Exhibit 99.2

www.thorindustries.com FIRST QUARTER OF FISCAL 2023 FINANCIAL RESULTS

FORWARD - LOOKING STATEMENTS This presentation includes certain statements that are “forward - looking” statements within the meaning of the U . S . Private Securities Litigation Reform Act of 1995 , Section 27 A of the Securities Act of 1933 , as amended, and Section 21 E of the Securities Exchange Act of 1934 , as amended . These forward - looking statements are made based on management’s current expectations and beliefs regarding future and anticipated developments and their effects upon THOR, and inherently involve uncertainties and risks . These forward - looking statements are not a guarantee of future performance . We cannot assure you that actual results will not differ materially from our expectations . Factors which could cause materially different results include, among others : the impact of inflation on the cost of our products as well as on general consumer demand ; the effect of raw material and commodity price fluctuations, and/or raw material, commodity or chassis supply constraints ; the impact of war, military conflict, terrorism and/or cyber - attacks, including state - sponsored or ransom attacks ; the impact of sudden or significant adverse changes in the cost and/or availability of energy or fuel, including those caused by geopolitical events, on our costs of operation, on raw material prices, on our suppliers, on our independent dealers or on retail customers ; the dependence on a small group of suppliers for certain components used in production, including chassis ; interest rate fluctuations and their potential impact on the general economy and, specifically, on our profitability and on our independent dealers and consumers ; the extent and impact from the continuation of the COVID - 19 pandemic, along with the responses to contain the spread of the virus, or its variants, by various governmental entities or other actors, which may have negative effects on retail customer demand, our independent dealers, our supply chain, our labor force, our production or other aspects of our business ; the ability to ramp production up or down quickly in response to rapid changes in demand while also managing costs and market share ; the level and magnitude of warranty and recall claims incurred ; the ability of our suppliers to financially support any defects in their products ; legislative, regulatory and tax law and/or policy developments including their potential impact on our independent dealers, retail customers or on our suppliers ; the costs of compliance with governmental regulation ; the impact of an adverse outcome or conclusion related to current or future litigation or regulatory investigations ; public perception of and the costs related to environmental, social and governance matters ; legal and compliance issues including those that may arise in conjunction with recently completed transactions ; lower consumer confidence and the level of discretionary consumer spending ; the impact of exchange rate fluctuations ; restrictive lending practices which could negatively impact our independent dealers and/or retail consumers ; management changes ; the success of new and existing products and services ; the ability to maintain strong brands and develop innovative products that meet consumer demands ; the ability to efficiently utilize existing production facilities ; changes in consumer preferences ; the risks associated with acquisitions, including : the pace and successful closing of an acquisition, the integration and financial impact thereof, the level of achievement of anticipated operating synergies from acquisitions, the potential for unknown or understated liabilities related to acquisitions, the potential loss of existing customers of acquisitions and our ability to retain key management personnel of acquired companies ; a shortage of necessary personnel for production and increasing labor costs and related employee benefits to attract and retain production personnel in times of high demand ; the loss or reduction of sales to key independent dealers ; disruption of the delivery of units to independent dealers or the disruption of delivery of raw materials, including chassis, to our facilities ; increasing costs for freight and transportation ; the ability to protect our information technology systems from data breaches, cyber - attacks and/or network disruptions ; asset impairment charges ; competition ; the impact of losses under repurchase agreements ; the impact of the strength of the U . S . dollar on international demand for products priced in U . S . dollars ; general economic, market and political conditions in the various countries in which our products are produced and/or sold ; the impact of changing emissions and other related climate change regulations in the various jurisdictions in which our products are produced, used and/or sold ; changes to our investment and capital allocation strategies or other facets of our strategic plan ; and changes in market liquidity conditions, credit ratings and other factors that may impact our access to future funding and the cost of debt . These and other risks and uncertainties are discussed more fully in our Quarterly Report on Form 10 - Q for the quarter ended October 31 , 2022 and in Item 1 A of our Annual Report on Form 10 - K for the year ended July 31 , 2022 . We disclaim any obligation or undertaking to disseminate any updates or revisions to any forward - looking statements contained in this presentation or to reflect any change in our expectations after the date hereof or any change in events, conditions or circumstances on which any statement is based, except as required by law . 2

FIRST QUARTER FISCAL 2023 HIGHLIGHTS 3 Resilient Financial Performance Continues in a Shifting Market Net sales of $3.1 billion in 1Q23, down from a fiscal first quarter record of $4.0 billion in the prior - year period ▪ Towable production continued to be actively managed to align to retail demand ▪ Continued progress in restocking dealer inventory levels of North American motorized product ▪ Interest in RV lifestyle and order backlogs remained elevated at 10/31/2022 versus pre - pandemic levels Diluted EPS of $2.53 ▪ Variable cost structure and management focus maintained strong gross margin performance (15.7%) through market volatility ▪ Solid pricing and execution contributed favorably to profitability Generated $94.0 million of net cash flow from operations ▪ Repurchased $25.4 million of common stock and increased regular quarterly dividend for the 13th consecutive year ▪ Debt also reduced by $27.4 million Entered into strategic partnership with Harbinger Motors, Inc. ▪ Furthers THOR’s innovation efforts to advance eMobility strategy

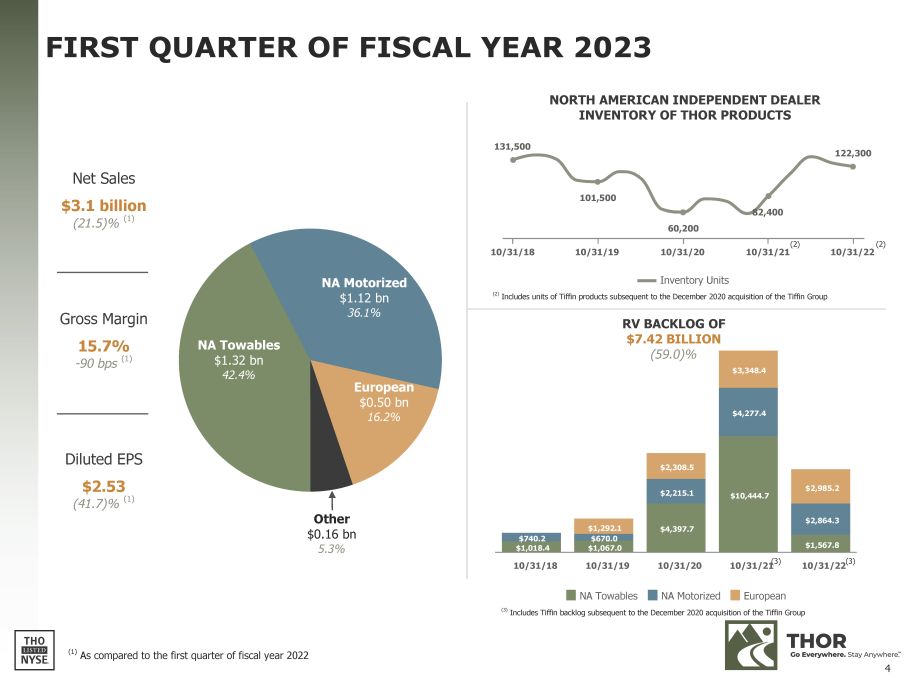

$4,397.7 $10,444.7 $740.2 $670.0 $2,215.1 $4,277.4 $2,864.3 $1,292.1 $2,308.5 $3,348.4 $2,985.2 NA Towables NA Motorized European (3) Includes Tiffin backlog subsequent to the December 2020 acquisition of the Tiffin Group European $0.50 bn 16.2% NA Motorized $1.12 bn 36.1% NA Towables $1.32 bn 42.4% Other $0.16 bn 5.3% 131,500 101,500 82,400 122,300 60,200 10/31/18 10/31/19 10/31/20 10/31/21 10/31/22 NORTH AMERICAN INDEPENDENT DEALER INVENTORY OF THOR PRODUCTS RV BACKLOG OF $7.42 BILLION (59.0)% Inventory Units (2) Includes units of Tiffin products subsequent to the December 2020 acquisition of the Tiffin Group (1) As compared to the first quarter of fiscal year 2022 FIRST QUARTER OF FISCAL YEAR 2023 Gross Margin 15.7% - 90 bps (1) Diluted EPS $2.53 (41.7)% (1) Net Sales $3.1 billion (21.5)% (1) (2) 4 (2) $1,018.4 $1,067.0 $1,567.8 10/31/18 10/31/19 10/31/20 10/31/21 (3) 10/31/22 (3)

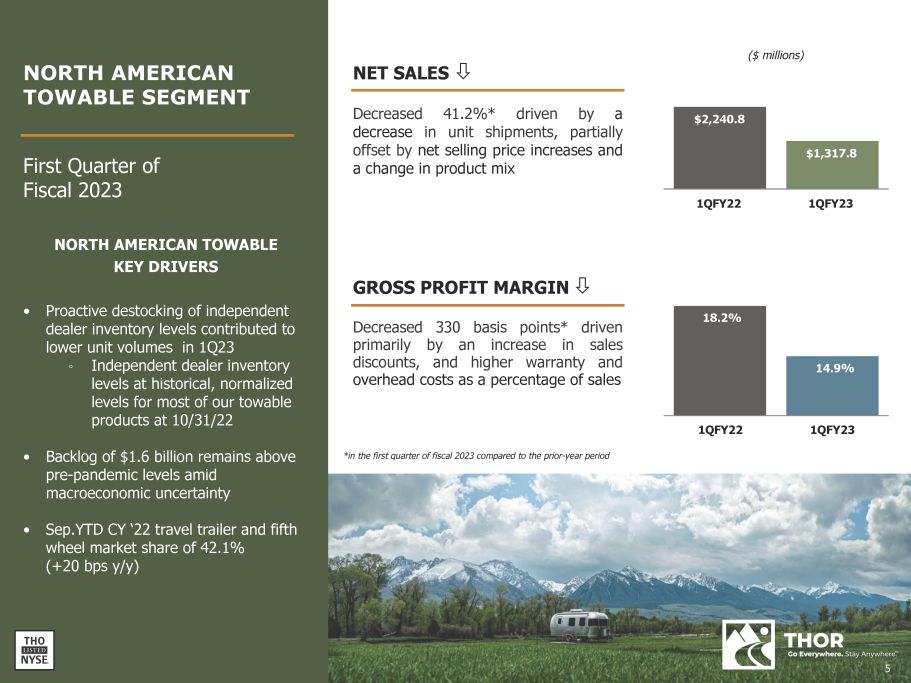

($ millions) $2,240.8 $1,317.8 1QFY22 1QFY23 18.2% 14.9% 1QFY22 1QFY23 NET SALES ,!J Decreased 41 . 2 % * driven by a decrease in unit shipments, partially offset by net selling price increases and a change in product mix Decreased 330 basis points* driven primarily by an increase in sales discounts, and higher warranty and overhead costs as a percentage of sales NORTH AMERICAN TOWABLE KEY DRIVERS GROSS PROFIT MARGIN ,!J • Proactive destocking of independent dealer inventory levels contributed to lower unit volumes in 1Q23 ◦ Independent dealer inventory levels at historical, normalized levels for most of our towable products at 10 / 31 / 22 • Backlog of $1.6 billion remains above pre - pandemic levels amid macroeconomic uncertainty • Sep.YTD CY ‘22 travel trailer and fifth wheel market share of 42.1% (+20 bps y/y) First Quarter of Fiscal 2023 *in the first quarter of fiscal 2023 compared to the prior - year period NORTH AMERICAN TOWABLE SEGMENT 5

