UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

[X]

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2011

or

|

[_]

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from _____________________________ to _____________________________

Commission file number: 0-18953

AAON, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 87-0448736 |

|

(State or other jurisdiction

|

(IRS Employer

|

| of incorporation or organization) | Identification No.) |

| 2425 South Yukon, Tulsa, Oklahoma | 74107 |

| (Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code: (918) 583-2266

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $.004

(Title of Class)

Rights to Purchase Series A Preferred Stock

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

[_] Yes [X] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

[_] Yes [X] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

[X] Yes [_] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

[X] Yes [_] No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

[X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934).

| Large accelerated filer [_] | Accelerated filer [X] |

| Non-accelerated filer [_] | Smaller reporting company [_] |

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Act.)

[_] Yes [X] No

The aggregate market value of the common equity held by non-affiliates computed by reference to the closing price of registrant’s common stock on the last business day of registrant’s most recently completed second quarter (June 30, 2011) was $404.5 million.

As of February 29, 2012, registrant had outstanding a total of 24,574,058 shares of its $.004 par value Common Stock.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of registrant's definitive Proxy Statement to be filed in connection with the Annual Meeting of Stockholders to be held May 15, 2012, are incorporated into Part III.

| TABLE OF CONTENTS | ||||

| Item Number and Caption |

Page

Number |

|||

| PART I | ||||

| 1. | Business. | 1 | ||

| 1A. | Risk Factors. | 4 | ||

| 1B. | Unresolved Staff Comments. | 6 | ||

| 2. | Properties. | 6 | ||

| 3. | Legal Proceedings. | 7 | ||

| 4. | Mine Safety Disclosure. | 7 | ||

| PART II | ||||

| 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. | 7 | ||

| 6. | Selected Financial Data. | 10 | ||

| 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations. | 10 | ||

| 7A. | Quantitative and Qualitative Disclosures About Market Risk. | 19 | ||

| 8. | Financial Statements and Supplementary Data. | 19 | ||

| 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure. | 19 | ||

| 9A. | Controls and Procedures. | 20 | ||

| 9B. | Other Information. | 22 | ||

| PART III | ||||

| 10. | Directors, Executive Officers and Corporate Governance. | 22 | ||

| 11. | Executive Compensation. | 22 | ||

| 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. | 22 | ||

| 13. | Certain Relationships and Related Transactions. | 22 | ||

| 14. | Principal Accountant Fees and Services. | 22 | ||

|

PART IV

|

||||

| 15. | Exhibits and Financial Statement Schedules. | 23 | ||

Forward-Looking Statements

This Annual Report includes “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “seeks”, “estimates”, “should”, “will”, and variations of such words and similar expressions are intended to identify such forward-looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions, which are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they are made. We undertake no obligations to update publicly any forward-looking statements, whether as a result of new information, future events or otherwise. Important factors that could cause results to differ materially from those in the forward-looking statements include (1) the timing and extent of changes in raw material and component prices, (2) the effects of fluctuations in the commercial/industrial new construction market, (3) the timing and extent of changes in interest rates, as well as other competitive factors during the year, and (4) general economic, market or business conditions.

PART I

Item 1. Business.

General Development and Description of Business

AAON, Inc., a Nevada corporation, was incorporated on August 18, 1987. We have two operating subsidiaries, AAON, Inc., an Oklahoma corporation and AAON Coil Products, Inc., a Texas corporation. Unless the context otherwise requires, references in this Annual Report to “AAON,” the “Company”, “we”, “us”, “our”, or “ours” refer to AAON, Inc., and our subsidiaries.

We are engaged in the manufacture and sale of air-conditioning and heating equipment. Our products consist of rooftop units, chillers, air-handling units, make-up air units, heat recovery units, condensing units, commercial self contained units and coils.

Products and Markets

Our products serve the commercial and industrial new construction and replacement markets. To date, our sales have been primarily to the domestic market. Foreign sales accounted for approximately 5% of our sales in 2011.

Our rooftop and condenser markets consist of units installed on commercial or industrial structures of generally less than 10 stories in height. Our air-handling units, commercial self-contained units, chillers, and coils are applicable to all sizes of commercial and industrial buildings.

The size of these markets is determined primarily by the number of commercial and industrial building completions. The replacement market consists of products installed to replace existing units/components that are worn or damaged. Historically, approximately half of the industry's market has consisted of replacement units.

The commercial and industrial new construction market is subject to cyclical fluctuations in that it is generally tied to housing starts, but has a lag factor of 6-18 months. Housing starts, in turn, are affected by such factors as interest rates, the state of the economy, population growth and the relative age of the population. When new construction is down, we emphasize the replacement market.

Based on our 2011 level of sales of $266 million, we estimate that we have approximately a 14% plus share of the rooftop market and a 1% share of the coil market. Approximately 55% of our sales were generated from the sale to the renovation and replacement markets and 45% from new construction. The percentage of sales for new construction vs. replacement to particular customers is related to the customer’s stage of development.

1

We purchase certain components, fabricate sheet metal and tubing and then assemble and test the finished products. Our primary finished products consist of a single unit system containing heating, cooling and/or heat recovery components in a self-contained cabinet, referred to in the industry as "unitary" products. Our other finished products are chillers, coils, air-handling units, condensing units, make-up air units, heat recovery units and commercial self-contained units.

We offer four groups of rooftop units. The RQ Series consisting of six cooling sizes ranging from one to six tons; the RN Series offered in 18 cooling sizes ranging from six to 70 tons, and an expansion of the RN series will be introduced in 2012 that will increase the cooling range up to 140 tons and the number of cooling sizes from 18 to 26. The RL Series, which is offered in 15 cooling sizes ranging from 40 to 230 tons; and the HA Series, which is a horizontal discharge package for either rooftop or ground installation offered in eight sizes ranging from seven and one-half to 50 tons. We also offer the SA and SB models as an indoor package water cooled units with cooling capacities of 2 to 70 tons.

We manufacture a Model LC Chiller, air cooled, and a Model LL chiller, which is available in both air-cooled condensing and evaporative cooled configurations covering a range of 3 to 540 tons.

Our air-handling units consist of the F1 and H3/V3 Series and the modular (M2 and M3) Series as well as air handling unit versions of the RN, RL and SA units.

Our heat recovery option applicable to our RQ, RN and RL units, as well as our M2 and M3 Series air handlers, respond to the U.S. Clean Air Act mandate to increase fresh air in commercial structures. Our products are designed to compete on the higher quality end of standardized products.

Performance characteristics of our products range in cooling capacity from 1½ to 540 tons and in heating capacity from 69,000 - 9,000,000 BTU's. All of our products meet the Department of Energy's minimum efficiency standards, which define the maximum amount of energy to be used in producing a given amount of cooling. Many of our units far exceed these minimum standards and are among the highest efficiency units currently available.

A typical commercial building installation requires a ton of air-conditioning for every 300-400 square feet or, for a 100,000 square foot building, 250 tons of air-conditioning, which can involve multiple units

Major Customers

No customer accounted for 10% of our sales during 2011, 2010 or 2009.

