UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended

OR

THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number

|

(Exact name of registrant as specified in its charter) |

||

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (

Securities registered subject to Section 12(b) of the Exchange Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer ☐ |

|

|

Non-accelerated filer ☐ |

Smaller reporting company |

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

As of April 1, 2023 (the last business day of the registrant’s most recently completed second quarter), the aggregate market value of the common stock held by non-affiliates of the registrant was $

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the registrant’s proxy statement to be delivered to shareholders in connection with the 2024 Annual Meeting of Shareholders are incorporated by reference as set forth in Part III hereof.

TABLE OF CONTENTS

|

Cautionary Note Regarding Forward-Looking Statements |

4 |

||

|

PART I |

|||

|

Item 1. |

Business |

5 |

|

|

Item 1A. |

Risk Factors |

8 |

|

|

Item 1B. |

Unresolved Staff Comments |

12 |

|

|

Item 2. |

Properties |

12 |

|

|

Item 3. |

Legal Proceedings |

12 |

|

|

Item 4. |

Mine Safety Disclosures |

12 |

|

|

Information About Our Executive Officers |

12 |

||

|

PART II |

|||

|

Item 5. |

Market for the Registrant's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities |

13 |

|

|

Item 6. |

Reserved |

14 |

|

|

Item 7. |

Management's Discussion and Analysis of Financial Condition and Results of Operations |

14 |

|

|

Item 7A. |

Quantitative and Qualitative Disclosures About Market Risk |

19 |

|

|

Item 8. |

Financial Statements and Supplementary Data |

20 |

|

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

44 |

|

|

Item 9A. |

Controls and Procedures |

44 |

|

|

Item 9B. |

Other Information |

46 |

|

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

46 |

|

|

PART III |

|||

|

Item 10. |

Directors, Executive Officers and Corporate Governance |

46 |

|

|

Item 11. |

Executive Compensation |

46 |

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

46 |

|

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

46 |

|

|

Item 14. |

Principal Accounting Fees and Services |

46 |

|

|

PART IV |

|||

|

Item 15. |

Exhibits, Financial Statement Schedules |

47 |

|

|

Item 16. |

Form 10-K Summary |

47 |

|

|

SIGNATURES |

50 |

||

Cautionary Note Regarding Forward-Looking Statements

This report contains forward-looking statements within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, particularly in the “Business,” “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of this report. When used in this report, the words “believes,” “anticipates,” “expects,” “estimates,” “appears,” “plans,” “intends,” “may,” “should,” “could,” “outlook,” “continues,” “remains” and similar expressions are intended to identify forward-looking statements. Although we believe that our plans, intentions and expectations reflected in or suggested by such forward-looking statements are reasonable, they are subject to a number of risks and uncertainties and involve certain assumptions. Actual results may differ materially from those expressed in forward-looking statements, and we can provide no assurances that such plans, intentions or expectations will be implemented or achieved. Many of these risks and uncertainties are discussed in the “Risk Factors” section of this report and are updated from time to time in our filings with the United States (“U.S.”) Securities and Exchange Commission (“SEC”).

All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these cautionary statements. All forward-looking statements speak only to the respective dates on which such statements are made, and we do not undertake any obligation to publicly release the results of any revisions to these forward-looking statements that may be made to reflect any future events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events, except as may be required by law.

It is not possible to anticipate and list all risks and uncertainties that may affect our business, future operations or financial performance; however, they include, but are not limited to, the following:

|

● |

general economic and competitive conditions in the markets in which we operate; |

|

● |

changes in the spending levels for nonresidential and residential construction and the impact on demand for our products; |

|

● |

changes in the amount and duration of transportation funding provided by federal, state and local governments and the impact on spending for infrastructure construction and demand for our products; |

|

● |

the cyclical nature of the steel and building material industries; |

|

● |

credit market conditions and the relative availability of financing for us, our customers and the construction industry as a whole; |

|

● |

the impact of rising interest rates on the cost of financing for our customers; |

|

● |

fluctuations in the cost and availability of our primary raw material, hot-rolled carbon steel wire rod, from domestic and foreign suppliers; |

|

● |

competitive pricing pressures and our ability to raise selling prices in order to recover increases in raw material or operating costs; |

|

● |

changes in U.S. or foreign trade policy affecting imports or exports of steel wire rod or our products; |

|

● |

unanticipated changes in customer demand, order patterns and inventory levels; |

|

● |

the impact of fluctuations in demand and capacity utilization levels on our unit manufacturing costs; |

|

● |

our ability to further develop the market for engineered structural mesh (“ESM”) and expand our shipments of ESM; |

|

● |

legal, environmental, economic or regulatory developments that significantly impact our business or operating costs; |

|

● |

unanticipated plant outages, equipment failures or labor difficulties; and |

|

● |

the risks and uncertainties discussed herein under “Item 1A. Risk Factors” in this Form 10-K. |

PART I

Item 1. Business

General

Insteel Industries Inc. (“we,” “us,” “our,” “the Company” or “Insteel”) is the nation’s largest manufacturer of steel wire reinforcing products for concrete construction applications. We manufacture and market prestressed concrete strand (“PC strand”) and welded wire reinforcement (“WWR”), including ESM, concrete pipe reinforcement (“CPR”) and standard welded wire reinforcement (“SWWR”). Our products are sold mainly to manufacturers of concrete products that are used primarily in nonresidential construction. For fiscal 2023, we estimate that approximately 85% of our sales were related to nonresidential construction and 15% were related to residential construction.

Insteel is the parent holding company for two wholly-owned subsidiaries, Insteel Wire Products Company (“IWP”), an operating subsidiary, and Intercontinental Metals Corporation, an inactive subsidiary. We were incorporated in 1958 in the State of North Carolina.

Our business strategy is focused on: (1) achieving leadership positions in our markets; (2) operating as the lowest cost producer in our industry; and (3) pursuing growth opportunities within our core businesses that further our penetration of the markets we currently serve or expand our footprint. Headquartered in Mount Airy, North Carolina, we operate ten manufacturing facilities that are all located in the U.S. in close proximity to our customers and raw material suppliers. Our growth strategy is focused on organic opportunities as well as strategic acquisitions in existing or related markets that leverage our infrastructure and core competencies in the manufacture and marketing of concrete reinforcing products.

Products

Our operations are entirely focused on the manufacture and marketing of steel wire reinforcing products for concrete construction applications. Our concrete reinforcing products consist of two product lines: PC strand and WWR. Based on the criteria specified in Financial Accounting Standards Board Accounting Standards Codification Topic 280, Segment Reporting, we have one reportable segment.

PC strand is a high strength, seven-wire strand that is used to impart compression forces into precast concrete elements and structures, which may be either pretensioned or posttensioned, providing reinforcement for bridges, parking decks, buildings and other concrete structures. Its high tensile strength allows for the casting of longer spans and thinner sections. Pretensioned or “prestressed” concrete elements or structures are primarily used in nonresidential construction while posttensioned concrete elements or structures are used in both nonresidential and residential construction.

WWR is produced as either a standard or a specially engineered reinforcing product for use in nonresidential and residential construction. We produce a full range of WWR products, including ESM, CPR and SWWR. ESM is an engineered made-to-order product that is used as the primary reinforcement for concrete elements or structures, frequently serving as a lower cost reinforcing solution than hot-rolled rebar. CPR is an engineered made-to-order product that is used as the primary reinforcement in concrete pipe, box culverts and precast manholes for drainage and sewage systems, water treatment facilities and other related applications. SWWR is a secondary reinforcing product that is produced in standard styles for crack control applications in residential and light nonresidential construction, including driveways, sidewalks and various slab-on-grade applications.

See Note 15 for the disaggregation of our net sales by product line and geography.

Marketing and Distribution

We market our products through sales representatives who are our employees. Our outside sales representatives are trained on the technical applications for our products and sell multiple product lines in their respective territories. We sell our products nationwide across the U.S. and, to a much lesser extent, into Canada, Mexico and Central and South America. Our products are shipped primarily by truck, using common or contract carriers. The delivery method selected is determined based on backhaul opportunities, comparative costs and customer service requirements.

Customers

We sell our products to a broad range of customers that includes manufacturers of concrete products, and to a lesser extent, distributors, rebar fabricators and contractors. In fiscal 2023, we estimate that approximately 70% of our net sales were to manufacturers of concrete products and 30% were to distributors, rebar fabricators and contractors. In many cases, we are unable to identify the specific end use for our products as most of our customers sell products that are used for both nonresidential and residential construction, and the same products can be used for different end uses. We did not have any single customers that represented 10% or more of our net sales in fiscal years 2023, 2022 or 2021. The loss of a single customer or a few customers would not have a material adverse impact on our business.

Backlog

Backlog for our business is minimal due to the relatively short lead times that are required by our customers. We believe that the majority of our firm orders as of the end of fiscal 2023 will be shipped during the first quarter of fiscal 2024.

Seasonality and Cyclicality

Demand in our markets is both seasonal and cyclical, driven by the level of construction activity, but can also be impacted by fluctuations in the inventory positions of our customers. Shipments are seasonal, typically reaching their highest level when weather conditions are the most conducive to construction activity. As a result, assuming normal seasonal weather patterns, shipments and profitability are usually higher in the third and fourth quarters of the fiscal year and lower in the first and second quarters. Construction activity and demand for our products is cyclical based on overall economic conditions, although there can be significant differences between the relative strength of nonresidential and residential construction for extended periods.

Raw Materials

The primary raw material used to manufacture our products is hot-rolled carbon steel wire rod, which we purchase from both domestic and foreign suppliers and can generally be characterized as a commodity product. We purchase several different grades and sizes of wire rod with varying specifications based on the diameter, chemistry, mechanical properties and metallurgical characteristics that are required for our products. High-carbon grades of wire rod are required for the production of PC strand while low-carbon grades are used to manufacture WWR.

Wire rod prices tend to fluctuate based on changes in scrap and other metallic prices for steel producers together with domestic and global market conditions. In most economic environments, domestic demand for wire rod exceeds domestic production capacity, and imports of wire rod are necessary to satisfy the supply requirements of the U.S. market. U.S. government trade policies and trade actions by domestic wire rod producers can significantly impact the pricing and availability of imported wire rod, which during fiscal years 2023 and 2022 represented approximately 14% and 26%, respectively, of our total wire rod purchases. We believe that our substantial wire rod requirements, desirable mix of sizes and grades and strong financial condition represent a competitive advantage by making us a relatively more attractive customer to our suppliers.

Our ability to source wire rod from overseas suppliers is limited by domestic content requirements generally referred to as “Buy America” or “Buy American” laws that exist at both the federal and state levels. These laws generally prescribe a domestic “melt and cast” standard for purposes of compliance. Customers purchasing PC strand and WWR for certain applications require the Company to certify compliance with Buy America laws.

Selling prices for our products tend to be correlated with changes in wire rod prices. However, the timing and magnitude of the relative price changes varies depending upon market conditions and competitive factors. Ultimately, the relative supply - demand balance in our markets and competitive dynamics determine whether our margins expand or contract during periods of rising or falling wire rod prices.

Competition

We are the nation’s largest manufacturer of steel wire reinforcing products for concrete construction applications. Our markets are highly competitive based on price, quality and service. Some of our competitors, such as Nucor Corporation, Liberty Steel USA (“Liberty”) and Oklahoma Steel and Wire, are vertically integrated companies that produce both wire rod and concrete reinforcing products and offer multiple product lines over broad geographic areas. Other competitors are smaller independent companies that offer limited competition in certain markets. Our primary competitors for WWR products are Engineered Wire Products, Inc. (a subsidiary of Liberty), Wire Mesh Corporation, Concrete Reinforcements, Inc., National Wire Products, Davis Wire Corporation and Oklahoma Steel & Wire Co., Inc. Our primary competitors for PC strand are Sumiden Wire Products Corporation and Wire Mesh Corporation. Import competition is also a significant factor in certain segments of the PC strand and SWWR markets that are not subject to “Buy America” requirements.

In response to illegally traded import competition from offshore PC strand suppliers, we have pursued trade cases, when necessary, as a means of ensuring that foreign producers were complying with the applicable trade laws and regulations. In 2003, we joined together with a coalition of domestic PC strand producers and filed petitions with the U.S. Department of Commerce (the “DOC”) alleging that imports of PC strand from Brazil, India, Korea, Mexico and Thailand were being “dumped” or sold in the U.S. at a price that was lower than fair value and had injured the domestic PC strand industry. The DOC ruled in our favor and imposed anti-dumping duties ranging from 12% up to 119%, which had the effect of limiting the participation of these countries in the domestic market. In 2010, we joined together with a coalition of domestic PC strand producers and filed petitions with the DOC alleging that imports of PC strand from China were being “dumped” or sold in the U.S. at a price that was lower than fair value and that subsidies were being provided to Chinese PC strand producers by the Chinese government, both of which had injured the domestic PC strand industry. The DOC ruled in our favor and imposed final countervailing duty margins ranging from 9% to 46% and anti-dumping margins ranging from 43% to 194%, which had the effect of limiting the continued participation of Chinese producers in the domestic market. In 2020, we joined two other domestic PC strand producers and filed anti-dumping petitions against Argentina, Columbia, Egypt, Indonesia, Italy, Malaysia, Netherlands, Saudi Arabia, South Africa, Spain, Taiwan, Tunisia, Turkey, Ukraine and the United Arab Emirates. In January 2021, with respect to 8 countries, and in April 2021, with respect to 7 countries, the DOC ruled in our favor and imposed anti-dumping duties ranging from 4% to 194%, which had the effect of limiting the participation of these countries in the domestic market. Additionally, in 2020, we and four other domestic producers of SWWR filed anti-dumping petitions against Mexico. In July 2021, the DOC ruled in our favor and imposed final countervailing duty margins ranging from 23% to 110%, which had the effect of limiting the continued participation of Mexican producers in the domestic market.

Quality and service expectations of customers have risen substantially over the years and are key factors that impact their selection of suppliers. Technology has become a critical competitive factor from the standpoint of manufacturing costs, quality and customer service capabilities. In view of our strong market positions, broad product offering and national footprint, technologically advanced manufacturing facilities, low-cost production capabilities, sophisticated information systems and financial strength and flexibility, we believe that we are well-positioned to compete favorably with other producers of our concrete reinforcing products.

Human Capital

We value all our employees and their important role in the long-term success of the company. Our human capital strategy is centered around four key areas: Safe Operations, Performance Based Compensation, Equal Opportunity and Hiring and Retention. As of September 30, 2023, we had 884 employees, none of which were represented by labor unions. In the event of production disruptions, we believe that our contingency plans would enable us to continue serving our customers, although there can be no assurances that a work slowdown or stoppage would not adversely impact our operating costs and financial results.

Safe Operations

Our employees are extensively trained in a formal process of risk assessment, risk reduction and hazard elimination and empowered with the authority to stop equipment or tasks until work can be safely accomplished. “Safe Operations with Zero Harm,” our internal safety philosophy, is a key part of our ongoing employee training and operations. Zero Harm is identifying and managing risk to avoid injuries, illness or other negative impacts experienced by employees, the community, customers, property, the environment and shareholders. We monitor our safety performance through a key range of leading and lagging measures of safety.

|

Leading Indicator Measures: |

Lagging Indicator Measures: |

|

● Hazard management process training ● Leadership engagement ● Employee involvement

|

● Rolling 12-month Incident Recordable Rate ● Lost Time Rate ● Severity Rate – Days Away, Restricted, and Transferred (DART) |

Performance Based Compensation

Our production and skilled trades team members earn pay increases through our “Pay for Skills” program and share in productivity pay through our “Team Share” incentive program. Our salaried team members also have a compensation structure that rewards individual performance in addition to company performance. The Team Share incentive program is driven by variables that are controllable at the plant level. We believe a compensation structure, which rewards both individual initiative and team accomplishments, leads to higher levels of performance.

Equal Opportunity

Our business depends on talented individuals who bring diverse skills, experiences and backgrounds. We believe in a collaborative workplace that is based on the fundamentals of dignity, respect, equality and opportunity for all and encourage transparency and access to leadership through our Open-Door Policy, Code of Business Conduct (including Whistleblower Hotline), Equal Opportunity Policy, Harassment Policy and Mission and Values. Our performance and succession development process includes all employees. We have many team members in key leadership roles who started in entry-level roles and have grown in their careers by partnering with us in their development plans.

Hiring and Retention

Our performance relies on people who are developed and empowered to achieve results. We are improving the future of our company by identifying, developing and retaining talent that reflects our corporate philosophy. Our goal is to create a positive and engaging work environment that meets evolving employee needs in areas like flexible work schedules beyond the traditional full-time work schedule (such as part-time, weekend only, shared shift and other flexible approaches that attract a broader candidate pool). In addition, we are involved in many outreach programs in our communities to provide opportunities to diverse talent sources that may otherwise be overlooked or face barriers to equal opportunity.

Product Warranties

Our products are used in applications that are subject to inherent risks, including performance deficiencies, personal injury, property damage, environmental contamination or loss of production. We warrant our products to meet certain specifications. Although actual or claimed deficiencies from these specifications may give rise to claims, we do not maintain a reserve for warranties as the historical claims have been immaterial. We maintain product liability insurance coverage to minimize our exposure to such risks.

Governmental Regulation and Environmental Matters

We are subject to federal, state and local laws and regulations in the United States that could affect our business, including regulations relating to generating emissions, water discharges, waste and workplace safety. We believe that we are in compliance in all material respects with applicable environmental laws and regulations. We have experienced no material difficulties in complying with legislative or regulatory standards and believe that these standards have not materially impacted our financial position or results of operations. However, laws and regulations may be changed, accelerated or adopted that impose significant operational restrictions and compliance requirements on us and which could negatively impact our operating results. See “Item 1A. Risk Factors”. We do not expect to incur material capital expenditures for environmental control facilities during fiscal 2024.

Available Information

Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to these reports are available at no cost on our website at https://investor.insteel.com and the SEC’s website at www.sec.gov as soon as reasonably practicable after we file these reports with the SEC. The information available on our website and the SEC’s website is not incorporated into this report or any of our filings with the SEC.

Item 1A. Risk Factors

An investment in our common stock involves risks and uncertainties. You should carefully consider the following risk factors, in addition to the other information contained in this annual report on Form 10-K, before deciding whether an investment in our common stock is suitable for you. The risk factors described below are not the only ones we face. There may be other risks and uncertainties that are currently unknown to us or that we currently consider to be immaterial that could adversely affect our business, results of operations, financial condition and cash flows.

Industry Specific Risks

Our business is cyclical and can be negatively impacted by prolonged economic downturns, rising interest rates or tightening in the financial markets that reduce the level of construction activity and demand for our products.

Demand for our products is cyclical in nature and sensitive to changes in the economy and in the financial markets. Our products are sold primarily to manufacturers of concrete products that are used for a broad range of nonresidential and residential construction applications. Demand for our products is driven by the level of construction activity, which tends to be correlated with conditions in the overall economy as well as other factors beyond our control. Rising interest rates or tightening in the financial markets could adversely impact demand for our products by increasing the cost of financing or reducing the availability of financing to our customers and the construction industry as a whole. Future prolonged periods of economic weakness, high interest rates or reduced availability of financing could have a material adverse impact on our business, results of operations, financial condition and cash flows.

Our business can be negatively impacted by reductions in the amount and duration of government funding for infrastructure projects that reduce the level of construction activity and demand for our products.

Certain of our products are used in the construction of highways, bridges and other infrastructure projects that are funded by federal, state and local governments. Reductions in the amount of funding for such projects or the period for which it is provided, including as a result of budget uncertainty, the potential for U.S. Government shutdowns, the use of continuing resolutions and the federal debt ceiling, could have a material adverse impact on our business, results of operations, financial condition and cash flows.

Foreign competition could adversely impact our financial results.

Certain of our PC strand and SWWR markets are subject to foreign import competition on an ongoing basis. If we are unable to purchase raw materials and achieve manufacturing costs that are competitive with those of foreign producers, or if the margin and return requirements of foreign producers are substantially lower, our market share and profit margins could be negatively impacted. In response to illegally traded import competition from offshore PC strand and SWWR suppliers, we have pursued trade cases, when necessary, as a means of ensuring that foreign producers were complying with the applicable trade laws and regulations. Such actions may be costly and may not be successful. Trade law enforcement is critical to our ability to maintain our competitive position against foreign PC strand and SWWR producers that engage in unlawful trade practices.

Our financial results can be negatively impacted by the volatility in the cost and availability of our primary raw material, hot-rolled carbon steel wire rod.

The primary raw material used to manufacture our products is hot-rolled carbon steel wire rod, which we purchase from both domestic and foreign suppliers. We do not use derivative commodity instruments to hedge our exposure to changes in the price of wire rod as such instruments are currently unavailable in the financial markets. Prices for wire rod have become increasingly volatile in recent years driven by the higher degree of variability in raw material costs for rod producers, changes in trade policy and the fluctuation of domestic supply. In response, wire rod producers have resorted to increasing the frequency of price adjustments, typically on a monthly basis, as well as unilaterally changing the terms of prior commitments.

Although changes in our wire rod costs and selling prices tend to be correlated, we may be unable to fully recover increased rod costs during weaker market environments, which would reduce our earnings and cash flows. Additionally, when raw material costs decline, our financial results would be negatively impacted if the selling prices for our products decrease to an even greater extent and if we are consuming higher cost material from inventory.

Our financial results can also be significantly impacted if raw material supplies are inadequate to satisfy our purchasing requirements. For example, U.S. government trade policies and trade actions by domestic wire rod producers against other countries can significantly impact the availability and cost of imported wire rod. The imposition of tariffs, quotas or anti-dumping or countervailing duty margins by the U.S. government against exporting countries can have the effect of reducing or eliminating their competitiveness and participation in the domestic market. If we were unable to obtain adequate and timely delivery of our raw material requirements, we may be unable to manufacture sufficient quantities of our products or operate our manufacturing facilities in an efficient manner, which could result in lost sales and higher operating costs. Because tight market conditions typically affect the entire industry, during past periods of short raw material supply, margins and profitability have been favorably impacted due to curtailed availability of PC strand and WWR that supported higher average selling prices. There is no assurance that future short supply conditions in raw material markets would result in similar outcomes, however.

Demand for our products is highly variable and difficult to forecast due to our minimal backlog and unanticipated changes that can occur in customer order patterns or inventory levels.

Demand for our products is highly variable. The short lead times for customer orders and minimal backlog that characterize our business make it difficult to forecast the future level of demand for our products. In some cases, unanticipated softening in demand can be exacerbated by inventory rebalancing measures pursued by our customers, which may cause significant fluctuations in our sales, profitability and cash flows.

Operational Risks

Our manufacturing facilities are subject to unexpected equipment failures, operational interruptions and casualty losses.

Our manufacturing facilities are subject to risks that may limit our ability to manufacture and sell our products, including unexpected equipment failures, operational interruptions and catastrophic losses due to other unanticipated events such as fires, explosions, accidents, adverse weather conditions and transportation interruptions. Any such equipment failures or events can subject us to plant shutdowns and periods of reduced production or unexpected downtime. Furthermore, the resolution of certain operational interruptions may require significant capital expenditures. Although our insurance coverage could offset the losses or expenditures relating to some of these events, our results of operations and cash flows would be negatively impacted to the extent that such claims were not covered or only partially covered by our insurance.

Our financial results could be adversely impacted by the escalation of our operating costs.

Consistent with the experience of other employers, our labor, medical and workers’ compensation costs have increased substantially in recent years and are expected to continue to rise. If this trend continues, the cost of labor and to provide healthcare and other benefits to our employees could increase, adversely impacting profitability. As the labor market continues to recover from the effects of the COVID-19 pandemic, availability of qualified employees and competition for them has escalated, which has increased costs associated with attracting and retaining employees. We cannot be certain that we will be able to maintain an adequately skilled labor force necessary to operate efficiently or that our labor costs will not increase as a result of a shortage in the availability of skilled employees. Additionally, employee turnover could result in lost time due to inefficiencies and the need for additional training, which could impact our operating results. Changes to healthcare regulations may also increase the cost of providing such benefits to our employees. We cannot predict the ultimate content, timing, or effect of any healthcare reform legislation or the impact of potential legislation or related proposals and policies on our results. Any significant increases in the costs attributable to our self-insured health and workers’ compensation plans could adversely impact our business, results of operations, financial condition and cash flows.

In addition, increasing transaction prices for freight, natural gas, electricity, fuel and consumables would adversely affect our manufacturing and distribution costs. For most of our business, we incur the transportation costs associated with the delivery of products to our customers. Although we have previously implemented numerous measures to offset the impact of increases in these costs, there can be no assurance that such actions will be effective. If we are unable to pass these additional costs through by raising our selling prices, our financial results could be adversely impacted.

Our business, financial condition and results of operations may be adversely impacted by the effects of inflation.

The recent rise in inflation has increased the costs of labor, energy, operating supplies and raw materials. If we are unable to pass these increases in costs to our customers it could adversely affect our business, financial condition and results of operations by increasing our overall cost structure.

Our business and operations are subject to risks related to climate change.

The long-term effects of global climate change could present both physical risks and transition risks (such as regulatory or technology changes), which are expected to be widespread and unpredictable. These changes could over time affect, for example, the availability and cost of raw materials, commodities and energy (including utilities), which in turn may impact our ability to procure goods or services required for the operation of our business at the quantities and levels we require. Additionally, we have facilities located in areas that may be impacted by the physical risks of climate change, and we face the risk of losses incurred as a result of physical damage to our facilities and inventory as well as business interruption caused by such events. Furthermore, periods of extended inclement weather or associated flooding may inhibit construction activity utilizing our products and delay shipments of our products to customers. We believe that adaptation strategies to accommodate rising sea levels and other climate related phenomena could stimulate demand for our products to the extent that reinforced concrete products are essential to managing surface waters.

We also use natural gas, diesel fuel, gasoline and electricity in our operations, all of which could face increased regulation as a result of climate change or other environmental concerns. Additionally, we may face increased costs to respond to future water laws and regulations, and operations in areas with limited water availability may be impacted if droughts become more frequent or severe. Any such events could have a material adverse effect on our costs or results of operations.

Financing Risks

Our operations are subject to seasonal fluctuations that may impact our cash flows.

Our shipments are typically lower in the first and second fiscal quarters due to the unfavorable impact of winter weather on construction activity during these periods and customer plant shutdowns associated with holidays. As a result, our cash flows may fluctuate from quarter to quarter due to these seasonal factors.

Our capital resources may not be adequate to provide for our capital investment and maintenance expenditures if we were to experience a substantial downturn in our financial performance.

Our operations are capital intensive and require substantial recurring expenditures for the routine maintenance of our equipment and facilities. Although we expect to finance our business requirements through internally generated funds or from borrowings under our $100 million revolving credit facility, we cannot provide any assurances these resources will be sufficient to support our business. A material adverse change in our operations or financial condition could limit our ability to borrow funds under our credit facility, which could further adversely impact our liquidity and financial condition. Any significant future acquisitions could require additional financing from external sources that may not be available on favorable terms, which could adversely impact our growth, operations, financial condition and results of operations.

Legal and Regulatory Risks

Changes in environmental compliance and remediation requirements could result in substantial increases in our capital investments and operating costs.

Our business is subject to numerous federal, state and local laws and regulations pertaining to the protection of the environment that could require substantial increases in capital investments and operating costs. These laws and regulations, which are constantly evolving, are becoming increasingly stringent, and the ultimate impact of compliance is not always clearly known or determinable because regulations under some of these laws have not yet been promulgated or are undergoing revision. Legislation and increased regulation regarding climate change, including mandatory reductions in energy consumption or emissions of greenhouse gases, could impose significant costs on us, including costs related to energy requirements, capital equipment, environmental monitoring and reporting and other costs to comply with such regulations.

General Risks

Our business, results of operations, financial condition, cash flows and stock price can be adversely affected by pandemics, epidemics or other public health emergencies, such as the COVID-19 pandemic.

The COVID-19 pandemic negatively impacted the global economy, disrupted supply chains and created significant volatility and disruption of financial markets. In the event of the renewed outbreak of COVID-19, the emergence of new variants or an outbreak of a different virus or disease, we could experience disruptions in our supply chain, operations, facilities and workforce which could negatively affect our results of operations, financial condition, cash flows and stock price.

Our stock price can be volatile, often in connection with matters beyond our control.

Equity markets in the U.S. have been increasingly volatile in recent years. During fiscal 2023, our common stock traded as high as $35.80 and as low as $24.00. There are numerous factors that could cause the price of our common stock to fluctuate significantly, including: variations in our financial results; changes in our business outlook and expectations for the construction industry; changes in market valuations of companies in our industry; and announcements by us, our competitors or industry participants that may be perceived to impact our financial results.

We are increasingly dependent on information technology systems that are susceptible to certain risks, including cybersecurity breaches and data leaks, which could adversely impact our business.

Our increasing reliance on technology systems and infrastructure heightens our potential vulnerability to system failure and malfunction, breakdowns due to natural disasters, human error, unauthorized access, power loss and other unforeseen events. Data privacy breaches by employees and others with or without authorized access to our systems poses risks that sensitive data may be permanently lost or leaked to the public or other unauthorized persons. With the growing use and rapid evolution of technology, not limited to cloud-based computing and mobile devices, there are additional risks of unintentional data leaks. There is also the risk of theft of confidential information, intentional vandalism, industrial espionage and a variety of cyber-attacks that could compromise our internal technology system and infrastructure or result in data leaks in-house or at our third-party providers and business partners. While we have taken reasonable steps to protect the Company from cybersecurity risks and security breaches, there can be no assurance that such events will not occur. Failures of technology or related systems, cybersecurity incidents, or improper release of confidential information, could adversely impact our business or subject us to unexpected liabilities, expenditures and recovery time.

Our financial results could be adversely impacted by the impairment of goodwill.

Our balance sheet includes intangible assets, including goodwill and other separately identifiable assets related to prior acquisitions, and we may acquire additional intangible assets in connection with future acquisitions. We are required to review goodwill for impairment on an annual basis or more frequently if certain indicators of permanent impairment arise such as, among other things, a decline in our stock price and market capitalization or a reduction in our projected operating results and cash flows. If our review indicates that goodwill has been impaired, the impaired portion would have to be written-off during that period which could adversely impact our business and financial results.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

Our corporate headquarters and IWP’s sales and administrative offices are located in Mount Airy, North Carolina. As of September 30, 2023, we operated ten manufacturing facilities located in Dayton, Texas; Gallatin, Tennessee; Hazleton, Pennsylvania; Hickman, Kentucky; Houston, Texas; Jacksonville, Florida; Kingman, Arizona; Mount Airy, North Carolina; Sanderson, Florida; and St. Joseph, Missouri.

We own all of our real estate. We believe that our properties are in good operating condition and that our machinery and equipment have been well maintained. We also believe that our manufacturing facilities are suitable for their intended purposes and have capacities adequate to satisfy the current and projected demand for our products.

Item 3. Legal Proceedings.

We are involved in lawsuits, claims, investigations and proceedings, including commercial, environmental and employment matters, which arise in the ordinary course of business. We do not anticipate that the ultimate cost to resolve these matters will have a material adverse effect on our financial position, results of operations or cash flows.

Item 4. Mine Safety Disclosures.

Not applicable.

Information About Our Executive Officers

Our executive officers are as follows:

|

Name |

Age |

Position |

|||

|

H. O. Woltz III |

67 |

President, Chief Executive Officer and Chairman of the Board |

|||

|

Scot R. Jafroodi |

54 |

Vice President, Chief Financial Officer and Treasurer |

|||

|

Elizabeth C. Southern |

42 |

Vice President Administration, Secretary and Chief Legal Officer |

|||

|

Richard T. Wagner |

64 |

Senior Vice President and Chief Operating Officer |

|||

|

James R. York |

65 |

Senior Vice President, Sourcing and Logistics |

|||

H. O. Woltz III, 67, has served as Chief Executive Officer since 1991, as President since 1989 and has been employed by us and our subsidiaries in various capacities since 1978. He was named President and Chief Operating Officer in 1989. He served as our Vice President from 1988 to 1989 and as President of Rappahannock Wire Company, formerly a subsidiary of our Company, from 1981 to 1989. Mr. Woltz has been a Director since 1986 and also serves as President of Insteel Wire Products Company. Mr. Woltz served as President of Florida Wire and Cable, Inc., formerly a subsidiary of our Company, until its merger with Insteel Wire Products Company in 2002. Mr. Woltz has served as Chairman of the Board since 2009.

Scot R. Jafroodi, 54, has served as Vice President, Chief Financial Officer and Treasurer since January 2023. Prior to 2023, he served as Vice President, Corporate Controller and Chief Accounting Officer from October 2020. He previously held the role of Corporate Controller and Chief Accounting Officer from February 2007 to October 2020 and Corporate Controller from July 2005 to February 2007. Before joining us, he was a Senior Manager at BDO Seidman, LLP from June 2003 through June 2005 and, prior to that, had been employed for ten years at Deloitte & Touche USA, LLP, most recently as a Senior Manager.

Elizabeth C. Southern, 42, has served as Vice President, Administration, Secretary and Chief Legal Officer since June 2023. From 2011 to 2023, she served in various senior management roles with Hanesbrands Inc., a publicly-held apparel company, including Deputy General Counsel and Assistant Secretary and Vice President, Human Resources. Prior to that, Ms. Southern was an associate attorney at Womble Bond Dickinson (US) LLP.

Richard T. Wagner, 64, has served as Senior Vice President, Chief Operating Officer since October 2020 and as Vice President and General Manager of the Concrete Reinforcing Products Business Unit of our subsidiary, Insteel Wire Products Company, since 1998. He joined us in 1992 serving in various other management roles. From 1977 until 1992, Mr. Wagner served in various positions with Florida Wire and Cable, Inc., a manufacturer of PC strand and galvanized strand products, which was later acquired by us in 2000.

James R. York, 65, has served as Senior Vice President, Sourcing and Logistics since October 2020, and as Vice President, Sourcing and Logistics since joining us in 2018. Prior to Insteel, he served in various senior management roles with Leggett & Platt, a publicly-held manufacturer of diversified engineered products, from 2002 to 2018, including Group President-Rod and Wire Products, Unit President-Wire Products and Unit President-Specialty Products. Mr. York served in a range of leadership positions at Bekeart Corporation, a U.S. subsidiary of N.V. Bekeart A.S. of Belgium, from 1983 to 2002.

PART II

Item 5. Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities.

Our common stock is listed on the New York Stock Exchange (“NYSE”) under the symbol “IIIN” and has traded on the NYSE since March 17, 2021. As of October 24, 2023, there were 449 shareholders of record.

We pay regular quarterly cash dividends and expect to continue to pay regular quarterly cash dividends in the foreseeable future, though each quarterly dividend payment is subject to review and approval by our Board of Directors. On November 15, 2022, our Board of Directors approved a one-time special cash dividend of $2.00 per share that was paid on December 23, 2022.

Issuer Purchases of Equity Securities

There were not any repurchases of common stock during the quarter ended September 30, 2023. Additional information regarding our share repurchase authorization is discussed in Note 18 to our consolidated financial statements and incorporated herein by reference.

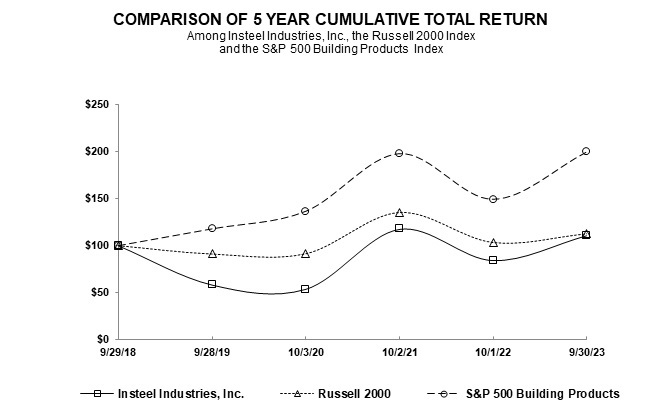

Stock Performance Graph

The graph below compares the cumulative total shareholder return on our common stock with the cumulative total return of the Russell 2000 Index and the S&P 500 Building Products Index for the five years ended September 30, 2023. The graph and table assume that $100 was invested on September 29, 2018 in our common stock and in each of the two indices and the reinvestment of all dividends. Cumulative total shareholder returns for our common stock, the Russell 2000 Index and the S&P 500 Building Products Index are based on our fiscal year.

|

Fiscal Year Ended |

||||||||||||||||||||||||

|

September 29, 2018 |

September 28, 2019 |

October 3, 2020 |

October 2, 2021 |

October 1, 2022 |

September 30, 2023 |

|||||||||||||||||||

|

Insteel Industries, Inc. |

$ | 100.00 | $ | 58.05 | $ | 53.49 | $ | 117.67 | $ | 84.30 | $ | 110.87 | ||||||||||||

|

Russell 2000 |

100.00 | 91.11 | 91.47 | 135.08 | 103.34 | 112.56 | ||||||||||||||||||

|

S&P 500 Building Products |

100.00 | 117.91 | 136.56 | 197.83 | 149.31 | 199.59 | ||||||||||||||||||

Item 6. Reserved.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The matters discussed in this section include forward-looking statements that are subject to numerous risks. You should carefully read the “Cautionary Note Regarding Forward-Looking Statements” and “Risk Factors” in this Form 10-K.

Overview

Our operations are entirely focused on the manufacture and marketing of concrete reinforcing products for the concrete construction industry. Our business strategy is focused on: (1) achieving leadership positions in our markets; (2) operating as the lowest cost producer in our industry; and (3) pursuing growth opportunities within our core businesses that further our penetration of the markets we currently serve or expand our footprint.

Critical Accounting Estimates

Our consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States. Our discussion and analysis of our financial condition and results of operations are based on these consolidated financial statements. The preparation of our consolidated financial statements requires the application of these accounting principles in addition to certain estimates and judgments based on currently available information, actuarial estimates, historical results and other assumptions believed to be reasonable. These estimates, assumptions and judgments are affected by our application of accounting policies, which are discussed in Note 2, "Summary of Significant Accounting Policies", and elsewhere in the accompanying consolidated financial statements. Estimates are used for, but not limited to, determining the net carrying value of trade accounts receivable, inventories, recording self-insurance liabilities and other accrued liabilities. Actual results could differ from these estimates.

Accounting estimates are considered critical if both of the following conditions are met: (1) the nature of the estimates or assumptions is material because of the levels of subjectivity and judgment needed to account for matters that are highly uncertain and susceptible to change and (2) the effect of the estimates and assumptions is material to the financial statements.

We have reviewed our accounting estimates, and none were deemed to be considered critical for the accounting periods presented.

Recent Accounting Pronouncements.

The nature and impact of recent accounting pronouncements is discussed in Note 3 to our consolidated financial statements and incorporated herein by reference.

Results of Operations

The following discussion and analysis of our financial condition and results of operations is for the year ended September 30, 2023 compared with the year ended October 1, 2022. Discussions of our financial condition and results of operations for the year ended October 1, 2022 compared to October 2, 2021 that have been omitted under this item can be found in Part II, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in our Annual Report on Form 10-K for the fiscal year ended October 1, 2022, which was filed with the SEC on October 27, 2022.

The table below presents a summary of our results of operations for fiscal 2023 and fiscal 2022.

Statements of Operations – Selected Data

(Dollars in thousands)

|

Year Ended |

||||||||||||

|

September 30, |

October 1, |

|||||||||||

|

2023 |

Change |

2022 |

||||||||||

|

Net sales |

$ | 649,188 | (21.5% | ) | $ | 826,832 | ||||||

|

Gross profit |

65,398 | (66.9% | ) | 197,310 | ||||||||

|

Percentage of net sales |

10.1 | % | 23.9 | % | ||||||||

|

Selling, general and administrative expense |

$ | 30,685 | (14.9% | ) | $ | 36,048 | ||||||

|

Percentage of net sales |

4.7 | % | 4.4 | % | ||||||||

|

Other (income) expense, net |

$ | (3,423 | ) |

N/M |

$ | 88 | ||||||

|

Interest income |

$ | (3,706 | ) |

N/M |

$ | (326 | ) | |||||

|

Effective income tax rate |

22.4 | % | 22.7 | % | ||||||||

|

Net earnings |

$ | 32,415 | (74.1% | ) | $ | 125,011 | ||||||

|

"N/M" = not meaningful |

||||||||||||

2023 Compared with 2022

Net Sales

Net sales decreased 21.5% to $649.2 million in 2023 from $826.8 million in 2022, reflecting a 17.1% decrease in selling prices along with a 5.3% decrease in shipments. The decrease in average selling prices was driven by competitive pricing pressures resulting from weakening demand for our products and declining raw material costs. The decrease in shipments was due to reduced demand resulting from inventory management measures pursued by our customers during the fiscal year and a decrease in new project activity.

Gross Profit

Gross profit decreased 66.9% to $65.4 million, or 10.1% of net sales, in 2023 from $197.3 million, or 23.9% of net sales, in 2022. The year-over-year decrease was primarily due to lower spreads between average selling prices and raw material costs ($105.7 million) along with a decrease in shipments ($11.8 million) and higher manufacturing costs ($14.4 million). The decrease in spreads was driven by lower average selling prices ($129.7 million) and an increase in freight expense ($1.4 million) partially offset by lower raw material costs ($25.4 million).

Selling, General and Administrative Expense

Selling, general and administrative expense (“SG&A expense”) decreased 14.9% to $30.7 million, or 4.7% of net sales, in 2023 from $36.0 million, or 4.4% of net sales, in 2022 primarily due to lower compensation ($2.9 million), the relative year-over-year changes in the cash surrender value of life insurance policies ($2.4 million) and depreciation expense ($577,000) partially offset by higher employee benefit expense ($489,000). The decrease in compensation expense was largely driven by lower incentive plan expense due to a decline in financial results in the current year. The cash surrender value of life insurance policies increased $531,000 in the current year compared with a decrease of $1.9 million in the prior year due to the corresponding changes in the value of the underlying investments. The increase in employee benefits expense was due to a net gain on the settlement of life insurance policies ($364,000) in the prior year along with higher employee health insurance costs in the current year period.

Other (Income) Expense, net

Other income of $3.4 million for 2023 was primarily related to a net gain from the sale of property, plant and equipment ($3.3 million).

Interest Income

Interest income increased to $3.7 million due to an increase in cash and higher average interest rates.

Income Taxes

Our effective income tax rate for 2023 decreased to 22.4% from 22.7% in 2022 due to changes in book versus tax differences.

Net Earnings

Net earnings decreased to $32.4 million ($1.66 per share) in 2023 from $125.0 million ($6.37 per diluted share) in 2022, primarily due to the decrease in gross profit partially offset by lower SG&A expense and increased other income and interest income.

Liquidity and Capital Resources

Overview

Our sources of liquidity include cash and cash equivalents, cash generated by operating activities and borrowing availability provided under our $100.0 million revolving credit facility (the “Credit Facility”). Our principal capital requirements include funding working capital, capital expenditures, dividends and any share repurchases. As of September 30, 2023, our cash and cash equivalents totaled $125.7 million compared with $48.3 million as of October 1, 2022.

We believe that, in the absence of significant unanticipated cash demands, cash and cash equivalents, cash generated by operating activities and the borrowing availability provided under the Credit Facility will be sufficient to satisfy our expected requirements for working capital, capital expenditures, dividends and share repurchases, if any, in both the short- and long-term. We also expect to have access to the amounts available under our Credit Facility as required. However, should we experience future reductions in our operating cash flows due to weakening conditions in our construction end-markets and reduced demand from our customers, we may need to curtail capital and operating expenditures, delay or restrict share repurchases, cease dividend payments and/or realign our working capital requirements.

Should we determine, at any time, that we require additional short-term liquidity, we would evaluate the alternative sources of financing that were potentially available to provide such funding. There can be no assurance that any such financing, if pursued, would be obtained, or if obtained, would be adequate or on terms acceptable to us. However, we believe that our strong balance sheet, flexible capital structure and borrowing capacity available to us under our Credit Facility position us to meet our anticipated liquidity requirements for the foreseeable future.

Selected Liquidity and Capital Resources Data

(Dollars in thousands)

|

Year Ended |

||||||||

|

September 30, |

October 1, |

|||||||

|

2023 |

2022 |

|||||||

|

Net cash provided by operating activities |

$ | 142,200 | $ | 5,670 | ||||

|

Net cash used for investing activities |

(20,896 | ) | (6,039 | ) | ||||

|

Net cash used for financing activities |

(43,950 | ) | (41,199 | ) | ||||

|

Cash and cash equivalents |

125,670 | 48,316 | ||||||

|

Net working capital |

252,698 | 272,736 | ||||||

|

Total debt |

- | - | ||||||

|

Percentage of total capital |

- | - | ||||||

|

Shareholders' equity |

$ | 381,505 | $ | 389,744 | ||||

|

Percentage of total capital |

100 | % | 100 | % | ||||

|

Total capital (total debt + shareholders' equity) |

$ | 381,505 | $ | 389,744 | ||||

Operating Activities

Operating activities provided $142.2 million of cash in 2023 primarily from net earnings adjusted for non-cash items together with a net decrease in working capital. Working capital provided $95.6 million of cash due to a $94.3 million decrease in inventories and an $18.2 million reduction in accounts receivable partially offset by a $16.9 million decrease in accounts payable and accrued expenses. The decrease in inventories was primarily due to lower raw material purchases along with lower average unit costs. The decrease in accounts receivable was largely driven by lower average selling prices. The decrease in accounts payable and accrued expenses was largely due to lower raw material purchases, lower unit costs and a reduction in accrued incentive plan expense.

Operating activities provided $5.7 million of cash in 2022 primarily from net earnings adjusted for non-cash items partially offset by an increase in working capital. Working capital used $134.3 million of cash due to a $118.6 million increase in inventories, a $13.7 million increase in accounts receivable and a $2.0 million decrease in accounts payable and accrued expenses. The increase in inventories was the result of higher raw material purchases during 2022 together with higher average unit costs. The increase in accounts receivable was due to higher average selling prices. The decrease in accounts payable and accrued expenses was primarily related to lower raw material purchases near the end of the current year.

We may elect to adjust our operating activities as there are changes in the conditions in our construction end-markets, which could materially impact our cash requirements. While a downturn in the level of construction activity affects sales to our customers, it generally reduces our working capital requirements.

Investing Activities

Investing activities used $20.9 million of cash in 2023 primarily due to capital expenditures ($30.7 million) partially offset by the receipt of proceeds from the sale of property, plant and equipment ($9.9 million). Investing activities used $6.0 million of cash in 2022 primarily due to capital expenditures ($15.9 million) partially offset by the receipt of proceeds from the sale of assets held for sale ($6.9 million), life insurance claims ($1.5 million) and a decrease in cash surrender value of life insurance policies ($1.4 million). Capital expenditures for both years focused on cost and productivity improvement initiatives in addition to recurring maintenance requirements. Capital expenditures are expected to total up to approximately $30.0 million in 2024, including expenditures to support costs and productivity initiatives, modernize our facilities and information systems and recurring maintenance requirements. Our investing activities are largely discretionary, providing us with the ability to significantly curtail outlays should future business conditions warrant that such actions be taken.

Financing Activities

Financing activities used $44.0 million of cash in 2023 and $41.2 million of cash in 2022. In 2023, $41.3 million of cash was used for dividend payments (including a special cash dividend of $38.9 million, or $2.00 per share, and regular cash dividends totaling $2.4 million) and $2.3 million for the repurchase of common stock. In 2022, $41.2 million of cash was used for dividend payments (including a special cash dividend of $38.8 million, or $2.00 per share, and regular cash dividends totaling $2.4 million) and $1.2 million for the repurchase of common stock, which was partially offset by $1.7 million of proceeds from the exercise of stock options.

Cash Management

Our cash is principally concentrated at one financial institution, which at times exceeds federally insured limits. We invest excess cash primarily in money market funds, which are highly liquid securities that bear minimal risk.

Credit Facility

We have a Credit Facility that is used to supplement our operating cash flow and fund our working capital, capital expenditure, general corporate and growth requirements. In March 2023, we amended our credit agreement to extend the maturity date of the Credit Facility from May 15, 2024, to March 15, 2028 and replaced the London Inter-Bank Offered Rate with the Secured Overnight Financing Rate. The Credit Facility provides for an accordion feature whereby its size may be increased by up to $50.0 million, subject to our lender’s approval. Advances under the Credit Facility are limited to the lesser of the revolving loan commitment amount (currently $100.0 million) or a borrowing base amount that is calculated based upon a percentage of eligible receivables and inventories. As of September 30, 2023, no borrowings were outstanding on the Credit Facility, $98.5 million of borrowing capacity was available and outstanding letters of credit totaled $1.5 million (see Note 8 to the consolidated financial statements). As of October 1, 2022, there were no borrowings outstanding on the Credit Facility.

Off-Balance Sheet Arrangements

We do not have any material transactions, arrangements, obligations (including contingent obligations) or other relationships with unconsolidated entities or other persons, as defined by Item 303(a)(4) of Regulation S-K of the SEC, that have or are reasonably likely to have a material current or future impact on our financial condition, results of operations, liquidity, capital expenditures, capital resources or significant components of revenues or expenses.

Contractual Obligations

In addition to our discussion and analysis surrounding our liquidity and capital resources, our contractual obligations and commitments as of September 30, 2023, include:

|

● |

Raw Material Purchase Commitments – See Note 12, “Commitments and Contingencies,” within our consolidated financial statements for further details concerning our non-cancelable raw material purchase commitments. |

|

● |

Supplemental Employee Retirement Plan Obligations – See Note 11, “Employee Benefit Plans,” within our consolidated financial statements for further detail of our obligations and the timing of expected future payments under our supplemental employee retirement plan. |

|

● |

Operating Leases – See Note 13, “Leases,” within our consolidated financial statements for further detail of our obligations and the timing of expected future payments, including a five-year maturity schedule. |

|

● |

Debt Obligations and Interest Payments - See Note 8, “Long-Term Debt,” within our consolidated financial statements for further detail of our debt and the timing of expected future principal and interest payments. As of September 30, 2023, there were no borrowings outstanding. |

|

● |

Capital Expenditures – As of September 30, 2023, we had contractual commitments for capital expenditures of $15.3 million. |

Impact of Inflation

We are subject to inflationary risks arising from fluctuations in the market prices for our primary raw material, hot-rolled carbon steel wire rod, and, to a much lesser extent, labor, freight, energy and other consumables that are used in our manufacturing processes. We have generally been able to adjust our selling prices to pass through increases in these costs or offset them through various cost reduction and productivity improvement initiatives. However, our ability to raise our selling prices depends on market conditions and competitive dynamics, and there may be periods during which we are unable to fully recover increases in our costs.

During 2023, we experienced a decline in wire rod prices primarily due to reductions in the cost of scrap for wire producers and a concurrent weakening in demand. Selling prices for our products fell in response to the softening demand and competitive pricing pressure. Consequently, our financial results were adversely affected as we consumed higher cost inventory that was purchased in prior periods. During 2022, we were successful in implementing price increases sufficient to recover the escalation in our raw material costs that occurred over the course of the year. The timing and magnitude of any future increases in raw material costs and the impact on selling prices for our products is uncertain at this time.

Outlook

Looking ahead to fiscal 2024, we are aware of the risks associated with higher interest rates and the implications for the broader U.S. economy and, ultimately, our end markets. Nevertheless, we remain optimistic about demand in our private and public nonresidential construction markets as customer sentiment is mostly positive. Furthermore, the outlook for infrastructure construction remains favorable as federal spending associated with the Infrastructure Investment and Jobs Act is expected to accelerate as we progress through fiscal 2024 and help drive demand.

Regardless of the market dynamics, we continue to focus on those factors we control, including closely managing and controlling our expenses; aligning our production schedules with demand in a proactive manner as there are changes in market conditions to minimize our operating costs; pursuing further improvements in the productivity and effectiveness of all our manufacturing, selling and administrative activities: and furthering our human capital strategy. We also expect increasing contributions from the substantial investments we have made in our facilities in recent years and expect to continue to make in the form of reduced operating costs and additional capacity to support future growth. Finally, we will continue to pursue acquisitions opportunistically to expand our penetration of markets we currently serve or expand our footprint.

The statements contained in this section are forward-looking statements. See “Cautionary Note Regarding Forward-Looking Statements” and “Risk Factors”.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

Our cash flows and earnings are subject to fluctuations resulting from changes in commodity prices, interest rates and foreign exchange rates. We manage our exposure to these market risks through internally established policies and procedures and, when appropriate, through the use of derivative financial instruments. We do not use financial instruments for trading purposes and are not a party to any leveraged derivatives. We monitor our underlying market risk exposures on an ongoing basis and believe we can modify or adapt our hedging strategies as necessary.

Commodity Prices

We are subject to significant fluctuations in the cost and availability of our primary raw material, hot-rolled carbon steel wire rod, which we purchase from both domestic and foreign suppliers. We negotiate quantities and pricing for both domestic and foreign wire rod purchases for varying periods (most recently monthly for domestic suppliers), depending upon market conditions, to manage our exposure to price fluctuations and to ensure adequate availability of material consistent with our requirements. We do not use derivative commodity instruments to hedge our exposure to changes in prices as such instruments are not currently available for wire rod. Our ability to acquire wire rod from foreign sources on favorable terms is impacted by fluctuations in strength of home markets, foreign currency exchange rates, foreign taxes, duties, tariffs, quotas and other trade actions. Although changes in our wire rod costs and selling prices tend to be correlated, in weaker market environments, we may be unable to fully recover increased wire rod costs, which would reduce our earnings and cash flows. Additionally, when raw material costs decline, our financial results may be negatively impacted if the selling prices for our products decrease to an even greater extent and if we are consuming higher cost material from inventory. Based on our 2023 shipments and average wire rod cost reflected in cost of sales, a 10% increase in the price of wire rod would have resulted in a $42.8 million decrease in our annual pre-tax earnings (assuming there was not a corresponding change in our selling prices).

Interest Rates

Although we did not have any balances outstanding on our Credit Facility as of September 30, 2023, future borrowings under the facility are subject to a variable rate of interest and are sensitive to changes in interest rates.

Foreign Exchange Exposure

We have not typically hedged foreign currency exposures related to transactions denominated in currencies other than U.S. dollars, as such transactions have not been material historically. We will occasionally hedge firm commitments for certain equipment purchases that are denominated in foreign currencies. The decision to hedge any such transactions is made by us on a case-by-case basis. There were no forward contracts outstanding as of September 30, 2023. During 2023, a 10% increase or decrease in the value of the U.S. dollar relative to foreign currencies to which we are typically exposed would not have had a material impact on our financial position, results of operations or cash flows.

Item 8. Financial Statements and Supplementary Data.

Financial Statements

|

Consolidated Statements of Operations for the years ended September 30, 2023, October 1, 2022 and October 2, 2021 |

21 |

|

Consolidated Statements of Comprehensive Income for the years ended September 30, 2023, October 1, 2022 and October 2, 2021 |

22 |

|

Consolidated Balance Sheets as of September 30, 2023 and October 1, 2022 |

23 |

|

Consolidated Statements of Shareholders’ Equity for the years ended September 30, 2023, October 1, 2022 and October 2, 2021 |

24 |

|

Consolidated Statements of Cash Flows for the years ended September 30, 2023, October 1, 2022 and October 2, 2021 |

25 |

|

Notes to Consolidated Financial Statements |

26 |

|

Report of Independent Registered Public Accounting Firm – Consolidated Financial Statements (PCAOB ID Number |

43 |

INSTEEL INDUSTRIES, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(In thousands, except per share amounts)

|

Year Ended |

||||||||||||

|

September 30, |

October 1, |

October 2, |

||||||||||

|

2023 |

2022 |

2021 |

||||||||||

|

Net sales |

$ | $ | $ | |||||||||

|

Cost of sales |

||||||||||||

|

Gross profit |

||||||||||||

|

Selling, general and administrative expense |

||||||||||||

|

Restructuring (recoveries) charges, net |

( |

) | ||||||||||

|

Other (income) expense, net |

( |

) | ||||||||||

|

Interest expense |

||||||||||||

|

Interest income |

( |

) | ( |

) | ( |

) | ||||||

|

Earnings before income taxes |

||||||||||||

|

Income taxes |

||||||||||||

|

Net earnings |

$ | $ | $ | |||||||||

|

Net earnings per share: |

||||||||||||

|

Basic |