UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2020

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _____________________________ to _____________________________

Commission file number: 0-18953

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction | (IRS Employer | ||||||||||||||||||||||

| of incorporation or organization) | Identification No.) | ||||||||||||||||||||||

| (Address of principal executive offices) (Zip Code) | |||||||||||||||||||||||

Registrant’s telephone number, including area code: (918 ) 583-2266

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934).

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Act.)

The aggregate market value of the common equity held by non-affiliates computed by reference to the closing price of registrant’s common stock on the last business day of registrant’s most recently completed second quarter June 30, 2020 was $2,213.5 million based upon the closing price reported for such date on the Nasdaq Global Select Market.

As of February 22, 2021, registrant had outstanding a total of 52,287,036 shares of its $.004 par value Common Stock.

DOCUMENTS INCORPORATED BY REFERENCE

| TABLE OF CONTENTS | |||||||||||

| Item Number and Caption | Page Number | ||||||||||

| PART I | |||||||||||

| 1. | Business. | ||||||||||

| 1A. | Risk Factors. | ||||||||||

| 1B. | Unresolved Staff Comments. | ||||||||||

| 2. | Properties. | ||||||||||

| 3. | Legal Proceedings. | ||||||||||

| 4. | Mine Safety Disclosure. | ||||||||||

| PART II | |||||||||||

| 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. | ||||||||||

| 6. | Selected Financial Data. | ||||||||||

| 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. | ||||||||||

| 7A. | Quantitative and Qualitative Disclosures About Market Risk. | ||||||||||

| 8. | Financial Statements and Supplementary Data. | ||||||||||

| 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure. | ||||||||||

| 9A. | Controls and Procedures. | ||||||||||

| 9B. | Other Information. | ||||||||||

| PART III | |||||||||||

| 10. | Directors, Executive Officers and Corporate Governance. | ||||||||||

| 11. | Executive Compensation. | ||||||||||

| 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. | ||||||||||

| 13. | Certain Relationships and Related Transactions, and Director Independence. | ||||||||||

| 14. | Principal Accountant Fees and Services. | ||||||||||

| PART IV | |||||||||||

| 15. | Exhibits and Financial Statement Schedules. | ||||||||||

Forward-Looking Statements

This Annual Report includes “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “seeks”, “estimates”, “should”, “will”, and variations of such words and similar expressions are intended to identify such forward-looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions, which are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they are made. We undertake no obligations to update publicly any forward-looking statements, whether as a result of new information, future events or otherwise. Important factors that could cause results to differ materially from those in the forward-looking statements include (1) the timing and extent of changes in raw material and component prices, (2) the effects of fluctuations in the commercial/industrial new construction market, (3) the timing and extent of changes in interest rates, as well as other competitive factors during the year, (4) general economic, market or business conditions, and (5) the correction of certain of our previously issued consolidated financial statements, which may affect investor confidence and raise reputational issues.

PART I

Item 1. Business.

Overview

AAON, Inc., a Nevada corporation, (“AAON Nevada”) was incorporated on August 18, 1987. Our operating subsidiaries include AAON, Inc., an Oklahoma corporation, and AAON Coil Products, Inc., a Texas corporation. Unless the context otherwise requires, references in this Annual Report to “AAON”, the “Company”, “we”, “us”, “our”, or “ours” refer to AAON Nevada and our subsidiaries.

We are engaged in the engineering, manufacturing, marketing, and sale of premium air conditioning and heating equipment consisting of standard, semi-custom, and custom rooftop units, chillers, packaged outdoor mechanical rooms, air handling units, makeup air units, energy recovery units, condensing units, geothermal/water-source heat pumps, and coils.

Business and Marketing Strategy

Our products serve the commercial and industrial new construction and replacement markets within the heating, ventilation, and air conditioning (“HVAC”) equipment industry. Our business strategy involves mass customization that uses flexible computer-aided manufacturing systems to produce standard, semi-custom, and custom outputs and combines the low unit costs of mass production processes with the flexibility of individual customization. Through a collaborative effort with our independent representative sales offices, we design and manufacture the precise semi-custom product offering that best serves the customer's needs.

Our marketing strategy focuses upon underserved market niches including establishing manufacturing methodologies to support market niche products. We further focus on developing a company culture focused upon customer satisfaction, reducing product delivery channel time and cost, and continuing with the goal of product and manufacturing technology leadership. Our product mix, with a heavy investment in research and development, has an emphasis on energy efficiency, environment, and indoor air quality.

Products

Our rooftop and condensing unit markets primarily consist of units installed on commercial or industrial structures of generally less than ten stories in height. Our air handling units, self-contained units, geothermal/water-source heat pumps, chillers, packaged outdoor mechanical rooms, and coils are suitable for all sizes of commercial and industrial buildings.

1

The size of these markets is determined primarily by the number of commercial and industrial building completions and replacement demand from existing buildings. The replacement market consists of products installed to replace existing units/components that are worn or damaged and products to upgrade certain components, such as low leakage dampers, high efficiency heat exchangers and modern controls components. Currently, over half of the industry’s market consists of replacement units.

The commercial and industrial new construction market is subject to cyclical fluctuations in that it is generally tied to housing starts and the general economy, but has a lag factor of six to 18 months. Housing starts, in turn, are affected by such factors as interest rates, the state of the economy, population growth and the relative age of the population. When new construction is down, we emphasize the replacement market.

Based on our 2020 sales of $514.6 million, we estimate that we have approximately a 13% share of the greater than five ton rooftop market and a 2% share of the less than five ton market. During 2020, approximately 50% of our sales were generated from the renovation and replacement markets and 50% from new construction. The ratio of sales for new construction vs. replacement to particular customers is related to various factors. Generally, the cyclicality of the new construction market fluctuates this ratio the most over an economic cycle.

To date, our sales have been primarily to the domestic market. Foreign sales accounted for approximately $11.7 million, $14.8 million, and $14.7 million of our sales in 2020, 2019, and 2018, respectively. As a percentage of sales, foreign sales accounted for approximately 2%, 3%, and 3% of our net sales in each of those years, respectively.

We purchase certain components, fabricate sheet metal and tubing and then assemble and test the finished products. Our primary finished products consist of a single unit system containing heating and cooling in a self-contained cabinet, referred to in the industry as “unitary products”. Our other finished products are chillers, packaged outdoor mechanical rooms, coils, air handling units, condensing units, makeup air units, energy recovery units, rooftop units, geothermal/water-source heat pumps, and controls.

We offer three groups of rooftop units: the RQ Series, consisting of five cooling sizes ranging from two to six tons; the RN Series, offered in 28 cooling sizes ranging from six to 140 tons; and the RZ Series, which is offered in 15 cooling sizes ranging from 45 to 240 tons.

We also offer the SA, SB and M2 Series as indoor packaged, water-cooled or geothermal/water-source heat pump self-contained units with cooling capacities of three to 70 tons.

Our small packaged geothermal/water-source heat pump units consist of the WH Series horizontal configuration and WV Series vertical configuration, from one-half to 30 tons.

We manufacture a LF Series air-cooled chiller, a LN Series air-cooled chiller, and a LZ Series chiller and packaged outdoor mechanical room, which are available in both air-cooled condensing and evaporative-condensed configurations, covering a range of four to 540 tons.

We offer two groups of condensing units: the CB Series, two to five tons and the CF Series, two to 70 tons.

Our air handling units consist of the indoor F1, H3, and V3 Series and the modular M2 Series, as well as air handling unit configurations of the RQ, RN, RZ, and SA Series units.

Our energy recovery option applicable to our RQ, RN, RZ, and SB units, as well as our H3, V3, and M2 Series air handling units, responds to the U.S. Clean Air Act mandate to increase fresh air in commercial structures. Our products are designed to compete on the higher quality end of standardized products.

Our air-cooled chillers (LF, LN, and LZ Series) are certified with the Air-Conditioning, Heating, and Refrigeration Institute (“AHRI”) in accordance with AHRI Standard 550/590. Our RN, RQ, M2, and SB Series, including our water-source heat pump products (WH, and WV Series), are AHRI certified in accordance with ANSI/AHRI/ASHRAE/ISO 13256.

Our unitary products (RQ, RN, and CB Series) are certified with the AHRI in accordance with AHRI Standard AHRI 210/240 up to 5 tons capacity and AHRI Standard AHRI 340/360 up to 63 tons capacity.

2

Performance characteristics of our products range in cooling capacity from one-half to 540 tons and in heating capacity from 7,200 to 9,000,000 British Thermal Units ("BTUs"). Many of our units far exceed these minimum standards and are among the highest efficiency units currently available.

A typical commercial building installation requires one ton of air conditioning for every 300-400 square feet or, for a 100,000 square foot building, 250 tons of air conditioning, which can involve multiple units.

AAON is committed to designing and manufacturing innovative HVAC products of the highest quality, efficiency, and performance. Our water-source heat pump products recover otherwise wasted energy and employ it to cool, heat, and provide dehumidification to a building, making it one of the most efficient and environmentally friendly systems. AAON packaged rooftop units with two stage compressors are optimized with high efficiency evaporator and condenser coils and variable speed fans, leading to an AHRI Certified performance up to 19.15 SEER and 20.2 IEER. AAON H3/V3 Series energy recovery wheel air handling units provide energy efficient 100% outside air ventilation by recovering energy that would otherwise be exhausted from a building. LZ Series packaged outdoor mechanical rooms are engineered to maximize the efficiency of the complete hydronic system - compressors, condenser, and evaporator. Factory installed 98% efficiency boilers with pumping packages are available for applications that require hot water. Energy saving waterside economizers are available for chilled water systems that require cooling at low ambient conditions.

AAON designs and produces controls solutions for all of our HVAC units including rooftop units, air handlers, chillers, and water-source heat pumps. In addition, we provide controls for variable air volume systems associated with those units, as well as controls products for other HVAC related equipment. Our controls are easily configurable to provide a wide variety of HVAC unit application options, and we are able to customize our controls, where necessary, to meet unique customers’ requirements. Most of our controls are Underwriters Laboratories category ZPVI2 complaint and BACnet Testing Laboratories certified. In addition our economizer function is California Title 24 certified. All of these factors allow us to provide AAON controls with factory developed, approved and tested sequences of operation to optimize the performance of the AAON units.

Other AAON controls options include providing terminal blocks for field-installed controls and factory installed customer provided controls. With all these controls options available to us, we are able to use controls to help sell more AAON equipment. We also offer six control options: the Pioneer Silver, Pioneer Gold, Touchscreen Controller, Orion Controller, and terminal block for field installed controls, and factory installed customer provided controls.

Air Quality Products

The coronavirus disease 2019 ("COVID-19") pandemic has fueled a great deal of concern over best practices in the design and operation of building HVAC systems. In order to mitigate the spread of COVID-19, influenza, and other similar type respiratory diseases, we have done a great deal of research on what affects the transmission of these diseases and how AAON HVAC systems can be best designed. The American Society of Heating, Refrigeration and Air-Conditioning Engineers ("ASHRAE"), a professional association with a goal of advancing HVAC systems designs and construction, put together an Epidemic Task Force in 2020 and determined several recommendations to mitigate the spread of the virus, including humidity control, air filtration, increased outdoor air ventilation, and air disinfection.

Humidity control - AAON continues to lead the market in developing energy efficient humidity control with the use of variable capacity compressors and modulating hot gas reheat. Designing HVAC systems with superior humidity control allows building management to maintain ASHRAE’s recommended ambient relative humidity levels of 40%-60%, the ideal level to inactivate viruses in the air and on surfaces.

Air Filtration - AAON standardizes a design that uses a backward curved fan wheel, which can accommodate higher airflow required for the ASHRAE recommended MERV 13 filtration, the minimum filter level for viruses, with very little reconfiguration. Prior to 2020, a vast majority of commercial buildings use filtration levels of MERV 4 to MERV 8, which has always been acceptable for filtering out typical particulates in the air stream.

Outdoor Air Ventilation - AAON’s innovative use of energy recovery wheels and energy recovery plates combined with its superior humidity control design can help building management follow outdoor ventilation air recommendations while limiting an increase of energy usage and maintaining recommended humidity levels.

3

Air Disinfection - AAON has basic design characteristics that allow for an easy installation of ultraviolet lighting and bipolar ionization equipment. In addition to this equipment offered as options in new AAON units sold, AAON has basic design characteristics that allow for easy installation in AAON units already used in the field.

Overall, AAON is well positioned to accommodate the heightened demand for features that can help mitigate virus transmission and improve air quality. The features that ASHRAE recommends requires premium designs and configurations that are standard in AAON units. As a result, we are able to incorporate air quality features into our units, at a minimal price premium and with no delivery delay.

Representatives

As of December 31, 2020, we employ a sales staff of 46 individuals and utilize approximately 63 independent manufacturer representatives’ organizations (“Representatives”) having 125 offices to market our products in the United States and Canada. We also have one international sales organization, which utilizes 28 distributors in other countries. Sales are made directly to the contractor or end user, with shipments being made from our Tulsa, Oklahoma, Longview, Texas, or our Parkville, Missouri, facilities to the job site.

Our products and sales strategy focuses on niche markets. The targeted markets for our equipment are customers seeking products of better quality than those offered, and/or options not offered, by standardized manufacturers.

To support and service our customers and the ultimate consumer, we provide parts availability through our Representatives' sales offices, as well as our two Tulsa, Oklahoma AAON operated retail parts stores, to serve the local markets. We also have factory service organizations at each of our plants. Additionally, a number of the Representatives we utilize have their own service organizations, which, in connection with us, provide the necessary warranty work and/or normal service to customers.

Warranties

Our product warranty policy is the earlier of one year from the date of first use or 18 months from date of shipment for parts only, including controls; an additional four years for compressors (if applicable); 15 years on aluminized steel gas-fired heat exchangers (if applicable); 25 years on stainless steel heat exchangers (if applicable); and ten years on gas-fired heat exchangers in our historical RL products (if applicable). Our warranty policy for the RQ series covers parts for two years from date of unit shipment. Our warranty policy for the WH and WV Series geothermal/water-source heat pumps covers parts for five years from the date of installation.

The Company also sells extended warranties on parts for various lengths of time ranging from six months to ten years. Revenue for these separately priced warranties is deferred and recognized on a straight-line basis over the separately priced warranty period.

Major Customers

One customer, Texas AirSystems, accounted for 10% or more of our sales during 2020, 2019, and 2018. No other customer accounted for more than 10% of our sales during 2020, 2019, and 2018.

Backlog

Our backlog as of February 1, 2021 was approximately $103.8 million, compared to approximately $129.2 million as of February 1, 2020. The current backlog consists of orders considered by management to be firm and our goal is to fill orders within approximately 60 to 90 days after an order is deemed to become firm; however, the orders are subject to cancellation by the customers in which case, cancellation charges apply up to the full price of the equipment.

Competition

In the standardized market, we compete primarily with Lennox (Lennox International, Inc.), Trane (Trane Technologies plc), York International (Johnson Controls International plc), Carrier (Carrier Global Corporation), and Daikin (Daikin Industries). All of these competitors are substantially larger and have greater resources than we do. Our products compete on the basis of total value, quality, function, serviceability, efficiency, availability of

4

product, reliability, product line recognition, and acceptability of sales outlets. However, in new construction where the contractor is the purchasing decision maker, we are often at a competitive disadvantage because of the emphasis placed on initial cost. In the replacement market and other owner-controlled purchases, we have a better chance of getting business since quality and long-term cost are generally taken into account.

Resources

Sources and Availability of Raw Materials

The most important materials we purchase are steel, copper, and aluminum. We also purchase from other manufacturers certain components, including compressors, electric motors, and electrical controls used in our products. We attempt to obtain the lowest possible cost in our purchases of raw materials and components, consistent with meeting specified quality standards. We are not dependent upon any one source for raw materials or the major components of our manufactured products. By having multiple suppliers, we believe that we will have adequate sources of supplies to meet our manufacturing requirements for the foreseeable future.

We attempt to limit the impact of price fluctuations on these materials by entering into cancellable and non-cancellable fixed price contracts with our major suppliers for periods of six to 18 months. We expect to receive delivery of raw materials from our fixed price contracts for use in our manufacturing operations.

We have not been significantly impacted by the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) that contains provisions to improve transparency and accountability concerning the supply of certain minerals, known as “conflict minerals”, originating from the Democratic Republic of Congo and adjoining countries.

Working Capital Practices

Working capital practices in the industry center on inventories and accounts receivable. Our management regularly reviews our working capital with a view of maintaining the lowest level consistent with requirements of anticipated levels of operation. Our greatest needs arise during the months of July - November, the peak season for inventory (primarily purchased material) and accounts receivable. Our working capital requirements are generally met by cash flow from operations and a bank revolving credit facility, which currently permits borrowings up to $30 million and had no balance outstanding at December 31, 2020. We believe that we will have sufficient funds available to meet our working capital needs for the foreseeable future.

Research and Development

Our products are engineered for performance, flexibility, and serviceability. This has become a critical factor in competing in the HVAC equipment industry. We must continually develop new and improved products in order to compete effectively and to meet evolving regulatory standards in all of our major product lines.

AAON is fortunate enough to be able to self-sponsor our Research and Development (“R&D”) activities, rather than needing to be customer-sponsored. R&D activities have involved the RQ, RN, and RZ (rooftop units), F1, H3, SA, V3, and M2 (air handling units), LF, LN, and LZ (chillers), CB and CF (condensing units), SA and SB (self-contained units), and WH and WV (water-source heat pumps), as well as component evaluation and refinement, development of control systems and new product development. R&D expenses incurred were approximately $17.4 million, $14.8 million, and $13.5 million in 2020, 2019, and 2018, respectively.

Our Norman Asbjornson Innovation Center ("NAIC") research and development laboratory facility that opened in 2019, includes many unique capabilities, which to our knowledge exist nowhere else in the world. A few features of the NAIC include supply, return, and outside sound testing at actual load conditions, testing of up to a 300 ton air conditioning system, up to a 540 ton chiller system, and 80 million BTU/hr of gas heating test capacity. Environmental application testing capabilities include -20 to 140°F testing conditions, up to 8 inches per hour rain testing, up to 2 inches per hour snow testing, and up to 50 mph wind testing. We believe we have the largest sound-testing chamber in the world for testing heating and air conditioning equipment and are not aware of any similar labs that can conduct this testing while putting the equipment under full environmental load. The unique capabilities of the NAIC will enable AAON to lead the industry in the development of quiet, energy efficient commercial and industrial heating and air conditioning equipment.

5

The NAIC currently houses ten testing chambers, with two new additional chambers scheduled to come online in early 2021. These testing chambers allow AAON to meet and maintain AHRI and U.S. Department of Energy ("DOE") certification and solidify the Company’s industry position as a technological leader in the manufacturing of HVAC equipment. Current voluntary industry certification programs and government regulations only go up to 63 tons of air conditioning as that is the largest environmental chamber currently available for testing outside of our facility. The NAIC contains both a 100 ton and a 540 ton chamber, allowing us to uniquely prove to customers our capacity and efficiency on these larger units.

The NAIC was designed to test units well beyond the standard AHRI rating points and allows us to offer testing services on AAON equipment throughout our range of product application. This capability is vital for critical facilities where the units must perform properly and allows our customers to verify the performance of our units in advance, rather than after installation. These same capabilities will enable AAON to develop a new extended range of operation equipment and prove its capabilities.

Patents, Trademarks, Licenses, and Concessions

We do not consider any patents, trademarks, licenses, or concessions to be material to our business operations, other than patents issued regarding our energy recovery wheel option, blower, gas-fired heat exchanger, evaporative-cooled condenser de-superheater, and low leakage damper which have terms of 20 years with expiration dates ranging from 2020 to 2033.

Seasonality

Sales of our products are moderately seasonal with the peak period being May-October of each year due to timing of construction projects being directly related to warmer weather.

Environmental & Regulatory Matters

Laws concerning the environment that affect or could affect our operations include, among others, the Clean Water Act, the Clean Air Act, the Resource Conservation and Recovery Act, the Occupational Safety and Health Act, the National Environmental Policy Act, the Toxic Substances Control Act, regulations promulgated under these Acts and any other federal, state or local laws or regulations governing environmental matters. We believe that we are in compliance with these laws and that future compliance will not materially affect our earnings or competitive position.

Since our founding in 1988, AAON has maintained a commitment to design, develop, manufacture and deliver heating and cooling products to perform beyond all expectations and to demonstrate AAON’s quality and value to our customers. AAON equipment is designed with energy efficiency in mind, without sacrificing premium features and options. In addition to our high standard of product performance, is a commitment to sustainability for our employees, our stockholders, and our customers. At AAON, we strive to conduct our business in a socially responsible and ethical manner with a focus on environmental stewardship, team member safety and community engagement. We comply with industry regulations and requirements while pursuing responsible economic growth and profitability.

AAON participates in a sustainability benchmarking initiative (Sustainable Tulsa Scor3card) through which we set goals, monitor and report in the areas of energy, material management, water, community stewardship, transportation, communication and health. AAON achieved Platinum level in this program in 2020 and was recognized with the Henry Bellmon Sustainability Award. We have an active internal sustainability committee that provides education opportunities, communications and recommendations to the company on a regular basis.

Two leading focus areas for AAON are energy efficiency and material management. In the area of energy efficiency and conservation, AAON has transitioned to over 90% LED lighting leading to considerable cost savings and reduced energy consumption. The company participates in an energy demand response program and saved over $32,000 by reducing energy loads during peak periods in 2020. Twenty-seven percent of AAON’s energy portfolio is currently derived from renewable sources, and the company’s carbon footprint has been calculated as part of the Scor3card sustainability benchmarking initiative. Energy efficiency has been a priority in ongoing capital investments which include the acquisition of new, energy efficient equipment for the production floor, new high-

6

speed overhead facility doors, the installation of new HVAC equipment, building control systems, the application of heat and light reflective material to production facilities along with other behavioral –based energy efficiency changes. We are tracking our energy usage intensity before and after these updates.

In the area of material management, there is a focus on recycling, reducing, reusing and sourcing more environmentally-friendly materials into our processes. AAON recycled over 11,741 tons of metal in 2020. Our facilities also recycle paper, wood and cardboard where available. Through our partnership with a waste to energy facility, we successfully diverted over 556 tons of waste from landfills. We continue to innovate ways to reduce and reuse shipping packaging between facilities and identify new opportunities to reduce or reuse items in our production and administrative areas.

Human Capital Resources

As of February 23, 2021, we employed 2,268 direct employees and contract personnel, a 2.8% decrease when compared to the same period 2020 and a 2.1% increase when compared to 2019. Our employees are not represented by unions or other collective bargaining agreements. Management considers its relations with our employees to be good.

We believe our employees are key to achieving our business objectives. In the early stages of the COVID-19 pandemic, we put COVID-19 prevention protocols in place to minimize the spread of COVID-19 in our workplaces. These protocols, which remain in place, meet or exceed the Centers for Disease Control guidelines and where applicable, state and local mandates.

Our key human capital measures include employee safety, turnover, absenteeism, and production. We frequently benchmark our compensation practices and benefits programs against those of comparable industries and in the geographic areas where our facilities are located. We believe that our compensation and employee benefits are competitive and allow us to attract and retain skilled and unskilled labor throughout our organization. Some of our notable health, welfare, and retirement benefits include:

•Employee medical plan (with 175% employer health saving plan match)

•401(k) Plan (with 175% employer match)

•Profit sharing bonus plan

•Tuition assistance program

•Paid time off

Available Information

Our Internet website address is http://www.aaon.com. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, will be available free of charge through our Internet website as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The information on our website is not a part of, or incorporated by reference into, this annual report on Form 10-K.

Copies of any materials we file with the SEC can also be obtained free of charge through the SEC’s website at http://www.sec.gov, at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549, or by calling the SEC at 1-800-732-0330.

7

Item 1A. Risk Factors.

The following risks and uncertainties may affect our performance and results of operations. The discussion below contains “forward-looking statements” as outlined in the Forward-Looking Statements section above. Our ability to mitigate risks may cause our future results to materially differ from what we currently anticipate. Additionally, the ability of our competitors to react to material risks will affect our future results.

Risks Related to the Covid-19 Pandemic

Our business, results of operations, financial condition, cash flows, and stock price can be adversely affected by pandemics, epidemics, or other public health emergencies, such as COVID-19.

Our business, results of operations, financial condition, cash flows, and stock price can be adversely affected by pandemics, epidemics, or other public health emergencies, such as COVID-19. In March 2020, the World Health Organization characterized COVID-19 as a pandemic, and the President of the United States declared the COVID-19 outbreak a national emergency. The outbreak has resulted in governments around the world implementing increasingly stringent measures to help control the spread of the virus, including quarantines, “shelter in place” and “stay at home” orders, travel restrictions, business curtailments, school closures, and other measures. In addition, governments and central banks in several parts of the world have enacted fiscal and monetary stimulus measures to counteract the impacts of COVID-19.

We are considered a critical infrastructure industry, as defined by the U.S. Department of Homeland Security. Although we have continued to operate our facilities to date consistent with federal guidelines and state and local orders, the outbreak of COVID-19 and any preventive or protective actions taken by governmental authorities may have a material adverse effect on our operations, supply chain, customers, and transportation networks, including business shutdowns or disruptions. The extent to which COVID-19 may adversely impact our business depends on future developments, which are highly uncertain and unpredictable, depending upon the severity and duration of the outbreak and the effectiveness of actions taken globally to contain or mitigate its effects. Any resulting financial impact cannot be estimated reasonably at this time, but may materially adversely affect our business, results of operations, financial condition, and cash flows. Even after the COVID-19 pandemic has subsided, we may experience materially adverse impacts to our business due to any resulting economic recession or depression. Additionally, concerns over the economic impact of COVID-19 have caused extreme volatility in financial and other capital markets which may adversely impact our stock price and our ability to access capital markets. To the extent the COVID-19 pandemic adversely affects our business and financial results, it may also have the effect of heightening many of the other risks described in this Annual Report, such as those relating to our products and financial performance.

Risks Related to Our Business

Our business can be hurt by economic conditions.

Our business is affected by a number of economic factors, including the level of economic activity in the markets in which we operate. Sales in the commercial and industrial new construction markets correlate to the number of new homes and buildings that are built, which in turn is influenced by cyclical factors such as interest rates, inflation, consumer spending habits, employment rates, and other macroeconomic factors over which we have no control. In the HVAC business, a decline in economic activity as a result of these cyclical or other factors typically results in a decline in new construction and replacement purchases which could impact our sales volume and profitability.

Our results of operations and financial condition could be negatively impacted by the loss of a major customer.

From time to time in the past we derived a significant portion of our sales from a limited number of customers, and such concentration may continue in the future. In 2020, 2019, and 2018, one customer, Texas AirSystems, accounted for more than 10% of our sales. The loss of, or significant reduction in sales to, a major customer could have a material adverse effect on our results of operations, financial condition and cash flow. Further, the addition of new major customers in the future could increase our customer concentration risks as described above.

8

We may incur material costs as a result of warranty and product liability claims that would negatively affect our profitability.

The development, manufacture, sale and use of our products involve a risk of warranty and product liability claims. Our product liability insurance policies have limits that, if exceeded, may result in material costs that would have an adverse effect on our future profitability. In addition, warranty claims are not covered by our product liability insurance and there may be types of product liability claims that are also not covered by our product liability insurance.

We depend on our senior leadership team and the loss of our chief executive officer or one or more key employees or an inability to attract and retain highly skilled employees could adversely affect our business.

Our success depends largely upon the continued services of our officers and senior leadership team. In particular, our chief executive officer, Gary D. Fields, is critical to our vision, strategic direction, culture, and overall business success. Furthermore, Mr. Fields' extensive industry knowledge and sales-channel experience would be difficult to replace. We also rely on our senior leadership team in the areas of research and development, marketing, production, sales, and general and administrative functions. From time to time, there may be changes in our senior leadership team resulting from the hiring or departure of senior leadership team members, which could disrupt our business. While we have have a robust succession plan in place for each one of our officers and senior leadership team members, the loss of one or more could have a serious adverse effect on our business.

We do not maintain key-man insurance for Gary D. Fields or any other member of our senior leadership team. We do not have employment agreements with our officers or senior leadership team members that require them to continue to work for us for any specified period and, therefore, they could terminate their employment with us at any time.

Operations may be affected by natural disasters, especially since most of our operations are performed at a single location.

Natural disasters such as tornadoes and ice storms, as well as accidents, acts of terror, infection, and other factors beyond our control could adversely affect our operations. Especially, as our facilities are in areas where tornadoes are likely to occur, and the majority of our operations are at our Tulsa facilities, the effects of natural disasters and other events could damage our facilities and equipment and force a temporary halt to manufacturing and other operations, and such events could consequently cause severe damage to our business. We maintain insurance against these sorts of events ($100 million of total coverage with a per occurrence deductible of $7.5 million); however, this is not guaranteed to cover all the losses and damages incurred. Furthermore, we may experience increases in our insurance premium costs in relation to these matters that may have a material adverse effect upon our business, liquidity, financial condition, or results of operations.

If we are unable to hire, develop or retain employees, it could have an adverse effect on our business.

We compete to hire new employees and then seek to train them to develop their skills. We may not be able to successfully recruit, develop, and retain the personnel we need. Unplanned turnover or failure to hire and retain a diverse, skilled workforce, could increase our operating costs and adversely affect our results of operations.

Variability in self-insurance liability estimates could impact our results of operations.

We self-insure for employee health insurance and workers’ compensation insurance coverage up to a predetermined level, beyond which we maintain stop-loss insurance from a third-party insurer for claims over $225,000 and $750,000 for employee health insurance claims and workers’ compensation insurance claims, respectively. Our aggregate exposure varies from year to year based upon the number of participants in our insurance plans. We estimate our self-insurance liabilities using an analysis provided by our claims administrator and our historical claims experience. Our accruals for insurance reserves reflect these estimates and other management judgments, which are subject to a high degree of variability. If the number or severity of claims for which we self-insure increases, it could cause a material and adverse change to our reserves for self-insurance liabilities, as well as to our earnings.

9

Risks Related to Our Brand and Product Offerings

We may not be able to compete favorably in the highly competitive HVAC business.

Competition in our various markets could cause us to reduce our prices or lose market share, which could have an adverse effect on our future financial results. Substantially all of the markets in which we participate are highly competitive. The most significant competitive factors we face are product reliability, product performance, service, and price, with the relative importance of these factors varying among our product line. Other factors that affect competition in the HVAC market include the development and application of new technologies and an increasing emphasis on the development of more efficient HVAC products. Moreover, new product introductions are an important factor in the market categories in which our products compete. Several of our competitors have greater financial and other resources than we have, allowing them to invest in more extensive research and development. We may not be able to compete successfully against current and future competition and current and future competitive pressures faced by us may materially adversely affect our business and results of operations.

We may not be able to successfully develop and market new products.

Our future success will depend upon our continued investment in research and new product development and our ability to continue to achieve new technological advances in the HVAC industry. Our inability to continue to successfully develop and market new products or our inability to implement technological advances on a pace consistent with that of our competitors could lead to a material adverse effect on our business and results of operations. Furthermore, our continued investment in new product development may render certain legacy products and components obsolete resulting in increased inventory obsolescence expense that may have a material adverse effect upon our financial condition or results of operations.

Risks Related to Material Sourcing and Supply

We may be adversely affected by problems in the availability, or increases in the prices, of raw materials and components.

Problems in the availability, or increases in the prices, of raw materials or components could depress our sales or increase the costs of our products. We are dependent upon components purchased from third parties, as well as raw materials such as steel, copper and aluminum. Occasionally, we enter into cancellable and non-cancellable contracts on terms from six to 18 months for raw materials and components at fixed prices. However, if a key supplier is unable or unwilling to meet our supply requirements, we could experience supply interruptions or cost increases, either of which could have an adverse effect on our gross profit.

We risk having losses resulting from the use of non-cancellable fixed price contracts.

Historically, we have attempted to limit the impact of price fluctuations on commodities by entering into non-cancellable fixed price contracts with our major suppliers for periods of six to 18 months. We expect to receive delivery of raw materials from our fixed price contracts for use in our manufacturing operations. These fixed price contracts are not accounted for using hedge accounting since they meet the normal purchases and sales exemption.

10

Risks Related to Electronic Data Processing and Digital Information

Our business is subject to the risks of interruptions by cybersecurity attacks.

We depend upon information technology infrastructure, including network, hardware and software systems to conduct our business. Despite our implementation of network and other cybersecurity measures, our information technology system and networks could be disrupted due to technological problems, a cyber-attack, acts of terrorism, severe weather, a solar event, an electromagnetic event, a natural disaster, the age and condition of information technology assets, human error, or other reasons. To date, we have not experienced a material impact to our business or operations resulting from cyber-security or other similar information attacks, but due to the ever-evolving attack methods, as well as the increased amount and level of sophistication of these attacks, our security measures may not be adequate to protect against highly targeted sophisticated cyber-attacks, or other improper disclosures of confidential and/or sensitive information. Additionally, we may have access to confidential or other sensitive information of our customers, which, despite our efforts to protect, may be vulnerable to security breaches, theft, or other improper disclosure. Any cyber-related attack or other improper disclosure of confidential information could have a material adverse effect on our business, as well as other negative consequences, including significant damage to our reputation, litigation, regulatory actions, and increased cost. The Company maintains cyber-security insurance, however, the coverage may not be sufficient to cover all financial losses.

Risks Related to Governmental Regulation and Policies

Exposure to environmental liabilities could adversely affect our results of operations.

Our future profitability could be adversely affected by current or future environmental laws. We are subject to extensive and changing federal, state and local laws and regulations designed to protect the environment in the United States and in other parts of the world. These laws and regulations could impose liability for remediation costs and result in civil or criminal penalties in case of non-compliance. Compliance with environmental laws increases our costs of doing business. Because these laws are subject to frequent change, we are unable to predict the future costs resulting from environmental compliance.

We are subject to potentially extreme governmental regulations and policies.

We always face the possibility of new governmental regulations, policies and trade agreements which could have a substantial or even extreme negative effect on our operations and profitability. Several intrusive component part governmental regulations are in process. If these proposals become final rules, the effect would be the regulation of compressors and fans in products for which the Department of Energy does not have current authority. This could affect equipment we currently manufacture and could have an impact on our product design, operations, and profitability.

The Dodd-Frank Wall Street Reform and Consumer Protection Act contains provisions to improve transparency and accountability concerning the supply of certain minerals, known as “conflict minerals”, originating from the Democratic Republic of Congo and adjoining countries. As a result, in August 2012, the SEC adopted annual disclosure and reporting requirements for those companies who use conflict minerals in their products. Accordingly, we began our reasonable country of origin inquiries in fiscal year 2013, with initial disclosure requirements beginning in May 2014. There are costs associated with complying with these disclosure requirements, including for due diligence to determine the sources of conflict minerals used in our products and other potential changes to products, processes or sources of supply as a consequence of such verification activities. The implementation of these rules could adversely affect the sourcing, supply, and pricing of materials used in our products. As there may be only a limited number of suppliers offering “conflict free” conflict minerals, we cannot be sure that we will be able to obtain necessary conflict minerals from such suppliers in sufficient quantities or at competitive prices. Also, we may face reputational challenges if we determine that certain of our products contain minerals not determined to be conflict free or if we are unable to sufficiently verify the origins for all conflict minerals used in our products through the procedures we may implement.

Our operations could be negatively impacted by new legislation as well as changes in regulations and trade agreements, including tariffs and taxes. Unfavorable conditions resulting from such changes could have a material adverse effect on our business, financial condition and results of operations.

11

We are subject to adverse changes in tax laws.

Our tax expense or benefits could be adversely affected by changes in tax provisions, unfavorable findings in tax examinations, or differing interpretations by tax authorities. We are unable to estimate the impact that current and future tax proposals and tax laws could have on our results of operations. We are currently subject to state and local tax examinations for which we do not expect any major assessments.

We are subject to international regulations that could adversely affect our business and results of operations.

Due to our use of representatives in foreign markets, we are subject to many laws governing international relations, including those that prohibit improper payments to government officials and commercial customers, and restrict where we can do business, what information or products we can supply to certain countries and what information we can provide to a non-U.S. government, including but not limited to the Foreign Corrupt Practices Act, U.K. Bribery Act and the U.S. Export Administration Act. Violations of these laws, which are complex, may result in criminal penalties or sanctions that could have a material adverse effect on our business, financial condition and results of operations.

Risks Inherent to an Investment in AAON, Inc.

In the fourth quarter of 2019, we identified a material weakness in our internal control over financial reporting. Our failure to establish and maintain effective internal control over financial reporting could result in material misstatements in our financial statements and cause investors to lose confidence in our reported financial information, which in turn could cause the trading price of our outstanding stock to decline.

During the year ended December 31, 2019, we identified a material weakness in our internal control over financial reporting related to the appropriate policies and procedures in place to properly recognize share-based compensation for retirement eligible participants in our Long-Term Incentive Plans. For further information regarding this matter, please refer to Item 9A. Controls and Procedures in the 2019 Annual Report on Form 10-K for further information and Item 4b. Controls and Procedures in the March 31, 2020 Quarterly Report on Form 10-Q for remediation efforts in 2020. We concluded that this material weakness was remediated as of March 31, 2020.

Management’s ongoing assessment of internal control over financial reporting may in the future identify additional weaknesses and conditions that need to be addressed. Any failure to improve our internal control over financial reporting to address identified weaknesses in the future, if they were to occur, could prevent us from maintaining accurate accounting records and discovering material accounting errors, which in turn, could adversely affect our business and the value of our outstanding stock.

We corrected certain of our previously issued consolidated financial statements, which may affect investor confidence and raise reputational issues.

As discussed in the Explanatory Note preceding Item 1, Business, in Note 2, Error Correction, and in Note 25, Quarterly Results (Unaudited), in the 2019 Annual Report on Form 10-K, we reached a determination to correct our consolidated financial statements at December 31, 2018 and for the years ended December 31, 2018 and December 31, 2017, selected financial data at and for the year ended December 31, 2016 and 2015, and each of the unaudited quarterly periods September 30, 2019, June 30, 2019, March 31, 2019, December 31, 2018, September 31, 2018, June 30, 2018 and March 31, 2018. These corrections were presented in the 2019 Annual Report on Form 10-K. As a result, we have become subject to a number of additional risks and uncertainties, which may affect investor confidence in the accuracy of our financial disclosures and may raise reputational issues for our business.

Item 1B. Unresolved Staff Comments.

None.

12

Item 2. Properties.

As of December 31, 2020, we own all of our Tulsa, Oklahoma, and Longview, Texas, facilities, consisting of approximately two million square feet of space for office, manufacturing, research and development, warehouse, assembly operations, and parts sales. We believe that our facilities are well maintained and are in good condition and suitable for the conduct of our business.

Our plant and office facilities in Tulsa, Oklahoma, consist of a 342,000 sq. ft. building (327,000 sq. ft. of manufacturing/warehouse space and 15,000 sq. ft. of office space) located on a 12-acre tract of land at 2425 South Yukon Avenue, and a 940,000 sq. ft. manufacturing/warehouse building and a 70,000 sq. ft. office building located on an approximately 79-acre tract of land across the street from the original facility (2440 South Yukon Avenue) (collectively, the “Tulsa facilities”).

Our plant and office facilities in Longview, Texas, consist of a 263,000 sq. ft. building (256,000 sq. ft. of manufacturing/warehouse space and 7,000 sq. ft. of office space) located on a 13-acre tract of land at 203-207 Gum Springs Road. In August 2019, construction began, adjacent to our current Longview, Texas facilities, on a 224,000 sq. ft. building expansion (210,000 sq. ft. of manufacturing/warehouse space and 12,000 sq. ft. of office space) located on an approximately 22-acre tract of land. The new building was completed and became operational in early 2021 and will be used for both equipment manufacturing operations and coil warehouse storage.

Our manufacturing areas are heavy industrial type buildings, with some coverage by overhead cranes, containing manufacturing equipment designed for sheet metal fabrication and metal stamping. The manufacturing equipment contained in the facilities consists primarily of automated sheet metal fabrication equipment, supplemented by presses. Assembly lines consist of cart-type and roller-type conveyor lines with variable line speed adjustment, which are motor driven. Subassembly areas and production line manning are based upon line speed.

Our operations in Parkville, Missouri, are conducted in a leased plant/office at 8500 NW River Park Drive, containing 51,000 sq. ft. We believe that the leased facility is well maintained and in good condition and suitable for the conduct of our business.

In addition to a retail parts store location at our Tulsa facilities, we also own a 13,500 sq. ft. stand alone building (7,500 sq. ft. warehouse and 6,000 sq. ft. office) which is utilized as an additional retail parts store to provide our customers more accessibly to our products. The building is on approximately one acre and is located at 9528 E 51st St in Tulsa, Oklahoma.

In 2019, we opened our new engineering research and development laboratory at the Tulsa facilities, since named the Norman Asbjornson Innovation Center. The three-story 134,000 square foot stand alone facility is both an acoustical and a performance measuring laboratory. This facility currently consists of ten test chambers, two more test chambers to be completed in first quarter 2021, allowing AAON to meet and maintain industry certifications. This facility is located West of the 940,000 sq. ft. manufacturing/warehouse building at 2425 South Yukon Avenue.

Item 3. Legal Proceedings.

We are not a party to any pending legal proceeding which management believes is likely to result in a material liability and no such action has been threatened against us, or, to the best of our knowledge, is contemplated.

Item 4. Mine Safety Disclosure.

Not applicable.

PART II

13

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock is quoted on the NASDAQ Global Select Market under the symbol “AAON”. The table below summarizes the intraday high and low reported sale prices for our common stock for the past two fiscal years. As of the close of business on February 22, 2021, there were 964 holders of record of our common stock.

| Quarter Ended | High | Low | ||||||||||||

| March 31, 2019 | $46.69 | $33.52 | ||||||||||||

| June 30, 2019 | $52.50 | $44.36 | ||||||||||||

| September 30, 2019 | $53.27 | $43.34 | ||||||||||||

| December 31, 2019 | $51.07 | $42.57 | ||||||||||||

| March 31, 2020 | $60.00 | $40.48 | ||||||||||||

| June 30, 2020 | $59.35 | $43.84 | ||||||||||||

| September 30, 2020 | $61.24 | $52.56 | ||||||||||||

| December 31, 2020 | $69.41 | $56.27 | ||||||||||||

Dividends - At the discretion of the Board of Directors, we pay semi-annual cash dividends. Board approval is required to determine the date of declaration and amount for each semi-annual dividend payment.

Our recent dividends are as follows:

| Declaration Date | Record Date | Payment Date | Dividend per Share | ||||||||

| May 18, 2018 | June 8, 2018 | July 6, 2018 | $0.16 | ||||||||

| November 8, 2018 | November 29, 2018 | December 20, 2018 | $0.16 | ||||||||

| May 20, 2019 | June 3, 2019 | July 1, 2019 | $0.16 | ||||||||

| November 6, 2019 | November 27, 2019 | December 18, 2019 | $0.16 | ||||||||

| May 15, 2020 | June 3, 2020 | July 1, 2020 | $0.19 | ||||||||

| November 10, 2020 | November 27, 2020 | December 18, 2020 | $0.19 | ||||||||

14

The following is a summary of our share-based compensation plans as of December 31, 2020:

| EQUITY COMPENSATION PLAN INFORMATION | ||||||||||||||||||||

| Plan category | (a) Number of securities to be issued upon exercise of outstanding options, warrants and rights | (b) Weighted-average exercise price of outstanding options, warrants and rights | (c) Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) | |||||||||||||||||

| The 2007 Long-Term Incentive Plan | 214,780 | $ | 18.80 | — | ||||||||||||||||

| The 2016 Long-Term Incentive Plan | 525,281 | $ | 37.18 | 4,228,769 | ||||||||||||||||

Repurchases during the fourth quarter of 2020, which include repurchases from our open market, 401(k) and employee repurchase programs, were as follows:

| ISSUER PURCHASES OF EQUITY SECURITIES | ||||||||||||||||||||||||||

(a) Total Number of Shares (or Units | (b) Average Price Paid (Per Share | (c) Total Number of Shares (or Units) Purchased as part of Publicly Announced | (d) Maximum Number (or Approximate Dollar Value) of Shares (or Units) that may yet be Purchased under the | |||||||||||||||||||||||

| Period | Purchased) | or Unit) | Plans or Programs | Plans or Programs | ||||||||||||||||||||||

