UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ACT OF 1934

For the fiscal year ended April 30, 2020

or

ACT OF 1934

For the transition period from _______________ to _______________

Commission File Number: 000-14798

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||

(Address of principal executive offices) | (Zip Code) | |||

(540 ) 665-9100

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

☒ | Accelerated filer | ☐ | ||

Non-accelerated filer | ☐ | Smaller reporting company | ||

Emerging growth company | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes ☐ No ☒

The aggregate market value of the registrant's Common Stock, no par value, held by non-affiliates of the registrant as of October 31, 2019, the last business day of the Company’s most recent second quarter was $1,662,345,906 .

As of June 19, 2020, 16,942,569 shares of the Registrant's Common Stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive Proxy Statement for the Annual Meeting of Shareholders to be held on August 20, 2020 (“Proxy Statement”) are incorporated by reference into Part III of this Form 10-K.

American Woodmark Corporation

2020 Annual Report on Form 10-K

TABLE OF CONTENTS

PART I | ||

Item 1. | 2 | |

Item 1A. | 5 | |

Item 1B. | 12 | |

Item 2. | 13 | |

Item 3. | 13 | |

Item 4. | 13 | |

13 | ||

PART II | ||

Item 5. | 14 | |

Item 6. | 16 | |

Item 7. | 17 | |

Item 7A. | 28 | |

Item 8. | 29 | |

Item 9. | 64 | |

Item 9A. | 64 | |

Item 9B. | 64 | |

PART III | ||

Item 10. | 64 | |

Item 11. | 65 | |

Item 12. | 65 | |

Item 13. | 65 | |

Item 14. | 65 | |

PART IV | ||

Item 15. | 65 | |

Item 16. | 69 | |

SIGNATURES | 70 | |

1

PART I

Item 1. BUSINESS

Our Company

American Woodmark Corporation (“American Woodmark,” the “Company,” “we,” “our” or “us”) was incorporated in 1980 by the four principal managers of the Boise Cascade Cabinet Division through a leveraged buyout of that division. We operated privately until 1986 when we became a public company through a registered public offering of common stock.

We manufacture and distribute kitchen, bath and home organization products for the remodeling and new home construction markets. Our products are sold on a national basis directly to home centers and builders and through a network of independent dealers and distributors. We presently operate 18 manufacturing facilities and eight primary service centers across the country and Mexico.

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements, and all amendments to those reports are available free of charge on our website, americanwoodmark.com, as soon as reasonably practicable after such material is electronically filed with, or furnished to, the Securities and Exchange Commission. The contents of our website are not, however, part of, or incorporated by reference into, this report.

Our Business

Our business offers made-to-order cabinetry in over 550 different cabinet lines, ranging in price from relatively inexpensive to medium-priced styles. These cabinets are offered in a broad range of sizes, construction and decorative options to achieve a wide array of design layouts. To satisfy the fashion and style needs of the market place we offer over 100 door designs with a targeted range of painted or stained finishes, or engineered finishes under the Duraform® mark; on fronts made in a variety of wood species, including maple, cherry and oak as well as engineered materials.

Additionally, we offer value-based assembled cabinet products for stock kitchen and bath, ready-to-assemble cabinetry for home organization, countertops and accessories. These lines are available in a more targeted finish and door style assortment, and include hundreds of products appropriate for home centers, builders, dealers and remodeling contractors.

Our products are sold under the brand names of American Woodmark®, Timberlake®, Shenandoah Cabinetry®, Waypoint Living Spaces®, Estate by RSI®, Continental Cabinets®, VillaBath by RSI®, Stor-It-All® and Professional Cabinet Solutions®. Products are also sold under key customer’s private label brands, such as Hampton Bay®, Glacier Bay®, Style Selections®, Allen + Roth®, Home Decorators Collection and Project Source.

Our Products

We offer a wide variety of products that fall into product lines including kitchen cabinetry, bath cabinetry, office cabinetry, home organization and hardware. Our cabinetry products are available in a variety of designs, finishes and finish colors and door styles.

We offer products in the following categories: made-to-order and stock. Stock products represent cash and carry products sold through home centers. Made-to-order products typically utilize higher grade materials with more options as compared to stock and are all special ordered and shipped directly to the home from the factory. Our home organization products are exclusively stock products. Our kitchen cabinetry and bath cabinetry are offered across all product categories (made-to-order and stock) and our office cabinetry is offered as stock. Our stock products are sold through home centers, while our made-to-order products are sold through home centers, builders and independent dealers and distributors.

Our Market

Our products are sold on a national basis across the United States to the remodeling and new home construction markets. We service these markets through three primary channels: home centers, builders, and independent dealers and distributors. We distribute our products to each market channel directly from our assembly plants and through a third party logistics network.

Our Customers

We serve three main categories of customers: home center customers, builders and independent dealers and distributors.

2

Home Center Customers

Contractors, builders, remodelers and do-it-yourself homeowners use our products primarily for repair and remodel (“R&R”) projects. Products for R&R projects are predominately purchased through home centers such as Home Depot and Lowe’s. Due to the market presence, store network and customer reach of these large home centers, our strategy has been to develop long-term strategic relationships with both Home Depot and Lowe’s to distribute our products. During the fiscal year ended April 30, 2020 (“fiscal 2020”), Home Depot and Lowe’s combined accounted for approximately 46.5% of net sales of the Company. The loss of either Home Depot or Lowe’s as a customer would have a material adverse effect on us.

Builders

The builder business represents a large portion of our overall revenue and has historically been a strategic component of our go-to-market strategy. We serve the majority of the top U.S. builders with a high degree of geographic concentration around major metro areas where single family starts are most robust. We also serve multi-family builders, primarily in the Southern California metro area. Our various service center locations serve the function of being close to this business and enable us to deliver exceptional service to our builder partners. During fiscal 2020, builders accounted for approximately 40.5% of net sales of the Company.

Independent Dealers & Distributors

In 2010, we expanded our business into the dealer channel with the launch of the Waypoint Living Spaces® brand. Today, we sell this brand to over 1,300 regional and local dealers across the country. The dealer channel of the market is the largest by volume, characterized by a high degree of entrepreneurship and one that rewards suppliers that deliver great service. Our ability to provide superior value delivered with exceptional service has helped drive our expansion into this channel and will continue to be a strong growth and market share opportunity for us. Within our distributor channel we also sell our Timberlake® brand through a network of regional distributors who are focused on selling a complete variety of building materials to small and midsized builders and contractors within their local markets. During fiscal 2020, independent dealers and distributors accounted for approximately 13.0% of net sales of the Company.

Manufacturing, Distribution and Service

Our manufacturing facilities are strategically located to serve our customers, which enhances our ability to provide high quality, value priced products with low production costs. We manufacture our products across 18 facilities located in Maryland, Indiana, West Virginia, Tennessee, Georgia, Arizona, Kentucky, Virginia, California, Texas, North Carolina and Tijuana, Mexico. The geographic distribution of our facilities throughout the United States, together with our third party logistics network for the American Woodmark business and beneficial freight arrangement with home centers, enable us to provide a “short supply chain” to our U.S. customers. The ordering patterns of Home Depot and Lowe’s, our two biggest customers, require suppliers to have sufficient manufacturing capacity to meet demand and to serve a large number (frequently hundreds to thousands) of stores. They impose strict logistics and performance criteria on us. The scale and strategic locations of our manufacturing facilities help us to meet these demands of the home center customers, as well as provide a logistics platform that we can leverage for builders and dealers. We distribute our products through distribution centers located in some of our manufacturing facilities and other third party locations to maximize efficiency. Our vertically-integrated production and assembly lines, standardized product construction and investments in automation have allowed us to continuously improve productivity and develop an expertise in wood processing and yield-maximizing technologies. We have standardized our raw material inputs and a number of our production processes, which reduces logistical requirements to manufacture and gives us increased economies of scale in sourcing these inputs. Certain of our inputs are also partially processed by our vendors, which reduces cost. In addition, our production of labor-intensive manufacturing and fabrication processes in our three Tijuana, Mexico facilities have enabled us to keep overall labor costs low while maintaining higher quality, greater speed-to-market and transportation cost advantage over Asian manufacturers.

We provide complete turnkey installation services to our direct builder customers via our network of eight primary service centers that are strategically located throughout the United States in Virginia, Texas, North Carolina, Georgia, Florida, Arizona and California.

We regularly evaluate our organizational productivity and supply chains and assess opportunities to reduce costs and enhance quality. We strive to improve quality, speed and flexibility to meet changing and uncertain market conditions, as well as manage cost inflation, including wages and employee medical costs.

3

Raw Materials and Suppliers

The primary raw materials used in our products include hard maple, oak, cherry and beech lumber and plywood. Additional raw materials include paint, particleboard, medium density fiberboard, high density fiberboard, manufactured components and hardware. We purchase these and other raw materials from more than one source and generally believe them to be readily available. We rely on outside suppliers for some of our key components and do not typically enter into long-term contracts with our suppliers or sourcing partners. We source a portion of our components from third parties in Asia. The distances involved in these arrangements, together with the differences in business practices, shipping and delivery requirements, and laws and regulations add complexity to our supply chain logistics and increase the potential for interruptions in our production scheduling. In addition, prices and availability of these components may be affected by world market conditions and government policies and tariffs.

Competition

We operate in a highly fragmented industry that is composed of several thousand local, regional and national manufacturers. Most of our competitors compete on a local or regional basis, but others, like us, compete on a national basis as well. Our competitors include importers and large consolidated operations as well as relatively small, local cabinet manufacturers. Moreover, companies in other building products industries may compete with us. Competitive factors within the industry include pricing, quality, product availability, service, delivery time and relationships with customers. Our principal means for competition is our breadth and variety of product offerings, expanded service capabilities, geographic reach, competitive price points for our products and affordable quality. We are the second or third largest manufacturer of kitchen, bath and home organization products in the United States based on publicly available information now that one of the top three manufacturers is privately held.

Environmental Matters and Regulatory Matters

Our operations are subject to federal, state and local environmental laws and regulations relating to, among other things, the generation, storage, handling, emission, transportation and discharge of regulated materials into the environment. Permits are required for certain of our operations, and these permits are subject to revocation, modification and renewal by issuing authorities. Governmental authorities have the power to enforce compliance with their regulations, and violations may result in the payment of fines or the entry of injunctions, or both. We may also incur liability for investigation and clean-up of soil or groundwater contamination on or emanating from current or formerly owned and operated properties, or at offsite locations at which regulated materials are located where we are identified as a responsible party. Discovery of currently unknown conditions could require responses that could result in significant costs.

Intellectual Property

We maintain trademarks, copyrights and trade secrets. We sell many of our products under a number of registered and unregistered trademarks, which we believe are widely recognized in our industry. We rely on trade secrets and confidentiality agreements to develop and maintain our competitive position. Monitoring the unauthorized use of our intellectual property is difficult, and the steps we have taken may not prevent unauthorized use of our intellectual property. The disclosure or misappropriation of our intellectual property could harm our ability to protect our rights and our competitive position. If we must litigate to protect our rights, we may incur significant expenses and divert significant attention from our business operations. To date, we have not relied on patents in operating our business.

Seasonality

Our business has been subject to seasonal influences, with higher sales typically realized in our first and fourth fiscal quarters, although sales were down in the fourth quarter of fiscal 2020 and we expect sales to be down in the first quarter of fiscal 2021 due to the novel coronavirus ("COVID-19") pandemic. General economic forces and changes in our customer mix have reduced seasonal fluctuations in revenue over the past few years. The costs of the Company’s products are subject to inflationary pressures and commodity price fluctuations. The Company has generally been able over time to recover the effects of inflation and commodity price fluctuations through sales price increases.

Employees

As of April 30, 2020, we employed approximately 9,900 full-time employees, with approximately 210 unionized employees in Anaheim, California. We believe that our employee relations and relationship with the union representing the employees in Anaheim are good.

4

Our Competitive Strengths

Market Leader with Nationwide Manufacturing and Distribution Network

We believe our company holds the number two or three market position in the United States cabinet market with an estimated 10% market share based on publicly available information now that one of the top three manufacturers is privately held. We are one of a select number of market participants with a national manufacturing and distribution footprint, including 18 manufacturing facilities and eight primary service centers across the United States and Mexico. Our operating footprint provides us an ability to service our builder, dealer and home center customers on a national basis, and we offer a broad set of products to serve our customers across a variety of price points. Our facilities are primarily located in or near major metropolitan markets to facilitate efficient product distribution to our customers. We believe the scale and breadth of our operations differentiate us and result in a competitive advantage providing superior customer service, low-cost distribution and on-time delivery.

Comprehensive Product Offering with Diversified End Markets

We believe that the diversity of our product portfolio across categories, channels and end markets benefits our financial performance, both in periods of growth and cyclicality. Our made-to-order offerings provide products for customers looking for a designer product, which can be used for both new home construction and remodeling applications. The addition of the stock offering allows us to further serve our existing end markets through the addition of a lower price point product that is well-suited for areas of growing demand such as new home construction targeting the first-time homebuyer. We also offer turnkey cabinet solutions for our builder customers which we believe is a unique aspect of our service platform. Our turnkey solution provides in-house design and measurement as well as installation service. We believe the ability to leverage our labor and expertise is a value-added service to our builder customers which has helped strengthen our position in the new home construction market.

Deep Relationships with Leading Retailers

We have built strong and stable relationships with a base of long-standing, customers across home centers, builders and independent dealers and distributors. We have an average relationship length of 20 plus years with our top 10 customers, including long-standing relationships with Home Depot and Lowe’s. We believe our customers value our national manufacturing and distribution footprint, which allows us to meet demanding logistics and performance criteria. We believe our focus on providing exceptional customer service and a quality product at a competitive price have enabled us to establish ourselves as a vendor of choice.

Best-in-Class Manufacturing Capabilities

We operate 18 manufacturing facilities across the United States and Mexico. Our vertically-integrated production and assembly lines, standardized product construction and investments in automation, have allowed us to continuously improve productivity and efficiency. We have standardized our raw material inputs and a number of our production processes, which reduces logistical requirements and provides increased economies of scale in sourcing these inputs. Our labor-intensive manufacturing and fabrication processes in Mexico offer a low cost alternative to Asian manufacturers, while providing a quality product with lower transportation costs.

Experienced Management Team

We have assembled an executive team from leading organizations with a deep base of management experience within industrial manufacturing companies. Our Chairman and Chief Executive Officer, Cary Dunston, joined our team in 2006 and was named Chief Executive Officer in 2015 and elected Chairman in 2017. Mr. Dunston has a broad range of experience in manufacturing and supply chain management including the implementation of continuous improvement programs and lean manufacturing initiatives. Our team has identified and begun to execute on opportunities for operational improvement.

Item 1A. RISK FACTORS

There are a number of risks and uncertainties that may affect the Company’s business, results of operations and financial condition. These risks and uncertainties could cause future results to differ from past performance or expected results, including results described in statements elsewhere in this report that constitute "forward-looking statements" under the Private Securities Litigation Reform Act of 1995. Additional risks and uncertainties not presently known to the Company or currently believed to be immaterial also may adversely impact the Company’s business. Should any risks or uncertainties develop into actual events, these developments could have material adverse effects on the Company’s business, financial condition, and results of operations. These risks and uncertainties, which the Company considers to be most relevant to specific business activities, include, but are not limited to, the following. Additional risks and uncertainties that may affect the Company’s business, results of operations and financial condition

5

are discussed elsewhere in this report, including in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” under the headings “Forward-Looking Statements,” “Seasonality,” and “Outlook for Fiscal 2021” and Item 7A. "Quantitative and Qualitative Disclosures about Market Risk."

The global spread of COVID-19 has significantly impacted our business and is expected to cause further disruptions to our business, financial performance and operating results. The global spread of COVID-19 in recent months has negatively impacted the global and U.S. economy, disrupted global supply chains and created significant volatility and disruption in financial markets. The impact of this pandemic has also created significant uncertainty in the global and U.S. economy and has had, and is expected to continue to have, a material adverse effect on our business, employees, suppliers, and customers. The duration and the magnitude of the impact of the COVID-19 pandemic cannot be precisely estimated at this time, as they are affected by a number of rapidly changing factors, many of which are outside of our control. As a result of the COVID-19 pandemic and potential future pandemic outbreaks, we face significant risks including, but not limited to:

• | Decreases in consumer sentiment, single family housing starts and disposable income and increases in unemployment could reduce demand for our products by our customers in all of our market channels. |

• | Tightening credit standards could negatively impact credit availability to consumers which could have an adverse effect on all of our market channels. |

• | Supply chain and shipping interruptions and constraints, volatility in demand for our products caused by sudden and significant changes in production levels by our suppliers or other restrictions affecting our business could adversely impact our planning and forecasting, our revenues and our operations. |

• | Disruptions in our manufacturing and supply arrangements caused by the loss or disruption of essential manufacturing and supply elements such as raw materials or other product components, transportation, work force, or other manufacturing and distribution capabilities, like the temporary suspension of our Mexican operations in April 2020, could result in our inability to meet our customer needs and achieve cost targets. |

• | Significant changes in the conditions in markets in which we manufacture, sell or distribute our products, including additional or expanded quarantines or "stay at home" orders, governmental or regulatory actions, closures or other restrictions that further limit or close our operating and manufacturing facilities, restrict our employees’ ability to travel or perform necessary business functions, restrict or prevent consumers from having access to our products, or otherwise prevent our suppliers or customers from sufficiently staffing operations, could adversely impact operations necessary for the production, distribution, sale, and support of our products. |

• | Certain of our customers may experience financial difficulties, including bankruptcy or insolvency, as a result of the impact of COVID-19. If any of our customers suffer significant financial difficulties, they may be unable to pay amounts due to us timely or at all. If we are unable to collect our accounts receivable as they come due, there may be a material adverse effect on our financial condition, results of operations and cash flows. |

• | If the Company is unable to continue to operate all of its facilities, our cash flows could be adversely affected, making it difficult to maintain adequate liquidity or meet debt covenants. As a result, the Company may be required to pursue additional sources of financing to meet our financial obligations and fund our operations and obtaining such financing with terms acceptable to the Company is not guaranteed and is largely dependent upon market conditions and other factors. |

• | Disruptions to our operations related to COVID-19 as a result of absenteeism by infected or ill employees, or absenteeism by employees who elect not to come to work due to the illness affecting others at our facilities, or due to quarantines. |

• | The COVID-19 pandemic has led to and could continue to lead to severe disruption and volatility in the United States and global capital markets, which could increase our cost of capital and adversely affect our ability to access the capital markets in the future. In addition, trading prices in the public equity markets, including prices of our common stock, have been highly volatile as a result of the COVID-19 pandemic. |

• | Sustained adverse impacts to the Company, certain suppliers, and customers may also affect the Company’s future valuation of certain assets and therefore may increase the likelihood of an impairment charge, write-off, or reserve associated with such assets, including goodwill, long-lived intangible assets, property and equipment, inventories, accounts receivable, tax assets and other assets. |

The ultimate impact of the COVID-19 pandemic on our business, results of operations, financial condition and cash flows is highly uncertain and cannot be accurately predicted and is dependent on future developments, including the duration of the pandemic and the length of its impact on the global and U.S. economy, as well as any new information that may emerge concerning the COVID-19 pandemic and the actions taken to contain it or mitigate its impact. The continued impact on our business as a result of the COVID-19 pandemic (directly or indirectly) could materially adversely affect our results of operations, financial condition, cash flows, prospects and the trading prices of our securities in the near-term and beyond fiscal 2021.

Because of the concentration of our sales to our two largest customers, the loss of either customer or a significant reduction in orders from either customer could adversely affect our financial results. Home Depot and Lowe’s collectively accounted for approximately 46.5% of total net sales during the fiscal year 2020. We do not typically enter into long-term sales contracts with

6

Home Depot or Lowe’s and our sales usually occur on a “purchase order” basis. Our customers can make significant changes in their purchase volumes and can seek to significantly affect the prices we receive for our products and services and the other terms and conditions on which we do business. They have discontinued, and may in the future choose to discontinue, purchasing some or all of our products with little or no notice. In the past, purchase volumes from our customers, including Home Depot and Lowe’s, have fluctuated substantially, and we expect such fluctuations to occur from time to time in the future. Any reduction in, or termination of, our sales to either Home Depot or Lowe’s could have a material adverse effect on our business, financial condition or results of operations.

In addition, the potential for orders from these large retail customers to increase significantly from time to time requires us to have sufficient manufacturing capacity. These large retailers also impose strict logistics and performance criteria. Failure to comply with these obligations may result in these customers reducing or stopping their purchase of our products.

We could also experience delays or defaults in payment from Home Depot or Lowe’s, which could adversely affect our business, financial condition or results of operations. The loss of a substantial portion of our order volumes or revenue from either Home Depot or Lowe’s for any reason would have a material adverse effect on our business, financial condition or results of operations.

Our business primarily relies on U.S. home improvement, repair and remodel and new home construction activity levels, all of which are impacted by risks associated with fluctuations in the housing market. Downward changes in the general economy, the housing market or other business conditions could adversely affect our results of operations, cash flows and financial condition. Our business primarily relies on home improvement, repair and remodel and new home construction activity levels in the United States. The housing market is sensitive to changes in economic conditions and other factors, such as the level of employment, access to labor, consumer confidence, consumer income, availability of financing and interest rate levels. Adverse changes in any of these conditions generally, or in any of the markets where we operate, including due to the COVID-19 pandemic, could decrease demand and could adversely impact our businesses by: causing consumers to delay or decrease homeownership; making consumers more price conscious resulting in a shift in demand to smaller, less expensive homes; making consumers more reluctant to make investments in their existing homes, including large kitchen and bath repair and remodel projects; or making it more difficult to secure loans for major renovations.

Prolonged economic downturns may adversely impact our sales, earnings and liquidity. Our industry historically has been cyclical in nature and has fluctuated with economic cycles. During economic downturns, our industry could experience longer periods of recession and greater declines than the general economy. We believe that our industry is significantly influenced by economic conditions generally and particularly by housing activity, consumer confidence, the level of personal discretionary spending, demographics and credit availability. These factors may affect not only the ultimate consumer of our products, but also may impact home centers, builders and our other primary customers. As a result, a worsening of economic conditions, including due to the COVID-19 pandemic, could adversely affect our sales and earnings as well as our cash flow and liquidity.

The U.S. cabinetry industry is highly competitive, and market share losses could occur. We operate within the highly competitive U.S. cabinetry industry, which is characterized by competition from a number of other manufacturers. Competition is further intensified during economic downturns. We compete with numerous large national and regional home products companies for, among other things, customers, orders from Home Depot and Lowe’s, raw materials and skilled management and labor resources. Purchase volumes from our main home center customers have fluctuated substantially from time to time in the past, and we expect such fluctuations to occur from time to time in the future.

Some of our competitors may have greater financial, marketing and other resources than we do and, therefore, may be able to adapt to changes in customer preferences more quickly, devote more resources to the marketing and sale of their products, generate greater national brand recognition or adopt more aggressive pricing policies than we can. In addition, some of our competitors may resort to price competition to sustain or gain market share and manufacturing capacity utilization, and we may have to adjust the prices on some of our products to stay competitive, which could reduce our revenues.

We also face competition with respect to some of our products from competitors in countries with lower regulatory, safety, environmental and other costs, such as China, Vietnam and Malaysia. These competitors may also benefit from certain local government subsidies or other incentives that are not available to us.

We may not ultimately succeed in competing with other manufacturers and distributors in our market, which may have a material adverse effect on our business, financial condition or results of operations.

Our failure to develop new products or respond to changing consumer preferences and purchasing practices could have a material adverse effect on our business, financial condition or results of operations. The U.S. cabinetry industry is subject to changing consumer trends, demands and preferences. The uncertainties associated with developing and introducing new products,

7

such as gauging changing consumer preferences and successfully developing, manufacturing, marketing and selling new products, could lead to, among other things, rejection of a new product line, reduced demand and price reductions for our products. If our products do not keep up with consumer trends, demands and preference, we could lose market share, which could have a material adverse effect on our business, financial condition or results of operations.

Changes to consumer shopping habits and potential trends toward “online” purchases could also impact our ability to compete. Further, the volatile and challenging economic environment of recent years has caused shifts in consumer trends, demands, preferences and purchasing practices and changes in the business models and strategies of our customers. Shifts in consumer preferences, which may or may not be long-term, have altered the quantity, type and prices of products demanded by the end-consumer and our customers. If we do not timely and effectively identify and respond to these changing consumer preferences and purchasing practices, our relationships with our customers could be harmed, the demand for our products could be reduced and our market share could be negatively affected.

We may fail to fully realize the anticipated benefits of our growth strategy within the dealer, multi-family and homebuilder channels. Part of our growth strategy depends on expanding our business in the dealer, multi-family and homebuilder channels. We may fail to compete successfully against other companies that are already established providers within the dealer and homebuilder channels. Demand for our products within the homebuilder and dealer channels may not grow, or might even decline. In addition, we may not accurately gauge consumer preferences and successfully develop, manufacture and market our products at a national level. Further, the implementation of our growth strategy may place additional demands on our administrative, operational and financial resources and may divert management’s attention away from our existing business and increase the demands on our financial systems and controls. If our management is unable to effectively manage growth, our business, financial condition or results of operations could be adversely affected. If our growth strategy is not successful then our revenue and earnings may not grow as anticipated or may decline, we may not be profitable, or our reputation and brand may be damaged. In addition, we may change our financial strategy or other components of our overall business strategy if we believe our current strategy is not effective, if our business or markets change, or for other reasons, which may cause fluctuations in our financial results.

Manufacturing expansion to add capacity, manufacturing realignments, and other cost savings programs could result in a decrease in our near-term earnings. We continually review our manufacturing operations. These reviews could result in the expansion of capacity, manufacturing realignments and various cost savings programs, such as our closure of the Humboldt, Tennessee manufacturing plant announced in the first quarter of fiscal 2021. See Note S -- Subsequent Events for further information. Effects of manufacturing expansion, realignments or cost savings programs could result in a decrease in our short-term earnings until the additional capacity is in place, cost reductions are achieved and/or production volumes stabilize. Such manufacturing expansions, realignments and programs involve substantial planning, often require capital investments, and may result in charges for fixed asset impairments or obsolescence and substantial severance costs. We also cannot assure you that we will achieve all of the intended cost savings. Our ability to achieve cost savings and other benefits within expected time frames is subject to many estimates and assumptions. These estimates and assumptions are subject to significant economic, competitive, and other uncertainties, some of which are beyond our control. If these estimates and assumptions are incorrect, if we experience delays, or if other unforeseen events occur, our business, financial condition, and results of operations could be materially and adversely affected. In addition, downturns in the economy could potentially have a larger impact on the Company as a result of any added capacity.

We manufacture our products internationally and are exposed to risks associated with doing business globally. We manufacture our products in the United States and Mexico and sell our products in the United States and Canada. Accordingly, we are subject to risks associated with potential disruption caused by changes in political, monetary, economic and social environments, including civil and political unrest, terrorism, possible expropriation, local labor conditions, changes in laws, regulations and policies of foreign governments and trade disputes with the United States (including tariffs), and compliance with U.S. laws affecting activities of U.S. companies abroad, including tax laws, economic sanctions and enforcement of contract and intellectual property rights.

We are also subject to the Foreign Corrupt Practices Act and other anti-bribery laws. While we have implemented safeguards and policies to discourage these practices by our employees and agents, our existing safeguards and policies to assure compliance and any future improvements may prove to be less than effective and our employees or agents may engage in conduct for which we might be held responsible. If employees violate our policies, we may be subject to regulatory sanctions. Violations of these laws or regulations could result in sanctions including fines, debarment from export privileges and penalties and could have a material adverse effect on our business, financial condition or results of operations.

We may hedge certain foreign currency transactions in the future; however, a change in the value of the currencies may impact our financial statements when translated into U.S. dollars. In addition, fluctuations in currency can adversely impact the cost position in local currency of our products, making it more difficult for us to compete. Our success will depend, in part, on our ability to effectively manage our business through the impact of these potential changes.

8

In addition, we source raw materials and components from Asia where we have recently experienced higher manufacturing costs and longer lead times due to currency fluctuations, higher wage rates, labor shortages and higher raw material costs. Our international operations and sourcing of materials (including from Asia and Mexico) could be harmed by a variety of factors including:

• | introduction of non-native invasive organisms into new environments; |

• | recessionary trends in international markets; |

• | legal and regulatory changes and the burdens and costs of our compliance with a variety of laws, including export controls, import and customs trade restrictions, tariffs and regulations related to the COVID-19 pandemic such as the temporary suspension of our operations in Mexico in April 2020; |

• | increases in transportation costs or transportation delays; |

• | work stoppages and labor strikes; |

• | fluctuations in exchange rates, particularly the value of the U.S. dollar relative to other currencies; and |

• | political unrest, terrorism and economic instability. |

If any of these or other factors were to render the conduct of our business in a particular country undesirable or impractical, our business, financial condition or results of operations could be materially adversely affected.

We may record future goodwill impairment charges or other asset impairment charges which could negatively impact our future results of operations and financial condition. We have recorded significant goodwill as a result of the acquisition of RSI Home Products, Inc. (the “RSI Acquisition”), and goodwill and other acquired intangible assets represent a substantial portion of our assets. We also have long-lived assets consisting of property and equipment and other identifiable intangible assets which we review both on an annual basis as well as when events or circumstances indicate that the carrying amount of an asset may not be recoverable. If a determination is made that a significant impairment in value of goodwill, other intangible assets or long-lived assets has occurred, such determination could require us to impair a substantial portion of our assets. Asset impairments could have a material adverse effect on our financial condition and results of operations. See Note B -- Acquisition of RSI Home Products, Inc. for further details.

Fluctuating raw material and energy costs could have a material adverse effect on our business and results of operations. We purchase various raw materials, including, among others, wood, wood-based and resin products, which are subject to price fluctuations that could materially increase our manufacturing costs. Further, increases in energy costs increase our production costs and also the cost to transport our products, each of which could have a material adverse effect on our business and results of operations. In addition, some of our suppliers have consolidated and other suppliers may do so in the future. Combined with increased demand, such consolidation could increase the price of our supplies and raw materials.

We also may be unwilling or unable to pass on to customers commensurate cost increases. Competitive considerations and customer resistance to price increases may delay or make us unable to adjust selling prices. To the extent we are unable to either re-engineer or otherwise offset increased costs or are unwilling or unable to build price increases into our sales prices, our margins will be negatively affected. Even if we are able to increase our selling prices, sustained price increases for our products may lead to sales declines and loss of market share, particularly if our competitors do not increase their prices. Conversely, when raw materials or energy prices decline, we may receive customer pressure to reduce our sales prices.

These prices are market-based and fluctuate based on factors beyond our control. We do not have long-term fixed supply agreements and do not hedge against price fluctuations. We, therefore, cannot predict our raw materials costs for the coming year.

The inability to obtain raw materials from suppliers in a timely manner would adversely affect our ability to manufacture and market our products. Our ability to offer a wide variety of products depends on our ability to obtain an adequate supply of components from manufacturers and other suppliers, particularly wood-based and resin products. Failure by our suppliers to provide us with quality products on commercially reasonable terms, and to comply with legal requirements for business practices, could have a material adverse effect on our business, financial condition or results of operations. Furthermore, we rely heavily or, in certain cases, exclusively, on outside suppliers for some of our key components. While we do not rely exclusively on any one supplier for any particular raw materials, the loss of a major supplier could increase our costs to obtain raw materials until we obtain an adequate alternative source.

We typically do not enter into long-term contracts with our suppliers or sourcing partners. Instead, most raw materials and sourced goods are obtained on a “purchase order” basis. Although these components are generally obtainable in sufficient quantities from other sources, resourcing them from another supplier could take time. Financial, operating, or other difficulties encountered by our suppliers or sourcing partners or changes in our relationships with them could result in manufacturing or sourcing interruptions, delays and inefficiencies, and prevent us from manufacturing enough products to meet customer demands. As an example, in fiscal 2020, we experienced several of the adverse impacts set forth above related to a particleboard supplier as more fully described

9

in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations - “Particleboard Supply” herein.

Our operations may be adversely affected by information systems interruptions or intrusions. We rely on a number of information technology systems to process, transmit, store and manage information to support our business activities. Increased global cybersecurity vulnerabilities, threats and more sophisticated and targeted attacks pose a risk to our information technology systems. We have established security policies, processes and layers of defense designed to help identify and protect against intentional and unintentional misappropriation or corruption of our systems and information and disruption of our operations. Despite these efforts, systems may be damaged, disrupted, or shut down due to attacks by unauthorized access, malicious software, undetected intrusion, hardware failures, or other events, and in these circumstances our disaster recovery planning may be ineffective or inadequate. These breaches or intrusions could lead to business interruption, exposure of proprietary or confidential information, data corruption, damage to our reputation, exposure to litigation and increased operational costs. Such events could have a material adverse impact on our business, financial condition and results of operation. In addition, we could be adversely affected if any of our significant customers or suppliers experience any similar events that disrupt their business operations or damage their reputation.

Increased compliance costs or liabilities associated with environmental regulations could have a material adverse effect on our business, financial condition or results of operations. Our facilities are subject to numerous environmental laws, regulations and permits, including those governing emissions to air, discharges to water, storage, treatment and disposal of waste, remediation of contaminated sites and protection of worker health and safety. We may not be in complete compliance with these laws, regulations or permits at all times. Our efforts to comply with environmental requirements do not remove the risk that we may incur material liabilities, fines or penalties for, among other things, releases of regulated materials occurring on or emanating from current or formerly owned or operated properties or any associated offsite disposal location, or for contamination discovered at any of our properties from activities conducted by previous occupants. Liability for environmental contamination or a release of hazardous materials may be joint and several, so that we may be held responsible for more than our share of the contamination or other damages, or even for the entire share.

Changes in environmental laws and regulations or the discovery of previously unknown contamination or other liabilities relating to our properties and operations could result in significant environmental liabilities that could impact our business, financial condition or results of operation. In addition, we may incur capital and other costs to comply with increasingly stringent environmental laws and enforcement policies. These laws, including, for example, the regulations relating to formaldehyde emissions promulgated by the California Air Resources Board, require us to rely on compliance by our suppliers of raw materials. Should a supplier fail to comply with such regulations, notify us of non-compliance, or provide us with a product that does not comply, we could be subject to disruption in our business and incur substantial liabilities.

Unauthorized disclosure of confidential information provided to us by customers, employees or third parties could harm our business. We rely on the internet and other electronic methods to transmit confidential information and store confidential information on our networks. If there were a disclosure of confidential information provided by, or concerning, our employees, customers or other third parties, including through inadvertent disclosure, unapproved dissemination, or unauthorized access, our reputation could be harmed and we could be subject to civil or criminal liability and regulatory actions.

Changes in government and industry regulatory standards could have a material adverse effect on our business, financial condition or results of operations. Government regulations pertaining to health and safety and environmental concerns continue to emerge, domestically as well as internationally, including regulations due to the COVID-19 pandemic. These regulations include the Occupational Safety and Health Administration and other worker safety regulations for the protection of employees, as well as regulations for the protection of consumers. It is necessary for us to comply with current requirements (including requirements that do not become effective until a future date), and even more stringent requirements could be imposed on our products or processes. Compliance with these regulations may require us to alter our manufacturing and installation processes and our sourcing. For example, our manufacturing locations enhanced cleaning processes, established health screening procedures, modified work centers and material flows with established social distancing practices in response to the COVID-19 pandemic in accordance with guidelines provided by the U.S. Centers for Disease Control and Prevention, as well as local and state health departments. Such actions could increase our capital expenditures and adversely impact our business, financial condition or results of operations, and our inability to effectively and timely meet such regulations could adversely impact our competitive position.

The loss of certain members of our management may have an adverse effect on our operating results. Our success will depend, in part, on the efforts of our senior management and other key employees. These individuals possess sales, marketing, engineering, manufacturing, financial and administrative skills and know-how that are critical to the operation of our business. If we lose or suffer an extended interruption in the services of one or more of our senior officers or other key employees, our financial condition and results of operations may be negatively affected. Moreover, the pool of qualified individuals may be highly competitive and we may not be able to attract and retain qualified personnel to replace or succeed members of our senior management or other

10

key employees, should the need arise. The loss of the services of any key personnel, or our inability to hire new personnel with the requisite skills, could impair our ability to develop new products or enhance existing products, sell products to our customers or manage our business effectively.

We could continue to pursue growth opportunities through either acquisitions, mergers or internally developed projects, which may be unsuccessful or may adversely affect future financial condition and operating results. We could continue to pursue opportunities for growth through either acquisitions, mergers or internally developed projects as part of our growth strategy. We cannot assure you that we will be successful in integrating an acquired business or that an internally developed project will perform at the levels we anticipate. We may pay for future acquisitions using cash, stock, the assumption of debt, or a combination of these. Future acquisitions could result in dilution to existing shareholders and to earnings per share. In addition, we may fail to identify significant liabilities or risks associated with a given acquisition that could adversely affect our future financial condition and operating results or result in us paying more for the acquired business or assets than they are worth.

Our ability to operate and our growth potential could be materially and adversely affected if we cannot employ, train and retain qualified personnel at a competitive cost. Many of the products that we manufacture and assemble require manual processes in plant environments. We believe that our success depends upon our ability to attract, employ, train and retain qualified personnel with the ability to design, manufacture and assemble these products. In addition, our ability to expand our operations depends in part on our ability to increase our skilled labor force as the housing market continues to recover in the United States. A significant increase in the wages paid by competing employers could result in a reduction of our qualified labor force, increases in the wage rates that we must pay, or both. In addition, we believe that our success depends in part on our ability to quickly and effectively train additional workforce to handle the increased volume and production while minimizing labor inefficiencies and maintaining product quality in a housing market recovery. If either of these events were to occur, our cost structure could increase, our margins could decrease, and any growth potential could be impaired.

Our failure to maintain acceptable quality standards could result in significant unexpected costs. Any failure to maintain acceptable quality standards could require us to recall or redesign such products, or pay substantial damages, any of which would result in significant unexpected costs. We may also have difficulty controlling the quality of products or components sourced from other manufacturers, so we are exposed to risks relating to the quality of such products and to limitations on our recourse against such suppliers. Further, any claim or product recall could result in adverse publicity against us, which could decrease our credibility, harm our reputation, adversely affect our sales, or increase our costs. Defects in our products could also result in decreased orders or sales to our customers, which could have a material adverse effect on our business, financial condition or results of operations.

Future tax law changes or the interpretation of existing tax laws may materially impact our effective income tax rate and the resolution of unrecognized tax benefits. Our businesses are subject to taxation in the United States as well as internationally. Tax legislation may be enacted that could have a material adverse impact on our worldwide income tax provision. Tax authorities in many jurisdictions routinely audit us. Because there are significant uncertainties in the outcome of such audits, the ultimate outcome from any audit could be materially different from amounts reflected in our income tax provisions and accruals. Future settlements of income tax audits may have a material adverse effect on earnings between the period of initial recognition of tax estimates in our financial statements and the point of ultimate tax audit settlement.

Natural disasters could have a material adverse effect on our business, financial condition or results of operations. Many of our facilities are located in regions that are vulnerable to natural disasters and other risks, such as earthquakes, fires, floods, tropical storms, hurricanes and snow and ice, which at times have disrupted the local economy and posed physical risks to our property. In addition, the continued threat of terrorism and heightened security and military action in response to this threat, or any future acts of terrorism, may cause further disruptions to the economies of the United States and other countries. Our redundant, multiple site capacity may not be sufficient in the event of a natural disaster, terrorist act or other catastrophic event. Such disruptions could, among other things, disrupt our manufacturing or distribution facilities and result in delays or cancellations of customer orders for our products, which in turn could have a material adverse effect on our business, financial condition and results of operations. Further, if a natural disaster occurs in a region from which we derive a significant portion of our revenue, end-user customers in that region may delay or forego purchases of our products, which may materially and adversely impact our operating results for a particular period.

Our ability to grow and compete in the future will be adversely affected if adequate capital is not available to us or not available on terms favorable to us. The ability of our business to grow and compete depends on the availability of adequate capital, which in turn depends in large part on our cash flow from operations and the availability of equity and debt financing. We cannot assure you that our cash flow from operations will be sufficient or that we will be able to obtain equity or debt financing on acceptable terms, if at all, to implement our growth strategy. As a result, we cannot assure you that adequate capital will be available to finance our current growth plans, take advantage of business opportunities or respond to competitive pressures, any of which could harm our business.

11

Certain of our customers have been expanding and may continue to expand through consolidation and internal growth, which may increase their buying power, which could materially and adversely affect our sales, results of operations and financial position. Certain of our customers are large companies with significant buying power. In addition, potential further consolidation in the distribution channels could enhance the ability of certain of our customers to seek more favorable terms, including pricing, for the products that they purchase from us. Accordingly, our ability to maintain or raise prices in the future may be limited, including during periods of raw material and other cost increases. If we are forced to reduce prices or to maintain prices during periods of increased costs, or if we lose customers because of pricing or other methods of competition, our sales, operating results and financial position may be materially and adversely affected.

Our level and terms of indebtedness could adversely affect our business and liquidity position. Our consolidated indebtedness level could have important consequences to us, including, among other things, increasing our vulnerability to general economic and industry conditions; requiring a portion of our cash flow used in operations to be dedicated to the payment of principal and interest on our indebtedness, therefore reducing our liquidity and our ability to use our cash flow to fund our operations, capital expenditures and future business opportunities; exposing us to the risk of increased interest rates, and corresponding increased interest expense, because borrowings under our credit facilities are at variable rates of interest; reducing funds available for working capital, capital expenditures, acquisitions and other general corporate purposes, due to the costs and expenses associated with such debt; limiting our ability to obtain additional financing for working capital, capital expenditures, debt service requirements, acquisitions, and general corporate or other purposes; and limiting our ability to adjust to changing marketplace conditions and placing us at a competitive disadvantage compared to our competitors who may have less debt.

If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay capital expenditures, sell assets, seek additional capital, or restructure or refinance our indebtedness. These alternative measures may not be successful and may not permit us to meet our scheduled debt service obligations, which could cause us to default on our debt obligations and impair our liquidity. In the event of a default under any of our indebtedness, the holders of the defaulted debt could elect to declare all the funds borrowed to be due and payable, together with accrued and unpaid interest, which in turn could result in cross-defaults under our other indebtedness. The lenders under our credit facilities could also elect to terminate their commitments thereunder and cease making further loans, and such lenders could institute foreclosure proceedings against their collateral, all of which could adversely affect our financial condition in a material way.

The credit agreement that governs our credit facility and the indenture that governs our senior notes impose significant operating and financial restrictions on us and our subsidiaries, which may prevent us from capitalizing on business opportunities or otherwise negatively impact our business. The credit agreement that governs our credit facility and the indenture that governs our senior notes impose significant operating and financial restrictions on us. These restrictions limit our ability and the ability of our subsidiaries to, among other things, incur additional indebtedness (including guarantee obligations); incur liens; engage in mergers, consolidations and certain other fundamental changes; dispose of assets; make advances, investments and loans; engage in sale and leaseback transactions; engage in certain transactions with affiliates; enter into contractual arrangements that encumber or restrict the ability to (A) (i) pay dividends or make distributions, (ii) pay indebtedness, (iii) make loans or advances or (iv) sell, lease or transfer property, in each case to us and our subsidiaries, or (B) incur liens; pay dividends, distributions and other payments in respect of capital stock or subordinated debt; repurchase or retire capital stock, warrants or options or subordinated debt; and amend the terms of documents governing, or make payments prior to the scheduled maturity of, certain other indebtedness.

As a result of these restrictions, each of which is subject to certain exceptions and qualifications, we will be limited as to how we conduct our business and we may be unable to raise additional debt or equity financing to compete effectively or to take advantage of new business opportunities. The terms of any future indebtedness we may incur could include more restrictive covenants. We cannot assure you that we will be able to maintain compliance with these existing covenants in the future and, if we fail to do so, that we will be able to obtain waivers from the lenders and/or amend the covenants.

Our failure to comply with the restrictive covenants described above as well as other terms of our indebtedness and/or the terms of any future indebtedness from time to time could result in an event of default, which, if not cured or waived, could result in our being required to repay these borrowings before their due date. If we are forced to refinance these borrowings on less favorable terms or cannot refinance these borrowings, our results of operations and financial condition could be adversely affected.

Item 1B. UNRESOLVED STAFF COMMENTS

None.

12

Item 2. PROPERTIES

We own our Corporate Office located in Winchester, Virginia. In addition, we lease eight manufacturing facilities and one manufacturing facility/service center in the United States and Mexico and own nine manufacturing facilities located primarily in the eastern and southern United States. We also lease seven primary service centers, 12 satellite service centers and four additional offices located throughout the United States that support the sale and distribution of products to each market channel. We consider our properties suitable for our business and adequate for our needs and believe that, if necessary, we could find additional and/or replacement facilities to lease without suffering a material adverse effect on our business.

Item 3. LEGAL PROCEEDINGS

The Company is involved in suits and claims in the normal course of business, including, without limitation, product liability and general liability claims and claims pending before the Equal Employment Opportunity Commission. On at least a quarterly basis, the Company consults with its legal counsel to ascertain the reasonable likelihood that such claims may result in a loss. As required by ASC Topic 450, “Contingencies” ("ASC 450"), the Company categorizes the various suits and claims into three categories according to their likelihood for resulting in potential loss: those that are probable, those that are reasonably possible and those that are deemed to be remote. The Company accounts for these loss contingencies in accordance with ASC 450. Where losses are deemed to be probable and estimable, accruals are made. Where losses are deemed to be reasonably possible, a range of loss estimate is determined and considered for disclosure. In determining these loss range estimates, the Company considers known values of similar claims and consults with independent counsel.

The Company believes that the aggregate range of estimated loss stemming from the various suits and asserted and unasserted claims which were deemed to be either probable or reasonably possible was not material as of April 30, 2020.

Item 4. MINE SAFETY DISCLOSURES

None.

EXECUTIVE OFFICERS OF THE REGISTRANT

Executive officers of the Company are elected by the Board of Directors and generally hold office until the next annual election of officers. There are no family relationships between any executive officer and any other officer or director of the Company or any arrangement or understanding between any executive officer and any other person pursuant to which such officer was elected. The executive officers of the Company, as of the date of this Report, are as follows:

Name | Age | Position(s) Held During Past Five Years | |

S. Cary Dunston | 55 | Company Chairman from August 2017 to present; Company President and Chief Executive Officer from August 2015 to present; Company President and Chief Operating Officer from August 2014 to August 2015. | |

M. Scott Culbreth | 49 | Company Senior Vice President and Chief Financial Officer from February 2014 to present. | |

R. Perry Campbell | 55 | Company Senior Vice President, Sales and Commercial Operations from April 2020 to present; Company Senior Vice President of Sales and Marketing from March 2016 to April 2020; Company Senior Vice President and General Manager, New Construction from August 2013 to March 2016. | |

Robert J. Adams, Jr. | 54 | Company Senior Vice President, Value Stream Operations from August 2015 to present; Company Vice President of Value Stream Operations from September 2012 to August 2015; Company Vice President of Manufacturing and Engineering from April 2012 to September 2012. | |

Teresa M. May | 55 | Company Senior Vice President and Chief Marketing Officer from April 2020 to present; Senior Vice President and Chief Marketing Officer of Asurion from May 2018 to April 2020; Vice President of Owens Corning from March 2012 to March 2018. | |

13

PART II

Item 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

American Woodmark Corporation common stock is listed on The NASDAQ Global Select Market under the “AMWD” symbol.

As of June 19, 2020 there were approximately 17,000 total shareholders of the Company's common stock, including 5,000 shareholders of record and 12,000 beneficial owners whose shares are held in "street" name by securities broker-dealers or other nominees. The Company's shareholders also include approximately 50% of the Company's employees who are eligible to participate in the American Woodmark Corporation Retirement Savings Plan. The Company suspended its quarterly dividend during fiscal 2012. The determination as to the payment of future dividends will be made by the Board of Directors (the "Board") from time to time and will depend on the Company's then current financial condition, capital requirements, and results of operations, as well as any other factors then deemed relevant by the Board of Directors, and will be subject to applicable restrictions in the credit agreement governing the Company's credit facility and the indenture governing the Company's senior notes.

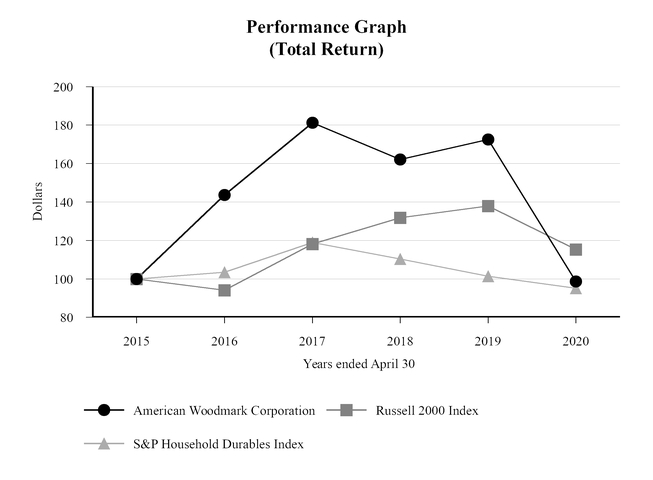

Stock Performance Graph

The performance graph shown below compares the percentage change in the cumulative total shareholder return on our common stock against the cumulative total return of the Russell 2000 Index and Standard & Poor’s Household Durables Index for the period from April 30, 2015 through April 30, 2020. The graph assumes an initial investment of $100 and the reinvestment of dividends. The graph is based on historical data and is not intended to be a forecast or indication of future performance of American Woodmark common stock.

14

2015 | 2016 | 2017 | 2018 | 2019 | 2020 | ||||||||

American Woodmark Corporation | $100.00 | $143.67 | $181.26 | $162.12 | $172.52 | $98.62 | |||||||

Russell 2000 Index | 100.00 | 94.06 | 118.16 | 131.79 | 137.87 | 115.27 | |||||||

S&P Household Durables Index | 100.00 | 103.51 | 118.87 | 110.36 | 101.4 | 95.17 | |||||||

The graph and related information above are not deemed to be "filed" with the Securities and Exchange ("SEC") for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, or incorporated by reference into any future filing made by us with the SEC, except to the extent that we specifically incorporate it by reference into any such filing.

15

Item 6. SELECTED FINANCIAL DATA

FISCAL YEARS ENDED APRIL 30 | |||||||||||||||||||

(Dollars in millions except per share data) | 20201,2,3 | 20191,2,3 | 20181,2 | 20172 | 2016 | ||||||||||||||

FINANCIAL STATEMENT DATA | |||||||||||||||||||

Net sales | $ | 1,650.3 | $ | 1,645.3 | $ | 1,250.3 | $ | 1,030.2 | $ | 947.0 | |||||||||

Operating income | 132.3 | 141.7 | 107.7 | 108.2 | 93.2 | ||||||||||||||

Net income | 74.9 | 83.7 | 63.1 | 71.2 | 58.7 | ||||||||||||||

Earnings per share: | |||||||||||||||||||

Basic | 4.43 | 4.84 | 3.80 | 4.38 | 3.61 | ||||||||||||||

Diluted | 4.42 | 4.83 | 3.77 | 4.34 | 3.57 | ||||||||||||||

Depreciation and amortization expense | 98.5 | 94.4 | 45.0 | 18.7 | 16.5 | ||||||||||||||

Total assets | 1,622.8 | 1,529.9 | 1,645.3 | 501.3 | 466.4 | ||||||||||||||

Long-term debt, less current maturities | 594.9 | 689.2 | 809.9 | 15.3 | 22.1 | ||||||||||||||

Total shareholders' equity | 700.5 | 620.4 | 581.7 | 352.4 | 280.8 | ||||||||||||||

Average shares outstanding | |||||||||||||||||||

Basic | 16.9 | 17.3 | 16.6 | 16.3 | 16.3 | ||||||||||||||

Diluted | 17.0 | 17.3 | 16.7 | 16.4 | 16.4 | ||||||||||||||

PERCENT OF SALES | |||||||||||||||||||

Gross profit | 19.9 | % | 21.1 | % | 20.4 | % | 21.8 | % | 21.1 | % | |||||||||

Selling, general and administrative expenses | 11.9 | 12.4 | 11.8 | 11.3 | 11.2 | ||||||||||||||

Income before income taxes | 6.1 | 6.7 | 7.6 | 10.6 | 9.7 | ||||||||||||||

Net income | 4.5 | 5.1 | 5.1 | 6.9 | 6.2 | ||||||||||||||

RATIO ANALYSIS | |||||||||||||||||||

Current ratio | 2.1 | 2.0 | 2.1 | 3.3 | 3.3 | ||||||||||||||

Inventory turnover4 | 12.0 | 12.2 | 13.5 | 19.6 | 19.8 | ||||||||||||||

Collection period - days5 | 34.1 | 35.3 | 33.6 | 32.5 | 31.2 | ||||||||||||||

Percentage of capital (long-term debt plus equity): | |||||||||||||||||||

Long-term debt, less current maturities | 45.9 | % | 52.6 | % | 58.2 | % | 4.2 | % | 7.4 | % | |||||||||

Equity | 54.1 | 47.4 | 41.8 | 95.8 | 92.6 | ||||||||||||||

Return on equity6 | 11.3 | 13.9 | 13.5 | 22.5 | 23.0 | ||||||||||||||

1 | The fiscal 2020, 2019 and 2018 year results include twelve, twelve and four months, respectively, of RSI activity. See Note B -- Acquisition of RSI Home Products, Inc. for further details. |

2 | The Company incurred corporate business development expenses. During fiscal 2020, these expenses decreased operating income, net income and earnings per share by $0.2 million, $0.2 million and $0.01, respectively. During fiscal 2019, these expenses decreased operating income, net income and earnings per share by $2.1 million, $1.6 million and $0.09, respectively. During fiscal 2018, these expenses decreased operating income, net income and earnings per share by $12.9 million, $8.6 million and $0.51, respectively. During fiscal 2017, these expenses decreased operating income, net income and earnings per share by $2.7 million, $1.8 million and $0.11, respectively. |

3 | The Company announced a reduction in workforce in fiscal 2020 and 2019. During fiscal 2020, the net restructuring charges related to the reduction in workforce did not materially affect the financial statements. During fiscal 2019, the net restructuring charges related to the reduction in workforce decreased operating income, net income and earnings per share by $2.0 million, $1.5 million and $0.09, respectively. |

4 | Based on average beginning and ending inventory. |

5 | Based on the ratio of average monthly customer receivables to average sales per day. |

6 | Based on net income divided by average beginning and ending shareholders equity. |

16

Item 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Results of Operations

The following table sets forth certain income and expense items as a percentage of net sales:

PERCENTAGE OF NET SALES | ||||||||

Fiscal Years Ended April 30 | ||||||||

2020 | 2019 | 2018 | ||||||

Net sales | 100.0 | % | 100.0 | % | 100.0 | % | ||

Cost of sales and distribution | 80.1 | 78.9 | 79.6 | |||||

Gross profit | 19.9 | 21.1 | 20.4 | |||||

Selling and marketing expenses | 5.1 | 5.5 | 6.2 | |||||

General and administrative expenses | 6.8 | 6.9 | 5.6 | |||||

Restructuring charges, net | — | 0.1 | — | |||||

Operating income | 8.0 | 8.6 | 8.6 | |||||

Interest expense/other (income) expense | 1.9 | 1.9 | 1.0 | |||||

Income before income taxes | 6.1 | 6.7 | 7.6 | |||||

Income tax expense | 1.6 | 1.6 | 2.5 | |||||

Net income | 4.5 | 5.1 | 5.1 | |||||

The following discussion should be read in conjunction with the Selected Financial Data and the Consolidated Financial Statements and the related notes contained elsewhere in this report.

Forward-Looking Statements