Sources and Availability of Raw Materials

The most important materials we purchase are steel, copper and aluminum, which are obtained from domestic suppliers. We also purchase from other domestic manufacturers certain components, including compressors, electric motors and electrical controls used in our products. We attempt to obtain the lowest possible cost in our purchases of raw materials and components, consistent with meeting specified quality standards. We are not dependent upon any one source for raw materials or the major components of our manufactured products. By having multiple suppliers, we believe that we will have adequate sources of supplies to meet our manufacturing requirements for the foreseeable future.

We attempt to limit the impact of increases in raw materials and purchased component prices on our profit margins by negotiating with each of our major suppliers on a term basis from six months to one year.

Distribution

We employ a sales staff of 20 individuals and utilize approximately 93 independent manufacturer representatives (“Representatives”) organizations having 108 offices to market our products in the United States and Canada. We also have one international sales organization, which utilizes 12 distributors in other countries. Sales are made directly to the contractor or end user, with shipments being made from our Tulsa, Oklahoma and Longview, Texas plants to the job site.

2

Our products and sales strategy focus on niche markets. The targeted markets for our equipment are customers seeking products of better quality than offered, and/or options not offered, by standardized manufacturers.

To support and service our customers and the ultimate consumer, we provide parts availability through our sales offices and have factory service organizations at each of our plants. Also, a number of the manufacturer representatives we utilize have their own service organizations, which, in connection with us, provide the necessary warranty work and/or normal service to customers.

Our product warranty policy is: the earlier of one year from the date of first use or 18 months from date of shipment for parts only; an additional four years for compressors (if applicable); 15 years on aluminized steel gas-fired heat exchangers (if applicable); 25 years on stainless steel heat exchangers (if applicable); and 10 years on gas-fired heat exchangers in RL products (if applicable). With the introduction of the RQ product line in 2010, our warranty policy for the RQ series was implemented to cover parts for two years from date of unit shipment and labor for one year from date of unit shipment.

Research and Development

The ability to successfully bring new products to market that meet new energy efficiency standards, environmental regulations, and are engineered for performance, flexibility, and serviceability in a timely manner has rapidly become a critical factor in competing in the heating, ventilation and air conditioning (“HVAC”) equipment industry. We must continually develop new and improved products in order to compete effectively and to meet evolving regulatory standards in all of our major product lines.

All of our R&D activities are self-sponsored, rather than customer-sponsored. R&D has involved the RQ, RN and RL (rooftop units), F1, H/V, M2 and M3 (air handlers), LC and LL (chillers), CB and CC (condensing units), SA (commercial self-contained units) and BL (boilers), as well as component evaluation and refinement, development of control systems and new product development. We incurred research and development expenses of approximately $4.8 million, $3.6 million and $3.1 million in 2011, 2010 and 2009, respectively.

Backlog

Our current backlog as of March 1, 2012 was approximately $55.3 million compared to approximately $37.9 million as of March 1, 2011. The current backlog consists of orders considered by management to be firm and generally are filled on average within approximately 60 days to 92 days after an order is deemed to become firm; however, the orders are subject to cancellation by the customers.

Working Capital Practices

Working capital practices in the industry center on inventories and accounts receivable. Our management regularly reviews our working capital with a view of maintaining the lowest level consistent with requirements of anticipated levels of operation. Our greatest needs arise during the months of July - November, the peak season for inventory (primarily purchased material) and accounts receivable. Our working capital requirements are generally met by cash flow from operations and a bank revolving credit facility, which currently permits borrowings up to $30 million. We believe that we will have sufficient funds available to meet our working capital needs for the foreseeable future. We expect to renew our revolving credit agreement in July 2012.

Seasonality

Sales of our products are moderately seasonal with the peak period being July - November of each year.

3

Competition

In the standardized market, we compete primarily with Lennox International, Inc., Ingersoll Rand Limited, Johnson Controls Inc. and United Technologies Corporation. All of these competitors are substantially larger and have greater resources than we do. In the custom market, we compete with many larger and smaller manufacturers. Our products compete on the basis of total value, quality, function, serviceability, efficiency, availability of product, product line recognition and acceptability of sales outlet. However, in new construction where the contractor is the purchasing decision maker, we are often at a competitive disadvantage because of the emphasis placed on initial cost. In the replacement market and other owner-controlled purchases, we have a better chance of getting the business since quality and long-term cost are generally taken into account.

Employees

As of March 1, 2012, we employed approximately 1,491 permanent employees and 15 temporary employees. Our employees are not currently represented by unions. Management considers relations with our employees to be good.

Patents, Trademarks, Licenses and Concessions

We do not consider any patents, trademarks, licenses or concessions to be material to our business operations, other than patents issued regarding our heat recovery wheel option, blower, gas-fired heat exchanger and evaporative condenser desuperheater which have terms of twenty years with expiration dates ranging from 2016 to 2022.

Environmental Matters

Laws concerning the environment that affect or could affect our domestic operations include, among others, the Clean Water Act, the Clean Air Act, the Resource Conservation and Recovery Act, the Occupational Safety and Health Act, the National Environmental Policy Act, the Toxic Substances Control Act, regulations promulgated under these Acts, and any other federal, state or local laws or regulations governing environmental matters. We believe that we are in compliance with these laws and that future compliance will not materially affect our earnings or competitive position.

Available Information

Our Internet website address is http://www.aaon.com. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act of 1934 will be available through our Internet website as soon as reasonably practical after we electronically file such material with, or furnish it to, the SEC.

Item 1A. Risk Factors.

The following risks and uncertainties may affect our performance and results of operations.

Our business has been hurt by the current economic downturn.

Our business is affected by a number of economic factors, including the level of economic activity in the markets in which we operate. The state of the United States economy has negatively impacted the commercial and industrial new construction markets. The current decline in economic activity in the United States could materially affect our financial condition and results of operations. Sales in the commercial and industrial new construction markets correlate closely to the number of new homes and buildings that are built, which in turn is influenced by cyclical factors such as interest rates, inflation, consumer spending habits, employment rates and other macroeconomic factors over which we have no control. In the heating, ventilation, and air conditioning (“HVAC”) business, a decline in economic activity as a result of these cyclical or other factors typically results in a decline in new construction and replacement purchases, which has resulted in a decrease in our sales volume and profitability.

4

We may be adversely affected by problems in the availability, or increases in the prices, of raw materials and components.

Problems in the availability, or increases in the prices, of raw materials or components could depress our sales or increase the costs of our products. We are dependent upon components purchased from third parties, as well as raw materials such as steel, copper and aluminum. We enter into cancelable and noncancelable contracts on terms from six months to one year for raw materials and components at fixed prices. However, if a key supplier is unable or unwilling to meet our supply requirements, we could experience supply interruptions or cost increases, either of which could have an adverse effect on our gross profit.

We risk having losses resulting from the use of non-cancelable fixed price contracts.

Historically, we attempted to limit the impact of price fluctuations on commodities by entering into non-cancelable fixed price contracts with our major suppliers for periods of 6 - 18 months. We expect to receive delivery of raw materials from our fixed price contracts for use in our manufacturing operations. These fixed price contracts are not accounted for as derivative instruments since they meet the normal purchases and sales exemption.

We may not be able to successfully develop and market new products.

Our future success will depend upon our continued investment in research and new product development and our ability to continue to realize new technological advances in the HVAC industry. Our inability to continue to successfully develop and market new products or our inability to achieve technological advances on a pace consistent with that of our competitors could lead to a material adverse effect on our business and results of operations.

