As filed with the Securities and Exchange Commission on April 8, 2024

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

| 4724 | ||||

(State or Other Jurisdiction of Incorporation) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Chief Executive Officer

NextTrip, Inc.

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Christopher L. Tinen, Esq. Caitlin M. Murphey, Esq. Procopio, Cory, Hargreaves & Savitch LLP 12544 High Bluff Drive, Suite 400 San Diego, CA 92130 (858) 720-6320 |

Ross D. Carmel, Esq.

Brian B. Margolis, Esq.

Sichenzia Ross Ference Carmel LLP 1185 Avenue of the Americas, 31st Floor New York, NY 10036 (212) 930-9700

|

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the

Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| Smaller

reporting company | ||

| Emerging

growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information contained in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION | DATED APRIL 8, 2024 |

Shares of Common Stock

Pre-Funded Warrants

Common Warrants

Shares of Common Stock Underlying the Common Warrants

and Pre-Funded Warrants

of

NextTrip, Inc.

This is a firm commitment public offering of shares of our common stock, par value $0.001 per share, and warrants to purchase shares of our common stock (the “Common Warrants”), to be sold together with each share of common stock, at an assumed combined public offering price of $ per share and Common Warrant (based upon the last reported sale price of our common stock on the Nasdaq Capital Market on , 2024). Each Common Warrant will have an exercise price of $ per share (100% of the combined public offering price per share of common stock and Common Warrant), will become exercisable commencing on the date of issuance, and will expire five years from the date of issuance.

We are also offering to those purchasers, if any, whose purchase of common stock in this offering would otherwise result in such purchaser, together with its affiliates and certain related parties, beneficially owning more than 4.99% (or, at the election of the purchaser, 9.99%) of our outstanding shares of common stock immediately following the consummation of this offering, the opportunity to purchase, if any such purchaser so chooses, pre-funded warrants (the “Pre-Funded Warrants”) in lieu of shares common stock that would otherwise result in such purchaser’s beneficial ownership exceeding 4.99% (or, at the election of the purchaser, 9.99%) of our outstanding shares of common stock. The purchase price of each Pre-Funded Warrant will be equal to the combined public offering price per share of common stock and Common Warrant sold in this offering minus $0.001, the exercise price per share of common stock of each Pre-Funded Warrant. The Pre-Funded Warrants are immediately exercisable and may be exercised at any time until all of the Pre-Funded Warrants are exercised in full.

For each Pre-Funded Warrant we sell, the number of shares of common stock we are offering will be decreased on a one-for-one basis. Because we will issue a Common Warrant for each share of common stock and each Pre-Funded Warrant sold in this offering, the number of Common Warrants sold in this offering will not change as a result of a change in the mix of shares of common stock and Pre-Funded Warrants sold. The shares of common stock (or Pre-Funded Warrants) and the accompanying Common Warrants can only be purchased together in this offering, but the securities will be immediately separable upon issuance and will be issued separately. The shares of common stock issuable from time to time upon exercise of the Common Warrants and the Pre-Funded Warrants are also being offered by this prospectus.

The actual combined public offering price per share of common stock (or Pre-Funded Warrant) and Common Warrant will be determined between us and the underwriter at the time of pricing, and may be at a discount to the current market price of our common stock. Therefore, the assumed combined public offering price used throughout this prospectus may not be indicative of the final offering price.

Our common stock is traded on The Nasdaq Capital Market tier of The Nasdaq Stock Market, LLC under the symbol “NTRP”. The last reported sale price of our common stock on the Nasdaq Capital Market on April 5, 2024 was $4.15 per share. There is currently no established trading market for the offered Common Warrants or the Pre-Funded Warrants. We do not intend to list the Common Warrants or Pre-Funded Warrants on the Nasdaq Capital Market or any other national securities exchange or nationally recognized trading system. Without an active trading market, the liquidity of the Common Warrants and the Pre-Funded Warrants will be limited.

We are a “smaller reporting company” as defined under the federal securities laws and, as such, are eligible for reduced public company reporting requirements.

Investing in our securities involves a high degree of risk. Before making an investment decision, please read “Risk Factors” on page 11 of this prospectus.

| Per Share of Common Stock and Accompanying Common Warrant | Per Pre-Funded Warrant and Accompanying Common Warrant | Total | ||||||||

| Public offering price | $ | $ | ||||||||

| Underwriting discounts and commissions(1) | $ | $ | ||||||||

| Proceeds to NextTrip, Inc. before expenses | $ | $ | ||||||||

| (1) | The underwriting discount does not include a non-accountable expense allowance of 1.0% of the gross proceeds of the shares sold in the offering. The registration statement, of which this prospectus is a part, also registers for sale those shares of common stock issuable upon exercise of warrants to purchase shares of our common stock to be issued to the underwriter, or its designated affiliates, in connection with this offering (the “Underwriter’s Warrants”). We have agreed to issue the warrants to the underwriter as a portion of the underwriting compensation payable to the underwriters in connection with this offering. See the section titled “Underwriting” for a description of the compensation payable to the underwriter. |

We have granted the underwriter an option for a period of 30 days after the closing date of the offering to purchase up to an additional shares of our common stock, Pre-Funded Warrants and/or Common Warrants at the combined public offering price, less the underwriting discounts and commissions, solely to cover over-allotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriter expects to deliver the securities to purchasers on or about , 2024.

Sole Bookrunner

The Benchmark Company, LLC

TABLE OF CONTENTS

| i |

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement that we filed with the U.S. Securities and Exchange Commission (the “SEC”). We have not, and the underwriter has not, authorized anyone to provide you with information that is different from that contained in this prospectus or in any free writing prospectus we may authorize to be delivered or made available to you. When you make a decision about whether to invest in our securities, you should not rely upon any information other than the information in this prospectus or in any free writing prospectus that we may authorize to be delivered or made available to you. Neither the delivery of this prospectus nor the sale of our securities means that the information contained in this prospectus or any free writing prospectus is correct after the date of this prospectus or such free writing prospectus. This prospectus is not an offer to sell or the solicitation of an offer to buy our securities in any circumstances under which the offer or solicitation is unlawful.

For investors outside the United States: We have not taken any action that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the securities covered hereby and the distribution of this prospectus outside the United States.

Unless otherwise indicated, information contained in this prospectus concerning our industry and the markets in which we operate, including our general expectations and market position, market opportunity and market share, is based on information from our own management’s estimates and research, as well as from industry and general publications and research, surveys and studies conducted by third parties. Management’s estimates are derived from publicly available information, our knowledge of our industry and assumptions based on such information and knowledge, which we believe to be reasonable. Our management’s estimates have not been verified by any independent source, and we have not independently verified any third-party information. In addition, assumptions and estimates of our and our industry’s future performance are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors.” These and other factors could cause our future performance to differ materially from our assumptions and estimates. See “Risk Factors” and “Cautionary Statement on Forward-Looking Statements.”

We further note that the representations, warranties and covenants made by us in any agreement that is filed as an exhibit to the registration statement of which this prospectus is a part were made solely for the benefit of the parties to such agreement, including, in some cases, for the purpose of allocating risk among the parties to such agreements, and should not be deemed to be a representation, warranty or covenant to you. Moreover, such representations, warranties or covenants were accurate only as of the date when made. Accordingly, such representations, warranties and covenants should not be relied on as accurately representing the current state of our affairs.

