UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||||||||

For the fiscal year ended December 31 , 2020

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||||||||

For the transition period from _______________ to _______________

Commission file number: 0-12015

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

Registrant’s telephone number, including area code:

(215 ) 639-4274

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| þ | Accelerated filer | ☐ | |||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||||||||

| Emerging growth company | |||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on the attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No þ

The aggregate market value of the voting stock (Common Stock, $.01 par value) held by non-affiliates of the Registrant as of the close of business on June 30, 2020 was approximately $1.80 billion based on the closing sale price of the Common Stock on the NASDAQ Global Select Market on that date. The determination of affiliate status is not a determination for any other purpose. The Registrant does not have any non-voting common equity authorized or outstanding.

Indicate the number of shares outstanding of each of the registrant’s classes of Common Stock (Common Stock, $.01 par value) as of the latest practicable date (February 24, 2021). 74,717,000

DOCUMENTS INCORPORATED BY REFERENCE

Healthcare Services Group, Inc.

Annual Report on Form 10-K

For the Fiscal Year Ended December 31, 2020

TABLE OF CONTENTS

| PART I | ||||||||

| PART II | ||||||||

| PART III | ||||||||

| PART IV | ||||||||

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Form 10-K may contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which are not historical facts but rather are based on current expectations, estimates and projections about our business and industry, and our beliefs and assumptions. Words such as “believes,” “anticipates,” “plans,” “expects,” “will,” “goal,” and similar expressions are intended to identify forward-looking statements. The inclusion of forward-looking statements should not be regarded as a representation by us that any of our plans will be achieved. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Such forward-looking information is also subject to various risks and uncertainties. Such risks and uncertainties include, but are not limited to, risks arising from our providing services to the healthcare industry, primarily providers of long-term care; the impact of and future effects of the COVID-19 pandemic or other potential pandemics; having a significant portion of our consolidated revenues contributed by one customer during the year ended December 31, 2020; credit and collection risks associated with the healthcare industry; our claims experience related to workers’ compensation and general liability insurance (including any litigation claims, enforcement actions, regulatory actions and investigations arising from personal injury and loss of life related to COVID-19); the effects of changes in, or interpretations of laws and regulations governing the healthcare industry, our workforce and services provided, including state and local regulations pertaining to the taxability of our services and other labor-related matters such as minimum wage increases; the Company's expectations with respect to selling, general, and administrative expense; continued realization of tax benefits arising from our corporate reorganization and self-funded health insurance program; changes in the federal corporate tax rate; the impact of the Securities and Exchange Commission investigation and related class action lawsuit; risks associated with the reorganization of our corporate structure; and the risk factors described in Part I of this report under “Government Regulation of Customers,” “Service Agreements and Collections,” and “Competition” under Item IA. “Risk Factors.”

These factors, in addition to delays in payments from customers and/or customers in bankruptcy, have resulted in, and could continue to result in, significant additional bad debts in the near future. Additionally, our operating results would be adversely affected if unexpected increases in the costs of labor and labor-related costs, materials, supplies and equipment used in performing services (including the impact of potential tariffs and COVID-19) could not be passed on to our customers.

In addition, we believe that to improve our financial performance we must continue to obtain service agreements with new customers, retain and provide new services to existing customers, achieve modest price increases on current service agreements with existing customers and/or maintain internal cost reduction strategies at our various operational levels. Furthermore, we believe that our ability to sustain the internal development of managerial personnel is an important factor impacting future operating results and the successful execution of our growth strategies.

PART I

In this Annual Report on Form 10-K for the year ended December 31, 2020, Healthcare Services Group, Inc. (together with its wholly-owned subsidiaries listed in Exhibit 21, which has been filed as part of this Report) is referred to using terms such as the “Company,” “we,” “us” or “our.”

Item I. Business.

General

Healthcare Services Group, Inc. is a Pennsylvania corporation, incorporated on November 22, 1976. We provide management, administrative and operating expertise and services to the housekeeping, laundry, linen, facility maintenance and dietary service departments of healthcare facilities, including nursing homes, retirement complexes, rehabilitation centers and hospitals located throughout the United States. We believe we are the largest provider of housekeeping and laundry management services to the long-term care industry in the United States, rendering such services to over 3,000 facilities throughout the continental United States as of December 31, 2020.

Segment Information

The information called for herein is discussed below in Description of Services, and within Item 8 of this Annual Report on Form 10-K under Note 15 — Segment Information in the Notes to Consolidated Financial Statements for the years ended December 31, 2020, 2019 and 2018.

Description of Services

We are organized into two reportable segments: housekeeping, laundry, linen and other services (“Housekeeping”) and dietary department services (“Dietary”). Our corporate headquarters provides centralized financial management and support, legal services, human resources management and other administrative services to the Housekeeping and Dietary business segments.

We provide Housekeeping services to essentially all of our customer facilities and provide Dietary services to over 1,500 facilities. Although we do not directly participate in any government reimbursement programs, our customers receive government reimbursements related to Medicare and Medicaid and are directly affected by any legislation and regulations relating to those programs.

We provide services primarily pursuant to full service agreements with our customers. Under such agreements, we are responsible for the day-to-day management of the employees located at our customers’ facilities, as well as for the provision of certain supplies. We also provide services on the basis of management-only agreements for a limited number of customers. Under a management-only agreement, we provide management and supervisory services while the customer facility retains payroll responsibility for the non-supervisory staff. Our agreements with customers typically provide for a renewable one year service term, cancellable by either party upon 30 to 90 days’ notice after an initial period of 60 to 120 days.

We typically adopt and follow our customers’ employee wage structures, including policies of wage rate increases, and pass through to the customer any labor cost increases associated with wage rate adjustments.

Our labor force is interchangeable with respect to the services within Housekeeping, while the Dietary labor force is specific to Dietary operations. In addition, there are some differences in the expertise of the professional management personnel responsible for the services of the respective segments. We believe each segment provides opportunities for growth.

1

Housekeeping

Housekeeping accounted for approximately 50.9%, or $895.3 million, of our consolidated revenues in 2020. The services provided under this segment include managing our customers’ housekeeping departments, which are principally responsible for the cleaning, disinfecting and sanitizing of resident rooms and common areas of the customers’ facilities, as well as the laundering and processing of the bed linens, uniforms, resident personal clothing and other assorted linen items utilized at the customers’ facilities. Upon beginning service with a customer facility, we typically hire and train the employees previously employed by such facility and assign an on-site manager to supervise and train the front-line personnel and coordinate housekeeping services with other facility support functions in accordance with customer requests. Such management personnel also oversee the execution of various cost and quality control procedures including continuous training and employee evaluation, and on-site testing for infection control.

Housekeeping’s operating performance is significantly impacted by our management of labor costs. Management reviews costs as a percentage of revenues, in order to normalize and evaluate such costs in the context of the Company’s growth. Housekeeping labor costs represented approximately 80.5% of Housekeeping revenues for 2020. Changes in employee compensation resulting from legislative or other governmental actions, market factors, adjustments to staffing levels, and the composition of our labor force may adversely impact these costs. Similarly, an increase in the costs of supplies consumed in performing Housekeeping services may impact Housekeeping’s operating performance. In 2020, the cost of Housekeeping supplies as a percentage of Housekeeping revenues was 6.9%. Generally, the cost of such supplies is dictated by specific product market conditions, subject to price fluctuations influenced by factors outside of our control. Where possible, we negotiate fixed pricing from vendors for an extended period of time on certain supplies to mitigate such price fluctuations.

