| Goldman Sachs Tax-Advantaged Global Equity Portfolio | ||||||||||||||||||||||||||||||||||||

| Goldman Sachs Tax-Advantaged Global Equity Portfolio—Summary | ||||||||||||||||||||||||||||||||||||

| Investment Objective | ||||||||||||||||||||||||||||||||||||

| The Goldman Sachs Tax-Advantaged Global Equity (“TAG”) Portfolio (the “Portfolio”) seeks long-term growth of capital. | ||||||||||||||||||||||||||||||||||||

| Fees and Expenses of the Portfolio | ||||||||||||||||||||||||||||||||||||

| This table describes the fees and expenses that you may pay if you buy and hold shares of the Portfolio. You may qualify for sales charge discounts on purchases of Class A Shares if you and your family invest, or agree to invest in the future, at least $50,000 in Goldman Sachs Funds. More information about these and other discounts is available from your financial professional and in “Shareholder Guide—Common Questions Applicable to the Purchase of Class A Shares” beginning on page 76 of this Prospectus and “Other Information Regarding Maximum Sales Charge, Purchases, Redemptions, Exchanges and Dividends” beginning on page B-119 of the Portfolio’s Statement of Additional Information (“SAI”). | ||||||||||||||||||||||||||||||||||||

| Shareholder Fees (fees paid directly from your investment) |

||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||

| Annual Portfolio Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||

| Expense Example | ||||||||||||||||||||||||||||||||||||

| This Example is intended to help you compare the cost of investing in the Portfolio with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in Class A Shares and Institutional Shares of the Portfolio for the time periods indicated and then redeem all of your Class A Shares and Institutional Shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Portfolio’s operating expenses remain the same (except that the Example incorporates the expense limitation arrangement for only the first year). Although your actual costs may be higher or lower, based on these assumptions your costs would be: | ||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||

| Portfolio Turnover | ||||||||||||||||||||||||||||||||||||

| The Portfolio does not pay transaction costs when it buys and sells shares of the Underlying Funds (as defined below). However, the Portfolio and the Underlying Funds pay transaction costs when they buy and sell other securities or instruments (i.e., “turn over” their portfolios). A high rate of portfolio turnover may result in increased transaction costs, including brokerage commissions, which must be borne by the Portfolio or Underlying Fund and its shareholders, including the Portfolio, and is also likely to result in higher short-term capital gains for taxable shareholders. These costs are not reflected in annual Portfolio operating expenses or in the expense example above, but are reflected in the Portfolio’s performance. The Portfolio’s portfolio turnover rate for the fiscal year ending August 31, 2012 was 24% of the average value of its portfolio. | ||||||||||||||||||||||||||||||||||||

| Principal Strategy | ||||||||||||||||||||||||||||||||||||

| The Portfolio seeks to achieve its investment objective by investing in securities or instruments and a combination of underlying funds that currently exist or that may become available for investment in the future for which GSAM or an affiliate now or in the future acts as investment adviser or principal underwriter (the “Underlying Funds”). Some of the Underlying Funds invest primarily in fixed income or money market instruments (the “Underlying Fixed Income Funds”) and other Underlying Funds invest primarily in equity securities (the “Underlying Equity Funds”). Under normal conditions, at least 80% of the Portfolio’s total assets measured at time of purchase (“Total Assets”) will be allocated among Underlying Funds. While it is expected that the Portfolio will invest primarily in the Underlying Funds, the Portfolio may also invest directly in other securities and instruments, including unaffiliated ETFs. The Portfolio is intended for investors who wish to minimize short-term gains and defer long-term gains. Additionally, under normal circumstances, the Portfolio intends to invest at least 80% of its net assets plus any borrowings for investment purposes (measured at time of purchase) (“Net Assets”) in Underlying Equity Funds and equity securities with a blend of domestic large cap, small cap and international exposure to seek capital appreciation. The Investment Adviser expects that the Portfolio will invest a relatively significant percentage of its equity allocation in the Goldman Sachs Structured Tax-Managed Equity and Goldman Sachs Structured International Tax-Managed Equity Funds (the “Underlying Tax-Managed Funds”). In addition, under normal circumstances, the Portfolio will have a small strategic allocation in U.S. investment grade bonds. This strategic allocation will normally be approximately 10% of the Portfolio’s Total Assets and may consist of an investment in the Goldman Sachs Core Fixed Income Fund or investments in other fixed income securities. This allocation in the Portfolio serves two purposes. First, it provides some ordinary income which can be netted against Portfolio expenses and may increase the net distributions of qualifying dividends (i.e., those dividends subject to the federal long-term capital gain tax rate) when paid in a taxable year beginning before January 1, 2013 (if not extended further by Congress). Second, it will provide the Investment Adviser with an allocation in which to implement its tactical views. The Investment Adviser may occasionally develop views regarding short-term expected returns, and may seek to temporarily change the allocations in the Portfolio in an attempt to improve short-term return. The Investment Adviser may implement such tactical views by selling and buying among the various Underlying Funds or by purchasing securities or other instruments, including ETFs. As part of a tactical allocation, the Portfolio, as of the date of this Prospectus, invests in the Goldman Sachs High Yield Fund. Under normal conditions, the Portfolio may have up to 20% of its Total Assets invested directly in securities and other instruments, including derivative instruments (such as swaps, forward currency contracts and futures contracts). These securities and other instruments may be denominated in currencies other than the U.S. dollar. Because the Investment Adviser may have both positive and negative views on stocks, the Portfolio may also establish short positions. In managing the Portfolio, the Investment Adviser balances investment considerations and tax considerations. The Portfolio seeks to achieve returns primarily in the form of price appreciation (which is not subject to current tax), and may use different strategies in seeking tax-efficiency. These strategies include:

|

||||||||||||||||||||||||||||||||||||

| Principal Risks of the Portfolio | ||||||||||||||||||||||||||||||||||||

| Loss of money is a risk of investing in the Portfolio. An investment in the Portfolio is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation (“FDIC”) or any government agency. The Portfolio should not be relied upon as a complete investment program. There can be no assurance that the Portfolio will achieve its investment objective. Affiliated Persons. The Investment Adviser will have the authority to select and substitute Underlying Funds. The Investment Adviser and/or its affiliates are compensated by the Portfolios and by the Underlying Funds for advisory and/or principal underwriting services provided. The Investment Adviser is subject to conflicts of interest in allocating Portfolio assets among the various Underlying Funds both because the fees payable to it and/or its affiliates by Underlying Funds differ and because the Investment Adviser and its affiliates are also responsible for managing the Underlying Funds. The portfolio managers may also be subject to conflicts of interest in allocating Portfolio assets among the various Underlying Funds because the Portfolio’s portfolio management team may also manage some of the Underlying Funds. The Trustees and officers of the Goldman Sachs Trust may also have conflicting interests in fulfilling their fiduciary duties to both the Portfolios and the Underlying Funds for which GSAM or its affiliates now or in the future serve as investment adviser or principal underwriter. Derivatives Risk. Loss may result from the Portfolio’s investments in options, futures, forwards, swaps, options on swaps, structured securities and other derivative instruments. These instruments may be illiquid, difficult to price and leveraged so that small changes may produce disproportionate losses to the Portfolio. Derivatives are also subject to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation. Expenses. By investing in the Underlying Funds indirectly through the Portfolio, the investor will incur not only a proportionate share of the expenses of the Underlying Funds held by the Portfolio (including operating costs and investment management fees), but also expenses of the Portfolio. Investing in the Underlying Funds. The investments of the Portfolio are concentrated in the Underlying Funds, and the Portfolio’s investment performance is directly related to the investment performance of the Underlying Funds it holds. The ability of the Portfolio to meet its investment objective is directly related to the ability of the Underlying Funds to meet their objectives as well as the allocation among those Underlying Funds by the Investment Adviser. Investments of the Underlying Funds. Because the Portfolio invests in the Underlying Funds, the Portfolio’s shareholders will be affected by the investment policies and practices of the Underlying Funds in direct proportion to the amount of assets the Portfolio allocates to those Underlying Funds. See the Principal Risks of the Underlying Funds below. Short Positions Risk. The Portfolio may use derivatives, including futures and swaps, to implement short positions. Taking short positions involves leverage of the Portfolio’s assets and presents various risks. If the price of the instrument or market which the Portfolio has taken a short position on increases, then the Portfolio will incur a loss equal to the increase in price from the time that the short position was entered into plus any premiums and interest paid to a counterparty. Therefore, taking short positions involves the risk that losses may be exaggerated, potentially losing more money than the actual cost of the investment. Tax-Managed Investment Risk. Because the Investment Adviser balances investment considerations and tax considerations, the pre-tax performance of the Portfolio may be lower than the performance of similar funds that are not tax-managed. Even though tax managed strategies are being used, they may not reduce the amount of taxable income and capital gains distributed by the Portfolio to shareholders. Temporary Investments. Although the Portfolio normally seeks to invest approximately 80% of its Total Assets in the Underlying Funds, the Portfolio may invest a portion of its assets in high-quality, short-term debt obligations to maintain liquidity, to meet shareholder redemptions and for other short-term cash needs. For temporary defensive purposes during abnormal market or economic conditions, the Portfolio may invest without limitation in short-term obligations. When the Portfolio’s assets are invested in such investments, the Portfolio may not be achieving its investment objective. Principal Risks of the Underlying Funds Credit/Default Risk. An issuer or guarantor of fixed income securities held by an Underlying Fund (which may have low credit ratings) may default on its obligation to pay interest and repay principal or default on any other obligation. Additionally, the credit quality of securities may deteriorate rapidly, which may impair an Underlying Fund’s liquidity and cause significant NAV deterioration. To the extent that an Underlying Fund invests in non-investment grade fixed income securities, these risks will be more pronounced. Derivatives Risk. Loss may result from an Underlying Fund’s investments in options, futures, forwards, swaps, structured securities and other derivative instruments. These instruments may be illiquid, difficult to price and leveraged so that small changes may produce disproportionate losses to an Underlying Fund. Derivatives are also subject to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation. Foreign and Emerging Countries Risk. Foreign securities may be subject to risk of loss because of more or less foreign government regulation, less public information and less economic, political and social stability in the countries in which an Underlying Fund invests. Loss may also result from the imposition of exchange controls, confiscations and other government restrictions, or from problems in registration, settlement or custody. Foreign risk also involves the risk of negative foreign currency rate fluctuations, which may cause the value of securities denominated in such foreign currency (or other instruments through which the Underlying Fund has exposure to foreign currencies) to decline in value. Currency exchange rates may fluctuate significantly over short periods of time. To the extent that the Underlying Fund also invests in issuers located in emerging markets, these risks may be more pronounced. Interest Rate Risk. When interest rates increase, fixed income securities or instruments held by an Underlying Fund will generally decline in value. Long-term fixed income securities or instruments will normally have more price volatility because of this risk than short-term fixed income securities or instruments. Investment Style Risk. Different investment styles (e.g., “growth”, “value” or “quantitative”) tend to shift in and out of favor depending upon market and economic conditions and investor sentiment. An Underlying Fund may outperform or underperform other funds that invest in similar asset classes but employ different investment styles. Liquidity Risk. An Underlying Fund may make investments that are illiquid or that may become less liquid in response to market developments or adverse investor perceptions. Illiquid investments may be more difficult to value. Liquidity risk may also refer to the risk that an Underlying Fund will not be able to pay redemption proceeds within the allowable time period because of unusual market conditions, an unusually high volume of redemption requests, or other reasons. To meet redemption requests, an Underlying Fund may be forced to sell securities at an unfavorable time and/or under unfavorable conditions. Management Risk. The risk that a strategy used by an Underlying Fund’s investment adviser may fail to produce the intended results. With respect to certain Underlying Funds, the Underlying Fund’s investment adviser attempts to execute a complex investment strategy using proprietary quantitative models. Investments selected using these models may perform differently than expected as a result of the factors used in the models, the weight placed on each factor, changes from the factors’ historical trends, and technical issues in the construction and implementation of the models (including, for example, data problems and/or software issues). There is no guarantee that an Underlying Fund’s investment adviser’s use of these quantitative models will result in effective investment decisions for the Underlying Fund. Additionally, commonality of holdings across quantitative money managers may amplify losses. Market Risk. The market value of the instruments in which an Underlying Fund invests may go up or down in response to the prospects of individual companies, particular sectors or governments and/or general economic conditions throughout the world due to increasingly interconnected global economies and financial markets. Mid-Cap and Small-Cap Risk. Investments in mid-capitalization and small-capitalization companies involve greater risks than investments in larger, more established companies. These securities may be subject to more abrupt or erratic price movements and may lack sufficient market liquidity, and these issuers often face greater business risks. Mortgage-Backed and Other Asset-Backed Securities Risk. Mortgage-related and other asset-backed securities are subject to certain additional risks, including “extension risk” (i.e., in periods of rising interest rates, issuers may pay principal later than expected) and “prepayment risk” (i.e., in periods of declining interest rates, issuers may pay principal more quickly than expected, causing an Underlying Fund to reinvest proceeds at lower prevailing interest rates). Mortgage-backed securities offered by non-governmental issuers are subject to other risks as well, including failures of private insurers to meet their obligations and unexpectedly high rates of default on the mortgages backing the securities. Other asset-backed securities are subject to risks similar to those associated with mortgage-backed securities, as well as risks associated with the nature and servicing of the assets backing the securities. Asset-backed securities may not have the benefit of a security interest in collateral comparable to that of mortgage assets, resulting in additional credit risk. Non-Diversification Risk. Certain of the Underlying Funds are non-diversified, meaning that they are permitted to invest more of their assets in fewer issuers than diversified mutual funds. Thus, an Underlying Fund may be more susceptible to adverse developments affecting any single issuer held in its portfolio, and may be more susceptible to greater losses because of these developments. Non-Hedging Foreign Currency Trading Risk. Certain Underlying Funds may engage in forward foreign currency transactions for speculative purposes. An Underlying Fund’s investment adviser may purchase or sell foreign currencies through the use of forward contracts based on the investment adviser’s judgment regarding the direction of the market for a particular foreign currency or currencies. In pursuing this strategy, the Underlying Fund’s investment adviser seeks to profit from anticipated movements in currency rates by establishing “long” and/or “short” positions in forward contracts on various foreign currencies. Foreign exchange rates can be extremely volatile and a variance in the degree of volatility of the market or in the direction of the market from the investment adviser’s expectations may produce significant losses to the Underlying Fund. Some of these transactions may also be subject to interest rate risk. Non-Investment Grade Fixed Income Securities Risk. Non-investment grade fixed income securities and unrated securities of comparable credit quality (commonly referred to as “junk bonds”) are considered speculative and are subject to the increased risk of an issuer’s inability to meet principal and interest payment obligations. These securities may be subject to greater price volatility due to such factors as specific corporate or municipal developments, interest rate sensitivity, negative perceptions of the junk bond markets generally and less secondary market liquidity. Option Writing Risk. Writing (selling) call options limits the opportunity to profit from an increase in the market value of stocks in exchange for up-front cash (premium) at the time of selling the call option. When an Underlying Fund writes stock index (or related ETF) call options, it receives cash but limits its opportunity to profit from an increase in the market value of the index beyond the exercise price (plus the premium received) of the option. In a rising market, such Underlying Funds could significantly underperform the market, and these Underlying Funds’ option strategies may not fully protect them against declines in the value of the market. Cash received from premiums will enhance return in declining markets, but each Underlying Fund will continue to bear the risk of a decline in the value of the securities held in its portfolio and in a period of a sharply falling equity market, these Underlying Funds will likely also experience sharp declines in their net asset value. Portfolio Turnover Rate Risk. A high rate of portfolio turnover (100% or more) involves correspondingly greater expenses which must be borne by an Underlying Fund and its shareholders (including the Portfolios), and is also likely to result in short-term capital gains taxable to shareholders of the Underlying Fund. Sovereign Risk. An issuer of non-U.S. sovereign debt, or the governmental authorities that control the repayment of the debt, may be unable or unwilling to repay the principal or interest when due. This may result from political or social factors, the general economic environment of a country, levels of foreign debt or foreign currency exchange rates. Stock Risk. Stock prices have historically risen and fallen in periodic cycles. U.S. and foreign stock markets have experienced periods of substantial price volatility in the past and may do so again in the future. Tax-Managed Investment Risk. Because the investment advisers of certain Underlying Funds balance investment considerations and tax considerations, the pre-tax performance of those Underlying Funds may be lower than the performance of similar funds that are not tax-managed. Even though tax-managed strategies are being used, they may not reduce the amount of taxable income and capital gains distributed by the Underlying Funds to shareholders. A high percentage of an Underlying Fund’s NAV may consist of unrealized capital gains, which represent a potential future tax liability to shareholders. U.S. Government Securities Risk. The U.S. government may not provide financial support to U.S. government agencies, instrumentalities or sponsored enterprises if it is not obligated to do so by law. U.S. Government Securities issued by those agencies, instrumentalities and sponsored enterprises, including those issued by the Federal National Mortgage Association (“Fannie Mae”), Federal Home Loan Mortgage Corporation (“Freddie Mac”) and the Federal Home Loan Banks, are neither issued nor guaranteed by the U.S. Treasury and, therefore, are not backed by the full faith and credit of the United States. The maximum potential liability of the issuers of some U.S. Government Securities held by an Underlying Fund may greatly exceed their current resources, including any legal right to support from the U.S. Treasury. It is possible that issuers of U.S. Government Securities will not have the funds to meet their payment obligations in the future. Further Information on Investment Objectives, Strategies and Risks of the Underlying Funds. A concise description of the investment objectives, practices and risks of each of the Underlying Funds that are currently expected to be used for investment by the Portfolio as of the date of this Prospectus is provided beginning on page 36 of this Prospectus. |

||||||||||||||||||||||||||||||||||||

| Performance | ||||||||||||||||||||||||||||||||||||

| The bar chart and table below provide an indication of the risks of investing in the Portfolio by showing how the average annual total returns of the Portfolio’s Class A Shares and Institutional Shares compare to those of certain broad-based securities market indices and to the Tax-Advantaged Global Composite Index (“TAG Composite Index”), a composite representation prepared by the Investment Adviser of the Portfolio’s asset classes weighted according to their respective weightings in the Portfolio’s target range. The TAG Composite Index is comprised of the Barclays U.S. Aggregate Bond Index (10%), the MSCI ACWI, ex North America (30%) and the Russell 3000 Index (60%). The Portfolio’s past performance, before and after taxes, is not necessarily an indication of how the Portfolio will perform in the future. Updated performance information is available at no cost at www.goldmansachsfunds.com/performance or by calling the appropriate phone number on the back cover of this Prospectus. The bar chart (including “Best Quarter” and “Worst Quarter” information) does not reflect the sales loads applicable to Class A Shares. If the sales loads were reflected, returns would be less. Performance reflects fee waivers and/or expense limitations in effect during the periods shown. |

||||||||||||||||||||||||||||||||||||

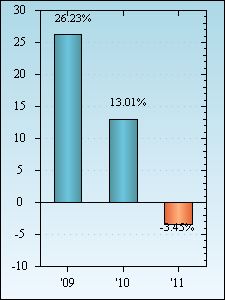

| TOTAL RETURN CALENDAR YEAR (CLASS A) | ||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||

| The total return for Class A Shares for the 9-month period ended September 30, 2012 was 14.01%. Best Quarter Q2 ’09 +17.52% Worst Quarter Q3 ‘11 −16.46% |

||||||||||||||||||||||||||||||||||||

| AVERAGE ANNUAL TOTAL RETURN For the period ended December 31, 2011 |

||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||

| The after-tax returns are for Class A Shares only. The after-tax returns for Institutional Shares will vary. After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. In addition, the after-tax returns shown are not relevant to investors who hold Portfolio shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. | ||||||||||||||||||||||||||||||||||||