Exhibit 1

|

Table of contents

| CORPORATE STRUCTURE | 8 |

| GENERAL DEVELOPMENT OF THE BUSINESS | 9 |

| Developments – Mines and Projects | 9 |

| Developments – Financial | 10 |

| DESCRIPTION OF THE BUSINESS | 11 |

| Specialized Skills and Knowledge | 11 |

| Principal Products | 12 |

| Competitive Conditions | 12 |

| Operations | 12 |

| Technical Information | 14 |

| Mineral Reserve and Mineral Resource Estimates | 12 |

| MINERAL PROPERTIES | 19 |

| Rainy River Mine, Canada | 19 |

| New Afton Mine, Canada | 25 |

| Blackwater Project, Canada | 31 |

| Cerro San Pedro Mine, Mexico | 33 |

| RISK FACTORS | 34 |

| NOTES | 53 |

| DIVIDENDS | 53 |

| DESCRIPTION OF CAPITAL STRUCTURE | 54 |

| MARKET FOR SECURITIES | 56 |

| DIRECTORS AND OFFICERS | 56 |

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS | 62 |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 63 |

| TRANSFER AGENT AND REGISTRAR | 63 |

| MATERIAL CONTRACTS | 63 |

| TECHNICAL REPORTS | 63 |

| SCHEDULE A Audit Committee Charter | A-1 |

| SCHEDULE B DEFINITIONS | B-1 |

| SCHEDULE C ABBREVIATIONS AND MEASUREMENT CONVERSION | C-1 |

| SCHEDULE D EXCHANGE RATE AND METAL PRICE INFORMATION | D-1 |

| 2 |  |

|

Annual

information form

for the financial year ended December 31, 2018

All information in this annual information form (“Annual Information Form”) is as at December 31, 2018 unless otherwise indicated.

Cautionary Note Regarding Forward-Looking Statements

Certain information contained in this Annual Information Form, including any information relating to New Gold’s future financial or operating performance are “forward looking”. All statements in this Annual Information Form, other than statements of historical fact, which address events, results, outcomes or developments that New Gold expects to occur are “forward-looking statements”. Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the use of forward-looking terminology such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “targeted”, “estimates”, “forecasts”, “intends”, “anticipates”, “projects”, “potential”, “believes” or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “should”, “might” or “will be taken”, “occur” or “be achieved” or the negative connotation of such terms. Forward-looking statements in this Annual Information Form include those under the headings “General Developments of the Business”, “Description of the Business” and “Mineral Properties” and include, among others, statements with respect to: guidance for production, operating expenses per gold ounce sold, total cash costs, all-in sustaining costs and capital costs, and the factors contributing to those expected results, as well as expected capital expenditures; mine life; Mineral Reserve and Mineral Resource estimates; grades expected to be mined at the Company’s operations; the expected production, costs, economics and operating parameters of Blackwater and New Afton C-zone; planned activities for 2019 and beyond at the Company’s operations and projects, as well as planned exploration activities; and targeted timing for permits.

All forward-looking statements in this Annual Information Form are based on the opinions and estimates of management as of the date such statements are made and are subject to important risk factors and uncertainties, many of which are beyond New Gold’s ability to control or predict. Certain material assumptions regarding such forward-looking statements are discussed in this Annual Information Form, New Gold’s annual and quarterly management’s discussion and analysis (“MD&A”) and its Technical Reports filed on SEDAR at www.sedar.com. In addition to, and subject to, such assumptions discussed in more detail elsewhere, the forward-looking statements in this Annual Information Form are also subject to the following assumptions: (1) there being no significant disruptions affecting New Gold’s operations; (2) political and legal developments in jurisdictions where New Gold operates, or may in the future operate, being consistent with New Gold’s current expectations; (3) the accuracy of New Gold’s current Mineral Reserve and Mineral Resource estimates; (4) the exchange rate between the Canadian dollar, U.S. dollar and, to a lesser extent, the Mexican peso being approximately consistent with current levels; (5) prices for diesel, natural gas, fuel oil, electricity and other key supplies being approximately consistent with current levels; (6) equipment, labour and material costs increasing on a basis consistent with New Gold’s current expectations; (7) arrangements with First Nations and other indigenous groups in respect of Rainy River and Blackwater being consistent with New Gold’s current expectations; (8) all required permits, licenses and authorizations being obtained from the relevant governments and other relevant stakeholders within the expected timelines; (9) the results of the feasibility studies for the New Afton C-zone and Blackwater being realized; (10) and in the case of production, cost and expenditure outlooks at operating mines for 2019, commodity prices and exchange rates being consistent with those estimated for the purposes of 2019 guidance.

Forward-looking statements are necessarily based on estimates and assumptions that are inherently subject to known and unknown risks, uncertainties and other factors that may cause actual results, level of activity, performance or achievements to be materially different from those expressed or implied by such forward-looking statements. Such

| 3 | |

|

factors include, without limitation: significant capital requirements and the availability and management of capital resources; additional funding requirements; price volatility in the spot and forward markets for metals and other commodities; fluctuations in the international currency markets and in the rates of exchange of the currencies of Canada, the United States and, to a lesser extent, Mexico; discrepancies between actual and estimated production, between actual and estimated Mineral Reserves and Mineral Resources and between actual and estimated metallurgical recoveries; changes in national and local government legislation in the countries in which New Gold does or may in the future carry on business; taxation; controls, regulations and political or economic developments in the countries in which New Gold does or may in the future carry on business; the speculative nature of mineral exploration and development, including the risks of obtaining and maintaining the validity and enforceability of the necessary licenses and permits and complying with the permitting requirements of each jurisdiction in which New Gold operates, including, but not limited to: in Canada, obtaining the necessary permits for the New Afton C-zone and the Blackwater Project; the uncertainties inherent to current and future legal challenges to which New Gold is or may become a party; diminishing quantities or grades of Mineral Reserves and Mineral Resources; competition; loss of key employees; rising costs of labour, supplies, fuel and equipment; actual results of current exploration or reclamation activities; uncertainties inherent to mining economic studies including the feasibility studies for New Afton C-zone and the Blackwater Project; the uncertainty with respect to prevailing market conditions necessary for a positive development or construction decision at the Blackwater Project; changes in project parameters as plans continue to be refined; accidents; labour disputes; defective title to mineral claims or property or contests over claims to mineral properties; unexpected delays and costs inherent to consulting and accommodating rights of First Nations and other indigenous groups; uncertainties and unanticipated delays associated with obtaining and maintaining necessary licenses, permits and authorizations, complying with permitting requirements, and receiving the environmental assessment approval for the Blackwater Project. In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental events and hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold bullion losses (and, in each case, the risk of inadequate insurance or inability to obtain insurance to cover these risks) as well as “Risk Factors” included in this Annual Information Form. Forward-looking statements are not guarantees of future performance, and actual results and future events could materially differ from those anticipated in such statements. All the forward-looking statements contained in this Annual Information Form are qualified by these cautionary statements. New Gold expressly disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, events or otherwise, except in accordance with applicable securities laws.

A significant portion of the historical financial information in this Annual Information Form is derived from New Gold’s audited consolidated financial statements for the year ended December 31, 2018 (a copy of which is available under the Company’s profile on SEDAR at www.sedar.com). Readers should refer to such financial statements for additional information.

Cautionary Note to U.S. Readers Concerning Estimates of Mineral Reserves and Mineral Resources

Information concerning the properties and operations of New Gold has been prepared in accordance with Canadian standards under applicable Canadian securities laws, and may not be comparable to similar information for United States companies. The terms “Mineral Reserve”, “Proven Mineral Reserve” and “Probable Mineral Reserve” are Canadian mining terms defined in accordance with Canadian National Instrument 43-101 — Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) — CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended. These definitions differ from the definitions in Industry Guide 7 (“SEC Industry Guide 7”) under the U.S. Securities Act of 1933, as amended (the “U.S. Securities Act”). Under SEC Industry Guide 7 standards, mineralization may not be classified as a “reserve” unless

| 4 | |

|

the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. Also, under SEC Industry Guide 7 standards, a “final” or “bankable” feasibility study is required to report reserves, the three-year historical average price is used in any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority.

