UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended December 31, 2023

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ________ to ________

Commission File Number: 1-11373

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |||||||||||||||||||

| , | , | |||||||||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||||||||

(614 ) 757-5000

(Registrant’s telephone number, including area code)

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☑ | Accelerated filer | ☐ | |||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||||||||

| Emerging growth company | |||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ

The number of the registrant’s common shares, without par value, outstanding as of January 26, 2024, was the following:243,233,153 .

Cardinal Health Q2 Fiscal 2024 Form 10-Q | ||

Table of Contents

| Page | |||||

About Cardinal Health

Cardinal Health, Inc., an Ohio corporation formed in 1979, is a global healthcare services and products company providing customized solutions for hospitals, healthcare systems, pharmacies, ambulatory surgery centers, clinical laboratories, physician offices and patients in the home. We provide pharmaceuticals and medical products and cost-effective solutions that enhance supply chain efficiency. We connect patients, providers, payers, pharmacists and manufacturers for integrated care coordination and better patient management. We manage our business and report our financial results in two segments: Pharmaceutical and Medical. As used in this report, “we,” “our,” “us,” and similar pronouns refer to Cardinal Health, Inc. and its majority-owned and consolidated subsidiaries, unless the context requires otherwise. Our fiscal year ends on June 30. References to fiscal 2024 and fiscal 2023 and to FY24 and FY23 are to the fiscal years ending or ended June 30, 2024 and June 30, 2023, respectively.

Forward-Looking Statements

This Quarterly Report on Form 10-Q for the quarter ended December 31, 2023 (this "Form 10-Q") (including information incorporated by reference) includes "forward-looking statements" addressing expectations, prospects, estimates and other matters that are dependent upon future events or developments. Many forward-looking statements appear in Management’s Discussion and Analysis of Financial Condition and Results of Operations ("MD&A"), but there are others in this Form 10-Q, which may be identified by words such as "expect," "anticipate," "intend," "plan," "believe," "will," "should," "could," "would," "project," "continue," "likely," and similar expressions, and include statements reflecting future results or guidance, statements of outlook and expense accruals. These matters are subject to risks and uncertainties that could cause actual results to differ materially from those made, projected or implied. The most significant of these risks and uncertainties are described in this Form 10-Q, including Exhibit 99.1, and in "Risk Factors" in our Annual Report on Form 10-K for the fiscal year ended June 30, 2023 (our “2023 Form 10-K”). Forward-looking statements in this Form 10-Q speak only as of the date of this document. Except to the extent required by applicable law, we undertake no obligation to update or revise any forward-looking statement.

Non-GAAP Financial Measures

In the "Overview of Consolidated Results" section of MD&A, we use financial measures that are derived from our consolidated financial data but are not presented in our condensed consolidated financial statements prepared in accordance with U.S. generally accepted accounting principles ("GAAP"). These measures are considered "non-GAAP financial measures" under the United States Securities and Exchange Commission ("SEC") rules. The reasons we use these non-GAAP financial measures and the reconciliations to their most directly comparable GAAP financial measures are included in the “Explanation and Reconciliation of Non-GAAP Financial Measures” section following MD&A in this Form 10-Q.

1 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Overview | |||||||

Management's Discussion and Analysis of Financial Condition and Results of Operations

The discussion and analysis presented below is concerned with material changes in financial condition and results of operations, including amounts and certainty of cash flows from operations and from outside sources, between the periods specified in our condensed consolidated balance sheets at December 31, 2023 and June 30, 2023, and in our condensed consolidated statements of earnings/(loss) for the three and six months ended December 31, 2023 and 2022. All comparisons presented are with respect to the prior-year period, unless stated otherwise. This discussion and analysis should be read in conjunction with the MD&A included in our 2023 Form 10-K.

2 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Overview | |||||||

Overview of Consolidated Results

Revenue

During the three and six months ended December 31, 2023, revenue increased 12 percent and 11 percent to $57.4 billion and $112.2 billion, respectively, primarily due to branded and specialty pharmaceutical sales growth from existing customers.

GAAP and Non-GAAP Operating Earnings/(Loss)

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||||||||||||||

| (in millions) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

| GAAP operating earnings/(loss) | $ | 482 | $ | (119) | N.M. | $ | 468 | $ | 18 | N.M. | |||||||||||||||||||||||||

Surgical gown recall income | (1) | — | (1) | — | |||||||||||||||||||||||||||||||

| State opioid assessment related to prior fiscal years | — | (6) | — | (6) | |||||||||||||||||||||||||||||||

| Shareholder cooperation agreement costs | — | 2 | — | 8 | |||||||||||||||||||||||||||||||

| Restructuring and employee severance | 28 | 17 | 53 | 46 | |||||||||||||||||||||||||||||||

| Amortization and other acquisition-related costs | 63 | 71 | 127 | 142 | |||||||||||||||||||||||||||||||

| Impairments and (gain)/loss on disposal of assets, net | 1 | 710 | 538 | 863 | |||||||||||||||||||||||||||||||

| Litigation (recoveries)/charges, net | (11) | (207) | (52) | (180) | |||||||||||||||||||||||||||||||

| Non-GAAP operating earnings | $ | 562 | $ | 467 | 20 | % | $ | 1,133 | $ | 891 | 27 | % | |||||||||||||||||||||||

The sum of the components and certain computations may reflect rounding adjustments.

We had GAAP operating earnings of $482 million during the three months ended December 31, 2023 and a GAAP operating loss of $119 million during the three months ended December 31, 2022, which reflects the $709 million pre-tax goodwill impairment charge related to the Medical segment recognized during the three months ended December 31, 2022.

We had GAAP operating earnings of $468 million and $18 million during the six months ended December 31, 2023 and 2022, respectively, which included $581 million and $863 million pre-tax goodwill impairment charges related to the Medical segment, respectively. See "Critical Accounting Policies and Sensitive Accounting Estimates" section of this MD&A and Note 4 of the "Notes to Condensed Consolidated Financial Statements" for additional detail related to goodwill impairment.

GAAP operating earnings during the three and six months ended December 31, 2022 were favorably impacted by litigation recoveries. See "Results of Operations" section of this MD&A and Note 6 of the "Notes to Condensed Consolidated Financial Statements" for additional detail related to litigation recoveries.

Non-GAAP operating earnings during the three and six months ended December 31, 2023 increased 20 percent and 27 percent, respectively, due to an increase in Pharmaceutical and Medical segment profit.

3 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Overview | |||||||

GAAP and Non-GAAP Diluted EPS

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||||||||||||||

| ($ per share) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

GAAP diluted EPS (1) | $ | 1.43 | $ | (0.50) | N.M. | $ | 1.44 | $ | (0.08) | N.M. | |||||||||||||||||||||||||

Surgical gown recall income | — | — | — | — | |||||||||||||||||||||||||||||||

| State opioid assessment related to prior fiscal years | — | (0.02) | — | (0.02) | |||||||||||||||||||||||||||||||

Shareholder cooperation agreement costs | — | 0.01 | — | 0.02 | |||||||||||||||||||||||||||||||

| Restructuring and employee severance | 0.09 | 0.05 | 0.16 | 0.13 | |||||||||||||||||||||||||||||||

| Amortization and other acquisition-related costs | 0.19 | 0.20 | 0.38 | 0.40 | |||||||||||||||||||||||||||||||

Impairments and (gain)/loss on disposal of assets, net (2) | 0.14 | 2.06 | 1.71 | 2.46 | |||||||||||||||||||||||||||||||

| Litigation (recoveries)/charges, net | (0.03) | (0.48) | (0.14) | (0.39) | |||||||||||||||||||||||||||||||

Non-GAAP diluted EPS (1) | $ | 1.82 | $ | 1.32 | 38 | % | $ | 3.55 | $ | 2.52 | 41 | % | |||||||||||||||||||||||

The sum of the components and certain computations may reflect rounding adjustments.

The reconciling items are presented within this table net of tax. See quantification of tax effect of each reconciling item in our GAAP to Non-GAAP Reconciliations in the "Explanation and Reconciliation of Non-GAAP Financial Measures."

(1)Diluted earnings/(loss) per share attributable to Cardinal Health, Inc. ("diluted EPS").

(2)For the six months ended December 31, 2023, impairments and (gain)/loss on disposal of assets, net includes a pre-tax goodwill impairment charge of $581 million related to the Medical segment. For fiscal 2024, the net tax benefit related to the impairment charge is $45 million and is included in the annual effective tax rate. As a result, the tax benefit for the six months ended December 31, 2023 increased approximately by an incremental $65 million and will increase the provision for income taxes for the remainder of fiscal 2024.

For the three and six months December 31, 2022, impairments and (gain)/loss on disposal of assets, net included cumulative pre-tax goodwill impairment charges of $709 million and $863 million, respectively, related to the Medical segment. For fiscal 2023, the net tax benefit related to these impairment charges was $68 million and was included in the annual effective tax rate. As a result, the amount of tax benefit increased approximately by an incremental $118 million and $140 million for the three and six months ended December 31, 2022, respectively, and increased the provision for income taxes for the remainder of fiscal 2023.

During the three and six months ended December 31, 2023, GAAP diluted EPS was favorably impacted by an increase in Pharmaceutical and Medical segment profit. GAAP diluted EPS was adversely impacted by the goodwill impairment charges related to the Medical segment, which had a $(1.91) per share after tax impact during the six months ended December 31, 2023, and $(2.05) and $(2.46) per share after tax impact during the three and six months ended December 31, 2022, respectively. See "Critical Accounting Policies and Sensitive Accounting Estimates" section of this MD&A, and Note 4 and Note 7 of the "Notes to Condensed Consolidated Financial Statements" for additional detail. GAAP EPS during the three and six months ended December 31, 2022 also includes the favorable impact of litigation recoveries as described further in the "Results of Operations" section of this MD&A and Note 6 of the "Notes to Condensed Consolidated Financial Statements."

During the three and six months ended December 31, 2023, non-GAAP diluted EPS increased 38 percent and 41 percent to $1.82 and $3.55 per share, respectively, due to higher non-GAAP operating earnings, a lower share count and interest expense.

Cash and Equivalents

Our cash and equivalents balance was $4.6 billion at December 31, 2023 compared to $4.0 billion at June 30, 2023. During the six months ended December 31, 2023, net cash provided by operating activities was $1.7 billion, which includes the impact of our annual payment of $378 million related to the agreement to settle the vast majority of the opioid lawsuits filed by states and local governmental entities (the "National Opioid Settlement Agreement"). In addition, during the six months ended December 31, 2023, we deployed $750 million for share repurchases, $255 million for cash dividends and $206 million for capital expenditures.

4 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Overview | |||||||

Significant Developments in Fiscal 2024 and Trends

Operating and Segment Reporting Structure Changes

In January 2024, we announced a change in our organizational structure and have re-aligned our reporting structure under two reportable segments, effective January 1, 2024: Pharmaceutical and Specialty Solutions segment and Global Medical Products and Distribution segment. All remaining operating segments that are not significant enough to require separate reportable segment disclosures are included in Other. Results in this Form 10-Q are reported under our prior organizational and reporting structure. The following indicates the changes from the second quarter of fiscal 2024 to the new reporting structure, which will be reported for the first time in the third quarter of fiscal 2024:

•Pharmaceutical and Specialty Solutions segment: This reportable segment will be comprised of all businesses formerly within our Pharmaceutical segment except Nuclear and Precision Health Solutions.

•Global Medical Products and Distribution segment: This reportable segment will be comprised of all businesses formerly within our Medical segment except at-Home Solutions and OptiFreight Logistics.

•Other: This will consist of the remaining operating segments, Nuclear and Precision Health Solutions, at-Home Solutions and OptiFreight Logistics.

Pharmaceutical Segment

Specialty Networks Acquisition

On January 31, 2024, we announced that we had entered into a definitive agreement to acquire Specialty Networks, a technology-enabled multi-specialty group purchasing and practice enhancement organization for a purchase price of $1.2 billion in cash, subject to certain adjustments. Specialty Networks creates clinical and economic value for independent specialty providers and partners across multiple specialty GPOs: UroGPO, Gastrologix and GastroGPO, and United Rheumatology. The acquisition will further expand our offering in key therapeutic areas by enhancing our downstream provider-focused analytics capabilities and service offerings and by accelerating our upstream data and research opportunities with biopharma manufacturers.

This transaction is subject to the satisfaction of customary closing conditions, including receipt of required regulatory approvals. We plan to fund the acquisition with available cash.

COVID-19 Vaccine Distribution

Pharmaceutical segment profit was favorably impacted during the three and six months ended December 31, 2023 on a year-over-year basis in part due to the company beginning to distribute the recently commercially available COVID-19 vaccines following U.S. Food and Drug Administration approval of updated vaccines in September 2023. The timing, magnitude and profit impact of vaccine distribution volume for the remainder of fiscal 2024 and beyond remains uncertain.

Generics Program

The performance of our Pharmaceutical segment generics program positively impacted the year-over-year comparison of Pharmaceutical segment profit during the three and six months ended December 31, 2023. The Pharmaceutical segment generics program includes, among other things, the impact of generic pharmaceutical product launches, customer volumes, pricing changes, the Red Oak Sourcing, LLC venture ("Red Oak Sourcing") with CVS Health Corporation ("CVS Health") and generic pharmaceutical contract manufacturing and sourcing costs.

The frequency, timing, magnitude and profit impact of generic pharmaceutical customer volumes, pricing changes, customer contract renewals, generic pharmaceutical manufacturer pricing changes and generic pharmaceutical contract manufacturing and sourcing costs all impact Pharmaceutical segment profit and are subject to risks and uncertainties. These risks and uncertainties may impact Pharmaceutical segment profit and consolidated operating earnings during the remainder of fiscal 2024.

Medical Segment

Inflationary Impacts

Beginning in fiscal 2022, Medical segment profit was negatively affected by incremental inflationary impacts, primarily related to transportation (including ocean and domestic freight), commodities and labor, and global supply chain constraints. Since that time, we have taken actions to partially mitigate these impacts, including implementing certain price increases and evolving our pricing and

5 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Overview | |||||||

commercial contracting processes to provide us with greater pricing flexibility. In addition, decreases in some product-related costs have been recognized as the higher-cost inventory moved through our supply chain and was replaced by lower-cost inventory. These net inflationary impacts negatively affected Medical segment profit during fiscal 2023. The net inflationary impacts were less significant during the three and six months ended December 31, 2023 and had a favorable impact on Medical segment profit on a year-over-year basis.

We expect these net inflationary impacts to continue to affect Medical segment profit during the remainder of fiscal 2024, but to a significantly lesser extent than in fiscal 2023 and prior periods, due to our mitigation actions, together with continued decreases in certain product-related costs. However, these inflationary costs are difficult to predict and may be greater than we expect or continue longer than our current expectations. Our actions to increase prices and evolve our contracting strategies are subject to contingencies and uncertainties and it is possible that our results of operations will be adversely impacted to a greater extent than we currently anticipate or that we may not be able to mitigate the negative impact to the extent or on the timeline we anticipate.

Volumes within Products and Distribution

Medical segment profit was adversely impacted during fiscal 2023 in part due to lower volumes within products and distribution, which includes our Cardinal Health branded medical products. We expect Cardinal Health branded medical products sales growth in fiscal 2024 and beyond. The timing, magnitude and profit impact of this anticipated sales growth is subject to risks and uncertainties, which may impact Medical segment profit.

Medical Segment Goodwill

The change in segment structure as discussed above will result in changes to the composition of our reporting units. Accordingly, we will be required to reallocate the goodwill in reporting units affected by the change using a relative fair value approach and assess goodwill for impairment both before and after the reallocation. While we have not identified any indicators of impairment during the three months ended December 31, 2023 within the current reporting units, we may recognize a goodwill impairment charge following the reallocation if the carrying value of a new reporting unit exceeds its estimated fair value.

During the three months ended September 30, 2023, we performed interim goodwill impairment testing for the Medical operating segment (excluding our Cardinal Health at-Home Solutions division) ("Medical Unit") due to an increase in the risk-free interest rate. This testing resulted in a pre-tax charge of $581 million which was included in impairments and (gain)/loss on disposal of assets, net in our condensed consolidated statements of earnings/(loss). See "Critical Accounting Policies and Sensitive Accounting Estimates" section of this MD&A and Note 4 of the "Notes to Condensed Consolidated Financial Statements" for additional detail. Adverse changes in key assumptions or a significant change in industry or economic trends during the remainder of fiscal 2024 and beyond could result in additional goodwill impairments.

Shareholder Cooperation Agreement

In September 2022, we entered into a Cooperation Agreement (the "Cooperation Agreement") with Elliott Associates, L.P. and Elliott International, L.P. (together, "Elliott") under which our Board of Directors (the "Board"), among other things, (1) appointed four new independent directors, including a representative from Elliott, and (2) formed an advisory Business Review Committee of the Board, which is tasked with undertaking a comprehensive review of our strategy, portfolio, capital-allocation framework and operations. In May 2023, we extended the term of the Cooperation Agreement until the later of July 15, 2024 or until Elliott's representative ceases to serve on, or resigns from, the Board. In connection with this extension, the Board has extended the term of the Business Review Committee until July 15, 2024.

The evaluation and implementation of any actions recommended by the Business Review Committee and the Board have impacted and may continue to impact our business, financial position and results of operations during the remainder of fiscal 2024 and beyond. We have incurred, and may incur additional legal, consulting and other expenses related to the Cooperation Agreement and the activities of the Business Review Committee.

6 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Results of Operations | |||||||

Results of Operations

Revenue

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||||||||||||||

| (in millions) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

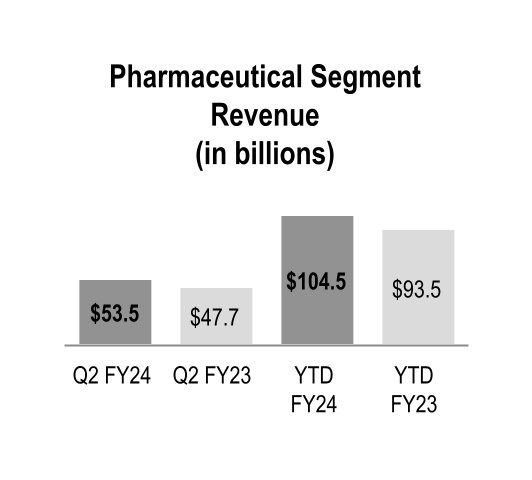

| Pharmaceutical | $ | 53,520 | $ | 47,673 | 12 | % | $ | 104,526 | $ | 93,501 | 12 | % | |||||||||||||||||||||||

| Medical | 3,928 | 3,797 | 3 | % | 7,688 | 7,575 | 1 | % | |||||||||||||||||||||||||||

| Total segment revenue | 57,448 | 51,470 | 12 | % | 112,214 | 101,076 | 11 | % | |||||||||||||||||||||||||||

| Corporate | (3) | (1) | N.M. | (6) | (4) | N.M. | |||||||||||||||||||||||||||||

| Total revenue | $ | 57,445 | $ | 51,469 | 12 | % | $ | 112,208 | $ | 101,072 | 11 | % | |||||||||||||||||||||||

Pharmaceutical Segment

Pharmaceutical segment revenue increased during the three and six months ended December 31, 2023 due to branded and specialty pharmaceutical sales growth, largely from existing customers, which increased revenue by $5.8 billion and $10.9 billion, respectively.

Medical Segment

Medical segment revenue increased during the three and six months ended December 31, 2023, primarily due to sales growth in at-Home Solutions and in products and distribution. The increase in products and distribution was primarily driven by higher Cardinal Health brand volumes and the effect of price increases to mitigate inflationary impacts partially offset by the adverse impact of personal protective equipment ("PPE") volumes and pricing.

Cost of Products Sold

Cost of products sold for the three and six months ended December 31, 2023 increased 12 percent to $55.6 billion and $108.6 billion, respectively, compared to the prior-year periods due to the factors affecting the changes in revenue and gross margin.

7 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Results of Operations | |||||||

Gross Margin

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||||||||||||||

| (in millions) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

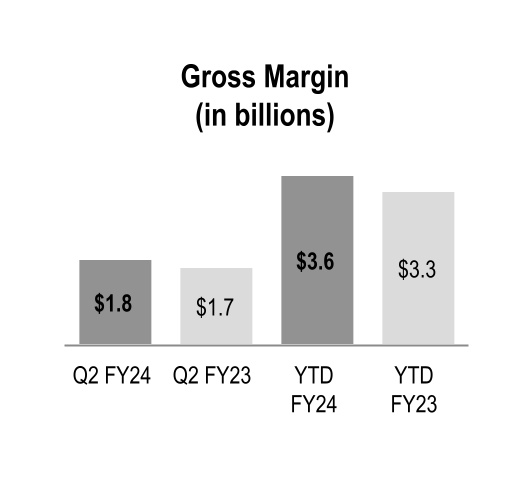

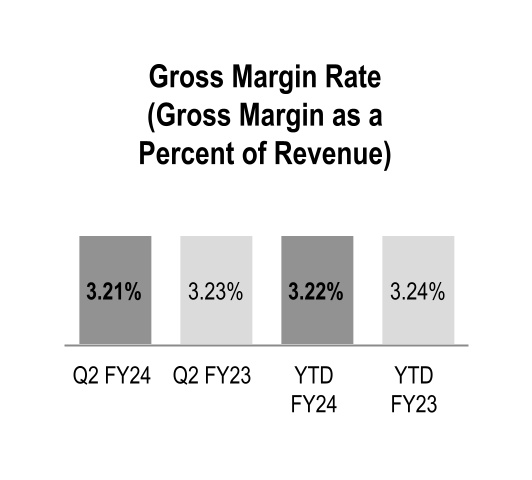

| Gross margin | $ | 1,846 | $ | 1,663 | 11 | % | $ | 3,614 | $ | 3,277 | 10 | % | |||||||||||||||||||||||

Gross margin increased during the three and six months ended December 31, 2023 primarily due to the beneficial comparison to the prior-year net inflationary impacts in the Medical segment, the performance of our generics program in the Pharmaceutical segment and increased contribution from branded pharmaceutical and specialty pharmaceutical products, which includes the favorable impact from COVID-19 vaccine distribution.

Gross margin rate declined 2 basis points during both the three and six months ended December 31, 2023, with the impact of unfavorable changes in overall product mix mostly offset by the beneficial comparison to the prior-year net inflationary impacts in the Medical segment and the performance of our generics program in the Pharmaceutical segment. The changes in overall product mix were primarily driven by increased pharmaceutical distribution branded sales, which have a dilutive impact on our overall gross margin rate.

Distribution, Selling, General and Administrative ("SG&A") Expenses

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||||||||||||||

| (in millions) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

| SG&A expenses | $ | 1,283 | $ | 1,191 | 8 | % | $ | 2,480 | $ | 2,388 | 4 | % | |||||||||||||||||||||||

During the three and six months ended December 31, 2023, SG&A expenses increased primarily due to higher costs to support sales growth, expenses related to investment projects and compensation-related costs.

8 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Results of Operations | |||||||

Segment Profit

We evaluate segment performance based on segment profit, among other measures. See Note 12 of the "Notes to Condensed Consolidated Financial Statements" for additional information on segment profit.

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||||||||||||||

| (in millions) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

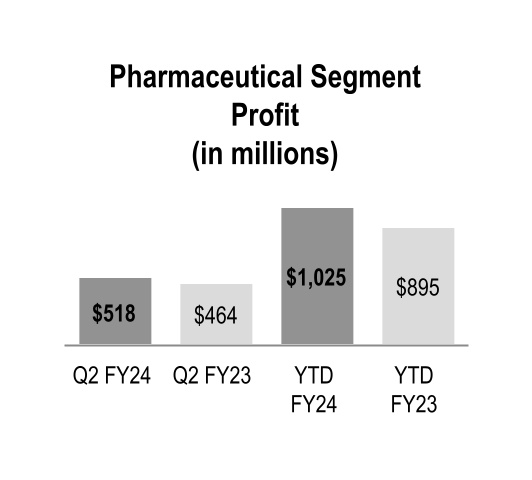

| Pharmaceutical | $ | 518 | $ | 464 | 12 | % | $ | 1,025 | $ | 895 | 15 | % | |||||||||||||||||||||||

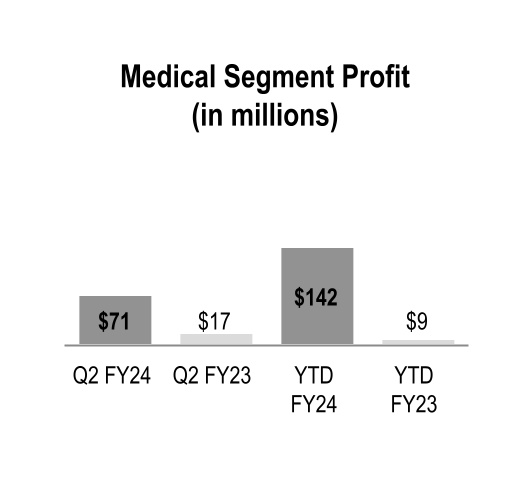

| Medical | 71 | 17 | N.M | 142 | 9 | N.M | |||||||||||||||||||||||||||||

| Total segment profit | 589 | 481 | 22 | % | 1,167 | 904 | 29 | % | |||||||||||||||||||||||||||

| Corporate | (107) | (600) | N.M. | (699) | (886) | N.M. | |||||||||||||||||||||||||||||

| Total consolidated operating earnings/(loss) | $ | 482 | $ | (119) | N.M. | $ | 468 | $ | 18 | N.M. | |||||||||||||||||||||||||

Pharmaceutical Segment Profit

Pharmaceutical segment profit increased during the three and six months ended December 31, 2023 primarily due to the performance of our generics program and increased contribution from branded pharmaceutical and specialty pharmaceutical products, which includes the favorable impact from COVID-19 vaccine distribution, partially offset by higher costs to support sales growth.

