03

)

8,381,868

8,429,911

See accompanying notes to unaudited

condensed consolidated financial statements

INNSUITES HOSPITALITY TRUST AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

|

FOR THE THREE MONTHS ENDED July 31, |

||||||||

|

2013 |

2012 |

|||||||

|

REVENUE |

||||||||

|

Room |

$ | 3,121,138 | $ | 3,030,877 | ||||

|

Food and Beverage |

205,596 | 243,681 | ||||||

|

Other |

57,885 | 42,776 | ||||||

|

Management and Trademark Fees |

42,393 | 54,168 | ||||||

|

TOTAL REVENUE |

3,427,012 | 3,371,502 | ||||||

|

OPERATING EXPENSES |

||||||||

|

Room |

954,550 | 962,446 | ||||||

|

Food and Beverage |

200,885 | 258,663 | ||||||

|

Telecommunications |

8,895 | 19,256 | ||||||

|

General and Administrative |

946,692 | 817,924 | ||||||

|

Sales and Marketing |

246,041 | 313,404 | ||||||

|

Repairs and Maintenance |

314,019 | 371,223 | ||||||

|

Hospitality |

212,061 | 215,197 | ||||||

|

Utilities |

343,012 | 344,326 | ||||||

|

Hotel Property Depreciation |

444,850 | 433,530 | ||||||

|

Real Estate and Personal Property Taxes, Insurance and Ground Rent |

256,371 | 257,857 | ||||||

|

Other |

2,032 | 2,645 | ||||||

|

TOTAL OPERATING EXPENSES |

3,929,408 | 3,996,471 | ||||||

|

OPERATING LOSS |

(502,396 | ) | (624,969 | ) | ||||

|

Interest Income |

1,803 | 5,294 | ||||||

|

TOTAL OTHER INCOME |

1,803 | 5,294 | ||||||

|

Interest on Mortgage Notes Payable |

190,686 | 267,946 | ||||||

|

Interest on Notes Payable to Banks |

8,852 | 890 | ||||||

|

Interest on Other Notes Payable |

10,440 | 8,635 | ||||||

|

TOTAL INTEREST EXPENSE |

209,978 | 277,471 | ||||||

|

CONSOLIDATED NET LOSS |

(710,571 | ) | (897,146 | ) | ||||

|

LESS: NET LOSS ATTRIBUTABLE TO NON-CONTROLLING INTEREST |

(43,514 | ) | (213,281 | ) | ||||

|

NET LOSS ATTRIBUTABLE TO CONTROLLING INTERESTS |

$ | (667,057 | ) | $ | (683,865 | ) | ||

|

NET LOSS PER SHARE-BASIC AND DILUTED |

$ | (0.08 | ) | $ | (0.08 | ) | ||

|

WEIGHTED AVERAGE NUMBER OF SHARES OUTSTANDING- |

8,376,472 | 8,417,899 | ||||||

|

BASIC AND DILUTED |

||||||||

See accompanying notes to unaudited

condensed consolidated financial statements

INNSUITES HOSPITALITY TRUST AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF SHAREHOLDERS’ EQUITY

FOR THE SIX MONTHS ENDED JULY 31, 2013

|

Shares of Beneficial Interest |

Treasury Stock |

Trust |

Non- |

|||||||||||||||||||||||||

|

Shares |

Amount |

Shares |

Amount |

Shareholder Equity | Controlling Interest |

Amount |

||||||||||||||||||||||

|

Balance, January 31, 2013 |

8,375,207 | $ | 14,940,048 | 8,429,539 | $ | (11,877,886 | ) | $ | 3,062,162 | $ | 164,123 | $ | 3,226,285 | |||||||||||||||

|

Net Income (Loss) |

- | (231,049 | ) | - | - | (231,049 | ) | 303,693 | 72,644 | |||||||||||||||||||

|

Purchase of Treasury Stock |

(21,219 | ) | - | 21,219 | (40,404 | ) | (40,404 | ) | - | (40,404 | ) | |||||||||||||||||

|

Shares of Beneficial Interest Issues for Services Rendered |

18,000 | 15,480 | - | - | 15,480 | - | 15,480 | |||||||||||||||||||||

|

Sale of Ownership Interests in Subsidiary |

- | 40,062 | - | - | 40,062 | (25,062 | ) | 15,000 | ||||||||||||||||||||

|

Repurchase of Ownership Interests in Subsidiary |

- | (20,000 | ) | - | - | (20,000 | ) | - | (20,000 | ) | ||||||||||||||||||

|

Distribution to Non-Controlling Interests |

- | 16,038 | - | - | 16,038 | (220,347 | ) | (204,309 | ) | |||||||||||||||||||

|

Reallocation of Non-Controlling Interests |

- | 81 | - | - | 81 | (81 | ) | - | ||||||||||||||||||||

|

Balance, July 31, 2013 |

8,371,988 | $ | 14,760,660 | 8,450,758 | $ | (11,918,290 | ) | $ | 2,842,370 | $ | 222,326 | $ | 3,064,696 | |||||||||||||||

See accompanying notes to unaudited

condensed consolidated financial statements

INNSUITES HOSPITALITY TRUST AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

|

FOR THE SIX MONTHS ENDED July 31, |

||||||||

|

2013 |

2012 |

|||||||

|

CASH FLOWS FROM OPERATING ACTIVITIES |

||||||||

|

Consolidated Net Income (Loss) |

$ | 72,644 | $ | (252,324 | ) | |||

|

Adjustments to Reconcile Consolidated Net Income (Loss) to Net Cash Provided by Operating Activities: |

||||||||

|

Provision for Uncollectible Receivables |

(366 | ) | (21,075 | ) | ||||

|

Stock-Based Compensation |

15,480 | 19,800 | ||||||

|

Hotel Property Depreciation |

899,481 | 867,187 | ||||||

|

Amortization of Deferred Loan Fees |

27,381 | 36,256 | ||||||

|

Loss on Disposal of Hotel Property |

6,533 | - | ||||||

|

Changes in Assets and Liabilities: |

||||||||

|

Accounts Receivable |

175,619 | (179,644 | ) | |||||

|

Prepaid Expenses and Other Assets |

(33,034 | ) | (246,178 | ) | ||||

|

Accounts Payable and Accrued Expenses |

(278,185 | ) | (158,628 | ) | ||||

|

NET CASH PROVIDED BY OPERATING ACTIVITIES |

885,553 | 65,394 | ||||||

|

CASH FLOWS FROM INVESTING ACTIVITIES |

||||||||

|

Payments Received on Notes Receivable from Related Party |

- | 454,577 | ||||||

|

Loans Made on Notes Receivable to Related Party |

- | (699,150 | ) | |||||

|

Change in Restricted Cash |

(28,172 | ) | 44,241 | |||||

|

Improvements and Additions to Hotel Properties |

(250,046 | ) | (657,895 | ) | ||||

|

NET CASH USED IN INVESTING ACTIVITIES |

(278,218 | ) | (858,227 | ) | ||||

|

CASH FLOWS FROM FINANCING ACTIVITIES |

||||||||

|

Principal Payments on Mortgage Notes Payable |

(602,750 | ) | (1,507,785 | ) | ||||

|

Payments on Notes Payable to Banks |

(1,277,909 | ) | (805,027 | ) | ||||

|

Borrowings on Notes Payable to Banks |

1,427,909 | 1,160,972 | ||||||

|

Purchase of Treasury Stock |

(29,544 | ) | (128,762 | ) | ||||

|

Purchase of Partnership Units |

- | (525 | ) | |||||

|

Purchase of Subsidiary Equity |

(20,000 | ) | - | |||||

|

Proceeds from Sale of Non-Controlling Ownership Interests in Subsidiaries |

15,000 | 1,604,068 | ||||||

|

Distributions to Non-Controlling Interest |

(204,309 | ) | (205,256 | ) | ||||

|

Payments on Other Notes Payable |

(102,058 | ) | (111,943 | ) | ||||

|

NET CASH PROVIDED BY (USED IN) FINANCING ACTIVITIES |

(793,661 | ) | 5,742 | |||||

|

NET DECREASE IN CASH AND CASH EQUIVALENTS |

(186,326 | ) | (787,091 | ) | ||||

|

CASH AND CASH EQUIVALENTS AT BEGINNING OF PERIOD |

493,953 | 983,424 | ||||||

|

CASH AND CASH EQUIVALENTS AT END OF PERIOD |

$ | 307,627 | $ | 196,333 | ||||

See Supplemental Disclosures at Note 9.

See accompanying notes to unaudited

condensed consolidated financial statements

INNSUITES HOSPITALITY TRUST AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

AS OF JULY 31 AND JANUARY 31, 2013

AND FOR THE THREE AND SIX MONTHS ENDED JULY 31, 2013 AND 2012

1. NATURE OF OPERATIONS AND BASIS OF PRESENTATION

As of July 31, 2013, InnSuites Hospitality Trust (the “Trust”, “we” or “our”) owns directly and through a partnership interest, five hotels with an aggregate of 843 suites in Arizona, southern California and New Mexico (the “Hotels”). The Hotels operate under the trade name “InnSuites Hotels.”

The Trust is the sole general partner of RRF Limited Partnership, a Delaware limited partnership (the “Partnership”), and owned 72.04% of the Partnership as of July 31, 2013 and January 31, 2013. The Trust’s weighted average ownership for the six month periods ended July 31, 2013 and 2012 was 72.04% and 72.03%, respectively. As of July 31, 2013, the Partnership owned 100% of one InnSuites® hotel located in Tucson, Arizona and together with the Trust owned a 58.11% interest in another InnSuites® hotel located in Tucson, Arizona and a 61.60% interest in an InnSuites® hotel located in Ontario, California. The Trust owns and operates a Yuma, Arizona hotel property directly, which it acquired from the Partnership on January 31, 2005, and owns a direct 50.63% interest in an InnSuites® hotel located in Albuquerque, New Mexico.

The Trust directly manages the Hotels through the Trust’s wholly-owned subsidiary, InnSuites Hotels. Under the management agreements, InnSuites Hotels manages the daily operations of the Hotels and three hotels owned by affiliates of Mr. Wirth, the Company’s Chief Executive Officer. All Trust managed Hotel expenses, revenues and reimbursements among the Trust, InnSuites Hotels and the Partnership have been eliminated in consolidation. The management fees for the Hotels are set at 2.5% of room revenue and a monthly accounting fee of $2,000 per hotel. The management fees for the three hotels owned by affiliates of Mr. Wirth were set at 2.5% of room revenue and an annual accounting fee of $27,000, payable $1,000 per month with an additional payment of $15,000 due at year-end for annual accounting closing activities. The additional year-end annual accounting closing fee of $15,000 was discontinued with no material effect on the financial operating results of the Trust at the end of fiscal year 2013. These agreements have no expiration date and may be cancelled by either party with 90-days written notice or 30-days written notice in the event the property changes ownership.

The Trust also provides the use of the “InnSuites” trademark to the Hotels and the three hotels owned by affiliates of Mr. Wirth through the Trust’s wholly-owned subsidiary, InnSuites Hotels. All such fees among InnSuites Hotels, the Trust and the Partnership have been eliminated in consolidation. From January 1, 2012 through December 31, 2012, the fees received by InnSuites Hotels were equal to $10 per month per room for the first 100 rooms, and $2 per month per room for the number of rooms exceeding 100. As of January 1, 2013, these trademark fees were discontinued. In their place, the per reservation fee is increased to a flat 10% of the value of the reservations received.

PARTNERSHIP AGREEMENT

The Partnership Agreement of the Partnership provides for the issuance of two classes of Limited Partnership units, Class A and Class B. Class A and Class B Partnership units are identical in all respects, except that each Class A Partnership unit is convertible into one newly-issued Share of Beneficial Interest of the Trust at any time at the option of the particular limited partner. The Class B Partnership units may only become convertible, each into one newly-issued Share of Beneficial Interest of the Trust, with the approval of the Board of Trustees, in its sole discretion. As of July 31 and January 31, 2013, 286,034 Class A Partnership units were issued and outstanding representing 2.17% of the total Partnership units. Additionally, as of July 31 and January 31, 2013, 3,407,938 Class B Partnership units were outstanding to James Wirth, the Trust’s Chairman and Chief Executive Officer, and Mr. Wirth’s affiliates. If all of the Class A and B Partnership units were converted on July 31, 2013, the limited partners in the Partnership would receive 3,693,972 Shares of Beneficial Interest of the Trust. As of July 31 and January 31, 2013, the Trust owns 9,517,545 general partner units in the Partnership, representing 72.04% of the total Partnership units.

BASIS OF PRESENTATION

The financial statements of the Partnership, InnSuites Hotels and Yuma Hospitality LP, are consolidated with the Trust, and all significant intercompany transactions and balances have been eliminated.

These condensed consolidated financial statements have been prepared in accordance with the instructions for Form 10-Q and Article 8 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by accounting principles generally accepted in the United States of America (“GAAP”) for complete consolidated financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. Operating results for the six-month period and the three-month period ended July 31, 2013 are not necessarily indicative of the results that may be expected for the Trust’s fiscal year ending January 31, 2014. For further information, refer to the consolidated financial statements and footnotes thereto included in the Trust’s Annual Report on Form 10-K as of and for the year ended January 31, 2013.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

USE OF ESTIMATES

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the condensed consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

The Trust’s operations are affected by numerous factors, including the economy, competition in the hotel industry and the effect of the economy on the travel and hospitality industries. The Trust cannot predict if any of the above items will have a significant impact in the future, nor can it predict what impact, if any, the occurrence of these or other events might have on the Trust’s operations and cash flows. Significant estimates and assumptions made by management include, but are not limited to, the estimated useful lives of long-lived assets and estimates of future cash flows used to test a long-lived asset for recoverability and the fair values of the long-lived assets.

LIQUIDITY

Our principal source of cash to meet our cash requirements, including distributions to our shareholders, is our share of the Partnership’s cash flow, quarterly distributions from Albuquerque, New Mexico property, and through the Partnership and our direct ownership of the Yuma, Arizona property. The Partnership’s principal source of revenue is hotel operations for the one hotel property it owns and quarterly distributions from the Tucson, Arizona and Ontario, California properties. Our liquidity, including our ability to make distributions to our shareholders, will depend upon our ability and the Partnership’s ability to generate sufficient cash flow from hotel operations and to service our debt.

Hotel operations are significantly affected by occupancy and room rates. Occupancy increased from the first six months of fiscal year 2013 to the six months of fiscal year 2014, while rates decreased. Results are also significantly impacted by overall economic conditions and, specifically, conditions in the travel industry. Unfavorable changes in these factors could negatively impact hotel room demand and pricing, which would reduce the Trust’s profit margins on rented studio suites.

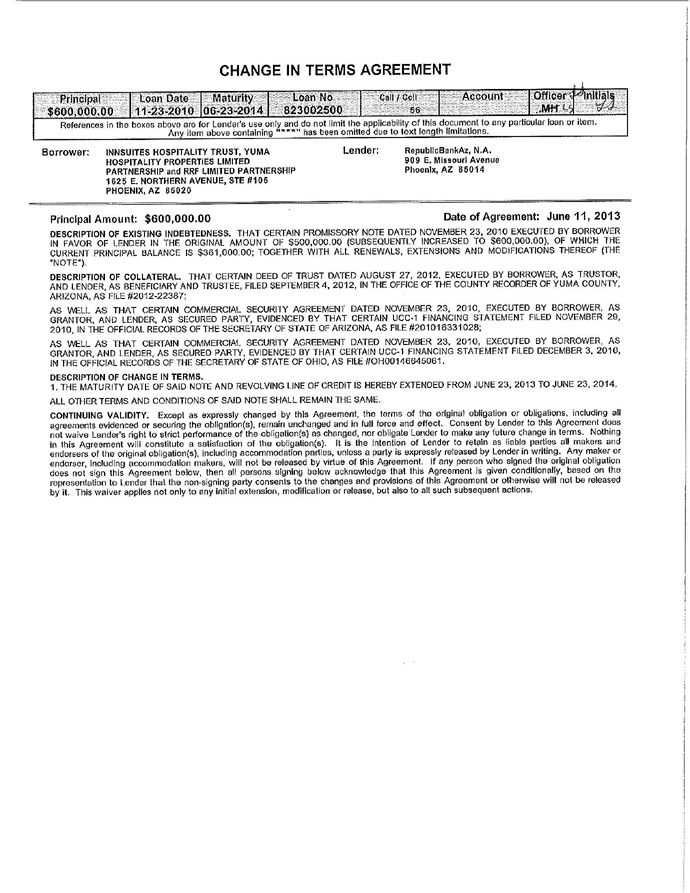

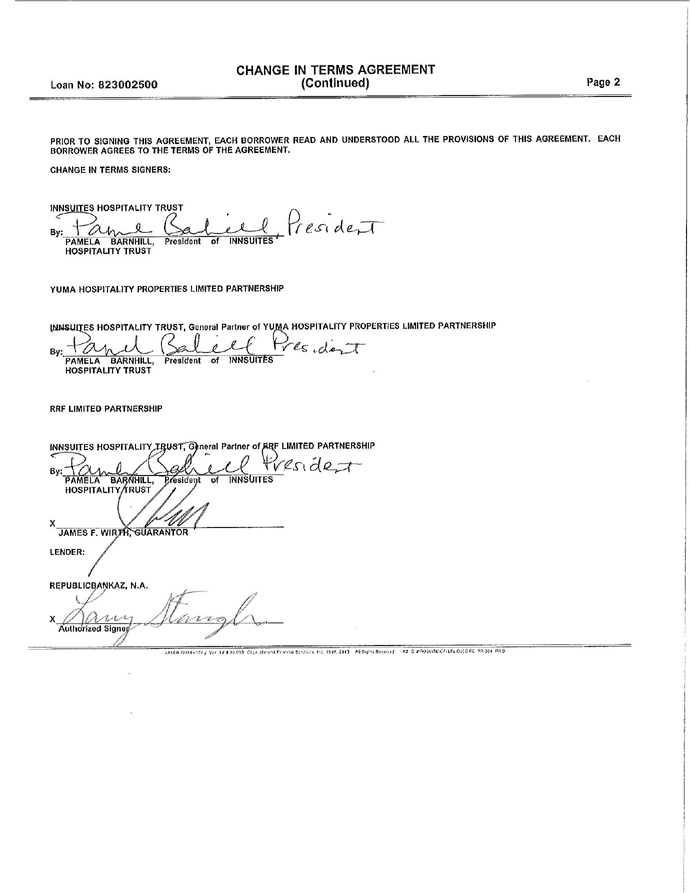

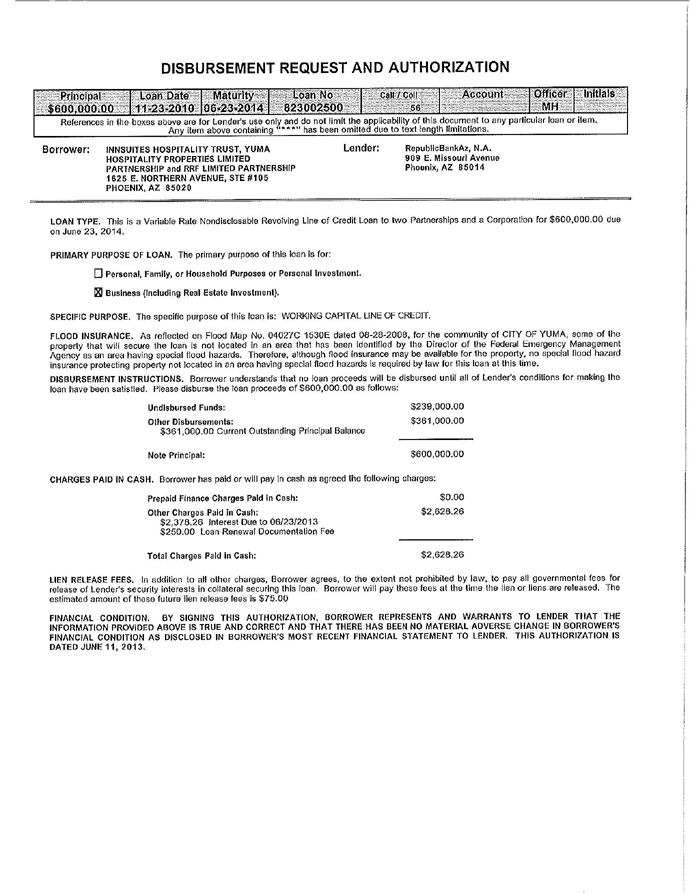

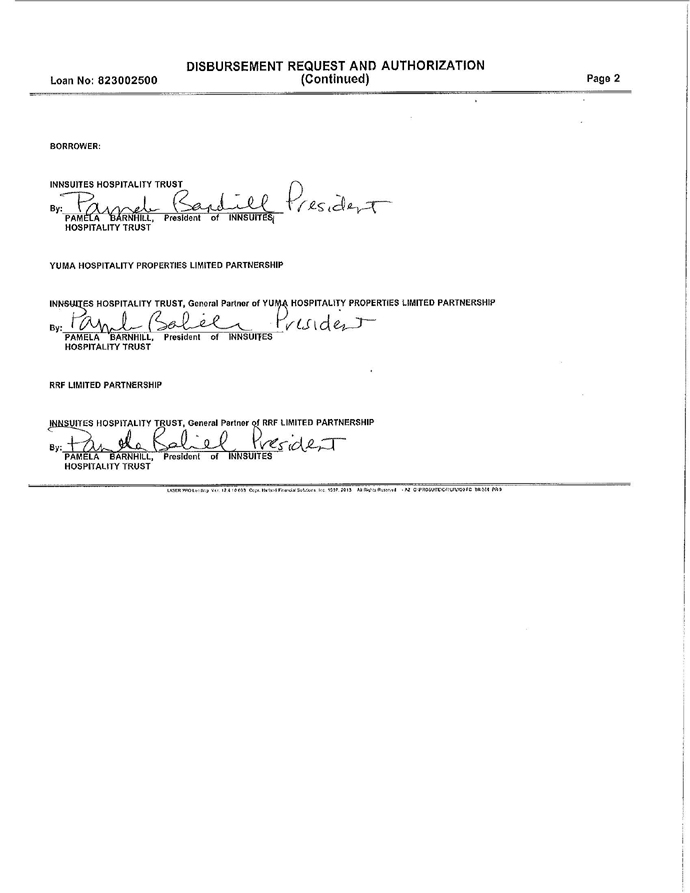

During fiscal year 2014, capital improvements are expected to be reduced by approximately $800,000 from the prior year and we expect increased cash flow from the reduction of principal and interest payments on the Ontario property. Additionally, we have a $600,000 bank line of credit which matures on June 23, 2014. As of July 31, 2013, the Trust had $600,000 drawn on this line of credit.

With the anticipated improved operations income, the expected decrease in capital improvements, and the increased cash flow from the reduction of principal and interest payments on the Ontario property, management believes that it will have enough cash on hand to meet all of our financial obligations as they become due for at least the next year. In addition, our management is analyzing other strategic options available to us, including the refinancing of another property or raising additional funds through additional non-controlling interest sales; however, such transactions may not be available or available on terms that are favorable to the Trust.

We anticipate a moderate improvement in the weak overall economic situation that negatively affected results in fiscal years 2012 and 2013, which could result in higher revenues and operating margins. Challenges in fiscal year 2014 are expected to continue to include continued competition for all types of business in the markets in which we operate and our ability to maintain room rates while maintaining market share.

REVENUE RECOGNITION

Room, food and beverage, management and licensing fees, and other revenue are recognized as earned as services are provided and items are sold. Sales taxes collected are excluded from gross revenue.

INCOME PER SHARE

Basic and diluted income per Share of Beneficial Interest is computed based on the weighted-average number of Shares of Beneficial Interest and potentially dilutive securities outstanding during the period. Dilutive securities are limited to the Class A and Class B units of the Partnership, which are convertible into 3,693,972 shares of the Beneficial Interest, as discussed in Note 1.

For the six month periods ended July 31, 2013 and 2012, there were Class A and Class B Partnership units outstanding, which are convertible into Shares of Beneficial Interest of the Trust. At the beginning of each period, the aggregate weighted-average of these Shares of Beneficial Interest would have been 3,693,972 and 3,694,894 for the quarters ended July 31, 2013 and 2012, respectively. Due to the net losses attributable to controlling interest, these Shares of Beneficial Interest issuable upon conversion of the Class A and Class B Partnership units were anti-dilutive during both six month periods ended July 31, 2013 and 2012. Therefore no reconciliation of basic and diluted income per share is presented.

3. STOCK-BASED COMPENSATION

For the six months ended July 31, 2013, the Trust recognized expenses of $15,480 related to stock-based compensation. The Trust issued 18,000 restricted shares with a total market value of $30,960 in February 2013 as compensation to its three outside Trustees for fiscal year 2014. On a monthly basis, each outside Trustee vests 500 shares.

The following table summarizes restricted share activity during the six months ended July 31, 2013:

|

Restricted Shares |

||||||||

|

Shares |

Weighted-Average Per Share Grant Date Fair Value |

|||||||

|

Balance at January 31, 2013 |

— | — | ||||||

|

Granted |

18,000 | $ | 1.72 | |||||

|

Vested |

(9,000 | ) | $ | 1.72 | ||||

|

Forfeited |

— | — | ||||||

|

Balance of unvested awards at July 31, 2013 |

9,000 | $ | 1.72 | |||||

4. RELATED PARTY TRANSACTIONS

As of July 31, 2013 and 2012, the Trust had notes receivable agreements with Rare Earth Financial, an affiliate of Mr. Wirth. The notes bear interest at 7.0% per annum and are interest only quarterly payments. On July 31, 2013 and 2012, the balance of the notes was $25,000 and $244,573, respectively.

As of July 31, 2013 and 2012, Mr. Wirth and his affiliates held 3,407,938 Class B limited partnership units in the Partnership. As of July 31, 2013 and 2012, Mr. Wirth and his affiliates held 5,573,624 Shares of Beneficial Interest of the Trust.

See Note 6 – “Sale of Membership Interests in Albuquerque Suite Hospitality, LLC”, Note 7 – “Sale of Partnership Interests in Tucson Hospitality Properties, LP” and Note 8 – “Sale of Partnership Interests in Ontario Hospitality Properties, LP” for additional information on related party transactions.

5. NOTE PAYABLE TO BANK

As of July 31, 2013, the Trust has a revolving bank line of credit agreement, with a credit limit of $600,000. The line of credit bears interest at the prime rate plus 1.00% per annum with a 6.0% rate floor, has no financial covenants and matures on June 23, 2014. The line is secured by a junior security interest in the Yuma, Arizona property and the Trust’s trade receivables. Mr. Wirth is a guarantor on the line of credit. The Trust had drawn funds of $600,000 on this line of credit as of July 31, 2013.

6. SALE OF MEMBERSHIP INTERESTS IN ALBUQUERQUE SUITE HOSPITALITY, LLC

As of July 31, 2013, the Trust holds a 50.63% ownership interest, Mr. Wirth and his affiliates hold a 0.12% interest, and other parties hold a 49.25% interest. The Albuquerque entity has minimum preference payments to unrelated unit holders of $137,900, to the Trust of $141,750 and to Rare Earth of $350 per year payable quarterly for calendar years 2014 and 2015.

7. SALE OF PARTNERSHIP INTERESTS IN TUCSON HOSPITALITY PROPERTIES, LP

At July 31, 2013, the Partnership had sold 259 units to unrelated parties at $10,000 per unit totaling $2,590,000. As of July 31, 2013, the Partnership holds a 56.42% ownership interest in the Tucson entity, the Trust holds a 1.70% ownership interest, Mr. Wirth and his affiliates hold a 1.85% interest, and other parties hold a 40.03% interest. The Tucson entity has minimum preference payments to unrelated unit holders of $181,300, to the Trust of $7,700, to the Partnership of $255,500 and to Rare Earth of $8,400 per year payable quarterly for calendar years 2014 and 2015.

8. SALE OF PARTNERSHIP INTERESTS IN ONTARIO HOSPITALITY PROPERTIES, LP

At July 31, 2013, the Partnership had sold 235 units to unrelated parties at $10,000 per unit totaling $2,350,000. As of July 31, 2013, the Partnership holds a 61.55% ownership interest in the Ontario entity, the Trust holds a 0.05% ownership interest, Mr. Wirth and his affiliates hold a 1.57% interest, and other parties hold a 36.83% interest. The Ontario entity has minimum preference payments to unrelated unit holders of $164,500, to the Trust of $210, to the Partnership of $274,890 and to Rare Earth of $7,000 per year payable quarterly for calendar years 2013 and 2014.

9. STATEMENTS OF CASH FLOWS, SUPPLEMENTAL DISCLOSURES

The Trust paid $396,997 and $485,097 in cash for interest for the six months ended July 31, 2013 and 2012, respectively.

During the second quarter of fiscal year 2014, the Trust issued a promissory note for $10,500 to an unrelated third party for the purchase of 5,656 Shares of Beneficial Interest of the Trust shares. The note is due in 24 monthly principal and interest installments of $470 and matures on July 9, 2015 with a down payment of $360.

10. COMMITMENTS AND CONTINGENCIES

Two of the Hotels are subject to non-cancelable ground leases expiring in 2033 and 2050. Total expense associated with the non-cancelable ground leases for the six months ended July 31, 2013 was $144,508, including a variable component based on gross revenues of each property that totaled approximately $47,791

During fiscal year 2010, the Trust entered into a five-year office lease for its corporate headquarters. The Trust recorded $21,470 and $17,237 of general and administrative expense related to the lease during the six-month period ended July 31, 2013 and 2012, respectively. The lease includes a base rent charge of $24,000 for the first lease year with annual increases to a final year base rent of $39,600. Currently our rent is $3,694 per month. The Trust has the option to cancel the lease after each lease year for penalties of four months rent after the first year with the penalty decreasing by one month’s rent each successive lease year. It is the Trust’s intention to remain in the office for the duration of the five-year lease period.

Future minimum lease payments under the non-cancelable ground leases and office lease are as follows:

|

Fiscal Year Ending |

||||

|

Remainder of 2014 |

$ | 127,660 | ||

|

2015 |

233,721 | |||

|

2016 |

212,121 | |||

|

2017 |

212,121 | |||

|

2018 |

212,121 | |||

|

Thereafter |

5,014,895 | |||

|

Total |

$ | 6,012,639 |

The Trust is obligated under loan agreements relating to three of its Hotels to deposit 4% of the individual Hotel’s room revenue into an escrow account to be used for capital expenditures. The escrow funds applicable to the three Hotel properties for which a mortgage lender escrow exists are reported on the Trust’s Condensed Consolidated Balance Sheet as “Restricted Cash.”

The nature of the operations of the Hotels exposes them to risks of claims and litigation in the normal course of their business. Although the outcome of these matters cannot be determined, management does not expect that the ultimate resolution of these matters will have a material adverse effect on the consolidated financial position, results of operations or liquidity of the Trust.

The Trust is involved from time to time in various other claims and legal actions arising in the ordinary course of business. In the opinion of management, the ultimate disposition of these matters will not have a material adverse effect on the Trust’s consolidated financial position, results of operations or liquidity.

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

GENERAL

The following discussion should be read in conjunction with our unaudited condensed consolidated financial statements and notes thereto appearing elsewhere in this Form 10-Q.

We own the sole general partner’s interest in the Partnership. Our principal source of cash to meet our cash requirements, including distributions to our shareholders, is our share of the Partnership’s cash flow, quarterly distributions from the Albuquerque, New Mexico property and through the Partnership and our direct ownership of the Yuma, Arizona property. The Partnership’s principal source of revenue is hotel operations for the one hotel property it owns and quarterly distributions from the Tucson, Arizona and Ontario, California properties.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

In our Annual Report on Form 10-K for the year ended January 31, 2013, we identified the critical accounting policies that affect our more significant estimates and assumptions used in preparing our consolidated financial statements. We believe that the policies we follow for the valuation of our Hotel properties, which constitute the majority of our assets, are our most critical policies. Those policies include methods used to recognize and measure any identified impairment of our Hotel property assets. There have been no material changes to our critical accounting policies since January 31, 2013.

HOTEL PROPERTIES LISTED FOR SALE

Our long-term strategic plan is to obtain the full benefit of our real estate equity and to migrate our focus from a hotel owner to a hospitality service company by expanding our trademark license, management, reservation, and marketing services. This plan is similar to strategies followed by internationally diversified hotel industry leaders, which over the last several years have reduced real estate holdings and concentrated on hospitality services. We began our long-term corporate strategy when we relinquished our REIT income tax status in January 2004, which had previously prevented us from providing management services to hotels. In June 2004, we acquired our trademark license and management agreements and began providing management, trademark and reservations services to our Hotels.

We expect to use proceeds from the sale of the Hotels, if any, as needed to support hospitality service operations as cash flow from current operations, primarily the sale of hotel rooms, declines with the sale of the Hotels.

The table below lists the Hotel properties, their respective carrying and mortgage value and the listed asking price for the hotel properties.

|

Hotel Property Asset Values as of July 31, 2013 |

||||||||||||

|

Hotel Property |

Book Value |

Mortgage Balance |

Listed Asking Price |

|||||||||

|

Albuquerque |

$ | 1,280,638 | $ | 1,178,336 | $ | 5,900,000 | ||||||

|

Ontario |

5,763,036 | 6,149,692 | 15,900,000 | |||||||||

|

Tucson Oracle |

4,077,523 | 1,478,330 | 12,500,000 | |||||||||

|

Tucson City Center |

7,615,414 | 5,133,961 | 9,995,000 | |||||||||

|

Yuma |

5,307,913 | 5,411,855 | 14,000,000 | |||||||||

| $ | 24,044,524 | $ | 19,352,174 | $ | 58,295,000 | |||||||

The listed asking price is the amount at which we would sell each of the Hotels and is based on the original listed selling price adjusted to reflect recent hotel sales in the areas of operation of the Hotels and current earnings of each of the Hotels. The listed asking price is not based on appraisals of the properties.

There is no assurance that the listed sales price for the individual Hotel properties will be realized. However, our management believes that these values are reasonable based on local market conditions and comparable sales. Changes in market conditions have in part resulted, and may in the future result, in our changing one or all of the listed asking prices.

LIQUIDITY AND CAPITAL RESOURCES

Our principal source of cash to meet our cash requirements, including distributions to our shareholders, is our share of the Partnership’s cash flow, quarterly distributions from the Albuquerque, New Mexico property, and through the Partnership and our direct ownership of the Yuma, Arizona property. The Partnership’s principal source of revenue is hotel operations for the one hotel property it owns and quarterly distributions from the Tucson, Arizona and Ontario, California properties. Our liquidity, including our ability to make distributions to our shareholders, will depend upon our ability, and the Partnership’s ability, to generate sufficient cash flow from hotel operations and to service our debt.

Hotel operations are significantly affected by occupancy and room rates at the Hotels. Occupancy increased from the first six months of fiscal year 2013 to the first six months of fiscal year 2014, while rates decreased. We anticipate this trend to continue throughout fiscal year 2014. Results are also significantly impacted by overall economic conditions and, specifically, conditions in the travel industry. Unfavorable changes in these factors could negatively impact hotel room demand and pricing, which would reduce the Trust’s profit margins on rented suites.

We have minimum debt payments of approximately $1.23 million remaining over the last six months of fiscal year 2014 and the first six months of fiscal year 2015. We have a revolving bank line of credit, with a credit limit of $600,000. The line of credit bears interest at the prime rate plus 1.0% per annum, with a 6.0% rate floor, and has no financial covenants. On June 11, 2013, we renewed the line of credit until June 23, 2014. All other terms and conditions remain the same. The line is secured by a junior security interest in the Yuma, Arizona property and our trade receivables. Mr. Wirth is a guarantor on the line of credit. On July 31, 2013, the Trust had drawn $600,000 under the line of credit. The largest outstanding balance on the line of credit during the quarter ended July 31, 2013 was $600,000.

During fiscal year 2014, capital improvements are expected to be reduced by approximately $800,000 from the prior year and we expect increased cash flow from the reduction of principal and interest payments on the Ontario property.

With the expected decrease in capital improvements and increased cash flow from the reduction of principal and interest payments on the Ontario property, management believes that it will have enough cash on hand to meet all of our financial obligations as they become due for the next 12 months. In addition, our management is analyzing other strategic options available to us, including the refinancing of another property or raising additional funds through additional non-controlling interest sales. However, such transactions may not be available on terms that are favorable to us.

We anticipate a moderate improvement in the weak overall economic situation that negatively affected results in fiscal year 2012 and 2013, which could result in higher revenues and operating margins. Challenges in fiscal year 2014 are expected to continue to include continued competition for all types of business in the markets in which we operate and our ability to maintain room rates while maintaining market share.

Net cash provided by operating activities totaled $885,000 and $65,000 for the six months ended July 31, 2013 and 2012, respectively. Partially offset by changes in Accounts Payable, the increase of net cash provided by operating activities during the first six months of fiscal year 2014 compared to the first six months of fiscal year 2013 was due to (a) the improvement in the consolidated net income; (b) the decrease in accounts receivable; and (c) the decrease in prepaid expenses and other assets offset by the increase in accounts payable and accrued expenses. We closely watched our expenses in the first six months of fiscal year 2014 resulting in an improvement in our consolidated net income.

Net cash used in investing activities totaled $278,000 and $858,000 for the six months ended July 31, 2013 and 2012, respectively. The decrease in net cash used in investing activities during the first six months of fiscal year 2014 compared to the first six months of fiscal year 2013 was due to the net decrease in loans made on notes receivables to related parties and the decreased capital refurbishment projects.

Net cash used in financing activities totaled $794,000 for the six months ended July 31, 2013, compared to net cash provided by financing activities of $6,000 for the six months ended July 31, 2012. The net cash used in financing activities for the first six months of fiscal year 2014 as compared the net cash provided in financing activities for the first sixth months of fiscal year 2013 was due to (a) $905,000 decrease in fiscal year 2014 of principal payments of mortgage notes payable; $473,000 increase in payments on notes payable to banks; (c) a $267,000 increase in borrowings on notes payable to banks; (d) a $99,000 decrease in purchase of treasury stock; and (e) a $1,589,000 decrease in proceeds from sale of non-controlling ownership interests in subsidiaries.

As of July 31, 2013, we had no commitments for capital expenditures beyond a 4% reserve for refurbishment and replacements that is set aside annually.

We continue to contribute to a Capital Expenditures Fund (the “Fund”) an amount equal to 4% of the InnSuites Hotels’ revenues from operation of the Hotels. The Fund is restricted by the mortgage lender for four of our properties. As of July 31, 2013, $41,955 was held in these accounts and is reported on our Condensed Consolidated Balance Sheet as “Restricted Cash.” The Fund is intended to be used for capital improvements to the Hotels and refurbishment and replacement of furniture, fixtures and equipment. During the six months ended July 31, 2013 and 2012, the Hotels spent approximately $250,000 and $658,000, respectively, for capital expenditures. We consider the majority of these improvements to be revenue producing. Therefore, these amounts are capitalized and depreciated over their estimated useful lives. The Hotels also spent approximately $606,240 and $767,220 during the six months ended July 31, 2013 and 2012 on repairs and maintenance and these amounts have been charged to expense as incurred.

As of July 31, 2013, we had mortgage notes payable of $19.35 million outstanding with respect to the Hotels, $261,000 in secured promissory notes outstanding to unrelated third parties arising from the Shares of Beneficial Interest and Partnership unit repurchases, $600,000 outstanding under our bank line of credit, and no principal due and payable under notes and advances payable to Mr. Wirth and his affiliates.

We may seek to negotiate additional credit facilities or issue debt instruments. Any debt incurred or issued by us may be secured or unsecured, long-term, medium-term or short-term, bear interest at a fixed or variable rate and be subject to such other terms as we consider prudent.

COMPLIANCE WITH CONTINUED LISTING STANDARDS OF NYSE MKT

On January 8, 2013, the Trust received a letter from the NYSE MKT LLC (f/k/a AMEX) (the "NYSE MKT") informing the Trust that the staff of the NYSE MKT’s Corporate Compliance Department has determined that the Trust is not in compliance with Section 1003(a)(ii) of the NYSE MKT Company Guide due to the Trust having stockholders' equity of less than $4.0 million and losses from continuing operations in three of its four most recent fiscal years.

The Trust was afforded the opportunity to submit a plan of compliance to the NYSE MKT and submitted its plan on February 5, 2013. On March 21, 2013, the NYSE MKT notified the Trust that it accepted the Trust’s plan of compliance and granted the Trust an extension until April 30, 2014 to regain compliance with the continued listing standards.

On May 2, 2013, the Trust received another letter from the NYSE MKT informing the Trust that the Trust is not in compliance with an additional continued listing standard of the NYSE MKT, Section 1003(a)(iii) of the NYSE MKT Company Guide, due to the Trust having stockholders’ equity of less than $6.0 million and net losses in five consecutive fiscal years as of January 31, 2013. The plan submitted in response to the first letter received increased stockholders’ equity in excess of $6.0 million before the April 30, 2014 deadline, therefore the Trust was not required to submit an additional plan to regain compliance with the continued listing standards.

The Trust will be subject to periodic review by the NYSE MKT’s staff during this extension period. Failure to make progress consistent with the plan or to regain compliance with continued listing standards by the end of the extension period could result in the Trust being delisted from the NYSE MKT.

RESULTS OF OPERATIONS

Our expenses consist primarily of hotel operating expenses, property taxes, insurance, corporate overhead, interest on mortgage debt, professional fees and depreciation of the Hotels. Our operating performance is principally related to the performance of the Hotels. Therefore, management believes that a review of the historical performance of the operations of the Hotels, particularly with respect to occupancy, calculated as rooms sold divided by the number of rooms available, average daily rate (“ADR”), calculated as total room revenue divided by number of rooms sold, and revenue per available room (“REVPAR”), calculated as total room revenue divided by the number of rooms available, is appropriate for understanding revenue from the Hotels. Occupancy was 74.72% for the six months ended July 31, 2013, an increase of 6.21% from the prior year period. ADR decreased $2.74, or 4.00%, to $66.84. The increased occupancy and decrease in ADR resulted in an increase of $3.20 in REVPAR to $50.87 from $47.67 in the prior year period. The increase in occupancy is due to the moderately improving trend in our economy.

The following table shows occupancy, ADR and REVPAR for the periods indicated:

|

FOR THE SIX MONTHS ENDED JULY 31, |

||||||||

|

2013 |

2012 |

|||||||

|

OCCUPANCY |

74.72 | % | 68.51 | % | ||||

|

AVERAGE DAILY RATE (ADR) |

$ | 66.84 | $ | 69.58 | ||||

|

REVENUE PER AVAILABLE ROOM (REVPAR) |

$ | 50.87 | $ | 47.67 | ||||

No assurance can be given that the trends reflected in this data will be maintained or improve or that occupancy, ADR or REVPAR will not decrease as a result of changes in national or local economic or hospitality industry conditions. We expect the economic conditions to positively affect our business levels for the remainder of this current fiscal year.

RESULTS OF OPERATIONS FOR THE SIX MONTHS ENDED JULY 31, 2013 COMPARED TO THE SIX MONTHS ENDED JULY 31, 2012

A summary of the operating results for the six months ended July 31, 2013 and 2012 is:

|

2013 |

2012 |

Change |

% Change |

|||||||||||||

|

Total Revenues |

$ | 8,223,210 | $ | 8,191,127 | $ | 32,083 | 0.39 | % | ||||||||

|

Operating Expenses |

$ | 7,755,380 | $ | 7,963,756 | $ | (208,376 | ) | -2.62 | % | |||||||

|

Operating Income |

$ | 467,830 | $ | 227,371 | $ | 240,459 | 105.76 | % | ||||||||

|

Interest Income |

$ | 1,811 | $ | 5,402 | $ | (3,591 | ) | -66.48 | % | |||||||

|

Interest Expense |

$ | 396,997 | $ | 485,097 | $ | (88,100 | ) | -18.16 | % | |||||||

|

Consolidated Net Income (Loss) |

$ | 72,644 | $ | (252,324 | ) | $ | 324,968 | 128.79 | % | |||||||

|

Net Loss Attributable to Controlling Interests |

$ | (231,049 | ) | $ | (221,777 | ) | $ | (9,272 | ) | -4.18 | % | |||||

|

Net Loss Per Share – Basic |

$ | (0.03 | ) | $ | (0.03 | ) | $ | - | 0.00 | % | ||||||

For the six months ended July 31, 2013 compared to our six months ended July 31, 2012, our revenues were $8.223 million, an increase of $32,000 or 0.39%. Revenues from hotel operations increased slightly during the first six months of fiscal year 2014 as compared to the same period during fiscal year 2013 due to higher occupancy as a result of moderately improving economic conditions.

Management closely watched its operating expenses as operating expenses decreased $208,000 during the first six months of fiscal year 2014 as compared to the first six months of fiscal year 2013. The net decrease in operating expenses was due to a decrease in room, food and beverage, telecommunications, sales and marketing, and repairs and maintenance operating expenses. We incurred additional general and administrative expenses during the first six months of fiscal year 2014 as compared to the first six months of fiscal year 2013 but expect a decrease in general and administrative expenses for the remainder of fiscal year 2014.

Operating income was $468,000 for the six months ended July 31, 2013 as compared to $227,000 for the six months ended July 31, 2012, an increase of $240,000. This increase was primarily due to flat revenues and a decrease in operating expenses. Management is continuing its evaluation of its sales and rate management program at the Hotels.

Our interest expense was $397,000 for the first six months of fiscal year 2014 as compared to $485,000 for the first six months of fiscal year 2013 primarily due to the successful debt restructure for our Ontario property.

Consolidated net income was $73,000 for the first six months of fiscal year 2014 and consolidated net loss for the first six months of fiscal year 2013 was ($252,000), an increase of $325,000 or 129%. Net loss attributable to controlling interest slightly increased to ($231,000) during the first six months of fiscal year 2014 as compared to the first six months of fiscal year 2013.

Net loss attributable to controlling interests increased by $9,000 for the six month period ended July 31, 2013 to ($231,000), or ($0.03) per basic share, from ($222,000), or ($0.03) per basic share, during the prior year period. The increase is primarily due to increased ownership in the hotels belonging to non-controlling interest, reducing the income allocated to controlling interests.

RESULTS OF OPERATIONS FOR THE THREE MONTHS ENDED JULY 31, 2013 COMPARED TO THE THREE MONTHS ENDED JULY 31, 2012

A summary of the operating results for the three months ended July 31, 2013 and 2012 is:

|

2013 |

2012 |

Change |

% Change |

|||||||||||||

|

Total Revenues |

$ | 3,427,012 | $ | 3,371,502 | $ | 55,510 | 1.65 | % | ||||||||

|

Operating Expenses |

$ | 3,929,408 | $ | 3,996,471 | $ | (67,063 | ) | -1.68 | % | |||||||

|

Operating Loss |

$ | (502,396 | ) | $ | (624,969 | ) | $ | 122,573 | 19.61 | % | ||||||

|

Interest Income |

$ | 1,803 | $ | 5,294 | $ | (3,491 | ) | -65.94 | % | |||||||

|

Interest Expense |

$ | 209,978 | $ | 277,471 | $ | (67,493 | ) | -24.32 | % | |||||||

|

Consolidated Net Loss |

$ | (710,571 | ) | $ | (897,146 | ) | $ | 186,575 | 20.80 | % | ||||||

|

Net Loss Attributable to Controlling Interests |

$ | (667,057 | ) | $ | (683,865 | ) | $ | 16,808 | 2.46 | % | ||||||

|

Net Loss Per Share – Basic |

$ | (0.08 | ) | $ | (0.08 | ) | $ | - | 0.00 | % | ||||||

For the second quarter of fiscal year 2014, our total revenue was $3.427 million, or 1.65% increase from the second quarter of fiscal year 2013. During the second quarter of fiscal year 2014 compared to the second quarter of fiscal year 2013, Room Revenues increased slightly by $90,000, food and beverage revenues decreased by $38,000 and other and management and trademark fees were relatively flat.

Management closely watched its operating expenses as operating expenses decreased $67,000 during the second quarter of fiscal year 2014 as compared to the second quarter of fiscal year 2013. The net decrease in operating expenses was due to a decrease in food and beverage, sales and marketing, and repairs and maintenance operating expenses saving the trust almost $181,000. The Trust incurred additional general and administrative expenses during the second quarter of fiscal year 2014 as compared to the second quarter of fiscal year 2014 but expects a decrease in general and administrative expenses for the remainder of fiscal year 2014.

Operating loss was ($502,000) for the three months ended July 31, 2013 as compared to ($625,000) for the three months ended July 31, 2012, a decrease of operating loss of $123,000. This decrease in operating loss was primarily due to an increase in revenues and a decrease in operating expenses. Management is continuing its evaluation of its sales and rate management program at the Hotels and is continuing to control operating expenses.

Our interest expense decreased by $67,000 for the three months ended July 31, 2013 as compared to the three months ended July 31, 2012 primarily due to the successful debt restructure for our Ontario property.

Net loss attributable to controlling interests increased by $16,000 or 2.46% for the three month period ended July 31, 2013, to ($667,000) or ($0.08) per basic share, from ($684,000), or ($0.08) per basic share, during the prior year period. While consolidated net loss decreased during the second quarter of fiscal year 2014 as compared to the second quarter of fiscal year 2013, the net loss attributable to controlling interests did not decrease to the same level due to the increased ownership in the Hotels belonging to non-controlling interest, reducing the loss allocated to controlling interests.

NON-GAAP FINANCIAL MEASURES

The following non-GAAP presentations of earnings before interest taxes depreciation and amortization (“EBITDA”) and funds from operations (“FFO”) are made to assist our investors in evaluating our operating performance.

Adjusted EBITDA is defined as earnings before minority interest, interest expense, amortization of loan costs, interest income, income taxes, depreciation and amortization, and non-controlling interests in the Trust. We present Adjusted EBITDA because we believe these measurements (a) more accurately reflect the ongoing performance of our hotel assets and other investments, (b) provide more useful information to investors as indicators of our ability to meet our future debt payment and working capital requirements, and (c) provide an overall evaluation of our financial condition. Adjusted EBITDA as calculated by us may not be comparable to Adjusted EBITDA reported by other companies that do not define Adjusted EBITDA exactly as we define the term. Adjusted EBITDA does not represent cash generated from operating activities determined in accordance with GAAP and should not be considered as an alternative to (a) GAAP net income or loss as an indication of our financial performance or (b) GAAP cash flows from operating activities as a measure of our liquidity.

A reconciliation of Adjusted EBITDA to net loss attributable to controlling interests for the six months and three months ended July 31, 2013, and 2012 follows:

|

Six Months Ended July 31, |

||||||||

|

2013 |

2012 |

|||||||

|

Net loss attributable to controlling interests |

$ | (231,049 | ) | $ | (221,777 | ) | ||

|

Add back: |

||||||||

|

Depreciation |

899,481 | 867,187 | ||||||

|

Interest expense |

396,997 | 485,097 | ||||||

|

Non-controlling interest |

303,693 | (30,547 | ) | |||||

|

Less: |

||||||||

|

Interest income |

1,811 | 5,402 | ||||||

|

ADJUSTED EBITDA |

$ | 1,367,311 | $ | 1,094,558 | ||||

|

Three Months Ended July 31, |

||||||||

|

2013 |

2012 |

|||||||

|

Net loss attributable to controlling interests |

$ | (667,057 | ) | $ | (683,865 | ) | ||

|

Add back: |

||||||||

|

Depreciation |

444,850 | 433,530 | ||||||

|

Interest expense |

209,978 | 277,471 | ||||||

|

Non-controlling interest |

(43,514 | ) | (213,281 | ) | ||||

|

Less: |

||||||||

|

Interest income |

1,803 | 5,294 | ||||||

|

ADJUSTED EBITDA |

$ | (57,546 | ) | $ | (191,439 | ) | ||

FFO is calculated on the basis defined by the National Association of Real Estate Investment Trusts (“NAREIT”), which is net income (loss) attributable to common shareholders, computed in accordance with GAAP, excluding gains or losses on sales of properties, asset impairment adjustments, and extraordinary items as defined by GAAP, plus depreciation and amortization of real estate assets, and after adjustments for unconsolidated joint ventures and noncontrolling interests in the operating partnership. NAREIT developed FFO as a relative measure of performance of an equity REIT to recognize that income-producing real estate historically has not depreciated on the basis determined by GAAP. The Trust is an unincorporated Ohio real estate investment trust; however, the Trust is not a real estate investment trust for federal taxation purposes. Management uses this measurement to compare itself to REITs with similar depreciable assets. We consider FFO to be an appropriate measure of our ongoing normalized operating performance. We compute FFO in accordance with our interpretation of standards established by NAREIT, which may not be comparable to FFO reported by other companies that either do not define the term in accordance with the current NAREIT definition or interpret the NAREIT definition differently than us. FFO does not represent cash generated from operating activities as determined by GAAP and should not be considered as an alternative to (a) GAAP net income or loss as an indication of our financial performance or (b) GAAP cash flows from operating activities as a measure of our liquidity, nor is it indicative of funds available to satisfy our cash needs, including our ability to make cash distributions. However, to facilitate a clear understanding of our historical operating results, we believe that FFO should be considered along with our net income or loss and cash flows reported in the consolidated financial statements.

A reconciliation of FFO to net loss attributable to controlling interests for the six months and three months ended July 31, 2013 and 2012 follows:

Six Months Ended July 31, 2013 2012 Net loss attributable to controlling interest Add back: Gains/Losses on Sales of Hotel Property Asset Impairment adjustments Extraordinary items Depreciation Non-controlling interest FFO Three Months Ending July 31, 2013 2012 Net loss attributable to controlling interest Add back: Gains/Losses on Sales of Hotel Property Asset Impairment adjustments Extraordinary items Depreciation Non-controlling interest FFO

$

(231,049

)

$

(221,777

)

6,533

-

-

-

-

-

899,481

867,187

303,693

(30,547

)

$

978,658

$

614,863

$

(667,057

)

$

(683,865

)

4,369

-

-

-

-

-

444,850

433,530

(43,514

)

(213,281

)

$

(261,352

)

$

(463,616

)

OFF-BALANCE SHEET FINANCINGS AND LIABILITIES

Other than lease commitments and legal contingencies incurred in the normal course of business, we do not have any off-balance sheet financing arrangements or liabilities. We do not have any majority-owned subsidiaries that are not included in our condensed consolidated financial statements.

SEASONALITY

The Hotels’ operations historically have been seasonal. The three southern Arizona hotels experience their highest occupancy in the first fiscal quarter and, to a lesser extent, the fourth fiscal quarter. The second fiscal quarter tends to be the lowest occupancy period at those three southern Arizona hotels. This seasonality pattern can be expected to cause fluctuations in the Trust’s quarterly revenues. The two hotels located in California and New Mexico historically experience their most profitable periods during the second and third fiscal quarters (the summer season), providing some balance to the general seasonality of the Trust’s hotel business.

The seasonal nature of the Trust’s business increases its vulnerability to risks such as labor force shortages and cash flow issues. Further, if an adverse event such as an actual or threatened terrorist attack, international conflict, data breach, regional economic downturn or poor weather conditions should occur during the first or fourth fiscal quarters, the adverse impact to the Trust’s revenues could likely be greater as a result of its southern Arizona seasonal business.

FORWARD-LOOKING STATEMENTS

Certain statements in this Form 10-Q, including statements containing the phrases “believes,” “intends,” “expects,” “anticipates,” “predicts,” “projects,” “will be,” “should be,” “looking ahead,” “may” or similar words, constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We intend that such forward-looking statements be subject to the safe harbors created by such Acts. These forward-looking statements include statements regarding our intent, belief or current expectations, those of our Trustees or our officers in respect of (i) the declaration or payment of dividends; (ii) the leasing, management or operation of the Hotels; (iii) the adequacy of reserves for renovation and refurbishment; (iv) our financing plans; (v) our position regarding investments, acquisitions, developments, financings, conflicts of interest and other matters; (vi) our plans and expectations regarding future sales of hotel properties; and (vii) trends affecting our or any Hotel’s financial condition or results of operations.

These forward-looking statements reflect our current views in respect of future events and financial performance, but are subject to many uncertainties and factors relating to the operations and business environment of the Hotels that may cause our actual results to differ materially from any future results expressed or implied by such forward-looking statements. Examples of such uncertainties include, but are not limited to:

|

● |

local, national or international economic and business conditions, including, without limitation, conditions that may, or may continue to, affect public securities markets generally, the hospitality industry or the markets in which we operate or will operate; |

|

● |

fluctuations in hotel occupancy rates; |

|

● |

changes in room rental rates that may be charged by InnSuites Hotels in response to market rental rate changes or otherwise; |

|

● |

seasonality of our business; |

|

● |

our ability to sell any of our Hotels at market value, listed sale price or at all; |

|

● |

interest rate fluctuations; |

|

● |

changes in governmental regulations, including federal income tax laws and regulations; |

|

● |

competition; |

|

● |

any changes in our financial condition or operating results due to acquisitions or dispositions of hotel properties; |

|

● |

insufficient resources to pursue our current strategy; |

|

● |

concentration of our investments in the InnSuites Hotels® brand; |

|

● |

loss of membership contracts; |

|

● |

real estate and hospitality market conditions; |

|

● |

hospitality industry factors; |

|

● |

the Trust’s ability to remain listed on the NYSE MKT; |

|

● |

effectiveness of the Trust’s software program; |

|

● |

availability of credit or other financing; |

|

● |

our ability to meet present and future debt service obligations; |

|

● |

our inability to refinance or extend the maturity of indebtedness at, prior to, or after the time it matures; |

|

● |

terrorist attacks or other acts of war; |

|

● |

outbreaks of communicable diseases; |

|

● |

natural disasters; |

|

● |

data breaches; and |

|

● |

loss of key personnel. |

We do not undertake any obligation to update publicly or revise any forward-looking statements whether as a result of new information, future events or otherwise. Pursuant to Section 21E(b)(2)(E) of the Securities Exchange Act of 1934, as amended, the qualifications set forth hereinabove are inapplicable to any forward-looking statements in this Form 10-Q relating to the operations of the Partnership.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not required for smaller reporting companies.

ITEM 4. CONTROLS AND PROCEDURES

Evaluation of Disclosure Controls and Procedures

As of the end of the period covered by this report, we conducted an evaluation under the supervision and with the participation of our management, including our principal executive officer and principal financial officer, of the effectiveness of the design and operation of our disclosure controls and procedures. The term "disclosure controls and procedures," as defined in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934, as amended (the "Exchange Act"), means controls and other procedures of a company that are designed to ensure that information required to be disclosed by the company in the reports it files or submits under the Exchange Act is recorded, processed, summarized and reported, within the time periods specified in the SEC's rules and forms. Based on this evaluation, our principal executive officer and our principal financial officer concluded that our disclosure controls and procedures were effective as of July 31, 2013.

Our management, including our principal executive officer and principal financial officer, does not expect that our disclosure controls and procedures or our internal controls will prevent all errors or fraud. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints and the benefits of controls must be considered relative to their costs. Due to the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, have been detected.

Changes in Internal Control over Financial Reporting

There were no changes in our internal control over financial reporting during our most recently completed fiscal quarter that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

PART II

OTHER INFORMATION

ITEM 1. LEGAL PROCEEDINGS

See Note 10 to the notes to unaudited condensed consolidated financial statements.

ITEM 1A. RISK FACTORS

Not required for smaller reporting companies.

ITEM 2. UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS

On January 2, 2001, the Board of Trustees approved a share repurchase program under Rule 10b-18 of the Securities Exchange Act of 1934, as amended, for the purchase of up to 250,000 limited partnership units in the Partnership and/or Shares of Beneficial Interest in open market or privately negotiated transactions. On September 10, 2002, August 18, 2005 and September 10, 2007, the Board of Trustees approved the purchase of up to 350,000 additional limited partnership units in the Partnership and/or Shares of Beneficial Interest in open market or privately negotiated transactions. Additionally, on January 5, 2009, September 15, 2009, January 31, 2010 and September 17, 2012, the Board of Trustees approved the purchase of up to 300,000, 250,000, 350,000 and 250,000 respectively, additional limited partnership units in the Partnership and/or Shares of Beneficial Interest in open market or privately negotiated transactions. Acquired Shares of Beneficial Interest will be held in treasury and will be available for future acquisitions and financings and/or for awards granted under the InnSuites Hospitality Trust 1997 Stock Incentive and Option Plan. During the six months ended July 31, 2013, the Trust acquired 21,219 Shares of Beneficial Interest in open and private market transactions at an average price of $1.90 per share. The average price paid includes brokerage commissions. The Trust intends to continue repurchasing Shares of Beneficial Interest in compliance with applicable legal and NYSE MKT requirements. The Trust remains authorized to repurchase an additional 257,601 limited partnership units and/or Shares of Beneficial Interest pursuant to the publicly announced share repurchase program, which has no expiration date.

Issuer Purchases of Equity Securities Period Total Number of Shares Purchased Average Price Paid per Share Total Number of Shares Purchased as Part of Publicly Announced Plans Maximum Number of Shares that May Be Yet Purchased Under the Plan May 1- May 31, 2013 June 1 - June 30, 2013 July 1- July 31, 2013

1,500

$

1.97

1,500

265,457

5,656

$

1.92

5,656

259,801

2,200

$

1.77

2,200

257,601

ITEM 3. DEFAULTS UPON SENIOR SECURITIES

None.

ITEM 4. MINE SAFETY DISCLOSURES

None.

ITEM 5. OTHER INFORMATION

None.

ITEM 6. EXHIBITS

|

Exhibit No. |

|

Exhibit |

|

10.1 |

Changes in Terms Agreement for Bank Line of Credit, dated as of June 11, 201, executed by InnSuites Hospitality Trust, Yuma Hospitality Properties Limited Partnership and RRF Limited Partnership, as Borrowers, and James F. Wirth, as Guarantor, in favor of RepublicBankAZ, N.A., as Lender | |

|

31.1 |

Section 302 Certification By Chief Executive Officer | |

|

31.2 |

Section 302 Certification By Chief Financial Officer | |

|

32.1 |

Section 906 Certification of Principal Executive Officer and Principal Financial Officer | |

|

101 |

XBRL Exhibits * | |

|

101.INS |

XBRL Instance Document* | |

|

101.SCH |

XBRL Schema Document* | |

|

101.CAL |

XBRL Calculation Linkbase Document* | |

|

101.LAB |

XBRL Labels Linkbase Document* | |

|

101.PRE |

XBRL Presentation Linkbase Document* | |

|

101.DEF |

XBRL Definition Linkbase Document* |

* In accordance with Rule 406T of Regulation S-T, the XBRL related information in Exhibit 101 to this Quarterly Report on Form 10-Q shall not be deemed “filed” for purposes of Section 18 of the Exchange Act, or otherwise subject to the liability of that section, and shall not be part of any registration or other document filed under the Securities Act or the Exchange Act, except as shall be expressly set forth by specific reference in such filing.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

|

INNSUITES HOSPITALITY TRUST | ||||

|

Dated: |

September 11, 2013 |

/s/ James F. Wirth |

||

|

James F. Wirth | ||||

|

Chairman and Chief Executive Officer | ||||

|

Dated: |

September 11, 2013 |

/s/ Adam B. Remis |

||

|

Adam B. Remis | ||||

|

Chief Financial Officer | ||||

22

Exhibit 10.1

Exhibit 31.1

CERTIFICATION BY CHIEF EXECUTIVE OFFICER

I, James F. Wirth, certify that:

1. I have reviewed this quarterly report on Form 10-Q of InnSuites Hospitality Trust;

2. Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report;

3. Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this report;

4. The registrant’s other certifying officer and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) and internal control over financial reporting (as defined in Exchange Act Rules 13a-15(f) and 15d-15(f)) for the registrant and have:

(a) Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared;

(b) Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles;

(c) Evaluated the effectiveness of the registrant’s disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this report based on such evaluation; and

(d) Disclosed in this report any change in the registrant’s internal control over financial reporting that occurred during the registrant’s most recent fiscal quarter (the registrant’s fourth fiscal quarter in the case of an annual report) that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and

5. The registrant’s other certifying officer and I have disclosed, based on our most recent evaluation of internal control over financial reporting, to the registrant’s auditors and the audit committee of registrant’s board of directors (or persons performing the equivalent functions):

(a) All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the registrant’s ability to record, process, summarize and report financial information; and

(b) Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant’s internal control over financial reporting.

|

Date: September 11, 2013 |

||||

|

/s/ James F. Wirth |

||||

|

James F. Wirth |

||||

|

Chairman and Chief Executive Officer |

||||

Exhibit 31.2

CERTIFICATION BY CHIEF FINANCIAL OFFICER

I, Adam B. Remis, certify that:

1. I have reviewed this quarterly report on Form 10-Q of InnSuites Hospitality Trust;

2. Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report;

3. Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this report;

4. The registrant’s other certifying officer and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) and internal control over financial reporting (as defined in Exchange Act Rules 13a-15(f) and 15d-15(f)) for the registrant and have:

(a) Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared;

(b) Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles;