UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 28, 2012

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number: 001-14543

____________________________________

TrueBlue, Inc.

(Exact name of Registrant as specified in its charter)

______________________________________

Washington | 91-1287341 | |

(State of Incorporation) | (IRS Employer ID) | |

1015 A Street, Tacoma, Washington | 98402 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (253) 383-9101

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common Stock without par value | The New York Stock Exchange | |

Securities registered under Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. Large accelerated filer ¨ Accelerated filer ý Non-accelerated filer ¨ (Do not check if a smaller reporting company) Smaller reporting company ¨

Indicate by check mark if the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

The aggregate market value (based on the NYSE quoted closing price) of the common stock held by non-affiliates of the registrant as of the last business day of the second fiscal quarter, June 29, 2012, was approximately $0.611 billion.

As of February 8, 2013, there were 40,609,618 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this report is incorporated by reference from the registrant’s definitive proxy statement relating to the Annual Meeting of Shareholders scheduled to be held May 15, 2013, which definitive proxy statement will be filed not later than 120 days after the end of the fiscal year to which this report relates.

COMMENT ON FORWARD LOOKING STATEMENTS

This Form 10-K contains forward-looking statements. These statements relate to our expectations for future events and future financial performance. Generally, the words “anticipate,” “believe,” “expect,” “intend,” “plan,” and similar expressions identify forward-looking statements. Forward-looking statements involve risks and uncertainties, and future events and circumstances could differ significantly from those anticipated in the forward-looking statements. These statements are only predictions. Actual events or results may differ materially. Factors which could affect our financial results are described in Item 1A of this Form 10-K. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Moreover, neither we nor any other person assume responsibility for the accuracy and completeness of the forward-looking statements. We undertake no duty to update any of the forward-looking statements after the date of this report to conform such statements to actual results or to changes in our expectations.

TrueBlue, Inc.

2012 Annual Report on Form 10-K

Table of Contents

Page | ||

PART I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

Page - 3

TrueBlue, Inc.

Form 10-K

PART I

Item 1. | BUSINESS |

TrueBlue, Inc. (“TrueBlue,” “we,” “us,” “our”) is a leading provider of temporary blue-collar staffing services. We provide a wide range of specialized blue-collar staffing services. We operate as Labor Ready for general labor, Spartan Staffing for light industrial services, CLP Resources for skilled trades, PlaneTechs for mechanics and technicians for the aviation and transportation industries, and Centerline Drivers for dedicated and temporary drivers. We have a network of 691 branches in all 50 states, Puerto Rico and Canada, customer on-site locations generally dedicated to one customer, and national service centers, which supply our customers with temporary workers.

We began operations in 1989 under the name Labor Ready, Inc. providing on-demand, general labor staffing services. We became a public company in 1995. In 2004 we began acquiring additional brands to expand our service offerings to customers in the blue-collar staffing market. Effective December 18, 2007, Labor Ready, Inc. changed its name to TrueBlue, Inc. We are headquartered in Tacoma, Washington.

Temporary Staffing Industry

The temporary staffing industry supplies temporary staffing services to minimize the cost and effort of hiring and administering permanent employees in order to rapidly respond to changes in business conditions, to temporarily replace absent employees, to temporarily fill new positions, and to convert fixed or permanent labor costs to variable or flexible costs. Temporary staffing companies act as intermediaries in matching available temporary workers to employer assignments. The demand for a flexible workforce continues to grow with competitive and economic pressures to reduce costs and respond to changing market conditions.

The temporary staffing industry is large and highly fragmented with many competing companies. No single company has a dominant share of the temporary staffing industry. Staffing companies compete both to recruit and retain a supply of temporary workers and to attract and retain customers to employ these workers. Customer demand for temporary staffing services is dependent on the overall strength of the labor market and trends toward greater workforce flexibility. The temporary staffing industry includes a number of markets focusing on business needs that vary widely in duration of assignment and level of technical specialization. We operate within the blue-collar staffing market of the temporary staffing industry.

The blue-collar staffing market is subject to volatility based on overall economic conditions. Historically, in periods of economic growth, the number of companies providing temporary staffing services has increased due to low barriers to entry and during recessionary periods the number of companies has decreased through consolidation, bankruptcies, or other events. The temporary staffing industry is experiencing increased demand in relation to total job growth as customers have placed a greater priority on maintaining a more flexible workforce.

Long-term Strategies

Our long term strategies are clearly focused on creating shareholder value. Creating differentiated services, developing transformational competitive advantages, and increasing the efficiency of our service delivery model are underlying strategic principles that guide our strategies.

Our primary strategic focus is creating specialization in the services we offer. Our customers have a variety of challenges in running their business, many of which are unique to the industry in which they operate. Our objective is to be the leading provider of blue-collar staffing by providing specialized service offerings which will improve the productivity and performance of our customers. We believe that specialization differentiates us from our competition and ensures we deliver industry specific solutions tailored to the specific needs of our customers. We have and continue to invest in building industry expertise in various blue collar markets. Those investments have strengthened our ability to provide compelling workforce solutions for our customers. We have also built our sales and service capabilities for national customers while maintaining our core strength of selling and servicing small to mid-sized businesses at the local level. Our specialization substantially improves our ability to provide quality solutions that customers value.

We believe technology can transform traditional methods of doing business in our industry. We are investing in mobile texting solutions which will drive substantial productivity gains in a variety of ways. We believe mobile solutions will increase the number and quality of potential workers as candidates are increasingly looking for efficient and convenient ways to connect with work

Page - 4

opportunities. We expect it will reduce the amount of time it takes our branches to match and assign temporary workers to jobs; particularly for hard-fill-jobs and large short-notice orders. We believe revenues will increase from new business and from fewer unfilled orders in our current business. Also, we believe the geographic reach of our branches will increase and provide the opportunity to reduce occupancy costs by consolidating local branches.

As we consolidate our branch network, we plan to centralize certain recruiting, placement, and customer service duties in major metropolitan areas. Historically, our branches are staffed by generalist positions performing a variety of sales and service activities. We plan to centralize and specialize selected sales and service activities to further improve the productivity and quality of our service.

Acquisitions continue to be a key growth strategy. We have completed a variety of acquisitions in the past and believe we have developed a strong set of competencies in assessing, valuing, and integrating acquisitions. We are excited about the future of the temporary staffing industry and believe we can continue to create shareholder value through acquisitions.

Operations

We provide a wide range of specialized blue-collar staffing services. We operate as Labor Ready for on-demand general labor, Spartan Staffing for skilled manufacturing and logistics labor, CLP Resources for skilled trades for commercial, industrial and energy construction as well as building and plant maintenance, PlaneTechs for skilled mechanics and technicians to the aviation and transportation industries, and, Centerline Drivers for temporary and dedicated drivers to the transportation and distribution industries. Our operations are all in the blue-collar staffing market of the temporary staffing industry. All our brands:

• | Provide blue-collar temporary labor services to our customers; |

• | Serve customers who have a need for temporary staff to perform blue-collar tasks which do not require a permanent employee; |

• | Build a temporary workforce through recruiting, screening and hiring. Temporary workers are dispatched to customers where they work under the supervision of our customers; |

• | Drive profitability by managing the bill rates to our customers and the pay rates to our workers. Profitable growth requires increased volume and or bill rates which grow faster than pay rates and leveraging our cost structure; and |

• | Use innovative technology to improve our ability to recruit quality workers, effectively match workers to the needs of our customers, and meet our customers' needs more efficiently. We are focused on improving the ease of doing business with us for both our temporary workers and customers. |

Our long-term financial performance expectations of all our brands are similar as are the underlying financial and economic metrics used to manage those brands. Profitable growth is driven by leveraging our cost structure across all brands to achieve economies of scale and investing in technology that improves our productivity.

Our business is generally conducted through a broad network of local branch locations, customer on-site locations generally dedicated to one customer and national service centers. We have a growing capability to service remote customer needs and work sites where we have no physical location. Management of our temporary staffing operations is coordinated from our headquarters in Tacoma, Washington where we provide support and centralized services to our brands and network of offices.

Customers

Our customer mix consists primarily of small and medium-sized businesses serviced by one or more branch offices. We also serve larger national customers. Our full range of blue-collar temporary staffing services enables us to meet all of the blue-collar staffing needs of our customers.

Methods used to sell temporary staffing services to customers vary depending on the customer’s need for temporary staffing services, the local labor supply, the length of assignment, the number of workers and skills required. We are a business-to-business sales provider. Our sales process takes place at the customer’s location. Success is often based on the experience and skill of the sales person and the strength of relationship with the customer. Retention of customers, exclusive of economic conditions, is dependent on the strength of our relationship with the customer, the skill, quality and tenure of temporary workers, and customer service skills.

During 2012, we served approximately 140,000 customers in the services, retail, wholesale, manufacturing, transportation, aviation, and construction industries. Our ten largest customers accounted for 22% of total revenue for 2012, 19% for 2011 and 19% for 2010. Sales to our largest customer accounted for 7% of total revenue for 2012, 8% for 2011 and 9% for 2010.

Page - 5

Employees and Temporary Associates

As of December 28, 2012 we employed approximately 2,900 full-time and part-time employees. In addition, we placed approximately 350,000 temporary workers on assignments with our customers during 2012. We recruit temporary workers daily so that we can be responsive to the planned as well as unplanned needs of the customers we serve. We attract our pool of temporary workers through personal referrals, online resources, extensive internal databases, advertising, job fairs, and various other methods. We identify the skills, knowledge, abilities, and personal characteristics of a temporary worker and match their competencies or capabilities to a customer’s requirements. This enables our customers to obtain immediate value by placing a highly productive and skilled employee on the job site. We use a variety of proprietary programs for identifying and assessing the skill level of our temporary workers when selecting a particular individual for a specific assignment and retaining those workers for future assignments. We believe that our assessment systems enable us to offer a higher quality of service by increasing productivity, decreasing turnover, and reducing absenteeism.

We provide a bridge to permanent, full-time employment for thousands of temporary workers each year. Temporary workers come to us to fill a short-term financial need, or as a flexible source of income while also working elsewhere or pursuing education. Many stay because of the flexibility that we offer. In many cases, we enable individuals to pay their rent, buy groceries, and remain self-sufficient. Temporary workers may be assigned to different jobs and job sites, and their assignments could last for as little as a single day or extend for several weeks or months. We provide our temporary workers meaningful work and the opportunity to improve their skills.

Our risk management practices have increased the safety of the work environment for our temporary workers. We have increased the involvement of our customers and temporary workers in our safety program. We have a variety of safety-related programs, provide safety information to temporary employees, and conduct job-site visits to increase the safety of employees while working for our customers.

We are considered the legal employer of our temporary workers and laws regulating the employment relationship are applicable to our operations. We consider our relations with our employees and temporary workers to be good.

Competition

We compete in the temporary staffing industry by offering a full range of blue-collar staffing services. The temporary staffing industry is large and fragmented, comprised of thousands of companies employing millions of people and generating billions of dollars in annual revenues.

We experience competition in attracting customers as well as qualified employment candidates. The staffing business is highly competitive with limited barriers to entry, with a number of firms offering services similar to those provided by us on a national, regional, or local basis. We compete with several multi-national full-service and specialized temporary staffing companies, as well as a multitude of local companies. In most geographic areas, no single company has a dominant share of the market. The majority of temporary staffing companies serving the blue-collar staffing market are locally-owned businesses. In many areas the local companies are the strongest competitors, largely due to their longevity in the market and the strength of their customer relationships.

Competitive forces have historically limited our ability to raise our prices to immediately and fully offset increased costs of doing business; some of which include increased temporary worker wages, costs for workers’ compensation, and unemployment insurance.

The most significant competitive factors in the staffing business are price, ability to promptly fill customer orders, success in meeting customers’ quality expectations of temporary workers, and appropriately addressing customer service issues. We believe we derive a competitive advantage from our service history and commitment to the blue-collar temporary employment market and our specialized approach in serving the industries of our customers. Also, our national presence and proprietary systems and programs including worker safety, risk management, and legal and regulatory compliance are key differentiators from many of our competitors.

Seasonality and Cyclical Nature of our Business

Our business experiences seasonal fluctuations. Our quarterly operating results are affected by the seasonality of our customers’ businesses. Demand for our staffing services is higher during the second and third quarters of the year and peaks in the third quarter. Demand is lower during the first and fourth quarters, in part due to limitations to outside work during the winter months. Our working capital requirements are primarily driven by temporary worker payroll and customer accounts receivable. Since receipts from customers lag payroll to temporary workers, working capital requirements increase substantially in periods of growth.

Page - 6

The staffing industry has historically been cyclical, often acting as an indicator of both economic downturns and upswings. Staffing customers tend to use temporary staffing to supplement their existing workforces and generally hire permanent workers when long-term demand is expected to increase. As a consequence, our revenues tend to increase quickly when the economy begins to grow and, conversely, our revenues also decrease quickly when the economy begins to weaken. While we have longer-term customer relationships, which are not directly dependent upon the economic cycle, these revenues are not significant enough to offset the impact of cyclical economic activity for our temporary staffing services.

Financial Information about Geographic Areas

The following table depicts our revenue earned from within the United States and from international operations for the past three fiscal years (in millions, except percentages).

2012 | 2011 | 2010 | ||||||||||||||||||

United States (including Puerto Rico) | $ | 1,341.5 | 96.5 | % | $ | 1,266.3 | 96.2 | % | $ | 1,105.5 | 96.2 | % | ||||||||

International operations (Canada) | 48.0 | 3.5 | % | 49.7 | 3.8 | % | 43.9 | 3.8 | % | |||||||||||

Total revenue from services | $ | 1,389.5 | 100.0 | % | $ | 1,316.0 | 100.0 | % | $ | 1,149.4 | 100.0 | % | ||||||||

The international operations are dependent on shared information and communications equipment housed and maintained in the United States. Net property and equipment located in international operations was less than 1% of total property and equipment in each of the last three fiscal years.

Available Information

Our Annual Report on Form 10-K, along with all other reports and amendments filed with or furnished to the Securities and Exchange Commission (“SEC”) are publicly available, free of charge, on our website at www.trueblue.com or at www.sec.gov as soon as reasonably practicable after such reports are filed with or furnished to the SEC. Our Corporate Governance Guidelines, Code of Business Conduct and Ethics, and Board Committee Charters are also posted to our website. The information on our website is not part of this or any other report we file with, or furnish to, the SEC.

Page - 7

Item 1A. | RISK FACTORS |

Investing in our securities involves risk. The following risk factors and all other information set forth in this Annual Report on Form 10-K should be considered in evaluating our future prospects. In particular, keep these risk factors in mind when you read “forward-looking” statements elsewhere in this report. Forward-looking statements relate to our expectations for future events and time periods. Generally, the words “anticipate,” “believe,” “expect,” “intend,” “plan” and similar expressions identify forward-looking statements. Forward-looking statements involve risks and uncertainties, and future events and circumstances could differ significantly from those anticipated in the forward-looking statements. If any of the events described below occurs, our business, financial condition, results of operations, liquidity or access to the capital markets could be materially and adversely affected.

Our business is significantly affected by fluctuations in general economic conditions.

The demand for our blue-collar staffing services is highly dependent upon the state of the economy and upon staffing needs of our customers. As economic activity slows, companies tend to reduce their use of temporary employees before terminating their regular employees. Significant declines in demand and corresponding revenues, can result in expense de-leveraging, which would result in lower profit levels. Any variation in the economic condition or unemployment levels of the United States, Puerto Rico and Canada or in the economic condition of any region or specific industry in which we have a significant presence may severely reduce the demand for our services and thereby significantly decrease our revenues and profits.

Our business is subject to extensive government regulation and a failure to comply with regulations could materially harm our business.

Our business is subject to extensive regulation. The cost to comply, and any inability to comply, with government regulation could materially harm our business. Increased government regulation of the workplace or of the employer-employee relationship, or judicial or administrative proceedings related to such regulation, could materially harm our business.

The Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010 (collectively, the “Health Care Reform Laws”) include various health-related provisions to take effect through 2014, including requiring most individuals to have health insurance and establishing new regulations on health plans. Although the Health Care Reform Laws do not mandate that employers offer health insurance, beginning in 2014 tax penalties will be assessed on large employers who do not offer health insurance that meets certain affordability or benefit requirements. Unless modified by regulations or subsequent legislation, providing such additional health insurance benefits to our temporary workers, or the payment of tax penalties if such coverage is not provided, will increase our costs. If we are unable to raise the rates we charge our customers to cover these costs, such increases in costs could materially harm our business.

We may incur employment related and other claims that could materially harm our business.

We employ individuals on a temporary basis and place them in our customers' workplaces. We have minimal control over our customers' workplace environments. As the employer of record of our temporary workers, we incur a risk of liability for various workplace events, including claims for personal injury, wage and hour violations, discrimination or harassment, and other actions or inactions of our temporary workers. In addition, some or all of these claims may give rise to litigation including class action litigation. A material adverse impact on our financial statements also could occur for the period in which the effect of an unfavorable final outcome becomes probable and can be reasonably estimated.

We cannot be certain that our insurance will be sufficient in amount or scope to cover all claims that may be asserted against us. Should the ultimate judgments or settlements exceed our insurance coverage, they could have a material effect on our business. We cannot be certain we will be able to obtain appropriate types or levels of insurance in the future, that adequate replacement policies will be available on acceptable terms or that the companies from which we have obtained insurance will be able to pay claims we make under such policies.

We are dependent on workers' compensation insurance coverage at commercially reasonable terms.

We provide workers' compensation insurance for our temporary workers. Our workers' compensation insurance policies are renewed annually. The majority of our insurance policies are with AIG, formerly known as Chartis. Our insurance carriers require us to collateralize a significant portion of our workers' compensation obligation. The majority of collateral is held in trust by a third party for the payment of these claims. The loss or decline in value of the collateral could require us to seek additional sources of capital to pay our workers' compensation claims. We cannot be certain we will be able to obtain appropriate types or levels of insurance in the future or that adequate replacement policies will be available on acceptable terms. As our business grows or our financial results deteriorate, the amount of collateral required will likely increase and the timing of providing collateral could be accelerated. Resources to meet these requirements may not be available. The loss of our workers' compensation insurance coverage

Page - 8

would prevent us from doing business in the majority of our markets. Further, we cannot be certain that our current and former insurance carriers will be able to pay claims we make under such policies.

Our liquidity may be materially adversely affected by constraints in the capital markets.

The principal sources of our liquidity are funds generated from operating activities, available cash and cash equivalents, and borrowings under our credit facility. We must have sufficient sources of liquidity to fund our working capital requirements, workers' compensation collateral requirements, service our outstanding indebtedness, and finance investment opportunities. Without sufficient liquidity, we could be forced to curtail our operations or we may not be able to pursue promising business opportunities.

Our failure to comply with the restrictive covenants under our revolving credit facility could result in an event of default, which, if not cured or waived, could result in our being required to repay these borrowings before their due date. If we are forced to refinance these borrowings on less favorable terms, or are unable to refinance at all, our results of operations and financial condition could be adversely affected by increased costs and rates.

Acquisitions and new business ventures may have an adverse effect on our business.

We expect to continue making acquisitions and entering into new business ventures or initiatives as part of our long-term business strategy. These acquisitions, new business ventures, and initiatives involve significant challenges and risks, including that they may not advance our business strategy, that we may not realize a satisfactory return on our investment, that we may experience difficulty in integrating operations, or diversion of management's attention from our other business. These events could cause harm to our operating results or financial condition.

We operate in a highly competitive business and may be unable to retain customers or market share.

The staffing services business is highly competitive and the barriers to entry are low. There are new competitors entering the market which may increase pricing pressures. In addition, long-term contracts form only a small portion of our revenue. Therefore, there can be no assurance that we will be able to retain customers or market share in the future. Nor can there be any assurance that we will, in light of competitive pressures, be able to remain profitable or, if profitable, maintain our current profit margins.

Our management information systems are vulnerable to damage and interruption.

The efficient operation of our business is dependent on our management information systems. We rely heavily on proprietary management information systems to manage our order entry, order fulfillment, pricing and collections, as well as temporary worker recruitment, dispatch and payment. Our management information systems, mobile device technology and related services, and other technology may not yield the intended results. Our systems may experience problems with functionality and associated delays. The failure of our systems to perform as we anticipate could disrupt our business and could result in decreased revenue and increased overhead costs, causing our business and results of operations to suffer materially. Our primary computer systems and operations are vulnerable to damage or interruption from power outages, computer and telecommunications failures, computer viruses, security breaches, catastrophic events and errors in usage by our employees. Failure of our systems to perform may require significant additional capital and management resources to resolve, causing material harm to our business.

Our results of operations could materially deteriorate if we fail to attract, develop and retain qualified employees.

Our performance is dependent on attracting and retaining qualified employees who are able to meet the needs of our customers. We believe our competitive advantage is providing unique solutions for each individual customer, which requires us to have highly trained and engaged employees. Our success depends upon our ability to attract, develop and retain a sufficient number of qualified employees, including management, sales, recruiting, service and administrative personnel. The turnover rate in the staffing industry is high, and qualified individuals of the requisite caliber and number needed to fill these positions may be in short supply. Our inability to recruit a sufficient number of qualified individuals may delay or affect the speed of our planned growth or strategy change. Delayed expansion, significant increases in employee turnover rates or significant increases in labor costs could have a material adverse effect on our business, financial condition and results of operations.

We may be unable to attract and retain sufficient qualified temporary workers.

We compete with other temporary staffing companies to meet our customer needs and we must continually attract qualified temporary workers to fill positions. Attracting and retaining some skilled temporary employees depends on factors such as desirability of the assignment, location, and the associated wages and other benefits. We have in the past experienced worker shortages and we may experience such shortages in the future. Further, if there is a shortage of temporary workers, the cost to employ these individuals could increase. If we are unable to pass those costs through to our customers, it could materially and adversely affect our business.

Page - 9

We may have additional tax liabilities that exceed our estimates.

We are subject to federal taxes and a multitude of state and local taxes in the United States and taxes in foreign jurisdictions. In the ordinary course of our business, there are transactions and calculations where the ultimate tax determination is uncertain. We are regularly subject to audit by tax authorities. Although we believe our tax estimates are reasonable, the final determination of tax audits and any related litigation could be materially different from our historical tax provisions and accruals. The results of an audit or litigation could materially harm our business.

Accidental disclosure of our employees' or customers' information could materially harm our business.

Failure to protect the integrity and security of our employees' and customers' information, including proprietary information, could expose us to litigation and materially damage our relationship with our employees and our customers. Further, data privacy is subject to frequently changing rules and regulations, which sometimes conflict among the various jurisdictions. Our failure to adhere to or successfully implement changes in response to the changing regulatory requirements could result in legal liability, additional compliance costs, and damage to our reputation.

Failure to maintain adequate financial and management processes and controls could lead to errors in our financial reporting.

Failure to maintain adequate financial and management processes and controls could lead to errors in our financial reporting. If our management is unable to certify the effectiveness of our internal controls or if our independent registered public accounting firm cannot render an opinion on the effectiveness of our internal control over financial reporting, or if material weaknesses in our internal controls are identified, we could be subject to regulatory scrutiny and a loss of public confidence. In addition, if we do not maintain adequate financial and management personnel, processes and controls, we may not be able to accurately report our financial performance on a timely basis, which could cause our stock price to fall.

Outsourcing certain aspects of our business could result in disruption and increased costs.

We have outsourced certain aspects of our business to third party vendors that subject us to risks, including disruptions in our business and increased costs. For example, we have engaged third parties to host and manage certain aspects of our data center information and technology infrastructure and to provide certain back office support activities. Accordingly, we are subject to the risks associated with the vendor's ability to provide these services to meet our needs. If the cost of these services is more than expected, or if the vendor or we are unable to adequately protect our data and information is lost, or our ability to deliver our services is interrupted, then our business and results of operations may be negatively impacted.

Item 1B. | UNRESOLVED STAFF COMMENTS |

None.

Item 2. | PROPERTIES |

We lease the building space at all of our branch offices except for two that we own in Florida. Under the majority of these leases, both parties have the right to terminate the lease on 90 days notice. We own an office building in Tacoma, Washington, which serves as our headquarters. Management believes all of our facilities are currently suitable for their intended use.

Item 3. | LEGAL PROCEEDINGS |

See discussion of legal contingencies and developments in Note 7 to the consolidated financial statements included in Part II, Item 8 of this Annual Report on Form 10-K.

Item 4. | MINE SAFETY DISCLOSURES |

None.

Page - 10

PART II

Item 5. | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information

Our common stock is listed on the New York Stock Exchange under the ticker symbol TBI. The table below sets forth the high and low sales prices for our common stock as reported by the New York Stock Exchange during the last two fiscal years:

High | Low | ||||||

December 28, 2012 | |||||||

Fourth Quarter | $ | 16.51 | $ | 11.84 | |||

Third Quarter | $ | 17.40 | $ | 14.18 | |||

Second Quarter | $ | 18.22 | $ | 13.59 | |||

First Quarter | $ | 18.13 | $ | 14.17 | |||

December 30, 2011 | |||||||

Fourth Quarter | $ | 14.69 | $ | 10.40 | |||

Third Quarter | $ | 16.43 | $ | 10.80 | |||

Second Quarter | $ | 17.58 | $ | 12.84 | |||

First Quarter | $ | 19.25 | $ | 14.68 | |||

Holders of the Corporation’s Capital Stock

We had approximately 561 shareholders of record as of February 8, 2013.

Dividends

No cash dividends have been declared on our common stock to date nor have any decisions been made to pay a dividend in the future. Payment of dividends is evaluated on a periodic basis and if a dividend were paid, it would be subject to the covenants of our lending facility, which may have the effect of restricting our ability to pay dividends.

Stock Repurchases

Under our authorized stock repurchase programs, we repurchased and retired 0.3 million shares of our common stock during 2012 for a total amount of $4.4 million, including commissions. In July 2011, our Board of Directors approved a program to repurchase $75 million of our outstanding common stock. As of December 28, 2012, $35.2 million remained available for repurchase of common stock under the current authorization, which has no expiration date. We repurchased and retired 4.5 million shares of our common stock during 2011 for a total amount of $56.9 million including commissions.

The table below includes repurchases of our common stock pursuant to publicly announced plans or programs and those not made pursuant to publicly announced plans or programs during the thirteen weeks ended December 28, 2012.

Period | Total number of shares purchased (1) | Weighted average price paid per share (2) | Total number of shares purchased as part of publicly announced plans or programs | Maximum number of shares (or approximate dollar value) that may yet be purchased under plans or programs at period end (3) | |||||||

9/29/12 through 10/26/12 | 842 | $15.86 | — | $35.2 million | |||||||

10/27/12 through 11/23/12 | 1,756 | $13.70 | — | $35.2 million | |||||||

11/24/12 through 12/28/12 | 2,880 | $14.60 | — | $35.2 million | |||||||

Total | 5,478 | $14.50 | — | ||||||||

____________________

(1) | During the thirteen weeks ended December 28, 2012, we purchased 5,478 shares in order to satisfy employee tax withholding obligations upon the vesting of restricted stock. These shares were not acquired pursuant to any publicly announced purchase plan or program. |

(2) | Weighted average price paid per share does not include any adjustments for commissions. |

(3) | Our Board of Directors authorized a $75 million share repurchase program in July 2011 that does not have an expiration date. As of December 28, 2012, $35.2 million remains available for repurchase of our common stock under the current authorization. |

Page - 11

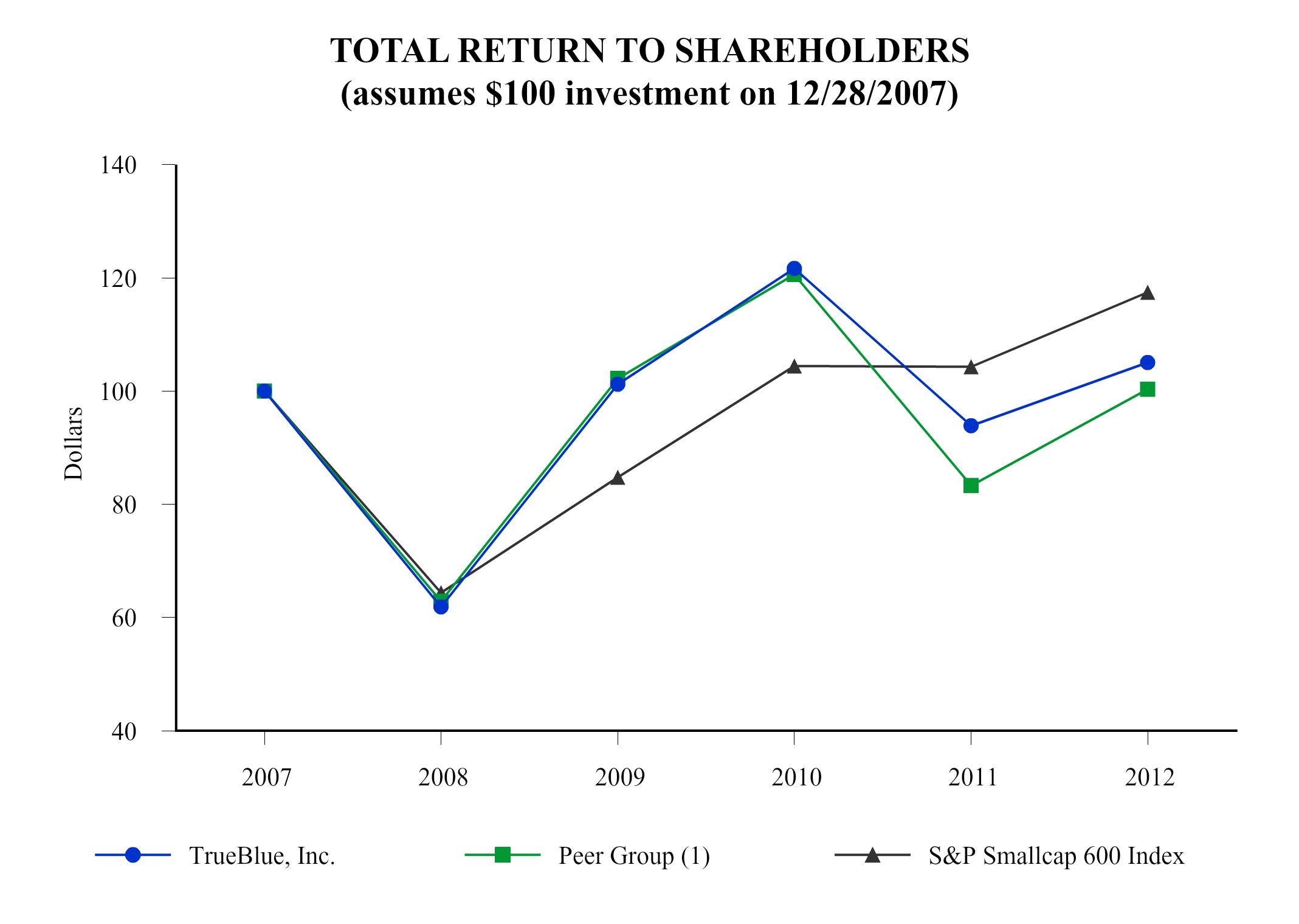

TrueBlue Stock Comparative Performance Graph

The following graph depicts our stock price performance from December 28, 2007 through December 28, 2012, relative to the performance of the S&P Smallcap 600 Index, and a peer group of companies in the temporary staffing industry. All indices shown in the graph have been reset to a base of 100 as of December 28, 2007, and assume an investment of $100 on that date and the reinvestment of dividends, if any, paid since that date.

COMPARISON OF 5-YEAR CUMULATIVE TOTAL RETURN

Among TrueBlue, Inc., the S&P Smallcap 600 Index

and Selected Peer Group

Total Return Analysis | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |||||||||||||||||

TrueBlue, Inc. | $ | 100 | $ | 62 | $ | 101 | $ | 122 | $ | 94 | $ | 105 | |||||||||||

Peer Group (1) | $ | 100 | $ | 63 | $ | 102 | $ | 121 | $ | 83 | $ | 100 | |||||||||||

S&P Smallcap 600 Index (2) | $ | 100 | $ | 64 | $ | 85 | $ | 104 | $ | 104 | $ | 117 | |||||||||||

___________________

(1) | The peer group includes Kelly Services, Inc., Manpower, Inc., Robert Half International, Adecco SA and Randstad. |

(2) | In 2012 we selected the S&P Smallcap 600 Index as an index comparison due to our market capitalization being more in line with this index as opposed to the using the S&P Midcap 400 Index. The S&P Midcap 400 Index had a 2012 total return of $116 based on an assumed $100 investment on 12/28/2007. |

Page - 12

Item 6. | SELECTED FINANCIAL DATA |

The following selected consolidated financial information has been derived from our audited Consolidated Financial Statements. The data should be read in conjunction with item 1A “Risk Factors”, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our Consolidated Financial Statements and the notes included in Item 8 of this Annual Report on Form 10-K.

Summary Consolidated Financial and Operating Data

As of and for the Fiscal Year Ended (1)

(in millions, except per share data and number of branches)

2012 (52 Weeks) | 2011 (52 Weeks) | 2010 (53 Weeks) | 2009 (52 Weeks) | 2008 (52 Weeks) | |||||||||||||||

Statements of Operations Data: | |||||||||||||||||||

Revenue from services | $ | 1,389.5 | $ | 1,316.0 | $ | 1,149.4 | $ | 1,018.4 | $ | 1,384.3 | |||||||||

Cost of services | 1,017.1 | 969.0 | 845.9 | 727.4 | 971.8 | ||||||||||||||

Gross profit | 372.4 | 347.0 | 303.5 | 291.0 | 412.5 | ||||||||||||||

Selling, general and administrative expenses | 300.5 | 282.8 | 258.8 | 262.2 | 332.1 | ||||||||||||||

Goodwill and intangible asset impairment | — | — | — | — | 61.0 | ||||||||||||||

Depreciation and amortization | 18.9 | 16.4 | 16.5 | 17.0 | 16.8 | ||||||||||||||

Interest and other income, net | 1.6 | 1.5 | 0.9 | 2.3 | 5.5 | ||||||||||||||

Income before tax expenses | 54.6 | 49.3 | 29.1 | 14.1 | 8.1 | ||||||||||||||

Income tax expense | 21.0 | 18.5 | 9.3 | 5.3 | 12.3 | ||||||||||||||

Net income (loss) | $ | 33.6 | $ | 30.8 | $ | 19.8 | $ | 8.8 | $ | (4.2 | ) | ||||||||

Net income (loss) per diluted share | $ | 0.84 | $ | 0.73 | $ | 0.46 | $ | 0.20 | $ | (0.10 | ) | ||||||||

Weighted average diluted shares outstanding | 39.9 | 42.3 | 43.5 | 43.0 | 42.9 | ||||||||||||||

At Fiscal Year End, | |||||||||||||||||||

2012 | 2011 | 2010 | 2009 | 2008 | |||||||||||||||

Balance Sheet Data: | |||||||||||||||||||

Working capital | $ | 203.6 | $ | 168.3 | $ | 207.6 | $ | 163.2 | $ | 147.5 | |||||||||

Total assets | $ | 601.7 | $ | 560.8 | $ | 546.5 | $ | 518.1 | $ | 519.7 | |||||||||

Long-term liabilities | $ | 154.5 | $ | 154.9 | $ | 147.8 | $ | 147.9 | $ | 154.2 | |||||||||

Total liabilities | $ | 268.1 | $ | 267.2 | $ | 233.8 | $ | 232.7 | $ | 249.5 | |||||||||

Branches open at period end | 691 | 712 | 721 | 754 | 850 | ||||||||||||||

____________________

(1) | Our fiscal year ends on the last Friday in December. The 2012 fiscal year ended on December 28, 2012, included 52 weeks. The 2010 fiscal year ended on December 31, 2010, included 53 weeks, with the 53rd week falling in our fourth fiscal quarter. All other prior years presented included 52 weeks. |

The operating results reported above include the results of acquisitions subsequent to their respective purchase dates. In February 2008, we acquired substantially all of the assets of TLC Services Group, Inc. and in April 2008, we acquired 100% of the common stock of Personnel Management, Inc.

No cash dividends have been declared on our common stock to date nor have any decisions been made to pay a dividend in the future.

Page - 13

Item 7. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION |

The following discussion should be read in conjunction with, and is qualified in its entirety by, the Consolidated Financial Statements and Notes thereto included in Item 8 in this Annual Report on Form 10-K. This item contains forward-looking statements that involve risks and uncertainties. Actual results may differ materially from those indicated in such forward-looking statements. Factors that may cause such a difference include, but are not limited to, those discussed in “Item 1A, Risk Factors.”

Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) is designed to provide the reader of our financial statements with a narrative from the perspective of management on our financial condition, results of operations, liquidity and certain other factors that may affect future results. Our MD&A is presented in six sections:

• | Overview |

• | Results of Operations |

• | Liquidity and Capital Resources |

• | Contractual Obligations and Commitments |

• | Summary of Critical Accounting Policies |

• | New Accounting Standards |

OVERVIEW

TrueBlue is a leading provider of temporary blue-collar staffing. We provide a wide range of specialized blue-collar staffing services. We have a network of 691 branches in all 50 states, Puerto Rico and Canada, customer on-site locations generally dedicated to one customer, and national service centers which supply our customers with temporary workers. In 2012, we connected approximately 350,000 people to work through the following blue-collar staffing brands: Labor Ready for general labor, Spartan Staffing for light industrial services, CLP Resources for skilled trades, PlaneTechs for aviation and diesel mechanics and technicians, and Centerline Drivers for dedicated and temporary drivers. Headquartered in Tacoma, Washington, we serve approximately 140,000 businesses primarily in the services, construction, transportation, manufacturing, retail and wholesale industries.

Revenue grew to $1.4 billion for 2012, a 5.6% increase compared to the prior year. Revenue growth slowed in the second half of 2012 due to lower revenue from a large customer and softening growth trends across the business. Services related to this large customer are project based and have been declining throughout the year as the project matures and our customer makes workforce adjustments. Excluding revenue from this customer, revenue grew 8.6%. The growth is driven primarily by our continued success in renewable energy construction projects along with an improving construction market.

Our revenue growth is also due to the continued success of our specialized market sales and service strategy. Our dedicated sales leaders have expertise in the specific industries we serve. They partner with our service teams to meet the specific project needs of our national customers. Likewise, they provide our branches with best practice industry knowledge including sales and service methods for each industry. Our local sales and service teams build strong customer relationships and loyalty in providing tailored solutions that meet the day to day needs of our local customers.

Gross profit as a percent of revenue for fiscal 2012 of 26.8% improved by 0.4% compared to 2011 primarily due to increased bill rates which more than offset increases to minimum wages and unemployment taxes in 2012. We continue to be selective in the customers we serve and diligent in our approach to setting appropriate bill rates.

Selling, general, and administrative expenses as a percentage of revenue remained relatively constant at 21.6% for 2012 as compared to 21.5% for the prior year. Revenue from a large customer declined approximately $30 million compared to 2011. The operations servicing this customer were not reduced as they are located in a national recruiting and service center that is being leveraged to grow other service lines.

Net income grew by 9.2% to $34 million, or $0.84 per diluted share for fiscal 2012, compared to a net income of $31 million, or $0.73 per diluted share, for fiscal 2011.

We are in a strong financial position to fund working capital needs for planned 2013 growth and expansion opportunities. We have cash and cash equivalents of $130 million at December 28, 2012. As of December 28, 2012, the maximum $80 million was available under the Revolving Credit Facility and $7 million of letters of credit had been issued against the facility, leaving an unused portion of $73 million.

Page - 14

RESULTS OF OPERATIONS

The following table presents selected financial data (in millions, except percentages and per share amounts):

2012 | 2011 | 2010 | |||||||||

Revenue from services | $ | 1,389.5 | $ | 1,316.0 | $ | 1,149.4 | |||||

Total revenue growth % | 5.6 | % | 14.5 | % | 12.9 | % | |||||

Gross profit as a % of revenue | 26.8 | % | 26.4 | % | 26.4 | % | |||||

Selling, general and administrative expenses | $ | 300.5 | $ | 282.8 | $ | 258.7 | |||||

Selling, general and administrative expenses as a % of revenue | 21.6 | % | 21.5 | % | 22.5 | % | |||||

Income from operations | $ | 53.0 | $ | 47.8 | $ | 28.3 | |||||

Income from operations as a % of revenue | 3.8 | % | 3.6 | % | 2.5 | % | |||||

Net Income | $ | 33.6 | $ | 30.8 | $ | 19.8 | |||||

Net Income per diluted share | $ | 0.84 | $ | 0.73 | $ | 0.46 | |||||

Our business experiences seasonal fluctuations. Our quarterly operating results are affected by the seasonality of our customers’ businesses as well as timing and duration of project work. Demand for our staffing services is higher during the second and third quarters of the year with demand peaking in the third quarter and lower during the first and fourth quarters, in part due to limitations to outside work during the winter months.

Revenue

Revenue from services in comparison with the same period in the prior year was as follows (in millions, except percentages):

2012 | 2011 | 2010 | |||||||||

Revenue from services | $ | 1,389.5 | $ | 1,316.0 | $ | 1,149.4 | |||||

Total revenue growth % | 5.6 | % | 14.5 | % | 12.9 | % | |||||

Revenue grew to $1.4 billion for 2012, a 5.6% increase compared to the prior year. Revenue growth slowed in the second half of 2012 due to manufacturing declines, softening growth trends across the business, and lower revenue from a large customer. Services related to this large customer are project based and have been declining throughout the year as the project matures and our customer makes workforce adjustments. Excluding revenue from this customer revenue grew 8.6%. Our revenue growth is also due to the continued success of our specialized market sales and service strategy. Our dedicated sales leaders have expertise in the specific industries we serve. They partner with our service teams to meet the specific project needs of our national customers. Likewise, they provide our branches with best practice industry knowledge including sales and service methods for each industry. Our local sales and service teams build strong customer relationships and loyalty in providing tailored solutions that meet the day to day needs of our local customers. As a result we have experienced continued success in renewable energy construction projects along with an improving construction market.

For fiscal 2011, revenue grew to $1.3 billion, a 14.5% increase compared to the prior year. The strong revenue growth in 2011 was primarily driven by strong demand for our services across most major industries and geographies. We experienced double digit revenue growth in most of the industry groups we serve.

Gross profit

Gross profit in comparison with the same period in the prior year was as follows (in millions, except percentages):

2012 | 2011 | 2010 | |||||||||

Gross profit | $ | 372.4 | $ | 347.0 | $ | 303.5 | |||||

Gross profit as a % of revenue | 26.8 | % | 26.4 | % | 26.4 | % | |||||

Page - 15

Gross profit represents revenues from services less direct costs of services, which consist of payroll, payroll taxes, workers' compensation insurance costs, and reimbursable costs. Gross profit as a percent of revenue improved by 0.4% for fiscal 2012 primarily due to increased bill rates which more than offset increases to minimum wages and unemployment taxes in 2012. Our team continues to leverage our specialized approach in the blue-collar market along with disciplined pricing to drive higher gross margin. We are selective in the customers we serve and diligent in our approach to setting appropriate bill rates.

Workers’ compensation expense was 3.8% of revenue for fiscal 2012 and 3.9% for fiscal 2011. We actively manage the safety of our temporary workers with our risk management programs and work together with our network of service providers to control costs. We further reduced accidents for fiscal 2012 and the associated cost of workers' compensation.

For Fiscal 2011, gross profit as a percentage of revenue was unchanged compared to fiscal 2010 due to offsetting factors. Gross profit as a percentage of revenue for fiscal 2010 included the benefit of HIRE Act credits, net of other payroll tax items, of 0.2% of revenue. The HIRE Act provided incentives for hiring and retaining workers by exempting the employer share of the social security tax on wages paid to qualified individuals beginning on March 18, 2010 and expired on December 31, 2010. Excluding the benefit of these net 2010 HIRE Act credits, gross profit as a percent of revenue for 2011 compared to 2010 has improved by 0.2%. The improvement was primarily due to our success with pricing and increased billing rates. Workers’ compensation expense was 3.9% of revenue for fiscal 2011 and 3.8% for fiscal 2010.

Selling, general and administrative expenses

Selling, general and administrative (“SG&A”) expenses were as follows (in millions, except percentages):

2012 | 2011 | 2010 | |||||||||

Selling, general and administrative expenses | $ | 300.5 | $ | 282.8 | $ | 258.7 | |||||

Percentage of revenue | 21.6 | % | 21.5 | % | 22.5 | % | |||||

SG&A as a percentage of revenue remained relatively constant at 21.6% for 2012 as compared to 21.5% for the prior year. The increase in SG&A spending of $17.7 million or 6.2% for fiscal 2012 is primarily due to the variable selling and other operating expenses associated with the revenue increase of $73.5 million or 5.6%. Excluding revenue from a large customer, revenue increased $103.8 million or 8.6% over the prior year. Revenue from this large customer declined approximately $30 million compared to 2011. The operations servicing this customer were not reduced as they are located in a national recruiting and service center that is being leveraged to grow other service lines. We remain focused on leveraging our cost structure which should produce incremental operating margins with additional future revenue.

We have continued to invest in our specialized vertical market sales and service strategy and projects to further improve our efficiency and effectiveness in recruiting and retaining our temporary workers and attracting and retaining our customers. We completed a major investment in the operating system of our largest brand during 2012. We are seeing the benefits of improved operating efficiency.

For fiscal 2011, SG&A declined to 21.5% as a percentage of revenue as compared to 22.5% for fiscal 2010. During 2011 we produced strong incremental operating margins as we leveraged our fixed cost structure. The increase in SG&A spending for 2011 was primarily due to two factors. First, we experienced an expected increase in variable expenses to support the increased revenue of $167 million over the prior year. Second, we invested in specialized sales and marketing personnel to sell to and serve our vertical market customer groups. Our vertical market specialists and their programs made significant contributions to our revenue growth. We also filled open sales and service positions in local markets and made a variety of market adjustment increases to compensation to retain our key performers.

Depreciation and amortization and interest

Depreciation and amortization and interest were as follows (in millions, except percentages):

2012 | 2011 | 2010 | |||||||||

Depreciation and amortization | $ | 18.9 | $ | 16.4 | $ | 16.5 | |||||

Percentage of revenue | 1.4 | % | 1.2 | % | 1.4 | % | |||||

Depreciation and amortization for fiscal 2012 increased over the prior year by $2.5 million primarily from increased capital spending on enterprise technology improvement projects. These projects are designed to further improve our efficiency and effectiveness in recruiting and retaining our temporary workers and attracting and retaining our customers.

Page - 16

Interest and other income, net

Depreciation and amortization and interest were as follows (in millions, except percentages):

2012 | 2011 | 2010 | |||||||||

Interest and other income, net | $ | 1.6 | $ | 1.5 | $ | 0.9 | |||||

Percentage of revenue | 0.1 | % | 0.1 | % | 0.1 | % | |||||

Net interest income for 2012 remained relatively flat when compared to 2011. Net interest income for 2011 increased over 2010 due to increased yields on our restricted cash and investments and the 2011 renewal of our revolving credit facility with lower fees and cost to borrow.

Income taxes

The effective income tax rate was as follows (in millions except percentages):

2012 | 2011 | 2010 | |||||||||

Income tax expense | $ | 21.0 | $ | 18.5 | $ | 9.3 | |||||

Effective income tax rate | 38.4 | % | 37.6 | % | 32.0 | % | |||||

Our effective tax rate on earnings for 2012 was 38.4% compared to 37.6% for the same period in 2011. The increase in the effective income tax rate is due primarily to federal Work Opportunity Tax Credits which largely expired at the end of 2011. This income tax credit was designed to encourage employers to hire workers from certain targeted groups with higher-than-average unemployment rates. The principal difference between the statutory federal income tax rate of 35% and our effective income tax rate results from state income taxes, federal tax credits and certain non-deductible expenses. The lower effective tax rate in 2010 was primarily due to the favorable resolution of certain prior year tax matters.

The American Taxpayer Relief Act of 2012 ("the Act") was signed into law on January 2, 2013. The Act retroactively restored the Work Opportunity Tax Credit. Because a change in tax law is accounted for in the period of enactment, the retroactive effect of the Act on the Company's U.S. federal taxes for 2012, a benefit of approximately $3.2 million, will be recognized in 2013. In addition, we expect the Act's extension of these provisions through the end of 2013 will reduce our estimated annual effective tax rate for 2013 compared to 2012.

Results of Operations Future Outlook

The following highlights represent our expectations in regard to operating trends for fiscal year 2013. These expectations are subject to revision as our business changes with the overall economy:

• | Our top priority remains to increase revenue and leverage our cost structure which should produce incremental operating margins with additional future revenue. We will continue to invest in our specialized sales and customer service programs which we believe will enhance our ability to capitalize on further revenue growth and customer retention. We actively pursue large project opportunities in vertical markets with growth opportunities. One of our largest successes is in the construction of renewable energy projects. While our growth rates have diminished due to more challenging prior year comparisons, renewable energy projects remain an attractive opportunity. |

• | Effective February 4, 2013, we acquired MDT Personnel, the third-largest general labor staffing firm in the United States. MDT supplies blue-collar labor to industries similar to those served by TrueBlue, including construction, event staffing, disaster recovery, hospitality, and manufacturing through its network of 105 branches and 15 customer on-site locations in 25 states. TrueBlue will expand the size of its general labor business by merging MDT's operations with those of the Labor Ready brand. Selected branches will be consolidated to leverage our cost structure and produce long term incremental operating margins. The acquisition will enhance TrueBlue's national position as the leading provider of dependable blue-collar temporary labor. The decision to acquire MDT's operations reflects our overall optimism about growth in the staffing industry. We will continue to pursue other opportunities to grow our share of the blue collar market through acquisitions. |

• | As the economy grows, we will continue to evaluate opportunities to expand our market presence. All of our multi-location brands have opportunities to expand through new physical locations or by sharing existing locations. Where possible, we plan to expand the presence of our brands by sharing existing locations to achieve cost synergies. We plan to build on our success with centralized recruitment and dispatch of our temporary workers to locations without physical branches and expand our geographic reach. |

Page - 17

• | We have been investing in mobile technology solutions. We see compelling opportunities to improve the speed in assigning candidates to jobs and increase the productivity of our branch employees resulting in the consolidation of branches and other benefits to our cost structure. These technologies are currently under development and we expect to deploy them during the middle of 2013. We believe this will position us to begin generating efficiencies during the back half of 2013. The extent of additional efficiencies will be understood after our deployment and evaluation in 2013. |

• | Services for a large customer project have been declining throughout 2012 as the project matures and our customer makes workforce adjustments. While we expect continued revenue from this customer, our work is project based and the completion of certain projects will continue to impact our revenue trends. Revenue from this customer was approximately $76 million in 2012. We expect that to continue to decline in 2013. |

• | Customer demand for blue-collar staffing services is dependent on the overall strength of the labor market and trends towards greater workforce flexibility within the blue-collar markets in which we operate. Due to our industry's sensitivity to economic factors, the inherent difficulty in forecasting the direction and strength of the economy and the short term nature of staffing assignments, our visibility for future demand is limited. As a result, we monitor a number of economic indicators as well as certain trends to estimate future revenue. Future results will be dependent on whether the underlying economic uncertainty continues, trends in customer preference towards a more flexible workforce continue, and our ability to more effectively and efficiently serve customer needs. Based on these anticipated trends, we expect continued uncertainty in the economy and pressure on revenue in 2013. However, we are encouraged by an improving construction market and diminishing uncertainty. |

LIQUIDITY AND CAPITAL RESOURCES

Our principal source of liquidity is operating cash flows. Our net income and, consequently, our cash provided from operations are impacted by sales volume, timing of collections, seasonal sales patterns and profit margins. Over the past three fiscal years, net cash provided by operations was approximately $124.9 million.

Cash flows from operating activities

Our cash flows from operating activities were as follows (in millions):

2012 | 2011 | 2010 | |||||||||

Net income | $ | 33.6 | $ | 30.8 | $ | 19.8 | |||||

Adjustments to reconcile net income to net cash from operating activities: | |||||||||||

Depreciation and amortization | 18.9 | 16.4 | 16.5 | ||||||||

Provision for doubtful accounts | 7.0 | 6.6 | 8.2 | ||||||||

Stock-based compensation | 7.9 | 7.4 | 7.2 | ||||||||

Deferred income taxes | 3.1 | (1.9 | ) | 5.3 | |||||||

Other operating activities | 1.9 | (0.5 | ) | (0.2 | ) | ||||||

Changes in operating assets and liabilities: | |||||||||||

Accounts receivable | (20.4 | ) | (51.8 | ) | (11.6 | ) | |||||

Income taxes | (3.7 | ) | 3.5 | (3.3 | ) | ||||||

Accounts payable and other accrued expenses | 1.3 | 16.2 | 3.4 | ||||||||

Workers' compensation claims reserve | 3.7 | 4.5 | (2.2 | ) | |||||||

Other assets and liabilities | (1.0 | ) | (0.6 | ) | (1.1 | ) | |||||

Net cash provided by operating activities | $ | 52.3 | $ | 30.6 | $ | 42.0 | |||||

Net cash provided by operating activities was $52.3 million for fiscal 2012 as compared to net cash provided by operating activities of $30.6 million for fiscal 2011.

• | The increase in cash from operating activities is primarily due to net income of $33.6 million. |

• | In 2012, accounts receivable increased by $20.4 million primarily due to continued revenue growth. In 2011, accounts receivable increased by $51.8 million due to revenue growth and a low beginning balance due to significant customer payments received at the end of 2010. |

Page - 18

• | The increase in depreciation and amortization during 2012 is primarily due to increased capital spending focused on enterprise technology improvement projects. These projects are designed to further improve our efficiency and effectiveness in recruiting and retaining our temporary workers and attracting and retaining our customers. |

• | Generally our workers' compensation reserve for estimated claims increases as temporary labor services increase and decreases as temporary labor services decline. During the current year, our workers' compensation reserve increased as we increased the delivery of temporary labor services, partially offset by the timing of claim payments. |

• | Income taxes receivable increased in 2012 due to over payments of estimated taxes as a result of larger than expected deductions. |

Cash flows from investing activities

Our cash flows from investing activities were as follows (in millions):

2012 | 2011 | 2010 | |||||||||

Capital expenditures | $ | (17.8 | ) | $ | (9.7 | ) | $ | (7.0 | ) | ||

Change in restricted cash and cash equivalents | 7.6 | 68.5 | 3.9 | ||||||||

Purchase of restricted investments | (33.8 | ) | (88.2 | ) | — | ||||||

Maturities of restricted investments | 18.1 | 9.3 | — | ||||||||

Other | (0.3 | ) | (6.8 | ) | (0.3 | ) | |||||

Net cash used in investing activities | $ | (26.2 | ) | $ | (26.9 | ) | $ | (3.4 | ) | ||

• | Capital expenditures were higher in 2012 primarily related to investments made to upgrade our proprietary information systems and invest in enterprise technology improvement projects. These projects are designed to further improve our efficiency and effectiveness in recruiting, dispatching and retaining our workers as well as leveraging our centralized service delivery and making it easier for the customer to do business. We anticipate that total capital expenditures will be approximately $10 million in 2013. |

• | Restricted cash and investments consist primarily of collateral that has been provided or pledged to insurance carriers and state workers' compensation programs. The change in restricted cash and cash equivalents is primarily a product of purchasing restricted investments, maturities on restricted investments, and payments to workers' compensation insurance providers.When combining this change with purchases of restricted investments net of maturities of restricted investments, restricted cash and investments increased by $8.1 million for fiscal 2012. This increase is primarily due to an increase in the collateral requirements by our workers' compensation insurance providers related to growth in operations and due the timing of payments to our insurance providers. |

In 2011, the changes to restricted cash and investments were primarily due an agreement we entered into with AIG, formerly known as Chartis, and the Bank of New York Mellon creating a trust ("Trust") which holds the majority of our collateral obligations under existing workers' compensation insurance policies previously held directly by AIG. Restricted investments increased by $10.4 million for 2011, primarily due to additional restricted cash and investments required as collateral due to growth.

• | The 2011 change to Other includes the purchase of a staffing company and a technology company in 2011. |

Page - 19

Cash flows from financing activities

Our cash flows from financing activities were as follows (in millions):

2012 | 2011 | 2010 | |||||||||

Purchases and retirement of common stock | $ | (4.4 | ) | $ | (56.9 | ) | $ | — | |||

Net proceeds from stock option exercises and employee stock purchase plans | 4.2 | 1.1 | 1.1 | ||||||||

Common stock repurchases for taxes upon vesting of restricted stock | (2.2 | ) | (1.8 | ) | (1.6 | ) | |||||

Payments on debt | (4.5 | ) | (0.3 | ) | (0.4 | ) | |||||

Other | 0.7 | 0.7 | 0.1 | ||||||||

Net cash used in financing activities | $ | (6.2 | ) | $ | (57.2 | ) | $ | (0.8 | ) | ||

• | Under our authorized stock repurchase program, we repurchased and retired 0.3 million shares of our common stock during fiscal 2012 for a total amount of $4.4 million including commissions. We repurchased and retired 4.5 million shares of our common stock during fiscal 2011 for a total amount of $56.9 million including commissions. |

Future outlook

We are in a strong financial position to fund working capital needs for planned growth. The strength of our current financial position is highlighted as follows:

• | We have cash and cash equivalents of $129.5 million as of December 28, 2012. |

• | Our borrowing availability under our credit facility is principally based on accounts receivable and the value of our corporate building. We have $72.8 million of borrowing available under our credit facility as of December 28, 2012. We believe the credit facility provides adequate borrowing availability. |

• | The majority of our workers’ compensation payments are made from restricted cash versus cash from operations. |

• | On July 25, 2012, we filed a $100 million Shelf Registration Statement with the Securities and Exchange Commission that replaced our previous Shelf Registration which expired in July 2012. The Shelf Registration allows us to sell various securities in amounts and prices determined at the time of sale. The filing enables us to access capital efficiently and quickly if needed, however, we have no current plans to make an offering. |

We believe that cash provided from operations and our capital resources will be adequate to meet our cash requirements over the next twelve months, and thereafter for the foreseeable future. However, should economic conditions again deteriorate, our financial results could be adversely impacted and we may need to seek additional sources of capital. These additional sources of financing may not be available, or may not be available on commercially reasonable terms.

Capital resources

We have a credit agreement with Bank of America, N.A. and Wells Fargo Capital Finance, LLC for a secured revolving credit facility of up to a maximum of $80 million (the “Revolving Credit Facility”). The Revolving Credit Facility expires in September 2016.

The maximum amount we can borrow under the Revolving Credit Facility is subject to certain borrowing limits. Specifically, we are limited to the sum of 85% of our eligible accounts receivable and the liquidation value of our Tacoma headquarters office building not to exceed $15 million, which is reduced quarterly by $0.4 million. As of December 28, 2012, the Tacoma headquarters office building liquidation value totaled $13.5 million. This borrowing limit is further reduced by the sum of a reserve in an amount equal to the payroll and payroll taxes for our temporary employees for one payroll cycle and other reserves if deemed applicable. As of December 28, 2012, the maximum $80 million was available and letters of credit in the amount of $7.2 million had been issued against the facility, leaving an unused portion of $72.8 million. The letters of credit collateralize a portion of our workers' compensation obligation.

The Revolving Credit Facility requires that we maintain liquidity in excess of $12 million or be subject to a fixed charge coverage ratio. Liquidity is defined as the amount we are entitled to borrow as advances under the Revolving Credit Facility plus the amount of cash and cash equivalents held in accounts subject to a control agreement benefiting the lenders. The amount we were entitled to borrow at December 28, 2012 was $72.8 million and the amount of cash and cash equivalents under control agreements was

Page - 20

$128.3 million for a total of $201.1 million of liquidity, which is well in excess of the minimum liquidity requirement. We are currently in compliance with all covenants related to the Revolving Credit Facility.

Under the terms of the Revolving Credit Facility, we pay a variable rate of interest on funds borrowed that is based on LIBOR or the Prime Rate, at our option, plus an applicable spread based on excess liquidity as set forth below:

Excess Liquidity | Prime Rate Loans | LIBOR Rate Loans | ||

Greater than $40 million | 0.50% | 1.50% | ||

Between $20 million and $40 million | 0.75% | 1.75% | ||

Less than $20 million | 1.00% | 2.00% | ||

A fee on borrowing availability of 0.25% is also applied against the unused portion of the Revolving Credit Facility. Letters of credit are priced at the margin in effect for LIBOR loans, plus a fronting fee of 0.125%.

Obligations under the Revolving Credit Facility are secured by substantially all of our domestic personal property and our headquarters located in Tacoma, Washington.

We have agreements with certain financial institutions that allow us to restrict cash and cash equivalents and investments for the purpose of providing collateral instruments to our insurance carriers to satisfy workers' compensation claims. At December 28, 2012, we had restricted cash and investments totaling approximately $136.3 million.

In 2011, we entered into an agreement with AIG, formerly known as Chartis, and the Bank of New York Mellon creating a trust ("Trust") which holds the majority of our collateral obligations under existing workers' compensation insurance policies previously held directly by AIG. We established investment policy directives for the Trust, with the first priority to be preservation of capital, second to maintain and ensure a high degree of liquidity, and third to maximize after-tax returns.

Trust investments must meet minimum acceptable quality standards. The primary investments include U.S. Treasury Securities, U.S. Agency Debentures, U.S. Agency Mortgages, Corporate Securities, and Municipal Securities. For those investments rated by the Nationally Recognized Statistical Rating Organizations the minimum ratings are:

S&P | Moody's | Fitch | ||||

Short-term Rating | A-1/SP-1 | P-1/MIG-1 | F-1 | |||

Long-term Rating | A | A2 | A | |||

Workers’ compensation insurance, collateral and claims reserves

Workers' compensation insurance

We provide workers’ compensation insurance for our temporary and permanent employees. For policy years beginning in July 2003 and thereafter, AIG, formerly known as Chartis, has been our workers' compensation carrier. The policy year is effective July 1 to June 30 and is subject to annual renewal. We completed our renewal with AIG for the 2012 - 2013 policy year in June. For certain states we pay workers’ compensation insurance premiums and obtain full coverage under government-administered programs. The majority of our current workers’ compensation insurance policies cover claims for an event above a $2.0 million deductible limit, on a “per occurrence” basis. This results in our being substantially self-insured. While we have primary responsibility for all claims, our insurance coverage provides reimbursement for certain losses and expenses beyond our deductible limits ("Excess Claims”).