UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTIONS 13 AND 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended September 29, 2018

or,

o TRANSITION REPORT PURSUANT TO SECTIONS 13 AND 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File No. 1-09453

| ARK RESTAURANTS CORP. |

| (Exact Name of Registrant as Specified in Its Charter) |

| New York | 13-3156768 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(IRS Employer Identification No.) |

| 85 Fifth Avenue, New York, NY | 10003 |

| (Address of Principal Executive Offices) | (Zip Code) |

Registrant’s telephone number, including area code: (212) 206-8800

Securities registered pursuant to section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |||

| Common Stock, par value $.01 per share | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | |

| Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller Reporting Company x | |

| Emerging Growth Company o |

Indicate by check mark whether the Registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yes o No x

As of March 31, 2018, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of voting and non-voting stock held by non-affiliates of the registrant was $50,978,496.

At December 11, 2018, there were outstanding 3,474,681 shares of the Registrant’s Common Stock, $.01 par value.

DOCUMENTS INCORPORATED BY REFERENCE

(1) In accordance with General Instruction G (3) of Form 10-K, certain information required by Part III hereof will either be incorporated into this Form 10-K by reference to the registrant’s definitive proxy statement for the registrant’s 2018 Annual Meeting of Stockholders filed within 120 days of September 29, 2018 or will be included in an amendment to this Form 10-K filed within 120 days of September 29, 2018.

PART I

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

On one or more occasions, we may make statements in this Annual Report on Form 10-K regarding our assumptions, projections, expectations, targets, intentions or beliefs about future events. All statements, other than statements of historical facts, included or incorporated by reference herein relating to management’s current expectations of future financial performance, continued growth and changes in economic conditions or capital markets are forward looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Words or phrases such as “anticipates,” “believes,” “estimates,” “expects,” “intends,” “plans,” “predicts,” “projects,” “targets,” “will likely result,” “hopes,” “will continue” or similar expressions identify forward looking statements. Forward-looking statements involve risks and uncertainties which could cause actual results or outcomes to differ materially from those expressed. We caution that while we make such statements in good faith and we believe such statements are based on reasonable assumptions, including without limitation, management’s examination of historical operating trends, data contained in records and other data available from third parties, we cannot assure you that our projections will be achieved. Factors that may cause such differences include: economic conditions generally and in each of the markets in which we are located, the amount of sales contributed by new and existing restaurants, labor costs for our personnel, fluctuations in the cost of food products, adverse weather conditions, changes in consumer preferences and the level of competition from existing or new competitors.

We have attempted to identify, in context, certain of the factors that we believe may cause actual future experience and results to differ materially from our current expectation regarding the relevant matter or subject area. In addition to the items specifically discussed above, our business, results of operations and financial position and your investment in our common stock are subject to the risks and uncertainties described in “Item 1A Risk Factors” of this Annual Report on Form 10-K.

From time to time, oral or written forward-looking statements are also included in our reports on Forms 10-K, 10-K/A, 10-Q, 10-Q/A and 8-K, our Schedule 14A, our press releases and other materials released to the public. Although we believe that at the time made, the expectations reflected in all of these forward-looking statements are and will be reasonable; any or all of the forward-looking statements in this Annual Report on Form 10-K, our reports on Forms 10-Q, 10-Q/A and 8-K, our Schedule 14A and any other public statements that are made by us may prove to be incorrect. This may occur as a result of inaccurate assumptions or as a consequence of known or unknown risks and uncertainties. Many factors discussed in this Annual Report on Form 10-K, certain of which are beyond our control, will be important in determining our future performance. Consequently, actual results may differ materially from those that might be anticipated from forward-looking statements. In light of these and other uncertainties, you should not regard the inclusion of a forward-looking statement in this Annual Report on Form 10-K or other public communications that we might make as a representation by us that our plans and objectives will be achieved, and you should not place undue reliance on such forward-looking statements.

We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. However, your attention is directed to any further disclosures made on related subjects in our subsequent periodic reports filed with the Securities and Exchange Commission on Forms 10-Q and 8-K and Schedule 14A.

Unless the context requires otherwise, references to “we,” “us,” “our,” “ARKR” and the “Company” refer specifically to Ark Restaurants Corp. and its subsidiaries, partnerships, variable interest entities and predecessor entities.

| 3 |

| Item 1. | Business |

Overview

We are a New York corporation formed in 1983. As of the fiscal year ended September 29, 2018, we owned and/or operated 20 restaurants and bars, 19 fast food concepts and catering operations through our subsidiaries. Initially our facilities were located only in New York City. As of the fiscal year ended September 29, 2018, five of our restaurant and bar facilities are located in New York City, two are located in Washington, D.C., five are located in Las Vegas, Nevada, three are located in Atlantic City, New Jersey, one is located in the Faneuil Hall Marketplace in Boston, Massachusetts, two are located on the east coast of Florida and two are located on the gulf coast of Alabama.

In addition to the shift from a Manhattan-based operation to a multi-city operation, the nature of the facilities operated by us has shifted from smaller, neighborhood restaurants to larger, destination properties intended to benefit from high patron traffic attributable to the uniqueness of the location and catered events. Most of our properties which have been opened in recent years are of the latter description. As of the fiscal year ended September 29, 2018, these include the operations at the 12 fast food facilities in Tampa, Florida and Hollywood, Florida (2004); the Gallagher’s Steakhouse and Gallagher’s Burger Bar in the Resorts Atlantic City Hotel and Casino in Atlantic City, New Jersey (2005); Durgin Park Restaurant and the Black Horse Tavern in the Faneuil Hall Marketplace in Boston, Massachusetts (2007); Yolos at the Planet Hollywood Resort and Casino in Las Vegas, Nevada (2007); Robert at the Museum of Arts & Design at Columbus Circle in Manhattan (2010); Broadway Burger Bar and Grill at the New York New York Hotel and Casino in Las Vegas, Nevada (2011); Clyde Frazier’s Wine and Dine in Manhattan (2012); Broadway Burger Bar and Grill in the Quarter at the Tropicana Hotel and Casino in Atlantic City, New Jersey (2013), The Rustic Inn in Dania Beach, Florida (2014), Shuckers in Jensen Beach, Florida (2016) and two Original Oyster Houses, one in Gulf Shores, Alabama and one in Spanish Fort, Alabama (2017).

The names and themes of each of our restaurants are different except for our two Gallagher’s Steakhouse restaurants, two Broadway Burger Bar and Grill restaurants, and two Original Oyster House restaurants. The menus in our restaurants are extensive, offering a wide variety of high-quality foods at generally moderate prices. The atmosphere at many of the restaurants is lively and extremely casual. Most of the restaurants have separate bar areas, are open seven days a week and most serve lunch as well as dinner. A majority of our net sales are derived from dinner as opposed to lunch service.

While decor differs from restaurant to restaurant, interiors are marked by distinctive architectural and design elements which often incorporate dramatic interior open spaces and extensive glass exteriors. The wall treatments, lighting and decorations are typically vivid, unusual and, in some cases, highly theatrical.

| 4 |

The following table sets forth the restaurant properties we lease, own and operate as of September 29, 2018:

| Name | Location | Year Opened(1) |

Restaurant Size (Square Feet) |

Seating Capacity(2) Indoor- (Outdoor) |

Lease Expiration(3) | ||||||

| Sequoia | Washington Harbour Washington, D.C. |

1990 | 26,000 | 600 | (400) | 2032 | |||||

| Bryant Park Grill & Café | Bryant Park New York, New York |

1995 | 25,000 | 180 | (820) | 2025 | |||||

| America(4) | New York-New York Hotel and Casino Las Vegas, Nevada |

1997 | 20,000 | 450 | 2023 | ||||||

| Gallagher’s Steakhouse(4) | New York-New York Hotel & Casino Las Vegas, Nevada |

1997 | 5,500 | 260 | 2023 | ||||||

| Gonzalez y Gonzalez(4) | New York-New York Hotel & Casino Las Vegas, Nevada |

1997 | 2,000 | 120 | 2021 | ||||||

| Village Eateries (4)(5) | New York-New York Hotel & Casino Las Vegas, Nevada |

1997 | 6,300 | 400 | (*) | 2021 | |||||

| Robert | Museum of Arts & Design New York, New York |

2009 | 5,530 | 150 | 2035 | ||||||

| Thunder Grill | Union Station Washington, D.C. |

1999 | 10,000 | 500 | 2019 | ||||||

| Gallagher’s Steakhouse | Resorts Atlantic City Hotel and Casino Atlantic City, New Jersey |

2005 | 6,280 | 196 | 2020 | ||||||

| Gallagher’s Burger Bar | Resorts Atlantic City Hotel and Casino Atlantic City, New Jersey |

2005 | 2,270 | 114 | 2020 | ||||||

| 5 |

| Name | Location | Year Opened(1) |

Restaurant Size (Square Feet) |

Seating Capacity(2) Indoor- (Outdoor) |

Lease Expiration(3) | ||||||

| Durgin Park Restaurant and the Black Horse Tavern | Faneuil Hall Marketplace Boston, Massachusetts |

2007 | 18,500 | 575 | 2032 | ||||||

| Yolos | Planet Hollywood Resort and Casino Las Vegas, Nevada |

2007 | 4,100 | 206 | 2026 | ||||||

| Clyde Frazier’s Wine and Dine | Tenth Avenue (between 37th and 38th Streets) New York, New York |

2012 | 10,000 | 250 | 2032 | ||||||

| Broadway Burger Bar and Grill | Tropicana Hotel and Casino Atlantic City, New Jersey |

2013 | 6,825 | 225 | 2033 | ||||||

| The Rustic Inn | Dania Beach, Florida | 2014 | 16,150 | 575 | (75) | Owned | |||||

| Southwest Porch (6) | Bryant Park New York, New York |

2015 | 2,240 | 0 | (160) | 2025 | |||||

| Shuckers | Jensen Beach, Florida | 2016 | 7,310 | 220 | (170) | Owned | |||||

| The Original Oyster House | Gulf Shores, Alabama | 2017 | 9,230 | 300 | Owned | ||||||

| The Original Oyster House | Spanish Fort, Alabama | 2017 | 10,500 | 420 | Owned | ||||||

| (1) | Restaurants are, from time to time, renovated, renamed and/or converted from or to managed or owned facilities. “Year Opened” refers to the year in which we, or an affiliated predecessor of us, first opened, acquired or began managing a restaurant at the applicable location, notwithstanding that the restaurant may have been renovated, renamed and/or converted from or to a managed or owned facility since that date. |

| (2) | Seating capacity refers to the seating capacity of the indoor part of a restaurant available for dining in all seasons and weather conditions. Outdoor seating capacity, if applicable, is set forth in parentheses and refers to the seating capacity of terraces and sidewalk cafes which are available for dining only in the warm seasons and then only inclement weather. |

| (3) | Assumes the exercise of all of our available lease renewal options. |

| (4) | Under the America lease, the sales goal is $6.0 million. Under the Gallagher’s Steakhouse lease the sales goal is $3.0 million. Under the lease for Gonzalez y Gonzalez and the Village Eateries, the combined sales |

| 6 |

| goal is $10.0 million. Each of the restaurants is currently operating at a level in excess of the minimum sales level required to exercise the renewal option for each respective restaurant. | |

| (5) | We operate six small food court restaurants and one full-service restaurant in the Village Eateries food court at the New York-New York Hotel & Casino. We also operate that hotel’s room service, banquet facilities and employee cafeteria. |

| (6) | This location is for a kiosk located at Bryant Park, New York, NY and all seating is outdoors. |

| (*) | Represents common area seating. |

The following table sets forth our less than wholly-owned properties that are managed by us, which have been consolidated as of September 29, 2018 – see Notes 1 and 2 to the Consolidated Financial Statements:

| Name | Location | Year Opened(1) |

Restaurant Size (Square Feet) |

Seating Capacity(2) Indoor- (Outdoor) |

Lease Expiration(3) | ||||||

| El Rio Grande (4)(5) | Third Avenue (between 38th and 39th Streets) New York, New York |

1987 | 4,000 | 160 | 2029 | ||||||

| Tampa Food Court(6)(7) | Hard Rock Hotel and Casino Tampa, Florida |

2004 | 4,000 | 250 | (*) | 2029 | |||||

| Hollywood Food Court(6)(7) | Hard Rock Hotel and Casino Hollywood, Florida |

2004 | 5,000 | 250 | (*) | 2029 | |||||

| Lucky Seven(6) | Foxwoods Resort Casino Ledyard, Connecticut |

2006 | 4,825 | 4,000 | (**) | 2026 | |||||

| (1) | Restaurants are, from time to time, renovated, renamed and/or converted from or to managed or owned facilities. “Year Opened” refers to the year in which we, or an affiliated predecessor of us, first opened, acquired or began managing a restaurant at the applicable location, notwithstanding that the restaurant may have been renovated, renamed and/or converted from or to a managed or owned facility since that date. |

| (2) | Seating capacity refers to the seating capacity of the indoor part of a restaurant available for dining in all seasons and weather conditions. Outdoor seating capacity, if applicable, is set forth in parentheses and refers to the seating capacity of terraces and sidewalk cafes which are available for dining only in the warm seasons and then only inclement weather. |

| (3) | Assumes the exercise of all our available lease renewal options. |

| (4) | Management fees earned, which have been eliminated in consolidation, are based on a percentage of cash flow of the restaurant. |

| (5) | We own a 19.2% interest in the partnership that owns El Rio Grande. |

| 7 |

| (6) | Management fees earned, which have been eliminated in consolidation, are based on a percentage of gross sales of the restaurant. |

| (7) | We own a 64.4% interest in the partnership that owns the Tampa and Hollywood Food Courts. |

| (*) | Represents common area seating. |

| (**) | Represents number of seats in the Bingo Hall at the Foxwoods Resort and Casino where our restaurant is located. |

Leases

We are currently not committed to any significant projects; however, we may take advantage of opportunities we consider to be favorable, when they occur, depending upon the availability of financing and other factors.

Restaurant Expansion

On November 30, 2016, the Company, through newly formed, wholly-owned subsidiaries, acquired the assets of the Original Oyster House, Inc., a restaurant and bar located in the City of Gulf Shores, Baldwin County, Alabama and the related real estate and an adjacent retail shopping plaza and the Original Oyster House II, Inc., a restaurant and bar located in the City of Spanish Fort, Baldwin County, Alabama and the related real estate. The total purchase price was for $10,750,000 plus inventory of approximately $293,000. The acquisition is accounted for as a business combination and was financed with a bank loan from the Company’s existing lender in the amount of $8,000,000 and cash from operations.

The opening of a new restaurant is invariably accompanied by substantial pre-opening expenses and early operating losses associated with the training of personnel, excess kitchen costs, costs of supervision and other expenses during the pre-opening period and during a post-opening “shake out” period until operations can be considered to be functioning normally. The amount of such pre-opening expenses and early operating losses can generally be expected to depend upon the size and complexity of the facility being opened.

Our restaurants generally do not achieve substantial increases in revenue from year to year, which we consider to be typical of the restaurant industry. To achieve significant increases in revenue or to replace revenue of restaurants that lose customer favor or which close because of lease expirations or other reasons, we would have to open additional restaurant facilities or expand existing restaurants. There can be no assurance that a restaurant will be successful after it is opened, particularly since in many instances we do not operate our new restaurants under a trade name currently used by us, thereby requiring new restaurants to establish their own identity.

Investment in New Meadowlands Racetrack

On March 12, 2013, the Company made a $4,200,000 investment in the New Meadowlands Racetrack LLC (“NMR”) through its purchase of a membership interest in Meadowlands Newmark, LLC, an existing member of NMR. On November 19, 2013, the Company invested an additional $464,000 in NMR through a purchase of an additional membership interest in Meadowlands Newmark, LLC resulting in a total ownership of 11.6% of Meadowlands Newmark, LLC, and an effective ownership interest in NMR of 7.4%, subject to dilution. In 2015, the Company invested an additional $222,000 in NMR with no change in ownership. In February 2017 the Company funded its proportionate share ($222,000) of a $3,000,000 capital call bringing its total investment to $5,108,000 with no change in ownership.

| 8 |

In addition to the Company’s ownership interest in NMR, if casino gaming is approved at the Meadowlands and NMR is granted the right to conduct said gaming, the Company shall be granted the exclusive right to operate the food and beverage concessions in the gaming facility with the exception of one restaurant.

In conjunction with this investment, the Company, through a 98% owned subsidiary, Ark Meadowlands LLC (“AM VIE”), also entered into a long-term agreement with NMR for the exclusive right to operate food and beverage concessions serving the new raceway facilities (the “Racing F&B Concessions”) located in the new raceway grandstand constructed at the Meadowlands Racetrack in northern New Jersey. Under the agreement, NMR is responsible to pay for the costs and expenses incurred in the operation of the Racing F&B Concessions, and all revenues and profits thereof inure to the benefit of NMR. AM VIE receives an annual fee equal to 5% of the net profits received by NMR from the Racing F&B Concessions during each calendar year.

On April 25, 2014, the Company loaned $1,500,000 to Meadowlands Newmark, LLC. The note bears interest at 3%, compounded monthly and added to the principal, and is due in its entirety on January 31, 2024. The note may be prepaid, in whole or in part, at any time without penalty or premium. On July 13, 2016, the Company made an additional loan to Meadowlands Newmark, LLC in the amount of $200,000. Such amount is subject to the same terms and conditions as the original loan discussed above. The principal and accrued interest related to this note in the amounts of $1,928,000 and $1,871,000, are included in Investment In and Receivable From New Meadowlands Racetrack in the Consolidated Balance Sheets at September 29, 2018 and September 30, 2017, respectively.

On June 7, 2018, the New Jersey State Legislature voted to legalize sports betting at casinos and racetracks in the state. Pursuant to this legislature NMR opened a sports book in partnership with Fanduel, a leading provider of daily fantasy sports, in June 2018.

Recent Restaurant Dispositions and Charges

Lease Expirations – The Company was advised by the landlord that it would have to vacate The Grill at Two Trees property at the Foxwoods Resort and Casino in Ledyard, CT, which had a no rent lease. The closure of this property occurred on January 1, 2017 and did not result in a material charge to the Company’s operations.

Other – On November 18, 2016, Ark Jupiter RI, LLC (“Ark Jupiter”), a wholly-owned subsidiary of the Company, entered into a ROFR Purchase and Sale Agreement (the “ROFR”) with SCFRC-HWG, LLC, the landlord (the “Seller”) to purchase the land and building in which the Company operates its Rustic Inn location in Jupiter, Florida. The Seller had entered into a Purchase and Sale Agreement with a third party to sell the premises; however, Ark Jupiter’s lease provided the Company with a right of first refusal to purchase the property. Ark Jupiter exercised the ROFR on October 4, 2016 and made a ten (10%) percent deposit on the purchase price of approximately $5,200,000. Concurrent with the execution of the ROFR, Ark Jupiter entered into a Purchase and Sale Agreement with 1065 A1A, LLC to sell this same property for $8,250,000. In connection with the sale, Ark Jupiter and 1065 A1A, LLC entered into a temporary lease and sub-lease arrangement which expired on July 18, 2017. The Company vacated the space in June. In connection with these transactions the Company recognized a gain in the amount of $1,637,000 during the year ended September 30, 2017.

The Company transferred its lease and the related assets of Canyon Road located in New York, NY to a former employee. In connection with this transfer, the Company recognized an impairment loss in the

| 9 |

amount of $75,000 which is included in depreciation and amortization expense for the year ended September 30, 2017.

Restaurant Management

Each restaurant is managed by its own manager and has its own chef. Food products and other supplies are purchased primarily from various unaffiliated suppliers, in most cases by our headquarter’s personnel. Each of our restaurants has two or more assistant managers and sous chefs (assistant chefs). Financial and management control is maintained at the corporate level through the use of automated systems that include centralized accounting and reporting.

Purchasing and Distribution

We strive to obtain quality menu ingredients, raw materials and other supplies and services for our operations from reliable sources at competitive prices. Substantially all menu items are prepared on each restaurant’s premises daily from scratch, using fresh ingredients. Each restaurant’s management determines the quantities of food and supplies required and then orders the items from local, regional and national suppliers on terms negotiated by our centralized purchasing staff. Restaurant-level inventories are maintained at a minimum dollar-value level in relation to sales due to the relatively rapid turnover of the perishable produce, poultry, meat, fish and dairy commodities that are used in operations.

We attempt to negotiate short-term and long-term supply agreements depending on market conditions and expected demand. However, we do not contract for long periods of time for our fresh commodities such as produce, poultry, meat, fish and dairy items and, consequently, such commodities can be subject to unforeseen supply and cost fluctuations. Independent foodservice distributors deliver most food and supply items daily to restaurants. The financial impact of the termination of any such supply agreements would not have a material adverse effect on our financial position.

Competition

The hospitality industry is highly competitive and is often affected by changes in taste and entertainment trends among the public, by local, national and economic conditions affecting spending habits, and by population and traffic patterns. We believe that the principal means of competition among restaurants include the location, type and quality of facilities and the type, quality and price of beverage and food served.

Our restaurants compete directly or indirectly with many well-established competitors, both nationally and locally owned, some with substantially greater financial resources than we do. Their resources and market presence may provide advantages in marketing, purchasing and negotiating leases. We compete with other restaurant and retail establishments for sites and finding management personnel.

Employees

At November 30, 2018, we employed 2,102 persons (including employees at managed facilities), 585 of whom were full-time employees, and 1,517 of whom were part-time employees; 49 of whom were headquarters personnel, 135 of whom were restaurant management personnel, 1,323 of whom were kitchen personnel and 595 of whom were restaurant service personnel. A number of our restaurant service personnel are employed on a part-time basis. Changes in minimum wage levels may adversely affect our labor costs and the restaurant industry generally because a large percentage of restaurant personnel are paid at or slightly above the minimum wage. Our employees are not covered by any collective bargaining agreements.

| 10 |

Government Regulation

We are subject to various federal, state and local laws affecting our business. Each restaurant is subject to licensing and regulation by a number of governmental authorities that may include alcoholic beverage control, health, sanitation, environmental, zoning and public safety agencies in the state or municipality in which the restaurant is located. Difficulties in obtaining or failures to obtain the required licenses or approvals could delay or prevent the development and openings of new restaurants, or could disrupt the operations of existing restaurants.

Alcoholic beverage control regulations require each of our restaurants to apply to a state authority and, in certain locations, county and municipal authorities for licenses and permits to sell alcoholic beverages on the premises. Typically, licenses must be renewed annually and may be subject to penalties, temporary suspension or revocation for cause at any time. Alcoholic beverage control regulations impact many aspects of the daily operations of our restaurants, including the minimum ages of patrons and employees consuming or serving such beverages; employee alcoholic beverages training and certification requirements; hours of operation; advertising; wholesale purchasing and inventory control of such beverages; seating of minors and the service of food within our bar areas; and the storage and dispensing of alcoholic beverages. State and local authorities in many jurisdictions routinely monitor compliance with alcoholic beverage laws. The failure to receive or retain, or a delay in obtaining, a liquor license for a particular restaurant could adversely affect our ability to obtain such licenses in jurisdictions where the failure to receive or retain, or a delay in obtaining, a liquor license occurred.

We are subject to “dram-shop” statutes in most of the states in which we have operations, which generally provide a person injured by an intoxicated person the right to recover damages from an establishment that wrongfully served alcoholic beverages to such person. We carry liquor liability coverage as part of our existing comprehensive general liability insurance. A settlement or judgment against us under a “dram-shop” statute in excess of liability coverage could have a material adverse effect on our operations.

Various federal and state labor laws govern our operations and our relationship with employees, including such matters as minimum wages, breaks, overtime, fringe benefits, safety, working conditions and citizenship requirements. We are also subject to the regulations of the Immigration and Naturalization Service. If our employees do not meet federal citizenship or residency requirements, their deportation could lead to a disruption in our work force. Significant government-imposed increases in minimum wages, paid leaves of absence and mandated health benefits, or increased tax reporting, assessment or payment requirements related to employees who receive gratuities could be detrimental to our profitability.

Our facilities must comply with the applicable requirements of the Americans With Disabilities Act of 1990 (“ADA”) and related state statutes. The ADA prohibits discrimination on the basis of disability with respect to public accommodations and employment. Under the ADA and related state laws, when constructing new restaurants or undertaking significant remodeling of existing restaurants, we must make them more readily accessible to disabled persons.

The New York State Liquor Authority must approve any transaction in which a shareholder of the licensee increases his holdings to 10% or more of the outstanding capital stock of the licensee and any transaction involving 10% or more of the outstanding capital stock of the licensee.

Seasonal Nature of Business

Our business is highly seasonal. The second quarter of our fiscal year, consisting of the non-holiday portion of the cold weather season in New York and Washington (January, February and March), is the poorest performing quarter. We achieve our best results during the warm weather, attributable to our

| 11 |

extensive outdoor dining availability, particularly at Bryant Park in New York and Sequoia in Washington, D.C. (our largest restaurants) and our outdoor cafes. However, even during summer months these facilities can be adversely affected by unusually cool or rainy weather conditions. Our facilities in Las Vegas are indoor and generally operate on a more consistent basis throughout the year.

Available Information

We make available free of charge through our Internet website, www.arkrestaurants.com, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, statements of beneficial ownership of securities on Forms 3, 4 and 5 and amendments to these reports and statements filed or furnished pursuant to Section 13(a) and Section 16 of the Securities Exchange Act of 1934 as soon as reasonably practicable after such materials are electronically filed with, or furnished to, the United States Securities and Exchange Commission, or SEC.

The above information is also available at the SEC’s Office of Investor Education and Advocacy at United States Securities and Exchange Commission, 100 F Street, N.E., Washington, D.C. 20549-0213 or obtainable by calling the SEC at (800) 732-0330. In addition, the SEC maintains an Internet website at www.sec.gov, where the above information can be viewed.

Our principal executive offices are located at 85 Fifth Avenue, New York, New York 10003, and our telephone number is (212) 206-8800. Unless the context specifically requires otherwise, the terms the “Company,” “Ark,” “we,” “us” and “our” mean Ark Restaurants Corp., a Delaware corporation, and its consolidated subsidiaries.

| Item 1A. | Risk Factors |

Not applicable.

| Item 1B. | Unresolved Staff Comments |

Not applicable.

| Item 2. | Properties |

Our restaurant facilities and our executive offices, with the exception of The Rustic Inn in Dania Beach, Florida, Shuckers in Jensen Beach, Florida and the two Original Oyster House properties in Alabama, are occupied under leases. Most of our restaurant leases provide for the payment of base rents plus real estate taxes, insurance and other expenses and, in certain instances, for the payment of a percentage of our sales at such facility. As of September 29, 2018, these leases (including leases for managed restaurants) have terms (including any available renewal options) expiring as follows:

| Fiscal Year Lease Terms Expire |

Number of Facilities |

| 2019-2023 | 5 |

| 2024-2028 | 7 |

| 2029-2034 | 9 |

| 2034-2038 | 1 |

| 12 |

Our executive, administrative and clerical offices are located in approximately 8,500 square feet of office space at 85 Fifth Avenue, New York, New York. Our lease for this office space expires in 2025.

For information concerning our future minimum rental commitments under non-cancelable operating leases, see Note 10 of the Notes to Consolidated Financial Statements for additional information concerning our leases.

| Item 3. | Legal Proceedings |

In the ordinary course of our business, we are a party to various lawsuits arising from accidents at our restaurants and workers’ compensation claims, which are generally handled by our insurance carriers.

Our employment of management personnel, waiters, waitresses and kitchen staff at a number of different restaurants has resulted in the institution, from time to time, of litigation alleging violation by us of employment discrimination laws. We do not believe that any of such suits will have a materially adverse effect upon us, our financial condition or operations.

| Item 4. | Mine Safety Disclosures |

Not Applicable.

| 13 |

PART II

| Item 5. | Market For The Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market for Our Common Stock

Our Common Stock, $.01 par value, is traded on the Nasdaq Capital Market under the symbol “ARKR.”

As of December 11, 2018, there were 30 holders of record of our common stock and approximately an additional 1,654 beneficial owners.

Dividend Policy

On December 7, 2016, March 1, 2017, June 5, 2017, September 6, 2017, December 5, 2017, March 6, 2018, June 12, 2018, September 17, 2018 and December 5, 2018 our Board of Directors declared quarterly cash dividends in the amount of $0.25 per share. We intend to continue to pay such quarterly cash dividends for the foreseeable future; however, the payment of future dividends is at the discretion of our Board of Directors and is based on future earnings, cash flow, financial condition, capital requirements, changes in U.S. taxation and other relevant factors.

Purchases of Equity Securities by Issuer and Affiliated Purchases

There were no purchases made during the fourth quarter of the issuer’s fiscal year.

Securities Authorized for Issuance under Equity Compensation Plans

The Company has options outstanding under two stock option plans, the 2010 Stock Option Plan (the “2010 Plan”) and the 2016 Stock Option Plan (the “2016 Plan”). Options granted under both plans are exercisable at prices at least equal to the fair market value of such stock on the dates the options were granted and expire ten years after the date of grant. No additional options are available for grant under the 2010 plan.

On August 10, 2018, options to purchase 5,000 shares of common stock were granted at an exercise price of $20.36 per share and on September 4, 2018 options to purchase 20,000 shares of common stock were granted at an exercise price of $22.30 per share. Both grants are exercisable as to 50% of the shares commencing on the date of grant and as to an additional 50% commencing on the first anniversary of the date of grant. Such options had an aggregate grant date fair value of approximately $94,000. The Company did not grant any options during the year ended September 30, 2017.

During the year ended September 29, 2018, options to purchase 26,050 shares of common stock at a weighted average exercise price of $18.60 per share expired unexercised or were forfeited. During the year ended September 30, 2017, options to purchase 90,000 shares of common stock at a weighted average exercise price of $32.15 per share expired unexercised.

| 14 |

The following is a summary of the securities issued and authorized for issuance under our Stock Option Plans at September 29, 2018:

| Plan Category | (a)

Number of securities to be issued upon exercise of outstanding options, warrants and rights |

(b)

Weighted - average exercise price of outstanding options, warrants and rights |

(c)

Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) | ||||||

| Equity compensation plans approved by shareholders | 378,750 | $18.46 | 475,000 | ||||||

| Equity compensation plans not approved by shareholders1 | None | N/A | None | ||||||

| Total | 378,750 | $18.46 | 475,000 |

Of the 378,750 options outstanding on September 29, 2018, 173,625 were held by the Company’s officers and directors.

| (1) | The Company has no equity compensation plan that was not approved by shareholders. |

On April 5, 2016, the shareholders of the Company approved the 2016 Stock Option Plan and the Section 162(m) Cash Bonus Plan. Under the 2016 Stock Option Plan, 500,000 options were authorized for future grant and are exercisable at prices at least equal to the fair market value of such stock on the dates the options were granted. The options expire ten years after the date of grant. Under the Section 162(m) Cash Bonus Plan, compensation paid in excess of $1,000,000 to any employee who is the chief executive officer, or one of the three highest paid executive officers on the last day of that tax year (other than the chief executive officer or the chief financial officer) will meet certain “performance-based” requirements of Section 162(m) and the related IRS regulations in order for it to be tax deductible.

| 15 |

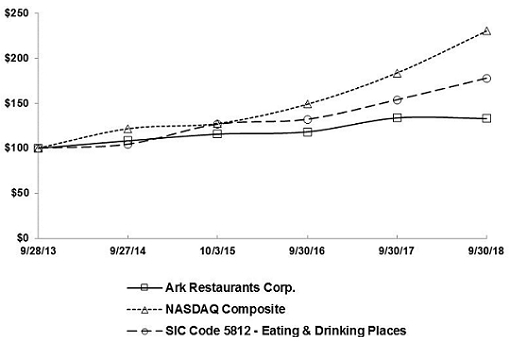

Stock Performance Graph

The graph set forth below compares the yearly percentage change in cumulative total shareholder return on the Company’s Common Stock for the five-year period commencing September 28, 2013 and ending September 29, 2018 against the cumulative total return on the NASDAQ Market Index and a peer group comprised of those public companies whose business activities fall within the same standard industrial classification code as the Company. This graph assumes a $100 investment in the Company’s Common Stock and in each index on September 28, 2013 and that all dividends paid by companies included in each index were reinvested.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among Ark Restaurants Corp., the NASDAQ Composite Index,

and SIC Code 5812 - Eating & Drinking Places

*$100 invested on 9/28/13 in stock or 9/30/13 in index, including reinvestment of dividends.

Indexes calculated on month-end basis.

| Cumulative Total Return | |||||||

| 9/28/13 | 9/27/14 | 10/3/15 | 9/30/16 | 9/30/17 | 9/30/18 | ||

| Ark Restaurants Corp. | $100.00 | $ 108.06 | $115.69 | $118.17 | $133.70 | $132.91 | |

| NASDAQ Composite | 100.00 | 121.64 | 127.37 | 148.79 | 183.54 | 230.21 | |

| SIC Code 5812 - Eating & Drinking Places | 100.00 | 104.42 | 126.61 | 132.00 | 153.65 | 177.56 | |

| 16 |

| Item 6. | Selected Consolidated Financial Data |

Not applicable.

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Overview

As of September 29, 2018, the Company owned and operated 20 restaurants and bars, 19 fast food concepts and catering operations, exclusively in the United States, that have similar economic characteristics, nature of products and service, class of customer and distribution methods. The Company believes it meets the criteria for aggregating its operating segments into a single reporting segment in accordance with applicable accounting guidance. The Consolidated Statement of Income for the year ended September 30, 2017 includes revenues and operating income of approximately $11,804,000 and $1,243,000, respectively, related to the Oyster House properties on the gulf coast of Alabama, which were acquired on November 30, 2016.

Accounting Period

Our fiscal year ends on the Saturday nearest September 30. We report fiscal years under a 52/53-week format. This reporting method is used by many companies in the hospitality industry and is meant to improve year-to-year comparisons of operating results. Under this method, certain years will contain 53 weeks. The fiscal years ended September 29, 2018 and September 30, 2017 included 52 weeks.

Seasonality

The Company has substantial fixed costs that do not decline proportionally with sales. The first and second fiscal quarters, which include the winter months, usually reflect lower customer traffic than in the third and fourth fiscal quarters. However, sales in the third and fourth fiscal quarters can be adversely affected by inclement weather due to the significant amount of outdoor seating at the Company’s restaurants.

Results of Operations

The Company’s restaurant operating income of $5,032,000 for the year ended September 29, 2018 decreased 6.3% compared to restaurant operating income of $5,371,000 (which excludes the recognition of a gain in the amount of $1,637,000 in connection with the sale of the real estate underlying our Rustic Inn, Jupiter, FL property) for the year ended September 30, 2017. This decrease resulted primarily from poor weather conditions in the Northeast during the fourth quarter of fiscal 2018, partially offset by: (a) an increase in operating income in 2018 at Sequoia in Washington, DC, which was closed for renovation for the second and third quarters of fiscal 2017, and (b) an increase in operating income at The Rustic Inn in Dania Beach, FL as a result of the completion of the road construction project in early fiscal 2018 that was started in the second quarter of fiscal 2016 by the local municipality.

| 17 |

The following table summarizes the significant components of the Company’s operating results for the years ended September 29, 2018 and September 30, 2017, respectively:

| Year Ended | Variance | |||||||||||||||

| September 29, 2018 | September 30, 2017 | $ | % | |||||||||||||

| (in thousands) | ||||||||||||||||

| REVENUES: | ||||||||||||||||

| Food and beverage sales | $ | 156,837 | $ | 151,196 | $ | 5,641 | 3.7 | % | ||||||||

| Other revenue | 3,153 | 2,681 | 472 | 17.6 | % | |||||||||||

| Total revenues | 159,990 | 153,877 | 6,113 | 4.0 | % | |||||||||||

| COSTS AND EXPENSES: | ||||||||||||||||

| Food and beverage cost of sales | 43,036 | 41,597 | 1,439 | 3.5 | % | |||||||||||

| Payroll expenses | 55,620 | 53,074 | 2,546 | 4.8 | % | |||||||||||

| Occupancy expenses | 18,577 | 17,100 | 1,477 | 8.6 | % | |||||||||||

| Other operating costs and expenses | 21,437 | 20,690 | 747 | 3.6 | % | |||||||||||

| General and administrative expenses | 11,214 | 11,504 | (290 | ) | -2.5 | % | ||||||||||

| Depreciation and amortization | 5,074 | 4,541 | 533 | 11.7 | % | |||||||||||

| Total costs and expenses | 154,958 | 148,506 | 6,452 | 4.3 | % | |||||||||||

| RESTAURANT OPERATING INCOME | 5,032 | 5,371 | (339 | ) | -6.3 | % | ||||||||||

| Gain on sale of Ark Jupiter RI LLC | - | 1,637 | (1,637 | ) | N/A | |||||||||||

| OPERATING INCOME | $ | 5,032 | $ | 7,008 | $ | (1,976 | ) | -28.2 | % | |||||||

Revenues

During the Company’s year ended September 29, 2018 (“fiscal 2018”), revenues increased 4.0% compared to the year ended September 30, 2017 (“fiscal 2018”). This increase resulted primarily from: (i) revenues related to the Sequoia in Washington, DC which was closed for renovation for the second and third quarters of fiscal 2017, (ii) revenues related to The Oyster House properties in Gulf Shores, Alabama (which were acquired on November 30, 2016), and (iii) the same-store sales impacts discussed below, partially offset by revenues related to the Rustic Inn, Jupiter, which was closed in June 2017.

| 18 |

Food and Beverage Same-Store Sales

On a Company-wide basis, same store food and beverage sales decreased 1.7% for the year ended September 29, 2018 as compared to the year ended September 30, 2017 as follows:

| Year Ended | Variance | |||||||||||||||

| September 29, 2018 | September 30, 2017 | $ | % | |||||||||||||

| (in thousands) | ||||||||||||||||

| Las Vegas | $ | 47,852 | $ | 45,852 | $ | 2,000 | 4.4 | % | ||||||||

| New York | 39,636 | 39,887 | (251 | ) | -0.6 | % | ||||||||||

| Washington, DC | 3,112 | 3,573 | (461 | ) | -12.9 | % | ||||||||||

| Atlantic City, NJ | 7,406 | 7,536 | (130 | ) | -1.7 | % | ||||||||||

| Boston | 2,839 | 3,235 | (396 | ) | -12.2 | % | ||||||||||

| Connecticut | 2,120 | 2,156 | (36 | ) | -1.7 | % | ||||||||||

| Alabama | 11,924 | 11,804 | 120 | 1.0 | % | |||||||||||

| Florida | 28,068 | 26,467 | 1,601 | 6.0 | % | |||||||||||

| Same store sales | 142,957 | 140,510 | $ | 2,447 | 1.7 | % | ||||||||||

| Other | 13,880 | 10,686 | ||||||||||||||

| Food and beverage sales | $ | 156,837 | $ | 151,196 | ||||||||||||

Same-store sales in Las Vegas increased 4.4% primarily as a result of increased traffic near the properties where we operate our restaurant in connection with the opening of the T-Mobile Arena nearby. Same-store sales in New York decreased 0.6%, primarily as a result of poor weather conditions during the months in which our properties with outdoor seating areas are open, partially offset by strong catering revenues. Same-store sales in Washington, DC (which excludes Sequoia, which was closed for renovation for the second and third fiscal quarter of 2017) decreased 12.9% due to decreased traffic at our Thunder Grill property as a result of a major tenant vacating the adjacent space. Same-store sales in Atlantic City decreased 1.7% primarily due to decreased traffic at the properties in which we operate our restaurants as a result of the re-opening of two properties in June 2018. Same-store sales in Boston decreased 12.2% primarily as a result of decreased traffic at Faneuil Hall Marketplace where our property is located. Same-store sales in Connecticut decreased 1.7% due to declining traffic at the Foxwoods Resort and Casino where our properties are located. Same-store sales in Alabama were consistent with last year as expected. Same-store sales in Florida increased 6.0% as a result of the completion of the road construction project started in the second quarter of fiscal 2016 by the local municipality near The Rustic Inn in Dania Beach, FL. Other food and beverage sales consist of sales related to Sequoia, which was closed in for the entire second and third fiscal quarters of 2017, new restaurants opened or acquired during the applicable period (e.g. the Oyster House properties in 2017) and sales related to properties that were closed due to lease expiration and other closures.

Our restaurants generally do not achieve substantial increases in revenue from year to year, which we consider to be typical of the restaurant industry. To achieve significant increases in revenue or to replace revenue of restaurants that lose customer favor or which close because of lease expirations or other reasons, we would have to open additional restaurant facilities or expand existing restaurants. There can be no assurance that a restaurant will be successful after it is opened, particularly since in many instances we do not operate our new restaurants under a trade name currently used by us, thereby requiring new restaurants to establish their own identity.

| 19 |

Other Revenue

Included in Other Revenues are purchase service fees which represent commissions earned by a subsidiary of the Company for providing purchasing services to other restaurant groups, as well as license fees, property management fees and other rentals. The increase in Other Revenue for fiscal 2018 as compared to fiscal 2017 is primarily due to an increase in property management fees and other rentals partially offset by decreased purchase service fees.

Costs and Expenses

Costs and expenses for the years ended September 29, 2018 and September 30, 2017 were as follows (in thousands):

| Year Ended September 29, | % to Total | Year Ended September 30, | % to Total | Increase (Decrease) | ||||||||||||||||||||

| 2018 | Revenues | 2017 | Revenues | $ | % | |||||||||||||||||||

| Food and beverage cost of sales | $ | 43,036 | 26.9 | % | $ | 41,597 | 27.0 | % | $ | 1,439 | 3.5 | % | ||||||||||||

| Payroll expenses | 55,620 | 34.8 | % | 53,074 | 34.5 | % | 2,546 | 4.8 | % | |||||||||||||||

| Occupancy expenses | 18,577 | 11.6 | % | 17,100 | 11.1 | % | 1,477 | 8.6 | % | |||||||||||||||

| Other operating costs and expenses | 21,437 | 13.4 | % | 20,690 | 13.4 | % | 747 | 3.6 | % | |||||||||||||||

| General and administrative expenses | 11,214 | 7.0 | % | 11,504 | 7.5 | % | (290 | ) | -2.5 | % | ||||||||||||||

| Depreciation and amortization | 5,074 | 3.2 | % | 4,541 | 3.0 | % | 533 | 11.7 | % | |||||||||||||||

| $ | 154,958 | $ | 148,506 | $ | 6,452 | |||||||||||||||||||

The small decrease in food and beverage costs as a percentage of total revenues for the year ended September 29, 2018 compared to the same period of last year is primarily the result of a better mix of catering versus a la carte business at our larger properties (i.e. Bryant Park, Sequoia) combined with a taking advantage of bulk purchasing discounts offset by higher commodity prices.

Payroll expenses as a percentage of total revenues for the year ended September 29, 2018 increased as compared to the same period of last year primarily as a result of minimum wage increases associated with changes to labor laws partially offset by a better mix of catering versus a la carte business at our larger properties.

Occupancy expenses as a percentage of total revenues increased as compared to the same period of last year as a result of rents that are paid based on a percentage of sales and base rent increase at our other properties, partially offset by higher sales at properties where rents are relatively fixed or where the Company owns the premises at which the property operates (The Rustic Inn in Dania Beach, FL, Shuckers in Jensen Beach, FL and The Oyster House properties in Gulf Shores, Alabama).

Other operating costs and expenses as a percentage of total revenues for fiscal 2018 were consistent with fiscal 2017.

General and administrative expenses (which relate solely to the corporate office in New York City) as a percentage of total revenues for fiscal 2018 decreased as compared to the same period of last year primarily as a result of lower headcount partially offset by annual wage increases.

Depreciation and amortization expense for fiscal 2018 increased as compared to the same period of last year primarily as a result of depreciation on the improvements made at our Sequoia property which were

| 20 |

placed in service in the fourth fiscal quarter of 2017, partially offset by additional depreciation in the amount of $358,000 related to asset write-offs at Sequoia and Canyon Road (whose lease was transferred to an unrelated party) in fiscal 2017.

Income Taxes

Our income tax expense, deferred tax assets and liabilities, and liabilities for uncertain tax positions reflect management’s best estimate of current and future taxes to be paid. We are subject to income tax in numerous state taxing jurisdictions. Significant judgement and estimates are required in the determination of consolidated income tax expense. The provision for income taxes reflects federal income taxes calculated on a consolidated basis and state and local income taxes which are calculated on a separate entity basis.

For state and local income tax purposes, certain losses incurred by a subsidiary may only be used to offset that subsidiary’s income, with the exception of the restaurants operating in the District of Columbia. Accordingly, our overall effective tax rate has varied depending on the level of income and losses incurred at individual subsidiaries.

Deferred income taxes arise from temporary differences between the tax bases of assets and liabilities and their reported amounts in the financial statements, which will result in taxable or deductible amounts in the future. In evaluating our ability to recover our deferred tax assets in the jurisdiction from which they arise, we consider all available positive and negative evidence, including scheduled reversals of deferred tax liabilities, projected future taxable income, tax-planning strategies, and results of recent operations. The assumptions about future taxable income require the use of significant judgment and are consistent with the plans and estimates we are using to manage the underlying businesses.

On December 22, 2017 the U.S. government enacted comprehensive tax reform commonly referred to as the Tax Cuts and Jobs Act (“TCJA”). Under Accounting Standards Codification (“ASC”) 740, the effects of changes in tax rates and laws are recognized in the period which the new legislation is enacted. The TCJA makes broad and complex changes to the U.S. tax code, including, but not limited to: (1) reducing the U.S. federal corporate tax rate from 35% to 21% effective January 1, 2018; (2) changing rules related to uses and limitations of net operating loss carryforwards created in tax years beginning after December 31, 2017; (3) accelerated expensing on certain qualified property; (4) creating a new limitation on deductible interest expense to 30% of tax adjusted EBITDA through 2021 and then 30% of tax adjusted EBIT thereafter; (5) eliminating the corporate alternative minimum tax; and (6) further limitations on the deductibility of executive compensation under IRC §162(m) for tax years beginning after December 31, 2017. As the reduction in the U.S. federal corporate tax rate is administratively effective on January 1, 2018, our blended U.S. federal tax rate for the year ended September 29, 2018 was approximately 24%.

In response to the TCJA, the U.S. Securities and Exchange Commission (“SEC”) staff issued Staff Accounting Bulletin No. 118 (“SAB 118”), which provides guidance on accounting for the tax effects of TCJA. The purpose of SAB 118 was to address any uncertainty or diversity of view in applying ASC Topic 740, Income Taxes in the reporting period in which the TCJA was enacted. SAB 118 addresses situations where the accounting is incomplete for certain income tax effects of the TJCA upon issuance of a company’s financial statements for the reporting period which include the enactment date. SAB 118 allows for a provisional amount to be recorded if it is a reasonable estimate of the impact of the TCJA. Additionally, SAB 118 allows for a measurement period to finalize the impacts of the TCJA, not to extend beyond one year from the date of enactment.

| 21 |

In connection with the TCJA, the Company recorded an income tax benefit of $1,382,000 related to the re-measurement of our deferred tax assets and liabilities for the reduced U.S. federal corporate tax rate of 21%. The Company’s accounting for the TCJA is complete as of September 29, 2018 with no significant differences from our provisional estimates recorded during interim periods.

The Company’s overall effective tax rate in the future will be affected by factors such as the utilization of state and local net operating loss carryforwards, the generation of FICA tax credits and the mix of earnings by state taxing jurisdictions as Nevada does not impose a state income tax, as compared to the other major state and local jurisdictions in which the Company has operations. Our overall effective tax rate in the future will be affected by factors such as income earned by our VIEs, generation of FICA TIP credits and the mix of geographical income for state tax purposes as Nevada does not impose an income tax.

Liquidity and Capital Resources

Our primary source of capital has been cash provided by operations and, in recent years, bank and other borrowings to finance specific transactions, acquisitions and large remodeling projects. We utilize cash generated from operations to fund the cost of developing and opening new restaurants and smaller remodeling projects of existing restaurants we own.

Net cash provided by operating activities for fiscal 2018 decreased to $9,575,000 as compared to $10,350,000 in fiscal 2017. This decrease was attributable to changes in net working capital primarily related to accounts receivable, prepaid, refundable and accrued income taxes and accounts payable and accrued expenses.

Net cash used in investing activities for fiscal 2018 was $5,050,000 and resulted primarily from purchases of fixed assets at existing restaurants and costs associated with the renovation of Sequoia.

Net cash used in investing activities for fiscal 2017 was $14,641,000 and resulted primarily from purchases of fixed assets at existing restaurants, costs associated with the renovation of Sequoia and the cash portion of the purchase of The Oyster House properties in the amount of $3,043,000, partially offset by the net proceeds in the amount of $2,474,000 from the sale of The Rustic Inn in Jupiter, Florida

Net cash used in financing activities for the years ended September 29, 2018 and September 30, 2017 of $919,000 and $1,542,000, respectively, resulted primarily from the payment of dividends, principal payments on notes payable and distributions to non-controlling interests, offset by borrowings under the credit facility.

The Company had a working capital deficiency of $4,628,000 at September 29, 2018 as compared with a deficiency of $16,072,000 at September 30, 2017. This decrease resulted primarily from the refinancing completed on June 1, 2018 as discussed in Note 9 – Notes Payable Bank. We believe that our existing cash balances, current banking facilities and cash provided by operations will be sufficient to meet our liquidity and capital spending requirements at least through December 31, 2019.

On January 4, 2018, April 4, 2018, July 6, 2018 and October 12, 2018, the Company paid quarterly cash dividends in the amount of $0.25 per share on the Company’s common stock. The Company intends to continue to pay such quarterly cash dividend for the foreseeable future; however, the payment of future dividends is at the discretion of the Company’s Board of Directors and is based on future earnings, cash flow, financial condition, capital requirements, changes in U.S. taxation and other relevant factors.

| 22 |

Restaurant Expansion

On November 30, 2016, the Company, through newly formed, wholly-owned subsidiaries, acquired the assets of the Original Oyster House, Inc., a restaurant and bar located in the City of Gulf Shores, Baldwin County, Alabama and the related real estate and an adjacent retail shopping plaza and the Original Oyster House II, Inc., a restaurant and bar located in the City of Spanish Fort, Baldwin County, Alabama and the related real estate. The total purchase price was for $10,750,000 plus inventory of approximately $293,000. The acquisition is accounted for as a business combination and was financed with a bank loan from the Company’s existing lender in the amount of $8,000,000 and cash from operations.

The opening of a new restaurant is invariably accompanied by substantial pre-opening expenses and early operating losses associated with the training of personnel, excess kitchen costs, costs of supervision and other expenses during the pre-opening period and during a post-opening “shake out” period until operations can be considered to be functioning normally. The amount of such pre-opening expenses and early operating losses can generally be expected to depend upon the size and complexity of the facility being opened.

Our restaurants generally do not achieve substantial increases in revenue from year to year, which we consider to be typical of the restaurant industry. To achieve significant increases in revenue or to replace revenue of restaurants that lose customer favor or which close because of lease expirations or other reasons, we would have to open additional restaurant facilities or expand existing restaurants. There can be no assurance that a restaurant will be successful after it is opened, particularly since in many instances we do not operate our new restaurants under a trade name currently used by us, thereby requiring new restaurants to establish their own identity.

We may take advantage of other opportunities we consider to be favorable, when they occur, depending upon the availability of financing and other factors.

Investment in and Receivable from New Meadowlands Racetrack

On March 12, 2013, the Company made a $4,200,000 investment in the New Meadowlands Racetrack LLC (“NMR”) through its purchase of a membership interest in Meadowlands Newmark, LLC, an existing member of NMR. On November 19, 2013, the Company invested an additional $464,000 in NMR through a purchase of an additional membership interest in Meadowlands Newmark, LLC resulting in a total ownership of 11.6% of Meadowlands Newmark, LLC, and an effective ownership interest in NMR of 7.4%, subject to dilution. In 2015, the Company invested an additional $222,000 in NMR with no change in ownership. In February 2017 the Company funded its proportionate share ($222,000) of a $3,000,000 capital call bringing its total investment to $5,108,000 with no change in ownership.

In addition to the Company’s ownership interest in NMR, if casino gaming is approved at the Meadowlands and NMR is granted the right to conduct said gaming, the Company shall be granted the exclusive right to operate the food and beverage concessions in the gaming facility with the exception of one restaurant.

In conjunction with this investment, the Company, through a 97% owned subsidiary, Ark Meadowlands LLC (“AM VIE”), also entered into a long-term agreement with NMR for the exclusive right to operate food and beverage concessions serving the new raceway facilities (the “Racing F&B Concessions”) located in the new raceway grandstand constructed at the Meadowlands Racetrack in northern New Jersey. Under the agreement, NMR is responsible to pay for the costs and expenses incurred in the operation of the Racing F&B Concessions, and all revenues and profits thereof inure to the benefit of

| 23 |

NMR. AM VIE receives an annual fee equal to 5% of the net profits received by NMR from the Racing F&B Concessions during each calendar year.

On April 25, 2014, the Company loaned $1,500,000 to Meadowlands Newmark, LLC. The note bears interest at 3%, compounded monthly and added to the principal, and is due in its entirety on January 31, 2024. The note may be prepaid, in whole or in part, at any time without penalty or premium. On July 13, 2016, the Company made an additional loan to Meadowlands Newmark, LLC in the amount of $200,000. Such amount is subject to the same terms and conditions as the original loan as discussed above.

Recent Restaurant Dispositions and Charges

Lease Expirations – The Company was advised by the landlord that it would have to vacate The Grill at Two Trees property at the Foxwoods Resort and Casino in Ledyard, CT, which had a no rent lease. The closure of this property occurred on January 1, 2017 and did not result in a material charge.

Other – On November 18, 2016, Ark Jupiter RI, LLC (“Ark Jupiter”), a wholly-owned subsidiary of the Company, entered into a ROFR Purchase and Sale Agreement (the “ROFR”) with SCFRC-HWG, LLC, the landlord (the “Seller”) to purchase the land and building in which the Company operated its Rustic Inn location in Jupiter, Florida. The Seller had entered into a Purchase and Sale Agreement with a third party to sell the premises; however, Ark Jupiter’s lease provided the Company with a right of first refusal to purchase the property. Ark Jupiter exercised the ROFR on October 4, 2016 and made a ten (10%) percent deposit on the purchase price of approximately $5,200,000. Concurrent with the execution of the ROFR, Ark Jupiter entered into a Purchase and Sale Agreement with 1065 A1A, LLC to sell this same property for $8,250,000. In connection with the sale, Ark Jupiter and 1065 A1A, LLC entered into a temporary lease and sub-lease arrangement which expired on July 18, 2017. The Company vacated the space in June 2017. In connection with these transactions the Company recognized a gain in the amount of $1,637,000 during the year ended September 30, 2017.

The Company transferred its lease and the related assets of Canyon Road located in New York, NY to a former employee. In connection with this transfer, the Company recognized an impairment loss included in depreciation and amortization expense in the amount of $75,000 for the year ended September 30, 2017.

Critical Accounting Policies

Our significant accounting policies are more fully described in Note 1 to our consolidated financial statements. While all of these significant accounting policies impact our financial condition and results of operations, we view certain of these policies as critical. Policies determined to be critical are those policies that have the most significant impact on our consolidated financial statements and require management to use a greater degree of judgment and estimates. Actual results may differ from those estimates.

We believe that given current facts and circumstances, it is unlikely that applying any other reasonable judgments or estimate methodologies would cause a material effect on our consolidated results of operations, financial position or cash flows for the periods presented in this report.

| 24 |

Below are listed certain policies that management believes are critical:

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. The accounting estimates that require management’s most difficult and subjective judgments include allowances for potential bad debts on receivables, the useful lives and recoverability of its assets, such as property and intangibles, fair values of financial instruments and share-based compensation, the realizable value of its tax assets and determining when investment impairments are other-than-temporary. Because of the uncertainty in such estimates, actual results may differ from these estimates.

Long-Lived Assets

Long-lived assets, such as property, plant and equipment, and purchased intangibles subject to amortization, are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. In the evaluation of the fair value and future benefits of long-lived assets, we perform an analysis of the anticipated undiscounted future net cash flows of the related long-lived assets. If the carrying value of the related asset exceeds the undiscounted cash flows, the carrying value is reduced to its fair value. Various factors including estimated future sales growth and estimated profit margins are included in this analysis.

Management continually evaluates unfavorable cash flows, if any, related to underperforming restaurants. Periodically it is concluded that certain properties have become impaired based on their existing and anticipated future economic outlook in their respective markets. In such instances, we may impair assets to reduce their carrying values to fair values. Estimated fair values of impaired properties are based on comparable valuations, cash flows and/or management judgment.

Recoverability of Investment in New Meadowlands Racetrack (“NMR”)

The carrying value of our Investment in Meadowlands Newmark LLC, which has a 63.7% ownership in NMR, is determined using the cost method. In accordance with the cost method, our initial investment is recorded at cost and we record dividend income when applicable, if dividends are declared. We review our Investment in NMR each reporting period to determine whether a significant event or change in circumstances has occurred that may have an adverse effect on its fair value.

As a result, we performed an assessment of the recoverability of our indirect Investment in NMR as of September 29, 2018 which involved critical accounting estimates. These estimates require significant management judgment, include inherent uncertainties and are often interdependent; therefore, they do not change in isolation. Factors that management estimated include, among others, the probability of gambling being approved in Northern New Jersey which is the most heavily weighted assumption and NMR obtaining a license to operate a casino, revenue levels, cost of capital, marketing spending, tax rates and capital spending.

In performing this assessment, we estimate the fair value of our Investment in NMR using our best estimate of these assumptions which we believe would be consistent with what a hypothetical marketplace participant would use. The variability of these factors depends on a number of conditions, including uncertainty about future events and our inability as a minority shareholder to control certain

| 25 |

outcomes and thus our accounting estimates may change from period to period. If other assumptions and estimates had been used when these tests were performed, impairment charges could have resulted.

As mentioned above, these factors do not change in isolation and, therefore, we do not believe it is practicable or meaningful to present the impact of changing a single factor. Furthermore, if management uses different assumptions or if different conditions occur in future periods, future impairment charges could result.

Leases

We recognize rent expense on a straight-line basis over the expected lease term, including option periods as described below. Within the provisions of certain leases there are escalations in payments over the base lease term, as well as renewal periods. The effects of the escalations have been reflected in rent expense on a straight-line basis over the expected lease term, which includes option periods when it is deemed to be reasonably assured that we would incur an economic penalty for not exercising the option. Percentage rent expense is generally based upon sales levels and is expensed as incurred. Certain leases include both base rent and percentage rent. We record rent expense on these leases based upon reasonably assured sales levels. The consolidated financial statements reflect the same lease terms for amortizing leasehold improvements as were used in calculating straight-line rent expense for each restaurant. Our judgments may produce materially different amounts of amortization and rent expense than would be reported if different lease terms were used.

Deferred Income Tax Valuation Allowance

We provide such allowance due to uncertainty that some of the deferred tax amounts may not be realized. Certain items, such as state and local tax loss carryforwards, are dependent on future earnings or the availability of tax strategies. Future results could require an increase or decrease in the valuation allowance and a resulting adjustment to income in such period.

Goodwill and Trademarks

Goodwill is recorded when the purchase price paid for an acquisition exceeds the estimated fair value of the net identified tangible and intangible assets acquired. Trademarks are considered to have an indefinite life. Goodwill and trademarks are not amortized, but are subject to impairment analysis at least once annually or more frequently upon the occurrence of an event or when circumstances indicate that a reporting unit’s carrying amount is greater than its fair value. At September 29, 2018, the Company performed a qualitative assessment of factors to determine whether further impairment testing is required. Based on the results of the work performed, the Company has concluded that no impairment loss was warranted at September 29, 2018. Qualitative factors considered in this assessment include industry and market considerations, overall financial performance and other relevant events, management expertise and stability at key positions. Additional impairment analyses at future dates may be performed to determine if indicators of impairment are present, and if so, such amount will be determined and the associated charge will be recorded to the Consolidated Statements of Income.

Stock-Based Compensation

The Company measures stock-based compensation cost at the grant date based on the fair value of the award and recognizes it as expense over the applicable vesting period using the straight-line method. Excess income tax benefits related to share-based compensation expense that must be recognized directly in equity are considered financing rather than operating cash flow activities.

| 26 |

The fair value of each of the Company’s stock options is estimated on the date of grant using a Black-Scholes option-pricing model that uses assumptions that relate to the expected volatility of the Company’s common stock, the expected dividend yield of our stock, the expected life of the options and the risk free interest rate. The Company issues new shares upon the exercise of employee stock options.

Recently Adopted and Issued Accounting Standards

See Note 1 of Notes to Consolidated Financial Statements for a description of recent accounting pronouncements, including those adopted in fiscal 2018 and the expected dates of adoption and the anticipated impact on the Consolidated Financial Statements.

Recent Developments

See Note 15 of Notes to Consolidated Financial Statements for a description of recent developments that have occurred subsequent to September 29, 2018.

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk |

Not applicable.

| Item 8. | Financial Statements and Supplementary Data |

Our Consolidated Financial Statements are included in this report immediately following Part IV.

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

None.

| Item 9A. | Controls and Procedures |

Evaluation of Disclosure Controls and Procedures.

As of September 29, 2018 (the end of the period covered by this report), management, with the participation of our Chief Executive Officer and Chief Financial Officer, evaluated the effectiveness of the design and operation of our disclosure controls and procedures (as defined in Rule 13a-15(e) and 15d-15(e) of the Securities Exchange Act of 1934, as amended). Based on that evaluation, our Chief Executive Officer and Chief Financial Officer concluded that, at the end of such period, our disclosure controls and procedures were effective and provided reasonable assurance that information required to be disclosed in our periodic SEC filings is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms, and that such information is accumulated and communicated to our management, including our Chief Executive Officer and Chief Financial Officer, as appropriate, to allow timely decisions regarding required disclosure. However, in evaluating the disclosure controls and procedures, management recognized that any controls and procedures, no matter how well designed and operated can provide only reasonable assurance of achieving the desired control objectives, and management necessarily was required to apply its judgment in evaluating the cost-benefit relationship of such possible controls and procedures.

| 27 |

Management’s Annual Report on Internal Control Over Financial Reporting.