Medical Segment Profit

Medical segment profit increased during the three and six months ended December 31, 2023 due to the beneficial comparison to the prior-year net inflationary impacts, including the effects of mitigation actions.

Corporate

The changes in Corporate during the three and six months ended December 31, 2023 were due to the factors discussed in the "Other Components of Consolidated Operating Earnings/(Loss)" section that follows.

9 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Results of Operations | |||||||

Other Components of Consolidated Operating Earnings/(Loss)

In addition to revenue, gross margin and SG&A expenses discussed previously, consolidated operating earnings/(loss) were impacted by the following:

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||

| (in millions) | 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||

| Restructuring and employee severance | $ | 28 | $ | 17 | $ | 53 | $ | 46 | |||||||||||||||

| Amortization and other acquisition-related costs | 63 | 71 | 127 | 142 | |||||||||||||||||||

| Impairments and (gain)/loss on disposal of assets, net | 1 | 710 | 538 | 863 | |||||||||||||||||||

| Litigation (recoveries)/charges, net | (11) | (207) | (52) | (180) | |||||||||||||||||||

Restructuring and Employee Severance

Restructuring and employee severance costs during the three and six months ended December 31, 2023 were primarily related to certain projects resulting from reviews of our strategy, portfolio, capital-allocation framework and operations and the implementation of certain enterprise-wide cost-savings measures. During the three and six months ended December 31, 2022, costs were primarily related to the implementation of certain enterprise-wide cost-savings measures.

Amortization and Other Acquisition-Related Costs

Amortization of acquisition-related intangible assets was $63 million and $71 million for the three months ended December 31, 2023 and 2022, respectively, and $127 million and $142 million for the six months ended December 31, 2023 and 2022, respectively.

Impairments and (Gain)/Loss on Disposal of Assets, Net

We recognized $581 million of pre-tax non-cash goodwill impairment charges related to our Medical segment during the six months ended December 31, 2023, and $709 million and $863 million during the three and six months ended December 31, 2022, respectively, as discussed further in the "Critical Accounting Policies and Sensitive Accounting Estimates" section of this MD&A and Note 4 of the "Notes to Condensed Consolidated Financial Statements."

Litigation (Recoveries)/Charges, Net

We recognized income for net recoveries in class action antitrust lawsuits in which we were a class member or plaintiff of $31 million and $71 million during the three and six months ended December 31, 2023, respectively, and $66 million during the three and six months ended December 31, 2022.

During the three and six months ended December 31, 2023, we recognized a $22 million charge related to an agreement in principle with the Alabama Attorney General, under which we would pay approximately $123 million to the State of Alabama over a period of ten years to resolve opioid-related claims brought by the State and its political subdivisions. See Note 6 of the "Notes to Condensed Consolidated Financial Statements" for additional information.

We recognized income of $46 million and $25 million during the three and six months ended December 31, 2022, respectively, primarily related to a reduction of the reserve for the estimated settlement and defense costs for the Cordis OptEase and TrapEase inferior vena cava ("IVC") product liability due to the execution of certain settlement agreements.

During the three and six months ended December 31, 2022, we recognized income of $93 million due to net proceeds from the settlement of a shareholder derivative litigation matter.

Earnings/(Loss) Before Income Taxes

In addition to the items discussed above, earnings/(loss) before income taxes were impacted by the following:

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||||||||||||||

| (in millions) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

| Other (income)/expense, net | $ | (16) | $ | (7) | N.M. | $ | (18) | $ | (5) | N.M. | |||||||||||||||||||||||||

| Interest expense, net | 8 | 25 | (68) | % | 22 | 50 | (56) | % | |||||||||||||||||||||||||||

Interest Expense, Net

During the three and six months ended December 31, 2023, interest expense decreased by 68 percent and 56 percent, respectively, primarily due to increased interest income from cash and equivalents.

10 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Results of Operations | |||||||

Provision for Income Taxes

The effective tax rate was 27.7 percent and 5.4 percent during the three months ended December 31, 2023 and 2022, respectively, and 22.4 percent and 30.0 percent during the six months ended December 31, 2023 and 2022, respectively. These tax rates reflect the impact of the tax effects of goodwill impairment charges as well as certain other discrete items. See Note 7 of the "Notes to Condensed Consolidated Financial Statements" for additional information, during the three and six months ended December 31, 2023 and 2022.

Tax Effects of Goodwill Impairment Charges

During the six months ended December 31, 2023, we recognized cumulative pre-tax goodwill impairment charges of $581 million related to the Medical Unit. The net tax benefit related to these charges is $45 million for fiscal 2024.

Unless an item is considered discrete because it is unusual or infrequent, the tax impact of the item is included in our estimated annual effective tax rate. When items are recognized through our estimated annual effective tax rate, we apply our estimated annual effective tax rate to the earnings/(loss) before income taxes for the year-to-date period to compute our impact from income taxes for the current quarter and year-to-date period. The tax impacts of discrete items are recognized in their entirety in the period in which they occur.

The tax effect of the goodwill impairment charges recorded during the six months ended December 31, 2023 was included in our estimated annual effective tax rate because it was not considered unusual or infrequent, given that we recorded goodwill impairments in prior fiscal years. The impact of the non-deductible goodwill increased the estimated annual effective tax rate for fiscal 2024. Applying the higher tax rate to the pre-tax income for the six months ended December 31, 2023 resulted in recognizing an incremental interim tax benefit of approximately $65 million which impacted the provision for income taxes in the condensed consolidated statements of earnings/(loss) during the three months ended December 31, 2023 and prepaid expenses and other assets in the condensed consolidated balance sheet at December 31, 2023. The incremental interim tax benefit will reverse in the future quarters of fiscal 2024.

11 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Liquidity and Capital Resources | |||||||

Liquidity and Capital Resources

We currently believe that, based on available capital resources and projected operating cash flow, we have adequate capital resources to fund our operations and expected future cash needs as described below. If we decide to engage in one or more acquisitions in addition to the acquisition of Specialty Networks, depending on the size and timing of such transactions, we may need to access capital markets for additional financing.

Cash and Equivalents

Our cash and equivalents balance was $4.6 billion at December 31, 2023 compared to $4.0 billion at June 30, 2023.

During the six months ended December 31, 2023, net cash provided by operating activities was $1.7 billion, which includes the impact of our annual payment of $378 million related to the National Opioid Settlement Agreement. In addition, we deployed cash of $750 million for share repurchases, $255 million for cash dividends and $206 million for capital expenditures.

At December 31, 2023, our cash and equivalents were held in cash depository accounts with major banks or invested in high quality, short-term liquid investments.

Changes in working capital, which impact operating cash flow, can vary significantly depending on factors such as the timing of

customer payments, inventory purchases, payments to vendors and tax payments in the regular course of business, as well as fluctuating working capital needs driven by customer and product mix.

The cash and equivalents balance at December 31, 2023 includes $670 million of cash held by subsidiaries outside of the United States.

Other Financing Arrangements and Financial Instruments

Credit Facilities and Commercial Paper

In addition to cash and equivalents and operating cash flow, other sources of liquidity at December 31, 2023 include a $2.0 billion commercial paper program, backed by a $2.0 billion revolving credit facility. We also have a $1.0 billion committed receivables sales facility. At December 31, 2023, we had no amounts outstanding under our commercial paper program, revolving credit facility, or our committed receivables sales facility.

In February 2023, we extended our $2.0 billion revolving credit facility through February 25, 2028. In September 2022, we renewed our committed receivables sales facility program through Cardinal Health Funding, LLC ("CHF") through September 30, 2025. In September 2023, Cardinal Health 23 Funding, LLC was added as a seller under our committed receivables sales facility.

Our revolving credit and committed receivables sales facilities require us to maintain a consolidated net leverage ratio of no more than 3.75-to-1. As of December 31, 2023, we were in compliance with this financial covenant.

Long-Term Debt and Other Short-Term Borrowings

We had total long-term obligations, including the current portion and other short-term borrowings, of $4.7 billion at both December 31, 2023 and June 30, 2023.

12 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Liquidity and Capital Resources | |||||||

Capital Deployment

Opioid Litigation Settlement Agreement

We had $5.47 billion accrued at December 31, 2023 related to certain opioid litigation, as further described within Note 6 of the "Notes to Condensed Consolidated Financial Statements." We expect the majority of the remaining payment amounts to occur through 2038. During the six months ended December 31, 2023, we made our third annual payment of $378 million under the National Opioid Settlement Agreement. The amounts of these future payments may differ from the payments that we have already made.

In January 2024, we made payments of approximately $238 million to prepay at a pre-negotiated discount certain future payment amounts totaling approximately $344 million owed under each of the National Opioid Settlement Agreement, West Virginia Subdivisions Settlement Agreement and settlement agreements with Native American tribes and Cherokee Nation. The majority of the prepayment relates to the seventh annual payment as due under the National Opioid Settlement Agreement. As a result of these prepayments, we expect to recognize income of approximately $100 million in litigation charges/(recoveries), net in our condensed consolidated statements of earnings/(loss) during the three months ended March 31, 2024.

Capital Expenditures

Capital expenditures during the six months ended December 31, 2023 and 2022 were $206 million and $155 million, respectively.

Dividends

On each of May 11, 2023, August 9, 2023, and November 14, 2023, our Board of Directors approved a quarterly dividend of $0.5006 per share, or $2.00 per share on an annualized basis, which were paid on July 15, 2023, October 15, 2023, and January 15, 2024 to shareholders of record on July 3, 2023, October 3, 2023, and January 2, 2024, respectively.

Share Repurchases

During the six months ended December 31, 2023, we deployed $750 million for repurchases of our common shares, in the aggregate, under accelerated share repurchase ("ASR") programs. We funded the ASR programs with available cash. See Note 10 of the "Notes to Condensed Consolidated Financial Statements" for additional information.

As of December 31, 2023, we have $3.5 billion remaining under our existing share repurchase authorization.

Specialty Networks Acquisition

On January 31, 2024, we announced that we had entered into a definitive agreement to acquire Specialty Networks, a technology-enabled multi-specialty group purchasing and practice enhancement organization for a purchase price of $1.2 billion in cash, subject to certain adjustments. We plan to fund the acquisition with available cash.

13 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Other Items | |||||||

Other Items

The MD&A in our 2023 Form 10-K addresses our contractual obligations and cash requirements, as of and for the fiscal year ended June 30, 2023. Other than in connection with our proposed acquisition of Specialty Networks, there have been no subsequent material changes outside of the ordinary course of business to those items. See Note 14 of the "Notes to Condensed Consolidated Financial Statements" for additional information.

Critical Accounting Policies and Sensitive Accounting Estimates

The discussion and analysis presented below is a supplemental disclosure to the critical accounting policies and sensitive accounting estimates specified in our consolidated balance sheet at June 30, 2023. This discussion and analysis should be read in conjunction with the Critical Accounting Policies and Sensitive Accounting Estimates included in our 2023 Form 10-K and our Form 10-Q for the quarters ended September 30, 2023.

Critical accounting policies are those accounting policies that (i) can have a significant impact on our financial condition and results of operations and (ii) require the use of complex and subjective estimates based upon past experience and management’s judgment. Other people applying reasonable judgment to the same facts and circumstances could develop different estimates. Because estimates are inherently uncertain, actual results may differ, including due to the risks discussed in "Risk Factors" and other risks discussed in our 2023 Form 10-K and our other filings with the SEC since June 30, 2023.

Goodwill

Purchased goodwill is tested for impairment annually or when indicators of impairment exist. Goodwill impairment testing involves a comparison of the estimated fair value of reporting units to the respective carrying amount, which may be performed utilizing either a qualitative or quantitative assessment. Qualitative factors are first assessed to determine if it is more likely than not that the fair value of a reporting unit is less than its carrying amount. If it is determined that it is more likely than not that the fair value does not exceed the carrying amount, then a quantitative test is performed. The quantitative goodwill impairment test involves a comparison of the estimated fair value of the reporting unit to the respective carrying amount. A reporting unit is defined as an operating segment or one level below an operating segment (also known as a component).

Our reporting units are: Pharmaceutical operating segment (excluding our Nuclear and Precision Health Solutions division); Nuclear and Precision Health Solutions division; Medical operating segment (excluding our Cardinal Health at-Home Solutions division) (“Medical Unit”); and Cardinal Health at-Home Solutions division.

Goodwill impairment testing involves judgment, including the identification of reporting units, qualitative evaluation of events and circumstances to determine if it is more likely than not that an impairment exists, and, if necessary, the estimation of the fair value of the applicable reporting unit. Our qualitative evaluation considers the weight of evidence and significance of all identified events and circumstances and most relevant drivers of fair value, both positive and negative, in determining whether it is more likely than not that the fair value of a reporting unit is less than its carrying amount.

Changes to Reportable Segments for Fiscal 2024

As discussed in the Overview section of this MD&A, effective January 1, 2024, we implemented a new enterprise operating and segment reporting structure. The updated structure comprises two reportable segments: Pharmaceutical and Specialty Solutions segment and Global Medical Products and Distribution segment. All remaining operating segments that are not significant enough to require separate reportable segment disclosures are included in Other.

This change in segment structure will result in changes to the composition of our reporting units. Accordingly, we will be required to reallocate the goodwill in reporting units affected by the change using a relative fair value approach and assess goodwill for impairment both before, and after the reallocation. While we have not identified any indicators of impairment during the three months ended December 31, 2023 within the current reporting units, we may recognize a goodwill impairment charge following the reallocation if the carrying value of a new reporting unit exceeds its estimated fair value.

Medical Unit Goodwill

Potential changes in the reporting units within our Medical operating segment may result in a goodwill impairment charge. As of December 31, 2023, the total goodwill balance within the Medical Unit was $139 million. As discussed above, we have not identified any indicators of impairment during the three months ended December 31, 2023 within our reporting units, including the Medical Unit.

During the three months ended September 30, 2023, we elected to bypass the qualitative assessment and perform quantitative goodwill impairment testing for the Medical Unit due to an increase

14 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| MD&A | Other Items | |||||||

in the risk-free interest rate used in the discount rate. Our determination of the estimated fair value of the Medical Unit is based on a combination of the income-based approach (using a discount rate of 11 percent and a terminal growth rate of 2 percent), and market-based approaches. Additionally, we assigned a weighting of 80 percent to the discounted cash flow method, 10 percent to the guideline public company method, and 10 percent to the guideline transaction method. The carrying amount exceeded the fair value, which resulted in a pre-tax impairment charge of $581 million for the Medical Unit, which was recognized during the six months ended December 31, 2023 and is included in impairments and (gain)/loss on disposal of assets, net in our condensed consolidated statements of earnings/(loss). This impairment charge was driven by an increase of 1 percent in the discount rate primarily due to an increase in the risk-free interest rate. The discount rate used for the interim goodwill impairment testing at June 30, 2023 was 10 percent. See Note 4 of the "Notes to Condensed Consolidated Financial Statements" for further discussion.

While we consider the assumptions used in our determination of the estimated fair value of the Medical Unit to be reasonable and appropriate, they are complex and subjective, and additional adverse changes in one key assumption or a combination of key assumptions during fiscal 2024 may significantly affect future estimates. These assumptions include, among other things, a failure to meet expected earnings or other financial plans, including the execution of key initiatives related to optimizing and growing sales of Cardinal Health branded medical products, increasing growth in certain strategic divisions within our Medical segment, and driving simplification efforts and cost optimization projects, or unanticipated events and circumstances, such as changes in assumptions about the duration and magnitude of increased supply chain and commodities costs and our planned efforts to mitigate such impact, including price increases or surcharges; further disruptions in the supply chain; manufacturing cost inefficiencies resulting from lower than anticipated sales volume, an increase in the discount rate; a decrease in the terminal growth rate; increases in tax rates; or a significant change in industry or economic trends.

Adverse changes in key assumptions may result in a decline in fair value below the carrying value in the future and therefore, an impairment of our Medical Unit goodwill in future periods, which could adversely affect our results of operations. For example, if we were to increase the discount rate by a hypothetical 0.5 percent, the fair value for the Medical Unit would have further decreased by approximately $450 million. Additionally, a hypothetical 25 basis point decrease in long-term gross margin rates, which could be impacted by changes in Cardinal Health branded medical product sales growth rate assumptions, would have further decreased the fair value for the Medical Unit by approximately $300 million.

During the three months ended December 31, 2022 and September 30, 2022, we performed quantitative goodwill impairment testing for the Medical Unit. This quantitative testing

resulted in the carrying amount of the Medical Unit exceeding the fair value, resulting in pre-tax goodwill impairment charges of $709 million and $154 million recorded during the three months ended December 31, 2022 and September 30, 2022, respectively.

15 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| Explanation and Reconciliation of Non-GAAP Financial Measures | ||||||||

Explanation and Reconciliation of Non-GAAP Financial Measures

The "Overview of Consolidated Results" section within MD&A in this Form 10-Q contains financial measures that are not calculated in accordance with GAAP.

In addition to analyzing our business based on financial information prepared in accordance with GAAP, we use these non-GAAP financial measures internally to evaluate our performance, engage in financial and operational planning, and determine incentive compensation because we believe that these measures provide additional perspective on and, in some circumstances are more closely correlated to, the performance of our underlying, ongoing business. We provide these non-GAAP financial measures to investors as supplemental metrics to assist readers in assessing the effects of items and events on our financial and operating results on a year-over-year basis and in comparing our performance to that of our competitors. However, the non-GAAP financial measures that we use may be calculated differently from, and therefore may not be comparable to, similarly titled measures used by other companies. The non-GAAP financial measures disclosed by us should not be considered a substitute for, or superior to, financial measures calculated in accordance with GAAP, and the financial results calculated in accordance with GAAP and reconciliations to those financial statements set forth below should be carefully evaluated.

Exclusions from Non-GAAP Financial Measures

Management believes it is useful to exclude the following items from the non-GAAP measures presented in this report for its own and for investors’ assessment of the business for the reasons identified below:

•LIFO charges and credits are excluded because the factors that drive last-in first-out ("LIFO") inventory charges or credits, such as pharmaceutical manufacturer price appreciation or deflation and year-end inventory levels (which can be meaningfully influenced by customer buying behavior immediately preceding our fiscal year-end), are largely out of our control and cannot be accurately predicted. The exclusion of LIFO charges and credits from non-GAAP metrics facilitates comparison of our current financial results to our historical financial results and to our peer group companies’ financial results. We did not recognize any LIFO charges or credits during the periods presented.

•Surgical gown recall costs or income includes inventory write-offs and certain remediation and supply disruption costs, net of related insurance recoveries, arising from the January 2020 recall of select Association for the Advancement of Medical Instrumentation ("AAMI") Level 3 surgical gowns and voluntary field actions (a recall of some packs and a corrective action allowing overlabeling of other packs) for Presource Procedure Packs containing affected gowns. Income from surgical gown recall costs represents insurance recoveries of these certain costs. We have excluded these costs from our non-GAAP metrics to allow investors to better understand the underlying operating results of the business and to facilitate comparison of our current financial results to our historical financial results and to our peer group companies’ financial results.

•State opioid assessments related to prior fiscal years is the portion of state assessments for prescription opioid medications that were sold or distributed in periods prior to the period in which the expense is incurred. This portion is excluded from non-GAAP financial measures because it is retrospectively applied to sales in prior fiscal years and inclusion would obscure analysis of the current fiscal year results of our underlying, ongoing business. Additionally, while states' laws may require us to make payments on an ongoing basis, the portion of the assessment related to sales in prior periods are contemplated to be one-time, nonrecurring items. Income from state opioid assessments related to prior fiscal years represents reversals of accruals due to changes in estimates or when the underlying assessments were invalidated by a Court or reimbursed by manufacturers.

•Shareholder cooperation agreement costs includes costs such as legal, consulting and other expenses incurred in relation to the agreement (the "Cooperation Agreement") entered into among Elliott Associates, L.P., Elliott International, L.P. (together, "Elliott") and Cardinal Health, including costs incurred to negotiate and finalize the Cooperation Agreement and costs incurred by the Business Review Committee of the Board of Directors, which was formed under this Cooperation Agreement. We have excluded these costs from our non-GAAP metrics because they do not occur in or reflect the ordinary course of our ongoing business operations and may obscure analysis of trends and financial performance.

•Restructuring and employee severance costs are excluded because they are not part of the ongoing operations of our underlying business and include, but are not limited to, costs related to divestitures, closing and consolidating facilities, changing the way we manufacture or distribute our products, moving manufacturing of a product to another location, changes in production or business process outsourcing or insourcing, employee severance and realigning operations.

16 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| Explanation and Reconciliation of Non-GAAP Financial Measures | ||||||||

•Amortization and other acquisition-related costs, which include transaction costs, integration costs, and changes in the fair value of contingent consideration obligations, are excluded because they are not part of the ongoing operations of our underlying business and to facilitate comparison of our current financial results to our historical financial results and to our peer group companies' financial results. Additionally, costs for amortization of acquisition-related intangible assets are non-cash amounts, which are variable in amount and frequency and are significantly impacted by the timing and size of acquisitions, so their exclusion facilitates comparison of historical, current and forecasted financial results. We also exclude other acquisition-related costs, which are directly related to an acquisition but do not meet the criteria to be recognized on the acquired entity’s initial balance sheet as part of the purchase price allocation. These costs are also significantly impacted by the timing, complexity and size of acquisitions.

•Impairments and gain or loss on disposal of assets, net are excluded because they do not occur in or reflect the ordinary course of our ongoing business operations and are inherently unpredictable in timing and amount, and in the case of impairments, are non-cash amounts, so their exclusion facilitates comparison of historical, current and forecasted financial results.

•Litigation recoveries or charges, net are excluded because they often relate to events that may have occurred in prior or multiple periods, do not occur in or reflect the ordinary course of our business and are inherently unpredictable in timing and amount.

•Loss on early extinguishment of debt is excluded because it does not typically occur in the normal course of business and may obscure analysis of trends and financial performance. Additionally, the amount and frequency of this type of charge is not consistent and is significantly impacted by the timing and size of debt extinguishment transactions.

The tax effect for each of the items listed above is determined using the tax rate and other tax attributes applicable to the item and the jurisdiction(s) in which the item is recorded. The gross, tax and net impact of each item are presented with our GAAP to non-GAAP reconciliations.

Definitions

Growth rate calculation: growth rates in this report are determined by dividing the difference between current-period results and prior-period results by prior-period results.

Non-GAAP operating earnings: operating earnings/(loss) excluding (1) LIFO charges/(credits), (2) surgical gown recall costs/(income), (3) state opioid assessment related to prior fiscal years, (4) shareholder cooperation agreement costs, (5) restructuring and employee severance, (6) amortization and other acquisition-related costs, (7) impairments and (gain)/loss on disposal of assets, net and (8) litigation (recoveries)/charges, net.

Non-GAAP earnings before income taxes: earnings/(loss) before income taxes excluding (1) LIFO charges/(credits), (2) surgical gown recall costs/(income), (3) state opioid assessment related to prior fiscal years, (4) shareholder cooperation agreement costs, (5) restructuring and employee severance, (6) amortization and other acquisition-related costs, (7) impairments and (gain)/loss on disposal of assets, net and (8) litigation (recoveries)/charges, net and (9) loss on early extinguishment of debt.

Non-GAAP net earnings attributable to Cardinal Health, Inc.: net earnings/(loss) attributable to Cardinal Health, Inc. excluding (1) LIFO charges/(credits), (2) surgical gown recall costs/(income), (3) state opioid assessment related to prior fiscal years, (4) shareholder cooperation agreement costs, (5) restructuring and employee severance, (6) amortization and other acquisition-related costs, (7) impairments and (gain)/loss on disposal of assets, net and (8) litigation (recoveries)/charges, net and (9) loss on early extinguishment of debt.

Non-GAAP effective tax rate: provision for/(benefit from) income taxes adjusted for the tax impacts of (1) LIFO charges/(credits), (2) surgical gown recall costs/(income), (3) state opioid assessment related to prior fiscal years, (4) shareholder cooperation agreement costs, (5) restructuring and employee severance, (6) amortization and other acquisition-related costs, (7) impairments and (gain)/loss on disposal of assets, net and (8) litigation (recoveries)/charges, net and (9) loss on early extinguishment of debt divided by (earnings/(loss) before income taxes adjusted for the nine items above).

Non-GAAP diluted earnings per share attributable to Cardinal Health, Inc.: non-GAAP net earnings attributable to Cardinal Health, Inc. divided by diluted weighted-average shares outstanding.

17 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| Explanation and Reconciliation of Non-GAAP Financial Measures | ||||||||

GAAP to Non-GAAP Reconciliation

| (in millions, except per common share amounts) | Operating Earnings/(Loss) | Operating Earnings Growth Rate | Earnings/(Loss) Before Income Taxes | Provision for/(Benefit From) Income Taxes | Net Earnings/(Loss)1 | Net Earnings1 Growth Rate | Diluted EPS1,2 | Diluted EPS1 Growth Rate | ||||||||||||||||||

| Three Months Ended December 31, 2023 | ||||||||||||||||||||||||||

| GAAP | $ | 482 | N.M. | $ | 490 | $ | 136 | $ | 353 | N.M. | $ | 1.43 | N.M. | |||||||||||||

Surgical gown recall income | (1) | (1) | — | (1) | — | |||||||||||||||||||||

| Restructuring and employee severance | 28 | 28 | 7 | 21 | 0.09 | |||||||||||||||||||||

| Amortization and other acquisition-related costs | 63 | 63 | 17 | 46 | 0.19 | |||||||||||||||||||||

Impairments and (gain)/loss on disposal of assets, net | 1 | 1 | (33) | 34 | 0.14 | |||||||||||||||||||||

| Litigation (recoveries)/charges, net | (11) | (11) | (5) | (6) | (0.03) | |||||||||||||||||||||

| Non-GAAP | $ | 562 | 20 | % | $ | 569 | $ | 121 | $ | 447 | 29 | % | $ | 1.82 | 38 | % | ||||||||||

| Three Months Ended December 31, 2022 | ||||||||||||||||||||||||||

| GAAP | $ | (119) | (87) | % | $ | (137) | $ | (7) | $ | (130) | N.M. | $ | (0.50) | N.M. | ||||||||||||

| State opioid assessment related to prior fiscal years | (6) | (6) | (2) | (4) | (0.02) | |||||||||||||||||||||

| Shareholder cooperation agreement costs | 2 | 2 | 1 | 1 | 0.01 | |||||||||||||||||||||

| Restructuring and employee severance | 17 | 17 | 4 | 13 | 0.05 | |||||||||||||||||||||

| Amortization and other acquisition-related costs | 71 | 71 | 18 | 53 | 0.20 | |||||||||||||||||||||

Impairments and (gain)/loss on disposal of assets, net 3 | 710 | 710 | 173 | 537 | 2.06 | |||||||||||||||||||||

| Litigation (recoveries)/charges, net | (207) | (207) | (83) | (124) | (0.48) | |||||||||||||||||||||

| Non-GAAP | $ | 467 | — | % | $ | 450 | $ | 104 | $ | 346 | (3) | % | $ | 1.32 | 4 | % | ||||||||||

| Six Months Ended December 31, 2023 | ||||||||||||||||||||||||||

GAAP | $ | 468 | N.M. | $ | 464 | $ | 104 | $ | 358 | N.M. | $ | 1.44 | N.M. | |||||||||||||

Surgical gown recall income | (1) | (1) | — | (1) | — | |||||||||||||||||||||

| Restructuring and employee severance | 53 | 53 | 14 | 39 | 0.16 | |||||||||||||||||||||

| Amortization and other acquisition-related costs | 127 | 127 | 33 | 94 | 0.38 | |||||||||||||||||||||

Impairments and (gain)/loss on disposal of assets, net 3 | 538 | 538 | 112 | 426 | 1.71 | |||||||||||||||||||||

| Litigation (recoveries)/charges, net | (52) | (52) | (16) | (36) | (0.14) | |||||||||||||||||||||

Non-GAAP | $ | 1,133 | 27 | % | $ | 1,129 | $ | 247 | $ | 880 | 30 | % | $ | 3.55 | 41 | % | ||||||||||

| Six Months Ended December 31, 2022 | ||||||||||||||||||||||||||

| GAAP | $ | 18 | N.M. | $ | (27) | $ | (8) | $ | (20) | N.M. | $ | (0.08) | N.M. | |||||||||||||

| State opioid assessment related to prior fiscal years | (6) | (6) | (2) | (4) | (0.02) | |||||||||||||||||||||

Shareholder cooperation agreement costs | 8 | 8 | 2 | 6 | 0.02 | |||||||||||||||||||||

| Restructuring and employee severance | 46 | 46 | 10 | 36 | 0.13 | |||||||||||||||||||||

| Amortization and other acquisition-related costs | 142 | 142 | 37 | 105 | 0.40 | |||||||||||||||||||||

Impairments and (gain)/loss on disposal of assets, net 3 | 863 | 863 | 207 | 656 | 2.46 | |||||||||||||||||||||

| Litigation (recoveries)/charges, net | (180) | (180) | (76) | (104) | (0.39) | |||||||||||||||||||||

| Non-GAAP | $ | 891 | (10) | % | $ | 846 | $ | 170 | $ | 675 | (7) | % | $ | 2.52 | (2) | % | ||||||||||

18 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| Explanation and Reconciliation of Non-GAAP Financial Measures | ||||||||

1 Attributable to Cardinal Health, Inc.

2 For the three and six months ended December 31, 2022, GAAP diluted EPS and the EPS impact from the GAAP to non-GAAP per share reconciling items are calculated using a weighted average of 261 million and 266 million common shares, respectively, which excludes potentially dilutive securities from the denominator due to their anti-dilutive effects resulting from our GAAP net loss for the periods. For the three and six months ended December 31, 2022, non-GAAP diluted EPS is calculated using a weighted average of 263 million and 268 million common shares, which includes potentially dilutive shares.

3 For the six months ended December 31, 2023, impairments and (gain)/loss on disposal of assets, net includes a pre-tax goodwill impairment charge of $581 million related to the Medical segment. For fiscal 2024, the net tax benefit related to the impairment charge is $45 million and is included in the annual effective tax rate. As a result, the tax benefit for the six months ended December 31, 2023 increased approximately by an incremental $65 million and will increase the provision for income taxes for the remainder of fiscal 2024.

For the three and six months December 31, 2022, impairments and (gain)/loss on disposal of assets, net included cumulative pre-tax goodwill impairment charges of $709 million and $863 million, respectively, related to the Medical segment. For fiscal 2023, the net tax benefit related to these impairment charges was $68 million and was included in the annual effective tax rate. As a result, the amount of tax benefit increased approximately by an incremental $118 million and $140 million for the three and six months ended December 31, 2022, respectively, and increased the provision for income taxes for the remainder of fiscal 2023.

The sum of the components and certain computations may reflect rounding adjustments.

We apply varying tax rates depending on the item's nature and tax jurisdiction where it is incurred.

19 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| Other | |||||

Quantitative and Qualitative Disclosures About Market Risk

There have been no material changes in the quantitative and qualitative market risk disclosures included in our 2023 Form 10-K since the end of fiscal 2023 through December 31, 2023.

Controls and Procedures

Evaluation of Disclosure Controls and Procedures

We evaluated, with the participation of our principal executive officer and principal financial officer, the effectiveness of our disclosure controls and procedures (as defined in Rule 13a-15(e) under the Securities Exchange Act of 1934 (the "Exchange Act")) as of December 31, 2023. Based on this evaluation, our principal executive officer and principal financial officer have concluded that as of December 31, 2023, our disclosure controls and procedures were effective to provide reasonable assurance that information required to be disclosed in our reports under the Exchange Act is recorded, processed, summarized, and reported within the time periods specified in the SEC rules and forms and that such information is accumulated and communicated to management as appropriate to allow timely decisions regarding required disclosure.

Changes in Internal Control Over Financial Reporting

There were no changes in our internal control over financial reporting during the quarter ended December 31, 2023 that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

20 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| Other | ||||||||

Legal Proceedings

The legal proceedings described in Note 6 of the "Notes to Condensed Consolidated Financial Statements" are incorporated in this "Legal Proceedings" section by reference.

Risk Factors

You should carefully consider the information in this Form 10-Q, and the risk factors discussed in "Risk Factors" and other risks discussed in our 2023 Form 10-K, our Form 10-Q for the quarter ended September 30, 2023, and our other filings with the SEC since June 30, 2023. These risks could materially and adversely affect our results of operations, financial condition, liquidity, and cash flows. Our business also could be affected by risks that we are not presently aware of or that we currently consider immaterial to our operations.

Our pending acquisition of Specialty Networks subjects us to various risks and uncertainties.

As discussed in the MD&A section, on January 31, 2024, we announced that we had entered into a definitive agreement to acquire Specialty Networks for a purchase price of $1.2 billion in cash, subject to certain adjustments. The acquisition will further expand the Pharmaceutical segment's portfolio of Specialty services. We plan to fund the acquisition with available cash.

Consummation of the pending acquisition is subject to various risks and uncertainties, including the following: the ability to successfully complete the acquisition on a timely basis, including receipt of required regulatory approvals and satisfaction of other closing conditions; and the conditions of the credit markets.

If we are successful in completing the acquisition, we will be subject to other risks, including the following: we may fail to realize the synergies and other benefits we expect from the acquisition; the use of a significant portion of our cash may have an adverse effect on our liquidity, limit our flexibility in responding to other business opportunities, and increase our vulnerability to adverse economic and industry conditions; we may fail to retain key personnel of the acquired businesses; future developments may impair the value of our purchased goodwill or intangible assets; we may face difficulties establishing, integrating or combining operations and systems; we may face challenges retaining the customers of the acquired businesses; we may encounter unforeseen internal control, regulatory or compliance issues; and we may face other additional risks relating to regulatory matters, legal proceedings, and tax laws or positions.

Unregistered Sales of Equity Securities, Use of Proceeds, and Issuer Purchases of Equity Securities

Issuer Purchases of Equity Securities

| Period | Total Number of Shares Purchased (1) | Average Price Paid per Share (2,3) | Total Number of Shares Purchased as Part of Publicly Announced Programs (2,3,4) | Approximate Dollar Value of Shares That May Yet be Purchased Under the Program (4) (in millions) | |||||||||||||||||||

| October 2023 | 1,251,107 | $ | 79.94 | 1,250,909 | $ | 3,843 | |||||||||||||||||

| November 2023 | 1,967,452 | 101.66 | 1,967,342 | 3,543 | |||||||||||||||||||

| December 2023 | 444,271 | 112.57 | 444,161 | 3,493 | |||||||||||||||||||

| Total | 3,662,830 | $ | 95.57 | 3,662,412 | $ | 3,493 | |||||||||||||||||

(1)Reflects 198, 110 and 110 common shares purchased in October, November and December 2023, respectively, through a rabbi trust as investments of participants in our Deferred Compensation Plan.

(2)On November 6, 2023, we entered into an ASR program to purchase common shares for an aggregate purchase price of $250 million and received an initial delivery of 2.0 million common shares using a reference price of $101.66. The ASR program concluded on December 13, 2023 at a volume weighted average price per common share of $103.67 resulting in a final delivery of 0.4 million common shares. See Note 10 of the "Notes to Condensed Consolidated Financial Statements" for additional information.

(3)On August 16, 2023, we entered into an ASR program to purchase common shares for an aggregate purchase price of $500 million and received an initial delivery of 4.4 million common shares using a reference price of $90.57. The ASR program concluded on October 31, 2023 at a volume weighted average price per common share of $88.22 resulting in a final delivery of 1.3 million common shares. See Note 10 of the "Notes to Condensed Consolidated Financial Statements" for additional information.

(4)On June 7, 2023, our Board of Directors approved a new $3.5 billion share repurchase program, which will expire on December 31, 2027. As of December 31, 2023, we had $3.5 billion authorized for share repurchases remaining under this program.

21 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| Other | |||||

Other Information

Rule 10b5-1 Plan Adoptions and Modifications

During the three months ended December 31, 2023, no director or officer adopted terminated

22 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| Financial Statements | ||||||||

Condensed Consolidated Statements of Earnings/(Loss)

(Unaudited)

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||

| (in millions, except per common share amounts) | 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||

| Revenue | $ | $ | $ | $ | |||||||||||||||||||

| Cost of products sold | |||||||||||||||||||||||

| Gross margin | |||||||||||||||||||||||

| Operating expenses: | |||||||||||||||||||||||

| Distribution, selling, general and administrative expenses | |||||||||||||||||||||||

| Restructuring and employee severance | |||||||||||||||||||||||

| Amortization and other acquisition-related costs | |||||||||||||||||||||||

| Impairments and (gain)/loss on disposal of assets, net | |||||||||||||||||||||||

| Litigation (recoveries)/charges, net | ( | ( | ( | ( | |||||||||||||||||||

| Operating earnings/(loss) | ( | ||||||||||||||||||||||

| Other (income)/expense, net | ( | ( | ( | ( | |||||||||||||||||||

| Interest expense, net | |||||||||||||||||||||||

| Earnings/(loss) before income taxes | ( | ( | |||||||||||||||||||||

| Provision for/(benefit from) income taxes | ( | ( | |||||||||||||||||||||

| Net earnings/(loss) | ( | ( | |||||||||||||||||||||

| Less: Net earnings attributable to noncontrolling interests | ( | ( | ( | ||||||||||||||||||||

| Net earnings/(loss) attributable to Cardinal Health, Inc. | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| Earnings/(Loss) per common share attributable to Cardinal Health, Inc.: | |||||||||||||||||||||||

| Basic | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| Diluted | ( | ( | |||||||||||||||||||||

| Weighted-average number of common shares outstanding: | |||||||||||||||||||||||

| Basic | |||||||||||||||||||||||

| Diluted | |||||||||||||||||||||||

| Cash dividends declared per common share | $ | $ | $ | $ | |||||||||||||||||||

See notes to condensed consolidated financial statements.

23 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| Financial Statements | ||||||||

Condensed Consolidated Statements of Comprehensive Income/(Loss)

(Unaudited)

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||

| (in millions) | 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||

| Net earnings/(loss) | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| Other comprehensive income/(loss): | |||||||||||||||||||||||

| Foreign currency translation adjustments and other | ( | ( | |||||||||||||||||||||

| Net unrealized gain on derivative instruments, net of tax | |||||||||||||||||||||||

| Total other comprehensive income/(loss), net of tax | ( | ( | |||||||||||||||||||||

| Total comprehensive income/(loss) | ( | ( | |||||||||||||||||||||

Less: comprehensive income attributable to noncontrolling interests | ( | ( | ( | ||||||||||||||||||||

| Total comprehensive income/(loss) attributable to Cardinal Health, Inc. | $ | $ | ( | $ | $ | ( | |||||||||||||||||

See notes to condensed consolidated financial statements.

24 | Cardinal Health | Q2 Fiscal 2024 Form 10-Q | |||||||

| Financial Statements | ||||||||

Condensed Consolidated Balance Sheets

| (in millions) | December 31, 2023 | June 30, 2023 | |||||||||

| (Unaudited) | |||||||||||

| Assets | |||||||||||

| Current assets: | |||||||||||

| Cash and equivalents | $ | $ | |||||||||

| Trade receivables, net | |||||||||||

| Inventories, net | |||||||||||

| Prepaid expenses and other | |||||||||||

| Assets held for sale | |||||||||||

| Total current assets | |||||||||||

| Property and equipment, net | |||||||||||

| Goodwill and other intangibles, net | |||||||||||

| Other assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and Shareholders’ Deficit | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Current portion of long-term obligations and other short-term borrowings | |||||||||||

| Other accrued liabilities | |||||||||||

| Liabilities related to assets held for sale | |||||||||||

| Total current liabilities | |||||||||||

| Long-term obligations, less current portion | |||||||||||

| Deferred income taxes and other liabilities | |||||||||||

| Shareholders’ deficit: | |||||||||||

| Preferred shares, without par value: | |||||||||||

Authorized— | |||||||||||

| Common shares, without par value: | |||||||||||

Authorized— | |||||||||||

| Accumulated deficit | ( | ( | |||||||||

Common shares in treasury, at cost: | ( | ( | |||||||||