We may incur material costs as a result of warranty and product liability claims that would negatively affect our profitability.

The development, manufacture, sale and use of our products involve a risk of warranty and product liability claims. Our product liability insurance policies have limits that, if exceeded, may result in material costs that would have an adverse effect on our future profitability. In addition, warranty claims are not covered by our product liability insurance and there may be types of product liability claims that are also not covered by our product liability insurance.

We may not be able to compete favorably in the highly competitive HVAC business.

Competition in our various markets could cause us to reduce our prices or lose market share, or could negatively affect our cash flow, which could have an adverse effect on our future financial results. Substantially all of the markets in which we participate are highly competitive. The most significant competitive factors we face are product reliability, product performance, service and price, with the relative importance of these factors varying among our product line. Other factors that affect competition in the HVAC market include the development and application of new technologies and an increasing emphasis on the development of more efficient HVAC products. Moreover, new product introductions are an important factor in the market categories in which our products compete. Several of our competitors have greater financial and other resources than we have, allowing them to invest in more extensive research and development. We may not be able to compete successfully against current and future competition and current and future competitive pressures faced by us may materially adversely affect our business and results of operations.

The loss of Norman H. Asbjornson could impair the growth of our business.

Norman H. Asbjornson, our founder, has served as our President and Chief Executive Officer from inception to date. He has provided the leadership and vision for our growth. Although important responsibilities and functions have been delegated to other highly experienced and capable management personnel, our products are technologically advanced and well positioned for sales into the future and we carry key man insurance on Mr. Asbjornson, his death, disability or retirement could impair the growth of our business. We do not have an employment agreement with Mr. Asbjornson.

5

Our stockholder rights plan and some provisions in our bylaws and Nevada law could delay or prevent a change in control.

Our stockholder rights plan and some provisions in our bylaws and Nevada law could delay or prevent a change in control, which could adversely affect the price of our common stock.

Our business is subject to the risks of interruptions by problems such as computer viruses.

Despite our implementation of network security measures, our services are vulnerable to computer viruses, break-ins and similar disruptions from unauthorized tampering with our computer systems. Any such event could have a material adverse affect on our business.

Exposure to environmental liabilities could adversely affect our results of operations.

Our future profitability could be adversely affected by current or future environmental laws. We are subject to extensive and changing federal, state and local laws and regulations designed to protect the environment in the United States and in other parts of the world. These laws and regulations could impose liability for remediation costs and result in civil or criminal penalties in case of non-compliance. Compliance with environmental laws increases our costs of doing business. Because these laws are subject to frequent change, we are unable to predict the future costs resulting from environmental compliance.

Extreme governmental regulations.

We always face the possibility of new governmental regulations which could have a substantial or even extreme negative effect on our operations and profitability. Specifically, Final Rule, Regulatory Identification No. 1904-AC23, published on March 7, 2011, which, if fully implemented subsequent to the current suspense date of January 1, 2013, would have highly detrimental consequences to all industries involving sales of energy using products by imposing burdensome, excessive and, in part, impossible testing requirements.

We are subject to adverse changes in tax laws.

Our tax expense or benefits could be adversely affected by changes in tax provisions, unfavorable findings in tax examinations or differing interpretations by tax authorities. We are unable to estimate the impact that current and future tax proposals and tax laws could have on our results of operations. We are currently under review by the IRS for tax years 2008 and 2009 and three state sales tax audits for which we do not expect any major assessments.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

As of December 31, 2011, we own approximately 1.5 million square feet of space for office, manufacturing, warehouse and assembly operations in Tulsa, Oklahoma and Longview, Texas. We believe that our facilities are well maintained and are in good condition and suitable for the conduct of our business.

Our plant and office facilities in Tulsa, Oklahoma, consist of a 342,000 sq. ft. building (327,000 sq. ft. of manufacturing/warehouse space and 15,000 sq. ft. of office space) located on a 12-acre tract of land at 2425 South Yukon Avenue (the “original facility”), and a 861,000 sq. ft. manufacturing/warehouse building and a 54,000 sq. ft. office building (the “expansion facility”) located on a 40-acre tract of land across the street from the original facility (2440 South Yukon Avenue). We own the original facility and the expansion facility. Both plants are of sheet metal construction.

6

Our manufacturing area is in heavy industrial type buildings, with total coverage by bridge cranes, containing manufacturing equipment designed for sheet metal fabrication and metal stamping. The manufacturing equipment contained in the facilities consists primarily of automated sheet metal fabrication equipment, supplemented by presses. Assembly lines consist of seven cart-type conveyor lines with variable line speed adjustment, which are motor driven. Subassembly areas and production line manning are based upon line speed.

Our operations in Longview, Texas, are conducted in a plant/office building at 203-207 Gum Springs Road, containing 258,000 sq. ft. on 14 acres. The manufacturing area (approximately 251,000 sq. ft.) is located in three 120-foot wide sheet metal buildings connected by an adjoining structure. The remaining 7,000 square feet are utilized as office space. The facility is built for light industrial manufacturing. An additional, contiguous 15 acres were purchased in 2004 and 2005 for future expansion. We own both the existing plant/office building, and the 15 acres designated for future expansion.

Item 3. Legal Proceedings.

We are not a party to any pending legal proceeding which management believes is likely to result in a material liability and no such action is contemplated by or, to the best of our knowledge, has been threatened against us.

Item 4. Mine Safety Disclosure.

Not applicable.

PART II

|

Item 5.

|

Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

|

Our common stock is quoted on the NASDAQ Global Select Market under the symbol "AAON".

The table below summarizes the high and low reported sale prices for our common stock for the past two fiscal years. As of the close of business on February 29, 2012, there were 1,006 holders of record, and approximately 4,321 beneficial owners, of our common stock.

|

Quarter Ended

|

High

|

Low

|

||

|

March 31, 2010

|

$15.37

|

$12.43

|

||

|

June 30, 2010

|

$16.84

|

$14.33

|

||

|

September 30, 2010

|

$17.42

|

$13.39

|

||

|

December 31, 2010

|

$19.76

|

$15.27

|

||

|

March 31, 2011

|

$21.98

|

$17.51

|

||

|

June 30, 2011

|

$23.44

|

$20.07

|

||

|

September 30, 2011

|

$24.23

|

$14.91

|

||

|

December 31, 2011

|

$22.98

|

$14.64

|

_______________

At the discretion of the Board of Directors we pay semi-annual cash dividends. Board approval is required to determine the date of declaration and amount for each semi-annual dividend payment. The Board of Directors approved dividend payments of $0.12 per share related to the 3-for-2 stock split effective June 13, 2011.

7

During 2011 we declared dividends to shareholders of record at the close of business on June 10, 2011 and December 1, 2011 which were paid on July 1, 2011 and December 22, 2011, respectively. We paid cash dividends of $5.9 million and $9.2 million in 2011 and 2010, respectively.

On November 6, 2007, our Board of Directors authorized a stock buyback program, targeting repurchases of up to approximately 10% (2.7 million shares) of our outstanding stock from time to time in open market transactions. On May 12, 2010, we completed the stock buyback program. Through May 12, 2010, we repurchased a total of 2.7 million shares under this program for an aggregate price of $36.1 million, or an average price of $13.36 per share. We purchased the shares at current market prices.

