Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2012

| Commission File Number |

Exact Name of Registrant as Specified in its Charter, State or Other Jurisdiction of Incorporation, |

I.R.S. Employer Identification Number | ||

| 001-31403 |

PEPCO HOLDINGS, INC. (Pepco Holdings or PHI), a Delaware corporation 701 Ninth Street, N.W. Washington, D.C. 20068 Telephone: (202)872-2000 |

52-2297449 | ||

| 001-01072 |

POTOMAC ELECTRIC POWER COMPANY (Pepco), a District of Columbia and Virginia corporation 701 Ninth Street, N.W. Washington, D.C. 20068 Telephone: (202)872-2000 |

53-0127880 | ||

| 001-01405 |

DELMARVA POWER & LIGHT COMPANY (DPL), a Delaware and Virginia corporation 500 North Wakefield Drive, 2nd Floor Newark, DE 19702 Telephone: (202)872-2000 |

51-0084283 | ||

| 001-03559 |

ATLANTIC CITY ELECTRIC COMPANY (ACE), a New Jersey corporation 500 North Wakefield Drive, 2nd Floor Newark, DE 19702 Telephone: (202)872-2000 |

21-0398280 | ||

Securities registered pursuant to Section 12(b) of the Act:

| Registrant |

Title of Each Class |

Name of Each Exchange on Which Registered | ||

| Pepco Holdings | Common Stock, $.01 par value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

| Registrant |

Title of Each Class | |

| Pepco | Common Stock, $.01 par value | |

| DPL | Common Stock, $2.25 par value | |

| ACE | Common Stock, $3.00 par value |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| Pepco Holdings | Yes x | No ¨ | Pepco | Yes ¨ | No x | |||||||

| DPL | Yes ¨ | No x | ACE | Yes ¨ | No x | |||||||

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

| Pepco Holdings | Yes ¨ | No x | Pepco | Yes ¨ | No x | |||||||

| DPL | Yes ¨ | No x | ACE | Yes ¨ | No x | |||||||

Indicate by check mark whether each registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to such filing requirements for the past 90 days.

| Pepco Holdings | Yes x | No ¨ | Pepco | Yes x | No ¨ | |||||||

| DPL | Yes x | No ¨ | ACE | Yes x | No ¨ | |||||||

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

| Pepco Holdings | Yes x | No ¨ | Pepco | Yes x | No ¨ | |||||||

| DPL | Yes x | No ¨ | ACE | Yes x | No ¨ | |||||||

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K (applicable to Pepco Holdings only). x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer |

Accelerated Filer |

Non- Accelerated Filer |

Smaller Reporting Company | |||||

| Pepco Holdings |

x | ¨ | ¨ | ¨ | ||||

| Pepco |

¨ | ¨ | x | ¨ | ||||

| DPL |

¨ | ¨ | x | ¨ | ||||

| ACE |

¨ | ¨ | x | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| Pepco Holdings | Yes ¨ | No x | Pepco | Yes ¨ | No x | |||||||

| DPL | Yes ¨ | No x | ACE | Yes ¨ | No x | |||||||

Pepco, DPL, and ACE meet the conditions set forth in General Instruction I(1)(a) and (b) of Form 10-K and are therefore filing this Form 10-K with the reduced disclosure format specified in General Instruction I(2) of Form 10-K.

| Registrant |

Aggregate Market Value of Voting and Non-Voting Common Equity Held by Non-Affiliates of the Registrant at June 29, 2012 |

Number of Shares of Common Stock of the Registrant Outstanding at February 15, 2013 | ||

| Pepco Holdings | $4,464,800,000(a) | 230,073,469 ($.01 par value) | ||

| Pepco | None (b) | 100 ($.01 par value) | ||

| DPL | None (c) | 1,000 ($2.25 par value) | ||

| ACE | None (c) | 8,546,017 ($3.00 par value) |

| (a) | Solely for purposes of calculating this aggregate market value, PHI has defined its affiliates to include (i) those persons who were, as of June 29, 2012, its executive officers, directors and beneficial owners of more than 10% of its common stock, and (ii) such other persons who were, as of June 29, 2012, controlled by, or under common control with, the persons described in clause (i) above. |

| (b) | All voting and non-voting common equity is owned by Pepco Holdings. |

| (c) | All voting and non-voting common equity is owned by Conectiv, LLC, a wholly owned subsidiary of Pepco Holdings. |

THIS COMBINED FORM 10-K IS SEPARATELY FILED BY PEPCO HOLDINGS, PEPCO, DPL AND ACE. INFORMATION CONTAINED HEREIN RELATING TO ANY INDIVIDUAL REGISTRANT IS FILED BY SUCH REGISTRANT ON ITS OWN BEHALF. EACH REGISTRANT MAKES NO REPRESENTATION AS TO INFORMATION RELATING TO THE OTHER REGISTRANTS.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Pepco Holdings, Inc. definitive proxy statement for the 2013 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission within 120 days after December 31, 2012 are incorporated by reference into Part III of this report.

Table of Contents

Table of Contents

The following is a glossary of terms, abbreviations and acronyms that are used in the Reporting Companies’ SEC reports. The terms, abbreviations and acronyms used have the meanings set forth below, unless the context requires otherwise.

| Term |

Definition | |

| 2012 LTIP | Pepco Holdings, Inc. 2012 Long-Term Incentive Plan | |

| ACE | Atlantic City Electric Company | |

| ACE Funding | Atlantic City Electric Transition Funding LLC | |

| AFUDC | Allowance for funds used during construction | |

| AOCL | Accumulated Other Comprehensive Loss | |

| AMI | Advanced metering infrastructure, a system that collects, measures and analyzes energy usage data from advanced digital electric and gas meters known as smart meters | |

| ASC | Accounting Standards Codification | |

| BGS | Basic Generation Service (the supply of electricity by ACE to retail customers in New Jersey who have not elected to purchase electricity from a competitive supplier) | |

| BGS-CIEP | BGS-Commercial and Industrial Energy Price | |

| BGS-FP | BGS-Fixed Price | |

| Bondable Transition Property | Principal and interest payments on the Transition Bonds and related taxes, expenses and fees | |

| BSA | Bill Stabilization Adjustment | |

| Budget Support Act | The Fiscal Year 2012 Budge Support Act of 2011, approved by the Council of the District of Columbia on June 14, 2011 | |

| CAA | Federal Clean Air Act | |

| Calpine | Calpine Corporation | |

| CERCLA | Comprehensive Environmental Response, Compensation, and Liability Act of 1980 | |

| Conectiv | Conectiv, LLC, a wholly owned subsidiary of PHI and the parent of DPL and ACE | |

| Conectiv Energy | Subsidiaries of Conectiv Energy Holding Company, a disposition plan for which was approved by PHI’s Board of Directors in April 2010 and has been completed | |

| CRMC | PHI’s Corporate Risk Management Committee | |

| DCPSC | District of Columbia Public Service Commission | |

| DDOE | District of Columbia Department of the Environment | |

| Default Electricity Supply | The supply of electricity by PHI’s electric utility subsidiaries at regulated rates to retail customers who do not elect to purchase electricity from a competitive supplier, and which, depending on the jurisdiction, is also known as Standard Offer Service or BGS | |

| DPL | Delmarva Power & Light Company | |

| DEDA | Delaware Economic Development Authority | |

| DOE | U.S. Department of Energy | |

| DPSC | Delaware Public Service Commission | |

| DRP | Shareholder Dividend Reinvestment Plan | |

| EBITDA | Earnings before interest, taxes, depreciation, and amortization | |

| EDC | Electricity Distribution Company | |

| EmPower Maryland | A Maryland demand-side management program for Pepco and DPL | |

| EPA | U.S. Environmental Protection Agency | |

| Exchange Act | Securities Exchange Act of 1934, as amended | |

| FASB | Financial Accounting Standards Board | |

| FERC | Federal Energy Regulatory Commission | |

| FPA | Federal Power Act | |

| GAAP | Accounting principles generally accepted in the United States of America | |

| GCR | Gas Cost Rate | |

| GWh | Gigawatt hour | |

| HPS | Hourly Priced Service | |

| IIP | ACE’s Infrastructure Investment Program | |

i

Table of Contents

| Term |

Definition | |

| IRS | Internal Revenue Service | |

| ISDA | International Swaps and Derivatives Association Master Agreement | |

| ISRA | Industrial Site Recovery Act | |

| LIBOR | London Interbank Offered Rate | |

| Line Losses | Estimates of electricity and gas expected to be lost in the process of its transmission and distribution to customers | |

| LTIP | The Pepco Holdings, Inc. Long-Term Incentive Plan | |

| MAPP | Mid-Atlantic Power Pathway | |

| Market Transition Charge Tax | Revenue ACE receives and pays to ACE Funding to recover income taxes associated with Transition Bond Charge revenue | |

| Mcf | Thousand Cubic Feet | |

| MDC | MDC Industries, Inc. | |

| Medicare Act | Medicare Prescription Drug Improvement and Modernization Act of 2003 | |

| Medicare Part D | A prescription drug benefit under the Medicare Act | |

| MFVRD | Modified fixed variable rate design | |

| Mirant | Mirant Corporation | |

| MMBtu | One Million British Thermal Units | |

| MPSC | Maryland Public Service Commission | |

| MW | Megawatt | |

| MWh | Megawatt hour | |

| NAV | Net Asset Value | |

| NERC | North American Electric Reliability Corporation | |

| New Jersey Settlement | A stipulation of settlement signed by the parties to ACE’s electric distribution base rate case, which was approved by the NJBPU on October 23, 2012 | |

| New Jersey Societal Benefit Charge | A surcharge related to the New Jersey Societal Benefit Program | |

| New Jersey Societal Benefit Program |

A New Jersey public interest program for low income customers | |

| NJBPU | New Jersey Board of Public Utilities | |

| NPCC | Northeast Power Coordinating Council | |

| NPDES | National Pollutant Discharge Elimination System | |

| NUGs | Non-utility generators | |

| NYMEX | New York Mercantile Exchange | |

| OPEB | Other postretirement benefit | |

| PCI | Potomac Capital Investment Corporation and its subsidiaries | |

| Pepco | Potomac Electric Power Company | |

| Pepco Energy Services | Pepco Energy Services, Inc. and its subsidiaries | |

| Pepco Holdings or PHI | Pepco Holdings, Inc. | |

| PHI OPEB Plan | The Pepco Holdings, Inc. Welfare Plan for Retirees | |

| PJM | PJM Interconnection, LLC | |

| PJM RTO | PJM regional transmission organization | |

| Power Delivery | The transmission, distribution and default supply of electricity and, to a lesser extent, the distribution and supply of natural gas, conducted through Pepco, DPL and ACE, PHI’s regulated public utility subsidiaries. | |

| PPA | Power purchase agreement | |

| PRP | Potentially responsible party | |

| PUHCA 2005 | Public Utility Holding Company Act of 2005 | |

| RECs | Renewable energy credits | |

ii

Table of Contents

| Term |

Definition | |

| Regulated T&D Electric Revenue | Revenue from the transmission and the distribution of electricity to PHI’s customers within its service territories at regulated rates | |

| Regulatory Asset Recovery Charge | Costs associated with deferred, NJBPU-approved expenses incurred as part of ACE’s obligation to serve the public | |

| Reporting Company | PHI, Pepco, DPL or ACE | |

| Revenue Decoupling Adjustment | An adjustment equal to the amount by which revenue from distribution sales differs from the revenue that Pepco and DPL are entitled to earn based on the approved distribution charge per customer | |

| RFC | ReliabilityFirst Corporation | |

| RI/FS | Remedial investigation and feasibility study | |

| RIM | Reliability investment recovery mechanism | |

| ROE | Return on equity | |

| RPS | Renewable Energy Portfolio Standards | |

| Sarbanes-Oxley Act | Sarbanes-Oxley Act of 2002 | |

| SEC | Securities and Exchange Commission | |

| SO2 | Sulfur dioxide | |

| SOCA | Standard Offer Capacity Agreement required to be entered into by ACE pursuant to a New Jersey law enacted to promote the construction of qualified electric generation facilities in New Jersey | |

| SOS | Standard Offer Service, how Default Electricity Supply is referred to in Delaware, the District of Columbia and Maryland | |

| SPCC | Spill Prevention, Control, and Countermeasure plans, required pursuant to federal regulations requiring plans for facilities using oil-containing equipment in proximity to surface waters | |

| SRECs | Solar renewable energy credits | |

| T&D | Transmission and distribution | |

| TEFA | Transitional Energy Facility Assessment, a New Jersey tax surcharge providing a gradual transition from the previous franchise and gross receipts tax eliminated in 1997, to its new total liability under the corporation business tax and the sales-and-use tax (this surcharge will be eliminated in 2013) | |

| Transition Bond Charge | Revenue ACE receives, and pays to ACE Funding, to fund the principal and interest payments on Transition Bonds and related taxes, expenses and fees | |

| Transition Bonds | Transition Bonds issued by ACE Funding | |

| VADEQ | Virginia Department of Environmental Quality | |

| VaR | Value at Risk | |

| VRDBs | Variable Rate Demand Bonds | |

| WACC | Weighted average cost of capital | |

iii

Table of Contents

Some of the statements contained in this Annual Report on Form 10-K with respect to Pepco Holdings, Inc. (PHI or Pepco Holdings), Potomac Electric Power Company (Pepco), Delmarva Power & Light Company (DPL) and Atlantic City Electric Company (ACE), including each of their respective subsidiaries, are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the Exchange Act), and Section 27A of the Securities Act of 1933, as amended, and are subject to the safe harbor created thereby under the Private Securities Litigation Reform Act of 1995. These statements include declarations regarding the intents, beliefs, estimates and current expectations of one or more of PHI, Pepco, DPL or ACE (each, a Reporting Company) or their subsidiaries. In some cases, you can identify forward-looking statements by terminology such as “may,” “might,” “will,” “should,” “could,” “expects,” “intends,” “assumes,” “seeks to,” “plans,” “anticipates,” “believes,” “projects,” “estimates,” “predicts,” “potential,” “future,” “goal,” “objective,” or “continue” or the negative of such terms or other variations thereof or comparable terminology, or by discussions of strategy that involve risks and uncertainties. Forward-looking statements involve estimates, assumptions, known and unknown risks, uncertainties and other factors that may cause one or more Reporting Companies’ or their subsidiaries’ actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward-looking statements. Therefore, forward-looking statements are not guarantees or assurances of future performance, and actual results could differ materially from those indicated by the forward-looking statements.

The forward-looking statements contained herein are qualified in their entirety by reference to the following important factors, which are difficult to predict, contain uncertainties, are beyond each Reporting Company’s or its subsidiaries’ control and may cause actual results to differ materially from those contained in forward-looking statements:

| • | Changes in governmental policies and regulatory actions affecting the energy industry or one or more of the Reporting Companies specifically, including allowed rates of return, industry and rate structure, acquisition and disposal of assets and facilities, operation and construction of transmission and distribution facilities and the recovery of purchased power expenses; |

| • | The outcome of pending and future rate cases and other regulatory proceedings, including the possible disallowance of recovery of costs and expenses; |

| • | The outcome of PHI’s litigation with the Internal Revenue Service (IRS) regarding its cross-border energy leases or the amount of Federal and state income taxes, including interest and the likelihood of penalties, that may be due as a result of the disallowance of prior deductions or a recharacterization of the leases as loans, and PHI’s method of funding such tax payments as well as the ability of PHI to timely liquidate the lease portfolio, if it determines to do so, and the impact of such liquidation on future earnings; |

| • | The expenditures necessary to comply with regulatory requirements, including regulatory orders, and to implement reliability enhancement, emergency response and customer service improvement programs; |

| • | Possible fines, penalties or other sanctions assessed by regulatory authorities against a Reporting Company or its subsidiaries; |

| • | The impact of adverse publicity and media exposure which could render one or more Reporting Companies or their subsidiaries vulnerable to increased regulatory oversight and negative customer perception; |

| • | Weather conditions affecting usage and emergency restoration costs; |

| • | Population growth rates and changes in demographic patterns; |

1

Table of Contents

| • | Changes in customer energy demand due to conservation measures and the use of more energy-efficient products; |

| • | General economic conditions, including the impact of an economic downturn or recession on energy usage; |

| • | Changes in and compliance with environmental and safety laws and policies; |

| • | Changes in tax rates or policies; |

| • | Changes in rates of inflation; |

| • | Changes in accounting standards or practices; |

| • | Unanticipated changes in operating expenses and capital expenditures; |

| • | Rules and regulations imposed by, and decisions of, federal and/or state regulatory commissions, PJM Interconnection, LLC (PJM), the North American Electric Reliability Corporation (NERC) and other applicable electric reliability organizations; |

| • | Legal and administrative proceedings (whether civil or criminal) and settlements that affect a Reporting Company’s or its subsidiaries’ business and profitability; |

| • | Pace of entry into new markets; |

| • | Interest rate fluctuations and the impact of credit and capital market conditions on the ability to obtain funding on favorable terms; and |

| • | Effects of geopolitical and other events, including the threat of domestic terrorism or cyber attacks. |

These forward-looking statements are also qualified by, and should be read together with, the risk factors included in Part I, Item 1A. “Risk Factors” and other statements in this Annual Report on Form 10-K, and investors should refer to such risk factors and other statements in evaluating the forward-looking statements contained in this Annual Report on Form 10-K.

Any forward-looking statements speak only as to the date this Annual Report on Form 10-K for each Reporting Company was filed with the SEC and none of the Reporting Companies undertakes an obligation to update any forward-looking statements to reflect events or circumstances after the date on which such statements are made or to reflect the occurrence of unanticipated events. New factors emerge from time to time, and it is not possible for a Reporting Company to predict all such factors. Furthermore, it may not be possible to assess the impact of any such factor on such Reporting Company’s or its subsidiaries’ business (viewed independently or together with the business or businesses of some or all of the other Reporting Companies or their subsidiaries), or the extent to which any factor, or combination of factors, may cause results to differ materially from those contained in any forward-looking statement. The foregoing factors should not be construed as exhaustive.

2

Table of Contents

| Item 1. | BUSINESS |

Overview

Pepco Holdings, a Delaware corporation incorporated in 2001, is a holding company that, through the following regulated public utility subsidiaries, is engaged primarily in the transmission, distribution and default supply of electricity and, to a lesser extent, the distribution and supply of natural gas (Power Delivery):

| • | Potomac Electric Power Company, which was incorporated in Washington, D.C. in 1896 and became a domestic Virginia corporation in 1949, |

| • | Delmarva Power & Light Company, which was incorporated in Delaware in 1909 and became a domestic Virginia corporation in 1979, and |

| • | Atlantic City Electric Company, which was incorporated in New Jersey in 1924. |

Through Pepco Energy Services, Inc. and its subsidiaries (collectively, Pepco Energy Services), PHI provides energy savings performance contracting services primarily to government customers, high voltage underground transmission cabling for industrial customers, construction and operations of combined heat and power and central energy plants for government and commercial customers, and is in the process of winding down its competitive electricity and natural gas retail supply business.

In addition, through Potomac Capital Investment Corporation (PCI), PHI holds six cross-border energy lease investments as described below under the heading “Other Business Operations.”

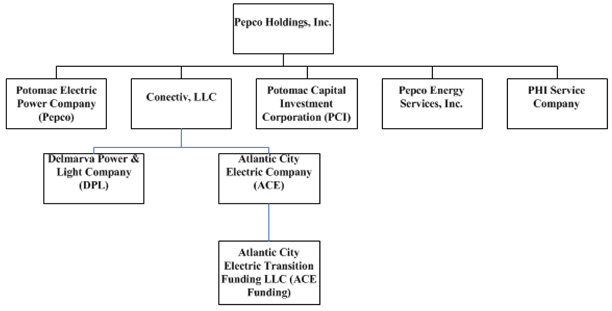

The following chart shows, in simplified form, the corporate structure of PHI and its principal subsidiaries:

3

Table of Contents

PHI Service Company, a subsidiary service company of PHI, provides a variety of support services, including legal, accounting, treasury, tax, purchasing and information technology services, to PHI and its operating subsidiaries. These services are provided pursuant to a service agreement among PHI, PHI Service Company and the participating operating subsidiaries. The expenses of PHI Service Company are charged to PHI and the participating operating subsidiaries in accordance with cost allocation methods set forth in the service agreement.

Pepco Holdings’ management has identified its operating segments at December 31, 2012 as (i) Power Delivery, consisting of the operations of Pepco, DPL and ACE, engaged primarily in the transmission, distribution and default supply of electricity and the distribution and supply of natural gas, (ii) Pepco Energy Services and (iii) Other Non-Regulated, consisting primarily of the operations of PCI. For financial information relating to PHI’s segments, see Note (5), “Segment Information,” to the consolidated financial statements of PHI.

Business Strategy

PHI’s business strategy is to be a top-performing, regulated power delivery company focused on:

| • | investing in transmission and distribution infrastructure to provide safe and reliable electric and natural gas service; |

| • | building a smarter grid to automate certain functions on the electric system, restore power more efficiently and provide customers detailed energy information to help them control their energy costs; |

| • | enhancing the customer experience and PHI’s communications with its customers through the development and use of the smart grid and other technology; and |

| • | providing comprehensive energy management solutions and developing, installing and operating renewable energy solutions. |

The elements of PHI’s business strategy support PHI’s core values of safety, diversity and environmental stewardship. PHI’s success in achieving this business strategy is dependent on its ability to earn reasonable rates of return on, and timely cost recovery of, its investments through its regulatory proceedings.

To further its business strategy, Pepco Holdings may consider transactions involving its existing businesses, including joint ventures, and dispositions and acquisitions of businesses. Pepco Holdings also may refine components of its business strategy as it deems necessary or appropriate in response to business factors and conditions, including regulatory requirements.

Description of Business

Power Delivery

PHI’s primary business is Power Delivery. Power Delivery in 2012, 2011 and 2010, produced 86%, 78% and 73%, respectively, of PHI’s consolidated operating revenues and 79%, 78% and 81%, respectively, of PHI’s consolidated operating income.

Each utility comprising Power Delivery is regulated in the jurisdictions that encompass its electricity distribution service territory and is regulated by the Federal Energy Regulatory Commission (FERC) for its electricity transmission facilities. DPL also is a regulated natural gas utility serving portions of Delaware. In the aggregate, Power Delivery distributes electricity to more than 1.8 million customers in the mid-Atlantic region and delivers natural gas to approximately 125,000 customers in Delaware. PHI no longer owns any electric generation facilities except for 17,400 kilowatts of generating capacity owned and operated by Pepco Energy Services.

4

Table of Contents

The Pepco, DPL and ACE service territories are located within a corridor extending from the District of Columbia to southern New Jersey. These service territories are economically diverse and include key industries that contribute to the regional economic base:

| • | Commercial activities in the region include banking and other professional services, government, insurance, real estate, shopping malls, casinos, stand alone construction and tourism. |

| • | Industrial activities in the region include chemical, glass, pharmaceutical, steel manufacturing, food processing and oil refining. |

Distribution and Default Supply of Electricity

Pepco, DPL and ACE each owns and operates a network of wires, substations and other equipment that are classified as transmission facilities, distribution facilities or common facilities (which are used for both transmission and distribution). Transmission facilities carry wholesale electricity into, out of and across, the utilties’ service territories. Distribution facilities carry electricity from the transmission facilities to the end-use customers located in the utilities’ service territories.

Each utility is responsible for the distribution of electricity in its service territory, for which it is paid tariff rates established by the applicable local public service commissions. Each utility also supplies electricity at regulated rates to retail customers in its service territory who do not elect to purchase electricity from a competitive retail supplier. The regulatory term for this default supply service is Standard Offer Service (SOS) in Delaware, the District of Columbia and Maryland, and Basic Generation Service (BGS) in New Jersey. In this Annual Report on Form 10-K, these supply services are referred to generally as Default Electricity Supply.

Transmission of Electricity and Relationship with PJM

The transmission facilities owned by Pepco, DPL and ACE are interconnected with the transmission facilities of contiguous utilities and are part of an interstate power transmission grid over which electricity is transmitted throughout the mid-Atlantic portion of the United States and parts of the Midwest. Pepco, DPL and ACE each is a member of the PJM Regional Transmission Organization (PJM RTO), the regional transmission organization designated by FERC to coordinate the movement of wholesale electricity within a region consisting of all or parts of Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia and the District of Columbia.

PJM, the FERC-approved independent grid operator, manages the transmission grid and the wholesale electricity market in the PJM RTO region. Any entity that wishes to have wholesale electricity delivered at any point within the PJM RTO region must obtain transmission services from PJM. In accordance with FERC-approved rules, Pepco, DPL, ACE and the other transmission-owning utilities in the region make their transmission facilities available to the PJM RTO, and PJM directs and controls the operation of these transmission facilities. For transmission services, transmission owners are paid rates proposed by the transmission owner and approved by FERC. PJM provides billing and settlement services, collects transmission service revenue from transmission service customers and distributes the revenue to the transmission owners. PJM also directs the regional transmission planning process within the PJM RTO region. The PJM Board of Managers reviews and approves each PJM regional transmission expansion plan, including whether to include new construction of transmission facilities proposed by PJM RTO members in the plan and, if so, the target in-service date for those facilities.

5

Table of Contents

Reliability Enhancement

Since 2010, PHI has implemented comprehensive reliability enhancement plans which include various initiatives to improve electrical system reliability, including:

| • | the identification and upgrading of under-performing feeder lines; |

| • | the addition of new facilities to support load; |

| • | the installation of distribution automation systems on both the overhead and underground network system; |

| • | the rejuvenation and replacement of underground residential cables; |

| • | selective undergrounding of portions of existing above-ground primary feeder lines, where appropriate to improve reliability; |

| • | improvements to substation supply lines; and |

| • | enhanced vegetation management. |

PHI’s capital expenditures for continuing reliability enhancement efforts are included in the table of projected capital expenditures within “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Capital Resources and Liquidity – Capital Requirements.”

Smart Grid

A key initiative for PHI in 2012 was the continued transformation of the electric grid owned and operated by Pepco Holdings’ utility subsidiaries into a “smart grid,” a sophisticated network of automated digital devices capable of communicating vast amounts of real-time information. The smart grid is designed to meet the challenges of rising energy costs, respond to concerns about the environment, improve reliability, provide timely and accurate customer information and address government energy reduction goals. During 2012, Power Delivery continued its development of the smart grid by replacing existing meters with smart meters, continuing construction of a wireless network and related information technology infrastructure to collect, manage and provide customers with the data made available by the smart meters and installing equipment to automate certain functions on the electric grid.

A central component of the smart grid is advanced metering infrastructure (AMI) which is a system that collects, measures and analyzes energy usage data from advanced digital electric and gas meters known as smart meters. In total, Power Delivery is deploying 1.3 million smart meters across the Pepco and DPL service territories. Also critical to the operation of the smart grid is distribution automation technology, which is comprised of automated devices that have internal intelligence and can be controlled remotely to better manage power flow and restore service quickly and more safely. Both AMI and distribution automation are enabled by advanced technology that is able to communicate with devices on the electric and gas delivery system and carry energy usage data to the host utility. The smart grid system will provide customers access to detailed energy information to help them better manage energy usage and costs, improve the customer experience during power restoration and enhance the ability of PHI’s utilities to manage and operate their electrical and natural gas distribution systems. The implementation of the AMI system and distribution automation involves an integration of technologies provided by multiple vendors.

The installation of smart meters is subject to the approval of applicable state regulators. Electric meter installation and activation are substantially complete for DPL electric customers in Delaware; installation of smart meters for natural gas delivery customers in Delaware is ongoing. Meter installation is substantially complete for Pepco customers in the District of Columbia, with activation expected to be completed in the first quarter of 2013. For Pepco customers in Maryland, installation and activation are expected to be completed in the third quarter of 2013. In 2012, the Maryland Public Service Commission (MPSC) approved the deployment of AMI for electric customers in DPL’s Maryland service territory, and installation is scheduled to begin in the first quarter of 2013.

The respective public service commissions have approved the creation of regulatory assets to defer AMI costs between rate cases, as well as the accrual of returns on the deferred costs. Thus, these costs will be recovered in the future through base rates. Approval of AMI has been deferred by the New Jersey Board of Public Utilities (NJBPU) for ACE in New Jersey.

6

Table of Contents

PHI’s implementation of dynamic pricing rate structures helps ensure that customers experience additional benefits from the smart grid. Dynamic pricing provides bill credits to reward eligible customers for lowering their energy use during those times when energy demand and, consequently, the cost of supplying electricity, are higher. In 2011, the Delaware Public Service Commission (DPSC) approved DPL’s request to implement dynamic pricing for Delaware customers. In Delaware, approximately 6,700 SOS customers participated in the phase-in stage of the program in 2012; the remaining residential SOS customers will be eligible to participate in 2013.

Dynamic pricing has been approved for all Pepco customers in Maryland, and the phase-in for approximately 5,000 residential customers has been completed; the remaining Maryland residential customers will be eligible to participate in 2013. Pepco intends to re-file the dynamic pricing proposal in its District of Columbia jurisdiction in 2013. Dynamic pricing has been approved in concept pending AMI deployment for DPL’s Maryland SOS customers, and has been deferred by the NJBPU for ACE’s customers in New Jersey.

In April 2010, PHI signed agreements to formalize $168 million in awards from the U.S. Department of Energy to support the rollout of smart grid initiatives. In the Pepco service area, $149 million was awarded for AMI, direct load control, distribution automation and communications infrastructure, while in the Atlantic City Electric service area, $19 million was awarded for direct load control, distribution automation and communications infrastructure. The grants effectively reduce the project costs of these initiatives. The cumulative award payments received by Pepco and ACE as of December 31, 2012, were $115 million and $13 million, respectively.

For projected 2013 through 2017 capital expenditures associated with the smart grid, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Capital Resources and Liquidity – Capital Requirements.”

Regulated Utility Subsidiaries

The following is a more detailed description of the business of each of PHI’s three regulated utility subsidiaries:

Pepco

Pepco is engaged in the transmission, distribution and default supply of electricity in the District of Columbia and major portions of Prince George’s County and Montgomery County in Maryland. Pepco’s service territory covers approximately 640 square miles and has a population of approximately 2.2 million. As of December 31, 2012, Pepco distributed electricity to 793,000 customers (of which 260,000 were located in the District of Columbia and 533,000 were located in Maryland), as compared to 788,000 customers as of December 31, 2011 (of which 257,000 were located in the District of Columbia and 531,000 were located in Maryland). As of December 31, 2010, Pepco distributed electricity to 787,000 customers (of which 256,000 were located in the District of Columbia and 531,000 were located in Maryland).

In 2012, Pepco distributed a total of 26,006,000 megawatt hours of electricity, of which 57% was distributed within its Maryland territory and 43% within the District of Columbia. Of this amount, 30% of the total megawatt hours were delivered to residential customers, 50% to commercial customers, and 20% to United States and District of Columbia government customers. In 2011, Pepco distributed a total of 26,895,000 megawatt hours of electricity, of which 57% was distributed within its Maryland territory and 43% within the District of Columbia. Of this amount, 30% of the total megawatt hours were distributed to residential customers, 50% to commercial customers, and 20% to United States and District of Columbia government customers. In 2010, Pepco distributed a total of 27,665,000 megawatt hours of electricity, of which 57% was distributed within its Maryland territory and 43% within the District of Columbia. Of this amount, 30% of the total megawatt hours were distributed to residential customers, 49% to commercial customers, and 21% to United States and District of Columbia government customers.

7

Table of Contents

Pepco has been providing SOS in Maryland since July 2004. Pursuant to orders issued by the MPSC, Pepco is obligated to provide SOS (i) to residential and small commercial customers until further action of the Maryland General Assembly and (ii) to medium-sized commercial customers through November 2013. Pepco purchases the electricity required to satisfy these SOS obligations from wholesale suppliers under contracts entered into in accordance with competitive bid procedures approved and supervised by the MPSC. Pepco also is obligated to provide Standard Offer Service, known as Hourly Priced Service (HPS), for large Maryland customers. Power to supply HPS customers is acquired in next-day and other short-term PJM RTO markets. Pepco is entitled to recover from its SOS customers the cost of acquiring the SOS supply, plus an administrative charge that is intended to allow Pepco to recover the administrative costs incurred to provide the SOS and a modest margin. Because the margin varies by customer class, the actual average margin over any given time period depends on the number of Maryland SOS customers in each customer class and the electricity used by such customers. Pepco is paid tariff rates for the distribution of electricity over its transmission and distribution facilities to all electricity customers in its Maryland service territory regardless of whether the customer receives SOS or purchases electricity from another supplier.

Pepco has been providing SOS in the District of Columbia since February 2005. Pursuant to orders issued by the District of Columbia Public Service Commission (DCPSC), Pepco is obligated to provide SOS to residential and small, medium-sized and large commercial customers indefinitely. Pepco purchases the electricity required to satisfy its SOS obligations from wholesale suppliers under contracts entered into in accordance with a competitive bid procedure approved and supervised by the DCPSC. Pepco is entitled to recover from its SOS customers the costs of acquiring the SOS supply, plus an administrative charge that is intended to allow Pepco to recover the administrative costs incurred to provide the SOS and a modest margin. Because the margin varies by customer class, the actual average margin over any given time period depends on the number of District of Columbia SOS customers in each customer class and the amount of electricity used by such customers. Pepco is paid tariff rates for the distribution of electricity over its transmission and distribution facilities to all electricity customers in its District of Columbia service territory regardless of whether the customer receives SOS or purchases electricity from another supplier.

For the year ended December 31, 2012, 40% of Pepco’s Maryland distribution sales (measured by megawatt hours) were to SOS customers, as compared to 43% and 46% in 2011 and 2010, respectively, and 25% of its District of Columbia distribution sales (measured by megawatt hours) were to SOS customers in 2012, as compared to 27% and 29% in 2011 and 2010, respectively.

DPL

DPL is engaged in the transmission, distribution and default supply of electricity in Delaware and portions of Maryland. In northern Delaware, DPL also supplies and delivers natural gas to retail customers and provides transportation-only services to retail customers that purchase natural gas from another supplier.

Distribution and Supply of Electricity

DPL’s electricity distribution service territory consists of the state of Delaware, and Caroline, Cecil, Dorchester, Harford, Kent, Queen Anne’s, Somerset, Talbot, Wicomico and Worcester counties in Maryland. This territory covers approximately 5,000 square miles and has a population of approximately 1.4 million. As of December 31, 2012, DPL delivered electricity to 503,000 customers (of which 303,000 were located in Delaware and 200,000 were located in Maryland), as compared to 501,000 customers as of December 31, 2011 (of which 301,000 were located in Delaware and 200,000 were located in Maryland). As of December 31, 2010, DPL delivered electricity to 500,000 customers (of which 301,000 were located in Delaware and 199,000 were located in Maryland).

8

Table of Contents

In 2012, DPL distributed a total of 12,641,000 megawatt hours of electricity to its customers, of which 67% was distributed within its Delaware territory and 33% within its Maryland territory. Of this amount, 40% of the total megawatt hours were distributed to residential customers, 41% to commercial customers and 19% to industrial customers. In 2011, DPL distributed a total of 12,688,000 megawatt hours of electricity, of which 66% was distributed within its Delaware territory and 34% within its Maryland territory. Of this amount, 41% of the total megawatt hours were distributed to residential customers, 42% to commercial customers and 17% to industrial customers. In 2010, DPL distributed a total of 12,853,000 megawatt hours of electricity, of which 66% was distributed within its Delaware territory and 34% within its Maryland territory. Of this amount, 42% of the total megawatt hours were distributed to residential customers, 41% to commercial customers and 17% to industrial customers.

DPL has been providing SOS in Delaware since May 2006. Pursuant to orders issued by the DPSC, DPL is obligated to provide SOS to residential, small commercial and industrial customers through May 2015, and to medium, large and general service commercial customers through May 2013. DPL purchases the electricity required to satisfy these SOS obligations from wholesale suppliers under contracts entered into in accordance with competitive bid procedures approved and supervised by the DPSC. DPL also has an obligation to provide SOS, known as HPS, for the largest Delaware customers. Power to supply the HPS customers is acquired in next-day and other short-term PJM RTO markets. DPL’s rates for supplying SOS and HPS reflect the associated capacity, energy (including satisfaction of renewable energy requirements), transmission and ancillary services costs and an amount referred to as a Reasonable Allowance for Retail Margin. Components of the Reasonable Allowance for Retail Margin include a fixed annual margin of approximately $2.75 million, plus estimated incremental expenses and a cash working capital allowance. DPL is paid tariff rates for the distribution of electricity over its transmission and distribution facilities to all electricity customers in its Delaware service territory regardless of whether the customer receives SOS or purchases electricity from another supplier.

DPL has been providing SOS in Maryland since June 2004. Pursuant to orders issued by the MPSC, DPL is obligated to provide SOS to residential and small commercial customers until further action of the Maryland General Assembly, and to medium-sized commercial customers through November 2013. DPL purchases the electricity required to satisfy these SOS obligations from wholesale suppliers under contracts entered into in accordance with a competitive bid procedure approved and supervised by the MPSC. DPL also is obligated to provide HPS for large Maryland customers. Power to supply the HPS customers is acquired in next-day and other short-term PJM RTO markets. DPL is entitled to recover from its SOS customers the costs of acquiring the SOS supply, plus an administrative charge that is intended to allow DPL to recover the administrative costs incurred to provide the SOS and a modest margin. Because the margin varies by customer class, the actual average margin over any given time period depends on the number of Maryland SOS customers in each customer class and the electricity used by such customers. DPL is paid tariff rates for the distribution of electricity over its transmission and distribution facilities to all electricity customers in its Maryland service territory regardless of whether the customer receives SOS or purchases electricity from another supplier.

For the year ended December 31, 2012, 47% of DPL’s Delaware distribution sales (measured by megawatt hours) were to SOS customers, as compared to 51% and 53% in 2011 and 2010, respectively, and 53% of its Maryland distribution sales (measured by megawatt hours) were to SOS customers in 2012, as compared to 58% in 2011 and 63% in 2010.

9

Table of Contents

Supply and Distribution of Natural Gas

DPL provides regulated natural gas supply and distribution service to customers in a service territory consisting of a major portion of New Castle County in Delaware. This service territory covers approximately 275 square miles and has a population of approximately 500,000. Large volume commercial, institutional, and industrial natural gas customers may purchase natural gas either from DPL or from other suppliers. DPL uses its natural gas distribution facilities to deliver natural gas to customers that choose to purchase natural gas from another supplier. Intrastate transportation customers pay DPL distribution service rates approved by the DPSC. DPL purchases natural gas supplies for resale to its retail service customers from marketers and producers through a combination of long-term agreements and next-day distribution arrangements. For the year ended December 31, 2012, DPL supplied 60% of the natural gas that it delivered, compared to 64% in 2011 and 65% in 2010.

As of December 31, 2012, DPL delivered natural gas to 125,000 customers as compared to 124,000 customers in 2011 and 123,000 customers in 2010. In 2012, DPL delivered 16,815,000 Mcf (thousand cubic feet) of natural gas to customers in its Delaware service territory, of which 38% were sales to residential customers, 22% to commercial customers, less than 1% to industrial customers and 40% to customers receiving a transportation-only service. In 2011, DPL delivered 18,754,000 Mcf of natural gas, of which 40% were sales to residential customers, 23% were sales to commercial customers, 1% were sales to industrial customers and 36% were sales to customers receiving a transportation-only service. In 2010, DPL delivered 19,336,000 Mcf of natural gas, of which 41% were sales to residential customers, 23% were sales to commercial customers, 1% were sales to industrial customers and 35% were sales to customers receiving a transportation-only service.

ACE

ACE is primarily engaged in the transmission, distribution and default supply of electricity in a service territory consisting of Gloucester, Camden, Burlington, Ocean, Atlantic, Cape May, Cumberland and Salem counties in southern New Jersey. ACE’s service territory covers approximately 2,700 square miles and has a population of approximately 1.1 million. As of December 31, 2012, ACE distributed electricity to 545,000 customers in its service territory, as compared to 547,000 and 548,000 customers as of December 31, 2011 and 2010, respectively.

In 2012, ACE distributed a total of 9,495,000 megawatt hours of electricity to its customers, of which 46% of the total was distributed to residential customers, 45% to commercial customers and 9% to industrial customers. In 2011, ACE distributed a total of 9,683,000 megawatt hours of electricity to its customers, of which 46% of the total was distributed to residential customers, 45% to commercial customers, and 9% to industrial customers. In 2010, ACE distributed a total of 10,185,000 megawatt hours of electricity to its customers, of which 46% was distributed to residential customers, 44% to commercial customers, and 10% to industrial customers.

Electric customers in New Jersey who do not choose another supplier receive BGS from their electric distribution company. New Jersey’s electric distribution companies, including ACE, jointly obtain the electricity to meet their BGS obligations from competitive suppliers selected through auctions authorized by the NJBPU for the supply of New Jersey’s total BGS requirements. Each winning bidder is required to supply its committed portion of the BGS customer load with full requirements service, consisting of power supply and transmission service.

ACE provides two types of BGS:

| • | BGS-Fixed Price (BGS-FP), which is supplied to smaller commercial and residential customers at seasonally-adjusted fixed prices. BGS-FP rates change annually on June 1 and are based on the average BGS price obtained at auction in the current year and the two prior years. As of December 31, 2012, ACE’s BGS-FP peak load was approximately 1,320 megawatts, which represents approximately 96% of ACE’s total BGS load. |

10

Table of Contents

| • | BGS-Commercial and Industrial Energy Price (BGS-CIEP), which is supplied to large customers at hourly PJM RTO real-time market prices for a term of 12 months. As of December 31, 2012, ACE’s peak BGS-CIEP load was approximately 54 megawatts, which represents approximately 4% of ACE’s BGS load. |

ACE is paid tariff supply rates established by the NJBPU that compensate it for the cost of obtaining the BGS supply. These rates are set such that ACE does not make any profit or incur any loss on the supply component of the BGS it supplies to customers. ACE is paid tariff rates for the distribution of electricity over its transmission and distribution facilities to all electricity customers in its service territory regardless of whether the customer receives BGS or purchases electricity from another supplier.

For the year ended December 31, 2012, 51% of ACE’s total distribution sales (measured by megawatt hours) were to BGS customers, as compared to 56% and 65% in 2011 and 2010, respectively.

ACE has contracts with three unaffiliated non-utility generators (NUGs) under which ACE is obligated to purchase capacity and the entire generation output of the facilities. One of the contracts expires in 2016 and the other two expire in 2024. In 2012, ACE purchased 1.7 million megawatt hours of power from the NUGs. ACE sells this electricity into the wholesale market administered by PJM.

In 2001, ACE established Atlantic City Electric Transitional Funding LLC (ACE Funding) solely for the purpose of securitizing authorized portions of ACE’s recoverable stranded costs through the issuance and sale of bonds (Transition Bonds). The proceeds of the sale of each series of Transition Bonds were transferred to ACE in exchange for the transfer by ACE to ACE Funding of the right to collect a non-bypassable transition bond charge (Transition Bond charge) from ACE customers pursuant to bondable stranded costs rate orders issued by the NJBPU in an amount sufficient to fund the principal and interest payments on the Transition Bonds and related taxes, expenses and fees (Bondable Transition Property). The assets of ACE Funding, including the Bondable Transition Property, and the Transition Bond Charges (representing revenue ACE receives, and pays to ACE Funding, to fund the principal and interest payments on Transition Bonds and related taxes, expenses and fees) collected from ACE’s customers, are not available to creditors of ACE. The holders of Transition Bonds have recourse only to the assets of ACE Funding.

Seasonality

The operating results of Power Delivery historically have been directly related to the volume of electricity delivered to its customers, producing higher revenues and net income during periods when customers consumed higher amounts of electricity (usually during periods of extreme temperatures) and lower revenues and net income during periods when customers consumed lower amounts of electricity (usually during periods of mild temperatures). This has been due in part to the long standing practice by which the applicable public service commissions set distribution rates based on a fixed charge per kilowatt-hour of electricity used by the customer. Because most of the costs associated with the distribution of electricity do not vary with the volume of electricity delivered, this pricing mechanism also contributed to seasonal variations in net income. As a result of the implementation of a bill stabilization adjustment (BSA) for retail customers of Pepco and DPL in Maryland and for customers of Pepco in the District of Columbia, distribution revenues have been decoupled from the amount of electricity delivered. Under the BSA, utility customers pay an approved distribution charge for their electric service which does not vary by electricity usage. This change has had the effect of aligning annual distribution revenues more closely with annual distribution costs. In addition, the change has had the effect of eliminating changes in customer electricity usage, whether due to weather conditions or for any other reason, as a factor having an impact on annual distribution revenue and net income in those jurisdictions. The BSA also eliminates what otherwise might be a disincentive for the utility to aggressively develop and promote efficiency programs. A comparable revenue decoupling mechanism for DPL electricity and natural gas customers in Delaware is under consideration by the DPSC. Distribution revenues are not decoupled for the distribution of electricity by ACE in New Jersey, and thus are subject to variability due to changes in customer consumption.

11

Table of Contents

In contrast to electricity distribution costs, the cost of the electricity supplied, which is the largest component of a customer’s bill, does vary directly in relation to the volume of electricity used by a customer. Accordingly, whether or not a BSA is in effect for the jurisdiction, the revenues of Pepco, DPL and ACE from the supply of electricity and natural gas vary based on consumption and on this basis are seasonal. Because the revenues received by each of the utility subsidiaries for the default supply of electricity and natural gas closely approximate the supply costs, the impact on net income is immaterial, and therefore is not seasonal.

MAPP Project

On August 24, 2012, the board of PJM terminated the Mid-Atlantic Power Pathway (MAPP) project and removed it from PJM’s regional transmission expansion plan. PHI had been directed to construct a 152-mile high-voltage interstate transmission line, to address the reliability needs of the region’s transmission system.

In a 2008 FERC order approving incentives for the MAPP project, FERC authorized the recovery of prudently incurred abandoned costs in connection with the MAPP project. Consistent with this order, on December 21, 2012, PHI submitted a filing to FERC seeking recovery over a period of five years of approximately $88 million of abandoned MAPP capital expenditures. The FERC filing addressed, among other things, the prudence of the recoverable costs incurred, the proposed period over which the abandoned costs are to be amortized and the rate of return on these costs during the recovery period (see Note (7), “Regulatory Matters – MAPP Project” to the consolidated financial statements of PHI for additional information).

Pepco Energy Services

Pepco Energy Services is engaged in the following businesses:

| • | providing energy savings performance contracting services principally to federal, state and local government customers, and designing, constructing and operating combined heat and power and central energy plants, |

| • | providing high voltage electric construction and maintenance services to customers throughout the United States, as well as low voltage electric construction and maintenance services and streetlight construction services to utilities, municipalities and other customers in the Washington, D.C. area, and |

| • | providing retail customers electricity and natural gas under its remaining contractual obligations. |

Since 2010, Pepco Energy Services has been focused on growing its energy savings performance contracting services business in the federal, state and local government markets. Activity in the state and local government markets, which are Pepco Energy Services’ largest markets, has slowed significantly in 2012, due to, among other factors, lower energy prices that have lessened the economic benefits of energy savings projects and the reluctance of state and local governments to incur new debt associated with these projects. As a result of this slowdown, Pepco Energy Services believes that new business in these markets will remain challenged for the foreseeable future. Consequently, during 2012, Pepco Energy Services reduced resources and personnel and limited geographic expansion in the energy savings services business, and has refocused its existing resources on developing business in the federal government market while continuing to pursue combined heat and power projects.

Most of Pepco Energy Services’ contracts with federal, state and local governments, as well as independent agencies such as housing and water authorities, contain provisions authorizing the governmental authority or independent agency to terminate the contract at any time. Those provisions include explicit mechanisms that, if exercised, would require the other party to pay Pepco Energy

12

Table of Contents

Services for work performed through the date of termination and for additional costs incurred as a result of the termination. In addition, Pepco Energy Services provides energy services guarantees in connection with its energy services performance contracts.

PHI guarantees the obligations of Pepco Energy Services under certain of its energy savings, combined heat and power and construction contracts. At December 31, 2012, PHI’s guarantees of Pepco Energy Services’ obligations under these contracts totaled $198 million.

Pepco Energy Services also has historically been engaged in the business of providing retail energy supply services, consisting of the sale of electricity, including electricity from renewable resources, primarily to commercial, industrial and government customers located in the mid-Atlantic and northeastern regions of the United States, as well as Texas and Illinois, and the sale of natural gas to customers located primarily in the mid-Atlantic region. In December 2009, PHI announced that it will wind down the retail energy supply component of the Pepco Energy Services business.

Pepco Energy Services’ retail natural gas sales volumes and revenues are seasonally dependent. Colder weather from November through March of each year generally translates into increased sales volumes, which, when coupled with higher natural gas prices during these months, allows Pepco Energy Services to recognize generally higher revenues as compared to other months of the year. Retail electricity sales volumes are also seasonally dependent, with sales in the summer and winter months being generally higher than other months of the year, which, when coupled with higher electricity prices during these periods, allows Pepco Energy Services to recognize generally higher revenues as compared to other periods during the year. The impact of this seasonality on Pepco Energy Services’ results is diminishing with the wind-down of the business. The energy services business is not seasonal.

To effectuate the wind-down of the retail energy supply business, Pepco Energy Services is continuing to fulfill all of its commercial and regulatory obligations and perform its customer service functions to ensure that it meets the needs of its existing customers, but is not entering into any new retail energy supply contracts.

Substantially all of Pepco Energy Services’ retail customer obligations will be fully performed by June 1, 2014. PHI is reviewing strategic alternatives that could accelerate into 2013 the completion of the wind-down of its remaining portfolio of retail energy contracts.

Pepco Energy Services’ remaining businesses will not be affected by the wind-down of the retail energy supply business.

During 2012, Pepco Energy Services deactivated its Buzzard Point and Benning Road oil-fired generation facilities. Pepco Energy Services has placed the facilities into an idle condition termed a “cold closure.” A cold closure requires that the utility service be disconnected so that the facilities are no longer operable and that the facilities require only essential maintenance until they are completely decommissioned.

Competition

Pepco Energy Services’ energy services business is highly competitive. Pepco Energy Services competes with other energy services companies primarily with respect to contracts with federal, state and local governments and independent agencies. Many of these energy services companies are subsidiaries of larger building controls and equipment providers or utility holding companies (as is the case with Pepco Energy Services). Among the factors as to which the energy services business competes are the amount and duration of the guarantees provided in energy savings performance contracts and the quality and value of service provided to customers. The energy services business is impacted by new entrants into the market, financial strength of customers, energy prices, and general economic conditions.

13

Table of Contents

Other Business Operations

Between 1994 and 2002, PCI, a subsidiary of PHI, entered into eight cross-border energy lease investments involving public utility assets (primarily consisting of hydroelectric generation and coal-fired electric generation facilities, and natural gas distribution networks) located outside of the United States. Each of these investments is structured as a sale and leaseback transaction commonly referred to as a sale-in, lease-out, or SILO, transaction. During the second quarter of 2011 and the third quarter of 2012, PHI entered into early termination agreements with several lessees involving all of the leases comprising two of the eight lease investments and a small portion of the leases comprising a third lease investment. As of December 31, 2012, PHI’s net investment in its six remaining cross-border energy lease investments was approximately $1.2 billion.

The net investment value of the cross-border energy lease investments and the pattern of recognizing the related cross-border energy lease income are based on the estimated timing and amount of all cash flows related to the investments, including the income tax-related cash flows. The Treasury Department and the Internal Revenue Service (IRS) have identified SILO transactions, such as PCI’s cross-border energy lease investments, as tax avoidance transactions and the IRS disallowed a substantial portion of the tax benefits claimed by PHI related to its cross-border energy lease investments beginning with PHI’s 2001 income tax return. IRS challenges related to SILO and lease-in, lease-out, or LILO, transactions also have been the subject of litigation, including litigation commenced by PHI in the U.S. Court of Federal Claims in January 2012 related to certain tax benefits claimed by PHI on its federal income tax returns for 2001 and 2002. PHI is required to assess on a periodic basis the likely outcome of tax positions relating to its cross-border energy lease investments and, if there is a change or a projected change in the timing of the estimated tax benefits generated by the transactions, PHI is required to recalculate the value of its net investment. In 2008, after evaluating court rulings that had been recently decided in favor of the IRS on certain SILO and LILO transactions, PHI significantly revised the projected timing of the tax benefits generated by the transactions and reduced the carrying value of its net investment by recording a non-cash charge of $86 million after tax.

On January 9, 2013, the U.S. Court of Appeals for the Federal Circuit issued an opinion in Consolidated Edison Company of New York, Inc. & Subsidiaries v. United States (to which PHI is not a party) that disallowed tax benefits associated with Consolidated Edison’s LILO transaction. PHI had viewed the initial trial court ruling on this matter, in which the U.S. Court of Federal Claims issued a decision in favor of the taxpayer in October 2009, as a favorable development in PHI’s dispute with the IRS. After analyzing the U.S. Court of Appeals ruling in this case, PHI has determined that its tax position with respect to the tax benefits associated with the cross-border energy lease investments no longer meets the more likely than not standard of recognition for accounting purposes. Accordingly, PHI expects to record a non-cash charge of between $355 million and $380 million (after-tax) in the first quarter of 2013, consisting of a charge to reduce the carrying value of the cross-border energy lease investments and a charge to reflect the anticipated additional interest expense related to changes in its estimated federal and state income tax obligations for the period over which the tax benefits may be disallowed. While the IRS could require PHI to pay a penalty of up to 20 percent of the amount of additional taxes due, PHI believes that it is more likely than not that no such penalty will be incurred, and therefore no amount for any potential penalty will be included in the charge expected to be recorded in the first quarter of 2013. PHI also is evaluating the liquidation of all or a portion of its remaining cross-border energy lease investments. The aggregate financial impact of a partial or complete liquidation of the cross-border leases is not determinable at this time, but could result in material gains or losses. PHI continues to weigh its options with respect to its litigation with the IRS.

For additional information concerning these cross-border energy lease investments, see Note (8), “Leasing Activities,” Note (16), “Commitments and Contingencies – PHI’s Cross-Border Energy Lease Investments,” and Note (20), “Subsequent Event,” to the consolidated financial statements of PHI.

14

Table of Contents

Discontinued Operations

In April 2010, the Board of Directors approved a plan for the disposition of PHI’s competitive wholesale power generation, marketing and supply business, which had been conducted through subsidiaries of Conectiv Energy Holding Company (collectively, Conectiv Energy). On July 1, 2010, PHI completed the sale of Conectiv Energy’s wholesale power generation business to Calpine Corporation (Calpine) for $1.64 billion. The disposition of Conectiv Energy’s remaining assets and businesses not included in the Calpine sale, including its load service supply contracts, energy hedging portfolio and certain tolling agreements, has been completed. The former operations of Conectiv Energy, which previously comprised a separate segment for financial reporting purposes, have been classified as a discontinued operation in PHI’s consolidated financial statements, and the business is no longer treated as a separate segment for financial reporting purposes. For further information on the former Conectiv Energy segment, see Note (19), “Discontinued Operations,” to the consolidated financial statements of PHI.

Regulation

The operations of PHI’s utility subsidiaries, including the rates and tariffs they are permitted to charge customers for the distribution and transmission of electricity and, in the case of DPL, the distribution and transportation of natural gas, are subject to regulation by governmental agencies in the jurisdictions in which the subsidiaries provide utility service as follows:

| • | Pepco’s electricity distribution operations are regulated in Maryland by the MPSC and in the District of Columbia by the DCPSC. |

| • | DPL’s electricity distribution operations are regulated in Maryland by the MPSC and in Delaware by the DPSC. |

| • | DPL’s natural gas distribution and intrastate transportation operations in Delaware are regulated by the DPSC. |

| • | ACE’s electricity distribution operations are regulated by the NJBPU. |

| • | Each utility subsidiary’s transmission facilities are regulated by FERC. |

| • | DPL’s interstate transportation and wholesale sale of natural gas are regulated by FERC. |

| • | Each utility subsidiary’s bulk power system is subject to reliability standards established by NERC. |

Rates and tariffs are established by these regulatory commissions. PHI’s utility subsidiaries have filed or plan to file rate cases in each of its jurisdictions as further described in Note (7), “Regulatory Matters – Rate Proceedings,” to the consolidated financial statements of PHI.

Regulatory Lag

An important factor in the ability of each of Pepco, DPL and ACE to earn its authorized rate of return is the willingness of applicable public service commissions to adequately recognize forward-looking costs in the utility’s rate structure in order to address the shortfall in revenues due to the delay in time or “lag” between when costs are incurred and when they are reflected in rates. This delay is commonly known as “regulatory lag.” Each of Pepco, DPL and ACE is currently experiencing significant regulatory lag because its investment in the rate base and its operating expenses are outpacing revenue growth.

Each of PHI’s utility subsidiaries will continue to seek cost recovery from applicable public service commissions to reduce the effects of regulatory lag. There can be no assurance that any attempts by PHI’s utility subsidiaries to mitigate regulatory lag will be approved, or that even if approved, the cost recovery mechanisms will fully mitigate the effects of regulatory lag. Until such time as any cost recovery mechanisms are approved, PHI’s utility subsidiaries plan to file rate cases at least annually in an effort to align more closely the revenue and cash flow levels of PHI’s utility subsidiaries with other operation and maintenance spending and capital investments. For additional discussion on this matter, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – General Overview – Power Delivery Initiatives and Activities – Regulatory Lag.”

15

Table of Contents

Reliability Task Forces

In July 2012, the Maryland governor signed an Executive Order directing his energy advisor, in collaboration with certain state agencies, to solicit input and recommendations from experts on how to improve the resiliency and reliability of the electric distribution system in Maryland (see Note (7), “Regulatory Matters – Reliability Task Forces” to the consolidated financial statements of PHI). The resulting Grid Resiliency Task Force issued its report in September 2012, in which it made 11 recommendations. The governor forwarded the report to the MPSC in October 2012, urging the MPSC to quickly implement the first four recommendations: (i) strengthen existing reliability and storm restoration regulations; (ii) accelerate the investment necessary to meet the enhanced metrics; (iii) allow surcharge recovery for the accelerated investment; and (iv) implement clearly defined performance metrics into the traditional ratemaking scheme. Pepco’s electric distribution base rate case filed with the MPSC on November 30, 2012, addresses the Grid Resiliency Task Force recommendations. See Note (7), “Regulatory Matters — Rate Proceedings — Pepco Electric Distribution Bases Rates,” to the consolidated financial statements of PHI. DPL will consider the Grid Resiliency Task Force recommendations in its next electric distribution base rate case expected to be filed with the MPSC in the first quarter of 2013.

In August 2012, the District of Columbia mayor issued an Executive Order establishing the Mayor’s Power Line Undergrounding Task Force. The purpose of the Power Line Undergrounding Task Force is to pool the collective resources available in the District of Columbia to produce an analysis of the technical feasibility, infrastructure options and reliability implications of undergrounding new or existing overhead distribution facilities in the District of Columbia. These resources include legislative bodies, regulators, utility personnel, experts and other parties who could contribute in a meaningful way to the Power Line Undergrounding Task Force. The options that are available for financing these efforts are also to be evaluated to identify required legislative or regulatory actions to implement these recommendations. The results of this analysis are intended to help determine the path forward for these types of infrastructure improvements and additions. A written report from the Power Line Undergrounding Task Force setting forth the findings and recommendations was originally due on January 31, 2013 but has been extended to early March 2013.

MPSC New Generation Contract Requirement

In September 2009, the MPSC initiated an investigation into whether the electricity distribution companies (EDCs) in Maryland should be required to enter into long-term contracts with entities that construct, acquire or lease, and operate, new electric generation facilities in Maryland.

In April 2012, the MPSC issued an order determining that there is a need for one new power plant in the range of 650 to 700 megawatts (MW) beginning in 2015. The order requires certain Maryland EDCs, including Pepco and DPL, to negotiate and enter into a contract with the winning bidder of a competitive bidding process in amounts proportional to their relative SOS loads. Under the contract, the winning bidder will construct a 661 MW natural gas-fired combined cycle generation plant in Waldorf, Maryland, with an expected commercial operation date of June 1, 2015. The order acknowledges certain of the EDCs’ concerns about the requirements of the contract and directs them to negotiate with the winning bidder and submit any proposed changes in the contract to the MPSC for approval. The order further specifies that the EDCs entering into the contract will recover the associated costs, in amounts proportional to their relative SOS loads, through surcharges on their respective SOS customers.

In April 2012, a group of generating companies operating in the PJM region filed a complaint in the U.S. District Court for the District of Maryland challenging the MPSC’s order on the grounds that it violates the Commerce Clause and the Supremacy Clause of the U.S. Constitution. In May 2012, Pepco, DPL, and other parties filed notices of appeal in circuit courts in Maryland requesting judicial review of the MPSC’s order. These appeals have been consolidated in the Circuit Court for Baltimore City and have

16

Table of Contents

been stayed pending the issuance of a final order from the MPSC approving the form of contract, including the payment obligations of the utilities in the event the utilities do not recover the costs for such payments from their customers.

Until the final form of the contract with the winning bidder and associated cost recovery are approved, PHI cannot predict (i) the extent of the negative effect that the order and, once finalized, the contract for new generation may have on PHI’s, Pepco’s and DPL’s balance sheets, as well as their respective credit metrics, as calculated by independent rating agencies that evaluate and rate PHI, Pepco and DPL and each of their debt issuances, (ii) the effect on Pepco’s and DPL’s ability to recover their associated costs of the contract for new generation if a significant number of SOS customers elect to buy their energy from alternative energy suppliers, and (iii) the effect of the order on the financial condition, results of operations and cash flows of each of PHI, Pepco and DPL.

ACE Standard Offer Capacity Agreements