united states

Securities and Exchange Commission

Washington, D. C. 20549

FORM

for the fiscal year ended

OR

for the transition period from …… to …….

Commission File Number

Cadiz Inc.

(Exact name of registrant specified in its charter)

| | |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | Identification No.) |

| | |

| | |

| (Address of principal executive offices) | (Zip Code) |

(

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| | | The |

| | | The |

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in rule 405 under the Securities Act of 1933. Yes ☐

Indicate by a check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act, (Check One).

☐ Large accelerated filer ☐ Accelerated filer ☑

If an emerging growth company, indicate by checkmark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yes

The aggregate market value of the common stock held by nonaffiliates as of June 30, 2023 was approximately $

As of March 26, 2024 the Registrant had

Documents Incorporated by Reference

Portions of the Registrant’s definitive Proxy Statement to be filed for its 2024 Annual Meeting of Stockholders are incorporated by reference into Part III of this Report. The Registrant is not incorporating by reference any other documents within this Annual Report on Form 10-K except those footnoted in Part IV under the heading “Item 15. Exhibits, Financial Statement Schedules”.

TABLE OF CONTENTS

| Part I |

||

| Item 1. |

1 |

|

| Item 1A. |

12 |

|

| Item 1B. |

16 |

|

| Item 1C. |

16 |

|

| Item 2. |

17 |

|

| Item 3. |

19 |

|

| Item 4. |

19 |

|

| Part II |

||

| Item 5. |

20 |

|

| Item 6. |

20 |

|

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

21 |

| Item 7A. |

29 |

|

| Item 8. |

30 |

|

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

30 |

| Item 9A. |

30 |

|

| Item 9B. |

31 |

|

| Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

31 |

| Part III |

||

| Item 10. |

32 |

|

| Item 11. |

32 |

|

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

32 |

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

32 |

| Item 14. |

32 |

|

| Part IV |

||

| Item 15. |

33 |

|

| Item 16. |

37 |

|

| 38 |

||

PART I

Cautionary Statement for Purposes of Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995

This Form 10-K contains forward-looking statements with regard to financial projections, proposed transactions such as those concerning the further development of our portfolio of assets, information or expectations about our business strategies, results of operations, products or markets, or otherwise makes statements about future events. Such forward-looking statements can be identified by the use of words such as “intends”, “anticipates”, “believes”, “estimates”, “projects”, “forecasts”, “expects”, “plans” and “proposes”. Although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, there are a number of risks and uncertainties that could cause actual results to differ materially from these forward-looking statements. These include, among others, the cautionary statements under the caption “Risk Factors”, as well as other cautionary language contained in this Form 10-K. These cautionary statements identify important factors that could cause actual results to differ materially from those described in the forward-looking statements. When considering forward-looking statements in this Form 10-K, you should keep in mind the cautionary statements described above.

ITEM 1. Description of Business

Business Overview

We are a water solutions provider with a unique combination of land, water, pipeline and water filtration technology assets located in Southern California between major water systems serving population centers in the Southwestern United States. Our portfolio of assets includes 2.5 million acre-feet of water supply (permits complete), 220 miles of existing, buried pipeline, 1 million acre-feet of groundwater storage capacity, and versatile, scalable and cost-effective water filtration technology. We will provide products and services to public water systems, government agencies and commercial clients.

We own approximately 46,000 acres of land with high-quality, naturally recharging groundwater resources in Southern California’s Mojave Desert (“Cadiz Property”). Our land holdings with vested water rights were assembled by our founders in the early 1980s, relying on NASA imagery that identified a desert aquifer system at the base of a vast Southern California watershed. The aquifer system underlying our property in the Cadiz Valley (“Cadiz Ranch”) presently holds 17 - 34 million acre-feet of groundwater in storage – comparable in size to the largest reservoir in the United States, Lake Mead.

In 2008, we entered into a 99-year lease with the Arizona & California Railroad Company (“ARZC”) that will allow us to co-locate and construct a 43-mile water conveyance pipeline (“Southern Pipeline”) within an existing, active railroad right-of-way (“ROW”) that extends from the Cadiz Ranch to the Colorado River Aqueduct (“CRA”), one of Southern California’s primary sources of water supply.

In 2021, we completed the acquisition of a 30” steel natural gas pipeline (“Northern Pipeline”) that extends 220-miles from the Cadiz Ranch across Kern and San Bernardino Counties terminating in California’s Central Valley. The pipeline, originally constructed to transport fossil fuels, is idle, and we are preparing to convert the pipeline to transport water. The route of the Northern Pipeline intersects several water conveyance facilities that serve Southern California, including the California Aqueduct, the Los Angeles Aqueduct, and the Mojave River Pipeline.

In 2022, we completed the acquisition of the assets of ATEC Systems, Inc., a producer of specialized filtration systems for removal of common groundwater contaminants that pose health risks in drinking water, including iron, manganese, arsenic, nitrates, Chromium 6 and other constituents of concern.

The Water Industry Value Chain

The water industry value chain today includes water supply, water storage, wastewater treatment, long-range conveyance, local distribution systems, and a wide range of products, technologies and services for monitoring, moving, trading, treating and integrating water resources across thousands of miles to address the challenges and demands of a diverse customer base. The water industry customer base includes regional wholesale water agencies responsible for acquiring, distributing and managing imported water resources; water and wastewater utilities that supply, treat and monitor clean water or transport, treat and analyze wastewater or storm water through an infrastructure network; government agencies responsible for public safety, environmental protection and economic security; and commercial and industrial customers requiring long-term, reliable supplies of clean, affordable water for their customers and businesses.

Climate change has disrupted hydrological cycles around the world. Extreme weather has created extreme unpredictability with regard to water supply for human consumption. Increasingly frequent and intense storms and swings between wet and dry years have created an urgent demand for technologies, services and infrastructure investment to capture, store and transport fresh water. Moreover, violent weather, extreme flooding and increasingly stringent regulatory restrictions on water quality have exceeded the capacity of existing water infrastructure and increased the cost of water over the last decade.

Water industry customers today require products, services, technology, and integrated solutions that address the challenges of scarcity of freshwater supplies, rising pollution, stricter regulations, infrastructure limitations and increasing operational costs.

Business Strategy

With the addition of pipeline infrastructure and water filtration technology to our portfolio of assets, our business now enables us to begin to offer integrated products and services to public water systems and other water industry customers in addition to products and services focused solely on water supply and water storage.

Description of Assets by Sector

Assets in our portfolio include Water Supply, Water Storage, Water Conveyance, Water Filtration Technology and Land. Each asset with an associated revenue model is described below.

Water Supply

In 2012, we received approvals from public agencies to implement the Cadiz Water Conservation & Storage Project (“Water Project”), a public-private partnership with California water agencies. The water supply element of our Water Project is expected to conserve 50,000 acre-feet per year at the Cadiz Property and make this new water supply available to underserved communities in Southern California. Because water in the aquifer system will continue to be lost to evaporation, surplus water that is captured and withdrawn before it evaporates is recognized as a new water supply (“conserved” water).

Under an extensive groundwater monitoring plan approved by local permitting authorities, Water Project operations and withdrawals of groundwater will be limited to sustainable amounts that preserve the health of the aquifer system and safeguard the desert ecosystem. An average of 50,000 acre-feet of water per year is expected to be captured and made available for beneficial use in Southern California communities over 50 years (2.5 million acre-feet in total), an amount of annual supply that could serve approximately 400,000 people each year.

In the first quarter of 2024, we entered into agreements with multiple public water systems to purchase 15,000 acre-feet per year (“AFY”) of annual water supply from us to be delivered via the Northern Pipeline. These agreements cumulatively represent 60% of the full capacity (25,000 AFY) of the Northern Pipeline.

The Water Project is structured as a public-private partnership in order for us and the participating public water agencies to cooperatively fund capital costs and operating and maintenance (“O&M”) costs required for us to deliver future contracted water supply to the agencies. In accordance with the structure of such agreements, it is anticipated that we will contribute an annual supply of 50,000 AFY of water from the Water Project into Fenner Gap Mutual Water Company ("FGMWC"), a mutual water company, to be owned jointly by the participating public water agencies. Through membership in the mutual water company, public water agencies will be able to purchase, for a 40-year term (take or pay), up to 50,000 AFY of water at our wellhead at an agreed upon market price estimated to start at approximately net $850/AFY to us and subject to annual inflation adjustment. Participating public water agencies will fund through FGMWC (a) capital costs for conversion of the Northern Pipeline from gas to water, construction of the Southern Pipeline, construction of pumping stations and appurtenant facilities, and (b) O&M costs.

Any contracts and off take facility construction will be subject to environmental review and a project level permitting process (see Item 1. “Description of Business - Permits”, below).

Water Storage

In addition to making available new water supply, the Water Project would also look to manage the groundwater basin to offer storage in our aquifer system for up to one-million acre-feet of fresh water that would be imported and held in storage until needed in future dry years. The total storage capacity of the aquifer system is larger than Southern California’s largest surface reservoir, Diamond Valley Lake, but unlike a surface reservoir would not suffer evaporative losses.

Water Conveyance

Water conveyance facilities are required to effectuate the sale of water supply and water storage. These water conveyance facilities must be the appropriate size and in the right locations to meet customer needs. We have invested in physical pipeline assets and the acquisition of rights-of-way to build water conveyance facilities that can transport our own water supplies and also be utilized by public water systems across California to trade and transport water supplies.

To deliver conserved water off-property or import water for storage at the Cadiz Ranch, we are currently developing two potential pipeline routes for the Water Project; the Southern Pipeline which would extend southwards from the Cadiz Property to the Colorado River Aqueduct in Rice, California and the Northern Pipeline which extends northwards from the Cadiz Property to Barstow, Antelope Valley, and Wheeler Ridge, California.

Cadiz’ Northern Pipeline is an existing 220-mile 30-inch steel pipeline that intersects several water storage and conveyance facilities in Southern California, including the California Aqueduct, the Los Angeles Aqueduct, and the Mojave River Pipeline. The capacity of the Northern Pipeline for water conveyance is 25,000 AFY. The capacity of the Southern Pipeline, which is expected to be constructed within the ARZC ROW, ranges from 75,000 AFY to 150,000 AFY depending on the pipeline diameter, ranging from 54” to 84”, that will be selected to accommodate imported water storage. When the Northern Pipeline becomes operational for water conveyance, and the Southern Pipeline is built, the Water Project would interconnect Southern California’s primary water delivery systems for the first time, enabling more flexible trading among participants on these systems. See also “Permits”, below, for details about the history and future requirements for local, state and federal permits for these pipelines.

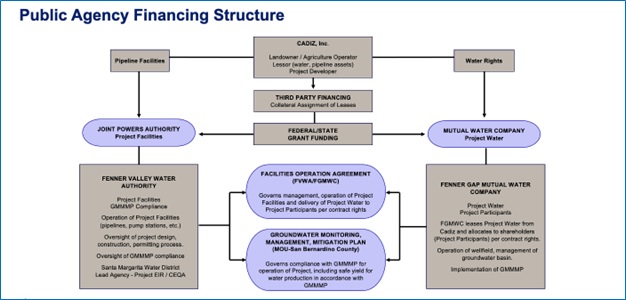

It is anticipated that conveyance facilities will be owned and operated by participating public agencies through Fenner Valley Water Authority, a Joint Powers Authority (“FVWA” or “JPA”) comprised of public water agencies participating in the Water Project that would operate the pipelines to deliver water to point of use. We will lease our pipeline facilities to the JPA for operation of the Water Project through a Facilities Operation Agreement. Participating public agencies may apply for grants and use municipal financing resources to fund the capital expenses for conversion of the pipeline and construction of pumping stations and distribution facilities. The amortized cost of capital for construction of conveyance facilities is expected to be paid for by participating agencies taking delivery of water via those facilities as described above. Lease payments to us for pipeline facilities will be included in the price for water supply. The chart below provides the anticipated structure of how the financing and operations of the Water Project would be handled between us and the participating public agencies through FGMWC and FVWA.

Water Filtration Technology

In the fourth quarter of 2022, we completed the acquisition of the assets of ATEC Systems, Inc. into ATEC Water Systems, LLC (“ATEC”), which provides innovative water filtration solutions for impaired or contaminated groundwater sources. Adding the ATEC filtration products to our business portfolio diversifies our range of innovative, sustainable clean water solutions offered in support of our mission to provide safe, affordable drinking water to underserved communities. ATEC, based in Hollister, California, has produced water filtration systems since 1982. It pioneered technology to provide cost-effective high-rate removal of iron and manganese and then expanded its reach to a full range of contaminants, including, arsenic, Chromium-6, nitrates, and other contaminants found in groundwater that limit the available supply of drinking water for many communities. We submitted a patent application for our treatment process of nitrate removal in 2023 and expect to file an application for another constituent during 2024.

We manufacture and sell an array of small, modular vertical steel tanks ranging from 14-inch to 48-inch diameter coupled with filter media to remove groundwater contaminants for our customers. ATEC’s modular, vertical tank systems can be scaled in size to serve small, rural communities as well as larger municipalities with system treatment capacities up to 60 million gallons per day (MGD) and require less maintenance and upkeep than traditional filtration systems. Our customers include municipalities, public and private utilities, and engineering and construction firms constructing new plants.

ATEC has built more than 450 water filtration systems for cities, water districts, investor-owned utilities and small communities and businesses in 10 U.S. states, as well as Canada and Sri Lanka. In March 2023, ATEC was awarded a $10 million contract to build filtration systems to remove iron and manganese from groundwater supply for the Central Utah Water Conservancy District’s Vineyard Wellfield Groundwater Polishing Project, a treatment facility that will deliver 60 MGD or approximately 54,000 acre-feet of groundwater per year to central Utah communities. The 320 48-inch filters to be delivered under this contract are expected to be completed in 2024.

In 2023, ATEC installed 10 small-scale filtration systems on community wells located on tribal lands in eastern Coachella Valley through a partnership with the Torres Martinez Desert Cahuilla Indian Tribe (“TMDCI”) and the Farmworker Institute of Education and Leadership Development (“FIELD”). The 14-inch ATEC systems installed on tribal lands are designed to remove arsenic from community wells used for drinking water.

Land

We have 46,000 acres of landholdings including:

| ● |

9,600 acres of land permitted for agriculture. |

| ● |

9,600 acres of land adjacent to the existing permit area that could be used for future agricultural development, but is not yet permitted. |

| ● |

26,800 acres of rangeland some of which is considered sensitive habitat for Desert Tortoise and other wildlife. |

We developed the land for our agricultural use and have farmed ourselves and extended leases to private farming operations since the 1980s. We maintain approximately 1,000 acres in current agriculture development of grain crops, primarily in alfalfa plantings, and have 2,100 acres leased for farming activities by Fenner Valley Farms LLC. Revenue from alfalfa totaled $0.8 million in 2023 and revenue from leased land totaled $0.4 million.

Permits

Water Supply and Storage Project

From 2010 – 2012, the Water Project completed a California Environmental Quality Act (“CEQA”) review process including the completion of a comprehensive Final Environmental Impact Report (“FEIR”). The FEIR concluded that Water Project operations, including the conservation of 2.5 million acre-feet of water from the aquifer system over a 50-year period (50,000 AFY for 50 years) would not cause any significant adverse environmental impacts. The FEIR was certified on July 31, 2012, by Santa Margarita Water District (“SMWD”), the lead participating water agency.

San Bernardino County, the local agency responsible for groundwater use at the Cadiz Property, approved the Groundwater Monitoring, Management and Mitigation Plan (‘GMMMP”) for the Water Project in 2012, and requires regular reporting of groundwater levels and conditions. The FEIR and GMMMP permits were challenged through litigation and were upheld and sustained in their entirety by judgements in California Superior Court in 2014 and the California Court of Appeal in 2016 and are no longer subject to legal challenge.

In August 2019, an Addendum to the FEIR was adopted by FVWA to address updates to the Water Project proposal, such as its water treatment program and pipeline route. The Addendum also assessed new studies published about natural springs in the Water Project watershed. The Addendum concluded that there are no significant adverse impacts associated with the minor changes to the Water Project and further summarized that the spring studies did not change the conclusions of the FEIR’s analysis. The Addendum was not challenged in court and the statute of limitations to challenge has expired.

Hydrological and geological study of the area has continued, and we regularly monitor and report groundwater conditions to the County of San Bernardino as part of our agricultural use. In 2023, the County of San Bernardino and SMWD, approved their oversight roles in an inter-agency Technical Review Panel (“TRP”) mandated by the GMMMP approvals to provide scientific and environmental monitoring of the Water Project. The GMMMP requires the TRP to be in place at least 12 months before the Water Project commences to establish baseline data on aquifer and watershed conditions for the monitoring program. In accordance with the GMMMP, the County and SMWD each appointed one member to the TRP, and the third member was selected by unanimous agreement of those representatives. The TRP started in 2022 and meets regularly to collect and assess pre-operational data and make recommendations for monitoring protocols to be implemented upon commencement of operations.

Northern Pipeline

The 220-mile Northern Pipeline is a former segment of a 1,200 mile, 30” steel pipeline constructed in 1985 by All American Pipeline Company to convey oil. In 2001, the pipeline was acquired by El Paso Natural Gas (“EPNG”) and authorized for natural gas conveyance. In 2011, we reserved the segment in an option agreement with EPNG and began to explore using the pipeline for water conveyance. In June 2021, we completed the acquisition of the pipeline for $19 million and own the entire 220-mile asset in fee. Changing the use of the Northern Pipeline to water conveyance is subject to applicable local, state and federal laws.

In December 2020, US Bureau of Land Management (“BLM”) granted to our subsidiary Cadiz Real Estate LLC two ROW permits to use the pipeline over federal lands. The first ROW was an assignment of a portion of an existing ROW held by EPNG and renewed by BLM under the Mineral Leasing Act (“MLA”) that enables the continued maintenance of the route and transportation of natural gas. The second ROW was issued under the Federal Land Policy and Management Act (“FLPMA”) and authorizes the conveyance of water in the pipeline over BLM-managed lands. In 2021, the two ROW grants were challenged in federal court by conservation organizations. In December 2021, the Biden Administration requested a voluntary remand of the permits to BLM, which was granted by the federal court in September 2022. In December 2022, we re-filed an application with the BLM for an assignment of the existing MLA ROW and worked cooperatively with BLM in preparing the new application. In December 2023, after a public review process, the BLM reissued the MLA ROW grant to us followed by an appeal period during which no appeals were filed.

The Northern Pipeline offers California water purveyors an opportunity to connect available supplies with rural areas of the State that are underserved. The Northern Pipeline crosses critically dry, rural and underserved regions of California and it could directly augment water supply access for 23 state-designated disadvantaged communities along its route. We presently hold agreements with parties interested in using the Northern Pipeline for conveyance, storage and supply to serve these disadvantaged communities. We expect to file an application with the BLM for a new FLPMA ROW in 2024 in coordination with public agency parties that will use the pipeline for water conveyance.

Southern Pipeline

In 2008, we entered into a 99-year lease agreement with the ARZC to utilize a portion of its existing ROW southwest from the Cadiz Property to the Colorado River Aqueduct for a conveyance pipeline and related facilities. As part of the lease arrangement, we agreed to provide necessary railroad improvements in furtherance of railroad purposes. This includes providing water and power to the railroad for fire protection and improving access roads and transloading operations, among other things. By co-locating the conveyance pipeline within this existing railroad ROW, Water Project construction would avoid impacts to desert habitats. The route and construction within the railroad ROW were evaluated and approved during the Water Project’s CEQA permitting process in 2012.

Our proposed co-location in the ROW was also separately assessed by the BLM to determine the need for any federal permitting related to the proposed use of the ARZC railroad ROW, which is a federal ROW originally granted to the railroad in accordance with the General Railroad Right-of-Way Act of 1875 (“1875 Act”). BLM’s evaluation, which was issued in February 2020, concluded that the proposed Southern Pipeline will further railroad purposes at least in part, is within the scope of the ROW, and requires no additional BLM approvals. In February 2022, the US Department of the Interior’s Solicitor Office issued a new legal opinion regarding third party use of 1875 Act ROWs that preserved the railroad purposes assessment for third party uses. The opinion was not specific to any railroad and did not alter our 2020 evaluation.

To deliver water from the Southern Pipeline to any point of use, the operating parties will require (i) an agreement with Metropolitan Water District of Southern California (“MWD”) to move water supplies from the Water Project in the CRA; and (ii) a finding by the California State Lands Commission (“SLC”) that conveying water from the Water Project in the CRA will not adversely affect the desert environment.

California Water Code Section 1815 requires desert groundwater projects to apply for a review by the SLC prior to moving water in facilities like the CRA. We expect an application to the SLC for review of the Water Project’s plans to convey water in the CRA from the Cadiz Property through the Southern Pipeline will be submitted by participating public agencies and accompanied by evidence of the Water Project’s extensive record of environmental sustainability as well as data and reports that we expect will withstand critical scrutiny.

Equity, Sustainability and Environmental Justice

Environmental Conservation

In 2014, we permanently dedicated approximately 7,400 acres of our Piute Valley properties to conservation. These properties, which are not associated with the Water Project or Cadiz Ranch agricultural operations, are located within terrain designated by the federal government as Critical Desert Tortoise Habitat and/or Desert Wilderness Areas. In February 2015, the California Department of Fish and Wildlife approved our establishment of the Fenner Valley Desert Tortoise Conservation Bank (“Fenner Bank”), a land conservation bank that makes available these properties for mitigation of impacts to tortoise and other sensitive species that would be caused by any development across the Southern California desert. Under its enabling documents, the Fenner Bank offers credits that can be acquired by entities that must mitigate or offset impacts linked to planned development. For example, this bank can service the mitigation requirements of renewable energy, military, residential and commercial development projects being considered throughout the Mojave Desert. Credits sold by the Fenner Bank are dedicated to funding the permanent preservation of the land by the San Diego Habitat Conservancy and research by San Diego Zoo Global into desert tortoise health and species protection.

In January 2023, we entered into an agreement with the TMDCI and the Farmworkers Institute of Education & Leadership Development (“FIELD”), to form a joint venture partnership to develop 11,000-acres of Cadiz-owned properties not in the Cadiz Valley (see Item 2. “Properties”, below), including the lands approved in the Fenner Bank. The joint venture envisions developing the property for conservation easements and sustainably managing the groundwater basins to make surplus groundwater available for beneficial uses, including farming, housing, and economic development in less fortunate communities. Subject to conditions precedent, including the construction of the Southern Pipeline, water and proceeds from the project will be shared equally among the parties.

The joint venture follows an agreement that we entered into with FIELD in September 2022 to create a state-of-the-art Innovation Campus at the Cadiz Ranch to offer work-based training, education and business opportunities for farmworkers. FIELD launched an English as a Second Language program at the Cadiz Ranch for ranch staff in Fall 2022, led by FIELD’s EPIC de Cesar Chavez High School Career Technical Education (CTE) program.

Social Impact

Our vision is a world where wealth and geography do not dictate access to clean, fresh, affordable water. It is available to all and delivered sustainably for generations to come.

| 1. |

Water for disadvantaged communities. We have committed to donate clean affordable water supply to disadvantaged communities. To date, we have committed more than 200,000 AF in water supply to serve disadvantaged communities in the Coachella Valley and California’s High Desert communities. Additionally, all public agency participants with agreements to contract for water from the Water Project must serve at least one disadvantaged community within their service area. |

| 2. |

Improve local water quality. The introduction of our low TDS groundwater to groundwater basins in the High Desert area of San Bernardino County or the CRA, which are known to be high in TDS, could provide water quality benefits that may reduce treatment costs for public water systems in Southern California. |

| 3. |

Repurposing carbon contributing assets. The use of the Northern Pipeline for water conveyance will convert a former oil and gas pipeline for the beneficial use of water conveyance. The recycling of an existing pipeline will reduce greenhouse gas emissions and reduce the energy load on the state’s current water transportation sources. |

| 5. |

Farmworker training. The Cadiz Ranch has a 35-year history of sustainable agriculture and best practices irrigation technologies. We offer farmworker training, partnerships with local high schools and colleges for irrigation and groundwater management training, and business and language education programs at no cost. |

| 6. |

Protection of habitats. All Water Project facilities will be built on private lands, disturbed public lands or within existing transportation corridors to avoid any impacts on habitats. We have dedicated portions of our Mojave Desert properties within protected areas and habitats to permanent conservation. |

| 7. |

Support stable water rates. The addition of new reliable supply, groundwater storage, improved water quality and system efficiency should support lower water rates in the service area of water agency participants. Reliability is associated with more stable rates and lower costs. |

| 8. |

Create and support good-paying jobs. The Water Project is expected to create and support nearly 6,000 jobs across the local economy during two phases of construction; 10% of jobs are reserved for veterans. We maintain a Project Labor Agreement with building trades and labor unions to employ their members during construction of Water Project facilities. |

Seasonality

Our water resource development and water filtration activities are not seasonal in nature.

Farming operations at the Cadiz Ranch include the year-round cultivation of grain crops, including alfalfa. These operations are subject to general seasonal trends that are characteristic of the agricultural industry.

Competition

We face competition in the acquisition, development and sale of water and land assets from a variety of parties. We also experience competition in the market for our water supply, storage and conveyance solutions and agriculture products associated with our water and land assets. Since California has scarce water resources and an increasing demand for available water, we believe that location, price and reliability of delivery are the principal competitive factors affecting agriculture and the demand for water supply, storage and conveyance in California. We believe our projects are competitive with other sources of water and farmland.

In the water filtration market, we compete with companies that offer products similar to ours. Some of these companies have greater financial resources, operational experience, and technical capabilities than we do. When bidding for water filtration projects, however, our current experience suggests that the market opportunity is very large, our products and services are highly competitively, and there is no clear dominant or preferred competitor in the markets in which we compete.

Human Capital Resources

As of December 31, 2023, we employed 18 full-time employees (i.e. those individuals working more than 1,000 hours per year) including 8 full-time employees at ATEC. Our business operations also rely on third-party contracted seasonal and temporary workers, as well as consultants and other professional vendors to help augment specialized human capital and talent needs. Our full-time and third-party contracted workers, as well as consultants and vendors, must follow our code of conduct and ethics policy, as well as our whistleblower and information security policies.

We appreciate the importance of retention, growth and development of our employees. The average tenure of our full-time employees is approximately 10 years, reflecting our positive work environment that offers opportunities to develop new skills and advance to new positions. We believe we offer competitive compensation (including salary, incentive bonus, and equity) and benefits packages to our employees, including a 401(k) plan. Further, we urge professional development opportunities and mentorship to cultivate talent throughout the Company.

As a small workforce, we focus on skill sharing and experience diversity in the workplace. Our full-time employees have regular opportunities to work with senior leadership and/or Board members in pursuit of business objectives. Management and Board leadership provide annual reviews of employee performance. Human capital is generally managed by our CEO and CFO, and employment policies are overseen by the Board, particularly the Compensation Committee. Our Board encourages diversity in the workforce. Approximately 65% of our senior executives are female.

We are focused on both executing a strategy to support progress and evaluating our diversity and inclusion strengths and opportunities to ensure our workforce reflects the communities in which we operate.

Regulation

Our operations are subject to various federal, state and local laws and regulations, as detailed throughout Item 1. In the normal course of developing our land, water and infrastructure assets, we are required to demonstrate to various regulatory authorities that we are in compliance with the laws, regulations and policies enforced by such authorities. Groundwater use and development, and the import and export of groundwater and surface supplies by public water agencies via conveyance pipelines, is subject to regulation by local, state and federal existing statutes pertaining to water supply and land use, but also general environmental statutes applicable to all forms of development. Agricultural operations are also generally subject to regulation by local agencies, such as county governments, as well as state environmental and water statutes. For example, we must obtain a variety of approvals and permits from state and federal governments with respect to assessment of environmental impact, particularly given the location of our assets in the California desert and in proximity to public lands. Because of the discretionary nature of these approvals, any concerns raised by governmental officials, public interest groups and/or other interested parties during both the development and/or approval process may impact our ability to develop our assets in the manner we believe would fulfill their highest and best use. The realization of income from our assets could be delayed, reduced or eliminated based on regulatory restrictions and/or processes.

Our water filtration products are manufactured to the specifications of our water provider customers in coordination with state and federal water quality and treatment regulatory approvals obtained by these providers in the ordinary course of permitting water treatment or groundwater well and pumping facilities. We are not directly impacted by these regulations.

Access to Our Information

Our annual, quarterly and current reports, proxy statements and other information are filed with the Securities and Exchange Commission (“SEC”) and are available free of charge on the internet through our website, http://www.cadizinc.com, as soon as reasonably practical after electronic filing of such material with the SEC. Our website address provided in this Annual Report on Form 10-K is not intended to function as a hyperlink and the information on our website is not, nor should it be considered, part of this report or incorporated by reference into this report.

Our SEC filings are also available to the public on the internet at the SEC’s website http://www.sec.gov.

Our business is subject to a number of risks, including those described below.

Our Development Activities Have Not Generated Significant Revenues

At present, our asset development activities include water resource (supply, storage and conveyance) and agricultural development at our San Bernardino County properties. We have not received significant revenues from these development activities to date and we cannot predict with certainty when, if ever, we will receive operating revenues from these business segments sufficient to offset the costs of our development activities. As a result, we continue to incur a net loss from operations.

We May Never Become Profitable Unless We Are Able to Successfully Implement Programs to Develop Our Land Assets and Related Water Resources and Water Filtration Technology Assets

Our agreements for water supply, storage, and conveyance projects are subject to financial and regulatory conditions, which may not be satisfied. Further, the circumstances under which water supply, storage, conveyance, water filtration or sustainable agriculture can be developed and the profitability of any such project are subject to significant uncertainties, including the risk of variable water supplies and changing water allocation priorities, our ability to fulfill the required contractual conditions of any water supply agreements, and our ability to complete the needed construction for water delivery to occur. Additional risks include our ability to obtain all necessary regulatory approvals and permits, litigation by community, environmental or other groups, unforeseen technical difficulties, general market conditions and competition for agriculture, water filtration products and water supplies, and the time needed to generate significant operating revenues from such programs after contracts are secured, crops are planted or operations commence.

The Development of Our Properties Is Heavily Regulated, Requires Governmental Approvals and Permits That Could Be Denied, and May Have Competing Governmental Interests and Objectives

In developing our land assets and related water resources, we are subject to local, state, and federal statutes, ordinances, rules and regulations concerning zoning, resource protection, environmental impacts, infrastructure design, subdivision of land, construction and similar matters. Our development activities are subject to the risk of adverse interpretations of such U.S. federal, state and local laws, regulations and policies and/or the adoption of new and amended laws, regulations and policies that prohibits, restrict, modify or delay our development activities.

Further, our development activities require governmental approvals and permits. If such permits were to be denied or granted subject to unfavorable conditions or restrictions, our ability to successfully implement our development programs as planned would be adversely impacted and could delay returns on our investments in the development of our assets.

For example, while we presently hold agreements with multiple public water systems to purchase 15,000 AFY and are in discussions with additional public water agencies to enter agreements to fill the remaining capacity of our Northern Pipeline (25,000 AFY) and whereby participating agencies would finance, own and operate the Northern Pipeline and lease 25,000 AFY of annual supply from us, any contracts and off take facility construction will be subject to standard environmental review and a project level permitting process as conditions precedent. There is no assurance that we can meet the conditions precedent for any of these contracts and even if we do, there is no assurance that we can receive the needed permits in a timely manner.

We cannot predict the terms, if any, which may be imposed in order to proceed with our water and other development programs.

Current regulations that could impact our water resources development activities are generally related to water conveyance functions, particularly the conversion of existing pipelines and construction of new pipelines and related facilities necessary to move water to and from the Cadiz Property, or between points along these pipelines for the benefit of California water users. In this regard, we will need to obtain certain permits and approvals from public water agencies in California, the California State Lands Commission, and agencies of the federal government, such as the US Department of the Interior. Such regulatory requirements will be determined by any contractual obligation to transport water between parties via our pipeline infrastructure.

Generally, opposition from third parties expressed at any regulatory venue can cause delays and increase the costs of our development efforts or preclude such development entirely. While we have worked with representatives of various environmental and third-party stakeholders to address any concerns about our projects, certain groups may remain opposed to our development plans regardless of our engagement and pursue legal and other actions.

Governmental approvals and permits granted authorizing our development activities may be challenged in court and such litigation could adversely impact our timelines, development plans, and ultimately the return on our investments.

A Portion of Our Total Assets Consists of Goodwill and Intangibles, Which Are Subject to a Periodic Impairment Analysis, and a Significant Impairment Determination in Any Future Period Could Have an Adverse Effect on Our Statement of Operations Even Without a Significant Loss of Revenue or Increase in Cash Expenses Attributable to such Period

We have goodwill of approximately $5.7 million including $1.9 million associated with the acquisition of assets of ATEC Systems, Inc. into ATEC Water Systems, LLC. We will be required to continue to evaluate this goodwill and intangibles for impairment based on the fair value of the operating business units to which the goodwill and intangible assets relate, at least once a year. These estimated fair values could change if we are unable to achieve revenue or operating results at the levels that have been forecasted, the market valuation of that business unit decreases based on transactions involving similar companies, or if there is a permanent, negative change in the market demand for the services offered by the business unit. These changes could result in further impairment of the existing goodwill and intangible balances and that could require a material non-cash charge to our results of operations.

Our Failure to Make Timely Payments of Principal and Interest on Our Indebtedness or To Obtain Additional Financing Will Impact our Ability to Implement Our Asset Development Programs

As of December 31, 2023, we had total indebtedness outstanding to our lenders of approximately $38.5 million which is secured by our assets. On March 6, 2024, we entered into a Third Amendment to Credit Agreement which, among other things, provided for (a) a new tranche of senior secured convertible term loans in an aggregate principal amount of $20,000,000 with a maturity date of June 30, 2027; (b) extension of the maturity date for the existing convertible loans ( $16.0 million in principal) and existing non-convertible loans ($21.2 million in principal) to June 30, 2027; and (c) subordination of the existing convertible loans to the existing non-convertible loans and new convertible loans (see Note 15 to the Condensed Consolidated Financial Statements – “Subsequent Events”). Interest is payable quarterly in cash at a 7% annual rate on the $21.2 million of non-convertible loans with PIK interest accruing quarterly at a 7% annual rate on the $16 million of existing convertible loans and $20 million of new convertible loans. To the extent that we do not make principal and interest payments on the indebtedness when due, or if we otherwise fail to comply with the terms of agreements governing our indebtedness, we may default on our obligations.

We will continue to require additional working capital to meet our cash resource needs until such time as our asset development programs, including the Water Project, and water filtration technology business produce revenues sufficient to fund operations. If we cannot raise funds if and when needed, we might be forced to make substantial reductions in our operating expenses, which could adversely affect our ability to implement our current business plan and ultimately our viability as a company. We cannot assure you that our current lenders, or any other lenders, will give us additional credit should we seek it. If we are unable to obtain additional credit, we may engage in further debt or equity financings. Our ability to obtain financing will depend, among other things, on the status of our asset development programs and water filtration technology business and general conditions in the capital markets at the time financing is sought. Any further equity or convertible debt financings would result in the dilution of ownership interests of our current stockholders.

The Issuance of Equity Securities and Management Equity Incentive Plans Will Cause Dilution

We have and may continue to issue equity securities pursuant to "at the market" issuance sales agreements or direct placements. Further, our compensation programs for management and consultants emphasize long-term incentives, primarily through the issuance of equity securities and options to purchase equity securities. It is expected that plans involving the issuance of shares, options, or both will be submitted from time to time to our stockholders for approval. In the event that any such plans are approved and implemented, the issuance of shares and options under such plans may result in the dilution of the ownership interest of other stockholders and will, under currently applicable accounting rules, result in a charge to earnings based on the value of our common stock at the time of issue and the fair value of options at the time of their award. The expense would be recorded over the vesting period of each stock and option grant.

The Volatility of the Stock Price of our Equity Securities Could Adversely Affect Current and Future Stockholders

The market price of our common stock and depositary shares is volatile and fluctuates in response to various factors which are beyond our control. Such fluctuations are particularly common in companies such as ours, which have not generated significant revenues. The following factors, in addition to other risk factors described in this section, could cause the market price of our common stock to fluctuate substantially:

| ● |

developments involving the execution of our business plan; |

| ● |

disclosure of any adverse results in litigation; |

| ● |

regulatory developments affecting our ability to develop our properties; |

| ● |

the dilutive effect or perceived dilutive effect of additional debt or equity financings; |

| ● |

perceptions in the marketplace of our company and the industry in which we operate; and |

| ● |

general economic, political and market conditions. |

In addition, the stock markets, from time to time, experience extreme price and volume fluctuations that may be unrelated or disproportionate to the operating performance of companies. These broad fluctuations may adversely affect the market price of our common stock. Price volatility could be worse if the trading volume of our common stock is low.

Information Technology Failures and Data Security Breaches Could Harm Our Business

We use information technology and other computer resources to carry out important operational and marketing activities and to maintain our business records. These information technology systems are dependent upon global communications providers, web browsers, telephone systems and other aspects of the Internet infrastructure that have experienced security breaches, cyber-attacks, significant systems failures and electrical outages in the past. A material network breach in the security of our information technology systems could include the theft of customer, employee or Company data. The release of confidential information as a result of a security breach may also lead to litigation or other proceedings against us by affected individuals or business partners, or by regulators, and the outcome of such proceedings, which could include penalties or fines, could have a significant negative impact on our business. We may also be required to incur significant costs to protect against damages caused by these information technology failures or security breaches in the future. However, we cannot provide assurance that a security breach, cyber-attack, data theft or other significant systems failure will not occur in the future, and such occurrences could have a material and adverse effect on our consolidated results of operations or financial position.

Increased Cybersecurity Requirements, Vulnerabilities, Threats and More Sophisticated and Targeted Computer Crime Could Pose a Risk to Our Systems, Networks, Products, Solutions, Services and Data

Increased global cybersecurity vulnerabilities, threats and more sophisticated and targeted cyber-related attacks pose a risk to our security and our customers', partners', suppliers' and third-party service providers' products, systems and networks and the confidentiality, availability and integrity of the data. We remain potentially vulnerable to additional known or unknown threats despite our attempts to mitigate these risks. We also may have access to sensitive, confidential or personal data or information that is subject to privacy and security laws, regulations or customer-imposed controls. Our efforts to protect sensitive, confidential or personal data or information, may nonetheless leave us vulnerable to material security breaches, theft, misplaced or lost data, programming errors, employee errors and/or malfeasance that could potentially lead to the compromising of sensitive, confidential or personal data or information, improper use of our systems, software solutions or networks, unauthorized access, use, disclosure, modification or destruction of information, production downtimes and operational disruptions. In addition, a cyber-related attack could result in other negative consequences, including damage to our reputation or competitiveness, remediation or increased protection costs, litigation or regulatory action. Additionally, violations of privacy or cybersecurity laws (including the California Consumer Privacy Act), regulations or standards increasingly lead to class-action and other types of litigation, which can result in substantial monetary judgments or settlements. Therefore, any such security breaches could have a material adverse effect on us.

ITEM 1B. Unresolved Staff Comments

Not applicable at this time.

Cybersecurity Risk Management and Strategy

We have developed and implemented a cybersecurity risk management program intended to protect the confidentiality, integrity and availability of our critical systems and information from cybersecurity threats.

Our cybersecurity risk management program includes:

| ● |

risk assessments designed to help identify material cybersecurity risks to our critical systems, information, products, services, and our broader enterprise IT environment; |

|

| ● |

offsite backup storage of critical systems and information; |

| ● |

the use of external service providers to assess, test or otherwise assist with aspects of our security controls; |

|

| ● |

cybersecurity awareness training; |

|

| ● |

a cybersecurity incident response plan that includes procedures for responding to cybersecurity incidents; and |

|

| ● |

a third-party risk management process to identify and mitigate risks from third parties, such as service providers, suppliers, and vendors. |

We have not identified any risks from known cybersecurity threats, including as a result of any prior cybersecurity incidents, that have materially affected or are reasonably likely to materially affect us, including our operations, business strategy, results of operations, or financial condition. For additional information regarding risks from cybersecurity threats, see Item 1A, “Risk Factors”, above.

Cybersecurity Governance

Our Board considers cybersecurity risk as part of its risk oversight function and has delegated to the Audit & Risk Committee (the “Committee”) oversight of cybersecurity and other information technology risks. The Committee oversees management’s implementation of our cybersecurity risk management program as part of our overall enterprise risk management program.

The Committee receives periodic reports from management on our cybersecurity risks. In addition, management promptly updates the Committee regarding any material cybersecurity incidents, and as necessary as to any incidents with lesser impact potential. The Committee reports to the full Board regarding its activities, including those related to cybersecurity.

Our management team, with the assistance of our external service providers, is responsible for assessing and managing our material risks from cybersecurity threats. The team has primary responsibility for our overall cybersecurity risk management program and supervises the cybersecurity activities of both our internal personnel and our retained external cybersecurity consultants.

Following is a description of our significant properties.

The Cadiz Valley Property

We own approximately 35,000 acres of largely contiguous desert land in the Cadiz and Fenner valleys of eastern San Bernardino County, California (the “Cadiz Property”). This area is located approximately 80 miles east of Barstow, California and 30 miles north of the Colorado River Aqueduct, and 110 miles north-east of Palm Springs. The Cadiz Property, which is at the base of a topographically diverse 1,300 square mile watershed, is the principal location of our business operations, including our agricultural operations and ongoing development of our water supply, storage and conveyance projects.

Independent geotechnical and engineering studies conducted since initial acquisition have confirmed that the Cadiz Property overlies a significant aquifer system that can support agricultural development, the conservation of groundwater for off property water supply and the storage of imported water. Approximately 3,100 acres of the Cadiz Property is actively farmed by us or leased to third parties for farming activities and includes agriculture and water infrastructure including wells, wellfield manifold, pipelines, worker housing, and energy and transportation facilities (see Item 1. “Description of Business”, above).

Additional Eastern Mojave Properties

In addition to the Cadiz Property, we also own approximately 11,000 additional acres in the eastern Mojave Desert portion of San Bernardino County, California at two separate properties.

Piute: We own approximately 9,000 acres in the Piute Valley. This landholding is located 15 miles from the resort community of Laughlin, Nevada, and about 12 miles from the Colorado River town of Needles, California. Extensive hydrological studies, including the drilling and testing of a full-scale production well, have demonstrated that this landholding is underlain by high-quality groundwater and could be suitable for agricultural development or solar energy production. The Piute Valley properties include private inholdings in the Mojave Trails National Monument and are proximate to or border areas designated by the state and federal government as the Mojave National Preserve, Critical Desert Tortoise Habitat and/or Desert Wilderness Areas and are therefore ideally suited for preservation and conservation. Approximately 7,400 acres of our Piute Valley properties are reserved in our Fenner Valley Desert Tortoise Conservation Bank, which is the largest land bank in California dedicated to protecting the desert tortoise. The Bank offers credits that can be acquired by public and private entities required to mitigate or offset impacts to the desert tortoise linked to planned development. We are presently marketing these credits to a variety of planned developments in the region.

Danby: We own nearly 2,000 acres near Danby Dry Lake in Ward Valley, approximately 30 miles southeast of the Cadiz Property. Our Danby Dry Lake property is located approximately 10 miles north of the Colorado River Aqueduct. Initial hydrological studies indicate that it has excellent potential for a water supply project. Certain of the properties in this area may also be suitable for agricultural development, renewable energy and/or preservation and conservation lands. The Danby properties are currently managed for open space purposes.

Executive Offices

We lease approximately 3,800 square feet of office space in Los Angeles, California for our executive offices. This lease is month-to-month. Current base rent under the lease is approximately $8,600 per month.

Cadiz Real Estate

Title to all of our real estate assets is held by Cadiz Real Estate LLC (“Cadiz Real Estate”), a wholly owned subsidiary of Cadiz Inc. The Board of Managers of Cadiz Real Estate currently consists of two managers appointed by the Company’s Board of Directors. As the ownership of the real estate held by Cadiz Real Estate has no effect on our ultimate beneficial ownership of these assets, we refer throughout this Report to assets owned of record either by Cadiz Real Estate or by us as “our” properties.

Cadiz Real Estate is a co-obligor under our senior secured term loan, for which assets of Cadiz Real Estate have been pledged as security.

Debt Secured by Properties

Our assets have been pledged as collateral for $38.1 million of senior secured debt outstanding as of December 31, 2023.

From time to time we are involved in various lawsuits and legal proceedings that arise in the ordinary course of business. At this time, we are not aware of any pending or threatened litigation that we expect will have a material effect on our business, financial condition, liquidity, or operating results. Legal claims are inherently uncertain, however, and it is possible that our business, financial condition, liquidity and/or operating results could be adversely affected in the future by legal proceedings.

ITEM 4. Mine Safety Disclosures

Not Applicable.

PART II

ITEM 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchase of Equity Securities

Our common stock is currently traded on The NASDAQ Global Market (“NASDAQ”) under the symbol “CDZI.”

As of March 26, 2024, the number of stockholders of record of our common stock was 56.

To date, we have not paid a cash dividend on our common stock and do not anticipate paying any cash dividends on our common stock in the foreseeable future.

Holders of Series A Preferred Stock, when and as authorized by the Company’s Board of Directors, are entitled to cumulative cash dividends at the rate of 8.875% of the $25,000.00 ($25.00 per Depositary Share) liquidation preference per year (equivalent to $2,218.75 per share per year or $2.21875 per Depositary Share per year). Dividends are payable quarterly in arrears, on or about the 15th of January, April, July and October, and began on or about October 15, 2021.

All securities sold by us during the three years ended December 31, 2023, which were not registered under the Securities Act of 1933, as amended, have been previously reported in accordance with the requirements of Rule 12b-2 of the Securities Exchange Act of 1934, as amended.

ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

In connection with the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995, the following discussion contains trend analysis and other forward-looking statements. Forward-looking statements can be identified by the use of words such as “intends”, “anticipates”, “believes”, “estimates”, “projects”, “forecasts”, “expects”, “plans” and “proposes”. Although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, there are a number of risks and uncertainties that could cause actual results to differ materially from these forward-looking statements. These include, among others, our ability to maximize value from our portfolio of assets and our ability to obtain new financings as needed to meet our ongoing working capital needs. See additional discussion under the heading “Risk Factors” above. Our forward-looking statements are made only as of the date hereof. We assume no duty to update these forward-looking statements to reflect new, changed or unanticipated events or circumstances, other than as may be required by law.

We are a water solutions provider with a unique combination of land, water, pipeline and water filtration technology assets located in Southern California between water systems serving population centers in the Southwestern United States. Our portfolio of assets includes 2.5 million acre-feet of water supply (permits complete), 220 miles of existing, buried pipeline, 1 million acre-feet of groundwater storage capacity, versatile, scalable and cost-effective water filtration technology.

We manage our landholdings, pipeline and water filtration technology assets to offer a suite of integrated products and services to public water systems, government agencies and commercial customers that include reliable water supply, groundwater storage, water conveyance and custom-designed water filtration technology systems.

Water Supply – We own vested water rights to withdraw 2.5 million acre-feet of groundwater for beneficial uses, including agricultural development on our property and export to serve communities across Southern California. Because all water in the aquifer system will eventually be lost to evaporation, surplus water that is captured and withdrawn before it evaporates is a new water supply (“conserved” water). We have completed environmental review in accordance with local, state and federal laws authorizing the management of the groundwater aquifer underlying the Cadiz Ranch which is expected to produce an average of 50,000 acre-feet of water per year for 50 years for beneficial use in Southern California communities.

Water Storage – The alluvium aquifer that lies beneath the Cadiz Property is also large enough for use as a water “banking” facility, capable of storing water “in-lieu” for supply customers and up to 1 million acre-feet of imported surplus water for return during drought periods. For comparison, MWD stores approximately 1.2 million acre-feet of water in the largest surface reservoir in the United States, Lake Mead.

Water Conveyance Infrastructure – We own the Northern Pipeline, an existing 220-mile 30-inch steel pipeline, that intersects several water storage and conveyance facilities in Southern California, including the California Aqueduct, the Los Angeles Aqueduct, and the Mojave River Pipeline. We also own a 99-year lease with the ARZC that will allow us to construct the Southern Pipeline within the existing, active railroad ROW that extends from the Cadiz Ranch to the Colorado River Aqueduct. The capacity of the Northern Pipeline for water conveyance is 25,000 AFY. The capacity of the Southern Pipeline, ranges from 75,000 AFY to 150,000 AFY depending on the pipeline diameter (54-inch to 84-inch) selected to accommodate imported water storage.

Water Filtration Technology – In 2022, we completed the acquisition of ATEC, which provides innovative water filtration solutions for impaired or contaminated groundwater sources. ATEC’s specialized filtration media provide cost-effective, high-rate of removal for common groundwater impairments and contaminants that pose health risks in drinking water including iron, manganese, arsenic, Chromium-6, nitrates, and other constituents of concern.

Our addition of pipeline infrastructure and ATEC water filtration technology to our portfolio of land and water assets enabled us in 2023 to adjust our business model to begin offering integrated services and solutions to public water systems that address the urgent challenges of climate change and make significant progress in advancing contract negotiations for water supply with public water systems.

In the first quarter of 2024, we entered into agreements with multiple public water systems to purchase 15,000 AFY of annual water supply from us to be delivered via the Northern Pipeline. These agreements cumulatively represent 60% of the full capacity (25,000 AFY) of the Northern Pipeline.

Through membership in FGMWC, a mutual water company to be owned by the participating water agencies, these agreements provide for delivery of purchased annual water supply over a 40-year term (take or pay), at an agreed upon market price estimated to start at approximately $850/AFY and subject to annual adjustment. Participating public agencies are expected to fund capital costs for conversion of the Northern Pipeline from gas to water, construction of pumping stations and appurtenant facilities, and would be able to seek infrastructure funding and grants.

These agreements and off take facility construction will be subject to standard environmental review and a project-level permitting process.

ATEC and our agricultural operations provide our current principal source of revenue, although our working capital needs are not fully supported by these operations at this time. We believe that our water supply, storage, pipeline conveyance and treatment solutions will provide a significant source of future cash flow for the business and our stockholders. We presently rely upon debt and equity financing to support our working capital needs and development of our water solutions.

Our current and future operations also include activities that further our commitments to sustainable stewardship of our land, water, pipeline and water filtration technology assets, good governance and corporate social responsibility. We believe these commitments are important investments that will assist in maintenance of sustained stockholder value.

Results of Operations

Year Ended December 31, 2023 Compared to Year Ended December 31, 2022

We have not received significant revenues from our water supply, storage, or conveyance assets to date. Our revenues have been limited to rental income from our agricultural leases, sales from our alfalfa plantings beginning in 2022 and ATEC sales beginning in 2023. As a result, we have historically incurred a net loss from operations. We currently operate in two reportable segments. Our largest segment is Land and Water Resources, which comprises all activities regarding our properties in the eastern Mojave Desert pre-revenue development of the Water Project (supply, storage and conveyance), and agricultural operations. Our second operating segment is Water Filtration Technology comprised of ATEC which provides innovative water filtration technology solutions for impaired or contaminated groundwater sources. Reporting of these two segments began in 2023 as the revenue and operating results for the water filtration technology segment were not material to our consolidated operations prior to the year ended December 31, 2023. We incurred a net loss of $31.4 million for the year ended December 31, 2023, compared with a net loss of $24.8 million for the year ended December 31, 2022. The higher loss in 2023 was primarily due to a loss on extinguishment of debt in the amount of $5.3 million resulting from issuance of a conversion instrument, a repayment fee and elimination of debt discount associated with the paydown of $15 million of senior secured debt in February 2023.

Our primary expenses are our ongoing overhead costs associated with the development of our water supply, storage and conveyance assets (i.e., general and administrative expense), farming expenses at the Cadiz Ranch, manufacturing operations of ATEC and our interest expense. We will continue to incur non-cash expense in connection with our management and director equity incentive compensation plans.

Revenues. Revenue totaled $2.0 million during the year ended December 31, 2023, primarily related to ATEC sales totaling $0.8 million, sales from the harvest from our 760 acres of commercial alfalfa crop totaling $0.8 million and rental income from our agricultural leases totaling $0.4 million. Revenue totaled $1.5 million during the year ended December 31, 2022, primarily related to rental income from our agricultural leases and sales from the harvest from our then 610 acres of commercial alfalfa crop.

Cost of Sales. Cost of sales totaled $2.9 million during the year ended December 31, 2023, comprised of $2.2 million related to our alfalfa crop harvest and $0.7 million related to ATEC. The 2023 alfalfa crop harvest net operating loss of $1.4 million primarily relates to increased diesel costs for farming as well as suppressed market conditions for alfalfa on the West Coast. Cost of sales totaled $2.1 million during the year ended December 31, 2022. In June 2022, the Company converted 610 acres of agricultural development to alfalfa commercial production. The 2022 loss was primarily due to non-recurring start-up costs for the initial short year of commercial production.

General and Administrative Expenses. General and administrative expenses during the year ended December 31, 2023, exclusive of stock-based compensation costs, totaled $17.3 million compared with $13.5 million for the year ended December 31, 2022. The increase in 2023 was primarily a result of community partnership and communications investments, including $2.2 million in water quality and infrastructure costs in coordination with community partners that will improve access to clean water in disadvantaged communities in the Coachella Valley and $1.3 million in corporate communications modernization expenses to the Company’s online, print, digital and social materials. General and administrative expense for ATEC totaled $0.8 million for 2023.

Compensation costs from stock and option awards for the year ended December 31, 2023, totaled $1.5 million compared with $1.9 million for the year ended December 31, 2022. The higher 2022 expense was primarily due to stock-based non-cash bonus awards to employees.

Depreciation. Depreciation expense totaled $1.2 million during the year ended December 31, 2023, compared to $0.7 million during the year ended December 31, 2022. The higher 2023 depreciation expense is primarily due to construction in progress placed into service in 2023, which included land development and stand establishment related to the planting of 150 acres of alfalfa, as well as $0.2 million of depreciation for ATEC assets in 2023.

Interest Expense, Net. Interest expense totaled $4.9 million during the year ended December 31, 2023, compared to $8.3 million during the year ended December 31, 2022. The following table summarizes the components of net interest expense for the two periods (in thousands):

| Year Ended December 31, |

||||||||

| 2023 |

2022 |

|||||||

| Interest on outstanding debt |

$ | 5,161 | $ | 5,849 | ||||

| Amortization of debt discount |

414 | 2,414 | ||||||

| Interest Income |

(606 | ) | - | |||||

| Other Income |

(25 | ) | - | |||||

| $ | 4,944 | $ | 8,263 | |||||

Interest income primarily relates to interest on investments in short-term deposits.

Losses on Derivative Liabilities. Losses on derivative liabilities totaled $220 thousand during the year ended December 31, 2023 compared to $0 in the year ended December 31, 2022. The losses recorded in 2023 were a result of a remeasurement of a conversion option under our senior secured debt.

Loss on Early Extinguishment of Debt. Loss on early extinguishment of debt totaled $5.3 million during the year ended December 31, 2023 compared to $0 in the year ended December 31, 2022. The 2023 loss on early extinguishment of debt was a result of a conversion instrument, a repayment fee and elimination of debt discount associated with the paydown of $15 million of senior secured debt in February 2023.

Liquidity and Capital Resources

| (a) |

Current Financing Arrangements |

As we have not received significant revenues or gross profits from our water, agriculture or water filtration technology activities to date, we have been required to obtain financing to bridge the gap between the time water resource and other development expenses are incurred and the time that revenue will commence. Historically, we have addressed these needs primarily through secured debt financing arrangements and private equity placements.

Equity Offerings

In July 2021, we completed the sale of 2,300,000 depositary shares each representing 1/1000th of a share of Series A Preferred Stock (“Depositary Share Offering”) for net proceeds of approximately $54 million.

On March 23, 2022, we completed the sale and issuance of 6,857,140 shares of our common stock to certain institutional and individual investors in a registered direct offering. The shares of common stock were sold at a purchase price of $1.75 per share, for aggregate gross proceeds of $12 million and aggregate net proceeds of approximately $11.8 million. The proceeds were used for working capital needs and for general corporate purposes.

On November 14, 2022, we completed the sale and issuance of 5,000,000 shares of our common stock to certain institutional investors in a registered direct offering (“November 2022 Direct Offering”). The shares of common stock were sold at a purchase price of $2.00 per share, for aggregate gross proceeds of $10 million and aggregate net proceeds of approximately $9.9 million.