UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM

| | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

| For the fiscal year ended: |

| | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

| Commission file number: |

|

| “COAL KEEPS YOUR LIGHTS ON” |

| “COAL KEEPS YOUR LIGHTS ON” |

|

| HALLADOR ENERGY COMPANY (www.halladorenergy.com) |

|

| | |

| (State of incorporation) | (IRS Employer Identification No.) |

|

|

|

| | |

| (Address of principal executive offices) | (Zip Code) |

Issuer’s telephone number:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

| |

| |

| |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15 (d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities and Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See the definitions of "larger accelerated filer," "accelerated filer", "smaller reporting company," and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☐ Large accelerated filer | ☐ Accelerated filer |

| ☑ | |

|

| |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

The aggregate market value of the common stock held by non-affiliates (public float) on June 30, 2020 was $

As of March 4, 2021, we had

FORWARD-LOOKING STATEMENTS

Certain statements and information in this Annual Report on Form 10-K may constitute “forward-looking statements.” These statements are based on our beliefs as well as assumptions made by, and information currently available to us. When used in this document, the words “anticipate,” “believe,” “continue,” “estimate,” “expect,” “forecast,” “may,” “project,” “will,” and similar expressions identify forward-looking statements. Without limiting the foregoing, all statements relating to our future outlook, anticipated capital expenditures, future cash flows and borrowings and sources of funding are forward-looking statements. These statements reflect our current views with respect to future events and are subject to numerous assumptions that we believe are open to a wide range of uncertainties and business risks, and actual results may differ materially from those discussed in these statements. Among the factors that could cause actual results to differ from those in the forward-looking statements are:

| ● | the severity, magnitude and duration of the COVID-19 pandemic, including impacts of the pandemic and of businesses' and governments' responses to the pandemic on our operations and personnel, and on demand for coal, the financial condition of our customers and suppliers, available liquidity and capital sources and broader economic disruptions; | |

| ● | changes in macroeconomic and market conditions and market volatility arising from the COVID-19 pandemic, including coal, oil, natural gas and natural gas liquids prices, and the impact of such changes and volatility on our financial position; | |

| ● | the effectiveness or lack of effectiveness in distributed vaccines to reduce the impact of COVID-19; | |

| ● |

changes in competition in coal markets and our ability to respond to such changes; |

|

| ● | changes in coal prices, demand, and availability which could affect our operating results and cash flows; | |

| ● | risks associated with the expansion of our operations and properties; | |

| ● | legislation, regulations, and court decisions and interpretations thereof, including those relating to the environment and the release of greenhouse gases, mining, miner health and safety, and health care; | |

| ● | deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; | |

| ● | dependence on significant customer contracts, including renewing customer contracts upon expiration of existing contracts; | |

| ● | changing global economic conditions or in industries in which our customers operate; | |

| ● | recent action and the possibility of future action on trade made by the United States and foreign governments; | |

| ● | the effect of changes in taxes or tariffs and other trade measures; | |

| ● | liquidity constraints, including those resulting from any future unavailability of financing; | |

| ● | customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; | |

| ● | customer delays, failure to take coal under contracts or defaults in making payments; | |

| ● | adjustments made in price, volume or terms to existing coal supply agreements; | |

| ● | changes in oil & gas prices, which could, among other things, affect our investments in oil & gas mineral interests; | |

| ● | our productivity levels and margins earned on our coal sales; | |

| ● | changes in raw material costs; | |

| ● | changes in the availability of skilled labor; | |

| ● | our ability to maintain satisfactory relations with our employees; | |

| ● | increases in labor costs, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; | |

| ● | increases in transportation costs and risk of transportation delays or interruptions; | |

| ● | operational interruptions due to geologic, permitting, labor, weather-related or other factors; | |

| ● | risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; | |

| ● | results of litigation, including claims not yet asserted; | |

| ● | difficulty maintaining our surety bonds for mine reclamation; | |

| ● | decline in or change in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion and the cost and perceived benefits of other sources of electricity, such as natural gas, nuclear energy, and renewable fuels; | |

| ● | difficulty in making accurate assumptions and projections regarding post-mine reclamation; | |

| ● | uncertainties in estimating and replacing our coal reserves; | |

| ● | the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; | |

| ● | difficulty obtaining commercial property insurance; | |

| ● | evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing-attacks, ransomware, malware, social engineering, physical breaches or other actions; |

| ● |

difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control; |

|

| ● |

other factors, including those discussed in “Item 1A. Risk Factors”; and |

|

| ● | investors' and other stakeholders' increasing attention to environmental, social and governance ("ESG") matters. |

If one or more of these or other risks or uncertainties materialize, or should underlying assumptions prove incorrect, our actual results may differ materially from those described in any forward-looking statement. When considering forward-looking statements, you should also keep in mind the risk factors described in “Item 1A. Risk Factors” below. The risk factors could also cause our actual results to differ materially from those contained in any forward-looking statement. We disclaim any obligation to update the above list or to announce publicly the result of any revisions to any of the forward-looking statements to reflect future events or developments, unless required by law.

You should consider the information above when reading any forward-looking statements contained in this Annual Report on Form 10-K; other reports filed by us with the U.S. Securities and Exchange Commission (“SEC”); our press releases; our website http://www.halladorenergy.com and written or oral statements made by us or any of our officers or other authorized persons acting on our behalf.

ITEM 1. BUSINESS.

See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” for a discussion of our business.

Regulation and Laws

The coal mining industry is subject to extensive regulation by federal, state and local authorities on matters such as:

| ● |

employee health and safety; |

|

| ● |

mine permits and other licensing requirements; |

|

| ● | air quality standards; | |

| ● | water quality standards; | |

| ● | storage of petroleum products and substances that are regarded as hazardous under applicable laws or that, if spilled, could reach waterways or wetlands; | |

| ● | plant and wildlife protection that could limit or prohibit mining or exploration; | |

| ● | restricting the types, quantities and concentration of materials that can be released into the environment in the performance of mining or exploration and production activities; | |

| ● | discharge of materials; | |

| ● | storage and handling of explosives; | |

| ● | wetlands protection; | |

| ● | surface subsidence from underground mining; and | |

| ● | the effects, if any, that mining has on groundwater quality and availability. | |

Failure to comply with environmental laws and regulations may result in the assessment of administrative, civil and criminal sanctions, including monetary penalties, the imposition of strict, joint and several liability, investigatory and remedial obligations and the issuance of injunctions limiting or prohibiting some or all of the operations on our properties. The regulatory burden on fossil fuel industries increases the cost of doing business and consequently affects profitability. The trend in environmental regulation has been to place more restrictions and limitations on activities that may affect the environment, and thus, any changes in environmental laws and regulations or re-interpretation of enforcement policies that result in more stringent and costly obligations could increase our or our mineral interest operators’ costs and adversely affect our performance. In addition, the utility industry is subject to extensive regulation regarding the environmental impact of its power generation activities, which has adversely affected demand for coal. It is possible that new legislation or regulations may be adopted, or that existing laws or regulations may be interpreted differently or more stringently enforced, any of which could have a significant impact on our mining operations or our customers’ ability to use coal. For more information, please see risk factors described in “Item 1A. Risk Factors” below.