On May 17, 2010, the Board authorized a new stock buyback program, targeting repurchases of up to approximately 5% (1.3 million shares) of our outstanding stock from time to time in open market transactions. Through June 28, 2010, we repurchased a total of approximately 0.718 million shares under this program for an aggregate price of $11.5 million, or an average price of $16.04 per share. We purchased the shares at current market prices. We did not repurchase any of our equity securities during 2011.

On July 1, 2005, we entered into a stock repurchase arrangement by which employee-participants in our 401(k) savings and investment plan are entitled to have shares of AAON stock in their accounts sold to us to provide diversification of their investments. The maximum number of shares to be repurchased is contingent upon the number of shares sold by employees. Through December 31, 2011, we repurchased approximately 1.7 million shares for an aggregate price of $21.5 million, or an average price of $12.71 per share. We purchased the shares at current market prices.

On November 7, 2006, the Board of Directors authorized us to repurchase shares from certain directors and officers following their exercise of stock options. The maximum number of shares to be repurchased is contingent upon the number of shares sold. Through December 31, 2011, we repurchased approximately 0.580 million shares for an aggregate price of $8.1 million, or an average price of $13.98 per share. We purchased the shares at current market prices.

Repurchases during the fourth quarter of 2011 were as follows:

ISSUER PURCHASES OF EQUITY SECURITIES

|

Period

|

(a)

Total Number of Shares (or Units) Purchased

|

(b)

Average Price Paid Per Share (or Unit)

|

(c)

Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs

|

(d)

Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs

|

||||||||||||

|

October 2011

|

15,549 | $ | 18.64 | 15,549 | - | |||||||||||

|

November 2011

|

13,852 | $ | 21.15 | 13,852 | - | |||||||||||

|

December 2011

|

20,118 | $ | 21.09 | 20,118 | - | |||||||||||

|

Total

|

49,519 | $ | 20.34 | 49,519 | - | |||||||||||

8

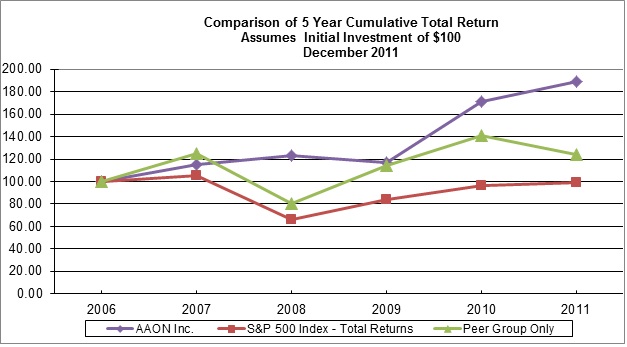

Comparative Stock Performance Graph

The following performance graph compares our cumulative total shareholder return, the NASDAQ Composite and a peer group of U.S. industrial manufacturing companies in the air conditioning, ventilation, and heating exchange equipment markets from December 31, 2006 through December 31, 2011. The graph assumes that $100 was invested at the close of trading December 31, 2006, with reinvestment of dividends. Our peer group includes Lennox International, Inc., Ingersoll Rand Limited, Johnson Controls Inc., and United Technologies Corporation. This table is not intended to forecast future performance of our Common Stock.

|

This stock performance Graph is not deemed to be “soliciting material” or otherwise be considered to be “filed” with the SEC or subject to Regulation 14A or 14C under the Securities Exchange Act of 1934 (Exchange Act) or to the liabilities of Section 18 of the Exchange Act, and should not be deemed to be incorporated by reference into any filing under the Securities Act of 1933 or the Exchange Act, except to the extent the Company specifically incorporates it by reference into such a filing.

9

Item 6. Selected Financial Data.

The following selected financial data should be read in conjunction with our Consolidated Financial Statements and Notes thereto included under Item 8 of this report and "Management's Discussion and Analysis of Financial Condition and Results of Operations" contained in Item 7.

|

Years Ended December 31,

|

||||||||||||||||||||

|

Results of Operations:

|

2011

|

2010

|

2009

|

2008

|

2007

|

|||||||||||||||

|

(in thousands, except per share data)

|

||||||||||||||||||||

|

Net sales

|

$ | 266,220 | $ | 244,552 | $ | 245,282 | $ | 279,725 | $ | 262,517 | ||||||||||

|

Net income

|

$ | 13,986 | $ | 21,894 | $ | 27,721 | $ | 28,589 | $ | 23,156 | ||||||||||

|

Earnings per share*:

|

||||||||||||||||||||

|

Basic

|

$ | 0.57 | $ | 0.87 | $ | 1.07 | $ | 1.09 | $ | 0.83 | ||||||||||

|

Diluted

|

$ | 0.56 | $ | 0.87 | $ | 1.07 | $ | 1.07 | $ | 0.81 | ||||||||||

|

Dividends per share*

|

$ | 0.24 | $ | 0.24 | $ | 0.24 | $ | 0.21 | $ | 0.21 | ||||||||||

|

Weighted average shares outstanding:

|

||||||||||||||||||||

|

Basic*

|

24,690 | 25,198 | 25,780 | 26,340 | 27,942 | |||||||||||||||

|

Diluted*

|

24,881 | 25,339 | 25,963 | 26,782 | 28,391 | |||||||||||||||

| December 31, | ||||||||||||||||||||

| Financial Position at End of

Fiscal Year:

|

2011

|

2010

|

2009

|

2008

|

2007

|

|||||||||||||||

| (in thousands) | ||||||||||||||||||||

|

Working capital

|

$ | 45,700 | $ | 55,502 | $ | 65,354 | $ | 40,600 | $ | 38,788 | ||||||||||

|

Total assets

|

$ | 178,981 | $ | 160,277 | $ | 156,211 | $ | 140,743 | $ | 137,140 | ||||||||||

|

Long-term and current debt

|

$ | 4,575 | $ | - | $ | 76 | $ | 3,113 | $ | 330 | ||||||||||

|

Total stockholders’ equity

|

$ | 122,504 | $ | 116,739 | $ | 117,999 | $ | 96,522 | $ | 95,420 | ||||||||||

* All share and per share amounts reflect a three-for-two stock split effective June 13, 2011.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

Overview

We engineer, manufacture and market air-conditioning and heating equipment consisting of rooftop units, chillers, air-handling units, make-up air units, heat recovery units, condensing units, commercial self-contained units and coils. These products are marketed and sold to retail, manufacturing, educational, medical and other commercial industries. We market our products to all 50 states in the United States and certain provinces in Canada. Foreign sales were approximately 5% of our 2011 sales.

Our business can be affected by a number of economic factors, including the level of economic activity in the markets in which we operate. The recent state of the economy has negatively impacted the commercial and industrial new construction markets. A further decline in economic activity could result in a decrease in our sales volume and profitability. Sales in the commercial and industrial new construction markets correlate closely to the number of new homes and buildings that are built, which in turn is influenced by cyclical factors such as interest rates, inflation, consumer spending habits, employment rates and other macroeconomic factors over which we have no control.

We sell our products to property owners and contractors through a network of manufacturers representatives and our internal sales force. The demand for our products is influenced by national and regional economic and demographic factors. The commercial and industrial new construction market is subject to cyclical fluctuations in that it is generally tied to housing starts, but has a lag factor of 6-18 months. Housing starts, in turn, are affected by such factors as interest rates, the state of the economy, population growth and the relative age of the population. When new construction is down, we emphasize the replacement market.

