UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2017

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number 1-09397

Baker Hughes, a GE company, LLC

(Exact name of registrant as specified in its charter)

Delaware | 76-0207995 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

17021 Aldine Westfield Road, Houston, Texas | 77073-5101 | |

(Address of principal executive offices) | (Zip Code) | |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

5.125% Senior Notes due 2040 | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES [ ] NO [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES [ ] NO [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES [X] NO [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES [X] NO [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [Not Applicable]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer" "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o | Non-accelerated filer þ | Smaller reporting company o | Emerging growth company o |

(Do not check if a smaller reporting company) | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES [ ] NO [X]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’fs most recently completed second fiscal quarter: [Not Applicable]

As of February 8, 2018, all of the common units of the registrant are held by affiliates of the registrant. None of the common units are publicly traded.

REDUCED DISCLOSURE FORMAT

The registrant meets the conditions set forth in General Instruction 1(1)(a) and (b) of Form 10-K and is therefore filing this report with the reduced disclosure format.

Baker Hughes, a GE company LLC

Table of Contents

Page | ||

BHGE LLC 2017 FORM 10-K | i

PART I

ITEM 1. BUSINESS

Baker Hughes, a GE company LLC, (the Company, BHGE LLC, we, us, or our), a Delaware limited liability company, and a successor to Baker Hughes Incorporated, a Delaware corporation (Baker Hughes) is a fullstream oilfield technology provider that has a unique mix of integrated equipment and service capabilities.

On July 3, 2017, we closed our business combination (the Transactions) to combine the oil and gas business (GE O&G) of General Electric Company (GE) and Baker Hughes (refer to "Note 2. Business Acquisition" of the Notes to the Consolidated and Combined Financial Statements in Item 8 herein for further details on the Transactions). In connection with the Transactions, we entered into and are governed by an Amended and Restated Limited Liability Company Agreement, dated as of July 3, 2017 (the BHGE LLC Agreement). Under the BHGE LLC Agreement, EHHC Newco, LLC (EHHC), a wholly owned subsidiary of Baker Hughes, a GE company (BHGE), is our sole managing member and BHGE is the sole managing member of EHHC. As our managing member, EHHC conducts, directs and exercises full control over all our activities, including our day-to-day business affairs and decision-making, without the approval of any other member. As such, EHHC is responsible for all our operational and administrative decisions and the day-to-day management of our business. GE owns approximately 62.5% of our common units and BHGE owns approximately 37.5% of our common units indirectly through two wholly owned subsidiaries.

The Transactions were treated as a “reverse acquisition” for accounting purposes and, as such, the historical financial statements of the accounting acquirer, GE O&G, are the historical financial statements of the Company. The Company’s financial statements have been prepared on a consolidated basis, effective July 3, 2017. For all periods prior to July 3, 2017, the Company’s financial statements were prepared on a combined basis. The combined financial statements combine certain accounts of GE and its subsidiaries that were historically managed as part of its oil & gas business. The historical financial results in the combined financial statements presented may not be indicative of the results that would have been achieved had GE O&G operated as a separate, stand-alone entity during those periods. The GE O&G numbers in the consolidated and combined statements of income (loss) and statements of cash flows have been reclassified to conform to the current presentation. We believe that the current presentation is a more appropriate presentation of the combined businesses.

OUR VISION

We are the only fullstream provider of integrated oilfield products, services and digital solutions with 2017 revenue of $17.3 billion and a presence in more than 120 countries. We strive to provide best-in-class physical and digital technology solutions for customer productivity, leveraging complementary technologies to serve customers across the full spectrum of the oil and gas value chain.

We believe that there are structural changes taking place in the oil and gas industry that require a change in how we work. No matter the oil price, our customers are looking for new models and solutions to deliver higher industrial yield, which means improving productivity and efficiency and leveraging economies of scale, with lower carbon impact. While we will continue to serve customers on a project basis, our fullstream portfolio, digital capabilities and leading technology and services will enable us to shift towards outcome-focused solutions, enabling customers to lower capital and operating costs, reduce non-productive time and boost resource recovery. This is the cornerstone of our corporate strategy that is based on three pillars.

• | We intend to build market leading product companies focused on comprehensively reducing product and service costs, while improving equipment efficiency and reliability to significantly lower project breakeven costs. |

• | We strive to create value through integrated and differentiated equipment and service modules that will impact our customers total cost of projects and operations as well as fundamentally improving industry productivity, and |

• | We plan to continue to develop fullstream opportunities that drive value creation through radical improvements in total cost reduction and productivity increases for the industry. |

BHGE LLC 2017 FORM 10-K | 1

We expect to benefit from the following:

• | Complete fullstream portfolio. Leading portfolio capable of serving upstream, midstream and downstream sectors of the oil and gas industry, matching oilfield service and equipment leaders in many areas. Our four product lines - Oilfield Services; Oilfield Equipment; Turbomachinery & Process Solutions; and Digital Solutions, as discussed below under "Products and Services," are each among the top four providers in their respective segments. |

• | Complementary technology. We have a culture built on a heritage of innovation and invention in research and development, with complementary capabilities. Technology remains a differentiator and enables us to deliver across the value chain. Given our breadth and depth, we can leverage our technology, talent and expertise across our portfolio to accelerate the pace of innovation. |

• | Digital capabilities. We expect to be able to continue to develop software offerings on any operating platform, for new and extended applications in the oil and gas and other industrial ecosystems, such as machine and equipment health, reliability management and maintenance optimization. |

We believe we are positioned to assist our customers as they balance investment decisions between greenfield projects, brownfield projects and optimizing existing assets as a result of the current macroeconomic environment and the potentially prolonged period of lower oil prices. We expect that aging fields will require increased maintenance and intervention to sustain production later into the well life cycle when depletion accelerates. We believe our strategy coupled with our capabilities will help us compete and win in the current environment, while positioning us for the future.

ORDERS AND BACKLOG

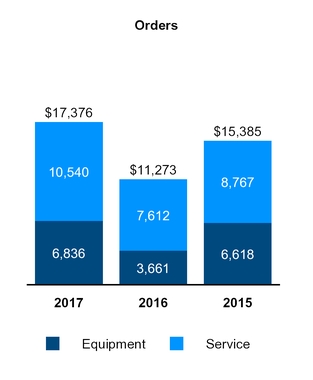

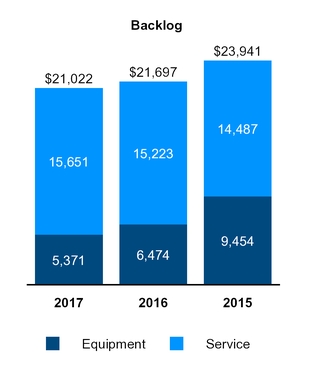

We are a global business with consolidated 2017 revenue of $17,259 million. We generate revenue and orders from a combination of equipment sales and services. In 2017, 42% of revenue was generated from equipment sales and 58% from services, while 39% of orders were for equipment and 61% for services. In 2016 and 2015, 46% and 50% of revenue was generated from equipment sales, and 54% and 50% of revenue was from services, respectively. We recognized orders of $17,376 million, $11,273 million, and $15,385 million, respectively, in 2017, 2016 and 2015. Due to the nature of our business, including the time required to manufacture equipment and the long-term nature of many of its service contracts, there is a backlog of unfilled customer orders for equipment sales and services, which as of December 31, 2017, 2016 and 2015 totaled $21,022 million, $21,697 million, and $23,941 million, respectively.

Our statement of income (loss) displays sales and costs of sales in accordance with SEC regulations under which “goods” is required to include all sales of tangible products and “services” must include all other sales, including other services activities. For the amounts shown above, as well as in the orders and backlog charts included in Management’s Discussion and Analysis of Financial Condition and Results of Operations included in Item 7 in this Form 10-K, we distinguish between “equipment” and “product services,” where product services refers to sales under product services agreements, including sales of both goods (such as spare parts and equipment upgrades) and related services (such as monitoring, maintenance and repairs), which is an important part of its operations. We refer to “product services” simply as “services” within this Business section and the Management’s Discussion and Analysis of Financial Condition and Results of Operations included in Item 7 in this Form 10-K.

Backlog is defined as unfilled customer orders for products and services believed to be firm. For product services, an amount is included for the expected life of the contract.

PRODUCTS AND SERVICES

We are a fullstream provider of oilfield products, services and digital solutions. Following the Transactions, we revised our segment structure and began to manage and report our operating results through four operating segments - Oilfield Services, Oilfield Equipment, Turbomachinery & Processing Solutions, and Digital Solutions. Our operating segments are organized based on the nature of our markets and customers. We have reflected this revised structure for all historical periods presented. The majority of the Baker Hughes business operations are included in the Oilfield Services (OFS) segment from July 3, 2017, the date of the Transactions.

BHGE LLC 2017 FORM 10-K | 2

Oilfield Services

The OFS segment provides products and services for on and offshore operations across the lifecycle of a well, ranging from drilling, evaluation, completion, production and intervention. The segment is comprised of eight product lines that design and manufacture products and services to help operators find, evaluate, drill, and produce hydrocarbons.

Products and services include diamond and tri-cone drill bits, drilling services, including directional drilling technology, measurement while drilling and logging while drilling, wireline services, drilling and completions fluids, completions tools and systems, wellbore intervention tools and services, artificial lift systems and oilfield and industrial chemicals.

OFS’ core evaluation and drilling technologies provide greater understanding of the subsurface to enable smoother, faster drilling and precise wellbore placement, leading to improved recovery and project economics. With the industry’s broadest completions portfolio, OFS can provide tailored well integrity solutions for all well types. Drawing from a wide range of artificial lift technology, coupled with enterprise optimization software, OFS can help lower the cost per barrel for the life of an asset.

Our customers include the large integrated major and super-major oil and natural gas companies, U.S. and international independent oil and natural gas companies and the national or state-owned oil companies as well as oilfield service companies.

Oilfield Equipment

The Oilfield Equipment (OFE) segment provides a broad portfolio of products and services required to facilitate the safe and reliable flow of hydrocarbons from the subsea wellhead to the surface production facilities. The OFE operation designs and manufactures onshore and offshore drilling and production systems and equipment for floating production platforms and provides a full range of services related to onshore and offshore drilling activities.

The OFE portfolio includes deepwater drilling equipment, subsea production systems (SPS), flexible pipe systems, and related service solutions. The OFE drilling and production systems product line offers blowout preventers, control systems, marine drilling risers, wellhead connectors, diverters and related services. OFE offers SPS, including trees, control systems, manifolds, connections, wellheads, specialty connectors & pipes, installation and decommissioning solutions, and related services. OFE also provides advanced flexible pipe products including risers, flowlines, fluid transfer lines and jumpers, for both subsea and FPSO (floating production storage & offloading)-based production across a range of operating environments. Investment in composite technology is enabling BHGE to extend the capabilities of BHGE’s flexibles even further. OFE also offers a range of comprehensive, worldwide services for installation, technical support, well access through subsea intervention systems, operating resources and tools, offshore products and brownfield asset integrity solutions.

OFE customers are oil and gas field developers, drilling and oil companies seeking to undertake new subsea projects, mid-life upgrades and maintenance, well interventions and workover campaigns. OFE differentiates itself in SPS and deepwater drilling systems. OFE’s key competitive areas are large-bore gas fields, deepwater oilfields and fields with long tieback distances. In addition to a robust presence in other subsea areas, including high-pressure high-temperature (HPHT) fields, OFE’s product lines’ production systems are among the industry’s most reliable, with uptime of the critical control system exceeding 99.8%.

BHGE LLC 2017 FORM 10-K | 3

Turbomachinery & Process Solutions

The Turbomachinery & Process Solutions (TPS) segment provides equipment and related services for mechanical-drive, compression and power-generation applications across the oil and gas industry as well as products and services to serve the downstream segments of the industry including refining, petrochemical, distributed gas, flow and process control and other industrial applications. The TPS segment is a leader in designing, manufacturing, maintaining and upgrading rotating equipment across the oil and gas, petro-chemical and industrial sectors.

The TPS portfolio includes drivers, driven equipment, flow control and turnkey solutions. Drivers are comprised of aero-derivative gas turbines, heavy-duty gas turbines, small- to medium-sized steam turbines, slow speed and integrated gas engines, hot gas and turbo expanders and synchronous and induction electric motors. TPS’ driven equipment consists of electric generators, reciprocating, centrifugal, axial, direct-drive high speed, integrated and subsea compressors, and turbo-expanders. TPS’ flow control includes pumps, valves, regulators, control systems and other flow and process control technologies. As part of its turnkey solutions, TPS offers power generation modules, waste heat/energy recovery, energy storage, modularized small and large liquefaction plants, carbon capture and storage/use facilities. TPS also offers a variety of system upgrades and conversion solutions, from a single machine to full plant debottlenecking and modernization.

TPS’ products enable customers to increase upstream oil and gas production, liquefy natural gas, compress gas for transport via pipelines, generate electricity, store gas and energy, refine oil and gas and produce petro-chemicals, while minimizing both operational and environmental risks in the most extreme service conditions. TPS’ customers are upstream, midstream and downstream, onshore and offshore, and small to large scale. Midstream and downstream customers include liquefied natural gas (LNG) plants, pipelines, storage facilities, refineries and a wide range of industrial and engineering, procurement and construction (EPC) companies.

TPS’ value proposition is founded on its turbomachinery and flow control technology, a unique competence to integrate gas turbines and compressors in the most critical natural gas applications, best-in-class manufacturing and testing capabilities, reliable maintenance and service operations, and innovative real-time diagnostics and control systems, enabling condition-based maintenance and increasing overall productivity, availability, efficiency and reliability for oil and gas assets. TPS differentiates itself from competitors with its expertise in technology and project management, local presence and partnerships, as well as the deep industry know-how of its teams to provide fully integrated equipment and services solutions with state-of-art technology from design and manufacture through to operations.

Digital Solutions

The Digital Solutions (DS) segment provides operating technologies helping to improve the health, productivity and safety of asset intensive industries and enable the Industrial Internet of Things. DS includes the Measurement & Controls business for industry-leading hardware technologies as well as the software businesses of GE Oil & Gas and Baker Hughes that leverages best-of-class cloud services, including GE's Predix application development platform.

The DS portfolio includes condition monitoring, inspection technologies, measurement, sensing and pipeline solutions. Condition monitoring technologies include the Bently Nevada® and System 1® brands, providing rack-based vibration monitoring equipment, sensors, software cyber security solutions and industrial controls primarily for power generation and oil and gas operations. The DS Inspection Technologies product line includes non-destructive testing technology, software, and services, including industrial radiography, ultrasonic sensors, testing machines and gauges, NDT film, and remote visual inspection.

The DS Process and Pipeline Services product line (PPS) provides pre-commissioning and maintenance services to improve throughput and asset integrity for process facilities and pipelines while achieving the highest returns possible. In addition, the PPS product line provides inline inspection solutions to support pipeline integrity and includes nitrogen, bolting, torqueing and leak detection services, as well as the world’s largest fleet of air compressors to dry pipelines after hydrotesting. The DS Measurement and Sensing product line provides instrumentation to better detect and analyze pressure, flow, gas, and moisture conditions and more.

The DS segment helps companies monitor and optimize industrial assets while mitigating risk and boosting safety, by providing performance management, and condition and asset health monitoring. It also provides

BHGE LLC 2017 FORM 10-K | 4

customers the technical capabilities to drive enterprise wide digital transformation of business processes and to focus on better production outcomes along the entire oil & gas value chain, using sensors, services and inspections to connect industrial assets to the Industrial Internet. The DS software portfolio is built to handle big data at an industrial scale and with industrial-strength security, giving customers the power to innovate and make faster, more confident decisions. The combination of deep domain expertise with modern data management and deep learning techniques gives customers the ability to maximize asset and operations performance.

Further information about our segments is set forth in Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations and "Note 13. Segment Information" of the Notes to Consolidated and Combined Financial Statements in Item 8 herein.

MARKETS AND COMPETITION

We sell to our customers through direct and indirect channels. Our primary sales channel is through our direct sales force, which has a strong regional focus with local teams close to the customer, who are able to draw support from centers of excellence in each of our major product lines. Our sales force also uses its application engineers, field application engineers, service engineers, commercial and sales managers, and account executives to help deliver and provide customers with the best product and service solutions which BHGE can offer. No single customer accounted for 10% or more of our revenue in the current year.

Our products and services are sold in highly competitive markets and the competitive environment varies by produce line, as discussed below:

Oilfield Services

Our OFS product line believes that the principal competitive factors in the industries and markets it serves are product and service quality, reliability and availability, health, safety and environmental standards, technical proficiency and price. Our products and services are sold in highly competitive markets and revenue and earnings are affected by changes in commodity prices, fluctuations in the level of drilling, workover and completion activity in major markets, general economic conditions, foreign currency exchange fluctuations and governmental regulations. While we may have contracts with customers that include multiple well projects and that may extend over a period of time ranging from two to four years, our services and products are generally provided on a well-by-well basis. Most contracts cover our pricing of the products and services, but do not necessarily establish an obligation to use our products and services. OFS product line competitors include Schlumberger, Halliburton and Weatherford International.

Oilfield Equipment

Our OFE product line believes that the principal competitive factors in the industries and markets it serves are product and service quality, reliability and on time delivery, health, safety and environmental standards, technical proficiency, availability of spare parts and price. Its strong track record of innovation enables OFE to enter into long-term, performance-based service agreements with our customers. In the SPS product line, the primary competitors of OFE include Schlumberger, TechnipFMC, Aker Solutions ASA, Proserv and Dril-Quip Inc. In the flexible pipe product line, competitors include TechnipFMC, National Oilwell Varco (NOV), Airborne, and Magma. In the drilling sub-product line, competitors include NOV, Schlumberger and Horn Equipment.

Turbomachinery & Process Solutions

Our TPS product line believes that the principal competitive factors in the industries and markets it serves are product range (or power range measured in Megawatts) coverage, efficiency, product reliability and availability, service capabilities, packages, references, emissions and price. In upstream and midstream applications, our primary equipment competitors include Siemens (Power and Gas business unit), Solar (a Caterpillar company), MAN Turbo and Mitsubishi Heavy Industries. In downstream applications, TPS primarily competes with OEMs and independent service providers, including Flowserve, Pentair, Emerson, Siemens, Hitachi, Solar (a Caterpillar company), Ariel, MAN Turbo, Burckhardt, Elliott Ebara and Mitsubishi Heavy Industries. Our aftermarket equipment product line competes with smaller independent local providers such as Masaood John Brown, Sulzer, MTU, Trans Canada Turbine, Chromalloy and Ethos Energy (a joint venture of Siemens and the Wood Group).

BHGE LLC 2017 FORM 10-K | 5

Digital Solutions

Our DS product line believes that the principal competitive factors in the industries and markets it serves are superior product technology, service, quality, and reliability. Our DS product line competes across a wide range of industries, including Oil & Gas, Power Generation, Aerospace, and Light and Heavy Industrials. The products and services are sold in a diversified, fragmented arena with a broad range of competitors. Although no single company competes directly with DS across all its product lines, various companies compete in one or more products. Primary competitors include Emerson, ABB, Schneider Electric, Fortive, Olympus, Comet Group, Honeywell Process Solutions, Roper Technology, Siemens, Spectris, Aspentech and OSISoft.

CONTRACTS

We conduct our business under various types of contracts in the upstream, midstream, and downstream segments, including fixed-fee or turnkey contracts, transactional agreements for products and services, and long-term aftermarket service agreements.

We enjoy stable relationships with many of our customers based on long-term project contracts and master service agreements. Several of those contracts require us to commit to a fixed price based on the customer’s technical specifications with little or no legal relief available due to changes in circumstances, such as changes in local laws or industry or geopolitical events. In some cases, failure to deliver products or perform services within contractual commitments may lead to liquidated damages claims. We seek to mitigate these exposures through close collaboration with our customers.

We strive to negotiate the terms of our customer contracts consistent with what we consider to be industry best practices. Our customers typically indemnify us for certain claims arising from: the injury or death of their employees and often their other contractors; the loss of or damage to their equipment and often that of their other contractors; pollution originating from their equipment or facility; and all liabilities related to the well and subsurface operations, including loss or damage to the well or reservoir, loss of well control, fire, explosion, or any uncontrolled flow of oil or gas. Conversely, we typically indemnify our customers for certain claims arising from: the injury or death of our employees and sometimes that of our subcontractors; the loss of or damage to our equipment (other than equipment lost in the hole); and pollution originating from our equipment above the surface of the earth while in our care, custody, and control. Where the above indemnities do not apply or are not consistent with industry best practices, we typically provide a capped indemnity for damages caused to the customer by our negligence or the negligence of our contractors, and include an overall limitation of liability clause. It is also our general practice to include a limitation of liability for consequential loss, including loss of profits and loss of revenue, in all customer contracts.

Our indemnity structure may not protect us in every case. Certain U.S. states such as Texas, Louisiana, Wyoming, and New Mexico have enacted oil and natural gas specific anti-indemnity statutes. These statutes can void the allocation of liability agreed to in a contract, however, both the Texas and Louisiana anti-indemnity statutes include important exclusions. The Louisiana statute does not apply to property damage, and the Texas statute allows mutual indemnity agreements that are supported by insurance and has exclusions, which include, among other things, loss or liability for property damage that results from pollution and the cost of well control events. State law, laws or public policy in countries outside the U.S., or the negotiated terms of a customer contract may also limit indemnity obligations in the event of the gross negligence or willful misconduct. We sometimes contract with customers that are not the end user of our products. It is our practice to seek to obtain an indemnity from our customer for any end-user claims, but this is not always possible. Similarly, government agencies and other third parties, including in some cases other contractors of our customers, may make claims in respect of which we are not indemnified and for which responsibility is assessed proportionate to fault. In all cases, deviations from our standard contracting practices are examined through an established risk deviation process.

The Company maintains a commercial general liability insurance policy program that covers against certain operating hazards, including product liability claims and personal injury claims, as well as certain limited environmental pollution claims for damage to a third party or its property arising out of contact with pollution for which the Company is liable, however, clean up and well control costs are not covered by such program. All of the insurance policies purchased by the Company are subject to deductible and/or self-insured retention amounts for which we are responsible for payment, specific terms, conditions, limitations and exclusions. There can be no

BHGE LLC 2017 FORM 10-K | 6

assurance that the nature and amount of Company insurance will be sufficient to fully indemnify us against liabilities related to our business.

RESEARCH AND DEVELOPMENT

We engage in research and development activities directed primarily toward the development of new products, services, technology and other solutions, as well as the improvement of existing products and services and the design of specialized products to meet specific customer needs. For information regarding the total amount of research and development expense in each of the three years in the period ended December 31, 2017, see "Note 1. Summary of Significant Accounting Policies" of the Notes to Consolidated and Combined Financial Statements in Item 8 herein.

In the OFS and OFE product lines, we continue to invest in products to develop capability, improve performance and reduce costs. In OFS, we invested in a range of formation evaluation capabilities and drilling services hardware. This included a new and cutting-edge line of drill bits with hydraulic actuators that offer customers improvements in reliability, efficiency and maintainability. In OFE, the recent focus has been to expand capability into deeper water, longer offsets and at higher pressures. Additionally, subsea power and processing is also an area in which we are investing, covering both pumping and compression. In the TPS product line, we continue to invest in continuous product improvement of reciprocating and centrifugal compressors, using advanced fluid dynamic simulation and advanced aeromechanics to improve capability, operability and efficiency of its centrifugal compressors family. DS continues to invest in advanced digital solutions designed to improve the efficiency, reliability and safety of oil and gas production operations. These systems integrate operational data from producing oil and gas facilities to deliver notifications and analytical reports to engineers so they can identify operational performance issues before they become significant, thus helping to prevent unplanned downtime and improve facility reliability.

INTELLECTUAL PROPERTY

Our technology, brands and other intellectual property rights are important elements of our business. We rely on patent, trademark, copyright and trade secret laws, as well as non-disclosure and employee invention assignment agreements to protect our intellectual property rights. Many of the patents and patent applications in our portfolio are owned by us, while other patents and patent applications in our portfolio are licensed to us by GE and third parties. We do not consider any individual patent or trademark to be material to our business operations.

In connection with the Transactions, GE entered into an IP cross-license agreement (the IP Cross-License Agreement) with us. GE agreed to perpetually license to us the right to use certain intellectual property owned or controlled by GE (other than GE Digital) pursuant to the terms of the IP Cross-License Agreement. We agreed to perpetually license to GE the right to use certain intellectual property rights pursuant to the terms of the IP Cross-License Agreement. This license allows us to have continued rights to use some of GE’s intellectual property so that they can be leveraged pursuant to the terms of the IP Cross-License Agreement. Any improvements to such intellectual property made or developed by us will be owned by us and licensed back to GE pursuant to the terms of the IP Cross-License Agreement and any improvements to such intellectual property made or developed by GE will be owned by GE and licensed to us. If we were to cease being a majority-owned subsidiary of GE, the licenses under the IP Cross-License Agreement are intended to survive.

We have followed a policy of seeking patent and trademark protection in numerous countries and regions throughout the world for products and methods that appear to have commercial significance. We believe that protection of our patents, trademarks, and related intellectual property rights is central to the conduct of our business, and aggressively pursue protection of our intellectual property rights against infringement worldwide as we deem appropriate to protect our business. Additionally, we consider the quality and timely delivery of our products, the service we provide to our customers and the technical knowledge and skills of our personnel to be other important components of the portfolio of capabilities and assets supporting our ability to compete.

BHGE LLC 2017 FORM 10-K | 7

SEASONALITY

Our operations can be affected by seasonal weather, which can temporarily affect the delivery and performance of our products and services, and our customers' budgetary cycles. Examples of seasonal events that can impact our business are set forth below:

• | The severity and duration of both the summer and the winter in North America can have a significant impact on activity levels. In Canada, the timing and duration of the spring thaw directly affects activity levels, which reach seasonal lows during the second quarter and build through the third and fourth quarters to a seasonal high in the first quarter. |

• | Adverse weather conditions, such as hurricanes in the Gulf of Mexico, may interrupt or curtail our coastal and offshore drilling, or our customers’ operations, cause supply disruptions and result in a loss of revenue and damage to our equipment and facilities, which may or may not be insured. |

• | Severe weather during the winter months normally results in reduced activity levels in the North Sea and Russia generally in the first quarter and may interrupt or curtail our operations, or our customers’ operations, in those areas and result in a loss of revenue. |

• | Scheduled repair and maintenance of offshore facilities in the North Sea can reduce activity in the second and third quarters. |

• | Many of our international oilfield customers increase orders for certain products and services in the fourth quarter. |

• | Our process & pipeline business in the DS segment typically experiences lower sales during the first and fourth quarters of the year due to the Northern Hemisphere winter. |

• | Our broader DS business typically experiences higher customer activity as a result of spending patterns in the second half of the year. |

RAW MATERIALS

We purchase various raw materials and component parts for use in manufacturing our products and delivering our services. The principal raw materials we use include steel alloys, chromium, nickel, titanium, barite, beryllium, copper, lead, tungsten carbide, synthetic and natural diamonds, gels, sand and other proppants, printed circuit boards and other electronic components and hydrocarbon-based chemical feed stocks. Raw materials that are essential to our business are normally readily available from multiple sources, but may be subject to price volatility. Market conditions can trigger constraints in the supply of certain raw materials, and we are always seeking ways to ensure the availability and manage the cost of raw materials. Our procurement department uses its size and buying power to enhance its access to key materials at competitive prices.

In addition to raw materials and component parts, we also use the products and services of metal fabricators, machine shops, foundries, forge shops, assembly operations, contract manufacturers, logistics providers, packagers, indirect material providers, and others in order to produce and deliver products to customers. These materials and services are generally available from multiple sources.

EMPLOYEES

As of December 31, 2017, we had over 64,000 employees, of which the majority are outside the U.S. Approximately 11% of these employees are represented under collective bargaining agreements or similar-type labor arrangements.

BHGE LLC 2017 FORM 10-K | 8

ENVIRONMENTAL MATTERS

We are committed to the health and safety of people, protection of the environment and compliance with environmental laws, regulations and our policies. Our past and present operations include activities that are subject to extensive domestic (including U.S. federal, state and local) and international regulations with regard to air, land and water quality and other environmental matters. Regulations continue to evolve, and changes in standards of enforcement of existing regulations, as well as the enactment of new legislation, may require us and our customers to modify, supplement or replace equipment or facilities or to change or discontinue present methods of operation. Our environmental compliance expenditures and our capital costs for environmental control equipment may change accordingly.

We are, and may in the future be, involved in voluntary remediation projects at current and former properties. On rare occasions, our remediation activities are conducted as specified by a government agency-issued consent decree or agreed order. Remediation costs at these properties are accrued using currently available facts, existing environmental permits, technology and presently enacted laws and regulations. For sites where we are primarily responsible for the remediation, our cost estimates are developed based on internal evaluations and are not discounted. We record accruals when it is probable that we will be obligated to pay amounts for environmental site evaluation, remediation or related activities, and such amounts can be reasonably estimated. Accruals are recorded even if significant uncertainties exist over the ultimate cost of the remediation. Ongoing environmental compliance costs, such as obtaining environmental permits, installation and maintenance of pollution control equipment and waste disposal, are expensed as incurred.

The Comprehensive Environmental Response, Compensation and Liability Act (known as "Superfund") imposes liability for the release of a "hazardous substance" into the environment. Superfund liability is imposed without regard to fault, even if the waste disposal was in compliance with laws and regulations. We have been identified as a potentially responsible party (PRP) at various Superfund sites, and we accrue our share of the estimated remediation costs for the site. PRPs in Superfund actions have joint and several liability and may be required to pay more than their proportional share of such costs.

In some cases, it is not possible to quantify our ultimate exposure because the projects are either in the investigative or early remediation stage, or superfund allocation information is not yet available. Based upon current information, we believe that our overall compliance with environmental regulations, including remediation obligations, environmental compliance costs and capital expenditures for environmental control equipment, will not have a material adverse effect on our capital expenditures, earnings or competitive position because we have either established adequate reserves or our compliance cost, based on available information, is not expected to be material to our consolidated and combined financial statements. Our total accrual for environmental remediation was $82 million and $28 million at December 31, 2017 and 2016, respectively. We continue to focus on reducing future environmental liabilities by maintaining appropriate Company standards and by improving our assurance programs.

AVAILABILITY OF INFORMATION FOR MEMBERS

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (Exchange Act), are made available free of charge on our Internet website at www.bhge.com as soon as reasonably practicable after these reports have been electronically filed with, or furnished to, the SEC. The public may read and copy any materials we have filed with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. Information contained on or connected to our website is not incorporated by reference into this annual report on Form 10-K and should not be considered part of this annual report or any other filing we make with the SEC.

We have a Code of Conduct to provide guidance to our officers and employees on matters of business conduct and ethics, including compliance standards and procedures. We have also required our principal executive officer, principal financial officer and principal accounting officer to sign a Code of Ethical Conduct Certification.

Our Code of Conduct and Code of Ethical Conduct Certifications are available on the Investor section of our website at www.bhge.com. We will disclose on a current report on Form 8-K or on our website information about any amendment or waiver of these codes for our executive officers and directors. Waiver information disclosed on

BHGE LLC 2017 FORM 10-K | 9

our website will remain on the website for at least 12 months after the initial disclosure of a waiver. In addition, a copy of our Code of Conduct and Code of Ethical Conduct Certifications are available in print at no cost.

EXECUTIVE OFFICERS OF BAKER HUGHES, A GE COMPANY, LLC

The following table shows, as of February 23, 2018, the name of each of our executive officers, together with his or her age and office presently or previously held. There are no family relationships among our executive officers.

Name | Age | Position and Background | ||

Lorenzo Simonelli | 44 | President and Chief Executive Officer Lorenzo Simonelli has been the Chief Executive Officer of the Company since July 2017. Before joining the Company in July 2017, Mr. Simonelli was Senior Vice President, GE and President and Chief Executive Officer, GE Oil & Gas from October 2013 to July 2017. Before joining GE Oil & Gas, he was the President and Chief Executive Officer of GE Transportation from July 2008 to October 2013. Mr. Simonelli joined GE in 1994 and held various finance and leadership roles from 1994 to 2008. | ||

Brian Worrell | 48 | Chief Financial Officer Brian Worrell is the Chief Financial Officer of the Company. Prior to joining the Company in July 2017, he served as Vice President and Chief Financial Officer of GE Oil & Gas from January 2014 to July 2017. He previously held the position of Vice President, Financial Planning & Analysis for GE from 2010 to January 2014 and Vice President Corporate Audit Staff for GE from 2006 to 2010. | ||

Maria Claudia Borras | 49 | President, Oilfield Services Maria Claudia Borras is the President and Chief Executive Officer, Oilfield Services of the Company. Before joining the Company in July 2017, she served as the Chief Commercial Officer of GE Oil & Gas from December 2014 to July 2017. Prior to joining GE Oil & Gas, she held various leadership positions at Baker Hughes Incorporated including President, Latin America from October 2013 to January 2015, President Europe Region from August 2011 to October 2013, Vice President, Global Marketing from May 2009 to July 2011 and other leadership roles at Baker Hughes Incorporated from 1994 to April 2009. | ||

Kurt Camilleri | 43 | Vice President, Controller and Chief Accounting Officer Kurt Camilleri is the Vice President, Controller and Chief Accounting Officer of the Company. Prior to joining the Company in July 2017, he served as the Global Controller for GE Oil & Gas from July 2013 to July 2017. Mr. Camilleri served as the Global Controller for GE Transportation from January 2013 to June 2013 and the Controller for Europe and Eastern and African Growth Markets for GE Healthcare from 2010 to January 2013. He began his career in 1996 with Pricewaterhouse in London, which subsequently became PricewaterhouseCoopers. | ||

Roderick Christie | 55 | President, Turbomachinery and Process Solutions Rod Christie is the President and Chief Executive Officer of Turbomachinery & Process Solutions of the Company. Prior to joining the Company in July 2017, he served as the Chief Executive Officer of Turbomachinery & Process Solutions at GE Oil & Gas from January 2016 to July 2017. He served as the Chief Executive Officer of GE Oil & Gas’ Subsea Systems & Drilling Business from August 2011 to 2016 and held various other leadership positions within GE between 1999 to 2011. | ||

Matthias Heilmann | 49 | President, Digital Solutions Matthias Heilmann is the President and Chief Executive Officer of Digital Solutions of the Company. Prior to joining the Company in July 2017, he served as the Chief Digital Officer, President & Chief Executive Officer of Digital Solutions within GE Oil & Gas from 2016 through July 2017. Prior to joining GE Oil & Gas, he led ABB’s Global Product Group Enterprise Software business from June 2014 to January 2016. He served as the Chief Operating Officer of Ryerson Holding Corporation from March 2010 until January 2012 and served as Executive Vice President and Chief Operating Officer of Ryerson Inc. from January 2009 to January 2012. | ||

BHGE LLC 2017 FORM 10-K | 10

William D. Marsh | 55 | Chief Legal Officer William D. Marsh is the Chief Legal Officer of the Company. Prior to joining the Company in July 2017, he served as the Vice President and General Counsel of Baker Hughes Incorporated from February 2013 to July 2017. He previously served as the Vice President-Legal for Western Hemisphere at Baker Hughes Incorporated from May 2009 to February 2013 and held various executive, legal and corporate roles within Baker Hughes Incorporated from 1998 to 2009. | ||

Derek Mathieson | 47 | Chief Marketing and Technology Officer Derek Mathieson is the Chief Marketing and Technology Officer of the Company. Prior to joining the Company in July 2017, he served in various leadership roles at Baker Hughes Incorporated including Chief Integration Officer from October 2016 to July 2017; Chief Commercial Officer from May 2016 to October 2016; Chief Technology and Marketing Officer from September 2015 to May 2016; Chief Strategy Officer from October 2013 to September 2015; President Western Hemisphere Operations from 2012 to 2013; President, Products and Technology from May 2009 to January 2012; and Chief Technology and Marketing Officer from December 2008 to May 2009. | ||

Neil Saunders | 48 | President, Oilfield Equipment Neil Saunders is the President and Chief Executive Officer of Oilfield Equipment of the Company. Prior to joining the Company in July 2017, he served as the President and Chief Executive Officer of the Subsea Systems & Drilling business at GE Oil & Gas from July 2016 to July 2017 and the Senior Vice President for Subsea Production Systems from August 2011 to July 2016. He served in various leadership roles within GE Oil & Gas from 2007 to August 2011. | ||

Uwem Ukpong | 46 | Chief Global Operations Officer Uwem Ukpong is the Chief Global Operations Officer of the Company. Prior to this role, he served as the Chief Integration Officer of the Company from July 2017 to January 2018. He served as Vice President, Baker Hughes Integration for GE Oil & Gas from October 2016 to July 2017 and President and CEO of the GE Oil & Gas Surface Business from January 2016 to October 2016. He held various technical and leadership roles at Schlumberger from 1993 to 2015. | ||

ITEM 1A. RISK FACTORS

The following risk factors should be considered carefully in addition to the other information contained in this Annual Report on Form 10-K. There may be additional risks, uncertainties and matters not listed below, that we are unaware of, or that we currently consider immaterial. Any of these may adversely affect our business, financial condition, results of operations and cash flows and, thus, the value of an investment in the Company.

Risk Factors Related to Our Business

We operate in a highly competitive environment, which may adversely affect our ability to succeed.

We operate in a highly competitive environment for marketing oilfield products and services and securing equipment and trained personnel. Our ability to continually provide competitive products and services can impact our ability to defend, maintain or increase prices for our products and services, maintain market share, and negotiate acceptable contract terms with our customers. In order to be competitive, we must provide new technologies, reliable products and services that perform as expected and that create value for our customers, and successfully recruit, train and retain competent personnel.

In addition, our investments in new technologies and properties, plants and equipment may not provide competitive returns. Our ability to defend, maintain or increase prices for our products and services is in part dependent on the industry’s capacity relative to customer demand, and on our ability to differentiate the value delivered by our products and services from our competitors’ products and services. Managing development of competitive technology and new product introductions on a forecasted schedule and at a forecasted cost can impact our financial results. If we are unable to continue to develop and produce competitive technology or deliver it to our clients in a timely and cost-competitive manner in various markets in which we operate, or if competing technology accelerates the obsolescence of any of our products or services, any competitive advantage that we

BHGE LLC 2017 FORM 10-K | 11

may hold, and in turn, our business, financial condition and results of operations could be materially and adversely affected.

The high cost or unavailability of infrastructure, materials, equipment, supplies and personnel, particularly in periods of rapid growth, could adversely affect our ability to execute our operations on a timely basis.

Our manufacturing operations are dependent on having sufficient raw materials, component parts and manufacturing capacity available to meet our manufacturing plans at a reasonable cost while minimizing inventories. Our ability to effectively manage our manufacturing operations and meet these goals can have an impact on our business, including our ability to meet our manufacturing plans and revenue goals, control costs, and avoid shortages or over-supply of raw materials and component parts. Raw materials and components of particular concern include steel alloys (including chromium and nickel), titanium, barite, beryllium, copper, lead, tungsten carbide, synthetic and natural diamonds, gels, sand and other proppants, printed circuit boards and other electronic components and hydrocarbon-based chemical feed stocks. Our ability to repair or replace equipment damaged or lost in the well can also impact our ability to service our customers. A lack of manufacturing capacity could result in increased backlog, which may limit our ability to respond to orders with short lead times.

People are a key resource to developing, manufacturing and delivering our products and services to our customers around the world. Our ability to manage the recruiting, training, retention and efficient usage of the highly skilled workforce required by our plans and to manage the associated costs could impact our business. A well-trained, motivated workforce has a positive impact on our ability to attract and retain business. Periods of rapid growth present a challenge to us and our industry to recruit, train and retain our employees, while also managing the impact of wage inflation and the limited available qualified labor in the markets where we operate.

Likewise, if the economy or markets decline or other changes occur, we may have to reduce utilization of our assets or adjust our workforce to control costs, which may cause us to lose some of our skilled employees. Labor-related actions, including strikes, slowdowns and facility occupations can also have a negative impact on our business.

Our business could be impacted by geopolitical and terrorism threats in countries where we or our customers do business and our business operations may be impacted by civil unrest, government expropriations and/or epidemic outbreaks.

Geopolitical and terrorism risks continue to grow in a number of key countries where we currently or may in the future do business. Geopolitical and terrorism risks could lead to, among other things, a loss of our investment in the country, impairment of the safety of our employees and impairment of our or our customers’ ability to conduct operations.

In addition to other geopolitical and terrorism risks, civil unrest continues to grow in a number of key countries where we do business. Our ability to conduct business operations may be impacted by that civil unrest and our assets in these countries may also be subject to expropriation by governments or other parties involved in civil unrest. Epidemic outbreaks may also impact our business operations by, among other things, restricting travel to protect the health and welfare of our employees and decisions by our customers to curtail or stop operations in impacted areas.

Compliance with and changes in laws could be costly and could affect operating results. In addition, government disruptions could negatively impact our ability to conduct our business.

We have operations in the United States and in more than 120 countries that can be impacted by expected and unexpected changes in the legal and business environments in which we operate. Compliance-related issues could also limit our ability to do business in certain countries and impact our earnings. Changes that could impact the legal environment include new legislation, new regulations, new policies, investigations and legal proceedings and new interpretations of existing legal rules and regulations, in particular, changes in export control laws or exchange control laws, additional restrictions on doing business in countries subject to sanctions, and changes in laws in countries where we operate. In addition, changes and uncertainty in the political environments in which our businesses operate can have a material effect on the laws, rules, and regulations that affect our operations. Government disruptions may also delay or halt the granting and renewal of permits, licenses and other items required by us and our customers to conduct our business. The continued success of our global business and

BHGE LLC 2017 FORM 10-K | 12

operations depends, in part, on our ability to continue to anticipate and effectively manage these and other political, legal and regulatory risks.

Increased cybersecurity requirements, vulnerabilities, threats and more sophisticated and targeted computer crime could pose risks to our systems, networks, products, solutions, services and data.

Increased global cybersecurity vulnerabilities, threats and more sophisticated and targeted cyber-related attacks pose risks to our systems, networks, products, solutions, services and data. Cybersecurity attacks also pose risks to our customers’, partners’, suppliers’ and third-party service providers’ products, systems and networks and the confidentiality, availability and integrity of our and our customers’ data. While we attempt to mitigate these risks, we remain vulnerable to additional known or unknown threats. Given our global footprint, the large number of customers with which we do business, and the increasing sophistication of cyber attacks, a cyber attack could occur and persist for an extended period of time without detection. We expect that any investigation of a cyber attack would be inherently unpredictable and that it would take time before the completion of any investigation and before there is availability of full and reliable information. During such time we would not necessarily know the extent of the harm or how best to remediate it, and certain errors or actions could be repeated or compounded before they are discovered and remediated, all or any of which would further increase the costs and consequences of a cyber attack.

We also may have access to sensitive, confidential or personal data or information in certain of our businesses that is subject to privacy and security laws, regulations and customer-imposed controls. Despite our efforts to protect sensitive, confidential or personal data or information, we may be vulnerable to material security breaches, theft, misplaced or lost data, programming errors, employee errors and/or malfeasance that could potentially lead to the compromising of sensitive, confidential or personal data or information, improper use of our systems, software solutions or networks, unauthorized access, use, disclosure, modification or destruction of information, defective products, production downtimes and operational disruptions. In addition, a cyber-related attack could adversely impact our operating results and result in other negative consequences, including damage to our reputation or competitiveness, remediation or increased protection costs, litigation or regulatory action.

Our failure to comply with the Foreign Corrupt Practices Act (FCPA) and other similar laws could have a negative impact on our ongoing operations.

Our ability to comply with the FCPA, the U.K. Bribery Act and various other anti-bribery and anti-corruption laws depends on the success of our ongoing compliance program, including our ability to successfully manage our agents and business partners, and supervise, train and retain competent employees. Our compliance program depends on the efforts of our employees to comply with applicable law and our internal policies. We could be subject to sanctions and civil and criminal prosecution, as well as fines and penalties, in the event of a finding of a violation of any of these laws by us or any of our employees.

Anti-money laundering and anti-terrorism financing laws could have significant adverse consequences for us.

We maintain an enterprise-wide program designed to enable us to comply with all applicable anti-money laundering and anti-terrorism financing laws and regulations, including the Bank Secrecy Act and the Patriot Act. This program includes policies, procedures, processes and other internal controls designed to identify, monitor, manage and mitigate the risk of money laundering or terrorist financing posed by our products, services, customers and geographic locale. These controls establish procedures and processes to detect and report suspicious transactions, perform customer due diligence, respond to requests from law enforcement, and meet all recordkeeping and reporting requirements related to particular transactions involving currency or monetary instruments. We cannot be sure our programs and controls are or will remain effective to ensure our compliance with all applicable anti-money laundering and anti-terrorism financing laws and regulations, and our failure to comply could subject us to significant sanctions, fines, penalties and reputational harm, all of which could have a material adverse effect on our business, results of operations and financial condition.

Changes in tax laws or tax rates, adverse positions taken by taxing authorities and tax audits could impact operating results.

Changes in tax laws or tax rates, changes in interpretation of tax laws, the resolution of tax assessments or audits by various tax authorities, and the ability to fully utilize tax loss carryforwards and tax credits could impact our operating results, including additional valuation allowances for deferred tax assets. In addition, we may periodically

BHGE LLC 2017 FORM 10-K | 13

restructure our legal entity organization. If taxing authorities were to disagree with our tax positions in connection with any such restructurings, our effective tax rate could be materially impacted. Our tax filings for various periods will be subject to audit by the tax authorities in most jurisdictions where we conduct business. For example, tax assessments have been received from various taxing authorities and are currently at varying stages of appeals and/or litigation regarding these matters. These audits may result in assessment of additional taxes that are resolved with the authorities or through the courts. We believe these assessments may occasionally be based on erroneous and even arbitrary interpretations of local tax law. Resolution of any tax matter involves uncertainties and there are no assurances that the outcomes will be favorable.

Our operations involve a variety of operating hazards and risks that could cause losses.

The products that we manufacture and the services that we provide are complex, and the failure of our equipment to operate properly or to meet specifications may greatly increase our customers’ costs. In addition, many of these products are used in inherently hazardous industries, such as the offshore oilfield business. These hazards include blowouts, explosions, nuclear-related events, fires, collisions, capsizings and severe weather conditions. These hazards could result in personal injury and loss of life, severe damage to or destruction of property and equipment, pollution or environmental damage and suspension of operations, as well as adversely affect our brand and reputation which is a key asset to our business. We may incur substantial liabilities or losses as a result of these hazards. While we maintain insurance protection against some of these risks, and seek to obtain indemnity agreements from our customers requiring the customers to hold us harmless from some of these risks, our insurance and contractual indemnity protection may not be sufficient or effective to protect us under all circumstances or against all risks. The occurrence of a significant event, against which we were not fully insured or indemnified or the failure of a customer to meet its indemnification obligations to us, could materially and adversely affect our results of operations and financial condition.

Compliance with, and rulings and litigation in connection with, environmental regulations and the environmental impacts of our or our customers’ operations may adversely affect our business and operating results.

We and our business are impacted by material changes in environmental laws, regulations, rulings and litigation. Our expectations regarding our compliance with environmental laws and regulations and our expenditures to comply with environmental laws and regulations, including (without limitation) our capital expenditures for environmental control equipment, are only our forecasts regarding these matters. These forecasts may be substantially different from actual results, which may be affected by factors such as: changes in law that impose restrictions on air emissions, wastewater management, waste disposal, hydraulic fracturing, or wetland and land use practices; more stringent enforcement of existing environmental laws and regulations; a change in our share of any remediation costs or other unexpected, adverse outcomes with respect to sites where we have been named as a potentially responsible party, including (without limitation) Superfund sites; the discovery of other sites where additional expenditures may be required to comply with environmental legal obligations; and the accidental discharge of hazardous materials.

International, national, and state governments and agencies continue to evaluate and promulgate legislation and regulations that are focused on restricting emissions commonly referred to as greenhouse gas (GHG) emissions. In the United States, the U.S. Environmental Protection Agency (EPA) has taken steps to regulate GHG emissions as air pollutants under the U.S. Clean Air Act of 1970, as amended. The EPA’s Greenhouse Gas Reporting Rule requires monitoring and reporting of GHG emissions from, among others, certain mobile and stationary GHG emission sources in the oil and natural gas industry, which in turn may include data from certain of our wellsite equipment and operations. In addition, the U.S. government has proposed rules in the past setting GHG emission standards for, or otherwise aimed at reducing GHG emissions from, the oil and natural gas industry. Caps on carbon emissions, including in the United States, have been and may continue to be established and the cost of such caps could disproportionately affect the fossil-fuel energy sector. We are unable to predict whether the proposed changes in laws or regulations ultimately will occur or what they ultimately will require, and accordingly, we are unable to assess the potential financial or operational impact they may have on our business.

Other developments focused on restricting GHG emissions include the United Nations Framework Convention on Climate Change, which includes the Paris Agreement and the Kyoto Protocol; the European Union Emission Trading System; the United Kingdom’s CRC Energy Efficiency and ESOS schemes; and, in the United States, the Regional Greenhouse Gas Initiative, the Western Climate Action Initiative, and various state programs implementing the California Global Warming Solutions Act of 2006 (known as Assembly Bill 32).

BHGE LLC 2017 FORM 10-K | 14

Current or future legislation, regulations and developments, including those related to climate change, may curtail production and demand for hydrocarbons such as oil and natural gas in areas of the world where our customers operate, by shifting demand towards relatively lower carbon energy sources such as wind, solar and other renewables. Many governments are providing tax advantages and other subsidies and promoting technological research to support renewable energy sources, or are mandating the use of renewable fuels or technologies. These governmental initiatives, as well as increased societal awareness of climate change impacts, have also resulted in increased investor and consumer demand for renewable energy. Any resulting reduction in demand for oil and natural gas could adversely affect future demand for our services and products, which may in turn adversely affect future results of operations.

Uninsured claims and litigation against us could adversely impact our operating results.

We could be impacted by the outcome of pending litigation, as well as unexpected litigation or proceedings. While we have insurance coverage against operating hazards, including product liability claims and personal injury claims related to our products, to the extent deemed prudent by our management and to the extent insurance is available; no assurance can be given that the nature and amount of that insurance will be sufficient to fully indemnify us against liabilities arising out of pending and future claims and litigation. This insurance has deductibles or self-insured retentions and contains certain coverage exclusions. The insurance does not cover damages from breach of contract by us or based on alleged fraud or deceptive trade practices. In addition, the following risks apply with respect to our insurance coverage:

• | we may not be able to continue to obtain insurance on commercially reasonable terms; |

• | we may be faced with types of liabilities that will not be covered by our insurance; |

• | our insurance carriers may not be able to meet their obligations under the policies; or |

• | the dollar amount of any liabilities may exceed our policy limits. |

Control of oil and natural gas reserves by state-owned oil companies may impact the demand for our services and products and create additional risks in our operations.

Much of the world’s oil and natural gas reserves are controlled by state-owned oil companies. State-owned oil companies may require their contractors to meet local content requirements or other local standards, such as conducting our operations through joint ventures with local partners that could be difficult or undesirable for us to meet. The failure to meet the local content requirements and other local standards may adversely impact our operations in those countries. In addition, our ability to work with state-owned oil companies is subject to our ability to negotiate and agree upon acceptable contract terms.

Providing services on an integrated or turnkey basis could require us to assume additional risks.

Many state-owned oil companies and other operators may require integrated contracts or turnkey contracts and we may choose to provide services outside our core business. Providing services on an integrated or turnkey basis may subject us to additional risks, such as costs associated with unexpected delays or difficulties in drilling or completion operations and risks associated with subcontracting arrangements.

Some of our customers require bids in the form of long-term, fixed pricing contracts.

Some of our customers require bids for contracts in the form of long-term, fixed pricing contracts that may require us to provide integrated project management services outside our normal discrete business and to act as project managers, as well as service providers, and may require us to assume additional risks associated with cost over-runs. These customers may provide us with inaccurate information in relation to their reserves. The estimation of reserves is a process that involves subjective judgment about likely location and volume, and estimates that prove inaccurate may result in cost over-runs, delays, and project losses for us or our customers, which may adversely impact our business.

Providing services on an integrated basis may also require us to assume additional risks associated with operating cost inflation, labor availability and productivity, supplier pricing and performance, and potential claims for liquidated damages. We typically rely on third-party subcontractors and equipment providers to assist us with the

BHGE LLC 2017 FORM 10-K | 15

completion of these types of contracts. To the extent that we cannot engage subcontractors or acquire equipment or materials in a timely manner and on reasonable terms, our ability to complete a project in accordance with stated deadlines or at a profit may be impaired. If the amount we are required to pay for these goods and services exceeds the amount we have estimated in bidding for fixed-price work, we could experience losses in the performance of these contracts. These delays and additional costs may be substantial and we may be required to compensate our customers for these delays. This may reduce the profit to be realized or result in a loss on a project or harm to our relationships with our customers.

The credit risks of having a concentrated customer base in the energy industry could result in losses.

Having a concentration of customers in the energy industry may impact our overall exposure to credit risk as our customers may be similarly affected by prolonged changes in economic and industry conditions. Some of our customers may experience extreme financial distress as a result of falling commodity prices and may be forced to seek protection under applicable bankruptcy laws, which may affect our ability to recover any amounts due from such customers. Furthermore, countries that rely heavily upon income from hydrocarbon exports have been and may in the future be negatively and significantly affected by a drop in oil prices, which could affect our ability to collect from our customers in these countries, particularly national oil companies. Laws in some jurisdictions in which we will operate could make collection difficult or time consuming. We will perform ongoing credit evaluations of our customers and do not expect to require collateral in support of our trade receivables. While we maintain reserves for potential credit losses, we cannot assure such reserves will be sufficient to meet write-offs of uncollectible receivables or that our losses from such receivables will be consistent with our expectations. Additionally, in the event of a bankruptcy of any of our customers, we may be treated as an unsecured creditor and may collect substantially less, or none, of the amounts owed to us by such customer.

Our backlog is subject to modification, termination or reduction of orders, which could negatively impact our sales.

Our backlog is comprised of unfilled customer orders for products and product services (expected life of contract sales for product services). Our backlog can be significantly affected by the timing of orders for large projects. Although modifications and terminations of orders may be partially offset by cancellation fees, customers can, and sometimes do, terminate or modify orders. Our failure to replace canceled orders could negatively impact our sales and results of operations. The total dollar amount of the Company’s backlog as of December 31, 2017 was $21,022 million.

We may not be able to satisfy technical requirements, testing requirements or other specifications required under our service contracts and equipment purchase agreements.

Our products are used in deepwater and other harsh environments and severe service applications. Our contracts with customers and customer requests for bids typically set forth detailed specifications or technical requirements for our products and services, which may also include extensive testing requirements. We anticipate that such testing requirements will become more common in our contracts. In addition, recent scrutiny of the offshore drilling industry has resulted in more stringent technical specifications for our products and more comprehensive testing requirements for our products to ensure compliance with such specifications. We cannot provide assurance that our products will be able to satisfy the specifications or that we will be able to perform the full-scale testing necessary to prove that the product specifications are satisfied in future contract bids or under existing contracts, or that the costs of modifications to our products to satisfy the specifications and testing will not adversely affect our results of operations. If our products are unable to satisfy such requirements, or we are unable to perform any required full-scale testing, our customers may cancel their contracts and/or seek new suppliers, and our business, results of operations, cash flows or financial position may be adversely affected.

Currency fluctuations or devaluations may impact our operating results.

Fluctuations or devaluations in foreign currencies relative to the U.S. dollar can impact our revenue and our costs of doing business, as well as the costs of doing business of our customers. Most of our products and services are sold through contracts denominated in U.S. dollars or local currency indexed to U.S. dollars, however, some of our revenue, local expenses and manufacturing costs are incurred in local currencies and therefore changes in the exchange rates between the U.S. dollar and foreign currencies can increase or decrease our revenue and expenses reported in U.S. dollars or revenue and expenses of our customers and, consequently, may impact the ability of our customers to satisfy their payment obligations and our results of operations.

BHGE LLC 2017 FORM 10-K | 16

Changes in economic and/or market conditions may impact our ability to borrow and/or cost of borrowing.