UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________________

FORM 10-K

_______________________________

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2019

or

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to

Commission File Number: 001-32886

_______________________________

(Exact name of registrant as specified in its charter)

_______________________________

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||

(Address of principal executive offices) | (Zip Code) | |||||

Registrant’s telephone number, including area code: (405 ) 234-9000

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading symbol(s) | Name of each exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act: None

_______________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

x | Accelerated filer | ☐ | ||||

Non-accelerated filer | ☐ | Smaller reporting company | ||||

Emerging growth company | ||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2019 was approximately $3.5 billion, based upon the closing price of $42.09 per share as reported by the New York Stock Exchange on such date.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement of Continental Resources, Inc. for the Annual Meeting of Shareholders to be held in May 2020, which will be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year, are incorporated by reference into Part III of this Form 10-K.

Table of Contents

PART I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

Glossary of Crude Oil and Natural Gas Terms

The terms defined in this section may be used throughout this report:

“basin” A large natural depression on the earth’s surface in which sediments generally brought by water accumulate.

“Bbl” One stock tank barrel, of 42 U.S. gallons liquid volume, used herein in reference to crude oil, condensate or natural gas liquids.

“Bcf” One billion cubic feet of natural gas.

“Boe” Barrels of crude oil equivalent, with six thousand cubic feet of natural gas being equivalent to one barrel of crude oil based on the average equivalent energy content of the two commodities.

“Btu” British thermal unit, which represents the amount of energy needed to heat one pound of water by one degree Fahrenheit and can be used to describe the energy content of fuels.

“completion” The process of treating a drilled well followed by the installation of permanent equipment for the production of crude oil and/or natural gas.

“conventional play” An area believed to be capable of producing crude oil and natural gas occurring in discrete accumulations in structural and stratigraphic traps.

“DD&A” Depreciation, depletion, amortization and accretion.

“de-risked” Refers to acreage and locations in which the Company believes the geological risks and uncertainties related to recovery of crude oil and natural gas have been reduced as a result of drilling operations to date. However, only a portion of such acreage and locations have been assigned proved undeveloped reserves and ultimate recovery of hydrocarbons from such acreage and locations remains subject to all risks of recovery applicable to other acreage.

“developed acreage” The number of acres allocated or assignable to productive wells or wells capable of production.

“development well” A well drilled within the proved area of a crude oil or natural gas reservoir to the depth of a stratigraphic horizon known to be productive.

“dry hole” Exploratory or development well that does not produce crude oil and/or natural gas in economically producible quantities.

“enhanced recovery” The recovery of crude oil and natural gas through the injection of liquids or gases into the reservoir, supplementing its natural energy. Enhanced recovery methods are sometimes applied when production slows due to depletion of the natural pressure.

“exploratory well” A well drilled to find crude oil or natural gas in an unproved area, to find a new reservoir in an existing field previously found to be productive of crude oil or natural gas in another reservoir, or to extend a known reservoir beyond the proved area.

“field” An area consisting of a single reservoir or multiple reservoirs all grouped on, or related to, the same individual geological structural feature or stratigraphic condition. The field name refers to the surface area, although it may refer to both the surface and the underground productive formations.

“formation” A layer of rock which has distinct characteristics that differs from nearby rock.

“fracture stimulation” A process involving the high pressure injection of water, sand and additives into rock formations to stimulate crude oil and natural gas production. Also may be referred to as hydraulic fracturing.

“gross acres” or “gross wells” Refers to the total acres or wells in which a working interest is owned.

“held by production” or “HBP” Refers to an oil and gas lease continued into effect into its secondary term for so long as a producing oil and/or gas well is located on any portion of the leased premises or lands pooled therewith.

“horizontal drilling” A drilling technique used in certain formations where a well is drilled vertically to a certain depth and then drilled horizontally within a specified interval.

“MBbl” One thousand barrels of crude oil, condensate or natural gas liquids.

“MBoe” One thousand Boe.

“Mcf” One thousand cubic feet of natural gas.

i

“MMBo” One million barrels of crude oil.

“MMBoe” One million Boe.

“MMBtu” One million British thermal units.

“MMcf” One million cubic feet of natural gas.

“net acres” or “net wells” Refers to the sum of the fractional working interests owned in gross acres or gross wells.

"Net crude oil and natural gas sales" Represents total crude oil and natural gas sales less total transportation expenses. Net crude oil and natural gas sales presented herein is a non-GAAP measure. See Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures for a discussion and calculation of this measure.

"Net sales price" Represents the average net wellhead sales price received by the Company for its crude oil or natural gas sales after deducting transportation expenses. Net sales price is calculated by taking revenues less transportation expenses divided by sales volumes for a period, whether for crude oil or natural gas, as applicable. Net sales prices presented herein for 2018 and 2019 are non-GAAP measures. See Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures for a discussion and calculation of this measure.

“NYMEX” The New York Mercantile Exchange.

“pad drilling” or “pad development” Describes a well site layout which allows for drilling multiple wells from a single pad resulting in less environmental impact and lower per-well drilling and completion costs.

“play” A portion of the exploration and production cycle following the identification by geologists and geophysicists of areas with potential crude oil and natural gas reserves.

“productive well” A well found to be capable of producing hydrocarbons in sufficient quantities such that proceeds from the sale of the production exceed production expenses and taxes.

“prospect” A potential geological feature or formation which geologists and geophysicists believe may contain hydrocarbons. A prospect can be in various stages of evaluation, ranging from a prospect that has been fully evaluated and is ready to drill to a prospect that will require substantial additional seismic data processing and interpretation.

“proved reserves” The quantities of crude oil and natural gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible from a given date forward, from known reservoirs and under existing economic conditions, operating methods, and government regulations prior to the time at which contracts providing the right to operate expire, unless evidence indicates renewal is reasonably certain.

“proved developed reserves” Reserves expected to be recovered through existing wells with existing equipment and operating methods.

“proved undeveloped reserves” or “PUD” Proved reserves expected to be recovered from new wells on undrilled acreage or from existing wells where a relatively major expenditure is required for completion.

“PV-10” When used with respect to crude oil and natural gas reserves, PV-10 represents the estimated future gross revenues to be generated from the production of proved reserves using a 12-month unweighted arithmetic average of the first-day-of-the-month commodity prices for the period of January to December, net of estimated production and future development and abandonment costs based on costs in effect at the determination date, before income taxes, and without giving effect to non-property-related expenses, discounted to a present value using an annual discount rate of 10% in accordance with the guidelines of the Securities and Exchange Commission (“SEC”). PV-10 is not a financial measure calculated in accordance with generally accepted accounting principles (“GAAP”) and generally differs from Standardized Measure, the most directly comparable GAAP financial measure, because it does not include the effects of income taxes on future net revenues. Neither PV-10 nor Standardized Measure represents an estimate of the fair market value of the Company’s crude oil and natural gas properties. The Company and others in the industry use PV-10 as a measure to compare the relative size and value of proved reserves held by companies without regard to the specific tax characteristics of such entities.

“reservoir” A porous and permeable underground formation containing a natural accumulation of producible crude oil and/or natural gas that is confined by impermeable rock or water barriers and is separate from other reservoirs.

“residue gas” Refers to gas that has been processed to remove natural gas liquids.

ii

“resource play” Refers to an expansive contiguous geographical area with prospective crude oil and/or natural gas reserves that has the potential to be developed uniformly with repeatable commercial success due to advancements in horizontal drilling and completion technologies.

“royalty interest” Refers to the ownership of a percentage of the resources or revenues produced from a crude oil or natural gas property. A royalty interest owner does not bear exploration, development, or operating expenses associated with drilling and producing a crude oil or natural gas property.

“SCOOP” Refers to the South Central Oklahoma Oil Province, a term used to describe properties located in the Anadarko basin of Oklahoma in which we operate. Our SCOOP acreage extends across portions of Garvin, Grady, Stephens, Carter, McClain and Love counties of Oklahoma and has the potential to contain hydrocarbons from a variety of conventional and unconventional reservoirs overlying and underlying the Woodford formation.

“STACK” Refers to Sooner Trend Anadarko Canadian Kingfisher, a term used to describe a resource play located in the Anadarko Basin of Oklahoma characterized by stacked geologic formations with major targets in the Meramec, Osage and Woodford formations. A significant portion of our STACK acreage is located in over-pressured portions of Blaine, Dewey and Custer counties of Oklahoma.

“spacing” The distance between wells producing from the same reservoir. Spacing is often expressed in terms of acres (e.g., 640-acre spacing) and is often established by regulatory agencies.

“Standardized Measure” Discounted future net cash flows estimated by applying the 12-month unweighted arithmetic average of the first-day-of-the-month commodity prices for the period of January to December to the estimated future production of year-end proved reserves. Future cash inflows are reduced by estimated future production and development costs based on period-end costs to determine pre-tax net cash inflows. Future income taxes, if applicable, are computed by applying the statutory tax rate to the excess of pre-tax cash inflows over the tax basis in the crude oil and natural gas properties. Future net cash inflows after income taxes are discounted using a 10% annual discount rate.

“unconventional play” An area believed to be capable of producing crude oil and natural gas occurring in accumulations that are regionally extensive, but may lack readily apparent traps, seals and discrete hydrocarbon-water boundaries that typically define conventional reservoirs. These areas tend to have low permeability and may be closely associated with source rock, as is the case with oil and gas shale, tight oil and gas sands and coalbed methane, and generally require horizontal drilling, fracture stimulation treatments or other special recovery processes in order to achieve economic production. In general, unconventional plays require the application of more advanced technology and higher drilling and completion costs to produce relative to conventional plays.

“undeveloped acreage” Lease acreage on which wells have not been drilled or completed to a point that would permit the production of commercial quantities of crude oil and/or natural gas.

“unit” The joining of all or substantially all interests in a reservoir or field, rather than a single tract, to provide for development and operation without regard to separate property interests. Also, the area covered by a unitization agreement.

“well bore” The hole drilled by the bit that is equipped for crude oil or natural gas production on a completed well. Also called a well or borehole.

“working interest” The right granted to the lessee of a property to explore for and to produce and own crude oil, natural gas, or other minerals. The working interest owners bear the exploration, development, and operating costs on either a cash, penalty, or carried basis.

iii

Cautionary Statement for the Purpose of the “Safe Harbor” Provisions of the Private Securities Litigation Reform Act of 1995

This report and information incorporated by reference in this report include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements other than statements of historical fact, including, but not limited to, forecasts or expectations regarding the Company’s business and statements or information concerning the Company’s future operations, performance, financial condition, production and reserves, schedules, plans, timing of development, rates of return, budgets, costs, business strategy, objectives, and cash flows, included in this report are forward-looking statements. The words “could,” “may,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project,” “budget,” “target,” “plan,” “continue,” “potential,” “guidance,” “strategy” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words.

Forward-looking statements may include, but are not limited to, statements about:

• | our strategy; |

• | our business and financial plans; |

• | our future operations; |

• | our crude oil and natural gas reserves and related development plans; |

• | technology; |

• | future crude oil, natural gas liquids, and natural gas prices and differentials; |

• | the timing and amount of future production of crude oil and natural gas and flaring activities; |

• | the amount, nature and timing of capital expenditures; |

• | estimated revenues, expenses and results of operations; |

• | drilling and completing of wells; |

• | competition; |

• | marketing of crude oil and natural gas; |

• | transportation of crude oil, natural gas liquids, and natural gas to markets; |

• | property exploitation, property acquisitions and dispositions, or joint development opportunities; |

• | costs of exploiting and developing our properties and conducting other operations; |

• | our financial position or dividend payments; |

• | general economic conditions; |

• | credit markets; |

• | our liquidity and access to capital; |

• | the impact of governmental policies, laws and regulations, as well as regulatory and legal proceedings involving us and of scheduled or potential regulatory or legal changes; |

• | our future operating and financial results; |

• | our future commodity or other hedging arrangements; and |

• | the ability and willingness of current or potential lenders, hedging contract counterparties, customers, and working interest owners to fulfill their obligations to us or to enter into transactions with us in the future on terms that are acceptable to us. |

Forward-looking statements are based on the Company’s current expectations and assumptions about future events and currently available information as to the outcome and timing of future events. Although the Company believes these assumptions and expectations are reasonable, they are inherently subject to numerous business, economic, competitive, regulatory and other risks and uncertainties, most of which are difficult to predict and many of which are beyond the Company’s control. No assurance can be given that such expectations will be correct or achieved or that the assumptions are accurate or will not change over time. The risks and uncertainties that may affect the operations, performance and results of the business and forward-looking statements include, but are not limited to, those risk factors and other cautionary statements described under Part I, Item 1A. Risk Factors and elsewhere in this report, registration statements we file from time to time with the Securities and Exchange Commission, and other announcements we make from time to time.

Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date on which such statement is made. Should one or more of the risks or uncertainties described in this report occur, or should underlying assumptions prove incorrect, the Company’s actual results and plans could differ materially from those expressed in any forward-looking statements. All forward-looking statements are expressly qualified in their entirety by this cautionary statement.

Except as expressly stated above or otherwise required by applicable law, the Company undertakes no obligation to publicly correct or update any forward-looking statement whether as a result of new information, future events or circumstances after the date of this report, or otherwise.

iv

Part I

You should read this entire report carefully, including the risks described under Part I, Item 1A. Risk Factors and our consolidated financial statements and the notes to those consolidated financial statements included elsewhere in this report. Unless the context otherwise requires, references in this report to “Continental Resources,” “Continental,” “we,” “us,” “our,” “ours” or “the Company” refer to Continental Resources, Inc. and its subsidiaries.

Item 1. | Business |

General

We are an independent crude oil and natural gas company formed in 1967 engaged in the exploration, development, and production of crude oil and natural gas in the North, South and East regions of the United States. Additionally, we pursue the acquisition and management of perpetually owned minerals located in our key operating areas. The North region consists of properties north of Kansas and west of the Mississippi River and includes North Dakota Bakken, Montana Bakken, and the Red River units. The South region includes all properties south of Nebraska and west of the Mississippi River including various plays in the SCOOP and STACK areas of Oklahoma. The East region is primarily comprised of undeveloped leasehold acreage east of the Mississippi River with no significant drilling or production operations.

A substantial portion of our operations is located in the North region, with that region comprising 60% of our crude oil and natural gas production and 71% of our crude oil and natural gas revenues for the year ended December 31, 2019. The Company’s principal producing properties in the North region are located in the Bakken field of North Dakota and Montana. Approximately 53% of our proved reserves as of December 31, 2019 are located in the North region. Our operations in the South region continue to expand with our increased activity in Oklahoma and that region comprised 40% of our crude oil and natural gas production, 29% of our crude oil and natural gas revenues, and 47% of our proved reserves as of and for the year ended December 31, 2019.

We focus our activities in large new or developing crude oil and natural gas plays that provide us the opportunity to acquire undeveloped acreage positions for future drilling operations. We have been successful in targeting large repeatable resource plays where three dimensional seismic, horizontal drilling, geosteering technologies, advanced completion technologies (e.g., fracture stimulation), pad/row development, and enhanced recovery technologies allow us to develop and produce crude oil and natural gas reserves from unconventional formations. As a result of these efforts, we have grown substantially through the drill bit.

As of December 31, 2019, our proved reserves were 1,619 MMBoe, with proved developed reserves representing 707 MMBoe, or 44%, of our total proved reserves. The standardized measure of our discounted future net cash flows totaled $10.5 billion at December 31, 2019. For 2019, we generated crude oil and natural gas revenues of $4.51 billion and operating cash flows of $3.12 billion. Crude oil accounted for 58% of our total production and 87% of our crude oil and natural gas revenues for 2019. Our total production averaged 340,395 Boe per day for 2019, a 14% increase compared to 2018.

The table below summarizes our total proved reserves, PV-10 (non-GAAP) and net producing wells as of December 31, 2019, average daily production for the quarter ended December 31, 2019 and the reserve-to-production index in our principal operating areas. The PV-10 values shown below are not intended to represent the fair market value of our crude oil and natural gas properties. There are numerous uncertainties inherent in estimating quantities of crude oil and natural gas reserves. See Part I, Item 1A. Risk Factors and “Critical Accounting Policies and Estimates” in Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations of this report for further discussion of uncertainties inherent in the reserve estimates.

1

December 31, 2019 | Average daily production for fourth quarter 2019 (Boe per day) | Annualized reserve/production index (2) | ||||||||||||||||||||

Proved reserves (MBoe) | Percent of total | PV-10 (1) (In millions) | Net producing wells | Percent of total | ||||||||||||||||||

North Region: | ||||||||||||||||||||||

Bakken field | ||||||||||||||||||||||

North Dakota Bakken | 795,091 | 49.1 | % | $ | 6,739 | 1,545 | 188,178 | 51.5 | % | 11.6 | ||||||||||||

Montana Bakken | 38,979 | 2.4 | % | 304 | 259 | 5,978 | 1.6 | % | 17.9 | |||||||||||||

Red River units | ||||||||||||||||||||||

Cedar Hills | 24,957 | 1.5 | % | 332 | 130 | 5,757 | 1.6 | % | 11.9 | |||||||||||||

Other Red River units | 2,952 | 0.2 | % | 33 | 116 | 1,861 | 0.5 | % | 4.3 | |||||||||||||

Other | 27 | — | % | — | 2 | 15 | — | % | 4.9 | |||||||||||||

South Region: | ||||||||||||||||||||||

SCOOP | 575,664 | 35.6 | % | 3,766 | 406 | 111,829 | 30.6 | % | 14.1 | |||||||||||||

STACK | 181,501 | 11.2 | % | 665 | 330 | 51,628 | 14.1 | % | 9.6 | |||||||||||||

Other | 94 | — | % | 1 | 2 | 95 | 0.1 | % | 2.7 | |||||||||||||

Total | 1,619,265 | 100.0 | % | $ | 11,840 | 2,790 | 365,341 | 100.0 | % | 12.1 | ||||||||||||

(1) | PV-10 is a non-GAAP financial measure and generally differs from Standardized Measure, the most directly comparable GAAP financial measure, because it does not include the effects of income taxes on future net revenues of approximately $1.4 billion. Neither PV-10 nor Standardized Measure represents an estimate of the fair market value of our crude oil and natural gas properties. We and others in the crude oil and natural gas industry use PV-10 as a measure to compare the relative size and value of proved reserves held by companies without regard to the specific income tax characteristics of such entities. See Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures for further discussion. |

(2) | The Annualized Reserve/Production Index is the number of years that estimated proved reserves would last assuming current production continued at the same rate. This index is calculated by dividing annualized fourth quarter 2019 production into estimated proved reserve volumes as of December 31, 2019. |

Business Environment and Outlook

Our industry is impacted by volatility and uncertainty in commodity prices. Crude oil prices remained volatile throughout 2019, with West Texas Intermediate crude oil benchmark prices ranging from approximately $46 to $66 per barrel, and price volatility has continued into early 2020. Our leadership team has significant experience with operating in challenging commodity price environments. With our portfolio of high quality assets and strong balance sheet, we are well-positioned to manage the ongoing challenges and price volatility facing our industry.

For 2020, our primary business strategies will focus on:

• | Continuing to increase shareholder value through free cash flow generation and shareholder capital return initiatives; |

• | Generating corporate returns on capital employed that compete with the broader market through operational excellence, technical innovations, pad and row development, optimized completion methods, well productivity, and strategic mineral ownership; |

• | Continuing to exercise disciplined capital spending to maintain financial flexibility and ample liquidity; and |

• | Stock repurchases and/or reducing outstanding debt using available operating cash flows, proceeds from asset dispositions, or joint development arrangements. |

Our Business Strategies

Despite volatility and uncertainty in commodity prices, our business strategies continue to be focused on increasing shareholder value by finding and developing crude oil and natural gas reserves at low costs that provide attractive rates of return. The principal elements of this strategy include:

Growing and sustaining a premier portfolio of assets focused on increasing shareholder value through free cash flow generation and shareholder capital return initiatives. We are focused on increasing shareholder value and returns. We hold a portfolio of leasehold acreage, drilling opportunities, uncompleted wells, perpetually owned minerals, and water infrastructure

2

assets in certain premier U.S. resource plays with varying access to crude oil, natural gas, and natural gas liquids. We pursue opportunities to develop our existing properties as well as explore for new resource plays where significant reserves may be economically developed. Our capital programs are designed to allocate investments to projects that provide opportunities to deliver production growth at low costs while generating cash flows in excess of operating and capital requirements, harvest our inventory of uncompleted wells, convert our undeveloped acreage to acreage held by production, and improve hydrocarbon recoveries and rates of return on capital employed.

Our assets and execution generated strong free cash flows in 2018 and 2019 and we plan to remain focused on generating cash flow positive growth for the foreseeable future. Accordingly, in 2019 we initiated a strategy to increase shareholder value and returns that included the commencement of a $1 billion share repurchase program and the payment of a quarterly dividend. Through year-end 2019 we had executed $190.2 million of share repurchases and we paid our first cash dividend of $0.05 per share in November 2019. We are strongly aligned with shareholders and our strategic vision is predicated on our desire to increase shareholder value through dividends, share repurchases, continued debt reduction, and other means.

Generating corporate returns on capital employed that compete with the broader market through operational excellence, technical innovations, pad and row development, optimized completions, well productivity, and strategic mineral ownership. We are focused on generating strong corporate returns on capital employed that compete with the broader market. We continue to manage our business in the volatile commodity price environment by focusing on improving operating efficiencies and reducing costs by exploiting technical innovations, pad and row development opportunities, and other means. Our key operating areas are characterized by large acreage positions in select unconventional resource plays with multiple stacked geologic formations that provide repeatable drilling opportunities and resource potential. We operate a significant portion of our wells and leasehold acreage and believe the concentration of our operated assets allows us to leverage our technical expertise and manage the development of our properties to enhance operating efficiencies and economies of scale. Our operational excellence has allowed us to achieve and maintain enviable low-cost operations.

Additionally, we capitalize on our geologic knowledge and land expertise to strategically acquire minerals in areas of future growth, thereby allowing us to enhance cash flows and project economics through the alignment of mineral ownership with our drilling schedule. Further, we continue to develop our water gathering, recycling, and disposal infrastructure which allows for uninterrupted flow back and recycling capabilities, supports timely completion activities, and generates additional service revenues and cash flows. Our strategies for growing our mineral ownership portfolio and water infrastructure assets serve as additional avenues to increase shareholder returns.

Maintaining capital discipline, financial flexibility, and a strong balance sheet. Maintaining capital discipline, a strong balance sheet, ample liquidity, and financial flexibility are key components of our business strategy. In 2019, we reduced our total debt by $442 million, or 8%. We are targeting further debt reduction using available cash, operating cash flows, or proceeds from potential sales of non-strategic assets and joint development opportunities and will continue our focus on preserving financial flexibility and ample liquidity as we manage the risks facing our industry.

Focusing on organic growth through disciplined capital investments. Although we consider various growth opportunities, including property acquisitions, our primary focus is on organic growth through leasing and drilling in our core areas where we can exploit our extensive inventory of repeatable drilling opportunities to achieve attractive rates of return.

Our Business Strengths

We have a number of strengths we believe will help us successfully execute our business strategies, including the following:

Large acreage inventory. We held approximately 458,500 net undeveloped acres and 1.23 million net developed acres under lease as of December 31, 2019 concentrated in certain premier U.S. resource plays. We are among the largest leaseholders in the Bakken, SCOOP and STACK plays. Being an early entrant in these plays has allowed us to capture significant acreage positions in core parts of the plays.

Expertise with pad and row development, horizontal drilling, and optimized completion methods. We have substantial experience with horizontal drilling and optimized completion methods and continue to be among industry leaders in the use of new drilling and completion technologies. We continue to improve drilling and completion efficiencies through the use of multi-well pad and row development strategies. Further, we are among industry leaders in drilling long lateral lengths. We have also been among industry leaders in testing and utilizing optimized completion technologies involving various combinations of fluid types, proppant types and volumes, and stimulation stage spacing to determine optimal methods for improving recoveries and rates of return. We continually refine our drilling and completion techniques in an effort to deliver improved results across our properties.

3

Control Operations Over a Substantial Portion of Our Assets and Investments. As of December 31, 2019, we operated properties comprising 86% of our total proved reserves. By controlling a significant portion of our operations, we are able to more effectively manage the cost and timing of exploration and development of our properties, including the drilling and completion methods used.

Experienced Management Team. Our senior management team has extensive expertise in the oil and gas industry and with operating in challenging commodity price environments. Our Executive Chairman, Harold G. Hamm, began his career in the oil and gas industry in 1967. Our 9 executive officers have an average of 41 years of oil and gas industry experience.

Financial Position and Liquidity. We have a credit facility with lender commitments totaling $1.5 billion that matures in April 2023. We had no outstanding borrowings on the facility at January 31, 2020. Our credit facility is unsecured and does not have a borrowing base requirement that is subject to periodic redetermination based on changes in commodity prices and proved reserves. Additionally, downgrades or other negative rating actions with respect to our credit rating do not trigger a reduction in our current credit facility commitments, nor do such actions trigger a security requirement or change in covenants.

Crude Oil and Natural Gas Operations

Proved Reserves

Proved reserves are those quantities of crude oil and natural gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible from a given date forward, from known reservoirs, and under existing economic conditions, operating methods, and government regulations prior to the time at which contracts providing the right to operate expire, unless evidence indicates renewal is reasonably certain. In connection with the estimation of proved reserves, the term “reasonable certainty” implies a high degree of confidence the quantities of crude oil and/or natural gas actually recovered will equal or exceed the estimate. To achieve reasonable certainty, our internal reserve engineers and Ryder Scott Company, L.P (“Ryder Scott”), our independent reserve engineers, employed technologies demonstrated to yield results with consistency and repeatability. The technologies and economic data used in the estimation of our proved reserves include, but are not limited to, well logs, geologic maps including isopach and structure maps, analogy and statistical analysis, and available downhole, production, seismic, and well test data.

The table below sets forth estimated proved crude oil and natural gas reserves information by reserve category as of December 31, 2019. Proved reserves attributable to noncontrolling interests are immaterial and are not separately presented herein. The standardized measure of our discounted future net cash flows totaled approximately $10.5 billion at December 31, 2019. Our reserve estimates as of December 31, 2019 are based primarily on a reserve report prepared by Ryder Scott. In preparing its report, Ryder Scott evaluated properties representing approximately 93% of our PV-10 and 91% of our total proved reserves as of December 31, 2019. Our internal technical staff evaluated the remaining properties. A copy of Ryder Scott’s summary report is included as an exhibit to this Annual Report on Form 10-K.

Our estimated proved reserves and related future net revenues, Standardized Measure and PV-10 at December 31, 2019 were determined using the 12-month unweighted arithmetic average of the first-day-of-the-month commodity prices for the period of January 2019 through December 2019, without giving effect to derivative transactions, and were held constant throughout the lives of the properties. These prices were $55.69 per Bbl for crude oil and $2.58 per MMBtu for natural gas ($51.95 per Bbl for crude oil and $2.02 per Mcf for natural gas adjusted for location and quality differentials).

Crude Oil (MBbls) | Natural Gas (MMcf) | Total (MBoe) | PV-10 (1) (in millions) | ||||||||||

Proved developed producing | 327,840 | 2,204,104 | 695,190 | $ | 7,942.2 | ||||||||

Proved developed non-producing | 8,565 | 22,013 | 12,234 | 158.1 | |||||||||

Proved undeveloped | 423,782 | 2,928,354 | 911,841 | 3,739.6 | |||||||||

Total proved reserves | 760,187 | 5,154,471 | 1,619,265 | $ | 11,839.9 | ||||||||

Standardized Measure (1) | $ | 10,461.6 | |||||||||||

(1) | PV-10 is a non-GAAP financial measure and generally differs from Standardized Measure, the most directly comparable GAAP financial measure, because it does not include the effects of income taxes on future net revenues of approximately $1.4 billion. See Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures for further discussion. |

4

The following table provides additional information regarding our estimated proved crude oil and natural gas reserves by region as of December 31, 2019.

Proved Developed | Proved Undeveloped | |||||||||||||||||

Crude Oil (MBbls) | Natural Gas (MMcf) | Total (MBoe) | Crude Oil (MBbls) | Natural Gas (MMcf) | Total (MBoe) | |||||||||||||

North Region: | ||||||||||||||||||

Bakken field | ||||||||||||||||||

North Dakota Bakken | 213,379 | 695,294 | 329,261 | 323,675 | 852,931 | 465,830 | ||||||||||||

Montana Bakken | 16,663 | 35,898 | 22,646 | 12,839 | 20,964 | 16,333 | ||||||||||||

Red River units | ||||||||||||||||||

Cedar Hills | 24,957 | — | 24,957 | — | — | — | ||||||||||||

Other Red River units | 2,952 | — | 2,952 | — | — | — | ||||||||||||

Other | 27 | — | 27 | — | — | — | ||||||||||||

South Region: | ||||||||||||||||||

SCOOP | 66,012 | 1,010,565 | 234,440 | 79,008 | 1,573,293 | 341,224 | ||||||||||||

STACK | 12,374 | 484,039 | 93,047 | 8,260 | 481,166 | 88,454 | ||||||||||||

Other | 41 | 321 | 94 | — | — | — | ||||||||||||

Total | 336,405 | 2,226,117 | 707,424 | 423,782 | 2,928,354 | 911,841 | ||||||||||||

The following table provides information regarding changes in total estimated proved reserves for the periods presented.

Year Ended December 31, | |||||||||

MBoe | 2019 | 2018 | 2017 | ||||||

Proved reserves at beginning of year | 1,522,365 | 1,330,995 | 1,274,864 | ||||||

Revisions of previous estimates | (148,848 | ) | (269,253 | ) | (82,012 | ) | |||

Extensions, discoveries and other additions | 365,034 | 565,030 | 240,206 | ||||||

Production | (124,244 | ) | (108,839 | ) | (88,562 | ) | |||

Sales of minerals in place | (1,840 | ) | (8,011 | ) | (15,197 | ) | |||

Purchases of minerals in place | 6,798 | 12,443 | 1,696 | ||||||

Proved reserves at end of year | 1,619,265 | 1,522,365 | 1,330,995 | ||||||

Revisions of previous estimates. Revisions for 2019 are comprised of (i) the removal of 17 MMBo and 108 Bcf (totaling 35 MMBoe) of PUD reserves no longer scheduled to be drilled within five years of initial booking due to the continual refinement of our drilling programs and reallocation of capital to areas providing the greatest opportunities to improve efficiencies, recoveries, and rates of return, (ii) downward revisions of 38 MMBo and 278 Bcf (totaling 85 MMBoe) from the removal of PUD reserves due to changes in economics, performance, and other factors, (iii) downward price revisions of 24 MMBo and 118 Bcf (totaling 43 MMBoe) due to a decrease in average crude oil and natural gas prices in 2019 compared to 2018, and (iv) net downward revisions for oil reserves of 9 MMBo and net upward revisions for natural gas reserves of 139 Bcf (netting to 14 MMBoe of upward revisions) due to changes in ownership interests, operating costs, anticipated production, and other factors.

Extensions, discoveries and other additions. Extensions, discoveries and other additions for each of the three years reflected in the table above were due to successful drilling and completion activities and continual refinement of our drilling programs in the Bakken, SCOOP, and STACK plays. Proved reserve additions in the Bakken totaled 160 MMBoe, 251 MMBoe, and 148 MMBoe for 2019, 2018, and 2017, respectively, while reserve additions in SCOOP totaled 186 MMBoe, 186 MMBoe, and 53 MMBoe for 2019, 2018, and 2017, respectively. Additionally, reserve additions in STACK totaled 19 MMBoe, 128 MMBoe, and 39 MMBoe in 2019, 2018, and 2017, respectively. See the subsequent section titled Summary of Crude Oil and Natural Gas Properties and Projects for a discussion of our 2019 drilling activities.

Sales of minerals in place. We had no individually significant dispositions of proved reserves in the past three years.

Purchases of minerals in place. We had no individually significant acquisitions of proved reserves in the past three years.

5

Proved Undeveloped Reserves

All of our PUD reserves at December 31, 2019 are located in the Bakken, SCOOP, and STACK plays, our most active development areas, with those plays comprising 53%, 37%, and 10%, respectively, of our total PUD reserves at year-end 2019. The following table provides information regarding changes in our PUD reserves for the year ended December 31, 2019. Our PUD reserves at December 31, 2019 include 91 MMBoe of reserves associated with wells where drilling has occurred but the wells have not been completed or are completed but not producing ("DUC wells"). Our DUC wells are classified as PUD reserves when relatively major expenditures are required to complete and produce from the wells.

Crude Oil (MBbls) | Natural Gas (MMcf) | Total (MBoe) | |||||||

Proved undeveloped reserves at December 31, 2018 | 409,271 | 2,627,325 | 847,159 | ||||||

Revisions of previous estimates | (72,759 | ) | (443,343 | ) | (146,650 | ) | |||

Extensions and discoveries | 151,441 | 1,143,773 | 342,070 | ||||||

Sales of minerals in place | (739 | ) | (1,980 | ) | (1,069 | ) | |||

Purchases of minerals in place | 471 | 11,298 | 2,354 | ||||||

Conversion to proved developed reserves | (63,903 | ) | (408,719 | ) | (132,023 | ) | |||

Proved undeveloped reserves at December 31, 2019 | 423,782 | 2,928,354 | 911,841 | ||||||

Revisions of previous estimates. As previously discussed, in 2019 we removed 17 MMBo and 108 Bcf (totaling 35 MMBoe) of PUD reserves no longer scheduled to be drilled within five years of initial booking due to the continual refinement of our drilling programs. Of these removals, 12 MMBo and 39 Bcf (totaling 19 MMBoe) was related to Bakken properties, 4 MMBo and 56 Bcf (totaling 13 MMBoe) was related to SCOOP properties, and 1 MMBo and 13 Bcf (totaling 3 MMBoe) was related to STACK properties. Additionally, changes in economics, performance, and other factors resulted in downward PUD reserve revisions of 38 MMBo and 278 Bcf (totaling 85 MMBoe) in 2019. Decreases in average crude oil and natural gas prices in 2019 resulted in downward price revisions of 11 MMBo and 67 Bcf (totaling 22 MMBoe). Finally, changes in ownership interests, operating costs, anticipated production, and other factors resulted in net downward revisions for oil PUD reserves of 6 MMBo and net upward revisions for natural gas PUD reserves of 9 Bcf (totaling a net downward revision of 5 MMBoe) in 2019.

Extensions and discoveries. Extensions and discoveries were due to successful drilling activities and continual refinement of our drilling programs in the Bakken, SCOOP and STACK plays. PUD reserve additions in the Bakken totaled 107 MMBo and 261 Bcf (totaling 150 MMBoe) in 2019, while SCOOP PUD reserve additions totaled 43 MMBo and 793 Bcf (totaling 176 MMBoe) and STACK PUD reserve additions totaled 1 MMBo and 90 Bcf (totaling 16 MMBoe).

Sales of minerals in place. We had no individually significant dispositions of PUD reserves in 2019.

Purchases of minerals in place. We had no individually significant acquisitions of PUD reserves in 2019.

Conversion to proved developed reserves. In 2019, we developed approximately 20% of our PUD locations and 16% of our PUD reserves booked as of December 31, 2018 through the drilling and completion of 480 gross (217 net) development wells at an aggregate capital cost of $1.1 billion incurred in 2019.

Development plans. We have acquired substantial leasehold positions in the Bakken, SCOOP and STACK plays. Our drilling programs to date in those areas have focused on proving our undeveloped leasehold acreage through strategic drilling, thereby increasing the amount of leasehold acreage in the secondary term of the lease with no further drilling obligations (i.e., categorized as held by production) and resulting in a reduced amount of leasehold acreage in the primary term of the lease. While we may opportunistically drill strategic exploratory wells, a substantial portion of our future capital expenditures will be focused on developing our PUD locations, including our drilled but not completed locations. Our inventory of DUC wells classified as PUDs total 386 gross (138 net) operated and non-operated locations at December 31, 2019 and represent 10% of our PUD reserves at that date. The costs to drill our uncompleted wells were incurred prior to December 31, 2019 and only the remaining completion costs are included in future development plans.

Estimated future development costs relating to the development of PUD reserves are projected to be approximately $1.8 billion in 2020, $2.2 billion in 2021, $2.0 billion in 2022, $2.3 billion in 2023, and $1.7 billion in 2024. These capital expenditure projections have been established based on an expectation of drilling and completion costs, available cash flows, borrowing capacity, and the commodity price environment in effect at the time of preparing our reserve estimates and may be adjusted as market conditions evolve. Development of our existing PUD reserves at December 31, 2019 is expected to occur within five years of the date of initial booking of the PUDs. PUD reserves not expected to be drilled within five years of initial booking

6

because of changes in business strategy or for other reasons have been removed from our reserves at December 31, 2019. We had no PUD reserves at December 31, 2019 that remain undeveloped beyond five years from the date of initial booking.

Qualifications of Technical Persons and Internal Controls Over Reserves Estimation Process

Ryder Scott, our independent reserves evaluation consulting firm, estimated, in accordance with generally accepted petroleum engineering and evaluation principles and definitions and guidelines established by the SEC, 93% of our PV-10 and 91% of our total proved reserves as of December 31, 2019 included in this Form 10-K. The Ryder Scott technical personnel responsible for preparing the reserve estimates presented herein meet the requirements regarding qualifications, independence, objectivity and confidentiality set forth in the Standards Pertaining to the Estimating and Auditing of Oil and Gas Reserves Information promulgated by the Society of Petroleum Engineers. Refer to Exhibit 99 included with this Form 10-K for further discussion of the qualifications of Ryder Scott personnel.

We maintain an internal staff of petroleum engineers and geoscience professionals who work closely with our independent reserves engineers to ensure the integrity, accuracy and timeliness of data furnished to Ryder Scott in their reserves estimation process. Our technical team is in contact regularly with representatives of Ryder Scott to review properties and discuss methods and assumptions used in Ryder Scott’s preparation of the year-end reserves estimates. Proved reserves information is reviewed by our Audit Committee with representatives of Ryder Scott and by our internal technical staff before the information is filed with the SEC on Form 10-K. Additionally, certain members of our senior management review and approve the Ryder Scott reserves report and on a semi-annual basis review any internal proved reserves estimates.

Our Vice President—Corporate Reserves is the technical person primarily responsible for overseeing the preparation of our reserve estimates. He has a Bachelor of Science degree in Petroleum Engineering, an MBA in Finance and 35 years of industry experience with positions of increasing responsibility in operations, acquisitions, engineering and evaluations. He has worked in the area of reserves and reservoir engineering most of his career and is a member of the Society of Petroleum Engineers. The Vice President—Corporate Reserves reports directly to our Vice Chairman of Strategic Growth Initiatives. The reserves estimates are reviewed and approved by certain members of the Company's executive management.

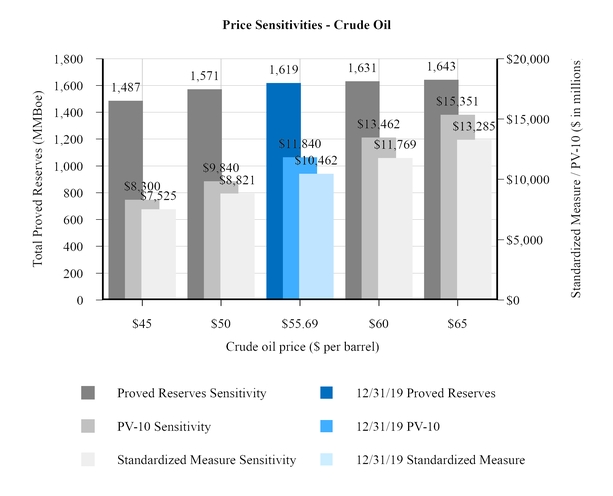

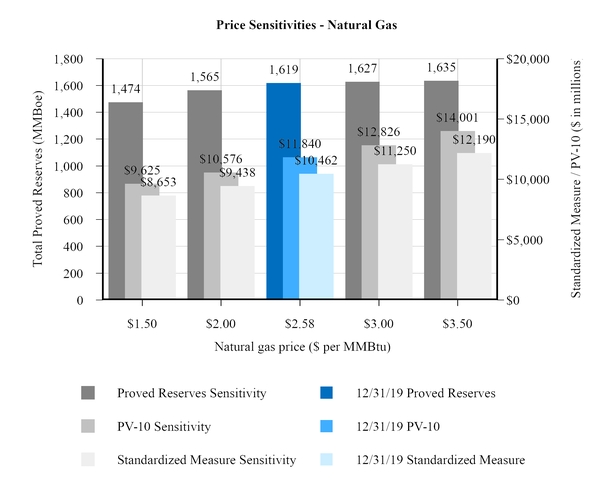

Proved Reserves, Standardized Measure, and PV-10 Sensitivities

Our year-end 2019 proved reserves, Standardized Measure, and PV-10 estimates were prepared using 2019 average first-day-of-the-month prices of $55.69 per Bbl for crude oil and $2.58 per MMBtu for natural gas ($51.95 per Bbl for crude oil and $2.02 per Mcf for natural gas adjusted for location and quality differentials). Actual future prices may be materially higher or lower than those used in our year-end estimates.

Provided below are sensitivities illustrating the potential impact on our estimated proved reserves, Standardized Measure, and PV-10 at December 31, 2019 under different commodity price scenarios for crude oil and natural gas. In these sensitivities, all factors other than the commodity price assumption have been held constant for each well. These sensitivities demonstrate the impact that changing commodity prices may have on estimated proved reserves, Standardized Measure, and PV-10 and there is no assurance these outcomes will be realized.

The crude oil price sensitivities provided below show the impact on proved reserves, Standardized Measure, and PV-10 under certain crude oil price scenarios, with natural gas prices being held constant at the 2019 average first-day-of-the-month price of $2.58 per MMBtu.

7

8

The natural gas price sensitivities provided below show the impact on proved reserves, Standardized Measure, and PV-10 under certain natural gas price scenarios, with crude oil prices being held constant at the 2019 average first-day-of-the-month price of $55.69 per Bbl.

9

Developed and Undeveloped Acreage

The following table presents our total gross and net developed and undeveloped acres by region as of December 31, 2019:

Developed acres | Undeveloped acres | Total | ||||||||||||||||

Gross | Net | Gross | Net | Gross | Net | |||||||||||||

North Region: | ||||||||||||||||||

Bakken field | ||||||||||||||||||

North Dakota Bakken | 952,366 | 564,681 | 129,920 | 81,590 | 1,082,286 | 646,271 | ||||||||||||

Montana Bakken | 172,247 | 137,972 | 34,730 | 25,913 | 206,977 | 163,885 | ||||||||||||

Red River units | 157,915 | 140,025 | 17,467 | 8,272 | 175,382 | 148,297 | ||||||||||||

Other | 83,070 | 58,229 | 51,623 | 44,834 | 134,693 | 103,063 | ||||||||||||

South Region: | ||||||||||||||||||

SCOOP | 267,796 | 159,367 | 184,200 | 101,880 | 451,996 | 261,247 | ||||||||||||

STACK | 264,535 | 143,981 | 128,705 | 77,944 | 393,240 | 221,925 | ||||||||||||

Other | 35,052 | 21,129 | 54,379 | 22,085 | 89,431 | 43,214 | ||||||||||||

East Region | 968 | 881 | 104,015 | 96,022 | 104,983 | 96,903 | ||||||||||||

Total | 1,933,949 | 1,226,265 | 705,039 | 458,540 | 2,638,988 | 1,684,805 | ||||||||||||

The following table sets forth the number of gross and net undeveloped acres as of December 31, 2019 scheduled to expire over the next three years by region unless production is established within the spacing units covering the acreage prior to the expiration dates or the leases are renewed.

2020 | 2021 | 2022 | ||||||||||||||||

Gross | Net | Gross | Net | Gross | Net | |||||||||||||

North Region: | ||||||||||||||||||

Bakken field | ||||||||||||||||||

North Dakota Bakken | 29,054 | 18,724 | 32,282 | 23,099 | 27,967 | 18,201 | ||||||||||||

Montana Bakken | — | — | 1,480 | 1,480 | 12,182 | 10,311 | ||||||||||||

Other | 3,755 | 1,343 | 17,217 | 17,217 | — | — | ||||||||||||

South Region: | ||||||||||||||||||

SCOOP | 55,908 | 29,469 | 33,633 | 16,621 | 31,304 | 20,979 | ||||||||||||

STACK | 53,933 | 33,714 | 27,210 | 19,884 | 9,855 | 8,554 | ||||||||||||

Other | 30,887 | 12,129 | 2,954 | 748 | 9,227 | 6,623 | ||||||||||||

East Region | 11,730 | 10,172 | 969 | 370 | 4,856 | 3,732 | ||||||||||||

Total | 185,267 | 105,551 | 115,745 | 79,419 | 95,391 | 68,400 | ||||||||||||

10

Drilling Activity

During the three years ended December 31, 2019, we drilled and completed exploratory and development wells as set forth in the table below:

2019 | 2018 | 2017 | ||||||||||||||||

Gross | Net | Gross | Net | Gross | Net | |||||||||||||

Exploratory wells: | ||||||||||||||||||

Crude oil | 2 | 1.6 | 4 | 1.0 | 34 | 9.0 | ||||||||||||

Natural gas | 4 | 1.8 | 9 | 4.6 | 9 | 3.1 | ||||||||||||

Dry holes | — | — | — | — | — | — | ||||||||||||

Total exploratory wells | 6 | 3.4 | 13 | 5.6 | 43 | 12.1 | ||||||||||||

Development wells: | ||||||||||||||||||

Crude oil | 615 | 222.9 | 636 | 213.7 | 474 | 175.4 | ||||||||||||

Natural gas | 68 | 9.7 | 151 | 39.1 | 91 | 26.8 | ||||||||||||

Dry holes | — | — | — | — | — | — | ||||||||||||

Total development wells | 683 | 232.6 | 787 | 252.8 | 565 | 202.2 | ||||||||||||

Total wells | 689 | 236.0 | 800 | 258.4 | 608 | 214.3 | ||||||||||||

As of December 31, 2019, there were 509 gross (190 net) operated and non-operated wells that have been spud and are in the process of drilling, completing or waiting on completion.

Summary of Crude Oil and Natural Gas Properties and Projects

In the following discussion, we review our budgeted number of wells and capital expenditures for 2020 in our key operating areas. Our 2020 capital budget, based on our current expectations of commodity prices and costs, is expected to be

funded from operating cash flows. Our drilling and completion activities and the actual amount and timing of our capital expenditures may differ materially from our budget as a result of, among other things, available cash flows, unbudgeted acquisitions, actual drilling and completion results, the availability of drilling and completion rigs and other services and equipment, the availability of transportation and processing capacity, changes in commodity prices, and regulatory, technological and competitive developments. We monitor our capital spending closely based on actual and projected cash flows and may scale back our spending should commodity prices decrease from current levels. Conversely, an increase in commodity prices from current levels could result in increased capital expenditures.

The following table provides information regarding well counts and budgeted capital expenditures for 2020.

2020 Plan | ||||||||||

Gross wells (1) | Net wells (1) | Capital expenditures (in millions) (2) | ||||||||

North Region | 406 | 154 | $ | 1,368 | ||||||

South Region | 254 | 91 | 843 | |||||||

Total exploration and development | 660 | 245 | $ | 2,211 | ||||||

Land (3) | 202 | |||||||||

Capital facilities, workovers and other corporate assets | 235 | |||||||||

Seismic | 2 | |||||||||

Total 2020 capital budget | $ | 2,650 | ||||||||

(1) Represents operated and non-operated wells expected to have first production in 2020.

(2) Represents total capital expenditures for operated and non-operated wells expected to have first production in 2020 and wells spud that will be in the process of drilling, completing or waiting on completion as of year-end 2020.

(3) | Includes $125 million of planned spending for mineral acquisitions under our relationship with Franco-Nevada Corporation described in Part II, Item 8. Notes to Consolidated Financial Statements—Note 15. Noncontrolling Interests. With a carry structure in place, Continental will recoup $100 million, or 80%, of such acquisition spending from Franco-Nevada. |

11

North Region

Our properties in the North region represented 53% of our total proved reserves as of December 31, 2019 and 55% of our average daily Boe production for the fourth quarter of 2019. Our principal producing properties in the North region are located in the Bakken field.

Bakken Field

The Bakken field of North Dakota and Montana is one of the largest crude oil resource plays in the United States. We are a leading producer, leasehold owner and operator in the Bakken. As of December 31, 2019, we controlled one of the largest leasehold positions in the Bakken with approximately 1.3 million gross (810,200 net) acres under lease.

Our total Bakken production averaged 194,156 Boe per day for the fourth quarter of 2019, up 6% from the 2018 fourth quarter. For the year ended December 31, 2019, our average daily Bakken production increased 16% over 2018, reflecting additional drilling and completion activities. In 2019, we participated in the drilling and completion of 379 gross (124 net) wells in the Bakken compared to 496 gross (169 net) wells in 2018. Our 2019 activities in the Bakken focused on ongoing multi-zone unit development of high rate-of-return areas in the play.

Our Bakken properties represented 52% of our total proved reserves at December 31, 2019 and 53% of our average daily Boe production for the 2019 fourth quarter. Our total proved Bakken field reserves as of December 31, 2019 were 834 MMBoe, an increase of 5% compared to December 31, 2018 primarily due to reserves added from our drilling and development program and continued improvement in recoveries driven by operating efficiencies and advances in optimized completion designs. Our inventory of proved undeveloped drilling locations in the Bakken totaled 1,997 gross (944 net) wells as of December 31, 2019.

For 2020, our budget for exploration and development capital expenditures in the North region is $1.37 billion. In 2020, we expect to have first production on 406 gross (154 net) operated and non-operated wells in the North region. We plan to average approximately nine operated rigs and four well completion crews in the North region throughout 2020. Our 2020 drilling and completion activities in the Bakken will focus on ongoing multi-zone unit development in areas that provide opportunities to improve capital efficiency, reduce finding and development costs, improve recoveries and rates of return, and achieve sustainable and repeatable results. Notably, in 2020 we plan to ramp up development activities on our 10-square mile Long Creek Bakken Unit in Williams County, North Dakota, with production from the project beginning in late 2020 and increasing into 2021. This unit is another high impact oil project for the Company that was formed to capitalize on our dominant ownership position in the area and will be exploited using row development to maximize efficiencies and value, much like our SpringBoard project in SCOOP described below.

South Region

Our properties in the South region represented 47% of our total proved reserves as of December 31, 2019 and 45% of our average daily Boe production for the fourth quarter of 2019. Our principal producing properties in the South region are located in the SCOOP and STACK areas of Oklahoma.

SCOOP

The SCOOP play extends across Garvin, Grady, Stephens, Carter, McClain and Love counties in Oklahoma and contains crude oil and condensate-rich fairways as delineated by numerous industry wells. We are a leading producer, leasehold owner and operator in the SCOOP play. As of December 31, 2019, we controlled one of the largest leasehold positions in SCOOP with approximately 452,000 gross (261,200 net) acres under lease.

SCOOP represented 36% of our total proved reserves as of December 31, 2019 and 31% of our average daily Boe production for the fourth quarter of 2019. Production in SCOOP averaged 111,829 Boe per day during the fourth quarter of 2019, up 66% compared to the 2018 fourth quarter. For the year ended December 31, 2019, average daily production in SCOOP increased 29% compared to 2018, reflecting increased drilling and completion activities in our Project SpringBoard play described below. We participated in the drilling and completion of 207 gross (93 net) wells in SCOOP during 2019 compared to 148 gross (48 net) wells in 2018, which helped generate a 25% increase in proved reserves during the year to 576 MMBoe as of December 31, 2019. Our inventory of proved undeveloped drilling locations in SCOOP totaled 577 gross (287 net) wells as of December 31, 2019.

Our 2019 activities in SCOOP were focused on ongoing row development of leasehold in our oil-weighted Project SpringBoard play. SpringBoard is a large, multi-year, crude oil project controlled and operated by Continental that covers approximately 73 square miles of contiguous leasehold in Grady County, Oklahoma where we are concurrently developing three stacked reservoirs in the Springer, Sycamore, and Woodford formations. These reservoirs are being developed in rows to maximize efficiencies and rates of return through the orderly sequencing of drilling and completion activities. This row development strategy allows us to realize significant cost savings. In addition to cost saving benefits, our SpringBoard production benefits

12

from access to premium sales markets through existing pipeline infrastructure, making our SpringBoard sales price realizations among the best in the Company. Additionally, water pipeline and recycling facilities are in place to allow for uninterrupted flow back and recycling capabilities to support timely completion activities in the project.

To date, Project SpringBoard has outperformed our production targets due to operational efficiency gains and strong well performance, which allowed us to reduce our rig count in Oklahoma in 2019 while still achieving our production growth objectives. This outperformance had a meaningful impact on our oil-weighted production growth during the year and contributed to a 69% increase in crude oil production from our SCOOP properties in 2019 compared to 2018.

STACK

STACK is a significant resource play located in the Anadarko Basin of Oklahoma characterized by stacked geologic formations with major targets in the Meramec, Osage, and Woodford formations. As of December 31, 2019, we controlled one of the largest leasehold positions in STACK with approximately 393,200 gross (221,900 net) acres under lease. A significant portion of our STACK acreage is located in over-pressured portions of Blaine, Dewey and Custer counties of Oklahoma where we believe the reservoirs are typically thicker and deliver superior production rates relative to normal-pressured areas of the STACK petroleum system.

Our STACK properties represented 11% of our total proved reserves as of December 31, 2019 and 14% of our average daily Boe production for the fourth quarter of 2019. Production in STACK averaged 51,628 Boe per day during the fourth quarter of 2019, down 18% over the 2018 fourth quarter due to changes in the timing of initial production from new well completions between periods. For the year ended December 31, 2019, average daily production in STACK decreased 3% from 2018 due to moderated drilling and completion activities resulting from a greater allocation of capital to other areas during the year. We participated in the drilling and completion of 103 gross (19 net) wells in STACK during 2019 compared to 154 gross (40 net) wells in 2018. Proved reserves in STACK decreased 21% year-over-year to 182 MMBoe as of December 31, 2019 due primarily to the removal of PUD reserves from changes in economics, performance, and other factors. Our inventory of proved undeveloped drilling locations in STACK totaled 156 gross (52 net) wells as of December 31, 2019.

Highlighting our 2019 activity in the STACK play was the completion of the Reba Jo and Schulte units, which consisted of 14 total wells targeting two separate benches in the Meramec formation in the STACK over-pressured oil window. These combined units delivered outstanding initial production results with initial 24-hour production averaging 4,092 Boe per day per well, ranking the wells amongst the best in Company history.

For 2020, our aggregate budget for exploration and development capital expenditures in the South region is $843 million. In 2020, we expect to have first production on 254 gross (91 net) operated and non-operated wells in the South region. We plan to average approximately 11 operated rigs and three well completion crews in the South region throughout 2020. Our 2020 activities in SCOOP will focus on continued row development in Project SpringBoard and achieving operational and technical advancements aimed at further improving capital efficiencies and rates of return. Our 2020 activities in STACK will focus on continued development of oil and liquids-rich assets in the over-pressured windows of the play and improving capital efficiencies, recoveries, and rates of return.

13

Production and Price History

The following table sets forth information concerning our production results, average sales prices and production costs for the years ended December 31, 2019, 2018 and 2017 in total and for each field containing 15 percent or more of our total proved reserves as of December 31, 2019.

Year ended December 31, | ||||||||||||

2019 | 2018 | 2017 | ||||||||||

Net production volumes: | ||||||||||||

Crude oil (MBbls) | ||||||||||||

North Dakota Bakken | 52,420 | 45,775 | 35,964 | |||||||||

SCOOP | 11,679 | 6,918 | 5,726 | |||||||||

Total Company | 72,267 | 61,384 | 50,536 | |||||||||

Natural gas (MMcf) | ||||||||||||

North Dakota Bakken | 98,186 | 78,448 | 59,232 | |||||||||

SCOOP | 111,436 | 99,397 | 98,563 | |||||||||

Total Company | 311,865 | 284,730 | 228,159 | |||||||||

Crude oil equivalents (MBoe) | ||||||||||||

North Dakota Bakken | 68,784 | 58,849 | 45,836 | |||||||||

SCOOP | 30,252 | 23,484 | 22,153 | |||||||||

Total Company | 124,244 | 108,839 | 88,562 | |||||||||

Average net sales prices (1): | ||||||||||||

Crude oil ($/Bbl) | ||||||||||||

North Dakota Bakken | $ | 50.96 | $ | 58.37 | $ | 45.21 | ||||||

SCOOP | 54.92 | 62.74 | 47.96 | |||||||||

Total Company | 51.82 | 59.19 | 45.70 | |||||||||

Natural gas ($/Mcf) | ||||||||||||

North Dakota Bakken | $ | 1.28 | $ | 3.33 | $ | 2.97 | ||||||

SCOOP | 2.36 | 3.41 | 3.26 | |||||||||

Total Company | 1.77 | 3.01 | 2.93 | |||||||||

Crude oil equivalents ($/Boe) | ||||||||||||

North Dakota Bakken | $ | 40.66 | $ | 49.83 | $ | 39.32 | ||||||

SCOOP | 29.80 | 32.88 | 26.93 | |||||||||

Total Company | 34.56 | 41.25 | 33.65 | |||||||||

Average costs per Boe: | ||||||||||||

Production expenses ($/Boe) | ||||||||||||

North Dakota Bakken | $ | 4.28 | $ | 4.40 | $ | 4.40 | ||||||

SCOOP | 1.21 | 1.34 | 1.01 | |||||||||

Total Company | 3.58 | 3.59 | 3.66 | |||||||||

Production taxes ($/Boe) | $ | 2.88 | $ | 3.25 | $ | 2.35 | ||||||

General and administrative expenses ($/Boe) | $ | 1.57 | $ | 1.69 | $ | 2.16 | ||||||

DD&A expense ($/Boe) | $ | 16.25 | $ | 17.09 | $ | 18.89 | ||||||

(1) | See Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures for a discussion and calculation of net sales prices, which are non-GAAP measures for 2018 and 2019. |

14

The following table sets forth information regarding our average daily production by region for the fourth quarter of 2019:

Fourth Quarter 2019 Daily Production | |||||||||

Crude Oil (Bbls per day) | Natural Gas (Mcf per day) | Total (Boe per day) | |||||||

North Region: | |||||||||

Bakken field | |||||||||

North Dakota Bakken | 139,527 | 291,910 | 188,178 | ||||||

Montana Bakken | 4,581 | 8,379 | 5,978 | ||||||

Red River units | |||||||||

Cedar Hills | 5,757 | 3 | 5,757 | ||||||

Other Red River units | 1,861 | — | 1,861 | ||||||

Other | 13 | 11 | 15 | ||||||

South Region: | |||||||||

SCOOP | 44,399 | 404,582 | 111,829 | ||||||

STACK | 10,071 | 249,341 | 51,628 | ||||||

Other | 40 | 330 | 95 | ||||||

Total | 206,249 | 954,556 | 365,341 | ||||||

Productive Wells

Gross wells represent the number of wells in which we own a working interest and net wells represent the total of our fractional working interests owned in gross wells. The following table presents the total gross and net productive wells by region and by crude oil or natural gas completion as of December 31, 2019. One or more completions in the same well bore are counted as one well.

Crude Oil Wells | Natural Gas Wells | Total Wells | ||||||||||||||||

Gross | Net | Gross | Net | Gross | Net | |||||||||||||

North Region: | ||||||||||||||||||

Bakken field | ||||||||||||||||||

North Dakota Bakken | 4,611 | 1,545 | — | — | 4,611 | 1,545 | ||||||||||||

Montana Bakken | 406 | 259 | — | — | 406 | 259 | ||||||||||||

Red River units | ||||||||||||||||||

Cedar Hills | 136 | 130 | — | — | 136 | 130 | ||||||||||||

Other Red River units | 130 | 116 | — | — | 130 | 116 | ||||||||||||

Other | 2 | 2 | — | — | 2 | 2 | ||||||||||||

South Region: | ||||||||||||||||||

SCOOP | 510 | 271 | 471 | 135 | 981 | 406 | ||||||||||||

STACK | 418 | 171 | 472 | 159 | 890 | 330 | ||||||||||||

Other | 1 | 1 | 22 | 1 | 23 | 2 | ||||||||||||

Total | 6,214 | 2,495 | 965 | 295 | 7,179 | 2,790 | ||||||||||||

15

Title to Properties

As is customary in the crude oil and natural gas industry, upon initiation of acquiring oil and gas leases covering fee mineral interests on undeveloped lands which do not have associated proved reserves, contract landmen conduct a title examination of courthouse records and production databases to determine fee mineral ownership and availability. Title, lease forms and terms are reviewed and approved by Company landmen prior to consummation.

For acquisitions from third parties, whether lands are producing crude oil and natural gas or non-producing, Company and contract landmen perform title examinations at applicable courthouses, obtain physical well site inspections, and examine the seller’s internal records (land, legal, operational, production, environmental, well, marketing and accounting) upon execution of a mutually acceptable purchase and sale agreement. Company landmen may also procure an acquisition title opinion from outside legal counsel on higher value properties.

Prior to the commencement of drilling operations, Company landmen procure an original title opinion, or supplement an existing title opinion, from outside legal counsel and perform curative work to satisfy requirements pertaining to material title defects, if any. Company landmen will not approve commencement of drilling operations until material title defects pertaining to the Company’s interest are cured.

The Company has cured material title opinion defects as to Company interests on substantially all of its producing properties and believes it holds at least defensible title to its producing properties in accordance with standards generally accepted in the crude oil and natural gas industry. The Company’s crude oil and natural gas properties are subject to customary royalty and leasehold burdens which do not materially interfere with the Company’s interest in the properties or affect the Company’s carrying value of such properties.

Marketing and Major Customers

We sell most of our operated crude oil production to crude oil refining companies or midstream marketing companies at major market centers. In the Bakken, SCOOP and STACK areas, we have significant volumes of production directly connected to pipeline gathering systems, with the remaining balance of production primarily transported by truck either directly to a refinery or to a point on a pipeline system for further delivery. We do not transport any of our oil production prior to sale by rail, but several purchasers of our Bakken production are connected to rail delivery systems and may choose those methods to transport the oil they purchase from us. We sell some operated crude oil production at the lease. Our share of crude oil production from non-operated properties is marketed at the discretion of the operators.

We sell our operated natural gas production to midstream customers at our lease locations based on market prices in the field where the sales occur. These contracts include multi-year term agreements, many with acreage dedication. Under certain arrangements, we have the right to take a volume of processed residue gas and/or natural gas liquids ("NGLs") in-kind at the tailgate of the midstream customer's processing plant in lieu of a monetary settlement for the sale of our operated natural gas production. We currently take certain processed residue gas volumes in kind in lieu of monetary settlement, but we do not currently take NGL volumes. When we do take volumes in kind, we pay third parties to transport the residue gas volumes taken in kind to downstream delivery points, where we then sell to customers at prices applicable to those downstream markets. Sales at the downstream markets are mostly under monthly interruptible packaged volume deals, short term seasonal packages, and long term multi-year contracts. We continue to develop relationships and have the potential to enter into additional contracts with end-use customers, including utilities, industrial users, and liquefied natural gas exporters, for sale of products we elect to take in-kind in lieu of monetary settlement for our leasehold sales. Our share of natural gas production from non-operated properties is generally marketed at the discretion of the operators.

For the year ended December 31, 2019, sales to Valero Energy Corporation and its affiliates accounted for approximately 13% of our total crude oil and natural gas revenues. No other purchaser accounted for more than 10% of our total crude oil and natural gas revenues for 2019. The loss of any single purchaser will not have a material adverse effect on our operations, as crude oil and natural gas are fungible products with well-established markets and numerous purchasers in various regions.

Competition