We are committed to conducting mining operations in compliance with applicable federal, state and local laws and regulations. However, because of the extensive and detailed nature of these regulatory requirements, particularly the regulatory system of the Mine Safety and Health Administration (“MSHA”) where citations can be issued without regard to fault, and many of the standards include subjective elements, it is not reasonable to expect any coal mining company to be free of citations. When we receive a citation, we attempt to remediate any identified condition immediately. While we have not quantified all of the costs of compliance with applicable federal and state laws and associated regulations, those costs have been and are expected to continue to be significant. Compliance with these laws and regulations has substantially increased the cost of coal mining for domestic coal producers.

Capital expenditures for environmental matters have not been material in recent years. We have accrued for the present value of the estimated cost of asset retirement obligations and mine closings, including the cost of treating mine water discharge, when necessary. The accruals for asset retirement obligations and mine closing costs are based upon permit requirements and the costs and timing of asset retirement obligations and mine closing procedures. Although management believes it has made adequate provisions for all expected reclamation and other costs associated with mine closures, future operating results would be adversely affected if these accruals were insufficient.

Mining Permits and Approvals

Numerous governmental permits or approvals are required for mining operations. Applications for permits require extensive engineering and data analysis and presentation and must address a variety of environmental, health and safety matters associated with a proposed mining operation. These matters include the manner and sequencing of coal extraction, the storage, use and disposal of waste and other substances and impacts on the environment, the construction of water containment areas, and reclamation of the area after coal extraction. Meeting all requirements imposed by any of these authorities may be costly and may delay or prevent commencement or continuation of mining operations.

The permitting process for certain mining operations can extend over several years and can be subject to administrative and judicial challenge, including by the public. Some required mining permits are becoming increasingly difficult to obtain in a timely manner, or at all. We cannot assure you that we will not experience difficulty or delays in obtaining mining permits in the future or that a current permit will not be revoked.

We are required to post bonds to secure performance under our permits. Under some circumstances, substantial fines and penalties, including revocation of mining permits, may be imposed under the laws and regulations described above. Monetary sanctions and, in severe circumstances, criminal sanctions may be imposed for failure to comply with these laws and regulations. Regulations also provide that a mining permit can be refused or revoked if the permit applicant or permittee owns or controls, directly or indirectly through other entities, mining operations that have outstanding environmental violations. Although like other coal companies, we have been cited for violations in the ordinary course of our business, we have never had a permit suspended or revoked because of any violation, and the penalties assessed for these violations have not been material.

Mine Health and Safety Laws

The Federal Mine Safety and Health Act of 1977 (“FMSHA”), and regulations adopted pursuant thereto, imposes extensive and detailed safety and health standards on numerous aspects of mining operations, including training of mine personnel, mining procedures, blasting, the equipment used in mining operations, and numerous other matters. MSHA monitors and rigorously enforces compliance with these federal laws and regulations. In addition, the states where we operate have state programs for mine safety and health regulation and enforcement. Federal and state safety and health regulations affecting the coal mining industry are perhaps the most comprehensive and rigorous system in the U.S. for protection of employee safety and have a significant effect on our operating costs. Although many of the requirements primarily impact underground mining, our competitors in all of the areas in which we operate are subject to the same laws and regulations.

FMSHA has been construed as authorizing MSHA to issue citations and orders pursuant to the legal doctrine of strict liability, or liability without fault, and FMSHA requires the imposition of a civil penalty for each cited violation. Negligence and gravity assessments and other factors can result in the issuance of various types of orders, including orders requiring withdrawal from the mine or the affected area, and some orders can also result in the imposition of civil penalties. FMSHA also contains criminal liability provisions. For example, criminal liability may be imposed upon corporate operators who knowingly and willfully authorize, order or carry out violations of the FMSHA, or its mandatory health and safety standards.

The Federal Mine Improvement and New Emergency Response Act of 2006 (“MINER Act”) significantly amended the FMSHA, imposing more extensive and stringent compliance standards, increasing criminal penalties and establishing a maximum civil penalty for non-compliance, and expanding the scope of federal oversight, inspection, and enforcement activities. Following the passage of the MINER Act, MSHA has issued new or more stringent rules and policies on a variety of topics, including:

| ● |

sealing off abandoned areas of underground coal mines; |

|

| ● |

mine safety equipment, training, and emergency reporting requirements; |

|

| ● | substantially increased civil penalties for regulatory violations; | |

| ● | training and availability of mine rescue teams; | |

| ● | underground “refuge alternatives” capable of sustaining trapped miners in the event of an emergency; | |

| ● | flame-resistant conveyor belts, fire prevention and detection, and use of air from the belt entry; and | |

| ● | post-accident two-way communications and electronic tracking systems. |

MSHA continues to interpret and implement various provisions of the MINER Act, along with introducing new proposed regulations and standards.

In 2014, MSHA began implementation of a finalized new regulation titled “Lowering Miner’s Exposure to Respirable Coal Mine Dust, Including Continuous Personal Dust Monitors.” The final rule implemented a reduction in the allowable respirable coal mine dust exposure limits, requires the use of sampling data taken from a single sample rather than an average of samples and increases oversight by MSHA regarding coal mine dust and ventilation issues at each mine, including the approval process for ventilation plans at each mine, all of which increase mining costs. The second phase of the rule began in February 2016 and requires additional sampling for designated and other occupations using the new continuous personal dust monitor technology, which provides real-time dust exposure information to the miner. Phase three of the rule began in August 2016 and resulted in lowering the current respirable dust level of 2.0 milligrams per cubic meter to 1.5 milligrams per cubic meter of air. Compliance with these rules can result in increased costs on our operations, including, but not limited to, the purchasing of new equipment and the hiring of additional personnel to assist with monitoring, reporting, and recordkeeping obligations. MSHA has published a request for information regarding engineering controls and best practices to lower miners’ exposure to respirable coal mine dust, which is currently set to close on July 9, 2022. It is uncertain whether MSHA will present additional proposed rules, or revisions to the final rule, following the closing of the comment period for the current request for information.

MSHA has also published, and may continue to publish, various proposed rules or requests for information, which may result in additional rulemakings. For example, in June 2016, MSHA published a request for information on Exposure of Underground Miners to Diesel Exhaust. Following a comment period that closed in November 2016, MSHA received requests for MSHA and the National Institute for Occupational Safety and Health to hold a Diesel Exhaust Partnership to address the issues covered by MSHA's request for information. The comment period for the request for information closed in September 2020. It is uncertain whether MSHA will present a proposed rule pertaining to exposure of underground miners to diesel exhaust, after completing its evaluation of the comments received.

Separately, in November 2020, MSHA published a proposed rule to revise Testing, Evaluation, and Approval of Electric Motor-Driven Mine Equipment and Accessories within underground mining environments. The comment period for the proposed rule closed in December 2020. It is uncertain whether MSHA will present a final rule addressing this issue.

Subsequent to the passage of the MINER Act, Illinois, Kentucky, Pennsylvania, and West Virginia have enacted legislation addressing issues such as mine safety and accident reporting, increased civil and criminal penalties, and increased inspections and oversight. Additionally, state administrative agencies can promulgate administrative rules and regulations affecting our operations. Other states may pass similar legislation or administrative regulations in the future.

Some of the costs of complying with existing regulations and implementing new safety and health regulations may be passed on to our customers. Although we have not quantified the full impact, implementing and complying with these new federal and state safety laws and regulations have had, and are expected to continue to have, an adverse impact on our results of operations and financial position.

Black Lung Benefits Act

The Black Lung Benefits Act of 1977 and the Black Lung Benefits Reform Act of 1977, as amended in 1981 (“BLBA”) requires businesses that conduct current mining operations to make payments of black lung benefits to current and former coal miners with black lung disease and to some survivors of a miner who dies from this disease. The BLBA levied a tax on coal sales of $1.10 per ton for underground-mined coal and $0.55 per ton for surface-mined coal, but not to exceed 4.4% of the applicable sales price in order to compensate miners who are totally disabled due to black lung disease and some survivors of miners who died from this disease, and who were last employed as miners prior to 1970 or subsequently where no responsible coal mine operator has been identified for claims. In addition, the BLBA provides that some claims for which coal operators had previously been responsible are or will become obligations of the government trust funded by the tax. The Revenue Act of 1987 extended the termination date of this tax from January 1, 1996, to the earlier of January 1, 2014, or the date on which the government trust becomes solvent. The Emergency Economic Stabilization Act of 2008 extended these rates through December 31, 2018. On January 1, 2019, the excise tax rates reverted to their original 1977 statutory levels of $0.50 per ton for underground-mined coal and $0.25 per ton for surface mined coal, but not to exceed 2% of the applicable sales price. In December 2019, the excise tax rates were increased to their 2018 levels and that rate increase was set to expire on December 31, 2020. However, in December 2020, the excise tax rate increase was extended another year, through December 31, 2021.

Workers' Compensation and Black Lung

We provide income replacement and medical treatment for work-related traumatic injury claims as required by applicable state laws. Workers’ compensation laws also compensate survivors of workers who suffer employment-related deaths. We generally self-insure this potential expense using our actuary estimates of the cost of present and future claims. In addition, coal mining companies are subject to federal legislation and various state statutes for the payment of medical and disability benefits to eligible recipients related to coal worker’s pneumoconiosis, or black lung. We also provide for these claims through self-insurance programs. Our actuarial calculations are based on numerous assumptions including disability incidence, medical costs, mortality, death benefits, dependents and discount rates.

The revised BLBA regulations took effect in January 2001, relaxing the stringent award criteria established under previous regulations and thus potentially allowing new federal claims to be awarded and allowing previously denied claimants to re-file under the revised criteria. These regulations may also increase black lung-related medical costs by broadening the scope of conditions for which medical costs are reimbursable and increase legal costs by shifting more of the burden of proof to the employer.

The Patient Protection and Affordable Care Act enacted in 2010 includes significant changes to the federal black lung program retroactive to 2005, including an automatic survivor benefit paid upon the death of a miner with an awarded black lung claim and establishes a rebuttable presumption with regard to pneumoconiosis among miners with 15 or more years of coal mine employment that are totally disabled by a respiratory condition. These changes could have a material impact on our costs expended in association with the federal black lung program.

Surface Mining Control and Reclamation Act

The Federal Surface Mining Control and Reclamation Act of 1977 (“SMCRA”) and similar state statutes establish operational, reclamation and closure standards for all aspects of surface mining as well as many aspects of underground mining. Currently, ~96% of our production capacity involves underground room and pillar mining (no surface subsidence), and ~4% involves surface mining. We do not engage in either mountain top removal or long-wall mining. SMCRA nevertheless requires that comprehensive environmental protection and reclamation standards be met during the course of and upon completion of our mining activities.

SMCRA and similar state statutes require, among other things, that surface disturbance be restored in accordance with specified standards and approved reclamation plans. SMCRA requires us to restore affected surface areas to approximate the original contours as contemporaneously as practicable. Federal law and some states impose on mine operators the responsibility for replacing certain water supplies damaged by mining operations and repairing or compensating for damage to certain structures occurring on the surface as a result of mine subsidence, a consequence of longwall mining and possibly other mining operations. We believe we are in compliance in all material respects with applicable regulations relating to reclamation.

In addition, the Abandoned Mine Lands Program, which is part of SMCRA, imposes a reclamation fee on all current mining operations, the proceeds of which are used to restore mines closed before 1977. The fee for surface-mined and underground-mined coal is $0.28 per ton and $0.12 per ton, respectively. The fee is currently scheduled to be in effect until September 30, 2021 and requires Congressional action to reauthorize. We have accrued the estimated costs of reclamation and mine closing, including the cost of treating mine water discharge when necessary. In addition, states from time to time have increased and may continue to increase their fees and taxes to fund reclamation or orphaned mine sites and acid mine drainage control on a statewide basis.

Under SMCRA, responsibility for unabated violations, unpaid civil penalties and unpaid reclamation fees of independent contract mine operators and other third parties can be imputed to other companies that are deemed, according to the regulations, to have “owned” or “controlled” the third-party violator. Sanctions against the “owner” or “controller” are quite severe and can include being blocked from receiving new permits and having any permits revoked that were issued after the time of the violations or after the time civil penalties or reclamation fees became due. We are not aware of any currently pending or asserted claims against us relating to the “ownership” or “control” theories discussed above. However, we cannot assure you that such claims will not be asserted in the future.

In April 2015, the United States Environmental Protection Agency ("EPA") finalized rules on coal combustion residuals ("CCRs"); however, the final rule does not address the placement of CCRs in minefills or non-minefill uses of CCRs at coal mine sites. The Federal Office of Surface Mining ("OSM ") has announced their intention to release a proposed rule to regulate placement and use of CCRs at coal mine sites, but to date, no further action has been taken. These actions by OSM potentially could result in additional delays and costs associated with obtaining permits, prohibitions or restrictions relating to mining activities, and additional enforcement actions.

Bonding Requirements

Federal and state laws require bonds to secure our obligations to reclaim lands used for mining, and to satisfy other miscellaneous obligations. These bonds are typically renewable on a yearly basis. It has become increasingly difficult for us and our competitors to secure new surety bonds without posting collateral and in some cases it is unclear what level of collateral will be required.

In addition to the greenhouse gas (“GHG”) issues discussed below, the air emissions programs that may affect our operations, directly or indirectly, include, but are not limited to, the following:

| ● |

The EPA’s Acid Rain Program, provided in Title IV of the CAA, regulates emissions of sulfur dioxide from electric generating facilities. Sulfur dioxide is a by-product of coal combustion. Affected facilities purchase or are otherwise allocated sulfur dioxide emissions allowances, which must be surrendered annually in an amount equal to a facility’s sulfur dioxide emissions in that year. Affected facilities may sell or trade excess allowances to other facilities that require additional allowances to offset their sulfur dioxide emissions. In addition to purchasing or trading for additional sulfur dioxide allowances, affected power facilities can satisfy the requirements of the EPA’s Acid Rain Program by switching to lower-sulfur fuels, installing pollution control devices such as flue gas desulfurization systems, or “scrubbers,” or by reducing electricity generating levels. These requirements would not be supplanted by a replacement rule for the Clean Air Interstate Rule (“CAIR”), discussed below.

|

|

| ● |

The CAIR calls for power plants in 28 states and Washington, D.C. to reduce emission levels of sulfur dioxide and nitrogen oxide pursuant to a cap-and-trade program similar to the system in effect for acid rain. In June 2011, the EPA finalized the Cross-State Air Pollution Rule (“CSAPR”), a replacement rule for CAIR, which would have required 28 states in the Midwest and eastern seaboard to reduce power plant emissions that cross state lines and contribute to ozone and/or fine particle pollution in other states. CSAPR has become increasingly irrelevant with continuing coal plant retirements making the nitrogen oxide ozone budget less stringent and lowering emission allowance prices to levels closer to average operating cost for many of our customers. The full impact of CSAPR are unknown at the present time due to the implementation of Mercury and Air Toxic Standards ("MATS"), discussed below, and the impact of the continuing coal plant retirements.

|

| ● |

In February 2012, the EPA adopted the MATS, which regulates the emission of mercury and other metals, fine particulates, and acid gases such as hydrogen chloride from coal and oil-fired power plants. In March 2013, the EPA finalized a reconsideration of the MATS rule as it pertains to new power plants, principally adjusting emissions limits to levels attainable by existing control technologies. In subsequent litigation, the U.S. Supreme Court struck down the MATS rule based on the EPA’s failure to take costs into consideration. The D.C. Circuit Court allowed the current rule to stay in place until the EPA issued a new finding. In April 2016, the EPA issued a final supplemental finding upholding the rule and concluding that a cost analysis supports the MATS rule. In April 2017, the D.C Circuit Court of Appeals granted the EPA’s request to cancel oral arguments and ordered the case held in abeyance for an EPA review of the supplemental finding. In December 2018, the EPA issued a proposed Supplemental Cost Finding, as well as the CAA required "risk and technology review." In May 2020, EPA issued a final rule that reverses the Agency's prior determination from 2000 and 2016 that it was "appropriate and necessary" to regulate hazardous air pollutants ("HAP") from coal-fueled Electric Generating Units ("EGUs") under the MATS rule. Notwithstanding the invalidation of this threshold regulatory determination, the final rule leaves in place all of the HAP emission control requirements imposed by the MATS rule based on the conclusion that the EGU source category cannot meet the statute's stringent requirements for delisting a source category from HAP regulation. Many electric generators have already announced retirements due to the MATS rule. Although various issues surrounding the MATS rule remain subject to litigation in the D.C. Circuit, the MATS rule has forced generators to make capital investments to retrofit power plants and could lead to additional premature retirements of older coal-fired generating units. The announced and possible additional retirements are likely to reduce the demand for coal. Apart from MATS, several states have enacted or proposed regulations requiring reductions in mercury emissions from coal-fired power plants, and federal legislation to reduce mercury emissions from power plants has been proposed. Regulation of mercury emissions by the EPA, states, or Congress may decrease the future demand for coal. We continue to evaluate the possible scenarios associated with CSAPR and MATS and the effects they may have on our business and our results of operations, financial condition or cash flows. |

| ● | The EPA is required by the CAA to periodically re-evaluate the available health effects information to determine whether the National Ambient Air Quality Standards (“NAAQS”) should be revised. Pursuant to this process, the EPA has adopted more stringent NAAQS for fine particulate matter (“PM”), ozone, nitrogen oxide, and sulfur dioxide. As a result, some states will be required to amend their existing SIPs to attain and maintain compliance with the new air quality standards and other states will be required to develop new SIPs for areas that were previously in “attainment” but do not attain the new standards. In addition, under the revised ozone NAAQS, significant additional emissions control expenditures may be required at coal-fired power plants. In March 2019, the EPA published a final rule that retained the current primary NAAQS for sulfur oxide. In December 2020, EPA published a final rule to retain the current NAAQS for both PM and ozone; however, various entities have filed litigation against one or both of these rulemakings, and the NAAQS may be subject to revision under the Biden Administration. New standards may impose additional emissions control requirements on new and expanded coal-fired power plants and industrial boilers. Because coal mining operations and coal-fired electric generating facilities emit particulate matter and sulfur dioxide, our mining operations and our customers could be affected when the new standards are implemented by the applicable states, and developments might indirectly reduce the demand for coal.

|

| ● | The EPA’s regional haze program is designed to protect and improve visibility at and around national parks, national wilderness areas, and international parks. Under the program, states are required to develop SIPs to improve visibility. Typically, these plans call for reductions in sulfur dioxide and nitrogen oxide emissions from coal-fueled electric plants. In prior cases, the EPA has decided to negate the SIPs and impose stringent requirements through FIPs. The regional haze program, including particularly the EPA’s FIPs, and any future regulations may restrict the construction of new coal-fired power plants whose operation may impair visibility at and around federally protected areas and may require some existing coal-fired power plants to install additional control measures designed to limit haze-causing emissions. These requirements could limit the demand for coal in some locations. In September 2018, the EPA issued a memorandum that detailed plans to assist states as they develop their SIPs.

|

|

| ● | The EPA’s new source review (“NSR”) program under the CAA in certain circumstances requires existing coal-fired power plants, when modifications to those plants significantly increase emissions, to install more stringent air emissions control equipment. The Department of Justice, on behalf of the EPA, has filed lawsuits against a number of coal-fired electric generating facilities alleging violations of the NSR program. The EPA has alleged that certain modifications have been made to these facilities without first obtaining certain permits issued. |

GHG Emissions

Combustion of fossil fuels, such as the coal we produce, results in the emission of GHGs, such as carbon dioxide and methane. Combustion of fuel for mining equipment used in coal production also emits GHGs. Future regulation of GHG emissions in the U.S. could occur pursuant to future U.S. treaty commitments, new domestic legislation or regulation by the EPA. Although no comprehensive climate change regulation has been adopted at the federal level in the United States, President Biden has announced that climate change will be a focus of his administration. For example, in January 2021, President Biden issued an executive order that commits to substantial action on climate change, calling for, among other things, the increased use of zero-emissions vehicles by the federal government, the elimination of subsidies provided to the fossil-fuel industry, a doubling of electricity generated by offshore wind by 2030, and increased emphasis on climate-related risks across governmental agencies and economic sectors. Internationally, the Paris Agreement requires member states to submit non-binding, individually-determined emissions reduction targets. These commitments could further reduce demand and prices for fossil fuels. Although the United States had withdrawn from the Paris Agreement, President Biden has signed executive orders recommitting the United States to the agreement and calling for the federal government to begin formulating the United States’ nationally determined emissions reduction targets under the agreement. However, the impact of these orders, and the terms of any legislation or regulation to implement the United States’ commitment under the Paris Agreement, remain unclear at this time. Moreover, many states, regions, and governmental bodies have adopted GHG initiatives and have or are considering the imposition of fees or taxes based on the emission of GHGs by certain facilities, including coal-fired electric generating facilities. Others have announced their intent to increase the use of renewable energy sources, displacing coal and other fossil fuels. Depending on the particular regulatory program that may be enacted, at either the federal or state level, the demand for coal could be negatively impacted, which would have an adverse effect on our operations.

Even in the absence of new federal legislation, the EPA has begun to regulate GHG emissions under the CAA based on the U.S. Supreme Court’s 2007 decision that the EPA has authority to regulate GHG emissions. Although the U.S. Supreme Court’s holding did not expressly involve the EPA’s authority to regulate GHG emissions from stationary sources, such as coal-fueled power plants, the EPA has determined on its own that it has the authority to regulate GHG emissions from power plants and issued a final rule which found that GHG emissions, including carbon dioxide and methane, endanger both the public health and welfare.

In August 2015, the EPA issued its final Clean Power Plan ("CPP") rules that establish carbon pollution standards for power plants, called CO2 emission performance rates. Judicial challenges led the U.S. Supreme Court to grant a stay in February 2016 of the implementation of the CPP before the United States Court of Appeals for the District of Columbia ("Circuit Court") even issued a decision. In October 2017 the EPA proposed to repeal the CPP. The EPA subsequently proposed the ACE rule to replace the CPP with a rule that utilizes heat rate improvement measures as the "best system of emission reduction." The ACE rule adopts new implementing regulations under the CAA to clarify the roles of the EPA and the states, including an extension of the deadline for state plans and EPA approvals; and, the rule revises the NSR permitting program to provide EGUs the opportunity to make efficiency improvements without triggering NSR permit requirements. In June 2019, the EPA published the final repeal of the CPP and promulgation of the ACE rule. The EPA’s attempts to replace the CPP with the ACE rule are currently subject to litigation, and on January 19, 2021 , the Circuit Court struck down the ACE rule, though the case is not yet final, and we cannot predict the final outcome.

Notwithstanding the ACE rule, these requirements have led to premature retirements and could lead to additional premature retirements of coal-fired generating units and reduce the demand for coal. Congress has not currently adopted legislation to restrict carbon dioxide emissions from existing power plants, and it is unclear whether the EPA has the legal authority to regulate carbon dioxide emissions from existing and modified power plants as proposed in the NSPS and CPP. Substantial limitations on GHG emissions could adversely affect demand for the coal we produce.

There have been numerous protests of and challenges to the permitting of new fossil fuel infrastructure, including coal-fired power plants and pipelines, by environmental organizations and state regulators for concerns related to GHG emissions. For instance, various state regulatory authorities have rejected the construction of new coal-fueled power plants based on the uncertainty surrounding the potential costs associated with GHG emissions from these plants under future laws limiting the emissions of carbon dioxide. In addition, several permits issued to new coal-fueled power plants without limits on GHG emissions have been appealed to the EPA’s Environmental Appeals Board. In addition, over thirty states have currently adopted “renewable energy standards” or “renewable portfolio standards,” which encourage or require electric utilities to obtain a certain percentage of their electric generation portfolio from renewable resources by a certain date. Several states have announced their intent to have renewable energy comprise 100% of their electric generation portfolio. Other states may adopt similar requirements, and federal legislation is a possibility in this area. To the extent these requirements affect our current and prospective customers, they may reduce the demand for fossil fuel energy, and may affect long-term demand for our coal. Finally, while the U.S. Supreme Court has held that federal common law provides no basis for public nuisance claims against utilities due to their carbon dioxide emissions, the Court did not decide whether similar claims can be brought under state common law. As a result, despite this favorable ruling, tort-type liabilities remain a concern.

In addition, environmental advocacy groups have filed a variety of judicial challenges claiming that the environmental analyses conducted by federal agencies before granting permits and other approvals necessary for certain coal activities do not satisfy the requirements of the National Environmental Policy Act (“NEPA”). These groups assert that the environmental analyses in question do not adequately consider the climate change impacts of these particular projects. In July 2020, the Council on Environmental Quality ("CEQ ") finalized revisions to NEPA that clarify the extent to which direct, indirect, and cumulative environmental impacts from a proposed project, including GHG emissions, should be examined under NEPA; however, these regulations may be subject to further regulation under the Biden Administration.

Many states and regions have adopted GHG initiatives, and certain governmental bodies have or are considering the imposition of fees or taxes based on the emission of GHG by certain facilities, including coal-fired electric generating facilities. For example, in 2005, ten Northeastern states entered into the Regional Greenhouse Gas Initiative agreement (“RGGI”), calling for the implementation of a cap and trade program aimed at reducing carbon dioxide emissions from power plants in the participating states. The members of RGGI have established in statutes and/or regulations a carbon dioxide trading program. Auctions for carbon dioxide allowances under the program began in September 2008. Since its inception, several additional northeastern states and Canadian provinces have joined RGGI as participants or observers.

Following the RGGI model, five Western states launched the Western Regional Climate Action Initiative to identify, evaluate, and implement collective and cooperative methods of reducing GHG in the region to 15% below 2005 levels by 2020. These states were joined by two additional states and four Canadian provinces and became collectively known as the Western Climate Initiative Partners. However, as of 2020, only California and certain Canadian provinces are currently active participants in the Western Climate Initiative. Nevertheless, it is likely that these regional efforts will continue based on current trends and concerns related to the reduction of GHG emissions.

It is possible that future international, federal and state initiatives to control GHG emissions could result in increased costs associated with fossil fuel production and consumption, such as costs to install additional controls to reduce carbon dioxide emissions or costs to purchase emissions reduction credits to comply with future emissions trading programs. Such increased costs for fossil fuel consumption could result in some customers switching to alternative sources of fuel, or otherwise adversely affect our operations and demand for our products, which could have a material adverse effect on our business, financial condition, and results of operations. Finally, activists may try to hamper fossil fuel companies by other means, including pressuring financing and other institutions into restricting access to capital, bonding and insurance, as well as pursuing tort litigation for various alleged climate-related impacts.

Water Discharge

The Federal Clean Water Act (“CWA”) and similar state and local laws and regulations regulate discharges into certain waters, primarily through permitting. Section 404 of the CWA imposes permitting and mitigation requirements associated with the dredging and filling of certain wetlands and streams. The CWA and equivalent state legislation, where such equivalent state legislation exists, affect coal mining operations that impact such wetlands and streams. Although permitting requirements have been tightened in recent years, we believe we have obtained all necessary permits required under CWA Section 404 as it has traditionally been interpreted by the responsible agencies. However, mitigation requirements under existing and possible future “fill” permits may vary considerably. For that reason, the setting of post-mine asset retirement obligation accruals for such mitigation projects is difficult to ascertain with certainty and may increase in the future. Although more stringent permitting requirements may be imposed in the future, we are not able to accurately predict the impact, if any, of such permitting requirements.

In order for us to conduct certain activities, an operator may need to obtain a permit for the discharge of fill material from the United States Army Corps of Engineers ("Corps of Engineers") and/or a discharge permit from the state regulatory authority under the state counterpart to the CWA. Our coal mining operations typically require Section 404 permits to authorize activities such as the creation of slurry ponds and stream impoundments. The CWA authorizes the EPA to review Section 404 permits issued by the Corps of Engineers, and in 2009, the EPA began reviewing Section 404 permits issued by the Corps of Engineers for coal mining in Appalachia. Currently, significant uncertainty exists regarding the obtaining of permits under the CWA for coal mining operations in Appalachia due to various initiatives launched by the EPA regarding these permits.

The EPA also has statutory “veto” power over a Section 404 permit if the EPA determines, after notice and an opportunity for a public hearing, that the permit will have an “unacceptable adverse effect.” In January 2011, the EPA exercised its veto power to withdraw or restrict the use of a previously issued permit for Spruce No. 1 Surface Mine in West Virginia, which is one of the largest surface mining operations ever authorized in Appalachia. This action was the first time that such power was exercised with regard to a previously permitted coal mining project which veto was subsequently upheld by the D.C. Circuit Court of Appeals in 2013. Any future use of the EPA’s Section 404 “veto” power could create uncertainty with regard to our continued use of current permits, as well as impose additional time and cost burdens on future operations, potentially adversely affecting our coal revenues. In addition, the EPA initiated a preemptive veto prior to the filing of any actual permit application for a copper and gold mine based on fictitious mine scenario. The implications of this decision could allow the EPA to bypass the state permitting process and engage in watershed and land use planning.

Total Maximum Daily Load (“TMDL”) regulations under the CWA establish a process to calculate the maximum amount of a pollutant that an impaired waterbody can receive and still meet state water quality standards and to allocate pollutant loads among the point and non-point pollutant sources discharging into that water body. Likewise, when water quality in a receiving stream is better than required, states are required to conduct an antidegradation review before approving discharge permits. The adoption of new TMDL-related allocations or any changes to antidegradation policies for streams near our coal mines could require more costly water treatment and could adversely affect our coal production.

Considerable legal uncertainty exists surrounding the standard for what constitutes jurisdictional waters and wetlands subject to the protections and requirements of the CWA. Rulemakings to establish the extent of such jurisdiction were finalized in 2015 and 2020, respectively, and both rulemakings have been subject to substantial litigation. It is also possible that the Biden Administration could propose a broader definition of WOTUS. Should any rule expanding the definition of what constitutes a water of the United States take effect a result of the EPA and the Corps of Engineers' rulemaking process, we could face increased costs and delays due to additional permitting and regulatory requirements and possible challenges to permitting decisions.

Hazardous Substances and Wastes

The Federal Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”), otherwise known as the “Superfund” law, and analogous state laws, impose liability, without regard to fault or the legality of the original conduct on certain classes of persons that are considered to have contributed to the release of a “hazardous substance” into the environment. These persons include the owner or operator of the site where the release occurred and companies that disposed or arranged for the disposal of the hazardous substances found at the site. Persons who are or were responsible for the release of hazardous substances may be subject to joint and several liability under CERCLA for the costs of cleaning up releases of hazardous substances and natural resource damages. Some products used in coal mining operations generate waste containing hazardous substances. We are currently unaware of any material liability associated with the release or disposal of hazardous substances from our past or present mine sites.

The Federal Resource Conservation and Recovery Act (“RCRA”) and analogous state laws impose requirements for the generation, transportation, treatment, storage, disposal, and cleanup of hazardous and non-hazardous wastes. Many mining wastes are excluded from the regulatory definition of hazardous wastes, and coal mining operations covered by SMCRA permits are by statute exempted from RCRA permitting. RCRA also allows the EPA to require corrective action at sites where there is a release of hazardous substances. In addition, each state has its own laws regarding the proper management and disposal of waste material. While these laws impose ongoing compliance obligations, such costs are not believed to have a material impact on our operations.

RCRA impacts the coal industry in particular because it regulates the disposal of certain coal combustion by-products (“CCB”). On April 17, 2015, the EPA finalized regulations under RCRA for the disposal of CCB. Under the finalized regulations, CCB is regulated as "non-hazardous" waste and avoids the stricter, more costly, regulations under RCRA's hazardous waste rules. While classification of CCB as a hazardous waste would have led to more stringent restrictions and higher costs, this regulation may still increase our customers’ operating costs and potentially reduce their ability to purchase coal.

On November 3, 2015, the EPA published the final rule Effluent Limitations Guidelines and Standards (“ELG”), revising the regulations for the Steam Electric Power Generating category which became effective on January 4, 2016. The rule sets the first federal limits on the levels of toxic metals in wastewater that can be discharged from power plants, based on technology improvements in the steam electric power industry over the last three decades. The combined effect of the CCB and ELG regulations has forced power generating companies to close existing ash ponds and will likely force the closure of certain older existing coal-burning power plants that cannot comply with the new standards. In November 2019, the EPA proposed revisions to the 2015 ELG rule and announced proposed changes to regulations for the disposal of coal ash in order to reduce compliance costs. In October 2020, the EPA published a final rule. It is unclear what impact these regulations will have on the market for our products.

Endangered Species Act

The federal Endangered Species Act (“ESA”) and counterpart state legislation protect species threatened with possible extinction. The U.S. Fish and Wildlife Service (the “USFWS”) works closely with the OSM and state regulatory agencies to ensure that species subject to the ESA are protected from potential impacts from mining-related activities. If the USFWS were to designate species indigenous to the areas in which we operate as threatened or endangered, or to re-designate a species from threatened to endangered, we could be subject to additional regulatory and permitting requirements, which in turn could increase operating costs or adversely affect our revenues.

Other Environmental, Health and Safety Regulations

In addition to the laws and regulations described above, we are subject to regulations regarding underground and above ground storage tanks in which we may store petroleum or other substances. Some monitoring equipment that we use is subject to licensing under the Federal Atomic Energy Act. Water supply wells located on our properties are subject to federal, state, and local regulations. In addition, our use of explosives is subject to the Federal Safe Explosives Act. We are also required to comply with the Federal Safe Drinking Water Act, the Toxic Substance Control Act, and the Emergency Planning and Community Right-to-Know Act. The costs of compliance with these regulations should not have a material adverse effect on our business, financial condition or results of operations.

Suppliers

The main types of goods we purchase are mining equipment and replacement parts, steel-related (including roof control) products, belting products, lubricants, electricity, fuel, and tires. Although we have many long, well-established relationships with our key suppliers, we do not believe that we are dependent on any of our individual suppliers other than for purchases of electricity. The supplier base providing mining materials has been relatively consistent in recent years. Purchases of certain underground mining equipment are concentrated with one principle supplier; however, supplier competition continues to develop.

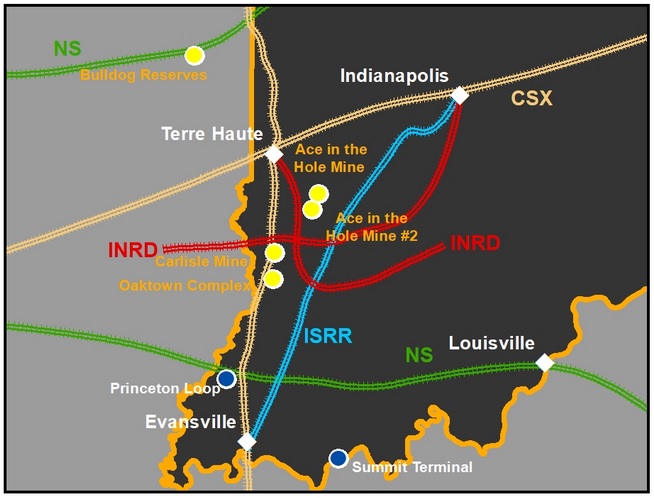

Illinois Basin (ILB)

The coal industry underwent a significant transformation in the early 1990s, as greater environmental accountability was established in the electric utility industry. Through the U.S. Clean Air Act, acceptable baseline levels were established for the release of sulfur dioxide in power plant emissions. In order to comply with the new law, most utilities switched fuel consumption to low-sulfur coal, thereby stripping the ILB of over 50 million tons of annual coal demand. This strategy continued until mid-2000 when a shortage of low-sulfur coal drove up prices. This price increase combined with the assurance from the U.S. government that the utility industry would be able to recoup their costs to install scrubbers caused utilities to begin investing in scrubbers on a large scale. With scrubbers, the ILB has re-opened as a significant fuel source for utilities and has enabled them to burn lower-cost high sulfur coal.

The ILB consists of coal mining operations covering more than 50,000 square miles in Illinois, Indiana, and western Kentucky. The ILB is centrally located between four of the largest regions that consume coal as fuel for electricity generation (East North Central, West South Central, West North Central, and East South Central). The region also has access to sufficient rail and water transportation routes that service coal-fired power plants in these regions as well as other significant coal consuming regions of the South Atlantic and Middle Atlantic.

U. S. Coal Industry

The major coal production basins in the U.S. include Central Appalachia (CAPP), Northern Appalachia (NAPP), Illinois Basin (ILB), Powder River Basin (PRB), and the Western Bituminous region (WB). CAPP includes eastern Kentucky, Tennessee, Virginia and southern West Virginia. NAPP includes Maryland, Ohio, Pennsylvania, and northern West Virginia. The ILB includes Illinois, Indiana, and western Kentucky. The PRB is located in northeastern Wyoming and southeastern Montana. The WB includes western Colorado, eastern Utah, and southern Wyoming. Hallador, through its wholly-owned subsidiary Sunrise Coal, LLC, mines coal exclusively in the ILB.

Coal type varies by basin. Heat value and sulfur content are important quality characteristics and determine the end-use for each coal type.

Coal in the U.S. is mined through surface and underground mining methods. The primary underground mining techniques are longwall mining and continuous (room-and-pillar) mining. The geological conditions dictate which technique to use. Our mines utilize the continuous mining technique. In continuous mining, rooms are cut into the coal bed leaving a series of pillars, or columns of coal, to help support the mine roof and control the flow of air. Continuous mining equipment cuts the coal from the mining face. Generally, openings are driven 20’ wide, and the pillars are rectangular in shape measuring 40’x 40’. As mining advances, a grid-like pattern of entries and pillars is formed. Roof bolts are used to secure the roof of the mine. Battery cars move the coal to the conveyor belt for transport to the surface. The pillars can constitute up to 50% of the total coal in a seam.

The United States coal industry is highly competitive, with numerous producers selling into all markets that use coal. We compete against large producers such as Peabody Energy Corporation (NYSE: BTU), Alliance Resource Partners (Nasdaq: ARLP), and other private producers.

Human Capital

As of December 31, 2020, Hallador Energy Company and its subsidiaries employed 690 full-time employees and temporary miners. 644 of those employees and temporary miners are directly involved in the coal mining or coal washing process. Our workforce is entirely union-free. To attract and retain top talent, we provide competitive wages, an annual bonus for all employees, excellent benefits, an employee health clinic, and a culture that is committed to health and safety at all levels.

Employee health and safety is a top priority at Hallador Energy’s wholly owned subsidiary, Sunrise Coal, LLC. With a robust safety department and safety standards that exceed mandated guidelines, we make safety the foundation of everything we do. While every precaution is taken to prevent mine emergencies, Sunrise Coal has its own private mine rescue team. This team is trained and ready to manage any emergency at a Sunrise Coal, LLC facility, but also ready and available to assist other mine rescue teams. In addition to a highly decorated private mine rescue team, Sunrise Coal in 2020 had three employees on the Indiana State Mine Rescue team and one team trainer which was more than any other mine in Indiana. We continuously monitor safety data such as incidence rate, injury severity, violations per inspection day, and significant and substantial citations and compare to the national averages noting that in 2020 we were at or below the national averages in all four categories. For more information about citations or orders for violations of standards under the FMSHA, as amended by the Miner Act, please see our Exhibit 95.1 to this Annual Report on Form 10-K.

While other companies have moved to high deductible health plans, Hallador Energy is committed to providing comprehensive affordable health insurance with low cost deductibles and co-pays to take care of our employees and their families. We believe in decreasing the barriers to healthcare, so employees and their dependents do not have to delay care. Our employees and their families also have access to a private full-time health and wellness clinic, with free medications, no cost diagnostics, and a wellness coach.

Beyond investing in the safety and health of its employees, Hallador Energy invests in educational opportunities for its employees. All continuing education requirements and training are completely paid for by the company and tuition reimbursement programs are available to every employee companywide.

We are committed to protecting our employees and doing our part to mitigate the spread of COVID-19 while implementing contingency plans to ensure that we continue to supply our customers without interruption. As the situation continues to evolve, we will monitor the Center for Disease Control and Prevention (CDC) guidelines to keep our employees and their families safe. We have taken measures to minimize the spread of germs at our offices and mining locations and educating our employees on how they can reduce the risk of spreading germs to one another. We have implemented social distancing measures while keeping our employees informed about health and safety. Management encourages employees to stay home when they are sick and has adapted our sick day policy to promote time off for illnesses.

Other

We have no significant patents, trademarks, licenses, franchises or concessions.

Our corporate office is located at 1183 East Canvasback Drive, Terre Haute, Indiana, 47802, and Sunrise Coal’s corporate office is at the same location, phone 812.299.2800. Terre Haute is approximately 70 miles west of Indianapolis.

ITEM 1A. RISK FACTORS.

Risks Related to our Business

We face various risks related to pandemics and similar outbreaks, which have had and may continue to have material adverse effects on our business, financial position, results of operations, and/or cash flows.

We face a wide variety of risks related to pandemics, including the global outbreak of COVID-19. Since first reported in late 2019, the COVID-19 pandemic has dramatically impacted the global health and economic environment, including millions of confirmed cases, business slowdowns or shutdowns, government challenges, and market volatility of an unprecedented nature. Although we have, to date, managed to continue most of our operations, we cannot predict the future course of events nor can we assure that this global pandemic, including its economic impact, will not continue to have a material adverse impact on our business, financial position, results of operations and/or cash flows. The COVID-19 pandemic and related economic repercussions have created significant volatility, uncertainty and turmoil in the coal industry. The COVID-19 outbreak and the responsive actions to limit the spread of the virus have significantly reduced global economic activity, resulting in a decline in the demand for coal and other commodities, and negatively impacted our results of operations for 2020. Our operations could be further impacted by the COVID-19 pandemic if significant portions of our workforce are unable to work effectively, including because of illness, quarantines, or absenteeism; steps the company has taken to protect health and well-being; government actions; facility closures; work slowdowns or stoppages; inadequate supplies or resources (such as reliable personal protective equipment, testing, and vaccines); or other circumstances related to COVID-19. Looking forward, we could be unable to perform fully on our contracts, we could experience interruptions in our business, and we could incur liabilities and suffer losses as a result. We will continue to incur additional costs because of the COVID-19 outbreak, including protecting the health and well-being of our employees and as a result of impacts on operations and performance, which costs we may not be fully able to recover. We could be subject to additional regulatory requirements, enforcement actions, and litigation, again with costs and liabilities that are not fully recoverable or insured. The continued spread of COVID-19 could also affect our ability to hire, develop and retain our talented and diverse workforce, and to maintain our corporate culture. The continued global pandemic, including the economic impact, is likely also to cause further disruption in our supply chain. If our suppliers have increased challenges with their workforce (including as a result of illness, absenteeism or government orders), facility closures, access to necessary components and supplies, access to capital, and access to fundamental support services (such as shipping and transportation), they could be unable to provide the agreed-upon goods and services in a timely, compliant and cost-effective manner. We could incur additional costs and delays in our business, including as a result of higher prices for materials and equipment and schedule delays. As a result of the COVID-19 crisis, there may be changes in our customers' priorities and practices, as our customers confront reduced demand. Our customers have and may continue to experience adverse effects as a result of the COVID-19 crisis which could impact their creditworthiness or their ability to make payment for our products. We continue to work with our stakeholders (including customers, employees, suppliers, and local communities) to address this global pandemic responsibly. We continue to monitor the situation, to assess further possible implications to our employees, business, supply chain, and customers, and to take certain actions to mitigate various adverse consequences. We expect that the longer the COVID-19 pandemic, including its economic disruption, continues, the greater the adverse impact on our business operations, financial performance, and results of operations could be. Given the tremendous uncertainties and variables, we cannot at this time predict the impact of the global COVID-19 pandemic, or any future pandemic, but any pandemic or similar outbreak could have a material adverse impact on our business, financial position, results of operations, and/or cash flows.

Global economic conditions or economic conditions in any of the industries in which our customers operate as well as sustained uncertainty in financial markets could have material adverse impacts on our business and financial condition that we currently cannot predict.

Weakness in global economic conditions or economic conditions in any of the industries we serve or in the financial markets could materially adversely affect our business and financial condition. For example:

| ● |

the demand for electricity in the U.S. and globally may decline if economic conditions deteriorate, which may negatively impact the revenues, margins, and profitability of our business; |

|

| ● |

any inability of our customers to raise capital could adversely affect their ability to honor their obligations to us; and |

|

| ● | our future ability to access the capital markets may be restricted as a result of future economic conditions, which could materially impact our ability to grow our business, including development of our coal reserves. |

The stability and profitability of our operations could be adversely affected if our customers do not honor existing contracts or do not extend existing or enter into new long-term contracts for coal.

In 2020, approximately 97% of our sales were under contracts having a term greater than one year, which we refer to as long-term contracts. Long-term sales contracts have historically provided a relatively secure market for the amount of production committed under the terms of the contracts. From time to time industry conditions may make it more difficult for us to enter into long-term contracts with our electric utility customers, and if supply exceeds demand in the coal industry, electric utilities may become less willing to lock in price or quantity commitments for an extended period of time. Accordingly, we may not be able to continue to obtain long-term sales contracts with reliable customers as existing contracts expire, which could subject a portion of our revenue stream to the increased volatility of the spot market.

Some of our long-term coal sales contracts contain provisions allowing for the renegotiation of prices and, in some instances, the termination of the contract or the suspension of purchases by customers.

Some of our long-term contracts contain provisions that allow for the purchase price to be renegotiated at periodic intervals. These price reopener provisions may automatically set a new price based on the prevailing market price or, in some instances, require the parties to the contract to agree on a new price. Any adjustment or renegotiation leading to a significantly lower contract price could adversely affect our operating profit margins. Accordingly, long-term contracts may provide only limited protection during adverse market conditions. In some circumstances, failure of the parties to agree on a price under a reopener provision can also lead to early termination of a contract.

Several of our long-term contracts also contain provisions that allow the customer to suspend or terminate performance under the contract upon the occurrence or continuation of certain events that are beyond the customer’s reasonable control. Such events may include labor disputes, mechanical malfunctions and changes in government regulations, including changes in environmental regulations rendering use of our coal inconsistent with the customer’s environmental compliance strategies. Additionally, most of our long-term contracts contain provisions requiring us to deliver coal within stated ranges for specific coal characteristics. Failure to meet these specifications can result in economic penalties, rejection or suspension of shipments or termination of the contracts. In the event of early termination of any of our long-term contracts, if we are unable to enter into new contracts on similar terms, our business, financial condition and results of operations could be adversely affected.

We depend on a few customers for a significant portion of our revenue, and the loss of one or more significant customers could affect our ability to maintain the sales volume and price of the coal we produce.

During 2020, we derived 79% of our revenue from four customers (6 power plants), with each of the four customers representing at least 10% of our coal sales. If in the future we lose any of these customers without finding replacement customers willing to purchase an equivalent amount of coal on similar terms, or if these customers were to decrease the amounts of coal purchased or the terms, including pricing terms, on which they buy coal from us, it could have a material adverse effect on our business, financial condition and results of operations.

Our ability to collect payments from our customers could be impaired if their creditworthiness declines or if they fail to honor their contracts with us.

Our ability to receive payment for coal sold and delivered depends on the continued creditworthiness of our customers. If the creditworthiness of our customers declines significantly, our business could be adversely affected. In addition, if a customer refuses to accept shipments of our coal for which they have an existing contractual obligation, our revenues will decrease, and we may have to reduce production at our mines until our customer’s contractual obligations are honored.

Although none of our employees are members of unions, our workforce may not remain union-free in the future.

None of our employees are represented under collective bargaining agreements. However, all of our workforce may not remain union-free in the future, and legislative, regulatory or other governmental action could make it more difficult to remain union-free. If some or all of our currently union-free operations were to become unionized, it could adversely affect our productivity and increase the risk of work stoppages at our mining complexes. In addition, even if we remain union-free, our operations may still be adversely affected by work stoppages at unionized companies, particularly if union workers were to orchestrate boycotts against our operations.

Completion of growth projects and future expansion could require significant amounts of financing that may not be available to us on acceptable terms, or at all.

We plan to fund capital expenditures for our current growth projects with existing cash balances, future cash flows from operations, borrowings under credit facilities and cash provided from the issuance of debt or equity. At times, weakness in the energy sector in general and coal, in particular, has significantly impacted access to the debt and equity capital markets. Accordingly, our funding plans may be negatively impacted by this constrained environment as well as numerous other factors, including higher than anticipated capital expenditures or lower than expected cash flow from operations. In addition, we may be unable to refinance our current debt obligations when they expire or obtain adequate funding prior to expiry because our lending counterparties may be unwilling or unable to meet their funding obligations. Furthermore, additional growth projects and expansion opportunities may develop in the future that could also require significant amounts of financing that may not be available to us on acceptable terms or in the amounts we expect, or at all.

Various factors could adversely impact the debt and equity capital markets as well as our credit ratings or our ability to remain in compliance with the financial covenants under our then current debt agreements, which in turn could have a material adverse effect on our financial condition, results of operations and cash flows. If we are unable to finance our growth and future expansions as expected, we could be required to seek alternative financing, the terms of which may not be attractive to us, or to revise or cancel our plans.

Terrorist attacks or cyber-incidents could result in information theft, data corruption, operational disruption and/or financial loss.