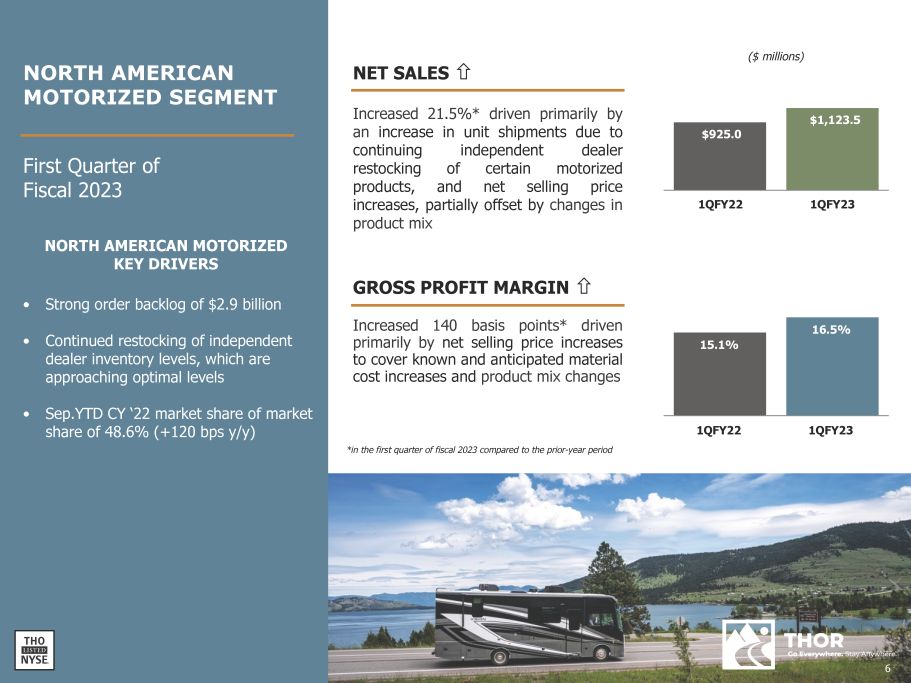

NET SALES is Increased 21.5%* driven primarily by an increase in unit shipments due to continuing independent dealer restocking of certain motorized products, and net selling price increases, partially offset by changes in product mix ($ millions) $925.0 $1,123.5 1QFY22 1QFY23 15.1% 16.5% 1QFY22 1QFY23 GROSS PROFIT MARGIN is Increased 140 basis points* driven primarily by net selling price increases to cover known and anticipated material cost increases and product mix changes *in the first quarter of fiscal 2023 compared to the prior - year period First Quarter of Fiscal 2023 NORTH AMERICAN MOTORIZED KEY DRIVERS • Strong order backlog of $2.9 billion • Continued restocking of independent dealer inventory levels, which are approaching optimal levels • Sep.YTD CY ‘22 market share of market share of 48.6% (+120 bps y/y) 6 NORTH AMERICAN MOTORIZED SEGMENT

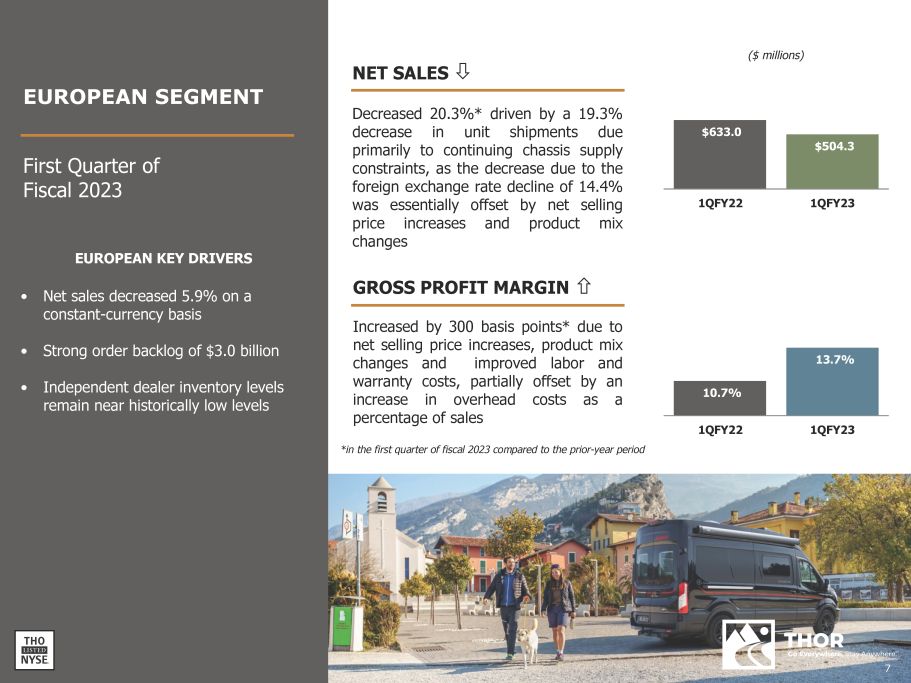

EUROPEAN KEY DRIVERS • Net sales decreased 5.9% on a constant - currency basis • Strong order backlog of $3.0 billion • Independent dealer inventory levels remain near historically low levels NET SALES - 0J Decreased 20 . 3 % * driven by a 19 . 3 % decrease in unit shipments due primarily to continuing chassis supply constraints, as the decrease due to the foreign exchange rate decline of 14 . 4 % was essentially offset by net selling price increases and product mix changes GROSS PROFIT MARGIN is Increased by 300 basis points* due to net selling price increases, product mix changes and improved labor and warranty costs, partially offset by an increase in overhead costs as a percentage of sales ($ millions) $633.0 $504.3 1QFY22 1QFY23 10.7% 13.7% 1QFY22 1QFY23 *in the first quarter of fiscal 2023 compared to the prior - year period EUROPEAN SEGMENT First Quarter of Fiscal 2023 7

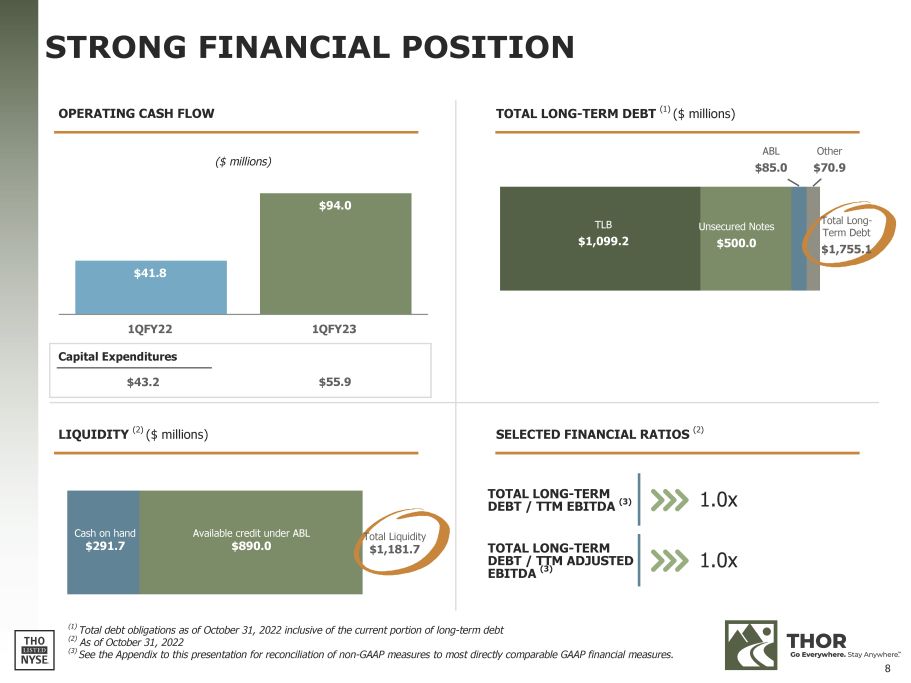

TOTAL LONG - TERM DEBT / TTM EBITDA (3) 1.0x TOTAL LONG - TERM DEBT / TTM ADJUSTED EBITDA (3) 1.0x STRONG FINANCIAL POSITION ($ millions) $41.8 $94.0 1QFY22 1QFY23 OPERATING CASH FLOW TOTAL LONG - TERM DEBT (1) ($ millions) (1) Total debt obligations as of October 31, 2022 inclusive of the current portion of long - term debt (2) As of October 31, 2022 (3) See the Appendix to this presentation for reconciliation of non - GAAP measures to most directly comparable GAAP financial measures. LIQUIDITY (2) ($ millions) SELECTED FINANCIAL RATIOS (2) TLB $1,099.2 Unsecured Notes $500.0 ABL $85.0 Other $70.9 Total Long - Term Debt $1,755.1 Cash on hand $291.7 Available credit under ABL $890.0 Total Liquidity $1,181.7 Capital Expenditures $43.2 $55.9 8

CAPITAL MANAGEMENT CAPITAL ALLOCATION PRIORITIES Invest in THOR’s business ▪ Capex spending of $55.9 million in 1Q23 Pay THOR's dividend ▪ Increased regular quarterly dividend to $0.45 ▪ Represents 13th consecutive year of dividend increases Reduce the Company's debt obligations ▪ Reduced debt with principal payments of $12.4 million on our Term Loan and paydown of $15.0 million on the ABL Repurchase shares on a strategic and opportunistic basis ▪ Repurchased $25.4 million in 1Q23 ▪ $507.8 million available to be repurchased as of October 31, 2022 under current authorizations Support opportunistic strategic investments 9

Proven Track Record of Managing Through Economic Cycles and Emerging a Stronger Company FAST + FLEXIBLE + FOCUSED BUSINESS MODEL Positions THOR to Outperform the Industry in Fiscal 2023 FAST & FLEXIBLE LONG - TERM FOCUS Variable Cost Structure Strategic Growth Opportunities ✓ Labor and variable costs managed to production levels ■ ~ 85% of COGS is variable ✓ Variable compensation automatically flexes with demand environment ✓ Efficient utilization and optimization of production footprint across network of >400 facilities worldwide ✓ Strong net cash from operations with flexible and prudent capital expenditures ✓ Working capital levels aligned to production levels ■ Identify and invest in high ROI capital projects ■ Accelerate innovation and automation ■ Pursue strategic partnerships ჲ announced partnership with Harbinger Motors, Inc ■ Grow recurring revenue streams in supply and aftermarkets business ■ Accretive share repurchases ■ Tuck - in acquisitions to drive long - term growth 10

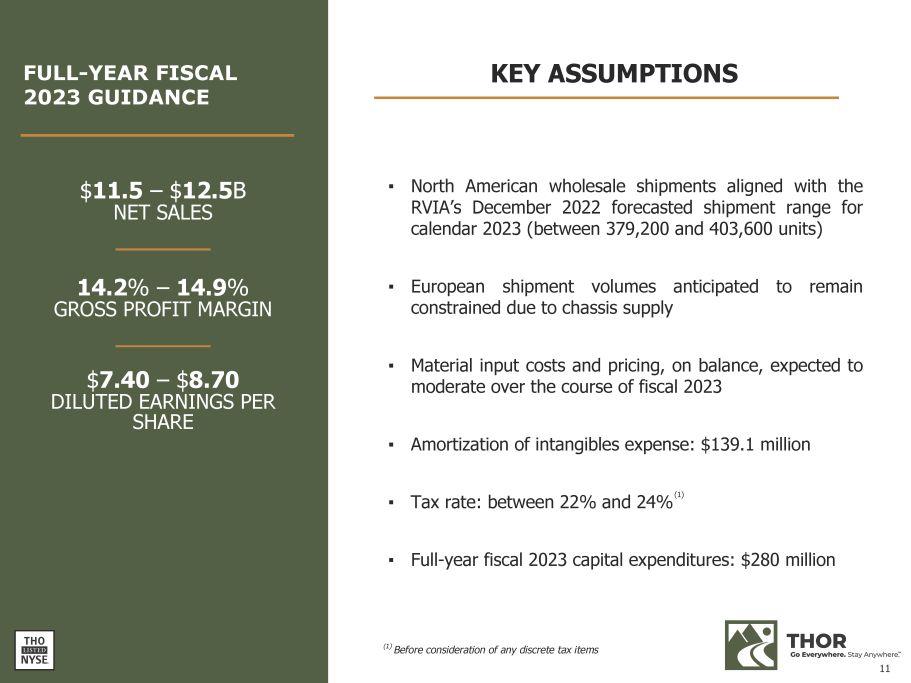

FULL - YEAR FISCAL 2023 GUIDANCE KEY ASSUMPTIONS ▪ North American wholesale shipments aligned with the RVIA’s December 2022 forecasted shipment range for calendar 2023 (between 379 , 200 and 403 , 600 units) ▪ European shipment volumes anticipated to remain constrained due to chassis supply ▪ Material input costs and pricing, on balance, expected to moderate over the course of fiscal 2023 ▪ Amortization of intangibles expense: $139.1 million ▪ Tax rate: between 22% and 24% (1) ▪ Full - year fiscal 2023 capital expenditures: $280 million $ 11.5 – $ 12.5 B NET SALES 14.2 % – 14.9 % GROSS PROFIT MARGIN $ 7.40 – $ 8.70 DILUTED EARNINGS PER SHARE (1) Before consideration of any discrete tax items 11

1Q 2023 KEY TAKEAWAYS THOR continues to deliver strong financial results while adjusting to dynamic market conditions Variable cost structure and experienced management teams to help maintain sustainable gross margin performance through market volatility Fast, flexible and focused business model to drive long - term sustainable growth Strong and resilient performance across the business cycle reinforces confidence in full - year fiscal 2023 outlook THOR Remains Well - Positioned to Outperform the Industry in Fiscal 2023 and Beyond 12

APPENDIX 13

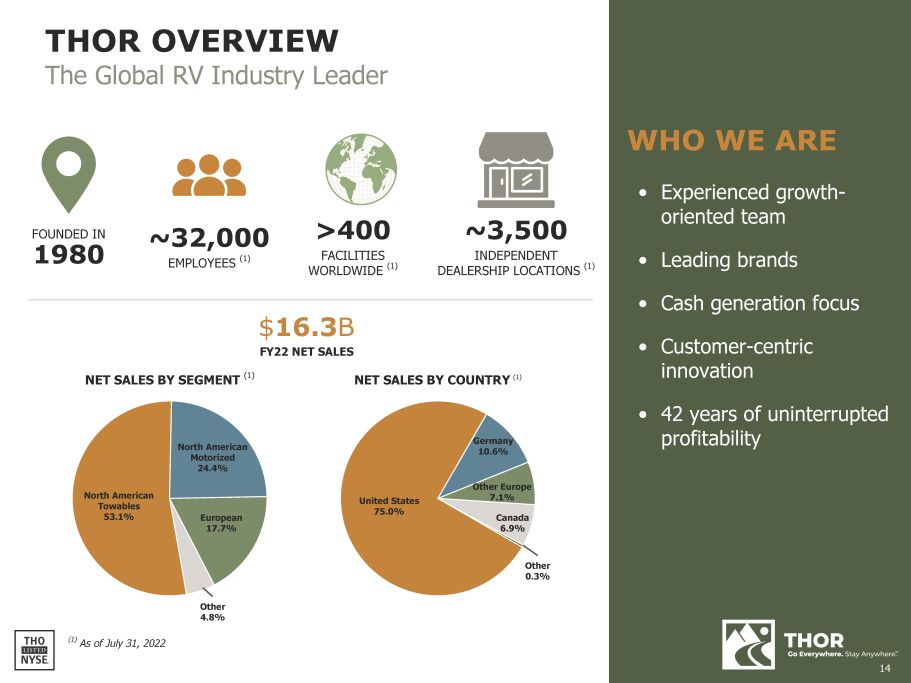

THOR OVERVIEW The Global RV Industry Leader WHO WE ARE • Experienced growth - oriented team • Leading brands • Cash generation focus • Customer - centric innovation • 42 years of uninterrupted profitability FOUNDED IN 1980 ~32,000 EMPLOYEES (1) >400 WORLDWIDE FACILITIES (1) ~3,500 INDEPENDENT DEALERSHIP LOCATIONS (1) NET SALES BY SEGMENT (1) NET SALES BY COUNTRY (1) $ 16.3 B FY22 NET SALES Other 4.8% (1) As of July 31, 2022 United States 75.0% Germany 10.6% Other Europe 7.1% Canada 6.9% Other 0.3% North American Towables 53.1% North American Motorized 24.4% European 17.7% 14

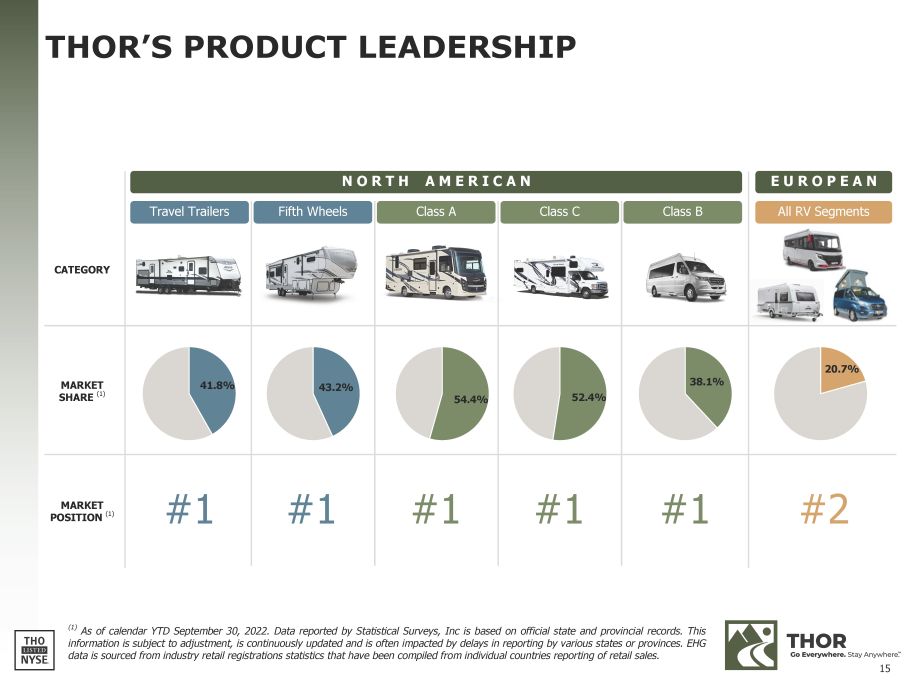

THOR’S PRODUCT LEADERSHIP ( 1 ) As of calendar YTD September 30 , 2022 . Data reported by Statistical Surveys, Inc is based on official state and provincial records . This information is subject to adjustment, is continuously updated and is often impacted by delays in reporting by various states or provinces . EHG data is sourced from industry retail registrations statistics that have been compiled from individual countries reporting of retail sales . CATEGORY N O R T H A M E R I C A N E U R O P E A N All RV Segments Travel Trailers Fifth Wheels Class A Class C Class B MARKET SHARE (1) 41.8% 43.2% 54.4% 52.4% 38.1% 20.7% MARKET POSITION (1) #1 #1 #1 #1 #1 #2 15

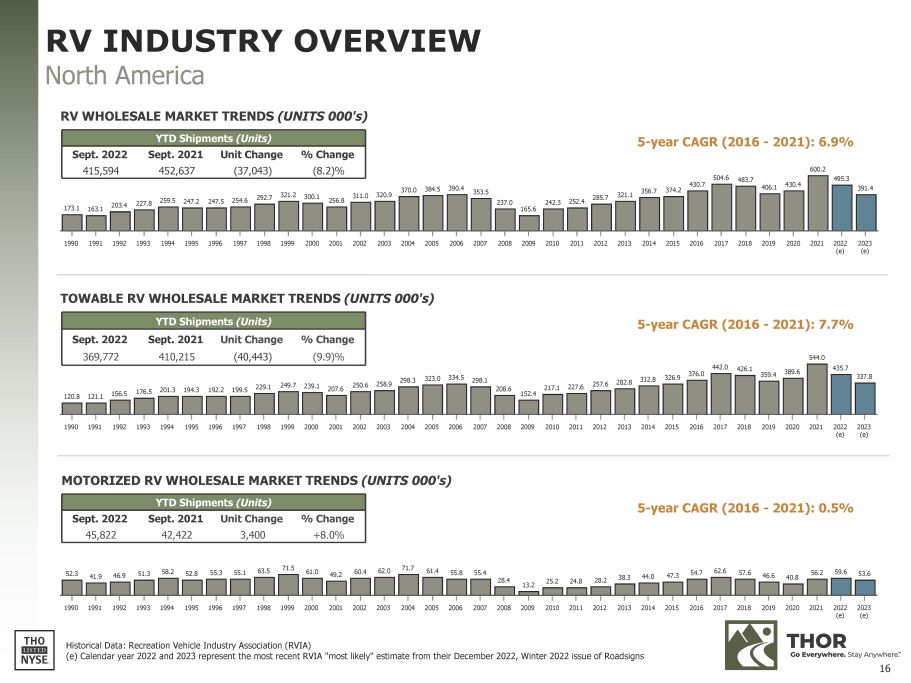

120.8 121.1 156.5 176.5 201.3 194.3 192.2 199.5 229.1 249.7 239.1 207.6 250.6 258.9 298.3 323.0 334.5 298.1 208.6 152.4 217.1 227.6 257.6 282.8 312.8 326.9 442.0 376.0 426.1 359.4 389.6 544.0 435.7 337.8 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 (e) (e) 173.1 163.1 203.4 227.8 259.5 247.2 247.5 254.6 292.7 321.2 300.1 256.8 311.0 320.9 370.0 384.5 390.4 353.5 237.0 165.6 242.3 252.4 285.7 321.1 356.7 430.7 374.2 504.6 483.7 406.1 430.4 600.2 495.3 391.4 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 (e) (e) TOWABLE RV WHOLESALE MARKET TRENDS (UNITS 000's) YTD Shipments (Units) Sept. 2022 415,594 Sept. 2021 452,637 Unit Change (37,043) % Change (8.2)% YTD Shipments (Units) Sept. 2022 Sept. 2021 Unit Change % Change 369,772 410,215 (40,443) (9.9)% 52.3 41.9 46.9 51.3 58.2 52.8 55.3 55.1 63.5 71.5 61.0 49.2 60.4 62.0 71.7 61.4 13.2 38.3 44.0 47.3 54.7 62.6 57.6 46.6 40.8 56.2 59.6 53.6 55.8 55.4 28.4 2006 2007 2008 25.2 24.8 28.2 2010 2011 2012 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2009 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 (e) (e) YTD Shipments (Units) Sept. 2022 Sept. 2021 Unit Change % Change 45,822 42,422 3,400 +8.0% Historical Data: Recreation Vehicle Industry Association (RVIA) 5 - year CAGR (2016 - 2021): 6.9% 5 - year CAGR (2016 - 2021): 7.7% 5 - year CAGR (2016 - 2021): 0.5% RV INDUSTRY OVERVIEW North America RV WHOLESALE MARKET TRENDS (UNITS 000's) MOTORIZED RV WHOLESALE MARKET TRENDS (UNITS 000's) (e) Calendar year 2022 and 2023 represent the most recent RVIA "most likely" estimate from their December 2022, Winter 2022 issue of Roadsigns 16

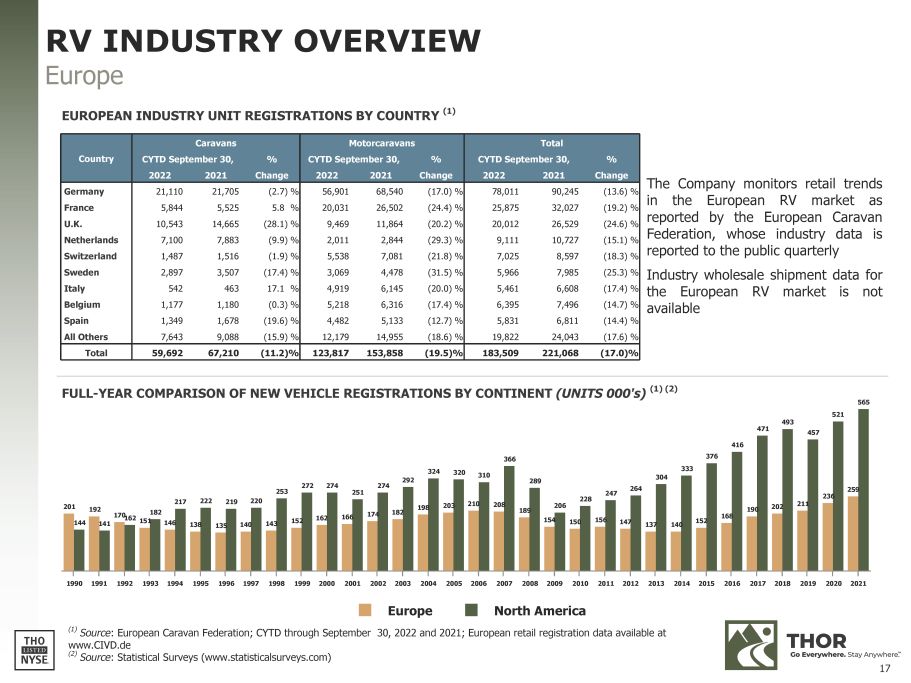

Country Caravans CYTD September 30, 2022 2021 % Change Motorcaravans CYTD September 30, 2022 2021 % Change Total CYTD September 30, 2022 2021 % Change Germany 21,110 21,705 (2.7) % 56,901 68,540 (17.0) % 78,011 90,245 (13.6) % France 5,844 5,525 5.8 % 20,031 26,502 (24.4) % 25,875 32,027 (19.2) % U.K. 10,543 14,665 (28.1) % 9,469 11,864 (20.2) % 20,012 26,529 (24.6) % Netherlands 7,100 7,883 (9.9) % 2,011 2,844 (29.3) % 9,111 10,727 (15.1) % Switzerland 1,487 1,516 (1.9) % 5,538 7,081 (21.8) % 7,025 8,597 (18.3) % Sweden 2,897 3,507 (17.4) % 3,069 4,478 (31.5) % 5,966 7,985 (25.3) % Italy 542 463 17.1 % 4,919 6,145 (20.0) % 5,461 6,608 (17.4) % Belgium 1,177 1,180 (0.3) % 5,218 6,316 (17.4) % 6,395 7,496 (14.7) % Spain 1,349 1,678 (19.6) % 4,482 5,133 (12.7) % 5,831 6,811 (14.4) % All Others 7,643 9,088 (15.9) % 12,179 14,955 (18.6) % 19,822 24,043 (17.6) % Total 59,692 67,210 (11.2)% 123,817 153,858 (19.5)% 183,509 221,068 (17.0)% The Company monitors retail trends in the European RV market as reported by the European Caravan Federation, whose industry data is reported to the public quarterly Industry wholesale shipment data for the European RV market is not available 201 192 146 138 135 140 143 152 162 166 174 182 198 203 210 208 189 154 150 156 147 137 140 152 168 190 202 211 236 259 144 141 170 162 151 182 217 222 219 220 253 272 274 251 274 292 324 320 310 366 289 206 228 247 264 304 333 376 416 471 493 457 565 521 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Europe North America (1) Source : European Caravan Federation; CYTD through September 30, 2022 and 2021; European retail registration data available at www.CIVD.de FULL - YEAR COMPARISON OF NEW VEHICLE REGISTRATIONS BY CONTINENT (UNITS 000's) (1) (2) RV INDUSTRY OVERVIEW Europe EUROPEAN INDUSTRY UNIT REGISTRATIONS BY COUNTRY (1) (2) Source : Statistical Surveys (www.statisticalsurveys.com) 17

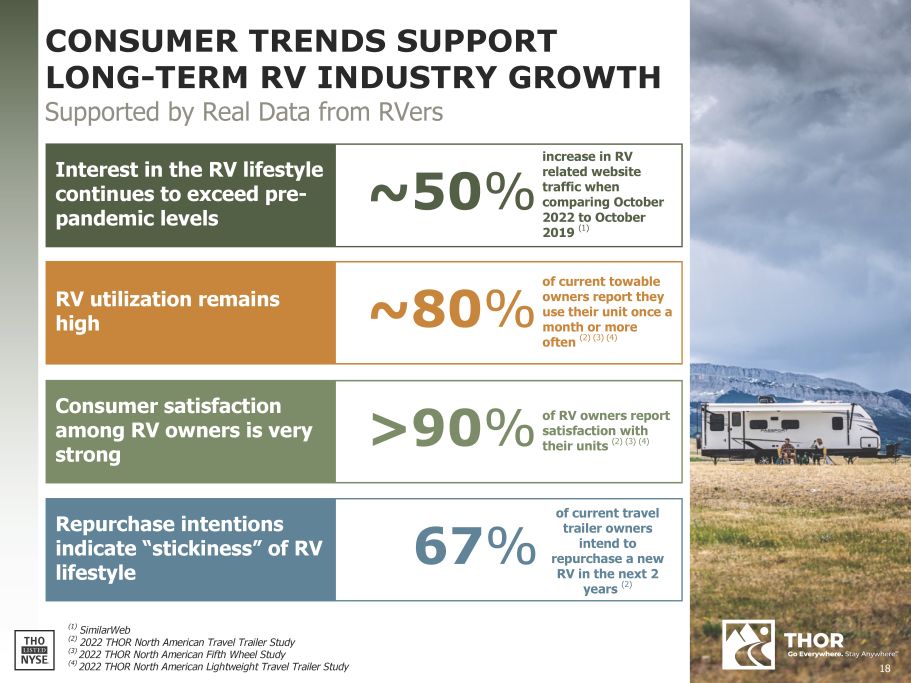

18 Repurchase intentions indicate “stickiness” of RV lifestyle Consumer satisfaction among RV owners is very strong RV utilization remains high Interest in the RV lifestyle continues to exceed pre - pandemic levels CONSUMER TRENDS SUPPORT LONG - TERM RV INDUSTRY GROWTH Supported by Real Data from RVers increase in RV ~50 % related website traffic when comparing October 2022 to October 2019 (1) >90 % (1) SimilarWeb (2) 2022 THOR North American Travel Trailer Study (3) 2022 THOR North American Fifth Wheel Study (4) 2022 THOR North American Lightweight Travel Trailer Study ~80 % of current towable owners report they use their unit once a month or more often (2) (3) (4) of RV owners report satisfaction with their units (2) (3) (4) of current travel 67 % trailer owners intend to repurchase a new RV in the next 2 years (2)

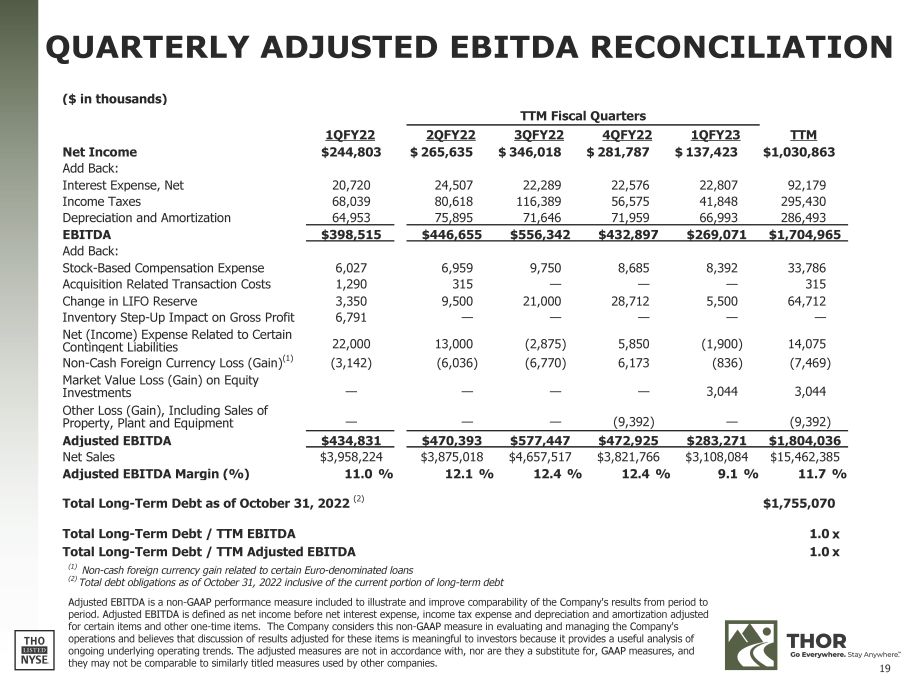

19 QUARTERLY ADJUSTED EBITDA RECONCILIATION ($ in thousands) TTM Fiscal Quarters Net Income 1QFY22 $244,803 2QFY22 $ 265,635 3QFY22 $ 346,018 4QFY22 $ 281,787 1QFY23 $ 137,423 TTM $1,030,863 Add Back: Interest Expense, Net 20,720 24,507 22,289 22,576 22,807 92,179 Income Taxes 68,039 80,618 116,389 56,575 41,848 295,430 Depreciation and Amortization 64,953 75,895 71,646 71,959 66,993 286,493 Contingent Liabilities EBITDA $398,515 $446,655 $556,342 $432,897 $269,071 $1,704,965 Add Back: Stock - Based Compensation Expense 6,027 6,959 9,750 8,685 8,392 33,786 Acquisition Related Transaction Costs 1,290 315 — — — 315 Change in LIFO Reserve 3,350 9,500 21,000 28,712 5,500 64,712 Inventory Step - Up Impact on Gross Profit 6,791 — — — — — Net (Income) Expense Related to Certain 22,000 13,000 (2,875) 5,850 (1,900) 14,075 Non - Cash Foreign Currency Loss (Gain) (1) (3,142) (6,036) (6,770) 6,173 (836) (7,469) Market Value Loss (Gain) on Equity Investments Other Loss (Gain), Including Sales of Property, Plant and Equipment — — — — 3,044 3,044 — — — (9,392) — (9,392) Adjusted EBITDA $434,831 $470,393 $577,447 $472,925 $283,271 $1,804,036 Net Sales $3,958,224 $3,875,018 $4,657,517 $3,821,766 $3,108,084 $15,462,385 Adjusted EBITDA Margin (%) 11.0 % 12.1 % 12.4 % 12.4 % 9.1 % 11.7 % Total Long - Term Debt as of October 31, 2022 (2) Total Long - Term Debt / TTM EBITDA Total Long - Term Debt / TTM Adjusted EBITDA (1) Non - cash foreign currency gain related to certain Euro - denominated loans (2) Total debt obligations as of October 31, 2022 inclusive of the current portion of long - term debt Adjusted EBITDA is a non - GAAP performance measure included to illustrate and improve comparability of the Company's results from period to period. Adjusted EBITDA is defined as net income before net interest expense, income tax expense and depreciation and amortization adjusted for certain items and other one - time items. The Company considers this non - GAAP measure in evaluating and managing the Company's operations and believes that discussion of results adjusted for these items is meaningful to investors because it provides a useful analysis of ongoing underlying operating trends. The adjusted measures are not in accordance with, nor are they a substitute for, GAAP measures, and they may not be comparable to similarly titled measures used by other companies. $1,755,070 1.0 x 1.0 x

www.thorindustries.com INVESTOR RELATIONS CONTACT Michael Cieslak, CFA mcieslak@thorindustries.com (574) 294 - 7724