UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2018

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 1-13738

PSYCHEMEDICS CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 58-1701987 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

| 289 Great Road Acton, Massachusetts |

01720 | |

| (Address of Principal Executive Offices) | (Zip Code) |

Registrant’s Telephone Number Including Area

Code: (978) 206-8220

Securities registered pursuant to Section 12(b) of the Act:

| Title of Class | Name of each exchange on which registered: | |

| Common Stock, $0.005 par value | The Nasdaq Stock Market L.L.C. |

Securities registered pursuant to Section 12(g)

of the Act: None

Indicate by a check mark if the registrant is a well-known seasoned issuer (as defined in Rule 405 of the Securities Exchange Act of 1934). Yes o No x

Indicate by a check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934). Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files.) Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or emerging growth company. See definitions of “accelerated filer”, “large accelerated filer”, “non-accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Securities Exchange Act of 1934.

| Large Accelerated Filer o | Accelerated Filer x | Non-Accelerated Filer o | ||

| Smaller Reporting Company x | Emerging Growth Company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by a check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities and Exchange Act of 1934). Yes o No x

As of June 30, 2018, there were 5,507,262 shares of Common Stock of the Registrant outstanding. The aggregate market value of the Common Stock of the Registrant held by non-affiliates (assuming for these purposes, but not conceding, that all executive officers, directors and 5% shareholders are “affiliates” of the Registrant) as of June 30, 2018 was approximately $76 million, computed based upon the closing price of $19.24 per share on June 30, 2018.

As of March 4, 2019, there were 5,507,262 shares of Common Stock of the Registrant outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Annual Report on Form 10-K incorporates by reference portions of the Registrant’s definitive proxy statement, to be filed with the Securities and Exchange Commission no later than 120 days after the close of its fiscal year; provided that if such proxy statement is not filed with the Commission in such 120-day period, an amendment to this Form 10-K shall be filed no later than the end of the 120-day period.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Some of the statements under “Business,” “Risk Factors,” “Legal Proceedings,” “Market for Registrant’s Common Stock and Related Stockholder Matters” and “Management Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this Annual Report on Form 10-K (this “Form 10-K”) constitute forward-looking statements under Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, including statements made with respect to future earnings, earnings per share, revenues, operating income, cash flows, competitive and strategic initiatives, potential stock repurchases, liquidity needs, dividends, future business, growth opportunities, profitability, pricing, new accounts, customer base, market share, test volume, sales volume, sales and marketing strategies, U.S. and foreign drug testing laws and regulations and the enforcement of such laws and regulations, required investments in plant, equipment and people, new test development, and contingencies, including litigation results. These statements involve known and unknown risks, uncertainties and other factors that may cause results, levels of activity, growth, performance, earnings per share or achievements to be materially different from any future results, levels of activity, growth, performance, earnings per share or achievements expressed or implied by such forward-looking statements.

The forward-looking statements included in this Form 10-K and referred to elsewhere are related to future events or our strategies or future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may,” “should,” “believe,” “anticipate,” “future,” “potential,” “estimate,” “encourage,” “opportunity,” “growth,” “leader,” “could”, “expect,” “intend,” “plan,” “expand,” “focus,” “through,” “strategy,” “provide,” “offer,” “allow,” “commitment,” “implement,” “result,” “increase,” “establish,” “perform,” “make,” “continue,” “can,” “ongoing,” “include” or the negative of such terms or comparable terminology. All forward-looking statements included in this Form 10-K are based on information available to us as of the filing date of this report, and the Company assumes no obligation to update any such forward-looking statements. Our actual results could differ materially from the forward-looking statements.

Factors that may cause such differences include but are not limited to: (1) intense competition in the drug testing industry, particularly among companies that test utilizing hair samples; (2) risks associated with the development of markets for new products and services offered; (3) pricing policies; (4) risks associated with capacity expansion; (5) risks associated with U.S. government regulations, including, but not limited to, FDA regulations, (6) risks associated with our international operations, including, but not limited to, Brazilian laws, proposed laws and regulations, market development and currency risks; (7) Psychemedics' ability to maintain its reputation and brand image; (8) the ability of Psychemedics to achieve its business plans, productivity improvements, cost controls, leveraging of its global operating platform, and acceleration of the rate of innovation; (9) information technology system failures and data security breaches; (10) the uncertain global economy; (11) our ability to attract, develop and retain executives and other qualified employees and independent contractors, including distributors; (12) Psychemedics' ability to obtain and protect intellectual property rights; (13) litigation risks; and (14) changes in economic conditions which affect demand for our products and services.

Additional important factors that could cause actual results to differ materially from expectations reflected in our forward-looking statements include those described in Item 1A, “Risk Factors.”

i

PSYCHEMEDICS CORPORATION

FORM 10-K

ANNUAL REPORT

For the Year Ended December 31, 2018

ii

Available Information; Background

Psychemedics Corporation (together with its subsidiaries, “the Company” or “Psychemedics”) maintains executive offices located at 289 Great Road, Acton, MA 01720. Our telephone number is (978) 206-8220. Our stock is traded on the NASDAQ Stock Market under the symbol “PMD”. Our Internet address is www.psychemedics.com. The Company makes available, free of charge, on the Investor Information section of its website, its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports as soon as reasonably practicable after such material is electronically filed with the Securities and Exchange Commission (the “SEC”). Copies are also available, without charge, from Psychemedics Corporation, Attn: Investor Relations, 289 Great Road, Acton, MA 01720. Alternatively, reports filed with the SEC may be viewed or obtained at the SEC Public Reference Room in Washington, D.C., or the SEC’s Internet site at www.sec.gov. We do not intend for information contained in our website to be part of this Annual Report on Form 10-K.

General

Psychemedics Corporation is a Delaware corporation organized on September 24, 1986. The consolidated financial statements of the Company include the accounts and results of operations of Psychemedics Corporation and its wholly-owned subsidiary Psychemedics International, LLC (Delaware) and their jointly-owned subsidiary Psychemedics Laboratórios Ltda (Brazil). All significant inter-company balances and transactions have been eliminated in consolidation. A majority of the Company’s assets are located within the United States. The Company provides testing services for the detection of drugs of abuse through the analysis of hair samples. The Company’s testing methods utilize a patented technology that digests the hair and releases drugs trapped in the hair without destroying the drugs. This is fundamental to the entire process because the patented method gets virtually 100% of the drug out of the hair, and if you cannot get the drug out of the hair, you cannot measure it. The Company then performs a proprietary custom-designed enzyme immunoassay (EIA) on the liquid supernatant, with confirmation testing by mass spectrometry.

The Company’s primary application of its patented technology is as a testing service that analyzes hair samples for the presence of certain drugs of abuse. The Company’s customized proprietary EIA procedures to drug test hair samples differ from the more commonly used immunoassay procedures employed to test urine samples. The Company’s tests provide quantitative information that can indicate the approximate amount of drug ingested as well as historical data, which can show a pattern of individual drug use over a longer period of time, thereby providing superior detection compared to other types of drug testing. This information is useful to employers for both applicant and employee testing, as well as treatment professionals, law enforcement agencies, school administrators, and parents concerned about their children’s drug use. The Company provides screening and confirmation by mass spectrometry using industry-accepted practices for cocaine, marijuana, PCP, amphetamines (including ecstasy, eve and Adderall), opiates (including heroin, hydrocodone, hydromorphone, oxycodone, oxymorphone and codeine), synthetic cannabinoids (including K2, Spice, Blaze) and benzodiazepines (Xanax®, Valium®, and Ativan®). In addition, in 2013, the Company launched a hair test for alcohol which also looks back on use over a 90 day period, as our hair drug tests do.

Testing services are currently performed at the Company’s Culver City, California campus located at 5832 Uplander Way and 6100 Bristol Parkway.

Background on Drug Testing with Hair

When certain chemical substances enter the bloodstream, the blood carries these substances to the hair where they become “entrapped” in the protein matrix in amounts approximately proportional to the amount ingested. The Company utilizes a patented drug extraction method followed by a unique enzyme immunoassay (EIA) procedure to identify drugs in the hair. The patented drug extraction method effectively releases drugs from the hair without destroying the drugs, getting virtually 100% of the drug out of the hair. The patented method can be used with a broad range of immunoassay screen techniques and mass spectrometry methods.

The immunoassays produced by the Psychemedics R&D team were uniquely designed specifically to meet and even exceed the standards of radioimmunoassay (“RIAH”), the original testing method created and utilized by the Company prior to 2013. Because Psychemedics is the only hair testing laboratory that manufactures its own screening assays, it has full control over all aspects of its technology, and that powerful advantage facilitated the Company's creation of its EIA assays with equivalence to its own previously FDA-cleared radioimmunoassays.

The EIA screened positive results are then confirmed by mass spectrometry. Depending upon the length of hair, the Company is able to provide historical information on drug use by the person from whom the sample was obtained. Because head hair grows approximately 1.3 centimeters per month, a 3.9 centimeter head hair sample can reflect drug ingestion over the approximate three months prior to the collection of the sample. Another option is sectional analysis of the head hair sample, in which the hair is sectioned into lengths which approximately correspond to certain time periods, thereby providing information on patterns of drug use.

| 1 |

Validation of the Company’s Proprietary Testing Methods

The process of analyzing human hair for the presence of drugs has been the subject of numerous peer-reviewed, scientific field studies. Many of the studies have been funded by the National Institute of Justice or the National Institute on Drug Abuse (“NIDA”). Several hundred research articles written by independent researchers have been published supporting the general validity and usefulness of hair analysis.

Some of the Company’s customers have also completed their own testing to validate the Company’s hair test results compared to other companies’ urine test results. These studies consistently confirmed the Company’s superior detection rate compared to urinalysis testing. When results from the Company’s hair testing methods were compared to urine results in side-by-side evaluations, 5 to 10 times as many drug abusers were accurately identified by the Company’s proprietary methods.

In 1998, the National Institute of Justice, utilizing Psychemedics’ previously utilized RIAH hair testing assay, completed a Pennsylvania Prison study where hair analysis revealed an average prison drug use level of approximately 7.9% in 1996. Comparatively, urinalysis revealed virtually no positives. After measures to curtail drug use were instituted (drug-sniffing dogs, searches and scanners), the use level fell to approximately 2% according to the results of hair analysis in 1998. Again, the urine tests showed virtually no positives. The study illustrates the usefulness of hair analysis to monitor populations and the weakness of urinalysis.

The Company has received 510k clearance from the Food and Drug Administration (FDA) on eight EIA assays used to test head and body hair for drugs of abuse.

The Company’s decontamination wash protocol and the effects in eliminating surface contamination were analyzed in a study conducted by scientists at the Laboratory of the Federal Bureau of Investigation and published in August 2014 in the Journal of Analytical Toxicology. The FBI concluded that the use of an extended wash protocol of the type used by the Company will exclude false positive results from environmental contact with cocaine. In the study, the FBI cited Psychemedics’ studies published in 1993, 2002, 2004, and 2005, and named our lab director, Dr. Michael Schaffer, and our lab, in its acknowledgments. The FBI study also supported the use of metabolites known as hydroxycocaines as evidence of ingestion. These metabolites were first identified in hair by Psychemedics.

Advantages of Using the Company’s Patented Method

The Company asserts that hair testing using its patented method confers substantive advantages over detection through urinalysis. Although urinalysis testing can provide accurate drug use information, the scope of the information is short-term and is generally limited to the type of drug ingested within a few days of the test. Studies published in many scientific publications have indicated that most drugs disappear from urine within a few days.

In contrast to urinalysis testing, hair testing using the Company’s patented method can provide long-term historical drug use information resulting in a significantly wider window of detection. This window may be several months or longer depending on the length of the hair sample. The Company’s standard test offering, however, uses a 3.9 centimeter length head hair sample cut close to the scalp, which measures use for approximately three months prior to collection of the sample.

This wider window enhances the detection efficiency of hair analysis, making it particularly useful in pre-employment and random testing. Hair testing not only identifies more drug users, but it may also uncover patterns and severity of drug use (information most helpful in determining the scope of an individual’s involvement with drugs), while serving as a deterrent against drug use. Hair testing employing the Company’s patented method greatly reduces the incidence of “false negatives” associated with evasive measures typically encountered with urinalysis testing. For example, urinalysis test results are adversely impacted by excessive fluid intake prior to testing and by adulteration or substitution of the urine sample. Moreover, a drug user who abstains from use for a few days prior to urinalysis testing can usually escape detection. Hair testing is effectively free of these problems, as it cannot be thwarted by evasive measures typically encountered with urinalysis testing. Hair testing is also attractive to customers since sample collection is typically performed under close supervision yet is less intrusive and less embarrassing for test subjects.

Hair testing using the Company’s patented method (with mass spectrometry confirmation) further reduces the prospects of error in conducting drug detection tests. Urinalysis testing is more susceptible to problems such as “evidentiary false positives” resulting from passive drug exposure or poppy seeds. To combat this problem, in federally mandated testing, the opiate cutoff levels for urine testing were raised 667% (from 300 to 2,000 ng/ml) on December 1, 1998, and testing for the presence of a heroin metabolite, 6-MAM, was required. These requirements, however, effectively reduced the detection time frame for confirmed heroin use, such that 6-MAM in urine can typically only be detected for several hours post drug use. In contrast, the metabolite 6-MAM is stable in hair and can be detected for months.

In the event a positive urinalysis test result is challenged, a test on a newly collected urine sample is not a viable remedy. Unless the forewarned individual continues to use drugs prior to the date of the newly collected sample, a re-test may yield a negative result when using urinalysis testing because of temporary abstinence. In contrast, when the Company’s hair testing method is offered on a repeat hair sample, the individual suspected of drug use cannot as easily affect the results because historical drug use data remains locked in the hair fiber.

When compared to other hair testing methods, not only are the Company’s assays cleared by the FDA for head and body hair, they also employ a unique patented method of digesting hair that the Company believes allows for the most efficient release of drugs from the hair without destroying the drugs. The Company’s method of releasing drugs from hair is a key advantage and results in superior detection rates.

| 2 |

Disadvantages of Hair Testing

There are some disadvantages of hair testing as compared to drug detection through urinalysis. Because hair starts growing below the skin surface, drug ingestion evidence does not appear in hair above the scalp until approximately five to seven days after use.

Thus, hair testing is not suitable for determining drug presence in “for cause” testing as is done in connection with an accident investigation. It does, however, provide a drug history which can complement urinalysis information in “for cause” testing.

The Company’s prices for its tests are generally somewhat higher than prices for tests using urinalysis, but the Company believes that its superior detection rates provide more value to the customer. This pricing policy could, however, adversely impact the growth of the Company’s sales volume.

Hair Alcohol Testing

In 2013, the Company launched a test for alcohol using hair. This test measures average alcohol consumption over a period of approximately three months, indicates the approximate level of alcohol use during that time period, and can provide a behavioral indication of excessive use. The test measures the amount of ethyl glucuronide (EtG) in the hair – a trace metabolite of ethanol and a direct alcohol biomarker.

Intellectual Property

Certain aspects of the hair analysis method currently used by the Company are covered by US and foreign patents owned by the Company. The Company has been granted a total of ten US patents, including a patent issued to the Company in 2011 that focuses on digesting hair and releasing drugs trapped in the hair without destroying the drugs. This patent can be used with a broad range of immunoassay screen techniques, mass spectrometry methods, and chromatographic procedures. In 2012, the Company received an additional patent that extended the range of the patent received in 2011. Additional patent applications are currently pending in the U.S. and internationally.

The Company also relies on trade secrets to protect certain aspects of its proprietary technology. The Company’s ability to protect the confidentiality of its trade secrets is dependent upon the Company’s internal safeguards and upon the laws protecting trade secrets and unfair competition.

In the event that patent protection or protection under the laws of trade secrets is not sufficient and the Company’s competitors succeed in duplicating the Company’s products, the Company’s business could be materially adversely affected.

Target Markets

Workplace

The Company focuses its primary marketing efforts on the private sector, with particular emphasis on job applicant and employee testing.

Most businesses use drug testing to screen job applicants and employees. The Hazeldon Foundation survey from 2007 indicated that 85 percent of human resource (“HR”) professionals believe that drug testing is an effective way to identify substance abuse. The prevalence of drug screening programs reflects a concern that drug use contributes to employee health problems and costs (as the same study found that 62 percent of HR professionals believe that absenteeism is the most significant problem caused by substance abuse and addiction, followed at 49 percent by reduced productivity, a lack of trustworthiness at 39 percent, a negative impact on the company’s external image at 32 percent, missed deadlines at 31 percent, and in certain industries, safety hazards.) It has been estimated that the cost to American businesses is more than $100 billion annually.

The principal criticism of employee drug testing programs centers on the effectiveness of the testing program. Most private sector testing programs use urinalysis. Such programs are susceptible to evasive maneuvers and the inability to obtain confirmation through repeat samples in the event of a challenged result. An industry has developed over the Internet, and through direct mail, marketing a wide variety of adulterants, dilutants, clean urine and devices to assist drug users in falsifying urine test results.

Moreover, scheduled tests such as pre-employment testing and some random testing programs provide an opportunity for many drug users to simply abstain for a few days in order to escape detection by urinalysis.

The Company presents its patented hair analysis method to potential clients as a better technology well suited to employer needs. Field studies and actual client results support the accuracy and superior effectiveness of the Company’s patented technology and its ability to detect varying levels of drug use.

The Company performs a confirmation test of all screened positive results through mass spectrometry. The use of mass spectrometry is an industry accepted practice used to confirm a positive test result from the screening process. The Company offers its clients an expanded drug screen with mass spectrometry confirmation of cocaine, PCP, marijuana, amphetamines, opiates, synthetic cannabinoids and benzodiazepines. In addition, the Company offers a hair test for alcohol which also looks back on use over a 90 day period, as our hair drug tests do.

| 3 |

Professional Drivers

In 2016, Brazil started drugs of abuse testing for all professional drivers in the country using a hair test. This is a mandated program from a law passed in 2015. In the United States, a similar requirement exists for professional drivers, however, a urine test is currently required. The U.S. government is currently evaluating alternative mediums for testing of drugs of abuse for professional drivers, including hair.

Schools

The Company currently serves hundreds of schools throughout the United States and in several foreign countries. The Company offers its school clients the same five-drug screen with mass spectrometry confirmation that is used with the Company’s workplace testing service.

Parents

The Company also offers a personal drug testing service, known as “PDT-90”®, for parents concerned about drug use by their children. It allows parents to collect a small sample of hair from their child in the privacy of the home, send it to the Company’s laboratory and have it tested for drugs of abuse by the Company. The PDT-90 testing service uses the same patented method that is used with the Company’s workplace testing service.

Research

The Company is involved in the following ongoing studies involving use of drugs of abuse in various populations: In 2017, the Company partnered with an NIH-funded study titled “Adolescent Brain Cognitive Development” (ABCD) which expects to enroll 12,000 youth age 9-10 over a 2-2.5 year recruitment period. The objective of the ABCD consortium is to establish a national, multisite, longitudinal cohort and database by studying youth prospectively in order to examine brain and cognitive development in children and adolescents through a period (10 years) when significant development of intellectual and emotional functions occurs. Psychemedics’ role in this study is to test hair to detect use of drugs over the time period. The Company is also partnering with Olin Neuropsychiatry Research Center Institute of Living Hartford Hospital in a research study entitled, “Neurochemical and Functional Correlates of Memory in Emerging Adult Marijuana Users.” The study is aiming to better characterize the impact of heavy marijuana use on memory and is funded by a grant from NIDA.

Geographic Scope

Revenues outside the United States were 32% of consolidated revenues for 2018 and 34% for 2017 and 2016.

Distribution

The Company markets its corporate drug testing services through its own sales force and through distributors. The Company markets its home drug testing service, PDT-90, through the internet.

The business in Brazil is sold exclusively through one independently owned and operated distributor which is only engaged in the sale of the Psychemedics tests.

In 2016, the Company was certified as a Center of Excellence by BenchmarkPortal for its customer service function. Customer service is a key component to the sales and support function and this certification validates the efforts by the Company to support our customers. The Company was recertified in 2017 and 2018.

Significant Customers

The Company had one customer, Psychemedics Brasil (an independent distributor in Brazil) that represented 31%, 33% and 34% of total revenue for the years ended December 31, 2018, 2017 and 2016, respectively. Psychemedics Brasil also accounted for 20% and 23% of the total accounts receivable balance as of December 31, 2018 and 2017, respectively.

Competition

The Company competes directly with numerous commercial laboratories that test for drugs primarily through urinalysis testing. Most of these laboratories, such as Quest Diagnostics, have substantially greater financial resources, market identity, marketing organizations, facilities, and more personnel than the Company. The Company has been steadily increasing its base of corporate customers and believes that future success with new customers is dependent on the Company’s ability to communicate the advantages of implementing a drug program utilizing the Company’s patented hair analysis method.

The Company’s ability to compete is also a function of pricing. The Company’s prices for its tests are generally somewhat higher than prices for tests using urinalysis. However, the Company believes that its superior detection rates, coupled with the customer’s ability to test less frequently due to hair testing’s wider window of detection (several months versus approximately three days with urinalysis), provide more value to the customer. This pricing policy could, however, lead to slower sales growth for the Company.

The Company also competes with other hair testing laboratories. The Company distinguishes itself from hair testing competitors by emphasizing the superior results the Company obtains through use of its unique patented extraction method (getting drug out of the hair), in combination with the Company’s FDA cleared immunoassay screen.

| 4 |

Government Regulation

The Company is licensed as a clinical laboratory by the State of California as well as certain other states. All tests are performed according to the laboratory standards established by the Department of Health and Human Services, through the Clinical Laboratories Improvement Amendments (“CLIA”), and various state licensing statutes.

A substantial number of states regulate drug testing. The scope and nature of such regulations varies greatly from state to state and is subject to change from time to time. The Company addresses state law issues on an ongoing basis.

The Federal Food, Drug and Cosmetic Act, as amended (the “FDC Act”) requires companies engaged in the business of testing for drugs of abuse using a test (screening assay) not previously recognized by the FDA to submit their assay to the FDA for recognition prior to marketing. In addition, the laboratory performing the tests is required to be certified by a recognized agency. In 2002, the Company received 510k clearance to market all five of its assays utilizing RIAH technology.

In 2008, the Company received the first CAP (College of American Pathologists) certification specifically including hair testing.

In 2011, the Company received ISO/IEC 17025 International Accreditation for a broad spectrum of laboratory testing including drugs of abuse and forensics in hair and urine specimens. ISO/IEC 17025 accreditation provides formal recognition to laboratories that demonstrate technical competency and maintains this recognition through periodic evaluations to ensure continued compliance.

In 2012, the Company received 510k clearance from the FDA to market five of its assays utilizing the Company’s custom developed EIA technology.

In 2013, the Company received 510k clearance from the FDA to market two additional assays utilizing the Company’s custom developed EIA technology.

In 2015, the Brazilian government signed into law a requirement for professional drivers to take a hair drug test when obtaining or renewing their driver's license. The law also requires professional drivers to be tested when they are hired or fired.

In 2016, the Company received accreditation from the Standards Council of Canada as an accredited testing laboratory.

In 2017, the Company received 510k clearance from the FDA to market one additional assay utilizing the Company’s custom developed EIA technology.

Research and Development

The Company is continuously engaged in research and development activities. During the years ended December 31, 2018, 2017 and 2016, $1.6 million, $1.4 million and $1.4 million, respectively, were expended for research and development. The Company continues to perform research activities to develop new products and services and to improve existing products and services utilizing the Company’s proprietary technology. The Company also continues to evaluate methodologies to enhance its drug screening capabilities. Additional research using the Company’s proprietary technology is being conducted by outside research organizations through government-funded studies.

Employees

As of December 31, 2018, the Company had 250 employees, six of whom are in R&D and one in Brazil. None of the Company’s employees are subject to a collective bargaining agreement.

| 5 |

In addition to other information contained in this Form 10-K, the following risk factors should be carefully considered in evaluating Psychemedics Corporation and its business because such factors could have a significant impact on our business, operating results and financial condition. These risk factors could cause actual results to materially differ from those projected in any forward-looking statements.

Companies may develop products that compete with our products and some of these companies may be larger and better capitalized than we are.

Many of our competitors and potential competitors are larger and have greater financial resources than we do and offer a range of products broader than our products. Some of the companies with which we now compete or may compete in the future may develop more extensive research and marketing capabilities and greater technical and personnel resources than we do, and may become better positioned to compete in an evolving industry. Inability to compete successfully could harm our business and prospects.

Increased competition, including price competition, could have a material impact on the Company’s net revenues and profitability.

Our business is intensely competitive, both in terms of price and service. Pricing of drug testing services is a significant factor often considered by customers in selecting a drug testing laboratory. As a result of the clinical laboratory industry undergoing significant consolidation, larger clinical laboratory providers are able to increase cost efficiencies afforded by large-scale automated testing. This consolidation results in greater price competition. The Company may be unable to increase cost efficiencies sufficiently, if at all, and as a result, its net earnings and cash flows could be negatively impacted by such price competition. The Company may also face increased competition from companies that do not comply with existing laws or regulations or otherwise disregard compliance standards in the industry. Additional competition, including price competition, could have a material adverse impact on the Company’s net revenues and profitability. The Company operations in Brazil are subject to price pressures as this is a new market with new competitors entering the market. The Company may also face changes in fee schedules, competitive bidding for laboratory services or other actions or pressures reducing payment schedules as a result of increased or additional competition.

Our results of operations are subject in part to variation in our customers’ hiring practices and other factors beyond our control.

Our results of operations have been and may continue to be subject to variation in our customers’ hiring practices, which in turn is dependent, to a large extent, on the general condition of the economy. Results for a particular quarter may vary due to a number of factors, including:

| • | economic conditions in our markets in general; |

| • | economic conditions affecting our customers and their particular industries; |

| • | the introduction of new products and product enhancements by us or our competitors; and |

| • | pricing and other competitive conditions. |

A failure to obtain and retain new customers, or a loss of existing customers, or a reduction in tests ordered, could impact the Company’s ability to successfully grow its business.

The Company needs to obtain and retain new customers. In addition, a reduction in tests ordered, without offsetting growth in its customer base, could impact the Company’s ability to successfully grow its business and could have a material adverse impact on the Company’s net revenues and profitability. We compete primarily on the basis of the quality of testing, reputation in the industry, the pricing of services and ability to employ qualified personnel. The Company’s failure to successfully compete on any of these factors could result in the loss of customers and a reduction in the Company’s ability to expand its customer base. See also the risk factor entitled, “We are subject to numerous political, legal, operational and other risks as a result of our international operations which could impact our business in many ways.”

Our business could be harmed if we are unable to protect our technology.

We rely primarily on a combination of trade secrets, patents and trademark laws and confidentiality procedures to protect our technology. Despite these precautions, unauthorized third parties may infringe or copy portions of our technology. In addition, because patent applications in the United States are not publicly disclosed until either (1) 18 months after the application filing date or (2) the publication date of an issued patent wherein applicant(s) seek only US patent protection, applications not yet disclosed may have been filed which relate to our technology. Moreover, there is a risk that foreign intellectual property laws will not protect our intellectual property rights to the same extent as United States intellectual property laws. In the absence of the foregoing protections, we may be vulnerable to competitors who attempt to copy our products, processes or technology.

Our business could be affected by IT system failures or Cybersecurity breaches.

A computer or IT system failure could affect our ability to perform tests, report test results or properly bill customers. Failures could occur as a result of the standardization of our IT systems and other system conversions, telecommunications failures, malicious human acts (such as electronic break-ins or computer viruses) or natural disasters. Sustained system failures or interruption of the Company’s systems in one or more of its operations could disrupt the Company’s ability to process and provide test results in a timely manner and/or bill the appropriate party. Failure of the Company’s information systems could adversely affect the Company’s business, profitability and financial condition.

| 6 |

Our technologies, systems and networks may be subject to cybersecurity breaches. Although we have experienced occasional, actual or attempted breaches of our cybersecurity, none of these breaches has had a material effect on our business, operations or reputation. If our systems for protecting against cybersecurity risks prove to be insufficient, we could be adversely affected by having our business systems compromised, our proprietary information altered, lost or stolen, or our business operations disrupted. As cyber attacks continue to evolve, we may be required to expend significant additional resources to continue to modify or enhance our protective measures or to investigate and remediate any information systems and related infrastructure security vulnerabilities.

Failure to maintain confidential information could result in a significant financial impact.

The Company maintains confidential information regarding the results of drug tests and other information including credit card and payment information from our customers. The failure to protect this information could result in lawsuits, fines or penalties. Any loss of data or breach of confidentiality, such as through a computer security breach, could expose the Company to a financial liability.

Our future success will depend on the continued services of our key personnel.

The loss of any of our key personnel could harm our business and prospects. We may not be able to attract and retain personnel necessary for the development of our business. We do not have key personnel under contract other than 3 officers who have agreements providing for severance and non-compete covenants in the event of termination of employment following a change of control. Further, we do not have any key man life insurance for any of our officers or other key personnel.

There is a risk that our insurance will not be sufficient to protect us from errors and omissions liability or other claims, or that in the future errors and omissions insurance will not be available to us at a reasonable cost, if at all.

Our business involves the risk of claims of errors and omissions and other claims inherent to our business. We maintain errors and omissions and general liability insurance subject to deductibles and exclusions. There is a risk that our insurance will not be sufficient to protect us from all such possible claims. An under-insured or uninsured claim could harm our operating results or financial condition.

Our research and development capabilities may not produce viable new services or products.

In order to remain competitive, we need to continually improve our products, develop new technologies to replace older technologies that have either become obsolete or for which patent protection is no longer available. It is uncertain whether we will continually be able to develop services that are more efficient, effective or that are suitable for our customers. Our ability to create viable products or services depends on many factors, including the implementation of appropriate technologies, the development of effective new research tools, the complexity of the chemistry and biology, the lack of predictability in the scientific process and the performance and decision-making capabilities of our scientists. There is no guarantee that our research and development teams will be successful in developing improvements to our technology.

Improved testing technologies, or the Company’s customers using new technologies to perform their own tests, could adversely affect the Company’s business.

Advances in technology may lead to the development of more cost-effective technologies that can be operated by third parties or customers themselves in their own offices, without requiring the services of a freestanding laboratory. Development of such technology and its use by the Company’s customers could reduce the demand for its testing services and negatively impact our revenues.

We may not be able to recruit and retain the experienced scientists and management we need to compete in our industry.

Our future success depends upon our ability to attract, retain and motivate highly skilled scientists and management. Our ability to achieve our business strategies depends on our ability to hire and retain high caliber scientists and other qualified experts. We compete with other testing companies, research companies and academic and research institutions to recruit personnel and face significant competition for qualified personnel. We may incur greater costs than anticipated, or may not be successful, in attracting new scientists or management or in retaining or motivating our existing personnel.

Our future success also depends on the personal efforts and abilities of the principal members of our senior management and scientific staff to provide strategic direction, to manage our operations and maintain a cohesive and stable environment.

Our facilities and practices may fail to comply with government regulations.

Our testing facilities and processes must be operated in conformity with current government regulations. These requirements include, among other things, quality control, quality assurance and the maintenance of records and documentation. If we fail to comply with these requirements, we may not be able to continue our services to certain customers, or we could be subject to fines and penalties, suspension of production, or withdrawal of our certifications. We operate a facility that we believe conforms to all applicable requirements. This facility and our testing practices are subject to periodic regulatory inspections to ensure compliance.

| 7 |

Our business could be harmed from the loss or suspension of any licenses.

The forensic laboratory testing industry is subject to significant regulation and many of these statutes and regulations are subject to change. The Company cannot assure that applicable statutes and regulations will not be interpreted or applied by a regulatory authority in a manner that would adversely affect its business. Potential sanctions for violation of these regulations could include the suspension or loss of various licenses, certificates and authorizations, which could have a material adverse effect on the Company’s business. In addition, potential delays in renewals of licenses could also harm the Company.

If our use of chemical and hazardous materials violates applicable laws or regulations or causes personal injury we may be liable for damages.

Our drug testing activities, including the analysis and synthesis of chemicals, involve the controlled use of chemicals, including flammable, combustible, and toxic materials that are potentially hazardous. Our use, storage, handling and disposal of these materials is subject to federal, state and local laws and regulations, including the Resource Conservation and Recovery Act, the Occupational Safety and Health Act and local fire codes, and regulations promulgated by the Department of Transportation, the Drug Enforcement Agency, the Department of Energy, and the California Department of Public Health and Environment. We may incur significant costs to comply with these laws and regulations in the future. In addition, we cannot completely eliminate the risk of accidental contamination or injury from these materials, which could result in material unanticipated expenses, such as substantial fines or penalties, remediation costs or damages, or the loss of a permit or other authorization to operate or engage in our business. Those expenses could exceed our net worth and limit our ability to raise additional capital.

Our operations could be interrupted by damage to our laboratory facilities.

Our operations are dependent upon the continued use of our laboratories and equipment in Culver City, California. Catastrophic events, including earthquakes, fires or explosions, could damage our laboratories, equipment, scientific data, work in progress or inventories of chemicals and may materially interrupt our business. We employ safety precautions in our laboratory activities in order to reduce the likelihood of the occurrence of certain catastrophic events; however, we cannot eliminate the chance that such events will occur. Rebuilding our facilities could be time consuming and result in substantial delays in fulfilling our agreements with our customers. We maintain business interruption insurance to cover continuing expenses and lost revenue caused by such occurrences. However, this insurance does not compensate us for the loss of opportunity and potential harm to customer relations that our inability to meet our customers’ needs in a timely manner could create.

Agreements we have with our employees, consultants and customers may not afford adequate protection for our trade secrets, confidential information and other proprietary information.

In addition to patent protection, we also rely on copyright and trademark protection, trade secrets, know-how, continuing technological innovation and licensing opportunities. In an effort to maintain the confidentiality and ownership of our trade secrets and proprietary information, we require our employees, consultants and advisors to execute confidentiality and proprietary information agreements. However, these agreements may not provide us with adequate protection against improper use or disclosure of confidential information and there may not be adequate remedies in the event of unauthorized use or disclosure. Furthermore, we may from time to time hire scientific personnel formerly employed by other companies involved in one or more areas similar to the activities we conduct. In some situations, our confidentiality and proprietary information agreements may conflict with, or be subject to, the rights of third parties with whom our employees, consultants or advisors have prior employment or consulting relationships. Although we require our employees and consultants to maintain the confidentiality of all proprietary information of their previous employers, these individuals, or we, may be subject to allegations of trade secret misappropriation or other similar claims as a result of their prior affiliations. Finally, others may independently develop substantially equivalent proprietary information and techniques or otherwise gain access to our trade secrets. Our failure or inability to protect our proprietary information and techniques may inhibit or limit our ability to compete effectively, or exclude certain competitors from the market.

We are subject to numerous political, legal, operational and other risks as a result of our international operations which could impact our business in many ways.

Although we conduct a majority of our business in the United States, a significant portion of our business is derived from Brazil. Our international operations increase our exposure to the inherent risks of doing business in international markets. Depending on the market, these risks include without limitation:

| • | changes in the local economic environment or local laws or regulations |

| • | political instability, social changes, local market practices and changes |

| • | intellectual property legal protections and remedies |

| • | trade regulations | |

| • | foreign currency exchange rate fluctuations |

| • | attracting and retaining qualified employees and independent contractors including distributors |

| • | export and import and exchange controls |

| • | weak legal systems which may affect our ability to enforce contractual rights |

| • | the Company reliance on one distributor in Brazil |

| 8 |

As the Company has previously disclosed, there are greater challenges and uncertainties in a new, large and developing market, such as Brazil. Psychemedics Brasil, our independent distributor in Brazil, has had 55% of its shares acquired by Instituto Hermes Pardini S.A., a provider of medical and diagnostic services in Brazil, including reference laboratory services. We are in discussions with our distributor and its acquirer about the future of our distribution agreement (which either party may terminate upon prior written notice following July 2019), including whether it will be extended, terminated or replaced by a transition agreement for us to continue to sell our drug tests to our current distributor for a period of time. The outcome of these discussions is not certain, and any significant decrease in sales to our distributor would have a materially adverse impact on our business. However, we believe that the overall market demand for drug testing services in Brazil will continue to grow, and it remains uncertain whether the acquirer will have the capacity to supply our distributor with the volume of drug tests that we currently provide, at least in the near term. At the same time, we have also been exploring additional options in Brazil.

International operations also require us to devote significant management resources to implement our controls and systems in new markets, to comply with the U.S. Foreign Corrupt Practices Act and similar anti-corruption laws in non-U.S. jurisdictions and to overcome challenges based on differing languages and cultures.

International trade policies may impact demand for our products and our competitive position.

Government policies on international trade and investment such as import quotas, capital controls or tariffs, whether adopted by individual governments or addressed by regional trade blocs, can affect the demand for our services, impact the competitive position of our products or prevent us from being able to sell products in certain countries. The implementation of more restrictive trade policies, such as more detailed inspections, higher tariffs or new barriers to entry, could negatively impact our business, results of operations and financial condition. For example, a government’s adoption of “buy national” policies or retaliation by another government against such policies could have a negative impact on our results of operations.

Global operations are subject to extensive trade and anti-corruption laws and regulations.

The U.S. Foreign Corrupt Practices Act and similar foreign anti-corruption laws generally prohibit companies and their intermediaries from making improper payments or providing anything of value to improperly influence foreign government officials for the purpose of obtaining or retaining business, or obtaining an unfair advantage. Recent years have seen a substantial increase in the global enforcement of anti-corruption laws. Our operations outside the United States could increase the risk of such violations. Violations of anti-corruption laws or regulations by our employees or by intermediaries acting on our behalf may result in severe criminal or civil sanctions, could disrupt our business, and result in an adverse effect on our business and results of operations or financial condition.

We may incur additional tax expense or become subject to additional tax exposure.

We are subject to income taxes in the United States and Brazil. Our future results of operations could be adversely affected by changes in the effective tax rate as a result of a change in the mix of earnings, changes in our method of distribution in foreign countries, changes in countries with differing statutory tax rates, changes in our Brazil-derived revenues, changes in our overall profitability, changes in tax laws or treaties or in their application or interpretation, changes in tax rates, changes in generally accepted accounting principles, changes in the valuation of deferred tax assets and liabilities, changes in the amount of earnings indefinitely reinvested offshore, the results of audits and examinations of previously filed tax returns and continuing assessments of our tax exposures. We may be subject to examination of our income tax returns by the U.S. Internal Revenue Service and other tax authorities. If our effective tax rates were to increase, or if the ultimate determination of our taxes owed is for an amount in excess of amounts previously accrued, our operating results, cash flows and financial condition could be adversely affected. For information regarding additional matters related to our taxes, please see Note 5 — "Income taxes" to the financial statements included in this Annual Report.

Currency exchange rate fluctuations affect our results of operations, as reported in our financial statements.

We currently have revenues from many countries, however, we are only subject to currency exchange risk related to the Brazilian Real. We are subject to currency exchange rate risk to the extent that our costs are denominated in currencies other than those in which we earn revenues. In addition, while we share currency exchange risk with our Brazilian distributor, changes in currency exchange rates have had, and will continue to have, an impact on our revenues, results of operations and comprehensive income. There can be no assurance that currency exchange rate fluctuations will not adversely affect our results of operations, financial condition and cash flows.

We also face risks arising from the imposition of exchange controls and currency devaluations. Exchange controls may limit our ability to convert foreign currencies into U.S. dollars or to remit dividends and other payments by our foreign subsidiaries or businesses located in or conducted within a country imposing controls. Currency devaluations result in a diminished value of funds denominated in the currency of the country instituting the devaluation.

Risks Related to Our Stock

Our quarterly operating results could fluctuate significantly, which could cause our stock price to decline.

Our quarterly operating results have fluctuated in the past and are likely to fluctuate in the future. Our results are impacted by the extent to which we are able to gain new customers, both domestically and internationally, competitive pricing, and on the hiring practices of our existing customers, including seasonality. Demand for drug testing can be impacted by changes in government requirements regarding testing for drugs of abuse, delays in implementation of such requirements, as well as general economic conditions. Entering into new customer contracts can involve a long lead time. Accordingly, negotiation can be lengthy and is subject to a number of significant risks, including customers’ budgetary constraints and internal reviews. Due to these and other market factors, our operating results could fluctuate significantly from quarter to quarter. In addition, we may experience significant fluctuations in quarterly operating results due to factors such as general and industry-specific economic conditions that may affect the budgets and the hiring practices of our customers.

| 9 |

Due to the possibility of fluctuations in our revenue and expenses, we believe that quarter-to-quarter comparisons of our operating results are not necessarily a good indication of our future performance. Our operating results in some quarters may not meet the expectations of stock market analysts and investors. If we do not meet analysts’ and/or investors’ expectations, our stock price could decline.

Our stock price could experience substantial volatility.

The market price of our common stock has historically experienced and may continue to experience extensive volatility. Our quarterly operating results, the success or failure of future development efforts, changes in general conditions in the economy or the financial markets and other developments affecting our customers, our distributors, our competitors or us could cause the market price of our common stock to fluctuate substantially. This volatility may adversely affect the price of our common stock. In the past, securities class action litigation has often been instituted following periods of volatility in the market price of a company’s securities. A securities class action suit against us could result in potential liabilities, substantial costs and the diversion of management’s attention and resources, regardless of whether we win or lose.

Payment of a dividend could decline or cease.

Because the Company has historically paid dividends, any cessation of our program or reduction in our quarterly dividend could affect our stock price. As of December 31, 2018, the Company has paid dividends on our common stock for eighty-nine consecutive quarters. It is our intent to continue this practice as long as we are able. However, if we are forced to cease this practice or reduce the amount of the regular dividend, due to operating or economic conditions, our stock price could suffer. Further, if the Company ceases its future dividends, a return on investment in our common stock would depend entirely upon future appreciation. There is no guarantee that our common stock will appreciate in value or even maintain the price at which stockholders have purchased their shares.

The general economic condition could deteriorate.

Our business is dependent upon new hiring and the supply of new jobs created by overall economic conditions. If the economy deteriorates, leading to a downturn in new job creation, our business and stock price could be adversely affected.

Item 1B. Unresolved Staff Comments

Not applicable.

The Company maintains its corporate office and northeast sales office at 289 Great Road, Acton, Massachusetts; the office consists of 6 thousand square feet and is leased through February 2023.

The Company leases two facilities for laboratory purposes in Culver City, California. The first is 14 thousand square feet of space with an additional 10 thousand square feet of storage space. This facility is leased through December 2020 with an option to renew for an additional two years. The second facility of 16 thousand square feet is leased through January 2020.

The Company is involved in various suits and claims in the ordinary course of business. The Company does not believe that the disposition of any such suits or claims will have a material adverse effect on the continuing operations or financial condition of the Company.

Item 4. Mine Safety Disclosures

Not applicable.

| 10 |

Item 5. Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities

The Company’s common stock is traded on the NASDAQ Stock Market under the symbol “PMD”. As of February 28, 2019, there were 159 record holders of the Company’s common stock. The number of record owners was determined from the Company’s stockholder records maintained by the Company’s transfer agent and does not include beneficial owners of the Company’s common stock whose shares are held in the names of various security holders, dealers and clearing agencies. The Company believes that the number of beneficial owners of the Company’s common stock held by others as or in nominee names exceeds 3,000.

The following table sets forth for the periods indicated the range of prices for the Company’s common stock as reported by the NASDAQ Stock Market and dividends declared by the Company.

| High | Low | Dividends | ||||||||||

| Fiscal 2018: | ||||||||||||

| First Quarter | $ | 22.88 | $ | 18.69 | $ | 0.15 | ||||||

| Second Quarter | 21.50 | 17.98 | 0.18 | |||||||||

| Third Quarter | 22.31 | 18.38 | 0.18 | |||||||||

| Fourth Quarter | 19.00 | 13.94 | 0.18 | |||||||||

| Fiscal 2017: | ||||||||||||

| First Quarter | $ | 27.46 | $ | 13.81 | $ | 0.15 | ||||||

| Second Quarter | 25.00 | 18.30 | 0.15 | |||||||||

| Third Quarter | 27.99 | 17.40 | 0.15 | |||||||||

| Fourth Quarter | 21.74 | 15.99 | 0.15 | |||||||||

The Company has paid dividends over the past twenty-one years. It most recently declared a dividend on March 4, 2019, which will be paid on March 25, 2019. The Company’s current intention is to continue to declare dividends to the extent funds are available and not required for operating purposes or capital requirements, and only then, upon approval by the Board of Directors.

Issuer Purchases of Equity Securities

During 2018, the Company did not repurchase any common shares for treasury.

Unregistered Sales of Equity Securities and Use of Proceeds

There were no unregistered sales of common stock of the Company during 2018.

| 11 |

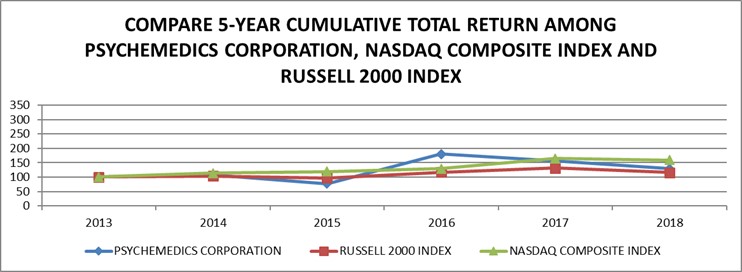

Performance Graph

Calculated by the Company using www.yahoo.com/finance historical prices

| 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | |||||||||||||||||||

| PSYCHEMEDICS CORPORATION | 100.00 | 107.22 | 77.20 | 180.26 | 156.30 | 129.07 | ||||||||||||||||||

| RUSSELL 2000 INDEX | 100.00 | 103.53 | 97.62 | 116.63 | 131.96 | 115.89 | ||||||||||||||||||

| NASDAQ COMPOSITE INDEX | 100.00 | 113.40 | 119.89 | 128.89 | 165.29 | 158.87 | ||||||||||||||||||

| (1) | The above graph assumes a $100 investment on December 31, 2013, through the end of the 5-year period ended December 31, 2018 in the Company’s Common Stock, the Russell 2000 Index and the NASDAQ Composite Index. The prices all assume the reinvestment of dividends. |

| (2) | The Russell 2000 Index is composed of the smallest 2,000 companies in the Russell 3,000 Index. The Company has been unable to identify a peer group of companies that engage in testing of drugs of abuse, except for large pharmaceutical companies where such business is insignificant to such companies’ other lines of businesses. The Company therefore uses in its proxy statements a peer index based on market capitalization. |

| (3) | The NASDAQ Composite Index includes companies whose shares are traded on the NASDAQ Stock Market. |

Item 6. Selected Financial Data

The selected financial data presented below is derived from our financial statements and should be read in connection with those statements.

| Year Ended December 31, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| (In thousands, except for per share data) | ||||||||||||||||||||

| Revenue | $ | 42,674 | $ | 39,701 | $ | 38,980 | $ | 26,975 | $ | 29,205 | ||||||||||

| Gross profit | 20,618 | 19,822 | 21,450 | 12,717 | 15,138 | |||||||||||||||

| Income from operations | 7,610 | 8,157 | 10,110 | 1,471 | 4,690 | |||||||||||||||

| Net income | 4,584 | 6,121 | 6,678 | 1,511 | 3,206 | |||||||||||||||

| Total assets | 24,974 | 26,508 | 25,032 | 22,036 | 23,701 | |||||||||||||||

| Working capital | 9,810 | 9,640 | 6,359 | 4,564 | 6,604 | |||||||||||||||

| Shareholders’ equity | 18,747 | 18,620 | 15,607 | 11,674 | 12,837 | |||||||||||||||

| Basic net income per share | $ | 0.83 | $ | 1.12 | $ | 1.23 | $ | 0.28 | $ | 0.60 | ||||||||||

| Diluted net income per share | $ | 0.83 | $ | 1.10 | $ | 1.22 | $ | 0.28 | $ | 0.60 | ||||||||||

| Cash dividends declared per common share | $ | 0.69 | $ | 0.60 | $ | 0.60 | $ | 0.60 | $ | 0.60 | ||||||||||

| 12 |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The Management’s Discussion and Analysis of Financial Condition and Results of Operations should be read together with the more detailed business information and financial statements and related notes that appear elsewhere in this annual report on Form 10-K. This annual report may contain certain “forward-looking” information within the meaning of the Private Securities Litigation Reform Act of 1995. This information involves risks and uncertainties. Actual results may differ materially from the results discussed in the forward-looking statements. Factors that might cause such a difference include, but are not limited to, those discussed in Item 1A — Risk Factors.

Overview

Psychemedics Corporation is the world’s largest provider of hair testing for drugs of abuse, utilizing a patented hair analysis method involving digestion of hair, enzyme immunoassay technology and confirmation by mass spectrometry to analyze human hair to detect abused substances. The Company’s customers include Fortune 500 companies, as well as small to mid-size corporations, schools and governmental entities, located in the United States and internationally. During the year ended December 31, 2018, the Company produced $42.7 million in revenue, while generating a gross margin of 48% and pre-tax margins of 18%. The Company had net income of $4.6 million and diluted earnings per share of $0.83 for the year ended December 31, 2018, a decrease of $1.5 million, or 25% from the prior year primarily due to a one-time tax benefit from the passage of the Tax Cuts and Jobs Act (“Tax Act”) in 2017 of $1.2 million or $0.22 per share and unfavorable changes in foreign exchange rates. Pre-tax income in 2018 was $7.7 million, down 6% due primarily to unfavorable changes in foreign exchange rates. If the exchange rate remained the same, the Company’s pre-tax income would have been $9.9 million or an increase of 21% over 2017. Due to the volatility of the US dollar to Brazilian Real exchange rate, the Company changed its distribution structure with its Brazilian distributor in the third quarter of 2018 to share in the exchange rate risk, as further described below in this Annual Report.

At December 31, 2018, the Company had $8.0 million of cash and marketable securities. During 2018, the Company had operating cash flow of $8.0 million and it distributed approximately $3.8 million or $0.69 per share of cash dividends to its shareholders. In addition, the Company spent approximately $1.4 million on equipment, leasehold improvements and software development. As of December 31, 2018, the Company has paid eighty-nine consecutive quarterly cash dividends.

The following table sets forth, for the periods indicated, the selected statements of operations data as a percentage of total revenue:

| Year Ended December 31, | ||||||||||||

| 2018 | 2017 | 2016 | ||||||||||

| Revenue | 100.0 | % | 100.0 | % | 100.0 | % | ||||||

| Cost of revenue | 51.7 | % | 50.1 | % | 45.0 | % | ||||||

| Gross profit | 48.3 | % | 49.9 | % | 55.0 | % | ||||||

| Operating expenses: | ||||||||||||

| General and administrative | 15.1 | % | 14.2 | % | 12.8 | % | ||||||

| Marketing and selling | 11.8 | % | 11.8 | % | 12.7 | % | ||||||

| Research and development | 3.6 | % | 3.4 | % | 3.6 | % | ||||||

| Total operating expenses | 30.5 | % | 29.4 | % | 29.1 | % | ||||||

| Operating income | 17.8 | % | 20.5 | % | 25.9 | % | ||||||

| Other income (expense) | 0.1 | % | 0.1 | % | -0.3 | % | ||||||

| Income before taxes | 17.9 | % | 20.6 | % | 25.6 | % | ||||||

| Provision for income taxes | 7.2 | % | 5.2 | % | 8.5 | % | ||||||

| Net income | 10.7 | % | 15.4 | % | 17.1 | % | ||||||

Revenue by Geographic Region

| Year Ended December 31, | ||||||||||||

| 2018 | 2017 | 2016 | ||||||||||

| Consolidated Revenue: | ||||||||||||

| United States | $ | 29,189 | $ | 26,327 | $ | 25,608 | ||||||

| Brazil | 13,046 | 13,069 | 13,083 | |||||||||

| Other | 439 | 305 | 289 | |||||||||

| Total Revenue | $ | 42,674 | $ | 39,701 | $ | 38,980 | ||||||

| 13 |

Results for the Year Ended December 31, 2018 Compared to Results for the Year Ended December 31, 2017 (in thousands)

| 2018 | 2017 | Change | % | |||||||||||||

| Revenue | $ | 42,674 | $ | 39,701 | $ | 2,973 | 7 | % | ||||||||

| Cost of revenue | 22,056 | 19,879 | 2,177 | 11 | % | |||||||||||

| Gross profit | 20,618 | 19,822 | 796 | 4 | % | |||||||||||

| Operating expenses: | ||||||||||||||||

| General and administrative | 6,430 | 5,642 | 788 | 14 | % | |||||||||||

| Marketing and selling | 5,027 | 4,666 | 361 | 8 | % | |||||||||||

| Research and development | 1,551 | 1,357 | 194 | 14 | % | |||||||||||

| Total operating expenses | 13,008 | 11,665 | 1,343 | 12 | % | |||||||||||

| Operating income | 7,610 | 8,157 | (547 | ) | -7 | % | ||||||||||

| Other income (expense) | 43 | 20 | 23 | 115 | % | |||||||||||

| Income before taxes | 7,653 | 8,177 | (524 | ) | -6 | % | ||||||||||

| Provision for income taxes | 3,069 | 2,056 | 1,013 | 49 | % | |||||||||||

| Net income | $ | 4,584 | $ | 6,121 | $ | (1,537 | ) | -25 | % | |||||||

Revenue: Domestic revenue was up 11% and international revenue was up 1% from 2017 to 2018. See geographic breakdown of revenue above. Total revenue growth of 7% was primarily due to a 15% increase in volume, offset by a 6% negative impact from foreign currency exchange and a 2% impact from decrease of average revenue per sample, primarily as a result of business mix.

Gross profit: The increase in costs of revenue was primarily due to higher costs associated with higher volume. Gross profit was adversely impacted by foreign currency exchange as noted in revenue section above. Without this impact, gross profit percentage would have been 51% as compared to 50% in 2017.

General and administrative (“G&A”) expenses: The increase in G&A expenses primarily related to additional audit related costs associated with the Company becoming an accelerated filer and implementing new accounting standards. These costs included external audit fees, internal control consultants and additional personnel. As a percentage of revenue, G&A expenses represented 15.1% in 2018 versus 14.2% in 2017.

Marketing and selling expenses: The increase in marketing and selling expenses was primarily a result of additional personnel and personnel related costs in 2018. Total marketing and selling expenses represented 11.8% of revenue for 2018 and 2017.

Research and development (“R&D”): R&D expenses represented 3.6% and 3.4% of revenue for 2018 and 2017, respectively.

Income Taxes: During the year ended December 31, 2018, the Company recorded a tax provision of $3.1 million representing a tax rate of 40% compared to a tax rate of 25% in 2017. Approximately half of the tax provision in 2018 was attributed to domestic taxes, with the other half attributed to Brazil. The increase in 2018 was primarily due a higher tax rate impact from Brazil in 2018 and to the passing of the Tax Act in 2017. The Tax Act impacted 2017 with a benefit of $1.2 million and it also had the effect of increasing the Brazil net tax rate, as the lower U.S. tax rate reduced the deductibility of Brazil taxes. For information regarding additional matters related to our taxes, please see Note 5 — "Income taxes" to the financial statements included in this Annual Report.

| 14 |

Results for the Year Ended December 31, 2017 Compared to Results for the Year Ended December 31, 2016 (in thousands)

| 2017 | 2016 | Change | % | |||||||||||||

| Revenue | $ | 39,701 | $ | 38,980 | $ | 721 | 2 | % | ||||||||

| Cost of revenue | 19,879 | 17,530 | 2,349 | 13 | % | |||||||||||

| Gross profit | 19,822 | 21,450 | (1,628 | ) | -8 | % | ||||||||||

| Operating expenses: | ||||||||||||||||

| General and administrative | 5,642 | 4,965 | 677 | 14 | % | |||||||||||

| Marketing and selling | 4,666 | 4,960 | (294 | ) | -6 | % | ||||||||||

| Research and development | 1,357 | 1,415 | (58 | ) | -4 | % | ||||||||||

| Total operating expenses | 11,665 | 11,340 | 325 | 3 | % | |||||||||||

| Operating income | 8,157 | 10,110 | (1,953 | ) | -19 | % | ||||||||||

| Other expense | 20 | (134 | ) | 154 | -115 | % | ||||||||||

| Income before taxes | 8,177 | 9,976 | (1,799 | ) | -18 | % | ||||||||||

| Provision for (benefit from) income taxes | 2,056 | 3,298 | (1,242 | ) | -38 | % | ||||||||||

| Net income | $ | 6,121 | $ | 6,678 | $ | (557 | ) | -8 | % | |||||||

Revenue: Domestic revenue was up 3% and the international revenue was flat from 2016 to 2017. See geographic breakdown of revenue above. In 2017, we implemented strategic initiatives, including certain pricing considerations, to defend and increase our market share in Brazil.

Gross profit: The increase in costs of revenue and decrease in gross profit was primarily due to higher costs associated with higher volume. Gross profit was also adversely impacted by our strategic pricing initiatives in Brazil noted above, including increased costs from Brazilian sales taxes, which the Company also incurred as a result of the establishment of a Brazilian subsidiary in the second quarter of 2017. Gross profit was also impacted by an increase in depreciation expense.

General and administrative (“G&A”) expenses: The increase in G&A expenses related to additional costs associated with the Brazil operations and higher legal and audit fees. As a percentage of revenue, G&A expenses represented 14.2% in 2017 versus 12.7% in 2016.

Marketing and selling expenses: The decrease in marketing and selling expenses was primarily a result of a temporary decrease in personnel and personnel related costs in 2017. Total marketing and selling expenses represented 11.8% and 12.7% of revenue for 2017 and 2016, respectively.

Research and development (“R&D”): R&D expenses represented 3.4% and 3.6% of revenue for 2017 and 2016, respectively.

Other income: Other income primarily consisted of interest earned on CD’s which was partially offset by interest expense related to debt. The increase in income came from a reduction of interest expense from a lower loan balance and an increase in interest income from CD’s which did not exist in 2016.

Income Taxes: During the year ended December 31, 2017, the Company recorded a tax provision of $2.1 million representing a tax rate of 25%, versus a tax rate of 33% in 2016. There were two significant items impacting the rate in 2017. The larger item was the passing of the Tax Act in December 2017. While this law changed tax rates for 2018, the lower tax rate required a remeasurement of the Company’s deferred tax liability at December 31, 2017. The law also allowed for additional depreciation for assets purchased and placed in service in the fourth quarter of 2017. The impact of this (primarily from the remeasurement of the deferred tax liability) was a reduction of tax liability and income tax benefit of $1.2 million for 2017. This benefit was partially offset by the imposition of income taxes in Brazil incurred as a result of the Company’s formation of a subsidiary in Brazil in the second quarter of 2017. The impact of this was an increase in the tax provision of $0.6 million.

Liquidity and Capital Resources