Dietary

Dietary services represented approximately 49.1%, or $865.0 million, of our consolidated revenues in 2020. Dietary services consist of managing our customers’ dietary departments, which are principally responsible for food purchasing, meal preparation and professional dietitian services, which include the development of menus that meet the dietary needs of residents. On-site management is responsible for all daily dietary department activities, with regular support provided by a District Manager specializing in dietary services. We also offer clinical consulting services to our dietary customers, which may be provided as a stand-alone service, or bundled with other dietary department services. Upon beginning service with a customer facility, we typically hire and train the employees previously employed by such facility and assign an on-site manager to supervise and train the front-line personnel and coordinate dietitian services with other facility support functions in accordance with customer requests. Such management personnel also oversee the execution of various cost and quality-control procedures including continuous training and employee evaluation.

Dietary operating performance is impacted by price fluctuations in labor and supply costs resulting from similar factors discussed above for Housekeeping. In 2020, the costs of labor and food-related supplies represented approximately 63.7% and 26.5% of Dietary revenues, respectively.

2

Significant Customers

For the years ended December 31, 2020, 2019 and 2018, both the Housekeeping and Dietary segments earned revenue from several significant customers, including Genesis Healthcare, Inc. ("Genesis"). For the years ended December 31, 2020, 2019 and 2018, Genesis accounted for $258.7 million or 14.7%, $287.8 million or 15.6% and $386.7 million or 19.3% of the Company's consolidated revenues, respectively.

Operational Management Structure

By applying our professional management techniques, we offer our customers the ability to manage certain housekeeping, laundry, linen, facility maintenance and dietary services and costs. We manage and provide our services through a network of management personnel, as illustrated below.

| Vice President of Operations | ||||||||||||||||||||||||||||||||||||||

| ↓ | ||||||||||||||||||||||||||||||||||||||

| Director of Operations | ||||||||||||||||||||||||||||||||||||||

| ↓ | ||||||||||||||||||||||||||||||||||||||

| District Manager | ||||||||||||||||||||||||||||||||||||||

| ↓ | ||||||||||||||||||||||||||||||||||||||

| Facility Manager | ||||||||||||||||||||||||||||||||||||||

Facilities are managed by an on-site Facility Manager, and if necessary, additional supervisory personnel. Such facility-level management personnel are responsible for the management of staff, scheduling, procurement, customer-service, quality control and overall day-to-day management of the Housekeeping or Dietary function.

District Managers oversee the operations of the facilities within their districts. Their responsibilities include oversight of Facility Managers and management of personnel, operational performance, quality control and customer satisfaction, while ensuring adherence to the Company’s systems and budgets.

Directors of Operations oversee District Managers and provide management support, training and personnel management, while ensuring operational performance is consistent with the Company’s systems and budgets.

Vice Presidents of Operations are ultimately responsible for all aspects of the operations, including the compliance and financial performance of the Directors of Operations they oversee.

We believe our organizational structure facilitates our ability to best serve and expand our service offerings to existing customers, while also securing new customers.

Market

The market for our services consists of a large number of facilities involved in various aspects of the healthcare industry, including long-term and post-acute care facilities (e.g., skilled nursing facilities, residential care and assisted living facilities) and hospitals (e.g., acute care, critical access, psychiatric). Such facilities may be specialized or general, privately owned or public, for-profit or not-for-profit, and may serve residents on a long-term or short-term basis. We market our services to facilities after consideration of a variety of factors including facility type, size, location, and service opportunities (Housekeeping or Dietary). The market for our services, particularly in long-term and post-acute care, is expected to continue to grow as the population of the United States ages and as government reimbursement policies require increased cost control or containment by the constituents that comprise our target market.

3

Marketing and Sales

Our services are primarily marketed by our Chief Revenue Officer, Vice Presidents of Sales, and Directors of Sales. These marketing and sales efforts are supported by all levels of our corporate and operational management team. We provide incentive compensation to our sales and operational personnel based on achieving financial and non-financial goals and objectives, which are aligned with the key elements we believe are necessary for us to achieve overall improvement in our results, along with continued business development.

Our services are marketed primarily through referrals and solicitation of target facilities. We also participate in industry trade shows, healthcare trade associations and healthcare support service seminars offered in conjunction with state or local health authorities in many of the states in which we conduct our business. Such programs are typically attended by facility owners, administrators and supervisory personnel, thus presenting marketing opportunities for us. Indications of interest in our services arising from initial marketing efforts are followed up with a presentation regarding our services and an assessment of the service requirements of the facility. Thereafter, a formal proposal, including operational recommendations and proposed costs, is submitted to the prospective customer. Once the prospective customer accepts the proposal and executes our service agreement, we are structured to timely and efficiently establish our operations and systems at the customer facilities.

Government Regulation of Customers

We do not directly participate in any government reimbursement programs and our contractual relationships with our customers determine their payment obligations to us. However, our customers are subject to government regulation and laws which directly affect how they are paid for certain services they provide. Therefore, because our customers’ revenues are generally highly reliant on Medicare and Medicaid reimbursement funding rates, the overall effect of laws and trends in the long-term care industry have affected and could adversely affect our customers’ cash flows, resulting in their inability to make payments to us in accordance with agreed upon payment terms (see “Liquidity and Capital Resources” included in our “Management’s Discussion and Analysis of Financial Condition and Results of Operations”).

The prospects for legislative action, both on the federal and state level, regarding funding for nursing homes are uncertain. We are unable to predict or to estimate the ultimate impact of any further changes in reimbursement programs affecting our customers’ future results of operations and/or their impact on our cash flows and operations.

Environmental Regulation

Our operations are subject to various federal, state and/or local laws concerning emissions into the air, discharges into waterways and the generation, handling and disposal of waste and hazardous substances. Our past expenditures relating to environmental compliance have not had a material effect on our cash flows or results of operations and are included in normal operating expenses. These laws and regulations are constantly evolving, and it is impossible to predict accurately the effect they may have upon the capital expenditures, earnings and our competitive position in the future. Based upon information currently available, we believe that expenditures relating to environmental compliance will not have a material impact on the financial position of the Company.

Service Agreements and Collections

We have historically had a favorable customer retention rate and expect to continue to maintain satisfactory relationships with our customers, despite many of our service agreements being cancellable on short notice.

4

We have had varying collections experiences with respect to our accounts and notes receivable. We have sometimes extended the period of payment for certain customers beyond contractual terms. Such customers include those who have terminated service agreements and slow payers experiencing financial difficulties. In order to provide for such collection issues and the general risk associated with the granting of credit terms, we have recorded bad debt provisions (in an Allowance for Doubtful Accounts) of $9.6 million, $25.5 million and $51.4 million in the years ended December 31, 2020, 2019 and 2018, respectively (see Schedule II - Valuation and Qualifying Accounts and Reserves for year-end balances). As a percentage of total revenues, these provisions represented approximately 0.5%, 1.4% and 2.6% for the years ended December 31, 2020, 2019 and 2018, respectively. In addition, the Company recorded a $32.1 million cumulative effect adjustment to Retained Earnings on January 1, 2020 in accordance with the Company's adoption of Financial Accounting Standards Board ("FASB") Accounting Standards Codification subtopic 326 Credit Losses - Measurement of Credit Losses on Financial Instruments ("ASC 326"), which represented 1.7% of consolidated revenues for the year ended December 31, 2020. In making credit evaluations, in addition to analyzing and anticipating, where possible, the specific cases described above, we consider the general collection risk associated with trends in the long-term care industry. We establish credit limits through our payment terms, perform ongoing credit evaluations and monitor accounts to minimize the risk of loss. Despite our efforts to minimize credit risk exposure, customers could be adversely affected if future industry trends change in such a manner as to negatively impact their cash flows. If our customers experience a negative impact on their cash flows, it could have a material adverse effect on our results of operations and financial condition.

Competition

We compete primarily with the in-house service departments of our potential customers. In addition, a number of regional and local firms compete with us in the regional markets in which we conduct business. There are also several national and multinational service firms that provide similar services primarily within non-healthcare markets, but also within the broader healthcare industry. Historically such firms have not invested significant resources on the long-term, post-acute and healthcare segments typically serviced by us.

Human Capital Resources

Ensuring a positive social impact is inherent in our mission to deliver exceptional services to an ever-changing healthcare industry. In delivering upon this goal, we strive for operational excellence while creating a safe working environment, promoting environmental and employee health and safety awareness, and seeking to continuously create opportunities for professional and career development for our employees. In order to continue to deliver on our strategic focus and Company Vision - To Be THE Choice For Our Customers - resulting in retention of and growth in relationships through good customer-service, expansion of our services, effective execution in all that we do, and cost management; it is crucial that we attract and retain talent in the markets that we serve. To facilitate talent attraction and retention, we strive to make Healthcare Services Group, Inc. an inclusive, safe and healthy workplace, with opportunities for our employees to grow and develop in their careers, supported by competitive compensation, benefits and health and welfare programs.

Supporting our diverse team of individuals drives us to continuously improve and provide developmental opportunities for every team member, encouraging all of our employees to reach their full potential. To support this we have launched a formal Employee Engagement and Recognition Program. We devise career development and promotional pathways for all employees, with staunch commitment to promotion from within, and our Manager-In-Training Program is accessible for all qualified and motivated employees, regardless of formal education level achieved. We advertise all on-demand opportunities to our employees in an effort to cultivate talent throughout the Company. We also focus on understanding our diversity and inclusion strengths and opportunities. We continue to focus on building a pipeline for talent to create more opportunities for workplace diversity and to support greater representation within the Company. Some highlights:

•Documented annual and ongoing training for employees at all levels on diversity and inclusion;

•Celebrating and creating diversity among our teams;

•Our workforce consists of 71% females and 64% minorities;

•Among field-based management positions, 74% are women and 49% are minorities; and

•Among our top quartile of compensation for employees, 62% are women and 57% are minorities.

5

Employee Profile

At December 31, 2020, we employed approximately 44,200 people, of whom approximately 5,300 were corporate and field management personnel. The Company's employment of some of its employees is subject to collective bargaining agreements that are negotiated by individual customer facilities and are assented by us, so as to bind us as an “employer” under the agreements. In other cases, we are direct parties to the agreements. We may be adversely affected by relations between our customer facilities and their employee unions, or between us and such unions. We consider our relationship with our employees to be good.

Health and Safety

Our ability to meet the day-to-day needs and expectations of our customers and to fulfill our common goal to ensure the well-being of America’s most vulnerable is organically connected to the well-being of our people. As such, we are committed to the health, safety and wellness of our employees. We provide our employees and their families access to a variety of flexible and convenient health and welfare programs, including benefits that support their physical and mental health by providing tools and resources to help them improve or maintain their health status; and that offer choice where possible so they can customize their benefits to meet their needs and the needs of their families. In response to the COVID-19 pandemic, we implemented significant operating environment changes that we determined were in the best interest of our employees, as well as the communities in which we operate, and which comply with government regulations. This includes having the vast majority of our corporate and field management personnel work from home, while implementing additional safety measures for employees continuing critical on-site work. All employees receive documented, annual training on our Environmental, Health and Safety Policy and are responsible for upholding and operating within the guidelines of this policy to ensure our business complies with all environmental and health and safety laws and regulations applicable to our operations.

Available Information

Healthcare Services Group, Inc. is a reporting company under the Securities Exchange Act of 1934, as amended, and files reports, proxy statements and other information with the Securities and Exchange Commission (the “Commission” or “SEC”). The public may read and copy any of our filings at the Commission’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the Commission at 1-800-SEC-0330. Additionally, because we make filings to the Commission electronically, you may access this information at the Commission’s internet site: www.sec.gov. This site contains reports, proxies and information statements and other information regarding issuers that file electronically with the Commission.

Website Access

Our website address is www.hcsg.com. Our filings with the Commission, as well as other pertinent financial and Company information, are available at no cost on our website as soon as reasonably practicable after the filing of such reports with the Commission.

6

Item 1A. Risk Factors

You should carefully consider the risk factors we have described below, as well as other related information contained within this annual report on Form 10-K as these factors could materially and adversely affect our business, results of operations, financial condition and cash flows. We believe that the risks described below are our most significant risk factors but there may be risks and uncertainties that are not currently known to us or that we currently deem to be immaterial.

Risks Related to Macroeconomic Conditions

COVID-19 and other pandemics, epidemics, or outbreaks of a contagious illness may adversely affect our operating results, cash flows and financial condition.

While the COVID-19 pandemic did not have a material net impact on our consolidated operating results for the year ended December 31, 2020, additional coronavirus outbreaks and other pandemics, epidemics, or outbreaks of a contagious illness, and similar events, may cause harm to us, our employees, our customers, our vendors and supply chain partners, and financial institutions, which could have a material adverse effect on our results of operations, financial condition and cash flows. The impacts may include, but would not be limited to:

•Decreased availability and/or increased cost of supplies due to increased demand around essential cleaning supplies including disinfecting agents, personal protective equipment (“PPE”), and food and food-related products due to increased global demand and disruptions along the global supply chains of these manufactures and distributors;

•Disruption to operations due to the unavailability of employees due to illness, quarantines, risk of illness, travel restrictions or factors that limit our existing or potential workforce;

•Limitations to the availability of our key personnel due to travel restrictions and access restrictions to our customers' facilities;

•Our ability to meet more stringent, medically-required procedures, and infection control requirements at customer facilities;

•Elevated employee turnover which may impact our facility level performance and/or increase payroll expense and recruiting-related expenses;

•Decreased census in the nursing home and long-term care industry, which could impact the financial health of our customers and thereby increasing our associated credit risk with customers and increased pressures to modify our contractual terms; and

•Significant disruption of global financial markets, which could negatively impact us or our customers’ ability to access capital in the future.

In addition, we have taken and will continue to take temporary precautionary measures intended to help minimize the risk of COVID-19 to our employees, including requiring administrative and other groups of our employees to work remotely, restricting non-essential travel and attendance at industry events and in-person work-related meetings.

The further spread of COVID-19, and the requirements to take action to help limit the spread of the virus, could impact the resources required to carry out our business as usual and may have a material adverse effect on our results of operations, financial condition and cash flows. The extent to which COVID-19 will impact our business and our financial results will depend on future developments, which are highly uncertain and cannot be predicted. Such developments may include the ongoing geographic spread of the virus, the severity of the disease, the duration of the outbreak and the type and duration of actions that may be taken by various governmental authorities in response to the outbreak and the impact on the United States and the global economy. Any of these developments, individually or in aggregate, could materially impact our business and our financial results and condition.

We may incur additional liabilities in our Paid Loss Retrospective Insurance Plan for general liability and workers’ compensation insurance related to COVID-19 which may adversely affect our operating results, cash flows and financial condition.

As a result of the impact of COVID-19, litigation claims, enforcement actions, regulatory actions and investigations arising from personal injury and loss of life, have been and may, in the future, be asserted against us. In the event that our known claims experience and/or industry trends result in an unfavorable change in initial estimates of costs to settle such claims resulting from, among other factors, the severity levels of reported claims and medical cost inflation, it would have an adverse effect on our consolidated results of operations, financial condition and cash flows. Although we engage third-party experts to assist us in estimating appropriate reserves, the determination of the required reserves is dependent upon significant actuarial

7

judgments. Changes in our insurance reserves as a result of our periodic evaluation of the related liabilities may cause significant fluctuations in our operating results. We expect many of these claims and actions, or any settlement of these claims and actions, to be covered by insurance and historically the maximum amount of our liability, net of any insurance recoverables, has been limited to our self-insurance retention levels.

We may be adversely affected by inflationary or market fluctuations, including impact of tariffs, in the cost of products consumed in providing our services or our cost of labor. Additionally, we rely on certain vendors for a substantial portion of housekeeping, laundry and dietary supplies.

The prices we pay for the principal items we consume in performing our services are dependent primarily on current market prices. We have consolidated certain supply purchases with national vendors through agreements containing negotiated prospective pricing. In the event such vendors are not able to comply with their obligations under the agreements and we are required to seek alternative suppliers, we may incur increased costs of supplies.

Dietary supplies, to a much greater extent than Housekeeping supplies, are impacted by commodity pricing factors, including the impact of tariffs, which in many cases are unpredictable and outside of our control. We seek to pass on to customers such increased costs but sometimes we are unable to do so. Even when we are able to pass on such costs to our customers, from time to time, sporadic unanticipated increases in the costs of certain supply items due to market or economic conditions may result in a timing delay in passing on such increases to our customers. It is this type of spike and unanticipated increase in Dietary supplies costs that could adversely affect Dietary’s operating performance. The adverse effect would be realized if we delay in passing on such costs to our customers or in instances where we may not be able to pass such increase on to our customers until the time of our next scheduled service billing review. We seek to mitigate the impact of an unanticipated increase in such supplies’ costs through consolidation of vendors, which increases our ability to obtain more favorable pricing.

Our cost of labor may be influenced by factors in certain market areas or changes in the respective collective bargaining agreements to which we are a party. A substantial number of our employees are hourly employees whose wage rates are affected by increases in the federal or state minimum wage rates, wage inflation or local job market adjustments. As collective bargaining agreements are renegotiated, we may need to increase the wages paid to bargaining unit employees covered by such collective bargaining agreements. Although we have contractual rights to pass such union and minimum wage increases through to our customers, our delay in, or inability to pass such wage increases through to our customers could have a material adverse effect on our financial condition, results of operations, and cash flows.

Changes in interest rates and changes in financial market conditions may result in fluctuating and even negative returns in our investments, and could increase the cost of the borrowings under our borrowing agreements.

Although management believes we have a prudent investment policy, we are exposed to fluctuations in interest rates and in the market value of our investment portfolio which could adversely impact our financial condition and results of operations. Our marketable securities consist of municipal bonds. We believe that our investment criteria, which include diversification among issuers of bonds, requirements regarding credit ratings and monitoring of our investments’ duration periods, reduce our exposure related to the financial distress and budget shortfalls that many state and local governments currently face. Increases in market interest rates could adversely affect our payment obligations with respect to our variable-rate borrowing agreements and adversely affect our liquidity and earnings.

Investor and market expectations regarding our financial performance are high and rely greatly on execution of our growth strategy and related increases in financial performance.

The historical performance of our common stock, $0.01 par value (the "Common Stock"), reflects high market expectations for our future operating results. Our business strategy focuses on growth and improving profitability through obtaining service agreements with new customers, providing new services to existing customers, obtaining modest price increases on service agreements with customers and maintaining internal cost reduction strategies at our various operational levels. If we are unable to continue either historical customer revenue and profitability growth rates or projected improvement, our operating performance may be adversely affected and the high expectations for our market performance may not be met. Any failure to meet the market’s high expectations for our revenue and operating results may have an adverse effect on the market price of our Common Stock.

8

Risks Related to Customers and Distributors

We provide services to several customers which contribute significantly, on an individual as well as an aggregate basis, to our total revenues.

Genesis contributed 14.7%, 15.6% and 19.3% of our total consolidated revenues for the years ended December 31, 2020, 2019 and 2018, respectively. On August 10, 2020 as part of Genesis' earnings release, Genesis disclosed significant doubt about its ability to continue as a going concern. Since such announcement, the Company's collection activity from Genesis has been largely unaffected with the Company closely monitoring such Genesis accounts. As of December 31, 2020, the Company had outstanding accounts receivable and notes receivable of $22.5 million and $21.3 million, respectively, from Genesis. Although we expect to continue the relationship with Genesis, there can be no assurance thereof. The loss of Genesis as a customer, or a significant reduction in the revenues we receive from Genesis, could have a material adverse effect on the results of operations of our two operating segments and the Company. In addition, if Genesis fails to abide by current payment terms it could increase our accounts receivable balance and have a material adverse effect on our financial condition, results of operations, and cash flows.

Our customers are concentrated in the healthcare industry, which is subject to changes in government regulation. Many of our customers rely on reimbursement from Medicare, Medicaid and other third-party payors. Rates from such payors may be altered or reduced, thus affecting our customers’ results of operations and cash flows.

We provide our services primarily to providers of long-term and post-acute care. We cannot predict what efforts, and to what extent, legislation and proposals to contain healthcare costs will ultimately impact our customers’ revenues through reimbursement rate modifications. Congress has enacted a number of laws during the past decade that have significantly altered, and may continue to alter, overall government reimbursement for nursing home services. Because many of our customers’ revenues are highly reliant on Medicare, Medicaid and other third-party payors’ reimbursement funding rates and mechanisms, the overall effect of these laws and trends in the long-term care industry have affected and could adversely affect our customers’ cash flows, resulting in their inability to make payments to us on agreed upon payment terms. These factors, in addition to delays in payments from customers have resulted in, and could continue to result in, significant additional bad debts.

The Company has substantial investment in the creditworthiness and financial condition of our customers.

The largest current asset on our balance sheet is the accounts and notes receivable balance from our customers. We grant credit to substantially all of our customers. Deterioration in the financial condition of a significant component of our customer base could hinder our ability to collect amounts due from our customers. Potential causes of such declines include national or local economic downturns, COVID-19's impact on census and operating costs, customers’ dependence on continued Medicare and Medicaid funding and the impact of additional regulatory actions and/or insufficient funding.

We have sometimes extended the period of payment for certain customers beyond contractual terms. Such customers include those who have terminated service agreements and slow payers experiencing financial difficulties. In order to provide for such collection issues and the general risk associated with the granting of credit terms, we have recorded bad debt provisions (in an Allowance for Doubtful Accounts) of $9.6 million for the year ended December 31, 2020 as compared to $25.5 million and $51.4 million for the years ended December 31, 2019 and 2018, respectively. In addition, the Company recorded a $32.1 million cumulative effect adjustment to Retained Earnings on January 1, 2020 in accordance with the Company's adoption of FASB ASC 326, which represented 1.7% of consolidated revenues for the year ended December 31, 2020. In making our credit evaluations, in addition to analyzing and anticipating, where possible, the specific cases described above, we consider the general collection risk associated with trends in the long-term care industry. We establish credit limits through our payment terms, perform ongoing credit evaluations and monitor accounts to minimize the risk of loss. Despite our efforts to minimize credit risk exposure, customers could be adversely affected if future industry trends change in such a manner as to negatively impact their cash flows. If our customers experience a negative impact on their cash flows, it could have a material adverse effect on our financial condition, results of operations, and cash flows.

9

A significant majority of our customer base are multi-facility management groups and independent facility operators who lease the buildings in which they operate and may experience risks relating to their leases including termination, escalators, extensions and special charges.

The credit worthiness of our existing customers, and potential customers, is impacted by their ability to maintain positive relationships with their respective landlords. Any loss or deterioration in the relationship between our customers and their respective landlords may adversely affect their financial condition and ability to make payments on their service agreement with us on agreed upon terms. Any failure by our customers to make rent payments or comply with the provisions of their lease terms could result in the termination of such lease agreements. In such cases, our customers may lose their ability to continue conducting operations and as a result terminate their service agreements with us.

In fiscal 2020, one distributor distributed approximately 50% of our food and non-food dining supplies, and if our relationship or their business were to be disrupted, we could experience disruptions to our operations and cost structure.

Although we negotiate the pricing and other terms for the majority of our purchases of food and dining supplies directly with national manufacturers, we procure these products and other items through Sysco Corporation ("Sysco"). Sysco, is responsible for tracking our orders and delivering products to our specific locations. If our relationship with, or the business of, Sysco were to be disrupted, we would have to arrange alternative distributors and our operations and cost structure could be adversely affected in the short term.

Risks Related to Our Operating Our Business

We have a Paid Loss Retrospective Insurance Plan for general liability and workers’ compensation insurance.

We carry a high deductible general liability and workers’ compensation program and therefore retain a substantial portion of the risk associated with the possible losses under such programs. Under our insurance plans for general liability and workers’ compensation, predetermined loss limits are arranged with our insurance company to limit both our per occurrence cash outlay and annual insurance plan cost. We regularly evaluate our claims pay-out experience and other factors related to the nature of specific claims in arriving at the basis for our accrued insurance claims estimate. Our evaluation is based primarily on current information derived from reviewing our claims experience and industry trends. In the event that our known claims experience and/or industry trends result in an unfavorable change in initial estimates of costs to settle such claims resulting from, among other factors, the severity levels of reported claims and medical cost inflation, it would have an adverse effect on our consolidated results of operations, financial condition and cash flows. Although we engage third-party experts to assist us in estimating appropriate reserves, the determination of the required reserves is dependent upon significant actuarial judgments. Changes in our insurance reserves as a result of our periodic evaluation of the related liabilities may cause significant fluctuations in our operating results.

We primarily provide our services pursuant to agreements which have a one year term, cancelable by either party upon 30 to 90 days’ notice after an initial 60 to 120 day service agreement period.

We typically do not enter into long-term contractual agreements with our customers for the rendering of our services. Our agreements with customers typically provide for a renewable one year service term, cancellable by either party upon 30 to 90 days’ notice after an initial period of 60 to 120 days. Consequently, our customers can often unilaterally decrease the amount of services we provide or terminate all services pursuant to the terms of our service agreements. Although we have historically had a favorable customer retention rate and expect to continue to maintain satisfactory relationships with our customers, in the event the Company were to lose a significant number of customers, such loss could in the aggregate materially adversely affect our consolidated results of operations and financial position.

The Company’s business success depends on the management experience of our key personnel.

We manage and provide our services through a network of management personnel, from on-site facility managers to our executive officers. Therefore, we believe that our ability to recruit and sustain the internal development of managerial personnel is an important factor impacting future operating results and our ability to successfully execute projected growth strategies. Our professional management personnel are the key personnel in maintaining current and selling additional services to existing customers and obtaining new customers.

10

Any perceived or real health risks related to the food industry could adversely affect our Dietary segment.

We are subject to risks affecting the food industry generally including food spoilage and food contamination. Products we purchase and utilize in production are susceptible to contamination by disease-producing organisms, or pathogens, such as listeria monocytogenes, salmonella, campylobacter, hepatitis A, trichinosis and generic E. coli. Because these pathogens are generally found in the environment, there is a risk that these pathogens could be introduced to our products as a result of improper handling at the manufacturing, processing or food service level. Our suppliers’ manufacturing facilities and products are subject to extensive laws and regulations relating to health, food preparation, sanitation and safety standards. Difficulties or failures by these companies in obtaining any required licenses or approvals or otherwise complying with such laws and regulations could disrupt their operations which could adversely affect our operations. Furthermore, there can be no assurance that compliance with governmental regulations by our suppliers will eliminate the risks related to food safety. To the extent there is an outbreak of food related illness in any of our customer facilities, it could materially harm our business, results of operations and financial condition.

Additionally, the Company may be subject to liability if the consumption of our food products causes injury, illness or death. Even if a product liability claim is unsuccessful or is not fully pursued, the negative publicity surrounding any assertion that our products caused injury or illness could adversely affect our reputation.

Failure to maintain effective internal control over financial reporting could have a material adverse effect on our ability to report our financial results on a timely and accurate basis.

Failure to maintain appropriate and effective internal controls over our financial reporting could result in misstatements in our financial statements and potentially subject us to sanctions or investigations by the SEC or other regulatory authorities, and could cause us to delay the filing of required reports with the SEC and our reporting of financial results. Any of these events could result in a decline in the market price of our Common Stock. Although we have taken steps to maintain our internal control structure as required, we cannot guarantee that a control deficiency will not result in a misstatement in the future.

Any decrease in or suspension of our dividend could cause our stock price to decline.

We expect to continue to pay a regular quarterly cash dividend. However, our dividend policy and the payment of future cash dividends under the policy are subject to the final determination each quarter by our Board of Directors that (i) the dividend will be made in compliance with laws applicable to the declaration and payment of cash dividends, including Section 1551(b) of the Pennsylvania Business Corporation Law, and (ii) the policy remains in our best interests, which determination will be based on a number of factors, including the impact of changing laws and regulations, economic conditions, our results of operations and/or financial condition, capital resources, financial covenants under our credit facility and other factors considered relevant by the Board of Directors. While we have continually increased the amount of our dividends, given these considerations, there can be no assurance these increases will continue and our Board of Directors may increase or decrease the amount of the dividend at any time and may also decide to suspend or discontinue the payment of cash dividends in the future. Any decrease in the amount of the dividend, or suspension or discontinuance of the payment of a dividend, could cause our stock price to decline.

11

Our business could be negatively affected as a result of actions of activist shareholders, and such activism could impact the trading value of our securities.

Shareholders may, from time to time, engage in proxy solicitations or advance shareholder proposals, or otherwise attempt to effect changes and assert influence on our board of directors and management. Activist campaigns that contest or conflict with our strategic direction or seek changes in the composition of our board of directors could have an adverse effect on our operating results and financial condition. A proxy contest would require us to incur significant legal and advisory fees, proxy solicitation expenses and administrative and associated costs and require significant time and attention by our board of directors and management, diverting their attention from the pursuit of our business strategy. Any perceived uncertainties as to our future direction and control, our ability to execute on our strategy, or changes to the composition of our board of directors or senior management team arising from a proxy contest could lead to the perception of a change in the direction of our business or instability which may result in the loss of potential business opportunities, make it more difficult to pursue our strategic initiatives, or limit our ability to attract and retain qualified personnel and business partners, any of which could adversely affect our business and operating results. If individuals are ultimately elected to our board of directors with a specific agenda, it may adversely affect our ability to effectively implement our business strategy and create additional value for our shareholders. We may choose to initiate, or may become subject to, litigation as a result of a proxy contest or matters arising from a proxy contest, which would serve as a further distraction to our board of directors and management and would require us to incur significant additional costs. In addition, actions such as those described above could cause significant fluctuations in our stock price based upon temporary or speculative market perceptions or other factors that do not necessarily reflect the underlying fundamentals and prospects of our business.

Risks Related to Governmental and Regulatory Changes

Changes to federal healthcare legislation may adversely affect our operating costs and results of operations.

Continued changes to the health insurance industry and its obligations on employers could impact our operating costs. Any requirements to provide additional benefits to our employees or the payment of penalties if such benefits are not provided, would increase our expenses. If we are unable to pass-through these charges to our customers to cover these expenses, such increases could adversely impact our operating costs and our results of operations.

In addition, often new regulations result in additional reporting requirements for businesses. These and other requirements could result in increased costs, expanded liability exposure, and other changes in the way we provide healthcare insurance and other benefits to our employees.

States in which our customers are located could experience significant budget deficits and such deficits may result in reduction of reimbursements to nursing homes.

States in which our customers are located could have budget deficits as a result of lower than projected revenue collections and increased demand for the funding of entitlements. As a result of these and other adverse economic factors, state Medicaid programs have and may revise reimbursement structures for nursing home services. Any disruption or delay in the distribution of Medicaid and related payments to our customers will adversely affect their cash flows and impact their ability to pay us as agreed upon for the services provided.

Governmental regulations related to labor, employment, immigration and health and safety could adversely impact our results of operations and financial condition.

Our business is subject to various federal, state, and local laws and regulations in areas such as labor, employment, immigration, and health and safety. These laws frequently evolve through case law, legislative changes and changes in regulatory interpretation, implementation and enforcement. Our policies and procedures and compliance programs are subject to adjustments in response to these changing regulatory and enforcement environments, which could increase our cost of services provided. Although we have contractual rights to pass through cost increases we incur to our customers due to regulatory changes, our delay in, or inability to pass such costs through to our customers, could have a material adverse effect on our financial condition, results of operations and cash flows.

12

In addition, if we fail to comply with applicable laws, we may be subject to lawsuits, investigations, criminal sanctions or civil remedies, including fines, penalties, damages, reimbursements, or injunctions. Also, our customers’ facilities are subject to periodic inspection by federal, state, and local authorities for compliance with state and local departments of health requirements. Expenses resulting from failed inspections of the departments that we service could result in our customers being fined and seeking recovery from us, which could also adversely impact our financial condition, results of operations, and cash flows.

Federal, state and local tax rules can adversely impact our results of operations and financial position.

We are subject to federal, state and local taxes in the United States. Significant judgment is required in determining the provision for income taxes. We believe our income tax estimates are reasonable, but such estimates assume no changes in current tax rates. In addition, if the Internal Revenue Service or other taxing authority disagrees on a tax position we have taken and upon final adjudication we are required to change such position, we could incur additional tax liability, including interest and penalties. Such costs and expenses could have a material adverse impact on our financial condition, results of operations, and cash flows. Additionally, the taxability of our services is subject to various interpretations within the taxing jurisdictions in which we operate. Consequently, in the ordinary course of business, a jurisdiction may contest our reporting positions with respect to the application of its tax code to our services. A conflicting position taken by a state or local taxation authority on the taxability of our services could result in additional tax liabilities and could negatively impact our competitive position in that jurisdiction. If we fail to comply with applicable tax laws and regulations, we could suffer civil or criminal penalties in addition to the delinquent tax assessment. In the taxing jurisdictions where our services have been determined to be subject to tax, the jurisdiction may increase the tax rate assessed on such services. We seek to pass-through to our customers such tax increases. In the event we are not able to pass-through any portion of the tax increase, our results of operations, financial condition and cash flows could be adversely impacted.

We assess contingencies to determine the degree of probability and range of possible loss for potential accrual in our financial statements. We would accrue an estimated loss contingency in our financial statements if it were probable that a liability had been incurred and the amount of the loss could be reasonably estimated. Due to the unpredictable nature of litigation, assessing contingencies is highly subjective and requires judgments about future events. The amount of actual losses may differ from our current assessment. As a result of the costs and expenses of defending ourselves against lawsuits or claims, and risks and consequences of legal actions, regardless of merit, our results of operations and financial position could be adversely affected or cause variability in our results compared to expectations.

13

The SEC’s investigation into our earnings per share (“EPS”) calculation practices could result in potential sanctions or penalties, distraction to our management and result in litigation from third parties, each of which could adversely affect or cause variability in our financial results.

Beginning in November 2017, the Company has been in dialogue with the SEC regarding EPS calculation, rounding and reporting practices and in March 2018 we learned that the SEC had opened a formal investigation into these matters. In response to the SEC’s investigation, during the fourth quarter of 2018, the Company authorized its outside counsel to conduct an internal investigation, under the direction of the Company’s Audit Committee regarding these matters. The internal investigation was completed in March 2019 and prior to the filing of our Annual Report on Form 10-K for the fiscal year ended December 31, 2018.

Notwithstanding the completion of the internal investigation, the SEC’s investigation is ongoing and there can be no assurance that the SEC or another regulatory body will not make further regulatory inquiries or pursue further action that could result in significant costs and expenses including potential sanctions or penalties as well as distraction to management. The ongoing SEC investigation and/or any related litigation could adversely affect or cause variability in our financial results.

On March 22, 2019, a putative shareholder class action lawsuit alleging violations of the federal securities laws was filed against the Company and our Chief Executive Officer in the U.S. District Court for the Eastern District of Pennsylvania in connection with the matters related to the SEC investigation. The class action complaint was amended on September 17, 2019. Please refer to “Item 3. Legal Proceedings” and “Note 17—Other Contingencies ” to the consolidated financial statements included in this Form 10-K for more information. We cannot predict the outcome of the lawsuit, the magnitude of any potential losses or the effect such litigation may have on us or our operations. Regardless of the outcome, lawsuits and investigations involving us, or our current or former officers and directors, could result in significant expenses and divert attention and resources of our management and other key employees. We could be required to pay damages or other penalties or have injunctions or other equitable remedies imposed against us or our current or former directors and officers including any obligation to indemnify our current and former directors and officers in connection with lawsuits, governmental investigations and related litigation or settlement amounts. Such amounts could exceed the coverage provided under our insurance policies. Any of these factors could harm our reputation, business, financial condition, results of operations or cash flows. In addition, the Company may be subject to further litigation from third parties related to the matters under review by the SEC.

Our business and financial results could be adversely affected by unfavorable results of material litigation or governmental inquiries.

In addition to the SEC investigation and class action lawsuit, we are currently involved in civil litigation and government inquiries which arise in the ordinary course of business. These matters relate to, among other things, general liability, payroll or employee-related matters. Legal actions could result in substantial monetary damages and expenses and may adversely affect our reputation and business status with our customers, whether or not we are ultimately determined to be liable. The outcome of litigation, particularly class action and collective action lawsuits and regulatory actions, is difficult to assess or quantify. The plaintiffs in these types of actions may seek recovery of very large or indeterminate amounts, and estimates may remain unknown for substantial periods of time.

Risks Related to Cybersecurity and Data Privacy

Cyber-attacks and breaches could cause operational disruptions, fraud or theft of sensitive information.

Aspects of our operations are reliant upon internet-based activities, such as ordering supplies and back-office functions such as accounting and transaction processing, making and accepting payments, processing payroll and other administrative functions, etc. A significant disruption or failure of our information technology systems may have a significant impact on our operations, potentially resulting in service interruptions, security violations, regulatory compliance failures and other operational difficulties. In addition, any attack perpetrated against our information systems including through a system failure, security breach or disruption by malware or other damage, could similarly impact our operations and result in loss or misuse of information, litigation and potential liability. Although we have taken steps intended to mitigate the risks presented by potential cyber incidents, it is not possible to protect against every potential power loss, telecommunications failure, cybersecurity attack or similar event that may arise. Moreover, the safeguards we use are subject to human implementation and maintenance and to other uncertainties. Any of these cyber incidents may result in a violation of applicable laws or regulations (including privacy and other laws), damage our reputation, cause a loss of customers and give rise to monetary fines and other penalties, which could be significant. Such events could have an adverse effect on our financial condition, results of operations, and liquidity.

14

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

We lease our corporate offices, located at 3220 Tillman Drive, Bensalem, Pennsylvania 19020. We also lease office space at other locations in Colorado, South Carolina, Connecticut, Texas, Florida and New Jersey. The New Jersey office is the headquarters of our wholly-owned subsidiaries. The other locations serve as divisional or regional offices providing management and administrative services to both of our operating segments in their respective geographical areas.

We are also provided with office and storage space at each of our customers’ facilities.

Management does not foresee any difficulties with regard to the continued utilization of these premises. We also believe that such properties are sufficient to support our current operations.

We own office furniture and equipment, housekeeping and laundry equipment, and vehicles. The office furniture and equipment and vehicles are primarily located at the corporate office, divisional and regional offices. We have housekeeping equipment at all customer facilities where we provide services under a full service housekeeping agreement. Generally, the aggregate cost of housekeeping equipment located at each customer facility is approximately $4,000. Additionally, we have laundry installations at certain customer facilities. We believe that such laundry equipment, office furniture and equipment, housekeeping equipment and vehicles are sufficient to support our current operations.

Item 3. Legal Proceedings.

In the normal course of business, the Company is involved in various administrative and legal proceedings, including labor and employment, contracts, personal injury, and insurance matters.

As previously disclosed, the SEC is conducting an investigation into our EPS calculation practices. Following receipt of a letter from the SEC in November 2017 regarding its inquiry into those practices followed by a subpoena in March 2018, we authorized our outside counsel to conduct an internal investigation, under the direction of the Company’s Audit Committee, into matters related to the SEC subpoena. This investigation was completed in March 2019 and we continue to cooperate with the SEC’s investigation and document requests.

The Company and the SEC have recently commenced discussions regarding a potential resolution of the investigation, which focuses on periods prior to 2018. As discussions regarding a potential resolution with the SEC are ongoing, Mr. John C. Shea, the Company’s Chief Financial Officer, has notified the Company that he is taking a temporary leave of absence from his duties, with effect from February 9, 2021. On February 9, 2021, the Board of Directors of the Company appointed Mr. Andrew Brophy as the Company’s Acting Principal Accounting Officer with immediate effect. Mr. Brophy has served as the Company’s Director of Accounting since November 2020 and SEC Reporting Manager since January 2018.

On March 22, 2019, a putative shareholder class action lawsuit was filed against the Company and our Chief Executive Officer in the U.S. District Court for the Eastern District of Pennsylvania. The initial complaint, which was filed by a plaintiff purportedly on behalf of all purchasers of our securities between April 11, 2017 and March 4, 2019, alleges violations of the federal securities laws in connection with the matters related to our EPS calculation practices. On September 17, 2019, the complaint was amended to, among other things, extend the Class Period to cover the period between April 8, 2014 and March 4, 2019, and to name additional individuals affiliated with the Company as defendants. The lead plaintiff seeks unspecified monetary damages and other relief on behalf of the plaintiff class.

While the Company is vigorously defending against all litigation claims asserted, this litigation—along with the ongoing SEC investigation—could result in substantial costs to the Company and a diversion of the Company’s management’s attention and resources, which could harm its business. In addition, the uncertainty of the pending lawsuit or potential filing of additional lawsuits could lead to more volatility and a reduction in the Company’s stock price. At this time the Company is unable to reasonably estimate possible losses or form a judgment that an unfavorable outcome is either probable or remote.

In light of the uncertainties involved in such proceedings, the ultimate outcome of a particular matter could become material to the Company’s results of operations for a particular period depending on, among other factors, the size of the loss or liability imposed and the level of the Company’s operating income for that period.

15

Item 4. Mine Safety Disclosures.

Not applicable.

16

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market Information

The Company’s Common Stock is traded under the symbol “HCSG” on the NASDAQ Global Select Market. As of February 24, 2021, there were approximately 74.7 million shares of our Common Stock outstanding.

Holders

As of February 24, 2021, we had approximately 405 holders of record of our Common Stock. This does not include persons who hold our Common Stock in nominee or “street name” accounts through brokers or banks.

Securities Authorized for Issuance Under Equity Compensation Plans

The following table sets forth the Company’s equity compensation plans, on an aggregated basis, the number of shares of our Common Stock subject to outstanding stock awards, the weighted-average exercise price of stock awards, and the number of shares remaining available for future award grants as of December 31, 2020.

| Plan Category | Number of Securities to be Issued Upon Exercise of Outstanding Options, Warrants and Rights | Weighted-Average Exercise Price of Outstanding Options, Warrants and Rights | Number of Securities Remaining Available for Future Issuance Under Equity Compensation Plans (Excluding Securities Issued and not Exercised) | ||||||||||||||||||||

| (in thousands, except per share amounts) | |||||||||||||||||||||||

| Equity compensation plans approved by security holders | 2,098 | 1 | $ | 33.35 | 4,920 | 2 | |||||||||||||||||

| Total | 2,098 | $ | 33.35 | 4,920 | |||||||||||||||||||

1.Represents shares of Common Stock issuable upon exercise of outstanding stock awards granted under the 2020 Omnibus Incentive Plan ("the 2020 Plan") and carryover shares from pre-existing equity plans.

2.Includes stock awards to purchase 2.5 million shares available for future grant under the 2020 Plan, 2.1 million shares available for issuance under the Company’s 1999 Employee Stock Purchase Plan as amended (the “1999 Plan”) and 0.3 million shares available for issuance under the Company’s Amended and Restated Deferred Compensation Plan (the "Deferred Compensation Plan"). Treasury shares may be issued under the 1999 Plan and the Company’s Deferred Compensation Plan.

17

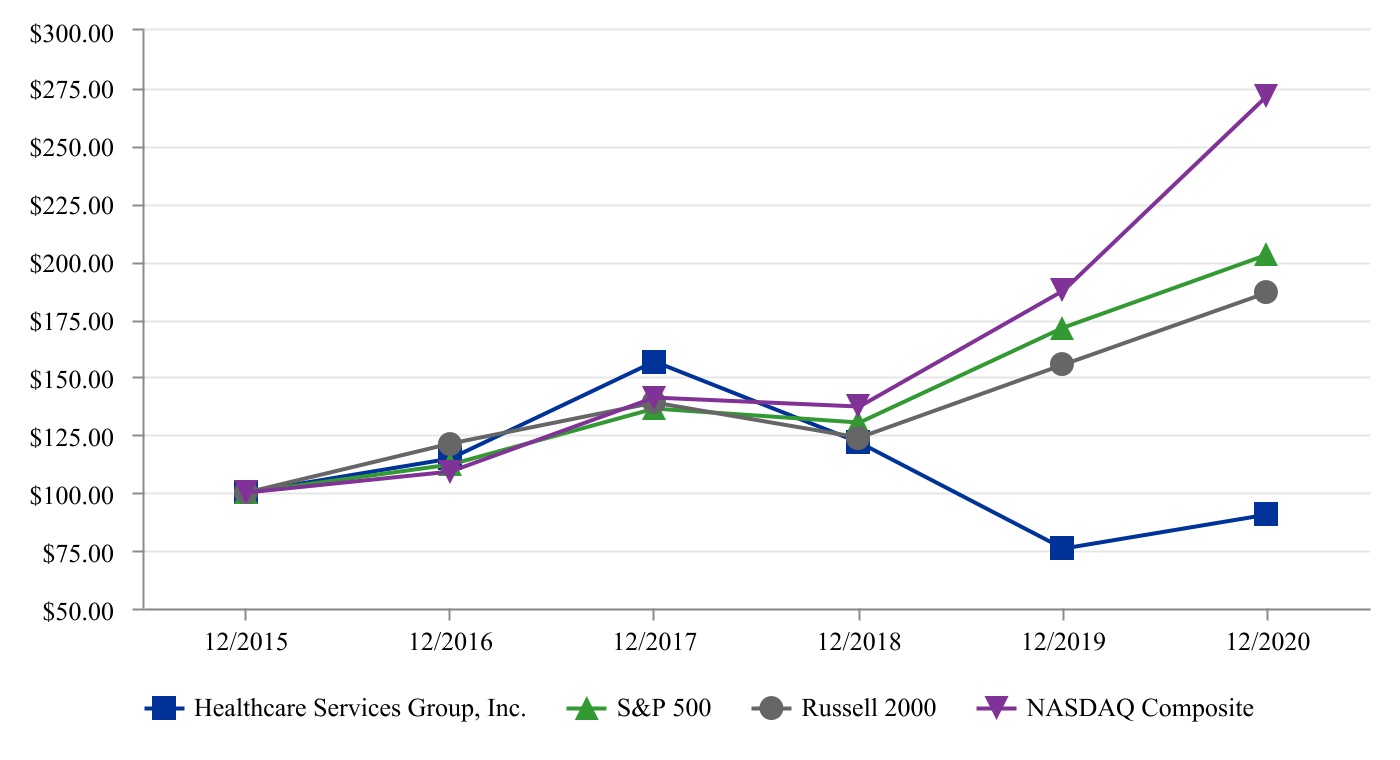

Performance Graph

The following graph matches the Company’s cumulative five-year total shareholder return on Common Stock with the cumulative total returns of the S&P 500 index, the NASDAQ Composite index and the Russell 2000 index. The graph tracks the performance of a $100 investment in our Common Stock and in each index (with the reinvestment of all dividends) from December 31, 2015 to December 31, 2020. The stock price performance included in this graph is not necessarily indicative of future stock price performance.

We have not defined a peer group based on either industry classification or financial characteristics. We believe the Company is unique in its service offerings and customer base, and among its closest industry peers, it is unique in size and financial profile. As such, we opted to utilize the Russell 2000 index to compare the Company performance to issuers with similar market capitalization.

Comparison of 5 Year Cumulative Total Return*

Among Healthcare Services Group, Inc., the S&P 500 Index, the NASDAQ Composite Index and the Russell 2000 Index

*$100 invested on December 31, 2015 in stock or index, including reinvestment of dividends.

Fiscal year ending December 31.

Copyright© 2021 Standard & Poor’s, a division of S&P Global. All rights reserved.

Copyright© 2021 Russell Investment Group. All rights reserved.

| December 31, | ||||||||||||||||||||||||||||||||||||||

| Company / Index | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | ||||||||||||||||||||||||||||||||

| Healthcare Services Group, Inc. | $ | 100.00 | $ | 114.57 | $ | 156.70 | $ | 121.61 | $ | 75.71 | $ | 90.51 | ||||||||||||||||||||||||||

| S&P 500 | $ | 100.00 | $ | 111.96 | $ | 136.40 | $ | 130.42 | $ | 171.49 | $ | 203.04 | ||||||||||||||||||||||||||

| Russell 2000 | $ | 100.00 | $ | 121.31 | $ | 139.08 | $ | 123.76 | $ | 155.35 | $ | 186.36 | ||||||||||||||||||||||||||

| NASDAQ Composite | $ | 100.00 | $ | 108.87 | $ | 141.13 | $ | 137.12 | $ | 187.44 | $ | 271.64 | ||||||||||||||||||||||||||

18

Unregistered Sales of Equity Securities and Use of Proceeds

None.

Item 6. Selected Financial Data.

Reserved.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operation.

You should read the following discussion and analysis of our financial condition and results of our operations in conjunction with our Consolidated Financial Statements and the related notes to those statements included elsewhere in this report. This discussion contains forward-looking statements reflecting our current expectations that involve risks and uncertainties. Our actual results and the timing of events may differ materially from those contained in these forward-looking statements due to a number of factors, including those discussed in the section entitled “Risk Factors,” and elsewhere in this report on Form 10-K. We are on a calendar year end, and except where otherwise indicated, “2020” refers to the year ended December 31, 2020, and “2019” refers to the year ended December 31, 2019. Discussions of 2018 items and year-to-year comparisons between 2019 and 2018 that are not included in this Form 10-K can be found in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II, Item 7 of our Annual Report on Form 10-K for the fiscal year ended December 31, 2019.

Results of Operations