UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| (Mark One) | |

| x | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| ¨ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2017

Commission File No. 1-8726

RPC, INC.

| Delaware (State of Incorporation) |

58-1550825 (I.R.S. Employer Identification No.) |

2801 BUFORD HIGHWAY NE, SUITE 520

ATLANTA, GEORGIA 30329

(404) 321-2140

| Securities registered pursuant to Section 12(b) of the Act: | |

| Title of each class COMMON STOCK, $0.10 PAR VALUE |

Name of each exchange on which registered NEW YORK STOCK EXCHANGE |

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes ¨ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every interactive data file required to be submitted and posted pursuant to Rule 405 of Regulations S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨ Emerging growth company ¨

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

The aggregate market value of RPC, Inc. Common Stock held by non-affiliates on June 30, 2017, the last business day of the registrant’s most recently completed second fiscal quarter, was $1,178,253,000 based on the closing price on the New York Stock Exchange on June 30, 2017 of $20.21 per share.

RPC, Inc. had 216,838,107 shares of Common Stock outstanding as of February 16, 2018.

Documents Incorporated by Reference

Portions of the Proxy Statement for the 2018 Annual Meeting of Stockholders of RPC, Inc. are incorporated by reference into Part III, Items 10 through 14 of this report.

PART I

Throughout this report, we refer to RPC, Inc., together with its subsidiaries, as “we,” “us,” “RPC” or “the Company.”

Forward-Looking Statements

Certain statements made in this report that are not historical facts are “forward-looking statements” under the Private Securities Litigation Reform Act of 1995. Such forward-looking statements may include, without limitation, statements that relate to our business strategy, plans and objectives, and our beliefs and expectations regarding future demand for our equipment and services and other events and conditions that may influence the oilfield services market and our performance in the future. Forward-looking statements made elsewhere in this report include without limitation statements regarding natural gas prices, production levels and drilling activities; our belief that oil-directed drilling will continue to represent the majority of the total drilling rig activity; our belief that the long-term demand outlook for natural gas is favorable and that natural gas-directed drilling will increase over the long-term; our continued belief in the long-term growth opportunities for our business; our expectation to continue to focus on the development of international business opportunities in current and other international markets; our expectations regarding acquisition targets in our industry; the adequacy of our insurance coverage; the impact of lawsuits, legal proceedings and claims on our business and financial condition; our expectations regarding payment of cash dividends to common stockholders; our belief that industry factors will continue to depress natural gas directed drilling activity during the near-term; our belief that U.S. oilfield activity will continue to increase during the near term; our belief that recovering commodity prices will have moderately positive implications for our near-term activity levels; our belief that the U.S. domestic rig count will continue to recover moderately during the near term; our belief regarding potential revenue related to uncompleted wells; our expectations regarding competition in our market; our ability to maintain sufficient liquidity and a conservative capital structure; our expectations about contributions to the defined benefit pension plan in 2018; our ability to fund capital requirements in the future; the estimated amount of our capital expenditures and contractual obligations for future periods; our expectations regarding the costs of skilled labor and many of the raw materials used in providing our services; estimates made with respect to our critical accounting policies; the effect of new accounting standards; and the effect of the changes in foreign exchange rates on our consolidated results of operations or financial condition.

The words “may,” “will,” “expect,” “believe,” “anticipate,” “project,” “estimate,” and similar expressions generally identify forward-looking statements. Such statements are based on certain assumptions and analyses made by our management in light of its experience and its perception of historical trends, current conditions, expected future developments and other factors it believes to be appropriate. We caution you that such statements are only predictions and not guarantees of future performance and that actual results, developments and business decisions may differ from those envisioned by the forward-looking statements. See “Risk Factors” contained in Item 1A. for a discussion of factors that may cause actual results to differ from our projections.

Item 1. Business

Organization and Overview

RPC is a Delaware corporation originally organized in 1984 as a holding company for several oilfield services companies and is headquartered in Atlanta, Georgia.

RPC provides a broad range of specialized oilfield services and equipment primarily to independent and major oil and gas companies engaged in the exploration, production and development of oil and gas properties throughout the United States, including the southwest, mid-continent, Gulf of Mexico, Rocky Mountain and Appalachian regions, and in selected international markets. RPC acts as a holding company for the following legal entity groupings: Cudd Energy Services, Thru Tubing Solutions and Patterson Services. Selected overhead including centralized support services and regulatory compliance are classified as Corporate. RPC is further organized into Technical Services and Support Services which are its operating segments. As of December 31, 2017, RPC had approximately 3,500 employees.

| 2 |

Business Segments

RPC manages its business as either services offered on the well site with equipment and personnel (Technical Services) or services and equipment offered off the well site (Support Services). The businesses under Technical Services generate revenues based on equipment, personnel operating the equipment and the materials utilized to provide the service. They are all managed, analyzed and reported based on the similarities of the operational characteristics and costs associated with providing the service. The businesses under Support Services are primarily able to generate revenues through equipment or services offered off the well site. During 2017, less than two percent of RPC’s consolidated revenues were generated from offshore operations in the U.S. Gulf of Mexico. We also estimate that 70 percent of our 2017 revenues were related to drilling and production activities for oil, and 30 percent were related to drilling and production activities for natural gas.

Technical Services include RPC’s oil and gas services that utilize people and equipment to perform value-added completion, production and maintenance services directly to a customer’s well. The demand for these services is generally influenced by customers’ decisions to invest capital toward initiating production in a new oil or natural gas well, improving production flows in an existing formation, or to address well control issues. This operating segment consists primarily of pressure pumping, downhole tools, coiled tubing, snubbing, nitrogen, well control, wireline and fishing. Customers include major multi-national and independent oil and gas producers, and selected nationally owned oil companies. The services offered under Technical Services are high capital and personnel intensive businesses. The common drivers of operational and financial success of these services include diligent equipment maintenance, strong logistical processes, and appropriately trained personnel who function well in a team environment. The Company considers all of these services to be closely integrated oil and gas well servicing businesses, and makes resource allocation and performance assessment decisions based on this operating segment as a whole across these various services. The principal markets for this business segment include the United States, including the southwest, mid-continent, Gulf of Mexico, Rocky Mountain and Appalachian regions, and selected international markets.

Support Services include all of the services that provide (i) equipment offered off the well site without RPC personnel and (ii) services that are provided in support of customer operations off the well site such as classroom and computer training, and other consulting services. The primary drivers of operational success for services and equipment provided off the well site without RPC personnel are offering safe, high quality and in-demand equipment appropriate for the well design characteristics. The drivers of operational success for the other Support Services relate to meeting customer needs off the well site and competitive marketing of such services. The equipment and services offered include rental tools, drill pipe and related tools, pipe handling, pipe inspection and storage services, and oilfield training and consulting services. The demand for these services tends to be influenced primarily by customer drilling-related activity levels. The principal markets for this segment include the United States, including the Gulf of Mexico, mid-continent, Rocky Mountain and Appalachian regions and project work in selected international locations in the last three years, including primarily Canada, Latin America and the Middle East. Customers primarily include domestic operations of independent oil and gas producers and major multi-nationals and selected nationally owned oil companies.

A brief description of the primary services conducted within each of the operating segments follows:

Technical Services

Pressure Pumping. Pressure pumping services, which accounted for approximately 62 percent of 2017 revenues, 46 percent of 2016 revenues and 54 percent of 2015 revenues are provided to customers throughout Texas, and the mid-continent and Rocky Mountain regions of the United States. We primarily provide these services to customers in order to enhance the initial production of hydrocarbons in formations that have low permeability. Pressure pumping services involve using complex, truck or skid-mounted equipment designed and constructed for each specific pumping service offered. The mobility of this equipment permits pressure pumping services to be performed in varying geographic areas. Principal materials utilized in pressure pumping operations include fracturing proppants, acid and bulk chemical additives. Generally, these items are available from several suppliers, and the Company utilizes more than one supplier for each item. Pressure pumping services offered include:

| 3 |

Fracturing — Fracturing services are performed to stimulate production of oil and natural gas by increasing the permeability of a formation. Fracturing is particularly important in shale formations, which have low permeability, and unconventional completion, because the formation containing hydrocarbons is not concentrated in one area and requires multiple fracturing operations. The fracturing process consists of pumping fluid gel and sometimes nitrogen into a cased well at sufficient pressure to fracture the formation at desired locations and depths. Sand, ceramics, or synthetic materials, which are often coated with a material to increase their resistance to crushing, are pumped into the fracture. When the pressure is released at the surface, the fluid gel returns to the well surface, but the proppant remains in the fracture, thus keeping it open so that oil and natural gas can flow through the fracture into the production tubing and ultimately to the well surface. In some cases, fracturing is performed in formations with a high amount of carbonate rock by an acid solution pumped under pressure without a proppant or with small amounts of proppant.

Acidizing — Acidizing services are also performed to stimulate production of oil and natural gas, but they are used in wells that have undergone formation damage due to the buildup of various materials that block the formation. Acidizing entails pumping large volumes of specially formulated acids into reservoirs to dissolve barriers and enlarge crevices in the formation, thereby eliminating obstacles to the flow of oil and natural gas. Acidizing services can also enhance production in limestone formations. Acid is also frequently used in the beginning of a fracturing operation.

Downhole Tools. Thru Tubing Solutions (“TTS”) accounted for approximately 19 percent of 2017 revenues, 23 percent of 2016 revenues and 18 percent of 2015 revenues. TTS provides services and proprietary downhole motors, fishing tools and other specialized downhole tools and processes to operators and service companies in drilling and production operations, including casing perforation and bridge plug drilling at the completion stage of an oil or gas well. The services that TTS provides are especially suited for unconventional drilling and completion activities. TTS’ experience providing reliable tool services allows it to work in a pressurized environment with virtually any coiled tubing unit or snubbing unit.

Coiled Tubing. Coiled tubing services, which accounted for approximately seven percent of revenues in 2017, 10 percent of revenues in 2016 and nine percent of revenues in 2015, involve the injection of coiled tubing into wells to perform various applications and functions for use principally in well-servicing operations and to facilitate completion of horizontal wells. Coiled tubing is a flexible steel pipe with a diameter of less than four inches manufactured in continuous lengths of thousands of feet and wound or coiled around a large reel. It can be inserted through existing production tubing and used to perform workovers without using a larger, costlier workover rig. Principal advantages of employing coiled tubing in a workover operation include: (i) not having to “shut-in” the well during such operations, (ii) the ability to reel continuous coiled tubing in and out of a well significantly faster than conventional pipe, (iii) the ability to direct fluids into a wellbore with more precision, and (iv) enhanced access to remote or offshore fields due to the smaller size and mobility of a coiled tubing unit compared to a workover rig. Increasingly, coiled tubing units are also used to support completion activities in directional and horizontal wells. Such completion activities usually require multiple entrances in a wellbore in order to complete multiple fractures during a pressure pumping operation. A coiled tubing unit can accomplish this type of operation because its flexibility allows it to be steered in a direction other than vertical, which is necessary in this type of wellbore. At the same time, the strength of the coiled tubing string allows various types of tools or motors to be conveyed into the well effectively. The uses for coiled tubing in directional and horizontal wells have been enhanced by improved fabrication techniques and higher-diameter coiled tubing which allows coiled tubing units to be used effectively over greater distances, thus allowing them to function in more of the completion activities currently taking place in the U.S. domestic market. There are several manufacturers of flexible steel pipe used in coiled tubing services, and the Company believes that its sources of supply are adequate.

Snubbing. Snubbing (also referred to as hydraulic workover services), which accounted for approximately two percent of revenues in 2017 and three percent of revenues in 2016 and 2015, involves using a hydraulic workover rig that permits an operator to repair damaged casing, production tubing and downhole production equipment in a high-pressure environment. A snubbing unit makes it possible to remove and replace downhole equipment while maintaining pressure on the well. Customers benefit because these operations can be performed without removing the pressure from the well, which stops production and can damage the formation, and because a snubbing unit can perform many applications at a lower cost than other alternatives. Because this service involves a very hazardous process that entails high risk, the snubbing segment of the oil and gas services industry is limited to a relative few operators who have the experience and knowledge required to perform such services safely and efficiently. Increasingly, snubbing units are used for unconventional completions at the outer reaches of long wellbores which cannot be serviced by coiled tubing because coiled tubing has a more limited range than drill pipe conveyed by a snubbing unit.

| 4 |

Nitrogen. Nitrogen accounted for approximately two percent of revenues in 2017, five percent of revenues in 2016 and four percent of revenues in 2015. There are a number of uses for nitrogen, an inert, non-combustible element, in providing services to oilfield customers and industrial users outside of the oilfield. For our oilfield customers, nitrogen can be used to clean drilling and production pipe and displace fluids in various drilling applications. Increasingly, it is used as a displacement medium to increase production in older wells in which production has depleted. It also can be used to create a fire-retardant environment in hazardous blowout situations and as a fracturing medium for our fracturing service. In addition, nitrogen can be complementary to our snubbing and coiled tubing services, because it is a non-corrosive medium and is frequently injected into a well using coiled tubing. Nitrogen is complementary to our pressure pumping service as well, because foam-based nitrogen stimulation is appropriate in certain sensitive formations in which the fluids used in fracturing or acidizing would damage a customer's well.

For non-oilfield industrial users, nitrogen can be used to purge pipelines and create a non-combustible environment. RPC stores and transports nitrogen and has a number of pumping unit configurations that inject nitrogen in its various applications. Some of these pumping units are set up for use on offshore platforms or inland waters. RPC purchases its nitrogen in liquid form from several suppliers and believes that these sources of supply are adequate.

Well Control. Cudd Energy Services specializes in responding to and controlling oil and gas well emergencies, including blowouts and well fires, domestically and internationally. In connection with these services, Cudd Energy Services, along with Patterson Services, has the capacity to supply the equipment, expertise and personnel necessary to restore affected oil and gas wells to production. During the past several years, the Company has responded to numerous well control situations in the domestic U.S. oilfield and in various international locations.

The Company’s professional firefighting staff has many years of aggregate industry experience in responding to well fires and blowouts. This team of experts responds to well control situations where hydrocarbons are escaping from a wellbore, regardless of whether a fire has occurred. In the most critical situations, there are explosive fires, the destruction of drilling and production facilities, substantial environmental damage and the loss of hundreds of thousands of dollars per day in well operators’ production revenue. Since these events ordinarily arise from equipment failures or human error, it is impossible to predict accurately the timing or scope of this work. Additionally, less critical events frequently occur in connection with the drilling of new wells in high-pressure reservoirs. In these situations, the Company is called upon to supervise and assist in the well control effort so that drilling operations can resume as promptly as safety permits.

Wireline Services. Wireline is classified into two types of services: slick or braided line and electric line. In both, a spooled wire is unwound and lowered into a well, conveying various types of tools or equipment. Slick or braided line services use a non-conductive line primarily for jarring objects into or out of a well, as in fishing or plug-setting operations. Electric line services lower an electrical conductor line into a well allowing the use of electrically-operated tools such as perforators, bridge plugs and logging tools. Wireline services can be an integral part of the plug and abandonment process near the end of the life cycle of a well.

Pump Down Services. Pump down services are an integral part of the well completion process and are critical in multiple-stage, unconventional well completions which use various types of bridge plugs and perforation techniques. Pump down services use fluids and low-capacity pressure pumping equipment, and work in coordination with wireline services, to place completion equipment at the desired location in a well bore. This process is repeated for each stage, moving from the most distant end of the wellbore to the end that is closest to the wellhead.

Fishing. Fishing involves the use of specialized tools and procedures to retrieve lost equipment from a well drilling operation and producing wells. It is a service required by oil and gas operators who have lost equipment in a well. Oil and natural gas production from an affected well typically declines until the lost equipment can be retrieved. In some cases, the Company creates customized tools to perform a fishing operation. The customized tools are maintained by the Company after the particular fishing job for future use if a similar need arises.

Support Services

Rental Tools. Rental tools accounted for approximately two percent of revenues in 2017, three percent of revenues in 2016 and four percent of revenues in 2015. The Company rents specialized equipment for use with onshore and offshore oil and gas well drilling, completion and workover activities. The drilling and subsequent operation of oil and gas wells generally require a variety of equipment. The equipment needed is in large part determined by the geological features of the production zone and the size of the well itself. As a result, operators and drilling contractors often find it more economical to supplement their tool and tubular assets with rental items instead of owning a complete set of assets. The Company’s facilities are strategically located to serve the major staging points for oil and gas activities in Texas, the Gulf of Mexico, mid-continent region, Appalachian region and the Rocky Mountains.

| 5 |

Patterson Rental Tools offers a broad range of rental tools including:

| Blowout Preventors | Diverters |

| High Pressure Manifolds and Valves | Drill Pipe |

| Hevi-wate Drill Pipe | Drill Collars |

| Tubing | Handling Tools |

| Production Related Rental Tools | Coflexip® Hoses |

| Pumps | Wear KnotTM Drill Pipe |

Oilfield Pipe Inspection Services, Pipe Management and Pipe Storage. Pipe inspection services include Full Body Electromagnetic and Phased Array Ultrasonic inspection of pipe used in oil and gas wells. These services are provided at both the Company’s inspection facilities and at independent tubular mills in accordance with negotiated sales and/or service contracts. Our customers are major oil companies and steel mills, for which we provide in-house inspection services, inventory management and process control of tubing, casing and drill pipe. Our locations in Channelview, Texas and Morgan City, Louisiana are equipped with large capacity cranes, specially designed forklifts and a computerized inventory system to serve a variety of storage and handling services for both oilfield and non-oilfield customers.

Well Control School. Well Control School provides industry and government accredited training for the oil and gas industry both in the United States and in limited international locations. Well Control School provides training in various formats including conventional classroom training, interactive computer training including training delivered over the internet, and mobile simulator training.

Energy Personnel International. Energy Personnel International provides drilling and production engineers, well site supervisors, project management specialists, and workover and completion specialists on a consulting basis to the oil and gas industry to meet customers’ needs for staff engineering and well site management.

Refer to Note 12 in the Notes to the Consolidated Financial Statements for additional financial information on our business segments.

Industry

United States. RPC provides its services to its domestic customers through a network of facilities strategically located to serve oil and gas drilling and production activities of its customers in Texas, the Gulf of Mexico, the mid-continent, the southwest, the Rocky Mountains and the Appalachian regions. Demand for RPC’s services in the U.S. tends to be extremely volatile and fluctuates with current and projected price levels of oil and natural gas and activity levels in the oil and gas industry. Customer activity levels are influenced by their decisions about capital investment toward the development and production of oil and gas reserves.

Due to aging oilfields and lower-cost sources of oil internationally, the drilling rig count in the U.S. has declined by approximately 79 percent from its peak in 1981. However, due to continuously enhanced rig and other completion technologies, more wells are drilled during periods of strong industry activity, and these wells are increasingly productive. For these reasons, the domestic production of natural gas rose to record levels in the third quarter of 2015, and domestic production of crude oil in the third quarter of 2015 reached its highest level since the third quarter of 1971. With the decline in domestic drilling and completion activities beginning in early 2015, domestic production of both natural gas and oil began to decline during the third and fourth quarters of 2015, although production continues to remain high in comparison to historical levels. Oil and gas industry activity levels have historically been volatile, experiencing multiple cycles, including six down cycle troughs between 1981 and 2016, with May 2016 marking the lowest U.S. domestic rig count in U.S. oilfield history. The rig count during the peak of the most recent cycle occurred at the end of the third quarter of 2014, and began to decline sharply during the fourth quarter of 2014. The rig count continued to decline in 2015 and 2016, until June of 2016 when it stabilized and began to increase. Early in 2018, the rig count had recovered by approximately 141 percent from the historical low set during the second quarter of 2016, but was still approximately 51 percent lower than the cyclical peak in the third quarter of 2014.

Because of the increased efficiency of drilling rigs, the Company also monitors well completions in the U.S. domestic oilfield. Well completions are particularly important to RPC because the majority of its services are utilized during the completion stage of an oil or gas well’s life cycle, so they are an important indicator of the demand for RPC’s services. From a cyclical peak of 21,355 wells completed during 2014, well completions fell by 62.3 percent to 8,060 in 2016. During 2017, well completions in the U.S. increased by 39.9 percent compared to 2016, but were still 47.2 percent lower than 2014 well completions.

| 6 |

The fluctuations in domestic drilling activity since the third quarter of 2014 peak are consistent with global supply of and demand for oil, the domestic supply of and demand for natural gas, U.S. domestic storage levels of oil and natural gas, fluctuations in the value of the U.S. dollar on world currency markets, and projected near-term economic growth. During 2015 and into the first quarter of 2016, the price of oil fell by approximately 78 percent from the cyclical peak in the third quarter of 2014. From its low price in early 2016, the price of oil had risen approximately 122 percent by early in the first quarter of 2018. RPC believes that the increase in the price of oil since early 2016 is due to increasing global demand, the moderation of global supply, and the belief that the actions of the Organization of the Petroleum Exporting Countries (OPEC) to moderate that cartel’s production will be effective. The price of natural gas fell during this time as well, declining by approximately 42 percent from the beginning of 2015 to the second quarter of 2016. Early in the first quarter of 2018, however, the price of natural gas had risen by approximately 122 percent from the low recorded in the second quarter of 2016, and was approximately 10 percent higher than its price at the same time in 2017. Early in 2018, the price of oil was high enough to encourage increased drilling and production activity, but the price of natural gas had not reached levels that were adequate to encourage natural gas-directed drilling activity in the U.S. domestic oilfield. In addition to oil and natural gas, the price of natural gas liquids is a determinant of our customers’ activity levels, since it is produced in many of the shale resource plays which also produce oil, and production of various natural gas liquids has increased to a level comparable to that of natural gas. During 2017 the average price of natural gas liquids increased by approximately 58 percent compared to 2016. Early in the first quarter of 2018, the price of natural gas liquids had increased by approximately 18 percent compared to the average price in 2017. The fluctuations in the prices of these commodities, and in particular, the extreme volatility in the price of oil, significantly impact RPC’s financial results.

From 2001 to 2009, gas drilling rigs represented over 80 percent of the drilling rig count. In 2010, the percentage of drilling rigs drilling for natural gas began to decline, and by early in the first quarter of 2015 had fallen to approximately 18 percent of total drilling activity. In absolute terms, the natural gas drilling rig count in the third quarter of 2016 was the lowest natural gas drilling rig count ever recorded. Early in the first quarter of 2018, the natural gas drilling rig count had risen by approximately 124 percent, although it remains very low by historical standards. Although the demand for natural gas has remained stable, the price of natural gas has fallen in recent years due to increased domestic reserves, productivity of new wells, and high associated natural gas production from oil-directed wells. In spite of these unfavorable near-term dynamics, the long-term demand outlook for natural gas is still favorable because, unlike oil, foreign imports of natural gas do not compete with domestic production to a meaningful degree, and for several years, the United States has exported increasing volumes of natural gas to other countries. We anticipate that oil-directed drilling will continue to represent the majority of the total drilling rig count during the near term. Over the long term, we believe that natural gas-directed drilling will increase due to the lack of natural gas production from oil-directed drilling and increased natural gas demand from U.S. exports of natural gas and changes in demand due to increased use of natural gas as a transportation fuel or for other purposes. We continue to believe in the long-term growth opportunities for our business due to the continued high demand for hydrocarbons generally and the growing production of oil in the domestic U.S. market in particular. Furthermore, we note that the techniques used to extract oil and natural gas in the U.S. domestic market increasingly require the types of services that RPC provides to its customers.

Unconventional wells generate a higher demand for RPC’s services because they are difficult and costly to complete. They comprise the majority of U.S. domestic drilling and during the fourth quarter of 2017 and early in the first quarter of 2018, have reached a historical high of approximately 93 percent of total drilling. Because they are drilled through a typically narrow and relatively impermeable formation such as shale, they require additional stimulation when they are completed. Also, many of these formations require high pumping rates of stimulation fluids under high pressures, which in turn require a great deal of pressure pumping horsepower on location to complete the well. Furthermore, since they are not drilled in a straight vertical direction from the Earth’s surface, they require tools and drilling mechanisms that are flexible, rather than rigid, and can be steered once they are downhole. Specifically, these types of wells require RPC’s pressure pumping and coiled tubing services, as well as our downhole tools and services.

International. RPC has historically operated in several countries outside of the United States, and international revenues accounted for approximately four percent of RPC’s consolidated revenues in 2017, seven percent in 2016 and six percent in 2015. RPC’s allocation of growth capital over the last several years have emphasized domestic rather than international expansion because of higher domestic activity levels and expected financial returns. International revenues increased 9.1 percent in 2017 compared to the prior year primarily due to higher customer activity levels in Canada, Argentina, Kuwait and Colombia, partially offset by decreased activity in Gabon and Bolivia. During 2017, RPC provided snubbing services in Gabon. We also provided downhole motors and tools in Argentina, Canada, China and Oman, and rental tools in Bolivia. We continue to focus on the selected development of international opportunities in these and other markets, although we believe that it will continue to be less than ten percent of total revenues in 2018.

| 7 |

RPC provides services to its international customers through branch locations or wholly owned foreign subsidiaries. The international market is prone to political uncertainties, including the risk of civil unrest and conflicts. However, due to the significant investment requirement and complexity of international projects, customers’ drilling decisions relating to such projects tend to be evaluated and monitored with a longer-term perspective with regard to oil and natural gas pricing, and therefore have the potential to be more stable than most U.S. domestic operations. Additionally, the international market is dominated by major oil companies and national oil companies which tend to have different objectives and more operating stability than the typical independent oil and gas producer in the U.S. Predicting the timing and duration of contract work is not possible. Refer to Note 12 in the Notes to Consolidated Financial Statements for further information on our international operations.

Growth Strategies

RPC’s primary objective is to generate excellent long-term returns on investment through the effective and conservative management of its invested capital to generate strong cash flow. This objective continues to be pursued through strategic investments and opportunities designed to enhance the long-term value of RPC while improving market share, product offerings and the profitability of existing businesses. Growth strategies are focused on selected customers and markets in which we believe there exist opportunities for higher growth, customer and market penetration, or enhanced returns achieved through consolidations or through providing proprietary value-added equipment and services. RPC intends to focus on specific market segments in which it believes that it has a competitive advantage and on potential large customers who have a long-term need for our services in markets in which we operate.

RPC seeks to expand its service capabilities through a combination of internal growth, acquisitions, joint ventures and strategic alliances. Historically, we have found that we generate higher financial returns from organic growth with our services and geographical locations in which we have experience. Because of the fragmented nature of the oil and gas services industry, RPC believes a number of acquisition opportunities exist, and we frequently consider such opportunities. We have consummated relatively few acquisitions, however, due to high seller valuation expectations and the risk of integrating acquired businesses into our existing operations. We will continue to consider the acquisitions of existing businesses but will also continue to maintain a conservative capital structure, which may limit our ability to consummate large transactions.

RPC has a revolving credit facility which can be used to fund working capital requirements. The borrowing base for this credit facility is the lesser of $125 million, or a specified percentage of eligible accounts receivable, less the amount of any outstanding letters of credit. There was no outstanding balance on this credit facility as of December 31, 2017. Our capital structure is more conservative than that of many of our peers.

Customers

Demand for RPC’s services and equipment depends primarily upon the number of oil and natural gas wells being drilled, the depth and drilling conditions of such wells, the number of well completions and the level of production enhancement activity worldwide. RPC’s principal customers consist of major and independent oil and natural gas producing companies. During 2017, RPC provided oilfield services to several hundred customers. Of these customers, there were no customers in 2017 or 2016 that accounted for more than 10 percent of revenues.

Sales are generated by RPC’s sales force and through referrals from existing customers. We monitor closely the financial condition of these customers, their capital expenditure plans, and other indications of their drilling and completion activities. Due to the short lead time between ordering services or equipment and providing services or delivering equipment, there is no significant sales backlog in most of our services.

Competition

RPC operates in highly competitive areas of the oilfield services industry. We sell our equipment and services in highly competitive markets, and the revenues and earnings generated are affected by changes in prices for our services, fluctuations in the level of customer activity in major markets, general economic conditions and governmental regulation. RPC competes with many large and small oilfield industry competitors, including the largest integrated oilfield services companies. During the oilfield downturn of 2015 and 2016, a number of smaller oilfield services companies as well as several of our publicly traded peers reduced the scope of their operations or became insolvent. More recently, however, an improving industry environment and the positive outlook on the industry from the financial markets have facilitated the formation of new companies and allowed existing companies to expand their operations. RPC believes that these expanded or newly formed companies will increase competitive pressures during the near term, as they seek to provide services to our existing customers at lower prices, and hire experienced personnel from more established companies such as RPC. Pricing for our services has improved significantly during 2017, but remains below the highest levels experienced during the most recent period of strong industry activity in 2014. RPC believes that the principal competitive factors in the market areas that it serves are product availability and quality of our equipment and raw materials used to provide our services, service quality, reputation for safety and technical proficiency, and price.

| 8 |

The oil and gas services industry includes dominant global competitors including, among others, Halliburton Energy Services Group, a division of Halliburton Company, Baker Hughes, a GE Company, and Schlumberger Ltd. The industry also includes a number of other publicly traded peers whose operations are more similar to RPC, including Basic Energy Services, C&J Energy Services, Keane Group, Inc., Liberty Oilfield Services, Mammoth Energy Services, Inc., NCS Multistage Holdings, Inc., Nine Energy Service, Patterson-UTI Energy, Inc., ProPetro Holding Corporation and Superior Energy Services, as well as numerous smaller, locally owned competitors.

Facilities/Equipment

RPC’s equipment consists primarily of oil and gas services equipment used either in servicing customer wells or provided on a rental basis for customer use. Substantially all of this equipment is Company owned. RPC purchases oilfield service equipment from a limited number of manufacturers. These manufacturers may not be able to meet our requests for timely delivery during periods of high demand which may result in delayed deliveries of equipment and higher prices for equipment.

RPC owns and leases regional and district facilities from which its oilfield services are provided to land-based and offshore customers. RPC’s principal executive offices in Atlanta, Georgia are leased. The Company has two primary administrative buildings, one leased facility in The Woodlands, Texas that includes the Company’s operations, engineering, sales and marketing headquarters, and one owned facility in Houma, Louisiana that includes certain administrative functions. RPC believes that its facilities are adequate for its current operations. For additional information with respect to RPC’s lease commitments, see Note 9 of the Notes to Consolidated Financial Statements.

Governmental Regulation

RPC’s business is affected by state, federal and foreign laws and other regulations relating to the oil and gas industry, as well as laws and regulations relating to worker safety and environmental protection. RPC cannot predict the level of enforcement of existing laws and regulations or how such laws and regulations may be interpreted by enforcement agencies or court rulings, whether additional laws and regulations will be adopted, or the effect such changes may have on it, its businesses or financial condition.

In addition, our customers are affected by laws and regulations relating to the exploration and production of natural resources such as oil and natural gas. These regulations are subject to change, and new regulations may curtail or eliminate our customers’ activities. We cannot determine the extent to which new legislation may impact our customers’ activity levels, and ultimately, the demand for our services.

Intellectual Property

RPC uses several patented items in its operations which management believes are important, but are not indispensable, to RPC’s success. Although RPC anticipates seeking patent protection when possible, it relies to a greater extent on the technical expertise and know-how of its personnel to maintain its competitive position.

Availability of Filings

RPC makes available, free of charge, on its website, www.rpc.net, its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports on the same day they are filed with the Securities and Exchange Commission.

Item 1A. Risk Factors

Demand for our equipment and services is affected by the volatility of oil and natural gas prices.

Oil and natural gas prices affect demand throughout the oil and gas industry, including the demand for our equipment and services. Our business depends in large part on the conditions of the oil and gas industry, and specifically on the capital investments of our customers related to the exploration and production of oil and natural gas. When these capital investments decline, our customers’ demand for our services declines.

| 9 |

The price of oil, a world-wide commodity, is affected by, among other things, the potential of armed conflict in politically unstable areas such as the Middle East as well as the actions of OPEC, an oil cartel which controls slightly less than 40 percent of global oil production. OPEC’s actions have historically been unpredictable and can contribute to the volatility of the price of oil on the world market.

Although the production sector of the oil and gas industry is less immediately affected by changing prices, and, as a result, less volatile than the exploration sector, producers react to declining oil and gas prices by curtailing capital spending, which would adversely affect our business. A prolonged low level of customer activity in the oil and gas industry adversely affects the demand for our equipment and services and our financial condition and results of operations.

Reliance upon a large customer may adversely affect our revenues and operating results.

At times our business has had a concentration of one or more major customers. There were no customers that accounted for more than 10 percent of the Company’s revenues in 2017 and 2016. However, one of our customers accounted for 23 percent of revenues in 2015. In addition, there was no customer as of December 31, 2017 and 2016 that accounted for more than 10 percent of accounts receivable. The reliance on a large customer for a significant portion of our total revenues exposes us to the risk that the loss or reduction in revenues from this customer, which could occur unexpectedly, could have a material and disproportionate adverse impact upon our revenues and operating results.

Our concentration of customers in one industry and periodic downturns may impact our overall exposure to credit risk and cause us to experience increased losses for doubtful accounts.

Substantially all of our customers operate in the energy industry. This concentration of customers in one industry may impact our overall exposure to credit risk, either positively or negatively, in that customers may be similarly affected by changes in economic and industry conditions. We perform ongoing credit evaluations of our customers and do not generally require collateral in support of our trade receivables. The periodic downturns that our industry experiences may adversely affect our customers' operations which could cause us to experience increased losses for doubtful accounts.

RPC’s success will depend on its key personnel, and the loss of any key personnel may affect its revenues.

RPC’s success will depend to a significant extent on the continued service of key management personnel. The loss or interruption of the services of any senior management personnel or the inability to attract and retain other qualified management, sales, marketing and technical employees could disrupt RPC’s operations and cause a decrease in its revenues and profit margins.

We may be unable to compete in the highly competitive oil and gas industry in the future.

We operate in highly competitive areas of the oilfield services industry. The equipment and services in our industry segments are sold in highly competitive markets, and our revenues and earnings have in the past been affected by changes in competitive prices, fluctuations in the level of activity in major markets and general economic conditions. We compete with the oil and gas industry’s many large and small industry competitors, including the largest integrated oilfield service providers. We believe that the principal competitive factors in the market areas that we serve are product and service quality and availability, reputation for safety, technical proficiency and price. Although we believe that our reputation for safety and quality service is good, we cannot assure you that we will be able to maintain our competitive position.

We may be unable to identify or complete acquisitions.

Acquisitions have been and may continue to be a key element of our business strategy. We cannot assure you that we will be able to identify and acquire acceptable acquisition candidates on terms favorable to us in the future. We may be required to incur substantial indebtedness to finance future acquisitions and also may issue equity securities in connection with such acquisitions. The issuance of additional equity securities could result in significant dilution to our stockholders. We cannot assure you that we will be able to integrate successfully the operations and assets of any acquired business with our own business. Any inability on our part to integrate and manage the growth from acquired businesses could have a material adverse effect on our results of operations and financial condition.

| 10 |

Our operations are affected by adverse weather conditions.

Our operations are directly affected by the weather conditions in several domestic regions, including the Gulf of Mexico, the Gulf Coast, the mid-continent, the Rocky Mountains and the Appalachian region. Hurricanes and other storms prevalent in the Gulf of Mexico and along the Gulf Coast during certain times of the year may also affect our operations, and severe hurricanes may affect our customers' activities for a period of several years. While the impact of these storms may increase the need for certain of our services over a longer period of time, such storms can also decrease our customers' activities immediately after they occur. Such hurricanes may also affect the prices of oil and natural gas by disrupting supplies in the short term, which may increase demand for our services in geographic areas not damaged by the storms. Prolonged rain, snow or ice in many of our locations may temporarily prevent our crews and equipment from reaching customer work sites. Due to seasonal differences in weather patterns, our crews may operate more days in some periods than others. Accordingly, our operating results may vary from quarter to quarter, depending on the impact of these weather conditions.

Our ability to attract and retain skilled workers may impact growth potential and profitability.

Our ability to be productive and profitable will depend substantially on our ability to attract and retain skilled workers. Our ability to expand our operations is, in part, impacted by our ability to increase our labor force. A significant increase in the wages paid by competing employers could result in a reduction in our skilled labor force, increases in the wage rates paid by us, or both. If either of these events occurred, our capacity and profitability could be diminished, and our growth potential could be impaired.

Our business has potential liability for litigation, personal injury and property damage claims assessments.

Our operations involve the use of heavy equipment and exposure to inherent risks, including blowouts, explosions and fires. If any of these events were to occur, it could result in liability for personal injury and property damage, pollution or other environmental hazards or loss of production. Litigation may arise from a catastrophic occurrence at a location where our equipment and services are used. This litigation could result in large claims for damages. The frequency and severity of such incidents will affect our operating costs, insurability and relationships with customers, employees and regulators. These occurrences could have a material adverse effect on us. We maintain what we believe is prudent insurance protection. We cannot assure you that we will be able to maintain adequate insurance in the future at rates we consider reasonable or that our insurance coverage will be adequate to cover future claims and assessments that may arise.

Our operations may be adversely affected if we are unable to comply with regulations and environmental laws.

Our business is significantly affected by stringent environmental laws and other regulations relating to the oil and gas industry and by changes in such laws and the level of enforcement of such laws. We are unable to predict the level of enforcement of existing laws and regulations, how such laws and regulations may be interpreted by enforcement agencies or court rulings, or whether additional laws and regulations will be adopted. The adoption of laws and regulations curtailing exploration and development of oil and gas fields in our areas of operations for economic, environmental or other policy reasons would adversely affect our operations by limiting demand for our services. We also have potential environmental liabilities with respect to our offshore and onshore operations, and could be liable for cleanup costs, or environmental and natural resource damage due to conduct that was lawful at the time it occurred, but is later ruled to be unlawful. We also may be subject to claims for personal injury and property damage due to the generation of hazardous substances in connection with our operations. We believe that our present operations substantially comply with applicable federal and state pollution control and environmental protection laws and regulations. We also believe that compliance with such laws has had no material adverse effect on our operations to date. However, such environmental laws are changed frequently. We are unable to predict whether environmental laws will, in the future, materially adversely affect our operations and financial condition. Penalties for noncompliance with these laws may include cancellation of permits, fines, and other corrective actions, which would negatively affect our future financial results.

Compliance with federal and state regulations relating to hydraulic fracturing and designation of economic development zones related to natural gas-directed drilling from shale formations could increase our operating costs, cause operational delays, and could reduce or eliminate the demand for our pressure pumping services.

RPC’s pressure pumping services are the subject of continuing federal, state and local regulatory oversight. This scrutiny is prompted in part by public concern regarding the potential impact on drinking and ground water and other environmental issues arising from the growing use of hydraulic fracturing. Among these regulatory entities is the White House Council on Environmental Quality, which coordinated a review of hydraulic fracturing practices. In addition, a committee of the United States House of Representatives investigated hydraulic fracturing practices and publicized information regarding the materials used in hydraulic fracturing. The U.S. Environmental Protection Agency (EPA) has also undertaken a study of the environmental impact of hydraulic fracturing practices. In the second quarter of 2015, the EPA issued a report which concluded that hydraulic fracturing had not caused a measureable impact on drinking water sources in the U.S. While this conclusion and other conclusions from similar efforts are favorable for our industry, we are unable to predict whether future scrutiny of RPC’s pressure pumping business and any resulting regulatory change will impact our business through increased operational costs, operational delays, or a reduction in demand for hydraulic fracturing services.

| 11 |

Our international operations could have a material adverse effect on our business.

Our operations in various international markets including, but not limited to, Africa, Canada, Argentina, China, Mexico, Eastern Europe, Latin America and the Middle East are subject to risks. These risks include, but are not limited to, political changes, expropriation, currency restrictions and changes in currency exchange rates, taxes, boycotts and other civil disturbances. The occurrence of any one of these events could have a material adverse effect on our operations.

Our common stock price has been volatile.

Historically, the market price of common stock of companies engaged in the oil and gas services industry has been highly volatile. Likewise, the market price of our common stock has varied significantly in the past.

Our management has a substantial ownership interest, and public stockholders may have no effective voice in the management of the Company.

The Company has elected the “Controlled Corporation” exemption under Section 303A of the New York Stock Exchange (“NYSE”) Listed Company Manual. The Company is a “Controlled Corporation” because a group that includes the Company’s Chairman of the Board, R. Randall Rollins and his brother, Gary W. Rollins, who is also a director of the Company, and certain companies under their control, controls in excess of fifty percent of the Company’s voting power. As a “Controlled Corporation,” the Company need not comply with certain NYSE rules including those requiring a majority of independent directors.

RPC’s executive officers, directors and their affiliates hold directly or through indirect beneficial ownership, in the aggregate, 73 percent of RPC’s outstanding shares of common stock. As a result, these stockholders effectively control the operations of RPC, including the election of directors and approval of significant corporate transactions such as acquisitions and other matters requiring stockholder approval. This concentration of ownership could also have the effect of delaying or preventing a third party from acquiring control over the Company at a premium.

Our management has a substantial ownership interest, and the availability of the Company’s common stock to the investing public may be limited.

The availability of RPC’s common stock to the investing public may be limited to those shares not held by the executive officers, directors and their affiliates, which could negatively impact RPC’s stock trading prices and affect the ability of minority stockholders to sell their shares. Future sales by executive officers, directors and their affiliates of all or a portion of their shares could also negatively affect the trading price of our common stock.

Provisions in RPC's certificate of incorporation and bylaws may inhibit a takeover of RPC.

RPC’s certificate of incorporation, bylaws and other documents contain provisions including advance notice requirements for stockholder proposals and staggered terms for the Board of Directors. These provisions may make a tender offer, change in control or takeover attempt that is opposed by RPC’s Board of Directors more difficult or expensive.

Some of our equipment and several types of materials used in providing our services are available from a limited number of suppliers.

We purchase equipment provided by a limited number of manufacturers who specialize in oilfield service equipment. During periods of high demand, these manufacturers may not be able to meet our requests for timely delivery, resulting in delayed deliveries of equipment and higher prices for equipment. There are a limited number of suppliers for certain materials used in pressure pumping services, our largest service line. While these materials are generally available, supply disruptions can occur due to factors beyond our control. Such disruptions, delayed deliveries, and higher prices may limit our ability to provide services, or increase the costs of providing services, which could reduce our revenues and profits.

| 12 |

We have used outside financing in prior years to accomplish our growth strategy, and outside financing may become unavailable or may be unfavorable to us.

Our business requires a great deal of capital in order to maintain our equipment and increase our fleet of equipment to expand our operations, and we have access to our credit facility to fund our necessary working capital and equipment requirements. Our credit facility, as amended June 30, 2016, provides a borrowing base at the lesser of (a) $125 million or (b) the difference between (i) a specified percentage (ranging from 70% to 80%) of eligible accounts receivable less (ii) the amount of any outstanding letters of credit, and bears interest at a floating rate, which exposes us to market risks as interest rates rise. If our existing capital resources become unavailable, inadequate or unfavorable for purposes of funding our capital requirements, we would need to raise additional funds through alternative debt or equity financings to maintain our equipment and continue our growth. Such additional financing sources may not be available when we need them, or may not be available on favorable terms. If we fund our growth through the issuance of public equity, the holdings of stockholders will be diluted. If capital generated either by cash provided by operating activities or outside financing is not available or sufficient for our needs, we may be unable to maintain our equipment, expand our fleet of equipment, or take advantage of other potentially profitable business opportunities, which could reduce our future revenues and profits.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

RPC owns or leases approximately 120 offices and operating facilities. The Company leases approximately 18,600 square feet of office space in Atlanta, Georgia that serves as its headquarters, a portion of which is allocated and charged to Marine Products Corporation. See “Related Party Transactions” contained in Item 7. The lease agreement on the headquarters is effective through October 2020. RPC believes its current operating facilities are suitable and adequate to meet current and reasonably anticipated future needs. Descriptions of the major facilities used in our operations are as follows:

Owned Locations

Broussard, Louisiana — Operations, sales and equipment storage yards

Vilonia, Arkansas — Maintenance and rebuild facilities

Elk City, Oklahoma — Operations, sales and equipment storage yards

Houma, Louisiana — Administrative office

Houston, Texas — Pipe storage terminal and inspection sheds

Kilgore, Texas — Operations, sales and equipment storage yards

Odessa, Texas — Operations, sales and equipment storage yards

Rock Springs, Wyoming — Operations, sales and equipment storage yards

Vernal, Utah — Operations, sales and equipment storage yards

Williston, North Dakota — Operations, sales and equipment storage yards

Leased Locations

Canton, Pennsylvania — Operations, sales and equipment storage yards

Hobbs, New Mexico — Pumping services facility

Oklahoma City, Oklahoma — Operations, sales and administrative office

San Antonio, Texas — Operations, sales and equipment storage yards

Seminole, Oklahoma — Pumping services facility

The Woodlands, Texas — Operations, sales and administrative office

Washington, Pennsylvania — Operations, sales and equipment storage yards

Williston, North Dakota — Operations, sales and equipment storage yards

Item 3. Legal Proceedings

RPC is a party to various routine legal proceedings primarily involving commercial claims, workers’ compensation claims and claims for personal injury. RPC insures against these risks to the extent deemed prudent by its management, but no assurance can be given that the nature and amount of such insurance will, in every case, fully indemnify RPC against liabilities arising out of pending and future legal proceedings related to its business activities. While the outcome of these lawsuits, legal proceedings and claims cannot be predicted with certainty, management believes that the outcome of all such proceedings, even if determined adversely, would not have a material adverse effect on RPC’s business or financial condition.

| 13 |

Item 4. Mine Safety Disclosures

The information required by Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act and Item 104 of Regulation S-K is included in Exhibit 95.1 to this Form 10-K.

Item 4A. Executive Officers of the Registrant

Each of the executive officers of RPC was elected by the Board of Directors to serve until the Board of Directors’ meeting immediately following the next annual meeting of stockholders or until his earlier removal by the Board of Directors or his resignation. The following table lists the executive officers of RPC and their ages, offices, and terms of office with RPC.

| Name and Office with Registrant | Age | Date First Elected to Present Office |

| R. Randall Rollins (1) | 86 | 1/24/84 |

| Chairman of the Board | ||

| Richard A. Hubbell (2) | 73 | 4/22/03 |

| President and Chief Executive Officer | ||

| Ben M. Palmer (3) | 57 | 7/8/96 |

| Vice President, Chief Financial Officer and Corporate Secretary |

| (1) | R. Randall Rollins began working for Rollins, Inc. (consumer services) in 1949. Mr. Rollins has served as Chairman of the Board of RPC since the spin-off of RPC from Rollins, Inc. in 1984. He has served as Chairman of the Board of Marine Products Corporation (boat manufacturing) since it was spun off from RPC in 2001 and as Chairman of the Board of Rollins, Inc. since October 1991. He is also a director of Dover Downs Gaming and Entertainment, Inc. and Dover Motorsports, Inc. |

| (2) | Richard A. Hubbell has been the President of RPC since 1987 and Chief Executive Officer since 2003. He has also been the President and Chief Executive Officer of Marine Products Corporation since it was spun off from RPC in 2001. Mr. Hubbell serves on the Board of Directors of both of these companies. |

| (3) | Ben M. Palmer has been the Vice President and Chief Financial Officer of RPC since 1996. He has also been the Vice President and Chief Financial Officer of Marine Products Corporation since it was spun off from RPC in 2001. He assumed the responsibilities as Corporate Secretary of RPC and Marine Products Corporation in July 2017. |

| 14 |

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

RPC’s common stock is listed for trading on the New York Stock Exchange under the symbol RES. As of February 16, 2018 there were 216,838,107 shares of common stock outstanding and approximately 22,600 beneficial holders of our common stock. The following table sets forth the high and low trading prices of RPC’s common stock and dividends paid for each quarter in the years ended December 31, 2017 and 2016:

| 2017 | 2016 | |||||||||||||||||||||||

| Quarter | High | Low | Dividends | High | Low | Dividends | ||||||||||||||||||

| First | $ | 23.32 | $ | 16.63 | $ | — | $ | 15.51 | $ | 9.73 | $ | — | ||||||||||||

| Second | 21.28 | 17.03 | — | 16.84 | 13.12 | — | ||||||||||||||||||

| Third | 24.99 | 17.70 | 0.06 | 16.92 | 13.50 | — | ||||||||||||||||||

| Fourth | 27.07 | 21.18 | 0.14 | 22.28 | 16.48 | 0.05 | ||||||||||||||||||

On January 23, 2018, RPC’s Board of Directors approved a 43 percent increase to the regular cash dividend from $0.07 per share to $0.10 per share payable March 9, 2018 to stockholders of record at the close of business on February 9, 2018. Subject to industry conditions and RPC’s earnings, financial condition, and other relevant factors, the Company expects to continue to pay regular quarterly cash dividends to common stockholders.

Issuer Purchases of Equity Securities

Shares repurchased by the Company and affiliated purchases in the fourth quarter of 2017 are outlined below.

| Period | Total Number of Shares (or Units) Purchased | Average Price Paid Per Share (or Unit) | Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs (1) | ||||||||||||

| October 1, 2017 to October 31, 2017 | 2,465 (2) | $ | 24.52 | — | 975,265 | |||||||||||

| November 1, 2017 to November 30, 2017 | — | — | — | 975,265 | ||||||||||||

| December 1, 2017 to December 31, 2017 | — | — | — | 975,265 | ||||||||||||

| Totals | 2,465 | $ | 24.52 | — | 975,265 | |||||||||||

| (1) | The Company has a stock buyback program initially adopted in 1998 and subsequently amended in 2013 that authorizes the repurchase of up to 31,578,125 shares. There were no shares repurchased as part of this program during the fourth quarter of 2017. As of December 31, 2017, there are 975,265 shares available to be repurchased under the current authorization. On February 12, 2018, the Board of Directors increased the number of shares authorized for repurchase by 10,000,000 shares. Currently the program does not have a predetermined expiration date. |

| (2) | Represents shares repurchased by the Company in connection with taxes related to vesting of restricted shares. |

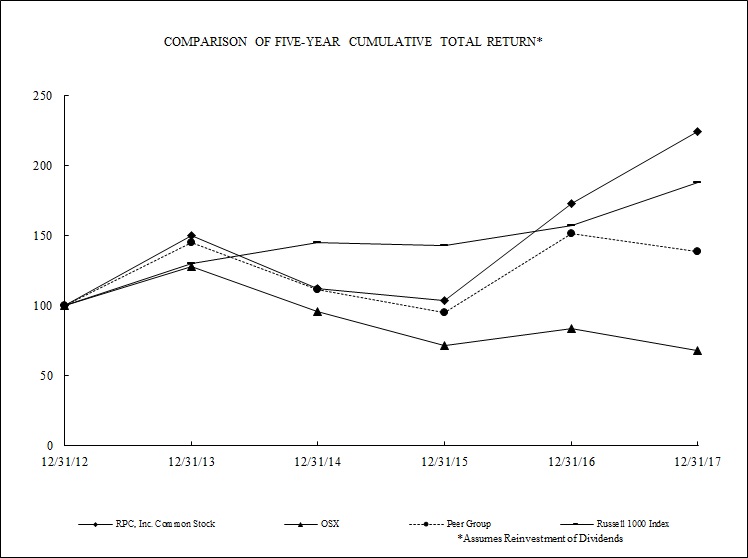

Performance Graph

The following graph shows a five-year comparison of the cumulative total stockholder return based on the performance of the stock of the Company, assuming dividend reinvestment, as compared with both a broad equity market index and an industry or peer group index. The indices included in the following graph are the Russell 1000 Index (“Russell 1000”), the Philadelphia Stock Exchange’s Oil Service Index (“OSX”), and a peer group which includes companies that are considered peers of the Company (the “Peer Group”). The Company has voluntarily chosen to provide both an industry and a peer group index.

| 15 |

The Company was a component of the Russell 1000 during 2017. The Russell 1000 is a stock index representing large capitalization U.S. stocks with high historical growth in revenues and earnings. The components of the index had a weighted average market capitalization in 2017 of $178 billion, and a median market capitalization of $10.5 billion. The Russell 1000 was chosen because it represents companies with comparable market capitalizations to the Company, and because the Company is a component of the index. The OSX is a stock index of 15 companies that provide oil drilling and production services, oilfield equipment, support services and geophysical/reservoir services. The Company is not a component of the OSX, but this index was chosen because it represents a large group of companies that provide the same or similar equipment and services as the Company. The companies included in the Peer Group are Weatherford International, Inc., Superior Energy Services, Inc., Patterson-UTI Energy, Inc., and Halliburton Company. The companies included in the Peer Group have been weighted according to each respective issuer's stock market capitalization at the beginning of each year.

| 16 |

Item 6. Selected Financial Data

The following table summarizes certain selected financial data of the Company. The historical information may not be indicative of the Company’s future results of operations. The information set forth below should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the Consolidated Financial Statements and the notes thereto included elsewhere in this document.

Statements of Operations Data:

| Years Ended December 31, | 2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||

| (in thousands, except employee and per share amounts) | ||||||||||||||||||||

| Revenues | $ | 1,595,227 | $ | 728,974 | $ | 1,263,840 | $ | 2,337,413 | $ | 1,861,489 | ||||||||||

| Cost of revenues | 1,050,809 | 607,888 | 986,144 | 1,493,082 | 1,178,412 | |||||||||||||||

| Selling, general and administrative expenses | 159,194 | 150,690 | 156,579 | 197,117 | 183,139 | |||||||||||||||

| Depreciation and amortization | 163,537 | 217,258 | 270,977 | 230,813 | 213,128 | |||||||||||||||

| (Gain) loss on disposition of assets, net | (4,530 | ) | (7,920 | ) | 6,417 | 15,472 | 9,371 | |||||||||||||

| Operating profit (loss) | 226,217 | (238,942 | ) | (156,277 | ) | 400,929 | 277,439 | |||||||||||||

| Interest expense | (426 | ) | (681 | ) | (2,032 | ) | (1,431 | ) | (1,822 | ) | ||||||||||

| Interest income | 1,494 | 467 | 83 | 19 | 408 | |||||||||||||||

| Other income (expense), net | 5,531 | (204 | ) | 5,185 | (131 | ) | 245 | |||||||||||||

| Income (loss) before income taxes | 232,816 | (239,360 | ) | (153,041 | ) | 399,386 | 276,270 | |||||||||||||

| Income tax provision (benefit) (1) | 70,305 | (98,114 | ) | (53,480 | ) | 154,193 | 109,375 | |||||||||||||

| Net income (loss) (1) | $ | 162,511 | $ | (141,246 | ) | $ | (99,561 | ) | $ | 245,193 | $ | 166,895 | ||||||||

| Earnings (loss) per share : (1) | ||||||||||||||||||||

| Basic | $ | 0.75 | $ | (0.66 | ) | $ | (0.47 | ) | $ | 1.14 | $ | 0.77 | ||||||||

| Diluted | $ | 0.75 | $ | (0.66 | ) | $ | (0.47 | ) | $ | 1.14 | $ | 0.77 | ||||||||

| Dividends paid per share | $ | 0.200 | $ | 0.050 | $ | 0.155 | $ | 0.420 | $ | 0.400 | ||||||||||

| Other Data: | ||||||||||||||||||||

| Operating profit (loss) margin percent | 14.2 | % | (32.8 | )% | (12.4 | )% | 17.2 | % | 14.9 | % | ||||||||||

| Net cash provided by operating activities | $ | 133,704 | $ | 101,704 | $ | 473,792 | $ | 322,757 | $ | 365,624 | ||||||||||

| Net cash used for investing activities | (104,386 | ) | (21,339 | ) | (157,583 | ) | (355,349 | ) | (207,654 | ) | ||||||||||

| Net cash (used for) provided by financing activities | (70,103 | ) | (13,726 | ) | (260,785 | ) | 33,664 | (163,433 | ) | |||||||||||

| Capital expenditures | $ | 117,509 | $ | 33,938 | $ | 167,426 | $ | 371,502 | $ | 201,681 | ||||||||||

| Employees at end of period | 3,500 | 2,500 | 3,100 | 4,500 | 3,900 | |||||||||||||||

Balance Sheet Data at Year End: | ||||||||||||||||||||

| Accounts receivable, net | $ | 377,853 | $ | 169,166 | $ | 232,187 | $ | 634,730 | $ | 437,132 | ||||||||||

| Working capital | 494,775 | 377,589 | 384,744 | 612,616 | 436,873 | |||||||||||||||

| Property, plant and equipment, net | 443,928 | 497,986 | 688,335 | 849,383 | 726,307 | |||||||||||||||

| Total assets | 1,147,224 | 1,035,452 | 1,237,094 | 1,759,358 | 1,383,860 | |||||||||||||||

| Long-term debt | — | — | — | 224,500 | 53,300 | |||||||||||||||

| Total stockholders’ equity | $ | 911,697 | $ | 806,799 | $ | 952,281 | $ | 1,078,382 | $ | 968,702 | ||||||||||

| (1) | The indicated Statement of Operations data for 2017 includes the impact of a net discrete tax benefit of $19.3 million, or $0.09 per share, recorded as a result of the Tax Cuts and Jobs Act enacted during the fourth quarter of 2017. |

| 17 |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Overview

The following discussion should be read in conjunction with “Selected Financial Data” and the Consolidated Financial Statements included elsewhere in this document. See also “Forward-Looking Statements” on page 2.

RPC, Inc. (“RPC”) provides a broad range of specialized oilfield services primarily to independent and major oilfield companies engaged in exploration, production and development of oil and gas properties throughout the United States, including the southwest, mid-continent, Gulf of Mexico, Rocky Mountain and Appalachian regions, and in selected international markets. The Company’s revenues and profits are generated by providing equipment and services to customers who operate oil and gas properties and invest capital to drill new wells and enhance production or perform maintenance on existing wells.

Our key business and financial strategies are:

| - | To focus our management resources on and invest our capital in equipment and geographic markets that we believe will earn high returns on capital. |

| - | To maintain a flexible cost structure that can respond quickly to volatile industry conditions and business activity levels. |

| - | To maintain an efficient, low-cost capital structure which includes an appropriate use of debt financing. |

| - | To maintain high asset utilization which leads to increased revenues and leverage of direct and overhead costs, while also ensuring that increased maintenance resulting from high utilization does not interfere with customer performance requirements or jeopardize safety. |

| - | To deliver product and services to our customers safely. |

| - | To secure adequate sources of supplies of certain high-demand raw materials used in our operations, both in order to conduct our operations and to enhance our competitive position. |

| - | To maintain and selectively increase market share. |

| - | To maximize stockholder return by optimizing the balance between cash invested in the Company's productive assets, the payment of dividends to stockholders, and the repurchase of our common stock on the open market. |