February 21, 2014

United States Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, D.C. 20549

Attention: Kevin W. Vaughn, Accounting Branch Chief

| Re: | Oppenheimer Holdings Inc. |

Form 10-K for Fiscal Year Ended December 31, 2012

Filed March 6, 2013

Form 10-Q for Quarterly Period Ended September 30, 2013

Filed November 1, 2013

Response dated January 15, 2014

File No. 001-12043

Dear Sirs:

Oppenheimer Holdings Inc. (the “Company”) is in receipt of a comment letter from the United States Securities and Exchange Commission (the “Commission” or the “SEC”) dated February 10, 2014 concerning the Company’s Form 10-K for the fiscal year ended December 31, 2012, filed on March 6, 2013, and its Form 10-Q for the quarterly period ended September 30, 2013, filed on November 1, 2013. The Company is pleased to respond to the Commission and below represents the comments restated along with the Company’s responses.

Form 10-K for Fiscal Year Ended December 31, 2012

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, page 45

Results of Operations, page 55

| 1. | In order to provide additional transparency in the trends experienced, please more clearly quantify the separate impact of the changes in fair value of your auction rate securities (ARS), the changes in fair value of your commitments to purchase ARS, and the incremental recognition of additional commitments in your future filings. |

Response:

In its future filings with the Commission, the Company will provide the following disclosure in the Results of Operations section of Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations:

During the year ended December 31, 2012, the valuation adjustment for ARS increased $3.1 million which resulted in a reduction of principal transactions revenue. The increase in the valuation adjustment was comprised of $2.5 million on ARS owned and $596,000 of ARS purchase commitments.

1

Off-Balance Sheet Arrangements, page 65

| 2. | We note the cross reference in this section to incorporate by reference the information provided in Note 4, Financial Instruments. In future filings please expand this section to more holistically discuss and identify your various ARS-related commitments. Clearly identify how each of these individual commitments has been accounted for, and clearly disclose the extent of the recognized versus unrecognized exposures for each commitment. |

Response:

In its future filings with the Commission, the Company will provide the following disclosure in the Off-Balance Sheet Arrangements section of Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations:

In February 2010, Oppenheimer finalized settlements with each of the New York Attorney General’s office (“NYAG”) and the Massachusetts Securities Division (“MSD” and, together with the NYAG, the “Regulators”) concluding investigations and administrative proceedings by the Regulators concerning Oppenheimer’s marketing and sale of ARS. Pursuant to the settlements with the Regulators, Oppenheimer agreed to extend offers to repurchase ARS from certain of its clients subject to certain terms and conditions more fully described below. In addition to the settlements with the Regulators, Oppenheimer has also reached settlements of and received adverse awards in legal proceedings with various clients where the Company is obligated to purchase ARS. Pursuant to completed Purchase Offers (as defined) under the settlements with Regulators and client related legal settlements and awards to purchase ARS, as of December 31, 2012, the Company purchased and holds approximately $77.0 million in ARS from its clients. In addition, the Company is committed to purchase another $38.3 million in ARS from clients through 2016 under legal settlements.

The Company’s purchases of ARS from its clients holding ARS eligible for repurchase will, subject to the terms and conditions of the settlements with the Regulators, continue on a periodic basis. Pursuant to these terms and conditions, the Company is required to conduct a financial review every six months, until the Company has extended Purchase Offers to all Eligible Investors (as defined), to determine whether it has funds available, after giving effect to the financial and regulatory capital constraints applicable to the Company, to extend additional Purchase Offers. The financial review is based on the Company’s operating results, regulatory net capital, liquidity, and other ARS purchase commitments outstanding under legal settlements and awards (described below). There are no predetermined quantitative thresholds or formulas used for determining the final agreed upon amount for the Purchase Offers. Upon completion of the financial review, the Company first meets with its primary regulator, FINRA, and then with representatives of the NYAG and other regulators to present the results of the review and to finalize the amount of the next Purchase Offer. Various offer scenarios are discussed in terms of which Eligible Investors should receive a Purchase Offer. The primary criteria to date in terms of determining which Eligible Clients should receive a Purchase Offer has been the amount of household account equity each Eligible Client had with the Company in February 2008. Once various Purchase Offer scenarios have been discussed, the regulators, not the Company, make the final determination of which Purchase Offer scenario to implement. The terms of settlements provide that the amount of ARS to be purchased during any period shall not risk placing the Company in violation of regulatory requirements.

2

Outside of the settlements with the Regulators, the Company has also reached various legal settlements with clients and received unfavorable legal awards requiring it to purchase ARS. The terms and conditions including the ARS amounts committed to be purchased under legal settlements are based on the specific facts and circumstances of each legal proceeding. In most instances, the purchase commitments are in increments and extend over a period of time. At December 31, 2012, no ARS purchase commitments related to legal settlements extended past 2016. To the extent the Company receives an unfavorable award, the Company usually must purchase the ARS provided for by the award within 30 days of the rendering of the award. The ultimate amount of ARS to be repurchased by the Company under both the settlements with Regulators and the legal settlements and awards cannot be predicted with any certainty and will be impacted by redemptions by issuers, the Company’s financial and regulatory constraints, and legal and other actions by clients during the relevant period, which also cannot be predicted.

The Company also held $150,000 in ARS in its proprietary trading account as of December 31, 2012 as a result of the failed auctions in February 2008. The ARS positions that the Company owns and is committed to purchase primarily represent Auction Rate Preferred Securities issued by closed-end funds and, to a lesser extent, Municipal Auction Rate Securities which are municipal bonds wrapped by municipal bond insurance and Student Loan Auction Rate Securities which are asset-backed securities backed by student loans.

3

Expressed in thousands of dollars

Auction Rate Securities Owned and Committed to Purchase at December 31, 2012

| Product |

Principal | Valuation Adjustment |

Fair Value | |||||||||

| Auction Rate Securities (“ARS”) Owned(1) |

$ | 76,965 | $ | 5,097 | $ | 71,868 | ||||||

| ARS Commitments to Purchase Pursuant to:(2)(3) |

||||||||||||

| – Settlements with Regulators(4) |

— | — | — | |||||||||

| – Legal Settlements and Awards(5) |

$ | 38,343 | 2,647 | 35,696 | ||||||||

|

|

|

|

|

|

|

|||||||

| Total |

$ | 115,308 | $ | 7,744 | $ | 107,564 | ||||||

|

|

|

|

|

|

|

|||||||

| (1) | Principal amount represents the par value of the ARS and is included in Securities Owned in the consolidated balance sheet at December 31, 2012. The Valuation Adjustment amount is included as a reduction to Securities Owned in the consolidated balance sheet at December 31, 2012. |

| (2) | Principal amount represents the present value of the ARS par value that the Company is committed to purchase at a future date. This principal amount is presented as an off-balance sheet item. The Valuation Adjustment amount is included in Accounts Payable and Other Liabilities on the consolidated balance sheet at December 31, 2012. |

| (3) | Specific ARS to be purchased under ARS Purchase Commitments are unknown until beneficial owner selects the individual ARS to be purchased |

| (4) | Commitments to purchase under settlements with Regulators at December 31, 2012. Clients eligible to participate in future purchases under the settlements with Regulators held at Oppenheimer approximately $212.9 million of ARS at December 31, 2012. |

| (5) | Commitments to purchase under various legal settlements and awards with clients through 2016. |

Per the above table, the Company has recorded a valuation adjustment on its ARS owned and ARS purchase commitments of $7.7 million as of December 31, 2012. The valuation adjustment is comprised of $5.1 million which represents the difference between principal value and fair value of the ARS the Company owns as of December 31, 2012 and $2.6 million which represents the difference between the principal value and the fair value of the ARS the Company is committed to purchase under the settlements with the Regulators and legal settlements and awards. At December 31, 2012, the Company did not have any outstanding ARS purchase commitments related to the settlements with Regulators. However, Eligible Investors for future buybacks under the settlements with Regulators held approximately $212.9 million of ARS as of December 31, 2012. Since the Company was not committed to purchase this amount as of December 31, 2012, there were no valuation adjustments booked to recognize the difference between the principal value and fair value for this remaining amount. Amounts held by Eligible Investors are exclusive of amounts that 1) were owned by Qualified Institutional Buyers (“QIBs”), 2) were transferred to the Company after February 2008, 3) were purchased by clients after February 2008, or 4) were transferred from the Company to other securities firms after February 2008.

4

Consolidated Financial Statements

Note 4. Financial Instruments, page 91

Other, page 92

| 3. | Please address the following regarding your response to our prior comment five where you indicate that current yields at active auctions are used to derive estimated interest payments in the discounted valuation model used to value your ARS for which auctions have failed: |

| • | Please explain to us how the current yields at the auctions referred to in the fourth bullet point of prior comment five compare to your historic returns actually received on your ARS where the auctions have failed. |

Response:

The Company uses the current yields on ARS positions for auctions in which the Company participates. The auctions take place on a 7, 28, and 35 day basis. A modified “Dutch” auction is used to set the short-term interest rate for ARS. The auction mechanism increases the interest rate until the demand for the ARS is equal to or greater than the supply, achieving what is called the “clearing rate.” If the auction fails to clear the market, the interest rate is set to a maximum rate formula per the security prospectus. The maximum rate formula is variable in nature as it is based on a percentage (e.g., 200%) of a short-term index such as LIBOR or U.S. the Treasury yield.

At December 31, 2012, all of the auctions that the Company participated in for auction rate preferred securities failed to clear the market. Thus the interest rates were set to a maximum rate formula. These interest rates were used as a proxy for the current yields on auction rate preferred securities that the Company held on December 31, 2012 and ranged from 0.18% to 0.43% with a weighted average of 0.32%. The current yields on auction rate preferred securities that the Company held at December 31, 2012 ranged from 0.04% to 2.69% with a weighted average of 0.39%. If the Company had used the current yields on auction rate preferred securities that the Company held on December 31, 2012, the valuation adjustment would have decreased by $196,000 from $1,873,000 to $1,677,000. Thus, the Company’s assumptions resulted in a more conservative valuation adjustment at December 31, 2012. Going forward, the Company will use the current yields on auction rate preferred securities that it holds as an input in the discounted valuation model instead of using the current yield on auction rate preferred securities in which the Company participates in the auction. At December 31, 2012, approximately 78% of the ARS owned represented auction rate preferred securities.

At December 31, 2012, approximately 70% of the auctions that the Company participated in for municipal auction rate securities failed to clear the market. Thus the interest rates for the municipal auction rate securities that failed to clear the market were set to a maximum rate formula and the rest at the clearing rate. The Company calculated and used a blended rate of 0.34% from the maximum rates and the clearing rates as a proxy for the current yields on municipal auction rate securities that the Company held on December 31, 2012. The current yields on municipal auction rate securities that the Company held at December 31, 2012 ranged from 0.03% to 1.62% with a weighted average of 0.48%. If the Company had used the current yields on municipal auction rate securities that the Company held on December 31, 2012, the valuation adjustment would have decreased by $30,000 from $251,000 to $221,000. Thus, the Company’s assumptions resulted in a more conservative valuation adjustment at December 31, 2012. Going forward, the Company will use the current yields on municipal auction rate securities that it holds as an input in the discounted valuation model instead of using the current yield on municipal auction rate securities in which the Company participates in the auction. At December 31, 2012, approximately 14% of the ARS owned represented municipal auction rate securities.

5

At December 31, 2012, the Company used a rate of 1.34% for student loan auction rate securities which was derived by adding a predetermined spread to the 1 year Treasury yield. The current yields on student loan auction rate securities that the Company held at December 31, 2012 ranged from 0.04% to 3.21% with a weighted average of 1.70%. If the Company had used the current yields on student loan auction rate securities that the Company held on December 31, 2012, the valuation adjustment would have decreased by $47,000 from $374,000 to $327,000. Thus, the Company’s assumptions resulted in a more conservative valuation adjustment at December 31, 2012. Going forward, the Company will use the current yields on student loan auction rate securities that it holds as an input in the discounted valuation model instead of using the method described above. At December 31, 2012, approximately 6% of the ARS owned represented student loan auction rate securities.

| • | Tell us why you use the implied current yield derived from similar actively traded securities as a proxy for modeling the interest payments in the discounted valuation model to value the ARS in your portfolio. |

Response:

See response to the question above.

| • | Tell us the specificity to which you are able to observe the current yields actually paid on the ARS subject to your purchase commitments and how you consider these yields in your valuation of the derivative liability. |

Response:

For ARS purchase commitments pursuant to the settlements with the Regulators, the Company only knows the actual ARS that it is required to buy back from a client once it has met with its primary regulatory and the NYAG and agreed upon a buyback amount, commenced the ARS buyback offer to clients, and received notice from its clients which ARS they are tendering. As a result, it is not possible to observe the current yields actually paid on the ARS until all of these events have happened which is typically very close to the time that the Company actually purchases the ARS. For ARS purchase commitments pursuant to legal settlements and awards, the criteria for purchasing ARS from clients is based on the nature of the settlement or award which will stipulate a time period and amount for each repurchase. The Company will not know which ARS will be tendered by the client until the stipulated time for repurchase is reached.

As indicated in the response to the first bullet point above, the Company uses the current yields on ARS positions for auctions in which the Company participates in its discounted valuation model to determine a fair value of ARS positions that the Company owns. The Company also uses these current yields by asset class (i.e., auction rate preferred securities, municipal auction rate securities, and student loan auction rate securities) in its discounted valuation model to determine the fair value of ARS purchase commitments.

6

Going forward, the Company will use the current yields on the actual ARS that the Company holds as a proxy for the current yield on ARS purchase commitments pursuant to the settlements with the Regulators and legal settlements and awards as an input in the discounted valuation model instead of using the current yield on ARS in which the Company participates in the auction.

| • | More clearly explain how the valuations produced under this methodology accurately reflect the lack of liquidity in the estimated current exit price for these untraded instruments in your ARS portfolio and in your ARS-related purchase commitments. |

Response:

The Company developed the discounted valuation model to value ARS back in 2010. The valuation premise of this model is that the value of the ARS is fundamentally the present value of expected payments of principal and interest. This present value would be a function, in both amounts and timing, of (i) expected interest payments (current yields); (ii) expected principal payments; and (iii) discount rate. The expected interest payments of an ARS are determined by the current yield mechanics specific to the security. For example, upon the failure of an auction, the current yield is typically determined by a maximum rate formula (as discussed more fully in the response to first bullet in item 4. below). While the expected principal payments are determined by an assumption of the timing of return of principal (referred to as “duration”), the critical factor influencing the value of the expected principal payments of ARS is that the ARS are not credit-risky (the ARS are highly rated due to the presence of credit enhancement or are obligations of highly-rated issuers); therefore, it is the Company’s assumption, which is consistent with our understanding of the assumptions of other market participants, that principal of the ARS will be repaid in full. Repayment of principal and a floating rate of interest (at a rate that is typically a multiple of the rate paid on a comparably-rated floating rate instrument) would be consistent with ARS price estimates that are not at distressed levels. The final valuation factor, the discount rate, is used to discount expected principal and interest to a present value; because there is uncertainty as to the timing of principal repayment and, to a lesser extent, the exact formulation of interest payments, market participants would typically impute a margin over risk-free rates when deriving a discount factor; this margin could comprise amounts that would account for both credit risk and for “illiquidity”; the Company believes that its discount rates appropriately capture the incremental “spread” to compensate for both credit risk and illiquidity (noting that, because there is no directly comparable liquid security from which to infer a yield absent an illiquidity premium, the illiquidity premium is a subjective assumption). The Company has applied this model and related assumptions consistently over a four year period during which it has produced reliable estimates of fair value.

There has been no active secondary market develop for ARS from which to obtain observable pricing. In many instances, the only liquidity in the ARS market for investors comes in the form of issuer redemptions and tender offers, or buybacks made by financial institutions under regulatory and legal settlements. When the ARS auctions failed in February 2008, investors were holding approximately $330 billion of ARS. Through issuer redemptions and tender offers, buybacks, and maturities, the outstanding amount of ARS as of January 31, 2014 was $51 billion, a reduction of approximately 85% from February 2008.

7

| $ Amounts in Billions | ||||||||||||||||

| ARS Type | Feb-08 | Jan-14 | $ Decline | % Decline | ||||||||||||

| ARPS |

80 | 8 | 72 | 90 | % | |||||||||||

| MARS |

150 | 16 | 134 | 89 | % | |||||||||||

| SLARS |

85 | 20 | 65 | 76 | % | |||||||||||

| Other |

15 | 7 | 8 | 53 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

330 | 51 | 279 | 85 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Source: | Second Market |

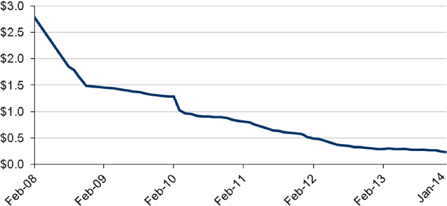

In February 2008, the amount of ARS held by the Company’s clients was approximately $2.8 billion. Through issuer redemptions and tender offers and Company buybacks pursuant to the settlements with Regulators and various legal settlements and awards, the Company’s client holdings have been reduced over 90% as of January 31, 2014.

Total ARS Value of the Company’s client holdings ($ Amounts in Billions)

Notes to Table:

| - | Table includes accounts and ARS positions transferred in after 2/29/08 (approximately $56.1 million at 1/31/14) |

| - | The amount of ARS held by clients eligible for future redemptions totaled $159.3 million at 1/31/14 |

The Company has purchased $138.5 million of ARS from its clients between the time the settlements were reached with the Regulators in the first quarter of 2010 through December 31, 2013. The Company held $91.5 million of ARS at December 31, 2013. As a result, approximately $47 million in issuer redemptions and tender offers transpired during that time period. Included in the $47 million is $30.3 million of ARS that were redeemed at par and $11.5 million that were tendered at an average price of $96.18. Included in the $30.3 million in issuer redemptions at par (or principal value) were $27.7 million of auction rate preferred securities, $1.2 million of municipal auction rate securities, and $1.4 million of student loan auction rate securities. Included in the $11.5 million that was tendered at an average price of $96.18 were $10.3 million of auction rate preferred securities and $1.2 million of municipal auction rate securities.

8

During 2013, the Company sold $4.1 million of student loan auction rate securities at a weighted average price of $91.12 while the discounted valuation model calculated a weighted average fair value of $90.27 for those positions sold.

When the ARS market stopped auctioning in February 2008, the Company also held $5.6 million in auction rate preferred securities in its inventory. The Company holds $150,000 of such securities as of December 31, 2013. This reduction was the result of issuer redemptions at par where the Company was able to recoup the full amount of its investment plus interest.

Per the below table, the Company purchased or held in inventory a total of $51.5 million of ARS that have been redeemed, tendered, or sold at a blended exit price of $98.44 (par value of $100) during the period from February 2008 through December 31, 2013.

| ($ Amounts in Thousands) | Principal Value | Exit Value | Exit Price | |||||||||

| ARS Redeemed at Par |

$ | 30,310 | $ | 30,310 | 100.00 | % | ||||||

| ARS Tender Offers |

$ | 11,475 | $ | 11,036 | 96.18 | % | ||||||

| ARS Held in Inventory Redeemed at Par |

$ | 5,600 | $ | 5,600 | 100.00 | % | ||||||

| Student Loan ARS Sold |

$ | 4,125 | $ | 3,759 | 91.12 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Total |

$ | 51,510 | $ | 50,705 | 98.44 | % | ||||||

|

|

|

|

|

|

|

|||||||

At December 31, 2013 and December 31, 2012, the Company had valuation adjustments on its ARS portfolio (includes both ARS owned and ARS purchase commitments) of $9.1 million and $7.7 million resulting in blended exit prices of $92.45 and $93.28, respectively. At December 31, 2013 and December 31, 2012, the Company’s discounted valuation model calculated a fair value for auction rate preferred securities, municipal auction rate securities, and student loan auction rate securities as follows:

| 12/31/13 | 12/31/12 | |||||||

| Auction Rate Preferred Securities |

$ | 94.93 | $ | 96.89 | ||||

| Municipal Auction Rate Securities |

$ | 90.12 | $ | 94.11 | ||||

| Student Loan Auction Rate Securities |

$ | 85.78 | $ | 91.19 | ||||

In summary, since February 2008, the rate of reduction of outstanding ARS in the marketplace (85%) and held by the Company’s clients (90%) demonstrates that there are exit strategies available for holders of ARS through issuer redemptions, tender offers, and buybacks by financial institutions. Specifically, the Company has experienced a substantial reduction in ARS that it has purchased from clients or held in its own inventory through issuer redemptions, tender offers, and sales in the secondary market. The exit prices received in those transactions (i.e., $98.44) compared to the fair values produced by the discounted valuation model at each of the last year end periods (see above table) reflects that the maximum spread used in the Company’s model as a risk premium is sufficient to account for both credit risk and illiquidity in the ARS market. Therefore, valuations produced under this methodology accurately reflect the lack of liquidity in the estimated current exit price for these untraded instruments in the Company’s ARS portfolio and in its ARS-related purchase commitments.

9

| 4. | We note your response to the fourth bullet of our prior comment 5 where you indicate that the duration of auction rate preferred securities is perpetual and municipal ARS have durations of 10 to 40 years. We also note the duration assumptions provided in your response to our prior comment eight of 5, 5.5, and 8 years for various products. |

| • | Tell us how you estimated durations for the ARS in your portfolio for valuation purposes. |

Determining an estimate of the ARS duration requires the most judgment of the assumptions used to estimate a fair value for the Company’s ARS portfolio as many variables need to be considered. The expected duration of an ARS is a projection of the period of time that an ARS will be outstanding (i.e., timing of principal repayment) and is based on factors such as the probability of issuer redemption, potential tender offers, anticipated liquidity in the primary market (i.e., auctions) or secondary markets, and interest rates projections. Perhaps the most significant determinant of duration revolves around expectations of future short-term interest rates. A modified “Dutch” auction is used to set the short-term interest rate for ARS. The auction mechanism increases the interest rate until the demand for the ARS is equal to or greater than the supply, achieving what is called the “clearing rate.” If the auction fails to clear the market, the interest rate is set to a maximum rate formula per the security prospectus. The maximum rate formula is variable in nature as it is based on a percentage (e.g., 200%) of a short-term index such as LIBOR or U.S. Treasury yield. As short-term interest rates rise, the maximum rate will also increase. The Company estimates that at some level of increases in short-term interest rates, ARS issuers will have a strong economic incentive to refinance the securities through redemptions.

As indicated in the fourth bullet to the response to item 3. above, when the ARS auctions failed in February 2008, investors were holding approximately $330 billion of ARS. Through issuer redemptions and tender offers, buybacks, and maturities, the outstanding amount of ARS as of January 31, 2014 was $51 billion, a reduction of approximately 85% from February 2008.

| $ Amounts in Billions | ||||||||||||||||

| ARS Type | Feb-08 | Jan-14 | $ Decline | % Decline | ||||||||||||

| ARPS |

80 | 8 | 72 | 90 | % | |||||||||||

| MARS |

150 | 16 | 134 | 89 | % | |||||||||||

| SLARS |

85 | 20 | 65 | 76 | % | |||||||||||

| Other |

15 | 7 | 8 | 53 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

330 | 51 | 279 | 85 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Source: | Second Market |

In February 2008, the amount of ARS held by the Company’s clients was approximately $2.8 billion. Through issuer redemptions and tender offers and buybacks pursuant to the settlements with Regulators and various legal settlements and awards, the Company’s client holdings have been reduced over 90% as of January 31, 2014.

10

Total ARS Value of the Company’s client holdings ($ Amounts in Billions)

Notes to Table:

| - | Table includes accounts and ARS positions transferred in after 2/29/08 (approximately $56.1 million at 1/31/14) |

| - | The amount of ARS held by clients eligible for future redemptions total $159.3 million at 1/31/14 |

At the end of December 2010, the first year the Company used the discounted valuation methodology, the durations used were 3.5, 4, and 7 for auction rate preferred securities, municipal auction rate securities, and student loan auction rate securities, respectively. At December 31, 2013, 90% of the ARS held in clients’ portfolios and 85% of the ARS in the marketplace as a whole no longer exist. Specifically, the Company’s duration assumption for auction rate preferred securities was 3.5 years at December 31, 2010. A little over three years later, 90% of that population of ARS has been redeemed. The Company’s duration assumption for municipal auction rate securities was 3.5 years and a little over three years later 89% of that population of ARS has been redeemed, tendered, or matured. The Company’s longest duration assumption was 7 years at December 31, 2010 for student loan auction rate securities and a little over three years later 76% of that population has been redeemed, tendered, or matured.

Based on the reduction of ARS in the overall market and in clients’ portfolios as well as expectations of future short-term interest rates, the Company believes that 5, 5.5, and 8 are reasonable estimates of duration for auction rate preferred securities, municipal auction rate securities, and student loan auction rate securities, respectively, at December 31, 2012. Furthermore, the Company’s understanding of methodologies used by other market participants is that an assumption related to the expected repayment of the principal is used; the Company’s understanding is that some market participants assume a similar expected duration.

| • | Tell us how you are adjusting the implied current yield on ARS that are actively traded to reflect the estimated duration specific to your own ARS. |

11

Response:

There are no adjustments made to the implied current yield used by the Company in the discounted valuation model to reflect the estimated duration specific to ARS that the Company owns. As indicated in the response to the first and third bullets to item 3. above, going forward the Company will use the current yields on the actual ARS that the Company holds as an input into the discounted valuation model in order to determine the fair value of the ARS that the Company holds and as a proxy for the current yield on ARS purchase commitments pursuant to the settlements with the Regulators and legal settlements and awards instead of using the current yield on ARS in which the Company participates in the auction.

| • | More clearly disclose in your future filings how you translate the estimated duration for the ARS in your portfolio to the ARS to which you are committed to purchase. |

Response:

In future filings the Company will describe the challenges associated with estimating the ARS that it will be required to repurchase under the settlements with Regulators and legal settlements and awards as described above in the response to the third bullet in item 3. It will further explain that, due to these challenges, the Company utilizes the duration of ARS that it holds as a proxy for the duration of the ARS that it will be committed to repurchase in the future. It will also explain that the present value of the future principal value of ARS purchase commitments under legal settlements and awards is used in the discounted valuation model to reflect the time value of money over the period of time that the commitments are outstanding.

| 5. | Please revise your future filings to address the following regarding your response to our prior comment six regarding the basis for which you are required to repurchase ARS under your settlement obligations with the New York Attorney General: |

| • | Please explain to us in further detail the criteria for, scope of, and your discretion in extending ARS purchase offers on the ARS subject to your legal and contractual settlement obligations. |

Response:

See proposed additional disclosure regarding the criteria for, scope of, and discretion in extending ARS purchase offers related to settlements with Regulators and legal settlements which is part of the response to item 2. above.

| • | Clarify the extent to which the criteria for repurchase are based on the credit quality of ARS held by investors or if all ARS issued within a specific period of time are required to be repurchased. |

Response:

The criteria for purchasing ARS under the settlements with the Regulators are based on those settlements. Upon completion of its financial review, the Company first meets with its primary regulator, FINRA, and then with representatives of the NYAG and other regulators to present the results of the financial review and to finalize the amount of the next Purchase Offer (as defined). Various offer scenarios are discussed in terms of which Eligible Clients (as defined) should receive a Purchase Offer. The primary criteria to date in terms of determining which Eligible Clients should receive a Purchase Offer has been the amount of household account equity each Eligible Client had with the Company on February 2008. The credit quality of the ARS held by investors has not been criteria utilized to date to determine any Purchase Offer scenario and there is no required time in which all ARS held by Eligible Clients must be repurchased. Once various Purchase Offer scenarios have been discussed, the regulators, not the Company, make the final determination of which Purchase Offer scenario to implement.

12

The criteria for purchasing ARS from clients under legal settlements is based on the nature of the settlement but in all cases to date there has been a date and amount to be repurchased from the settling client. On any such date, the client chooses the ARS to be repurchased from such ARS that are still held by the client.

| • | Revise to clearly identify the terms of your settlement with the New York Attorney General as well as the language from the applicable accounting guidance that are integral to your conclusion that it is not appropriate to record the overall settlement obligation or exposure. |

Response:

See proposed additional disclosure regarding the terms of the settlement with the NYAG which is part of the response to item 2. above.

A loss contingency, as defined in ASC 450 Loss Contingencies, exists for potential client purchases under the settlements with Regulators for the incurrence of a liability resulting from the determination of fair value on any ARS purchase commitments made in the future. Due to the low interest rate environment and the amount that remains outstanding (i.e., $212.9 million at December 31, 2012) under these settlements, it is reasonably possible that some ARS purchase commitments will need to be extended to clients holding ARS that are eligible for future purchases prior to redemptions (or tender offers) by issuers of the full amount that remains outstanding under the settlement with Regulators. However, based on the information available to the Company at each reporting period, no liability has been incurred for outstanding ARS held by Eligible Investors (as defined) that have not yet been committed to be repurchased by the Company. The amount of any potential loss that would result from issuing an ARS purchase commitment to Eligible Investors under the settlements with Regulators and the resulting valuation adjustment to reflect the difference between principal value and fair value cannot be reasonably estimated. The amount of any potential loss cannot be estimated primarily for the following three reasons. First, under the terms of the settlements with the Regulators as described more fully above in the response to item 2. above, the Company is not committed to make any ARS purchase commitments without first meeting with its primary regulator and then the NYAG and other regulators. The financial review that is conducted at that meeting will determine what dollar amount, if any, that the Company will be required to purchase during the next Purchase Offer. There are some uncertainties associated with this financial review. The Company’s operating results, regulatory net capital, and liquidity need to be sufficient to warrant additional buybacks. If the Company has sufficient resources available, then the amount will be determined based on the financial review. As indicated above in the response to item 2. above, there are no predetermined quantitative thresholds or formulas used for determining the final agreed upon amount for the buyback offer. Thus it is not possible to determine the buyback

13

amount that may result from the financial review. The Company’s primary regulator, FINRA, also needs to approve any buyback amount after making the determination that the additional purchases will not cause any violations of regulatory requirements by the Company. Any amounts that result from the financial review and are approved by FINRA will then be discussed with and agreed to by the NYAG. Secondly, there are uncertainties surrounding the amount, if any, that will be required to be bought back at each six month buyback interval. As discussed in the response to item 3. above, ARS issuers may announce redemptions or tender offers for outstanding ARS prior to the required buyback deadline. In addition, a secondary market could develop which would enable holders of ARS to liquidate their positions. ARS issuers could also be forced by regulators to redeem outstanding ARS. Also, the Company’s clients holding ARS may decide not to tender their ARS holdings. Thirdly, the economic environment for each subsequent six-month buyback is unpredictable. As discussed in the response to item 4. above, at some level of increases in short-term interest rates, ARS issuers will have an economic incentive to refinance the securities through redemptions. There may be other factors driving a refinance decision by ARS issuers. For example, auction rate preferred securities that are issued by closed end funds are required, under the Investment Company Act of 1940, to maintain an asset coverage ratio of 200%. Should the asset coverage ratio drop below this level, the fund will not be able to pay cash dividends or make distributions to common shareholders until such level is restored. Maintenance of this asset coverage ratio could impact decisions to redeem outstanding ARS.

Due to the nature of the loss contingency associated with the potential buybacks of ARS under the settlements with Regulators, any potential losses will be unrealized for the difference in the principal value versus the fair value. As pointed out above, a substantial amount of ARS have been redeemed at par and thus any unrealized loss would be reversed for the full amount upon an issuer redemption.

Given what is described above, the loss contingency associated with the potential buybacks of ARS under the settlements with Regulators does not meet the criteria for accruing a charge to income under ASC 450-20-25. Based on the current interest rate environment and the amount of ARS outstanding under the settlement with Regulators, it is reasonably possible that a loss may have been incurred. However, due to the many unknowns described above, the Company is unable to determine an estimated loss or a range of estimated loss.

| • | To the extent that you are able to support your conclusion, please revise your Note 13, Commitments and contingencies, in future filings to clearly quantify the maximum outstanding exposure of this settlement. |

Response:

In its future filings, the Company will add a disclosure to Note 13, Commitments and Contingencies, which quantifies the remaining principal value of ARS outstanding under the settlements with the Regulators noting that, once additional commitments are made in the future, the Company will record an additional valuation adjustment for the difference between the principal value and the fair value. The Company will also add disclosure indicating that it is unable to estimate potential losses or a range of estimated potential losses associated with future additional purchases and the reasons it cannot make such estimates as described in the previous bullet point to this item.

14

| 6. | Please address the following regarding your response to our prior comment eight where you have provided your proposed disclosures for quantitative information about Level 3 fair value measurements for ARS Owned and ARS Commitments to Purchase: |

| • | Clarify why your internal discounted cash flow models for auction rate preferred securities and municipal ARS yield significantly smaller discounts of 3.1% and 11.5%, respectively, compared to discount from par of the observable trade in an inactive market as depicted in this table of 24.2%. Provide a comparison of the credit quality of these securities, and identify the features that resulted in such a disparity in valuation. |

Response:

As discussed below in the third bullet to this item, the revised average discount rates are 5.9% and 26.7% for municipal auction rate securities owned valued using the Company’s internal discounted valuation model and using prices obtained from secondary market trading activity, respectively. The Company’s municipal auction rate securities valued using secondary market trading activity include two positions: $6 million of the New Jersey State Turnpike Authority bonds valued at $75.80 at December 31, 2012 and $625,000 of various Jefferson County, Alabama Sewer Revenue bonds valued at an average price of $50.00 at December 31, 2012. The New Jersey State Turnpike Authority bonds were trading in the secondary market at $85.50 at December 31, 2013. As noted in the Company’s response on January 15, 2014 to the SEC’s comment letter dated December 31, 2013, Jefferson County, Alabama filed for bankruptcy in November 2011. In December 2013, Jefferson County emerged from bankruptcy. As part of a Chapter 9 bankruptcy restructuring, the Company voted to release certain claims against Jefferson County, Alabama in exchange for a price of $80.00 on the Jefferson County, Alabama Sewer Revenue bonds. Accordingly, in December 2013, the Company exchanged the $750,000 in principal value of Jefferson County Alabama Sewer Revenue bonds for $600,000 in cash (or $80.00 per $100.00 par value).

At December 31, 2012, Moody’s rated the New Jersey State Turnpike Authority bonds at A3 (Upper Medium Grade – Strong). At December 31, 2012, Moody’s rated $475,000 of the Jefferson County Alabama Sewer Revenue bonds at Caa3 (Poor Quality – May Default) and $150,000 at Aa3 (High Quality – Very Strong). At December 31, 2012, the Company held municipal auction rate securities with a value of $2.25 million that were rated Aa3 or better (High Quality – Very Strong), $310,000 that were rated A3 or better (Upper Medium Grade – Strong), $850,000 that were rated Baa3 or better (Medium Grade) by Moody’s as well as $855,000 that was not rated by Moody’s.

| • | More clearly explain the extent to which the length of time you intend to hold your ARS has impacted your measurement of their fair value and how that would reconcile with the guidance of ASC 820-10 which requires your estimate of fair value to reflect the price to sell your ARS in an orderly transaction between willing market participants at the measurement date under current market conditions. |

15

Response:

The length of time the Company intends to hold ARS it owns is not determinative of the fair value measurement of ARS. ASC 820-10 Fair Value Measurement defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date under current market conditions (or exit price). The ASC Master Glossary defines an orderly transaction as “A transaction that assumes exposure to the market for a period before the measurement date to allow for marketing activities that are usual and customary for transactions involving such assets or liabilities; it is not a forced transaction (for example, a forced liquidation or distress sale).” The concept of an orderly transaction excludes a distressed sale or a forced liquidation as an input in the determination of fair value. Since the ARS market ceased functioning in February 2008, a secondary market has not developed for most ARS positions. For ARS positions where the Company can obtain pricing in the secondary trading market, it will assess those trades for reasonableness and use that price to value its holdings. For the remaining ARS positions, the Company’s discounted valuation model excludes distressed sales or forced liquidation from its determination of fair value. Instead, the Company considers the characteristics of a market participant to which it would hypothetically sell the asset if it were able to do so and identifies the assumptions that those market participants would consider when pricing the asset. It is those assumptions that are used in the Quantification Information about Level 3 Fair Value Measurements at December 31, 2012 table as presented in the response to the next bullet point.

From time-to-time, the Company calibrates the results of its fair value measurements. The results of which are presented in the response to the third bullet point under item 3. above. The Company believes that the results of these calibration efforts is supportive of its fair value measurement methods and provides a fair value measurement that is reflective of the price to sell its ARS holdings in an orderly transaction between willing market participants at each measurement date under existing current market conditions.

| • | Please tell us why the municipal ARS owned and measured at fair value using the discounted cash flow model results in an average discount of 11.5% whereas the average discount is only 5.9% for municipal ARS purchase commitments. As part of your response, provide a comparison of the updated credit quality of these securities, and identify the features which resulted in such a disparity in valuation. |

Response:

The table provided in the Company’s prior response to item 8. included positions valued using secondary market trading activity in the average discount calculation of 11.5% for municipal auction rate securities owned. The below table has been revised and now reflects an average discount of 5.9% for both ARS owned and ARS purchase commitments for municipal auction rate securities owned. The Quantitative Information about Level 3 Fair Value Measurements at December 31, 2012 in Note 4. “Financial instruments” in the Form 10-K for the Fiscal Year Ended December 31, 2012 will be revised in future filings to include the following table:

16

Expressed in thousands of dollars

Quantitative Information about Level 3 Fair Value Measurements at December 31, 2012

| Product |

Principal | Valuation Adjustment |

Fair Value |

Valuation Technique |

Unobservable Input |

Range | Weighted Average | |||||||||||||

| Auction Rate Securities (“ARS”) Owned(1) |

|

|||||||||||||||||||

| Auction Rate Preferred Securities |

$ | 60,250 | $ | 1,873 | $ | 58,377 | Discounted Cash Flow | Discount Rate | 0.80% to 1.09% | 0.96% | ||||||||||

| Duration | 5 Years | 5 Years | ||||||||||||||||||

| Current Yield(2) | 0.18% to 0.43% | 0.32% | ||||||||||||||||||

| Municipal Auction Rate Securities |

4,265 | 251 | 4,014 | Discounted Cash Flow | Discount Rate | 1.47% | 1.47% | |||||||||||||

| Duration | 5.5 Years | 5.5 Years | ||||||||||||||||||

| Current Yield(2) | 0.34% | 0.34% | ||||||||||||||||||

| 6,600 | 1,759 | 4,841 | Secondary Market Trading Activity | Observable trades in inactive market for in-portfolio securities | 50.0% to 75.8% of par |

73.4% of par | ||||||||||||||

| Student Loan Auction Rate Securities |

4,250 | 374 | 3,876 | Discounted Cash Flow | Discount Rate | 2.57% | 2.57% | |||||||||||||

| Duration | 8 Years | 8 Years | ||||||||||||||||||

| Current Yield(2) | 1.34% | 1.34% | ||||||||||||||||||

| Other(4) |

1,600 | 840 | 760 | Secondary Market Trading Activity | Observable trades in inactive market for in-portfolio securities | 47.5% of par | 47.5% of par | |||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| 76,965 | 5,097 | 71,868 | ||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| ARS Commitments to Purchase(3) |

||||||||||||||||||||

| Auction Rate Preferred Securities |

$ | 17,307 | $ | 526 | $ | 16,781 | Discounted Cash Flow | Discount Rate | 0.80% to 1.09% | 0.96% | ||||||||||

| Duration | 5 Years | 5 Years | ||||||||||||||||||

| Current Yield(2) | 0.18% to 0.43% | 0.32% | ||||||||||||||||||

| Municipal Auction Rate Securities |

19,144 | 1,127 | 18,017 | Discounted Cash Flow | Discount Rate | 1.47% | 1.47% | |||||||||||||

| Duration | 5.5 Years | 5.5 Years | ||||||||||||||||||

| Current Yield(2) | 0.34% | 0.34% | ||||||||||||||||||

| Other(4) |

1,892 | 994 | 898 | Secondary Market Trading Activity | Observable trades in inactive market for in-portfolio securities | 47.5% of par | 47.5% of par | |||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| 38,343 | 2,647 | 35,696 | ||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Total |

$ | 115,308 | $ | 7,744 | $ | 107,564 | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| (1) | Principal amount represents the par value of the ARS and is included in Securities Owned in the consolidated balance sheet at December 31, 2012. The Valuation Adjustment amount is included as a reduction to Securities Owned in the consolidated balance sheet at December 31, 2012. |

| (2) | Based on current auctions in comparable securities that have not failed. |

| (3) | Principal amount represents the present value of the ARS par value that the Company is committed to purchase at a future date. This principal amount is presented as an off-balance sheet item. The Valuation Adjustment amount is included in Accounts Payable and Other Liabilities on the consolidated balance sheet at December 31, 2012. |

| (4) | Represents ARS issued under credit linked obligation structure that the Company has purchased and is committed to purchase as a result of a legal settlement. |

Fair Value of Derivative Instruments, page 98

| 7. | Please revise your proposed sensitivity disclosure responding to our prior comment 15 to address situations where the ARS ultimately repurchased under your purchase commitments are of higher or lower credit quality than your ARS owned. |

17

Response:

As described to the response to the second bullet to item 5. above, the credit quality of the ARS held by investors has not been criteria utilized to date under the settlements with the Regulators to determine any Purchase Offer scenario and there is no required time in which all ARS held by Eligible Clients must be repurchased. Once various Purchase Offer scenarios have been discussed, the regulators, not the Company, make the final determination of which Purchase Offer scenario to implement. The criteria for purchasing ARS from clients under legal settlements and awards is based on the nature of the settlement but in all cases to date there has been a date and amount to be repurchased from the settling client. On any such date, the client chooses the ARS to be repurchased from such ARS that are still held by the client. Due to the nature of these settlements and uncertainties around what the credit environment might look like overall or for a specific credit when the Company commits to repurchase ARS, it is not possible to determine how that might impact the proposed ARS sensitivity disclosure given the number of variables and the uncertainty as to the population of eligible ARS to be repurchased.

Note 13. Commitments and Contingencies, page 120

| 8. | Revise your future filings to address the following regarding your various ARS-related commitments and disclosures: |

| • | Revise this footnote to more clearly differentiate between your various ARS-related commitments, presenting the amounts recorded separately from the amounts yet to be recognized for each individual commitment. Clearly identify how you are accounting for each commitment as well as the remaining uncertainties and exposures surrounding each individual commitment. |

Response:

The Company will revise its future filings to more clearly differentiate its ARS purchase commitments between those that are a result of settlements with Regulators and those resulting from legal settlements and awards by including the table in the response to item 2. above. in its Note 13. Commitments and Contingencies.

As discussed in the response to the fourth bullet in item 5. above, in its future filings, the Company will add a disclosure to Note 13, Commitments and Contingencies, that quantifies the remaining principal value of ARS outstanding under the settlements with the Regulators noting that, once additional commitments are made in the future, the Company will record an additional valuation adjustment for the difference between the principal value and the fair value. The Company will also add disclosure indicating that it is unable to estimate potential losses or a range of estimated potential losses associated with future additional purchases and the reasons it cannot make such estimates.

| • | Revise your disclosures throughout your filing to better correlate with this stratification. Such disclosures would specifically include, but are not limited to, your Risk Factor on page 18, Results of Operations on page 55, Liquidity and Capital Resources on page 61, Off-Balance Sheet Arrangements on page 65, Contractual and Contingent Obligations on page 65, and Quantitative Information about Level 3 Fair Value Measurements at December 31, 2012 on page 93. |

18

Response:

For clarity and consistency purposes, in future filings the Company will provide a reference in each of the sections listed above to the new disclosure and table in the Off-Balance Sheet Arrangements section of Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations with the intent that this new disclosure will provide sufficient background on the ARS settlements with Regulators and legal settlements and awards and stratification of ARS owned and ARS purchase commitments along with any remaining amounts to be repurchased at future dates and any remaining potential exposures.

*****

The Company acknowledges that it is responsible for the adequacy and accuracy of the disclosure in its filings with the Commission; staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filings; and the Company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

Should you have further questions or comments, do not hesitate to contact the undersigned.

Yours truly,

Oppenheimer Holdings Inc.

Jeffrey J. Alfano,

Chief Financial Officer

19