UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number | 811-05245 | |||||

| BNY Mellon Strategic Municipals, Inc. | ||||||

| (Exact name of Registrant as specified in charter) | ||||||

|

c/o BNY Mellon Investment Adviser, Inc. 240 Greenwich Street New York, New York 10286 |

||||||

| (Address of principal executive offices) (Zip code) | ||||||

|

Deirdre Cunnane, Esq. 240 Greenwich Street New York, New York 10286 |

||||||

| (Name and address of agent for service) | ||||||

| Registrant's telephone number, including area code: | (212) 922-6400 | |||||

|

Date of fiscal year end:

|

09/30 | |||||

| Date of reporting period: |

09/30/2021

|

|||||

FORM N-CSR

Item 1. Reports to Stockholders.

BNY Mellon Strategic Municipals, Inc.

ANNUAL REPORT September 30, 2021 |

|

BNY Mellon Strategic Municipals, Inc. Protecting

Your Privacy THE FUND IS COMMITTED TO YOUR PRIVACY. On this page, you will find the fund’s policies and practices for collecting, disclosing, and safeguarding “nonpublic personal information,” which may include financial or other customer information. These policies apply to individuals who purchase fund shares for personal, family, or household purposes, or have done so in the past. This notification replaces all previous statements of the fund’s consumer privacy policy, and may be amended at any time. We’ll keep you informed of changes as required by law. YOUR ACCOUNT IS PROVIDED IN A SECURE ENVIRONMENT. The fund maintains physical, electronic and procedural safeguards that comply with federal regulations to guard nonpublic personal information. The fund’s agents and service providers have limited access to customer information based on their role in servicing your account. THE FUND COLLECTS INFORMATION IN ORDER TO SERVICE AND ADMINISTER YOUR ACCOUNT. The fund collects a variety of nonpublic personal information, which may include: • Information we receive from you, such as your name, address, and social security number. • Information about your transactions with us, such as the purchase or sale of fund shares. • Information we receive from agents and service providers, such as proxy voting information. THE FUND DOES NOT SHARE NONPUBLIC PERSONAL INFORMATION WITH ANYONE, EXCEPT AS PERMITTED BY LAW. Thank you for this opportunity to serve you. |

The views expressed in this report reflect those of the portfolio manager(s) only through the end of the period covered and do not necessarily represent the views of BNY Mellon Investment Adviser, Inc. or any other person in the BNY Mellon Investment Adviser, Inc. organization. Any such views are subject to change at any time based upon market or other conditions and BNY Mellon Investment Adviser, Inc. disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund in the BNY Mellon Family of Funds are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any fund in the BNY Mellon Family of Funds. |

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value |

Contents

THE FUND

FOR MORE INFORMATION

Back Cover

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.im.bnymellon.com and sign up for eCommunications. It’s simple and only takes a few minutes. |

DISCUSSION OF FUND PERFORMANCE (Unaudited)

For the period from October 1, 2020 through September 30, 2021, as provided by Daniel Rabasco and Jeffrey Burger, Primary Portfolio Managers

Market and Fund Performance Overview

For the 12-month period ended September 30, 2021, BNY Mellon Strategic Municipals, Inc. produced a total return of 9.22% on a net-asset-value basis and 10.29% on a market price basis.1 Over the same period, the fund provided aggregate income dividends of $0.42 per share, which reflects a distribution rate of 4.83%.2

Municipal bonds rose during the reporting period as the market benefited from a continuing economic recovery and robust demand. Strong tax revenues and credit fundamentals also supported performance.

The Fund’s Investment Approach

The fund’s investment objective is to maximize current income exempt from federal income tax to the extent consistent with the preservation of capital. Under normal market conditions, the fund invests at least 80% of its net assets in municipal obligations. Generally, the fund invests at least 50% of its net assets in municipal bonds considered investment grade or the unrated equivalent as determined by BNY Mellon Investment Adviser, Inc. in the case of bonds, and in the two highest rating categories or the unrated equivalent as determined by BNY Mellon Investment Adviser, Inc. in the case of short-term obligations having or deemed to have maturities of less than one year.

To this end, portfolio construction focuses on income opportunities, through analysis of each bond’s structure, including close attention to each bond’s yield, maturity and early redemption features. When making new investments, we focus on identifying undervalued sectors and securities, and we minimize reliance on interest-rate forecasting. We select municipal bonds based on fundamental credit analysis to estimate the relative value and attractiveness of various sectors and securities and to exploit pricing inefficiencies in the municipal bond market. We actively trade among various sectors, such as escrowed, general obligation and revenue, based on their apparent relative values. Leverage, which is utilized in the portfolio in order to generate a higher level of current income exempt from regular federal income taxes, does amplify the fund’s exposure to interest-rate movements, and potentially, gains or losses, especially those among the longest maturities. The use of leverage had a positive impact on performance during the period.

Market Benefits from Policy Support, Strong Fundamentals and Robust Inflows

During the reporting period, the market continued to benefit from policies put in place in response to the COVID-19 pandemic, including support from the Federal Reserve (the “Fed”). While the Fed made no notable changes to monetary policy, early in the period it did commit to continuing its bond purchasing program. In the second half of the period, the Fed adopted a more hawkish tone, however.

Robust fiscal support also benefited the market. The $1.9 trillion American Rescue Plan extended unemployment benefits, provided aid to schools and businesses and sent stimulus checks to families. That supported the U.S. economy and also the municipal bond market.

2

The election also increased the likelihood of income tax hikes for higher-income households, adding to the appeal of tax-exempt municipal securities. The prospect of an increase in the corporate tax rate made municipal bonds more appealing to institutional buyers, and low interest rates overseas attracted foreign investors to the market.

Performance in the Treasury market was generally poor as the market sold off midway through the reporting period, especially at the long end of the curve. Performance in fixed-income risk markets, however, was stronger as the approval of COVID-19 vaccines provided support. Both the investment-grade and high yield corporate segments of the market posted positive returns.

In the municipal bond market, performance was also strong, supported especially by strong supply-and-demand factors. While supply surged prior to the November 2020 election, it tapered off later in the year but has remained near the record supply of last year. At the same time, flows into municipal bond mutual funds were strong, helped in part by a surge in investor optimism resulting from the approval of COVID-19 vaccines. Credit conditions also improved over the period, which resulted in spread tightening in the municipal market, with the revenue segment outperforming the general obligation segment.

Volatility experienced in the Treasury market also occurred in the municipal bond market, though to a lesser extent. Generally, the municipal yield curve flattened during the period.

Late in the reporting period, inflows slowed somewhat, and the market experienced some uncertainty in response to political debates in Washington D.C. regarding federal spending plans and the debt ceiling. The municipal bond market generally finished the period relatively richly valued versus Treasuries.

Security Selection Drove Returns

The fund’s performance was helped primarily by favorable security selections. Holdings in the education, hospital, senior living, special tax, tobacco and transportation segments were especially beneficial. A position in uninsured Puerto Rico general obligation bonds also contributed positively, as did Illinois general obligation bonds and New Jersey appropriation bonds. An overweight position in revenue bonds was also somewhat beneficial, with hospital, senior living and tobacco bonds performing best. The fund’s duration positioning also contributed positively to returns, especially its holdings of bonds having intermediate to longer maturity dates.

On a less positive note, the fund’s performance was hampered by certain positions in higher credit quality revenue bonds. Specifically, bonds in the utilities and water & sewer segment were detrimental, and security selection in these segments also hindered returns. We permitted the fund’s leverage to modestly decline during the period, and we did not employ derivatives.

Strong Fundamentals and Demand

Economic fundamentals, as well as supply-and-demand factors, bode well for the municipal bond market. Issuers generally have healthy fundamentals resulting from a recovering economy and strong tax revenues. They have also benefitted from prior federal fiscal stimulus measures and should also benefit from a federal infrastructure spending package that is likely to pass in the near term. Demand for municipal bonds is likely to remain strong and investor support could increase if higher corporate and personal income tax rates are legislated to pay for federal spending programs.

3

DISCUSSION OF FUND PERFORMANCE (Unaudited) (continued)

Inflation remains a risk, but with the healthy condition of the municipal bond market, we anticipate it will outperform the Treasury market. Given the outlook for inflation and interest rates, we have lowered the fund’s leverage modestly. We will continue to focus on identifying undervalued credits in the lower investment grade category and, when warranted by fundamentals and valuations, also purchase bonds in the sub-investment grade rating category in order to provide the fund additional yield and excess total return potential.

October 15, 2021

1 Total return includes reinvestment of dividends and any capital gains paid, based upon net asset value per share or market price per share, as applicable. Past performance is no guarantee of future results. Market price per share, net asset value per share and investment return fluctuate. Income may be subject to state and local taxes, and some income may be subject to the federal alternative minimum tax (AMT) for certain investors. Capital gains, if any, are fully taxable. Return figures provided reflects the absorption of certain fund expenses by BNY Mellon Investment Adviser, Inc. pursuant to an agreement in effect until November 30, 2021, at which time it may be extended, modified or terminated. Had these expenses not been absorbed, the fund’s return would have been lower.

2 Distribution rate per share is based upon dividends per share paid from net investment income during the period, divided by the market price per share at the end of the period, adjusted for any capital gain distributions.

Bonds are subject generally to interest-rate, credit, liquidity and market risks, to varying degrees. Generally, all other factors being equal, bond prices are inversely related to interest-rate changes, and rate increases can cause price declines. High yield bonds are subject to increased credit risk and are considered speculative in terms of the issuer’s perceived ability to continue making interest payments on a timely basis and to repay principal upon maturity. The use of leverage may magnify the fund’s gains or losses. For derivatives with a leveraging component, adverse changes in the value or level of the underlying asset can result in a loss that is much greater than the original investment in the derivative.

Recent market risks include pandemic risks related to COVID-19. The effects of COVID-19 have contributed to increased volatility in global markets and will likely affect certain countries, companies, industries and market sectors more dramatically than others. To the extent the fund may overweight its investments in certain countries, companies, industries or market sectors, such positions will increase the fund’s exposure to risk of loss from adverse developments affecting those countries, companies, industries or sectors.

4

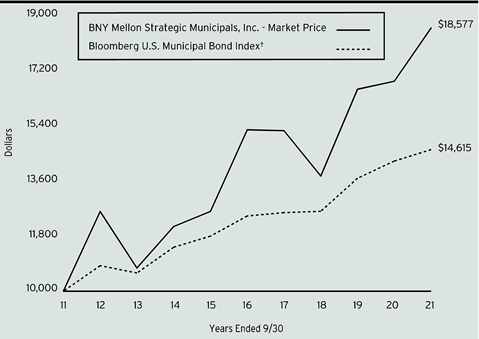

FUND PERFORMANCE (Unaudited)

Comparison

of change in value of a $10,000 investment in BNY Mellon Strategic Municipals, Inc. with a hypothetical

investment of $10,000 in the Bloomberg U.S. Municipal Bond Index (the “Index”).

† Source: Lipper Inc.

Past performance is not predictive of future performance.

The above graph compares a hypothetical $10,000 investment made in BNY Mellon Strategic Municipals, Inc. on 9/30/11 to a hypothetical investment of $10,000 made in the Index on that date. All figures for the fund are based on market price. All dividends and capital gain distributions are reinvested.

The fund invests primarily in municipal securities and its performance shown in the line graph takes into account fees and expenses. The Index covers the U.S. dollar-denominated long-term tax-exempt bond market. Unlike a fund, the Index is not subject to fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights within this report and elsewhere in this report.

Average Annual Total Returns as of 9/30/2021 | |||

| 1 Year | 5 Years | 10 Years |

BNY Mellon Strategic Municipals, Inc. - Market Value | 10.29% | 4.01% | 6.39% |

BNY Mellon Strategic Municipals, Inc. - Net Asset Value | 9.22% | 4.55% | 6.52% |

Bloomberg U.S. Municipal Bond Index | 2.63% | 3.26% | 3.87% |

The performance data quoted represents past performance, which is no guarantee of future results. Share price and investment return fluctuate and an investor’s shares may be worth more or less than original cost upon sale of the shares. All dividends and capital gain distributions are reinvested. Current performance may be lower or higher than the performance quoted. Go to www.im.bnymellon.com for the fund’s most recent month-end returns.

The fund’s performance shown in the graph and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the sale of fund shares.

5

FUND PERFORMANCE (Unaudited) (continued)

DISTRIBUTION INFORMATION

The following information regarding the fund’s distributions is current as of September 30, 2021, the fund’s fiscal year end. The fund’s returns during the period were sufficient to meet fund distributions.

The fund’s distribution policy is intended to provide shareholders with stable, but not guaranteed, cash flow, independent of the amount or timing of income earned or capital gains realized by the fund. The fund intends to distribute all or substantially all of its net investment income through its regular monthly distribution and to distribute realized capital gains at least annually. In addition, in any monthly period, in order to try to maintain a level distribution amount, the fund may pay out more or less than its net investment income during the period. As a result, distributions sources may include net investment income, realized gains and return of capital. You should not draw any conclusions about the fund’s investment performance from the amount of the distribution or from the terms of the level distribution program. A return of capital is a non-taxable distribution of a portion of a fund’s capital. A return of capital distribution does not necessarily reflect a fund’s investment performance and should not be confused with “yield” or “income.”

The amounts and sources of distributions reported below are for financial reporting purposes and are not being provided for tax reporting purposes. The actual amounts and character of the distributions for tax reporting purposes will be reported to shareholders on Form 1099-DIV, which will be sent to shareholders shortly after calendar year-end. Because distribution source estimates are updated throughout the current fiscal year based on the fund’s performance, those estimates may differ from both the tax information reported to you in your fund’s 1099 statement, as well as the ultimate economic sources of distributions over the life of your investment. The figures in the table below provide the sources of distributions and may include amounts attributed to realized gains and/or returns of capital.

Distributions | |||||||

Current Month | Fiscal Year Ended | ||||||

| Net Investment Income | Realized Gains | Return of Capital | Total Distributions | Net Investment Income | Realized Gains | Return of Capital |

BNY Mellon Strategic Municipals, Inc. | 100.00% | 0.00% | 0.00% | $0.42 | $0.42 | $0.00 | $0.00 |

6

SELECTED INFORMATION

September 30, 2021 (Unaudited)

Market Price per share September 30, 2021 | $8.70 | |||

Shares Outstanding September 30, 2021 | 62,276,212 | |||

New York Stock Exchange Ticker Symbol | LEO | |||

MARKET PRICE (NEW YORK STOCK EXCHANGE) | ||||

Fiscal Year Ended September 30, 2021 | ||||

Quarter | Quarter | Quarter | Quarter | |

Ended | Ended | Ended | Ended | |

December 31, 2020 | March 31, 2021 | June 30, 2021 | September 30, 2021 | |

High | $8.61 | $8.83 | $8.98 | $9.48 |

Low | 8.02 | 8.30 | 8.56 | 8.70 |

Close | 8.49 | 8.54 | 8.97 | 8.70 |

PERCENTAGE GAIN (LOSS) based on change in Market Price† | ||||

September 23, 1987 (commencement of operations) through September 30, 2021 | 754.74% | |||

October 1, 2011 through September 30, 2021 | 85.78 | |||

October 1, 2016 through September 30, 2021 | 21.74 | |||

October 1, 2020 through September 30, 2021 | 10.29 | |||

January 1, 2021 through September 30, 2021 | 6.22 | |||

April 1, 2021 through September 30, 2021 | 4.31 | |||

July 1, 2021 through September 30, 2021 | (1.86) | |||

NET ASSET VALUE PER SHARE | ||||

September 23, 1987 (commencement of operations) | $9.32 | |||

September 30, 2020 | 8.37 | |||

December 31, 2020 | 8.66 | |||

March 31, 2021 | 8.63 | |||

June 30, 2021 | 8.89 | |||

September 30, 2021 | 8.71 | |||

PERCENTAGE GAIN (LOSS) based on change in Net Asset Value† | ||||

September 23, 1987 (commencement of operations) through September 30, 2021 | 818.08% | |||

October 1, 2011 through September 30, 2021 | 87.99 | |||

October 1, 2016 through September 30, 2021 | 24.94 | |||

October 1, 2020 through September 30, 2021 | 9.22 | |||

January 1, 2021 through September 30, 2021 | 4.26 | |||

April 1, 2021 through September 30, 2021 | 3.35 | |||

July 1, 2021 through September 30, 2021 | (0.86) | |||

† Total return includes reinvestment of dividends and any capital gains paid.

7

STATEMENT OF INVESTMENTS

September 30, 2021

Description | Coupon | Maturity Date | Principal Amount ($) |

| Value ($) | ||||

Bonds and Notes - .3% | |||||||||

Collateralized Municipal-Backed Securities - .3% | |||||||||

Arizona

Industrial Development Authority, Revenue Bonds, Ser. 2019-2 | 3.63 | 5/20/2033 | 1,692,550 | 1,891,421 | |||||

| |||||||||

Long-Term Municipal Investments - 148.9% | |||||||||

Alabama - 3.6% | |||||||||

Alabama Special Care Facilities Financing Authority, Revenue Bonds (Methodist Home for the Aging Obligated Group) | 5.75 | 6/1/2045 | 6,000,000 | 6,285,953 | |||||

Jefferson County, Revenue Bonds, Refunding, Ser. F | 7.90 | 10/1/2050 | 2,500,000 | a | 2,570,638 | ||||

The Lower Alabama Gas District, Revenue Bonds, Ser. A | 5.00 | 9/1/2046 | 6,000,000 | 8,548,381 | |||||

University of Alabama at Birmingham, Revenue Bonds, Ser. B | 4.00 | 10/1/2036 | 2,000,000 | 2,347,535 | |||||

19,752,507 | |||||||||

Arizona - 7.7% | |||||||||

Arizona Industrial Development Authority, Revenue Bonds (Academics of Math & Science Project) | 5.00 | 7/1/2054 | 1,275,000 | b | 1,451,821 | ||||

Arizona Industrial Development Authority, Revenue Bonds (Cadence Campus Project) Ser. A | 4.00 | 7/15/2030 | 625,000 | b | 686,672 | ||||

Arizona Industrial Development Authority, Revenue Bonds (Cadence Campus Project) Ser. A | 4.00 | 7/15/2040 | 925,000 | b | 996,050 | ||||

Arizona Industrial Development Authority, Revenue Bonds (Legacy Cares Project) Ser. A | 6.00 | 7/1/2051 | 1,000,000 | b | 1,096,705 | ||||

Arizona Industrial Development Authority, Revenue Bonds (Legacy Cares Project) Ser. A | 7.75 | 7/1/2050 | 5,770,000 | b | 6,865,821 | ||||

Arizona Industrial Development Authority, Revenue Bonds (Phoenix Children's Hospital Obligated Group) | 4.00 | 2/1/2050 | 1,500,000 | 1,726,066 | |||||

Arizona Industrial Development Authority, Revenue Bonds, Refunding (Basis Schools Projects) Ser. D | 5.00 | 7/1/2051 | 380,000 | b | 436,413 | ||||

8

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Arizona - 7.7% (continued) | |||||||||

Arizona Industrial Development Authority, Revenue Bonds, Refunding (Basis Schools Projects) Ser. D | 5.00 | 7/1/2047 | 1,035,000 | b | 1,191,683 | ||||

Glendale Industrial Development Authority, Revenue Bonds, Refunding (Sun Health Services Obligated Group) Ser. A | 5.00 | 11/15/2054 | 1,000,000 | 1,145,500 | |||||

La Paz County Industrial Development Authority, Revenue Bonds (Harmony Public Schools) Ser. A | 5.00 | 2/15/2036 | 2,480,000 | b | 2,778,518 | ||||

Maricopa County Industrial Development Authority, Revenue Bonds (Benjamin Franklin Charter School Obligated Group) | 6.00 | 7/1/2052 | 3,000,000 | b | 3,559,566 | ||||

Maricopa County Industrial Development Authority, Revenue Bonds, Refunding (Paradise Schools Projects Paragon Management) | 5.00 | 7/1/2047 | 2,000,000 | b | 2,211,783 | ||||

Salt Verde Financial Corp., Revenue Bonds | 5.00 | 12/1/2037 | 1,000,000 | 1,377,600 | |||||

Tender Option Bond Trust Receipts (Series 2018-XF2537), (Salt Verde Financial Corporation, Revenue Bonds) Recourse, Underlying Coupon Rate (%) 5.00 | 17.63 | 12/1/2037 | 4,030,000 | b,c,d | 5,479,406 | ||||

The Phoenix Industrial Development Authority, Revenue Bonds, Refunding (BASIS Schools Projects) Ser. A | 5.00 | 7/1/2035 | 2,360,000 | b | 2,629,297 | ||||

The Phoenix Industrial Development Authority, Revenue Bonds, Refunding (BASIS Schools Projects) Ser. A | 5.00 | 7/1/2046 | 2,000,000 | b | 2,209,878 | ||||

The Pima County Industrial Development Authority, Revenue Bonds (American Leadership Academy Project) | 5.00 | 6/15/2047 | 6,000,000 | b | 6,067,784 | ||||

41,910,563 | |||||||||

California - 5.5% | |||||||||

California Municipal Finance Authority, Revenue Bonds, Refunding (William Jessup University) | 5.00 | 8/1/2039 | 1,000,000 | 1,115,621 | |||||

9

STATEMENT OF INVESTMENTS (continued)

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

California - 5.5% (continued) | |||||||||

California Statewide Communities Development Authority, Revenue Bonds (Loma Linda University Medical Center Obligated Group) | 5.50 | 12/1/2058 | 1,000,000 | b | 1,170,698 | ||||

Jefferson Union High School District, COP (Teacher & Staff Housing Project) (Insured; Build America Mutual) | 4.00 | 8/1/2055 | 1,000,000 | 1,139,100 | |||||

San Francisco City & County Redevelopment Agency, Special Tax Bonds, Refunding, Ser. A | 5.00 | 8/1/2023 | 1,000,000 | 1,037,117 | |||||

Tender Option Bond Trust Receipts (Series 2016-XM0379), (Los Angeles Department of Water & Power, Revenue Bonds, Refunding) Non-recourse, Underlying Coupon Rate (%) 5.00 | 18.19 | 7/1/2043 | 5,000,000 | b,c,d | 5,171,668 | ||||

Tender Option Bond Trust Receipts (Series 2016-XM0434), (The Regents of the University of California, Revenue Bonds, Refunding) Recourse, Underlying Coupon Rate (%) 5.00 | 18.18 | 5/15/2038 | 10,000,000 | b,c,d | 10,722,467 | ||||

Tender Option Bond Trust Receipts (Series 2020-XF2876), (San Francisco California City & County Airport Commission, Revenue Bonds, Refunding, Ser. E) Recourse, Underlying Coupon Rate (%) 5.00 | 17.81 | 5/1/2050 | 7,780,000 | b,c,d | 9,376,780 | ||||

29,733,451 | |||||||||

Colorado - 7.7% | |||||||||

Colorado Health Facilities Authority, Revenue Bonds, Refunding (Covenant Living Communities & Services Obligated Group) Ser. A | 4.00 | 12/1/2050 | 4,500,000 | 5,106,303 | |||||

Denver City & County, Revenue Bonds, Refunding (United Airlines Project) | 5.00 | 10/1/2032 | 1,000,000 | 1,058,650 | |||||

Dominion Water & Sanitation District, Revenue Bonds | 6.00 | 12/1/2046 | 4,560,000 | 4,680,084 | |||||

Hess Ranch Metropolitan District No. 6, GO, Ser. A1 | 5.00 | 12/1/2049 | 2,000,000 | 2,173,549 | |||||

Rampart Range Metropolitan District No. 5, Revenue Bonds | 4.00 | 12/1/2051 | 2,000,000 | e | 2,023,729 | ||||

Regional Transportation District, Revenue Bonds, Refunding (Denver Transit Partners) Ser. A | 4.00 | 7/15/2035 | 1,250,000 | 1,492,814 | |||||

10

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Colorado - 7.7% (continued) | |||||||||

Tender Option Bond Trust Receipts (Series 2016-XM0385), (Board of Governors of the Colorado State University, Revenue Bonds) Non-recourse, Underlying Coupon Rate (%) 5.00 | 18.16 | 3/1/2038 | 7,500,000 | b,c,d | 7,643,945 | ||||

Tender Option Bond Trust Receipts (Series 2016-XM0433), (Colorado Springs, Revenue Bonds) Recourse, Underlying Coupon Rate (%) 5.00 | 18.14 | 11/15/2043 | 9,752,907 | b,c,d | 10,589,481 | ||||

Tender Option Bond Trust Receipts (Series 2020-XM0829), (Colorado Health Facilities Authority, Revenue Bonds, Refunding (CommonSpirit Health Obligated Group, Ser. A1)) Recourse, Underlying Coupon Rate (%) 4.00 | 17.18 | 8/1/2044 | 4,440,000 | b,c,d | 5,993,113 | ||||

Vauxmont Metropolitan District, GO, Refunding (Insured; Assured Guaranty Municipal Corp.) | 3.25 | 12/15/2050 | 800,000 | 861,936 | |||||

41,623,604 | |||||||||

Connecticut - 2.6% | |||||||||

Connecticut, Revenue Bonds (Special Tax Obligation) Ser. A | 5.00 | 5/1/2040 | 1,000,000 | 1,267,299 | |||||

Connecticut, Revenue Bonds, Ser. A | 5.00 | 5/1/2034 | 2,000,000 | 2,630,830 | |||||

Connecticut Health & Educational Facilities Authority, Revenue Bonds, Refunding (Trinity Health Obligated Group) | 5.00 | 12/1/2045 | 2,500,000 | 2,952,287 | |||||

Connecticut Health & Educational Facilities Authority, Revenue Bonds, Refunding, Ser. S | 4.00 | 6/1/2051 | 2,000,000 | 2,349,392 | |||||

Connecticut Housing Finance Authority, Revenue Bonds, Refunding, Ser. A1 | 3.65 | 11/15/2032 | 610,000 | 639,935 | |||||

Harbor Point Infrastructure Improvement District, Tax Allocation Bonds, Refunding (Harbor Point Project) | 5.00 | 4/1/2039 | 3,500,000 | b | 4,008,747 | ||||

13,848,490 | |||||||||

District of Columbia - 4.3% | |||||||||

Metropolitan Washington Airports Authority, Revenue Bonds, Refunding (Dulles Metrorail & Capital Improvement Projects) Ser. A | 5.00 | 10/1/2039 | 1,000,000 | 1,229,576 | |||||

11

STATEMENT OF INVESTMENTS (continued)

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

District of Columbia - 4.3% (continued) | |||||||||

Metropolitan Washington Airports Authority, Revenue Bonds, Refunding, Ser. B | 4.00 | 10/1/2049 | 1,000,000 | 1,123,199 | |||||

Tender Option Bond Trust Receipts (Series 2016-XM0437), (District of Columbia, Revenue Bonds) Recourse, Underlying Coupon Rate (%) 5.00 | 18.15 | 12/1/2035 | 19,992,830 | b,c,d | 21,021,202 | ||||

23,373,977 | |||||||||

Florida - 7.7% | |||||||||

Alachua County Health Facilities Authority, Revenue Bonds (Shands Teaching Hospital & Clinics Obligated Group) | 4.00 | 12/1/2049 | 1,625,000 | 1,861,470 | |||||

Atlantic Beach, Revenue Bonds (Fleet Landing Project) Ser. A | 5.00 | 11/15/2053 | 3,000,000 | 3,392,960 | |||||

Capital Trust Agency, Revenue Bonds (WFCS Portfolio Projects) Ser. A | 5.00 | 1/1/2056 | 750,000 | b | 844,446 | ||||

Florida Development Finance Corp., Revenue Bonds (Miami Arts Charter School Project) Ser. A | 6.00 | 6/15/2044 | 5,000,000 | b | 4,693,609 | ||||

Greater Orlando Aviation Authority, Revenue Bonds, Ser. A | 4.00 | 10/1/2044 | 2,000,000 | 2,278,765 | |||||

Miami-Dade County, Revenue Bonds | 0.00 | 10/1/2045 | 3,000,000 | f | 1,400,473 | ||||

Palm Beach County Health Facilities Authority, Revenue Bonds (ACTS Retirement-Life Communities Obligated Group) | 5.00 | 11/15/2045 | 2,850,000 | 3,284,488 | |||||

Palm Beach County Health Facilities Authority, Revenue Bonds (ACTS Retirement-Life Communities Obligated Group) Ser. B | 5.00 | 11/15/2042 | 735,000 | 892,741 | |||||

Palm Beach County Health Facilities Authority, Revenue Bonds (Lifespace Communities Obligated Group) Ser. B | 4.00 | 5/15/2053 | 2,600,000 | 2,853,441 | |||||

Pinellas County Industrial Development Authority, Revenue Bonds (Foundation for Global Understanding) | 5.00 | 7/1/2029 | 900,000 | 1,006,933 | |||||

Seminole County Industrial Development Authority, Revenue Bonds, Refunding (Legacy Pointe at UCF Project) | 5.75 | 11/15/2054 | 2,500,000 | 2,795,115 | |||||

12

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Florida - 7.7% (continued) | |||||||||

Tender Option Bond Trust Receipts (Series 2019-XF0813), (Fort Myers Florida Utility, Revenue Bonds) Non-recourse, Underlying Coupon Rate (%) 4.00 | 14.40 | 10/1/2049 | 3,435,000 | b,c,d | 3,897,324 | ||||

Tender Option Bond Trust Receipts (Series 2019-XM0782), (Palm Beach County Florida Health Facilities Authority, Revenue Bonds, Refunding (Baptist Health South Florida Obligated Group)) Recourse, Underlying Coupon Rate (%) 4.00 | 14.36 | 8/15/2049 | 5,535,000 | b,c,d | 6,275,179 | ||||

Tender Option Bond Trust Receipts (Series 2020-XF2877), (Greater Orlando Aviation Authority, Revenue Bonds, Ser. A) Recourse, Underlying Coupon Rate (%) 4.00 | 14.29 | 10/1/2049 | 4,685,000 | b,c,d | 5,283,754 | ||||

Village Community Development District No. 10, Special Assessment Bonds | 6.00 | 5/1/2044 | 900,000 | 963,964 | |||||

41,724,662 | |||||||||

Georgia - 5.3% | |||||||||

Atlanta Water & Wastewater, Revenue Bonds, Ser. D | 3.50 | 11/1/2028 | 1,460,000 | b | 1,582,103 | ||||

Georgia Municipal Electric Authority, Revenue Bonds, Refunding (Plant Vogtle Units 3&4 Project) Ser. A | 5.00 | 1/1/2056 | 1,250,000 | 1,514,267 | |||||

Tender Option Bond Trust Receipts (Series 2016-XM0435), (Private Colleges & Universities Authority, Revenue Bonds, Refunding (Emory University)) Recourse, Underlying Coupon Rate (%) 5.00 | 18.15 | 10/1/2043 | 10,000,000 | b,c,d | 10,821,384 | ||||

Tender Option Bond Trust Receipts (Series 2019-XF2847), (Municipal Electric Authority of Georgia, Revenue Bonds (Plant Vogtle Unis 3&4 Project, Ser. A)) Recourse, Underlying Coupon Rate (%) 5.00 | 17.97 | 1/1/2056 | 3,600,000 | b,c,d | 4,286,134 | ||||

Tender Option Bond Trust Receipts (Series 2020-XM0825), (Brookhaven Development Authority, Revenue Bonds (Children's Healthcare of Atlanta, Ser. A)) Recourse, Underlying Coupon Rate (%) 4.00 | 15.65 | 7/1/2044 | 6,340,000 | b,c,d | 7,819,859 | ||||

13

STATEMENT OF INVESTMENTS (continued)

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Georgia - 5.3% (continued) | |||||||||

The Burke County Development Authority, Revenue Bonds, Refunding (Oglethorpe Power Corp.) Ser. D | 4.13 | 11/1/2045 | 2,400,000 | 2,698,407 | |||||

28,722,154 | |||||||||

Hawaii - .6% | |||||||||

Hawaii Department of Budget & Finance, Revenue Bonds, Refunding (Hawaiian Electric Co.) | 4.00 | 3/1/2037 | 1,500,000 | 1,653,162 | |||||

Honolulu City & County, GO, Ser. C | 4.00 | 7/1/2044 | 1,500,000 | 1,750,393 | |||||

3,403,555 | |||||||||

Idaho - .9% | |||||||||

Power County Industrial Development Corp., Revenue Bonds (FMC Corp. Project) | 6.45 | 8/1/2032 | 5,000,000 | 5,023,996 | |||||

Illinois - 13.9% | |||||||||

Chicago Board of Education, GO, Refunding, Ser. A | 5.00 | 12/1/2034 | 1,400,000 | 1,707,088 | |||||

Chicago Board of Education, GO, Ser. D | 5.00 | 12/1/2046 | 2,000,000 | 2,397,390 | |||||

Chicago Board of Education, GO, Ser. H | 5.00 | 12/1/2036 | 2,000,000 | 2,383,515 | |||||

Chicago II, GO, Refunding, Ser. A | 6.00 | 1/1/2038 | 3,000,000 | 3,679,967 | |||||

Chicago II, GO, Ser. A | 5.00 | 1/1/2044 | 4,000,000 | 4,763,876 | |||||

Chicago II, GO, Ser. A | 5.50 | 1/1/2049 | 1,000,000 | 1,218,440 | |||||

Chicago O'Hare International Airport, Revenue Bonds, Refunding, Ser. A | 5.00 | 1/1/2048 | 3,585,000 | 4,319,892 | |||||

Chicago Transit Authority, Revenue Bonds, Refunding, Ser. A | 5.00 | 12/1/2045 | 1,000,000 | 1,228,092 | |||||

Illinois, GO, Refunding, Ser. A | 5.00 | 10/1/2029 | 1,100,000 | 1,351,228 | |||||

Illinois, GO, Ser. A | 5.00 | 5/1/2038 | 3,900,000 | 4,611,657 | |||||

Illinois, GO, Ser. C | 5.00 | 11/1/2029 | 1,120,000 | 1,343,151 | |||||

Illinois, GO, Ser. D | 5.00 | 11/1/2028 | 2,825,000 | 3,417,132 | |||||

Illinois Finance Authority, Revenue Bonds, Refunding (Lutheran Life Communities Obligated Group) Ser. A | 5.00 | 11/1/2040 | 1,750,000 | 1,956,957 | |||||

Illinois Toll Highway Authority, Revenue Bonds, Ser. A | 4.00 | 1/1/2044 | 1,500,000 | 1,727,310 | |||||

Metropolitan Pier & Exposition Authority, Revenue Bonds (McCormick Place Expansion Project) | 5.00 | 6/15/2057 | 2,000,000 | 2,344,659 | |||||

14

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Illinois - 13.9% (continued) | |||||||||

Metropolitan Pier & Exposition Authority, Revenue Bonds (McCormick Place Project) (Insured; National Public Finance Guarantee Corp.) Ser. A | 0.00 | 12/15/2036 | 2,500,000 | f | 1,750,630 | ||||

Metropolitan Pier & Exposition Authority, Revenue Bonds, Refunding (McCormick Place Expansion Project) | 0.00 | 12/15/2054 | 21,800,000 | f | 7,767,708 | ||||

Metropolitan Pier & Exposition Authority, Revenue Bonds, Refunding (McCormick Place Project) Ser. B | 5.00 | 6/15/2052 | 1,650,000 | 1,704,320 | |||||

Metropolitan Pier & Exposition Authority, Revenue Bonds, Refunding (McCormick Place Project) Ser. B | 5.00 | 12/15/2028 | 1,000,000 | 1,032,921 | |||||

Sales Tax Securitization Corp., Revenue Bonds, Refunding, Ser. A | 4.00 | 1/1/2038 | 2,000,000 | 2,332,026 | |||||

Tender Option Bond Trust Receipts (Series 2016-XM0378), (Greater Chicago Metropolitan Water Reclamation District, GO) Non-recourse, Underlying Coupon Rate (%) 5.00 | 18.13 | 12/1/2032 | 7,500,000 | b,c,d | 7,556,050 | ||||

Tender Option Bond Trust Receipts (Series 2017-XM0492), (Illinois Finance Authority, Revenue Bonds, Refunding (The University of Chicago)) Non-recourse, Underlying Coupon Rate (%) 5.00 | 18.16 | 10/1/2040 | 12,000,000 | b,c,d | 13,887,664 | ||||

University of Illinois, Revenue Bonds (Auxiliary Facilities System) Ser. A | 5.00 | 4/1/2044 | 1,000,000 | 1,101,407 | |||||

75,583,080 | |||||||||

Indiana - 1.8% | |||||||||

Indiana Finance Authority, Revenue Bonds (Green Bond) (RES Polyflow Indiana) | 7.00 | 3/1/2039 | 6,175,000 | b | 5,859,803 | ||||

Indiana Finance Authority, Revenue Bonds (Ohio Valley Electric Project) Ser. A | 5.00 | 6/1/2039 | 1,585,000 | 1,616,053 | |||||

Indiana Finance Authority, Revenue Bonds (Ohio Valley Electric Project) Ser. B | 3.00 | 11/1/2030 | 1,000,000 | 1,053,870 | |||||

Indiana Finance Authority, Revenue Bonds (Parkview Health System Obligated Group) Ser. A | 5.00 | 11/1/2043 | 1,000,000 | 1,226,100 | |||||

9,755,826 | |||||||||

15

STATEMENT OF INVESTMENTS (continued)

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Iowa - 2.4% | |||||||||

Iowa Finance Authority, Revenue Bonds, Refunding (Iowa Fertilizer Co. Project) | 5.25 | 12/1/2025 | 7,375,000 | 7,983,022 | |||||

Iowa Finance Authority, Revenue Bonds, Refunding (Lifespace Communities Obligated Group) Ser. A | 4.00 | 5/15/2046 | 1,500,000 | 1,659,887 | |||||

Iowa Tobacco Settlement Authority, Revenue Bonds, Refunding, Ser. A2 | 4.00 | 6/1/2049 | 1,500,000 | 1,714,101 | |||||

Iowa Tobacco Settlement Authority, Revenue Bonds, Refunding, Ser. B1 | 4.00 | 6/1/2049 | 1,500,000 | 1,707,148 | |||||

13,064,158 | |||||||||

Kansas - .1% | |||||||||

Kansas Development Finance Authority, Revenue Bonds, Ser. B | 4.00 | 11/15/2025 | 600,000 | 606,334 | |||||

Kentucky - .5% | |||||||||

Kentucky Public Energy Authority, Revenue Bonds, Ser. A1 | 4.00 | 6/1/2025 | 2,500,000 | g | 2,787,617 | ||||

Louisiana - 3.2% | |||||||||

Louisiana Local Government Environmental Facilities & Community Development Authority, Revenue Bonds, Refunding (Westlake Chemical Project) | 3.50 | 11/1/2032 | 3,100,000 | 3,420,746 | |||||

Louisiana Public Facilities Authority, Revenue Bonds, Refunding (Tulane University) | 4.00 | 4/1/2050 | 1,000,000 | 1,138,438 | |||||

Tender Option Bond Trust Receipts (Series 2018-XF2584), (Louisiana Public Facilities Authority, Revenue Bonds (Franciscan Missionaries of Our Lady Health System Project)) Non-recourse, Underlying Coupon Rate (%) 5.00 | 17.98 | 7/1/2047 | 10,755,000 | b,c,d | 12,653,649 | ||||

17,212,833 | |||||||||

Maryland - 3.0% | |||||||||

Maryland Economic Development Corp., Tax Allocation Bonds (Port Covington Project) | 4.00 | 9/1/2050 | 1,000,000 | 1,126,769 | |||||

Maryland Health & Higher Educational Facilities Authority, Revenue Bonds (Adventist Healthcare Obligated Group) Ser. A | 5.50 | 1/1/2046 | 3,250,000 | 3,856,411 | |||||

16

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Maryland - 3.0% (continued) | |||||||||

Maryland Health & Higher Educational Facilities Authority, Revenue Bonds, Refunding (Stevenson University Project) | 4.00 | 6/1/2051 | 1,000,000 | 1,130,473 | |||||

Tender Option Bond Trust Receipts (Series 2016-XM0391), (Mayor & City Council of Baltimore, Revenue Bonds, Refunding (Water Projects)) Non-recourse, Underlying Coupon Rate (%) 5.00 | 18.16 | 7/1/2042 | 9,000,000 | b,c,d | 9,926,969 | ||||

16,040,622 | |||||||||

Massachusetts - 5.7% | |||||||||

Lowell Collegiate Charter School, Revenue Bonds | 5.00 | 6/15/2049 | 1,750,000 | 1,874,452 | |||||

Massachusetts Development Finance Agency, Revenue Bonds, Refunding (NewBridge Charles Obligated Group) | 5.00 | 10/1/2057 | 1,000,000 | b | 1,084,748 | ||||

Massachusetts Development Finance Agency, Revenue Bonds, Refunding, Ser. A | 5.00 | 7/1/2025 | 1,400,000 | 1,617,820 | |||||

Tender Option Bond Trust Receipts (Series 2016-XM0389), (Massachusetts School Building Authority, Revenue Bonds) Non-recourse, Underlying Coupon Rate (%) 5.00 | 18.16 | 5/15/2043 | 10,000,000 | b,c,d | 10,749,505 | ||||

Tender Option Bond Trust Receipts (Series 2018-XF0610), (Massachusetts Transportation Fund, Revenue Bonds (Rail Enhancement & Accelerated Bridge Programs)) Non-recourse, Underlying Coupon Rate (%) 5.00 | 18.46 | 6/1/2047 | 12,750,000 | b,c,d | 15,475,844 | ||||

30,802,369 | |||||||||

Michigan - 5.8% | |||||||||

Detroit, GO, Ser. A | 5.00 | 4/1/2050 | 2,305,000 | 2,781,980 | |||||

Great Lakes Water Authority Sewage Disposal System, Revenue Bonds, Refunding, Ser. C | 5.00 | 7/1/2036 | 3,000,000 | 3,565,757 | |||||

Michigan Finance Authority, Revenue Bonds (Beaumont Health Credit Obligated Group) | 5.00 | 11/1/2044 | 5,165,000 | 6,021,170 | |||||

Michigan Finance Authority, Revenue Bonds, Refunding (Great Lakes Water Authority) (Insured; Assured Guaranty Municipal Corp.) Ser. C3 | 5.00 | 7/1/2031 | 2,000,000 | 2,243,684 | |||||

17

STATEMENT OF INVESTMENTS (continued)

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Michigan - 5.8% (continued) | |||||||||

Michigan Finance Authority, Revenue Bonds, Refunding (Insured; National Public Finance Guarantee Corp.) Ser. D6 | 5.00 | 7/1/2036 | 2,000,000 | 2,232,633 | |||||

Michigan Finance Authority, Revenue Bonds, Refunding, Ser. A2 | 5.00 | 6/1/2040 | 4,435,000 | 5,649,710 | |||||

Michigan Finance Authority, Revenue Bonds, Refunding, Ser. D2 | 5.00 | 7/1/2034 | 2,000,000 | 2,306,366 | |||||

Tender Option Bond Trust Receipts (Series 2019-XF2837), (Michigan State Finance Authority, Revenue Bonds (Henry Ford Health System)) Recourse, Underlying Coupon Rate (%) 4.00 | 14.30 | 11/15/2050 | 5,840,000 | b,c,d | 6,626,840 | ||||

31,428,140 | |||||||||

Minnesota - .7% | |||||||||

Duluth Economic Development Authority, Revenue Bonds, Refunding (Essentia Health Obligated Group) Ser. A | 5.00 | 2/15/2058 | 3,000,000 | 3,546,473 | |||||

Mississippi - 1.0% | |||||||||

Mississippi Development Bank, Revenue Bonds, Refunding (Magnolia Regional Health Center Project) Ser. A | 6.50 | 10/1/2031 | 5,500,000 | 5,517,257 | |||||

Missouri - 3.3% | |||||||||

Kansas City Industrial Development Authority, Revenue Bonds, Ser. A | 5.00 | 3/1/2044 | 1,000,000 | 1,211,224 | |||||

St. Louis County Industrial Development Authority, Revenue Bonds (Friendship Village St. Louis Obligated Group) Ser. A | 5.13 | 9/1/2049 | 2,975,000 | 3,336,632 | |||||

St. Louis County Industrial Development Authority, Revenue Bonds (Friendship Village St. Louis Obligated Group) Ser. A | 5.13 | 9/1/2048 | 2,025,000 | 2,271,964 | |||||

St. Louis Land Clearance for Redevelopment Authority, Revenue Bonds | 5.13 | 6/1/2046 | 4,760,000 | 5,349,356 | |||||

The Missouri Health & Educational Facilities Authority, Revenue Bonds (Mercy Health) | 4.00 | 6/1/2050 | 2,000,000 | 2,290,250 | |||||

18

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Missouri - 3.3% (continued) | |||||||||

The St. Louis Missouri Industrial Development Authority, Tax Allocation Bonds (St. Louis Innovation District Project) | 4.38 | 5/15/2036 | 3,500,000 | 3,547,313 | |||||

18,006,739 | |||||||||

Multi-State - .5% | |||||||||

Federal Home Loan Mortgage Corp. Multifamily Variable Rate Certificates, Revenue Bonds, Ser. M048 | 3.15 | 1/15/2036 | 2,375,000 | b | 2,633,182 | ||||

Nevada - .9% | |||||||||

Clark County School District, GO (Insured; Assured Guaranty Municipal Corp.) Ser. A | 4.00 | 6/15/2036 | 1,500,000 | 1,776,683 | |||||

Reno, Revenue Bonds, Refunding (Insured; Assured Guaranty Municipal Corp.) | 4.00 | 6/1/2058 | 2,750,000 | 3,012,570 | |||||

4,789,253 | |||||||||

New Hampshire - .2% | |||||||||

New Hampshire Business Finance Authority, Revenue Bonds, Refunding (Green Bond) Ser. B | 3.75 | 7/2/2040 | 1,000,000 | b,g | 1,058,682 | ||||

New Jersey - 4.8% | |||||||||

New Jersey, GO (COVID-19 Emergency Bonds) Ser. A | 4.00 | 6/1/2031 | 1,000,000 | 1,229,695 | |||||

New Jersey Economic Development Authority, Revenue Bonds, Refunding, Ser. XX | 5.25 | 6/15/2027 | 4,000,000 | 4,659,898 | |||||

New Jersey Housing & Mortgage Finance Agency, Revenue Bonds, Refunding, Ser. D | 4.00 | 4/1/2025 | 1,560,000 | 1,714,249 | |||||

New Jersey Transportation Trust Fund Authority, Revenue Bonds | 5.00 | 6/15/2046 | 1,775,000 | 2,162,011 | |||||

New Jersey Transportation Trust Fund Authority, Revenue Bonds | 5.25 | 6/15/2043 | 2,000,000 | 2,488,094 | |||||

New Jersey Transportation Trust Fund Authority, Revenue Bonds, Ser. AA | 5.25 | 6/15/2033 | 1,500,000 | 1,742,996 | |||||

New Jersey Turnpike Authority, Revenue Bonds, Ser. A | 4.00 | 1/1/2051 | 3,000,000 | 3,475,710 | |||||

Tender Option Bond Trust Receipts (Series 2018-XF2538), (New Jersey Economic Development Authority, Revenue Bonds) Recourse, Underlying Coupon Rate (%) 5.25 | 18.64 | 6/15/2040 | 3,250,000 | b,c,d | 3,725,675 | ||||

19

STATEMENT OF INVESTMENTS (continued)

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

New Jersey - 4.8% (continued) | |||||||||

Tobacco Settlement Financing Corp., Revenue Bonds, Refunding, Ser. A | 5.25 | 6/1/2046 | 750,000 | 905,383 | |||||

Tobacco Settlement Financing Corp., Revenue Bonds, Refunding, Ser. B | 5.00 | 6/1/2046 | 3,410,000 | 3,998,198 | |||||

26,101,909 | |||||||||

New York - 7.9% | |||||||||

Monroe County Industrial Development Corp., Revenue Bonds, Refunding (University of Rochester Project) Ser. A | 4.00 | 7/1/2050 | 1,500,000 | 1,731,216 | |||||

New York City, GO, Ser. D1 | 4.00 | 3/1/2050 | 5,040,000 | 5,752,189 | |||||

New York Convention Center Development Corp., Revenue Bonds (Insured; Assured Guaranty Municipal Corp.) Ser. B | 0.00 | 11/15/2049 | 6,885,000 | f | 3,209,474 | ||||

New York Liberty Development Corp., Revenue Bonds, Refunding (Class 1-3 World Trade Center Project) | 5.00 | 11/15/2044 | 7,000,000 | b | 7,670,774 | ||||

New York State Dormitory Authority, Revenue Bonds, Refunding (Montefiore Obligated Group) Ser. A | 4.00 | 9/1/2045 | 1,000,000 | 1,127,599 | |||||

New York State Thruway Authority, Revenue Bonds, Refunding, Ser. A1 | 4.00 | 3/15/2053 | 2,600,000 | 2,977,461 | |||||

New York Transportation Development Corp., Revenue Bonds (LaGuardia Airport Terminal B Redevelopment Project) Ser. A | 5.25 | 1/1/2050 | 3,500,000 | 3,902,905 | |||||

New York Transportation Development Corp., Revenue Bonds, Refunding (JFK International Air Terminal) Ser. A | 4.00 | 12/1/2039 | 1,475,000 | 1,673,714 | |||||

Niagara Area Development Corp., Revenue Bonds, Refunding (Covanta Holding Project) Ser. A | 4.75 | 11/1/2042 | 2,000,000 | b | 2,090,816 | ||||

Port Authority of New York & New Jersey, Revenue Bonds, Refunding, Ser. 223 | 4.00 | 7/15/2046 | 3,000,000 | 3,442,176 | |||||

Tender Option Bond Trust Receipts (Series 2020-XM0826), (Metropolitan Transportation Authority, Revenue Bonds, Refunding (Green Bond) (Insured; Assured Guaranty Municipal Corp., Ser. C)) Non-recourse, Underlying Coupon Rate (%) 4.00 | 14.25 | 11/15/2046 | 7,045,000 | b,c,d | 8,101,772 | ||||

20

Description | Coupon | Maturity Date | Principal Amount ($) |

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

New York - 7.9% (continued) | |||||||||

TSASC, Revenue Bonds, Refunding, Ser. B | 5.00 | 6/1/2045 | 1,165,000 | 1,279,974 | |||||

42,960,070 | |||||||||

North Carolina - 2.9% | |||||||||

North Carolina Medical Care Commission, Revenue Bonds, Refunding (Lutheran Services for the Aging Obligated Group) | 4.00 | 3/1/2051 | 3,000,000 | 3,251,949 | |||||

North Carolina Medical Care Commission, Revenue Bonds, Refunding (Pennybyrn at Maryfield Obligated Group) | 5.00 | 10/1/2035 | 1,005,000 | 1,070,407 | |||||

Tender Option Bond Trust Receipts (Series 2019-XF0792), (North Carolina Medical Care Commission, Revenue Bonds, Ser. A) Non-recourse, Underlying Coupon Rate (%) 4.00 | 14.55 | 11/1/2049 | 10,000,000 | b,c,d | 11,496,358 | ||||

15,818,714 | |||||||||

Ohio - 9.9% | |||||||||

Buckeye Tobacco Settlement Financing Authority, Revenue Bonds, Refunding, Ser. A2 | 4.00 | 6/1/2048 | 1,250,000 | 1,391,013 | |||||

Buckeye Tobacco Settlement Financing Authority, Revenue Bonds, Refunding, Ser. B2 | 5.00 | 6/1/2055 | 14,250,000 | 16,142,387 | |||||

Canal Winchester Local School District, GO, Refunding (Insured; National Public Finance Guarantee Corp.) | 0.00 | 12/1/2031 | 3,955,000 | f | 3,293,149 | ||||

Canal Winchester Local School District, GO, Refunding (Insured; National Public Finance Guarantee Corp.) | 0.00 | 12/1/2029 | 3,955,000 | f | 3,485,809 | ||||

Cuyahoga County, Revenue Bonds, Refunding (The MetroHealth System) | 5.00 | 2/15/2052 | 2,000,000 | 2,319,939 | |||||

Franklin County Convention Facilities Authority, Revenue Bonds (GRTR Columbus Convention Center) | 5.00 | 12/1/2044 | 1,250,000 | 1,451,604 | |||||

Muskingum County, Revenue Bonds (Genesis HealthCare System Project) | 5.00 | 2/15/2022 | 4,590,000 | 4,654,384 | |||||

Ohio Air Quality Development Authority, Revenue Bonds (Pratt Paper OH Project) | 4.50 | 1/15/2048 | 2,250,000 | b | 2,607,738 | ||||

21

STATEMENT OF INVESTMENTS (continued)

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Ohio - 9.9% (continued) | |||||||||

Tender Option Bond Trust Receipts (Series 2016-XM0380), (Hamilton County, Revenue Bonds, Refunding (The Metropolitan Sewer District of Greater Cincinnati)) Non-recourse, Underlying Coupon Rate (%) 5.00 | 18.16 | 12/1/2038 | 17,000,000 | b,c,d | 18,531,512 | ||||

53,877,535 | |||||||||

Oklahoma - .3% | |||||||||

Oklahoma Development Finance Authority, Revenue Bonds (OU Medicine Project) Ser. B | 5.25 | 8/15/2048 | 1,500,000 | 1,808,989 | |||||

Oregon - .6% | |||||||||

Clackamas County Hospital Facility Authority, Revenue Bonds, Refunding (Senior Living-Willamette View Project) Ser. A | 5.00 | 11/15/2047 | 1,500,000 | 1,645,470 | |||||

Yamhill County Hospital Authority, Revenue Bonds, Refunding (Friendsview Manor Obligated Group) Ser. A | 5.00 | 11/15/2036 | 1,220,000 | 1,459,838 | |||||

3,105,308 | |||||||||

Pennsylvania - 3.2% | |||||||||

Allentown School District, GO, Refunding (Insured; Build America Mutual) Ser. B | 5.00 | 2/1/2031 | 1,500,000 | 1,907,416 | |||||

Crawford County Hospital Authority, Revenue Bonds, Refunding (Meadville Medical Center Project) Ser. A | 6.00 | 6/1/2046 | 1,175,000 | 1,309,408 | |||||

Pennsylvania Higher Educational Facilities Authority, Revenue Bonds, Refunding (University of Sciences) | 5.00 | 11/1/2036 | 3,675,000 | 4,139,648 | |||||

Pennsylvania Turnpike Commission, Revenue Bonds, Ser. A | 4.00 | 12/1/2050 | 1,500,000 | 1,730,417 | |||||

Pennsylvania Turnpike Commission, Revenue Bonds, Ser. B | 4.00 | 12/1/2051 | 1,500,000 | 1,724,987 | |||||

Philadelphia Water & Wastewater, Revenue Bonds, Refunding | 5.00 | 10/1/2033 | 1,250,000 | 1,648,484 | |||||

Philadelphia Water & Wastewater, Revenue Bonds, Ser. A | 5.00 | 11/1/2050 | 1,500,000 | 1,872,663 | |||||

The Philadelphia School District, GO (Insured; State Aid Withholding) Ser. A | 4.00 | 9/1/2036 | 2,740,000 | 3,191,584 | |||||

17,524,607 | |||||||||

22

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Rhode Island - 1.6% | |||||||||

Providence Public Building Authority, Revenue Bonds (Insured; Assured Guaranty Municipal Corp.) Ser. A | 5.00 | 9/15/2038 | 7,035,000 | 8,647,449 | |||||

South Carolina - 3.2% | |||||||||

South Carolina Jobs-Economic Development Authority, Revenue Bonds (Bishop Gadsden Episcopal Retirement Community Obligated Group) | 5.00 | 4/1/2054 | 1,000,000 | 1,134,210 | |||||

Tender Option Bond Trust Receipts (Series 2016-XM0384), (South Carolina Public Service Authority, Revenue Bonds, Refunding (Santee Cooper)) Non-recourse, Underlying Coupon Rate (%) 5.13 | 14.03 | 12/1/2043 | 15,000,000 | b,c,d | 16,342,091 | ||||

17,476,301 | |||||||||

Tennessee - 1.0% | |||||||||

Tender Option Bond Trust Receipts (Series 2016-XM0388), (Metropolitan Government of Nashville & Davidson County, Revenue Bonds, Refunding) Non-recourse, Underlying Coupon Rate (%) 5.00 | 17.95 | 7/1/2040 | 5,000,000 | b,c,d | 5,382,195 | ||||

Texas - 10.2% | |||||||||

Central Texas Regional Mobility Authority, Revenue Bonds | 5.00 | 1/1/2048 | 2,500,000 | 2,968,539 | |||||

Central Texas Regional Mobility Authority, Revenue Bonds, Ser. A | 5.00 | 1/1/2045 | 1,500,000 | 1,714,993 | |||||

Clifton Higher Education Finance Corp., Revenue Bonds (International Leadership) Ser. A | 5.75 | 8/15/2045 | 4,500,000 | 5,124,348 | |||||

Clifton Higher Education Finance Corp., Revenue Bonds (International Leadership) Ser. D | 6.13 | 8/15/2048 | 6,000,000 | 6,908,471 | |||||

Clifton Higher Education Finance Corp., Revenue Bonds (Uplift Education) Ser. A | 4.50 | 12/1/2044 | 2,500,000 | 2,659,749 | |||||

Grand Parkway Transportation Corp., Revenue Bonds, Refunding | 4.00 | 10/1/2049 | 1,000,000 | 1,145,117 | |||||

Harris County-Houston Sports Authority, Revenue Bonds, Refunding (Insured; Assured Guaranty Municipal Corp.) Ser. A | 0.00 | 11/15/2050 | 6,500,000 | f | 1,869,656 | ||||

Mission Economic Development Corp., Revenue Bonds, Refunding (Natgasoline Project) | 4.63 | 10/1/2031 | 1,500,000 | b | 1,577,509 | ||||

23

STATEMENT OF INVESTMENTS (continued)

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Texas - 10.2% (continued) | |||||||||

Tarrant County Cultural Education Facilities Finance Corp., Revenue Bonds, Refunding (MRC Stevenson Oaks Project) | 6.75 | 11/15/2051 | 1,000,000 | 1,176,737 | |||||

Tender Option Bond Trust Receipts (Series 2016-XM0377), (San Antonio, Revenue Bonds) Non-recourse, Underlying Coupon Rate (%) 5.00 | 18.16 | 2/1/2043 | 16,750,000 | b,c,d | 17,768,721 | ||||

Texas Private Activity Bond Surface Transportation Corp., Revenue Bonds (Blueridge Transportation Group) | 5.00 | 12/31/2050 | 1,300,000 | 1,446,963 | |||||

Texas Private Activity Bond Surface Transportation Corp., Revenue Bonds (Segment 3C Project) | 5.00 | 6/30/2058 | 8,930,000 | 10,693,027 | |||||

55,053,830 | |||||||||

U.S. Related - 2.1% | |||||||||

Guam Housing Corp., Revenue Bonds (Insured; Federal Home Loan Mortgage Corp.) Ser. A | 5.75 | 9/1/2031 | 965,000 | 1,005,309 | |||||

Puerto Rico, GO, Refunding (Insured; Assured Guaranty Municipal Corp.) Ser. A | 5.00 | 7/1/2035 | 3,500,000 | 3,534,361 | |||||

Puerto Rico, GO, Refunding, Ser. A | 8.00 | 7/1/2035 | 8,010,000 | h | 6,928,650 | ||||

11,468,320 | |||||||||

Utah - .8% | |||||||||

Utah Charter School Finance Authority, Revenue Bonds, Refunding (Summit Academy) Ser. A | 5.00 | 4/15/2049 | 1,190,000 | 1,396,318 | |||||

Utah Infrastructure Agency, Revenue Bonds, Refunding, Ser. A | 5.00 | 10/15/2037 | 2,345,000 | 2,750,275 | |||||

4,146,593 | |||||||||

Virginia - 3.2% | |||||||||

Chesterfield County Economic Development Authority, Revenue Bonds, Refunding (Brandermill Woods Project) | 5.13 | 1/1/2043 | 2,100,000 | 2,108,559 | |||||

Tender Option Bond Trust Receipts (Series 2018-XM0593), (Hampton Roads Transportation Accountability Commission, Revenue Bonds) Non-recourse, Underlying Coupon Rate (%) 5.50 | 20.50 | 7/1/2057 | 7,500,000 | b,c,d | 9,127,350 | ||||

Virginia Small Business Financing Authority, Revenue Bonds (Transform 66 P3 Project) | 5.00 | 12/31/2056 | 3,380,000 | 4,001,015 | |||||

24

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Virginia - 3.2% (continued) | |||||||||

Virginia Small Business Financing Authority, Revenue Bonds (Transform 66 P3 Project) | 5.00 | 12/31/2052 | 1,620,000 | 1,918,869 | |||||

17,155,793 | |||||||||

Washington - 6.0% | |||||||||

King County School District No. 210, GO (Insured; School Bond Guaranty) | 4.00 | 12/1/2034 | 2,000,000 | 2,344,276 | |||||

Port of Seattle, Revenue Bonds, Ser. D | 5.00 | 5/1/2027 | 4,300,000 | 5,229,636 | |||||

Tender Option Bond Trust Receipts (Series 2018-XM0680), (Washington Convention Center Public Facilities District, Revenue Bonds) Non-recourse, Underlying Coupon Rate (%) 5.00 | 9.12 | 7/1/2058 | 17,000,000 | b,c,d | 20,407,101 | ||||

Washington Housing Finance Commission, Revenue Bonds, Refunding (Presbyterian Retirement Communities Northwest Obligated Group) Ser. A | 5.00 | 1/1/2051 | 3,200,000 | b | 3,471,932 | ||||

Washington Housing Finance Commission, Revenue Bonds, Ser. A1 | 3.50 | 12/20/2035 | 995,359 | 1,149,687 | |||||

32,602,632 | |||||||||

Wisconsin - 2.3% | |||||||||

Public Finance Authority, Revenue Bonds (ACTS Retirement-Life Communities Obligated Group) Ser. A | 5.00 | 11/15/2041 | 1,000,000 | 1,216,578 | |||||

Public Finance Authority, Revenue Bonds (Appalachian State University Project) (Insured; Assured Guaranty Municipal Corp.) Ser. A | 4.00 | 7/1/2059 | 2,050,000 | 2,271,460 | |||||

Public Finance Authority, Revenue Bonds (Roseman University of Health Sciences) | 5.00 | 4/1/2040 | 1,175,000 | b | 1,398,489 | ||||

Public Finance Authority, Revenue Bonds (Southminster Obligated Group) | 5.00 | 10/1/2048 | 2,000,000 | b | 2,198,696 | ||||

Public Finance Authority, Revenue Bonds, Refunding (Blue Ridge Healthcare Obligated Group) Ser. 2020 | 4.00 | 1/1/2045 | 1,835,000 | 2,079,629 | |||||

25

STATEMENT OF INVESTMENTS (continued)

Description | Coupon | Maturity

| Principal

|

| Value ($) | ||||

Long-Term Municipal Investments - 148.9% (continued) | |||||||||

Wisconsin - 2.3% (continued) | |||||||||

Public Finance Authority, Revenue Bonds, Refunding (Mary's Woods at Marylhurst Project) | 5.25 | 5/15/2047 | 750,000 | b | 820,832 | ||||

Wisconsin Health & Educational Facilities Authority, Revenue Bonds, Refunding (St. Camillus Health System Obligated Group) | 5.00 | 11/1/2054 | 2,000,000 | 2,219,428 | |||||

12,205,112 | |||||||||

Total Long-Term

Municipal Investments | 807,284,881 | ||||||||

Total Investments (cost $736,155,663) | 149.2% | 809,176,302 | |||||||

Liabilities, Less Cash and Receivables | (34.7%) | (187,934,576) | |||||||

Preferred Stock, at redemption value | (14.5%) | (78,900,000) | |||||||

Net Assets Applicable to Common Shareholders | 100.0% | 542,341,726 | |||||||

a Zero coupon until a specified date at which time the stated coupon rate becomes effective until maturity.

b Security exempt from registration pursuant to Rule 144A under the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At September 30, 2021, these securities were valued at $379,095,787 or 69.9% of net assets.

c The Variable Rate shall be determined by the Remarketing Agent in its sole discretion based on prevailing market conditions and may, but need not, be established by reference to one or more financial indices.

d Collateral for floating rate borrowings. The coupon rate given represents the current interest rate for the inverse floating rate security.

e Security purchased on a when-issued or delayed basis for which the fund has not taken delivery as of September 30, 2021.

f Security issued with a zero coupon. Income is recognized through the accretion of discount.

g These securities have a put feature; the date shown represents the put date and the bond holder can take a specific action to retain the bond after the put date.

h Non-income producing—security in default.

26

Portfolio Summary (Unaudited) † | Value (%) |

General | 25.9 |

Education | 22.8 |

Medical | 17.7 |

Transportation | 14.8 |

Water | 12.1 |

Nursing Homes | 10.8 |

General Obligation | 9.2 |

Development | 9.1 |

Tobacco Settlement | 6.0 |

Utilities | 5.2 |

Airport | 4.6 |

Power | 4.6 |

School District | 4.2 |

Multifamily Housing | 1.0 |

Single Family Housing | .6 |

Housing | .4 |

Special Tax | .2 |

149.2 |

† Based on net assets.

See notes to financial statements.

27

Summary of Abbreviations (Unaudited) | |||

ABAG | Association of Bay Area Governments | AGC | ACE Guaranty Corporation |

AGIC | Asset Guaranty Insurance Company | AMBAC | American Municipal Bond Assurance Corporation |

BAN | Bond Anticipation Notes | BSBY | Bloomberg Short-Term Bank Yield Index |

CIFG | CDC Ixis Financial Guaranty | COP | Certificate of Participation |

CP | Commercial Paper | DRIVERS | Derivative Inverse Tax-Exempt Receipts |

EFFR | Effective Federal Funds Rate | FGIC | Financial Guaranty Insurance Company |

FHA | Federal Housing Administration | FHLB | Federal Home Loan Bank |

FHLMC | Federal Home Loan Mortgage Corporation | FNMA | Federal National Mortgage Association |

GAN | Grant Anticipation Notes | GIC | Guaranteed Investment Contract |

GNMA | Government National Mortgage Association | GO | General Obligation |

IDC | Industrial Development Corporation | LIBOR | London Interbank Offered Rate |

LOC | Letter of Credit | LR | Lease Revenue |

NAN | Note Anticipation Notes | MFHR | Multi-Family Housing Revenue |

MFMR | Multi-Family Mortgage Revenue | MUNIPSA | Securities Industry and Financial Markets Association Municipal Swap Index Yield |

OBFR | Overnight Bank Funding Rate | PILOT | Payment in Lieu of Taxes |

PRIME | Prime Lending Rate | PUTTERS | Puttable Tax-Exempt Receipts |

RAC | Revenue Anticipation Certificates | RAN | Revenue Anticipation Notes |

RIB | Residual Interest Bonds | SFHR | Single Family Housing Revenue |

SFMR | Single Family Mortgage Revenue | SOFR | Secured Overnight Financing Rate |

TAN | Tax Anticipation Notes | TRAN | Tax and Revenue Anticipation Notes |

U.S. T-Bill | U.S. Treasury Bill Money Market Yield | XLCA | XL Capital Assurance |

See notes to financial statements.

28

STATEMENT OF ASSETS AND LIABILITIES

September 30, 2021

|

|

|

|

|

|

|

|

|

| Cost |

| Value |

|

Assets ($): |

|

|

|

| ||

Investments in securities—See Statement of Investments | 736,155,663 |

| 809,176,302 |

| ||

Cash |

|

|

|

| 799,060 |

|

Interest receivable |

| 10,066,439 |

| |||

Prepaid expenses |

|

|

|

| 26,627 |

|

|

|

|

|

| 820,068,428 |

|

Liabilities ($): |

|

|

|

| ||

Due to BNY Mellon Investment Adviser, Inc. and affiliates—Note 2(b) |

| 341,176 |

| |||

Payable for floating rate notes issued—Note 3 |

| 195,855,737 |

| |||

Payable for investment securities purchased |

| 2,015,160 |

| |||

Interest and expense payable

related to |

| 454,491 |

| |||

Commissions payable—Note 1 |

| 31,362 |

| |||

Dividends payable to Preferred Shareholders |

| 607 |

| |||

Other accrued expenses |

|

|

|

| 128,169 |

|

|

|

|

|

| 198,826,702 |

|

Auction Preferred Stock, Series M,T,W,Th and F, par value $.001 per share (3,156 shares issued and outstanding at $25,000 per share liquidation value)—Note 1 |

| 78,900,000 |

| |||

Net Assets Applicable to Common Shareholders ($) |

|

| 542,341,726 |

| ||

Composition of Net Assets ($): |

|

|

|

| ||

Common Stock, par value, $.001 per share |

|

|

|

| 62,276 |

|

Paid-in capital |

|

|

|

| 492,864,560 |

|

Total distributable earnings (loss) |

|

|

|

| 49,414,890 |

|

Net Assets Applicable to Common Shareholders ($) |

|

| 542,341,726 |

| ||

Shares Outstanding |

|

| ||

(500 million shares authorized) | 62,276,212 |

| ||

Net Asset Value Per Share of Common Stock ($) |

| 8.71 |

| |

|

|

|

|

|

See notes to financial statements. |

|

|

|

|

29

STATEMENT OF OPERATIONS

Year Ended September 30, 2021

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment Income ($): |

|

|

|

| ||

Interest Income |

|

| 31,610,686 |

| ||

Expenses: |

|

|

|

| ||

Management fee—Note 2(a) |

|

| 4,657,022 |

| ||

Interest and expense related to floating rate notes issued—Note 3 |

|

| 1,432,049 |

| ||

Commission fees—Note 1 |

|

| 165,132 |

| ||

Professional fees |

|

| 140,227 |

| ||

Registration fees |

|

| 90,881 |

| ||

Directors’ fees and expenses—Note 2(c) |

|

| 70,751 |

| ||

Shareholder servicing costs |

|

| 46,793 |

| ||

Shareholders’ reports |

|

| 46,044 |

| ||

Custodian fees—Note 2(b) |

|

| 11,138 |

| ||

Chief Compliance Officer fees—Note 2(b) |

|

| 8,442 |

| ||

Miscellaneous |

|

| 38,133 |

| ||

Total Expenses |

|

| 6,706,612 |

| ||

Less—reduction in expenses due to undertaking—Note 2(a) |

|

| (620,936) |

| ||

Less—reduction in fees due to earnings credits—Note 2(b) |

|

| (7,431) |

| ||

Net Expenses |

|

| 6,078,245 |

| ||

Investment Income—Net |

|

| 25,532,441 |

| ||

Realized and Unrealized Gain (Loss) on Investments—Note 3 ($): |

|

| ||||

Net realized gain (loss) on investments | 2,969,621 |

| ||||

Net change in unrealized appreciation (depreciation) on investments | 18,800,839 |

| ||||

Net Realized and Unrealized Gain (Loss) on Investments |

|

| 21,770,460 |

| ||

Dividends to Preferred Shareholders |

|

| (94,802) |

| ||

Net

Increase in Net Assets Applicable to Common |

| 47,208,099 |

| |||

|

|

|

|

|

|

|

See notes to financial statements. | ||||||

30

STATEMENT OF CASH FLOWS

Year Ended September 30, 2021

|

|

|

|

|

| |

|

|

|

|

|

|

|

Cash Flows from Operating Activities ($): |

|

|

|

|

| |

Purchases of portfolio securities |

| (70,902,421) |

|

|

| |

Proceeds from sales of portfolio securities | 97,182,616 |

|

|

| ||

Dividends paid to Preferred Shareholders | (95,927) |

|

|

| ||

Interest receivable |

| 32,554,974 |

|

|

| |

Interest and expense related to floating rate notes issued |

| (1,613,895) |

|

|

| |

Paid to BNY Mellon Investment Adviser, Inc. and affiliates |

| (4,040,501) |

|

|

| |

Operating expenses paid |

| (573,652) |

|

|

| |

Net Cash Provided (or Used) in Operating Activities |

|

|

| 52,511,194 |

| |

Cash Flows from Financing Activities ($): |

|

|

|

|

| |

Dividends paid to Common Shareholders |

| (25,543,727) |

|

|

| |

Decrease in payable for floating rate notes issued |

| (26,700,000) |

|

|

| |

Net Cash Provided (or Used) in Financing Activities |

| (52,243,727) |

| |||

Net Increase (Decrease) in Cash |

| 267,467 |

| |||

Cash at beginning of period |

| 531,593 |

| |||

Cash at End of Period |

| 799,060 |

| |||

Reconciliation of Net Increase (Decrease) in Net Assets Applicable to |

|

|

| |||

| Common Shareholders Resulting from Operations to |

|

|

| ||

| Net Cash Provided (or Used) in Operating Activities ($): |

|

|

| ||

Net Increase in Net Assets Resulting From Operations |

| 47,208,099 |

| |||

Adjustments to Reconcile Net Increase in Net Assets |

|

|

| |||

| Applicable to Common Shareholder Resulting from |

|

|

| ||

| Operations to Net Cash Provided (or Used) in Operating Activities ($): |

|

|

| ||

Decrease in investments in securities at cost |

| 21,295,414 |

| |||

Decrease in interest receivable |

| 944,288 |

| |||

Decrease in prepaid expenses |

| 30,386 |

| |||

Increase in Due to BNY Mellon Investment Adviser, Inc. and affiliates |

| 15,165 |

| |||

Increase in payable for investment securities purchased |

| 2,015,160 |

| |||

Decrease in interest and expense payable related to floating rate notes issued |

| (181,846) |

| |||

Decrease in dividends payable to Preferred Shareholders |

| (1,125) |

| |||

Decrease in Directors' fees and expenses payable |

| (5,122) |

| |||

Decrease in commissions payable and other accrued expenses |

| (8,386) |

| |||

Net change in unrealized (appreciation) depreciation on investments |

| (18,800,839) |

| |||

Net Cash Provided (or Used) in Operating Activities |

| 52,511,194 |

| |||

Supplemental Disclosure Cash Flow Information ($): |

|

|

| |||

Non-cash financing activities: |

|

|

| |||

Reinvestment of dividends |

| 588,440 |

| |||

|

|

|

|

|

|

|

See notes to financial statements. | ||||||

31

STATEMENT OF CHANGES IN NET ASSETS

|

|

|

| Year Ended September 30, | |||||

|

|

|

| 2021 |

| 2020 |

| ||

Operations ($): |

|

|

|

|

|

|

|

| |

Investment income—net |

|

| 25,532,441 |

|

|

| 26,682,006 |

| |

Net realized gain (loss) on investments |

| 2,969,621 |

|

|

| (11,651,577) |

| ||

Net

change in unrealized appreciation |

| 18,800,839 |

|

|

| (7,079,086) |

| ||

Dividends to Preferred Shareholders |

|

| (94,802) |

|

|

| (1,203,179) |

| |

Net Increase

(Decrease) in Net Assets Applicable | 47,208,099 |

|

|

| 6,748,164 |

| |||

Distributions ($): |

| ||||||||

Distributions to Common Shareholders |

|

| (26,132,167) |

|

|

| (26,125,626) |

| |

Capital Stock Transactions ($): |

| ||||||||

Distributions reinvested |

|

| 588,440 |

|

|

| 124,964 |

| |

Increase

(Decrease) in Net Assets | 588,440 |

|

|

| 124,964 |

| |||

Total

Increase (Decrease) in Net Assets | 21,664,372 |

|

|

| (19,252,498) |

| |||

Net Assets Applicable to Common Shareholders ($): |

| ||||||||

Beginning of Period |

|

| 520,677,354 |

|

|

| 539,929,852 |

| |

End of Period |

|

| 542,341,726 |

|

|

| 520,677,354 |

| |

Capital Share Transactions (Common Shares): |

| ||||||||

Shares issued for distributions reinvested |

|

| 66,450 |

|

|

| 14,184 |

| |

Net Increase (Decrease) in Shares Outstanding | 66,450 |

|

|

| 14,184 |

| |||

|

|

|

|

|

|

|

|

|

|

See notes to financial statements. | |||||||||

32

FINANCIAL HIGHLIGHTS

The following table describes the performance for the fiscal periods indicated. Market price total return is calculated assuming an initial investment made at the market price at the beginning of the period, reinvestment of all dividends and distributions at market price during the period, and sale at the market price on the last day of the period. These figures have been derived from the fund’s financial statements and, with respect to common stock, market price data for the fund’s common shares.

Year Ended September 30, | ||||||

| 2021 | 2020 | 2019 | 2018 | 2017 | |

Per Share Data ($): | ||||||

Net asset value, beginning of period | 8.37 | 8.68 | 8.28 | 8.63 | 9.12 | |

Investment Operations: | ||||||

Investment income—neta | .41 | .43 | .45 | .50 | .51 | |

Net

realized and unrealized | .35 | (.30) | .40 | (.42) | (.45) | |

Dividends to Preferred Shareholders from investment income—net | (.00)b | (.02) | (.03) | (.03) | (.03) | |

Total from Investment Operations | .76 | .11 | .82 | .05 | .03 | |

Distributions to | ||||||

Dividends from | (.42) | (.42) | (.42) | (.45) | (.52) | |

Net

asset value resulting from | - | - | - | .05 | - | |

Net asset value, end of period | 8.71 | 8.37 | 8.68 | 8.28 | 8.63 | |

Market value, end of period | 8.70 | 8.28 | 8.58 | 7.50 | 8.79 | |

Market Price Total Return (%) | 10.29 | 1.58 | 20.59 | (9.72) | (.19) | |

33

FINANCIAL HIGHLIGHTS (continued)

Year Ended September 30, | ||||||

| 2021 | 2020 | 2019 | 2018 | 2017 | |

Ratios/Supplemental Data (%): | ||||||

Ratio

of total expenses to average | 1.24 | 1.70 | 1.88 | 1.81 | 1.49 | |

Ratio

of net expenses to average | 1.12 | 1.58 | 1.77 | 1.69 | 1.37 | |

Ratio

of interest and expense | .26 | .73 | .91 | .76 | .39 | |

Ratio

of net investment income | 4.71 | 5.11 | 5.41 | 5.99 | 5.96 | |

Ratio

of total expenses | 1.08 | 1.48 | 1.64 | 1.50 | 1.18 | |

Ratio

of net expenses to | .98 | 1.37 | 1.54 | 1.40 | 1.08 | |

Ratio of interest and expense related to floating rate notes issued to total average net assets | .23 | .63 | .79 | .63 | .31 | |

Ratio

of net investment income | 4.11 | 4.44 | 4.70 | 4.96 | 4.71 | |

Portfolio Turnover Rate | 11.05 | 36.52 | 33.21 | 17.93 | 8.77 | |

Asset Coverage of Preferred Stock, end of period | 787 | 760 | 784 | 753 | 476 | |

Net Assets, applicable to | 542,342 | 520,677 | 539,930 | 514,880 | 535,958 | |

Preferred

Stock Outstanding, | 78,900 | 78,900 | 78,900 | 78,900 | 142,500 | |

Floating

Rate Notes Outstanding, | 195,856 | 222,556 | 246,228 | 229,398 | 148,574 | |

a Based on average common shares outstanding.

b Amount represents less than $.01 per share.

c Does not reflect the effect of dividends to Preferred Shareholders.

See notes to financial statements.

34

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

BNY Mellon Strategic Municipals, Inc. (the “fund”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), is a diversified closed-end management investment company. The fund’s investment objective is to maximize current income exempt from federal income tax to the extent consistent with the preservation of capital. BNY Mellon Investment Adviser, Inc. (the “Adviser”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser. Effective September 1, 2021 (the “Effective Date”), the Adviser has engaged its affiliate, Insight North America LLC (the “Sub-Adviser”) as the fund’s sub-investment adviser pursuant to a sub-investment advisory agreement between the Adviser and Sub-Adviser. As the fund’s sub-investment adviser, the Sub-Adviser provides the day-to-day management of the fund’s investments, subject to the Adviser’s supervision and approval. The Adviser (and not the fund) pays the Sub-Adviser for its sub-advisory services. As of the Effective Date, portfolio managers responsible for managing the fund’s investments who were employees of Mellon Investments Corporation (“Mellon”) in a dual employment arrangement with the Adviser, have become employees of the Sub-Adviser, and are no longer employees of Mellon. The fund’s Common Stock trades on the New York Stock Exchange (the “NYSE”) under the ticker symbol LEO.