10

The principal components of cost of goods sold are labor, raw materials, component costs, factory overhead, freight and engineering expense. The principal high volume raw materials used in our manufacturing processes are steel, copper and aluminum and are obtained from domestic suppliers. We also purchase from domestic manufacturers certain components, including compressors, motors and electrical controls. The raw materials market has been volatile during 2011 and 2010 due to the economic environment and uncertainty in the financial markets. For the year ended December 31, 2011 prices for copper and steel increased approximately 3% and 10%, respectively from prior year, while the cost of aluminum decreased approximately 2%. For the year ended December 31, 2010 the cost of copper, steel, and aluminum increased approximately 88.7% and 11.5%, and 66.7% from 2009.

We attempt to limit the impact of price fluctuations of the raw materials used in our manufacturing processes by entering into cancelable and non-cancelable fixed price contracts with our major suppliers for periods of approximately 6 - 18 months. In addition, from time to time we use derivative contracts to partially mitigate the volatility in the prices for some of these commodities.

The following are key highlights and events that impacted our results of operations, cash flows, and financial condition in 2011:

|

·

|

Net sales for 2011 were $266 million, the second highest in the Company’s history in the last 10 years, compared to $245 million in 2010. The increase in net sales was a direct result of the increase in market acceptance of products released during the year and the signing into law of the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act on December 31, 2010 which provided 100 percent tax depreciation bonus on qualified capital investments put in service through December 31, 2011 which prompted our customers to benefit and take advantage of this provision of the law.

|

|

·

|

We estimate that we have captured approximately 14% plus share of the rooftop market and a 1% share of the coil market. Approximately 55% of our sales were generated from the sale to the renovation and replacement markets and 45% from new construction markets.

|

|

·

|

Income from operations was $22.2 million compared to $32.7 million in 2010. The decline in operational income was primarily due to lower gross margins caused by increases in raw materials and component costs and lost production for 8.5 days that resulted from the collapse of the roof for one of our manufacturing facilities.

|

|

·

|

Net income for 2011 was $13.9 million down by $7.9 million compared to $21.9 million in 2010. The decrease was the result of higher commodity and purchase parts prices and our inability to fully pass on the additional costs to our customers as a result of tight market conditions and fierce competition.

|

|

·

|

We paid $35.9 million in capital expenditures. A loss of approximately $1.8 million was incurred from the trade-in of production equipment that was replaced with new state of the art equipment that combines the latest advancement in automation and laser technology as a result of our strategic vision to improve current manufacturing efficiencies.

|

|

·

|

We paid cash dividends of $5.9 million, and announced a 3-for-2 stock split effective on June 13, 2011.

|

11

Results of Operations

The following is a summary of the income statement information as a percentage of net sales:

|

Years Ending December 31,

|

||||||||||||||||||||||||

|

2011

|

2010

|

2009

|

||||||||||||||||||||||

|

(in thousands)

|

||||||||||||||||||||||||

|

Net sales

|

$ | 266,220 | 100.0% | $ | 244,552 | 100.0% | $ | 245,282 | 100.0% | |||||||||||||||

|

Cost of sales

|

219,939 | 82.6% | 189,364 | 77.4% | 177,737 | 72.5% | ||||||||||||||||||

|

Gross profit

|

46,281 | 17.4% | 55,188 | 22.6% | 67,545 | 27.5% | ||||||||||||||||||

|

Selling, general and

administrative expenses

|

22,310 | 8.4% | 22,546 | 9.2% | 23,850 | 9.7% | ||||||||||||||||||

|

Loss (gain) on disposal of assets

|

1,802 | 0.7% | (73 | ) | (0.03)% | (59 | ) | (0.02)% | ||||||||||||||||

|

Income from operations

|

22,169 | 8.3% | 32,715 | 13.4% | 43,754 | 17.8% | ||||||||||||||||||

|

Interest expense

|

(277 | ) | (0.1)% | (45 | ) | (0.02)% | (9 | ) | 0.0% | |||||||||||||||

| Interest income | 98 | 0.04% | 258 | 0.10% | 71 | 0.03% | ||||||||||||||||||

| Other income (expense), net | (477 | ) | (0.2)% | (235 | ) | (0.10)% | 76 | 0.03% | ||||||||||||||||

|

Income before income taxes

|

21,513 | 8.1% | 32,693 | 13.4% | 43,892 | 17.9% | ||||||||||||||||||

| Income tax provision | 7,527 | 2.8% | 10,799 | 4.4% | 16,171 | 6.6% | ||||||||||||||||||

|

Net income

|

$ | 13,986 | 5.3% | $ | 21,894 | 9.0% | $ | 27,721 | 11.3% | |||||||||||||||

Year Ended December 31, 2011 vs. Year Ended December 31, 2010

Net Sales

Net sales for the year ended December 31, 2011 increased by 9%, or $21.7 million to $266.2 million, compared with the same period in 2010. The increase in net sales was the result of the favorable reception to our new products, a significant increase in the replacement market of approximately 10% over prior year, and increased market share.

Gross Profit

Gross margin decreased by $8.9 million (16.1%) to $46.3 million in 2011 compared to 2010. As a percentage of sales, gross margins were 17.4% and 22.6% in 2011 and 2010, respectively. The decrease in gross profit was caused by increases in raw material and component part costs of approximately 6% that we were unable to neutralize completely with price increases for some of our product lines, and increased labor costs and freight cost of 8% and 1%, respectively.

The principal components of cost of goods sold are labor, raw materials, component costs, factory overhead, freight out and engineering expense. The principal high volume raw materials used in our manufacturing processes are steel, copper and aluminum, which are obtained from domestic suppliers. For the year ended December 31, 2011 we experienced price increases in copper and steel of approximately 3% and 10%, and an overall price decrease in aluminum of approximately 2% as compared to 2010.

Selling, General and Administrative Expenses

Selling, General and Administrative (“SG&A”) expenses decreased by $0.236 million, or 1.1% to $22.3 million in 2011 compared to 2010, and as a percentage of net sales, SG&A expenses declined to 8.4% in 2011 from 9.2% in 2010. The decrease was primarily due to lower profit sharing expense of approximately $1.4 million as a result of lower operating income before income tax offset by increases in salaries and employee benefits of $0.6 million, and advertising expense and professional fees of approximately $0.6 million.

12

Interest Expense

Interest expense was approximately $0.277 million and $0.045 million in 2011 and 2010, respectively. The increase in interest expense of $0.232 million in 2011 from prior year was due to increased borrowings on the revolving credit facility. During 2011 we borrowed $82.1 million from the revolving credit facility as compared to $20.8 million in 2010. Interest on borrowings is payable monthly at LIBOR plus 2.5%. For the year ended December 31, 2011, we paid a weighted average interest rate of approximately 3.4%.

Interest Income

Interest income decreased by approximately $0.160 million to $0.098 million in 2011 compared to the same period in 2010. The decreased was due primarily to all of our investments maturing and no additional funds invested in 2011.

Other Income (Expense)

Other expense, net increased by $0.242 million to $0.477 million in 2011 from $0.235 million in 2010. The increase in other expense is primarily due to repair expenses related to roof damage to one of our manufacturing facilities in Tulsa, Oklahoma caused by a severe snowstorm in February 2011.

Year Ended December 31, 2010 vs. Year Ended December 31, 2009

Net Sales

Net sales were $244.6 million and $245.3 in 2010 and 2009, respectively. Sales in 2010 remained substantially level with 2009 despite poor economic conditions that caused the non-residential construction market spending to decline by approximately 14.1% from 2009 overall spending, as a result of our strategy of releasing new products in the markets in which we compete while maintaining prices constant which resulted in increased market share.

Gross Profit

Gross margin declined by $12.4 million or 18.3% to $55.2 million in 2010 from $67.5 million in 2010. As a percentage of sales, gross margins were 22.6% and 27.5% in 2010 and 2009, respectively. The decrease in gross margin was primarily a result of the absence of a derivative related to a copper hedge of $2.2 million that we benefited from in 2009, higher raw material and commodity costs, increased labor expenses to relocate a production line and set up new production lines for the Tulsa building addition and related supplies to stock the new lines, and our inability in the current economic environment to implement price increases to our minimum sales prices for HVAC units.

The raw materials market was volatile during 2010 and 2009 due to the economic environment. We experienced price increases for copper, steel and aluminum of approximately 88.7%, 11.5%, and 66.7%, respectively in 2010 compared to 2009.

Selling, General and Administrative Expenses

Selling, General and Administrative (“SG&A”) expenses decreased by $1.3 million, or 5.5% to $22.5 million in 2010 compared to 2009, and as a percentage of net sales, SG&A expenses declined to 9.2% in 2010 from 9.7% in 2009. The decrease was primarily due to lower profit sharing expense of $1.0 million as a result of lower operating income before income tax.

Interest Expense

Interest expense was approximately $0.045 million and $0.009 million in 2010 and 2009, respectively. The increase in interest expense of approximately $0.036 million was due to increased borrowings on the revolving credit facility. We borrowed $20.8 million from the revolving credit facility during 2010 compared to $10.0 million during 2009. We paid interest on borrowings at the greater of 4.0% or LIBOR plus 2.5% or at an average of approximately 4.0% for the year ended December 31, 2010.

13

Interest Income

Interest income was approximately $0.258 million and $0.071 million in 2010 and 2009, respectively. The increase in interest income of $0.187 million in 2010 from 2009 was due primarily to interest income generated from investments in corporate notes and bonds that average approximately $10.9 million in invested funds through September 30, 2010 and ended with a balance of $9.5 million at December 31, 2010.

Other Income (Expense)

Other expense, net decreased by $0.311 million to $0.235 million in 2010 from income of $0.076 million in 2009 due to the termination of a lease for one of our facilities during the second quarter of 2009.

Liquidity and Capital Resources

Our working capital and capital expenditure requirements are generally met through net cash provided by operations and the occasional use of the revolving bank line of credit based on our current liquidity at the time.

General

On July 30, 2011 we renewed and increased the line of credit with the Bank of Oklahoma, National Association from $15.2 million to $30 million. The revolving line of credit matures on July 29, 2012. We expect to renew our line of credit in July 2012 with favorable terms as we do not anticipate a tightening of funds in the financial markets. Under the line of credit, there is one standby letter of credit of $0.9 million. At December 31, 2011 we have approximately $ 24.5 million of borrowings available under the revolving credit facility. No fees are associated with the unused portion of the committed amount.

As of December 31, 2011 our outstanding balance under the revolving credit facility is $4.6 million and no borrowings were outstanding at December 31, 2010. Interest on borrowings is payable monthly at LIBOR plus 2.5%. The weighted average interest rate was 3.4% and 4.0% for the years ended December 31, 2011 and 2010, respectively.

At December 31, 2011 we were in compliance with all of the covenants under the revolving credit facility. We are obligated to comply with certain financial covenants under the revolving credit facility. These covenants require that we meet certain parameters related to our tangible net worth, total liabilities to tangible net worth ratio and working capital. At December 31, 2011 our tangible net worth was $122.5 million which meets the requirement of being at or above $95.0 million. Our total liabilities to tangible net worth ratio were 0.46 to 1.0 which meets the requirement of not being above 2 to 1. Our working capital was $45.7 million which meets the requirement of being at or above $35.0 million. Starting on June 30, 2012 our working capital requirement will change from $35.0 million to $40.0 million.

We repurchased shares of stock under our authorized stock buyback programs, employees’ 401(k) savings, investment plan, and from option exercises of our directors and officers in the open market in the amount of $3.7 million for 0.212 million shares, $19.5 million for 1.2 million shares and $3.1 million for approximately 0.246 million shares of stock in 2011, 2010 and 2009, respectively.

For the year ended December 31, 2011, 2010 and 2009 we paid cash dividends of $5.9 million, $9.2 million, and $5.9 million respectively.

During the quarter ended December 31, 2011, the Company recognized an income tax receivable of approximately $10.0 million. The tax receivable represents the anticipated Federal and State estimated tax over payments as of December 31, 2011 primarily as a result of new equipment purchases placed in service during the year which qualified for the 100% bonus tax depreciation expense allowed under the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010.

14

Based on historical performance and current expectations, we believe our cash and cash equivalents balance, the projected cash flows generated from our operations, our existing committed revolving credit facility (or comparable financing) and our expected ability to access capital markets will satisfy our working capital needs, capital expenditures and other liquidity requirements associated with our operations in 2012 and the foreseeable future.

Statement of Cash Flows

The table below reflects a summary of our net cash flows provided by operating activities, net cash flows used in investing activities, and net cash flows used in financing activities for the years indicated.

|

2011

|

2010

|

2009

|

|||||||||||

|

(in millions)

|

|||||||||||||

|

Net cash provided by operating activities

|

$ | 26.5 | $ | 32.2 | $ | 45.2 | |||||||

|

Net cash used in investing activities

|

(24.5 | ) | (28.3 | ) | (9.6 | ) | |||||||

|

Net cash used in financing activities

|

(4.3 | ) | (27.2 | ) | (10.1 | ) | |||||||

Cash Flows from Operating Activities

Net cash provided by operating activities was $26.5 million in 2011 compared to $32.2 million in 2010. This decrease was due to lower net income, and an unfavorable change in working capital. For the year ended December 31, 2011, net income decreased by $7.9 million and includes a non-cash loss on the sale of assets of $1.8 million. For 2010, net income decreased by $5.8 million from 2009.

Significant fluctuations in working capital were as follows:

|

·

|

Inventory - more cash was used in 2011 as improved demand resulted in increased volume and higher prices for raw materials, component, and parts in our inventory balance as compared to 2010 resulting in decreased cash flows of $1.3 million. In 2010, inventory increased by $4.8 million primarily as a result of increased inventory levels associated with an increase in our backlog from 2009 and valuation of inventories associated with higher raw material and component part prices.

|

|

·

|

Accounts receivable - impact of $6.1 million. We experienced improved collection rates as a result of targeted sales discounts for some of our selected customers. In 2010, accounts receivable negatively impacted cash flows by $6.4 million due primarily to slow customer payments and relatively flat sales from the previous year.

|

|

·

|

Accounts payable – accounts payable decreased cash flows by approximately $2.8 million to support the growth in the business. For the year ended December 31, 2010 accounts payable increased cash flows by approximately $6.5 million as a result of the increase in inventory levels and timing of payments to vendors.

|

|

·

|

Accrued liabilities – accrued liabilities decreased cash flows by approximately $3.0 million due to changes in certain reserves estimates as a result of better and improved experience and a decreased in amounts due to our representatives offset by a slight increase in accrued payroll and employee benefits. For the year ended December 31, 2010 accrued liabilities increased cash flows by approximately $2.4 million due to an increase in amounts due to our representatives, payroll and workers compensation partially offset by a decrease in medical self-insurance reserves.

|

15

Cash Flows from Investing Activities

Net cash used by investing activities was $24.5 million for the year ended December 31, 2011 compared with net cash used in investing activities of $28.3 million in 2010. The change in investing activities is primarily attributable to net proceeds from investments of $11.0 million, as well as proceeds from the sale of assets of approximately $0.5 million. These proceeds were offset by an increase in capital expenditures during 2011.

Net cash used in investing activities was $28.3 million for the year ended December 31, 2010 compared with $9.6 million in 2009. The change in investing activities is primarily attributable to an increase in investments in corporate bonds and notes and certificates of deposits of approximately $14.8 million and capital expenditures during 2010.

Capital expenditures were $35.9 million, $17.5 million and $9.8 million in 2011, 2010 and 2009, respectively. Capital expenditures in 2011 were primarily investments in our manufacturing and production equipment to support our growth and improve efficiencies with equipment which combines the latest advancement in automation and laser technology.

The capital expenditure program for 2012 is estimated to be approximately in the range of $10 million to $12 million, including amounts approved in prior periods. Many of these projects are subject to review and cancellation at the discretion of our CEO and Board of Directors without incurring substantial charges

Cash Flows from Financing Activities

Net cash used in financing activities during the year ended December 31, 2011 was $4.3 million, compared with $27.2 million during 2010. The change in financing activities is primarily related to approximately $3.7 million of share repurchases as well as dividend payments of $5.9 million, partially offset by an increase in borrowing of approximately $4.6 million and stock options and restricted stock awards exercised.

Net cash used in financing activities during the year ended December 31, 2010 was $27.2 million, compared with $10.1 million during 2009. The change in financing activities is primarily related to increase share repurchases of approximately $19.5 million and cash dividend payments of $9.2 million in 2010, partially offset by stock options exercised.

Off-Balance Sheet Arrangements

We are not party to any off-balance sheet arrangements that have or are reasonably likely to have a material current or future effect on our financial condition, changes in financial condition, revenues, expenses, results of operations, liquidity, capital expenditures or capital resources.

Commitments and Contractual Agreements

The following table summarizes our contractual agreements as of December 31, 2011:

| Payments Due By Period | ||||||||||||||||||||

| Contractual Obligations | Total | Less Than 1 Year | 1-3

Years

|

4-5

Years

|

After 5 Years | |||||||||||||||

|

(in millions)

|

||||||||||||||||||||

|

Revolving credit facility

|

$ | 4.6 | $ | 4.6 | ||||||||||||||||

|

Purchase obligations(1)

|

$ | 4.6 | $ | 2.3 | $ | 2.3 | - | - | ||||||||||||

|

Total contractual obligations

|

$ | 9.2 | $ | 6.9 | $ | 2.3 | $ | - | $ | - | ||||||||||

(1)The purchase obligation consists of delivery of R-410A refrigerant from one supplier. The price used to calculate the purchased obligation amount is the average price paid during 2011 as the quantity is fixed, but not the price.

16

Contingencies

We are subject to various claims and legal actions that arise in the ordinary course of business. We closely monitor these claims and legal actions and frequently consult with our legal counsel to determine whether they may, when resolved, have a material adverse effect on our financial position or results of operations. While we are unable to estimate the ultimate dollar amount of exposure or loss in connection with these matters, we make accruals as warranted. We believe that we have adequately provided in our consolidated financial statements for the potential impact of these contingencies. We also believe that the outcomes will not significantly affect the long-term results of operations, our financial position or our cash flows.

Critical Accounting Policies

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (“US GAAP”) requires management to make estimates and assumptions about future events, and apply judgments that affect the reported amounts of assets, liabilities, revenue and expenses in our consolidated financial statements and related notes. We base our estimates, assumptions and judgments on historical experience, current trends and other factors believed to be relevant at the time our consolidated financial statements are prepared. However, because future events and their effects cannot be determined with certainty, actual results could differ from our estimates and assumptions, and such differences could be material. We believe the following critical accounting policies affect our more significant estimates, assumptions and judgments used in the preparation of our consolidated financial statements.

Revenue Recognition – We recognize revenues from sales of products when the products are shipped and the title and risk of ownership pass to the customer. Final sales prices are fixed based on purchase orders. Sales allowances and customer incentives are treated as reductions to sales and are provided for based on historical experiences and current estimates. Our policy is to record the collection and payment of sales taxes through a liability account.

We present revenues net of certain payments to our independent manufacturer representatives (“Representatives”). Representatives are national companies that are in the business of providing HVAC units and other related products and services to customers. The end user customer orders a bundled group of products and services from the Representative and expects the Representative to fulfill the order. Only after the specifications are agreed to by the Representative and the customer, and the decision is made to use an AAON HVAC unit, will we receive notice of the order. We establish the amount we must receive for our HVAC unit (“minimum sales price”), but do not control the total order price which is negotiated by the Representative with the end user customer.

We are responsible for billings and collections resulting from all sales transactions, including those initiated by our Representatives. The Representatives submit the total order price to us for invoicing and collection. The total order price includes our minimum sales price and an additional amount which may include both the Representatives’ fee and amounts due for additional products and services required by the customer. These additional products and services may include controls purchased from another manufacturer to operate the unit, start-up services, and curbs for supporting the unit (“Third Party Products”). All are associated with the purchase of a HVAC unit but may be provided by the Representative or another third party. The Company is under no obligation related to Third Party Products.

The Representatives do not provide us with a break-out of the amount of the total order price over the minimum sales price which includes the Representatives’ fee and Third Party Product amounts (“Due to Representatives”). The Due to Representatives amount is paid only after all amounts associated with the order are collected from the customer. The amount of payments to our Representatives was $51.6 million, $51.4 million and $58.0 million for the years ended December 31, 2011, 2010, and 2009, respectively.

17

Allowance for Doubtful Accounts - Our allowance for doubtful accounts is estimated to cover the risk of loss related to accounts receivable. We establish an allowance for doubtful accounts based upon factors surrounding the credit risk of specific customers, historical trends in collections and write-offs, current customer status, the age of the receivable, economic conditions and other information. Aged receivables are reviewed on a monthly basis to determine if the reserve is adequate and adjusted accordingly at that time. The evaluation of these factors involves subjective judgments. Thus, changes in these factors or changes in economic circumstances may significantly impact our Consolidated Financial Statements.

Inventory Reserves – We establish a reserve for inventories based on the change in inventory requirements due to product line changes, the feasibility of using obsolete parts for upgraded part substitutions, the required parts needed for part supply sales, replacement parts and for estimated shrinkage.

Warranty – A provision is made for estimated warranty costs at the time the product is shipped and revenue is recognized. The warranty period is: the earlier of one year from the date of first use or 18 months from date of shipment for parts only; an additional four years on compressors (if applicable); 15 years on aluminized steel gas-fired heat exchangers (if applicable); 25 years on stainless steel heat exchangers (if applicable); and 10 years on gas-fired heat exchangers in RL products (if applicable). With the introduction of the RQ product line in 2010, our warranty policy for the RQ series was implemented to cover parts for two years from date of unit shipment and labor for one year from date of unit shipment. Warranty expense is estimated based on the warranty period, historical warranty trends and associated costs, and any known identifiable warranty issue.

Due to the absence of warranty history on new products, an additional provision may be made for such products. Our estimated future warranty cost is subject to adjustment from time to time depending on changes in actual warranty trends and cost experience. Should actual claim rates differ from our estimates, revisions to the estimated product warranty liability would be required.

Medical Insurance – A provision is made for medical costs associated with our Medical Employee Benefit Plan, which is primarily a self-funded plan. A provision is made for estimated medical costs based on historical claims paid and potential significant future claims. The plan is supplemented by employee contributions and any claim over $125,000 is covered by insurance.

Stock Compensation – We measure and recognize compensation expense for all share-based payment awards made to our employees and directors, including stock options and restricted stock awards, based on their fair values at the time of grant. Compensation expense, net of estimated forfeitures, is recognized on a straight-line basis during the service period of the related share-based compensation award. The fair value of each option award and restricted stock award is estimated on the date of grant using the Black-Scholes-Merton option pricing model. The use of the Black-Scholes option valuation model requires the input of subjective assumptions such as: the expected volatility, the expected term of the options granted, expected dividend yield, and the risk free rate.

Actual results have been within management’s expectations.

New Accounting Pronouncements

In January 2010, the FASB issued ASU No. 2010-06, Improving Disclosures about Fair Value Measurements (ASU 2010-06). The provisions of ASU 2010-06 amend Topic 820 to require reporting entities to make new disclosures about recurring and nonrecurring fair value measurements including significant transfers into and out of Level 1 and Level 2 fair value measurements and information on purchases, sales, issuances, and settlements on a gross basis in the reconciliation of Level 3 fair value measurements. ASU 2010-6 was effective for annual reporting periods beginning after December 15, 2009, except for Level 3 reconciliation disclosures which are effective for annual periods beginning after December 15, 2010. The adoption of the standard did not have a material impact of the consolidated financial statements.

In May 2011, the FASB issued ASU No. 2011-04, Fair Value Measurement (Topic 820): Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs. The ASU amends the fair value measurement and disclosure guidance for measuring amounts at fair value as well as disclosures about these measurements. The amendments introduced are effective for annual periods beginning after December 15, 2011, and should be applied prospectively. This ASU clarifies existing concepts and the amendments are not expected to result in significant changes to how the Company currently applies the fair value principles.

18

In June 2011, the FASB issued ASU No. 2011-05, Presentation of Comprehensive Income. This standard eliminates the current option to report other comprehensive income and its components in the statement of changes in equity. The amendment requires that all non-owner changes in stockholders’ equity be presented either in a single continuous statement of comprehensive income or in two separate but consecutive statements. In the two-statement approach, the first statement should present total net income and its components followed consecutively by a second statement that should present total other comprehensive income, the components of other comprehensive income, and the total of comprehensive income. The amendment must be applied retrospectively and is effective for fiscal years and interim periods within those years, beginning after December 15, 2011. We do not expect the adoption of this standard to have a material effect on our consolidated financial statements.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

We experience various market risks, primarily from commodity prices and interest rates. We do not use derivative financial instruments to hedge our interest rate risk. However, occasionally we use financial derivatives to economically hedge our commodity price risk. We do not use financial derivatives for speculative purposes.

Interest Rate Risk

We are exposed to interest rate risk on our revolving credit facility, which bears a variable interest rate of LIBOR plus 2.5%. At December 31, 2011 we had borrowings of $4.6 million outstanding under the revolving credit facility. The weighted average interest rate was 3.4% and 4.0% for the years ended December 31, 2011 and 2010, respectively.

Commodity Price Risk

We are exposed to volatility in the prices of commodities used in some of our products and occasionally we use fixed price cancellable and non-cancellable contracts with our major suppliers for periods of 6 to 18 months to manage this exposure. From time to time we use financial derivatives to economically hedge our commodity price risk. We do not have committed commodity derivative instruments in place at December 31, 2011.

Item 8. Financial Statements and Supplementary Data.

The financial statements and supplementary data are included commencing at page 28.

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure.

Not Applicable.

19

Item 9A. Controls and Procedures.

(a) Evaluation of Disclosure Controls and Procedures

At the end of the period covered by this Annual Report on Form 10-K, our management, under the supervision and with the participation of our Chief Executive Officer and Chief Financial Officer, has evaluated the effectiveness of the design and operation of our disclosure controls and procedures. Based on that evaluation, our Chief Executive Officer and Chief Financial Officer believe that:

|

·

|

Our disclosure controls and procedures are designed at a reasonable assurance threshold to ensure that information required to be disclosed by us in the reports we file under the Securities Exchange Act of 1934 is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms; and

|

|

·

|

Our disclosure controls and procedures operate at a reasonable assurance threshold such that important information flows to appropriate collection and disclosure points in a timely manner and are effective to ensure that such information is accumulated and communicated to our management, and made known to our Chief Executive Officer and Chief Financial Officer, particularly during the period when this Annual Report was prepared, as appropriate to allow timely decisions regarding the required disclosure.

|

Our Chief Executive Officer and Chief Financial Officer have evaluated our disclosure controls and procedures and concluded that these controls and procedures were effective as of December 31, 2011.

(b) Management's Annual Report on Internal Control over Financial Reporting

Our management is responsible for establishing and maintaining adequate internal control over our financial reporting. Our internal control over financial reporting is a process designed by, or under the supervision of, our principal executive and principal financial officer, and effected by our board of directors, management and other personnel, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with U.S. generally accepted accounting principles.

All internal control systems, no matter how well designed, have inherent limitations. Therefore, even those systems determined to be effective can provide only reasonable assurance with respect to financial statement preparation and presentation.

In making our assessment of internal control over financial reporting, management used the criteria issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO) in Internal Control—Integrated Framework. Based on our assessment, we believe that, as of December 31, 2011, our internal control over financial reporting is effective at the reasonable assurance level based on those criteria.

The effectiveness of the Company’s internal control over financial reporting as of December 31, 2011 has been audited by Grant Thornton LLP, our independent registered public accounting firm, as stated in their report which is included in this Item 9A of this report on Form 10-K.

(c) Changes in Internal Control over Financial Reporting

There have been no changes in internal control over financial reporting that occurred during the fourth quarter of 2011 that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

20

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Board of Directors and Stockholders

AAON, Inc.

We have audited AAON, Inc.’s (a Nevada Corporation) and subsidiaries, collectively, the “Company”, internal control over financial reporting as of December 31, 2011, based on criteria established in Internal Control – Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). The Company’s management is responsible for maintaining effective internal control over financial reporting and for its assessment of the effectiveness of internal control over financial reporting, included in the accompanying Management’s Annual Report on Internal Control over Financial Reporting. Our responsibility is to express an opinion of the Company’s internal control over financial reporting based on our audit.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether effective internal control over financial reporting was maintained in all material respects. Our audit included obtaining an understanding of internal control over financial reporting, assessing the risk that a material weakness exists, testing and evaluating the design and operating effectiveness of internal control based on the assessed risk, and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion.