UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended September 30 , 2022

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ______ to ______

Commission file number 0-16255

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices, including zip code)

(262 ) 631-6600

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name of Exchange on Which Registered | ||||||

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| Large Accelerated Filer | ☐ | ||||||||||

| ☒ | |||||||||||

| Non-Accelerated Filer | ☐ | ||||||||||

| Smaller Reporting Company | |||||||||||

| Emerging Growth Company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of November 25, 2022, 8,985,510 shares of Class A and 1,207,798 shares of Class B common stock of the registrant were outstanding. The aggregate market value of voting and non-voting common stock of the registrant held by non-affiliates of the registrant was approximately $420,000,000 on April 1, 2022 (the last business day of the registrant’s most recently completed fiscal second quarter) based on approximately 5,301,000 shares of Class A common stock held by non-affiliates as of such date. For purposes of this calculation only, shares of all voting stock are deemed to have a market value of $79.26 per share, the closing price of the Class A common stock as reported on the NASDAQ Global Select MarketSM on April 1, 2022 (the last trading day of the registrant’s most recently completed fiscal second quarter). Shares of common stock held by any executive officer or director of the registrant (including all shares beneficially owned by the Johnson Family, as defined herein) have been excluded from this computation because such persons may be deemed to be affiliates. This determination of affiliate status is not a conclusive determination for other purposes.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 2023 Annual Meeting of the Shareholders of the Registrant are incorporated by reference into Part III of this report.

As used in this report, the terms “we,” “us,” “our,” “Johnson Outdoors” and the “Company” mean Johnson Outdoors Inc. and its subsidiaries collectively, unless the context indicates another meaning.

| TABLE OF CONTENTS | Page | ||||

F-1 | |||||

Forward Looking Statements

Certain matters discussed in this Form 10-K are “forward-looking statements,” and the Company intends these forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995 and is including this statement for purposes of those safe harbor provisions. These statements may be identified by the use of forward-looking words or phrases such as “anticipate,” “believe,” “confident,” “could,” “expect,” “intend,” “may,” “planned,” “potential,” “should,” “will,” “would” or the negative of those terms or other words of similar meaning. Similarly, statements that describe the Company’s future plans, objectives or goals are also forward-looking statements. Such forward-looking statements are subject to certain risks and uncertainties which could cause actual results or outcomes to differ materially from those currently anticipated.

Factors that could affect actual results or outcomes include the matters described under the caption “Risk Factors” in Item 1A of this report and the following: changes in economic conditions, consumer confidence levels and discretionary spending patterns in key markets; uncertainties stemming from political instability (and its impact on the economies in jurisdictions where the Company has operations), changes in US trade policies, tariffs, and the reaction of other countries to such changes; the global outbreaks of disease, such as the COVID-19 pandemic, which has affected, and may continue to affect, market and economic conditions, along with wide-ranging impacts on employees, customers and various aspects of our operations; the Company’s success in implementing its strategic plan, including its targeted sales growth platforms, innovation focus and its increasing digital presence; litigation costs related to actions of and disputes with third parties, including competitors; the Company’s continued success in working capital management and cost-structure reductions; the Company’s success in integrating strategic acquisitions; the risk of future writedowns of goodwill or other long-lived assets; the ability of the Company's customers to meet payment obligations; the impact of actions of the Company's competitors with respect to product development or enhancement or the introduction of new products into the Company's markets; movements in foreign currencies, interest rates or commodity costs; fluctuations in the prices of raw materials or the availability of raw materials or components used by the Company; any disruptions in the Company's supply chain as a result of material fluctuations in the Company's order volumes

2

and requirements for raw materials and other components, or the demand for those same raw materials and components by third parties, necessary to manufacture and produce the Company's products, including related to shortages in procuring necessary raw materials and components to manufacture and produce such products; the success of the Company’s suppliers and customers and the impact of any consolidation in the industries of the Company's suppliers and customers; the ability of the Company to deploy its capital successfully; unanticipated outcomes related to outsourcing certain manufacturing processes; unanticipated outcomes related to litigation matters; and adverse weather conditions. Shareholders, potential investors and other readers are urged to consider these factors in evaluating the forward-looking statements and are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements included herein are only made as of the date of this filing. The Company assumes no obligation, and disclaims any obligation, to update such forward-looking statements to reflect subsequent events or circumstances.

Trademarks

We have registered the following trademarks, among others, which may be used in this report: Minn Kota®, Cannon®, Humminbird®, Eureka!®, Jetboil®, Old Town®, Ocean KayakTM, Carlisle® and SCUBAPRO®.

PART I

ITEM 1. BUSINESS

Johnson Outdoors is a leading global manufacturer and marketer of branded seasonal, outdoor recreation products used primarily for fishing from a boat, diving, paddling, hiking and camping. The Company’s portfolio of well-known consumer brands has attained leading market positions due to continuous innovation, marketing excellence, product performance and quality. Company values and culture support innovation in all areas, promoting and leveraging best practices and synergies within and across its subsidiaries to advance the Company’s strategic vision set by executive management and approved by the Board of Directors. The Company is controlled by Helen P. Johnson-Leipold (Chairman and Chief Executive Officer), members of her family and related entities.

The Company was incorporated in Wisconsin in 1987 as successor to various businesses.

Fishing

The Company’s Fishing segment key brands are: Minn Kota electric motors for quiet trolling or primary propulsion, marine battery chargers and shallow water anchors; Humminbird sonar and GPS equipment for fish finding, navigation and marine cartography; and Cannon downriggers for controlled-depth fishing.

Minn Kota trolling motors and shallow water anchors and Cannon downriggers are designed and manufactured primarily at the Company's Mankato, Minnesota facility. Humminbird sonar and GPS equipment are designed and manufactured primarily in Eufaula, Alabama and Alpharetta, Georgia.

Fishing brands and related accessories are sold across the globe, with the majority of sales coming from North America through large outdoor specialty retailers, such as Bass Pro Shops and Cabela’s; large retail store chains; distributors that service independent marine, sporting goods and internet dealers; and original equipment manufacturers (OEM) of boat brands such as Tracker, Skeeter and Ranger. The Company also sells direct to consumers via its Minn Kota, Humminbird and Cannon websites. Markets outside of North America are accessed through a network of independent international distributors. The Company markets its Fishing brands through several media channels, and is focused on innovation leadership, reliable technology, and quality products.

Camping

The Company’s Camping segment key brands are: Eureka! consumer, commercial and military tents and accessories, camping furniture and stoves and other recreational camping products; and Jetboil portable outdoor cooking systems.

Eureka! consumer tents, camping stoves, and other recreational camping products are mid to high-price range products sold in the U.S. and Canada, primarily to camping and backpacking specialty stores, sporting goods stores, internet retailers and direct to consumer via the Eureka! brand website. The Company’s consumer camping products are produced by third party manufacturing sources in Asia. Marketing of the brand is focused on building brand awareness and leadership in product features and innovation, primarily through digital marketing and social media.

Eureka! commercial tents include party tents and accessories, sold primarily to general rental stores, and other commercial tents and accessories sold directly to tent erectors. The Company’s commercial tent products range from 10’x10’ canopies to 120’

3

wide pole tents and other large scale frame structures and are primarily manufactured by the Company at the Company’s Binghamton, New York location.

Eureka! also designs and manufactures large, heavy-duty tents and lightweight backpacking tents primarily for the U.S. military at its Binghamton, New York location. Tents produced for military use include modular general purpose tents, rapid deployment shelters and various lightweight one and two person tents. The Company manufactures military tent accessories like fabric floors and insulated thermal liners and is also a subcontract manufacturer for other providers of military tents.

Jetboil portable outdoor cooking systems, single burner and two burner stoves, and accessories are sold in the U.S. and Canada, primarily to camping and backpacking specialty stores, sporting goods stores, internet retailers, and direct to consumer via the Jetboil brand website. Markets outside of North America are accessed through a network of independent international distributors. Marketing of Jetboil systems is focused on building brand awareness and leadership in product features and innovation, primarily through digital marketing and social media. Jetboil products are designed at the Company’s operating locations in Manchester, New Hampshire and Old Town, Maine, and manufactured by third party sources in Asia.

Watercraft Recreation

The Company’s Watercraft Recreation segment designs and markets canoes and kayaks under the Ocean Kayaks and Old Town brand names for family recreation, touring and angling. These brands are manufactured at the Company’s facility in Old Town, Maine.

Watercraft Recreation accessory brands, including Carlisle branded paddles, are produced primarily by third party sources located in North America and Asia. The company's personal flotation devices are manufactured by third party sources located in Asia and are sold under the Old Town brand.

The Company’s kayaks, canoes and accessories are sold through multiple channels primarily in the U.S. and Canada with an emphasis on independent specialty dealers and outdoor specialty chain retailers. The Company also sells products direct to consumers via the Old Town and Ocean Kayak websites, and internet retailer sites. The Company has a network of distributors who sell Company products outside of North America.

The Company’s Watercraft Recreation business competes in the mid to high-end of the product category by introducing product innovations, creating quality products and by focusing on the product-specific needs of each marketing channel. Marketing of brands is focused on building brand awareness and leadership in product features and innovation, primarily through digital marketing and social media.

Diving

The Company manufactures and markets underwater diving products for recreational divers, which it sells and distributes under the SCUBAPRO brand name.

The Company markets a complete line of underwater diving and snorkeling equipment, including regulators, buoyancy compensators, dive computers and gauges, wetsuits, masks, fins, snorkels and accessories. SCUBAPRO diving equipment is marketed to the premium recreational segment and high-performance technical diving market. Products are sold via select distribution to independent specialty dive stores worldwide. These specialty dive stores generally provide a wide range of services to divers, including regular maintenance, product repair, diving education and travel programs. The Company also sells diving gear direct to consumers via the SCUBAPRO website and to dive training centers, resorts and public safety units.

The Company manufactures regulators, dive computers, gauges, and instruments at its Italian and Indonesian facilities. The Company designs and develops buoyancy compensators, neoprene goods, diving and snorkeling soft goods, proprietary materials, and other components from third party contract manufacturers.

The Company’s consumer communication focuses on building brand awareness and highlighting exclusive product features and consumer benefits of its product lines. The Company’s communication and distribution strategies reinforce the SCUBAPRO brand’s position as the industry’s quality and innovation leader. The Company markets its equipment via websites, through social media, through information and displays in dive specialty stores, and in diving magazines.

Financial Information for Business Segments

As noted above, the Company has four reportable business segments. See Note 13 to the consolidated financial statements included elsewhere in this report for financial information concerning each business segment.

4

International Operations

See Note 13 to the consolidated financial statements included elsewhere in this report for financial information regarding the Company’s domestic and international operations. See Note 1, subheading “Foreign Operations and Related Derivative Financial Instruments,” to the consolidated financial statements included elsewhere in this report, along with the information under “Risk Factors” below, for information regarding risks related to the Company’s foreign operations.

Research and Development

The Company commits significant resources to new product research and development in each of its business segments. Fishing conducts its product research, design, engineering and software development activities at its locations in Mankato and Little Falls, Minnesota; Alpharetta, Georgia; Toronto, Canada; and Eufaula, Alabama. Diving maintains research and development facilities in Zurich, Switzerland and Casarza Ligure, Italy. Research and development activities for Watercraft Recreation are performed in Old Town, Maine and Racine, Wisconsin. Product research, design and innovation for Camping products are conducted at the Company's Binghamton, New York, Racine, Wisconsin, Manchester, New Hampshire, and Old Town, Maine locations.

The Company expenses research and development costs as incurred, except for software development for new electronics products and bathymetry data collection and processing. These software development and bathymetry data collection and processing costs are capitalized once technological feasibility is established and then amortized over the expected useful life of the software or database. The amounts expensed by the Company in connection with research and development activities for each of the last three fiscal years are set forth in the Company’s Consolidated Statements of Operations included elsewhere in this report.

Industry and Competitive Environment

The Company believes its products compete favorably on the basis of product innovation, product performance and marketing support and, to a lesser extent, price.

Fishing: Minn Kota’s primary competitors in the electric trolling motors business are Motor Guide® and Lowrance™, owned by Brunswick Corporation, and Garmin™. Power-Pole is Minn Kota's main competitor in the shallow water anchor business. Competition in both businesses is focused on technological innovation, product quality and durability as well as product features and benefits for fishing.

Humminbird’s main competitors in the market for on-boat electronics are Garmin™, Lowrance™, and Raymarine®. Competition in this business is primarily focused on the quality of sonar imaging and display, easy to use graphical interfaces as well as the integration of mapping and GPS technology. Humminbird's competitors in marine cartography include Navionics®, owned by Garmin, and C-Map®, owned by Brunswick Corporation. Competition in this business focuses primarily on quality of data and quantity of available charts for inland lakes and ocean shoreline.

Cannon’s main competitors in the downrigger market are Big Jon Sports®, Walker and Scotty®. Competition in this business primarily focuses on ease of operation, speed and durability.

Camping: The Company’s Camping brands and products compete in the sporting goods and specialty segments of the Camping market. Competitive brands with a strong position in the sporting goods channel include Coleman® and private label brands. The Company also competes with specialty companies such as Kelty®, The North Face®, Marmot® and Big Agnes® on the basis of materials and innovative designs for consumers who want performance products priced at a value.

The Company’s portable outdoor cooking systems compete in the specialty and higher end performance backpacking and camping markets. The primary competitor in portable outdoor cooking systems is MSR®. Competition in this market is based on product size and weight, ease of use, reliability and performance.

The Company’s competitors in the commercial tent market include Anchor Industries® and Aztec Tents for tension, frame and canopy tents. Competition in the commercial tent business is based on price, quality, structure, styling, ease of installation and technical support.

The Company sells military tents via third party distributors who hold supply contracts primarily with the U.S. Government, as well as to international governments. Such supply contracts can be for commercial off-the-shelf products in addition to products required to be built to unique specifications. Competitors in the military tent business include HDT®, Alaska Structures®, Camel, Outdoor Venture, and Diamond Brand.

5

Watercraft Recreation: The Company primarily competes in this segment in the kayak and canoe product categories of the paddlesports market. The Company’s main competitors in this market are Hobie Cat®, Pelican International Inc., Wenonah Canoe, Jackson Kayak and Legacy Paddlesports™, each of which competes on the basis of their product’s design, performance, quality and price.

Diving: The main competitors in the Diving segment include Aqua Lung®, Suunto®, Atomic Aquatics, Oceanic, Cressi and Mares®. Competitive advantage in the life support product category of this segment, which consists of regulators, dive computers, and buoyancy compensators, is a function of product innovation, performance, quality and safety. Competition in the general diving product category of fins, masks, snorkels and wetsuits is characterized by low barriers to entry and numerous competitors who compete on the basis of product innovation, performance, quality and price.

Backlog

Unfilled orders for future delivery of products varies as a result of numerous factors impacting the Company (including those described in the section titled “Risk Factors” below) and because of the non-binding nature of such orders, the Company does not believe that backlog information is material to the understanding of its business.

Employees and Human Capital Resources

At September 30, 2022, the Company had approximately 1,500 regular, full-time employees, of which approximately 1,200 were employed in the United States and approximately 300 were employed outside of the United States. Approximately 55 or 4% were represented by a collective bargaining agreement, all of whom are located at our facilities in Batam, Indonesia. In recent years, we have not experienced any significant work slowdowns, stoppages, or other labor disruptions. The Company considers its employee relations to be excellent. Temporary employees are utilized primarily to manage peaks in the seasonal manufacturing of products.

The Company remains committed to areas of work place safety, product quality and customer satisfaction. Successful execution of our mission is dependent on attracting, developing and retaining key employees and members of our management team, as well as providing competitive pay and benefits.

Patents, Trademarks and Proprietary Rights

The Company holds patents for various of the products it sells and regularly files applications for patents. The Company has numerous trademarks and trade names which it considers important to its business, many of which are noted in this report. Historically, the Company has vigorously defended its intellectual property rights and expects to continue to do so.

Supply Chain and Sourcing of Materials

The Company manufactures some products that use parts or materials that, due to geographical distance, limited supplier capacity or availability or competing demands for such parts or materials, are only available in a cost effective manner from a single vendor or require the Company to place orders several months in advance of required delivery.

Historically, the Company attempted to mitigate product availability and these supply chain risks when possible through the purchase of safety stock, use of forecast-based supply contracts, and, to a lesser extent, with just in time inventory deliveries or supplier-owned inventory located close to the Company’s manufacturing locations. In doing so, the Company strived to balance the businesses’ need to maintain adequate inventory levels with the cost of holding such inventory by manufacturing to forecast for high volume products, utilizing build-to-order strategies wherever possible, and by having contract-manufactured products delivered to customers directly from the supplier. The Company also seeks to manage its inventory through on-going product design and logistical initiatives with its suppliers to reduce lead times.

Since the start of the COVID-19 pandemic, there have been significant widely-documented supply chain and logistics disruptions across industries, including those in which the Company operates. While the Company expects that these supply chain disruptions will continue into fiscal 2023, the Company remains focused on evaluating and pursuing additional options (beyond building inventory) to manage its supply chain and meet consumer demand for its products. Supply chain disruptions are dynamic and may impact the cost of goods sold for future sales of product or the Company’s ability to fill demand for its products, especially given the volatility and changing circumstances brought on by the COVID-19 pandemic and the resulting economic environment.

Seasonality

6

The Company’s products in each of its business segments are primarily warm-weather, outdoor recreation-related, which has historically resulted in seasonal variations in sales and profitability for the Company. This seasonal variability was traditionally due to customers’ increasing their inventories in the quarters ending March and June, which is the typical primary selling season for the Company’s outdoor recreation products, with lower inventory volumes during the quarters ending September and December.

Due to the timing of the COVID-19 outbreak, the Company’s primary-selling season during fiscal 2020 was interrupted resulting in a significant shift in sales volumes during the 2020 fiscal year toward the last fiscal quarter of that year versus the typical primary selling season which usually occurs during the second and third fiscal quarters, as noted above. During fiscal years 2021 and 2022, as described above under "Supply Chain and Sourcing of Materials," the Company was impacted by supply chain disruptions that impacted sales and operating profit towards the latter half of fiscal 2022. Accordingly, because of the ongoing supply chain disruption and the current macroeconomic conditions (including related to rising prices and inflationary conditions), the Company cannot predict at this time whether it will experience typical seasonality in demand for its products during fiscal 2023 and beyond.

Typically and prior to the impact of COVID-19 as noted above, the Company had mitigated the seasonality of its businesses somewhat by encouraging customers to purchase and take delivery of products more evenly through the year. The following table shows, for the past three fiscal years, the total consolidated net sales and operating profit or loss of the Company for each quarter, as a percentage of the total year. See “Coronavirus (COVID-19)” in Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operations for additional information of the impact of COVID-19 on the Company’s seasonality for fiscal 2021 and 2022.

| Fiscal Year | |||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||||||||||||||||||||

| Quarter Ended | Net Sales | Operating Profit | Net Sales | Operating Profit | Net Sales | Operating Profit | |||||||||||||||||||||||||||||

| December | 21 | % | 21 | % | 22 | % | 22 | % | 22 | % | 10 | % | |||||||||||||||||||||||

| March | 26 | % | 23 | % | 27 | % | 32 | % | 27 | % | 45 | % | |||||||||||||||||||||||

| June | 27 | % | 36 | % | 29 | % | 34 | % | 23 | % | 17 | % | |||||||||||||||||||||||

| September | 26 | % | 20 | % | 22 | % | 12 | % | 28 | % | 28 | % | |||||||||||||||||||||||

| 100 | % | 100 | % | 100 | % | 100 | % | 100 | % | 100 | % | ||||||||||||||||||||||||

Environment and Climate Change

The Company is subject to various supranational, federal, state and local environmental laws, ordinances, regulations, and other requirements of governmental authorities. We believe we comply with such laws and regulations. Expenditures on environmental compliance have not had, and we believe in the future, are not expected to have, a material adverse effect on the Company’s capital expenditures, earnings or competitive position. We do not believe that any direct or indirect consequences of legislation related to climate change will have a material adverse effect on our operating costs, facilities or products. However, risk of environmental liability and charges associated with maintaining compliance with environmental laws is inherent in the nature of the Company’s business and there is no assurance that material liabilities or charges could not arise.

Available Information

The Company maintains a website at www.johnsonoutdoors.com. On its website, the Company makes available, free of charge, its Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports, as soon as reasonably practical after the reports have been electronically filed or furnished to the Securities and Exchange Commission. In addition, the Company makes available on its website, free of charge, its (a) proxy statement for its annual meeting of shareholders; (b) Code of Business Conduct; (c) Code of Ethics for its Chief Executive Officer and Senior Financial and Accounting Officers; (d) the charters for the following committees of the Board of Directors: Audit; Compensation; Executive; and Nominating and Corporate Governance; and (e) Corporate Governance Guidelines, Insider Trading Policy and Incentive Compensation Recovery Policy. Except as specifically provided herein, the Company is not including the information contained on or available through its website as a part of, or incorporating such information by reference into, this Annual Report on Form 10-K. This report includes all material information about the Company that is included on the Company’s website and is otherwise required to be included in this report. Copies of any materials the Company files with the Securities and Exchange Commission (SEC) can also be obtained free of charge through the SEC’s website at www.sec.gov. The SEC’s Public Reference Room can be contacted at 100 F Street, N.E., Washington, D.C. 20549, or by calling 1 (800) 732-0330.

7

ITEM 1A. RISK FACTORS

The risks described below are not the only risks we face. Additional risks that we do not yet know of or that we currently think are immaterial may also impair our future business operations. If any of the events or circumstances described in the following risks actually occur, our business, financial condition or results of operations could be materially adversely affected. In such cases, the trading price of our common stock could decline.

Operational Risk Factors

Our net sales and profitability depend on our ability to continue to conceive, design and market products that appeal to our consumers.

Our business depends on our ability to continue to conceive, design, manufacture and market new products and upon continued market acceptance of our product offering. As described elsewhere in this Report, product research and development is an important component of our success and our market strategy. Rapidly changing consumer preferences and trends make it difficult to predict how long consumer demand for our existing products will continue or what new products will be successful. A decline in consumer demand for our products, our failure to develop new products on a timely basis in anticipation of changing consumer preferences or the failure of our new products to achieve and sustain consumer acceptance could reduce our net sales and profitability.

Intellectual property disputes relating to our products could increase our costs.

Our industry is susceptible to litigation regarding patent infringement and infringement of other intellectual property rights. We could be either a plaintiff or a defendant in trademark, patent and/or other intellectual property infringement or misappropriation claims and claims of breach of license from time to time. The prosecution or defense of any intellectual property litigation is both costly and disruptive of the time and resources of our management and product development teams, even if the claim or defense against us is without merit. The scope of any patent or other intellectual property to which we have or may obtain rights also may not prevent others from developing and selling competing products. The validity and breadth of claims covered in patents and other intellectual property involve complex legal and factual questions, and the resolution of such claims may be highly uncertain, lengthy and expensive. In addition, our patents or other intellectual property may be held invalid upon challenge, or others may claim that we have improperly or invalidly sought patent or other intellectual property protection for our technology, thus exposing us to direct or counter claims in any patent or intellectual property proceeding. We could also be required to pay substantial damages or settlement costs to resolve intellectual property litigation. Furthermore, we may rely on trade secret law to protect technologies and proprietary information that we cannot or have chosen not to patent. Trade secrets, however, are difficult to protect. Although we attempt to maintain protection through confidentiality agreements with necessary personnel, contractors and consultants, we cannot guarantee that such contracts will not be breached. In the event of a breach of a confidentiality agreement or the divulgence of proprietary information, we may not have adequate legal remedies to maintain our trade secret protection. Litigation to determine the scope of intellectual property rights, even if ultimately successful, could be costly and could divert management’s attention away from the Company’s business. Any of these negative events could adversely affect our profitability or operating results.

Product recalls and other claims could affect our financial position and results of operations.

As a manufacturer and distributor of consumer products, we could be required to repurchase or recall one or more of our products if they are found to not meet quality or safety standards or be defective. A repurchase or recall of our products could be costly to us and could damage the reputation of our brands. If we were required to remove, or voluntarily remove our products from the market, our reputation could be tarnished and we might have large quantities of finished products that we could not sell. As a result, product recalls could have a material adverse effect on our business, results of operations and financial condition.

We may experience difficulties in integrating strategic acquisitions.

We have, as part of our strategy, historically pursued strategic acquisitions. The pursuit of future growth through acquisitions involves significant risks that could have a material adverse effect on our business. Risks associated with integrating strategic acquisitions include, but are not limited to:

•unanticipated costs relating to the integration of acquired businesses may increase our expenses and reduce our profitability;

•difficulties in achieving planned cost savings and synergies may increase our expenses;

8

•unanticipated management or operational problems or liabilities may adversely affect our profitability and financial condition; and/or

•breaches of the representations or warranties or other violations of the contractual obligations required by the acquisition agreement of other parties to the acquisition transaction and any contractual remedies related thereto may not adequately protect or compensate us.

We are dependent upon certain key members of management.

Our success will depend to a significant degree on the abilities and efforts of our senior management. Moreover, our success depends on our ability to attract, retain and motivate qualified management, marketing, technical and sales personnel. These people are in high demand and often have competing employment opportunities. The labor market for skilled employees is highly competitive and we may lose key employees or be forced to increase their compensation to retain these people. Employee turnover could significantly increase our recruitment, training and other related employee costs. The loss of key personnel, or the failure to attract qualified personnel, could have a material adverse effect on our business, financial condition or results of operations.

We rely on our credit facilities to provide us with sufficient working capital to operate our business.

Because of the historic seasonal nature of our business, we have from time to time relied upon our credit facilities to provide us with adequate working capital to operate our business. To the extent we again become more dependent upon our credit facilities to fund our operations, if our lenders reduce or terminate our access to amounts under our credit facilities, we may not have sufficient capital to fund our working capital needs and/or we may need to secure additional capital or financing to fund our working capital requirements or to repay outstanding debt under our credit facilities. We can make no assurance that we will be successful in ensuring our availability of amounts under our credit facilities when they are needed or in connection with raising additional capital and that any amount, if raised, will be sufficient to meet our cash flow requirements. In the event we do not have available cash balances on hand for funding future operations, and if we are not able to maintain our borrowing availability under our credit facilities at that time and/or raise additional capital when needed, we may be forced to sharply curtail our efforts to manufacture and promote the sale of our products or to curtail our operations.

Our debt covenants may limit our ability to complete acquisitions, incur debt, make investments, sell assets, merge or complete other significant transactions.

Our credit facilities and certain other of our debt instruments include limitations on a number of our activities in the event of a default, and in some cases regardless of whether a default has occurred, including our ability to:

•incur additional debt;

•create liens on our assets or make guarantees;

•make certain investments or loans; or

•dispose of or sell assets, make acquisitions above certain amounts or enter into a merger or similar transaction.

Although in recent periods we have not had to borrow funds under our credit facilities, we still are required to comply with certain restrictive covenants in our credit facilities, any of which may limit our ability to engage in acts that may be in our best long term interests. Additionally, a breach of any of the restrictive covenants in our credit facilities could result in a default under these facilities. If a default occurs while we have borrowing amounts outstanding, the lenders under our credit facilities may elect to declare all outstanding borrowings, together with accrued interest, to be immediately due and payable, to terminate any commitments they have to provide further borrowings and to exercise any other rights they have under the facilities or applicable law.

We may be subject to disruptions or failures in our information technology systems and network infrastructures that could have a material adverse effect on our business.

We rely on the efficient and uninterrupted operation of complex information technology systems and network infrastructures to operate our business. We also hold data in various company-owned and third party data center facilities upon which our business depends. A disruption, infiltration, breach or failure of these information technology systems or any of these data centers as a result of software or hardware malfunctions, system implementations or upgrades, computer viruses, third-party security breaches, employee error, theft or misuse, malfeasance, power disruptions, natural disasters or accidents could cause breaches of data security, loss of intellectual property and critical data and the release and misappropriation of sensitive competitive information. Any of these events could result in the loss of key information, impair our production and supply chain processes, harm our competitive position, damage our reputation with customers, cause us to incur significant costs to remedy any damages and ultimately materially and adversely affect our business, results of operations and financial condition.

9

While we have implemented a number of protective measures, such measures may not be adequate or implemented properly to prevent or fully address the adverse effect of such events.

Regulatory Risk Factors

Uncertainty over global tariffs, or the financial impact of tariffs, may negatively affect our results.

Changes in U.S. domestic and global tariff frameworks over the last three years have increased our costs of producing goods and resulted in additional risks to our supply chain. More tariff changes are also possible. We have developed strategies to mitigate, in part, previously implemented and, in some cases, proposed tariff increases, but there is no assurance we will be able to continue to mitigate the impact of tariff increases in substantial part on our financial and operating results. Further, uncertainties about future tariff changes could result in mitigation actions undertaken by us that could prove to be detrimental to our business and our relationships with our customers and suppliers. The scope of the tariffs and the rates at which they are implemented may continue to fluctuate and change in an unpredictable manner that further complicates our ability to implement mitigation actions.

The effective tax rate of the Company may be negatively impacted by future changes to tax laws in global jurisdictions in which we operate.

Changes in tax laws or tax rulings could have a material impact on our effective tax rate. Many countries in the European Union, as well as a number of other countries and organizations such as the Organization for Economic Cooperation and Development, are actively considering changes to existing tax laws. Certain proposals could include recommendations that could increase our tax obligations in many countries where we do business. Any changes in the taxation of our activities in such jurisdictions may result in a material increase in our effective tax rate.

We are subject to environmental, climate change, safety and human rights regulations and legislation.

We are subject to supranational, federal, state, local and foreign laws and other legal requirements related to the generation, storage, transport, treatment and disposal of materials as a result of our manufacturing and assembly operations. These laws include the Resource Conservation and Recovery Act (as amended), the Clean Air Act (as amended) and the Comprehensive Environmental Response, Compensation and Liability Act (as amended), as well as similar laws in foreign jurisdictions. Risk of environmental liability and changes associated with maintaining compliance with environmental laws is inherent in the nature of our business and there is no assurance that material liabilities or changes would not arise.

We are also subject to various supranational, federal, state and local environmental, laws, ordinances, regulations and other legislation or requirements of governmental authorities as it relates to climate change. We believe we comply with such laws and regulations. We do not believe that any direct or indirect consequences of legislation related to climate change will have a material adverse effect on our operating costs, facilities, or products. However, evolving regulatory and legislative measures related to protecting against climate change could ultimately pose a risk to our business by influencing the buying patterns of our customers or increasing internal compliance costs.

The Company is also subject to the requirement of Section 1502 of the Dodd-Frank Wall Street Reform and Consumer Protection Act and SEC rules related thereto to conduct due diligence and disclose and report on whether certain minerals and metals, known as “conflict minerals,” are contained in the Company’s products and whether they originate from the Democratic Republic of Congo (“DRC”) and adjoining countries. We may face reputational challenges if we determine that certain of our products contain minerals not determined to be conflict free or if we are unable to sufficiently verify the origins of all conflict minerals used in our products through the procedures we implement.

Our failure to adequately protect personal information could have a material adverse effect on our business.

A wide variety of local, state, national, and international laws, directives and regulations apply to the collection, use, retention, protection, disclosure, transfer, and other processing of personal data (including with respect to the European Union's General Data Protection Regulation and U.S. state laws such as the California Consumer Privacy Act). These data protection and privacy-related laws and regulations continue to evolve and may result in ever-increasing regulatory and public scrutiny and escalating levels of enforcement and sanctions and increased costs of compliance. Our failure to comply with applicable laws and regulations, or to protect such data, could result in enforcement actions against us, including fines, imprisonment of company officials and public censure, claims for damages by end-customers and other affected individuals, damage to our reputation and loss of goodwill (both in relation to existing end-customers and prospective end-customers), any of which could have a material adverse effect on our operations, financial performance, and business. Changing definitions of personal data and personal information, within the European Union, the United States, and elsewhere may limit or inhibit our ability to operate or

10

expand our business, including limiting strategic partnerships that may involve the sharing of data. The evolving data protection regulatory environment may require significant management attention and financial resources to analyze and modify our information technology infrastructure to meet these changing requirements all of which could reduce our operating margins and impact our operating results and financial condition.

Market and Economic Risk Factors

The COVID-19 pandemic has significantly impacted worldwide economic conditions and could continue to have a material adverse effect on our operations and business.

Our operations are exposed to risks associated with pandemics, epidemics or other public health emergencies, such as the outbreak of coronavirus disease (COVID-19). Outbreaks such as these have resulted, and can continue to result, in governments around the world implementing stringent or restrictive measures to help control the spread of the virus, including quarantines, "shelter in place" and "stay at home" orders, travel restrictions, business curtailments, school closures, and other measures. Depending on the timing of these actions, and the scope of the economic activity they impact, we may experience negative impacts on our operations, supply chain, transportation networks, customers and employees and any of such events can impact or adjust the historic seasonality or buying patterns for our products. Further, any health pandemic (or any worsening thereof), including COVID-19 or a similar pandemic, may result in public health measures that may cause an economic downturn that adversely affects demand for our products, and negatively impacts our business or results of operations through the temporary closure of our operating locations or those of our customers or suppliers. The pandemic (or the continuing worsening of it) may also impact the buying patterns and demand for our products (either positively or negatively) by our customers including by generally limiting or discouraging various leisure and travel activities that may adversely impact consumer use of certain of our products.

As we have previously disclosed in our public filings with the Securities and Exchange Commission, during the latter half of fiscal 2020 and throughout fiscal 2021, we saw favorable impact of COVID-19 on our results due to increased participation in fishing, camping and watercraft recreation and related demand for our products, largely driven by consumer desire to engage in socially distant and safe activities in the great outdoors. It is not certain any previously experienced favorable impacts will continue or will recur in the future, especially as demand for outdoor recreation products moderate. Additionally, even where demand may be strong, we face the potential for supply chain constraints and disruptions (including as it relates to the timing, sourcing, availability and cost of raw materials and components) given the overall increased stress on global supply chains and the need to operate with appropriate safety measures in operating environments. The extent to which COVID-19 or another similar pandemic may continue to adversely or favorably impact our business depends on future developments, which are highly uncertain and unpredictable, including new information concerning the severity of the outbreak, the effectiveness of actions globally to contain or mitigate its effects, including government actions to stimulate the economy and prevent further downturns, and the impact of these events on the timing, sourcing, availability and cost of raw materials and components for production of our products. The current level of uncertainty over the economic and operational impacts of any pandemic (including COVID-19 or similar health pandemic) and the impact of such a pandemic on our supply chain requirements means the related financial impact cannot be reasonably estimated at this time.

Competition, consolidation and financial distress in our markets could reduce our net sales, profitability and cash flows.

We operate in highly competitive markets. We compete with several large domestic and foreign companies such as Brunswick, Garmin, and Aqua Lung, with private label products sold by many of our retail customers and with other producers of outdoor recreation products. Some of our competitors have longer operating histories, stronger brand recognition and greater financial, technical, marketing and other resources than us. In addition, due to limited barriers to entry in some of the product industries we engage in, we may face competition from new participants in our markets or from existing participants developing and introducing new products into our market segments. Further, we experience price competition for our products, and competition for shelf space at retailers, all of which may increase in the future. Consolidation of our retail markets could result in fewer but larger retail customers, which may further result in lower selling prices or reduced sales volumes of our products or greater competition for shelf space in these retail markets. Further, financial distress or bankruptcies in our retail markets could negatively impact our operating results and cash flows. If we cannot compete in our product markets successfully in the future, our net sales, profitability and cash flows will likely decline.

General economic conditions affect the Company’s results.

Our revenues are affected by economic conditions and consumer confidence worldwide, but especially in the United States and Europe. In times of economic uncertainty, consumers tend to defer expenditures for discretionary items, which affects demand for our products. Moreover, our businesses are cyclical and seasonal in nature, and their success is impacted by general economic conditions and specific economic conditions affecting the regions and markets we serve, the overall level of

11

consumer confidence in the economy and discretionary income levels. Any substantial deterioration in general economic conditions that diminishes consumer confidence or discretionary income can reduce our sales and adversely affect our financial results. Moreover, declining economic conditions create the potential for future impairments of goodwill and other intangible and long-lived assets that may negatively impact our financial condition and results of operations. Various uncertainties tied to economic conditions, including significant adverse changes in business climate, adverse actions by regulators, unanticipated competition, loss of key customers, a downturn in the economy or in discretionary income levels or changes in consumer preferences could impact the expected cash flows to be generated by an asset or group of assets, and may result in an impairment of those assets. The impact of weak consumer credit markets, corporate restructurings, layoffs, prolonged high unemployment rates, declines in the value of investments and residential real estate, higher fuel prices and increases in federal and state taxation all can negatively affect our operating results.

As noted above, because a substantial majority of our net revenue is generated through discretionary spending by consumers for our outdoor recreation products, a downturn in the economy resulting from prolonged supply chain disruptions or labor shortages, a significant increase in inflation rates (including in connection with rising interest rates through government action to fight inflationary trends), or a reduction in consumer confidence in the U.S. economy may have a material adverse impact on our business, financial condition and results of operations, as consumers generally reduce their discretionary spending during such periods. Inflation rates have increased and may continue to rise or stay elevated for some time, all of which negatively impact consumer confidence and discretionary spending patterns. Additionally, inflationary trends and uncertainties in the economic climate in the United States and elsewhere could have a similar negative impact on the rate and amounts of purchases by our current and potential customers, create price inflation for our products, or otherwise have a negative impact on our expenses, gross margins and revenues, all of which could hinder our growth.

A limited number of our shareholders can exert significant influence over the Company.

As of September 30, 2022, Helen P. Johnson-Leipold, members of her family and related entities (hereinafter the Johnson Family), held approximately 75% of the voting power of both classes of our common stock taken as a whole. This voting power would permit these shareholders, if they chose to act together, to exert significant influence over the outcome of shareholder votes, including votes concerning the election of directors, by-law amendments, possible mergers, corporate control contests and other significant corporate transactions. Moreover, certain members of the Johnson Family have entered into a voting trust agreement covering approximately 99% of our outstanding class B common shares. This voting trust agreement permits these shareholders, if they continue to choose to act together, to exert significant influence over the outcome of shareholder votes, including votes concerning the election of directors, by-law amendments, possible mergers, corporate control contests and other significant corporate transactions.

Our shares of common stock are thinly traded and our stock price may be volatile.

Because our common stock is thinly traded, its market price may fluctuate significantly more than the stock market in general or the stock prices of similar companies, which are exchanged, listed or quoted on NASDAQ or another stock exchange. We believe there are approximately 5,301,000 shares of our Class A common stock held by non-affiliates as of September 30, 2022. Thus, our common stock will be less liquid than the stock of companies with broader public ownership, and as a result, the trading price for our shares of common stock may be more volatile. Among other things, trading of a relatively small volume of our common stock may have a greater impact on the trading price for our stock than would be the case if our public float were larger.

Our stock price is volatile and our shareholders may not be able to resell shares of Class A Common Stock at or above the price they paid.

The trading price of our Class A Common Stock is highly volatile and could be subject to wide fluctuations in response to various factors, some of which are beyond our control. These factors include:

•announcements relating to our earnings trends or with respect to any cost-cutting actions or other strategic transactions involving Johnson Outdoors;

•announcements relating to, and disruptions in, the sourcing, timing, availability and cost of raw materials and components necessary for the production of our products;

•announcements relating to product development efforts of Johnson Outdoors or competitors;

•announcements relating to the receipt, modification or termination of customer or supplier contracts, including with respect to any government contracts or grants;

•prevailing economic conditions;

•business disruptions caused by weather events, pandemics, or other natural disasters;

•disputes concerning Johnson Outdoors' or its competitors' intellectual property or other proprietary rights;

12

•sales of our Class A Common Stock by our executive officers and directors or our significant shareholders in the future;

•the lack of an active, liquid, and orderly market in our Class A Common Stock;

•fluctuations in our quarterly operating results; and

•the issuance of new or changed securities analysts' reports or recommendations regarding the shares of our Class A Common Stock

In addition, the stock markets in general, and the markets for equity securities in companies principally operating in the outdoor leisure or recreational product markets, have experienced periods of high volatility that have been often unrelated to the operating performance of the issuer. These broad market fluctuations may adversely affect the trading price or liquidity of our Class A Common Stock.

Sources of and fluctuations in market prices of raw materials can affect our operating results.

The primary raw materials we use in manufacturing our products are metals, resins, electronic components, and packaging materials. These materials are generally available from a number of suppliers, but traditionally we have chosen to concentrate our sourcing with a limited number of vendors for each commodity or purchased component. Under normal circumstances, we believe our sources of raw materials are reliable and adequate for our needs. However, many materials and components continue to be subject to shortages and significant commodity pricing fluctuations due to deterioration of the global supply chain. The development of future sourcing issues related to the availability of these materials as well as significant fluctuations in the market prices of these materials may have an adverse effect on our financial results.

Our profitability is also affected by significant fluctuations in the prices of the raw materials and components we use in our products, including the effect of fluctuations in foreign currency exchange rates on raw materials and purchased components. We may not be able to pass along any price increases in our raw materials or other component costs to our customers. As a result, an increase in the cost of raw materials, labor or other costs associated with the manufacturing of our products could increase our costs of sales and reduce our gross margins.

Financial distress in supply chain and shortage of raw materials or components of supply.

Deteriorating industry conditions can adversely affect our supply base. Lower production levels at our major suppliers and volatility in certain raw material and energy costs may result in severe financial distress among many companies within our supply base, which may result in issues impacting the sourcing, timing, availability and cost of raw materials and components necessary to manufacture our products. Financial distress within our supply base and/or our suppliers’ inability to obtain credit from lending institutions could lead to commercial disputes and possible supply chain interruptions to our business. In addition, potential adverse industry conditions may require us to provide financial assistance or other measures to ensure uninterrupted production of key components or materials used in the production of our products which could have a material adverse effect on our existing and future revenues and net income. For example, our inventory levels have increased significantly in recent periods as we attempt to build inventory with the goal of mitigating and/or preparing for a continuing disruption of the supply chain, originally starting as a result of the COVID-19 pandemic, but continuing as a result of global economic conditions, including due to rising interest rates, inflationary pressures and the conflict in the Ukraine.

We are currently experiencing supply shortages and cost increases for certain components and raw materials that are crucial to our manufacturing process. Continued higher levels of consumer demand or growth in demand for our outdoor recreation products may exacerbate these pressures, and, therefore, depending upon the severity of, and any continuing adverse impact to, global economic conditions affecting the cost and availability of raw materials and components used in our products, these supply chain challenges described above may continue for the foreseeable future, and may continue to adversely impact our margins for some time. As noted above, we have chosen to take action to increase our inventories and purchase commitments in an attempt to ensure we have adequate inventory levels to meet customer expectations and demand for our products. Nonetheless not all necessary components to build inventory have been readily available at reasonable prices or at all.

Additionally, in the event of catastrophic acts of nature such as fires, tsunamis, hurricanes and earthquakes or a rapid increase in production demands, either we, or our suppliers may experience supply shortages of raw materials or components. This could be caused by a number of factors, including a lack of production line capacity or manpower or working capital constraints. As our industry consolidates its supply base in order to manage the costs of purchased goods and services, there is greater dependence on fewer sources of supply for certain components and materials used in our products, which could increase the possibility of a supply shortage of any particular component. If we or one of our own suppliers experience a supply shortage, we may become unable to produce the affected products if we cannot procure the components from another source. Such production interruptions could impede a ramp-up in production and could have a material adverse effect on our business, results of operations and financial condition.

13

We consider the production capacities and financial condition of suppliers in our selection process, and expect that they will meet our delivery requirements. However, there can be no assurance that strong demand, capacity limitations, shortages of raw materials, labor disputes, freight capacity or other problems will not result in any shortages or delays in the supply of components to us.

Currency exchange rate fluctuations could adversely affect the Company’s results.

We have significant foreign operations, for which the functional currencies are denominated primarily in euros, Swiss francs, Hong Kong dollars and Canadian dollars. As the values of the currencies of the foreign countries in which we have operations increase or decrease relative to the U.S. dollar, the sales, expenses, profits, losses, assets and liabilities of our foreign operations, as reported in our consolidated financial statements, increase or decrease, accordingly. Approximately 13% of our revenues for the year ended September 30, 2022 were denominated in currencies other than the U.S. dollar. Approximately 4% were denominated in euros and approximately 6% were denominated in Canadian dollars with the remaining 3% denominated in various other foreign currencies. We may mitigate a portion of the impact of fluctuations in certain foreign currencies on our operations through the purchase of foreign currency swaps, forward contracts and options to hedge known commitments denominated in foreign currencies or to reduce the risk of changes in foreign currency exchange rates on foreign currency borrowings.

Because we rely on foreign suppliers and we sell products in foreign markets, we are susceptible to numerous international business risks that could increase our costs or disrupt the supply of our products.

Our international operations subject us to risks, including:

•economic and political instability;

•restrictive actions by foreign governments, including with respect to tariffs or trade policies;

•opportunity costs and reputational damage related to the presence of counterfeit versions of the Company’s products in such foreign markets;

•greater difficulty enforcing intellectual property rights and weaker laws protecting intellectual property rights;

•changes in tariffs, import duties or import or export restrictions;

•timely shipping of product and unloading of product, including the timely rail/truck delivery to our warehouses and/or a customer’s warehouse of our products;

•complications in complying with the laws and policies of the United States affecting the importation of goods, including tariffs, duties, quotas and taxes;

•required compliance with U.S. laws that impact the Company’s operations in foreign jurisdictions that do not impact local operating companies; and

•complications in complying with trade and foreign tax laws.

General Risk Factors

Cyber security vulnerabilities, threats and more sophisticated and targeted computer crime could pose a risk to our systems, networks, products, solutions, services and data.

Increased global cyber security vulnerabilities, threats, computer viruses and more sophisticated and targeted cyber-related attacks, as well as cyber security failures resulting from human error and technological errors, pose a risk to our systems, products and data as well as potentially to our employees’, customers’ and suppliers’ data and systems that may ultimately impact us. We attempt to mitigate these risks by employing a number of measures, including employee training, monitoring and testing, and maintenance of protective systems and contingency plans, but we remain potentially vulnerable to additional known or unknown threats. There is no assurance the impact from such threats will not be material to our financial results or reputation and it could result in security breaches, theft, lost or corrupted data, misappropriation of sensitive, confidential or personal data or information, loss of trade secrets and commercially valuable information, production downtimes and operational disruptions, any of which may adversely affect our profitability or operating results.

Future terror attacks, war, natural disasters or other catastrophic events beyond our control could negatively impact our business.

Terror attacks, war or other civil disturbances, natural disasters and other catastrophic events could lead to economic instability and decreased demand for our products, which could negatively impact our business, financial condition, results of operations and cash flows. In the past, terrorist attacks have caused instability in global financial markets and the industries in which we compete and have negatively affected spending on consumer discretionary products. In addition, our facilities are located throughout the world and could be subject to damage from terrorism incidents or from fires, floods, earthquakes or other natural

14

or man-made disasters. Terrorist incidents could also lead to increased border security which could in turn negatively impact our global supply chain by causing shipping delays or shortages in key materials or components, increasing the cost of such goods or requiring us to keep greater inventories, any of which may adversely impact our business, results of operations, financial condition or cash flows.

Our business is susceptible to adverse weather conditions or events.

Our success is in part affected by adverse weather conditions, including fires, floods, tornadoes, severe cold and other natural disasters. Such events have the tendency to create fluctuations in demand for our products which may increase our expenses and reduce our profitability. Moreover, our profitability is affected by our ability to successfully manage our inventory levels and demand for our products, which, in part depends upon the efficient operation of our production and delivery systems. These systems are vulnerable to damage or interruption from the aforementioned natural disasters. Such natural disasters could adversely impact our ability to meet delivery requirements of our customers, which may result in our need to incur extra costs to expedite production and delivery of product to meet customer demand. Any of these events could negatively impact our profitability.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not Applicable

ITEM 2. PROPERTIES

The Company maintains leased and owned manufacturing, warehousing, distribution and office facilities throughout the world. The Company believes that its facilities are well maintained and have capacity adequate to meet its current needs.

See Note 5 to the consolidated financial statements included elsewhere in this report for a discussion of the Company’s lease obligations.

As of September 30, 2022, the Company’s principal manufacturing (identified with an asterisk) and other locations are:

Alpharetta, Georgia (Fishing)

Antibes, France (Diving)

Batam, Indonesia* (Diving)

Binghamton, New York* (Camping)

Burlington, Ontario, Canada (Fishing, Camping, Watercraft Recreation)

Casarza Ligure, Italy* (Diving)

Chai Wan, Hong Kong (Diving)

Chatswood, Australia (Diving)

El Cajon, California (Diving)

Eufaula, Alabama* (Fishing)

Little Falls, Minnesota (Fishing)

Manchester, New Hampshire (Camping)

Mankato, Minnesota* (Fishing)

Mexicali, Mexico* (Fishing)

Old Town, Maine* (Watercraft Recreation)

Toronto, Ontario, Canada (Fishing)

Nuremberg, Germany (Diving)

Zurich, Switzerland (Diving)

The Company’s corporate headquarters is located in a facility in Racine, Wisconsin.

ITEM 3. LEGAL PROCEEDINGS

In the normal course of business, we may be involved in various legal proceedings from time to time. As of the date of the filing of this Report, we are not involved in any litigation involving amounts deemed to be material to the business or financial condition of the Company.

ITEM 4. MINE SAFETY DISCLOSURES

None.

15

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Certain information with respect to this item is included in Notes 9 and 10 to the Company’s consolidated financial statements included elsewhere in this report. The Company’s Class A common stock is traded on the NASDAQ Global Select MarketSM under the symbol: JOUT. There is no public market for the Company’s Class B common stock. However, the Class B common stock is convertible at all times at the option of the holder into shares of Class A common stock on a share for share basis. As of September 30, 2022, the Company had 419 holders of record of its Class A common stock and 20 holders of record of its Class B common stock. We believe the number of beneficial owners of our Class A common stock on that date was substantially greater.

A summary of the high and low closing prices for the Company’s Class A common stock during each quarter of the years ended September 30, 2022, October 1, 2021 and October 2, 2020 is as follows:

| First Quarter | Second Quarter | Third Quarter | Fourth Quarter | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | 2022 | 2021 | 2020 | 2022 | 2021 | 2020 | 2022 | 2021 | 2020 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock prices: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| High | $ | 115.87 | $ | 113.21 | $ | 78.17 | $ | 95.60 | $ | 148.50 | $ | 78.84 | $ | 82.48 | $ | 154.09 | $ | 88.41 | $ | 73.32 | $ | 122.23 | $ | 95.54 | |||||||||||||||||||||||||||||||||||||||||||||||

| Low | 92.82 | 83.60 | 57.53 | 77.44 | 109.00 | 51.29 | 59.04 | 117.92 | 57.46 | 50.54 | 105.51 | 80.27 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Dividends

The Company’s Articles of Incorporation provide that no dividend, other than a dividend payable in shares of the Company’s common stock, may be declared or paid upon the Class B common stock unless such dividend is declared or paid upon both classes of common stock. Whenever a dividend (other than a dividend payable in shares of Company common stock) is declared or paid upon any shares of Class B common stock, at the same time there must be declared and paid a dividend on the shares of Class A common stock equal in value to 110% of the amount per share of the dividend declared and paid on the shares of Class B common stock. Whenever a dividend is payable in shares of Company common stock, such dividend must be declared or paid at the same rate on the Class A common stock and the Class B common stock.

Quarterly dividends declared in the first three quarters of fiscal 2022 were $0.30 per share of Class A common stock, and $0.31 per share for the fourth fiscal quarter of 2022. Quarterly dividends declared per share of Class B common stock were $0.27 for the first three quarters of fiscal 2022, and $0.28 per share for the fourth fiscal quarter of 2022. Total dividends declared in fiscal 2022 were $12,171. Cash dividends paid in fiscal 2022 totaled $12,056 and dividends payable of $3,120 were included in current liabilities at September 30, 2022.

While the Board of Directors of the Company presently intends to continue the payment of regular quarterly cash dividends on the Company’s common stock, they review the Company’s dividend quarterly and may elect to increase, decrease or not pay a dividend at any time. The Company’s ability to pay dividends could be affected by future business performance (including as a result of the continued impact of supply chain disruption, inflation and macroeconomic dynamics on our operations and cash flows), liquidity, capital needs, alternative investment opportunities and compliance with debt covenants in its loan agreements.

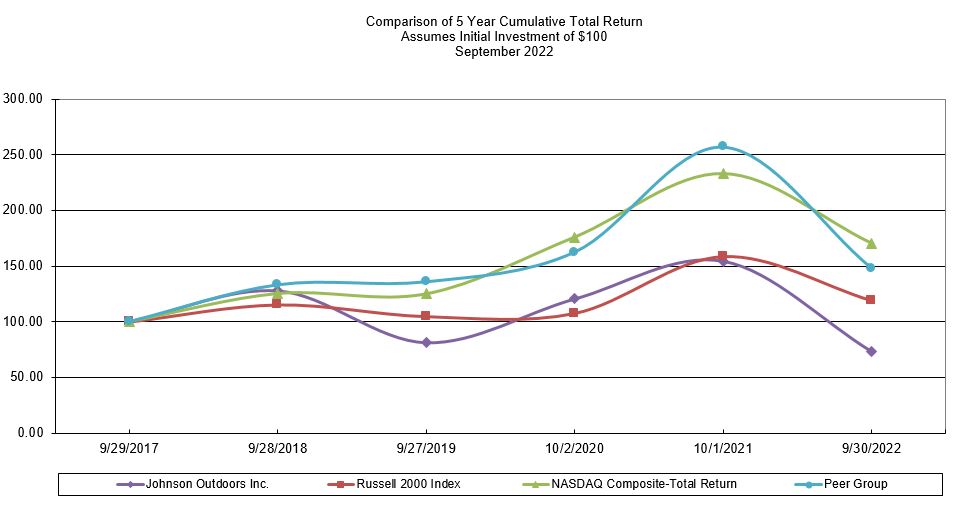

Total Shareholder Return

The graph below compares on a market cap weighted cumulative basis the yearly percentage change since September 29, 2017 in the total return (assuming reinvestment of dividends) to shareholders on the Class A common stock with (a) the total return (assuming reinvestment of dividends) on The NASDAQ Stock Market-U.S. Index; (b) the total return (assuming reinvestment of dividends) on the Russell 2000 Index; and (c) the total return (assuming reinvestment of dividends) on a self-constructed peer group index. The Company’s peer group consists of Clarus Corporation, Brunswick Corporation, Callaway Golf Company, Escalade Inc., Garmin Ltd., Marine Products Corporation, Malibu Boats Inc. and Nautilus, Inc. The graph assumes $100 was invested on September 29, 2017 in the Company’s Class A common stock, The NASDAQ Stock Market-U.S. Index, the Russell 2000 Index and the peer group index.

16

* $100 invested on September 29, 2017 in stock or index, including reinvestment of dividends.

Indices calculated on a mid-month basis.

| 9/29/2017 | 9/28/2018 | 9/27/2019 | 10/2/2020 | 10/1/2021 | 9/30/2022 | ||||||||||||||||||||||||||||||

| Johnson Outdoors Inc. | $ | 100.0 | $ | 127.7 | $ | 81.1 | $ | 120.4 | $ | 154.4 | $ | 73.3 | |||||||||||||||||||||||

| NASDAQ Composite | 100.0 | 125.2 | 124.9 | 175.9 | 232.9 | 170.4 | |||||||||||||||||||||||||||||

| Russell 2000 Index | 100.0 | 115.2 | 104.8 | 107.6 | 158.3 | 119.1 | |||||||||||||||||||||||||||||

| Peer Group | 100.0 | 133.1 | 135.8 | 162.5 | 257.1 | 148.1 | |||||||||||||||||||||||||||||

The information in this section titled “Total Shareholder Return” shall not be deemed to be “soliciting material” or “filed” with the Securities and Exchange Commission or subject to Regulation 14A or 14C promulgated by the Securities and Exchange Commission or subject to the liabilities of section 18 of the Securities Exchange Act of 1934, as amended, and this information shall not be deemed to be incorporated by reference into any filing under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended.

ITEM 6. RESERVED

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS