UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

[X] | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended December 31, 2017

OR

[ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ----- to -----

Commission file number 0-13163

Acxiom Corporation | |

(Exact Name of Registrant as Specified in Its Charter) | |

DELAWARE (State or Other Jurisdiction of Incorporation or Organization) | 71-0581897 (I.R.S. Employer Identification No.) |

301 E. Dave Ward Drive Conway, Arkansas (Address of Principal Executive Offices) | 72032 (Zip Code) |

(501) 342-1000 (Registrant's Telephone Number, Including Area Code) | |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer [X] | Accelerated filer [ ] |

Non-accelerated filer [ ] | Smaller reporting company [ ] |

(Do not check if a smaller reporting company) | Emerging growth company [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [X]

The number of shares of common stock, $ 0.10 par value per share, outstanding as of February 2, 2018 was 79,100,637.

ACXIOM CORPORATION AND SUBSIDIARIES

INDEX

REPORT ON FORM 10-Q

December 31, 2017

Page No. | ||

2

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

ACXIOM CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(Dollars in thousands)

December 31, 2017 | March 31, 2017 | |||||||

ASSETS | (Unaudited) | |||||||

Current assets: | ||||||||

Cash and cash equivalents | $ | 177,807 | $ | 170,343 | ||||

Trade accounts receivable, net | 155,634 | 142,768 | ||||||

Refundable income taxes | 6,365 | 7,098 | ||||||

Other current assets | 42,357 | 48,310 | ||||||

Total current assets | 382,163 | 368,519 | ||||||

Property and equipment, net of accumulated depreciation and amortization | 153,039 | 155,974 | ||||||

Software, net of accumulated amortization | 37,489 | 47,638 | ||||||

Goodwill | 592,827 | 592,731 | ||||||

Purchased software licenses, net of accumulated amortization | 7,775 | 7,972 | ||||||

Deferred income taxes | 9,621 | 10,261 | ||||||

Other assets, net | 43,576 | 51,443 | ||||||

$ | 1,226,490 | $ | 1,234,538 | |||||

LIABILITIES AND EQUITY | ||||||||

Current liabilities: | ||||||||

Current installments of long-term debt | $ | 1,837 | $ | 39,819 | ||||

Trade accounts payable | 46,211 | 40,208 | ||||||

Accrued payroll and related expenses | 36,592 | 53,238 | ||||||

Other accrued expenses | 53,999 | 59,861 | ||||||

Deferred revenue | 34,169 | 37,087 | ||||||

Total current liabilities | 172,808 | 230,213 | ||||||

Long-term debt | 227,943 | 189,241 | ||||||

Deferred income taxes | 34,300 | 58,374 | ||||||

Other liabilities | 17,328 | 17,730 | ||||||

Commitments and contingencies | ||||||||

Equity: | ||||||||

Common stock | 13,552 | 13,288 | ||||||

Additional paid-in capital | 1,216,565 | 1,154,429 | ||||||

Retained earnings | 623,156 | 602,609 | ||||||

Accumulated other comprehensive income | 9,826 | 7,999 | ||||||

Treasury stock, at cost | (1,088,988 | ) | (1,039,345 | ) | ||||

Total equity | 774,111 | 738,980 | ||||||

$ | 1,226,490 | $ | 1,234,538 | |||||

See accompanying notes to condensed consolidated financial statements.

3

ACXIOM CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

(Dollars in thousands, except per share amounts)

For the three months ended | ||||||||

December 31, | ||||||||

2017 | 2016 | |||||||

Revenues | $ | 234,871 | $ | 223,312 | ||||

Cost of revenue | 115,920 | 116,468 | ||||||

Gross profit | 118,951 | 106,844 | ||||||

Operating expenses: | ||||||||

Research and development | 23,318 | 20,950 | ||||||

Sales and marketing | 53,730 | 43,048 | ||||||

General and administrative | 30,886 | 31,620 | ||||||

Gains, losses and other items, net | (41 | ) | 2,111 | |||||

Total operating expenses | 107,893 | 97,729 | ||||||

Income from operations | 11,058 | 9,115 | ||||||

Other income (expense): | ||||||||

Interest expense | (2,566 | ) | (1,743 | ) | ||||

Other, net | 419 | 35 | ||||||

Total other expense | (2,147 | ) | (1,708 | ) | ||||

Income before income taxes | 8,911 | 7,407 | ||||||

Income taxes (benefit) | (14,030 | ) | 6,334 | |||||

Net earnings | $ | 22,941 | $ | 1,073 | ||||

Basic earnings per share | $ | 0.29 | $ | 0.01 | ||||

Diluted earnings per share | $ | 0.28 | $ | 0.01 | ||||

See accompanying notes to condensed consolidated financial statements.

4

ACXIOM CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

(Dollars in thousands, except per share amounts)

For the nine months ended | ||||||||

December 31, | ||||||||

2017 | 2016 | |||||||

Revenues | $ | 672,625 | $ | 655,380 | ||||

Cost of revenue | 344,952 | 359,392 | ||||||

Gross profit | 327,673 | 295,988 | ||||||

Operating expenses: | ||||||||

Research and development | 70,894 | 58,631 | ||||||

Sales and marketing | 152,288 | 118,243 | ||||||

General and administrative | 95,166 | 91,993 | ||||||

Gains, losses and other items, net | 3,521 | 2,724 | ||||||

Total operating expenses | 321,869 | 271,591 | ||||||

Income from operations | 5,804 | 24,397 | ||||||

Other income (expense): | ||||||||

Interest expense | (7,432 | ) | (5,244 | ) | ||||

Other, net | (61 | ) | 135 | |||||

Total other expense | (7,493 | ) | (5,109 | ) | ||||

Income (loss) before income taxes | (1,689 | ) | 19,288 | |||||

Income taxes (benefit) | (19,994 | ) | 7,099 | |||||

Net earnings | $ | 18,305 | $ | 12,189 | ||||

Basic earnings per share | $ | 0.23 | $ | 0.16 | ||||

Diluted earnings per share | $ | 0.22 | $ | 0.15 | ||||

See accompanying notes to condensed consolidated financial statements.

5

ACXIOM CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited)

(Dollars in thousands)

For the three months ended | ||||||||

December 31, | ||||||||

2017 | 2016 | |||||||

Net earnings | $ | 22,941 | $ | 1,073 | ||||

Other comprehensive income: | ||||||||

Change in foreign currency translation adjustment | 416 | (1,340 | ) | |||||

Unrealized gain on interest rate swap | — | 21 | ||||||

Other comprehensive income | 416 | (1,319 | ) | |||||

Comprehensive income | $ | 23,357 | $ | (246 | ) | |||

See accompanying notes to condensed consolidated financial statements.

6

ACXIOM CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited)

(Dollars in thousands)

For the nine months ended | ||||||||

December 31, | ||||||||

2017 | 2016 | |||||||

Net earnings | $ | 18,305 | $ | 12,189 | ||||

Other comprehensive income (loss): | ||||||||

Change in foreign currency translation adjustment | 1,827 | (2,410 | ) | |||||

Unrealized gain on interest rate swap | — | 117 | ||||||

Other comprehensive income (loss) | 1,827 | (2,293 | ) | |||||

Comprehensive income | $ | 20,132 | $ | 9,896 | ||||

See accompanying notes to condensed consolidated financial statements.

7

ACXIOM CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF EQUITY

NINE MONTHS ENDED DECEMBER 31, 2017

(Unaudited)

(Dollars in thousands)

Accumulated | ||||||||||||||||||||||||||||||

Common Stock | Additional | other | Treasury Stock | |||||||||||||||||||||||||||

Number | paid-in | Retained | comprehensive | Number | Total | |||||||||||||||||||||||||

of shares | Amount | Capital | earnings | income | of shares | Amount | Equity | |||||||||||||||||||||||

Balances at March 31, 2017 | 132,875,373 | $ | 13,288 | $ | 1,154,429 | $ | 602,609 | $ | 7,999 | (54,582,392 | ) | $ | (1,039,345 | ) | $ | 738,980 | ||||||||||||||

Cumulative-effect adjustment from adoption of ASU 2016-09 | — | — | 384 | 2,242 | — | — | — | $ | 2,626 | |||||||||||||||||||||

Employee stock awards, benefit plans and other issuances | 805,768 | 80 | 15,229 | — | — | (389,912 | ) | (10,202 | ) | $ | 5,107 | |||||||||||||||||||

Non-cash stock-based compensation | 487,385 | 49 | 46,658 | — | — | — | — | $ | 46,707 | |||||||||||||||||||||

Restricted stock units vested | 1,351,652 | 135 | (135 | ) | — | — | — | — | $ | — | ||||||||||||||||||||

Acquisition of treasury stock | — | — | — | — | — | (1,588,964 | ) | (39,441 | ) | $ | (39,441 | ) | ||||||||||||||||||

Comprehensive income: | ||||||||||||||||||||||||||||||

Foreign currency translation | — | — | — | — | 1,827 | — | — | $ | 1,827 | |||||||||||||||||||||

Net earnings | — | — | — | 18,305 | — | — | — | $ | 18,305 | |||||||||||||||||||||

Balances at December 31, 2017 | 135,520,178 | $ | 13,552 | $ | 1,216,565 | $ | 623,156 | $ | 9,826 | (56,561,268 | ) | $ | (1,088,988 | ) | $ | 774,111 | ||||||||||||||

See accompanying notes to condensed consolidated financial statements

8

ACXIOM CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(Dollars in thousands)

For the nine months ended | ||||||||

December 31, | ||||||||

2017 | 2016 | |||||||

Cash flows from operating activities: | ||||||||

Net earnings | $ | 18,305 | $ | 12,189 | ||||

Adjustments to reconcile net earnings to net cash provided by operating activities: | ||||||||

Depreciation and amortization | 63,719 | 61,097 | ||||||

Loss (gain) on disposal or impairment of assets | 2,646 | (520 | ) | |||||

Accelerated deferred debt costs | 720 | — | ||||||

Deferred income taxes | (20,451 | ) | (1,982 | ) | ||||

Non-cash stock compensation expense | 46,707 | 33,955 | ||||||

Changes in operating assets and liabilities: | ||||||||

Accounts receivable, net | (11,432 | ) | (6,161 | ) | ||||

Other assets | (1,277 | ) | 8,653 | |||||

Accounts payable and other liabilities | (18,232 | ) | (11,819 | ) | ||||

Deferred revenue | (4,314 | ) | (10,247 | ) | ||||

Net cash provided by operating activities | 76,391 | 85,165 | ||||||

Cash flows from investing activities: | ||||||||

Capitalized software development costs | (10,332 | ) | (11,171 | ) | ||||

Capital expenditures | (26,950 | ) | (30,096 | ) | ||||

Data acquisition costs | (621 | ) | (463 | ) | ||||

Equity investments | (1,000 | ) | — | |||||

Net cash received from disposition | 4,000 | 16,988 | ||||||

Net cash paid in acquisitions | — | (137,383 | ) | |||||

Net cash used in investing activities | (34,903 | ) | (162,125 | ) | ||||

Cash flows from financing activities: | ||||||||

Proceeds from debt | 230,000 | 70,000 | ||||||

Payments of debt | (226,732 | ) | (24,173 | ) | ||||

Fees for debt refinancing | (4,001 | ) | — | |||||

Sale of common stock, net of stock acquired for withholding taxes | 5,107 | 9,670 | ||||||

Excess tax benefits from stock-based compensation | — | 1,785 | ||||||

Acquisition of treasury stock | (39,441 | ) | (30,542 | ) | ||||

Net cash provided by (used) in financing activities | (35,067 | ) | 26,740 | |||||

Effect of exchange rate changes on cash | 1,043 | (1,559 | ) | |||||

Net change in cash and cash equivalents | 7,464 | (51,779 | ) | |||||

Cash and cash equivalents at beginning of period | 170,343 | 189,629 | ||||||

Cash and cash equivalents at end of period | $ | 177,807 | $ | 137,850 | ||||

See accompanying notes to condensed consolidated financial statements.

9

ACXIOM CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (Continued)

(Unaudited)

(Dollars in thousands)

For the nine months ended | ||||||||

December 31, | ||||||||

2017 | 2016 | |||||||

Supplemental cash flow information: | ||||||||

Cash paid during the period for: | ||||||||

Interest | $ | 6,712 | $ | 5,301 | ||||

Income taxes, net of refunds | 1,152 | 4,796 | ||||||

Non-cash investing and financing activities: | ||||||||

Leasehold improvements paid directly by lessor | 978 | — | ||||||

See accompanying notes to condensed consolidated financial statements.

10

ACXIOM CORPORATION AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES:

These condensed consolidated financial statements have been prepared by Acxiom Corporation (“Registrant,” “Acxiom,” we, us or the “Company”), without audit, pursuant to the rules and regulations of the Securities and Exchange Commission (the “SEC” or the “Commission”). In the opinion of the Registrant’s management, all adjustments necessary for a fair presentation of the results for the periods included have been made, and the disclosures are adequate to make the information presented not misleading. All such adjustments are of a normal recurring nature. Certain note information has been omitted because it has not changed significantly from that reflected in Notes 1 through 19 of the Notes to Consolidated Financial Statements filed as part of Item 8 of the Registrant’s annual report on Form 10-K for the fiscal year ended March 31, 2017 (“2017 Annual Report”), as filed with the Commission on May 26, 2017. This quarterly report and the accompanying condensed consolidated financial statements should be read in connection with the 2017 Annual Report. The financial information contained in this quarterly report is not necessarily indicative of the results to be expected for any other period or for the full fiscal year ending March 31, 2018.

Management of the Company has made a number of estimates and assumptions relating to the reporting of assets and liabilities and the disclosure of contingent assets and liabilities to prepare these condensed consolidated financial statements in conformity with accounting principles generally accepted in the United States (“U.S. GAAP”). Actual results could differ from those estimates. Certain of the accounting policies used in the preparation of these condensed consolidated financial statements are complex and require management to make judgments and/or significant estimates regarding amounts reported or disclosed in these financial statements. Additionally, the application of certain of these accounting policies is governed by complex accounting principles and their interpretation. A discussion of the Company’s significant accounting principles and their application is included in Note 1 of the Notes to Consolidated Financial Statements and in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, of the Company’s 2017 Annual Report.

Accounting Pronouncements Adopted During the Current Year

In January 2017, the Financial Accounting Standards Board ("FASB") issued Accounting Standards Update ("ASU") No. 2017-01, "Business Combinations (Topic 805): Clarifying the Definition of a Business" ("ASU 2017-01"), which amended the existing FASB Accounting Standards Codification. The standard provides additional guidance to assist entities with evaluation of whether transactions should be accounted for as acquisitions (or disposals) of assets or businesses. The definition of a business affects many areas of accounting, including acquisitions, disposals, goodwill, and consolidation. ASU 2017-01 is effective for the Company beginning in fiscal 2019, with early adoptions permitted. We adopted the standard in the current fiscal year, on a prospective basis, and do not expect the adoption of this guidance to have a material impact on our condensed consolidated financial statements and related disclosures.

In November 2016, the FASB issued ASU 2016-18, "Statement of Cash Flows (Topic 230): Restricted Cash" ("ASU 2016-18"). This standard is intended to reduce diversity in the presentation of restricted cash and restricted cash equivalents in the statement of cash flows. The standard requires that restricted cash and restricted cash equivalents be included as components of total cash and cash equivalents as presented on the statement of cash flows. As a result, entities will no longer present transfers between cash and cash equivalents and restricted cash and restricted cash equivalents in the statement of cash flows. ASU 2016-18 is effective for annual periods beginning after December 15, 2017 (fiscal 2019 for the Company), including interim periods within those fiscal years; earlier adoption is permitted. We adopted the standard during the current fiscal year. Early adoption did not result in any changes to our existing accounting policies, presentation of items in our condensed consolidated financial statements and related disclosures, or any changes resulting from the retrospective application to all periods reported.

In March 2016, the FASB issued ASU No. 2016-09, "Compensation - Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting" ("ASU 2016-09"), which is intended to improve the accounting for stock-based payment transactions as part of the FASB's simplification initiative. The ASU changes five aspects of the accounting for stock-based payment award transactions that will affect public companies,

11

including: (1) accounting for income taxes; (2) classification of excess tax benefits on the statement of cash flows; (3) forfeitures; (4) minimum statutory tax withholding requirements; and (5) classification of employee taxes paid on the statement of cash flows when an employer withholds shares for tax-withholding purposes. The inclusion of excess tax benefits and deficiencies as a component of income tax expense will increase volatility within our provision for income taxes as the amount of excess tax benefits or deficiencies from stock-based compensation awards depends on our stock price at the date the awards vest or the date of option exercises. This guidance also requires excess tax benefits to be presented as an operating activity on the statement of cash flows and allows an entity to make an accounting policy election to either estimate expected forfeitures or to account for them as they occur.