NextTrip, Inc., the NextTrip logo and other trademarks or service marks of NextTrip appearing in this prospectus are the property of NextTrip, Inc. This prospectus also includes trademarks, tradenames and service marks that are the property of other organizations. Solely for convenience, trademarks and tradenames referred to in this prospectus appear without the ® and ™ symbols, but those references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights, or that the applicable owner will not assert its rights, to these trademarks and tradenames.

| ii |

PROSPECTUS SUMMARY

The following summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision in our securities. Before investing in our securities, you should carefully read this entire prospectus, including our financial statements and the related notes included in this prospectus and the information set forth under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” As used in this prospectus, unless the context otherwise requires, references to “we,” “us,” “our,” “Company,” and “NextTrip” refer to NextTrip, Inc. and its subsidiaries.

Business Overview

NextTrip is an innovative technology company that is building next generation solutions to power the travel industry. NextTrip, through its subsidiaries, provides travel technology solutions with sales originating in the United States, leisure travel, business travel, groups travel, media and tech. We connect people to new places and discoveries by utilizing digital media engagement, seasoned planning expertise, and unique inventory to curate custom vacations and business travel across the globe. Our proprietary booking engine, branded as NXT2.0, provides travel distributors access to a sizeable inventory.

Our vision is to drive the evolution of the travel industry by merging advanced digital solutions with personalized travel services. Our core technology – a fully integrated travel booking platform – focuses on untapped and underserved sectors of the travel industry, intending to capture new markets. We expect that our future growth will be accelerated by interactive technology, immersive media and unparalleled travel industry expertise.

Organizational History

Historical Monaker Group Business

NextTrip’s travel business was the principal business of NextPlay (then, Monaker Group, Inc. (“Monaker”)) until June 30, 2020, when Monaker entered into a share exchange transaction with HotPlay Enterprise Limited (“HotPlay”), resulting in HotPlay becoming a wholly owned subsidiary of Monaker and HotPlay’s business becoming the principal business of Monaker. Prior to this share exchange, the primary focus of Monaker had been its travel business, which included the sale of vacation rentals, and in particular, alternative lodging rentals (“ALRs”), to consumers through its proprietary booking engine. To support its travel offerings, Monaker introduced travelmagazine.com, featuring travel and lifestyle content to appeal to travelers researching destinations and planning future vacations. In January 2023, NextPlay spun the NextTrip business out to its founders to separate it from NextPlay’s primary business.

COVID-era Transition and Technology Development

The spread of the COVID-19 virus globally beginning in January 2020 severely impacted our business. Beginning in March 2020, many U.S. states and foreign countries began issuing “stay-at-home” orders and closed their borders to interstate and international travel. Such restrictions on travel, together with other measures implemented by governments around the world, severely restricted the level of economic activity around the world and had an unprecedented effect on the global travel industry. The public’s ability to travel was severely curtailed through border closures, mandated travel restrictions and limited operations of hotels, airlines, and additional voluntary or mandated closures of travel-related businesses from December 2019 through the beginning of 2022 (and beyond in some jurisdictions). Measures implemented during the COVID-19 pandemic led to unprecedented levels of temporary and permanent business closures, cancellations and limited new travel bookings, having a severe negative impact on our business, financial condition and results of operations.

Due to the significant decrease in demand for the travel related services provided by us during the peak of the COVID-19 pandemic, we shifted our focus to developing and enhancing our program offerings. For example, we began to develop our online media platform - TravelMagazine.com - allowing consumers to research future travel options as well as enhancing the functionality of our booking engines, including developing a booking engine platform that allows customers to book packaged vacations and wellness programs along with the development of a platform to arrange and manage business travel.

Acquisition of Bookit.com Asset

Following NextTrip’s separation from NextPlay, our team focused on the continued technological development of our booking platform. As part of this development, we acquired a travel platform in June 2022 to help power our proprietary NXT2.0 booking technology. Previously, this technology powered the Bookit.com business, a well-established online leisure travel agent generating over $400 million in annual sales as recently as 2019 (pre-pandemic). As part of the acquisition of the assets of Bookit.com, we were not only able to acquire a proven technology platform that could be integrated with our core travel sectors, but we were also able to secure the Bookit.com database with millions of past travelers and opt-in consumers.

Since 2022 and the acquisition of the bookit.com business, we have been focused on the holistic development and integration of the NXT2.0 technology platform, which serves as a base for current and future technology projects as well as proprietary system enhancements. This integration includes re-engaging with and re-negotiating more than 250 contracts with hotel, airline, and cruise suppliers, and securing unique product inventory of more than 3 million lodging, air and tour product suppliers at exceptional rates to over 2,100 destinations in 200+ countries worldwide.

Through this strategic offering, we will focus on key areas of opportunity in the travel sector and drive enhanced booking conversion rates. Our proprietary technology, when combined with media, product offerings and customer service, provides a unique lane to serve mid- to luxury travelers.

| 1 |

Our Fully Integrated Travel Booking Platform

We have established a direct-to-consumer presence though a number of websites, powered by the NXT2.0 booking platform. Today, the primary leisure platform is hosted on nexttrip.com. The business platform is hosted on nexttripbusiness.com.

We sell travel services to leisure and corporate customers across these websites. Our primary focus is our current offerings of scheduling, pricing and availability information for booking reservations for airlines, hotels, rental cars, as well as other travel products such as transfers, sightseeing tours, shows and event tickets. We sell these travel services both individually and as components of dynamically assembled packaged travel vacations and trips. In addition, we provide content that presents travelers with information about travel destinations, maps and other travel details.

Our online travel publication, travelmagazine.com, provides travelers around the world with inspiration for future vacation destinations and trips. The publication offers written articles, videos, and podcasts. The website is expected to be supported by advertising and allow for research and booking of vacation products.

Travel Products and Services

We are building an ecosystem with technology and product offerings that will include leisure travel, wellness travel, business travel, alternative lodging, technology and media solutions. We engage with consumers and distributors throughout the travel planning journey from planning through post-travel. Our online products also offer efficient management and booking solutions for distributors, suppliers, and property managers. Through direct relationships, we have established robust product offerings and preferred rates across the top destinations world-wide. Our primary product offerings are as follows:

| ● | NextTrip Leisure brings travel solutions and a proprietary booking engine that allows customers to book customized travel, including vacation packages, airline tickets, hotel reservations, tours and activities, curated journeys, cruises, wellness and group travel. | |

| ● | NextTrip Business offers corporate travel management solutions for small to medium-sized businesses. This system allows companies to easily manage travel from anywhere, including bookings, expense reports, travel concierge, and 24/7 support services. | |

| ● | NextTrip Solutions offers technology solutions for product and inventory management as well as white label offerings including: NextTrip products under their brand, technology solutions, vacation rental homes, and property management systems. We are also developing a travel agent portal to drive bookings and travel agent brand loyalty. | |

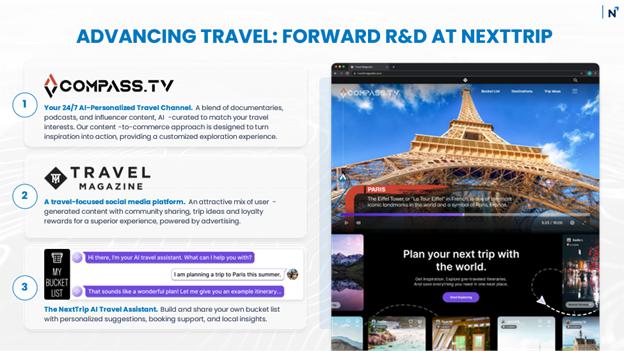

| ● | NextTrip Media includes Travel Magazine and the Compass.TV experience, which is currently in development. These digital solutions engage consumers at the initial phases of travel planning, offering relevant content, destination information and immersive online experiences as well as solutions for travel suppliers. This ecosystem, once fully developed, is expected to allow users to create their own fully customized FAST channel featuring vacation journey opportunities that customers can explore prior to booking the actual vacation. |

Products and Services for Travelers

Search Tools and Ability to Compare. Our online marketplace, nexttrip.com, provides travelers with the tools to search for and filter several travel products including air, car, accommodations (including ALRs) and activities based on various criteria, such as destination, travel dates, type of property, number of bedrooms, amenities, price, or keywords.

| 2 |

Traveler Login. Travelers are able to create accounts on our website(s) that give them access to their booking activity through the website.

Travel Blog. Travel guides, videos and pictures as well as travel articles can be accessed through travelmagazine.com.

Security. We use a combination of technology and human review to evaluate the content of listings and to screen for inaccuracies or fraud with the goal of providing only accurate and trustworthy information to travelers. NextTrip is Payment Card Industry compliant to ensure the safety and security of our customer credit card data.

Communication. Travelers who create an account on our websites will receive regular communications, including notices about places of interest, special offers, new listings, and an email newsletter. The newsletter will be available to any traveler who agrees to receive it and offers introductions to new destinations and vacation rentals, as well as tips and useful information when staying in vacation rentals.

Since the COVID-19 pandemic arose, we have primarily focused on developing our booking engine and establishing relationships with suppliers to increase the size of our instantly bookable inventory. The booking engine has produced little revenue to date because of, among other reasons, the efforts that have been taken to integrate the NextTrip travel platforms with the Bookit.com technology since its acquisition in the summer of 2022. The new platform was launched in beta in May 2023 with a limited number of hotel properties in Mexico and the Caribbean. We have expanded our distribution since launch to include over one million hotel properties worldwide and have completed a full launch of the leisure travel website.

Technology and Infrastructure

Our websites are hosted using cloud services distributed globally across multiple regions. Our systems architecture has been designed to manage increases in traffic through additional computing power without making software changes. Our cloud services provide our online marketplace with scalable and redundant Internet connectivity and redundant power and cooling to its hosting environments. We use security methods to ensure the integrity of our networks and protection of confidential data collected and stored on our servers, and have developed and use internal policies and procedures to protect the personal information of our property owners, managers and travelers using our websites that we collect and use as part of our normal operations. Access to NextTrip’s networks, and the servers and databases, on which confidential data is stored, is protected by industry standard firewall and encryption technology. Physical access to our servers and related equipment is secured by limiting access to the data center to operations personnel only.

Competition

The U.S. travel market is highly competitive and rapidly evolving. The markets are dominated by a few key distributors, which has caused suppliers to look for viable alternatives that would diversify their business mix.

Our competition, which is strong and increasing, includes online and offline travel companies that target leisure and corporate travelers, including travel agencies, tour operators, travel supplier direct websites and their call centers, consolidators and wholesalers of travel products and services, large online portals and search websites, certain travel metasearch websites, mobile travel applications, social media websites, as well as traditional consumer eCommerce and group buying websites. These companies include Expedia, Booking.com, TripAdvisor, Sabre Corp., TravelZoo and AirBnb. In some cases, competitors are offering more favorable terms and improved interfaces to suppliers and travelers, which make competition increasingly difficult. We also face competition for customer traffic on internet search engines and metasearch websites, which impacts our customer acquisition and marketing costs.

| 3 |

Seasonality

We experience seasonal fluctuations in the demand for our travel products and services. For example, traditional leisure travel bookings are generally the highest in the first three quarters as travelers plan and book their spring, summer and winter holiday travel. The number of bookings typically decreases in the fourth quarter. Because revenue for most of our travel products is recognized when the travel takes place rather than when it is booked, revenue typically lags bookings by several weeks to several months. As a result, although travel bookings through our platforms tend to be highest from the period from January to June, moderate from July through September and low from October through December, the majority of revenue is recognized in the summer months (June, July, and August), and during the winter holidays (November and December).

Intellectual Property

Our intellectual property includes the content of our websites, registered domain names, registered and unregistered trademarks, business plan, business strategies and trade secrets, proprietary and acquired software platforms and related assets, licensed software platforms, and customer and third-party supplier lists. We believe that our intellectual property is an essential asset of our business and that our registered domain names and our technology infrastructure will give us a competitive advantage in the online market and arrangements with attractions and tour operators. We rely on a combination of trademark, copyright and trade secret laws in the United States, as well as contractual provisions, to protect our proprietary technology and our brands. We also rely on copyright laws to protect the appearance and design of our sites and applications. We have registered numerous Internet domain names related to our business in order to protect our proprietary interests.

Regulation

Our ability to provide our services and any future services is affected by legal regulations of governments and regulatory authorities around the world, many of which are evolving and subject to revised interpretations. Violations of any laws or regulations could result in fines, penalties, and criminal sanctions against us, our officers or employees, and prohibitions on how or where we conduct our business, which could damage our reputation, brands, global expansion efforts, ability to attract and retain employees and business partners, business, and operating results. Even if we comply with these laws and regulations, doing business in certain jurisdictions or violations of these laws and regulations by the parties with which we conduct business runs the risk of harming our reputation and our brands. Regulations that impact our business or our industry include in the areas of data protection and privacy, payment processing and travel-related regulations on “overtourism” and climate-related issues.

Recent Developments

Acquisition of NextTrip

On October 12, 2023, Sigma Additive Solutions, Inc. (“Sigma”) entered into a Share Exchange Agreement with NextTrip Holdings, Inc. (“NextTrip”), NextTrip Group, LLC (“NextTrip Parent”) and William Kerby (the “NextTrip Representative”), pursuant to which the Company acquired NextTrip (the “Acquisition”) in exchange for shares of our common stock, which we refer to as the Exchange Shares. The Acquisition was consummated on December 29, 2023. As a result, NextTrip became a wholly owned subsidiary of the Company.

Upon the closing of the Acquisition, the shareholders of NextTrip, which we refer to collectively as the NextTrip Sellers, were issued a number of Exchange Shares equal to 19.99% or our issued and outstanding shares of common stock immediately prior to the closing. Under the Share Exchange Agreement, the NextTrip Sellers will be entitled to receive additional shares of our common stock, referred to as the Contingent Shares, subject to NextTrip’s achievement of future business milestones specified in the Share Exchange Agreement as follows:

| Milestone | Date Earned | Contingent Shares | ||

| Launch of NextTrip’s leisure travel booking platform by either (i) achieving $1,000,000 in cumulative sales under its historical “phase 1” business, or (ii) commencement of its marketing program under its enhanced “phase 2” business. | As of a date six months after the closing date | 1,450,000 Contingent Shares | ||

| Launch of NextTrip’s group travel booking platform and signing of at least five (5) entities to use the groups travel booking platform. | As of a date nine months from the closing date (or earlier date six months after the closing date) | 1,450,000 Contingent Shares | ||

| Launch of NextTrip’s travel agent platform and signing up of at least 100 travel agents to the platform (which calculation includes individual agents of an agency that signs up on behalf of multiple agents). | As of a date 12 months from the closing date (or earlier date six months after the closing date) | 1,450,000 Contingent Shares | ||

| Commercial launch of PayDelay technology in the NXT2.0 system. | As of a date 15 months after the closing date (or earlier date six months after the closing date) | 1,650,000 Contingent Shares, less the Exchange Shares issued at the closing of the Acquisition |

| 4 |

Alternatively, independent of the aforementioned milestones, for each month during the fifteen (15) month period following the closing date that in which $1,000,000 or more in gross travel bookings are generated by the combined company, to the extent not previously issued, the Contingent Shares will be issuable up to the maximum Contingent Shares issuable under the Share Exchange Agreement.

The Contingent Shares, together with the shares of our common stock issued at the closing, will not exceed 6,000,000 shares of our common stock, or approximately 90.2% of our issued and outstanding shares of common stock immediately prior to the closing. Assuming all the business milestones are achieved, historical Sigma shareholders will retain 9.8% of the Company’s outstanding shares. Based on analysis presented by our financial advisors, NextTrip has an implied enterprise value of $50 million.

The Share Exchange Agreement provided that William Kerby, the Chief Executive Officer and co-founder of NextTrip, was appointed as Chief Executive Officer of the Company and Donald P. Monaco was appointed as a director of the Company as of the closing of the Acquisition. The NextTrip Representative (Mr. Kerby) will be entitled to designate a replacement for one additional director of the Company upon achievement of each of the milestones under the Share Exchange Agreement.

Asset Sale to Divergent

On October 6, 2023, the Company entered into an Asset Purchase Agreement with Divergent Technologies, Inc., or Divergent, pursuant to which the Company agreed to sell to Divergent, and Divergent agreed to purchase from us, certain legacy Sigma assets of the Company consisting primarily of patents, software code and other intellectual property for a purchase price of $1,626,242, including a $37,000 earnest-money deposit previously paid to us by Divergent. In the interim, between the signing date and closing date of the Asset Purchase Agreement, we granted Divergent a non-exclusive, non-transferable, non-sublicensable (except to Divergent customers and affiliates), limited, irrevocable (except in connection with the termination of the Asset Purchase Agreement in certain circumstances as described below), worldwide, royalty-free license to the “Licensed IP” (as defined) for testing, evaluation, and commercialization purposes.

The Asset Purchase Agreement closed on January 12, 2024. As a result, the NextTrip business became the primary business of the Company.

Name Change and Increase in Authorized Shares

Following the closing of the NextTrip Acquisition and the asset sale of the legacy Sigma assets to Divergent, the Company sought and obtained stockholder approval to change the name of the Company to NextTrip, Inc. and to increase the authorized shares from 1,200,000 shares of common stock to 250,000,000 shares of common stock. The name change and increase in authorized shares were approved by the Company’s stockholders at a Special Meeting of Stockholders held on March 8, 2024.

On March 11, 2024, the Company filed a Certificate of Amendment to its Amended and Restated Articles of Incorporation (the “Charter Amendment”), as amended to date (the “Current Articles”), with the Secretary of State of the State of Nevada, pursuant to which effective as of 12:01 a.m. Pacific time on March 13, 2024, (i) the Company’s corporate name was changed from Sigma Additive Solutions, Inc. to “NextTrip, Inc.”, and (ii) the number of shares of Company common stock authorized for issuance under the Current Articles will be increased from 1,200,000 shares to 250,000,000 shares.

| 5 |

In connection with the name change, effective as of the open of the market on March 13, 2024, the Company’s common stock began trading on the Nasdaq Capital Market under the new ticker symbol “NTRP”.

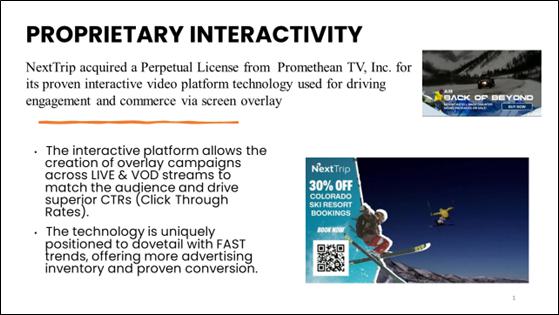

Promethean TV License Agreement

On January 26, 2024, the Company and NextTrip Holdings, Inc., a wholly owned subsidiary of the Company, entered into a Perpetual License Agreement (the “License Agreement”) with Promethean TV, Inc. (“Promethean”), pursuant to which Promethean (i) sold NextTrip the code for the Licensed Software (as defined in the License Agreement) and (ii) granted NextTrip an irrevocable, worldwide, perpetual right and non-exclusive license to forever retain and use the code and each executable copy of the Licensed Software for the commercial exploitation by NextTrip in the travel solutions industry, subject to certain limitations set forth in the License Agreement (the “Perpetual License”). Promethean is the owner and developer of the Ignite TV interactive video platform used for driving engagement and commerce.

The term of the License Agreement commenced on the Effective Date and shall continue in perpetuity unless and until terminated by either party pursuant to the terms of the License Agreement.

As consideration for the Perpetual License and the other rights granted pursuant to the License Agreement, the Company issued Promethean 100,000 restricted shares of its Series G Convertible Preferred Stock (“Series G Preferred”), and NextTrip waived all past debts to NextTrip previously incurred by Promethean. For a period of six months from the Effective Date, the Company has the right to repurchase up to fifty percent of the Series G Preferred issued to Promethean, or the shares of Company common stock underlying the Series G Preferred if converted during such period, for $1.00 as consideration for any breaches of representations and warranties or indemnities of Promethean pursuant to certain provisions of the License Agreement.

Nasdaq Compliance

On August 17, 2023, the Company received a letter from Nasdaq Listing Qualifications (“Nasdaq”) notifying the Company that it no longer complied with Nasdaq Listing Rule 5550(b)(1), which requires companies listed on the Nasdaq Capital Market to maintain minimum stockholders’ equity of $2,500,000 (the “Minimum Stockholder Equity Requirement”), and did not meet the alternatives of market value of listed securities or net income from continuing operations. On October 2, 2023, the Company submitted its plan to regain compliance to Nasdaq and requested an extension to February 13, 2024 to regain compliance with the Minimum Stockholder Equity Requirement. On October 23, 2023, Nasdaq granted the requested extension and provided the Company until February 13, 2024 to demonstrate compliance. Nasdaq further informed the Company that if the Company fails to show compliance upon filing its next periodic report with the SEC and Nasdaq, the Company may be subject to delisting.

Since submitting its plan to Nasdaq, the Company completed the following transactions, which the Company believes resulted in the Company regaining compliance with the Minimum Stockholder Equity Requirement:

| ● | On December 29, 2023, the Company acquired 100% of the outstanding equity interests of NextTrip Holdings, Inc. pursuant to a share exchange agreement by and among the Company, NextTrip and certain other parties (the “Acquisition”). As consideration for the Acquisition, at closing the Company issued 156,007 restricted shares of its common stock, constituting 19.99% of its issued and outstanding shares of common stock immediately prior to execution of the share exchange agreement, and agreed to issue up to an aggregate of 5,843,993 shares as further consideration upon NextTrip’s achievement of certain milestones set forth in the exchange agreement. | |

| ● | On January 16, 2024, the Company completed the sale of certain assets, consisting primarily of patents, software code and other intellectual property, to Divergent Technologies, Inc. for a purchase price of $1,626,242, resulting in net proceeds to the Company of $1,533,563. | |

| ● | In October 2023, the Company sold an aggregate of 128,887 shares of its common stock under its existing at-the-market agreement, resulting in net proceeds to the Company of approximately $772,468. |

| 6 |

An unaudited condensed combined pro-forma balance sheet of the Company as of September 30, 2023, which presents the combination of the financial information of the Company and NextTrip adjusted to give effect to completion of the Acquisition and the Asset Sale, reflects total stockholders’ equity of approximately $5.4 million.

On February 12, 2024, the Company filed a Current Report on Form 8-K disclosing that the Company believes it has regained compliance with the Minimum Stockholder Equity Requirement based upon the specific transactions and events referenced above. Nasdaq informed the Company that it will continue to monitor the Company’s ongoing compliance with Minimum Stockholder Equity Requirement and, if at the time of its next periodic report the Company does not evidence compliance, the Company may be subject to delisting.

Reverse Stock Split

On September 22, 2023, Sigma effected a reverse stock split (the “Reverse Split”) of the issued and outstanding shares of our common stock and the number of shares of common stock that we are authorized to issue. The Reverse Split combined each 20 shares of the issued and outstanding common stock into one share of common stock. No fractional shares were issued in connection with the Reverse Split, and any fractional shares resulting from the Reverse Split were rounded up to the nearest whole share. All stock options, warrants, shares issuable upon conversion of the Company’s preferred stock and stock awards of the Company outstanding immediately prior to the Reverse Split were adjusted in accordance with their terms. All share and earnings per share information presented in this prospectus have been adjusted for the Reverse Split.

Corporate Information

We were incorporated as Messidor Limited in Nevada on December 23, 1985, and changed our name to Framewaves Inc. in 2001. On September 27, 2010, we changed our name to Sigma Labs, Inc. On May 17, 2022, we began doing business as Sigma Additive Solutions, and on August 9, 2022, changed our name to Sigma Additive Solutions, Inc. On March 13, 2024, we changed our name to NextTrip, Inc.

Our principal executive offices are located at 3900 Paseo del Sol, Santa Fe, New Mexico 87507, and our telephone number is (954) 526-9688. Our website address is www.nexttrip.com. Unless expressly noted, none of the information on our corporate website is part of this prospectus or any prospectus supplement.

Risk Factor Summary

Below is a summary of the principal factors that make an investment in our securities speculative or risky. This summary does not address all of the risks that we face. Additional discussion of the risks summarized in this risk factor summary, and other risks that we face, can be found below and should be carefully considered, together with other information included in this prospectus.

We face risks and uncertainties related to our business, many of which are beyond our control. In particular, risks associated with our business include:

● Uncertainty and illiquidity in credit and capital markets can impair our ability to obtain credit and financing on acceptable terms and can adversely affect the financial strength of our business partners;

● The Company will need to raise additional funding to support its operations, which funding may not be available on favorable terms, if at all;

● The Company’s operations have been negatively affected by, and have experienced material declines as a result of, COVID-19 and the governmental responses thereto, additional future government shutdowns or travel restrictions may have a material adverse impact on our business and financial condition;

● The Company’s operations are subject to uncertainties and risks outside of its control, including third party delays in submissions of ALR listings and failures to maintain such rental listings, integrations of such listings and the renewal of such listings;

● The Company is subject to extensive government regulations and rules, the failure to comply which may have a material adverse effect on the Company;

● There is no assurance that we will continue to satisfy the listing requirements of The Nasdaq Capital Market;

● The success of the Company is subject to the development of new products and services over time;

● The Company is subject to competition with competitors who have significantly more resources, more brand recognition and a longer operating history than the Company;

| 7 |

● The Company is subject to risks associated with failures to maintain intellectual property and claims by third parties relating to an allegation that the Company violated such third parties’ intellectual property rights;

● The Company relies on third party service providers and the failure of such third parties to provide the services contracted for, on the terms contracted, or otherwise, could have a material adverse effect on the Company;

● The Company relies on the internet and internet infrastructure for its operations and in order to generate revenues;

● The Company’s ability to raise funding, and dilution caused by such fundings, anti-dilution rights included in outstanding warrants;

● The officers and directors of the Company have the ability to exercise significant influence over the Company;

● Our business depends substantially on property owners and managers renewing their listings;

● The market in which we participate is highly competitive, and we may be unable to compete successfully with our current or future competitors;

● If we are unable to adapt to changes in technology, our business could be harmed;

● We have incurred significant losses to date and require additional capital which may not be available on commercially acceptable terms, if at all;

● There is no public market for the Pre-Funded Warrants or the Common Warrants being offered in this offering;

● We may not receive any additional funds upon the exercise of the Common Stock Warrants or the Pre-Funded Warrants; and

● Those discussed under the caption “Risk Factors” of this Registration Statement.

| 8 |

THE OFFERING

| Common stock outstanding before this | 1,345,932 shares. | |

| offering | ||

| Common stock offered by us | shares. | |

| Common Warrants offered by us | Common Warrants to purchase up to shares of our common stock. Each Common Warrant will have an exercise price of $ per share, will be exercisable commencing on the date of issuance and will expire five (5) years from the date of issuance. The shares of common stock and Common Warrants will be sold together, with each share of common stock to be sold together in a fixed combination with a Common Warrant to purchase a share of common stock. This offering also relates to the shares of common stock issuable upon exercise of Common Warrants sold in this offering. To better understand the terms of the Common Warrants, you should carefully read the section of the prospectus entitled “Description of Securities We Are Offering–Common Warrants.” You should also read the form of Common Warrant, which is filed as an exhibit to the registration statement of which this prospectus forms a part. | |

| Pre-Funded Warrants offered by us | We are also offering to those purchasers, if any, whose purchase of common stock in this offering would otherwise result in such purchaser, together with its affiliates and certain related parties, beneficially owning more than 4.99% (or, at the election of the purchaser, 9.99%) of our outstanding shares of common stock immediately following the consummation of this offering, the opportunity to purchase, if any such purchaser so chooses, Pre-Funded Warrants in lieu of shares common stock that would otherwise result in such purchaser’s beneficial ownership exceeding

4.99% (or, at the election of the purchaser, 9.99%) of our outstanding shares of common stock. This offering also relates to the shares of common stock issuable upon exercise of any Pre-Funded Warrant sold in this offering.

For each Pre-Funded Warrant that we sell, the number of shares of common stock that we are offering will be decreased on a one-for-one basis.

The purchase price of each Pre-Funded Warrant will be equal to the combined public offering price per share of common stock and Common Warrant sold in this offering minus $0.001, the exercise price per share of common stock of each Pre-Funded Warrant. The Pre-Funded Warrants are immediately exercisable and may be exercised at any time until all of the Pre-Funded Warrants are exercised in full. To better understand the terms of the Pre-Funded Warrants, you should carefully read the section of the prospectus entitled “Description of Securities We Are Offering–Pre-Funded Warrants.” You should also read the form of Pre-Funded Warrant, which is filed as an exhibit to the registration statement of which this prospectus forms a part. | |

| Option to purchase additional shares | We have granted the underwriter an option, exercisable for 30 days after closing of this offering, to purchase up to additional shares of Common Stock, Pre-Funded Warrants and/or Common Warrants from us at the combined public offering price per share less the underwriting discounts and commissions, solely to cover over-allotments, if any. | |

| Common stock to be outstanding immediately after this offering | shares (or shares if the underwriter exercises its over-allotment option in full), assuming no sales of Pre-Funded Warrants, which, if sold, would reduce the number of shares of common stock that we are offering on a one-for-one basis, and no exercise of Common Warrants sold in this offering or Underwriter’s Warrants issued in connection with this offering. | |

| Use of proceeds | We estimate that our net proceeds from the sale of the shares of common stock (or Pre-Funded Warrants in lieu thereof) and accompanying Common Warrants we are offering under this prospectus will be approximately $ million (or approximately $ million if the underwriter exercises its option to purchase additional shares in full), assuming a public offering price of $ per share, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us.

We currently intend to use the net proceeds we receive from this offering for general corporate purposes, including operating expenses, capital expenditures and working capital. See the section titled “Use of Proceeds” for additional information. | |

| Underwriter’s Warrants | We have agreed to issue to the underwriter warrants to purchase up to a total of shares of our common stock (or shares assuming the over-allotment option is exercised in full), representing seven percent (7%) of the aggregate number of shares of our common stock and Pre-Funded Warrants (if any) sold in this offering. The warrants will be exercisable, at a price per share equal to 100% of the combined public offering price per share of common stock and Common Warrant, at any time and from time to time, in whole or in part, from 180 days after the commencement of sales in this offering to the fifth anniversary thereof. The registration statement of which this prospectus is a part also registers for sale the number of shares of common stock issuable upon exercise of the Underwriter’s Warrants. Please see “Underwriting – Underwriter’s Warrants” for a description of these warrants. | |

| Risk factors | You should read the “Risk Factors” section of this prospectus beginning on page 11 and the other information in this prospectus for a discussion of factors to consider carefully before deciding to invest in our securities. | |

| Market symbol and trading | Our common stock is listed on the Nasdaq Capital Market under the ticker symbol “NTRP”. We do not intend to apply for a listing of the Pre-Funded Warrants or the Common Warrants on any national securities exchange or other nationally recognized trading system. Without an active trading market, the liquidity of the Pre-Funded Warrants and Common Warrants will be limited. |

The number of shares of our common stock to be outstanding after this offering, as set forth above, is based on 1,345,932 shares of our common stock outstanding as of April 8, 2024. The number of shares of our common stock to be outstanding after this offering, as set forth above, excludes the following:

| ● | 85,185 shares of our common stock subject to outstanding options having a weighted-average exercise price of $59.93 per share; | |

| ● | 484,063 shares of our common stock subject to outstanding warrants having a weighted-average exercise price of $8.58 per share; | |

| ● | 3,172 shares of our common stock issuable upon conversion of our Series E Convertible Preferred Stock; | |

| ● | 33,000 shares of our common stock issuable upon conversion of our Series H Convertible Preferred Stock; | |

| ● | 30,178 shares of our common stock issuable upon conversion of our Series I Convertible Preferred Stock; | |

| ● | shares of our common stock issuable upon exercise of the Common Warrants being offered hereunder; and | |

| ● | shares of common stock (or shares assuming the over-allotment option is exercised in full), issuable upon exercise of Underwriter’s Warrants to be issued to the underwriter or its designees as compensation in connection with this offering at an exercise price equal to 100% of the combined public offering price of the shares of common stock (or Pre-Funded Warrants in lieu thereof) and Common Warrants being offered hereunder. |

Except as otherwise indicated, all information in this prospectus assumes no exercise by the underwriter of its option to purchase additional shares from us.

Unless otherwise indicated, this prospectus reflects and assumes the following:

| ● | the sale and issuance by us of all shares of common stock (or Pre-Funded Warrants in lieu thereof) and accompanying Common Warrants being offered hereunder; | |

| ● | no exercise of the Common Warrants being offered hereunder; | |

| ● | no exercise of the Underwriter’s Warrants to be issued upon consummation of this offering; | |

| ● | no exercise of outstanding options or warrants; and | |

| ● | no exercise by the underwriters of their option to purchase up to additional shares of our Common Stock, Pre-Funded Warrants and/or Common Warrants from us to cover over-allotments, if any. |

To the extent that any outstanding options, warrants, and convertible securities are exercised or converted, there may be further dilution to new investors. In addition, we may choose to raise additional capital due to market conditions or strategic considerations even if we believe we have sufficient funds for our current or future operating plans. To the extent that additional capital is raised through the sale of equity or convertible debt securities, the issuance of these securities could result in further dilution to our stockholders.

| 9 |

SUMMARY FINANCIAL DATA

The following tables summarize our historical financial data for the periods ended on and as of the dates indicated. We have derived the statements of operations data for the years ended February 28, 2023 and 2022 from our

audited financial statements and related notes included elsewhere in this prospectus.

We have derived the unaudited financial data as of and for the nine months ended November 30, 2023 and 2022 from our unaudited condensed financial statements included elsewhere in this prospectus, which have been prepared in accordance with generally accepted accounting principles in the United States of America on the same basis as the annual audited financial statements and, in the opinion of management, the unaudited data reflects all adjustments, consisting only of normal recurring adjustments, necessary for the fair presentation of the financial information in those statements.

Our historical results are not necessarily indicative of results that may be expected in the future, and results for the period ended November 30, 2023 are not necessarily indicative of the results to be expected for the full year ending February 28, 2024.

You should read the following summary financial data together with our financial statements and the related notes appearing elsewhere in this prospectus, as well as with the information in the section of this prospectus entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

| (in thousands, except per share data) | Year Ended February 28, | Nine Months Ended November 30, | ||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||

| Revenue | $ | 382 | $ | 176 | $ | 253 | $ | 418 | ||||||||

| Cost of revenue | $ | 355 | $ | 155 | $ | 204 | $ | 346 | ||||||||

| Operating expenses: | ||||||||||||||||

| General and administrative | $ | 3,574 | $ | 2,941 | $ | 2,225 | $ | 2,679 | ||||||||

| Sales and marketing | $ | 708 | $ | 1,371 | $ | 232 | $ | 612 | ||||||||

| Depreciation and amortization | $ | 807 | $ | 1,060 | $ | 918 | $ | 586 | ||||||||

| Total operating expenses | $ | 5,089 | $ | 5,372 | $ | 3,374 | $ | 3,877 | ||||||||

| Other income | $ | — | $ | (1,129 | ) | $ | — | $ | (18 | ) | ||||||

| Impairment of intangible assets | $ | — | $ | 1,216 | $ | — | $ | — | ||||||||

| Interest (income) expense, net | $ | 71 | $ | — | $ | 216 | $ | 2 | ||||||||

| Foreign exchange (gain) loss | $ | — | $ | — | $ | — | $ | — | ||||||||

| Provision for income taxes | $ | — | $ | — | $ | — | $ | — | ||||||||

| Net loss | $ | (5,133 | ) | $ | (5,438 | ) | $ | (3,542 | ) | $ | (3,789 | ) | ||||

| Net loss per share – basic and diluted | $ | (71.71 | ) | $ | (77.27 | ) | $ | (42.48 | ) | $ | (53.84 | ) | ||||

| (in thousands) | As of November 30, 2023 | |||||||

| Actual | As Adjusted (1) | |||||||

| (unaudited) | (unaudited) | |||||||

| Balance Sheet Data: | ||||||||

| Cash and cash equivalents | $ | 546 | $ | |||||

| Current Assets | $ | 2,542 | $ | |||||

| Total Assets | $ | 5,754 | $ | |||||

| Current Liabilities | $ | 7,897 | $ | |||||

| Total Liabilities | $ | 8,651 | $ | |||||

| Accumulated Deficit | $ | (20,193 | ) | $ | ||||

| Total Stockholders’ Equity/(Deficit) | $ | (2,897 | ) | $ | ||||

| (1) | As adjusted balance sheet data gives effect to our sale of shares of common stock in this offering at a public offering price of $ per share, after deducting underwriting discounts and commissions and estimated offering expenses payable by us. As adjusted balance sheet data is illustrative only and will change based on the actual public offering price and other terms of this offering determined at pricing. Each $0.10 increase (decrease) in the combined public offering price per share of common stock and Common Warrant would increase (decrease) the amount of cash and cash equivalents, working capital, total assets, and total stockholders’ equity by approximately $ million, assuming no sale of Pre-Funded Warrants, that the number of shares of common stock offered by us, as set forth on the cover page of this prospectus, remains the same, and after deducting underwriting discounts and commissions, estimated offering expenses payable by us. We may also increase or decrease the number of shares of common stock and Common Warrants to be issued in this offering. Each increase (decrease) of 500,000 shares of common stock and Common Warrants offered by us would increase (decrease) the as adjusted amount of cash and cash equivalents, working capital, total assets and total stockholders’ deficit by approximately $ million, assuming no sale of Pre-Funded Warrants, that the combined public offering price per share of common stock remains the same, and after deducting underwriting discounts and commissions, and estimated offering expenses payable by us. |

| 10 |

RISK FACTORS

Investing in our securities involves a high degree of risk. You should carefully consider the risks described below, as well as the other information in this prospectus, including our financial statements and the related notes and the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” before deciding whether to invest in our securities. The occurrence of any of the events or developments described below could harm our business, financial condition, operating results, and/or growth prospects. The risks described below are not the only ones facing us. Our business is also subject to the risks that affect many other companies, such as competition, labor relations, general economic conditions, inflation, supply chain constraints, geopolitical changes, and international operations. We operate in a rapidly changing environment that involves a number of risks, some of which are beyond our control. Additional risks not currently known to us or that we currently believe are immaterial also may impair our business operations and our liquidity. The risks described below could cause our actual results to differ materially from those contained in the forward-looking statements we have made in this prospectus, the information incorporated herein by reference, and those forward-looking statements we may make from time to time. You should understand that it is not possible to predict or identify all such factors. Consequently, you should not consider the following to be a complete discussion of all potential risks or uncertainties.

Risks Related to Our Business

Our revenue is derived from the global travel industry, and a prolonged or substantial decrease in global travel, particularly air travel, could adversely affect our operating results.

Our revenue is derived from the global travel industry and would be significantly impacted by declines in, or disruptions to, travel activity, particularly air travel. Global factors over which we have no control, but which could impact our clients’ willingness to travel and, depending on the scope and duration, cause a significant decline in travel volumes include, among other things:

● widespread health concerns, epidemics or pandemics, such as the COVID-19 pandemic, the Zika virus, H1N1 influenza, the Ebola virus, avian flu, SARS or any other serious contagious diseases;

● global security concerns caused by terrorist attacks, the threat of terrorist attacks, or the precautions taken in anticipation of such attacks, including elevated threat warnings or selective cancellation or redirection of travel;

● cyber-terrorism, political unrest, the outbreak of hostilities or escalation or worsening of existing hostilities or war, such as Russia’s invasion of Ukraine and the military conflict in Israel, resulting sanctions imposed by the U.S. and other countries and retaliatory actions taken by sanctioned countries in response to such sanctions;

● natural disasters or severe weather conditions, such as hurricanes, flooding and earthquakes;

● climate change-related impact to travel destinations, such as extreme weather, natural disasters and disruptions, and actions taken by governments, businesses and supplier partners to combat climate change;

● the occurrence of travel-related accidents or the grounding of aircraft due to safety concerns;

● the impact of macroeconomic conditions and labor shortages on the cost and availability of airline travel; and

● adverse changes in visa and immigration policies or the imposition of travel restrictions or more restrictive security procedures.

| 11 |

Any decrease in demand for consumer or business travel could materially and adversely affect our business, financial condition and results of operations.

We need additional capital, which may not be available on commercially acceptable terms, if at all, which raises questions about our ability to continue as a going concern.

As of November 30, 2023, we had $5.8 million in total assets, $8.7 million in total liabilities, negative working capital of $5.4 million and a total accumulated deficit of $20.2 million. We had a net loss of $5.1 million for the fiscal year ended February 28, 2023 and $3.5 million for the nine months ended November 30, 2023.

We are subject to all the substantial risks inherent in the development of a new business enterprise within an extremely competitive industry. Due to the absence of a long-standing operating history and the emerging nature of the markets in which it competes, we anticipate operating losses until we can successfully implement our business strategy, which includes all associated revenue streams. Our revenue model is new and evolving, and we cannot be certain that it will be successful. The potential profitability of this business model is unproven. We may never achieve profitable operations or generate significant revenues. Our future operating results depend on many factors, including demand for our products, the level of competition, and the ability of our officers to manage our business and growth. Additional development expenses may delay or negatively impact our ability to generate profits. Accordingly, we cannot assure you that our business model will be successful or that we can sustain revenue growth, achieve, or sustain profitability, or continue as a going concern.

The Company believes that, in the aggregate, it could require several millions of dollars to support and expand the marketing and development of its products, repay debt obligations, provide capital expenditures for additional equipment and development costs, payment obligations, office space and systems for managing the business, and cover other operating costs until its planned revenue streams from all products are fully implemented and begin to offset its operating costs.

In the event the Company is unable to raise adequate funding in the future for its operations and to pay its outstanding debt obligations, the Company may be forced to scale back its business plan and/or liquidate some or all of its assets or may be forced to seek bankruptcy protection.

We have outstanding indebtedness, which could adversely affect our business and financial condition.

Risks relating to its indebtedness include:

| ● | increasing our vulnerability to general adverse economic and industry conditions; | |

| ● | requiring us to dedicate a portion of our cash flow from operations to principal and interest payments on our indebtedness, thereby reducing the availability of cash flow to fund working capital, capital expenditures, acquisitions and investments and other general corporate purposes; | |

| ● | making it more difficult for us to optimally capitalize and manage the cash flow for our businesses; | |

| ● | limiting our flexibility in planning for, or reacting to, changes in our businesses and the markets in which we operate; | |

| ● | possibly placing us at a competitive disadvantage compared to our competitors that have less debt; and | |

| ● | limiting our ability to borrow additional funds or to borrow funds at rates or on other terms that we find acceptable. |

| 12 |

If distributors are unable to drive customers to our websites and/or we are unable to drive visitors to our websites, from search engines or otherwise, this could negatively impact transactions on the websites of our distributors as well as our own websites and consequently cause our travel revenue to decrease.

Many visitors find the distributors and NextTrip’s websites by searching for vacation rental information through Internet search engines. A critical factor in attracting visitors to NextTrip’s websites, and those of our distributors, is how prominently our distributors and NextTrip are displayed in response to search queries. Accordingly, we utilize search engine marketing, or SEM, as a means to provide a significant portion of our visitor acquisition. SEM includes both paid visitor acquisition (on a cost-per-click basis) and unpaid visitor acquisition, which is often referred to as organic search.

We plan to employ search engine optimization, or SEO, to acquire visitors. SEO involves developing NextTrip’s websites in order to rank highly in relevant search queries. In addition to SEM and SEO, we may also utilize other forms of marketing to drive visitors to our websites, including branded search, display advertising and email marketing.

The various search engine providers, such as Google and Bing, employ proprietary algorithms and other methods for determining which websites are displayed for a given search query and how highly websites rank. Search engine providers may change these methods in a way that may negatively affect the number of visitors to our distributors’ websites as well as our own websites and may do so without public announcement or detailed explanation. Therefore, the success of our SEO and SEM strategy depends, in part, on our ability to anticipate and respond to such changes in a timely and effective manner.

In addition, websites must comply with search engine guidelines and policies. These guidelines and policies are complex and may change at any time. If we or our distributors fail to follow such guidelines and policies properly, the search engine may cause our content to rank lower in search results or could remove the content altogether. If we or our distributors fail to understand and comply with these guidelines and policies and ensure their websites’ compliance, our SEO and SEM strategy may not be successful.

Unfavorable changes in, or interpretations of, government regulations or taxation of the evolving product offerings, Internet and e-commerce industries could harm our travel division operating results.

We have contracted for products in markets throughout the world, in jurisdictions which have various regulatory and taxation requirements that can affect our travel division operations or regulate the rental activity of property owners and managers.

Compliance with laws and regulations of different jurisdictions imposing different standards and requirements is very burdensome because each region has different regulations with respect to licensing and other requirements. Our online marketplaces are accessible by travelers in many states and foreign jurisdictions. Compliance requirements that vary significantly from jurisdiction to jurisdiction impose added costs and increased liabilities for compliance deficiencies. In addition, laws or regulations that may harm our business could be adopted, or interpreted in a manner that affects our activities, including but not limited to the regulation of personal and consumer information and real estate licensing requirements. Violations or new interpretations of these laws or regulations may result in penalties, negatively impact our operations and damage our reputation and business.

In addition, many of the fundamental statutes and regulations that impose taxes or other obligations on travel and lodging companies were established before the growth of the Internet and e-commerce, which creates a risk of these laws being used, in ways not originally intended, that could burden property owners and managers or otherwise harm our business. These and other similar new and newly interpreted regulations could increase costs for, or otherwise discourage, owners and managers from listing their property with NextTrip, which could harm its business and operating results.

Furthermore, as we expand or change the products and services that we offer or the methods by which we offer them, we may become subject to additional legal regulations, tax requirements or other risks. Regulators may seek to impose regulations and requirements on us even if we utilize third parties to offer the products or services. These regulations and requirements may apply to payment processing, insurance products or the various other products and services we may now or in the future offer or facilitate through our marketplace. Whether we comply with or challenge these additional regulations, our costs may increase, and our business may otherwise be harmed.

| 13 |

If we are not able to maintain and enhance our NextTrip brand and the brands associated with each of our websites, our reputation and business may suffer.

It is important for NextTrip to maintain and enhance its brand identity in order to attract and retain property owners, managers, distributors and travelers. The successful promotion of our brands will depend largely on our marketing and public relations efforts. We expects that the promotion of our brands will require us to make substantial investments, and, as its market becomes more competitive, these branding initiatives may become increasingly difficult and expensive. In addition, we may not be able to successfully build our NextTrip brand identity without losing value associated with, or decreasing the effectiveness of, our other brand identities. If we do not successfully maintain and enhance our brands, we could lose traveler traffic, which could, in turn, cause property owners and managers to terminate or elect not to renew their listings with us. In addition, our brand promotion activities may not be successful or may not yield revenue sufficient to offset their cost, which could adversely affect our reputation and business.

Our long-term success depends, in part, on our ability to expand our property owner, manager and traveler bases outside of the United States and, as a result, our business is susceptible to risks associated with international operations.

We have limited operating and e-commerce experience in many foreign jurisdictions and are making significant investments to build our international operations. We plan to continue our efforts to expand globally, including potentially acquiring international businesses and conducting business in jurisdictions where we do not currently operate. Managing a global organization is difficult, time-consuming and expensive and any international expansion efforts that we undertake may not be profitable in the near or long term or otherwise be successful. In addition, conducting international operations subjects the Company to risks that include:

| ● | the cost and resources required to localize its services, which requires the translation of our websites and their adaptation for local practices and legal and regulatory requirements; | |

| ● | adjusting the products and services we provide in foreign jurisdictions, as needed, to better address the needs of local owners, managers, distributors and travelers, and the threats of local competitors; | |

| ● | being subject to foreign laws and regulations, including those laws governing Internet activities, email messaging, collection and use of personal information, ownership of intellectual property, taxation and other activities important to our online business practices, which may be less developed, less predictable, more restrictive, and less familiar, and which may adversely affect financial results in certain regions;

| |

| ● | competition with companies that understand the local market better than we do or who have pre-existing relationships with property owners, managers, distributors and travelers in those markets; | |

| ● | legal uncertainty regarding our liability for the transactions and content on our websites, including online bookings, property listings and other content provided by property owners and managers, including uncertainty resulting from unique local laws or a lack of clear precedent of applicable law; | |

| ● | lack of familiarity with and the burden of complying with a wide variety of other foreign laws, legal standards and foreign regulatory requirements, including invoicing, data collection and storage, financial reporting and tax compliance requirements, which are subject to unexpected changes; | |

| ● | laws and business practices that favor local competitors or prohibit or limit foreign ownership of certain businesses; | |

| ● | challenges associated with joint venture relationships and minority investments; | |

| ● | adapting to variations in foreign payment forms; |

| 14 |

| ● | difficulties in managing and staffing international operations and establishing or maintaining operational efficiencies; | |

| ● | difficulties in establishing and maintaining adequate internal controls and security over our data and systems; | |

| ● | currency exchange restrictions and fluctuations in currency exchange rates; | |

| ● | potentially adverse tax consequences, which may be difficult to predict, including the complexities of foreign value added tax systems and restrictions on the repatriation of earnings; | |

| ● | political, social and economic instability abroad, war, terrorist attacks and security concerns in general; | |

| ● | the potential failure of financial institutions internationally; | |

| ● | reduced or varied protection for intellectual property rights in some countries; and | |

| ● | higher telecommunications and Internet service provider costs. |

Operating in international markets also requires significant management attention and financial resources. We cannot guarantee that our international expansion efforts in any or multiple territories will be successful. The investment and additional resources required to establish operations and manage growth in other countries may not produce desired levels of revenue or profitability and could instead result in increased costs.

The market in which we participate is highly competitive, and we may be unable to compete successfully with our current or future competitors.