0000785956J&J SNACK FOODS CORPfalse--09-28FY20199.59.555101000000009,275,0000310Includes share-based compensation expense of $24 and $65 for the three months and nine months ended June 29, 2019, respectively and $20 and $56 for the three months and nine months ended June 30, 2018.Includes share-based compensation expense of $435 and $1,191 for the three months and nine months ended June 29, 2019, respectively and $412 and $1,178 for the three months and nine months ended June 30, 2018.Total of quarterly amounts do not necessarily agree to the annual report amounts due to separate quarterly calculations of weighted average shares outstanding.Includes share-based compensation expense of $391 and $1,061 for the three months and nine months ended June 29, 2019, respectively and $349 and $998 for the three months and nine months ended June 30, 2018.Includes share-based compensation expense of $271 and $735 for the three months and nine months ended June 29, 2019, respectively and $225 and $642 for the three months and nine months ended June 30, 2018.Write-offs of uncollectible accounts receivable.1110,000,00010,000,000000050,000,00050,000,00018,895,00018,754,00018,895,00018,754,00000007859562018-09-302019-09-28xbrli:shares00007859562019-11-11thunderdome:itemiso4217:USD00007859562019-09-2800007859562019-03-2900007859562018-09-2900007859562017-10-012018-09-2900007859562016-09-252017-09-30iso4217:USDxbrli:shares0000785956us-gaap:CommonStockIncludingAdditionalPaidInCapitalMember2016-09-240000785956us-gaap:AccumulatedOtherComprehensiveIncomeMember2016-09-240000785956us-gaap:RetainedEarningsMember2016-09-2400007859562016-09-240000785956us-gaap:CommonStockIncludingAdditionalPaidInCapitalMember2016-09-252017-09-300000785956us-gaap:AccumulatedOtherComprehensiveIncomeMember2016-09-252017-09-300000785956us-gaap:RetainedEarningsMember2016-09-252017-09-300000785956us-gaap:CommonStockIncludingAdditionalPaidInCapitalMember2017-09-300000785956us-gaap:AccumulatedOtherComprehensiveIncomeMember2017-09-300000785956us-gaap:RetainedEarningsMember2017-09-3000007859562017-09-300000785956us-gaap:CommonStockIncludingAdditionalPaidInCapitalMember2017-10-012018-09-290000785956us-gaap:AccumulatedOtherComprehensiveIncomeMember2017-10-012018-09-290000785956us-gaap:RetainedEarningsMember2017-10-012018-09-290000785956us-gaap:CommonStockIncludingAdditionalPaidInCapitalMember2018-09-290000785956us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-09-290000785956us-gaap:RetainedEarningsMember2018-09-290000785956us-gaap:CommonStockIncludingAdditionalPaidInCapitalMember2018-09-302019-09-280000785956us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-09-302019-09-280000785956us-gaap:RetainedEarningsMember2018-09-302019-09-280000785956us-gaap:AccountingStandardsUpdate201601Memberus-gaap:CommonStockIncludingAdditionalPaidInCapitalMember2018-09-302019-09-280000785956us-gaap:AccountingStandardsUpdate201601Memberus-gaap:AccumulatedOtherComprehensiveIncomeMember2018-09-302019-09-280000785956us-gaap:AccountingStandardsUpdate201601Memberus-gaap:RetainedEarningsMember2018-09-302019-09-280000785956us-gaap:AccountingStandardsUpdate201601Member2018-09-302019-09-280000785956us-gaap:CommonStockIncludingAdditionalPaidInCapitalMember2019-09-280000785956us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-09-280000785956us-gaap:RetainedEarningsMember2019-09-2800007859562019-06-29xbrli:pure0000785956jjsf:CustomerGroupOneMember2019-09-280000785956jjsf:CustomerGroupOneMembersrt:MinimumMember2019-09-280000785956jjsf:CustomerGroupOneMembersrt:MaximumMember2019-09-280000785956us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMember2018-09-302019-09-280000785956us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMemberjjsf:TopTenCustomersMember2018-09-302019-09-280000785956us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMemberjjsf:TopTenCustomersMember2017-10-012018-09-290000785956us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMemberjjsf:TopTenCustomersMember2016-09-252017-09-300000785956us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMemberjjsf:LargestCustomerMember2018-09-302019-09-280000785956us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMemberjjsf:LargestCustomerMember2017-10-012018-09-290000785956us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMemberjjsf:LargestCustomerMember2016-09-252017-09-30utr:Y0000785956srt:MinimumMember2018-09-302019-09-280000785956srt:MaximumMember2018-09-302019-09-280000785956us-gaap:StateAndLocalJurisdictionMemberus-gaap:NewJerseyDivisionOfTaxationMember2017-10-012018-09-290000785956us-gaap:EmployeeStockOptionMember2018-09-302019-09-280000785956us-gaap:EmployeeStockOptionMember2017-10-012018-09-290000785956us-gaap:EmployeeStockOptionMember2016-09-252017-09-300000785956us-gaap:StockCompensationPlanMember2018-09-302019-09-280000785956us-gaap:StockCompensationPlanMember2017-10-012018-09-290000785956us-gaap:StockCompensationPlanMember2016-09-252017-09-300000785956jjsf:StockIssuedToOutsideDirectorsMember2018-09-302019-09-280000785956jjsf:StockIssuedToOutsideDirectorsMember2017-10-012018-09-290000785956jjsf:StockIssuedToOutsideDirectorsMember2016-09-252017-09-300000785956us-gaap:RestrictedStockMember2018-09-302019-09-280000785956us-gaap:RestrictedStockMember2017-10-012018-09-290000785956us-gaap:RestrictedStockMember2016-09-252017-09-300000785956srt:MinimumMember2017-10-012018-09-290000785956srt:MinimumMember2016-09-252017-09-300000785956srt:MaximumMember2017-10-012018-09-290000785956srt:MaximumMember2016-09-252017-09-30utr:M0000785956jjsf:YearOptionsMembersrt:MinimumMember2018-09-302019-09-280000785956jjsf:YearOptionsMembersrt:MaximumMember2018-09-302019-09-280000785956jjsf:TenYearOptionsMember2018-09-302019-09-280000785956us-gaap:AccountingStandardsUpdate201602Memberus-gaap:SubsequentEventMember2019-09-290000785956jjsf:HillValleyIncMember2016-12-302016-12-300000785956jjsf:HillValleyIncMember2016-12-302016-12-300000785956jjsf:HillValleyIncMember2017-10-012018-09-290000785956jjsf:HillValleyIncMember2016-09-252017-09-300000785956jjsf:ICEEDistributorMember2017-05-222017-05-220000785956jjsf:ICEEDistributorMember2017-10-012018-09-290000785956jjsf:ICEEDistributorMember2016-09-252017-09-300000785956jjsf:LabriolaBakingCompanyMember2017-08-162017-08-160000785956jjsf:LabriolaBakingCompanyMember2017-08-162017-08-160000785956jjsf:LabriolaBakingCompanyMember2017-10-012018-09-290000785956jjsf:LabriolaBakingCompanyMember2016-09-252017-09-300000785956jjsf:HillValleyIncMember2016-12-300000785956jjsf:ICEEDistributorMember2017-05-220000785956jjsf:LabriolaBakingCompanyMember2017-08-160000785956jjsf:HillValleyIncMemberus-gaap:TradeNamesMember2016-12-300000785956jjsf:ICEEDistributorMemberus-gaap:TradeNamesMember2017-05-220000785956jjsf:LabriolaBakingCompanyMemberus-gaap:TradeNamesMember2017-08-160000785956jjsf:HillValleyIncMemberus-gaap:CustomerRelationshipsMember2016-12-300000785956jjsf:ICEEDistributorMemberus-gaap:CustomerRelationshipsMember2017-05-220000785956jjsf:LabriolaBakingCompanyMemberus-gaap:CustomerRelationshipsMember2017-08-160000785956jjsf:HillValleyIncMemberus-gaap:DistributionRightsMember2016-12-300000785956jjsf:ICEEDistributorMemberus-gaap:DistributionRightsMember2017-05-220000785956jjsf:LabriolaBakingCompanyMemberus-gaap:DistributionRightsMember2017-08-160000785956jjsf:HillValleyIncMemberus-gaap:NoncompeteAgreementsMember2016-12-300000785956jjsf:ICEEDistributorMemberus-gaap:NoncompeteAgreementsMember2017-05-220000785956jjsf:LabriolaBakingCompanyMemberus-gaap:NoncompeteAgreementsMember2017-08-160000785956us-gaap:CorporateBondSecuritiesMember2019-09-280000785956us-gaap:CertificatesOfDepositMember2019-09-280000785956jjsf:MutualFundsMember2019-09-280000785956us-gaap:PreferredStockMember2019-09-280000785956us-gaap:MutualFundMember2018-09-302019-09-280000785956us-gaap:PreferredStockMember2018-09-302019-09-280000785956us-gaap:CorporateBondSecuritiesMember2018-09-302019-09-280000785956us-gaap:CorporateBondSecuritiesMember2018-09-290000785956us-gaap:CertificatesOfDepositMember2018-09-290000785956jjsf:MutualFundsMember2018-09-290000785956us-gaap:PreferredStockMember2018-09-290000785956us-gaap:LandMember2019-09-280000785956us-gaap:LandMember2018-09-290000785956us-gaap:BuildingMember2019-09-280000785956us-gaap:BuildingMember2018-09-290000785956us-gaap:BuildingMembersrt:MinimumMember2018-09-302019-09-280000785956us-gaap:BuildingMembersrt:MaximumMember2018-09-302019-09-280000785956us-gaap:MachineryAndEquipmentMember2019-09-280000785956us-gaap:MachineryAndEquipmentMember2018-09-290000785956us-gaap:MachineryAndEquipmentMembersrt:MinimumMember2018-09-302019-09-280000785956us-gaap:MachineryAndEquipmentMembersrt:MaximumMember2018-09-302019-09-280000785956us-gaap:EquipmentMember2019-09-280000785956us-gaap:EquipmentMember2018-09-290000785956us-gaap:EquipmentMembersrt:MinimumMember2018-09-302019-09-280000785956us-gaap:EquipmentMembersrt:MaximumMember2018-09-302019-09-280000785956us-gaap:TransportationEquipmentMember2019-09-280000785956us-gaap:TransportationEquipmentMember2018-09-290000785956us-gaap:TransportationEquipmentMember2018-09-302019-09-280000785956us-gaap:OfficeEquipmentMember2019-09-280000785956us-gaap:OfficeEquipmentMember2018-09-290000785956us-gaap:OfficeEquipmentMembersrt:MinimumMember2018-09-302019-09-280000785956us-gaap:OfficeEquipmentMembersrt:MaximumMember2018-09-302019-09-280000785956jjsf:ImprovementsMember2019-09-280000785956jjsf:ImprovementsMember2018-09-290000785956jjsf:ImprovementsMembersrt:MinimumMember2018-09-302019-09-280000785956jjsf:ImprovementsMembersrt:MaximumMember2018-09-302019-09-280000785956us-gaap:ConstructionInProgressMember2019-09-280000785956us-gaap:ConstructionInProgressMember2018-09-290000785956us-gaap:TradeNamesMemberjjsf:FoodServiceMember2019-09-280000785956us-gaap:TradeNamesMemberjjsf:FoodServiceMember2018-09-290000785956us-gaap:NoncompeteAgreementsMemberjjsf:FoodServiceMember2019-09-280000785956us-gaap:NoncompeteAgreementsMemberjjsf:FoodServiceMember2018-09-290000785956us-gaap:CustomerRelationshipsMemberjjsf:FoodServiceMember2019-09-280000785956us-gaap:CustomerRelationshipsMemberjjsf:FoodServiceMember2018-09-290000785956jjsf:LicenseAndRightsMemberjjsf:FoodServiceMember2019-09-280000785956jjsf:LicenseAndRightsMemberjjsf:FoodServiceMember2018-09-290000785956jjsf:FoodServiceMember2019-09-280000785956jjsf:FoodServiceMember2018-09-290000785956us-gaap:TradeNamesMemberjjsf:RetailSupermarketMember2019-09-280000785956us-gaap:TradeNamesMemberjjsf:RetailSupermarketMember2018-09-290000785956jjsf:FiniteLivedTradeNamesMemberjjsf:RetailSupermarketMember2019-09-280000785956jjsf:FiniteLivedTradeNamesMemberjjsf:RetailSupermarketMember2018-09-290000785956us-gaap:CustomerRelationshipsMemberjjsf:RetailSupermarketMember2019-09-280000785956us-gaap:CustomerRelationshipsMemberjjsf:RetailSupermarketMember2018-09-290000785956jjsf:RetailSupermarketMember2019-09-280000785956jjsf:RetailSupermarketMember2018-09-290000785956us-gaap:TradeNamesMemberjjsf:FrozenBeveragesMember2019-09-280000785956us-gaap:TradeNamesMemberjjsf:FrozenBeveragesMember2018-09-290000785956jjsf:DistributionRightsIndefinitelivedMemberjjsf:FrozenBeveragesMember2019-09-280000785956jjsf:DistributionRightsIndefinitelivedMemberjjsf:FrozenBeveragesMember2018-09-290000785956us-gaap:CustomerRelationshipsMemberjjsf:FrozenBeveragesMember2019-09-280000785956us-gaap:CustomerRelationshipsMemberjjsf:FrozenBeveragesMember2018-09-290000785956jjsf:LicenseAndRightsMemberjjsf:FrozenBeveragesMember2019-09-280000785956jjsf:LicenseAndRightsMemberjjsf:FrozenBeveragesMember2018-09-290000785956jjsf:FrozenBeveragesMember2019-09-280000785956jjsf:FrozenBeveragesMember2018-09-290000785956jjsf:ICEEDistributorMemberjjsf:FrozenBeveragesMember2016-09-252017-09-300000785956jjsf:HillValleyIncMemberjjsf:FoodServiceMember2016-09-252017-09-300000785956jjsf:LabriolaBakingCompanyMemberjjsf:FoodServiceMember2016-09-252017-09-300000785956jjsf:ICEEDistributorMemberjjsf:FrozenBeveragesMember2018-09-302019-09-2800007859562016-11-300000785956jjsf:PhillySwirlMemberus-gaap:DomesticCountryMemberus-gaap:InternalRevenueServiceIRSMember2019-09-280000785956jjsf:PhillySwirlMemberus-gaap:DomesticCountryMemberus-gaap:InternalRevenueServiceIRSMember2018-09-290000785956jjsf:EmployeeStockPurchasePlanMember2018-09-302019-09-280000785956jjsf:EmployeeStockPurchasePlanMember2017-10-012018-09-290000785956jjsf:EmployeeStockPurchasePlanMember2016-09-252017-09-300000785956jjsf:EmployeeStockPurchasePlanMember2019-09-280000785956jjsf:EmployeeStockPurchasePlanMember2018-09-290000785956jjsf:EmployeeStockPurchasePlanMember2017-09-300000785956jjsf:IncentiveStockOptionsMember2016-09-240000785956jjsf:NonQualifiedStockOptionsMember2016-09-240000785956jjsf:IncentiveStockOptionsMember2016-09-252017-09-300000785956jjsf:NonQualifiedStockOptionsMember2016-09-252017-09-300000785956jjsf:IncentiveStockOptionsMember2017-09-300000785956jjsf:NonQualifiedStockOptionsMember2017-09-300000785956jjsf:IncentiveStockOptionsMember2017-10-012018-09-290000785956jjsf:NonQualifiedStockOptionsMember2017-10-012018-09-290000785956jjsf:IncentiveStockOptionsMember2018-09-290000785956jjsf:NonQualifiedStockOptionsMember2018-09-290000785956jjsf:IncentiveStockOptionsMember2018-09-302019-09-280000785956jjsf:NonQualifiedStockOptionsMember2018-09-302019-09-280000785956jjsf:IncentiveStockOptionsMember2019-09-280000785956jjsf:NonQualifiedStockOptionsMember2019-09-280000785956jjsf:IncentiveStockOptionsMemberjjsf:ExercisePriceRange1Member2018-09-302019-09-280000785956jjsf:IncentiveStockOptionsMemberjjsf:ExercisePriceRange1Member2019-09-280000785956jjsf:IncentiveStockOptionsMemberjjsf:ExercisePriceRange2Member2018-09-302019-09-280000785956jjsf:IncentiveStockOptionsMemberjjsf:ExercisePriceRange2Member2019-09-280000785956jjsf:NonQualifiedStockOptionsMemberjjsf:ExercisePriceRange1Member2018-09-302019-09-280000785956jjsf:NonQualifiedStockOptionsMemberjjsf:ExercisePriceRange1Member2019-09-280000785956jjsf:NonQualifiedStockOptionsMemberjjsf:ExercisePriceRange2Member2018-09-302019-09-280000785956jjsf:NonQualifiedStockOptionsMemberjjsf:ExercisePriceRange2Member2019-09-280000785956jjsf:NonQualifiedStockOptionsMemberjjsf:ExercisePriceRange3Member2018-09-302019-09-280000785956jjsf:NonQualifiedStockOptionsMemberjjsf:ExercisePriceRange3Member2019-09-280000785956jjsf:SoftPretzelsMemberjjsf:FoodServiceMember2018-09-302019-09-280000785956jjsf:SoftPretzelsMemberjjsf:FoodServiceMember2017-10-012018-09-290000785956jjsf:SoftPretzelsMemberjjsf:FoodServiceMember2016-09-252017-09-300000785956jjsf:FrozenJuicesAndIcesMemberjjsf:FoodServiceMember2018-09-302019-09-280000785956jjsf:FrozenJuicesAndIcesMemberjjsf:FoodServiceMember2017-10-012018-09-290000785956jjsf:FrozenJuicesAndIcesMemberjjsf:FoodServiceMember2016-09-252017-09-300000785956jjsf:ChurrosMemberjjsf:FoodServiceMember2018-09-302019-09-280000785956jjsf:ChurrosMemberjjsf:FoodServiceMember2017-10-012018-09-290000785956jjsf:ChurrosMemberjjsf:FoodServiceMember2016-09-252017-09-300000785956jjsf:HandheldsMemberjjsf:FoodServiceMember2018-09-302019-09-280000785956jjsf:HandheldsMemberjjsf:FoodServiceMember2017-10-012018-09-290000785956jjsf:HandheldsMemberjjsf:FoodServiceMember2016-09-252017-09-300000785956jjsf:BakeryMemberjjsf:FoodServiceMember2018-09-302019-09-280000785956jjsf:BakeryMemberjjsf:FoodServiceMember2017-10-012018-09-290000785956jjsf:BakeryMemberjjsf:FoodServiceMember2016-09-252017-09-300000785956jjsf:OtherProductsMemberjjsf:FoodServiceMember2018-09-302019-09-280000785956jjsf:OtherProductsMemberjjsf:FoodServiceMember2017-10-012018-09-290000785956jjsf:OtherProductsMemberjjsf:FoodServiceMember2016-09-252017-09-300000785956jjsf:FoodServiceMember2018-09-302019-09-280000785956jjsf:FoodServiceMember2017-10-012018-09-290000785956jjsf:FoodServiceMember2016-09-252017-09-300000785956jjsf:SoftPretzelsMemberjjsf:RetailSupermarketMember2018-09-302019-09-280000785956jjsf:SoftPretzelsMemberjjsf:RetailSupermarketMember2017-10-012018-09-290000785956jjsf:SoftPretzelsMemberjjsf:RetailSupermarketMember2016-09-252017-09-300000785956jjsf:FrozenJuicesAndIcesMemberjjsf:RetailSupermarketMember2018-09-302019-09-280000785956jjsf:FrozenJuicesAndIcesMemberjjsf:RetailSupermarketMember2017-10-012018-09-290000785956jjsf:FrozenJuicesAndIcesMemberjjsf:RetailSupermarketMember2016-09-252017-09-300000785956jjsf:HandheldsMemberjjsf:RetailSupermarketMember2018-09-302019-09-280000785956jjsf:HandheldsMemberjjsf:RetailSupermarketMember2017-10-012018-09-290000785956jjsf:HandheldsMemberjjsf:RetailSupermarketMember2016-09-252017-09-300000785956jjsf:CouponRedemtionMemberjjsf:RetailSupermarketMember2018-09-302019-09-280000785956jjsf:CouponRedemtionMemberjjsf:RetailSupermarketMember2017-10-012018-09-290000785956jjsf:CouponRedemtionMemberjjsf:RetailSupermarketMember2016-09-252017-09-300000785956jjsf:OtherProductsMemberjjsf:RetailSupermarketMember2018-09-302019-09-280000785956jjsf:OtherProductsMemberjjsf:RetailSupermarketMember2017-10-012018-09-290000785956jjsf:OtherProductsMemberjjsf:RetailSupermarketMember2016-09-252017-09-300000785956jjsf:RetailSupermarketMember2018-09-302019-09-280000785956jjsf:RetailSupermarketMember2017-10-012018-09-290000785956jjsf:RetailSupermarketMember2016-09-252017-09-300000785956jjsf:BeverageMemberjjsf:FrozenBeveragesMember2018-09-302019-09-280000785956jjsf:BeverageMemberjjsf:FrozenBeveragesMember2017-10-012018-09-290000785956jjsf:BeverageMemberjjsf:FrozenBeveragesMember2016-09-252017-09-300000785956jjsf:RepairAndMaintenanceServiceMemberjjsf:FrozenBeveragesMember2018-09-302019-09-280000785956jjsf:RepairAndMaintenanceServiceMemberjjsf:FrozenBeveragesMember2017-10-012018-09-290000785956jjsf:RepairAndMaintenanceServiceMemberjjsf:FrozenBeveragesMember2016-09-252017-09-300000785956jjsf:MachineSalesMemberjjsf:FrozenBeveragesMember2018-09-302019-09-280000785956jjsf:MachineSalesMemberjjsf:FrozenBeveragesMember2017-10-012018-09-290000785956jjsf:MachineSalesMemberjjsf:FrozenBeveragesMember2016-09-252017-09-300000785956jjsf:OtherProductsMemberjjsf:FrozenBeveragesMember2018-09-302019-09-280000785956jjsf:OtherProductsMemberjjsf:FrozenBeveragesMember2017-10-012018-09-290000785956jjsf:OtherProductsMemberjjsf:FrozenBeveragesMember2016-09-252017-09-300000785956jjsf:FrozenBeveragesMember2018-09-302019-09-280000785956jjsf:FrozenBeveragesMember2017-10-012018-09-290000785956jjsf:FrozenBeveragesMember2016-09-252017-09-300000785956jjsf:FoodServiceMember2017-09-300000785956jjsf:RetailSupermarketMember2017-09-300000785956jjsf:FrozenBeveragesMember2017-09-300000785956us-gaap:AccumulatedTranslationAdjustmentMember2018-09-290000785956us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2018-09-290000785956us-gaap:AccumulatedTranslationAdjustmentMember2018-09-302019-09-280000785956us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2018-09-302019-09-280000785956us-gaap:AccumulatedTranslationAdjustmentMember2019-09-280000785956us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2019-09-280000785956us-gaap:AccumulatedTranslationAdjustmentMember2017-09-300000785956us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2017-09-300000785956us-gaap:AccumulatedTranslationAdjustmentMember2017-10-012018-09-290000785956us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2017-10-012018-09-2900007859562018-09-302018-12-2900007859562018-12-302019-03-3000007859562019-03-312019-06-2900007859562019-06-302019-09-280000785956jjsf:ICEEDistributorMemberus-gaap:SubsequentEventMember2019-10-012019-10-010000785956jjsf:AcquiredAssetsOfICEEDistributorsLLCMemberus-gaap:SubsequentEventMember2019-10-012019-10-01

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED SEPTEMBER 28, 2019

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO

Commission File No. 000-14616

Registrant's telephone number, including area code: (856) 665-9533

J&J SNACK FOODS CORP.

(Exact name of registrant as specified in its charter)

| New Jersey |

22-1935537 |

| (State or other jurisdiction of |

(I.R.S. Employer Identification No.) |

| incorporation or organization) |

|

| |

|

| 6000 Central Highway |

08109 |

| Pennsauken, New Jersey |

(Zip Code) |

| (Address of principal executive offices) |

|

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of Each Class |

Trading Symbols(s) |

Name of Each Exchange on Which Registered |

| Common Stock, no par value |

JJSF |

The NASDAQ Global Select Market |

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☒ Non-accelerated filer ☐ |

Accelerated filer ☐ Smaller reporting company ☐ Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

March 29, 2019 was the last business day of the registrant’s most recently completed second fiscal quarter. The aggregate market value of the registrant’s common stock held by non-affiliates was $2,393,370,414, based on the last sale price on March 29, 2019 of $158.54 per share. As of November 11, 2019, 18,898,529 shares of the registrant’s common stock were issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for its Annual Meeting of Shareholders scheduled for February 11, 2020 are incorporated by reference into Part III of this report.

J & J SNACK FOODS CORP.

2017 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS

| Page |

| PART I |

|

| Note About Forward-Looking Statements |

1 |

|

| Item 1 |

Business |

1 |

|

| Item 1A |

Risk Factors |

6 |

|

| Item 1B |

Unresolved Staff Comments |

10 |

|

| Item 2 |

Properties |

10 |

|

| Item 3 |

Legal Proceedings |

11 |

|

| Item 4 |

Mine Safety Disclosures |

11 |

|

| |

|

|

|

| PART II |

|

| |

|

|

|

| Item 5 |

Market For Registrant’s Common Equity, Related Stockholder Matters And Issuer Purchases Of Equity Securities |

12 |

|

| Item 6 |

Selected Financial Data |

13 |

|

| Item 7 |

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations |

14 |

|

| Item 7A |

Quantitative And Qualitative Disclosures About Market Risk |

26 |

|

| Item 8 |

Financial Statements And Supplementary Data |

27 |

|

| Item 9 |

Changes In And Disagreements With Accountants On Accounting And Financial Disclosure |

27 |

|

| Item 9A |

Controls and Procedures |

27 |

|

| Item 9B |

Other Information |

28 |

|

| |

|

|

|

| PART III |

|

| |

|

|

|

| Item 10 |

Directors, Executive Officers and Corporate Governance |

29 |

|

| Item 11 |

Executive Compensation |

30 |

|

| Item 12 |

Security Ownership Of Certain Beneficial Owners And Management And Related Stockholder Matters |

30 |

|

| Item 13 |

Certain Relationships And Related Transactions, and Director Independence |

30 |

|

| Item 14 |

Principal Accountant Fees and Service |

30 |

|

| |

|

|

|

| PART IV |

|

| |

|

|

|

| Item 15 |

Exhibits, Financial Statement Schedules |

31 |

|

Note About Forward-Looking Statements

In addition to historical information, this report contains forward-looking statements. The forward-looking statements contained herein are subject to certain risks and uncertainties that could cause actual results to differ materially from those projected in the forward-looking statements. Important factors that might cause such a difference include, but are not limited to, those discussed in the “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Readers are cautioned not to place undue reliance on these forward-looking statements, which reflect management’s analysis only as of the date hereof. We undertake no obligation to publicly revise or update these forward-looking statements to reflect events or circumstances that arise after the date hereof.

Part I

General

J & J Snack Foods Corp. (the “Company” or “J & J”) manufactures snack foods and distributes frozen beverages which it markets nationally to the food service and retail supermarket industries. The Company’s principal snack food products are soft pretzels marketed primarily under the brand names SUPERPRETZEL, BRAUHAUS, AUNTIE ANNE’S* and BAVARIAN BAKERY, frozen juice treats and desserts marketed primarily under the LUIGI’S, WHOLE FRUIT, ICEE, PHILLY SWIRL, SOUR PATCH** and MINUTE MAID*** brand names, churros marketed primarily under the TIO PEPE’S and CALIFORNIA CHURROS brand names and bakery products sold primarily under the READI-BAKE, COUNTRY HOME, MARY B’S, DADDY RAY’S and HILL & VALLEY brand names as well as for private label and contract packing. J & J believes it is the largest manufacturer of soft pretzels in the United States. Other snack food products include funnel cake sold under THE FUNNEL CAKE FACTORY brand and dough enrobed handheld products sold under the PATIO brand and other smaller brands as well. The Company’s principal frozen beverage products are the ICEE brand frozen carbonated beverage and the SLUSH PUPPIE brand frozen non-carbonated beverage.

The Company’s Food Service and Frozen Beverages sales are made primarily to food service customers including snack bar and food stand locations in leading chain, department, discount, warehouse club and convenience stores; malls and shopping centers; fast food and casual dining restaurants; stadiums and sports arenas; leisure and theme parks; movie theatres; independent retailers; and schools, colleges and other institutions. The Company’s retail supermarket customers are primarily supermarket chains.

The Company was incorporated in 1971 under the laws of the State of New Jersey.

The Company has made acquisitions as described in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes thereto.

The Company operates in three business segments: Food Service, Retail Supermarkets and Frozen Beverages. These segments are described below.

The Chief Operating Decision Maker for Food Service and Retail Supermarkets and the Chief Operating Decision Maker for Frozen Beverages monthly review detailed operating income statements and sales reports in order to assess performance and allocate resources to each individual segment. Sales and operating income are key variables monitored by the Chief Operating Decision Makers and management when determining each segment’s and the company’s financial condition and operating performance. In addition, the Chief Operating Decision Makers review and evaluate depreciation, capital spending and assets of each segment on a quarterly basis to monitor cash flow and asset needs of each segment (see Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 8 – Financial Statements and Supplementary Data for financial information about segments).

| * |

AUNTIE ANNE’S is a registered trademark of Auntie Anne’s LLC |

| ** |

SOUR PATCH is a registered trademark of Mondelçz International Group |

| *** |

Minute Maid is a registered trademark of the Coca-Cola Company |

Food Service

The primary products sold by the food service segment are soft pretzels, frozen juice treats and desserts, churros, dough enrobed handheld products and baked goods. Our customers in the food service segment include snack bars and food stands in chain, department and discount stores; malls and shopping centers; casual dining restaurants; fast food and casual dining restaurants; stadiums and sports arenas; leisure and theme parks; convenience stores; movie theatres; warehouse club stores; schools, colleges and other institutions. Within the food service industry, our products are purchased by the consumer primarily for consumption at the point-of-sale.

Retail Supermarkets

The primary products sold to the retail supermarket channel are soft pretzel products – including SUPERPRETZEL and AUNTIE ANNE’S, frozen juice treats and desserts including LUIGI’S Real Italian Ice, MINUTE MAID Juice Bars and Soft Frozen Lemonade, WHOLE FRUIT frozen fruit bars and sorbet, PHILLY SWIRL cups and sticks, SOUR PATCH sticks, ICEE Squeeze-Up Tubes and dough enrobed handheld products including PATIO burritos. Within the retail supermarket channel, our frozen and prepackaged products are purchased by the consumer for consumption at home.

Frozen Beverages

We sell frozen beverages to the food service industry primarily under the names ICEE, SLUSH PUPPIE and PARROT ICE in the United States, Mexico and Canada. We also provide repair and maintenance service to customers for customers’ owned equipment.

Products

Soft Pretzels

The Company’s soft pretzels are sold under many brand names; some of which are: SUPERPRETZEL, PRETZEL FILLERS, PRETZELFILS, GOURMET TWISTS, MR. TWISTER, SOFT PRETZEL BITES, SOFTSTIX, SOFT PRETZEL BUNS, TEXAS TWIST, BAVARIAN BAKERY, SUPERPRETZEL BAVARIAN, NEW YORK PRETZEL, KIM & SCOTT’S GOURMET PRETZELS, SERIOUSLY TWISTED!, BRAUHAUS, AUNTIE ANNE’S AND LABRIOLA; and, to a lesser extent, under private labels.

Soft pretzels are sold in the Food Service and Retail Supermarket segments. Soft pretzel sales amounted to 21% of the Company’s revenue in fiscal year 2019, 21% in 2018 and 20% in 2017

Certain of the Company’s soft pretzels qualify under USDA regulations as the nutritional equivalent of bread for purposes of the USDA school lunch program, thereby enabling a participating school to obtain partial reimbursement of the cost of the Company’s soft pretzels from the USDA.

The Company’s soft pretzels are manufactured according to a proprietary formula. Soft pretzels, ranging in size from one to twenty-four ounces in weight, are shaped and formed by the Company’s twister machines. These soft pretzel tying machines are automated, high-speed machines for twisting dough into the traditional pretzel shape. Additionally, we make soft pretzels which are extruded or shaped by hand. Soft pretzels, after processing, are primarily quick-frozen in either raw or baked form and packaged for delivery.

The Company’s principal marketing program in the Food Service segment includes supplying ovens, mobile merchandisers, display cases, warmers and similar merchandising equipment to the retailer to prepare and promote the sale of soft pretzels. Some of this equipment is proprietary, including combination warmer and display cases that reconstitute frozen soft pretzels while displaying them, thus eliminating the need for an oven. The Company retains ownership of the equipment placed in customer locations, and as a result, customers are not required to make an investment in equipment.

Frozen Juice Treats and Desserts

The Company’s frozen juice treats and desserts are marketed primarily under the LUIGI’S, WHOLE FRUIT, PHILLY SWIRL, SOUR PATCH, ICEE and MINUTE MAID brand names. Frozen juice treats and desserts are sold in the Food Service and Retail Supermarkets segments. Frozen juice treats and dessert sales were 10% of the Company’s revenue in fiscal year 2019, 10% in 2018 and 11% in 2017.

The Company’s school food service LUIGI’S and WHOLE FRUIT frozen juice bars and cups contain three to four ounces of 100% apple or pineapple juice with no added sugar and 100% of the daily US FDA value of vitamin C. The juice bars are produced in various flavors and are packaged in a sealed push-up paper container referred to as the Milliken M-pak, which the Company believes has certain sanitary and safety advantages.

The balance of the Company’s frozen juice treats and desserts products are manufactured from water, sweeteners and fruit juice concentrates in various flavors and packaging including cups, tubes, sticks, M-paks and pints. Several of the products contain ice cream and WHOLE FRUIT contains pieces of fruit.

Churros

The Company’s churros are sold primarily under the TIO PEPE’S and CALIFORNIA CHURROS brand names. Churros are sold to the Food Service and Retail Supermarkets segments. Churro sales were 6% of the Company’s sales in fiscal year 2019, 6% in 2018 and 6% in 2017. Churros are Hispanic pastries in stick form which the Company produces in several sizes according to a proprietary formula. The churros are deep fried, frozen and packaged. At food service point-of-sale they are reheated and topped with a cinnamon sugar mixture. The Company also sells fruit and crème-filled churros. The Company supplies churro merchandising equipment similar to that used for its soft pretzels.

Handheld Products

The Company's dough enrobed handheld products are marketed under the PATIO, SUPREME STUFFERS and SWEET STUFFERS brand names and under private labels. Handheld products are sold to the Food Service and Retail Supermarket segments. Handheld product sales amounted to 4% of the Company’s sales in fiscal year 2019, 5% in 2018 and 5% in 2017.

Bakery Products

The Company’s bakery products are marketed under the MRS. GOODCOOKIE, READI-BAKE, COUNTRY HOME, MARY B’S, DADDY RAY’S and HILL & VALLEY brand names, and under private labels. Bakery products include primarily biscuits, fig and fruit bars, cookies, breads, rolls, crumb, muffins and donuts. Bakery products are sold to the Food Service segment. Bakery products sales amounted to 32% of the Company’s sales in fiscal year 2019, 33% in 2018 and 32% in 2017.

Frozen Beverages

The Company markets frozen beverages primarily under the names ICEE, SLUSH PUPPIE and PARROT ICE which are sold primarily in the United States, Mexico and Canada. Frozen beverages are sold in the Frozen Beverages segment.

Frozen beverage sales amounted to 15% of the Company’s revenue in fiscal year 2019, 15% in 2018 and 15% in 2017.

Under the Company’s principal marketing program for frozen carbonated beverages, it installs frozen beverage dispensers for its ICEE brand at customer locations and thereafter services the machines, arranges to supply customers with ingredients required for production of the frozen beverages, and supports customer retail sales efforts with in-store promotions and point-of-sale materials. The Company sells frozen non-carbonated beverages under the SLUSH PUPPIE and PARROT ICE brands through a distributor network and through its own distribution network. The Company also provides repair and maintenance service to customers for customers’ owned equipment and sells equipment in its Frozen Beverages segment. Revenue from equipment sales and repair and maintenance services totaled 11% of the Company’s sales in fiscal year 2019, 10% in 2018 and 9% in 2017.

Each new frozen carbonated customer location requires a frozen beverage dispenser supplied by the Company or by the customer. Company-supplied frozen carbonated dispensers are purchased from outside vendors or rebuilt by the Company.

The Company provides managed service and/or products to approximately 145,000 Company-owned and customer-owned dispensers.

The Company has the rights to market and distribute frozen beverages under the name ICEE to the entire continental United States (except for portions of two states) as well as internationally.

Other Products

Other products sold by the Company include funnel cakes sold under the FUNNEL CAKE FACTORY brand name and smaller amounts of various other food products. These products are sold in the Food Service and Frozen Beverages segments.

Customers

The Company sells its products to two principal channels: food service and retail supermarkets. The primary products sold to the food service channel are soft pretzels, frozen beverages, frozen juice treats and desserts, churros, dough enrobed handheld products and baked goods. The primary products sold to the retail supermarket channel are soft pretzels, frozen juice treats and desserts and dough enrobed handheld products.

We have several large customers that account for a significant portion of our sales. Our top ten customers accounted for 43%, 43% and 42% of our sales during fiscal years 2019, 2018 and 2017, respectively, with our largest customer accounting for 11% of our sales in 2019, 9-1/2% of our sales in 2018 and 9-1/2% of our sales in 2017. Four of the ten customers are food distributors who sell our product to many end users. The loss of one or more of our large customers could adversely affect our results of operations. These customers typically do not enter into long-term contracts and make purchase decisions based on a combination of price, product quality, consumer demand and customer service performance. If our sales to one or more of these customers are reduced, this reduction may adversely affect our business. If receivables from one or more of these customers become uncollectible, our operating income would be adversely impacted.

The Food Service and the Frozen Beverages segments sell primarily to food service channels. The Retail Supermarkets segment sells primarily to the retail supermarket channel.

The Company’s customers in the food service segment include snack bars and food stands in chain, department and mass merchandising stores, malls and shopping centers, fast food and casual dining restaurants, stadiums and sports arenas, leisure and theme parks, convenience stores, movie theatres, warehouse club stores, schools, colleges and other institutions, and independent retailers. Machines and machine parts are sold to other food and beverage companies. Within the food service industry, the Company’s products are purchased by the consumer primarily for consumption at the point-of-sale.

The Company sells its products to an estimated 85-90% of supermarkets in the United States. Products sold to retail supermarket customers are primarily soft pretzel products, including SUPERPRETZEL and AUNTIE ANNE’S, frozen juice treats and desserts including LUIGI’S Real Italian Ice, MINUTE MAID Juice Bars and Soft Frozen Lemonade, WHOLE FRUIT frozen fruit bars, WHOLE FRUIT Sorbet, PHILLY SWIRL cups and sticks, MARY B’S biscuits and dumplings, DADDY RAY’S fig and fruit bars, HILL & VALLEY baked goods, ICEE Squeeze-Up Tubes and PATIO burritos. Within the retail supermarket industry, the Company’s frozen and prepackaged products are purchased by the consumer for consumption at home.

Marketing and Distribution

The Company has developed a national marketing program for its products. For the Food Service and Frozen Beverages segments’ customers, this marketing program includes providing ovens, mobile merchandisers, display cases, warmers, frozen beverage dispensers and other merchandising equipment for the individual customer’s requirements and point-of-sale materials as well as participating in trade shows and in-store demonstrations. The Company’s ongoing advertising and promotional campaigns for its Retail Supermarket segment’s products include trade shows, newspaper advertisements with coupons and consumer advertising campaigns.

The Company develops and introduces new products on a routine basis. The Company evaluates the success of new product introductions on the basis of sales levels, which are reviewed no less frequently than monthly by the Company’s Chief Operating Decision Makers.

The Company’s products are sold through a network of about 100 food brokers, independent sales distributors and the Company’s own direct sales force. For its snack food products, the Company maintains warehouse and distribution facilities in Pennsauken, Bellmawr and Bridgeport, New Jersey; Vernon (Los Angeles) and Colton, California; Brooklyn, New York; Scranton, Pittsburgh, Hatfield and Lancaster, Pennsylvania; Carrollton (Dallas), Texas; Atlanta, Georgia; Moscow Mills (St. Louis), Missouri; Pensacola and Tampa, Florida; Solon, Ohio; Weston, Oregon; Holly Ridge, North Carolina; Alsip (Chicago) and Rock Island, Illinois. Frozen beverages and machine parts are distributed from 166 Company managed warehouse and distribution facilities located in 43 states, Mexico and Canada, which allow the Company to directly service its customers in the surrounding areas. The Company’s products are shipped in refrigerated and other vehicles from the Company’s manufacturing and warehouse facilities on a fleet of Company operated tractor-trailers, trucks and vans, as well as by independent carriers.

Seasonality

The Company’s sales are seasonal because frozen beverage sales and frozen juice treats and desserts sales are generally higher during the warmer months.

Trademarks and Patents

The Company has numerous trademarks, the most important of which are SUPERPRETZEL, TEXAS TWIST, NEW YORK PRETZEL, BAVARIAN BAKERY, MR. TWISTER, SOFT PRETZEL BITES, SOFTSTIX, PRETZEL FILLERS, PRETZELFILS, BRAUHAUS and LABRIOLA for its pretzel products; SHAPE-UPS, WHOLE FRUIT, PHILLY SWIRL and LUIGI’S for its frozen juice treats and desserts; TIO PEPE’S and CALIFORNIA CHURROS for its churros; ARCTIC BLAST, SLUSH PUPPIE and PARROT ICE for its frozen beverages; FUNNEL CAKE FACTORY for its funnel cake products, PATIO for its handheld burritos and MRS. GOODCOOKIE, READI-BAKE, COUNTRY HOME, CAMDEN CREEK, MARY B’S, DADDY RAY’S and HILL & VALLEY for its bakery products.

The Company markets frozen beverages under a license to use the trademark ICEE in all of the continental United States, except for portions of four states, and in Mexico and Canada. Additionally, the Company has the international rights to the trademark ICEE.

The trademarks, when renewed and continuously used, have an indefinite term and are considered important to the Company as a means of identifying its products. The Company considers its trademarks important to the success of its business.

The Company has numerous patents related to the manufacturing and marketing of its product.

Supplies

The Company’s manufactured products are produced from raw materials which are readily available from numerous sources. With the exception of the Company’s churro production equipment, funnel cake production equipment and soft pretzel twisting equipment, all of which are made for J & J by independent third parties, and certain specialized packaging equipment, the Company’s manufacturing equipment is readily available from various sources. Syrup for frozen beverages is purchased primarily from The Coca-Cola Company, Dr Pepper Snapple Group, Inc., the Pepsi Cola Company, and Jogue, Inc. Cups, straws and lids are readily available from various suppliers. Parts for frozen beverage dispensing machines are purchased from several sources. Frozen beverage dispensers are purchased primarily from IMI Cornelius, Inc. and FBD Partnership.

Competition

Snack food and bakery products markets are highly competitive. The Company’s principal products compete against similar and different food products manufactured and sold by numerous other companies, some of which are substantially larger and have greater resources than the Company. As the soft pretzel, frozen juice treat and dessert, bakery products and related markets evolve, additional competitors and new competing products may enter the markets. Competitive factors in these markets include product quality, customer service, taste, price, identity and brand name awareness, method of distribution and sales promotions.

The Company believes it is the only national distributor of soft pretzels. However, there are numerous regional and local manufacturers of food service and retail supermarket soft pretzels as well as several chains of retail pretzel stores.

In Frozen Beverages the Company competes directly with other frozen beverage companies. These include several companies which have the right to use the ICEE name in portions of four states. There are many other regional frozen beverage competitors throughout the country and one large retail chain which uses its own frozen beverage brand.

The Company competes with large soft drink manufacturers for counter and floor space for its frozen beverage dispensing machines at retail locations and with products which are more widely known than the ICEE, SLUSH PUPPIE and PARROT ICE frozen beverages.

The Company competes with several other companies in the frozen juice treat and dessert and bakery products markets.

Risks Associated with Foreign Operations

Foreign operations generally involve greater risk than doing business in the United States. Foreign economies differ favorably or unfavorably from the United States’ economy in such respects as the level of inflation and debt, which may result in fluctuations in the value of the country’s currency and real property. Sales of our foreign operations were $33,906,000, $32,459,000 and $31,001,000 in fiscal years 2019, 2018 and 2017, respectively. At September 28, 2019, the total assets of our foreign operations were approximately $26 million or 2.6% of total assets which was significantly less than the prior year as we moved cash to the United States. At September 29, 2018, the total assets of our foreign operations were approximately $45 million or 4.8% of total assets.

Employees

The Company has about 4,600 full and part time employees and approximately 1,500 workers employed by staffing agencies as of September 28, 2019. About 1,200 production and distribution employees throughout the Company are covered by collective bargaining agreements.

The Company considers its employee relations to be good.

Available Information

The Company’s internet address is www.jjsnack.com. On the investor relations section of its website, the Company provides free access to its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to these reports, as soon as reasonably practicable after such materials are electronically filed with, or furnished to, the Securities and Exchange Commission (“SEC”). The information on the website listed above is not and should not be considered part of this annual report on Form 10-K and is not incorporated by reference in this document.

You should carefully consider the risks described below, together with all of the other information included in this report, in considering our business and prospects. The risks and uncertainties described below are not the only ones facing us. Additional risks and uncertainties not presently known to us or that we currently deem insignificant may also impair our business operations. Following is a discussion of known potentially significant risks which could result in harm to our business, financial condition or results of operations.

Risks of Shortages or Increased Cost of Raw Materials

We are exposed to the market risks arising from adverse changes in commodity prices, affecting the cost of our raw materials and energy. The raw materials and energy which we use for the production and distribution of our products are largely commodities that are subject to price volatility and fluctuations in availability caused by changes in global supply and demand, weather conditions, agricultural uncertainty or governmental controls. We purchase these materials and energy mainly in the open market. Our procurement practices are intended to reduce the risk of future price increases, but also may potentially limit the ability to benefit from possible price decreases. If commodity price changes result in increases in raw materials and energy costs, we may not be able to increase our prices to offset these increased costs without suffering reduced volume, revenue and operating income.

General Risks of the Food Industry

Food processors are subject to the risks of adverse changes in general economic conditions; evolving consumer preferences and nutritional and health-related concerns; changes in food distribution channels; federal, state and local food processing controls or other mandates; changes in federal, state, local and international laws and regulations, or in the application of such laws and regulations; consumer product liability claims; risks of product tampering and contamination; and negative publicity surrounding actual or perceived product safety deficiencies. The increased buying power of large supermarket chains, other retail outlets and wholesale food vendors could result in greater resistance to price increases and could alter the pattern of customer inventory levels and access to shelf space.

Risks of Shortages or Increased Costs of Labor

Our businesses operate in highly competitive markets. The labor market in the United States is very competitive and the unemployment rate is at historic lows. We depend on the skills, working relationships, and continued services of key personnel, including our experienced management team. We must hire, train and develop effective employees. We compete with other companies both within and outside of our industry for talented personnel, and we may lose key personnel or fail to attract, train, and retain other talented personnel. In addition, our ability to achieve our operating goals depends on our ability to identify, hire, train, and retain qualified individuals. Any such loss or failure could adversely affect our product sales, financial condition, and operating results.

Environmental Risks

The disposal of solid and liquid waste material resulting from the preparation and processing of foods is subject to various federal, state and local laws and regulations relating to the protection of the environment. Such laws and regulations have an important effect on the food processing industry as a whole, requiring substantially all firms in the industry to incur material expenditures for modification of existing processing facilities and for construction of upgraded or new waste treatment facilities.

We cannot predict what environmental legislation or regulations will be enacted in the future, how existing or future laws or regulations will be administered or interpreted or what environmental conditions may be found to exist. Enactment of more stringent laws or regulations or more strict interpretation of existing laws and regulations may require additional expenditures by us, some of which could be material.

Risks Resulting from Customer Concentration

We have several large customers that account for a significant portion of our sales. Our top ten customers accounted for 43%, 43% and 42% of our sales during fiscal years 2019, 2018 and 2017, respectively, with our largest customer accounting for 11% of our sales in 2019, 9-1/2% of our sales in 2018 and 9-1/2% of our sales in 2017.

Four of the ten customers are food distributors who sell our product to many end users. The loss of one or more of our large customers could adversely affect our results of operations. These customers typically do not enter into long-term contracts and make purchase decisions based on a combination of price, product quality, consumer demand and customer service performance. If our sales to one or more of these customers are reduced, this reduction may adversely affect our business. If receivables from one or more of these customers become uncollectible, our operating income would be adversely impacted.

Competition

Our businesses operate in highly competitive markets. We compete against national and regional manufacturers and distributors on the basis of price, quality, product variety and effective distribution. Many of our major competitors in the market are larger and have greater financial and marketing resources than we do. Increased competition and anticipated actions by our competitors could lead to downward pressure on prices and/or a decline in our market share, either of which could adversely affect our results. See “Competition” in Item 1 for more information about our competitors.

Risks Relating to Manufacturing and Distribution

Our ability to purchase, manufacture and distribute products is critical to our success. Because we source certain products from single manufacturing sites, it is possible that we could experience a production disruption that results in a reduction or elimination of the availability of some of our products. If we are not able to obtain alternate production capability in a timely manner, or on favorable terms, it could have a negative impact on our business, results of operations, financial condition and cash flows, including the potential for long-term loss of product placement with various customers. We are also subject to risks of other business disruptions associated with our dependence on production facilities and distribution systems. Natural disasters, terrorist activity, cyberattacks or other unforeseen events could interrupt production or distribution and have a material adverse effect on our business, results of operations, financial condition and cash flows, including the potential for long-term loss of product placement with our customers.

Risks Relating to the Availability and Costs of Transportation

Our ability to obtain adequate and reasonably priced methods of transportation to distribute our products, including refrigerated trailers for many of our products, is a key factor to our success. Delays in transportation, including weather-related delays, could have a material adverse effect on our business and results of operations. Further, higher fuel costs and increased line haul costs due to industry capacity constraints, customer delivery requirements and a more restrictive regulatory environment could also negatively impact our financial results. We pay fuel surcharges that fluctuate with the price of diesel fuel to third-party transporters of our products, and such surcharges can be substantial. Any sudden or dramatic increases in the price of diesel fuel would serve to increase our fuel surcharges and our cost of goods sold. If we were unable to pass higher freight costs to our customers in the form of price increases, those higher costs could have a material adverse effect on our business, results of operations, financial condition and cash flows.

Risks Relating to Manufacturing Capacity Constraints

Our current manufacturing resources may be inadequate to meet significantly increased demand for some of our food products. Our ability to increase our manufacturing capacity depends on many factors, including the equipment delivery, construction lead-times, installation, qualification, regulatory permitting and regulatory requirements. A lack of sufficient manufacturing capacity to meet demand could cause our customer service levels to decrease, which may negatively affect customer demand for our products and customer relations generally, which in turn could have a material adverse effect on our business, results of operations, financial condition and cash flows. In addition, operating facilities at or near capacity may also increase production and distribution costs and negatively affect relations with our employees or contractors, which could result in disruptions in our operations.

New Jersey Law and Provisions of Our Amended and Restated Certificate of Incorporation and Bylaws May Inhibit a Change In Control

The New Jersey Shareholders' Protection Act, N.J.S.A. 14A:10A-1, et seq., may delay, deter or prevent a change in control by prohibiting the Company from engaging in a business combination transaction with an interested shareholder for a period of five years after the person becomes an interested stockholder, even if a majority of our shareholders believe a change in control would be in the best interests of the Company and its shareholders. In addition, our Amended and Restated Certificate of Incorporation and Bylaws contain provisions that may delay, deter or prevent a future acquisition of J & J Snack Foods Corp. not approved by our Board of Directors. This could occur even if our shareholders are offered an attractive value for their shares or if a substantial number or even a majority of our shareholders believe the takeover is in their best interest. These provisions are intended to encourage any person interested in acquiring us to negotiate with and obtain the approval of our Board of Directors in connection with the transaction. Provisions of our Amended and Restated Certificate of Incorporation and Bylaws that could delay, deter or prevent a future acquisition include the following:

| -- |

a classified Board of Directors; |

| -- |

the requirement that our shareholders may only remove Directors for cause; |

| -- |

limitations on share holdings and voting of certain persons; |

| -- |

special Director voting rights; |

| -- |

the ability of the Board of Directors to consider the interests of various constituencies, including our employees, customers, suppliers, creditors and the local communities in which we operate; |

| -- |

shareholders do not generally have the right to call special meetings or to act by written consent; |

| -- |

our Bylaws contain advance notice procedures for nominations of Directors or submission of shareholder proposals at an annual meeting; and |

| -- |

our Bylaws contain a forum selection clause providing that certain litigation against the Company can only be brought in New Jersey state or federal courts. |

Risks Relating to Gerald B. Shreiber

Gerald B. Shreiber is the founder, President, Chief Executive Officer and Chairman of the Board of Directors of the Company and the current beneficial owner of 19% of its outstanding common stock. Our Amended and Restated Certificate of Incorporation provides that Mr. Shreiber has three votes on any matter to be acted upon by the Board of Directors (subject to certain adjustments). Therefore, he and one other director would have the ability to approve any matter before the Board. The performance of the Company is greatly impacted by his leadership and decisions.

Risk Related to Increases in our Health Insurance Costs

The costs of employee health care insurance have been increasing in recent years due to rising health care costs, legislative changes, and general economic conditions. Because of the breadth and complexity of health care regulations as well as other health care reform legislation considered by Congress and state legislatures, we cannot predict with certainty the future effect of these laws on us. A continued increase in health care costs or additional costs incurred as a result of the Health Care Reform Laws or the enforcement of the Health Care Reform Laws or other future health care reform laws imposed by Congress or state legislations could have a negative impact on our financial position and results of operations.

Risk Related to Product Changes

There are risks in the marketplace related to trade and consumer acceptance of product improvements, packing initiatives and new product introductions.

Risks Related to Changes in the Business

Our ability to successfully manage changes to our business processes, including selling, distribution, product capacity, information management systems and the integration of acquisitions, will directly affect our results of operations.

Risks Associated with Foreign Operations

Foreign operations generally involve greater risk than doing business in the United States. Foreign economies differ favorably or unfavorably from the United States’ economy in such respects as the level of inflation and debt, which may result in fluctuations in the value of the country’s currency and real property. Further, there may be less government regulation in various countries, and difficulty in enforcing legal rights outside the United States. Additionally, in some foreign countries, there is the possibility of expropriation or confiscatory taxation limitations on the removal of property or other assets, political or social instability or diplomatic developments which could affect the operations and assets of U.S. companies doing business in that country. Sales of our foreign operations were $33,906,000, $32,459,000 and $31,001,000 in fiscal years 2019, 2018 and 2017, respectively. At September 28, 2019, the total assets of our foreign operations were approximately $26 million or 2.6% of total assets which was significantly less than the prior year as we moved cash to the United States. At September 29, 2018, the total assets of our foreign operations were approximately $45 million or 4.8% of total assets.

Risks Associated with our Information Technology Systems

The efficient operation of our business depends on our information technology systems. We rely on our information technology systems to effectively manage our business data, communications, supply chain, manufacturing, order entry and fulfillment, and other business processes. The failure of our information technology systems (including those provided to us by third parties) to perform as we anticipate could disrupt our business and could result in billing, collecting, and ordering errors, processing inefficiencies, and the loss of sales and customers, causing our business and results of operations to suffer.

Our information technology systems may be vulnerable to damage or interruption from circumstances beyond our control, including fire, natural disasters, systems failures, security breaches or intrusions (including theft of customer, consumer or other confidential data), and viruses. If we are unable to prevent physical and electronic break-ins, cyber-attacks and other information security breaches, we may suffer financial and reputational damage, be subject to litigation or incur remediation costs or penalties because of the unauthorized disclosure of confidential information belonging to us or to our partners, customers, suppliers or employees.

We may experience difficulties in implementing the final phases of our new enterprise resource planning system. We are in the late stages of a multi-year implementation of a new enterprise resource planning system (“ERP”), which is replacing our existing financial and operating systems. The design and implementation of this new ERP has required an investment of significant personnel and financial resources, including substantial expenditures for outside consultants and software. We may not be able to implement the ERP successfully without experiencing delays, increased costs and other difficulties, including potential design defects, miscalculations, testing requirements, and the diversion of management’s attention from day-to-day business operations. If we are unable to implement the new ERP as planned, the effectiveness of our internal control over financial reporting could be adversely affected, our ability to assess those controls adequately could be delayed, and our business, results of operations, financial condition and cash flows could be negatively impacted.

Risks Associated with Real or Perceived Safety Issues Regarding our Food Products

We sell food products for human consumption, which involves risks such as product contamination or spoilage, product tampering, other adulteration of food products, mislabeling, and misbranding. We can be impacted by both real and unfounded claims regarding the safety of our operations, or concerns regarding mislabeled, adulterated, contaminated or spoiled food products. Any of these circumstances could necessitate a voluntary or mandatory recall due to a substantial product hazard, a need to change a product’s labeling or other consumer safety concerns. A pervasive product recall may result in significant loss due to the costs of a recall, related legal claims, including claims arising from bodily injury or illness caused by our products, the destruction of product inventory, or lost sales due to product unavailability. A highly publicized product recall, whether involving us or any related products made by third parties, also could result in a loss of customers or an unfavorable change in consumer sentiment regarding our products or any category in which we operate. In addition, an allegation of noncompliance with federal or state food laws and regulations could force us to cease production, stop selling our products or create significant adverse publicity that could harm our credibility and decrease market acceptance of our products. Any of these events could have a material adverse effect on our business, results of operations, financial condition and cash flows.

Seasonality and Quarterly Fluctuations

Our sales are affected by the seasonal demand for our products. Demand is greater during the summer months primarily as a result of the warm weather demand for our ICEE and frozen juice treats and desserts products. Because of seasonal fluctuations, there can be no assurance that the results of any particular quarter will be indicative of results for the full year or for future years.

| Item 1B. |

Unresolved Staff Comments |

We have no unresolved SEC staff comments to report.

The Company’s primary east coast manufacturing facility is located in Pennsauken, New Jersey in a 70,000 square foot building on a two-acre lot. Soft pretzels, churros, and funnel cake are manufactured at this Company-owned facility which also serves as the Company’s corporate headquarters. The Company owns a 128,000 square foot building adjacent to this manufacturing facility which contains a large freezer for warehousing and distribution purposes. The Company leases, through January 2022, 16,000 square feet of office and warehouse space located next to the Pennsauken, New Jersey plant and owns a 43,000 square foot office and warehouse building in the same complex.

The Company owns a 150,000 square foot building on eight acres in Bellmawr, New Jersey. The facility is used by the Company to manufacture soft pretzels.

The Company’s primary west coast manufacturing facility is located in Vernon (Los Angeles), California. It consists of a 137,000 square foot facility in which soft pretzels, churros and various lines of baked goods are produced and warehoused. Included in the 137,000 square foot facility is a 30,000 square foot freezer used for warehousing and distribution purposes. The facility is leased through November 2030. The Company leases an additional 80,000 square feet of office and warehouse space, adjacent to its manufacturing facility, through November 2030.

The Company leases a 22,000 square foot soft pretzel manufacturing facility located in Brooklyn, New York. The lease runs through August 2023.

The Company leases through June 2030 a 45,000 square foot churros and funnel cake manufacturing facility located in Colton, California.

The Company leases an 85,000 square foot bakery manufacturing facility located in Atlanta, Georgia. The lease runs through December 2020.

The Company leases a 129,000 square foot bakery manufacturing facility located in Rock Island, Illinois. The lease runs through December 2034.

The Company owns a 46,000 square foot frozen juice treat and dessert manufacturing facility and a 42,000 square foot dry storage warehouse located on six acres in Scranton, Pennsylvania.

The Company leases a 29,600 square foot soft pretzel manufacturing facility located in Hatfield, Pennsylvania. The lease runs through June 2032.

The Company leases a 48,000 square foot soft pretzel manufacturing facility located in Carrollton, Texas. The lease runs through April 2026. The Company leases an additional property containing a 6,500 square foot storage freezer across the street from the manufacturing facility, which lease expires May 2021.

The Company leases a 177,500 square foot soft pretzel manufacturing facility located in Alsip, Illinois. The lease runs through March 2030.

The Company’s fresh bakery products manufacturing facility and offices are located in Bridgeport, New Jersey in three buildings totaling 133,000 square feet. The buildings are leased through December 2025.

The Company owns a 165,000 square foot fig and fruit bar manufacturing facility located on 9-1/2 acres in Moscow Mills (St. Louis), Missouri.

The Company owns an 84,000 square foot handheld products manufacturing facility in Holly Ridge, North Carolina.

The Company leases a 70,000 square foot handheld products manufacturing facility in Weston, Oregon which is leased through May 13, 2021.

The Company leases a 39,000 square foot frozen juice treat and dessert manufacturing facility in Tampa, Florida which is leased through September 2023.

The Company also leases approximately 160 warehouse and distribution facilities in 44 states, Mexico and Canada.

| Item 3. |

Legal Proceedings |

The Company has no material pending legal proceedings, other than ordinary routine litigation incidental to the business, to which the Company or any of its subsidiaries is a party or of which any of their property is subject.

| Item 4. |

Mine Safety Disclosures |

Not Applicable

PART II

| Item 5. |

Market For Registrant’s Common Equity, Related Stockholder Matters And Issuer Purchases Of Equity Securities |

The Company’s common stock is traded on the NASDAQ Global Select Market under the symbol “JJSF.” The following table sets forth the high and low sale price quotations as reported by NASDAQ and dividend information for the common stock for each quarter of the years ended September 29, 2018 and September 28, 2019.

| |

|

Common Stock Market Price |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

Dividend |

|

| |

|

High |

|

|

Low |

|

|

Declared |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Fiscal 2018 |

|

|

|

|

|

|

|

|

|

|

|

|

| First quarter |

|

$ |

157.33 |

|

|

$ |

127.00 |

|

|

$ |

0.4500 |

|

| Second quarter |

|

|

153.99 |

|

|

|

128.53 |

|

|

|

0.4500 |

|

| Third quarter |

|

|

158.41 |

|

|

|

125.98 |

|

|

|

0.4500 |

|

| Fourth quarter |

|

|

159.05 |

|

|

|

139.90 |

|

|

|

0.4500 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Fiscal 2019 |

|

|

|

|

|

|

|

|

|

|

|

|

| First quarter |

|

$ |

162.80 |

|

|

$ |

138.65 |

|

|

$ |

0.5000 |

|

| Second quarter |

|

|

162.84 |

|

|

|

138.40 |

|

|

|

0.5000 |

|

| Third quarter |

|

|

167.50 |

|

|

|

150.61 |

|

|

|

0.5000 |

|

| Fourth quarter |

|

|

196.84 |

|

|

|

159.63 |

|

|

|

0.5000 |

|

As of September 28, 2019, we had approximately 23,000 beneficial shareholders.

In our fiscal year ended September 30, 2017, we purchased and retired 142,665 shares of our common stock at a cost of $18,228,763.

In our fiscal year ended September 29, 2018, we purchased and retired 20,604 shares of our common stock at a cost of $2,794,027.

We did not purchase any shares of our common stock in our fiscal year ended September 28, 2019.

A plan to purchase 500,000 shares was announced on November 8, 2012. 500,000 shares were purchased under this plan with the last purchase in August 2017. A plan to purchase 500,000 shares was announced on August 4, 2017 with no expiration date. 384,506 shares remain to be purchased under this plan.

For information on the Company’s Equity Compensation Plans, please see Item 12 herein.

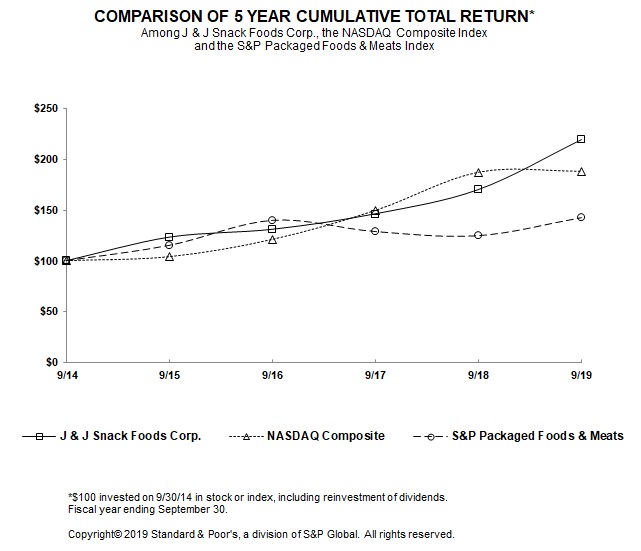

Stock Performance Graph

| Item 6. |

Selected Financial Data |

The selected financial data for the last five years was derived from our audited consolidated financial statements. The following selected financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes thereto, especially as the information pertains to fiscal 2017, 2018 and 2019.

| |

|

Fiscal year ended in September (In thousands except per share data) |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

2019 |

|

|

2018 |

|

|

2017 |

|

|

2016 |

|

|

2015 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net Sales |

|

$ |

1,186,487 |

|

|

$ |

1,138,265 |

|

|

$ |

1,084,224 |

|

|

$ |

992,781 |

|

|

$ |

976,256 |

|

| Net Earnings |

|

$ |

94,819 |

|

|

$ |

103,596 |

|

|

$ |

79,174 |

|

|

$ |

75,975 |

|

|

$ |

70,183 |

|

| Total Assets |

|

$ |

1,019,339 |

|

|

$ |

932,013 |

|

|

$ |

867,228 |

|

|

$ |

790,487 |

|

|

$ |

739,669 |

|

| Long-Term Debt |

|

$ |

- |

|

|

$ |

- |

|

|

$ |

- |

|

|

$ |

- |

|

|

$ |

- |

|

| Capital Lease Obligations |

|

$ |

1,057 |

|

|

$ |

1,077 |

|

|

$ |

1,244 |

|

|

$ |

1,600 |

|

|

$ |

1,469 |

|

| Stockholders' Equity |

|

$ |

833,751 |

|

|

$ |

759,091 |

|

|

$ |

682,322 |

|

|

$ |

637,974 |

|

|

$ |

599,919 |

|

| Common Share Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Earnings Per Diluted Share |

|

$ |

5.00 |

|

|

$ |

5.51 |

|

|

$ |

4.21 |

|

|

$ |

4.05 |

|

|

$ |

3.73 |

|

| Earnings Per Basic Share |

|

$ |

5.04 |

|

|

$ |

5.54 |

|

|

$ |

4.23 |

|

|

$ |

4.07 |

|

|

$ |

3.76 |

|

| Common Shares Outstanding At Year End |

|

|

18,895 |

|

|

|

18,754 |

|

|

|

18,663 |

|

|

|

18,668 |

|

|

|

18,676 |

|

| Cash Dividends Declared Per Common Share |

|

$ |

2.00 |

|

|

$ |

1.80 |

|

|

$ |

1.68 |

|

|

$ |

1.56 |

|

|

$ |

1.44 |

|

| Item 7. |

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations |