00007899332020FYfalseP3YP3YP5Y1111P10YP7Yus-gaap:PropertyPlantAndEquipmentAndFinanceLeaseRightOfUseAssetAfterAccumulatedDepreciationAndAmortizationus-gaap:PropertyPlantAndEquipmentAndFinanceLeaseRightOfUseAssetAfterAccumulatedDepreciationAndAmortizationus-gaap:OtherLiabilitiesCurrentus-gaap:OtherLiabilitiesCurrentus-gaap:LongTermDebtAndCapitalLeaseObligationsCurrentus-gaap:LongTermDebtAndCapitalLeaseObligationsCurrentus-gaap:LongTermDebtAndCapitalLeaseObligationsus-gaap:LongTermDebtAndCapitalLeaseObligations00007899332020-01-012020-12-31iso4217:USD00007899332020-06-30xbrli:shares0000789933us-gaap:CommonClassAMember2021-02-190000789933us-gaap:CommonClassBMember2021-02-1900007899332019-01-012019-12-31iso4217:USDxbrli:shares00007899332020-12-3100007899332019-12-310000789933us-gaap:CommonClassAMember2020-12-310000789933us-gaap:CommonClassAMember2019-12-310000789933us-gaap:CommonClassBMember2020-12-310000789933us-gaap:CommonClassBMember2019-12-31xbrli:pure00007899332018-12-310000789933us-gaap:CommonClassAMemberus-gaap:CommonStockMember2018-12-310000789933us-gaap:CommonClassBMemberus-gaap:CommonStockMember2018-12-310000789933us-gaap:AdditionalPaidInCapitalMember2018-12-310000789933us-gaap:RetainedEarningsMember2018-12-310000789933us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2018-12-310000789933us-gaap:CommonClassAMemberus-gaap:CommonStockMember2019-01-012019-12-310000789933us-gaap:AdditionalPaidInCapitalMember2019-01-012019-12-310000789933us-gaap:RetainedEarningsMember2019-01-012019-12-310000789933us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2019-01-012019-12-310000789933us-gaap:CommonClassAMemberus-gaap:CommonStockMember2019-12-310000789933us-gaap:CommonClassBMemberus-gaap:CommonStockMember2019-12-310000789933us-gaap:AdditionalPaidInCapitalMember2019-12-310000789933us-gaap:RetainedEarningsMember2019-12-310000789933us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2019-12-310000789933us-gaap:CommonClassAMemberus-gaap:CommonStockMember2020-01-012020-12-310000789933us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310000789933us-gaap:CommonClassBMemberus-gaap:CommonStockMember2020-01-012020-12-310000789933us-gaap:RetainedEarningsMember2020-01-012020-12-310000789933us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2020-01-012020-12-310000789933us-gaap:CommonClassAMemberus-gaap:CommonStockMember2020-12-310000789933us-gaap:CommonClassBMemberus-gaap:CommonStockMember2020-12-310000789933us-gaap:AdditionalPaidInCapitalMember2020-12-310000789933us-gaap:RetainedEarningsMember2020-12-310000789933us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2020-12-31nacco:segmentutr:T0000789933nacco:TheSabineMiningCompanyMembernacco:CoalMiningMember2020-01-012020-12-310000789933nacco:TheSabineMiningCompanyMembernacco:CoalMiningMember2019-01-012019-12-310000789933nacco:TheSabineMiningCompanyMembernacco:CoalMiningMembersrt:MinimumMember2020-01-012020-12-310000789933nacco:TheSabineMiningCompanyMembernacco:CoalMiningMembersrt:MaximumMember2020-01-012020-12-310000789933nacco:CoalMiningMembernacco:CaddoCreekResourcesCompanyLLCMember2020-01-012020-12-310000789933nacco:CoalMiningMembernacco:CaddoCreekResourcesCompanyLLCMember2019-01-012019-12-310000789933nacco:CaminoRealFuelsLLCMembernacco:CoalMiningMember2020-01-012020-12-310000789933nacco:CaminoRealFuelsLLCMembernacco:CoalMiningMember2019-01-012019-12-310000789933nacco:TheFalkirkMiningCompanyMembernacco:CoalMiningMemberus-gaap:LongTermContractWithCustomerMember2020-01-012020-12-310000789933nacco:TheFalkirkMiningCompanyMembernacco:CoalMiningMember2020-01-012020-12-310000789933nacco:TheFalkirkMiningCompanyMembernacco:CoalMiningMember2019-01-012019-12-310000789933us-gaap:BuildingAndBuildingImprovementsMember2020-01-012020-12-310000789933us-gaap:MachineryAndEquipmentMembersrt:MinimumMember2020-01-012020-12-310000789933us-gaap:MachineryAndEquipmentMembersrt:MaximumMember2020-01-012020-12-3100007899332020-12-012020-12-3100007899332020-11-012020-11-3000007899332020-08-012020-08-310000789933nacco:MississippiLigniteMiningCompanyMember2020-12-310000789933srt:ExecutiveOfficerMemberus-gaap:CommonClassAMembernacco:ParticipantsRetirementDateMemberus-gaap:StockCompensationPlanMember2020-01-012020-12-310000789933srt:ExecutiveOfficerMemberus-gaap:CommonClassAMembernacco:AwardDateMembersrt:MinimumMemberus-gaap:StockCompensationPlanMember2020-01-012020-12-310000789933srt:ExecutiveOfficerMemberus-gaap:CommonClassAMembernacco:AwardDateMemberus-gaap:StockCompensationPlanMember2020-01-012020-12-310000789933srt:ExecutiveOfficerMemberus-gaap:CommonClassAMembernacco:AwardDateMembersrt:MaximumMemberus-gaap:StockCompensationPlanMember2020-01-012020-12-310000789933srt:ExecutiveOfficerMemberus-gaap:CommonClassAMemberus-gaap:StockCompensationPlanMember2020-01-012020-12-310000789933srt:ExecutiveOfficerMemberus-gaap:CommonClassAMemberus-gaap:StockCompensationPlanMember2019-01-012019-12-310000789933srt:ExecutiveOfficerMemberus-gaap:CommonClassAMemberus-gaap:StockCompensationPlanMember2020-12-310000789933srt:DirectorMemberus-gaap:CommonClassAMemberus-gaap:RestrictedStockMember2020-01-012020-12-310000789933us-gaap:CommonClassAMembersrt:BoardOfDirectorsChairmanMemberus-gaap:RestrictedStockMember2020-01-012020-12-310000789933srt:DirectorMemberus-gaap:CommonClassAMemberus-gaap:RestrictedStockMember2020-12-310000789933us-gaap:CommonClassAMembersrt:BoardOfDirectorsChairmanMemberus-gaap:RestrictedStockMember2020-12-310000789933srt:DirectorMemberus-gaap:CommonClassAMemberus-gaap:RestrictedStockMember2019-01-012019-12-310000789933us-gaap:CommonClassAMembersrt:BoardOfDirectorsChairmanMemberus-gaap:RestrictedStockMember2019-01-012019-12-310000789933srt:DirectorMemberus-gaap:CommonClassAMemberus-gaap:RestrictedStockMember2019-12-310000789933us-gaap:CommonClassAMembersrt:BoardOfDirectorsChairmanMemberus-gaap:RestrictedStockMember2019-12-310000789933srt:DirectorMemberus-gaap:CommonClassAMembernacco:AwardDateMemberus-gaap:StockCompensationPlanMember2020-01-012020-12-310000789933nacco:ParticipantsRetirementFromBoardOfDirectorsMembersrt:DirectorMemberus-gaap:CommonClassAMemberus-gaap:StockCompensationPlanMember2020-01-012020-12-310000789933srt:DirectorMemberus-gaap:CommonClassAMembernacco:MinimumAgeOfDirectorUponRetirementFromBoardMemberus-gaap:StockCompensationPlanMember2020-01-012020-12-310000789933srt:DirectorMemberus-gaap:CommonClassAMembernacco:VoluntarySharesMember2020-12-310000789933srt:DirectorMemberus-gaap:CommonClassAMembernacco:VoluntarySharesMember2020-01-012020-12-310000789933srt:DirectorMemberus-gaap:CommonClassAMembernacco:VoluntarySharesMember2019-01-012019-12-310000789933srt:DirectorMemberus-gaap:CommonClassAMemberus-gaap:StockCompensationPlanMember2020-12-310000789933srt:DirectorMemberus-gaap:CommonClassAMemberus-gaap:StockCompensationPlanMember2020-01-012020-12-310000789933srt:DirectorMemberus-gaap:CommonClassAMemberus-gaap:StockCompensationPlanMember2019-01-012019-12-310000789933nacco:CoalMiningMemberus-gaap:OperatingSegmentsMember2020-01-012020-12-310000789933nacco:CoalMiningMemberus-gaap:OperatingSegmentsMember2019-01-012019-12-310000789933nacco:NorthAmericanMiningMemberus-gaap:OperatingSegmentsMember2020-01-012020-12-310000789933nacco:NorthAmericanMiningMemberus-gaap:OperatingSegmentsMember2019-01-012019-12-310000789933nacco:MineralsManagementMemberus-gaap:OperatingSegmentsMember2020-01-012020-12-310000789933nacco:MineralsManagementMemberus-gaap:OperatingSegmentsMember2019-01-012019-12-310000789933us-gaap:CorporateNonSegmentMember2020-01-012020-12-310000789933us-gaap:CorporateNonSegmentMember2019-01-012019-12-310000789933srt:ConsolidationEliminationsMember2020-01-012020-12-310000789933srt:ConsolidationEliminationsMember2019-01-012019-12-310000789933us-gaap:TransferredAtPointInTimeMember2020-01-012020-12-310000789933us-gaap:TransferredAtPointInTimeMember2019-01-012019-12-310000789933us-gaap:TransferredOverTimeMember2020-01-012020-12-310000789933us-gaap:TransferredOverTimeMember2019-01-012019-12-3100007899332021-01-012020-12-3100007899332022-01-012020-12-3100007899332023-01-012020-12-3100007899332024-01-012020-12-310000789933nacco:CoalLandsAndRealEstateMember2020-12-310000789933nacco:CoalLandsAndRealEstateMember2019-12-310000789933nacco:MineralInterestsMember2020-12-310000789933nacco:MineralInterestsMember2019-12-310000789933nacco:PlantAndEquipmentMember2020-12-310000789933nacco:PlantAndEquipmentMember2019-12-310000789933us-gaap:CoalSupplyAgreementsMember2020-12-310000789933us-gaap:CoalSupplyAgreementsMember2019-12-310000789933nacco:NacoalMember2020-12-310000789933nacco:CoalMiningMemberus-gaap:OperatingSegmentsMember2018-12-310000789933nacco:NorthAmericanMiningMemberus-gaap:OperatingSegmentsMember2018-12-310000789933us-gaap:CorporateNonSegmentMember2018-12-310000789933nacco:CoalMiningMemberus-gaap:OperatingSegmentsMember2019-12-310000789933nacco:NorthAmericanMiningMemberus-gaap:OperatingSegmentsMember2019-12-310000789933us-gaap:CorporateNonSegmentMember2019-12-310000789933nacco:CoalMiningMemberus-gaap:OperatingSegmentsMember2020-12-310000789933nacco:NorthAmericanMiningMemberus-gaap:OperatingSegmentsMember2020-12-310000789933us-gaap:CorporateNonSegmentMember2020-12-310000789933nacco:MississippiLigniteMiningCompanyMember2020-01-012020-12-310000789933nacco:CentennialMember2020-01-012020-12-310000789933nacco:CentennialMember2020-12-310000789933nacco:CentennialMemberus-gaap:SuretyBondMember2020-12-310000789933nacco:CentennialMember2019-01-012019-12-310000789933nacco:MississippiLigniteMiningCompanyMember2019-01-012019-12-310000789933nacco:BellaireCorporationMember2020-12-310000789933nacco:BellaireCorporationMember2019-12-310000789933nacco:NacoalMember2019-12-310000789933us-gaap:BaseRateMembernacco:NacoalMember2020-01-012020-12-310000789933nacco:NacoalMemberus-gaap:LondonInterbankOfferedRateLIBORMember2020-01-012020-12-310000789933nacco:NacoalMember2020-01-012020-12-310000789933nacco:NacoalMembersrt:MaximumMember2020-01-012020-12-310000789933nacco:DemandNotePayableToUnconsolidatedSubsidiaryMemberus-gaap:SecuredDebtMember2020-12-310000789933nacco:DemandNotePayableToUnconsolidatedSubsidiaryMemberus-gaap:SecuredDebtMember2019-12-310000789933nacco:NotesPayableMaturingDecember2026AndApril12027Memberus-gaap:SecuredDebtMember2020-12-310000789933us-gaap:SecuredDebtMembernacco:NotesPayableMaturingDecember2026Member2020-01-012020-12-310000789933srt:ScenarioForecastMemberus-gaap:SecuredDebtMembernacco:NotesPayableMaturingDecember2026Member2026-12-150000789933nacco:NotesPayableMaturingApril12027Memberus-gaap:SecuredDebtMember2020-01-012020-12-310000789933nacco:NotesPayableMaturingDecember2026AndApril12027Memberus-gaap:SecuredDebtMember2019-12-310000789933us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2020-12-310000789933us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2020-12-310000789933us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2020-12-310000789933us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2020-12-310000789933us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2019-12-310000789933us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2019-12-310000789933us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2019-12-310000789933us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2019-12-310000789933us-gaap:FairValueInputsLevel1Membernacco:BellaireCorporationMemberus-gaap:FairValueMeasurementsRecurringMember2020-01-012020-12-310000789933us-gaap:FairValueInputsLevel1Membernacco:BellaireCorporationMemberus-gaap:FairValueMeasurementsRecurringMember2019-01-012019-12-310000789933us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2020-01-012020-12-310000789933us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2020-01-012020-12-310000789933nacco:MineralManagementMember2020-01-012020-12-310000789933nacco:CoalMiningMember2020-01-012020-12-31nacco:vote0000789933us-gaap:CommonClassAMember2020-01-012020-12-310000789933us-gaap:CommonClassBMember2020-01-012020-12-310000789933nacco:A2019StockRepurchaseProgramMember2019-11-060000789933us-gaap:CommonClassAMembernacco:A2019StockRepurchaseProgramMember2020-01-012020-12-310000789933nacco:A2019StockRepurchaseProgramMember2020-01-012020-12-310000789933us-gaap:CommonClassAMembernacco:A2019StockRepurchaseProgramMember2019-01-012019-12-310000789933us-gaap:CommonClassAMembernacco:A2018StockRepurchaseProgramMember2019-01-012019-12-310000789933nacco:A2019StockRepurchaseProgramMember2019-01-012019-12-310000789933us-gaap:StateAndLocalJurisdictionMember2020-12-310000789933us-gaap:DomesticCountryMember2020-12-310000789933us-gaap:StateAndLocalJurisdictionMember2019-12-310000789933us-gaap:DomesticCountryMember2019-12-310000789933us-gaap:ForeignCountryMember2019-12-310000789933us-gaap:PensionPlansDefinedBenefitMember2019-01-012019-12-310000789933us-gaap:PensionPlansDefinedBenefitMembersrt:MinimumMember2020-12-310000789933us-gaap:PensionPlansDefinedBenefitMembersrt:MaximumMember2020-12-310000789933us-gaap:PensionPlansDefinedBenefitMembersrt:MinimumMember2019-12-310000789933us-gaap:PensionPlansDefinedBenefitMembersrt:MaximumMember2019-12-310000789933us-gaap:PensionPlansDefinedBenefitMembersrt:MinimumMember2020-01-012020-12-310000789933us-gaap:PensionPlansDefinedBenefitMembersrt:MaximumMember2020-01-012020-12-310000789933us-gaap:PensionPlansDefinedBenefitMembersrt:MinimumMember2019-01-012019-12-310000789933us-gaap:PensionPlansDefinedBenefitMembersrt:MaximumMember2019-01-012019-12-310000789933us-gaap:PensionPlansDefinedBenefitMember2020-01-012020-12-310000789933us-gaap:PensionPlansDefinedBenefitMember2019-12-310000789933us-gaap:PensionPlansDefinedBenefitMember2018-12-310000789933us-gaap:PensionPlansDefinedBenefitMember2020-12-310000789933us-gaap:DefinedBenefitPlanEquitySecuritiesUsMemberus-gaap:PensionPlansDefinedBenefitMember2020-12-310000789933us-gaap:DefinedBenefitPlanEquitySecuritiesUsMemberus-gaap:PensionPlansDefinedBenefitMember2019-12-310000789933us-gaap:DefinedBenefitPlanEquitySecuritiesUsMemberus-gaap:PensionPlansDefinedBenefitMembersrt:MinimumMember2020-12-310000789933us-gaap:DefinedBenefitPlanEquitySecuritiesUsMemberus-gaap:PensionPlansDefinedBenefitMembersrt:MaximumMember2020-12-310000789933us-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMemberus-gaap:PensionPlansDefinedBenefitMember2020-12-310000789933us-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMemberus-gaap:PensionPlansDefinedBenefitMember2019-12-310000789933us-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMemberus-gaap:PensionPlansDefinedBenefitMembersrt:MinimumMember2020-12-310000789933us-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMemberus-gaap:PensionPlansDefinedBenefitMembersrt:MaximumMember2020-12-310000789933us-gaap:PensionPlansDefinedBenefitMemberus-gaap:FixedIncomeSecuritiesMember2020-12-310000789933us-gaap:PensionPlansDefinedBenefitMemberus-gaap:FixedIncomeSecuritiesMember2019-12-310000789933us-gaap:FixedIncomeSecuritiesMemberus-gaap:PensionPlansDefinedBenefitMembersrt:MinimumMember2020-12-310000789933us-gaap:FixedIncomeSecuritiesMemberus-gaap:PensionPlansDefinedBenefitMembersrt:MaximumMember2020-12-310000789933us-gaap:PensionPlansDefinedBenefitMemberus-gaap:MoneyMarketFundsMember2020-12-310000789933us-gaap:PensionPlansDefinedBenefitMemberus-gaap:MoneyMarketFundsMember2019-12-310000789933us-gaap:PensionPlansDefinedBenefitMemberus-gaap:MoneyMarketFundsMembersrt:MinimumMember2020-12-310000789933us-gaap:PensionPlansDefinedBenefitMemberus-gaap:MoneyMarketFundsMembersrt:MaximumMember2020-12-310000789933us-gaap:DefinedBenefitPlanEquitySecuritiesUsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:PensionPlansDefinedBenefitMember2020-12-310000789933us-gaap:DefinedBenefitPlanEquitySecuritiesUsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:PensionPlansDefinedBenefitMember2019-12-310000789933us-gaap:FairValueInputsLevel1Memberus-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMemberus-gaap:PensionPlansDefinedBenefitMember2020-12-310000789933us-gaap:FairValueInputsLevel1Memberus-gaap:DefinedBenefitPlanEquitySecuritiesNonUsMemberus-gaap:PensionPlansDefinedBenefitMember2019-12-310000789933us-gaap:FairValueInputsLevel1Memberus-gaap:FixedIncomeSecuritiesMemberus-gaap:PensionPlansDefinedBenefitMember2020-12-310000789933us-gaap:FairValueInputsLevel1Memberus-gaap:FixedIncomeSecuritiesMemberus-gaap:PensionPlansDefinedBenefitMember2019-12-310000789933us-gaap:FairValueInputsLevel1Memberus-gaap:PensionPlansDefinedBenefitMemberus-gaap:MoneyMarketFundsMember2020-12-310000789933us-gaap:FairValueInputsLevel1Memberus-gaap:PensionPlansDefinedBenefitMemberus-gaap:MoneyMarketFundsMember2019-12-310000789933us-gaap:FairValueInputsLevel1Memberus-gaap:PensionPlansDefinedBenefitMember2020-12-310000789933us-gaap:FairValueInputsLevel1Memberus-gaap:PensionPlansDefinedBenefitMember2019-12-310000789933us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2020-12-310000789933us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2019-12-310000789933us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMembersrt:MinimumMember2020-01-012020-12-310000789933us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMembersrt:MaximumMember2020-01-012020-12-310000789933us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2019-01-012019-12-310000789933us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2020-01-012020-12-310000789933us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2018-12-310000789933us-gaap:CustomerConcentrationRiskMembernacco:CoalMiningCustomerMembernacco:CoalMiningMemberus-gaap:RevenueFromContractWithCustomerMember2020-01-012020-12-310000789933us-gaap:CustomerConcentrationRiskMembernacco:CoalMiningCustomerMembernacco:CoalMiningMemberus-gaap:RevenueFromContractWithCustomerMember2019-01-012019-12-310000789933nacco:NAMiningCustomerMemberus-gaap:CustomerConcentrationRiskMembernacco:NorthAmericanMiningMemberus-gaap:RevenueFromContractWithCustomerMember2020-01-012020-12-310000789933nacco:NAMiningCustomerMemberus-gaap:CustomerConcentrationRiskMembernacco:NorthAmericanMiningMemberus-gaap:RevenueFromContractWithCustomerMember2019-01-012019-12-310000789933us-gaap:CustomerConcentrationRiskMembernacco:MineralsManagementMemberus-gaap:RevenueFromContractWithCustomerMembernacco:MineralsManagementLesseeMember2020-01-012020-12-310000789933us-gaap:CustomerConcentrationRiskMembernacco:MineralsManagementMemberus-gaap:RevenueFromContractWithCustomerMembernacco:MineralsManagementLesseeMember2019-01-012019-12-310000789933us-gaap:CustomerConcentrationRiskMembernacco:CoalMiningMembernacco:EarningsOfUnconsolidatedMinesMembernacco:TopTwoCustomersBasinElectricAndGREMember2020-01-012020-12-310000789933srt:ParentCompanyMember2020-12-310000789933srt:ParentCompanyMember2019-12-310000789933nacco:BellaireCorporationMembersrt:ParentCompanyMember2020-12-310000789933nacco:BellaireCorporationMembersrt:ParentCompanyMember2019-12-310000789933nacco:UnconsolidatedMinesMembernacco:NacoalMember2020-12-310000789933nacco:UnconsolidatedMinesMembernacco:NacoalMember2019-12-310000789933nacco:UnconsolidatedMinesMemberus-gaap:VariableInterestEntityNotPrimaryBeneficiaryMembernacco:NacoalMember2020-01-012020-12-310000789933nacco:UnconsolidatedMinesMemberus-gaap:VariableInterestEntityNotPrimaryBeneficiaryMembernacco:NacoalMember2019-01-012019-12-310000789933nacco:UnconsolidatedMinesMemberus-gaap:VariableInterestEntityNotPrimaryBeneficiaryMembernacco:NacoalMember2020-12-310000789933nacco:UnconsolidatedMinesMemberus-gaap:VariableInterestEntityNotPrimaryBeneficiaryMembernacco:NacoalMember2019-12-310000789933nacco:UnconsolidatedMinesMembernacco:NacoalMember2020-01-012020-12-310000789933nacco:UnconsolidatedMinesMembernacco:NacoalMember2019-01-012019-12-310000789933nacco:JonesDayMember2020-01-012020-12-310000789933nacco:JonesDayMember2019-01-012019-12-310000789933nacco:AlfredM.RankinJr.Member2019-01-012019-12-310000789933nacco:AlfredM.RankinJr.Member2020-01-012020-12-3100007899332020-10-012020-12-310000789933srt:ParentCompanyMember2020-01-012020-12-310000789933srt:ParentCompanyMember2019-01-012019-12-310000789933srt:ParentCompanyMember2018-12-310000789933us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2019-12-310000789933us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-01-012020-12-310000789933us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-12-310000789933us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2018-12-310000789933us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2019-01-012019-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

| | | | | | | | | | | |

| (Mark One) | | | |

| ☑ | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the fiscal year ended | December 31, 2020 |

or

| | | | | | | | |

| ☐ | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File No. 1-9172

NACCO INDUSTRIES, INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | | | | | | | | | | | | | |

| Delaware | | 34-1505819 | |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) | |

| | | | | | | | |

| 5875 Landerbrook Drive, | Suite 220 | | | |

| Cleveland, | Ohio | | | | 44124-4069 | |

| (Address of principal executive offices) | | (Zip Code) | |

Registrant's telephone number, including area code: (440) 229-5151

Securities registered pursuant to Section 12(b) of the Act

| | | | | | | | | | | | | | |

Title of each class

| | Trading Symbol

| | Name of each exchange on which registered

|

| Class A Common Stock, $1 par value per share | | NC | | New York Stock Exchange |

Class B Common Stock is not publicly listed for trade on any exchange or market system; however, Class B Common Stock is convertible into Class A Common Stock on a share-for-share basis.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes þ No £

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes þ No £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☐ | Accelerated filer | ☑ | Non-accelerated filer | ☐ | Smaller reporting company | ☑ | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act)

Yes ☐ No ☑

Aggregate market value of Class A Common Stock and Class B Common Stock held by non-affiliates as of June 30, 2020 (the last business day of the registrant's most recently completed second fiscal quarter): $96,645,091

Number of shares of Class A Common Stock outstanding at February 19, 2021: 5,490,948

Number of shares of Class B Common Stock outstanding at February 19, 2021: 1,566,877

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company's Proxy Statement for its 2021 annual meeting of stockholders are incorporated herein by reference in Part III of this Form 10-K.

NACCO INDUSTRIES, INC.

TABLE OF CONTENTS

PART I

Item 1. BUSINESS

General

NACCO Industries, Inc.® (“NACCO” or the “Company”), through a portfolio of mining and natural resources businesses, operates under three business segments: Coal Mining, North American Mining ("NAMining") and Minerals Management. The Coal Mining segment operates surface coal mines under long-term contracts with power generation companies and an activated carbon producer pursuant to a service-based business model. The NAMining segment provides value-added contract mining and other services for producers of aggregates, lithium and other minerals. The Minerals Management segment acquires and promotes the development of oil, gas and coal mineral interests, generating income primarily from royalty-based lease payments from third parties. In addition, the Company has a business providing stream and wetland mitigation solutions.

The Company has items not directly attributable to a reportable segment which are not included as part of the measurement of segment operating profit, which are primarily administrative costs related to public company reporting requirements at the parent company and the financial results of Mitigation Resources of North America® (“MRNA”) and Bellaire Corporation (“Bellaire”). MRNA generates and sells stream and wetland mitigation credits (known as mitigation banking) and provides services to those engaged in permittee-responsible stream and wetland mitigation. Bellaire manages the Company’s long-term liabilities related to former Eastern U.S. underground mining activities.

NACCO was incorporated as a Delaware corporation in 1986 in connection with the formation of a holding company structure for a predecessor corporation organized in 1913.

The Company has continued to operate as an essential business during the COVID-19 pandemic because it supports critical infrastructure industries. The extent to which COVID-19 impacts the Company going forward will depend on numerous factors and future developments that remain uncertain.

Business Strategy

The Company is leveraging its core mining and natural resources management skills to develop a strong and diverse portfolio of affiliated businesses operating in the mining and natural resources industries while maintaining a conservative capital structure. Diversified strategic growth is the key to enhancing net income as well as increasing free cash flow available to continue to reinvest in and expand the businesses.

NAMining continues to expand the scope of its business development activities to grow and diversify by targeting geographically diverse customers who require a broad range of minerals and materials. NAMining also continues to leverage the Company’s core mining skills to expand the range of contract mining services provided, in addition to providing comprehensive mining services to operate entire mines when appropriate, such as the long-term mining contract with Lithium Americas to provide mining services for its Thacker Pass lithium project in Nevada.

The Company’s efforts to grow and diversify the Minerals Management segment include acquiring additional mineral interests or similar investments in the energy industry. Once mineral and royalty interests have been acquired, the Minerals Management segment will benefit from the continued development of its mineral properties without the need for investment of additional capital. This business model can deliver higher average operating margins over the life of a reserve than traditional oil and gas companies that bear the cost of exploration, production and/or development.

MRNA creates and sells stream and wetland mitigation credits and provides services to those engaged in permittee-responsible mitigation. This business offers opportunity for growth and diversification in an industry where the Company has substantial knowledge and expertise. MRNA has achieved impressive initial growth and is positioned for additional growth.

One of the Company’s core strategies is to pursue activities which can provide resiliency to its existing coal mining

operations. The Company works to drive down coal production costs and maximize efficiencies and operating capacity at mine locations to help customers with management fee contracts be more competitive. These activities benefit both customers and the Company's Coal Mining segment, as fuel cost is a significant driver for power plant dispatch. Increased power plant dispatch results in increased demand for coal by the Coal Mining segment's customers.

The Company evaluates opportunities to expand its coal mining business, but opportunities are few. Low natural gas prices and growth in renewable energy sources, such as wind and solar, are likely to continue to unfavorably affect the amount of electricity dispatched from coal-fired power plants. The political and regulatory environment is not receptive to development of new coal-fired power generation projects which would create opportunities to build and operate new coal mines. However, the Company would consider opportunities where it can apply its management fee business model to assume operation of existing

surface coal mining operations in the United States. Outright acquisitions of existing coal mines or mining companies with exposure to fluctuating coal commodity markets, or structures that would create significant leverage, are outside the Company’s area of focus.

In all of its business endeavors, the Company continues to maintain the highest levels of customer service and operational excellence, with an unwavering focus on safety, environmental stewardship and people.

Business Developments

During 2020, the Minerals Management segment acquired mineral interests for approximately 65.5 thousand gross acres and 1.2 thousand net royalty acres in the Permian Basin in Texas for a total purchase price of approximately $14.2 million. The acquired interests align with the Company’s strategy of selectively acquiring mineral interests with a balance of near-term cash flow yields and long-term growth potential, in oil-rich basins offering diversification from the Company’s legacy mineral interests in predominately natural gas-rich basins.

The Sabine Mining Company (“Sabine”) operates the Sabine Mine in Texas. All production from Sabine is delivered to Southwestern Electric Power Company's (“SWEPCO”) Henry W. Pirkey Plant (the “Pirkey Plant”). SWEPCO is an American Electric Power (“AEP”) company. On November 5, 2020, AEP announced it intends to retire the Pirkey Plant in 2023 in order to comply with the U.S. Environmental Protection Agency’s Coal Combustion Residuals rule. The Sabine Mine delivered 1.9 million and 2.6 million tons to the Pirkey Plant in 2020 and 2019, respectively. During 2020, SWEPCO reduced its expected future annual delivery requirements to be between 1.4 million and 1.7 million tons. The Sabine Mine contributed $3.9 million and $4.6 million to NACCO’s Earnings from Unconsolidated Operations during 2020 and 2019, respectively.

The Coteau Properties Company (“Coteau”) operates the Freedom Mine in North Dakota. All coal production from the Freedom Mine is delivered to Basin Electric Power Cooperative (“Basin Electric”). Basin Electric utilizes the coal at the Great Plains Synfuels Plant (the “Synfuels Plant”), Antelope Valley Station and Leland Olds Station. The Synfuels Plant is a coal gasification plant that manufactures synthetic natural gas and produces fertilizers, solvents, phenol, carbon dioxide, and other chemical products for sale. On November 5, 2020, Basin Electric informed its employees and Coteau that it is considering changes that may result in modifications to its Synfuels Plant that could potentially reduce or eliminate coal requirements at the Synfuels Plant beginning in 2026. Basin Electric indicated that if it decides to proceed with any changes that could reduce or eliminate the use of coal, the feedstock change is not expected to occur before 2026. As a result, coal deliveries to the Synfuels Plant are expected to continue until at least 2026.

On September 30, 2020, Caddo Creek Resources Company, LLC's (“Caddo Creek's”) customer, a division of Cabot Corporation, entered into a long-term supply agreement with a subsidiary of Advanced Emissions Solutions (“AES”) as well as an agreement for the sale of the Marshall Mine, operated by Caddo Creek, to a subsidiary of AES. AES announced its intent to close the Marshall Mine. Caddo Creek entered into a contract with a subsidiary of AES to perform the required mine reclamation. The Marshall Mine delivered 0.1 million and 0.2 million tons during 2020 and 2019, respectively.

The contract mining agreement between Camino Real Fuels, LLC (“Camino Real”) and its customer, Dos Republicas Coal Partnership (“DRCP”), terminated effective July 1, 2020 as a result of the unexpected termination by Comisión Federal de Electricidad (“CFE”) of its coal supply contract with an affiliate of DRCP. The termination of the contract between CFE and DRCP eliminated DRCP’s need for coal from Camino Real's Eagle Pass Mine, and resulted in mine closure. Mine reclamation is the responsibility of DRCP. Camino Real has no legal obligation to perform mine reclamation. The Eagle Pass Mine delivered 0.3 million and 1.6 million tons during 2020 and 2019, respectively.

On May 7, 2020, Great River Energy ("GRE"), Falkirk Mine's customer, announced its intent to retire the Coal Creek Station power plant in the second half of 2022 and modify the Spiritwood Station power plant to be fueled by natural gas. As noted in the announcement, GRE is willing to consider opportunities to sell Coal Creek Station. Falkirk Mine is the sole supplier of lignite coal to Coal Creek Station pursuant to a long-term contract under which Falkirk also supplies approximately 0.3 million tons of lignite coal per year to Spiritwood Station. Falkirk delivered a total of 7.2 million and 7.4 million tons of lignite coal and contributed $16.1 million and $15.9 million to NACCO’s Earnings from Unconsolidated Operations during 2020 and 2019, respectively.

In 2019, NAMining, through a new subsidiary, Sawtooth Mining, entered into a mining agreement to serve as exclusive contract miner for the Thacker Pass lithium project in northern Nevada. The Thacker Pass Project is 100% owned by Lithium Nevada Corp, a subsidiary of Lithium Americas Corp. Lithium Nevada plans to develop a lithium production facility near what is believed to be the largest known lithium deposit in the United States. Sawtooth Mining will provide comprehensive mining services similar to the Company's typical scope of work in the Coal Mining segment. The mining agreement provides that

Lithium Nevada will reimburse Sawtooth Mining for its operating and mine reclamation costs, and pay Sawtooth Mining a management fee per metric ton of lithium delivered during the 20-year contract term commencing with receipt of construction and operating permits by Lithium Nevada.

Coal Mining Segment

The Coal Mining segment, operating as North American Coal Corporation® ("NACoal"), operates surface coal mines under long-term contracts with power generation companies and an activated carbon producer pursuant to a service-based business model. Coal is surface-mined in North Dakota, Texas, Mississippi, Louisiana and on the Navajo Nation in New Mexico. Each mine is fully integrated with its customer's operations.

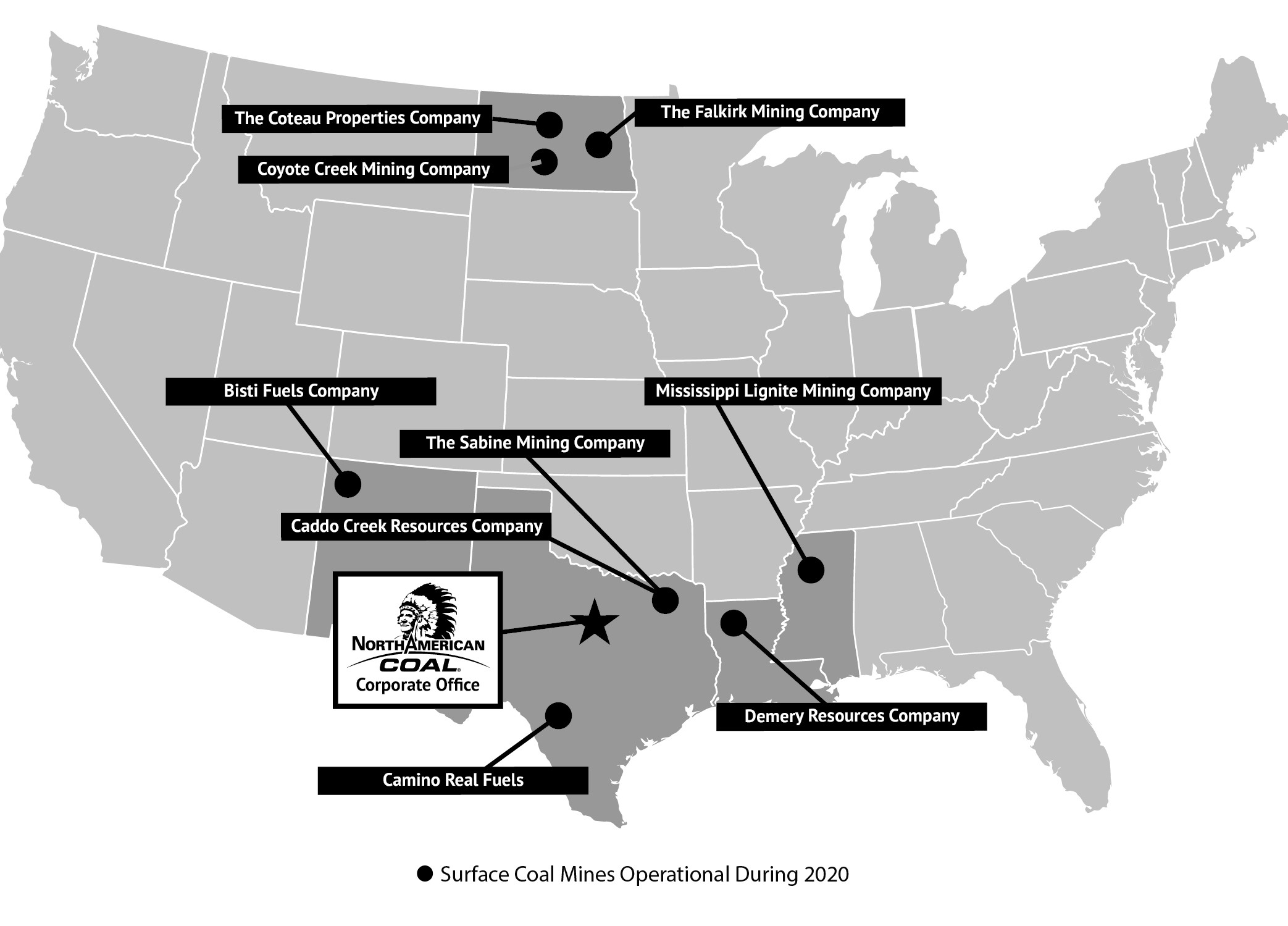

During 2020, the Company's operating coal mines were: Bisti Fuels Company, LLC (“Bisti”), Caddo Creek, Camino Real, Coteau, Coyote Creek Mining Company, LLC (“Coyote Creek”), Demery Resources Company, LLC (“Demery”), Falkirk, Mississippi Lignite Mining Company (“MLMC”) and Sabine.

Coteau, Coyote, Falkirk, MLMC and Sabine supply lignite coal for power generation. Bisti supplies sub-bituminous coal for power generation. Demery supplies lignite coal for the production of activated carbon. Each of these mines deliver their coal production to adjacent or nearby power plants, synfuels plants or an activated carbon processing facility under long-term supply contracts. Each mine is the exclusive supplier of coal to its customers' facilities. MLMC’s coal supply contract contains a take or pay provision; all other coal supply contracts are requirements contracts under which earnings can fluctuate. In addition, certain coal supply contracts can be terminated early, which would result in a reduction to future earnings.

At all operating coal mines other than MLMC, the Company is paid a management fee per ton of coal or heating unit (MMBtu) delivered. Each contract specifies the indices and mechanics by which fees change over time, generally in line with broad measures of U.S. inflation. The customers are responsible for funding all mine operating costs, including final mine reclamation, and directly or indirectly providing all of the capital required to build and operate the mine. This contract structure eliminates exposure to spot coal market price fluctuations while providing cash flow with minimal capital investment. Other than at Coyote Creek, debt financing provided by or supported by the customers is without recourse to NACCO and NACoal. See Note 17 to the Consolidated Financial Statements in this Form 10-K for further discussion of Coyote Creek's guarantees.

All operating coal mines other than MLMC meet the definition of a variable interest entity (“VIE”). In each case, NACCO is not the primary beneficiary of the VIE as it does not exercise financial control; therefore, NACCO does not consolidate the results of these operations within its financial statements. Instead, these contracts are accounted for as equity method investments. The income before income taxes associated with these VIEs is reported as Earnings of unconsolidated operations on the Consolidated Statements of Operations, and the Company’s investment is reported on the line Investments in Unconsolidated Subsidiaries in the Consolidated Balance Sheets. The mines that meet the definition of a VIE are referred to collectively as the “Unconsolidated Subsidiaries.” For tax purposes, the Unconsolidated Subsidiaries are included within the NACCO consolidated U.S. tax return; therefore, the income tax expense line on the Consolidated Statements of Operations includes income taxes related to these entities. See Note 17 to the Consolidated Financial Statements in this Form 10-K for further information on the Unconsolidated Subsidiaries.

The MLMC contract is the only operating coal contract in which the Company is responsible for all operating costs, capital requirements and final mine reclamation; therefore, MLMC is consolidated within NACCO’s financial statements. MLMC sells coal to its customer at a contractually agreed-upon price which adjusts monthly, primarily based on changes in the level of established indices which reflect general U.S. inflation rates. Profitability at MLMC is affected by customer demand for coal and changes in the indices that determine sales price and actual costs incurred. As diesel fuel is heavily weighted among the indices used to determine the coal sales price, the persistence of low diesel fuel prices can negatively affect earnings at MLMC.

MLMC delivers coal to the Red Hills Power Plant in Ackerman, Mississippi. The Red Hills Power Plant supplies electricity to the Tennessee Valley Authority ("TVA") under a long-term Power Purchase Agreement ("PPA"). MLMC’s contract with its customer runs through 2032. TVA’s power portfolio includes coal, nuclear, hydroelectric, natural gas and renewables. The decision of which power plants to dispatch is determined by TVA.

The coal reserves at Coteau, Falkirk, Coyote, MLMC and Centennial Natural Resources ("Centennial") are owned or controlled by the Company. The coal reserves at all other mines are owned or controlled by the respective mine’s customer. Total coal reserves approximate 1.9 billion tons (including the unconsolidated coal mining subsidiaries), with approximately 0.7 billion tons committed to customers pursuant to long-term contracts.

The Company performs contemporaneous reclamation activities at each mine in the normal course of operations. Under all of the Unconsolidated Subsidiaries’ contracts, the customer has the obligation to fund final mine reclamation activities. Under

certain contracts, the Unconsolidated Subsidiary holds the mine permit and is therefore responsible for final mine reclamation activities. To the extent the Unconsolidated Subsidiary performs such final reclamation, it is compensated for providing those services in addition to receiving reimbursement from customers for costs incurred.

NAMining Segment

The NAMining segment provides value-added contract mining and other services for producers of aggregates, lithium and other minerals. The segment is a primary platform for the Company’s growth and diversification of mining activities outside of the coal industry. NAMining provides contract mining services for independently owned mines and quarries, creating value for its customers by performing the mining aspects of its customers’ operations. This allows customers to focus on their areas of expertise: materials handling and processing, product sales and distribution. NAMining operates primarily at limestone quarries in Florida, but is focused on expanding outside of Florida and into mining materials other than limestone. In addition, NAMining will serve as exclusive contract miner for the Thacker Pass lithium project in northern Nevada.

NAMining utilizes both fixed price and management fee contract structures. Certain of the entities within the NAMining segment are VIEs and are accounted for under the equity method as Unconsolidated Subsidiaries. See Note 17 to the Consolidated Financial Statements in this Form 10-K for further information on the Unconsolidated Subsidiaries.

Minerals Management Segment

The Minerals Management segment derives income primarily by leasing its royalty and mineral interests to third-party exploration and production companies, and, to a lesser extent, other mining companies, granting them the rights to explore, develop, mine, produce, market and sell gas, oil, and coal in exchange for royalty payments based on the lessees' sales of those minerals.

During 2020, the Minerals Management segment acquired mineral interests in the Permian Basin in Texas and intends to make future acquisitions of mineral and royalty interests that meet the Company’s acquisition criteria as part of its growth strategy. The acquisition criteria includes building a blended portfolio of mineral and royalty interests (i) with new wells anticipated to come online within one to two years of investment, (ii) in areas with forecasted future development within five years after acquisition, or (iii) with existing producing wells further along the decline curve that will generate stable cash flow. In addition, acquisitions should extend the geographic footprint to diversify across multiple basins with a preliminary focus on the more oil-rich Permian and Williston basins and a secondary focus on other diversifying basins to increase regional exposure. While the current focus is on the acquisition of mineral and royalty interests, the Company would also consider investments in overriding royalty interests, non-participating royalty interests or non-operated working interests under certain circumstances. The current acquisition strategy does not contemplate any near-term working interest investments in which the Company would act as the operator.

Total consideration for the 2020 acquisitions of mineral and royalty interests was $14.2 million, of which $12.0 million closed in December 2020, $2.0 million closed in November 2020 and $0.2 million closed in August 2020. The acquisitions include 65.5 thousand gross acres and 1.2 thousand net royalty acres. The Company did not acquire any mineral interests in 2019. Including the 2020 acquisitions, total mineral and royalty interests include approximately 109.2 thousand gross acres and 58.1 thousand net royalty acres.

The Company’s legacy royalty and mineral interests are located in Ohio (Utica and Marcellus shale natural gas), Louisiana (Haynesville shale and Cotton Valley formation natural gas), Texas (Cotton Valley and Austin Chalk formation natural gas), Mississippi (coal), Pennsylvania (coal, coalbed methane and Marcellus shale natural gas), Alabama (coal, coalbed methane and natural gas) and North Dakota (coal, oil and natural gas). The majority of the Company’s legacy reserves were acquired as part of its historical coal mining operations.

The Minerals Management segment owns royalty interests, mineral interests, nonparticipating royalty interests, and overriding royalty interests.

•Royalty Interest. Royalty interests generally result when the owner of a mineral interest leases the underlying minerals to an exploration and production company pursuant to an oil and gas lease. Typically, the resulting royalty interest is a cost-free percentage of production revenues for minerals extracted from the acreage. Holders of royalty interests are generally not responsible for capital expenditures or lease operating expenses, but may be responsible for certain post-production expenses, and typically have no environmental liability. Royalty interests expire upon the expiration of the oil and gas lease.

•Mineral Interest. Mineral interests are perpetual rights of the owner to explore, develop, exploit, mine, and/or produce any or all of the minerals lying below the surface of the property. The holder of a mineral interest has the right to lease the minerals to an exploration and production company. Upon the execution of an oil and gas lease, the lessee (the exploration and production company) becomes the working interest owner and the lessor (the mineral interest owner) has a royalty interest.

•Non-Participating Royalty Interest (“NPRIs”). NPRI is an interest in oil and gas production which is created from the mineral estate. The NPRI is expense-free, bearing no operational costs of production. The term “non-participating” indicates that the interest owner does not share in the bonus, rentals from a lease, nor the right to participate in the execution of oil and gas leases.

•Overriding Royalty Interest (“ORRIs”). ORRIs are created by carving out the right to receive royalties from a working interest. Like royalty interests, ORRIs do not confer an obligation to make capital expenditures or pay for lease operating expenses and have limited environmental liability, however ORRIs may be calculated net of post-production expenses, depending on how the ORRI is structured. ORRIs that are carved out of working interests are linked to the same underlying oil and gas lease that created the working interest, and therefore, such ORRIs are typically subject to expiration upon the expiration or termination of the oil and gas lease.

The Company may own more than one type of mineral and royalty interest in the same tract of land. For example, where the Company owns an ORRI in a lease on the same tract of land in which it owns a mineral interest, the ORRI in that tract will relate to the same gross acres as the mineral interest in that tract.

The Minerals Management segment will benefit from the continued development of its mineral properties without the need for investment of additional capital once mineral and royalty interests have been acquired. The Minerals Management segment does not have any investments under which it would be required to bear the cost of exploration, production or development.

As an owner of royalty and mineral interests, the Company’s access to information concerning activity and operations of its royalty and mineral interests is limited. The Company does not have information that would be available to a company with oil and natural gas operations because detailed information is not generally available to owners of royalty and mineral interests. Consequently, the exact number of wells producing from or drilling on the Company’s mineral interests at a given point in time is not determinable. The following table sets forth information about Company’s best estimate of the number of gross and net productive wells as of December 31, 2020:

| | | | | | | | | | | |

| Gross | | Net |

| Oil | 279 | | 0.2 |

| Natural Gas | 408 | | 26.5 |

| Total | 687 | | 26.7 |

Gross wells are the total wells in which an interest is owned.

Net wells are the sum of the fractional interest owned in gross wells.

The majority of the Company’s producing mineral and royalty interest acreage is, or in the future, can be pooled with third-party acreage to form pooled units. Pooling proportionately reduces the Company’s royalty interest in wells drilled in a pooled unit, and it proportionately increases the number of wells in which the Company has such reduced royalty interest.

Customers

The principal customers of the Coal Mining segment are electric utilities, an independent power provider and a producer of activated carbon.

The principal customers of the NAMining segment are limestone producers. In addition, NAMining will serve as exclusive contract miner for the Thacker Pass lithium project in northern Nevada.

The Minerals Management segment generates income primarily from royalty-based lease payments from oil, gas and to a lesser extent, coal producers. The pricing of oil, gas and coal sales is primarily determined by supply and demand in the marketplace

and can fluctuate considerably. As a royalty owner and non-operator, the Company has limited access to timely information, involvement, and operational control over the volumes of oil, gas and coal produced and sold and the terms and conditions on which such volumes are marketed and sold.

In 2020, two customers individually accounted for more than 10% of consolidated revenue. In 2019, two customers and an oil and gas lessee individually accounted for more than 10% of consolidated revenue. The following represents the revenue attributable to each of these entities as a percentage of consolidated revenue for those years:

| | | | | | | | | | | | | | | | | |

| | | Percentage of Consolidated Revenue |

| Segment | | 2020 | | 2019 | | |

| Coal Mining customer | | 55 | % | | 48 | % | | |

| NAMining customer | | 19 | % | | 21 | % | | |

| Minerals Management lessee | | less than 10% | | 12 | % | | |

The loss of either of these customers or the lessee could have a material adverse effect on the results of operations attributable to the applicable segment and on the Company's consolidated results of operations.

In addition to the customers listed above, the Company has certain subsidiaries that meet the definition of a VIE; therefore, NACCO does not consolidate the results of these operations within its financial statements. Instead, these contracts are accounted for as equity method investments. For the year ended December 31, 2020, the Coal Mining segment derived approximately 60% of the Earnings of Unconsolidated Operations from two customers, Basin Electric and GRE. GRE announced its intent to close Coal Creek station in 2022. The loss of either of these contracts could have a material adverse effect on the Earnings of Unconsolidated Operations of the Coal Mining segment and a material adverse effect on the Company's Consolidated Statements of Operations.

Competition

The Company's coal mines are directly adjacent to the customer’s property, with economical delivery methods that include conveyor belt delivery systems linked to the customer’s facilities or short-haul rail systems. All of the mines in the Coal Mining segment are the most economical suppliers to each of their respective customers as a result of transportation advantages over competitors. In addition, the customers' facilities were specifically designed to use the coal being mined.

The coal industry competes with other sources of energy, particularly oil, gas, hydro-electric power and nuclear power. In addition, it competes with subsidized sources of energy, primarily wind and solar. Among the factors that affect competition are the price and availability of oil and natural gas, environmental and related political considerations, the time and expenditures required to develop new energy sources, the cost of transportation, the cost of compliance with governmental regulations, the impact of federal and state energy policies, the impact of subsidies on renewable pricing and the Company's customers' dispatch decisions, which may take into account carbon dioxide emissions. The ability of the Coal Mining Segment to maintain comparable levels of coal production at existing facilities and to market and develop its reserves will depend upon the interaction of these factors.

Electricity generating units are chosen to run primarily based on operating costs, of which fuel costs account for the largest share. Sustained low natural gas prices have resulted in an increase in electricity generated from natural gas leading to a decline in the use of coal-fired capacity in the United States. Natural gas-fired power plants have the most potential to continue to displace coal-fired electric baseload power generation in the near term. There also continues to be an increase in the amount of electricity generated by wind and solar. As an example, the Company estimates wind capacity in North Dakota has increased over 60% since 2015 to approximately 3,600 megawatts and wind developers have expressed an interest in building more than 3,000 megawatts of additional wind generation in North Dakota over the next several years. Federal and state mandates for increased use of electricity derived from renewable energy sources have also negatively affected demand for coal. Such mandates, combined with other incentives to use renewable energy sources, such as tax credits, make alternative fuel sources competitive with coal. The Taxpayer Certainty and Disaster Tax Relief Act of 2020 extended the production tax credit (“PTC”) under Section 45 of the Internal Revenue Code and the investment tax credit (“ITC”) under Section 48 of the Code. The PTC for wind was extended at the current phase-out level (60% of the otherwise allowable credits) for facilities where construction begins in 2021. The ITC for solar was extended at 26% for energy property where construction begins in 2021-2022 and at 22% where construction begins in 2023-2025. Solar energy property placed in service after December 31, 2025 receives only a 10% ITC.

Certain of the Coal Mining segment's customers continue to invest in efficiency and environmental upgrades to their facilities. Because the Coal Mining segment's customers’ power plants are competitive suppliers of electricity in their respective dispatch

areas relative to other coal-fired generating units in those dispatch areas, the Company considers its surface coal mining operations to be well positioned relative to most other mines servicing coal-fired generating units.

Based on industry information, the Company believes it was one of the five largest coal producers in the U.S. in 2020 based on total coal tons produced.

NAMining faces competition from aggregates producers which choose to self-perform mining operations and from other mining companies.

In the Minerals Management segment, the oil and gas industry is intensely competitive; the Company primarily competes with companies and investors for the acquisition of oil and gas properties, some of which have greater resources and who may be able to pay more for productive oil and natural gas properties or to define, evaluate, bid for and purchase a greater number of properties than the Company’s financial or human resources permit. Additionally, many of the Minerals Management segment's competitors are, or are affiliated with, operators that engage in the exploration and production of their oil and gas properties, which allows them to acquire larger assets that include operated properties. Larger or more integrated competitors may be able to absorb the burden of existing, and any changes to, federal, state and local laws and regulations more easily than the Company can, which would adversely affect its competitive position. The integrated competitors may also have a better understanding of when minerals they acquire will be developed, as they are often the developer. The Minerals Management segment’s ability to acquire additional properties in the future will be dependent upon its ability to evaluate and select suitable properties and to consummate transactions in a highly competitive environment. In addition, because the Company has fewer financial and human resources than many companies in the oil and gas industry, the Company may be at a disadvantage in bidding for oil and natural gas properties.

Seasonality

The Company has experienced limited variability in its results due to the effect of seasonality; however, variations in coal demand can occur as a result of the timing and duration of planned or unplanned outages at customers' facilities. Variations in coal demand can also occur as a result of changes in market prices of competing fuels such as natural gas, wind and solar power and demand for electricity, which can fluctuate based on changes in weather patterns. The NAMining segment extracts a significant amount of the annual limestone produced in Florida. The Florida construction industry can be affected by the cyclicality of the economy, seasonal weather conditions and pandemics, all of which can result in variations in limestone demand.

In the Minerals Management segment, oil and natural gas wells have high initial production rates and follow a natural decline before settling into relatively stable, long-term production. Decline rates can vary due to factors like well depth, well length, formation pressure, and facility design. In addition to the natural production decline curve, royalty income can fluctuate favorably or unfavorably in response to a number of factors outside of the Company's control, including the number of wells being operated by third parties, fluctuations in commodity prices (primarily oil and natural gas), fluctuations in production rates associated with operator decisions, regulatory risks, the Company's lessees' willingness and ability to incur well-development and other operating costs, and changes in the availability and continuing development of infrastructure.

Human Capital

As of December 31, 2020, the Company and its subsidiaries had approximately 2,000 employees, including approximately 1,500 employees at the Company’s unconsolidated mining operations, of which 261 are represented by a union at Bisti. NACCO believes it has good relations with both union and non-union employees.

NACCO believes its employees are critical to its success and invests in its employees by offering a competitive total rewards package that includes a combination of salaries and wages, health and wellness benefits, retirement benefits and educational benefits. The Company provides employee wages that are competitive and consistent with employee positions, skill levels, experience, knowledge and geographic location. The Company recognizes the sustainability of its culture and success is strengthened when employees are respected, motivated and engaged. The Company works to match employees with assignments to capitalize on the skills, talents and potential of each employee. The Company believes in hiring, engaging, developing and promoting people who are fully able to meet the demands of each position, regardless of race, color, religion, gender, sexual orientation, gender identity, national origin, age, veteran status or disability. Employee safety in the workplace is one of the Company’s core values. Hazards in the workplace are actively identified and management tracks incidents so remedial actions can be taken to improve workplace safety. The Company supports its local communities and is committed to helping them remain safe, healthy and resilient. The Company's past activities include corporate donations, volunteerism and education.

Available Information

The Company makes its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports available, free of charge, through its website, www.nacco.com, as soon as reasonably practicable after such material is electronically filed with, or furnished to, the Securities and Exchange Commission (“SEC”). The content of the Company's website is not incorporated by reference into this Form 10-K or in any other report or document filed with the SEC, and any reference to the Company's website is intended to be inactive textual references only.

Under Rule 12b-2 of the Exchange Act, the Company qualifies as a “smaller reporting company” because its public float as of the last business day of the Company’s most recently completed second quarter was less than $250 million. For as long as the Company remains a “smaller reporting company,” it may take advantage of certain exemptions from the SEC’s reporting requirements that are otherwise applicable to public companies that are not smaller reporting companies.

SEC Industry Guide 7 Information

The following map shows the Coal Mining segment's locations:

The location, mine type, reserve data, coal quality characteristics, sales tonnage and contract expiration date for the Coal Mining segment were as follows:

COAL MINING OPERATIONS ON AN “AS RECEIVED” BASIS

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2020 | | 2019 | | | |

| | | Proven and Probable Reserves (a)(b) | | | | | | | | | | | | |

| | | Committed

Under

Contract | | Uncommitted | | Total | | Tons

Delivered

(Millions) | | Owned

Reserves

(%) | | Leased

Reserves

(%) | | Total

Committed

and

Uncommitted

(Millions of

Tons) | | Tons

Delivered

(Millions) | | Contract

Expires |

| Mine/Reserve | Type of Mine | (Millions of Tons) | | | | | | |

| Unconsolidated Mines | | | | | | | | | | | | | | | | | | | |

Freedom Mine (c)-

The Coteau Properties Company | Surface Lignite | 438.0 | | | — | | | 438.0 | | | 12.6 | | | 3 | % | | 97 | % | | 432.8 | | | 13.5 | | | 2022 | (d) |

Falkirk Mine (c)(e)-

The Falkirk Mining Company | Surface Lignite | 12.0 | | | 358.6 | | | 370.6 | | | 7.2 | | | 1 | % | | 99 | % | | 375.7 | | | 7.4 | | | 2045 | (e) |

South Hallsville No. 1 Mine (c)(f)(g)-

The Sabine Mining Company | Surface Lignite | 3.4 | | | 97.3 | | | 100.7 | | | 1.9 | | | (f)(g) | | (f)(g) | | 102.6 | | | 2.6 | | | 2035 | (g) |

Five Forks Mine (c)(f)-

Demery Resources Company, LLC | Surface Lignite | 4.9 | | | — | | | 4.9 | | | 0.2 | | | (f) | | (f) | | 4.9 | | | 0.1 | | | 2030 | |

Marshall Mine (c)(f)(h)-

Caddo Creek Resources Company, LLC | Surface Lignite | (h) | | (h) | | (h) | | 0.1 | | | (f)(h) | | (f)(h) | | 19.2 | | 0.2 | | | (h) | |

Eagle Pass Mine (c)(f)(i)-

Camino Real Fuels, LLC | Surface

Bituminous | (i) | | (i) | | (i) | | 0.3 | | | (f)(i) | | (f)(i) | | 15.6 | | 1.5 | | | (i) | |

Coyote Creek Mine (c)-

Coyote Creek Mining Company, LLC | Surface Lignite | 72.4 | | | — | | | 72.4 | | | 2.0 | | | 0 | % | | 100 | % | | 69.6 | | | 1.7 | | | 2040 | |

| Navajo Mine (c)(j)- Bisti Fuels Company | Surface

Sub-bituminous | (j) | | (j) | | (j) | | 4.2 | | | (j) | | (j) | | (j) | | 5.0 | | | 2031 | |

| Consolidated Mines | | | | | | | | | | | | | | | | | | | |

Red Hills Mine-

Mississippi Lignite Mining Company | Surface Lignite | 161.0 | | | 76.3 | | | 237.3 | | | 2.5 | | | 44 | % | | 56 | % | | 240.0 | | | 2.6 | | | 2032 | |

| Centennial Natural Resources | Surface Bituminous | 17.0 | | | — | | | 17.0 | | | — | | | 40 | % | | 60 | % | | 43.0 | | | — | | | (k) | |

| Total Developed | | 708.7 | | | 532.2 | | | 1,240.9 | | | 31.0 | | | | | | | 1,303.4 | | | 34.6 | | | | |

| Undeveloped Mines | | | | | | | | | | | | | | | | | | | |

| North Dakota | | — | | | 221.4 | | | 221.4 | | | — | | | | | 100 | % | | 243.9 | | | — | | | | |

| Texas | | — | | | 210.3 | | | 210.3 | | | — | | | | | 100 | % | | 222.5 | | | — | | | | |

| Eastern (l) | | — | | | 41.0 | | | 41.0 | | | — | | | | | 100 | % | | 41.0 | | | — | | | | |

| Mississippi | | — | | | 188.2 | | | 188.2 | | | — | | | | | 100 | % | | 188.2 | | | — | | | | |

| Total Undeveloped | | — | | | 660.9 | | | 660.9 | | | — | | | | | | | 695.6 | | | — | | | | |

| Total Developed/Undeveloped | | 708.7 | | | 1,193.1 | | | 1,901.8 | | | | | | | | | 1,999.0 | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | Average Coal Quality (As received) |

| Mine/Reserve | | Type of Mine | | Coal Formation or

Coal Seam(s) | | Average Seam

Thickness (feet) | | Average

Depth (feet) | | BTUs/lb | | Sulfur

(%) | | Ash

(%) | | Moisture (%) |

| Unconsolidated Mines | | | | | | | | | | | | | | | | |

Freedom Mine (c)-

The Coteau Properties Company | | Surface Lignite | | Beulah-Zap Seam | | 16 | | | 100 | | | 6,700 | | | 0.90 | % | | 9 | % | | 36 | % |

Falkirk Mine (c)-

The Falkirk Mining Company | | Surface Lignite | | Hagel A&B, Tavis

Creek, Kinneman Creek Seams | | 8 | | | 115 | | | 6,200 | | | 0.62 | % | | 11 | % | | 38 | % |

South Hallsville No. 1 Mine (c)(f)-

The Sabine Mining Company | | Surface Lignite | | Wilcox Formation | | 3 | | | 85 | | | 6,448 | | | 0.79 | % | | 18.2 | % | | 32 | % |

Five Forks Mine (c)(f)-

Demery Resources Company, LLC | | Surface Lignite | | Wilcox Formation I Seam | | 4.4 | | | 44 | | | 7,033 | | | 0.44 | % | | 7.8 | % | | 37 | % |

Marshall Mine (c)(f)(h)-

Caddo Creek Resources Company, LLC | | Surface Lignite | | (h) | | (h) | | (h) | | (h) | | (h) | | (h) | | (h) |

Eagle Pass Mine (c)(f)(i)-

Camino Real Fuels, LLC | | Surface Bituminous | | (i) | | (i) | | (i) | | (i) | | (i) | | (i) | | (i) |

Coyote Creek Mine (c)-

Coyote Creek Mining Company, LLC | | Surface Lignite | | Beulah-Zap Seam | | 10 | | | 95 | | | 6,900 | | | 0.93 | % | | 9 | % | | 35 | % |

| Navajo Mine (c)(j)- Bisti Fuels Company | | Surface

Sub-bituminous | | (j) | | (j) | | (j) | | (j) | | (j) | | (j) | | (j) |

| Consolidated Mines | | | | | | | | | | | | | | | | |

Red Hills Mine-

Mississippi Lignite Mining Company | | Surface Lignite | | C, D, E, F, G, H Seams | | 3.4 | | | 150 | | | 5,100 | | | 0.60 | % | | 15 | % | | 43 | % |

| Centennial Natural Resources | | Surface Bituminous | | Black Creek, New Castle, Mary Lee, Jefferson, American, Nickel Plate, Pratt Seams | | 1.75 | | | 178 | | | 13,226 | | | 2.00 | % | | 10 | % | | 4 | % |

| Undeveloped Mines | | | | | | | | | | | | | | | | |

| North Dakota | | — | | | Fort Union Formation | | 13 | | | 130 | | | 6,500 | | | 0.8 | % | | 8 | % | | 38 | % |

| Texas | | — | | | Wilcox Formation | | 5 | | | 120 | | | 6,800 | | | 1.0 | % | | 16 | % | | 30 | % |

| Eastern | | — | | | Freeport & Kittanning Seams | | 4 | | | 400 | | | 12,070 | | | 3.3 | % | | 12 | % | | 3 | % |

| Mississippi | | — | | | Wilcox Formation | | 5 | | | 130 | | | 5,200 | | | 0.6 | % | | 13 | % | | 44 | % |

(a)Committed and uncommitted tons represent in-place estimates. The projected extraction loss is approximately 10% of the proven and probable reserves, except with respect to the Eastern Undeveloped Mines, in which case the projected extraction loss is approximately 50% of the proven and probable reserves.

(b)The Company's reserve estimates are generally based on the entire drill hole database for each reserve, which was used to develop a geologic computer model using triangulation methods and inverse distance to the second power as an interpolator for NACCO's reserves. As such, all reserves are considered proven (measured) within the Company's reserve estimate. None of the Company's coal reserves have been reviewed by independent experts. The Company’s estimate of the economic viability of the proven and probable reserve estimates for tons committed to customers pursuant to long-term contracts are supported by existing long-term contracts to mine coal on behalf of customers and life-of-mine plans associated with those contracts. The contracts with each customer of the Unconsolidated Mines eliminate Company exposure to spot coal market price fluctuations. At the Unconsolidated Mines, compensation from each customer to the Company includes reimbursement of all mine operating costs plus a contractually-agreed fee based on the amount of coal delivered. Red Hills Mine - MLMC sells coal to its customer at a contractually agreed-upon price which adjusts monthly, primarily based on changes in the level of established indices which reflect general U.S. inflation rates. MLMC is the exclusive supplier of coal to its customer’s power plant under its contract that runs through 2032. The Company’s assessment of the economic viability of the mineral reserves associated with MLMC takes into account estimated customer demand, including the minimum annual take provision in the contract, as well as cost of production. The economic viability of the uncommitted reserves assumes coal would be mined in a mine-mouth operation that minimizes or eliminates transportation costs and under contract terms, which are similar to those contained in the Company’s existing long-term management fee contracts, or leased to other miners. The majority of the Company’s uncommitted reserves are located in close proximity to power generation or other facilities, which could allow a mine-mouth operation. Lessees of this coal generally would mine the coal if the coal sale price would exceed the lessee operating costs. As to coal mined and sold by lessees, the Company would receive a royalty based on a percentage of the sale price. See footnote (h) for coal reserves currently leased to others.

(c)The contracts for these mines require the customer to cover the cost of the ongoing replacement and upkeep of the plant and equipment of the mine.

(d)Although the term of the existing coal sales agreement terminates in 2027, the term may be extended for two additional periods of five years, or until 2037, at the option of the Company.

(e)On May 7, 2020, GRE, Falkirk Mine's customer, announced its intent to retire the Coal Creek Station power plant in the second half of 2022 and modify the Spiritwood Station power plant to be fueled by natural gas.

(f)These reserves are owned or controlled by customers. The Company conducts activities to extract these customer-owned and controlled reserves pursuant to long-term service contracts.

(g)On November 5, 2020, AEP, Sabine Mine's customer, announced its intent to retire the Pirkey Plant in 2023 in order to comply with the U.S. Environmental Protection Agency’s Coal Combustion Residuals rule.

(h)On September 30, 2020, a division of Cabot Corporation, Marshall Mine's customer, entered into an agreement for the sale of the Marshall Mine to a subsidiary of AES. AES announced its intent to close the Marshall Mine. Caddo Creek entered into a contract with a subsidiary of AES to perform the required mine reclamation.

(i)The contract mining agreement between Camino Real and its customer, DRCP, terminated effective July 1, 2020 and resulted in the closure of Camino Real's Eagle Pass Mine.

(j)These reserves are owned or controlled by Bisti's customer and it controls proven and probable reserve data. Bisti’s customer declined to allow us to include the proven and probable reserve data in this Form 10-K. The Company conducts activities to extract these customer-owned and controlled reserves pursuant to a long-term service contract.

(k)Centennial ceased active mining operations at the end of 2015.

(l)The proven and probable reserves included in the table do not include coal that is leased to others. The Company had 69.0 million tons and 70.0 million tons in 2020 and 2019, respectively, of Eastern Undeveloped Mines with leased coal committed under contract.

Unconsolidated Mines

Freedom Mine — The Coteau Properties Company

The Freedom Mine generally produces between 12.5 million and 13.5 million tons of lignite coal annually. The mine started delivering coal in 1983. All production from the mine is delivered to Dakota Coal Company, a wholly owned subsidiary of Basin Electric. Dakota Coal Company then sells the coal to the Synfuels Plant, Antelope Valley Station and Leland Olds Station, all of which are operated by affiliates of Basin Electric. The Synfuels Plant is a coal gasification plant that manufactures synthetic natural gas and produces fertilizers, solvents, phenol, carbon dioxide, and other chemical products for sale.

On November 5, 2020, Basin Electric informed its employees and Coteau that it is considering changes that may result in modifications to its Synfuels Plant that could potentially reduce or eliminate coal requirements at the Synfuels Plant beginning in 2026. Basin Electric indicated that if it decides to proceed with any changes that could reduce or eliminate the use of coal, the feedstock change is not expected to occur before 2026. As a result, coal deliveries to the Synfuels Plant are expected to continue until at least 2026.

The Freedom Mine, operated by Coteau, is located approximately 90 miles northwest of Bismarck, North Dakota. The main entrance to the Freedom Mine is accessed by means of a paved road and is located on County Road 15. Coteau holds 381 leases granting the right to mine approximately 34,715 acres of coal interests and the right to utilize approximately 23,575 acres of surface interests. In addition, Coteau owns in fee 33,525 acres of surface interests and 4,107 acres of coal interests. Substantially all of the leases held by Coteau were acquired in the early 1970s and have been replaced with new leases or have lease terms for a period sufficient to meet Coteau’s contractual production requirements.

The reserves are located in Mercer County, North Dakota, starting approximately two miles north of Beulah, North Dakota. The center of the basin is located near the city of Williston, North Dakota, approximately 100 miles northwest of the Freedom Mine. The economically mineable coal in the reserve occurs in the Sentinel Butte Formation, and is overlain by the Coleharbor Formation. The Coleharbor Formation unconformably overlies the Sentinel Butte Formation. It includes all of the unconsolidated sediments resulting from deposition during glacial and interglacial periods. Lithologic types include gravel, sand, silt, clay and till. The modified glacial channels are in-filled with gravels, sands, silts and clays overlain by till. The coarser gravel and sand beds are generally limited to near the bottom of the channel fill. The general stratigraphic sequence in the upland portions of the reserve area consists of till, silty sands and clayey silts.

Falkirk Mine — The Falkirk Mining Company

The Falkirk Mine started delivering coal in 1978 primarily for the Coal Creek Station, an electric power generating station owned by GRE. In 2014, Falkirk began delivering coal to Spiritwood Station, another electric power generating station owned by GRE.

On May 7, 2020, GRE announced its intent to retire the Coal Creek Station power plant in the second half of 2022 and modify the Spiritwood Station power plant to be fueled by natural gas. The Falkirk Mine delivered 7.2 million and 7.4 million tons of lignite coal, primarily for the Coal Creek Station, during 2020 and 2019, respectively. The terms of the contract between the Company and GRE specify that GRE is responsible for all costs related to mine closure, including but not limited to, final mine reclamation costs, post-retirement medical benefits and pension costs with respect to Falkirk employees.

The Falkirk Mine, operated by Falkirk, is located approximately 50 miles north of Bismarck, North Dakota on a paved access road off U.S. Highway 83. Falkirk holds 311 leases granting the right to mine approximately 43,084 acres of coal interests and the right to utilize approximately 24,061 acres of surface interests. In addition, Falkirk owns in fee 41,275 acres of surface interests and 1,789 acres of coal interests. Substantially all of the leases held by Falkirk were acquired in the early 1970s with initial terms that have been further extended by the continuation of mining operations.

The reserves are located in McLean County, North Dakota, from approximately nine miles northwest of the town of Washburn, North Dakota to four miles north of the town of Underwood, North Dakota. Structurally, the area is located on an intercratonic basin containing a thick sequence of sedimentary rocks. The economically mineable coals in the reserve occur in the Sentinel Butte Formation and the Bullion Creek Formation and are unconformably overlain by the Coleharbor Formation. The Sentinel Butte Formation conformably overlies the Bullion Creek Formation. The general stratigraphic sequence in the upland portions of the reserve area (Sentinel Butte Formation) consists of till, silty sands and clayey silts, main hagel lignite bed, silty clay, lower lignite of the hagel lignite interval and silty clays. Beneath the Tavis Creek, there is a repeating sequence of silty to sand clays with generally thin lignite beds.

South Hallsville No. 1 Mine — The Sabine Mining Company

The South Hallsville No. 1 Mine started delivering coal in 1985. All production from the mine is delivered to Southwestern Electric Power Company's ("SWEPCO") Henry W. Pirkey Plant (the "Pirkey Plant"). SWEPCO is an American Electric Power (“AEP”) company.