UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________

FORM

| | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

| OR | |

| | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the transition period from ___________________ to ___________________ |

Commission File Number

THE SHYFT GROUP, INC.

(Exact Name of Registrant as Specified in Its Charter)

|

|

|

|

|

|

|

|

Registrant’s Telephone Number, Including Area Code: (

| Securities registered pursuant to Section 12(b) of the Securities Exchange Act: |

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on which Registered |

| Securities registered pursuant to Section 12(g) of the Securities Exchange Act: None |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

|

| Yes | ☐ |

| | ☒ |

|

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

|

| Yes | ☐ |

| | ☒ |

|

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

|

| | ☒ |

| No | ☐ |

|

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

|

| | ☒ |

| No | ☐ |

|

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | ☒ |

| Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | | Emerging growth company | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

|

| Yes | |

| No | ☒ |

|

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant, based on the last sales price of such stock on NASDAQ Global Select Market on June 30, 2022, the last business day of the registrant’s most recently completed second fiscal quarter: $

The number of shares outstanding of the registrant’s Common Stock as of February 17, 2023:

Documents Incorporated by Reference

Portions of the definitive proxy statement for the registrant’s May 17, 2023 annual meeting of shareholders, to be filed with the Securities and Exchange Commission no later than 120 days after December 31, 2022 are incorporated by reference in Part III.

FORWARD-LOOKING STATEMENTS

This Form 10-K contains some statements that are not historical facts. These statements are called “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements involve important known and unknown risks, uncertainties and other factors and generally can be identified by phrases using “estimate,” “anticipate,” “believe,” “project,” “expect,” “intend,” “predict,” “potential,” “future,” “may,” “will,” “should” or similar expressions or words. The Shyft Group, Inc.'s (the “Company,” “we,” “us” or “our”) future results, performance or achievements may differ materially from the results, performance or achievements discussed in the forward-looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions (“Risk Factors”) that are difficult to predict with regard to timing, extent, likelihood and degree of occurrence. Therefore, actual results and outcomes may materially differ from what may be expressed or forecasted in such forward-looking statements.

Risk Factors include the risk factors listed and more fully described in Item 1A below, “Risk Factors,” as well as risk factors that we have discussed in previous public reports and other documents filed with the Securities and Exchange Commission. The list in Item 1A below includes the primary risks our management believes could materially affect the potential results described by forward-looking statements contained in this Form 10-K. However, these risks may not be the only risks we face. Our business, operations and financial performance could also be affected by additional factors that are not presently known to us or that we currently consider to be immaterial to our operations. In addition, new Risk Factors may emerge from time to time that may cause actual results to differ materially from those contained in any forward-looking statements. Given these risks and uncertainties, although we believe that the forward-looking statements contained in this Form 10-K are reasonable, we cannot provide you with any guarantee that the results described in those forward-looking statements will be achieved. All forward-looking statements in this Form 10-K are expressly qualified in their entirety by the cautionary statements contained in this section, and investors should not place undue reliance on forward-looking statements as a prediction of actual results. The Company undertakes no obligation to update or revise any forward-looking statements to reflect developments or information obtained after the date this Form 10-K is filed with the Securities and Exchange Commission.

Trademarks and Service Marks

We own or have rights to trademarks, service marks or trade names that we use in connection with the operation of our business. Solely for convenience, some of the copyrights, trademarks, service marks and trade names referred to in this Annual Report on Form 10-K are listed without the ©, ® and ™ symbols, but we will assert, to the fullest extent under applicable law, our rights to our copyrights, trademarks, service marks, trade names and domain names. The trademarks, service marks and trade names of other companies appearing in this Annual Report on Form 10-K are, to our knowledge, the property of their respective owners.

PART I

| Item 1. |

Business. |

General

As used herein, the term “Company”, “we”, “us” or “our” refers to The Shyft Group, Inc. and its subsidiaries unless designated or identified otherwise.

We are a niche market leader in specialty vehicle manufacturing and assembly for the commercial vehicle (including last-mile delivery, specialty service and vocation-specific upfit segments) and recreational vehicle industries. Our products include walk-in vans, truck bodies, and cargo van and pick-up truck upfits used in e-commerce/parcel delivery, upfit equipment used in the mobile retail and utility trades, as well as luxury Class A diesel motorhome custom chassis and contract manufacturing and assembly services. We also supply replacement parts and offer repair, maintenance, field service and refurbishment services for the vehicles that we manufacture. Our operating activities are conducted through our wholly-owned operating subsidiary, The Shyft Group USA, Inc., with locations in Novi, Charlotte, and Plymouth, Michigan; Bristol, Indiana; Waterville, Maine; Landisville, Pennsylvania; North Charleston, South Carolina; Pompano Beach and West Palm Beach, Florida; Kansas City, Missouri; Carson, McClellan Park, and Montebello, California; Mesa, Arizona; Dallas and Weatherford, Texas; and Saltillo, Mexico.

Our vehicles, parts and services are sold to commercial users, original equipment manufacturers (OEMs), dealers, individual end users, and municipalities and other governmental entities. Our diversification across several sectors provides numerous opportunities while reducing overall risk as the various markets we serve tend to have different cyclicality. We have an innovative team focused on building lasting relationships with our customers by designing and delivering market leading specialty vehicles, vehicle components and services. Additionally, our business structure provides agility to quickly respond to market needs, take advantage of strategic opportunities when they arise and correctly size and scale operations to ensure stability and growth. Our growing opportunities that we have capitalized on in last mile delivery as a result of the rapidly changing e-commerce market is an excellent example of our ability to generate growth and profitability by quickly fulfilling customer needs.

Performance Overview

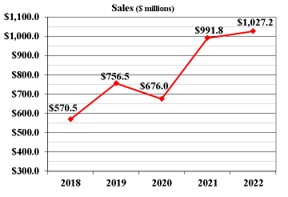

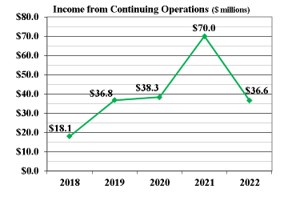

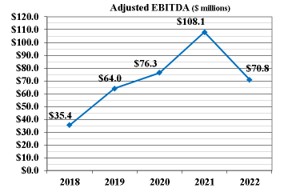

Unless noted otherwise, the data in this Form 10-K reflects our continuing operations and, therefore, excludes the performance of our prior Emergency Response Vehicles (“ERV”) business. Over the past five years our sales have increased by $456.7 million, a compound annual growth rate (CAGR) of 15.8%, while income from continuing operations has grown by $18.5 million, a CAGR of 19.2%, and Adjusted EBITDA has grown by $35.4 million, a CAGR of 18.9%. Please see the reconciliation of income from continuing operations to Adjusted EBITDA near the end of Item 1 of this Form 10-K.

|

|

|

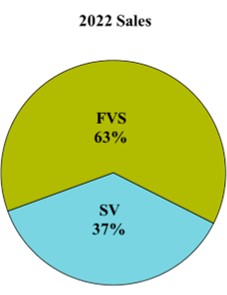

Our Segments

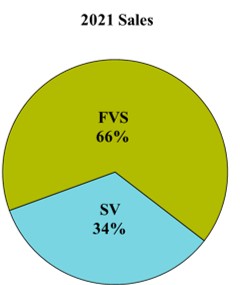

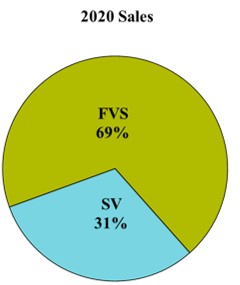

We identify our reportable segments based on our management structure and the financial data utilized by our chief operating decision maker to assess segment performance and allocate resources among our operating units. We have two reportable segments: Fleet Vehicles and Services (“FVS”) and Specialty Vehicles (“SV”). Sales by segment are as follows:

|

|

|

Fleet Vehicles and Services Segment

We manufacture commercial vehicles used in the e-commerce/last mile/parcel delivery, beverage and grocery delivery, laundry and linen, mobile retail, and trades and construction industries through our Bristol, Indiana; Landisville, Pennsylvania; and Charlotte, Michigan locations. Our commercial vehicles are marketed under the Utilimaster brand name, which serves a diverse customer base and sells aftermarket parts and accessories for walk-in vans and other delivery vehicles. We also provide vocation-specific equipment upfit services, which are marketed and sold as Utilimaster Upfit Services, through our manufacturing operations in Kansas City, Missouri; North Charleston, South Carolina; and Saltillo, Mexico. Our Fleet Vehicles and Services segment employed approximately 2,600 employees and 400 contractors as of December 31, 2022.

We offer fleet vehicles in Gross Vehicle Weight Rating (“GVWR”) Class 1 through Class 7, the largest range of product offerings amongst our competitors.

| Cargo Van Upfit | “Velocity” | Traditional Walk-in-Van | Truck Body |

|

|

|

|

| Class 1 & 2 | Class 2 & 3 | Class 4 & 5 | Class 6 & 7 |

Innovation

Our Solution Experts employ a customer-centric approach by working with customers through a process of listening and learning, needs assessment, and design innovation through building and implementing solutions designed with our customers and their end customers in mind. Innovations implemented by our Solution Experts include efficiency improvements and cost saving solutions for the service segment, utility industry, food and beverage delivery, and mobile retail industry, such as safe loading equipment, keyless entry and cargo access systems, backup camera systems, and refrigeration solutions. Our teams can deliver product customization ranging from out-of-the-box to 100% custom solutions, based on customer needs and business requirements.

Innovations launched by the product development team include a new walk-in-van format, named the Velocity. Available in GVWR Class 2 and Class 3 designs, the Velocity lineup spans multiple OEM chassis formats to accommodate buyer preference and to increase manufacturing and distribution scale.

Products

|

Walk-in Vans Assembled on a de-contented or “stripped” truck chassis supplied with engine and drive train components, our walk-in vans are used across a variety of vocations for multiple delivery and mobile service options. The vehicles feature a durable and lightweight aluminum body with a highly modularized cargo area, featuring extensive driver ergonomics options and a low step-in height for easy entry and egress. |

|

|

|

|

|

Truck Bodies Utilimaster dry van truck bodies are the industry standard for heavy-duty commercial delivery and are installed on chassis from a variety of manufacturers, which are supplied with a finished cab. They feature a highly customizable cargo area for maximum versatility and are manufactured with anti-rust galvanized steel, Utiliplate, and aluminum component parts. Available with cargo lengths from 10 to 28 feet and interior heights ranging from 72 to 108 inches. |

|

|

|

|

Cutaway Utilimaster cutaway truck bodies are the industry standard for medium-duty commercial delivery and are installed on chassis from a variety of manufacturers that are supplied with a finished cab. The highly configurable design can be configured with a set-back walk-through bulkhead allowing access to the cargo area from the cab. Available with cargo lengths from 10 to 18 feet and interior heights ranging from 72 to 90 inches. |

|

|

|

|

|

Velocity® A nimble, fuel efficient, and ergonomically designed walk-in van lineup built on commercial cargo van chassis across OEMs is designed to combine the cargo capacity of a traditional walk-in-van with the drivability of a smaller format vehicle. The Velocity lineup makes large product/package deliveries easy, with lower entry/egress height and 3-point grab rails at side and rear doors, and comfortable safe seats. Economical to operate, the Velocity features a lower total cost of ownership than that of a traditional walk-in van. |

|

|

|

|

Specialty Upfit We install specialty interior and exterior upfit equipment for walk-in vans, truck bodies, cargo vans, and light duty pick-up trucks for added safety, cargo handling efficiency, and vocational functionality. |

|

Parts and Accessories We provide a full line of parts and accessories for our walk-in vans and truck bodies. |

Marketing

We market our commercial vehicles, including walk-in vans, cutaway vans, and truck bodies, under the Aeromaster®, Velocity, Trademaster®, and Utilivan® product brand names. We sell our fleet vehicles to leasing companies, national and fleet accounts (national accounts typically have 1,000+ vehicle fleets and fleet accounts typically have 100+ vehicle fleets), and through a network of independent truck dealers in the U.S. and Canada. We also market our truck bodies direct to retail customers in select markets. We provide aftermarket support, including parts sales and field services, to all of our fleet vehicle customers through our Customer Service Department located in Bristol, Indiana.

Manufacturing

We have implemented the Shyft Production System, lean manufacturing and continuous improvement in all of our fleet vehicle facilities in order to maximize efficiency and reduce costs. Our facilities are aligned with our commercial and OEM customers for the installation of upfit equipment. Our walk-in vans and truck bodies are manufactured on non-automated assembly lines utilizing a combination of high-skilled tradespeople and assemblers. Our upfit facilities utilize teams of workers requiring minimal capital investment for efficient and timely installation of a variety of equipment for various vocations.

Specialty Vehicles Segment

Our Specialty Vehicles segment includes our Spartan RV Chassis and Builtmore Contract Manufacturing brands, service bodies, and vocation specific upfit. Spartan RV is manufactured out of our Charlotte, Michigan facility where we engineer and manufacture luxury Class A diesel motorhome chassis, provide contract assembly of specialty vehicles and other commercial vehicles, and distribute related aftermarket parts and accessories under the Red Diamond Aftermarket Solutions and Builtmore Contract Manufacturing brand names. Our service body operations include locations in Charlotte, Michigan; Carson, McClellan Park, and Montebello, California; Mesa, Arizona; Dallas and Weatherford, Texas; and Waterville, Maine. We also provide vocation-specific equipment upfit services, which are marketed and sold under the Strobes-R-Us brand, through our manufacturing operations in Pompano and West Palm Beach, Florida. Our specialty vehicle products are manufactured to customer specifications upon receipt of confirmed purchase orders. As a specialty chassis and vehicle manufacturer, we believe we hold a unique position for continued growth due to the high quality and performance of our products, our proactive engineering, manufacturing expertise and flexibility, and the scalability of our operations. Our specialty vehicle products are generally sold through original equipment manufacturers in the case of chassis and vehicles and to dealers, distributors or directly to consumers for service bodies and aftermarket parts and accessories. The Specialty Vehicles segment employed approximately 1,000 employees and less than 100 contractors as of December 31, 2022.

Innovation

Through trade shows and motorhome rallies, we talk with a wide variety of motorhome owners to identify needs and provide our customers the latest technology and highest quality in our motorhome and specialty chassis. Recent innovations to our motorhome chassis include: our Premier Drive™ system, with custom tuned shocks, 20k independent front suspension, and passive steer tag axle that greatly improve ride, handling and maneuverability; automatic air leveling that adds convenience and functionality to luxury motorhomes; and updates to the Connected Coach experience with the Tri-Pod Steering Wheel, rain sensing wiper controls, a 15in anti-glare Digital Dash that receives direct notifications from the Spartan RV Chassis Advanced Protection System™ (APS), which includes adaptive cruise control, collision mitigation, electronic stability control and lane departure warning – all designed to create a safer, more intuitive driving experience. We also support trade shows, OEM and dealer events to promote our service body products and upfit services. We continue to expand our product portfolio and execute innovations in that segment.

Products

|

|

Motorhome Chassis We custom manufacture diesel chassis for luxury Class A motorhome to the individual specifications of our motorhome OEM customers under the Spartan RV Chassis brand name. These specifications vary based on specific interior and exterior design specifications, gross vehicle weight, horsepower, and electrical needs of the motorhome bodies to be attached to our chassis. Our motorhome chassis feature diesel engines of 360 to 605 horsepower and are used in motorhomes ranging from 34 to 45 feet. Our motorhome chassis are separated into four models: the K1, K2, K3, and K4 series chassis. |

|

Contract Manufacturing We provide final assembly services for Isuzu N-gas and F-series chassis for the North American market under the Builtmore Contract Manufacturing brand name. These class 3 and class 5 chassis are utilized in a variety of final configurations for light duty freight hauling and industrial uses. We have an efficient, flexible and a highly skilled team of assembly workers and management, which, along with a dedication to lean manufacturing and continuous improvement, allow us to deliver superior quality and value in contract manufacturing. |

|

|

Service Bodies We manufacture and assemble truck bodies for a variety of trades and vocations. Those body configurations include utility bodies, stake bodies, contractor bodies, dump/landscape bodies and vocational dry freight bodies under the Royal Truck Body and DuraMag brand names. |

|

Specialty Upfit We design and install custom lighting and upfit solutions to meet the unique needs of certain fleet industries including a range of specialty industries such as law enforcement, Department of Transportation, security companies, and providers of funeral, towing, and utility services. We provide durable, reliable, and high-quality product installations for any vehicle requiring specialty exterior and interior accessory upfits. |

|

Parts and Accessories We provide truck accessories under our Magnum brand and provide a full line of parts and accessories as well as maintenance and repair services for our motorhome and specialty chassis. |

Marketing

We sell our Class A diesel motorhome chassis to OEMs for use in the manufacturing of luxury motorhomes. We actively participate in a variety of trade shows and motorhome rallies that promote our products and Red Diamond aftermarket solutions in addition to providing an opportunity to communicate with our end customers to showcase our latest innovations and identify needs and opportunities for continuous improvement of our chassis. We sell our service bodies through a commercial dealer network and through OEM pools, and we actively participate in a variety of regional and national trade shows that promote our products. We also provide vocation-specific equipment upfit services, which are marketed and sold under the Strobes-R-Us brand. We are expanding the marketing of Magnum accessories beyond work trucks to include outdoor enthusiasts and truck owners.

Manufacturing

Our motorhome chassis, service body, and specialty manufacturing operations employ the Shyft Production System, lean manufacturing, and continuous improvement to bring efficiency and cost reduction throughout our Specialty Vehicles segment. We engineer, manufacture, and assemble Spartan RV chassis, as well as other specialty vehicles on non-automated assembly lines. We assemble both the Isuzu N-gas and F-series chassis on high-volume assembly lines that utilize a variety of state-of-the-art automation and testing equipment. Our upfit facilities utilize teams of workers requiring minimal capital investment for efficient and timely installation of a variety of equipment.

Competition

The principal methods we use to build competitive advantages include short engineering reaction time, custom design capability, high product quality, superior customer service and quick delivery. We employ a solutions-based approach to offer specialized products tailored to customer needs across the spectrum of our products. We compete with companies that manufacture for similar markets, including some divisions of large diversified organizations that have total sales and financial resources exceeding ours. Our competition in the fleet vehicle market ranges from one large manufacturer in the walk-in van market to a number of smaller manufacturers in the truck body and equipment upfit markets. Our competitors in the specialty vehicle market are principally large multi-product line manufacturers of specialty and heavy-duty vehicles. In addition to established mature competitors, we also face competition from new market entrants including technology companies.

Suppliers

We are dedicated to establishing long-term and mutually beneficial relationships with our suppliers. Through these relationships, we benefit from new innovations, higher quality, reduced lead times, smoother/faster manufacturing ramp-up of new vehicle introductions and lower total costs of doing business. Our accelerating growth and company-wide supply chain management initiatives allow us to benefit from economies of scale and maximize focus on a common vision.

The single largest commodity directly utilized in production is aluminum, which we purchase under purchase agreements based on forecasted production requirements. To a lesser extent we are dependent upon suppliers of lumber, fiberglass and steel for our manufacturing. We have initiated long-term supplier agreements and are consolidating suppliers where beneficial to gain pricing advantages. There are several readily available sources for the majority of these raw materials. However, we are heavily dependent on specific component part products from a few single source vendors. We maintain a qualification, on-site inspection, assistance, and performance measurement system to control risks associated with reliance on suppliers. We normally do not carry inventories of such raw materials or components in excess of those reasonably required to meet production and shipping schedules. Material and component cost increases are passed on to our customers whenever possible. There can be no assurance that there will not be any supply issues over the long-term.

In the assembly of certain of our vehicles, we use chassis supplied by third parties, and we generally do not purchase these chassis for inventory. For this market, we typically accept shipment of truck chassis owned by dealers or end users, for the purpose of installing and/or manufacturing our specialized commercial vehicles on such chassis, but from time to time we do purchase chassis for use in fulfilling certain customer orders.

Research and Development

Our success depends on our ability to innovate and add new products and features ahead of changing market demands and new regulatory requirements. Thus, we emphasize research and development and commit significant resources to develop and adapt new products and production techniques. Our engineering team is looking past “current practices” and “best practices” to deliver “next practices” for our customers and shareholders. Our engineering group's goal throughout the company: to deliver world class products and manufacturing processes regardless of product line or location. Results are accomplished with the appropriate blend of predictive analysis and physical property testing in our Research and Development facilities along with ride-and-drive analysis. Our efforts range from executing special orders for current production; to new production development for new functionality and product improvements; to exciting technologies that are new to the markets we serve, like vehicle electrification. Our engineering actions are driven by our firm commitment to safety, quality, delivery, and productivity. We spent $25.3 million, $8.5 million, and $4.4 million on research and development in 2022, 2021, and 2020, respectively.

Shyft’s Blue Arc™ EV Solutions brought forward an all-electric purpose-built Class 3, 4, and 5 chassis platform built from the ground up and designed to serve a wide array of medium-duty truck markets, from last mile parcel delivery fleets to work trucks, passenger busses, recreational vehicles, and more. The EV-powered chassis will feature customizable length and wheelbase, making it well-suited for a variety of vehicle types. The chassis’ modular design can accommodate multiple GVWR classifications, based on build out and usage. With this high degree of configurability, the all-electric chassis is adaptable to last mile delivery, work truck, mass transit, recreational vehicle, and other emerging EV markets.

Product Warranties

We provide limited warranties against assembly and construction defects. These warranties generally provide for the replacement or repair of defective parts or workmanship for specified periods, ranging from one year to twenty years, following the date of sale. With the use of validation testing, predictive analysis tools and engineering and design standards, we strive to continuously improve product quality and durability, and reduce our exposure to warranty claims. The end users also may receive limited warranties from suppliers of components that are incorporated into our chassis and vehicles. For more information concerning our product warranties, see “Note 11 – Commitments and Contingent Liabilities” of the Notes to Consolidated Financial Statements in Item 8 appearing in this Form 10-K.

Patents, Trademarks and Licenses

We have 18 United States patents, which include rights to the design and structure of chassis and certain peripheral equipment, and we have 22 United States, Canada, and Patent Cooperation Treaty pending patent applications. The existing patents will expire on various dates from 2025 through 2040 and utility patents are subject to payment of required maintenance fees. We also own or license 103 federal and international trademark and service mark registrations. The trademark and service mark registrations are generally renewable under applicable laws, subject to payment of required fees and the filing of affidavits of use. In addition, we have various pending trademark applications.

Our products and services are identified by our trademarks and service marks. Our trademarks and service marks are valuable assets to both of our business segments. We are not aware of any infringing uses or any prior claims of ownership of our trademarks that could materially affect our business. It is our policy to pursue registration of our primary marks whenever possible and to vigorously defend our patents, trademarks and other proprietary marks against infringement or other threats to the extent practicable under applicable laws.

Human Capital Management

We believe people are the most critical component in our continued success, and we strive to attract high-performing talent. As of December 31, 2022, we employed approximately 4,200 employees and contractors. Approximately 10% of our total workforce consists of contractors, including all personnel at our Saltillo, Mexico operation. Our production processes leverage a combination of skilled tradespeople and high-touch assemblers working in body, electrical, mechanical, paint, and assembly operations. As a team, our employees and contractors put the Company’s core values into action, while executing on key growth initiatives to maintain long-term sustainable growth. We strive to create a workplace of choice to attract, retain, and develop top talent to achieve our vision and deliver shareholder results.

In our locations, we compete with many local companies for talent. We have implemented talent strategies and market competitive wages and benefits to support talent acquisition and retention. In addition to these actions, we have implemented employee surveys and focus groups that encourage our employees to share their opinions and feedback on the culture of our company. The results of the surveys are analyzed and measured to learn how we can enhance and accelerate improvements in the attraction and retention in a difficult talent environment.

We adhere to a philosophy that includes, among other things, commitments to create ongoing job opportunities, pay fair wages, and protect worker health and safety. Fundamental to these commitments are our Company’s core values of honesty and integrity, accountability, trust, and performance excellence. Management considers relations with the Company’s workforce to be positive.

Compensation and Benefits

We believe the structure of our compensation packages provides the appropriate incentives to attract, retain and motivate our employees. We provide base pay that is competitive and that aligns with employee positions, skill levels, experience and geographic location. In addition to base pay, we seek to reward employees with incentive awards, recognition programs, educational opportunities, paid time off, and equity awards for employees in certain roles.

Diversity and Inclusion

We value and advance the diversity and inclusion of the people with whom we work. We are committed to equal opportunity and are intolerant of discrimination and harassment. We strive to maintain workplaces that are free from discrimination or harassment on the basis of race, sex, color, national or social origin, ethnicity, religion, age, disability, sexual orientation, gender identification or expression, political opinion or any other status protected by applicable law.

The basis for recruitment, hiring, placement, development, training, compensation and advancement at the Company includes qualifications, performance, skills and experience.

We do not tolerate disrespectful or inappropriate behavior, unfair treatment or retaliation of any kind. Harassment is not tolerated in the workplace and in any work-related circumstance outside the workplace.

Customer Base

We serve customers ranging from municipalities to OEMs to commercial customers and vehicle dealers throughout our product lines. Sales to our top 10 customers in 2022 accounted for 52.6% of our sales. Sales to customers that individually exceeded 10% of our consolidated sales for 2022, 2021 and 2020 are detailed in the chart below.

|

Year |

Customer |

Sales ($ millions) |

Percentage of consolidated sales |

Segment |

||||||||

| 2022 | Amazon | $ | 153.6 | 15.0 | % | FVS | ||||||

| 2022 | Newmar | $ | 107.7 | 10.5 | % | SV | ||||||

| 2021 | Amazon | $ | 248.6 | 25.1 | % | FVS | ||||||

| 2020 |

Amazon |

$ |

198.3 |

29.3 |

% |

FVS |

||||||

We do have other significant customers which, if the relationship changes significantly, could have a material adverse impact on our financial position and results of operations. We believe that we have developed strong relationships with our customers and continually work to develop new customers and markets. See related risk factors in Item 1A of this Form 10-K.

Sales to customers outside the United States were $7.7 million, $11.7 million, and $9.5 million for the years ended December 31, 2022, 2021 and 2020, respectively, or 0.7%, 1.2%, and 1.4%, respectively, of sales for those years. Substantially all of our long-lived assets are located in the United States.

Order Backlog

Our order backlog by reportable segment is summarized in the following table (in thousands).

| December 31, 2022 |

December 31, 2021 |

Decrease |

||||||||||

| FVS |

$ | 736,690 | $ | 859,442 | $ | (122,752 | ) | |||||

| SV |

96,023 | 104,117 | (8,094 | ) | ||||||||

| Total consolidated |

$ | 832,713 | $ | 963,559 | $ | (130,846 | ) | |||||

Our FVS backlog decreased by $122.8 million, or 14.3%. Our SV segment backlog decreased by $8.1 million, or 7.8%.

While orders in the backlog are subject to modification, cancellation or rescheduling by customers, this has not been a major factor in the past. Although the backlog of unfilled orders is one of many indicators of market demand, several factors, such as chassis and component availability, changes in production rates, available capacity, new product introductions and competitive pricing actions, may affect actual sales. Accordingly, a comparison of backlog from period-to-period is not necessarily indicative of eventual actual shipments.

Non-GAAP Financial Measure

This Form 10-K presents Adjusted EBITDA (earnings before interest, taxes, depreciation and amortization), which is a non-GAAP financial measure. This non-GAAP measure is calculated by excluding items that we believe to be infrequent or not indicative of our underlying operating performance, as well as certain non-cash expenses. We define Adjusted EBITDA as income from continuing operations before interest, income taxes, depreciation and amortization, as adjusted to eliminate the impact of restructuring charges, acquisition related expenses and adjustments, non-cash stock-based compensation expenses, and other gains and losses not reflective of our ongoing operations.

We present the non-GAAP measure Adjusted EBITDA because we consider it to be an important supplemental measure of our performance. The presentation of Adjusted EBITDA enables investors to better understand our operations by removing items that we believe are not representative of our continuing operations and may distort our longer-term operating trends. We believe this measure to be useful to improve the comparability of our results from period to period and with our competitors, as well as to show ongoing results from operations distinct from items that are infrequent or not indicative of our continuing operating performance. We believe that presenting this non-GAAP measure is useful to investors because it permits investors to view performance using the same tools that management uses to budget, make operating and strategic decisions, and evaluate our historical performance. We believe that the presentation of this non-GAAP measure, when considered together with the corresponding GAAP financial measures and the reconciliations to that measure, provides investors with additional understanding of the factors and trends affecting our business than could be obtained in the absence of this disclosure.

Our management uses Adjusted EBITDA to evaluate the performance of and allocate resources to our segments. Adjusted EBITDA is also used, along with other financial and non-financial measures, for purposes of determining annual incentive compensation for our management team and long-term incentive compensation for certain members of our management team.

The following table reconciles Income from continuing operations to Adjusted EBITDA for the periods indicated.

| 2022 | 2021 |

2020 |

2019 |

2018 |

||||||||||||||||

| Income from continuing operations |

$ | 36,558 | $ | 69,974 | $ | 38,289 | $ | 36,790 | $ | 18,116 | ||||||||||

| Net (income) attributable to non-controlling interest |

- | (1,230 | ) | (347 | ) |

(140 | ) |

- | ||||||||||||

| Interest expense |

2,833 | 414 | 1,293 | 1,839 | 1,080 | |||||||||||||||

| Income tax expense |

7,368 | 14,506 | 9,867 | 10,355 | 3,334 | |||||||||||||||

| Depreciation and amortization |

14,774 | 11,356 | 13,903 | 6,073 | 6,214 | |||||||||||||||

| Restructuring and other related charges |

757 | 505 | 1,873 | 316 | 662 | |||||||||||||||

| Acquisition related expenses and adjustments |

884 | 1,585 | 1,332 | 3,531 | 1,952 | |||||||||||||||

| Non-cash stock-based compensation expense |

7,619 | 8,745 | 7,706 | 5,281 | 4,027 | |||||||||||||||

| Loss from write-off of construction in process |

- | - | 2,430 | - | - | |||||||||||||||

| Loss from liquidation of JV | - | 643 | - | - | - | |||||||||||||||

| Non-recurring professional fees | - | 1,568 | - | - | - | |||||||||||||||

| Adjusted EBITDA |

$ | 70,793 | $ | 108,066 | $ | 76,346 | $ | 64,045 | $ | 35,385 | ||||||||||

Available Information

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other reports (and amendments thereto) filed or furnished pursuant to Section 13(a) of the Securities Exchange Act are available, free of charge, on our internet website (www.TheShyftGroup.com) as soon as reasonably practicable after we electronically file or furnish such materials with the Securities and Exchange Commission (“SEC”).

The SEC maintains an internet website (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

Information About our Executive Officers

The executive officers of the Company, their business experience and their ages as of February 1, 2023, are as follows:

| Name |

Position |

Business Experience |

Age |

Executive Officer Since |

||

| Daryl M. Adams |

President and Chief Executive Officer |

President and Chief Executive Officer since February 2015. Director since December 2014. Chief Operating Officer from July 2014 to February 2015. Chief Executive Officer, Midway Products from 2007 to 2014. |

61 |

2015 |

| Name |

Position |

Business Experience |

Age |

Executive Officer Since |

||

| Jonathan C. Douyard |

Chief Financial Officer |

Chief Financial Officer since March 2020. Vice President and Chief Financial Officer, Fluke Corporation from June 2016 to February 2020. Prior roles included finance leadership positions with Commercial Systems & Services business unit, Sikorsky Aircraft (United Technologies) and General Electric subsidiaries. |

43 |

2020 |

||

| Todd A. Heavin |

Chief Operating Officer |

Chief Operating Officer since June 2019. Independent Management Consultant from August 2017 to May 2019. Division President, American Axle from April 2017 to August 2017. Division General Manager, Metaldyne Performance Group from 2014 to April 2017. |

61 |

2019 |

||

| John Dunn |

President, Fleet Vehicles and Services |

President, Shyft Fleet Vehicles and Services since January 2023. President and CEO, North and South America of Plastic Omnium, Clean Energy Systems from April 2014 to December 2022. President, Brose North America from July 2012 to April 2014. |

56 |

2023 |

||

| Stephen K. Guillaume |

President, Specialty Vehicles |

President, Shyft Specialty Vehicles since May 2015. Vice President of New Business Development and Joint Ventures from January 2015 to May 2015.Vice President and General Manager, Navistar Commercial Trucks from 2010 through 2014. |

55 |

2015 |

||

| Joshua A. Sherbin |

Chief Legal Officer, Chief Compliance Officer and Corporate Secretary |

Chief Legal Officer, Chief Compliance Officer and Corporate Secretary since May 2021. Senior Vice President, General Counsel, Chief Compliance Officer and Corporate Secretary, TriMas Corporation from March 2016 to May 2021. |

59 |

2021 |

||

| Colin Hindman | Chief Human Resources Officer | Chief Human Resources Officer since June 2020. Chief Human Resources Officer, Dayco Products LLC from March 2017 to June 2020. Vice President, Human Resources, TriMas Corporation from March 2010 to November 2016. | 48 | 2022 |

| Item 1A. |

Risk Factors. |

Our financial condition, results of operations and cash flows are subject to various risks, many of which are not exclusively within our control that may cause actual performance to differ materially from historical or projected future performance. The risks described below are the primary risks known to us that we believe could materially affect our business, financial condition, results of operations, or cash flows. However, these risks may not be the only risks we face. Our business could also be affected by additional factors that are not presently known to us, factors we currently consider to be immaterial to our operations, or factors that emerge as new risks in the future. Readers should not interpret the disclosure of any risk factor to imply that the risk has not already materialized.

Risks Related to Global Events

Uncertain global macro-economic and political conditions could materially adversely affect our business, financial condition, results of operations, or cash flows.

Global and local business conditions include inflation, recession, interest rates, availability of capital, energy and commodity prices, trade laws and the effects of governmental initiatives to manage economic conditions. We have experienced, and are continuing to experience, challenges and increases in costs for logistics and in our supply chains, such as increased port congestion, intermittent supplier delays, and volatility in prices of commodities such as base metals and raw materials. In addition, we are experiencing varying levels of inflation resulting in part from various supply chain disruptions, increased shipping and transportation costs, increased raw material and labor costs, and other disruptions caused by the COVID-19 pandemic and general economic conditions. Further unfavorable conditions such as a general slowdown of the U.S. economy, uncertainty and volatility in the financial markets, uncertainty or volatility in commodity prices or additional inflationary factors and rising interest rates could result in higher operating costs and expenses for our Company and could make it more difficult and expensive for us to obtain financing.

The current invasion of Ukraine by Russia has escalated tensions among the United States, the North Atlantic Treaty Organization (NATO) and Russia. Such invasion, ongoing military conflict, resulting sanctions and related countermeasures by NATO states, the United States and other countries could lead to market disruptions, including significant volatility in commodity prices, credit and capital markets, as well as supply chain interruptions for equipment, which could have an adverse impact on our business, financial condition, results of operations, or cash flows.

These challenges also impact our suppliers, and we have experienced supply chain disruptions as a result. Our inability to obtain raw materials, chassis and other supplies on a timely basis negatively impacts our ability to fulfill customer orders, which may have a material adverse impact on our results of operations, financial condition, and liquidity.

Risks Related to Our Company and Business

Any negative change in our relationship with our major customers could have significant adverse effects on revenues and profits.

Our financial success is directly related to the willingness of our customers to continue to purchase our products. Failure to fill customers’ orders in a timely manner or on the terms and conditions they may impose could harm our relationships with our customers. The importance of maintaining excellent relationships with our major customers may also give these customers leverage in our negotiations with them, including pricing and other supply terms, as well as post-sale disputes. This leverage may lead to increased costs to us. Furthermore, if any of our major customers experience a significant downturn in their business or fail to remain committed to our products or brands, then these customers may reduce or discontinue purchases from us, which could have an adverse effect on our business, results of operations and financial condition. There were two customers that each accounted for 10 percent or greater of consolidated sales in 2022. Sales to our top 10 customers in 2022 accounted for 52.6 percent of our sales in the aggregate. In addition, our largest customer owns a significant share of a new entrant competitor, and our business may be adversely affected if the customer’s ownership of or our competitive relationship in the marketplace with our competitor results in a decline or discontinuation of the customer’s purchases from us.

We may not be able to remain competitive in the rapidly changing markets in which we compete.

The markets we serve are undergoing rapid transformation, particularly with respect to parcel delivery services and electric vehicle (EV) technologies. Our current and potential competitors include companies that have significantly greater financial, technical, manufacturing, marketing and other resources than we do, including OEMs and certain of our customers, and which are highly motivated by market opportunities to deploy those resources to the design, development, manufacturing, distribution, promotion, sale and support of their products, including their electric vehicles. In addition to these established, mature competitors, we also face competition from new market entrants, including technology companies. As a result of these market opportunities, OEMs and other companies have taken actions to reduce costs, including through in-sourcing and supply base consolidation. We expect these trends to continue and even accelerate. We expect competition for electric vehicles to intensify due to increased demand and a regulatory push for alternative fuel vehicles, continuing globalization, and consolidation in the worldwide vehicle industry. Increased competition may lead to lower vehicle unit sales and increased inventory, which may result in downward price pressure and adversely affect our business, financial condition, operating results, and prospects. Our business will be adversely affected if we are unable to adequately respond to these pressures or otherwise continue to compete in these markets.

Amounts included in order backlog may not result in actual revenue and are an uncertain indicator of our future revenue.

Backlog is generally comprised of agreements and purchase orders from customers that are subject to modification, cancellation, or rescheduling. While realization of revenue related to order backlog has not been a major issue in the past, we cannot assure that we will recognize revenue with respect to each order included in order backlog. Should a cancellation occur, our order backlog and anticipated revenue would be reduced unless we are able to replace the cancelled order. As a result, the order backlog may not be indicative of future sales and can vary significantly from period to period. Reductions in our order backlog could negatively impact our future results of operations.

We evaluate our order backlog at least quarterly to determine if the orders continue to meet our criteria for inclusion in order backlog. We may adjust our reported order backlog to account for any changes, including those arising from continued customer intent and ability to fulfill order, supply base capacity, and changes in our ability, or the methodology used, to determine whether an order is likely to be completed. We cannot assure that our order backlog will result in revenue on a timely basis or at all, or that any cancelled contracts will be replaced.

As a result, the order backlog may not be indicative of future sales and can vary significantly from period to period. In addition, it is possible that the methodology for determining the order backlog may not be comparable to methods used by other companies.

The integration of businesses or assets we have acquired or may acquire in the future involves challenges that could disrupt our business and harm our financial condition.

As part of our growth strategy, we have pursued and expect we will continue to selectively pursue acquisitions of businesses or assets in order to diversify, expand our capabilities, enter new markets, or increase our market share. Integrating any newly acquired business or assets can be expensive and can require a great deal of management time and other resources. We cannot guarantee that we will be able to identify attractive acquisition targets or assets. If we are unable to successfully integrate the newly acquired businesses with our existing business, we may not realize the synergies we expect from the acquisition and our business and results of operations may be adversely impacted.

Re-configuration or relocation of our production operations could negatively impact our earnings.

We may, from time to time, reconfigure our production lines or relocate production of products between buildings or locations or to new locations to maximize the efficient utilization of our existing production capacity or take advantage of opportunities to increase manufacturing efficiencies. Costs incurred to affect these reconfigurations or relocations may exceed our estimates, and efficiencies gained may be less than anticipated, each of which may have a negative impact on our results of operations and financial position.

Disruptions within our dealer network could adversely affect our business.

We rely, for certain of our products, on a network of independent dealers to market, deliver, provide training for, and service our products to and for customers. Our business is influenced by our ability to initiate and manage new and existing relationships with dealers.

From time to time, we or an individual dealer may choose to terminate the relationship, or the dealership could face financial difficulty leading to failure or difficulty in transitioning to new ownership. In addition, our competitors could engage in a strategy to attempt to acquire or convert our dealers to carry their products. We do not believe our business is dependent on any single dealer, the loss of which would have a sustained material adverse effect upon our business.

However, disruption of dealer coverage within a specific local market could have an adverse impact on our business within the affected market. The loss or termination of a significant number of dealers could cause difficulties in marketing and distributing our products and have an adverse effect on our business, operating results or financial condition. In the event that a dealer in a strategic market experiences financial difficulty, we may choose to provide financial support such as extending credit to a dealership, reducing the risk of disruption, but increasing our financial exposure.

We may not be able to successfully implement and manage our growth strategy.

Our growth strategy includes expanding existing market share through product innovation, continued expansion into industrial and global markets and merger or acquisition related activities. We believe our future success depends in part on our research and development and engineering efforts, our ability to manufacture or source the products and customer acceptance of our products. As it relates to new markets, our success also depends on our ability to create and implement local supply chain, sales and distribution strategies to reach these markets.

The potential inability to successfully implement and manage our growth strategy could adversely affect our business and our results of operations. The successful implementation of our growth strategy will depend, in part, on our ability to integrate operations with acquired companies.

Our efforts to grow our business in emerging markets are subject to all of these risks plus additional, unique risks. In certain markets, the legal and political environment can be unstable and uncertain which could make it difficult for us to compete successfully and could expose us to liabilities.

We also make investments in new business development initiatives which could have a relatively high failure rate. We limit our investments in these initiatives and establish governance procedures to contain the associated risks, but losses could result and may be material. Our growth strategy also may involve acquisitions, joint venture alliances and additional arrangements of distribution. We may not be able to enter into acquisitions or joint venture arrangements on acceptable terms, and we may not successfully integrate these activities into our operations. We also may not be successful in implementing new distribution channels, and changes could create discord in our existing channels of distribution.

Increased costs, including costs of raw materials, component parts and labor costs, potentially impacted by changes in labor rates and practices, disruptions in supply chains and/or new or increased tariffs or similar restrictions, could reduce our operating income.

Our results of operations may be significantly affected by the availability and pricing of manufacturing components and labor, changes in labor rates and practices, and increases in tariffs or similar restrictions on materials we import. Increases in costs of raw materials used in our products could affect the cost of our supply materials and components, as rising steel and aluminum prices as well as increased tariffs have impacted the cost of certain of our manufacturing components. In addition, a growth in popularity of EVs without a significant expansion in battery cell production capacity could result in shortages, which could result in increased materials costs to us and could adversely impact our projected manufacturing and delivery timelines. Although we attempt to mitigate the effect of any escalation in components, labor costs, and tariffs by negotiating with current or new suppliers and by increasing productivity or, where possible, by increasing the sales prices of our products, we cannot be certain that we will be able to do so without it having an adverse impact on the competitiveness of our products and, therefore, our sales volume. If we cannot successfully offset increases in our manufacturing costs, this could have a material adverse impact on our margins, operating income and cash flows. Our profit margins may decrease if prices of purchased component parts, labor rates, and/or tariffs increase, and we are unable to pass on those increases to our customers.

Implementing new information systems could interfere with our business or operations.

We are in the process of implementing new information systems infrastructure and applications that impact multiple locations. These projects require significant investment of capital and human resources, the re-engineering of many processes of our business, and the attention of many employees and managers who would otherwise be focused on other aspects of our business. Should the systems not be implemented successfully, we may incur impairment charges that could materially impact our financial results. If the systems do not perform in a satisfactory manner once implementation is complete, our business and operations could be disrupted and our results of operations negatively affected, including our ability to report accurate and timely financial results.

Our EVs will rely on software and hardware that is highly technical, and if these systems contain errors, bugs, vulnerabilities, or design defects, or if we are unsuccessful in addressing or mitigating technical limitations in our systems, our EV business could be adversely affected.

Our EVs will rely on software and hardware that is highly technical and complex and will require modification and updates over the life of the vehicles. Our software and hardware may contain errors, bugs, vulnerabilities or design defects, and our systems are subject to certain technical limitations that may compromise our ability to meet our objectives. Some errors, bugs, vulnerabilities, or design defects inherently may be difficult to detect and may only be discovered after the product has been released. Although we will attempt to remedy any issues we observe in our vehicles effectively and rapidly, such efforts may not be timely, may hamper production or may not be to the satisfaction of our customers.

If we are unable to prevent or effectively remedy errors, bugs, vulnerabilities or defects in our software and hardware, or fail to deploy updates to our software properly, we would suffer damage to our reputation, loss of customers, loss of revenue or liability for damages, any of which could adversely affect our business, prospects, financial condition, results of operations, and cash flows.

There are complex software and technology systems that need to be developed by us and in coordination with vendors and suppliers to reach mass production for our EVs, and there can be no assurance such systems will be successfully developed or integrated.

Our EVs and EV operations will use a substantial amount of complex third-party and in-house software and hardware. The development and integration of such advanced technologies are inherently complex, and we will need to coordinate with our vendors and suppliers to reach mass production for our EVs. Defects and errors may be revealed over time and our control over the performance of third-party services and systems may be limited. Thus, our potential inability to develop and integrate the necessary software and technology systems may adversely affect our EV business.

We rely on third-party suppliers to develop a number of emerging technologies for use in our EVs, including battery technology and the use of different battery cell chemistries. Certain of these technologies and chemistries are not today, and may not ever be, commercially viable. There can be no assurances that our suppliers will be able to meet the technological requirements, production timing, and volume requirements to support our business plan. Furthermore, if we experience delays by our third-party suppliers, we could experience delays in delivering on our timelines. In addition, the technology may not comply with the cost, performance useful life, and warranty characteristics we anticipate in our business plan. As a result, our business plan could be significantly impacted and we may incur significant liabilities under warranty claims which could materially and adversely affect our business, prospects, financial condition, results of operations, and cash flows.

Our EVs will make use of lithium-ion battery cells, which, if not appropriately managed and controlled, have been observed to catch fire or vent smoke and flame.

The battery packs within our EVs will make use of lithium-ion cells. If not properly managed or subject to environmental stresses, lithium-ion cells can rapidly release the energy they contain by venting smoke and flames in a manner that can ignite nearby materials as well as other lithium-ion cells. While the battery pack is designed to contain any single cell’s release of energy without spreading to neighboring cells, a field or testing failure of battery packs in our vehicles could occur, which could result in bodily injury or death and could subject us to lawsuits, field actions (including product recalls), or redesign efforts, all of which would be time consuming and expensive and could harm our brand image. Also, negative public perceptions regarding the suitability of lithium-ion cells for automotive applications, the social and environmental impacts of mineral mining or procurement associated with the constituents of lithium-ion cells, or any future incident involving lithium-ion cells, such as a vehicle or other fire, could materially and adversely affect our reputation and business, prospects, financial condition, results of operations, and cash flows.

Disruption of our supply base could affect our ability to obtain component parts.

We increasingly rely on component parts from global sources in order to manufacture our products. Disruption of this supply base due to international political events (including the conflict between Russia and Ukraine), natural disasters or adverse weather conditions (including any disasters or weather conditions caused by climate change), the COVID-19 pandemic, or other factors could affect our ability to obtain component parts at acceptable prices, or at all, and have a negative impact on our sales, results of operations and financial position.

When we introduce new products, we may incur expenses that we did not anticipate, such as recall expenses, resulting in reduced earnings.

The introduction of new products is critical to our future success. We have additional costs when we introduce new products, such as initial labor or purchasing inefficiencies, but we may also incur unexpected expenses. For example, we may experience unexpected engineering or design issues that will force a recall of a new product or increase production costs of the product above levels needed to ensure profitability. In addition, we may make business decisions that include offering incentives to stimulate the sales of products not adequately accepted by the market, or to stimulate sales of older or less marketable products. The costs resulting from these types of problems could be substantial and have a significant adverse effect on our earnings.

We depend on a small group of suppliers for some of our components, and the loss of any of these suppliers could affect our ability to obtain components at competitive prices, which would decrease our sales or earnings.

Most chassis and specialty vehicle commodity components are readily available from a variety of sources. However, a few proprietary or specialty components are produced by a small group of suppliers.

In addition, we generally do not purchase chassis for our delivery vehicles. Rather, we accept shipments of vehicle chassis owned by dealers or end-users for the purpose of installing and/or manufacturing our specialized truck bodies on such chassis. There are four primary sources for commercial chassis, and we have established relationships with all major chassis manufacturers.

Changes in our relationships with these suppliers, shortages, production delays, their ability to secure components required for chassis production or work stoppages by the employees of such suppliers could have a material adverse effect on our ability to timely manufacture our products and secure sales. If we cannot obtain an adequate supply of components or commercial chassis, this could result in a decrease in our sales and earnings.

Our business could be adversely affected by the decision of our employees to unionize.

Currently, none of our U.S. employees are represented by a collective bargaining agreement. If in the future our employees decide to unionize, this would increase our operating costs and potentially force us to alter the way we operate causing an adverse effect on our operating results.

The ability to hire or retain management and other key personnel is critical to our continued success, and the loss of or inability to hire such personnel could have a material adverse effect on our business, financial condition and results of operations.

Our ability to sustain and grow our business requires us to hire, retain and develop a highly skilled and diverse management team and workforce. Overall, there is intense competition for qualified and skilled employees. As all key personnel devote their full time to our business, the loss of any member of our management team, or other key persons, or the inability to hire key persons, could have an adverse effect on us. If we lose key members of our senior management team or are unable to effect successful transitions from one executive to another as part of our succession plan, we may not be able to effectively manage our current operations or meet ongoing and future business challenges, and this could have a material adverse effect on our business, financial condition and results of operations.

Risks associated with international sales and contracts could have a negative effect on our business.

In 2022, 2021, and 2020, we derived 0.7%, 1.2%, and 1.4% of our revenue from sales to, or related to, end customers outside the United States. We face numerous risks associated with conducting international operations, any of which could negatively affect our financial performance, including changes in foreign country regulatory requirements, the strength of the U.S. dollar compared to foreign currencies, import/export restrictions, the imposition of foreign tariffs and other trade barriers and disruptions in the shipping of exported products.

Additionally, as a public company, we are subject to the Foreign Corrupt Practices Act, which may place us at a competitive disadvantage to foreign companies that are not subject to similar regulations.

Changes in the method of determining London Interbank Offered Rate (LIBOR), or the replacement of LIBOR with an alternative rate, may adversely affect interest charged on our outstanding debt.

The interest rate charged on our outstanding borrowings pursuant to our credit facility is currently based on LIBOR, as described in “Note 13 – Debt” below. On July 27, 2017, the Financial Conduct Authority in the U.K. announced that it would phase out LIBOR by the end of 2021. On November 30, 2020, the ICE Benchmark Administration Limited (ICE) announced plans to delay the phase out of LIBOR to June 30, 2023. The U.S. Federal Reserve is considering replacing U.S. dollar LIBOR with a newly created index called the Secured Overnight Funding Rate (SOFR), a broad measure of the cost of borrowing cash overnight collateralized by U.S. Treasury securities. Our credit facility provides for the transition to a replacement for LIBOR, and it also provides for an alternative to LIBOR. When LIBOR ceases to exist, our interest expense may increase. It is also possible that the overall financing market may be disrupted as a result of the phase-out or replacement of LIBOR with SOFR or any other reference rate. Increased interest expense and/or disruption in the financial market could have a material adverse effect on our business, financial condition, or results of operations.

More General Risks Applicable to Our Industry

General economic, market, and/or political conditions, whether on a global, national, or more regional scale, could have a negative effect on our business.

Acts of terrorism, armed conflicts, natural disasters (including those caused by climate change), budget shortfalls, cyber events, civil unrest, governmental actions, and epidemics have in the past and could in the future create significant uncertainties that may have material and adverse effects on consumer demand, shipping and transportation, the availability of manufacturing components, commodity prices and our ability to engage in overseas markets as tariffs are implemented. An economic recession, whether resulting from one of these events or others, would have a material adverse impact on our financial condition and results of operations.

If there is a rise in the frequency and size of product liability, warranty and other claims against us, including wrongful death claims, our business, results of operations and financial condition may be harmed.

We are frequently subject, in the ordinary course of business, to litigation involving product liability and other claims, including wrongful death claims, related to personal injury and warranties. We insure our product liability claims in the commercial insurance market. We cannot be certain that our insurance coverage will be sufficient to cover all future claims against us. Any increase in the frequency and size of these claims, as compared to our experience in prior years, may cause the premiums that we are required to pay for such insurance to rise significantly. It may also increase the amounts we pay in punitive damages, which may not be covered by our insurance. In addition, a major product recall or increased levels of warranty claims could have a material adverse effect on our results of operations.

Changes to laws and regulations governing our business could have a material impact on our operations.

Our manufactured products and the industries in which we operate are subject to extensive federal and state regulations. Changes to any of these regulations or the implementation of new regulations could significantly increase the costs of manufacturing, purchasing, operating or selling our products and could have a material adverse effect on our results of operations. Our failure to comply with present or future regulations could result in fines, potential civil and criminal liability, suspension of sales or production, or cessation of operations.

Certain U.S. tax laws currently afford favorable tax treatment for financing the purchase of recreational vehicles that are used as the equivalent of second homes. These laws and regulations have historically been amended frequently, and it is likely that further amendments and additional regulations will be applicable to us and our products in the future. Amendments to these laws and regulations and the implementation of new regulations could have a material adverse effect on our results of operations.

Our operations are subject to a variety of federal and state environmental regulations relating to noise pollution and the use, generation, storage, treatment, emission and disposal of hazardous materials and wastes. Our failure to comply with present or future regulations could result in fines, potential civil and criminal liability, suspension of production or operations, alterations to the manufacturing process, costly cleanup or capital expenditures. Climate change regulations at the federal, state or local level could require us to change our manufacturing processes or product portfolio or undertake other activities that may require us to incur additional expense, which may be material.

Our vehicles are subject to motor vehicle safety standards, and the failure to satisfy such mandated safety standards could have a material adverse effect on our business, financial condition, results of operations, and cash flows.

All vehicles sold must comply with international, federal, and state motor vehicle safety standards. In the United States, vehicles that meet or exceed all federally mandated safety standards are self-certified by the manufacturer under the federal regulations. Rigorous testing and the use of approved materials and equipment are among the requirements for achieving federal certification. Other jurisdictions outside the United States require us to meet Type Approval requirements proving to regulators that our vehicles meet those relevant safety standards in effect in those countries. Failure by us to maintain compliance of our current vehicles or obtain certification of compliance for any future vehicle, including future EV models, with motor vehicle safety standards in the United States, Canada or other jurisdictions could have a material adverse effect on our business, prospects, financial condition, results of operations, and cash flows.

Our operating results may fluctuate significantly on a quarter-to-quarter basis.

Our quarterly operating results depend on a variety of factors including the timing and volume of orders, the completion of product inspections and acceptance by our customers, and various restructuring initiatives that may be undertaken from time to time. As an example, our Fleet Vehicles and Services segment experiences seasonality whereby product shipments in the first and fourth quarters are generally lower than other quarters as a result of the busy holiday delivery operations experienced by some of its largest customers. Accordingly, our financial results may be subject to significant and/or unanticipated quarter-to-quarter fluctuations.

Our businesses are cyclical, and this can lead to fluctuations in our operating results.

The industries in which we operate are highly cyclical and there can be substantial fluctuations in our manufacturing, shipments and operating results, and the results for any prior period may not be indicative of results for any future period. Companies within these industries are subject to volatility in operating results due to external factors such as economic, demographic and political changes. Factors affecting the manufacture of chassis, specialty vehicles, delivery vehicles and other of our products include but are not limited to:

| ● |

Commodity prices; |

| ● |

Fuel availability and prices. |

| ● |

Unemployment trends; |

| ● |

International tensions and hostilities; |

| ● |

General economic conditions; |

| ● |

Various tax incentives; |

| ● |

Strength of the U.S. dollar compared to foreign currencies; |

| ● |

Overall consumer confidence and the level of discretionary consumer spending; |

| ● |

Dealers’ and manufacturers’ inventory levels; and |

| ● |

Interest rates and the availability of financing. |

Economic, legal and other factors could impact our customers’ ability to pay accounts receivable balances due from them.

In the ordinary course of business, customers are granted terms related to the sale of goods and services delivered to them. These terms typically include a period between when the goods and services are tendered for delivery to the customer and when the customer needs to pay for these goods and services. The amounts due under these payment terms are listed as accounts receivable on our balance sheet. Prior to collection of these accounts receivable, our customers could encounter drops in sales, unexpected increases in expenses, or other factors which could impact their ability to continue as a going concern and which could affect the collectability of these amounts. Writing off uncollectible accounts receivable could have a material adverse effect on our earnings and cash flow as we have major customers with material accounts receivable balances at any given time.

Our business operations could be disrupted if our information technology systems fail to perform adequately or experience a security breach.

We rely on our information technology systems to effectively manage our business data, communications, supply chain, product engineering, manufacturing, accounting and other business processes. If these systems are damaged, cease to function properly or are subject to a cyber-security breach such as ransomware, phishing, infection with viruses or intentional attacks aimed at theft or destruction of sensitive data, we may suffer an interruption in our ability to manage and operate the business, and our results of operations and financial condition may be adversely affected.