| OMB APPROVAL |

| OMB Number: |

| 3235-0570 |

| Expires: January |

| 31, 2017 |

| Estimated average |

| burden hours per |

| response: 20.6 |

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| FORM N-CSR |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT |

| INVESTMENT COMPANIES |

| Investment Company Act file number: 811-05371 |

| Russell Investment Funds |

| (Exact name of registrant as specified in charter) |

| 1301 2nd Avenue 18th Floor, Seattle Washington 98101 |

| (Address of principal executive offices) (Zip code) |

| Mary Beth R. Albaneze, Secretary and Chief Legal Officer |

| Russell Investment Funds |

| 1301 2nd Avenue |

| 18th Floor |

| Seattle, Washington 98101 |

| 206-505-4846 |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: 800-787-7354 | |

| Date of fiscal year end: | December 31 |

| Date of reporting period: | January 1, 2014 to December 31, 2014 |

Item 1. Reports to Stockholders

![]()

2014 ANNUAL REPORT

Russell Investment Funds

DECEMBER 31, 2014

FUND

Multi-Style Equity Fund

Aggressive Equity Fund

Non-U.S. Fund

Core Bond Fund

Global Real Estate Securities Fund

Russell Investment Funds

Russell Investment Funds is a series investment company with nine different investment portfolios referred to as Funds. These financial statements report on five of these Funds.

Russell Investment Funds

Annual Report

December 31, 2014

Table of Contents

| To Our Shareholders ........................................................................................... 3 |

| Market Summary ................................................................................................. 4 |

| Multi-Style Equity Fund ...................................................................................... 14 |

| Aggressive Equity Fund ...................................................................................... 32 |

| Non-U.S. Fund .................................................................................................. 52 |

| Core Bond Fund ................................................................................................ 72 |

| Global Real Estate Securities Fund .................................................................... 106 |

| Notes to Schedules of Investments .................................................................... 124 |

| Notes to Financial Highlights ............................................................................. 126 |

| Notes to Financial Statements ........................................................................... 127 |

| Report of Independent Registered Public Accounting Firm ................................ 147 |

| Tax Information ................................................................................................ 148 |

| Affiliated Brokerage Transactions ..................................................................... 149 |

| Basis for Approval of Investment Advisory Contracts ....................................... 150 |

| Shareholder Requests for Additional Information .............................................. 161 |

| Disclosure of Information about Fund Trustees and Officers .............................. 162 |

| Adviser, Money Managers and Service Providers ............................................. 167 |

Russell Investment Funds

Copyright © Russell Investments 2015. All rights reserved.

Russell Investments is a Washington, USA corporation, which operates through subsidiaries worldwide and is part of London Stock Exchange Group.

Fund objectives, risks, charges and expenses should be carefully considered before investing. A prospectus containing this and other important information must precede or accompany this material. Please read the prospectus carefully before investing.

Securities distributed through Russell Financial Services, Inc., member FINRA and part of Russell Investments.

Indices and benchmarks are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Index return information is provided by vendors and although deemed reliable, is not guaranteed by Russell Investments or its affiliates.

Russell Investments is the owner of the trademarks, service marks, and copyrights related to its respective indexes.

Performance quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted.

To Our Shareholders

Dear Shareholder,

After strong performance in 2013, equity markets in the U.S. continued to move higher through the end of December 2014.

The broad-based Russell 3000® Index returned 12.56% for the year ending December 31, 2014.

A number of factors contributed to this strong performance. After a somewhat slow start, the U.S economy has shown its resilience as corporate profits remain robust. Unemployment dropped below 6% in October for the first time since July 2008. And inflation remained tame, standing at just 1.3% through November 30, 2014.

At the same time, global markets contended with their fair share of concerns: instability in the Middle East, an Ebola outbreak in western Africa that spread fears across the globe, and unrest in the Ukraine. Add to that doubts about Europe’s economic recovery and a burst of volatility in the U.S. equity and Treasury markets in the fourth quarter and you might wonder how U.S. markets had such a strong year.

What all of this shows us is that the markets can – and often do – react to short-term events. But what matters most is to have a thoughtful financial plan, a long-term investment horizon, and a diversified, multi-asset portfolio that can weather periods of market volatility. We believe your financial advisor can also play a critical role in helping you stay on track and focus on your financial goals.

On the following pages you can gain additional insights on the markets and your investments by reviewing our Russell Investment Funds’ 2014 Annual Report for the fiscal year ending December 31, 2014, including portfolio management discussions and fund performance information.

Thank you for the trust you have placed in our firm. All of us at Russell Investments appreciate the opportunity to help you achieve financial security.

CEO, U.S. Private Client Services

Russell Investment Management Company

To Our Shareholders 3

Russell Investment Funds

Market Summary as of December 31, 2014 (Unaudited)

U.S. Equity Markets

The U.S. equity market performed well during the fiscal year ended December 31, 2014 despite various geopolitical concerns and the end of U.S. quantitative easing. Broadly measured by the Russell 3000® Index, U.S. stocks returned 12.56% over the year, which is the sixth straight calendar year that the Russell 3000® Index has finished with a positive absolute return. The Russell 3000® Index finished flat or higher in nine of the year’s twelve months, with exceptions in January, July, and September.

During the year, larger capitalization stocks were rewarded as the Russell 1000® Index outpaced the Russell 2000® Index by 8.35%, with the indexes returning 13.24% and 4.89% respectively. The year was led by defensive stocks, as the Russell 1000® Defensive™ Index returned 13.80% while the Russell 1000® Dynamic™ Index returned 12.64%. The Russell 1000® Value Index returned 13.45% compared to 13.05% for the Russell 1000® Growth Index. Although value stocks slightly edged out growth stocks, the cheapest stocks (those with the lowest price-to-book ratios and lowest price-to-earnings ratios) lagged the market. Interest rate sensitive areas of the market, specifically electric utilities and real estate investment trusts (“REITs”), outpaced the broader market returning 28.86% and 28.17%, respectively as measured by the Russell 1000® Index. Within the Russell 1000® Index, stocks that were rewarded during the year included stocks with rising earnings estimates, low earnings variability, and positive earnings surprises. On the other hand, stocks that underperformed included high beta stocks (stocks with high price sensitivity to market movements) and stocks with high financial quality (lowest debt-to-capital ratios).

U.S. equities rebounded from a challenging start to 2014 to record positive returns for the first quarter, with the Russell 3000® Index returning 1.97%. The Russell 1000 Index returned 2.05% and the Russell 1000® Value Index surged near the end of the quarter to end with a 3.02% quarterly return, surpassing the Russell 1000® Growth Index return of 1.12%. The small cap Russell 2000® Index lagged the Russell 1000® Index with a return of 1.12%. There was almost no differentiation between defensive and dynamic stocks with the Russell 1000® Defensive Index returning 2.00% and the Russell 1000® Dynamic™ Index returning 2.09% for the first quarter.

During the first quarter, investors shrugged off disappointing U.S. non-farm payroll numbers for December and January, which were generally blamed on unusually cold weather. Markets jumped considerably in February on “dovish” comments from Federal Reserve (the “Fed”) Chair Janet Yellen in her first Congressional testimony. In March, high dividend yield stocks briefly underperformed after comments from Yellen suggesting that U.S. short term interest rates may rise sooner than some were expecting, but the market’s focus quickly shifted to profit taking among momentum stocks during the final seven trading days of the quarter. The final U.S. gross domestic product (“GDP”) growth rate for the fourth quarter came in at 2.6%, slightly behind forecasts. Elsewhere, consumer confidence continued to improve and durable goods orders picked up in February. However, data suggested the U.S. housing market continued to slow. A series of concerns about Ukraine, Crimea, and Russia also kept a lid on market appreciation for the quarter.

The Russell 3000® Index gained 4.87% in the second quarter, ending the quarter at a new record high. The equity market was led by high dividend yield stocks early in the quarter, as investors bid up interest rate sensitive stocks in pursuit of more yield from equity oriented investments as long term interest rates fell. For the quarter, “bond substitutes” within the Russell 1000® Index (REITs and utilities) outperformed. The Russell 1000® Growth Index slightly edged out the Russell 1000® Value Index for the quarter, returning 5.13% compared to 5.10%, respectively. However within small cap space, the Russell 2000 Value Index beat the Russell 2000® Growth Index. Elsewhere, dynamic stocks outperformed defensive stocks across various market capitalization levels. The payoff to market capitalization was mixed as the Russell Top 200 Index returned 5.18%, beating the broader Russell 1000® Index which climbed 5.12%, although the Russell Top 50 Mega Cap Index returned only 4.51%. The Russell 2000® Index lagged the Russell 2500 Index, returning 2.05% compared with 3.56% for the second quarter.

Economic data released during the second quarter generally provided indications of a continued economic expansion. The standout anomaly was the third revision to U.S. first-quarter real GDP (an inflation adjusted GDP measure), which

4 Market Summary

Russell Investment Funds

Market Summary as of December 31, 2014, continued — (Unaudited)

was sharply revised downward to -2.9% largely driven by a decrease in personal consumption expenditures. The Fed downwardly revised its 2014 GDP forecasts from 2.9% to 2.2%. Elsewhere, non-farm payrolls remained healthy, with June being the fifth straight month of growth above 200,000 jobs, which is the first time this has happened in 14 years. Meanwhile, the Fed cut its monthly asset purchases by $10 billion at each monthly meeting, reducing the amount to $35 billion at June’s meeting. Additionally, Fed Chair Yellen continued to reiterate the committee’s “dovish” tone, which helped enable the outperformance of interest rate sensitive stocks.

The Russell 3000® Index finished third quarter 2014 virtually unchanged from where it started the quarter. However, U.S. equities suffered negative returns in July and September. Geopolitical risks and negative investor reaction to the Fed’s monthly statement (which was perceived as being more hawkish) dragged down equities in July, while the sell-off in the final days of September was driven in part by fears of a potentially larger than anticipated rise in interest rates. The Russell 1000® Index gained 0.65% in the third quarter. The largest market gains came higher up the capitalization spectrum, as the Russell Top 50 Mega Cap Index returned 3.04% and the Russell Top 200 Index returned 1.71%. In contrast, the Russell Mid Cap Index, Russell 2000® Index and Russell Microcap Index posted negative returns (-1.67%, -7.36% and -8.21%, respectively). Defensive stocks outperformed dynamic stocks, in a reversal of the second quarter leadership. Growth stocks beat value stocks across all capitalization tiers except microcap for the third quarter.

Economic data released during the third quarter demonstrated positive economic growth with an ongoing improvement in employment. GDP grew at a revised annual rate of 4.6% in the second quarter, up from a previous estimate of 4.2%. Non-farm payrolls missed estimates in August at 180,000 jobs, the second weakest number during the year, although this followed six months of 200,000+ job additions. Unemployment fell to 6.1% in August, partially due to a marginal tick down in the participation rate. Meanwhile, the Fed continued its monthly reductions in quantitative easing as it prepared to fully halt the program in October. The U.S. dollar experienced its strongest quarter against other G10 currencies since 2008 after enjoying an eleven week run of successive gains.

The Russell 3000® Index advanced 5.24% in the fourth quarter of 2014, extending another strong year of returns for U.S. equities. Small cap stocks bounced back strongly for the quarter but still did not catch up with large cap for the year. The Russell 2000® Index returned 9.73% compared with the Russell 1000® Index and the Russell Top 50 Index, which returned 4.88% and 3.18%, respectively. At all market capitalization levels, defensive stocks outperformed dynamic stocks. Value stocks finished in a virtual tie with growth stocks in large and mid-capitalization stocks, but further down the capitalization scale, growth outperformed value. Within the Russell 1000® Index, the payoff to the value factor was mixed as both the cheapest stocks (lowest price-to-book ratios) and most expensive stocks (highest price-to-book ratios) underperformed for the quarter.

The fourth quarter got off to a rocky start with a market pullback in early October as investors considered the potential worst case scenario related to Ebola. However, market volatility receded and the market regained its previous highs as encouraging domestic economic releases outweighed global growth concerns. Labor market data remained healthy, with the unemployment rate hitting a six-year low of 5.8% in October. Initial jobless claims fell to pre-recession levels and U.S. non-farm payrolls in November came in significantly above estimates at the highest monthly reading in over two years. U.S. real GDP growth was sharply revised upward for the 3rd quarter from 3.9% to 5.0% annualized. However, jitters about declining oil prices threatened the rally at various points during the quarter. As broadly expected, the Fed ended its quantitative easing program in October. In December’s policy statement, the central bank revealed that it would be “patient” in judging when to start raising interest rates, rather than keeping them low for a “considerable time” as had been previously repeated. Investors interpreted this change of language as a sign of central bank confidence in the strength of the U.S. economy, but it also was clear that multiple months without rate increases were still ahead.

Non-U.S. Developed Equity Markets

Market Summary 5

Russell Investment Funds

Market Summary as of December 31, 2014, continued — (Unaudited)

For the fiscal year ended December 31, 2014, the non-U.S. equity market, as measured by the Russell Developed ex-U.S. Large Cap® Index (the “Index”), was down 4.00%. U.S. Dollar strength was a significant headwind during the period as other major currencies fell against the U.S. dollar - the Euro (-12.09%), Yen (-12.32%), Canadian dollar (-7.71%), Swiss Franc (-10.48%), and British Pound (-5.68%). Concerns heightened in the latter part of the period over the impact of falling oil prices on oil dependent economies.

Geo-politics and policymaker rhetoric dominated headlines in what was a relatively volatile first quarter of 2014. The Index registered positive returns of 1.2%, after recovering strongly from a sharp decline at the end of January. The quarter began with concerns over the outlook for growth in emerging markets, amid ongoing speculation regarding the U.S. Federal Reserve’s (“Fed”) plans for the reversal of quantitative easing (“QE”). Political upheaval in a number of emerging market countries also caused concern, most notably in Ukraine and Venezuela, as the currencies of a series of emerging market countries sold-off. However, comments from Fed Chair Yellen soothed investor concerns as she stated that “a highly accommodative policy will remain appropriate for considerable time after asset purchases end.” European Central Bank (“ECB”) Chairman Draghi added to the positive mood as he re-iterated the ECB was “ready and willing” to act. However, an uptick in political risk weighed on markets at the beginning of March as fallout from Crimea’s independence referendum and its resulting decision to join with Russia stoked wider international tensions. Despite sanctions between Russia and its Western critics, a feared escalation of tensions did not materialize and markets rebounded. Although macro data out of China worsened towards the second half of March, comments from the country’s Premier Li served to boost equity markets and spark a reversal in sentiment as he reassured investors that the government would support the economy.

A challenging start to the second quarter of 2014 saw equity markets track lower as policymaker inaction and an intensification of geopolitical events in Ukraine and the Middle East led to heightened investor risk aversion. However, non-U.S. equities maintained a largely positive trajectory through the quarter, as the Index advanced 4.4%.

The ECB’s announcement of renewed stimulus efforts in early June, as well as moderation of tensions between Russia and the West, contributed to an improvement in market sentiment toward the end of the second quarter. Consistently dovish comments from Fed Chair Janet Yellen, in particular her assertion that “a high degree of monetary accommodation remains warranted,” were also well received. Emerging markets also enjoyed a strong quarter, boosted by a series of welcome election results, most notably in India, and less dire concern toward the Chinese government’s restraint in policy support in the face of a decelerating economy.

Equity markets tracked lower over the third quarter of 2014, as the strengthening recovery in the U.S. wasn’t enough to offset a resurgence of geopolitical tension in the Middle East and sluggishness in Europe. Once again, monetary policy was key to equity performance across the world. Markets seemed unperturbed by the imminent end of QE in the U.S., preferring to focus on the country’s strong economic fundamentals, but concerns over interest rate hikes prompted Fed Chair Yellen to insist that interest rates would remain low for a “considerable time.” Low inflation and high unemployment in the Eurozone pushed the ECB to cut deposit and interest rates to record lows and pledge to start buying covered bonds. By quarter-end, however, poor economic data highlighted that further stimulatory action would likely be necessary. Emerging markets had a patchy quarter, with underwhelming data from China doing little to quell concerns that the country may yet face a hard economic landing.

Overall, the non-U.S. market fell 5.9% in the third quarter of 2014, as measured by the Index. Japan shed 2.57% as the after-effects of the consumer-tax hike continued to weigh on inflation and consumer sentiment. European markets were the biggest laggards, dropping 7.5% on the back of persistently bad economic news from the region’s key economies: Italy fell into recession in the second quarter, France stagnated and Germany saw business confidence slump to its lowest level in 17 months. Emerging market equities declined 3.3% in U.S. dollar terms during the quarter, largely driven by a September sell-off. Over the period, strength in the U.S. economy and a likelihood of further monetary easing in Europe and Japan wasn’t enough to overcome broader fears over the health of the global economy. Though emerging markets fell overall, they contained several bright spots, especially in East Asia.

6 Market Summary

Russell Investment Funds

Market Summary as of December 31, 2014, continued — (Unaudited)

Global markets followed increasingly divergent paths over the fourth quarter of 2014, reflecting the widening gap between a strong U.S. economy and the weaker economies of other developed markets. With the U.S. recovery continuing to gather steam, the Fed wound up its QE program in October. On the other hand, markets in Europe, Japan and China gained on poor economic news, as investors took it as a sign that central banks would be forced to loosen their purse strings still further. Japan duly obliged with a massive increase in its monetary stimulus, from 60 trillion yen to 80 trillion yen, at the end of October.

Also dominating global economic news was the rapid decline in oil prices, which by the end of the year had dropped roughly 50% from their June 2014 peak. Causes for the rapid decline in prices were the booming shale-oil industry in the U.S., higher-than-expected production from trouble spots such as Libya, a slowing economy in China, and in late November, the decision by OPEC countries not to cut production.

Non-U.S. equities, as measured by the Index, fell by 3.5% in the fourth quarter of 2014. In commodities, oil continued its slide and base metals also had a challenging quarter on worries over the Chinese economy. Emerging market countries had a tough time overall. However, China defied its mediocre economic indicators to rise by 7.2% as measured by the MSCI China Index, helped by a cut in interest rates and better-than-expected export figures in September. A more common story was that seen in Russia (-32.9%), where the slumping oil price, along with Western sanctions, sent stocks and the currency plunging. Colombia (-22.9%), Mexico (-12.3%) and Malaysia (-10.5%) also felt the ill effects of a lower oil price.

In 2014, mid to large cap companies outperformed smaller cap companies, while growth companies outperformed value companies, as measured by various Russell Global Developed Indexes. Stocks that exhibited higher quality and strong balance sheets tended to outperform lower quality companies, as evidenced by defensive stocks outperforming their dynamic peers.

This defensiveness was reflected in sector performance, as health care and utility stocks far outpaced more cyclically oriented sectors such as energy and materials, which were the worst performing sectors over the period. The technology sector performed well during the period led primarily by semiconductor and hardware companies, while software and services lagged within the sector.

Regionally, Asia ex-Japan had the most positive performance over the year, led by countries like Hong Kong and Singapore. Continental Europe struggled over the period as the larger economies such as France and Germany weighed on the region. Some of the peripheral countries such as Portugal and Greece sold off meaningfully, while Norway struggled due to dependence on oil. Emerging markets generally outperformed non-U.S. developed markets, as countries such as India, Indonesia, Philippines, Thailand and Turkey were able to outpace very poor performance in Russia, Hungary and Brazil.

Emerging Markets

The Russell Emerging Markets Index (the “Index”) was down 1.73% for the fiscal year ending December 31, 2014. The Index rallied for a strong second quarter driven by positive geopolitical developments but gave back returns in the latter half of the year due to the strong U.S. dollar and a significant drop in the price of oil. The largest contributor to negative returns was the Index’s exposure to the Russian equity market, which lost nearly half its value in U.S. dollar terms. This was driven by the combination of a strong dollar, U.S. sanctions driven by the Ukraine conflict and the plummeting price of oil. Offsetting this loss, the election of strong pro-market candidates in Indonesia and India led for sizeable gains in Indonesian and Indian markets.

The Index slipped 0.2% in the first quarter of 2014. The asset class got off to a tough start amid uncertainty surrounding the U.S. Federal Reserve’s (“Fed”) plans for quantitative easing (“QE”) reduction and increasing concerns over the Chinese economy. Uncertainty linked to Fed tapering began to evaporate in February and emerging markets rebounded, bolstered by comments from new Fed chair Janet Yellen.

Market Summary 7

Russell Investment Funds

Market Summary as of December 31, 2014, continued — (Unaudited)

However, a rise in political risk spurred bouts of renewed volatility, primarily due to Crimea’s independence referendum and its resulting decision to join with Russia. Meanwhile, Chinese macro data continued to deteriorate. In conjunction with comments from Premier Li, this sparked a reversal in sentiment amid expectations that the government may take action to support the economy. Despite tit-for-tat sanctions between Russia and its Western critics, a feared escalation of tensions did not materialize and combined with a drop in risk aversion in China, emerging markets rebounded. In this environment, there was a high dispersion in country returns while emerging market currencies also registered some sizeable movements. China (-5.6%) underperformed as Purchasing Managers Indices (“PMI”) manufacturing data continued to worsen and the central bank moved to tighten liquidity conditions.

Indonesia (+21.7%) bounced back as markets reacted positively to news that popular Jakarta governor, Joko Widodo, would run for president. Data showing that its current account deficit had narrowed also helped to restore investor confidence and spurred a gain in the rupiah. The Philippines (+8.9%) and Thailand (+8.7%) also outperformed while Korea (-2.1%) lagged. India (+8.9%) recorded solid gains, boosted by central bank action, which contributed to a 3.2% gain in the rupee, and by polls which indicated the opposition BJP may win upcoming elections.

In Latin America, Colombia (+4.2%) and Brazil (+1.8%) were the only countries to outperform. In Brazil, expectations that the central bank’s interest rate hiking cycle was coming to an end, and polls which indicated lower approval ratings for president Rousseff, sparked resurgence in the local market. Russia (-14.4%) was the worst performing country in the Index, as events in Crimea were the catalyst for a significant sell-off which also saw the ruble fall 6.5%.

Emerging Europe was mixed with Greece (+15.8%) benefiting from increased stability in the eurozone. In contrast, Hungary (-8.8%) lagged, as the central bank cut interest rates more than anticipated. Turkey (+3.2%) epitomized the high levels of volatility, with its perceived fragility to Fed tapering resulting in sizeable capital outflows and a sell-off in the lira early in the quarter. However, the central bank’s decision to hike interest rates 300bps served to stabilize the currency, and as wider concerns over emerging markets eased, the local market more than recouped losses.

South Africa (+4.4%) finished in positive territory while Egypt (+14.7%) registered strong gains ahead of Presidential elections. From an investment style perspective, growth was strongly outperforming value coming into the first quarter of 2014, particularly stocks with the highest price-to-book valuations and high return-on-equity. However, mid-March saw a sharp reversal with value stocks, in particular deep value stocks outperforming significantly. On a market capitalization basis small capitalization equities outperformed large capitalization equities, as measured by the Russell Emerging Markets Small Cap Index (+2.6% over the quarter).

In the second quarter, the Index returned 7.1% in U.S. dollar terms. Diminished concerns over a nearer term rise in global interest rates provided a tailwind to market returns. However, the main catalyst for gains was a series of favorable election results, most notably in India (+17%) where Narendra Modi’s BJP party became the first to attain a majority in the lower house for more than 30 years. Elections in South Africa (+2.1%), Egypt (-2.0%) and frontier market Ukraine also completed relatively smoothly, with no major surprises.

The Chinese market (+5.0%) witnessed some large swings through the period. Concerns over PMI data early in the quarter dissipated as renewed fears over a hard landing were allayed by upside data surprises and as investors appeared more at ease with the government’s restraint in implementing large scale policy intervention through the current period of transition. Elsewhere in Asia, the Philippines (+9.6%) outperformed, despite the publication of a weak first quarter gross domestic product (“GDP”) report which was hit by the effects of typhoon Yolanda. However, the market gained on expectations that higher private consumption and reconstruction spending may boost full year GDP growth as the World Bank increased its Philippine outlook. After initial fears, a military coup in Thailand (+8.4%) was interpreted as a stabilizing factor, generating more optimistic sentiment in financial markets. Indonesia (-1.3%) was the regional laggard, hampered by uncertainty over July’s Presidential election. India was the standout country in the Index, buoyed by high expectations that the new administration would succeed in delivering economic reforms to restore growth and battle high inflation.

8 Market Summary

Russell Investment Funds

Market Summary as of December 31, 2014, continued — (Unaudited)

In Latin America, Brazil (+7.0%) outperformed as polls showed support for President Rousseff was declining ahead of October’s Presidential election. However, fundamentals for the country’s economy remained weak with the Brazilian Central Bank raising its already above target inflation outlook for 2014 and the World Bank cutting its GDP growth forecast to 1.5%. Peru (+8.5%) outperformed, while Chile (+2.0%) lagged as the economy continued to slow.

An easing in tensions between Russia (+11.7%) and the West, and a cooling of events in Ukraine, was beneficial for various emerging European markets. Turkey (+15.0%) enjoyed a strong quarter, as its current account deficit continued to recede. Greece (-9.8%) was the worst performing country in the Index as data for the eurozone remained weak and some Greek bank equities declined sharply on concerns over the banks’ exposure to Ukraine and Bulgaria. South Africa (+5.1%) capped a solid quarter, as the ruling ANC party held control of the national assembly, albeit with a reduced majority. The United Arab Emirates (-6.1%) underperformed, particularly in June.

In the third quarter, the Index declined 3.2% in U.S. dollar terms, largely driven by a September sell-off. Emerging markets sold off on the back of speculation around rising interest rates and U.S. dollar strength: the 5 year U.S. Treasury rate rose by 16 basis points over the quarter and the dollar strengthened relative to most currencies. China ended the quarter in mildly positive territory (+1.6%) despite enduring some poor economic data towards the end of the period. While the government had been making positive statements about reform, investors remained concerned – given falling industrial production and a surprise drop in lending – that it won’t be sufficient for the country to hit its growth targets for the year.

Meanwhile, geopolitics played a large role in the performance of emerging markets over the period. Brazil fell 9.2% amid a resurgence in support for the incumbent presidential candidate, Dilma Rousseff. The Russian markets slumped 15.8% as geopolitical tensions in Ukraine rumbled on, and sanctions imposed by Europe and the U.S. began to bite. A significant portion of returns for both Russia and Brazil were driven by currency weakness relative to the U.S. dollar. Over the quarter, the Brazilian and Russian currencies declined by more than 10% against the greenback. Emerging markets in Europe had a poor quarter overall, with Hungary falling 12.1% and Turkey by 11.5%. Turkey is considered particularly vulnerable to interest rate hikes due to its high current account deficit. Thailand rose sharply (+8.0%) after the appointment of a new prime minister appeared to assure a period of greater stability. Indonesia climbed (+2.9%) following the election of Joko Widodo.

Elsewhere, India continued to do well (+1.7%) as recently elected Prime Minister Narendra Modi pressed forward with a reformist agenda. Notably, GDP growth of 5.7% year over year recorded in the second-quarter was the fastest rate since the first quarter of 2012. In the Middle East, the United Arab Emirates enjoyed a strong quarter, with its market rising by 18.4% to add to its leading year-to-date returns. Mexico (+0.6%) also gained despite the sell-off in September and the Philippines (+2.8%) posted strong GDP growth which helped drive gains.

Additional laggards included Greece, which ended down 19.9%, and South Korea, which was also among the biggest detractors as markets fell by 5.8%. With China being one of its biggest export markets, South Korea is especially vulnerable to the economic travails of its giant northern neighbor. Taiwan also declined (-4.3%), as the recent strong run of its technology companies led to profit taking. Elsewhere, Malaysia (-2.4%), Peru (-3.8%) and Chile (-5.1%) all slipped lower.

The Index shed 4.8% in U.S. dollar terms in a highly volatile fourth quarter. The strong U.S. dollar was a key contributor to the emerging markets selloff. The local markets were actually neutral for the quarter, meaning that the negative moves were expressed through currency rather than local equity markets. The rallying dollar was driven by a U.S. economy poised to outperform non-U.S. developed markets. Despite a positive return in October, the Index was additionally dragged down by the effects of a tumbling oil price on key oil exporting nations.

Russia was the worst-performing market over the fourth quarter (-34.1%), driven by the weakness of the ruble. During the quarter, the Russian central bank notably hiked its key interest rate to 17% in an attempt to control inflation and stem capital outflows. Meanwhile, the joint effects of the plunge in oil prices coupled with Western sanctions hammered the country’s economic prospects. Colombia (-20.8%), as the fourth-largest oil producer in South America, saw the peso and

Market Summary 9

Russell Investment Funds

Market Summary as of December 31, 2014, continued — (Unaudited)

government revenues slump over the quarter, casting a pall over the country’s markets. Meanwhile, Malaysia, the second largest oil and natural gas producer in Southeast Asia, slipped 11.1%. While declining oil prices proved very damaging to countries that depend heavily on oil revenues, they provided a boost to consumers and oil-importing nations. Turkey climbed 10.9%, as the oil importer benefited from falling energy prices and an uptick in private demand.

In Europe, Greece was the biggest laggard as it dropped 27.5%. Having recently shown signs of revival, Greek markets were thrown back into turmoil after the failure of the governing New Democracy party to elect a new president in December. This failure triggered a full Parliamentary general election scheduled for the end of January, with the jump in financial market uncertainty stemming from the popularity of the far-left, anti-austerity Syriza party. Elsewhere in Europe, Hungary performed poorly (-12.7%) primarily due to its heavy export exposure to Russia. Polish equities declined 12.5% amid worries about debt levels among the country’s real-estate developers and a fall in the zloty.

Elsewhere, the depreciating value of the real saw Brazil fall sharply (-14.4%). During the quarter, investors spurned the reelection of President Dilma Rousseff. President Rousseff sought to mitigate the economic downfall by announcing a broad package of tax increases and budget cuts in a bid to restore faith in her government, with investors taking hope from the appointment of new finance minister Joaquim Levy. In addition, the ongoing corruption scandal at Petrobras, a key state owned oil producer, led the company to lose nearly half its value. Mexican equities had a poor quarter, dropping 11.6% amid the falling peso, political unrest and a series of soft economic data. Korea extended its losses over the second half of the year with a further 8.2% decline in the fourth quarter, largely driven by the government’s continued devaluation of the won.

More positively, Chinese markets had a strong fourth quarter, gaining 4.3% as Chinese financial stocks surged. Although the country’s economic data was mixed, its stock market rose strongly in the latter half of 2014, as investors become increasingly convinced that the Chinese government would implement more aggressive stimulus measures. South Africa gained 2.8%, spurred by dovish sentiment from the Fed in mid-December. India climbed a steady 1.1%.

Energy was the worst performing sector globally and within emerging markets in the fourth quarter, retreating over 23%. The materials & processing sector was also impacted by the commodities slide, down 11%. Technology and financial services were the only two sectors to advance, adding to their 2014 positive returns.

U.S./Global Fixed Income Markets

The fiscal year ended December 31, 2014 was a positive period for global fixed income markets overall, although not without a few surprises along the way. Sovereign yields ended the period lower than they began across virtually all regions, buoying the returns of various fixed income sectors. Globally, credit sectors largely outperformed similar-duration government bonds as spreads generally held or narrowed slightly over the period. Corporate credit underperformed securitized assets due to commodity price weakness and heightened illiquidity concerns, particularly toward the end of the year.

While 2013 ended with a burst of optimism and positive data flow out of the U.S. in particular, 2014 began with a brief stumble as disappointing U.S. non-farm payrolls data was released and concern grew over the global economic outlook for China as the potential for accelerating credit defaults became more apparent. However, this was more than offset by a fourth quarter 2013 U.S. GDP growth reading coming in ahead of expectations, as well as the smooth leadership transition at the U.S. Federal Reserve (the “Fed”). Chairwoman Janet Yellen’s first testimony to the U.S. Congress was positively received by global financial markets, during which she stressed continuity, if not a slightly more dovish stance than her predecessor. The result was a modestly positive end to the first quarter of 2014 for global fixed income markets, particularly for credit sectors.

The moderate rally in global fixed income markets extended through the second quarter of 2014 amid economic data that supported a progressive economic recovery in the U.S. and bottoming-out in Europe. Given gradual tapering in the Fed’s asset purchasing program and positive U.S. growth outlook, the mid-year rally in U.S. Treasuries caught many market

10 Market Summary

Russell Investment Funds

Market Summary as of December 31, 2014, continued — (Unaudited)

participants by surprise. The rally was driven by a lull in new issuance squeezing supply (and yields) of longer-term bonds as well as demand from price-insensitive buyers (de-risking pension funds, the Fed and China). Increasingly, accommodative monetary policy out of Japan and Europe put significant downward pressure on yields globally, including in the U.S. While the impact of a particularly harsh winter became more evident in the second quarter, accentuated by a meaningful downwards revision in first quarter GDP growth, fixed income markets proved resilient. Improving unemployment, job gains and consumer confidence re-affirmed the market’s optimism, as did Chairwoman Yellen’s commitment to maintain an accommodative stance even as unemployment and inflation approached target levels.

Market calm turned to concern in the latter half of the year amid heightened uncertainty surrounding geopolitical events and the robustness of global growth, despite generally positive economic data out of the U.S. Israeli-Palestinian tension in the Gaza Strip escalated dramatically in July, putting investors a little more on edge, although the immediate market impact was relatively muted. More impactful was news of a Malaysia Airlines passenger jet being shot down over Ukraine later in the month, raising the stakes in the conflict between Kiev and pro-Moscow rebels in which Russia and the West backed opposing sides. The Ukraine conflict continued to escalate throughout July and August, but was halted by a tense cease-fire in September. As a result, the third quarter of 2014 was challenging for global fixed income markets, particularly credit sectors. Safe-haven U.S. and core European government bonds posted modestly positive returns.

On the other hand, the U.S. economy continued to show strength, with employment gains, consumer confidence and second quarter GDP growth coming in largely ahead of expectations. However, weak economic data out of core Europe and China scared credit markets, tempering the outlook for growth globally. Moves by the European Central Bank to loosen monetary policy, including its own form of asset purchasing program, put further downward pressure on government bond yields, most notably in Europe, but with sympathy downward moves in North America and Asia-Pacific. Volatility spiked in October amid weak data releases out of Europe (namely Germany) and China, sending yields and risk assets plummeting globally, only to nearly revert to prior levels days later. Growing fears over the spread of Ebola from Africa also contributed to investors being more on edge as the first cases were reported in the U.S. and Europe.

By year-end, global government bond yields remained lower for the year, while credit spreads, which had contracted during the first half of the period, ended flat overall. A key indicator of global fixed income performance, the Barclays Global Aggregate Index, returned 7.6% for the year, in USD hedged terms, buoyed by lower government bond yields and broadly flat credit spreads.

Over the year, European bonds outperformed those of other regions (returning 11.1% as measured by the Barclays European Aggregate Index) on the back of strong sovereign bond returns, most notably among lower-rated “peripheral” countries such as Ireland, Spain, Italy and Slovenia as both “core” (e.g., German) yields and spreads between peripheral and core countries fell materially. U.S. bonds posted solid gains (returning 6.0% as measured by the Barclays U.S. Aggregate Index) as U.S. Treasury yields ended the year modestly lower and credit spreads held. Asia-Pacific bonds also posted solid gains (returning 6.3% as measured by the Barclays Asian Pacific Aggregate Index) despite a slowing Chinese growth outlook weighing on the region, likely at least partially offset by the Bank of Japan’s commitment to and later ramp-up of its aggressive monetary policy support.

Strong new issuance volumes characterized most credit sectors, particularly in the U.S., over the year, in both corporate and securitized markets. Sectors generally performed in-line with spreads, with corporate credit outperforming securitized credit across regions (returning 3.1% vs. 3.3% on a global basis, respectively, as measured by Barclays Global Aggregate Index - Corporates and Barclays Global Aggregate Index - Securitized). Overall, lower-quality investment grade corporates outperformed higher-quality investment grade corporates, and utilities and industrials outperformed financials. U.S. agency mortgage-backed securities (“MBS”) performed well (returning 6.1% as measured by Barclays U.S. Aggregate Index – Agency MBS) despite concerns of reduced demand from tapering Fed purchases.

Market Summary 11

Russell Investment Funds

Market Summary as of December 31, 2014, continued — (Unaudited)

Similar to 2013, non-Agency MBS outperformed most other sectors, aided by favorable supply and demand forces and solid housing fundamentals. High yield corporate credit marginally underperformed investment grade corporate credit on an equivalent-duration basis, largely as a result commodity price weakness late in the year disproportionately impacting high yield issuers. The lowest-quality segments of the sector underperformed significantly. Emerging market (“EM”) debt slightly lagged developed fixed income markets on mounting growth concerns and commodity price weakness, despite a bounce-back from weakness earlier in the year. Local currency bonds (those denominated in the currency of the issuing EM country) significantly underperformed hard currency bonds (those issued by EM issuers but denominated in “hard currencies” such as the U.S. dollar or Euro), largely as a result of EM currency weakness amid global and market-specific growth, commodity price declines and geopolitical concerns.

12 Market Summary

(This page intentionally left blank)

Russell Investment Funds Multi-Style Equity Fund

Portfolio Management Discussion and Analysis — December 31, 2014 (Unaudited)

14 Multi-Style Equity Fund

Russell Investment Funds

Multi-Style Equity Fund

Portfolio Management Discussion and Analysis, continued — December 31, 2014 (Unaudited)

| The Multi-Style Equity Fund (the “Fund”) employs a multi- | to be “non-cyclical” and/or interest rate sensitive. However, |

| manager approach whereby portions of the Fund are allocated to | certain industries that tend to be viewed as “bond substitutes,” |

| different money managers. Fund assets not allocated to money | such as electric utilities and real estate investment trusts (REITs), |

| managers are managed by Russell Investment Management | outperformed given the decline in interest rates and this detracted |

| Company (“RIMCo”), the Fund’s advisor. RIMCo may change | from the Fund’s benchmark-relative performance. |

| the allocation of the Fund’s assets among money managers at | |

| any time. An exemptive order from the Securities and Exchange | How did the investment strategies and techniques employed |

| Commission (“SEC”) permits RIMCo to engage or terminate a | by the Fund and its money managers affect its benchmark- |

| money manager at any time, subject to approval by the Fund’s | relative performance? |

| Board, without a shareholder vote. Pursuant to the terms of the | Stock selection effects within the technology sector (an |

| exemptive order, the Fund is required to notify its shareholders | underweight to Apple Inc. and Microsoft Corporation) and |

| within 90 days of when a money manager begins providing | within the energy sector (an overweight to Occidental Petroleum |

| services. As of December 31, 2014, the Fund had six money | Corporation) detracted from the Fund’s benchmark-relative |

| managers. | returns for the fiscal year. With respect to sector allocation |

| decisions, overweights to health care and financial services were | |

| What is the Fund’s investment objective? | rewarded. A tilt toward stocks with the lowest valuations (lowest |

| The Fund seeks to provide long term capital growth. | price-to-book and price-to-cash flow ratios) detracted, however an |

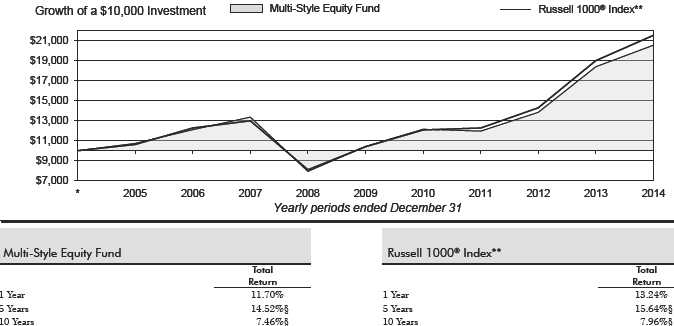

| How did the Fund perform relative to its benchmark for the | overweight to stocks with rising earnings estimates was beneficial |

| fiscal year ended December 31, 2014? | to benchmark-relative returns. |

| For the fiscal year ended December 31, 2014, the Fund gained | Columbus Circle Investors (“Columbus Circle”) underperformed |

| 11.70%. This is compared to the Fund’s benchmark, the Russell | the Russell 1000® Growth Index for the fiscal year. Tilts toward |

| 1000® Index, which gained 13.24% during the same period. The | stocks with high beta (stocks with high sensitivity to market |

| Fund’s performance includes operating expenses, whereas index | movements) and high financial quality (lowest debt-to-capital |

| returns are unmanaged and do not include expenses of any kind. | ratios) were not rewarded. An overweight to the health care |

| sector and to the financial services sector were beneficial. Stock | |

| For the fiscal year ended December 31, 2014, the Morningstar® | selection within the energy sector (overweights to Pioneer Natural |

| Large Insurance Blend, a group of funds that Morningstar | Resources Company and Halliburton Company) detracted from |

| considers to have investment strategies similar to those of the | benchmark-relative performance. |

| Fund, gained 10.73%. This result serves as a peer comparison | |

| and is expressed net of operating expenses. | Sustainable Growth Advisers, LP (“Sustainable”) underperformed |

| the Russell 1000® Growth Index for the fiscal year. Stock | |

| RIMCo may assign a money manager a specific style or | selection within the technology sector (an underweight to Apple, |

| capitalization benchmark other than the Fund’s index. However, | Inc., and an overweight to SAP SE) and within the health care |

| the Fund’s primary index remains the benchmark for the Fund | sector (an overweight to Sanofi) detracted from benchmark- |

| and is representative of the aggregate of each money manager’s | relative performance. An overweight to the health care sector |

| benchmark index. | and to the financial services sector were beneficial. |

| How did the market conditions described in the Market | Suffolk Capital Management, LLC (“Suffolk”) outperformed the |

| Summary report affect the Fund’s performance? | Russell 1000® Index for the fiscal year. A tilt toward stocks with |

| During the fiscal year, the U.S. large capitalization equity market | rising earnings estimates contributed positively to benchmark- |

| produced positive returns. Relevant Fund exposures included | relative returns. An underweight to the energy sector and an |

| tilts toward stocks with the lowest valuation metrics (lowest price- | overweight to the health care sector were beneficial. Stock |

| to-book and price-to-cash flow ratios), rising earnings estimates, | selection within the technology sector (an overweight to Avago |

| the highest financial quality (lowest debt-to-capital ratios), and | Technologies Limited and an overweight to Hewlett-Packard |

| the health care sector. Overweights to stocks with the lowest | Company) was additive to benchmark-relative performance. |

| valuation metrics and the highest financial quality detracted from | Institutional Capital LLC (“ICAP”) underperformed the Russell |

| the Fund’s benchmark-relative performance, while overweights to | 1000® Value Index for the fiscal year. Sector allocation decisions |

| stocks with rising earnings estimates and the health care sector | were beneficial, specifically an underweight to the energy sector |

| were beneficial to the Fund’s benchmark-relative returns. | and an overweight to the health care sector. However, stock |

| With the continuation of the economic recovery, the Fund was | selection within the consumer discretionary sector (an overweight |

| underweight in most of the sectors that are traditionally considered | to Viacom Inc. and an overweight to Johnson Controls, Inc.) and |

Multi-Style Equity Fund 15

Russell Investment Funds

Multi-Style Equity Fund

Portfolio Management Discussion and Analysis, continued — December 31, 2014 (Unaudited)

| within the producer durables sector (an overweight to General | intended to help control the Fund’s beta (beta is a measure of | |

| Electric Company and an overweight to Boeing Company) | a portfolio’s volatility and its sensitivity to the direction of the | |

| detracted from benchmark-relative performance. | market). This strategy performed in-line with expectations, as it | |

| Jacobs Levy Equity Management, Inc. (“Jacobs Levy”) slightly | reduced the Fund’s beta and smoothed the Fund’s return pattern. | |

| underperformed the Russell 1000® Value Index for the fiscal | During the market environment of this fiscal year, low beta stocks | |

| year. Factor exposures were mixed as a tilt toward stocks with | (stocks with low sensitivity to market movements) produced | |

| high earnings variability detracted while a tilt toward stocks with | higher returns than high beta stocks, and this was reflected in the | |

| positive earnings surprises was beneficial. Overweights to the | investment returns of this strategy. | |

| technology and health care sectors were additive to benchmark- | During the period, RIMCo used index futures contracts to equitize | |

| relative returns. Stock selection within the financial services | the Fund’s cash. The decision to equitize the Fund’s cash was | |

| sector (an underweight to Berkshire Hathaway, Inc.) and within | beneficial to Fund performance for the fiscal year. | |

| the energy sector (an overweight to Patterson-UTI Energy, Inc. and | ||

| an overweight to Nabors Industries LTD.) held back benchmark- | Describe any changes to the Fund’s structure or the money | |

| relative performance. | manager line-up. | |

| DePrince, Race & Zollo, Inc. (“DePrince”) was terminated from | ||

| the Fund in May 2014 and underperformed the Russell 1000® | In May, 2014, DePrince was terminated and its assets were | |

| Value Index for the portion of the fiscal year that it was a manager | reallocated to Jacobs Levy, ICAP and Mar Vista. Due to changes | |

| in the Fund. Sector exposures were not rewarded, specifically | in the roles of certain investment professionals at DePrince, | |

| an underweight to health care and an overweight to consumer | RIMCo believed that the termination of DePrince and reallocation | |

| discretionary. Stock selection within the consumer discretionary | of assets to the other money managers was an appropriate step to | |

| sector (an overweight to American Eagle Outfitters, Inc. and an | improve future return potential of the Fund. | |

| overweight to Coach, Inc.) detracted from benchmark-relative | Money Managers as of December 31, | |

| performance. | 2014 | Styles |

| Mar Vista Investment Partners, LLC (“Mar Vista”) outperformed | Columbus Circle Investors | Growth |

| the Russell 1000® Index for the fiscal year. Many of Mar Vista’s | Suffolk Capital Management LLC | Market-Oriented |

| portfolio exposures were rewarded, specifically tilts away from | Institutional Capital LLC | Value |

| Mar Vista Investment Partners, LLC | Market-Oriented | |

| stocks with high beta and the highest earnings variability. Stock | Sustainable Growth Advisers, LP | Growth |

| selection within the health care sector (an overweight to Allergan, | Jacobs Levy Equity Management, Inc. | Value |

| Inc. and an overweight to Covidien) and within the consumer | The views expressed in this report reflect those of the portfolio | |

| discretionary sector (overweight O’Reilly Automotive, Inc. and | managers only through the end of the period covered by | |

| TJX Companies, Inc.) contributed to positive benchmark-relative | the report. These views do not necessarily represent the | |

| performance. | views of RIMCo, or any other person in RIMCo or any other | |

| RIMCo manages the portion of the Fund’s assets that RIMCo | affiliated organization. These views are subject to change | |

| determines not to allocate to the money managers. Assets not | at any time based upon market conditions or other events, | |

| allocated to managers include the Fund’s liquidity reserves and | and RIMCo disclaims any responsibility to update the views | |

| assets which may be managed directly by RIMCo to modify the | contained herein. These views should not be relied on | |

| Fund’s overall portfolio characteristics to seek to achieve the | as investment advice and, because investment decisions | |

| desired risk/return profile for the Fund. | for a Russell Investment Funds (“RIF”) Fund are based on | |

| numerous factors, should not be relied on as an indication | ||

| RIMCo pursues an investment strategy for the Fund that is a | of investment decisions of any RIF Fund. | |

| replication of the Russell Top 200® Defensive™ Index and is | ||

16 Multi-Style Equity Fund

Russell Investment Funds

Multi-Style Equity Fund

Portfolio Management Discussion and Analysis, continued — December 31, 2014 (Unaudited)

| * | Assumes initial investment on January 1, 2005. |

| ** | The Russell 1000® Index includes the 1,000 largest companies in the Russell 3000® Index. The Russell 1000® Index represents the universe of stocks from which most active money managers typically select. The Russell 1000® Index return reflects adjustments from income dividends and capital gain distributions reinvested as of the ex-dividend dates. |

| § | Annualized. |

The performance shown in this section does not reflect any Insurance Company Separate Account or Policy Charges. Performance is historical and assumes reinvestment of all dividends and capital gains. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased. Past performance is not indicative of future results.

Multi-Style Equity Fund 17

Russell Investment Funds Multi-Style Equity Fund

Shareholder Expense Example — December 31, 2014 (Unaudited)

| Fund Expenses | Please note that the expenses shown in the table are meant | ||||||

| The following disclosure provides important information | to highlight your ongoing costs only and do not reflect any | ||||||

| regarding the Fund’s Shareholder Expense Example | transactional costs. Therefore, the information under the heading | ||||||

| (“Example”). | “Hypothetical Performance (5% return before expenses)” is | ||||||

| useful in comparing ongoing costs only, and will not help you | |||||||

| Example | determine the relative total costs of owning different funds. In | ||||||

| As a shareholder of the Fund, you incur two types of costs: (1) | addition, if these transactional costs were included, your costs | ||||||

| transaction costs, and (2) ongoing costs, including advisory and | would have been higher. The fees and expenses shown in this | ||||||

| administrative fees and other Fund expenses. The Example is | section do not reflect any Insurance Company Separate Account | ||||||

| intended to help you understand your ongoing costs (in dollars) | Policy Charges. | ||||||

| of investing in the Fund and to compare these costs with the | Hypothetical | ||||||

| ongoing costs of investing in other mutual funds. The Example | Performance (5% | ||||||

| is based on an investment of $1,000 invested at the beginning of | Actual | return before | |||||

| the period and held for the entire period indicated, which for this | Performance | expenses) | |||||

| Beginning Account Value | |||||||

| Fund is from July 1, 2014 to December 31, 2014. | July 1, 2014 | $ | 1,000.00 | $ | 1,000.00 | ||

| Ending Account Value | |||||||

| Actual Expenses | December 31, 2014 | $ | 1,048.00 | $ | 1,020.82 | ||

| The information in the table under the heading “Actual | Expenses Paid During Period* | $ | 4.49 | $ | 4.43 | ||

| Performance” provides information about actual account values | |||||||

| and actual expenses. You may use the information in this column, | * Expenses are equal to the Fund's annualized expense ratio of 0.87% | ||||||

| (representing the six month period annualized), multiplied by the average | |||||||

| together with the amount you invested, to estimate the expenses | account value over the period, multiplied by 184/365 (to reflect the one-half | ||||||

| that you paid over the period. Simply divide your account value by | year period). | ||||||

| $1,000 (for example, an $8,600 account value divided by $1,000 | |||||||

| = 8.6), then multiply the result by the number in the first column | |||||||

| in the row entitled “Expenses Paid During Period” to estimate | |||||||

| the expenses you paid on your account during this period. | |||||||

| Hypothetical Example for Comparison Purposes | |||||||

| The information in the table under the heading “Hypothetical | |||||||

| Performance (5% return before expenses)” provides information | |||||||

| about hypothetical account values and hypothetical expenses | |||||||

| based on the Fund’s actual expense ratio and an assumed rate of | |||||||

| return of 5% per year before expenses, which is not the Fund’s | |||||||

| actual return. The hypothetical account values and expenses | |||||||

| may not be used to estimate the actual ending account balance or | |||||||

| expenses you paid for the period. You may use this information | |||||||

| to compare the ongoing costs of investing in the Fund and other | |||||||

| funds. To do so, compare this 5% hypothetical example with the | |||||||

| 5% hypothetical examples that appear in the shareholder reports | |||||||

| of other funds. | |||||||

18 Multi-Style Equity Fund

| Russell Investment Funds | ||||||||

| Multi-Style Equity Fund | ||||||||

| Schedule of Investments — December 31, 2014 | ||||||||

| Amounts in thousands (except share amounts) | Amounts in thousands (except share amounts) | |||||||

| Principal | Fair | Principal | Fair | |||||

| Amount ($) or | Value | Amount ($) or | Value | |||||

| Shares | $ | Shares | $ | |||||

| Common Stocks - 95.7% | Molson Coors Brewing Co. Class B | 7,047 | 525 | |||||

| Consumer Discretionary - 14.3% | Mondelez International, Inc. Class A | 93,796 | 3,407 | |||||

| Amazon.com, Inc.(Æ) | 8,707 | 2,703 | PepsiCo, Inc. | 16,650 | 1,575 | |||

| Carnival Corp. | 31,400 | 1,423 | Philip Morris International, Inc. | 10,558 | 860 | |||

| CBS Corp. Class B | 7,903 | 437 | Procter & Gamble Co. (The) | 37,212 | 3,390 | |||

| Chipotle Mexican Grill, Inc. Class A(Æ) | 1,094 | 749 | Reynolds American, Inc. | 682 | 44 | |||

| Choice Hotels International, Inc. | 7,100 | 398 | Sysco Corp. | 1,347 | 53 | |||

| Comcast Corp. Class A(Æ) | 105,836 | 6,139 | Walgreens Boots Alliance, Inc. | 596 | 45 | |||

| Costco Wholesale Corp. | 9,488 | 1,344 | Whole Foods Market, Inc. | 40,420 | 2,038 | |||

| DIRECTV(Æ) | 488 | 42 | 20,477 | |||||

| Estee Lauder Cos., Inc. (The) Class A | 7,664 | 584 | ||||||

| Ford Motor Co. | 225,750 | 3,499 | Energy - 6.7% | |||||

| Garmin, Ltd. | 7,900 | 417 | Anadarko Petroleum Corp. | 4,521 | 373 | |||

| GateHouse Media, Inc.(Æ) | 40,947 | 1,978 | Atwood Oceanics, Inc. | 6,300 | 179 | |||

| General Motors Co. | 53,100 | 1,854 | California Resources Corp.(Æ) | 708 | 4 | |||

| Home Depot, Inc. | 3,101 | 326 | Cameron International Corp.(Æ) | 30,800 | 1,538 | |||

| Hyatt Hotels Corp. Class A(Æ) | 12,600 | 759 | Chevron Corp. | 37,674 | 4,226 | |||

| Jarden Corp.(Æ) | 17,896 | 857 | ConocoPhillips | 2,782 | 192 | |||

| Johnson Controls, Inc. | 65,750 | 3,178 | Core Laboratories NV | 10,198 | 1,227 | |||

| Kohl's Corp. | 9,200 | 562 | Devon Energy Corp. | 30,634 | 1,876 | |||

| L Brands, Inc. | 8,170 | 707 | EOG Resources, Inc. | 5,600 | 516 | |||

| Las Vegas Sands Corp. | 23,200 | 1,349 | EP Energy Corp. Class A(Æ) | 14,000 | 146 | |||

| Liberty Media Corp.(Æ) | 37,150 | 1,301 | Exxon Mobil Corp. | 90,589 | 8,373 | |||

| Lowe's Cos., Inc. | 43,790 | 3,013 | Halliburton Co. | 160 | 6 | |||

| lululemon athletica, Inc.(Æ)(Ñ) | 4,000 | 223 | Hess Corp. | 15,969 | 1,179 | |||

| McDonald's Corp. | 2,240 | 210 | Marathon Oil Corp. | 1,302 | 37 | |||

| News Corp. Class A(Æ) | 62,200 | 976 | Nabors Industries, Ltd. | 53,800 | 698 | |||

| Nike, Inc. Class B | 19,429 | 1,868 | National Oilwell Varco, Inc. | 897 | 59 | |||

| Omnicom Group, Inc. | 41,300 | 3,200 | Newfield Exploration Co.(Æ) | 13,400 | 363 | |||

| O'Reilly Automotive, Inc.(Æ) | 11,605 | 2,235 | Occidental Petroleum Corp. | 49,019 | 3,952 | |||

| Priceline Group, Inc. (The)(Æ) | 1,520 | 1,733 | Patterson-UTI Energy, Inc. | 38,600 | 640 | |||

| PVH Corp. | 6,568 | 842 | PBF Energy, Inc. Class A | 12,400 | 330 | |||

| Royal Caribbean Cruises, Ltd. | 28,196 | 2,325 | Phillips 66(Æ) | 292 | 21 | |||

| Starbucks Corp. | 53,225 | 4,367 | Pioneer Natural Resources Co. | 3,740 | 557 | |||

| Target Corp. | 8,539 | 648 | Schlumberger, Ltd. | 48,935 | 4,180 | |||

| Tiffany & Co. | 4,372 | 467 | Spectra Energy Corp. | 1,094 | 40 | |||

| Time Warner, Inc. | 35,702 | 3,050 | Tesoro Corp. | 9,800 | 729 | |||

| TJX Cos., Inc. | 32,165 | 2,206 | Valero Energy Corp. | 26,300 | 1,302 | |||

| Ulta Salon Cosmetics & Fragrance, Inc.(Æ) | 6,962 | 890 | 32,743 | |||||

| Under Armour, Inc. Class A(Æ) | 7,846 | 533 | ||||||

| Viacom, Inc. Class B | 46,824 | 3,523 | Financial Services - 19.5% | |||||

| Wal-Mart Stores, Inc. | 24,313 | 2,088 | ACE, Ltd. | 769 | 88 | |||

| Walt Disney Co. (The) | 43,180 | 4,067 | Aflac, Inc. | 23,278 | 1,423 | |||

| Whirlpool Corp. | 4,360 | 845 | Allstate Corp. (The) | 984 | 69 | |||

| Yum! Brands, Inc. | 890 | 65 | Ally Financial, Inc.(Æ) | 37,400 | 883 | |||

| 69,980 | American Express Co. | 24,370 | 2,267 | |||||

| American International Group, Inc. | 19,400 | 1,087 | ||||||

| Consumer Staples - 4.2% | American Tower Corp. Class A(ö) | 41,275 | 4,080 | |||||

| Altria Group, Inc. | 4,502 | 222 | Aon PLC | 27,700 | 2,626 | |||

| Anheuser-Busch InBev - ADR | 15,966 | 1,793 | Arch Capital Group, Ltd.(Æ) | 20,000 | 1,182 | |||

| Archer-Daniels-Midland Co. | 28,173 | 1,465 | Aspen Insurance Holdings, Ltd. | 8,000 | 350 | |||

| Coca-Cola Co. (The) | 8,998 | 380 | Axis Capital Holdings, Ltd. | 19,500 | 996 | |||

| Colgate-Palmolive Co. | 30,543 | 2,114 | Bank of America Corp. | 280,288 | 5,014 | |||

| Constellation Brands, Inc. Class A(Æ) | 5,761 | 566 | Bank of New York Mellon Corp. (The) | 12,600 | 511 | |||

| CVS Health Corp. | 2,650 | 255 | BB&T Corp. | 326 | 13 | |||

| General Mills, Inc. | 1,393 | 74 | Berkshire Hathaway, Inc. Class B(Æ) | 34,676 | 5,207 | |||

| Hershey Co. (The) | 14,360 | 1,492 | BlackRock, Inc. Class A | 3,931 | 1,406 | |||

| Kellogg Co. | 589 | 39 | BOK Financial Corp. | 700 | 42 | |||

| Kimberly-Clark Corp. | 858 | 99 | Capital One Financial Corp. | 37,496 | 3,095 | |||

| Kraft Foods Group, Inc.(Æ) | 657 | 41 | ||||||

| See accompanying notes which are an integral part of the financial statements. | ||||||||

| Multi -Style Equity Fund 19 | ||||||||

| Russell Investment Funds | |||||||

| Multi-Style Equity Fund | |||||||

| Schedule of Investments, continued — December 31, 2014 | |||||||

| Amounts in thousands (except share amounts) | Amounts in thousands (except share amounts) | ||||||

| Principal | Fair | Principal | Fair | ||||

| Amount ($) or | Value | Amount ($) or | Value | ||||

| Shares | $ | Shares | $ | ||||

| CDK Global, Inc.(Æ) | 358 | 15 | Bristol-Myers Squibb Co. | 75,555 | 4,460 | ||

| Charles Schwab Corp. (The) | 47,400 | 1,431 | Brookdale Senior Living, Inc. Class A(Æ) | 6,600 | 242 | ||

| Chubb Corp. (The) | 541 | 56 | Cardinal Health, Inc. | 17,100 | 1,380 | ||

| Citigroup, Inc. | 63,577 | 3,441 | Celgene Corp.(Æ) | 11,465 | 1,283 | ||

| CME Group, Inc. Class A | 39 | 3 | Cerner Corp.(Æ) | 30,060 | 1,944 | ||

| Comerica, Inc. | 23,800 | 1,115 | Clovis Oncology, Inc.(Æ)(Ñ) | 18,432 | 1,032 | ||

| Cullen/Frost Bankers, Inc. | 14,610 | 1,032 | Community Health Systems, Inc.(Æ) | 11,500 | 620 | ||

| Discover Financial Services | 37,787 | 2,475 | Covidien PLC | 35,829 | 3,664 | ||

| Equity Residential(ö) | 49 | 4 | Edwards Lifesciences Corp.(Æ) | 2,500 | 318 | ||

| Everest Re Group, Ltd. | 5,670 | 966 | Eli Lilly & Co. | 31,730 | 2,189 | ||

| FleetCor Technologies, Inc.(Æ) | 4,671 | 695 | Express Scripts Holding Co.(Æ) | 39,566 | 3,350 | ||

| Franklin Resources, Inc. | 7,475 | 414 | Gilead Sciences, Inc.(Æ) | 19,513 | 1,839 | ||

| Goldman Sachs Group, Inc. (The) | 17,750 | 3,440 | Halyard Health, Inc.(Æ) | 107 | 5 | ||

| Hartford Financial Services Group, Inc. | 19,729 | 823 | HCA Holdings, Inc.(Æ) | 22,863 | 1,678 | ||

| Intercontinental Exchange, Inc. | 8,650 | 1,897 | Health Net, Inc.(Æ) | 10,500 | 562 | ||

| Invesco, Ltd. | 30,000 | 1,186 | Humana, Inc. | 11,924 | 1,713 | ||

| JPMorgan Chase & Co. | 20,454 | 1,280 | Illumina, Inc.(Æ) | 2,529 | 467 | ||

| KeyCorp | 67,800 | 942 | Intercept Pharmaceuticals, Inc.(Æ)(Ñ) | 4,324 | 675 | ||

| Kimco Realty Corp.(ö) | 45,100 | 1,134 | Intuitive Surgical, Inc.(Æ) | 841 | 445 | ||

| Lincoln National Corp. | 14,850 | 856 | Johnson & Johnson | 56,997 | 5,960 | ||

| M&T Bank Corp.(Ñ) | 6,520 | 819 | McKesson Corp. | 6,263 | 1,300 | ||

| Markel Corp.(Æ) | 3,397 | 2,320 | Medtronic, Inc. | 13,644 | 985 | ||

| Marsh & McLennan Cos., Inc. | 1,246 | 71 | Merck & Co., Inc. | 55,431 | 3,148 | ||

| MasterCard, Inc. Class A | 17,319 | 1,492 | Mylan, Inc.(Æ) | 16,055 | 905 | ||

| McGraw Hill Financial, Inc. | 4,758 | 423 | Perrigo Co. PLC | 7,440 | 1,244 | ||

| MetLife, Inc. | 15,065 | 815 | Pfizer, Inc. | 306,268 | 9,539 | ||

| Morgan Stanley | 30,800 | 1,195 | Pharmacyclics, Inc.(Æ) | 5,801 | 709 | ||

| Northern Trust Corp. | 66,199 | 4,461 | Regeneron Pharmaceuticals, Inc.(Æ) | 2,558 | 1,049 | ||

| PartnerRe, Ltd. | 4,020 | 459 | Sanofi - ADR | 37,947 | 1,731 | ||

| PNC Financial Services Group, Inc. (The) | 61,912 | 5,648 | St. Jude Medical, Inc. | 35,121 | 2,284 | ||

| Principal Financial Group, Inc. | 15,400 | 800 | Stryker Corp. | 768 | 72 | ||

| Progressive Corp. (The) | 45,300 | 1,223 | Thermo Fisher Scientific, Inc. | 7,150 | 896 | ||

| Prologis, Inc.(ö) | 24,200 | 1,041 | UnitedHealth Group, Inc. | 40,621 | 4,107 | ||

| Prudential Financial, Inc. | 27,385 | 2,477 | Valeant Pharmaceuticals International, Inc. | ||||

| Public Storage(ö) | 318 | 59 | (Æ) | 23,501 | 3,364 | ||

| Regions Financial Corp. | 120,000 | 1,267 | 82,987 | ||||

| Simon Property Group, Inc.(ö) | 488 | 89 | |||||

| State Street Corp. | 27,120 | 2,129 | Materials and Processing - 5.1% | ||||

| TCF Financial Corp. | 29,500 | 469 | Air Products & Chemicals, Inc. | 180 | 26 | ||

| Thomson Reuters Corp. | 667 | 27 | Alcoa, Inc. | 107,205 | 1,693 | ||

| Travelers Cos., Inc. (The) | 11,287 | 1,194 | Dow Chemical Co. (The) | 34,700 | 1,583 | ||

| US Bancorp | 3,890 | 175 | Ecolab, Inc. | 37,539 | 3,924 | ||

| Visa, Inc. Class A | 25,576 | 6,706 | EI du Pont de Nemours & Co. | 6,343 | 469 | ||

| Voya Financial, Inc. | 27,300 | 1,157 | Fastenal Co.(Ñ) | 37,850 | 1,800 | ||

| Wells Fargo & Co. | 92,620 | 5,077 | Huntsman Corp. | 30,974 | 706 | ||

| 95,137 | LyondellBasell Industries Class A | 8,337 | 662 | ||||

| Monsanto Co. | 55,423 | 6,620 | |||||

| Health Care - 17.0% | Mosaic Co. (The) | 31,600 | 1,443 | ||||

| Abbott Laboratories | 45,448 | 2,046 | Nucor Corp. | 7,500 | 368 | ||

| Actavis PLC(Æ) | 7,597 | 1,956 | PPG Industries, Inc. | 7,574 | 1,751 | ||

| Aetna, Inc. | 12,953 | 1,151 | Praxair, Inc. | 12,004 | 1,555 | ||

| Alexion Pharmaceuticals, Inc.(Æ) | 1,357 | 251 | Precision Castparts Corp. | 5,845 | 1,408 | ||

| Allergan, Inc. | 13,055 | 2,775 | Steel Dynamics, Inc. | 36,900 | 728 | ||

| Amgen, Inc. | 30,984 | 4,936 | United States Steel Corp.(Ñ) | 12,200 | 326 | ||

| Anthem, Inc. | 11,730 | 1,474 | 25,062 | ||||

| Baxter International, Inc. | 1,236 | 91 | |||||

| Becton Dickinson and Co. | 438 | 61 | Producer Durables - 10.3% | ||||

| Biogen Idec, Inc.(Æ) | 5,405 | 1,834 | 3M Co. | 1,483 | 244 | ||

| Boston Scientific Corp.(Æ) | 94,600 | 1,253 | Accenture PLC Class A | 1,436 | 128 | ||

| See accompanying notes which are an integral part of the financial statements. | |||||||

| 20 Multi-Style Equity Fund | |||||||

Russell Investment Funds Multi-Style Equity Fund

Schedule of Investments, continued — December 31, 2014

| Amounts in thousands (except share amounts) | Amounts in thousands (except share amounts) | ||||||||

| Principal | Fair | Principal | Fair | ||||||

| Amount ($) or | Value | Amount ($) or | Value | ||||||

| Shares | $ | Shares | $ | ||||||

| American Airlines Group, Inc. | 16,368 | 878 | Intuit, Inc. | 19,264 | 1,776 | ||||

| Automatic Data Processing, Inc. | 26,803 | 2,234 | Juniper Networks, Inc. | 38,500 | 859 | ||||

| B/E Aerospace, Inc.(Æ) | 32,525 | 1,887 | Lam Research Corp. | 9,756 | 774 | ||||

| Babcock & Wilcox Co. (The) | 20,028 | 607 | LinkedIn Corp. Class A(Æ) | 4,760 | 1,093 | ||||

| Boeing Co. (The) | 34,350 | 4,465 | Marvell Technology Group, Ltd. | 75,600 | 1,096 | ||||

| Canadian Pacific Railway, Ltd. | 4,707 | 907 | Microsoft Corp. | 57,136 | 2,654 | ||||

| Caterpillar, Inc. | 17,050 | 1,561 | Motorola Solutions, Inc. | 18,000 | 1,207 | ||||

| CSX Corp. | 1,939 | 70 | NetApp, Inc. | 70,600 | 2,926 | ||||

| Cummins, Inc. | 126 | 18 | Nuance Communications, Inc.(Æ) | 19,500 | 278 | ||||

| Danaher Corp. | 1,382 | 118 | NXP Semiconductors(Æ) | 9,400 | 718 | ||||

| Deere & Co. | 135 | 12 | Oracle Corp. | 156,180 | 7,025 | ||||

| Delta Air Lines, Inc. | 24,120 | 1,186 | Plexus Corp.(Æ) | 3,300 | 136 | ||||

| Emerson Electric Co. | 1,516 | 94 | Polycom, Inc.(Æ) | 16,400 | 221 | ||||

| FedEx Corp. | 4,944 | 859 | QUALCOMM, Inc. | 84,847 | 6,306 | ||||

| General Dynamics Corp. | 11,937 | 1,643 | Red Hat, Inc.(Æ) | 20,760 | 1,435 | ||||

| General Electric Co. | 263,166 | 6,650 | Salesforce.com, Inc.(Æ) | 31,111 | 1,845 | ||||

| Honeywell International, Inc. | 62,103 | 6,205 | SAP AG - ADR(Ñ) | 25,580 | 1,782 | ||||

| Huntington Ingalls Industries, Inc. | 540 | 61 | ServiceNow, Inc.(Æ) | 8,007 | 543 | ||||

| Illinois Tool Works, Inc. | 733 | 69 | Splunk, Inc.(Æ) | 7,657 | 451 | ||||

| Itron, Inc.(Æ) | 11,300 | 478 | Symantec Corp. | 50,100 | 1,285 | ||||

| KLX, Inc.(Æ) | 16,263 | 671 | Synopsys, Inc.(Æ) | 26,300 | 1,143 | ||||

| L-3 Communications Holdings, Inc. Class 3 | 9,200 | 1,161 | Tableau Software, Inc. Class A(Æ) | 4,100 | 348 | ||||

| Lexmark International, Inc. Class A | 19,910 | 822 | Texas Instruments, Inc. | 2,450 | 131 | ||||

| Lockheed Martin Corp. | 615 | 118 | VeriFone Systems, Inc.(Æ) | 372 | 14 | ||||

| Mettler-Toledo International, Inc.(Æ) | 9,360 | 2,831 | VMware, Inc. Class A(Æ) | 21 | 2 | ||||

| Norfolk Southern Corp. | 6,781 | 744 | Vodafone Group PLC - ADR | 87,331 | 2,984 | ||||

| Northrop Grumman Corp. | 456 | 67 | Western Digital Corp. | 15,734 | 1,742 | ||||

| Paychex, Inc. | 22,000 | 1,016 | Workday, Inc. Class A(Æ) | 6,235 | 509 | ||||

| Pentair PLC | 6,500 | 432 | Yahoo!, Inc.(Æ) | 19,336 | 977 | ||||

| Raytheon Co. | 22,322 | 2,414 | Zynga, Inc. Class A(Æ) | 138,400 | 368 | ||||

| Rockwell Collins, Inc. | 12,100 | 1,022 | 79,478 | ||||||

| Sensata Technologies Holding(Æ) | 34,489 | 1,808 | |||||||

| TransDigm Group, Inc. | 12,024 | 2,361 | Utilities - 2.3% | ||||||

| Union Pacific Corp. | 16,342 | 1,947 | American Electric Power Co., Inc. | 894 | 54 | ||||

| United Continental Holdings, Inc.(Æ) | 17,265 | 1,155 | AT&T, Inc. | 108,063 | 3,629 | ||||

| United Parcel Service, Inc. Class B | 1,603 | 178 | Dominion Resources, Inc. | 395 | 30 | ||||

| United Technologies Corp. | 9,210 | 1,059 | Duke Energy Corp. | 6,011 | 502 | ||||

| Waste Management, Inc. | 593 | 30 | Edison International | 21,900 | 1,434 | ||||

| 50,210 | Encana Corp. | 66,100 | 917 | ||||||

| Exelon Corp. | 62,484 | 2,317 | |||||||

| Technology - 16.3% | NextEra Energy, Inc. | 845 | 90 | ||||||

| Adobe Systems, Inc.(Æ) | 40,726 | 2,961 | PG&E Corp. | 27,594 | 1,470 | ||||

| Altera Corp. | 24,048 | 888 | Southern Co. | 5,921 | 291 | ||||

| Analog Devices, Inc. | 34,109 | 1,894 | Verizon Communications, Inc. | 9,385 | 439 | ||||

| Apple, Inc. | 60,050 | 6,628 | 11,173 | ||||||

| ASML Holding Class G | 16,600 | 1,790 | |||||||

| Broadcom Corp. Class A | 31,000 | 1,343 | Total Common Stocks | ||||||

| Cisco Systems, Inc. | 37,064 | 1,031 | (cost $377,959) | 467,247 | |||||

| Cognizant Technology Solutions Corp. Class | |||||||||