In addition, the terms “Mineral Resource”, “Measured Mineral Resource”, “Indicated Mineral Resource” and “Inferred Mineral Resource” are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the United States Securities and Exchange Commission (the “SEC”). Investors are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into reserves. “Inferred Mineral Resources” have a great amount of uncertainty as to their existence and as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred Mineral Resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred Mineral Resource exists or is economically or legally mineable. Mineral resources that are not mineral reserves do not have demonstrated economic viability. Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian regulations; however, SEC Industry Guide 7 normally only permits issuers to report mineralization that does not constitute “reserves” by SEC Industry Guide 7 standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this Annual Information Form describes the Company’s mineral deposits may not be comparable to similar information made public by United States companies subject to reporting and disclosure requirements under United States federal securities laws and the rules and regulations thereunder.

Non-GAAP Measures

Total Cash Costs per Gold Ounce

“Total cash costs per gold ounce” is a non-GAAP measure that is a common financial performance measure in the gold mining industry but with no standard meaning under International Financial Reporting Standards (“IFRS”). New Gold reports total cash costs on a sales basis. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate the Company’s performance and ability to generate liquidity through operating cash flow to fund future capital expenditures and working capital needs. New Gold believes that this measure, along with sales, is a key indicator of a company’s ability to generate operating earnings and cash flow from its mining operations.

Total cash cost figures are calculated in accordance with a standard developed by The Gold Institute, a worldwide association of suppliers of gold and gold products that ceased operations in 2002. Adoption of the standard is voluntary and the cost measures presented may not be comparable to other similarly titled measures of other companies. Total cash costs include mine site operating costs such as mining, processing and administration costs, royalties, production taxes, but are exclusive of depreciation, amortization, reclamation, capital and exploration costs and net of by-product sales. Total cash costs are then divided by gold ounces sold to arrive at the total cash costs per ounce sold.

The Company produces copper and silver as by-products of its gold production. The calculation of total cash costs per gold ounce for Rainy River and Cerro San Pedro is net of by-product silver sales revenue, and the calculation of total cash costs per gold ounce sold for New Afton is net of by-product silver and copper sales revenue. New Gold notes that in connection with New Afton, the copper by-product revenue is sufficiently large to result in a negative total cash cost on a single mine basis. Notwithstanding this by-product contribution, as a company focused on gold production, New Gold aims to assess the economic results of its operations in relation to gold, which is the primary driver of New Gold’s business. New Gold believes this metric is of interest to its investors, who invest in the Company primarily as a gold

| 5 | |

|

mining company. To determine the relevant costs associated with gold only, New Gold believes it is appropriate to reflect all operating costs, as well as any revenue related to metals other than gold that are extracted in its operations.

To provide additional information to investors, New Gold has also calculated total cash costs on a co-product basis, which removes the impact of other metal sales that are produced as a by-product of gold production and apportions the cash costs to each metal produced on a percentage of revenue basis, and subsequently divides the amount by the total gold ounces, silver ounces or pounds of copper sold, as the case may be, to arrive at per ounce or per pound figures. In 2019, in addition to reporting total cash costs on a co-product basis per gold ounce, silver ounce or pound of copper sold, the Company will also report gold equivalent total cash costs per ounce on a co-product basis. Gold equivalent ounces of copper and silver produced will be computed as pounds of copper and silver ounces produced multiplied by the ratio of the average realized copper and silver price, respectively, to the average realized gold price. Unless indicated otherwise, all total cash cost information in this Annual Information Form is net of by-product sales.

Total cash costs are intended to provide additional information only and do not have any standardized meaning under IFRS and may not be comparable to similar measures presented by other mining companies. They should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. The measure is not necessarily indicative of cash flow from operations under IFRS or operating costs presented under IFRS. Further details regarding historical total cash costs and a reconciliation to the nearest IFRS measures are provided in the MD&A accompanying New Gold’s financial statements and filed at www.sedar.com.

All-in Sustaining Costs per Gold Ounce

“All-in sustaining costs per gold ounce” is a non-GAAP measure based on guidance announced by the World Gold Council (“WGC”) in September 2013. The WGC is a non-profit association of the world’s leading gold mining companies established in 1987 to promote the use of gold to industry, consumers and investors. The WGC is not a regulatory body and does not have the authority to develop accounting standards or disclosure requirements. The WGC has worked with its member companies, to develop a measure that expands on IFRS measures such as operating expenses and non-GAAP measures to provide visibility into the economics of a gold mining company. Current IFRS measures used in the gold industry, such as operating expenses, do not capture all of the expenditures incurred to discover, develop and sustain gold production. New Gold believes the all-in sustaining costs measure provides further transparency into costs associated with producing gold and will assist analysts, investors and other stakeholders of the Company in assessing its operating performance, its ability to generate free cash flow from current operations and its overall value. In addition, the Human Resources and Compensation Committee of the Board of Directors uses all-in sustaining costs, together with other measures, in the corporate scorecard to set incentive compensation goals and assess performance.

All-in sustaining costs per gold ounce is intended to provide additional information only and does not have any standardized meaning under IFRS and may not be comparable to similar measures presented by other mining companies. It should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. The measure is not necessarily indicative of cash flow from operations under IFRS or operating costs presented under IFRS. Further details regarding historical all-in sustaining costs and a reconciliation to the nearest IFRS measures are provided in the MD&A accompanying New Gold’s financial statements and filed at www.sedar.com.

New Gold defines all-in sustaining costs per ounce as the sum of total cash costs, net capital expenditures that are sustaining in nature, corporate general and administrative costs, capitalized and expensed exploration costs that are sustaining in nature, and environmental reclamation costs, all divided by the total gold ounces sold to arrive at a per ounce figure. To determine sustaining capital expenditures, New Gold uses cash flow related to mining interests from its statement of cash flows and deducts any expenditures that are non-sustaining (growth). Capital expenditures to develop new operations or capital expenditures related to major projects at existing operations where these projects will materially benefit the operation are classified as non-sustaining and are excluded. The table “Sustaining Capital Expenditure Reconciliation” (in New Gold’s MD&A available under the Company’s profile on SEDAR at www.sedar.com)

| 6 | |

|

reconciles New Gold’s sustaining capital to its cash flow statement. The definition of sustaining versus non-sustaining is similarly applied to capitalized and expensed exploration costs. Exploration costs to develop new operations or that relate to major projects at existing operations where these projects are expected to materially benefit the operation are classified as non-sustaining and are excluded.

Costs excluded from all-in sustaining costs are non-sustaining capital expenditures and exploration costs, financing costs, tax expense, transaction costs associated with mergers, acquisitions and divestitures, and any items that are deducted for the purposes of adjusted earnings.

To provide additional information to investors, New Gold has also calculated all-in sustaining costs per ounce on a co-product basis, which removes the impact of other metal sales that are produced as a by-product of gold production and apportions the all-in sustaining costs to each metal produced on a percentage of revenue basis, and subsequently divides the amount by the total gold ounces, silver ounces or pounds of copper sold, as the case may be, to arrive at per ounce or per pound figures. In 2019, in addition to reporting all-in sustaining costs on a co-product basis per gold ounce, silver ounce or pound of copper sold, the Company will also report gold equivalent all-in sustaining costs per ounce on a co-product basis. Gold equivalent ounces of copper and silver produced will be computed as pounds of copper and silver ounces produced multiplied by the ratio of the average realized copper and silver price, respectively, to the average realized gold price. Unless indicated otherwise, all all-in sustaining costs information in this MD&A is net of by-product sales. By including total cash costs as a component of all-in sustaining costs, the measure deducts by-product revenue from gross cash costs.

Currency Presentation and Exchange Rate Information

All dollar amounts referenced in this Annual Information Form are in United States dollars unless otherwise indicated. Canadian dollars are referred to as “Canadian dollars” or “C$”. See Schedule D of this Annual Information Form for applicable exchange rate information.

Technical Information

The scientific and technical information relating to the Mineral Reserves contained herein has been reviewed and approved by Mr. Nicholas Kwong, Director of Technical Services for the Company. The scientific and technical information relating to the Mineral Resources contained herein has been reviewed and approved by Mr. Mark A. Petersen a consultant to New Gold and its former Vice President, Exploration. All other scientific and technical information in this Annual Information Form has been reviewed and approved by Mr. Eric Vinet, Vice President, Technical Services for the Company. Mr. Kwong is a Professional Engineer and a member of the Association of Professional Engineers and Geoscientists of British Columbia. Mr. Petersen is a Professional Geoscientist (P.Geo.) and Practicing Member of the Association of Professional Geoscientists of Ontario, an SME Registered Member and an AIPG Certified Professional Geologist. Mr. Vinet is a Professional Engineer and member of the Ordre des ingénieurs du Québec. Mr. Kwong, Mr. Petersen and Mr. Vinet are "Qualified Persons" for the purposes of NI 43-101. To the Company’s knowledge, each of the aforementioned persons holds less than 1% of the outstanding securities of the Company.

The estimates of Mineral Reserves and Mineral Resources discussed in this Annual Information Form may be materially affected by environmental, permitting, legal, title, taxation, sociopolitical, marketing and other risks and relevant issues. New Gold’s current NI 43-101 Technical Reports, which are available at www.sedar.com, contain further information regarding Mineral Reserve and Mineral Resource estimates, classification, reporting parameters, key assumptions and risks for each of New Gold's material mineral properties.

| 7 | |

|

Additional Information

Additional information about the Company, including, without limitation, directors’ and officers’ remuneration and indebtedness, principal holders of the Company’s securities and securities authorized for issuance under equity compensation plans, may be found in the Management Information Circular of the Company for its most recent annual meeting of shareholders and other continuous disclosure documents of the Company filed on SEDAR at www.sedar.com. Additional financial information is provided in the Company’s audited consolidated financial statements and MD&A for the three months and year ended December 31, 2018. These documents and other information about the Company are available under the Company’s profile on SEDAR at www.sedar.com.

CORPORATE STRUCTURE

The Company was incorporated on January 31, 1980 as DRC Resources Corporation under the Company Act (British Columbia) and was transitioned on May 10, 2005 under the Business Corporations Act (British Columbia). On May 4, 2005, the shareholders of the Company passed a special resolution to remove the pre-existing company provisions and adopt new articles. On June 1, 2005 the Company changed its name to New Gold Inc. Effective January 1, 2012, New Gold amalgamated with its wholly owned subsidiaries Silver Quest Resources Ltd. (“Silver Quest”), Geo Minerals Ltd. (“Geo”) and Richfield Ventures Corp. (“Richfield”). The amalgamated company continued as New Gold Inc. Effective October 1, 2014, New Gold amalgamated with its wholly owned subsidiaries Rainy River Resources Ltd. (“RRRL”) and 0608457 B.C. Ltd, with the amalgamated company continuing as New Gold Inc. On January 1, 2016, New Gold amalgamated with its wholly owned subsidiaries Peak Gold Ltd. and New Gold Bayfield Corp. The amalgamated company continued as New Gold Inc.

The registered office of the Company is Suite 610, 1100 Melville Street, Vancouver, British Columbia V6E 4A6, Canada and its head office is at Suite 3510, 181 Bay Street, Toronto, Ontario, M5J 2T3, Canada.

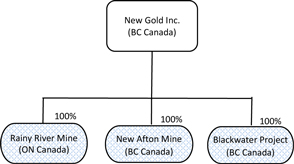

As at the date of this Annual Information Form, the Company does not have any material subsidiaries. The Rainy River Mine, New Afton Mine and Blackwater Project are all held by New Gold Inc.

In this Annual Information Form, except as otherwise required by the context, reference to “New Gold” or the “Company” means, collectively, New Gold Inc. and its subsidiaries.

| 8 | |

|

GENERAL DEVELOPMENT OF THE BUSINESS

New Gold is a Canadian-focused intermediate gold mining company engaged in the acquisition, exploration, development and operation of mineral properties. New Gold currently has the following mines and development projects which are described in greater detail in the “Mineral Properties” section of this Annual Information Form:

| · | 100% interest in the Rainy River gold-silver mine in Ontario, Canada (“Rainy River Mine”) |

| · | 100% interest in the New Afton gold-copper mine British Columbia, Canada (“New Afton Mine”) |

| · | 100% interest in the Blackwater gold-silver project in British Columbia, Canada (“Blackwater Project”) |

New Gold also owns a 100% interest in the Cerro San Pedro gold-silver mine in San Luis Potosí, Mexico (“Cerro San Pedro Mine”), which concluded active mining in June 2016 and transitioned to the reclamation phase on December 31, 2018.

New Gold has been engaged in the acquisition, exploration and development of natural resource properties since 1980. The Company’s current structure arose through two accretive business combinations in mid-2008 and mid-2009. To achieve its growth strategy, New Gold focuses on:

| · | Delivering on operational targets (safety, cost, production, environment and social responsibility); |

| · | Maintaining a strong financial position; |

| · | Internal growth through project development and continuous improvement of existing operations; and |

| · | External growth through value enhancing merger and acquisition opportunities. |

Developments – Mines and Projects

Rainy River Mine

Construction of the Rainy River Mine commenced in early 2015. In January 2017, the Company announced an increase in the expected total capital cost to build the Rainy River Mine to $1,292 million, including contingency, and that startup was scheduled for September 2017 with commercial production expected to commence November 2017. The first gold pour at the Rainy River Mine occurred on October 5, 2017 and commercial production was achieved on October 19, 2017.

New Afton Mine

In January 2016, the Company completed a Feasibility Study, which indicated positive economics for mining the C-zone consistent with a scoping study announced in February 2015. The C-zone is the down plunge extension of the B-zone block cave that is currently being mined at New Afton. In January 2019, the Company announced it would begin underground development of the C-zone in 2019. See “Exploration and Development – New Afton C-zone” on page 31.

Peak Mines

On November 20, 2017, New Gold announced that it had entered into an agreement with Aurelia Metals Limited to sell its 100% interest in the Peak gold-copper mines in New South Wales, Australia (“Peak Mines”) for cash consideration of $58 million. The transaction closed on April 10, 2018.

| 9 | |

|

Mesquite Mine

On September 19, 2018, New Gold announced that it had entered into an agreement with Equinox Gold Corp. to sell its 100% interest in the Mesquite gold mine in California (“Mesquite Mine”) for cash consideration of $158 million. The transaction closed on October 30, 2018.

Cerro San Pedro Mine

The Cerro San Pedro Mine completed active mining in June 2016 and transitioned to residual leaching. The Cerro San Pedro Mine transitioned to the reclamation phase on December 31, 2018.

Blackwater Project

The Blackwater Project continues to move through the permitting phase with the Environmental Assessment (“EA”) expected in 2019. In 2019, the Company will continue to assess alternative project scenarios that may involve lower initial capital requirements and a high-grade pit configuration that would generate positive returns at current metal prices.

Sale of El Morro Stream

In November 2015, as a part of an agreement to sell New Gold’s 30% interest in the El Morro Project to an affiliate of Goldcorp Inc. (“Goldcorp”), the Company entered into an agreement to receive a 4% stream on gold production from the El Morro property, under which New Gold would pay $400 per ounce for the first 217,000 ounces of gold delivered as part of the stream, and would pay $400 per ounce plus a 1% annual inflation adjustment for subsequent ounces of gold delivered as part of the stream (the “El Morro Gold Stream”). In February 2017, New Gold sold the El Morro Gold Stream to Goldcorp for $65 million.

Developments – Financial

In August 2014, New Gold entered into a $300 million revolving secured credit facility with a syndicate of banks led by The Bank of Nova Scotia and RBC Capital Markets (the “Credit Facility”). The Credit Facility was amended in November 2015, February 2016, October 2016, May 2017, June 2017, and amended and restated in October 2018. The size of the Credit Facility is now $400 million and term extends to August 2021. The terms of the Credit Facility require the Company to satisfy various affirmative and negative covenants and to meet certain financial ratios and tests. Following the amendment and restatement of the Credit Facility in October 2018, the maximum ratio of net debt to earnings before interest, taxes, depreciation, amortization, exploration, impairment and other non-cash adjustments (“Adjusted EBITDA”) covenant (“Leverage Ratio”) for future periods (as measured on a rolling four-quarter basis at the end of every quarter) is 4.5 to 1.0 and the maximum ratio of total secured debt to Adjusted EBITDA covenant for future periods is 2.0 to 1.0.

In October 2016, New Gold purchased put options with a strike price of $1,300 per ounce covering 120,000 ounces of gold and simultaneously sold call options with a strike price of $1,400 per ounce covering 120,000 ounces of gold. These contracts covered 20,000 ounces of gold per month for the first six months of 2017. In June 2017, New Gold purchased put options with a strike price of $1,250 per ounce covering 120,000 ounces of gold and simultaneously sold call options with a strike price of $1,400 per ounce covering 120,000 ounces of gold. These contracts covered 20,000 ounces of gold per month for the last six months of 2017. In December 2018, New Gold purchased put options with a strike price of $1,230 per ounce covering 192,000 ounces of gold and simultaneously sold call options with a strike price of $1,300 per ounce covering 192,000 ounces of gold. These contracts covered 16,000 ounces of gold per month for 2019.

| 10 | |

|

In November 2016, New Gold fixed the price for 31.7 million pounds of the Company's copper production in the first six months of 2017 at $2.52 per pound using swap contracts that settled against the monthly average London Metals Exchange price. The swap contracts covered 5.3 million pounds of copper per month from January through June 2017. In February 2017, New Gold fixed the price for 43.7 million pounds of the Company’s copper production in the second half of 2017 at $2.73 per pound using swap contracts that settled against the monthly average London Metals Exchange price. The swap contracts covered 7.3 million pounds of copper per month from July through December 2017. In October 2017, New Gold purchased put options with a strike price of $3.00 per pound covering 60 million pounds of its 2018 production and simultaneously sold call options with a strike price of $3.37 per ounce covering 60 million pounds of its 2018 production. In December 2018, New Gold purchased put options with a strike price of $2.50 per pound covering 21,600 tonnes of its 2018 production and simultaneously sold call options with a strike price of $3.00 per ounce covering 21,600 tonnes of its 2018 production.

On February 22, 2017, New Gold announced that it had entered into an agreement with a syndicate of underwriters (the “Underwriters”) pursuant to which they agreed to purchase, on a bought deal basis, 53,600,000 of the Company’s common shares (“Common Shares”) at a price of $2.80 per share (the “Offering”), for aggregate gross proceeds to the Company of approximately $150 million. In addition, the Company agreed to grant to the Underwriters an option to purchase up to an additional 8,040,000 Common Shares at a price of $2.80 per share, on the same terms and conditions as the Offering, which was exercised in full by the Underwriters. The Offering closed on March 10, 2017. The aggregate gross proceeds of the Offering to the Company were approximately $173 million and proceeds net of underwriting fees and expenses were approximately $164.5 million.

On May 18, 2017, New Gold announced that it had completed an offering of $300 million aggregate principal amount of 6.375% Senior Notes due 2025. The Company used the net proceeds from the offering, together with cash on hand, to fund the redemption of all of its outstanding $300 million 7.00% Senior Notes due 2020.

DESCRIPTION OF THE BUSINESS

The Company’s material operating assets consist of the Rainy River Mine and New Afton Mine in Canada. New Gold also owns the Cerro San Pedro Mine in Mexico, which transitioned to the reclamation phase on December 31, 2018. It also owns the Blackwater Project in Canada. For purposes of NI 43-101, the Company considers the Rainy River Mine and the New Afton Mine to be its material properties.

New Gold is continually working to maximize shareholder value through diversified production, maintaining an attractive risk profile and enhancing growth potential in a safe and an environmentally and socially responsible manner.

Refer to the Company’s MD&A for the year ended December 31, 2018, available under the Company’s profile on SEDAR at www.sedar.com, for a detailed description of the Company’s business, including each of its operating segments.

Specialized Skills and Knowledge

All aspects of New Gold’s business require specialized skills and knowledge. Such required areas of specialized skills and knowledge include geology, drilling, mineral resource estimation, mine planning and mineral reserve estimation,

| 11 | |

|

metallurgy, engineering, construction, technology, community and public relations, regulatory compliance, legal and accounting.

Principal Products

The Company’s principal products are gold, copper and silver, which generally require refining or smelting to become marketable metal. As described in more detail with respect to each operation, the Company uses the services of refiners to refine gold doré. The refined gold is sold to bullion banks or gold trading counterparties at market prices, though in some cases the Company sells doré to such banks and counterparties with delivery to the refinery. Copper concentrate produced by the New Afton Mine is sold to various smelters or concentrate marketing firms. The Company has also entered into financial instruments, such as option or swap contracts, for the purpose of hedging gold and copper prices – see “Developments – Financial” on page 10. There are worldwide gold, copper and silver markets into which the Company can sell and, as a result, the Company is not dependent on a particular purchaser with regard to the sale of the gold, copper and silver which it produces. Further, due to the availability of alternative refineries and smelters, the Company is not dependent on the services on any one refiner or smelter.

Competitive Conditions

The precious and base mineral exploration and mining business is competitive. The Company competes with numerous other companies and individuals in the search for and the acquisition of attractive mineral properties. The ability of the Company to acquire mineral properties in the future will depend on its ability to develop its present properties, and on its ability to select and acquire suitable producing properties or prospects for development or mineral exploration.

Operations

Mineral Reserves and Mineral Resources

The Company has the following Mineral Reserves and Mineral Resources: gold and silver at the Rainy River Mine; gold, copper and silver at the New Afton Mine; and gold and silver at the Blackwater Project. See “Mineral Reserve and Mineral Resource Estimates” on page 14.

Foreign Operations

The Company currently owns 100% of the Cerro San Pedro Mine in Mexico. Any changes in regulations (or the application of regulations) or shifts in political attitudes in these foreign jurisdictions are beyond the control of the Company and may adversely affect its business. Future development and operations may be affected in varying degrees by factors such as government regulations (or changes to such regulations or the application of regulations) with respect to the restrictions on production, export controls, income taxes, expropriation of property, repatriation of profits, environmental legislation, land use, water use, operating activities, land claims of local people and mine safety. The impact of these factors cannot be accurately predicted. See “Risk Factors – Foreign Operations” on page 53.

| 12 | |

|

Employees

As at December 31, 2018, the Company had the following employees:

| Location | Employees |

| Corporate Office | 33 |

| Rainy River Mine | 682 |

| New Afton Mine | 411 |

| Cerro San Pedro Mine(1) | 135 |

| Blackwater Project | 6 |

| Total | 1267 |

| (1) | As at December 31, 2018, 41 employees at the Cerro San Pedro Mine belonged to a union. |

Environmental Protection and Social and Environmental Practices

New Gold is committed to excellence in corporate social responsibility. The Company considers its ability to make a lasting and positive contribution toward sustainable development a key driver to achieving a productive and profitable business. New Gold aims to achieve these objectives through the protection of the health and well-being of its people and host communities as well as maintaining industry leading practices in the areas of environmental stewardship and community engagement and development. As a partner of the United Nations Global Compact, New Gold’s policies and practices are guided by its principles with reference to human rights, labour, environmental stewardship and anti-corruption. As a member of the Mining Association of Canada (“MAC”), New Gold’s operations adopt the MAC’s Towards Sustainable Mining protocols which form part of the New Gold Environmental Management Standards and Community Engagement and Development Management Standards.

New Gold’s corporate social responsibility objectives include promoting and protecting the welfare of its employees through safety-first work practices, upholding fair employment practices and encouraging a diverse workforce, where people are treated with respect and supported to realize their full potential. New Gold believes that people are its most valuable assets and strives to create a culture of inclusiveness that begins at the top and is reflected in its hiring, promotion and overall human resources practices. New Gold encourages tolerance and respect in worker-to-worker relationships. The Company strives to be an employer of choice through the provision of competitive wages and benefits, the implementation of policies that recognize and reward employee performance, and promotion from within wherever possible.

The Company is committed to preserving the long-term health and viability of the natural environments that host its operations. Wherever New Gold operates – in all stages of mining activity, from early exploration and planning, to commercial mining operations through to eventual closure – the Company is committed to excellence in environmental management. Prior to commencing significant construction activities, New Gold carries out comprehensive environmental studies to establish baseline measurements for flora, fauna, earth, air and water. During operations, it promotes the efficient use of raw materials and resources, works to minimize environmental impacts and maintains robust monitoring programs. After mining activities are complete, New Gold’s objective is to restore the land to a level of productivity equivalent to its pre-mining capacity or to an alternative land use determined through consultation with regulatory authorities and the communities of interest.

New Gold is committed to establishing relationships with host communities based on mutual benefit and active engagement with these communities to contribute to their sustainability. Wherever the Company’s operations interact with Indigenous peoples, New Gold promotes understanding of, and respect for, traditional values, customs and culture

| 13 | |

|

and takes meaningful action to consider the interests of Indigenous peoples. New Gold aims to foster open communication with local residents and community leaders so that issues can be resolved collaboratively. The Company believes that by thoroughly understanding the people, their histories, and their needs and aspirations, it can engage in a meaningful and sustainable development process.

The Company’s mining, exploration and development activities are subject to various federal, provincial, state, county and municipal laws and regulations relating to the protection of the environment, including requirements for closure and reclamation of mining properties. In all jurisdictions where New Gold operates, specific statutory and regulatory requirements and standards must be met throughout the exploration, development and operations stages of a mining property with regard to air quality, water quality, fisheries and wildlife protection, solid and hazardous waste management and disposal, noise, land use and reclamation. Details and quantification of New Gold’s reclamation and closure costs obligations are set out in Note 17 of the Company’s audited consolidated financial statements for the year ended December 31, 2018.

Management estimates the undiscounted closure cost for all of its properties is $116.6 million as at December 31, 2018. As at December 31, 2018, the Company had posted letters of credit or other financial assurance in an aggregate amount of $110.8 million to address these liabilities.

Technical Information

CIM Standards Definitions

New Gold’s estimates of Mineral Reserves and Mineral Resources have been calculated in accordance with the CIM Definitions Standards for Mineral Reserves and Mineral Resources adopted by the Canadian Institute of Mining, Metallurgy and Petroleum ("CIM”) Council on May 10, 2014 (the “CIM Standards”).

Technical Terms and Abbreviations

Unless otherwise defined, technical terms used in this Annual Information Form are set out in Schedule B and abbreviations terms used are defined in Schedule C.

Mineral Reserve and Mineral Resource Estimates

On February 14, 2019, the Company reported consolidated Mineral Reserve and Mineral Resource estimates for its mines and development projects as at December 31, 2018. A summary of total gold, silver and copper contained within New Gold’s estimated Mineral Reserves and Mineral Resources is set out in the table below:

| Contained metal | |||

| Gold Koz |

Silver Koz |

Copper Mlbs | |

| PROVEN AND PROBABLE RESEVES | 13,433 | 76,196 | 903 |

| Rainy River | 4,186 | 12,116 | - |

| New Afton | 1,077 | 3,280 | 903 |

| Blackwater | 8,170 | 60,800 | - |

| MEASURED AND INDICATED RSOURCES (Exclusive of Reserves) | 4,600 | 19,699 | 891 |

| INFERRED RESOURCES | 1,001 | 3,860 | 132 |

Notes to the Company’s Mineral Reserve and Mineral Resource estimates are provided on pages 17-18.

Details of the Company’s Mineral Reserve and Mineral Resource estimates are presented in the following tables.

| 14 | |

|

Mineral Reserves Estimates (as at December 31, 2018)

| Metal grade | Contained metal | ||||||

| Tonnes 000s |

Gold g/t |

Silver g/t |

Copper % |

Gold Koz |

Silver Koz |

Copper Mlbs | |

| RAINY RIVER | |||||||

| Direct processing reserves | |||||||

| Open Pit | |||||||

| Proven | 18,663 | 1.24 | 2.4 | - | 744 | 1,450 | - |

| Probable | 47,670 | 1.18 | 3.0 | - | 1,810 | 4,542 | - |

| Open Pit P&P (direct proc.) | 66,333 | 1.20 | 2.8 | - | 2,554 | 5,993 | - |

| Underground | |||||||

| Proven | - | - | - | - | - | - | - |

| Probable | 8,954 | 3.55 | 9.5 | - | 1,021 | 2,728 | - |

| Underground P&P (direct proc.) | 8,954 | 3.55 | 9.5 | - | 1,021 | 2,728 | - |

| Low grade reserves | |||||||

| Open Pit | |||||||

| Proven | 8,430 | 0.36 | 2.0 | - | 97 | 541 | - |

| Probable | 32,714 | 0.35 | 2.3 | - | 366 | 2,428 | - |

| Open Pit P&P (low grade) | 41,145 | 0.35 | 2.2 | - | 463 | 2,969 | - |

| Surface Stockpiles | |||||||

| Proven | 7,307 | 0.63 | 1.8 | - | 147 | 426 | - |

| Open Pit P&P (stockpile) | 7,307 | 0.63 | 1.8 | - | 147 | 426 | - |

| Combined P&P | |||||||

| Proven | 34,400 | 0.89 | 2.4 | - | 989 | 2,291 | - |

| Probable | 89,339 | 1.11 | 3.4 | - | 3,197 | 9,825 | - |

| Total Rainy River P&P | 123,739 | 1.05 | 3.0 | - | 4,186 | 12,116 | - |

| NEW AFTON | |||||||

| A&B Zones | |||||||

| Proven | - | - | - | - | - | - | - |

| Probable | 25,731 | 0.51 | 1.9 | 0.74 | 420 | 1,612 | 420 |

| C-zone | |||||||

| Proven | - | - | - | - | - | - | - |

| Probable | 26,911 | 0.76 | 1.9 | 0.82 | 657 | 1,668 | 484 |

| Total New Afton P&P | 52,642 | 0.64 | 1.9 | 0.78 | 1,077 | 3,280 | 903 |

| BLACKWATER | |||||||

| Direct processing reserves | |||||||

| Proven | 124,500 | 0.95 | 5.5 | - | 3,790 | 22,100 | - |

| Probable | 169,700 | 0.68 | 4.1 | - | 3,730 | 22,300 | - |

| P&P (direct proc.) | 294,300 | 0.79 | 4.7 | - | 7,510 | 44,400 | - |

| Low grade reserves | |||||||

| BLACKWATER | |||||||

| Direct processing reserves | |||||||

| Proven | 124,500 | 0.95 | 5.5 | - | 3,790 | 22,100 | - |

| Probable | 169,700 | 0.68 | 4.1 | - | 3,730 | 22,300 | - |

| P&P (direct proc.) | 294,300 | 0.79 | 4.7 | - | 7,510 | 44,400 | - |

| Low grade reserves | |||||||

| Proven | 20,100 | 0.50 | 3.6 | - | 330 | 2,300 | - |

| Probable | 30,100 | 0.34 | 14.6 | - | 330 | 14,100 | - |

| P&P (low grade) | 50,200 | 0.40 | 10.2 | - | 650 | 16,400 | - |

| Combined Direct proc. & Low grade | |||||||

| Proven | 144,600 | 0.88 | 5.3 | - | 4,110 | 24,400 | - |

| Probable | 199,800 | 0.63 | 5.7 | - | 4,050 | 36,400 | - |

| Total Blackwater P&P | 344,400 | 0.74 | 5.5 | - | 8,170 | 60,800 | - |

| Total Proven & Probable Reserves | 13,433 | 76,196 | 903 | ||||

| 15 | |

|

Measured & Indicated Mineral Resources Estimates (exclusive of Mineral Reserves) (as at December 31, 2018)

| Metal grade | Contained metal | ||||||

| Tonnes 000s |

Gold g/t |

Silver g/t |

Copper % |

Gold Koz |

Silver Koz |

Copper Mlbs | |

| RAINY RIVER | |||||||

| Direct processing resources | |||||||

| Open Pit | |||||||

| Measured | 2,990 | 1.13 | 5.6 | - | 109 | 534 | - |

| Indicated | 26,370 | 1.13 | 3.3 | - | 955 | 2,759 | - |

| Open Pit M&I (direct proc.) | 29,360 | 1.13 | 3.5 | - | 1,064 | 3,292 | - |

| Underground | |||||||

| Measured | - | - | - | - | - | - | - |

| Indicated | 7,908 | 3.06 | 8.6 | - | 778 | 2,188 | - |

| Underground M&I (direct proc.) | 7,908 | 3.06 | 8.6 | - | 778 | 2,188 | - |

| Low grade resources | |||||||

| Open Pit | |||||||

| Measured | 2,465 | 0.35 | 3.1 | - | 28 | 248 | - |

| Indicated | 23,135 | 0.36 | 2.1 | - | 269 | 1,592 | - |

| Open Pit M&I (low grade) | 25,600 | 0.36 | 2.2 | - | 297 | 1,840 | - |

| Combined M&I | |||||||

| Measured | 5,455 | 0.78 | 4.5 | - | 137 | 782 | - |

| Indicated | 57,412 | 1.08 | 3.5 | - | 2,002 | 6,539 | - |

| Total Rainy River M&I | 62,867 | 1.06 | 3.6 | - | 2,139 | 7,321 | - |

| NEW AFTON | |||||||

| A&B Zones | |||||||

| Measured | 15,239 | 0.64 | 2.0 | 0.86 | 315 | 972 | 289 |

| Indicated | 8,530 | 0.51 | 2.8 | 0.77 | 140 | 776 | 145 |

| A&B Zone M&I | 23,769 | 0.60 | 2.3 | 0.83 | 455 | 1,748 | 434 |

| C-zone | |||||||

| Measured | 5,711 | 0.79 | 2.0 | 0.96 | 144 | 366 | 120 |

| Indicated | 11,976 | 0.72 | 2.1 | 0.87 | 279 | 809 | 230 |

| C-zone M&I | 17,687 | 0.74 | 2.1 | 0.90 | 423 | 1,174 | 350 |

| HW Lens | |||||||

| Measured | - | - | - | - | - | - | - |

| Indicated | 10,951 | 0.52 | 2.1 | 0.44 | 183 | 722 | 107 |

| HW Lens M&I | 10,951 | 0.52 | 2.1 | 0.44 | 183 | 722 | 107 |

| Combined M&I | |||||||

| Measured | 20,950 | 0.68 | 2.0 | 0.89 | 459 | 1,338 | 410 |

| Indicated | 31,457 | 0.60 | 2.3 | 0.69 | 602 | 2,307 | 481 |

| Total New Afton M&I | 52,407 | 0.63 | 2.2 | 0.77 | 1,061 | 3,645 | 891 |

| BLACKWATER | |||||||

| Direct processing resources | |||||||

| Measured | 288 | 1.39 | 6.6 | - | 13 | 61 | - |

| Indicated | 45,249 | 0.84 | 4.6 | - | 1,225 | 6,692 | - |

| M&I (direct proc.) | 45,537 | 0.85 | 4.6 | - | 1,238 | 6,753 | - |

| Low grade resources | |||||||

| Measured | - | - | - | - | - | - | - |

| Indicated | 15,779 | 0.32 | 3.9 | - | 162 | 1,980 | - |

| M&I (low grade) | 15,779 | 0.32 | 3.9 | - | 162 | 1,980 | - |

| Total Blackwater M&I | 61,316 | 0.71 | 4.4 | - | 1,400 | 8,733 | - |

| Total M&I RESOURCES | 4,600 | 19,699 | 891 | ||||

| 16 | |

|

Inferred Mineral Resources (as at December 31, 2018)

| Metal grade | Contained metal | ||||||

| Tonnes 000s |

Gold g/t |

Silver g/t |

Copper % |

Gold Koz |

Silver Koz |

Copper Mlbs |

|

| RAINY RIVER | |||||||

| Direct processing | |||||||

| Open Pit | 5,883 | 1.17 | 3.1 | - | 222 | 578 | - |

| Underground | 1,270 | 3.68 | 3.8 | - | 150 | 156 | - |

| Total Direct Processing | 7,153 | 1.62 | 3.2 | - | 372 | 733 | - |

| Low grade resources | |||||||

| Open Pit | 6,049 | 0.37 | 1.4 | - | 72 | 274 | - |

| Rainy River Inferred | 13,202 | 1.05 | 2.4 | - | 444 | 1,007 | - |

| NEW AFTON | |||||||

| A&B Zones | 6,530 | 0.35 | 1.4 | 0.38 | 74 | 295 | 54 |

| C-zone | 7,034 | 0.43 | 1.4 | 0.51 | 98 | 309 | 77 |

| HW Lens | - | - | - | - | - | - | - |

| New Afton Inferred | 13,564 | 0.39 | 1.4 | 0.45 | 172 | 605 | 132 |

| BLACKWATER | |||||||

| Direct processing | 13,905 | 0.76 | 4.0 | - | 341 | 1,788 | - |

| Low grade resources | 4,207 | 0.33 | 3.4 | - | 44 | 460 | - |

| Blackwater Inferred | 18,112 | 0.66 | 3.9 | - | 385 | 2,248 | - |

| Total Inferred | 1,001 | 3,860 | 132 | ||||

Notes to Mineral Reserve and Resource Estimates

| 1. | New Gold’s Mineral Reserves and Mineral Resources have been estimated in accordance with the CIM Standards, which are incorporated by reference in NI 43-101. |

| 2. | All Mineral Reserve and Mineral Resource estimates for New Gold’s properties and projects are effective December 31, 2018. |

| 3. | New Gold’s year-end 2018 Mineral Reserves and Mineral Resources have been estimated based on the following metal prices and foreign exchange (FX) rate criteria: |

|

Gold $/ounce |

Silver $/ounce |

Copper $/pound |

FX CAD:USD | |

| Mineral Reserves | $1,275 | $17.00 | $3.00 | 1.30 |

| Mineral Resources | $1,350 | $18.00 | $3.25 | 1.30 |

| 4. | Lower cut-offs for the Company’s Mineral Reserves and Mineral Resources are outlined in the following table: |

| Mineral Property |

Mineral Reserves Lower cut-off |

Mineral Resources Lower Cut-off | |

| Rainy River | O/P direct processing: | 0.30 – 0.50 g/t AuEq | 0.30 – 0.50 g/t AuEq |

| O/P low grade material: | 0.30 g/t AuEq | 0.30 g/t AuEq | |

| U/G direct processing: | 2.20 g/t AuEq | 2.00 g/t AuEq | |

| New Afton | Main Zone – B1 & B2 Blocks: | C$ 17.00/t | All Resources: 0.40% CuEq |

| B3 Block & C-zone: | C$ 24.00/t | ||

| Blackwater | O/P direct processing: | 0.26 – 0.38 g/t AuEq | All Resources: 0.40 g/t AuEq |

| O/P low grade material: | 0.32 g/t AuEq | ||

| 17 | |

|

| 5. | New Gold reports its measured and indicated mineral resources exclusive of mineral reserves. Measured and indicated mineral resources that are not mineral reserves do not have demonstrated economic viability. Inferred mineral resources have a greater amount of uncertainty as to their existence and technical feasibility, do not have demonstrated economic viability, and are likewise exclusive of mineral reserves. Numbers may not add due to rounding. |

| 6. | Mineral resources are classified as measured, indicated and inferred based on relative levels of confidence in their estimation and on technical and economic parameters consistent with the methods considered most suitable to their potential commercial extraction. For Rainy River the designators ‘open pit’ and ‘underground’ have been applied to differentiate the envisioned mining method for different portions of a resource. The designators ‘direct processing’ and ‘lower grade material’ have been applied to differentiate material envisioned to be mined and processed directly from material to be mined and stored separately for future processing. Proven mineral reserves referred to as ‘Surface Stockpiles’ represents material that has been mined and stockpiled for future processing. |

| 7. | Mineral reserves and mineral resources may be materially affected by environmental, permitting, legal, title, taxation, sociopolitical, marketing and other risks and relevant issues. Additional details regarding mineral reserve and mineral resource estimation, classification, reporting parameters, key assumptions and associated risks for each of New Gold’s material properties are provided in the respective NI 43-101 Technical Reports, which are available at www.sedar.com. |

| 8. | The preparation of New Gold's consolidated statement and estimate of mineral reserves has been completed under the oversight and review of Mr. Nicholas Kwong, Director of Technical Services for the Company. Mr. Kwong is a Professional Engineer and member of the of Professional Engineers Ontario. Preparation of the Company’s consolidated statement and estimate of mineral resources has been completed under the oversight and review of Mr. Mark Petersen, a consultant to New Gold and former Vice President, Exploration for the Company. Mr. Petersen is a Professional Geoscientist (P. Geo.) and Practising Member of the Association of Professional Geoscientists of Ontario, an SME Registered Member and an AIPG Certified Professional Geologist. Messrs. Kwong and Petersen are "Qualified Persons" as defined by NI 43-101. |

| 18 | |

|

MINERAL PROPERTIES

Rainy River Mine, Canada

Project Description, Location, Access and Other Information

The Rainy River Mine is located in the southern half of Richardson Township, approximately 50 kilometres northwest of Fort Frances in northwestern Ontario, Canada. Regional population centres Kenora and Thunder Bay lie 162 kilometres to the north and 418 kilometres to the east, respectively. Access to the mine area is via secondary all-weather roads branching off Trans-Canada Highways 11 and 71. An east-west rail line is located 21 kilometres to the south, populated by a number of small towns and villages. Temperature extremes generally range from 35 degrees Celsius to minus 40 degrees Celsius. Annual precipitation averages approximately 60 centimetres rainfall and 150 centimetres snowfall. Mining activities are conducted year-round.

Terrain in the vicinity of the Rainy River Mine is dominated by a distinct northwest to southeast divide known as the Rainy Lake-Lake of the Woods Moraine. Topography is relatively gentle, with relief ranging from zero southwest of the divide to up to 90 metres northeast of the divide. In areas of low relief, bedrock typically is overlain by glacial till, thick silts and clays and, in poorly drained areas, by thick peat.

The Rainy River Mine occupies approximately 6,050 hectares, comprising 87 patented mining rights and surface rights claims (including 8 leasehold interest mining rights and/or surface rights claims). In addition, the Company has a land package of approximately 31,114 hectares surrounding the mine site, including patented mining rights and/or, surface rights and unpatented claims. The land package includes claims acquired from GoldON Resources Ltd. in January 2019 northeast of the mine site. All unpatented claims are in good standing and assessment work credits are sufficient to maintain that standing for several years.

All mineral tenures are held in the name of New Gold. The currently defined mineral reserves and mineral resources lie largely within nine patented claims, a portion of which are covered by either a 2% NSR royalty or a 10% net profits interest royalty. In addition, New Gold has agreed to financial participation in the Mine in the form of royalties in favour of certain First Nations.

In July 2015, New Gold entered into a $175 million streaming agreement with Royal Gold A.G. a wholly owned subsidiary of Royal Gold Inc. (“Royal Gold”) in which Royal Gold agreed to provide New Gold with an upfront deposit of $175 million, which was used for the development of the Rainy River Mine, in return for: (i) 6.5% of the Project’s gold production up to a total of 230,000 ounces of gold, and 3.25% of the Mine’s gold production thereafter; and (ii) 60% of the Project’s silver production up to a total of 3.1 million ounces of silver, and 30% of the Project’s silver production thereafter. In addition to the upfront deposit, Royal Gold will pay 25% of the average spot gold or silver price at the time each ounce of gold or silver is delivered under the stream. The terms of the streaming agreement also require the Company to meet a Leverage Ratio for future periods (as measured on a rolling four-quarter basis at the end of every quarter) of 3.5 to 1.0, among other covenants.

History

Exploration commenced in the Rainy River area during the period 1967 to 1989, during which time the Ontario Geological Survey conducted sporadic geologic mapping, and companies including Noranda, International Nickel Corporation of Canada, Hudson’s Bay Exploration and Development and Mingold Resources were active in the area.

| 19 | |

|

Nuinsco Resources Limited (“Nuinsco”) initiated exploration of the area in 1990. During the period 1993 through 2004, Nuinsco engaged in geologic mapping, geochemical grid sampling, magnetic and IP geophysical surveys and Landsat remote sensing studies. Additionally, Nuinsco completed 597 reverse circulation holes and 217 diamond drill holes (49,515 metres) during the period. The program resulted in the discovery of three significant zones of gold mineralization (the 17, 34 and 433 Zones). Nuinsco drilled a final eight diamond drill holes (1,549 metres) in 2004 to test the depth continuity of the 34 Zone.

RRRL acquired a 100% interest in the Rainy River Mine from Nuinsco in June 2005. RRRL re-logged portions of historical core, established a GIS database, conducted petrographical studies, and carried out airborne and ground-based geophysical surveys. During the period 2005 through 2007, RRRL drilled more than 100 reverse circulation holes and 209 diamond drill holes (95,340 metres). Additional diamond drilling by RRRL from 2008 through February 2011 totaled 449 diamond drill holes (239,329 metres) and 375 diamond drill holes (181,682 metres) drilled from March to December 2011. RRRL published a Feasibility Study for the Project in May 2013 based on 1,435 diamond drill holes (662,849 metres) representing drill results through June 10, 2012.

RRRL drilled an additional 225 diamond drill holes (77,969 metres) between August 2012 and June 2013, focusing on the Intrepid Zone situated one kilometre east of the proposed open pit. By June 2013, a number of significant gold mineralized zones had been defined over a 3.5-kilometre strike length. New Gold acquired the Rainy River Mine through its purchase of RRRL in 2013. New Gold completed an updated Feasibility Study in January 2014 incorporating the previous exploration results. In 2015, New Gold acquired Bayfield Ventures Ltd. (“Bayfield”), which held a 100% interest in six patented mining rights claims and six unpatented claims totaling approximately 11 square kilometres adjacent to the Rainy River Mine.

Geological Setting and Mineralization

The Rainy River Mine lies within the Rainy River Greenstone Belt, part of the larger Late Archean age Wabigoon Subprovince of komatiitic to calc-alkaline metavolcanics overlain by clastic and chemical sediments and intruded by granitoid batholiths. The intrusions deformed their host rocks into synformal fold structures, often producing shear zones along the axial planes. Rocks within the immediate area of the mine comprise a series of tholeiitic mafic rocks structurally overlain by calc-alkalic intermediate to felsic metavolcanic rocks. Rocks of intermediate dacitic composition host most of the gold mineralization.

In much of the mine area and surrounding region the Archean metavolcanic and sedimentary rocks are overlain by a sequence of unconsolidated Mesozoic and Quaternary age glacial sediments and tills containing locally anomalous concentrations of detrital gold, auriferous pyrite and copper-zinc sulphides derived from the underlying mineralized bedrock. This sequence is in turn overlain by a younger sequence of glacially-derived clays, silts and till that are devoid of any anomalous detrital gold or sulphides.

Four main styles of gold and silver mineralization have been identified at Rainy River: gold-bearing sulphide ± quartz stringers and veins in felsic quartz-phyric rocks (ODM/17 and 34, Beaver Pond, 433 and HS Zones); quartz-ankerite-pyrite shear veins in mafic volcanic rocks (CAP/South Zone); sulphide-bearing silver-enriched quartz veinlets in dacitic tuffs and breccias (Intrepid Zone) and copper-nickel-platinum group metals mineralization hosted in a small younger mafic-ultramafic intrusion (34 Zone) situated within the main cluster of gold and silver deposits. All deposits show some degree of deformation, excepting the copper-nickel-platinum-bearing type. Most of the gold mineralization identified to date occurs in the sulphide-bearing stringers and veins within the felsic quartz-phyric rocks.

| 20 | |

|

Mineralized zones hosted by the felsic rocks generally follow the regional northwesterly strike and southerly dip of stratigraphy. The largest of these is the ODM/17 Zone which extends 1600 metres along strike, 975 metres down dip, and over a true width of 200 metres.

The Rainy River mineralization is interpreted to be a hybrid deposit type consisting of early gold-rich volcanogenic sulphide mineralization overprinted by shear-hosted mesothermal gold mineralization associated with regional deformation. A final stage of hydrothermal mineralization in the main auriferous zones crosscuts both types of earlier mineralization.

Exploration and Drilling

Exploration targeting and drilling undertaken in the Rainy River project area of the mine prior to New Gold’s acquisition of the property through its acquisition of RRRL are summarized in the section entitled “History”.

Since New Gold’s acquisition of RRRL, the Company has focused its exploration efforts within a five kilometre radius of the central mine development area. From January 2014 through December 2018, a total of 96,750 metres of core drilling in 353 holes has been completed to delineate and improve estimation confidence for the classified mineral resource both laterally and at depth, and to provide geotechnical information for the mining operation. The results of this drilling in combination with the historic drilling described above provide the basis for the current mineral resource and mineral reserve estimates.

Drilling procedures conducted by Nuinsco from 1994 to 1998 are not well documented. Drilling carried out from 2005 through 2018 by RRRL, Bayfield and New Gold have utilized predominantly NQ diameter (4.76 cm) drill core. Some deeper holes have been collared in HQ diameter (6.35 cm) and later reduced to NQ diameter to attain target depths. PQ diameter (8.5 cm) drill core was utilized for certain metallurgical samples. Both RRRL and New Gold have realized excellent core recoveries and have surveyed all drill holes and collars according to accepted industry standards. The drilling procedures utilized by RRRL and New Gold are considered consistent with industry best practices and the quantity and quality of the lithological, geotechnical, collar and down-hole survey data collected in the exploration and infill drill programs completed by RRRL and New Gold are considered sufficient to support mineral resource estimation.

Sampling and Analysis

There are no records describing the sampling and analytical methods used by Nuinsco during its drilling programs. Mineralized sections of core were re-sampled and analyzed by RRRL to incorporate into the drill database.

Sampling and analysis of drill core has been conducted via industry best practices under New Gold, RRRL and Bayfield drilling programs. Sampling was typically conducted at nominal 1.5 metre intervals, though Bayfield sampling intervals vary from 0.5 to 1.5 metres in length. Core was sawn and half placed in sample bags for laboratory analysis. Certified reference standards, blanks and duplicates were systematically inserted into the sample batches to be shipped to the lab. Samples were collected on site by a Fort Frances shipping company and delivered directly to the laboratory.

RRRL used two principal accredited laboratories for analyses: ALS Vancouver, British Columbia from 2005 to 2006 and from early 2011 onward; and Accurassay Laboratories in Thunder Bay, Ontario from 2006 to 2011. Bayfield’s drill core was analyzed by Activation Laboratories (“Actlabs”), an accredited laboratory located in Thunder Bay, Ontario. New Gold uses ALS for the analysis of its exploration and resource delineation drilling at the Rainy River Mine. Since the start of commercial production in late 2017, analyses of grade control samples for the open pit (and future underground) mine have been done by an onsite analytical laboratory. All of these laboratories use standard industry analytical procedures: fire assay procedures for precious metal analyses; aqua regia digestion and atomic absorption spectrometry

| 21 | |

|

for metal analyses; and ICP and graphite furnace analyses for calcium, sulfur and other elements required for waste rock characterization. Each laboratory employs an internal QA/QC program in accordance with its accreditation requirements. Additionally, the company employs a separate set of best practice QA/QC protocols for all of its exploration and resource definition sampling programs. These protocols involve a combination of routine checks and duplicate analyses on a minimum of 25 percent of the total number of samples analyzed to assure acceptable levels of sampling accuracy and precision are maintained.

Data verification includes site visits to inspect procedures, QA/QC data validation and examination of database accuracy. Since ALS’s 2011 reinstatement as the primary laboratory for mineral resource drilling at the Rainy River Mine, an overall improvement in QA/QC performance has been noted. The results of data verification as well as 2018 mine production and reconciliation data indicate the data collected for mineral resource definition at the Rainy River Mine adequately reflect deposit dimensions, style, and true widths of mineralization; adequately support the geological interpretations; and are of sufficient analytical and database quality for use in mineral resource estimation.

Mineral Processing and Metallurgical Testing

Metallurgical testing was performed to evaluate the mineralogy of the deposit and contribute to the design of the Rainy River Mine’s processing plant and tailings facility. A number of studies and tests were performed, including mineralization, comminution, gravity separation, flotation, flotation concentrate leaching, whole ore leaching, cyanidation, carbon adsorption modelling, cyanide destruction and solid-liquid separation. It was determined that whole rock leaching with gravity separation was the most economical processing alternative for the ore mainly because, among other reasons, it required less energy and cyanide inputs than other processing alternatives.

Infrastructure, Permitting and Compliance Activities

Infrastructure and local terrain are accessible, with numerous gravel/paved roads, power and water resources and areas for tailings management facilities available within close proximity. Personnel for the mine, including skilled trades and professions, have been and will continue to be sourced through a combination of local hiring and broader recruitment efforts.

Power is supplied to the mine through a connection to a provincial transmission line approximately 17 kilometres to the east. There is a supply of water in the area from the Pinewood River, and a pipeline has been constructed from the Pinewood River to the site. A site water management pond contains water for mineral processing. A water treatment plant will be constructed in 2019. Other infrastructure includes open pit infrastructure, the processing plant, assay laboratory facilities, administrative offices, storage facilities and other support infrastructure.

In 2012, RRRL (prior to its acquisition by New Gold), and six Rainy River-area First Nations entered into a Participation Agreement with respect to the development and operation of the Rainy River Mine. The Participation Agreement identifies key project milestones to be met through mutual cooperation and consultation with the First Nations. In 2014, the Company concluded an Impacts and Benefits Agreement with Naicatchewenin First Nation and Rainy River First Nations embracing commitments to environmental and sustainable development and ensuring that First Nation communities and members benefit from opportunities resulting from the Project in their traditional territory. The Company also concluded Participation Agreements with the Métis Nation of Ontario in 2014, the Big Grassy River First Nation in 2015, the Naotkamegwanning First Nation, Ojibways of Onigaming First Nation and the Anishinaabeg of Naongashing First Nation in 2017, and the Animakee Wa Zhing 37 First Nation in 2018. The Participation Agreements provide for how each of these communities will benefit from the Rainy River Mine. New Gold has ongoing dialogue with local communities and various First Nations in the area surrounding the Rainy River Mine.

| 22 | |

|

During the course of construction of the water and tailings management area (“TMA”) at the Rainy River Mine, deformations were identified at one of the dams associated with such facilities. In line with best practices in Canada, the Company has established an Independent Tailings Review Board (“ITRB”), which is comprised of four independent experts, to provide input with respect to tailings management at New Gold’s operations and projects in Canada. After receiving feedback from the ITRB and the Ministry of Natural Resources and Forestry (“MNRF”) and completion of additional geotechnical drilling to further investigate the ground conditions, New Gold redesigned Rainy River’s tailings management facility. The final redesign included the use of flatter slopes, rock toe buttresses and wick drains, and New Gold also implemented enhanced construction management procedures. The Company has decided to extend aspects of the redesign across all of the water and tailings management facilities. The Company received approval to recommence construction of the TMA from MNRF in mid-November 2016. On September 28, 2017, New Gold announced that the amendment to Schedule 2 of the Metal Mining Effluent Regulations under the Fisheries Act (Canada) to close two small creeks and deposit tailings under the Fisheries Act (Canada), had become effective, which was also required to complete construction of the TMA. The TMA is made up of three cells. Cell 1 is the start-up cell, which provided capacity for mill tailings through March 2018, followed by Cells 2 and 3. Cell 2 was brought into operation in 2018.

In 2017, New Gold was subject to charges in relation to two incidents from 2016. Specifically, on July 13, 2017, New Gold was charged with five breaches of the Environmental Protection Act (Ontario) in connection with alleged effluent discharges at the Rainy River project in July 2016 in excess of permit limits. On November 9, 2017, New Gold plead guilty to discharging un-ionized ammonia above the EPA limit on July 27, 2016 and failing to report a July 20, 2016 discharge above the standard for un-ionized ammonia. The three remaining charges were withdrawn. New Gold was sentenced to a fine of C$100,000 for the July 27, 2016 discharge and C$50,000 for the failure to report the July 20, 2016 discharge. A mandatory victim surcharge of 25% applies to the fines, for a total amount owing of $187,500. In addition, on July 24, 2017, New Gold was charged with two breaches of the Lakes and Rivers Improvement Act (Ontario) in connection with water allegedly overtopping a dam on the Rainy River construction site prior to completion of construction of the dam. On July 11, 2018, New Gold pleaded guilty to one charge and was sentenced to a fine of C$100,000 (plus a mandatory surcharge of 25%); the other charge was withdrawn.

The mine closure plan was accepted by the Ontario Ministry of Energy, Northern Development and Mines (“ENDM”) on February 23, 2015. As of December 31, 2018, bonding of C$83.9 million has been posted pursuant to the closure plan. The undiscounted closure cost liability for Rainy River as at December 31, 2018 is estimated to be $68.5 million. An updated closure plan is expected to be approved by ENDM in 2019, which may affect the amount required for reclamation security.

Mineral Reserve and Mineral Resource Estimates

The Rainy River Mine Mineral Reserves, effective December 31, 2018, are presented in the “Mineral Reserve Estimates” table. The Rainy River Mine Mineral Resources, effective December 31, 2018, are presented in the “Measured and Indicated Mineral Resource Estimates (Exclusive of Mineral Reserves)” and “Inferred Mineral Resource Estimates” tables. See “Description of Business – Mineral Reserve and Mineral Resource Estimates” on page 14. The parameters, assumptions and methodologies applied in generating the mineral reserve and mineral resource estimates are considered reasonable and appropriate. Furthermore, the mining, metallurgical, infrastructure, permitting and other relevant factors relating to the Rainy River Mineral Reserves and Mineral Resources fully support these estimates.

| 23 | |

|

Mining Operations

The Rainy River Mine commenced processing ore on September 14, 2017 and completed its first gold pour on October 5, 2017. Commercial production was achieved on October 19, 2017. The projected life of the Rainy River Mine extends through 2032 based on current mineral reserves and throughput levels.

The life-of-mine plan for Rainy River includes an underground mine. Development of the underground mine began in the second half of 2018 but further development has been deferred to 2020. During 2019, the Company will launch a comprehensive review that includes assessing alternative underground mining scenarios with the overall objective of reducing capital and improving the return on investment for the underground portion of the life of mine.

Mining Methods