| October 2020 | 48,353 | $ | 62.73 | 48,353 | — | |||||||||||||||||||||

| November 2020 | 50,651 | 64.42 | 50,651 | — | ||||||||||||||||||||||

| December 2020 | 37,423 | 64.48 | 37,423 | — | ||||||||||||||||||||||

| Total | 136,427 | $ | 63.84 | 136,427 | — | |||||||||||||||||||||

15

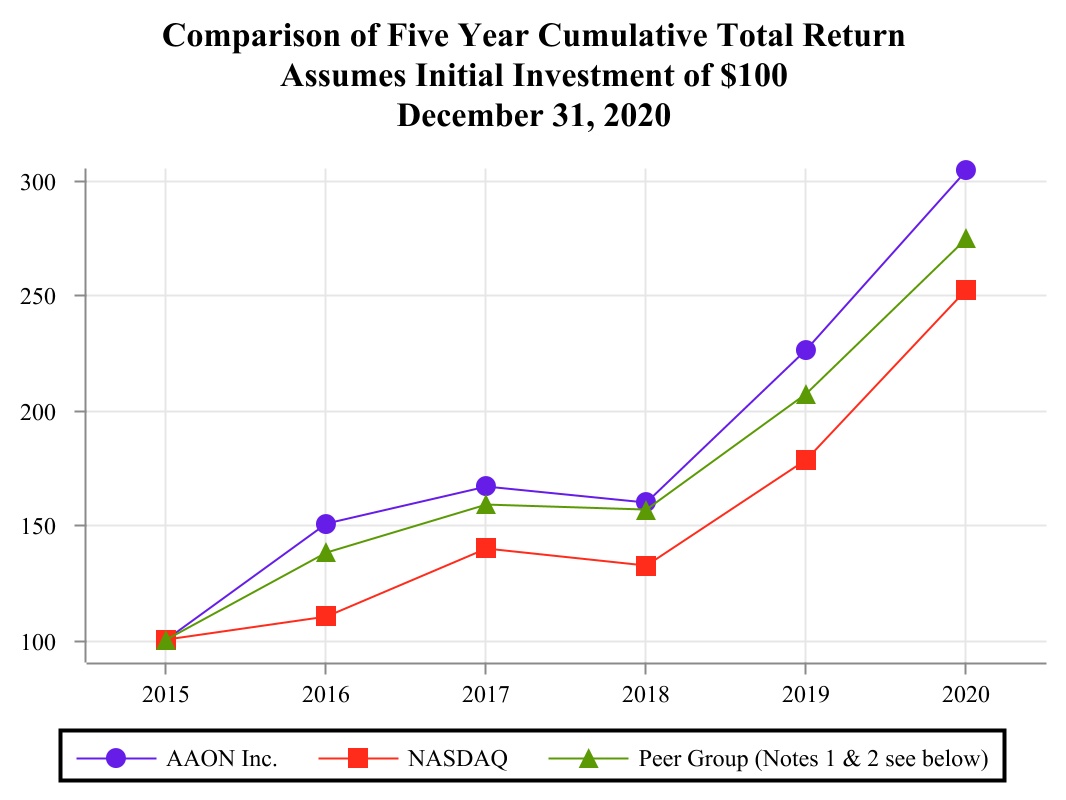

Comparative Stock Performance Graph

The following performance graph compares our cumulative total shareholder return, the NASDAQ Composite and a peer group of publically traded U.S. industrial manufacturing companies in the air conditioning, ventilation, and heating exchange equipment markets from December 31, 2015 through December 31, 2020. Our peer group includes Lennox International, Inc., Trane Technologies plc (formerly Ingersoll-Rand plc), Johnson Controls International plc, and Carrier Global Corporation (formerly United Technologies Corporation). The graph assumes that $100 was invested at the close of trading December 31, 2015, with reinvestment of dividends. This table is not intended to forecast future performance of our Common Stock.

1On March 2, 2020, Trane Technologies PLC (formerly known as Ingersoll-Rand plc) spun off its industrial assets, which made up over 50% of the company’s sales. Thus, historical stock performance prior to the divestiture is not fully representative of the current company’s assets.

2On April 3, 2020, Carrier Global Corporation was spun off from its parent company, United Technologies Corporation. We have included Carrier's cumulative total shareholder return from April 3, 2020 through December 31, 2020 assuming $100 was invested at the close of trading on April 3, 2020.

This stock performance graph is not deemed to be “soliciting material” or otherwise be considered to be “filed” with the SEC or subject to Regulation 14A or 14C under the Securities Exchange Act of 1934 (Exchange Act) or to the liabilities of Section 18 of the Exchange Act, and should not be deemed to be incorporated by reference into any filing under the Securities Act of 1933 or the Exchange Act, except to the extent the Company specifically incorporates it by reference into such a filing.

16

Item 6. Selected Financial Data.

The following selected financial data should be read in conjunction with our Financial Statements and Supplementary Data thereto included under Item 8 of this report and Management’s Discussion and Analysis of Financial Condition and Results of Operations contained in Item 7.

| Years Ended December 31, | |||||||||||||||||||||||||||||

| Results of Operations: | 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||||||||

| (in thousands, except per share data) | |||||||||||||||||||||||||||||

| Net sales | $ | 514,551 | $ | 469,333 | $ | 433,947 | $ | 405,232 | $ | 383,977 | |||||||||||||||||||

| Net income | $ | 79,009 | $ | 53,711 | $ | 42,329 | $ | 53,830 | $ | 53,020 | |||||||||||||||||||

| Earnings per share: | |||||||||||||||||||||||||||||

| Basic | $ | 1.51 | $ | 1.03 | $ | 0.81 | $ | 1.02 | $ | 1.00 | |||||||||||||||||||

| Diluted | $ | 1.49 | $ | 1.02 | $ | 0.80 | $ | 1.01 | $ | 0.99 | |||||||||||||||||||

| Cash dividends declared per common share: | $ | 0.38 | $ | 0.32 | $ | 0.32 | $ | 0.26 | $ | 0.24 | |||||||||||||||||||

| December 31, | |||||||||||||||||||||||||||||

| Financial Position at End of Fiscal Year: | 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||||||||

| (in thousands) | |||||||||||||||||||||||||||||

| Working capital | $ | 161,218 | $ | 131,521 | $ | 93,167 | $ | 104,002 | $ | 102,287 | |||||||||||||||||||

| Total assets | 449,008 | 371,424 | 307,994 | 296,590 | 256,335 | ||||||||||||||||||||||||

| Revolving credit facility | — | — | — | — | — | ||||||||||||||||||||||||

| New market tax credit obligation | 6,363 | 6,320 | — | — | — | ||||||||||||||||||||||||

| Total stockholders’ equity | 350,865 | 290,140 | 249,443 | 238,925 | 208,410 | ||||||||||||||||||||||||

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Overview

The following discussion should be read in conjunction with the other sections of this Annual Report on Form 10-K, including the consolidated financial statements and related notes contained in Item 8, Financial Statements and Supplementary Data.

Description of the Company

We engineer, manufacture, market, and sell air conditioning and heating equipment consisting of standard, semi-custom, and custom rooftop units, chillers, packaged outdoor mechanical rooms, air handling units, makeup air units, energy recovery units, condensing units, geothermal/water-source heat pump, coils, and controls. These products are marketed and sold to retail, manufacturing, educational, lodging, supermarket, medical, and other commercial industries. We market our products to all 50 states in the United States and certain provinces in Canada.

Our business can be affected by a number of economic factors, including the level of economic activity in the markets in which we operate. The recent uncertainty of the economy has negatively impacted the commercial and industrial new construction markets. A further decline in economic activity could result in a decrease in our sales volume and profitability. Sales in the commercial and industrial new construction markets correlate closely to the number of new homes and buildings that are built, which in turn is influenced by cyclical factors such as interest rates, inflation, consumer spending habits, employment rates, and other macroeconomic factors over which we have no control.

17

We sell our products to property owners and contractors through a network of independent manufacturers’ representatives and our internal sales force. The demand for our products is influenced by national and regional economic and demographic factors. The commercial and industrial new construction market is subject to cyclical fluctuations in that it is generally tied to housing starts, but has a lag factor of six to 18 months. Housing starts, in turn, are affected by such factors as interest rates, the state of the economy, population growth, and the relative age of the population. When new construction is down, we emphasize the replacement market. The new construction market in 2020 continued to be unpredictable and uneven. Thus, throughout the year, we emphasized promotion of the benefits of AAON equipment to property owners in the replacement market.

The principal components of cost of sales are labor, raw materials, component costs, factory overhead, freight out, and engineering expense. The principal high volume raw materials used in our manufacturing processes are steel, copper, and aluminum. We also purchase from other manufacturers certain components, including compressors, motors, and electrical controls.

The price levels of our raw materials fluctuate given that the market continues to be volatile and unpredictable as a result of the uncertainty related to the U.S. economy and global economy. For the year ended December 31, 2020, the prices for copper, galvanized steel, stainless steel and aluminum increased approximately 0.6%, 12.2%, 8.5%, and 12.8%, respectively, from 2019. For the year ended December 31, 2019, the prices for copper, galvanized steel and stainless steel decreased approximately 3.2%, 5.8%, 2.3%, and 1.6%, respectively, from 2018.