We adopted ASU No. 2016-09 during the current fiscal year, which required us to reflect any adjustments as of April 1, 2017. We elected to account for forfeitures as they occur rather than estimating expected forfeitures. We recorded the cumulative impact of adoption through an increase in retained earnings of $2.2 million, of which $2.6 million related to deferred tax assets from certain federal and state research tax credit carryforwards attributable to excess tax benefits from stock-based compensation that had not been previously recognized, offset by $0.4 million related to elimination of the forfeiture pool. We elected to prospectively adopt the effect on the statement of cash flows and accordingly, did not restate the Condensed Consolidated Statement of Cash Flows for the nine months ended December 31, 2016.

Recent Accounting Pronouncements Not Yet Adopted

In January 2017, the FASB issued ASU 2017-04, "Intangibles-Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment" ("ASU 2017-04"), which eliminates step two from the goodwill impairment test. Under ASU 2017-04, an entity should recognize an impairment charge for the amount by which the carrying amount of a reporting unit exceeds its fair value; however, the loss recognized should not exceed the total amount of goodwill allocated to that reporting unit. ASU 2017-04 is effective for annual periods beginning after December 15, 2019 (fiscal 2021 for the Company), including interim periods within those fiscal years; earlier adoption is permitted for goodwill impairment tests performed on testing dates after January 1, 2017. The Company does not expect the adoption of this guidance to have a material impact on its consolidated financial statements and related disclosures.

In February 2016, the FASB issued ASU No. 2016-02, "Leases (Topic 842)" ("ASU 2016-02"), as a comprehensive new standard that amends various aspects of existing guidance for leases and requires additional disclosures about leasing arrangements. The new standard will require lessees to recognize a right-of-use asset and a lease liability on the balance sheet for all leases with the exception of short-term leases. For lessees, leases will continue to be classified as either operating or finance in the income statement. Lessor accounting is similar to the current model but updated to align with certain changes to the lessee model. Lessors will continue to classify leases as operating, direct financing or sales-type leases. ASU 2016-02 is effective for annual periods beginning after December 15, 2018 (fiscal 2020 for the Company), including interim periods within those fiscal years. Earlier adoption is permitted. In the financial statements in which the ASU is first applied, leases shall be measured and recognized at the beginning of the earliest comparative period presented with an adjustment to equity. The Company is continuing to evaluate the impact of the adoption of this guidance on its consolidated financial statements and related disclosures.

In May 2014, the FASB issued update ASU 2014-09, "Revenue from Contracts with Customers (Topic 606)" ("ASU 2014-09") and issued subsequent amendments to the initial guidance in August 2015, March 2016, April 2016, May 2016, and December 2016 within ASU 2015-14, ASU 2016-08, ASU 2016-10, ASU 2016-12 and ASU 2016-20, respectively (ASU 2014-09 and the subsequent amendments, collectively, "Topic 606"). Topic 606 supersedes nearly all existing revenue recognition guidance under U.S. GAAP. The core principle of the new guidance is to recognize revenues when promised goods or services are transferred to customers in an amount that reflects the consideration that is expected to be received for those goods or services. The guidance defines a five-step process to achieve this core principle and, in doing so, it is possible more judgment and estimates may be required within the revenue recognition process than are required under existing U.S. GAAP, including identifying performance obligations in the contract, estimating the amount of variable consideration to include in the transaction price and allocating the transaction price to each separate performance obligation, among others. Topic 606 also provides guidance on the recognition of costs related to obtaining customer contracts. The effective date for the Company is the first quarter of fiscal 2019 using either of two methods: (i) retrospective application to each prior reporting period presented with the option to elect certain practical expedients; or (ii) retrospective application with the cumulative effect recognized at the date of initial application and providing certain additional disclosures. The Company has completed its preliminary assessment of the new standard and is continuing assessment as we complete

12

implementation design activities. We plan to adopt Topic 606 in the first quarter of fiscal 2019 pursuant to the aforementioned adoption method (ii), and we do not believe there will be a material impact to our revenues upon adoption. We are continuing to evaluate the impact to our revenues related to our pending adoption of Topic 606 and our preliminary assessments are subject to change. We are also continuing to evaluate the provisions of Topic 606 related to costs of obtaining customer contracts.

The Company does not anticipate that the adoption of any other recent accounting pronouncements will have a material impact on the Company's consolidated financial position, results of operations or cash flows.

2. EARNINGS PER SHARE AND STOCKHOLDERS’ EQUITY:

Earnings Per Share

A reconciliation of the numerator and denominator of basic and diluted earnings per share is shown below (in thousands, except per share amounts):

For the three months ended | For the nine months ended | |||||||||||||||

December 31, | December 31, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Basic earnings per share: | ||||||||||||||||

Net earnings | $ | 22,941 | $ | 1,073 | $ | 18,305 | $ | 12,189 | ||||||||

Basic weighted-average shares outstanding | 79,043 | 77,507 | 78,983 | 77,475 | ||||||||||||

Basic earnings per share | $ | 0.29 | $ | 0.01 | $ | 0.23 | $ | 0.16 | ||||||||

Diluted earnings per share: | ||||||||||||||||

Basic weighted-average shares outstanding | 79,043 | 77,507 | 78,983 | 77,475 | ||||||||||||

Dilutive effect of common stock options, warrants, and restricted stock as computed under the treasury stock method | 2,826 | 2,344 | 2,611 | 2,019 | ||||||||||||

Diluted weighted-average shares outstanding | 81,869 | 79,851 | 81,594 | 79,494 | ||||||||||||

Diluted earnings per share | $ | 0.28 | $ | 0.01 | $ | 0.22 | $ | 0.15 | ||||||||

Options and warrants to purchase shares of common stock and restricted stock units that were outstanding during the periods presented but were not included in the computation of diluted earnings per share because the effect was anti-dilutive are shown below (shares in thousands):

For the three months ended | For the nine months ended | |||||||||||

December 31, | December 31, | |||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||

Number of shares outstanding under options, warrants and restricted stock units | 97 | 156 | 89 | 345 | ||||||||

Range of exercise prices for options | $32.85 | $32.85 | $32.85 | $20.27-$32.85 | ||||||||

Stockholders’ Equity

On August 29, 2011, the board of directors adopted a common stock repurchase program. That program was subsequently modified and expanded, most recently on July 28, 2016. Under the modified common stock repurchase program, the Company may purchase up to $400.0 million of its common stock through the period ending June 30, 2018. During the nine months ended December 31, 2017, the Company repurchased 1.6 million shares of its common stock for $39.4 million. Through December 31, 2017, the Company had repurchased a total

13

of 18.4 million shares of its stock for $325.2 million, leaving remaining capacity of $74.8 million under the stock repurchase program.

Accumulated Other Comprehensive Income

Accumulated other comprehensive income accumulated balances of $9.8 million and $8.0 million at December 31, 2017 and March 31, 2017, respectively, reflect accumulated foreign currency translation adjustments.

3. SHARE-BASED COMPENSATION:

Share-based Compensation Plans

The Company has stock option and equity compensation plans for which a total of 34.5 million shares of the Company’s common stock have been reserved for issuance since the inception of the plans. These plans provide that the exercise prices of qualified options will be at or above the fair market value of the common stock at the time of the grant. Board policy requires that nonqualified options also be priced at or above the fair market value of the common stock at the time of grant. At December 31, 2017, there were a total of 6.2 million shares available for future grants under the plans.

During the quarter ended June 30, 2017, the Board voted to amend the Amended and Restated 2005 Equity Compensation Plan to increase the number of shares available under the plan from 28.4 million shares to 32.9 million shares, bringing the total number of shares reserved for issuance since inception of the plans from 30.0 million shares at March 31, 2017 to 34.5 million shares at December 31, 2017. That amendment received shareholder approval at the August 8, 2017 annual shareholders' meeting.

Stock Option Activity

Stock option activity for the nine months ended December 31, 2017 was:

Weighted-average | |||||||||||||

Weighted-average | remaining | Aggregate | |||||||||||

Number of | exercise price | contractual term | Intrinsic value | ||||||||||

shares | per share | (in years) | (in thousands) | ||||||||||

Outstanding at March 31, 2017 | 3,033,071 | $ | 13.14 | ||||||||||

Performance units converted to options | 299,641 | $ | 21.32 | ||||||||||

Exercised | (526,842 | ) | $ | 15.05 | $ | 6,044 | |||||||

Forfeited or canceled | (88,870 | ) | $ | 20.08 | |||||||||

Outstanding at December 31, 2017 | 2,717,000 | $ | 13.45 | 5.7 | $ | 38,448 | |||||||

Exercisable at December 31, 2017 | 2,109,993 | $ | 13.53 | 5.1 | $ | 29,701 | |||||||

The aggregate intrinsic value at period end represents the total pre-tax intrinsic value (the difference between Acxiom’s closing stock price on the last trading day of the period and the exercise price for each in-the-money option) that would have been received by the option holders had option holders exercised their options on December 31, 2017. This amount changes based upon changes in the fair market value of Acxiom’s common stock.

A summary of stock options outstanding and exercisable as of December 31, 2017 was:

Options outstanding | Options exercisable | |||||||||||||||||||||||

Range of | Weighted-average | Weighted-average | Weighted-average | |||||||||||||||||||||

exercise price | Options | remaining | exercise price | Options | exercise price | |||||||||||||||||||

per share | outstanding | contractual life | per share | exercisable | per share | |||||||||||||||||||

$ | 0.61 | — | $ | 9.99 | 690,169 | 6.4 years | $ | 1.68 | 474,434 | $ | 1.77 | |||||||||||||

$ | 10.00 | — | $ | 19.99 | 1,262,595 | 4.9 years | $ | 14.94 | 1,076,909 | $ | 14.47 | |||||||||||||

$ | 20.00 | — | $ | 24.99 | 744,684 | 6.6 years | $ | 21.31 | 539,098 | $ | 21.33 | |||||||||||||

$ | 25.00 | — | $ | 32.85 | 19,552 | 5.9 years | $ | 32.85 | 19,552 | $ | 32.85 | |||||||||||||

2,717,000 | 5.7 years | $ | 13.45 | 2,109,993 | $ | 13.53 | ||||||||||||||||||

14

Total expense related to stock options for the nine months ended December 31, 2017 and 2016 was approximately $4.1 million and $5.4 million, respectively. Future expense for these options is expected to be approximately $7.1 million in total over the next four years.

Performance Stock Option Unit Activity

Performance stock option unit activity for the nine months ended December 31, 2017 was:

Weighted-average | ||||||||||||||

Weighted-average | remaining | Aggregate | ||||||||||||

Number | exercise price | contractual term | intrinsic value | |||||||||||

of shares | per share | (in years) | (in thousands) | |||||||||||

Outstanding at March 31, 2017 | 555,123 | $ | 21.41 | |||||||||||

Performance units converted to options | (183,322 | ) | $ | 21.41 | ||||||||||

Forfeited or canceled | (25,201 | ) | $ | 21.32 | ||||||||||

Outstanding at December 31, 2017 | 346,600 | $ | 21.41 | 1.9 | $ | 2,131 | ||||||||

Exercisable at December 31, 2017 | — | $ | — | — | $ | — | ||||||||

Of the performance stock option units outstanding at March 31, 2017, 183,322 reached maturity of the relevant performance period at March 31, 2017. During the quarter ended June 30, 2017, the units vested at an approximate 163% attainment level resulting in issuance of 299,641 stock options having a weighted average exercise price of $21.32.

Total expense related to performance stock option units for the nine months ended December 31, 2017 and 2016 was $0.9 million and $1.0 million, respectively. Future expense for these performance stock option units is expected to be approximately $2.1 million in total over the next four years.

Stock Appreciation Right ("SAR") Activity

SAR activity for the nine months ended December 31, 2017 was:

Weighted-average | ||||||||||||||

Weighted-average | remaining | Aggregate | ||||||||||||

Number | exercise price | contractual term | intrinsic value | |||||||||||

of shares | per share | (in years) | (in thousands) | |||||||||||

Outstanding at March 31, 2017 | 245,404 | $ | 40.00 | |||||||||||

Forfeited or canceled | (245,404 | ) | $ | 40.00 | ||||||||||

Outstanding at December 31, 2017 | — | $ | — | — | $ | — | ||||||||

All of the SAR units outstanding at March 31, 2017 reached maturity of the relevant performance period on March 31, 2017. The units achieved a 100% performance attainment level. However, application of the vesting multiplier resulted in zero shares granted and cancellation of all the units during the quarter ended June 30, 2017.

Restricted Stock Unit Activity

During the nine months ended December 31, 2017, the Company granted time-vesting restricted stock units covering 1,687,416 shares of common stock with a fair value at the date of grant of $44.2 million. Of the restricted stock units granted in the current period, 358,812 vest in equal annual increments over four years, 106,571 vest in equal annual increments over three years, 1,008,851 vest 25% at the one-year anniversary and 75% in equal quarterly increments over the subsequent three years, 174,368 vest 50% at the one-year anniversary and 50% in equal quarterly increments over the following year, and 38,814 vest in one year. Grant date fair value of these units is equal to the quoted market price for the shares on the date of grant.

15

Non-vested time-vesting restricted stock unit activity for the nine months ended December 31, 2017 was:

Weighted-average | |||||||||

fair value per | Weighted-average | ||||||||

Number | share at grant | remaining contractual | |||||||

of shares | date | term (in years) | |||||||

Outstanding at March 31, 2017 | 3,307,577 | $ | 22.57 | 2.45 | |||||

Granted | 1,687,416 | $ | 26.17 | ||||||

Vested | (1,067,370 | ) | $ | 22.30 | |||||

Forfeited or canceled | (345,581 | ) | $ | 23.36 | |||||

Outstanding at December 31, 2017 | 3,582,042 | $ | 24.27 | 2.48 | |||||

During the nine months ended December 31, 2017, the Company granted performance-based restricted stock units covering 425,880 shares of common stock having a fair value at the date of grant of $11.2 million. Of the performance-based restricted stock units granted in the current period, 221,746 units - having a fair value at the date of grant of $6.2 million, determined using a Monte Carlo simulation model - vest subject to attainment of performance criteria established by the compensation committee of the board of directors (“compensation committee”) and continuous employment through the vesting date. The 221,746 units may vest in a number of shares from zero to 200% of the award, based on the total shareholder return of Acxiom common stock compared to total shareholder return of a group of peer companies (“TSR”) established by the compensation committee for the period from April 1, 2017 to March 31, 2020.

Of the performance-based restricted stock units granted in the current period, 87,184 units - having a fair value at the date of grant of $2.1 million, based on the quoted market price for the shares on the date of grant - vest over two periods, each being subject to attainment of performance criteria established by the compensation committee and continuous employment through the vesting date. At the end of the first year, the performance units may vest in a number of shares, from zero to 75% of the initial award. At the end of the second year, the performance units may vest in a number of shares, from zero to 150% of the initial award, less the number of shares awarded at completion of year one. The units will vest based on the attainment of certain revenue growth initiatives for the period from October 1, 2017 to September 30, 2019.

The remaining 116,950 performance-based restricted stock units granted in the current period - having a fair value at the date of grant of $2.9 million, based on the quoted market price for the shares on the date of grant - vest in three equal tranches, each being subject to attainment of performance criteria established by the compensation committee and continuous employment through the vesting date. Each of the three tranches may vest in a number of shares, from zero to 300% of the initial award, based on the attainment of certain revenue growth and operating margin targets for the years ending March 31, 2018, 2019, and 2020, respectively.

Non-vested performance-based restricted stock unit activity for the nine months ended December 31, 2017 was:

Weighted-average | |||||||||

fair value per | Weighted-average | ||||||||

Number | share at grant | remaining contractual | |||||||

of shares | date | term (in years) | |||||||

Outstanding at March 31, 2017 | 732,711 | $ | 20.89 | 1.13 | |||||

Granted | 425,880 | $ | 26.22 | ||||||

Additional earned performance shares | 94,775 | $ | 19.46 | ||||||

Vested | (252,760 | ) | $ | 19.46 | |||||

Forfeited or canceled | (48,422 | ) | $ | 22.00 | |||||

Outstanding at December 31, 2017 | 952,184 | $ | 23.45 | 1.37 | |||||

16

Of the performance-based restricted stock units outstanding at March 31, 2017, 157,985 related to a performance period ended March 31, 2017. During the quarter ended June 30, 2017, the units vested at a 160% attainment level based on performance results approved by the compensation committee, resulting in issuance of 252,760 shares of common stock, of which 94,775 were the additional earned performance shares referenced in the table above.

Of the performance-based restricted stock units outstanding at December 31, 2017, 251,399 will reach maturity of the relevant performance period at March 31, 2018. The units are expected to vest at an approximate 200% attainment level, resulting in issuance of approximately 502,798 shares of common stock, before consideration of the TSR multiplier, in the first quarter of fiscal 2019.

Total expense related to restricted stock for the nine months ended December 31, 2017 and 2016 was approximately $29.5 million and $24.4 million, respectively. Future expense for restricted stock units is expected to be approximately $11.8 million for the three months ending March 31, 2018, $36.0 million in fiscal 2019, $24.6 million in fiscal 2020, $11.7 million in fiscal 2021, and $2.0 million in fiscal 2022.

Other Performance Unit Activity

Other performance-based stock unit activity for the nine months ended December 31, 2017 was:

Weighted-average | |||||||||

fair value per | Weighted-average | ||||||||

Number | share at grant | remaining contractual | |||||||

of shares | date | term (in years) | |||||||

Outstanding at March 31, 2017 | 597,193 | $ | 4.14 | 0.30 | |||||

Vested | (24,573 | ) | $ | 2.94 | |||||

Forfeited or canceled | (461,509 | ) | $ | 3.92 | |||||

Outstanding at December 31, 2017 | 111,111 | $ | 5.33 | 0.25 | |||||

Of the other performance-based stock units outstanding at March 31, 2017, 201,464 reached maturity of the relevant performance period on March 31, 2017. The units achieved a 100% performance attainment level. However, application of the share price adjustment factor resulted in zero shares granted and cancellation of all the units during the quarter ended June 30, 2017.

Of the other performance-based stock units outstanding at March 31, 2017, 284,618 reached maturity of the relevant performance period on June 30, 2017. The units achieved an approximate 9% performance attainment level, resulting in issuance of 24,573 shares of common stock during the quarter ended September 30, 2017.

The remaining 111,111 performance-based units outstanding at December 31, 2017 will reach maturity of the relevant performance period on March 31, 2018. The units are expected to achieve a 100% performance attainment level. However, application of the share price adjustment factor is expected to result in an approximate 75% reduction in shares granted, in the first quarter of fiscal 2019.

Total expense related to other performance units for the nine months ended December 31, 2017 and 2016 was $0.1 million and $0.7 million, respectively. Future expense for these performance units is expected to be approximately $0.1 million over the next three months ending March 31, 2018.

Consideration Holdback

As part of the Company’s acquisition of Arbor in fiscal 2017, $38.3 million of the acquisition consideration otherwise payable with respect to shares of restricted Arbor common stock held by certain key employees was subject to holdback by the Company pursuant to agreements with those employees (each, a “Holdback Agreement”). The consideration holdback vests in 30 equal monthly increments following the date of close, subject to the Arbor key employees' continued employment through each monthly vesting date. At each vesting date, 1/30th of the $38.3 million holdback consideration vests and is settled in shares of Company common stock. The number of shares is based on the then-current market price of the Company common stock.

Total expense related to the Holdback Agreement for the nine months ended December 31, 2017 was approximately $11.5 million.

17

4. DISPOSITION:

Disposition of Impact email business

In fiscal 2017, the Company completed the sale of its Impact email business to Zeta Interactive for total consideration of $22.0 million, including a $4.0 million subordinated promissory note with interest accruing at a rate of 6.0% per annum. The note was paid in full during the quarter ended September 30, 2017. The Company also entered into a separate multi-year contract to provide Zeta Interactive with Connectivity and Audience Solutions services. Prior to the disposition, the Impact email business was included in the Marketing Services segment results. The business did not meet the requirements of a discontinued business; therefore, all financial results are included in continuing operations.

Revenue and income from operations from the disposed Impact email business are shown below (dollars in thousands):

For the three months ended | For the nine months ended | |||||||||||||||

December 31, | December 31, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Revenues | $ | — | $ | — | $ | — | $ | 20,375 | ||||||||

Income from operations | $ | — | $ | — | $ | — | $ | 120 | ||||||||

5. OTHER CURRENT AND NONCURRENT ASSETS:

Other current assets consist of the following (dollars in thousands):

December 31, 2017 | March 31, 2017 | |||||||

Prepaid expenses and other | $ | 28,246 | $ | 25,714 | ||||

Escrow deposit | — | 5,880 | ||||||

Note receivable | — | 4,000 | ||||||

Assets of non-qualified retirement plan | 14,111 | 12,716 | ||||||

Other current assets | $ | 42,357 | $ | 48,310 | ||||

Other noncurrent assets consist of the following (dollars in thousands):

December 31, 2017 | March 31, 2017 | |||||||

Acquired intangible assets, net | $ | 36,183 | $ | 43,884 | ||||

Deferred data acquisition costs | 982 | 1,116 | ||||||

Other miscellaneous noncurrent assets | 6,411 | 6,443 | ||||||

Noncurrent assets | $ | 43,576 | $ | 51,443 | ||||

6. OTHER ACCRUED EXPENSES:

Other accrued expenses consist of the following (dollars in thousands):

December 31, 2017 | March 31, 2017 | |||||||

Accrued purchase consideration | $ | — | $ | 5,880 | ||||

Liabilities of non-qualified retirement plan | 14,111 | 12,716 | ||||||

Other accrued expenses | 39,888 | 41,265 | ||||||

Other accrued expenses | $ | 53,999 | $ | 59,861 | ||||

18

7. GOODWILL:

The following table summarizes Goodwill activity, by segment, for the nine months ended December 31, 2017 (dollars in thousands):

Marketing Services | Audience Solutions | Connectivity | Total | |||||||||||||

Balance at March 31, 2017 | $ | 118,890 | $ | 273,448 | $ | 200,393 | $ | 592,731 | ||||||||

Arbor adjustment | — | — | (21 | ) | (21 | ) | ||||||||||

Change in foreign currency translation adjustment | 82 | — | 35 | 117 | ||||||||||||

Balance at December 31, 2017 | $ | 118,972 | $ | 273,448 | $ | 200,407 | $ | 592,827 | ||||||||

Goodwill by component included in each segment as of December 31, 2017 was:

Marketing Services | Audience Solutions | Connectivity | Total | |||||||||||||

U.S. | $ | 110,910 | $ | 273,448 | $ | 196,812 | $ | 581,170 | ||||||||

APAC | 8,062 | — | 3,595 | 11,657 | ||||||||||||

Balance at December 31, 2017 | $ | 118,972 | $ | 273,448 | $ | 200,407 | $ | 592,827 | ||||||||

8. LONG-TERM DEBT:

Long-term debt consists of the following (dollars in thousands):

December 31, 2017 | March 31, 2017 | |||||||

Term loan credit agreement | $ | — | $ | 155,000 | ||||

Revolving credit borrowings | 230,000 | 70,000 | ||||||

Other debt | 3,881 | 5,612 | ||||||

Total long-term debt | 233,881 | 230,612 | ||||||

Less current installments | 1,837 | 39,819 | ||||||

Less deferred debt financing costs | 4,101 | 1,552 | ||||||

Long-term debt, excluding current installments and deferred debt financing costs | $ | 227,943 | $ | 189,241 | ||||

On June 20, 2017, the Company entered into a Sixth Amended and Restated Credit Agreement (the "restated credit agreement") as part of refinancing its prior credit agreement. On that day, the Company used an initial draw of $230 million to pay off the outstanding $225 million term and revolving loan balances, with interest, along with $4.0 million in fees related to the restated credit agreement. The fees are being amortized over the term of the agreement.

The Company's restated credit agreement provides for (1) revolving credit facility borrowings consisting of revolving loans, letters of credit participation, and swing-line loans (the “revolving loans”) in an aggregate amount of $600 million and (2) a provision allowing the Company to request an increase of the aggregate amount of the revolving loans in an amount not to exceed $150 million. The restated credit agreement is secured by the accounts receivable of the Company and its domestic subsidiaries, as well as by the outstanding stock of certain subsidiaries of the Company. The restated credit agreement contains customary representations, warranties, affirmative and negative covenants, and default and acceleration provisions. The restated credit agreement matures, and is fully due and payable, on June 20, 2022 and allows for prepayments before maturity.

19

The revolving loan borrowings bear interest at LIBOR or at an alternative base rate plus a credit spread. At December 31, 2017, the revolving loan borrowing bears interest at LIBOR plus a credit spread of 2%. The weighted-average interest rate on revolving credit borrowings at December 31, 2017 was 3.6%. There were no material outstanding letters of credit at December 31, 2017 or March 31, 2017.

Under the terms of the restated credit agreement, the Company is required to maintain certain debt-to-cash flow and interest coverage ratios, among other restrictions. At December 31, 2017, the Company was in compliance with these covenants and restrictions.

9. ALLOWANCE FOR DOUBTFUL ACCOUNTS:

Trade accounts receivable are presented net of allowances for doubtful accounts, returns and credits of $6.3 million at December 31, 2017 and $6.1 million at March 31, 2017.

10. SEGMENT INFORMATION:

The Company reports segment information consistent with the way management internally disaggregates its operations to assess performance and to allocate resources.

Revenues and cost of revenue are generally directly attributed to the segments. Certain revenue contracts are allocated among the segments based on the relative value of the underlying products and services. Cost of revenue, excluding non-cash stock compensation expense and purchased intangible asset amortization, is directly charged in most cases and allocated in certain cases based upon proportional usage.

Operating expenses, excluding non-cash stock compensation expense and purchased intangible asset amortization, are attributed to the segment groups as follows:

• | Research and development expenses are primarily directly recorded to each segment group based on identified products supported. |

• | Sales and marketing expenses are primarily directly recorded to each segment group based on products supported and sold. |

• | General and administrative expenses are generally not allocated to the segments unless directly attributable. |

• | Gains, losses and other items, net are not allocated to the segment groups. |

We do not track our assets by operating segments. Consequently, it is not practical to show assets by operating segment.

20

The following table presents information by business segment (dollars in thousands):

For the three months ended | For the nine months ended | |||||||||||||||

December 31, | December 31, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Revenues: | ||||||||||||||||

Marketing Services | $ | 94,457 | $ | 101,177 | $ | 280,093 | $ | 316,571 | ||||||||

Audience Solutions | 84,436 | 83,399 | 238,984 | 235,669 | ||||||||||||

Connectivity | 55,978 | 38,736 | 153,548 | 103,140 | ||||||||||||

Total segment revenues | $ | 234,871 | $ | 223,312 | $ | 672,625 | $ | 655,380 | ||||||||

Gross profit(1): | ||||||||||||||||

Marketing Services | $ | 35,798 | $ | 37,494 | $ | 101,476 | $ | 109,440 | ||||||||

Audience Solutions | 52,821 | 53,120 | 148,352 | 143,030 | ||||||||||||

Connectivity | 37,914 | 23,091 | 100,730 | 60,509 | ||||||||||||

Total segment gross profit | $ | 126,533 | $ | 113,705 | $ | 350,558 | $ | 312,979 | ||||||||

Income from operations(1): | ||||||||||||||||

Marketing Services | $ | 22,063 | $ | 21,127 | $ | 63,721 | $ | 61,109 | ||||||||

Audience Solutions | 33,112 | 34,572 | 91,151 | 89,640 | ||||||||||||

Connectivity | 6,808 | 1,877 | 12,475 | 3,831 | ||||||||||||

Total segment income from operations | $ | 61,983 | $ | 57,576 | $ | 167,347 | $ | 154,580 | ||||||||

(1) Gross profit and income from operations reflect only the direct and allocable controllable costs of each segment and do not include allocations of corporate expenses (primarily general and administrative expenses) and gains, losses, and other items, net. Additionally, segment gross profit and income from operations do not include non-cash stock compensation expense and purchased intangible asset amortization.

The following table reconciles total segment gross profit to gross profit and total operating segment income from operations to income from operations (dollars in thousands):

For the three months ended | For the nine months ended | |||||||||||||||

December 31, | December 31, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Total segment gross profit | $ | 126,533 | $ | 113,705 | $ | 350,558 | $ | 312,979 | ||||||||

Less: | ||||||||||||||||

Purchased intangible asset amortization | 5,971 | 4,621 | 17,958 | 12,588 | ||||||||||||

Non-cash stock compensation | 1,611 | 2,240 | 4,927 | 4,403 | ||||||||||||

Gross profit | $ | 118,951 | $ | 106,844 | $ | 327,673 | $ | 295,988 | ||||||||

Total segment income from operations | $ | 61,983 | $ | 57,576 | $ | 167,347 | $ | 154,580 | ||||||||

Less: | ||||||||||||||||

Corporate expenses (principally general and administrative) | 23,862 | 24,184 | 75,582 | 75,342 | ||||||||||||

Separation and transformation costs included in general and administrative | 5,214 | 4,118 | 17,775 | 5,573 | ||||||||||||

Gains, losses and other items, net | (41 | ) | 2,111 | 3,521 | 2,725 | |||||||||||

Purchased intangible asset amortization | 5,971 | 4,621 | 17,958 | 12,588 | ||||||||||||

Non-cash stock compensation | 15,919 | 13,427 | 46,707 | 33,955 | ||||||||||||

Income from operations | $ | 11,058 | $ | 9,115 | $ | 5,804 | $ | 24,397 | ||||||||

21

11. RESTRUCTURING, IMPAIRMENT AND OTHER CHARGES:

The following table summarizes the restructuring activity for the nine months ended December 31, 2017 (dollars in thousands):

Associate-related reserves | Lease accruals | Total | ||||||||||

March 31, 2017 | $ | 2,400 | $ | 4,308 | $ | 6,708 | ||||||

Restructuring charges and adjustments | 1,476 | 2,068 | 3,544 | |||||||||

Payments | (2,842 | ) | (1,187 | ) | (4,029 | ) | ||||||

December 31, 2017 | $ | 1,034 | $ | 5,189 | $ | 6,223 | ||||||

The above balances are included in other accrued expenses and other liabilities on the condensed consolidated balance sheet.

Restructuring Plans

In the nine months ended December 31, 2017, the Company recorded a total of $3.5 million in restructuring charges and adjustments included in gains, losses and other items, net in the condensed consolidated statement of operations. The expense included severance and other associate-related charges of $1.5 million, lease accruals and adjustments of $1.0 million, and leasehold improvement write-offs of $1.1 million.

The associate-related accruals of $1.5 million relate to the termination of associates in the United States. Of the amount accrued, $0.3 million remained accrued as of December 31, 2017. These costs are expected to be paid out in fiscal 2018.

The lease accruals and adjustments of $1.0 million result from the Company's exit from certain leased office facilities. Of the amount accrued, together with the deferred rent credits of $1.4 million related to the space, $2.1 million remained accrued as of December 31, 2017.

In fiscal 2017, the Company recorded a total of $8.9 million in restructuring charges and adjustments included in gains, losses and other items, net in the condensed consolidated statement of operations. The expense included severance and other associate-related charges of $3.8 million, lease accruals and adjustments of $3.0 million, and leasehold improvement write-offs of $2.1 million. Of the associate-related accruals of $3.8 million, $0.2 million remained accrued as of December 31, 2017. These costs are expected to be paid out in fiscal 2018. The lease accruals and adjustments of $3.0 million resulted from the Company's exit from certain leased office facilities ($1.5 million) and adjustments to estimates related to the fiscal 2015 lease accruals ($1.5 million). Of the amount accrued for fiscal 2017 lease accruals, $2.3 million remained accrued as of December 31, 2017.

In fiscal 2016, the Company recorded a total of $12.0 million in restructuring charges and adjustments included in gains, losses and other items, net in the condensed consolidated statement of operations. The expense included severance and other associate-related charges of $8.6 million, lease termination charges and accruals of $3.0 million, and leasehold improvement write-offs of $0.4 million. Of the associate-related accruals of $8.6 million, $0.2 million remained accrued as of December 31, 2017. These amounts are expected to be paid out in fiscal 2018. The lease termination charges and accruals of $3.0 million were fully paid during fiscal 2016.

In fiscal 2015, the Company recorded a total of $21.8 million in restructuring charges and adjustments included in gains, losses and other items, net in the condensed consolidated statement of operations. The expense included severance and other associate-related charges of $13.3 million, lease accruals of $6.5 million, and the write-off of leasehold improvements of $2.0 million. Of the associate-related accruals of $13.3 million, $0.3 million remained accrued as of December 31, 2017. These amounts are expected to be paid out in fiscal 2018. Of the lease accruals of $6.5 million, $0.8 million remained accrued as of December 31, 2017.

With respect to the fiscal 2015, 2017, and 2018 lease accruals described above, the Company intends to sublease the facilities to the extent possible. The liabilities will be satisfied over the remainder of the leased properties' terms, which continue through November 2025. Actual sublease receipts may differ from the estimates originally made by

22

the Company. Any future changes in the estimates or in the actual sublease income could require future adjustments to the liabilities, which would impact net earnings (loss) in the period the adjustment is recorded.

Gains, Losses and Other Items

Gains, losses and other items for each of the periods presented are as follows (dollars in thousands):

For the three months ended | For the nine months ended | |||||||||||||||

December 31, | December 31, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Restructuring plan charges and adjustments | $ | (18 | ) | $ | 899 | $ | 3,545 | $ | 2,107 | |||||||

Gain on disposition of Impact email business | — | (155 | ) | — | (784 | ) | ||||||||||

Arbor and Circulate acquisition-related costs | — | 1,365 | — | 1,365 | ||||||||||||

Other | (23 | ) | 2 | (24 | ) | 36 | ||||||||||

$ | (41 | ) | $ | 2,111 | $ | 3,521 | $ | 2,724 | ||||||||

12. COMMITMENTS AND CONTINGENCIES:

Legal Matters

The Company is involved in various claims and legal proceedings. Management routinely assesses the likelihood of adverse judgments or outcomes to these matters, as well as ranges of probable losses, to the extent losses are reasonably estimable. The Company records accruals for these matters to the extent that management concludes a loss is probable and the financial impact, should an adverse outcome occur, is reasonably estimable. These accruals are reflected in the Company’s condensed consolidated financial statements. In management’s opinion, the Company has made appropriate and adequate accruals for these matters, and management believes the probability of a material loss beyond the amounts accrued to be remote. However, the ultimate liability for these matters is uncertain, and if accruals are not adequate, an adverse outcome could have a material effect on the Company’s consolidated financial condition or results of operations. The Company maintains insurance coverage above certain limits. There are currently no matters pending against the Company or its subsidiaries for which the potential exposure is considered material to the Company’s condensed consolidated financial statements.

Commitments

The Company leases data processing equipment, office furniture and equipment, land and office space under noncancellable operating leases. The Company has a future commitment for lease payments over the next 23 years of $84.5 million.

In connection with the Impact email disposition during fiscal 2017, the Company assigned a facility lease to the buyer of the business. The Company guaranteed the facility lease as required by the asset disposition agreement. Should the assignee default, the Company would be required to perform under the terms of the facility lease, which continues through September 2021. At December 31, 2017, the Company’s maximum potential future rent payments under this guarantee totaled $2.3 million.

13. INCOME TAX:

On December 22, 2017, the United States (“U.S.”) enacted significant changes to U.S. tax law following the passage of H.R.1, “An Act to Provide for Reconciliation Pursuant to Titles II and V of the Concurrent Resolution on the Budget for Fiscal Year 2018” (the “Tax Act”) (previously known as “The Tax Cuts and Jobs Act”). The Tax Act included significant changes to existing tax law, including a permanent reduction to the U.S. federal corporate income tax rate from 35% to 21%, a one-time repatriation tax on deferred foreign income (“Transition Tax”), and numerous other changes to business-related deductions.

The permanent reduction to the U.S. federal corporate income tax rate from 35% to 21% is effective January 1, 2018 (the “Effective Date”). Because the Effective Date does not fall on the first day of our fiscal year, we are required to apply a blended tax rate for the entire fiscal year by applying a prorated percentage of the number of

23

days before and after the Effective Date. As a result of the Tax Act, we have determined that our U.S. federal statutory corporate income tax rate will be 31.5% for the fiscal year ending March 31, 2018.

We recorded a $20.3 million benefit for the remeasurement of net deferred tax liabilities, which was included in income tax expense (benefit) in the Company's Condensed Consolidated Statements of Operations. We remeasured our deferred taxes to reflect the reduced Federal tax rate that will apply when these deferred taxes are settled or realized in future periods. To calculate the remeasurement of deferred taxes we estimated the periods during which the existing deferred taxes will be settled or realized. The remeasurement of deferred taxes included in our condensed consolidated financial statements will be subject to further revisions if our current estimates are different from our actual future operating results.

Given the Company's aggregate deficit related to foreign earnings and profits, we have determined that the Company will not incur a Transition Tax liability.

On December 22, 2017, the SEC issued Staff Accounting Bulletin 118 (“SAB 118”) which provides guidance on accounting for the tax effects of the Tax Act. The SEC staff (the “Staff”) recognized that a registrant’s review of certain income tax effects of the Tax Act may be incomplete at the time financial statements are issued for the reporting period that includes the enactment date, including interim periods therein. If a company does not have the necessary information available, prepared or analyzed for certain income tax effects of the Tax Act, SAB 118 allows a company to report provisional numbers and adjust those amounts during the measurement period not to extend beyond one year. The adjustments to net deferred tax liabilities are provisional amounts estimated based on information available as of December 31, 2017. These amounts are subject to change as we obtain information necessary to complete the calculations. We will recognize any changes to the provisional amounts as we refine our estimates of the cumulative temporary differences, including those related to immediate deduction for qualified property, and our interpretations of the application of the Tax Act.

We continue to review the anticipated impacts of the global intangible low taxed income (“GILTI”) and base erosion anti-abuse tax (“BEAT”) on the Company, which are not effective until fiscal year 2019. The Company has not recorded any impact associated with either GILTI or BEAT in the tax rate for the third quarter of fiscal year 2018.

Within the calculation of its annual effective tax rate the Company has used assumptions and estimates that may change as a result of future guidance, interpretation, and rule-making from the Internal Revenue Service, the SEC, and the FASB and/or various other taxing jurisdictions. For example, the Company anticipates that the U.S. state jurisdictions will continue to determine and announce their conformity to the Tax Act, which could have an impact on the annual effective tax rate.

In determining the quarterly provision for income taxes, the Company makes its best estimate of the effective income tax rate expected to be applicable for the full fiscal year. The estimated effective income tax rate for the current fiscal year is impacted by nondeductible stock-based compensation, state income taxes, research tax credits, and losses in foreign jurisdictions. State income taxes are influenced by the geographic and legal entity mix of the Company’s U.S. income as well as the diversity of rules among the states. The Company does not record a tax benefit for certain foreign losses due to uncertainty of future utilization.

As a result of adopting ASU 2016–09 during the first quarter of the current fiscal year, all excess tax benefits and deficiencies from stock–based compensation are recognized as income tax benefit and expense in the Company’s Condensed Consolidated Statement of Operations in the reporting period in which they occur. For the three months and nine months ended December 31, 2017, the Company recognized discrete income tax expense of $0.1 million and benefit of $1.9 million, respectively, related to net excess tax benefits and deficiencies.

14. FAIR VALUE OF FINANCIAL INSTRUMENTS:

The following methods and assumptions were used to estimate the fair value of each class of financial instruments for which it is practicable to estimate that value.

Cash and cash equivalents, trade receivables, unbilled and notes receivable, short-term borrowings and trade payables - The carrying amount approximates fair value because of the short maturity of these instruments.

Long-term debt - The interest rate on the revolving credit agreement is adjusted for changes in market rates and therefore the carrying value approximates fair value. The estimated fair value of other long-term debt was

24

determined based upon the present value of the expected cash flows considering expected maturities and using interest rates currently available to the Company for long-term borrowings with similar terms. At December 31, 2017, the estimated fair value of long-term debt approximates its carrying value.

Under applicable accounting standards financial assets and liabilities are classified in their entirety based on the lowest level of input that is significant to the fair value measurements. The Company assigned assets and liabilities to the hierarchy in the accounting standards, which is Level 1 - quoted prices in active markets for identical assets or liabilities, Level 2 - significant other observable inputs and Level 3 - significant unobservable inputs.

The following table presents the balances of assets measured at fair value as of December 31, 2017 (dollars in thousands):

Level 1 | Level 2 | Level 3 | Total | |||||||||||||

Assets: | ||||||||||||||||

Other current assets | $ | 14,111 | $ | — | $ | — | $ | 14,111 | ||||||||

Total assets | $ | 14,111 | $ | — | $ | — | $ | 14,111 | ||||||||

25

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

We begin Management’s Discussion and Analysis of Financial Condition and Results of Operations with an overview of our operating segments, summary financial results and notable events. This overview is followed by a summary of our critical accounting policies and estimates that we believe are important to understanding the assumptions and judgments incorporated in our reported financial results. We then provide a more detailed analysis of our results of operations and financial condition.

Introduction and Overview

Acxiom Corporation is a global technology and enablement services company with a vision to transform data into value for everyone. Through a simple, open approach to connecting systems and data, we provide the data foundation for the world’s best marketers. By making it safe and easy to activate, validate, enhance, and unify data, we provide marketers with the ability to deliver relevant messages at scale and tie those messages back to actual results. Our products and services enable people-based marketing, allowing our clients to generate higher return on investment and drive better omnichannel customer experiences.

Acxiom is a Delaware corporation founded in 1969 in Conway, Arkansas. Our common stock is listed on the NASDAQ Global Select Market under the symbol “ACXM.” We serve a global client base from locations in the United States, Europe, and the Asia-Pacific (“APAC”) region. Our client list includes many of the world’s largest and best-known brands across most major industry verticals, including but not limited to financial, insurance and investment services, automotive, retail, telecommunications, high tech, healthcare, travel, entertainment, non-profit, and government.

Operating Segments

Our operating segments provide management with a comprehensive view of our key businesses based on how we manage our operations and measure results. Additional information related to our operating segments and geographic information is contained in Note 10 - Segment Information of the Notes to Condensed Consolidated Financial Statements.

Connectivity

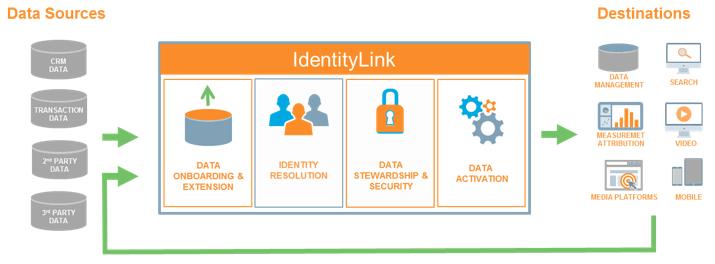

As shown in the illustration below, our Connectivity segment enables our clients to build an omnichannel view of the consumer and activate that understanding across the marketing ecosystem.

Through integrations with more than 550 leading digital marketing platforms and data providers, we have become a key point of entry into the digital ecosystem, helping our clients eliminate data silos and unlock greater value from the marketing tools they use every day. We provide a foundational identity resolution layer enabling our clients to identify and reach consumers across channels and measure the impact of marketing on sales, using the marketing platform of their choice.

Today, our primary Connectivity offering is LiveRamp IdentityLink, an identity resolution service that ties data back to real people and makes it possible to onboard that data for people-based marketing initiatives across digital channels. Leveraging AbiliTec and the LiveRamp identity graph, IdentityLink first resolves a client’s first-, second-,

26

and third-party exposure, and transaction data to persistent anonymous consumer identifiers that represent real people in a privacy-safe way. This omnichannel view of the consumer can then be onboarded to and between any of the 550 plus partners in our ecosystem to support targeting, personalization and measurement use cases.

Targeting | Personalization | Measurement |

|  |  |

Example | Example | Example |

Clients can upload known data from first-, second-, and third-party data sources, resolve it to an omnichannel privacy-safe link with IdentityLink, then onboard to one of 550+ LiveRamp partners to deploy targeted ads to known customers. | Clients can deliver highly relevant content the moment viewers visit their website landing page, no login required. Leveraging IdentityLink, clients can resolve customer segment data to devices and digital IDs, onboard that data to a personalization platform and provide one-to-one experiences without compromising user privacy. | Clients can connect exposure data with first- and third-party purchase data across channels by resolving all customer devices back to the customers to which they belong. Then, clients can onboard that data to a measurement platform to clearly establish cause, effect and impact. |

IdentityLink operates in an Acxiom SafeHaven® certified environment with technical, operational, and personnel controls designed to ensure our clients’ data is kept private and secure.

IdentityLink is sold to brands and the companies brands partner to execute their marketing, including marketing technology providers, data providers, publishers and agencies.

• | IdentityLink for Brands and Agencies. IdentityLink allows brands and their agencies to execute people-based marketing by creating an omnichannel understanding of the consumer and activating that understanding across their choice of best-of-breed digital marketing platforms. |

• | IdentityLink for Marketing Technology Providers. IdentityLink provides marketing technology providers with the ability to offer people-based targeting, measurement and personalization within their platforms. This adds value for brands by increasing reach, as well as the speed at which they can activate their marketing data. |

• | IdentityLink for Data Owners. IdentityLink allows data owners to easily connect their data to the digital ecosystem and better monetize it. Data can be distributed directly to clients or made available through the IdentityLink Data Store feature. This adds value for brands as it allows them to augment their understanding of consumers, and increase both their reach to and understanding of customers and prospects. |

• | IdentityLink for Publishers. IdentityLink allows publishers to offer people-based marketing on their properties. This adds value for brands by providing direct access to their customers and prospects in the publisher’s premium inventory. |

Our Connectivity revenue consists primarily of monthly recurring subscription fees sold on an annual basis. To a lesser extent, we generate revenue from data providers and certain digital publishers in the form of revenue-sharing agreements.

27

Audience Solutions (“AS”)

Our AS segment helps clients validate the accuracy of their data, enhance it with additional insight, and keep it up to date, enabling clients to reach desired audiences with highly relevant messages. Leveraging our recognition and data assets, clients can identify, segment, and differentiate their audiences for more effective marketing and superior customer experiences. AS offerings include InfoBase, our large consumer data store that serves as the basis for Acxiom’s consumer demographics products, and AbiliTec, our patented identity resolution technology that assists our clients in reconciling and managing variations of customer identity over time and across multiple channels.

• | InfoBase. With more than 1,500 demographic, socio-economic and lifestyle data elements and several thousand predictive models, our InfoBase products provide marketers with the ability to identify and reach the right audience with the right message across both traditional and digital channels. Through partnerships with over 100 online publishers and digital marketing platforms, including Facebook, Google, Twitter, 4INFO, AOL, eBay and MSN, marketers can use InfoBase data to create and target specific audiences. Data can be accessed directly or through the Acxiom Audience Cloud, a web-based, self-service tool that makes it easy to build and distribute third-party custom data segments. |

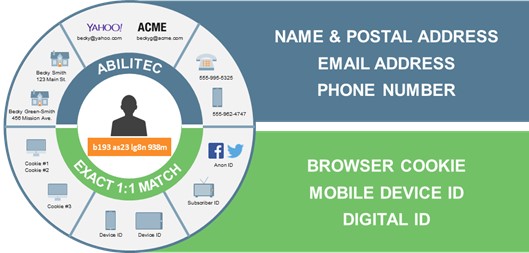

• | AbiliTec. As shown in the illustration below, AbiliTec helps brands recognize individuals and households using a number of different input variables and connects identities online and offline. |

By identifying and linking multiple identifiers and data elements back to a persistent ID, our clients are able to create a single view of the customer, which allows them to perform more effective audience targeting and deliver better, more relevant customer experiences.

Our AS revenue includes licensing fees, which are typically in the form of recurring monthly billings, as well as transactional revenue based on volume or one-time usage. In addition, AS generates digital data revenue from certain digital publishers and addressable television providers in the form of revenue sharing agreements. Our Marketing Database clients are a significant channel for our AS offerings.

Marketing Services (“MS”)

Our MS segment helps clients unify data at the individual level in a privacy-safe environment, so they can execute people-based marketing campaigns, tie back to real results, and drive a continual cycle of optimization. We help architect the foundation for data-driven marketing by delivering solutions that integrate customer and prospect data across the enterprise, thereby enabling our clients to establish a single view of the customer. We also support our clients in navigating the complexities of consumer privacy regulation, making it easy and safe for them to use innovative technology, maintain choice in channels and media, and stay agile in this competitive era of the consumer. These services allow our clients to generate higher return on marketing investments and, at the same time, drive better, more relevant customer experiences.

The MS segment includes the following service offerings: Marketing Database Services and Strategy and Analytics. The MS segment also included Impact Email Platform and Services until the disposition of the business in August 2016.

28

• | Marketing Database Services. Our Marketing Database offering provides solutions that unify consumer data across an enterprise, enabling clients to execute relevant, people-based marketing and activate data across the marketing ecosystem. Our consumer marketing databases, which we design, build, and manage for our clients, make it possible for our clients to collect and analyze information from all sources, thereby increasing customer acquisition, retention, and loyalty. Through our growing partner network, clients are able to integrate their data with best-of-breed marketing solutions while respecting and protecting consumer privacy. |

Marketing Database Services are generally provided under long-term contracts. Our revenue consists primarily of recurring monthly billings, and to a lesser extent, other volume and variable based billings.