false2022FY0000811532P5Yhttp://fasb.org/us-gaap/2022#OtherAccruedLiabilitiesCurrenthttp://www.cedarfair.com/20221231#GainLossOnRetirementAndImpairmentOfPropertyPlantAndEquipmentP5Y6Mhttp://fasb.org/us-gaap/2022#DerivativeLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2022#DerivativeLiabilitiesNoncurrentP3Y0M0D00008115322022-01-012022-12-3100008115322022-06-24iso4217:USD00008115322023-02-10xbrli:shares00008115322022-12-3100008115322021-12-310000811532us-gaap:AdmissionMember2022-01-012022-12-310000811532us-gaap:AdmissionMember2021-01-012021-12-310000811532us-gaap:AdmissionMember2020-01-012020-12-310000811532fun:FoodMerchandiseandGamingMember2022-01-012022-12-310000811532fun:FoodMerchandiseandGamingMember2021-01-012021-12-310000811532fun:FoodMerchandiseandGamingMember2020-01-012020-12-310000811532fun:AccommodationsExtraChargeProductsandOtherMember2022-01-012022-12-310000811532fun:AccommodationsExtraChargeProductsandOtherMember2021-01-012021-12-310000811532fun:AccommodationsExtraChargeProductsandOtherMember2020-01-012020-12-3100008115322021-01-012021-12-3100008115322020-01-012020-12-31iso4217:USDxbrli:shares0000811532us-gaap:LimitedPartnerMember2019-12-310000811532us-gaap:GeneralPartnerMember2019-12-310000811532fun:SpecialLPInterestsMember2019-12-310000811532us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-3100008115322019-12-310000811532us-gaap:LimitedPartnerMember2020-01-012020-12-310000811532us-gaap:GeneralPartnerMember2020-01-012020-12-3100008115322020-12-310000811532us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310000811532us-gaap:LimitedPartnerMember2020-12-310000811532us-gaap:GeneralPartnerMember2020-12-310000811532fun:SpecialLPInterestsMember2020-12-310000811532us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310000811532us-gaap:LimitedPartnerMember2021-01-012021-12-310000811532us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310000811532us-gaap:LimitedPartnerMember2021-12-310000811532us-gaap:GeneralPartnerMember2021-12-310000811532fun:SpecialLPInterestsMember2021-12-310000811532us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310000811532us-gaap:LimitedPartnerMember2022-01-012022-12-310000811532us-gaap:GeneralPartnerMember2022-01-012022-12-310000811532us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310000811532us-gaap:LimitedPartnerMember2022-12-310000811532us-gaap:GeneralPartnerMember2022-12-310000811532fun:SpecialLPInterestsMember2022-12-310000811532us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310000811532fun:CedarFairManagementIncMember2022-01-012022-12-31xbrli:purefun:property00008115322022-09-262022-12-3100008115322021-09-272021-12-31fun:segment0000811532us-gaap:LandImprovementsMember2022-01-012022-12-310000811532us-gaap:BuildingMembersrt:MinimumMember2022-01-012022-12-310000811532us-gaap:BuildingMembersrt:MaximumMember2022-01-012022-12-310000811532fun:RidesMembersrt:MinimumMember2022-01-012022-12-310000811532fun:RidesMembersrt:MaximumMember2022-01-012022-12-310000811532srt:MinimumMemberus-gaap:EquipmentMember2022-01-012022-12-310000811532srt:MaximumMemberus-gaap:EquipmentMember2022-01-012022-12-310000811532srt:MinimumMember2022-01-012022-12-310000811532srt:MaximumMember2022-01-012022-12-310000811532fun:InParkRevenuesMember2022-01-012022-12-310000811532fun:InParkRevenuesMember2021-01-012021-12-310000811532fun:InParkRevenuesMember2020-01-012020-12-310000811532fun:OutofParkRevenuesMember2022-01-012022-12-310000811532fun:OutofParkRevenuesMember2021-01-012021-12-310000811532fun:OutofParkRevenuesMember2020-01-012020-12-3100008115322022-01-010000811532fun:PandemicCOVID19Memberfun:NonCurrentDeferredRevenueMember2022-12-31fun:monthlyInstallment0000811532fun:CaliforniasGreatAmericaMember2022-06-272022-06-270000811532us-gaap:LandMember2022-06-270000811532us-gaap:OtherMachineryAndEquipmentMember2022-06-272022-06-2700008115322022-06-272022-06-270000811532fun:SchlitterbahnMember2020-01-012020-03-2900008115322020-01-012020-03-290000811532us-gaap:TradeNamesMemberfun:CaliforniasGreatAmericaMember2022-06-260000811532us-gaap:TradeNamesMemberfun:CaliforniasGreatAmericaMember2022-03-282022-06-260000811532us-gaap:TradeNamesMember2022-06-262022-06-260000811532fun:SchlitterbahnMember2022-09-260000811532fun:SchlitterbahnMember2022-12-310000811532fun:SchlitterbahnMember2020-01-012020-03-290000811532fun:DorneyParkMember2020-01-012020-03-290000811532us-gaap:TradeNamesMemberfun:SchlitterbahnMember2020-01-012020-03-290000811532fun:SchlitterbahnMember2020-06-292020-09-270000811532fun:DorneyParkMember2020-06-292020-09-270000811532us-gaap:TradeNamesMemberfun:SchlitterbahnMember2020-06-292020-09-270000811532fun:CaliforniasGreatAmericaMemberus-gaap:TradeNamesMember2022-01-012022-12-310000811532fun:CaliforniasGreatAmericaMemberus-gaap:TradeNamesMember2022-12-310000811532fun:LicenseAndFranchiseAgreementsMember2022-01-012022-12-310000811532fun:LicenseAndFranchiseAgreementsMember2022-12-310000811532us-gaap:TradeNamesMember2021-12-310000811532fun:LicenseAndFranchiseAgreementsMember2021-01-012021-12-310000811532fun:LicenseAndFranchiseAgreementsMember2021-12-310000811532fun:A2017CreditAgreementMemberfun:SeniorSecuredTermLoanMember2022-01-012022-12-310000811532fun:A2017CreditAgreementMemberfun:SeniorSecuredTermLoanMember2021-01-012021-12-310000811532fun:A2017CreditAgreementMemberfun:SeniorSecuredTermLoanMember2022-12-310000811532fun:A2017CreditAgreementMemberfun:SeniorSecuredTermLoanMember2021-12-310000811532us-gaap:SecuredDebtMemberfun:A2025SeniorNotesMember2022-12-310000811532us-gaap:SecuredDebtMemberfun:A2025SeniorNotesMember2021-12-310000811532fun:A2027SeniorNotesat5.375Member2022-12-310000811532fun:A2027SeniorNotesat5.375Member2021-12-310000811532fun:A2028NotesIn6500Member2022-12-310000811532fun:A2028NotesIn6500Member2021-12-310000811532fun:A2029SeniorNotesat5.250Member2022-12-310000811532fun:A2029SeniorNotesat5.250Member2021-12-310000811532us-gaap:SecuredDebtMemberfun:A2017CreditAgreementMember2022-01-012022-12-310000811532fun:A2017CreditAgreementMemberus-gaap:SecuredDebtMember2022-06-272022-09-250000811532fun:A2017CreditAgreementMemberfun:SeniorSecuredTermLoanMemberus-gaap:LondonInterbankOfferedRateLIBORMember2017-04-300000811532fun:ThirdAmendment2017CreditAgreementMemberus-gaap:SecuredDebtMemberus-gaap:RevolvingCreditFacilityMember2022-12-310000811532us-gaap:BridgeLoanMemberfun:SecondAmended2017CreditAgreementMember2022-12-310000811532fun:ThirdAmendment2017CreditAgreementMember2022-12-310000811532fun:CanadianDollarOfferedRateCDORMemberfun:ThirdAmendment2017CreditAgreementMember2022-12-310000811532fun:ThirdAmendment2017CreditAgreementMemberfun:SeniorSecuredRevolvingCreditFacilityMember2022-01-012022-12-3100008115322022-04-012022-04-300000811532fun:SecondAmended2017CreditAgreementMember2022-04-300000811532fun:CanadianDollarOfferedRateCDORMemberfun:SecondAmended2017CreditAgreementMember2022-04-300000811532fun:SeniorSecuredRevolvingCreditFacilityMemberfun:SecondAmended2017CreditAgreementMember2022-04-012022-04-300000811532fun:A2017CreditAgreementMemberfun:SeniorSecuredRevolvingCreditFacilityMember2022-12-310000811532fun:A2017CreditAgreementMemberfun:SeniorSecuredRevolvingCreditFacilityMember2021-12-310000811532us-gaap:StandbyLettersOfCreditMember2022-12-310000811532us-gaap:StandbyLettersOfCreditMember2021-12-310000811532us-gaap:SecuredDebtMemberfun:A2025SeniorNotesMember2020-04-300000811532fun:A2017CreditAgreementMemberus-gaap:SecuredDebtMember2020-04-012020-04-300000811532fun:NotesPayabledue2024Member2014-06-300000811532fun:NotesPayabledue2024Member2021-12-172021-12-170000811532fun:NotesPayabledue2024Member2021-09-272021-12-310000811532fun:A2027SeniorNotesat5.375Memberus-gaap:UnsecuredDebtMember2017-04-300000811532us-gaap:UnsecuredDebtMemberfun:A2029SeniorNotesat5.250Member2019-06-300000811532us-gaap:UnsecuredDebtMemberfun:A2029SeniorNotesat5.250Member2019-06-012019-06-300000811532fun:A2028SeniorNotesMemberus-gaap:SecuredDebtMember2020-10-310000811532fun:A2028SeniorNotesMemberus-gaap:SecuredDebtMember2020-10-012020-10-310000811532fun:ThirdAmendment2017CreditAgreementMemberus-gaap:DebtInstrumentRedemptionPeriodOneMemberus-gaap:SecuredDebtMember2022-01-012022-12-310000811532fun:ThirdAmendment2017CreditAgreementMemberus-gaap:DebtInstrumentRedemptionPeriodTwoMemberus-gaap:SecuredDebtMember2022-01-012022-12-310000811532fun:ThirdAmendment2017CreditAgreementMemberus-gaap:DebtInstrumentRedemptionPeriodThreeMemberus-gaap:SecuredDebtMember2022-01-012022-12-310000811532fun:RestrictedPaymentPeriodMember2022-01-012022-12-310000811532us-gaap:CashFlowHedgingMemberfun:InterestRateSwapAt288Member2021-12-31fun:contract0000811532fun:InterestRateSwapat4.63Memberus-gaap:CashFlowHedgingMember2021-12-310000811532fun:ForwardStartingInterestRateSwapMemberus-gaap:CashFlowHedgingMember2021-12-3100008115322022-06-272022-09-250000811532us-gaap:NondesignatedMemberus-gaap:InterestRateSwapMember2022-12-310000811532us-gaap:NondesignatedMemberus-gaap:InterestRateSwapMember2021-12-310000811532fun:A2016OmnibusincentivePlanMember2016-06-300000811532fun:A2008OmnibusIncentivePlanMember2016-06-300000811532fun:CompensationPlansSettableinCashorEquityMemberfun:DeferredUnitsMember2022-01-012022-12-310000811532fun:CompensationPlansSettableinCashorEquityMemberfun:DeferredUnitsMember2021-01-012021-12-310000811532fun:CompensationPlansSettableinCashorEquityMemberfun:DeferredUnitsMember2020-01-012020-12-310000811532fun:CompensationPlansSettableinEquityMemberfun:PerformanceUnitsMember2022-01-012022-12-310000811532fun:CompensationPlansSettableinEquityMemberfun:PerformanceUnitsMember2021-01-012021-12-310000811532fun:CompensationPlansSettableinEquityMemberfun:PerformanceUnitsMember2020-01-012020-12-310000811532fun:CompensationPlansSettableinEquityMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310000811532fun:CompensationPlansSettableinEquityMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310000811532fun:CompensationPlansSettableinEquityMemberus-gaap:RestrictedStockUnitsRSUMember2020-01-012020-12-310000811532fun:PerformanceUnitsMember2022-01-012022-12-310000811532fun:DeferredUnitsMember2021-12-310000811532fun:DeferredUnitsMember2022-01-012022-12-310000811532fun:DeferredUnitsMember2022-12-310000811532fun:CompensationPlansSettableinCashorEquityMemberfun:DeferredUnitsMember2022-12-310000811532fun:PerformanceUnitsMember2021-12-310000811532fun:PerformanceUnitsMember2022-12-31fun:performanceTarget0000811532srt:MinimumMemberfun:PerformanceUnitsMember2022-01-012022-12-310000811532srt:MaximumMemberfun:PerformanceUnitsMember2022-01-012022-12-310000811532fun:CompensationPlansSettableinEquityMemberfun:PerformanceUnitsMember2022-12-310000811532us-gaap:RestrictedStockUnitsRSUMember2021-12-310000811532us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310000811532us-gaap:RestrictedStockUnitsRSUMember2022-12-310000811532us-gaap:ShareBasedCompensationAwardTrancheOneMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310000811532us-gaap:ShareBasedCompensationAwardTrancheTwoMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310000811532us-gaap:ShareBasedCompensationAwardTrancheThreeMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310000811532fun:CompensationPlansSettableinEquityMember2022-12-310000811532fun:OtherAccruedLiabilitiesMemberfun:CompensationPlansSettableinEquityMember2022-12-310000811532us-gaap:OtherLiabilitiesMemberfun:CompensationPlansSettableinEquityMember2022-12-310000811532fun:CompensationPlansSettableinEquityMemberus-gaap:RestrictedStockUnitsRSUMember2022-12-310000811532us-gaap:EmployeeStockOptionMember2021-12-310000811532us-gaap:EmployeeStockOptionMember2022-01-012022-12-310000811532us-gaap:EmployeeStockOptionMember2022-12-310000811532fun:CompensationPlansSettableinEquityMemberfun:A2013and2012optionawardsDomain2022-01-012022-12-310000811532fun:FixedPriceOptionsMemberfun:A2008OmnibusIncentivePlanMember2022-12-310000811532fun:A2016OmnibusincentivePlanMember2022-01-012022-12-3100008115322022-08-03fun:employee0000811532us-gaap:ForeignCountryMember2022-12-310000811532us-gaap:ForeignCountryMember2022-01-012022-12-310000811532us-gaap:StateAndLocalJurisdictionMember2022-12-310000811532country:CAus-gaap:ForeignCountryMember2022-12-310000811532us-gaap:CapitalLossCarryforwardMember2022-12-310000811532us-gaap:StateAndLocalJurisdictionMember2022-01-012022-12-310000811532country:CAus-gaap:ForeignCountryMember2022-01-012022-12-3100008115322022-06-260000811532country:US2022-12-3100008115322022-03-2700008115322022-06-270000811532us-gaap:FairValueInputsLevel1Memberus-gaap:OtherCurrentAssetsMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310000811532us-gaap:FairValueInputsLevel1Memberus-gaap:OtherCurrentAssetsMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310000811532us-gaap:FairValueInputsLevel1Memberus-gaap:OtherCurrentAssetsMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310000811532us-gaap:FairValueInputsLevel1Memberus-gaap:OtherCurrentAssetsMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310000811532us-gaap:FairValueInputsLevel2Memberus-gaap:InterestRateSwapMemberfun:DerivativeLiabilityMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310000811532us-gaap:FairValueInputsLevel2Memberus-gaap:InterestRateSwapMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberfun:DerivativeLiabilityMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310000811532us-gaap:FairValueInputsLevel2Memberus-gaap:InterestRateSwapMemberfun:DerivativeLiabilityMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310000811532us-gaap:FairValueInputsLevel2Memberus-gaap:InterestRateSwapMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberfun:DerivativeLiabilityMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310000811532fun:A2017CreditAgreementMemberus-gaap:FairValueInputsLevel2Memberus-gaap:LongTermDebtMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310000811532fun:A2017CreditAgreementMemberus-gaap:FairValueInputsLevel2Memberus-gaap:LongTermDebtMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310000811532fun:A2017CreditAgreementMemberus-gaap:FairValueInputsLevel2Memberus-gaap:LongTermDebtMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310000811532fun:A2017CreditAgreementMemberus-gaap:FairValueInputsLevel2Memberus-gaap:LongTermDebtMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310000811532us-gaap:FairValueInputsLevel2Memberus-gaap:LongTermDebtMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberfun:A2025SeniorNotesMember2022-12-310000811532us-gaap:FairValueInputsLevel2Memberus-gaap:LongTermDebtMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMemberfun:A2025SeniorNotesMember2022-12-310000811532us-gaap:FairValueInputsLevel2Memberus-gaap:LongTermDebtMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberfun:A2025SeniorNotesMember2021-12-310000811532us-gaap:FairValueInputsLevel2Memberus-gaap:LongTermDebtMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMemberfun:A2025SeniorNotesMember2021-12-310000811532us-gaap:FairValueInputsLevel1Memberfun:A2027SeniorNotesat5.375Memberus-gaap:LongTermDebtMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310000811532us-gaap:FairValueInputsLevel1Memberfun:A2027SeniorNotesat5.375Memberus-gaap:LongTermDebtMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310000811532us-gaap:FairValueInputsLevel1Memberfun:A2027SeniorNotesat5.375Memberus-gaap:LongTermDebtMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310000811532us-gaap:FairValueInputsLevel1Memberfun:A2027SeniorNotesat5.375Memberus-gaap:LongTermDebtMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310000811532us-gaap:FairValueInputsLevel1Memberus-gaap:LongTermDebtMemberfun:A2028NotesIn6500Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310000811532us-gaap:FairValueInputsLevel1Memberus-gaap:LongTermDebtMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberfun:A2028NotesIn6500Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310000811532us-gaap:FairValueInputsLevel1Memberus-gaap:LongTermDebtMemberfun:A2028NotesIn6500Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310000811532us-gaap:FairValueInputsLevel1Memberus-gaap:LongTermDebtMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberfun:A2028NotesIn6500Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310000811532us-gaap:FairValueInputsLevel1Memberus-gaap:LongTermDebtMemberfun:A2029SeniorNotesat5.250Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310000811532us-gaap:FairValueInputsLevel1Memberus-gaap:LongTermDebtMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberfun:A2029SeniorNotesat5.250Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310000811532us-gaap:FairValueInputsLevel1Memberus-gaap:LongTermDebtMemberfun:A2029SeniorNotesat5.250Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310000811532us-gaap:FairValueInputsLevel1Memberus-gaap:LongTermDebtMemberus-gaap:EstimateOfFairValueFairValueDisclosureMemberfun:A2029SeniorNotesat5.250Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310000811532us-gaap:SecuredDebtMemberus-gaap:SubsequentEventMemberfun:A2025SeniorNotesMember2023-02-100000811532us-gaap:SecuredDebtMemberfun:A2027SeniorNotesMemberus-gaap:SubsequentEventMember2023-02-100000811532fun:SecuredOvernightFinancingRateSOFRMemberfun:ThirdAmendment2017CreditAgreementMemberus-gaap:SubsequentEventMember2023-02-102023-02-10

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| | | | | |

| ☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: December 31, 2022

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number 1-9444

CEDAR FAIR, L.P.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 34-1560655 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer

Identification No.) |

One Cedar Point Drive, Sandusky, Ohio 44870-5259

(Address of principal executive offices) (Zip Code)

(419) 626-0830

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Depositary Units (Representing

Limited Partner Interests) | FUN | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☑ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

☐ Yes ☑ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☑ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☑ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | | ☑ | | Accelerated filer | | ☐ |

| | | |

| Non-accelerated filer | | ☐ | | Smaller reporting company | | ☐ |

| | | | | | |

| | | | Emerging growth company | | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☑ No

The aggregate market value of Depositary Units held by non-affiliates of the Registrant based on the closing price of such units on June 24, 2022 of $42.80 per unit was approximately $2,404,874,220.

Number of Depositary Units representing limited partner interests outstanding as of February 10, 2023: 51,930,650 units

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Form 10-K incorporates by reference certain information from the Registrant's definitive proxy statement to be used in connection with its annual meeting of limited partner unitholders to be held in May 2023.

************

Page 1 of 59 pages

CEDAR FAIR, L.P.

2022 FORM 10-K CONTENTS

PART I

Unless the context otherwise indicates, all references to "we," "us," "our," or the "Partnership" in this Annual Report on Form 10-K refer to Cedar Fair, L.P. together with its affiliated companies.

ITEM 1. BUSINESS.

We are one of the largest regional amusement park operators in the world with 13 properties in our portfolio consisting of amusement parks, water parks and complementary resort facilities. We are a publicly traded Delaware limited partnership formed in 1987 and managed by Cedar Fair Management, Inc., an Ohio corporation (the "General Partner"), whose shares are held by an Ohio trust. Our parks are family-oriented, with recreational facilities for people of all ages, and provide clean and attractive environments with exciting rides and immersive entertainment. We generate revenue from sales of admission to our amusement parks and water parks, from purchases of food, merchandise and games both inside and outside our parks, and from the sale of accommodations and other extra-charge products.

Our parks operate seasonally except for Knott's Berry Farm, which is typically open daily on a year-round basis. Our seasonal parks are generally open daily from Memorial Day until Labor Day. Outside of daily operations, our seasonal parks are open during select weekends, including at most properties in the fourth quarter for Halloween and winter events. As a result, a substantial portion of our revenues from these seasonal parks are generated from Memorial Day through Labor Day with the major portion concentrated during the peak vacation months of July and August.

The demographic groups that are most important to our business are families and young people ages 12 through 24. Families are believed to be attracted by a combination of rides, live entertainment and the clean, wholesome atmosphere. Young people are believed to be attracted by the action-packed rides. We conduct active television, radio, newspaper and internet advertising campaigns in our major market areas geared toward these two groups.

IMPACT OF COVID-19 PANDEMIC

The novel coronavirus (COVID-19) pandemic had a material impact on our business in 2020, had a continuing negative impact in 2021 and may have a longer-term negative effect. Beginning on March 14, 2020, we closed our properties for several months in response to the spread of COVID-19 and local government mandates. We ultimately resumed partial operations at 10 of our 13 properties in 2020, operating in accordance with local and state guidelines. We delayed the opening of our U.S. properties for the 2021 operating season until May 2021 and opened our Canadian property in July 2021. Upon opening in 2021, we operated with capacity restrictions, guest reservations, and other operating protocols in place. As vaccination distribution efforts continued during the second quarter of 2021 and we were able to hire additional labor, we removed most capacity restrictions, guest reservation requirements and other protocols at our U.S. properties beginning in July 2021. Canada's Wonderland operated with capacity restrictions, guest reservations, and other operating protocols in place throughout 2021.

Each of our properties opened for the 2022 operating season as planned and without restrictions. We currently anticipate continuing to operate without restrictions for the 2023 operating season. However, we have and may continue to adjust future park operating calendars as we respond to changes in guest demand, labor availability and any federal, provincial, state and local restrictions. Our future operations are dependent on factors beyond our knowledge or control, including any future actions taken to contain the COVID-19 pandemic and changing risk tolerances of our employees and guests regarding health matters.

DESCRIPTION OF OUR PARKS

Cedar Point

Cedar Fair's flagship park, Cedar Point, was first developed as a recreational area in 1870. Located on a peninsula in Sandusky, Ohio bordered by Lake Erie between Cleveland and Toledo, Cedar Point serves a six-state region which includes nearly all of Ohio and Michigan, western Pennsylvania and New York, northern West Virginia and Indiana, as well as southwestern Ontario, Canada. Attractive to both families and thrill-seekers, the park features 18 roller coasters, including many record-breakers, and three children's areas. Located adjacent to the park is Cedar Point Shores Water Park, a separately gated water park featuring more than 15 water rides and attractions. Cedar Point also features four hotels, three marinas, an upscale campground, and the nearby Cedar Point Sports Center which features both indoor and outdoor sports facilities. Cedar Point's four hotels include:

Hotel Breakers - the park's largest hotel and only hotel located on the Cedar Point peninsula, featuring various dining and lounge facilities, a mile-long beach, lake swimming, a conference/meeting center, an indoor pool and multiple outdoor pools;

Castaway Bay Indoor Waterpark Resort - a year-round hotel located adjacent to the entrance to the park featuring tropical, Caribbean themed hotel rooms centered around an indoor water park, as well as a marina and dining facilities;

Cedar Point's Express Hotel - a limited-service seasonal hotel located adjacent to the entrance to the park; and

Sawmill Creek Resort - a year-round resort lodge located near Cedar Point in Huron, Ohio, featuring a golf course, marina, half-mile beach, dining and shopping facilities, and a conference/meeting center.

Knott's Berry Farm

Knott's Berry Farm, located near Los Angeles in Buena Park, California, first opened in 1920 and was acquired by the Partnership in 1997. The park is one of several year-round theme parks in Southern California and serves a market area centered in Orange County with a large national and international tourism population. The park is renowned for its seasonal events, including a spring culinary festival, Boysenberry Festival; a special holiday event, Knott's Merry Farm; and a Halloween event, Knott's Scary Farm, which has been held for nearly 50 years and is annually rated one of the best Halloween events in the industry by Amusement Today's international survey. Adjacent to Knott's Berry Farm is Knott's Soak City, a separately gated seasonal water park that features multiple water rides and attractions. Knott's Berry Farm also features the Knott's Berry Farm Hotel, a full-service hotel located adjacent to Knott's Berry Farm featuring a pool, fitness facilities and meeting/banquet facilities.

Canada's Wonderland

Canada's Wonderland, a combination amusement and water park located near Toronto in Vaughan, Ontario, first opened in 1981 and was acquired by the Partnership in 2006. It contains numerous attractions, including 18 roller coasters, and is one of the most attended amusement parks in North America. Canada's Wonderland is in a culturally diverse metropolitan market with large populations of different ethnicities and national origins. Each year the park showcases an extensive entertainment and special event line-up which includes cultural festivals.

Kings Island

Kings Island, a combination amusement and water park located near Cincinnati, Ohio, first opened in 1972 and was acquired by the Partnership in 2006. Kings Island is also one of the most attended amusement parks in North America. The park features a children's area that has been consistently named one of the "Best Kids' Area in the World" by Amusement Today. The park's market area includes Cincinnati, Dayton and Columbus, Ohio; Louisville and Lexington, Kentucky; and Indianapolis, Indiana.

Carowinds

Carowinds, a combination amusement and water park located in Charlotte, North Carolina, first opened in 1973 and was acquired by the Partnership in 2006. Carowinds' major markets include Charlotte, Greensboro, and Raleigh, North Carolina; as well as Greenville and Columbia, South Carolina. The park also features Camp Wilderness Resort, an upscale campground, and a SpringHill Suites by Marriott hotel located adjacent to the park entrance. The SpringHill Suites is a Marriott franchise operated by Cedar Fair. The hotel is open year-round and features suites, an outdoor pool, fitness center and bar.

Kings Dominion

Kings Dominion, a combination amusement and water park located near Richmond, Virginia, first opened in 1975 and was acquired by the Partnership in 2006. The park's market area includes Richmond and Norfolk, Virginia; Raleigh, North Carolina; Baltimore, Maryland and Washington, D.C. Additionally, the park offers Kings Dominion Camp Wilderness Campground, an upscale campground.

California's Great America

California's Great America, a combination amusement and water park located in Santa Clara, California, first opened in 1976 and was acquired by the Partnership in 2006. The park draws its visitors primarily from San Jose, San Francisco, Sacramento, Modesto and Monterey, among other cities in northern California. On June 27, 2022, we sold the land at California's Great America. Concurrently with the sale, we entered into a lease contract that allows us to operate the park during a six-year term, and we have an option to extend the term for an additional five years. The lease is subject to early termination by the buyer with at least two years' prior notice.

Dorney Park

Dorney Park, a combination amusement and water park located in Allentown, Pennsylvania, was first developed as a summer resort area in 1884 and was acquired by the Partnership in 1992. Dorney Park's major markets include Philadelphia, Lancaster, Harrisburg, York, Scranton, Wilkes-Barre, Hazleton and the Lehigh Valley, Pennsylvania; New York City; and New Jersey.

Worlds of Fun

Worlds of Fun, which opened in 1973 and was acquired by the Partnership in 1995, is a combination amusement and water park located in Kansas City, Missouri. Worlds of Fun serves a market area centered in Kansas City, as well as most of Missouri and portions of Kansas and Nebraska. Worlds of Fun also features Worlds of Fun Village, an upscale campground.

Valleyfair

Valleyfair, which opened in 1976 and was acquired by the Partnership's predecessor in 1978, is a combination amusement and water park located near Minneapolis-St. Paul in Shakopee, Minnesota. Valleyfair's market area is centered in Minneapolis-St. Paul, but the park also draws visitors from other areas in Minnesota and surrounding states.

Michigan's Adventure

Michigan's Adventure, which opened in 1956 as Deer Park and was acquired by the Partnership in 2001, is a combination amusement and water park located in Muskegon, Michigan. Michigan's Adventure serves a market area principally from central and western Michigan and eastern Indiana.

Schlitterbahn Waterpark & Resort New Braunfels

Schlitterbahn Waterpark & Resort New Braunfels began as a resort in 1966, was introduced as a water park in 1979 and was acquired by the Partnership in 2019. The park is consistently rated the best water park in the industry by Amusement Today's international survey and is one of the most attended water parks in North America. The park, located in New Braunfels, Texas, features many river rides, water slides and attractions along the Comal River. The Resort at Schlitterbahn New Braunfels includes hotel rooms, suites, cabins, luxury suites and vacation homes. Schlitterbahn Waterpark & Resort New Braunfels’ major markets include San Antonio, Austin and Houston, Texas.

Schlitterbahn Waterpark Galveston

Schlitterbahn Waterpark Galveston opened in 2006 and was acquired by the Partnership in 2019. The park is one of the most attended water parks in North America. The park, located in Galveston, Texas, features many water attractions including an award-winning water coaster and a one-mile long river system. Schlitterbahn Waterpark Galveston serves a market area centered in Houston, Texas, as well as the tourism population in Galveston Island, Texas, a barrier island on the Texas Gulf Coast.

CAPITAL EXPENDITURES

We believe that annual park attendance is influenced by annual investments in our properties, including new attractions and infrastructure, among other factors. Capital expenditures are planned on a seasonal basis with most expenditures made prior to the beginning of the peak operating season. Capital expenditures made in a calendar year may differ materially from amounts identified with a particular operating season because of timing considerations such as weather conditions, site preparation requirements and availability of ride components, which may result in accelerated or delayed expenditures around calendar year-end. Due to the effects of the COVID-19 pandemic, some capital expenditures were suspended in 2020 and 2021 in order to maintain flexibility and retain liquidity.

COMPETITION

We compete for discretionary spending with all aspects of the recreation industry within our primary market areas, including other destination and regional amusement parks. We also compete with other forms of entertainment and recreational activities, including movies, sports events, restaurants and vacation travel.

The principal competitive factors in the amusement park industry include the uniqueness and perceived quality of the rides and attractions in a particular park, proximity to metropolitan areas, the atmosphere and cleanliness of the park, and the quality and variety of the food and immersive entertainment available. We believe that our parks feature a variety of high-quality rides and attractions, restaurants, gift shops and family atmosphere to make them highly competitive with other parks and forms of entertainment.

GOVERNMENT REGULATION

Our operations are subject to regulatory requirements, such as those relating to employment practices, environmental requirements, and other regulatory matters. We are subject to extensive federal and state employment laws and regulations, including wage and hour laws and other pay practices and employee record-keeping requirements. We may be required to incur costs to comply with these requirements, and the costs of compliance, investigation, remediation, litigation, and resolution of regulatory matters could be substantial.

We also are subject to federal, state and local environmental laws and regulations such as those relating to water resources; discharges to air, water and land; the handling and disposal of solid and hazardous waste; and the cleanup of properties affected by regulated materials. Under these laws and regulations, we may be required to investigate and clean up hazardous or toxic substances or chemical releases from current or formerly owned or operated facilities or to mitigate potential environmental risks. Environmental laws typically impose cleanup responsibility and liability without regard to whether the relevant entity knew of or caused the presence of the contaminants. The costs of investigation, remediation or removal of regulated materials may be substantial, and the presence of those substances, or the failure to remediate a property properly, may impair our ability to use, transfer or obtain financing with respect to our property.

Currently, we believe we are in substantial compliance with applicable requirements under these laws and regulations. However, such requirements have generally become stricter over time, and there can be no assurance that new requirements, changes in enforcement policies or newly discovered conditions relating to our properties or operations will not require significant expenditures in the future.

All rides are inspected daily by both our maintenance and ride operations personnel before being placed into operation for our guests. The parks are also periodically inspected by our insurance carrier and, at all parks except Valleyfair, Worlds of Fun, Schlitterbahn Waterpark New Braunfels, Schlitterbahn Waterpark Galveston and Carowinds' South Carolina rides, by state or county ride-safety inspectors. Valleyfair, Worlds of Fun, Schlitterbahn Waterpark New Braunfels, Schlitterbahn Waterpark Galveston and Carowinds each contract with a third party to inspect our rides pursuant to Minnesota, Missouri, Texas and South Carolina law, respectively, and submit the third-party report to the respective state agency. Additionally, all parks have added ride maintenance and operation inspections completed by third party qualified inspectors to make sure our standards are being maintained.

HUMAN CAPITAL

We employ approximately 4,400 full-time employees and employed approximately 48,800 seasonal and part-time employees in 2022, many of whom are high school and college students. We house some of our seasonal employees in dormitories owned by us at Cedar Point, Kings Island, Carowinds, Kings Dominion and Valleyfair, or rented by us at Dorney Park, Worlds of Fun, Schlitterbahn Waterpark New Braunfels and Schlitterbahn Waterpark Galveston. Approximately 260 of our employees are represented by labor unions. We believe we maintain good relations with our employees.

Our employee guidelines and policies are founded on our cornerstones of safety, service and cleanliness and our core values of integrity, courtesy and inclusiveness. Our highest priority continues to be the safety and well-being of our guests and employees. We continue to monitor developments of the COVID-19 pandemic, as well as federal, state and local guidelines, and update our safety protocols based on the most recent recommendations and requirements. We are committed to equal opportunity employment and prohibit harassment or discrimination of any kind. We have adopted an open door policy to encourage an honest employer-associate relationship, which includes a confidential hotline available to all employees. As part of our commitment to our core values, we created a diversity, equity and inclusion ("DE&I") council and provided DE&I training to our employees in 2021. In 2022, we published our first Environmental, Social and Governance ("ESG") Strategy Report to establish an enterprise-wide framework to address ESG issues. The framework includes the prioritization of five key strategic pillars: Safety, Associate Happiness, Community, Environment, and Operations and Governance. The report included the introduction of the Associate Happiness Model, focusing on DE&I, and the Cedar Fair Safety Model, focusing on the safety of our employees and guests.

We maintain training programs for new employees, including safety training specific to job responsibilities. We participate in the J-1 Visa program providing cultural and educational exchange opportunities for our associates. We also have partnered with Bowling Green State University to create the Cedar Fair Resort and Attraction Management program, a bachelor's degree program, which is housed in downtown Sandusky, Ohio in a facility jointly owned by the Partnership and a third party developer. The bachelor's degree program prepares students for management careers at Cedar Fair parks or a similar establishment. We encourage a promote-from-within policy.

Our executive compensation program is designed to incentivize our key employees to drive superior results, to give key employees a vested interest in our growth and performance, and to enhance our ability to attract and retain exceptional managerial talent. Our executive compensation program rewards both successful individual performance and the consolidated operating results of the Partnership by directly tying compensation to our performance.

AVAILABLE INFORMATION

Copies of our annual report on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K and all amendments to those reports as filed or furnished with the SEC are available without charge upon written request to our Investor Relations Office or through our website (www.ir.cedarfair.com).

We use our website www.ir.cedarfair.com as a channel of distribution of information. The information we post through this channel may be deemed material. Accordingly, investors should monitor this channel, in addition to following our news releases, SEC filings, and public conference calls and webcasts. The contents of our website, including without limitation the ESG Strategy Report referenced above, shall not be deemed to be incorporated herein by reference.

The SEC maintains an Internet site at http://www.sec.gov that contains our reports, proxy statements and other information.

SUPPLEMENTAL ITEM. Information about our Executive Officers

| | | | | | | | | | | | | | |

| Name | | Age | | Position(s) |

| | | | |

| Richard A. Zimmerman | | 62 | | | Richard Zimmerman has been President and Chief Executive Officer since January 2018 and a member of the Board of Directors since April 2019. Prior to becoming CEO, he served as President and Chief Operating Officer from October 2016 through December 2017 and served as Chief Operating Officer from 2011 through 2016. Prior to that, he was appointed as Executive Vice President in 2010 and as Regional Vice President in 2007. He has been with Cedar Fair since 2006, when Kings Dominion was acquired. Richard served as Vice President and General Manager of Kings Dominion from 1998 through 2006. |

| Brian C. Witherow | | 56 | | | Brian Witherow has served as Executive Vice President and Chief Financial Officer since 2012. Prior to that, he served as Vice President and Corporate Controller beginning in 2005. Brian has been with Cedar Fair in various other positions since 1995. |

| Tim V. Fisher | | 62 | | | Tim Fisher joined Cedar Fair as Chief Operating Officer in December 2017. Prior to joining Cedar Fair, he served as Chief Executive Officer of Village Roadshow Theme Parks International, an Australian-based theme park operator, since March 2017. Prior to this appointment with Village Roadshow Theme Parks International, Tim served as Chief Executive Officer of Village Roadshow Theme Parks since 2009. |

| Brian M. Nurse | | 51 | | | Brian Nurse joined Cedar Fair as Executive Vice President, Chief Legal Officer and Secretary in November 2021. Prior to joining Cedar Fair, he served as Senior Vice President, General Counsel and Secretary for World Wrestling Entertainment, Inc. ("WWE"), an integrated media and entertainment company, from September 2018 to November 2020. Prior to joining WWE, Brian served as Vice President, Associate General Counsel and Secretary at Nestle Waters North America, Inc., a former division of Nestle S.A. which is a multinational food and drink corporation, from 2012 to 2018. Prior to that, he was Senior Legal Counsel for North American beverage/soft drink brands at PepsiCo, Inc., a multinational food, snack and beverage corporation, from 2003 to 2012. |

| Kelley S. Ford | | 58 | | | Kelley Ford has served as Executive Vice President and Chief Marketing Officer since 2012. Prior to joining Cedar Fair, she served as Senior Vice President, Marketing Planning Director for TD Bank from 2010 through 2012. Prior to joining TD Bank, Kelley served as Senior Vice President of Brand Strategy and Management at Bank of America from 2005 through 2010. |

| David R. Hoffman | | 54 | | | Dave Hoffman has served as Senior Vice President and Chief Accounting Officer since 2012. Prior to that, he served as Vice President of Finance and Corporate Tax since 2010. He served as Vice President of Corporate Tax from 2006 through 2010. Prior to joining Cedar Fair, Dave served as a business advisor with Ernst & Young from 2002 through 2006. |

| Charles E. Myers | | 59 | | | Charles Myers joined Cedar Fair as Senior Vice President, Creative Development in June 2019. Prior to joining Cedar Fair, he held a variety of Senior Leadership roles including Show Design, Production Management and Producing at Walt Disney Imagineering, the research and development arm of the Walt Disney Company, from 2013 to June 2019. Prior to this, he served as Senior Vice President, Licensing, Project Development & Business Development of Paramount Pictures from 2002 to 2013. |

ITEM 1A. RISK FACTORS.

Risks Related to the Amusement Park Industry

Instability in economic conditions could impact our business, including our results of operations and financial condition.

Uncertain or deteriorating economic conditions, including during inflationary and recessionary periods, may adversely impact attendance figures and guest spending patterns at our parks as uncertain economic conditions affect our guests' levels of discretionary spending. Both attendance and in-park spending at our parks are key drivers of our revenues and profitability, and reductions in either can directly and negatively affect revenues and profitability. A decrease in discretionary spending due to a decline in consumer confidence in the economy, an economic slowdown or deterioration in the economy could adversely affect the frequency with which our guests choose to attend our parks and the amount that our guests spend on our products when they visit.

Periods of inflation or economic downturn could also impact our ability to obtain supplies and services and increase our operating costs. We continue to see some inflationary effects and supply chain disruptions on our business, which may continue or worsen. In addition, the existence of unfavorable general economic conditions may also hinder the ability of those with which we do business, including vendors, concessionaires and customers, to satisfy their obligations to us. The materialization of these risks could lead to a decrease in our revenues, operating income and cash flows.

The COVID-19 pandemic has adversely impacted our business and may continue to adversely impact our business, as well as intensify certain risks we face, for an unknown length of time.

Since 2020, the COVID-19 pandemic has had a material negative impact on our business. On March 14, 2020, we closed our properties in response to federal and local recommendations and restrictions to mitigate the spread of COVID-19. We were ultimately able to resume partial operations, subject to capacity, social distancing mandates and other governmental restrictions, at 10 of our 13 properties on a staggered basis in 2020. We operated all of our properties in 2021. However, 2021 operating seasons were delayed and certain restrictions remained in place at some of our properties. Each of our properties opened for the 2022 operating season as planned and without restrictions.

Consumer behavior and preferences changed in response to the effects of the COVID-19 pandemic and may remain changed both in the short term and long term, including impacts on discretionary consumer spending due to significant economic uncertainty and changing risk tolerances of our employees and guests regarding health matters. In 2020, we experienced lower demand upon reopening our properties resulting in a material decrease in revenues generated. In 2021 and 2022, attendance improved, but we experienced lower demand at certain times and at certain properties. Future significant volatility or reductions in demand for, or interest in, our parks could materially adversely impact attendance, in-park per capita spending and revenue. In addition, we could experience damage to our brand and reputation due to actual or perceived health risks associated with our parks or the amusement park industry which could have a similar material adverse effect on attendance, in-park per capita spending and revenue. We may also continue to experience operational risks due to the COVID-19 pandemic, including limitations on our ability to recruit and train employees in sufficient numbers to fully staff our parks as a result of changing risk tolerances.

Because our amusement and water parks are the primary sources of net income and operating cash flows, any future mandated or voluntary closures or other operating restrictions would adversely impact our business and financial results. Our parks are geographically located throughout the United States and in Canada. The duration and severity of the COVID-19 pandemic and the related restrictions at any one location could result in a potentially disproportionate amount of risk if concentrated amongst our largest properties.

We have not previously experienced the level of disruption caused by the COVID-19 pandemic. It is difficult for management to estimate future performance under these conditions, and the ultimate impact of the COVID-19 pandemic on our business, results of operations and financial condition cannot be reasonably predicted.

The high fixed cost structure of amusement park operations can result in significantly lower margins, profitability and cash flows if attendance levels do not meet expectations.

A large portion of our expense is relatively fixed because the costs for full-time employees, maintenance, utilities, advertising and insurance do not vary significantly with attendance. These fixed costs may increase and may not be able to be reduced at a rate proportional with ongoing attendance levels. If cost-cutting efforts are insufficient or are impractical, we could experience a material decline in margins, profitability and cash flows. Such effects can be especially pronounced during periods of economic contraction or slow economic growth.

Bad or extreme weather conditions can adversely impact attendance at our parks, which in turn would reduce our revenues.

Because most of the attractions at our parks are outdoors, attendance at our parks can be adversely affected by continuous bad or extreme weather and by forecasts of bad or mixed weather conditions, which would negatively affect our revenues. We believe that our ownership of many parks in different geographic locations reduces, but does not completely eliminate, the effect that adverse weather can have on our consolidated results.

Our insurance coverage may not be adequate to cover all possible losses that we could suffer, and our insurance costs may increase.

Although we carry liability insurance to cover possible incidents, there can be no assurance that our coverage will be adequate to cover liabilities, that we will be able to obtain coverage at commercially reasonable rates, or that we will be able to obtain adequate coverage should a catastrophic incident occur at our parks or at other parks. Companies engaged in the amusement park business may be sued for substantial damages in the event of an actual or alleged incident. An incident occurring at our parks or at competing parks could reduce attendance, increase insurance premiums, and negatively impact our operating results.

Unanticipated construction delays in completing capital improvement projects in our parks and resort facilities, significant ride downtime, or other unplanned park closures could adversely affect our revenues.

A principal competitive factor for an amusement park is the uniqueness and perceived quality of its rides and attractions in a particular market area. Accordingly, the regular addition of new rides and attractions is important, and a key element of our revenue growth is strategic capital spending on new rides and attractions. Any construction delays could adversely affect our attendance and our ability to realize revenue growth. Further, when rides, attractions, or an entire park, have unplanned downtime and/or closures, our revenue could be adversely affected.

There is a risk of accidents or other incidents occurring at amusement and water parks, which may reduce attendance and negatively impact our revenues.

The safety of our guests and employees is one of our top priorities. Our amusement and water parks feature thrill rides. There are inherent risks involved with these attractions, and an accident or a serious injury at any of our parks could result in negative publicity and could reduce attendance and result in decreased revenues. In addition, accidents or injuries at parks operated by our competitors could influence the general attitudes of amusement park patrons and adversely affect attendance at our parks. Other types of incidents such as food borne illnesses and disruptive, negative guest behavior which have either been alleged or proved to be attributable to our parks or our competitors could adversely affect attendance and revenues.

Extended disruptions to our technology platforms may adversely impact our sales and revenues.

A large portion of our sales are processed online and utilize third party technology platforms. Our increased dependence on these technology platforms may adversely impact our sales, and therefore our revenues, if key systems are disrupted for an extended period of time.

Risks Related to Our Strategy

Our growth strategy may not achieve the anticipated results.

Our future success will depend on our ability to grow our business, including fully recovering from the effects of the COVID-19 pandemic. We grow our business through acquisitions and capital investments to improve our parks through new rides and attractions, as well as in-park product offerings and product offerings outside of our parks. Our growth and innovation strategies require significant commitments of management resources and our investments may not grow our revenues at the rate we expect or at all. As a result, we may not be able to recover the costs incurred in developing new projects and initiatives, or to realize their intended or projected benefits, which could have a material adverse effect on our business, financial condition or results of operations.

We compete for discretionary spending and discretionary free time with many other entertainment alternatives and are subject to factors that generally affect the recreation and leisure industry, including general economic conditions.

Our parks compete for discretionary spending and discretionary free time with other amusement, water and theme parks and with other types of recreational activities and forms of entertainment, including movies, sporting events, restaurants and vacation travel. Our business is also subject to factors that generally affect the recreation and leisure industries and are not within our control. Such factors include, but are not limited to, general economic conditions, including relative fuel prices, and changes in consumer tastes and spending habits. There may be a material adverse effect on our business, financial condition or results of operations if we are unable to effectively compete with other entertainment alternatives.

The operating season at most of our parks is of limited duration, which can magnify the impact of adverse conditions or events occurring within that operating season.

Twelve of our properties are seasonal and are generally open daily from Memorial Day through Labor Day. Outside of daily operations, our seasonal properties are typically open during select weekends, including at most properties in the fourth quarter for Halloween and winter events. As a result, a substantial portion of our revenues from these seasonal parks are generated from Memorial Day through Labor Day with the major portion concentrated during the peak vacation months of July and August. Consequently, when adverse conditions or events occur during the operating season, particularly during the peak vacation months of July and August or the important fall season, there is only a limited period of time during which the impact of those conditions or events can be mitigated. Accordingly, the timing of such conditions or events may have a disproportionate adverse effect upon our revenues.

Risks Related to Human Capital

Increased costs of labor and employee health and welfare benefits may impact our results of operations.

Labor is a primary component in the cost of operating our business. Increased labor costs, due to competition, inflationary pressures, increased federal, state or local minimum wage requirements, and increased employee benefit costs, including health care costs, could adversely impact our operating expenses. Over the past two to three years, we experienced a meaningful increase in seasonal labor rate in order to recruit employees in a challenging labor market. Continued increases to both market wage rates and the statutory minimum wage rates could also materially impact our future seasonal labor rates. It is possible that these changes could significantly increase our labor costs, which would adversely affect our operating results and cash flows.

Our business depends on our ability to meet our workforce needs.

Our success depends on our ability to attract, motivate and retain qualified employees to keep pace with our needs. If we are unable to do so, our results of operations and cash flows may be adversely affected. We employ a significant workforce each season. We recruit year-round to fill thousands of staffing positions to ensure the appropriate workforce is in place at the right time. There is no assurance that we will be able to recruit and hire adequate personnel as the business requires or that we will not experience material increases in the cost of securing our workforce in the future.

If we lose key personnel, our business may be adversely affected.

Our success depends in part upon a number of key employees, including our senior management team, whose members have been involved in the leisure and hospitality industries for an average of more than 20 years. The loss of services of our key employees or our inability to replace our key employees could cause disruption in important operational, financial and strategic functions and have a material adverse effect on our business.

Risks Related to Our Capital Structure

The amount of our indebtedness could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or our industry and prevent us from fulfilling our obligations under our debt agreements.

We had $2.3 billion of outstanding indebtedness as of December 31, 2022 (before reduction of debt issuance costs).

The amount of our indebtedness could have important consequences. For example, it could:

•limit our ability to borrow money for our working capital, capital expenditures, debt service requirements, strategic initiatives or other purposes;

•limit our flexibility in planning or reacting to changes in business and future business operations; and

•make it more difficult for us to satisfy our obligations with respect to our indebtedness, and any failure to comply with the obligations of any of our debt instruments, including restrictive covenants and borrowing conditions, could result in an event of default under the agreements governing other indebtedness.

In addition, we may not be able to generate sufficient cash flow from operations, or be able to draw under our revolving credit facility or otherwise, in an amount sufficient to fund our liquidity needs, including the payment of principal and interest on our debt obligations. If our cash flows and capital resources are insufficient to service our indebtedness, we may be forced to reduce or delay capital expenditures, suspend partnership distributions, sell assets, seek additional capital or restructure or refinance our indebtedness. These alternative measures may not be successful and may not permit us to meet our scheduled debt service obligations. Our ability to restructure or refinance our debt in the future will depend on the condition of the capital and credit markets and our financial condition at such time. Any refinancing of our debt could be at higher interest rates and may require us to comply with more onerous covenants, which could further restrict our business operations. In addition, the terms of our existing or future debt agreements, including our credit agreement and the indentures governing our notes, may restrict us from adopting some of these alternatives. In the absence of sufficient operating results and resources, we could face substantial liquidity problems and might be required to dispose of material assets or operations to meet our debt service and other obligations. We may not be able to consummate those dispositions for fair market value or at all. Furthermore, any proceeds that we could realize from any such dispositions may not be adequate to meet our debt service obligations then due.

Despite the amount of our indebtedness, we may be able to incur additional indebtedness, which could further exacerbate the risks associated with the amount of our indebtedness.

Our debt agreements contain restrictions that could limit our flexibility in investing in our business, including the ability to pay partnership distributions.

Our credit agreement and the indentures governing our notes contain, and any future indebtedness of ours will likely contain, a number of covenants that could impose significant financial restrictions on us, including restrictions on our and our subsidiaries' ability to, among other things:

•pay distributions on or make distributions in respect of our partnership units or make other Restricted Payments, including unit repurchases;

•incur additional debt or issue certain preferred equity;

•make certain investments;

•sell certain assets;

•create restrictions on distributions from restricted subsidiaries;

•create liens on certain assets to secure debt;

•consolidate, merge, amalgamate, sell or otherwise dispose of all or substantially all our assets;

•enter into certain transactions with our affiliates; and

•designate our subsidiaries as unrestricted subsidiaries.

Our credit agreement includes a Senior Secured Leverage Ratio of 4.50x Total First Lien Senior Secured Debt-to-Consolidated EBITDA, which will step down to 4.00x in the second quarter of 2023 and which will step down further to 3.75x in the third quarter of 2023. Following an amendment in the first quarter of 2023, this financial covenant is only required to be tested at the end of any fiscal quarter in which revolving credit facility borrowings are outstanding.

Our credit agreement and fixed rate note agreements include Restricted Payment provisions, which could limit our ability to pay partnership distributions. Pursuant to the terms of the indenture governing the 2027 senior notes, which includes the most restrictive of these Restricted Payments provisions, if our pro forma Total-Indebtedness-to-Consolidated-Cash-Flow Ratio is greater than 5.25x, we can still make Restricted Payments of $100 million annually so long as no default or event of default has occurred and is continuing. If our pro forma Total-Indebtedness-to-Consolidated-Cash-Flow Ratio is less than or equal to 5.25x, we can make Restricted Payments up to our Restricted Payment pool.

Variable rate indebtedness could subject us to the risk of higher interest rates, which could cause our future debt service obligations to increase.

Certain of our borrowings may be at variable rates of interest and expose us to interest rate risk. If interest rates increase, our annual debt service obligations on any variable-rate indebtedness would increase even though the amount borrowed remained the same, and our net income would decrease.

Risks Related to Legal, Regulatory and Compliance Matters

Cyber-security risks and the failure to maintain the integrity of internal or customer data could result in damages to our reputation and/or subject us to costs, fines or lawsuits.

In the normal course of business, we, or third parties on our behalf, collect and retain large volumes of internal and customer data, including credit card numbers and other personally identifiable information, which is used for marketing and promotional purposes, and our various information technology systems enter, process, summarize and report such data. We also maintain personally identifiable information about our employees. The integrity and protection of such data is critical to our business, and our guests and employees have a high expectation that we will adequately protect their personal information. The regulatory environment, as well as the requirements imposed on us by the credit card industry, governing information, security and privacy laws is increasingly demanding and continues to evolve. Maintaining compliance with applicable security and privacy regulations may increase our operating costs and/or adversely impact our ability to market our parks, products and services to our guests. Furthermore, if a person could circumvent our security measures, he or she could destroy or steal valuable information or disrupt our operations. Any security breach could expose us to risks of data loss, which could harm our reputation and result in remedial and other costs, fines or lawsuits. Although we carry liability insurance to cover this risk, there can be no assurance that our coverage will be adequate to cover liabilities, or that we will be able to obtain adequate coverage should a catastrophic incident occur.

Our operations, our workforce and our ownership of property subject us to various laws and regulatory compliance, which may create uncertainty regarding future expenditures and liabilities.

We may be required to incur costs to comply with regulatory requirements, such as those relating to employment practices, environmental requirements, and other regulatory matters, and the costs of compliance, investigation, remediation, litigation, and resolution of regulatory matters could be substantial. We may also be required to incur additional costs and commit management resources to comply with proposed regulatory requirements that may become effective in the near future, including environmental, social and governance initiatives ("ESG") which continue to be a focus for investors and other stakeholders. Any ESG initiatives entered into by us may not realize their intended or projected benefits.

We are subject to extensive federal and state employment laws and regulations, including wage and hour laws and other pay practices and employee record-keeping requirements. We periodically have had to, and may have to, defend against lawsuits asserting non-compliance. Such lawsuits can be costly, time consuming and distract management, and adverse rulings in these types of claims could negatively affect our business, financial condition or results.

We also are subject to federal, state and local environmental laws and regulations such as those relating to water resources; discharges to air, water and land; the handling and disposal of solid and hazardous waste; and the cleanup of properties affected by regulated materials. Under these laws and regulations, we may be required to investigate and clean up hazardous or toxic substances or chemical releases from current or formerly owned or operated facilities or to mitigate potential environmental risks. Environmental laws typically impose cleanup responsibility and liability without regard to whether the relevant entity knew of or caused the presence of the contaminants. The costs of investigation, remediation or removal of regulated materials may be substantial, and the presence of those substances, or the failure to remediate a property properly, may impair our ability to use, transfer or obtain financing regarding our property.

Our tax treatment is dependent on our status as a partnership for federal income tax purposes. If the tax laws were to treat us as a corporation or we become subject to a material amount of entity-level taxation, it may substantially reduce our available cash.

We are a limited partnership under Delaware law and are treated as a partnership for federal income tax purposes. A change in current tax law may cause us to be taxed as a corporation for federal income tax purposes or otherwise subject us to taxation as an entity. If we were treated as a corporation for federal income tax purposes, we would pay federal income tax on our entire taxable income at the corporate tax rate, rather than only on the taxable income from our corporate subsidiaries, and may be subject to additional state taxes at varying rates. Further, unitholder distributions would generally be taxed again as corporate distributions or dividends and no income, gains, losses, or deductions would flow through to unitholders. Because additional entity level taxes would be imposed upon us as a corporation, our available cash could be substantially reduced. Although we are not currently aware of any legislative proposal that would adversely impact our treatment as a partnership, we are unable to predict whether any changes or other proposals will ultimately be enacted.

Our status as a partnership for federal income tax purposes subjects us and our unitholders to additional tax reporting that may be costly and may increase complexity.

Because we are treated as a partnership for federal income tax purposes, we are required to annually report to our unitholders certain partnership items. The nature of these items and the evolving legislation surrounding these reporting requirements may increase our unitholders' compliance cost and the cost of owning our units.

General Risk Factors

Other factors, including local events, natural disasters, pandemics and terrorist activities, or threats of these events, could adversely impact park attendance and our revenues.

Lower attendance may result from various local events, natural disasters, pandemics or terrorist activities, or threats of these events, all of which are outside of our control.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

None.

ITEM 2. PROPERTIES.

| | | | | | | | | | | | | | | | | |

| Park | | Location | Approximate Total

Acreage | Approximate Developed Acreage | Approximate Undeveloped Acreage |

Cedar Point

Cedar Point Shores | (1) | Sandusky, Ohio | 835 | | 725 | | 110 | |

Knott's Berry Farm

Knott's Soak City | | Buena Park, California | 175 | | 175 | | — | |

| Canada's Wonderland | | Vaughan, Ontario, Canada | 295 | | 295 | | — | |

| Kings Island | | Mason, Ohio | 680 | | 330 | | 350 | |

| Carowinds | | Charlotte, North Carolina and Fort Mill, South Carolina | 400 | | 300 | | 100 | |

| Kings Dominion | | Doswell, Virginia | 740 | | 280 | | 460 | |

| California's Great America | (2) | Santa Clara, California | 175 | | 175 | | — | |

| Dorney Park | | Allentown, Pennsylvania | 210 | | 180 | | 30 | |

| Worlds of Fun | | Kansas City, Missouri | 350 | | 250 | | 100 | |

| Valleyfair | | Shakopee, Minnesota | 190 | | 110 | | 80 | |

| Michigan's Adventure | | Muskegon, Michigan | 260 | | 120 | | 140 | |

| Schlitterbahn Waterpark & Resort New Braunfels | | New Braunfels, Texas | 90 | | 75 | | 15 | |

| Schlitterbahn Waterpark Galveston | (3) | Galveston, Texas | 40 | | 35 | | 5 | |

(1) Cedar Point and Cedar Point Shores are located on approximately 365 acres, virtually all of which have been developed, on the Cedar Point peninsula in Sandusky, Ohio. We also own approximately 470 acres of property on the mainland near Cedar Point with approximately 110 acres undeveloped. Cedar Point's Express Hotel, Castaway Bay Indoor Waterpark Resort and an adjoining restaurant, Castaway Bay Marina, seasonal-employee housing complexes, Cedar Point Sports Center and Sawmill Creek Resort are located on this property.

We control, through ownership or an easement, a six-mile public highway and own approximately 40 acres of vacant land adjacent to this highway, which is a secondary access route to Cedar Point and serves about 250 private residences. We maintain this roadway pursuant to deed provisions. We also own the Cedar Point Causeway, a four-lane roadway across Sandusky Bay, which is the principal access road to Cedar Point.

(2) We sold the land at California's Great America on June 27, 2022. Concurrently with the sale of the land, we entered into a lease contract that allows us to operate the park during a six-year term, and we have an option to extend the term for an additional five years. The lease is subject to early termination by the buyer with at least two years' prior notice; see Note 11.

(3) We lease the land at Schlitterbahn Waterpark Galveston through a long-term lease agreement. The lease is renewable in 2024 with options to renew at our discretion through 2049 and a right of first refusal clause to purchase the land.

All of our property is owned in fee simple and is encumbered by our credit agreement and the 2025 senior notes, with the exception of the land at California's Great America, the land at Schlitterbahn Waterpark Galveston, the land at the location of the Cedar Fair Resort and Attraction Management program, and portions of the six-mile public highway that serves as secondary access route to Cedar Point. We consider our properties to be well maintained, in good condition and adequate for our present uses and business requirements.

ITEM 3. LEGAL PROCEEDINGS.

None.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

PART II

ITEM 5. MARKET FOR REGISTRANT'S DEPOSITARY UNITS, RELATED UNITHOLDER MATTERS AND ISSUER

PURCHASES OF DEPOSITARY UNITS.

Cedar Fair, L.P. Depositary Units representing limited partner interests are listed for trading on The New York Stock Exchange under the symbol "FUN". As of February 10, 2023, there were approximately 4,600 registered holders of Cedar Fair, L.P. Depositary Units, representing limited partner interests. Item 12 in this Form 10-K includes information regarding our equity incentive plan, which is incorporated herein by reference.

Our credit agreement and fixed rate note agreements include Restricted Payment provisions, which could limit our ability to pay partnership distributions. Pursuant to the terms of the indenture governing the 2027 senior notes, which includes the most restrictive of these Restricted Payments provisions, if our pro forma Total-Indebtedness-to-Consolidated-Cash-Flow Ratio is greater than 5.25x, we can still make Restricted Payments of $100 million annually so long as no default or event of default has occurred and is continuing. If our pro forma Total-Indebtedness-to-Consolidated-Cash-Flow Ratio is less than or equal to 5.25x, we can make Restricted Payments up to our Restricted Payment pool. Our pro forma Total-Indebtedness-to-Consolidated-Cash-Flow Ratio was less than 5.25x as of December 31, 2022.

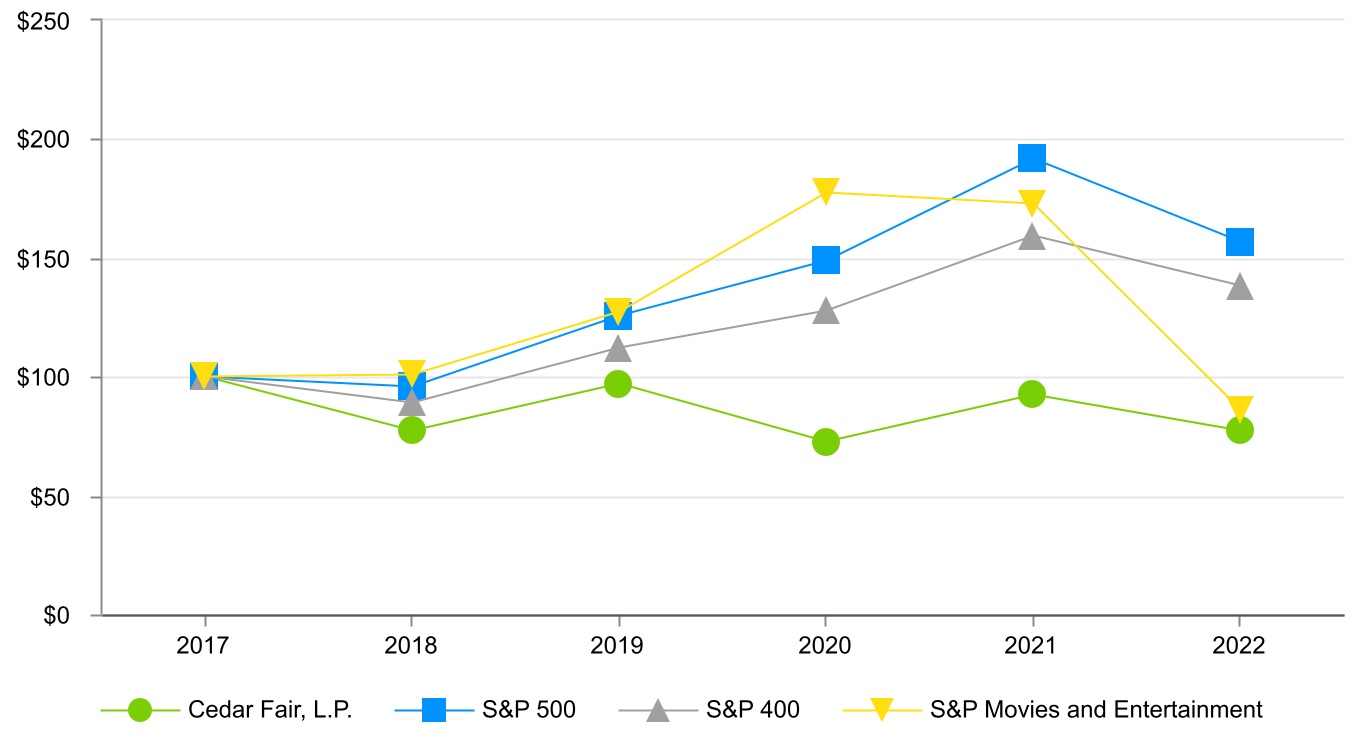

Unitholder Return Performance Graph

The graph below shows a comparison of the five-year cumulative total return (assuming all distributions/dividends reinvested) for Cedar Fair, L.P. limited partnership units, the S&P 500 Index, the S&P 400 Index, and the S&P - Movies and Entertainment Index, assuming investment of $100 on December 31, 2017.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Base Period | | | Return |

| | | 2017 | | | 2018 | | 2019 | | 2020 | | 2021 | | 2022 |

| Cedar Fair, L.P. | | | $ | 100.00 | | | | $ | 77.35 | | | $ | 97.04 | | | $ | 72.57 | | | $ | 92.35 | | | $ | 77.36 | |

| S&P 500 | | | 100.00 | | | | 95.62 | | | 125.73 | | | 148.87 | | | 191.60 | | | 156.90 | |

| S&P 400 | | | 100.00 | | | | 88.92 | | | 112.22 | | | 127.55 | | | 159.13 | | | 138.34 | |

| S&P Movies and Entertainment | | | 100.00 | | | | 100.61 | | | 127.49 | | | 177.32 | | | 172.96 | | | 86.08 | |

Issuer Purchases of Equity Securities

The following table summarizes repurchases of Cedar Fair, L.P. Depositary Units representing limited partner interests by the Partnership during the three months ended December 31, 2022:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | (a) | | (b) | | (c) | | (d) |