We attempt to limit the impact of price fluctuations on these materials by entering into cancellable and non-cancellable fixed price contracts with our major suppliers for periods of six to 18 months. We expect to receive delivery of raw materials from our fixed price contracts for use in our manufacturing operations.

The following are highlights of our results of operations, cash flows, and financial condition:

•In 2020, we fully realized the price increases put in place during 2019.

•We continued to become more efficient. Our gross profit percentage improved from 25.4% during the year ended in 2019 to 30.3% in 2020 despite employee absenteeism, mostly in June, related to COVID-19.

•Our warranty expense has continued to improve from 2018 through 2020.

•We honored our founder and Executive Chairman, Norman Asbjornson, with a donation to Winifred Public Schools of $1.25 million.

•With a record year, were able to reward our employees with increased profit sharing and bonuses.

•We spent $67.8 million in capital expenditures in 2020, over half of which was for our new building in Longview, Texas.

•We recognized a gain of $6.4 million from the receipt of insurance proceeds related to our roof on our Tulsa facility that sustained hail damage in the spring.

•Total cash, cash equivalents and restricted cash was $82.3 million at December 31, 2020.

Results of Operations

Units sold for years ended December 31:

| 2020 | 2019 | 2018 | ||||||||||||||||||

| Rooftop Units | 15,713 | 14,448 | 15,273 | |||||||||||||||||

| Condensing Units | 1,920 | 1,738 | 2,007 | |||||||||||||||||

| Air Handlers | 2,073 | 2,372 | 2,500 | |||||||||||||||||

| Outdoor Mechanical Rooms | 33 | 33 | 38 | |||||||||||||||||

| Water-Source Heat Pumps | 6,492 | 7,716 | 5,334 | |||||||||||||||||

| Total Units | 26,231 | 26,307 | 25,152 | |||||||||||||||||

18

Year Ended December 31, 2020 vs. Year Ended December 31, 2019

Net Sales

| Years Ended December 31, | |||||||||||||||||||||||

| 2020 | 2019 | $ Change | % Change | ||||||||||||||||||||

| (in thousands, except unit data) | |||||||||||||||||||||||

| Net sales | $ | 514,551 | $ | 469,333 | $ | 45,218 | 9.6 | % | |||||||||||||||

| Total units | 26,231 | 26,307 | (76) | (0.3) | % | ||||||||||||||||||

Our sales increased 9.6%, or $45.2 million mostly due to the increase in rooftop sales which increased by $51.5 million (increase of 15%). The increase in rooftop units sales was due in part to our increased sheet metal production from the additional Salvagnini machines that were placed into operation allowing increased production (1,265 units or 9% unit increase over 2019) and from price increases put in place over the last year.

Cost of Sales

| Years Ended December 31, | Percent of Sales | |||||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||||

| Cost of sales | $ | 358,702 | $ | 349,908 | 69.7 | % | 74.6 | % | ||||||||||||||||||

| Gross Profit | $ | 155,849 | $ | 119,425 | 30.3 | % | 25.4 | % | ||||||||||||||||||

The principal components of cost of sales are labor, raw materials, component costs, factory overhead, freight out, and engineering expense. The principal high volume raw materials used in our manufacturing processes are steel, copper, and aluminum. As shown below, our average raw material prices increased during the year. However, the Company had increased its inventory levels in 2019 and early 2020 at lower prices and was able to benefit from these lower priced raw materials as the stock was consumed in 2020. The Company continues to closely monitor its raw materials prices to try and purchase quantities when there are dips in the market. The Company improved its labor and overhead efficiencies with our new sheet metal machines that were placed into service in the last quarter of 2019 and early 2020, eliminating any bottlenecks in our sheet metal production. The Company's headcount was also down compared to 2019, resulting in a higher production output per employee.

Twelve month average raw material cost per pound as of December 31:

| 2020 | 2019 | % Change | ||||||||||||||||||

| Copper | $ | 3.65 | $ | 3.63 | 0.6 | % | ||||||||||||||

| Galvanized Steel | $ | 0.55 | $ | 0.49 | 12.2 | % | ||||||||||||||

| Stainless Steel | $ | 1.41 | $ | 1.30 | 8.5 | % | ||||||||||||||

| Aluminum | $ | 2.02 | $ | 1.79 | 12.8 | % | ||||||||||||||

19

Selling, General and Administrative Expenses

| Years Ended December 31, | Percent of Sales | |||||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||||

| Warranty | $ | 6,621 | $ | 8,047 | 1.3 | % | 1.7 | % | ||||||||||||||||||

| Profit Sharing | 11,593 | 7,448 | 2.3 | % | 1.6 | % | ||||||||||||||||||||

| Salaries & Benefits | 20,159 | 13,394 | 3.9 | % | 2.9 | % | ||||||||||||||||||||

| Stock Compensation | 5,341 | 6,690 | 1.0 | % | 1.4 | % | ||||||||||||||||||||

| Advertising | 823 | 818 | 0.2 | % | 0.2 | % | ||||||||||||||||||||

| Depreciation | 1,999 | 1,524 | 0.4 | % | 0.3 | % | ||||||||||||||||||||

| Insurance | 1,066 | 805 | 0.2 | % | 0.2 | % | ||||||||||||||||||||

| Professional Fees | 2,514 | 2,738 | 0.5 | % | 0.6 | % | ||||||||||||||||||||

| Donations | 2,115 | 1,137 | 0.4 | % | 0.2 | % | ||||||||||||||||||||

| Bad Debt Expense | 153 | 91 | — | % | — | % | ||||||||||||||||||||

| Other | 8,107 | 9,385 | 1.6 | % | 2.0 | % | ||||||||||||||||||||

| Total SG&A | $ | 60,491 | $ | 52,077 | 11.8 | % | 11.1 | % | ||||||||||||||||||

The Company experienced a decrease in warranty claims paid of 15.6% in 2020. Our profit sharing expenses are up due to higher earnings. Salaries & benefits increased due to additional bonuses and employee incentives. Stock compensation was lower because the valuation of the Company-wide equity grant awarded in March 2020 was less than the grant awarded in March 2019. Donations increased due to the contribution of approximately $1.3 million to Winifred, Montana Public Schools in recognition of Norman H. Asbjornson's transition from CEO to Executive Chairman.

Income Taxes

| Years Ended December 31, | Effective Tax Rate | |||||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||||

| Income tax provision | $ | 22,966 | $ | 13,320 | 22.5 | % | 19.9 | % | ||||||||||||||||||

Upon completion of the Company's 2018 tax return in 2019, the Company recorded additional benefit due to higher than expected research and development credit of $0.6 million. Additionally in 2019, the Company determined it could take advantage of an additional 1% tax credit in Oklahoma for years in which the Company's location was deemed to be within an enterprise zone. The additional Oklahoma Credit for being in an enterprise zone, or otherwise allowable under Oklahoma law, resulted in a benefit of $1.2 million.

20

Year Ended December 31, 2019 vs. Year Ended December 31, 2018

Net Sales

| Years Ended December 31, | |||||||||||||||||||||||

| 2019 | 2018 | $ Change | % Change | ||||||||||||||||||||

| (in thousands, except unit data) | |||||||||||||||||||||||

| Net sales | $ | 469,333 | $ | 433,947 | $ | 35,386 | 8.2 | % | |||||||||||||||

| Total units | 26,307 | 25,152 | 1,155 | 4.6 | % | ||||||||||||||||||

Most of the increase in revenues was due to our price increases in 2018 which were realized during 2019. Additionally, our parts sales and water-source heat pumps sales grew with increases of $7.0 million and $10.8 million, respectively.

Cost of Sales

| Years Ended December 31, | Percent of Sales | |||||||||||||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||||

| Cost of sales | $ | 349,908 | $ | 330,414 | 74.6 | % | 76.1 | % | ||||||||||||||||||

| Gross Profit | $ | 119,425 | $ | 103,533 | 25.4 | % | 23.9 | % | ||||||||||||||||||