UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended March 31, 2023

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ________ to ________

Commission File Number: 1-11373

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |||||||||||||||||||

| , | , | |||||||||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||||||||

(614 ) 757-5000

(Registrant’s telephone number, including area code)

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☑ | Accelerated filer | ☐ | |||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||||||||

| Emerging growth company | |||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ

The number of the registrant’s common shares, without par value, outstanding as of April 30, 2023, was the following: 254,600,182 .

Cardinal Health Q3 Fiscal 2023 Form 10-Q | ||

Table of Contents

| Page | |||||

About Cardinal Health

Cardinal Health, Inc., an Ohio corporation formed in 1979, is a globally integrated healthcare services and products company providing customized solutions for hospitals, healthcare systems, pharmacies, ambulatory surgery centers, clinical laboratories, physician offices and patients in the home. We provide pharmaceuticals and medical products and cost-effective solutions that enhance supply chain efficiency. We connect patients, providers, payers, pharmacists and manufacturers for integrated care coordination and better patient management. We manage our business and report our financial results in two segments: Pharmaceutical and Medical. As used in this report, “we,” “our,” “us,” and similar pronouns refer to Cardinal Health, Inc. and its majority-owned and consolidated subsidiaries, unless the context requires otherwise. Our fiscal year ends on June 30. References to fiscal 2023 and fiscal 2022 and to FY23 and FY22 are to the fiscal years ending or ended June 30, 2023 and June 30, 2022, respectively.

Forward-Looking Statements

This Quarterly Report on Form 10-Q for the quarter ended March 31, 2023 (this "Form 10-Q") (including information incorporated by reference) includes "forward-looking statements" addressing expectations, prospects, estimates and other matters that are dependent upon future events or developments. Many forward-looking statements appear in Management’s Discussion and Analysis of Financial Condition and Results of Operations ("MD&A"), but there are others in this Form 10-Q, which may be identified by words such as "expect," "anticipate," "intend," "plan," "believe," "will," "should," "could," "would," "project," "continue," "likely," and similar expressions, and include statements reflecting future results or guidance, statements of outlook and expense accruals. These matters are subject to risks and uncertainties that could cause actual results to differ materially from those made, projected or implied. The most significant of these risks and uncertainties are described in this Form 10-Q, including Exhibit 99.1, and in "Risk Factors" in our Annual Report on Form 10-K for the fiscal year ended June 30, 2022 (our “2022 Form 10-K”). Forward-looking statements in this Form 10-Q speak only as of the date of this document. Except to the extent required by applicable law, we undertake no obligation to update or revise any forward-looking statement.

Non-GAAP Financial Measures

In the "Overview of Consolidated Results" section of MD&A, we use financial measures that are derived from our consolidated financial data but are not presented in our condensed consolidated financial statements prepared in accordance with U.S. generally accepted accounting principles ("GAAP"). These measures are considered "non-GAAP financial measures" under the United States Securities and Exchange Commission ("SEC") rules. The reasons we use these non-GAAP financial measures and the reconciliations to their most directly comparable GAAP financial measures are included in the “Explanation and Reconciliation of Non-GAAP Financial Measures” section following MD&A in this Form 10-Q.

1 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Overview | |||||||

Management's Discussion and Analysis of Financial Condition and Results of Operations

The discussion and analysis presented below is concerned with material changes in financial condition and results of operations, including amounts and certainty of cash flows from operations and from outside sources, between the periods specified in our condensed consolidated balance sheets at March 31, 2023 and June 30, 2022, and in our condensed consolidated statements of earnings/(loss) for the three and nine months ended March 31, 2023 and 2022. All comparisons presented are with respect to the prior-year period, unless stated otherwise. This discussion and analysis should be read in conjunction with the MD&A included in our 2022 Form 10-K.

2 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Overview | |||||||

Overview of Consolidated Results

Revenue

During the three and nine months ended March 31, 2023, revenue increased 13 percent to $50.5 billion and $151.6 billion, respectively, primarily due to branded and specialty pharmaceutical sales growth from existing customers. During the nine months ended March 31, 2023, pharmaceutical sales growth from net new customers also contributed to increased revenue.

GAAP and Non-GAAP Operating Earnings/(Loss)

| Three Months Ended March 31, | Nine Months Ended March 31, | ||||||||||||||||||||||||||||||||||

| (in millions) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

| GAAP operating earnings/(loss) | $ | 572 | $ | (97) | N.M. | $ | 590 | $ | (632) | N.M. | |||||||||||||||||||||||||

| Surgical gown recall costs/(income) | — | — | — | 1 | |||||||||||||||||||||||||||||||

| State opioid assessment related to prior fiscal years | — | — | (6) | — | |||||||||||||||||||||||||||||||

Shareholder cooperation agreement costs | — | — | 8 | — | |||||||||||||||||||||||||||||||

| Restructuring and employee severance | 16 | 31 | 62 | 56 | |||||||||||||||||||||||||||||||

| Amortization and other acquisition-related costs | 74 | 79 | 216 | 237 | |||||||||||||||||||||||||||||||

| Impairments and (gain)/loss on disposal of assets, net | 20 | 471 | 883 | 1,764 | |||||||||||||||||||||||||||||||

| Litigation (recoveries)/charges, net | (76) | 61 | (256) | 113 | |||||||||||||||||||||||||||||||

| Non-GAAP operating earnings | $ | 606 | $ | 545 | 11 | % | $ | 1,497 | $ | 1,540 | (3) | % | |||||||||||||||||||||||

The sum of the components and certain computations may reflect rounding adjustments.

We had GAAP operating earnings of $572 million during the three months ended March 31, 2023 and a GAAP operating loss of $97 million during the three months ended March 31, 2022, which reflects no goodwill impairment charge recognized during the three months ended March 31, 2023 and the $474 million pre-tax non-cash goodwill impairment charge related to the Medical segment recognized during the three months ended March 31, 2022.

We had GAAP operating earnings of $590 million and a GAAP operating loss of $632 million during the nine months ended March 31, 2023 and 2022, respectively, which included the $863 million and $1.8 billion pre-tax non-cash goodwill impairment charges related to the Medical segment, respectively. See "Critical Accounting Policies and Sensitive Accounting Estimates" section of this MD&A and Note 4 of the "Notes to Condensed Consolidated Financial Statements" for additional detail related to goodwill impairment.

GAAP operating earnings during the three and nine months ended March 31, 2023 were favorably impacted by litigation recoveries. See "Results of Operations" section of this MD&A and Note 6 of the "Notes to Condensed Consolidated Financial Statements" for additional detail related to litigation recoveries.

Non-GAAP operating earnings during the three months ended March 31, 2023 increased 11 percent to $606 million primarily due to an increase in Pharmaceutical segment profit largely driven by the performance of our generics program and an increased contribution from branded and specialty pharmaceutical products. This increase was partially offset by a decrease in Medical segment profit largely resulting from lower volumes and unfavorable product sales mix within products and distribution.

Non-GAAP operating earnings during the nine months ended March 31, 2023 decreased 3 percent to $1.5 billion primarily due to a decrease in Medical segment profit largely resulting from lower volumes and unfavorable product sales mix within products and distribution and net inflationary impacts. This decrease was partially offset by an increase in Pharmaceutical segment profit primarily driven by the performance of our generics program and an increased contribution from branded and specialty pharmaceutical products.

3 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Overview | |||||||

GAAP and Non-GAAP Diluted EPS

| Three Months Ended March 31, | Nine Months Ended March 31, | ||||||||||||||||||||||||||||||||||

| ($ per share) | 2023 | 2022(2) | Change | 2023 | 2022(2) | Change | |||||||||||||||||||||||||||||

GAAP diluted EPS (1) | $ | 1.34 | $ | (5.05) | N.M. | $ | 1.23 | $ | (3.82) | N.M. | |||||||||||||||||||||||||

| State opioid assessment related to prior fiscal years | — | — | 0.02 | — | |||||||||||||||||||||||||||||||

Shareholder cooperation agreement costs | — | — | (0.02) | — | |||||||||||||||||||||||||||||||

| Restructuring and employee severance | 0.05 | 0.08 | 0.18 | 0.15 | |||||||||||||||||||||||||||||||

| Amortization and other acquisition-related costs | 0.21 | 0.21 | 0.61 | 0.63 | |||||||||||||||||||||||||||||||

Impairments and (gain)/loss on disposal of assets, net (3) | 0.35 | 6.03 | 2.82 | 6.71 | |||||||||||||||||||||||||||||||

| Litigation (recoveries)/charges, net | (0.21) | 0.18 | (0.60) | 0.33 | |||||||||||||||||||||||||||||||

| Loss on early extinguishment of debt | — | — | — | 0.03 | |||||||||||||||||||||||||||||||

Non-GAAP diluted EPS (1) | $ | 1.74 | $ | 1.45 | 20 | % | $ | 4.24 | $ | 4.01 | 6 | % | |||||||||||||||||||||||

The sum of the components and certain computations may reflect rounding adjustments.

The reconciling items are presented within this table net of tax. See quantification of tax effect of each reconciling item in our GAAP to Non-GAAP Reconciliations in the "Explanation and Reconciliation of Non-GAAP Financial Measures."

(1)Diluted earnings/(loss) per share attributable to Cardinal Health, Inc. ("diluted EPS").

(2)For the three and nine months ended March 31, 2022, GAAP diluted EPS and the EPS impact from the GAAP to non-GAAP per share reconciling items are calculated using a weighted average of 275 million and 281 million common shares, respectively, which excludes potentially dilutive securities from the denominator due to their anti-dilutive effects resulting from our GAAP net loss for the periods. For the three and nine months ended March 31, 2022, non-GAAP diluted EPS is calculated using a weighted average of 277 million and 282 million common shares, respectively, which includes potentially dilutive shares.

(3)Impairments and (gain)/loss on disposal of assets, net included pre-tax goodwill impairment charges related to the Medical segment of $863 million recorded during the nine months ended March 31, 2023. For fiscal 2023, the estimated net tax benefit related to the impairments is $68 million and is included in the annual effective tax rate. As a result, the amount of tax expense recognized increased approximately by an incremental $74 million during the three months ended March 31, 2023. The incremental interim tax benefit recognized during the nine months ended March 31, 2023 was $66 million and will reverse in the fourth quarter of the fiscal year.

During the three and nine months ended March 31, 2022, impairments and (gain)/loss on disposal of assets, net included pre-tax goodwill impairment charges of $474 million and $1.8 billion, respectively, related to the Medical segment. For fiscal 2022, the estimated net tax benefit related to the impairment was $126 million and was included in the annual effective tax rate. As a result, the amount of tax expense recognized during the three and nine months ended March 31, 2022 increased approximately by an incremental $1.2 billion and $180 million, respectively, and lowered the provision for income taxes during the fourth quarter of fiscal 2022 by approximately $180 million.

GAAP diluted EPS was adversely impacted by the goodwill impairment charges related to the Medical segment, which had a $(2.76) per share after tax impact during the nine months ended March 31, 2023, and $(6.01) and $(6.67) per share after tax impact during the three and nine months ended March 31, 2022, respectively. See "Critical Accounting Policies and Sensitive Accounting Estimates" section of this MD&A, and Note 4 and Note 7 of the "Notes to Condensed Consolidated Financial Statements" for additional detail. GAAP EPS during the three and nine months ended March 31, 2023 also includes the favorable impact of litigation recoveries as described further in the "Results of Operations" section of this MD&A and Note 6 of "Notes to Condensed Consolidated Financial Statements."

During the three months ended March 31, 2023, non-GAAP diluted EPS increased 20 percent to $1.74 per share due to higher non-GAAP operating earnings and a lower share count.

During the nine months ended March 31, 2023, non-GAAP diluted EPS increased 6 percent to $4.24 per share due to a lower share count and interest expense, partially offset by lower non-GAAP operating earnings.

Cash and Equivalents

Our cash and equivalents balance was $4.0 billion at March 31, 2023 compared to $4.7 billion at June 30, 2022. During the nine months ended March 31, 2023, net cash provided by operating activities was $2.0 billion, which includes the impact of our second annual payment of $372 million related to the agreement to settle the vast majority of the opioid lawsuits filed by states and local governmental entities (the "Settlement Agreement"). In addition, during the nine months ended March 31, 2023, we deployed $1.5 billion for share repurchases, $571 million for debt repayments, $399 million for cash dividends and $264 million for capital expenditures.

4 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Overview | |||||||

Significant Developments in Fiscal 2023 and Trends

Inflationary Impacts

Beginning in fiscal 2022, Medical segment profit was negatively affected by incremental inflationary impacts, primarily related to transportation (including ocean and domestic freight), commodities and labor, and global supply chain constraints. Since that time, we have taken certain actions to mitigate these impacts, including implementing certain price increases and evolving our pricing and commercial contracting processes to provide us with greater pricing flexibility. In addition, certain decreases in some product-related costs are beginning to be recognized as the higher-cost inventory is moving through our supply chain. As a result, during the three months ended March 31, 2023, these inflationary impacts, net of our mitigation actions, and global supply chain constraints had a slightly favorable impact on Medical segment profit on a year-over-year basis. During the nine months ended March 31, 2023, these net inflationary impacts negatively affected Medical segment profit on a year-over-year basis.

We expect these net inflationary impacts to continue to affect Medical segment profit in fiscal 2023 and beyond, but to a lesser extent than in prior periods. These inflationary costs are difficult to predict and may be greater than we expect or continue longer than our current expectations. Any additional benefit to Medical segment profit from further decreases in these product-related costs will be delayed until the higher-cost inventory has moved through our supply chain. Our actions to increase prices and evolve our contracting strategies are subject to contingencies and uncertainties and it is possible that our results of operations will be adversely impacted to a greater extent than we currently anticipate or that we may not be able to mitigate the negative impact to the extent or on the timeline we anticipate.

To a lesser extent, inflationary impacts, primarily related to increased transportation and labor costs, also adversely affected Pharmaceutical segment profit during the three and nine months ended March 31, 2023 and on a year-over-year basis during the nine months ended March 31, 2023. During the three months ended March 31, 2023, these inflationary impacts did not have a meaningful impact on Pharmaceutical segment profit on a year-over-year basis.

PPE Demand and Pricing

Personal protective equipment ("PPE") refers to protective clothing, medical gloves, face shields, face masks and other equipment designed to protect the wearer from injury or the spread of infection or illness.

PPE adversely impacted Medical segment revenue during the three and nine months ended March 31, 2023 on a year-over-year basis, primarily due to declines in volumes and pricing.

Medical segment profit was favorably impacted during the three and nine months ended March 31, 2023 and on a year-over-year basis by a net positive contribution from PPE, primarily driven by lower costs.

The demand and pricing for PPE is subject to risks and uncertainties, which may continue to impact Medical segment revenue, Medical segment profit and consolidated operating earnings during the remainder of fiscal 2023.

Medical Goodwill

Due to changes in our long-term financial plan assumptions made during the three months ended March 31, 2023, we performed interim goodwill impairment testing for the Medical operating segment (excluding our Cardinal Health at-Home Solutions division) (the “Medical Unit”) at March 31, 2023. We concluded that there was no impairment of goodwill at March 31, 2023, as the estimated fair value of the Medical Unit exceeded its carrying value.

We performed quantitative goodwill impairment testing for the Medical Unit at December 31, 2022 and September 30, 2022, which resulted in pre-tax goodwill impairment charges of $709 million and $154 million, respectively. The cumulative pre-tax goodwill impairment charges of $863 million were recognized in impairments and (gain)/loss on disposal of assets, net in our condensed consolidated statements of earnings/(loss) for the nine months ended March 31, 2023. See "Critical Accounting Policies and Sensitive Accounting Estimates" section of this MD&A and Note 4 of the "Notes to Condensed Consolidated Financial Statements" for additional detail.

Adverse changes in key assumptions, including an increase in the discount rate, or a significant change in industry or economic trends during the remainder of fiscal 2023 and beyond could result in additional goodwill impairments.

5 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Overview | |||||||

Shareholder Cooperation Agreement

In September 2022, we entered into a Cooperation Agreement (the "Cooperation Agreement") with Elliott Associates, L.P. and Elliott International, L.P. (together, "Elliott") under which our Board of Directors (the "Board"), among other things, (1) appointed four new independent directors, including a representative from Elliott, and (2) formed an advisory Business Review Committee of the Board, which is tasked with undertaking a comprehensive review of our strategy, portfolio, capital-allocation framework and operations. In May 2023, we extended the term of the Cooperation Agreement until the later of July 15, 2024 or until Elliott's representative ceases to serve on, or resigns from, the Board. In connection with this extension, the Board has extended the term of the Business Review Committee until July 15, 2024.

The evaluation and implementation of any actions recommended by the Business Review Committee and the Board may impact our financial position and results of operations during the remainder of fiscal 2023 and beyond. In addition, during the nine months ended March 31, 2023, we incurred $8 million of expenses related to the negotiation and finalization of the Cooperation Agreement and other consulting expenses. We have incurred, and expect to continue to incur additional legal, consulting and other expenses related to the Cooperation Agreement and the activities of the Business Review Committee. See "Risk Factors" section for additional detail related to risks associated with the Cooperation Agreement.

Pharmaceutical Segment Generics Program

The performance of our Pharmaceutical segment generics program positively impacted the year-over-year comparison of Pharmaceutical segment profit during the three and nine months ended March 31, 2023. The Pharmaceutical segment generics program includes, among other things, the impact of generic pharmaceutical product launches, customer volumes, pricing changes, the Red Oak Sourcing, LLC venture ("Red Oak Sourcing") with CVS Health Corporation ("CVS Health") and generic pharmaceutical contract manufacturing and sourcing costs. During the nine months ended March 31, 2023, generic pharmaceutical contract manufacturing inventory-related charges adversely impacted the performance of our generics program.

The frequency, timing, magnitude and profit impact of generic pharmaceutical customer volumes, pricing changes, customer contract renewals, generic pharmaceutical manufacturer pricing changes and generic pharmaceutical contract manufacturing and sourcing costs all impact Pharmaceutical segment profit and are subject to risks and uncertainties. These risks and uncertainties may impact Pharmaceutical segment profit and consolidated operating earnings during the remainder of fiscal 2023.

6 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Results of Operations | |||||||

Results of Operations

Revenue

| Three Months Ended March 31, | Nine Months Ended March 31, | ||||||||||||||||||||||||||||||||||

| (in millions) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

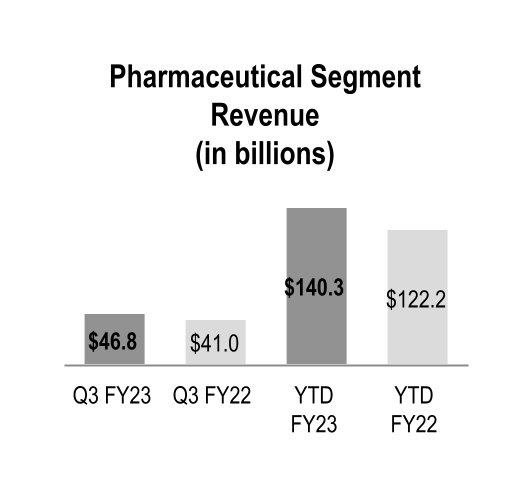

| Pharmaceutical | $ | 46,809 | $ | 40,957 | 14 | % | $ | 140,310 | $ | 122,154 | 15 | % | |||||||||||||||||||||||

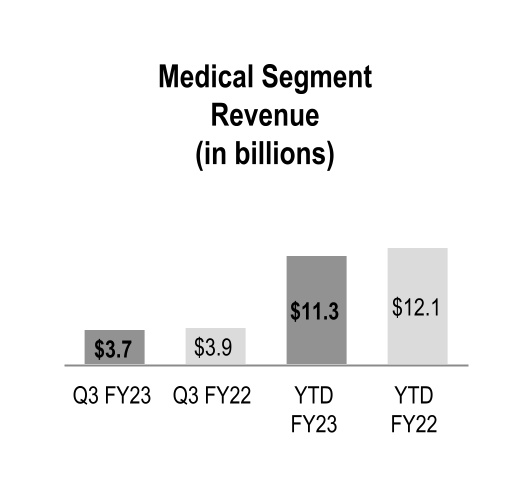

| Medical | 3,684 | 3,884 | (5) | % | 11,259 | 12,118 | (7) | % | |||||||||||||||||||||||||||

| Total segment revenue | 50,493 | 44,841 | 13 | % | 151,569 | 134,272 | 13 | % | |||||||||||||||||||||||||||

| Corporate | (6) | (5) | N.M. | (10) | (11) | N.M. | |||||||||||||||||||||||||||||

| Total revenue | $ | 50,487 | $ | 44,836 | 13 | % | $ | 151,559 | $ | 134,261 | 13 | % | |||||||||||||||||||||||

Pharmaceutical Segment

Pharmaceutical segment revenue increased during the three and nine months ended March 31, 2023 due to branded and specialty pharmaceutical sales growth, which increased revenue by $5.8 billion and $17.9 billion, respectively, primarily from existing customers. During the nine months ended March 31, 2023, pharmaceutical sales growth from net new customers also contributed to increased revenue.

Medical Segment

Medical segment revenue decreased during the three months ended March 31, 2023 primarily due to an adverse impact of PPE volumes and pricing within products and distribution.

Medical segment revenue decreased during the nine months ended March 31, 2023 primarily due to lower sales within products and distribution, which includes an adverse impact from PPE volumes and pricing, and was partially offset by sales growth in at-Home Solutions.

Cost of Products Sold

Cost of products sold for the three and nine months ended March 31, 2023 increased 13 percent to $48.7 billion and $146.5 billion, respectively, compared to the prior-year periods due to the factors affecting the changes in revenue and gross margin.

7 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Results of Operations | |||||||

Gross Margin

| Three Months Ended March 31, | Nine Months Ended March 31, | ||||||||||||||||||||||||||||||||||

| (in millions) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

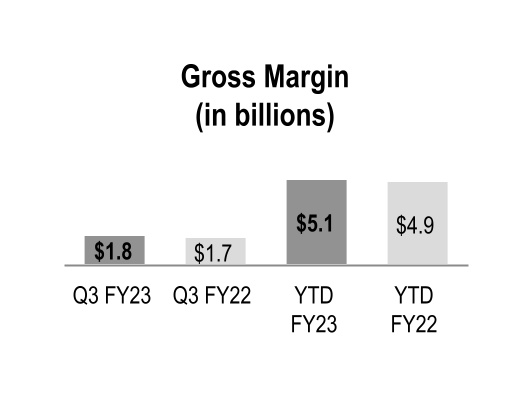

| Gross margin | $ | 1,785 | $ | 1,682 | 6 | % | $ | 5,062 | $ | 4,940 | 2 | % | |||||||||||||||||||||||

Gross margin increased during the three and nine months ended March 31, 2023 primarily due to the Pharmaceutical segment, which included the performance of our generics program and a higher contribution from branded and specialty pharmaceutical products. The increase in gross margin due to the Pharmaceutical segment during the nine months ended March 31, 2023 was partially offset by the performance of products and distribution within the Medical segment, primarily driven by lower volumes and unfavorable product sales mix.

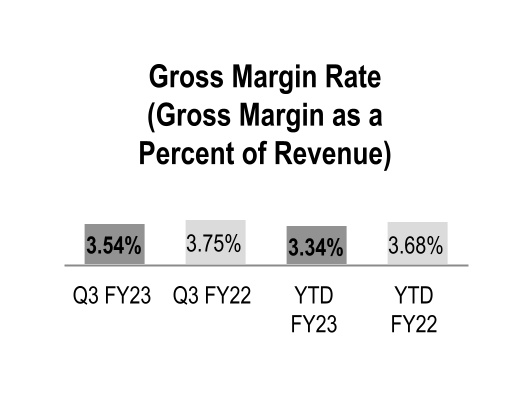

Gross margin rate declined 21 basis points and 34 basis points during the three and nine months ended March 31, 2023, respectively, mainly due to changes in overall product mix, primarily driven by increased pharmaceutical distribution branded sales, which have a dilutive impact on our overall gross margin rate.

Distribution, Selling, General and Administrative ("SG&A") Expenses

| Three Months Ended March 31, | Nine Months Ended March 31, | ||||||||||||||||||||||||||||||||||

| (in millions) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

| SG&A expenses | $ | 1,179 | $ | 1,137 | 4 | % | $ | 3,567 | $ | 3,402 | 5 | % | |||||||||||||||||||||||

During the three and nine months ended March 31, 2023, SG&A expenses increased primarily due to inflationary impacts, primarily related to increased transportation and labor costs, and higher operating expenses (which were partially offset by the beneficial impact of enterprise-wide cost-savings measures).

During the nine months ended March 31, 2023, we incurred $8 million of expenses primarily related to the finalization of the Cooperation Agreement. See "Significant Developments in Fiscal 2023 and Trends" section in this MD&A for additional detail related to the Cooperation Agreement.

During the nine months ended March 31, 2023, we recorded $6 million of income to reduce our accrual for the assessment on prescription opioid medications that were sold or distributed in New York state in calendar year 2018 to the amount invoiced. See Note 6 of the "Notes to Condensed Consolidated Financial Statements" for additional information.

8 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Results of Operations | |||||||

Segment Profit

We evaluate segment performance based on segment profit, among other measures. See Note 12 of the "Notes to Condensed Consolidated Financial Statements" for additional information on segment profit.

| Three Months Ended March 31, | Nine Months Ended March 31, | ||||||||||||||||||||||||||||||||||

| (in millions) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

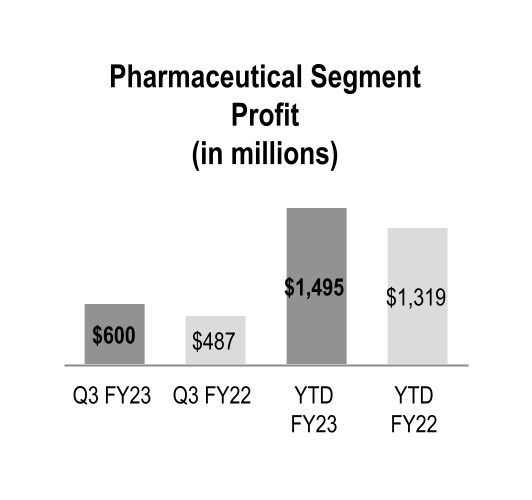

| Pharmaceutical | $ | 600 | $ | 487 | 23 | % | $ | 1,495 | $ | 1,319 | 13 | % | |||||||||||||||||||||||

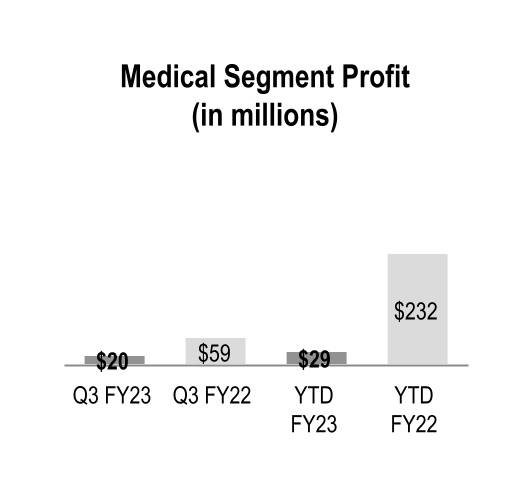

| Medical | 20 | 59 | (66) | % | 29 | 232 | (88) | % | |||||||||||||||||||||||||||

| Total segment profit | 620 | 546 | 14 | % | 1,524 | 1,551 | (2) | % | |||||||||||||||||||||||||||

| Corporate | (48) | (643) | N.M. | (934) | (2,183) | N.M. | |||||||||||||||||||||||||||||

| Total consolidated operating earnings/(loss) | $ | 572 | $ | (97) | N.M. | $ | 590 | $ | (632) | N.M. | |||||||||||||||||||||||||

Pharmaceutical Segment Profit

Pharmaceutical segment profit increased during the three and nine months ended March 31, 2023 primarily due to the performance of our generics program and an increased contribution from branded and specialty pharmaceutical products.

Medical Segment Profit

Medical segment profit decreased during the three and nine months ended March 31, 2023 primarily due to the performance of products and distribution, largely driven by lower volumes and unfavorable product sales mix. Medical segment profit during the nine months ended March 31, 2023 was also unfavorably affected by net inflationary impacts.

Corporate

The changes in Corporate during the three and nine months ended March 31, 2023 were due to the factors discussed in the "Other Components of Consolidated Operating Earnings/(Loss)" section that follows.

9 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Results of Operations | |||||||

Other Components of Consolidated Operating Earnings/(Loss)

In addition to revenue, gross margin and SG&A expenses discussed previously, consolidated operating earnings/(loss) were impacted by the following:

| Three Months Ended March 31, | Nine Months Ended March 31, | ||||||||||||||||||||||

| (in millions) | 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||

| Restructuring and employee severance | $ | 16 | $ | 31 | $ | 62 | $ | 56 | |||||||||||||||

| Amortization and other acquisition-related costs | 74 | 79 | 216 | 237 | |||||||||||||||||||

| Impairments and (gain)/loss on disposal of assets, net | 20 | 471 | 883 | 1,764 | |||||||||||||||||||

| Litigation (recoveries)/charges, net | (76) | 61 | (256) | 113 | |||||||||||||||||||

Restructuring and Employee Severance

Restructuring and employee severance costs during the three and nine months ended March 31, 2023 were primarily related to the implementation of certain enterprise-wide cost-savings measures and the divestiture of the Cordis business. During the three and nine months ended March 31, 2022, restructuring also included facility exit costs related to decreasing our overall office space.

Amortization and Other Acquisition-Related Costs

Amortization of acquisition-related intangible assets was $69 million and $78 million for the three months ended March 31, 2023 and 2022, respectively, and $211 million and $235 million for the nine months ended March 31, 2023 and 2022, respectively.

Impairments and (Gain)/Loss on Disposal of Assets, Net

We recognized $863 million of pre-tax non-cash goodwill impairment charges related to our Medical segment during the nine months ended March 31, 2023, and $474 million and $1.8 billion during the three and nine months ended March 31, 2022, respectively, as discussed further in the "Critical Accounting Policies and Sensitive Accounting Estimates" section of this MD&A and Note 4 of the "Notes to Condensed Consolidated Financial Statements."

Litigation (Recoveries)/Charges, Net

We recognized income of $71 million and $95 million during the three and nine months ended March 31, 2023, respectively, primarily related to a reduction of the reserve for the estimated settlement and defense costs for the Cordis OptEase and TrapEase inferior vena cava ("IVC") product liability due to the execution of certain settlement agreements. During the three and nine months ended March 31, 2022, we recognized estimated losses and legal defense costs associated with the IVC filter product liability claims of $24 million and $63 million, respectively. See Note 6 of the "Notes to Condensed Consolidated Financial Statements" for additional information.

During the nine months ended March 31, 2023, we recognized income of $93 million due to net proceeds from the settlement of a shareholder derivative litigation matter as described further in the "Legal Proceedings" section.

We recognized income for net recoveries in class action antitrust lawsuits in which we were a class member or plaintiff of $66 million and $17 million during the nine months ended March 31, 2023 and 2022, respectively.

During the three and nine months ended March 31, 2022, we incurred a one-time contingent attorney fee of $18 million related to the finalization of the Settlement Agreement resulting in the settlement of the vast majority of opioid lawsuits filed by state and local governmental entities. Due to the unique nature and significance of the Settlement Agreement, and the one-time, contingent nature of the fee, this related fee was included in litigation (recoveries)/charges, net.

Earnings/(Loss) Before Income Taxes

In addition to the items discussed above, earnings/(loss) before income taxes were impacted by the following:

| Three Months Ended March 31, | Nine Months Ended March 31, | ||||||||||||||||||||||||||||||||||

| (in millions) | 2023 | 2022 | Change | 2023 | 2022 | Change | |||||||||||||||||||||||||||||

| Other (income)/expense, net | $ | — | $ | 3 | N.M. | $ | (5) | $ | (14) | N.M. | |||||||||||||||||||||||||

| Interest expense, net | 28 | 38 | (26) | % | 78 | 115 | (32) | % | |||||||||||||||||||||||||||

| Loss on early extinguishment of debt | — | — | N.M. | — | 10 | N.M. | |||||||||||||||||||||||||||||

| (Gain)/loss on sale of equity interest in naviHealth | — | (1) | N.M. | — | (2) | N.M. | |||||||||||||||||||||||||||||

10 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Results of Operations | |||||||

Interest Expense, Net

During the three and nine months ended March 31, 2023, interest expense decreased by 26 percent and 32 percent, respectively, primarily due to increased interest income from cash and equivalents.

Loss on Early Extinguishment of Debt

During the nine months ended March 31, 2022, we recognized a $10 million loss in connection with the debt redemption as described further in Note 5 of the “Notes to Condensed Consolidated Financial Statements.”

Provision for Income Taxes

The effective tax rate was 36.3 percent and (916.5) percent during the three months ended March 31, 2023 and 2022, respectively, and 36.7 percent and (44.4) percent during the nine months ended March 31, 2023 and 2022, respectively. These tax rates reflect the impact of the tax effects of goodwill impairment charges recognized during the three and nine months ended March 31, 2023 and 2022.

Tax Effects of Goodwill Impairment Charges

During the nine months ended March 31, 2023, we recognized cumulative pre-tax goodwill impairment charges of $863 million related to the Medical Unit. The net tax benefit related to these charges is $68 million for fiscal 2023.

Unless an item is considered discrete because it is unusual or infrequent, the tax impact of the item is included in our estimated annual effective tax rate. When items are recognized through our estimated annual effective tax rate, we apply our estimated annual effective tax rate to the earnings/(loss) before income taxes for the year-to-date period to compute our impact from income taxes for the current quarter and year-to-date period. The tax impacts of discrete items are recognized in their entirety in the period in which they occur.

The tax effect of the goodwill impairment charges recorded during the nine months ended March 31, 2023 was included in our estimated annual effective tax rate because it was not considered unusual or infrequent, given that we recorded goodwill impairments in prior fiscal years. The impact of the non-deductible goodwill increased the estimated annual effective tax rate for fiscal 2023. Applying the higher tax rate to the pre-tax income for the nine months ended March 31, 2023 resulted in recognizing an incremental interim tax expense of approximately $74 million, which impacted the provision for income taxes in the condensed consolidated statements of earnings/(loss) during the three months ended March 31, 2023 and prepaid expenses and other assets in the condensed consolidated balance sheet at March 31, 2023. The incremental interim tax benefit recognized during the nine months ended March 31, 2023 was $66 million and will reverse in the fourth quarter of fiscal 2023.

11 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Liquidity and Capital Resources | |||||||

Liquidity and Capital Resources

We currently believe that, based on available capital resources (cash on hand and committed credit facilities) and projected operating cash flow, we have adequate capital resources to fund working capital needs; currently anticipated capital expenditures; currently anticipated business growth and expansion; contractual obligations and cash requirements; tax payments; current and projected debt service requirements, upcoming debt maturities, dividends and share repurchases; and known opioid litigation settlement payments. If we decide to engage in one or more acquisitions, depending on the size and timing of such transactions, we may need to access capital markets for additional financing.

Cash and Equivalents

Our cash and equivalents balance was $4.0 billion at March 31, 2023 compared to $4.7 billion at June 30, 2022.

During the nine months ended March 31, 2023, net cash provided by operating activities was $2.0 billion, which includes the impact of our second annual payment of $372 million related to the Settlement Agreement. For additional information, see "Opioid Litigation Settlement Agreement" section below. In addition, we deployed cash of $1.5 billion for share repurchases, $571 million for debt repayments, $399 million for cash dividends and $264 million for capital expenditures.

At March 31, 2023, our cash and equivalents were held in cash depository accounts with major banks or invested in high quality, short-term liquid investments.

Changes in working capital, which impact operating cash flow, can vary significantly depending on factors such as the timing of customer payments, inventory purchases, payments to vendors and tax payments in the regular course of business, as well as fluctuating working capital needs driven by customer and product mix.

The cash and equivalents balance at March 31, 2023 includes $689 million of cash held by subsidiaries outside of the United States.

Other Financing Arrangements and Financial Instruments

Credit Facilities and Commercial Paper

In addition to cash and equivalents and operating cash flow, other sources of liquidity at March 31, 2023 include a $2.0 billion commercial paper program, backed by a $2.0 billion revolving credit facility. We also have a $1.0 billion committed receivables sales facility. During the nine months ended March 31, 2023, under our commercial paper program and our committed receivables program, we had maximum combined total daily amounts outstanding of $445 million and average combined daily amount outstanding of $4 million. At March 31, 2023, we had no amounts outstanding under our commercial paper program, revolving credit facility, or our committed receivables sales facility.

In February 2023, we extended our revolving credit facility through February 25, 2028. In September 2022, we renewed our committed receivables sales facility program through Cardinal Health Funding, LLC ("CHF") through September 30, 2025.

Our revolving credit and committed receivables sales facilities require us to maintain a consolidated net leverage ratio of no more than 3.75-to-1. As of March 31, 2023, we were in compliance with this financial covenant.

Long-Term Debt and Other Short-Term Borrowings

At March 31, 2023 and June 30, 2022, we had total long-term obligations, including the current portion and other short-term borrowings, of $4.7 billion and $5.3 billion, respectively. In March 2023, we repaid $550 million 3.2% Notes due 2023 at maturity with available cash.

12 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Liquidity and Capital Resources | |||||||

Capital Deployment

Opioid Litigation Settlement Agreement

We had $5.85 billion accrued at March 31, 2023 related to certain opioid litigation, as further described within Note 6 of the "Notes to Condensed Consolidated Financial Statements." We expect the majority of the remaining payment amounts to be spread over the next 17 years. The effective date of the Settlement Agreement was April 2, 2022. During the nine months ended March 31, 2023, we made our second annual payment of $372 million under the Settlement Agreement. We expect to make subsequent annual payments under the Settlement Agreement every July for the remainder of the 18-year term of the Settlement Agreement. The amounts of these future payments may differ from the payments that we have already made.

Capital Expenditures

Capital expenditures during the nine months ended March 31, 2023 and 2022 were $264 million and $223 million, respectively.

Dividends

On each of May 10, 2022, August 10, 2022, November 8, 2022 and February 10, 2023, our Board of Directors approved a quarterly dividend of $0.4957 per share, or $1.98 per share on an annualized basis, which were paid on July 15, 2022, October 17, 2022, January 15, 2023 and April 15, 2023 to shareholders of record on July 1, 2022, October 3, 2022, January 3, 2023 and April 3, 2023, respectively.

Share Repurchases

During the nine months ended March 31, 2023, we repurchased $1.5 billion of our common shares, in the aggregate, under accelerated share repurchase ("ASR") programs. We funded the ASR programs with available cash. See Note 10 of the "Notes to Condensed Consolidated Financial Statements" for additional information.

On November 4, 2021, our Board of Directors approved a new $3.0 billion share repurchase program, which will expire on December 31, 2024. As of March 31, 2023, we have $1.2 billion authorized for share repurchases remaining under this program.

13 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Other Items | |||||||

Other Items

The MD&A in our 2022 Form 10-K addresses our contractual obligations and cash requirements, as of and for the fiscal year ended June 30, 2022. There have been no subsequent material changes outside the ordinary course of business to those items.

Critical Accounting Policies and Sensitive Accounting Estimates

The discussion and analysis presented below is a supplemental disclosure to the critical accounting policies and sensitive accounting estimates specified in our consolidated balance sheet at June 30, 2022. This discussion and analysis should be read in conjunction with the Critical Accounting Policies and Sensitive Accounting Estimates included in our 2022 Form 10-K and our Form 10-Q for the quarters ended September 30, 2022 and December 31, 2022.

Critical accounting policies are those accounting policies that (i) can have a significant impact on our financial condition and results of operations and (ii) require the use of complex and subjective estimates based upon past experience and management’s judgment. Other people applying reasonable judgment to the same facts and circumstances could develop different estimates. Because estimates are inherently uncertain, actual results may differ, including due to the risks discussed in "Risk Factors" and other risks discussed in our 2022 Form 10-K and our other filings with the SEC since June 30, 2022.

Goodwill

Purchased goodwill is tested for impairment annually or when indicators of impairment exist. Goodwill impairment testing involves a comparison of the estimated fair value of reporting units to the respective carrying amount, which may be performed utilizing either a qualitative or quantitative assessment. Qualitative factors are first assessed to determine if it is more likely than not that the fair value of a reporting unit is less than its carrying amount. If it is determined that it is more likely than not that the fair value does not exceed the carrying amount, then a quantitative test is performed. The quantitative goodwill impairment test involves a comparison of the estimated fair value of the reporting unit to the respective carrying amount. A reporting unit is defined as an operating segment or one level below an operating segment (also known as a component).

Our reporting units are: Pharmaceutical operating segment (excluding our Nuclear and Precision Health Solutions division); Nuclear and Precision Health Solutions division; Medical operating segment (excluding our Cardinal Health at-Home Solutions division) (“Medical Unit”); and Cardinal Health at-Home Solutions division.

Goodwill impairment testing involves judgment, including the identification of reporting units, qualitative evaluation of events and circumstances to determine if it is more likely than not that an impairment exists, and, if necessary, the estimation of the fair value of the applicable reporting unit. Our qualitative evaluation considers the weight of evidence and significance of all identified events and circumstances and most relevant drivers of fair value, both positive and negative, in determining whether it is more likely than not that the fair value of a reporting unit is less than its carrying amount.

Medical Unit Goodwill

Due to changes in our long-term financial plan assumptions made during the three months ended March 31, 2023, we elected to bypass the qualitative assessment and perform quantitative goodwill impairment testing for the Medical Unit. We concluded that there was no impairment of goodwill at March 31, 2023, as the estimated fair value of the Medical Unit exceeded its carrying value by approximately 4 percent, primarily driven by a lower discount rate as described below.

We performed quantitative goodwill impairment testing for the Medical Unit at December 31, 2022 and September 30, 2022, which resulted in pre-tax goodwill impairment charges of $709 million and $154 million, respectively. The impairment charge recognized in the second quarter was driven by certain reductions in our long-term financial plan assumptions, and the impairment charge recognized in the first quarter was driven by an increase in the discount rate primarily due to an increase in the risk-free interest rate. The cumulative pre-tax goodwill impairment charges of $863 million were recognized in impairments and (gain)/loss on disposal of assets, net in our condensed consolidated statements of earnings/(loss) for the nine months ended March 31, 2023.

Our determinations of the estimated fair value of the Medical Unit at March 31, 2023, December 31, 2022 and September 30, 2022 were based on a combination of the income-based approach (using a terminal growth rate of 2 percent), and the market-based approaches. For the income-based approach, we used discount rates of 10 percent, 10.5 percent and 10.5 percent for each quarter, respectively. Additionally, we assigned a weighting of 80 percent to the discounted cash flow method, 10 percent to the guideline public company method, and 10 percent to the guideline transaction method. The decrease in the discount rate for the interim testing performed at March 31, 2023 was primarily due to a decrease in the risk-free interest rate.

14 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| MD&A | Other Items | |||||||

While we consider the assumptions used in our determination of the estimated fair value of the Medical Unit to be reasonable and appropriate, they are complex and subjective, and additional adverse changes in one key assumption or a combination of key assumptions during fiscal 2023 may significantly affect future estimates. These assumptions include, among other things, a failure to meet expected earnings or other financial plans, including the execution of key initiatives related to optimizing and growing sales of Cardinal Health branded medical products, increasing growth in certain strategic divisions within our Medical segment, and driving simplification efforts and cost optimization projects, or unanticipated events and circumstances, such as changes in assumptions about the duration and magnitude of increased supply chain and commodities costs and our efforts to mitigate such impact, including price increases or surcharges; further disruptions in the supply chain; manufacturing cost inefficiencies resulting from lower than anticipated sales volume; estimated demand and selling prices for PPE; an increase in the discount rate; a decrease in the terminal growth rate; increases in tax rates; or a significant change in industry or economic trends.

Adverse changes in key assumptions may result in a decline in fair value below the carrying value in the future and therefore, an impairment of our Medical Unit goodwill in future periods, which could adversely affect our results of operations. For example, if we were to increase the discount rate by a hypothetical 0.5 percent to 10.5 percent or decrease the terminal growth rate by a hypothetical 1.7 percent to 0.3 percent, the carrying value would have exceeded the fair value of the Medical Unit by approximately 1 percent.

During the three months ended March 31, 2022 and December 31, 2021, we performed quantitative goodwill impairment testing for the Medical Unit. This quantitative testing resulted in the carrying amount of the Medical Unit exceeding the fair value, resulting in pre-tax impairment charges of $474 million and $1.3 billion recorded during the three months ended March 31, 2022 and December 31, 2021, respectively. Refer to our 2022 Form 10-K for additional detail.

15 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| Explanation and Reconciliation of Non-GAAP Financial Measures | ||||||||

Explanation and Reconciliation of Non-GAAP Financial Measures

The "Overview of Consolidated Results" section within MD&A in this Form 10-Q contains financial measures that are not calculated in accordance with GAAP.

In addition to analyzing our business based on financial information prepared in accordance with GAAP, we use these non-GAAP financial measures internally to evaluate our performance, engage in financial and operational planning, and determine incentive compensation because we believe that these measures provide additional perspective on and, in some circumstances are more closely correlated to, the performance of our underlying, ongoing business. We provide these non-GAAP financial measures to investors as supplemental metrics to assist readers in assessing the effects of items and events on our financial and operating results on a year-over-year basis and in comparing our performance to that of our competitors. However, the non-GAAP financial measures that we use may be calculated differently from, and therefore may not be comparable to, similarly titled measures used by other companies. The non-GAAP financial measures disclosed by us should not be considered a substitute for, or superior to, financial measures calculated in accordance with GAAP, and the financial results calculated in accordance with GAAP and reconciliations to those financial statements set forth below should be carefully evaluated.

Exclusions from Non-GAAP Financial Measures

Management believes it is useful to exclude the following items from the non-GAAP measures presented in this report for its own and for investors’ assessment of the business for the reasons identified below:

•LIFO charges and credits are excluded because the factors that drive last-in first-out ("LIFO") inventory charges or credits, such as pharmaceutical manufacturer price appreciation or deflation and year-end inventory levels (which can be meaningfully influenced by customer buying behavior immediately preceding our fiscal year-end), are largely out of our control and cannot be accurately predicted. The exclusion of LIFO charges and credits from non-GAAP metrics facilitates comparison of our current financial results to our historical financial results and to our peer group companies’ financial results. We did not recognize any LIFO charges or credits during the periods presented.

•Surgical gown recall costs or income includes inventory write-offs and certain remediation and supply disruption costs, net of related insurance recoveries, arising from the January 2020 recall of select Association for the Advancement of Medical Instrumentation ("AAMI") Level 3 surgical gowns and voluntary field actions (a recall of some packs and a corrective action allowing overlabeling of other packs) for Presource Procedure Packs containing affected gowns. Income from surgical gown recall costs represents insurance recoveries of these certain costs. We have excluded these costs from our non-GAAP metrics to allow investors to better understand the underlying operating results of the business and to facilitate comparison of our current financial results to our historical financial results and to our peer group companies’ financial results.

•State opioid assessments related to prior fiscal years is the portion of state assessments for prescription opioid medications that were sold or distributed in periods prior to the period in which the expense is incurred. This portion is excluded from non-GAAP financial measures because it is retrospectively applied to sales in prior fiscal years and inclusion would obscure analysis of the current fiscal year results of our underlying, ongoing business. Additionally, while states' laws may require us to make payments on an ongoing basis, the portion of the assessment related to sales in prior periods are contemplated to be one-time, nonrecurring items. Income from state opioid assessments related to prior fiscal years represents reversals of accruals due to changes in estimates or when the underlying assessments were invalidated by a Court or reimbursed by manufacturers.

•Shareholder cooperation agreement costs includes costs such as legal, consulting and other expenses incurred in relation to the agreement (the "Cooperation Agreement") entered into among Elliott Associates, L.P., Elliott International, L.P. (together, "Elliott") and Cardinal Health, including costs incurred to negotiate and finalize the Cooperation Agreement and costs incurred by the new Business Review Committee of the Board of Directors, which was formed under this Cooperation Agreement. We have excluded these costs from our non-GAAP metrics because they do not occur in or reflect the ordinary course of our ongoing business operations and may obscure analysis of trends and financial performance.

•Restructuring and employee severance costs are excluded because they are not part of the ongoing operations of our underlying business.

•Amortization and other acquisition-related costs, which include transaction costs, integration costs, and changes in the fair value of contingent consideration obligations, are excluded because they are not part of the ongoing operations of our underlying business and to facilitate comparison of our current financial results to our historical financial results and to our peer group

16 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| Explanation and Reconciliation of Non-GAAP Financial Measures | ||||||||

companies' financial results. Additionally, costs for amortization of acquisition-related intangible assets are non-cash amounts, which are variable in amount and frequency and are significantly impacted by the timing and size of acquisitions, so their exclusion facilitates comparison of historical, current and forecasted financial results. We also exclude other acquisition-related costs, which are directly related to an acquisition but do not meet the criteria to be recognized on the acquired entity’s initial balance sheet as part of the purchase price allocation. These costs are also significantly impacted by the timing, complexity and size of acquisitions.

•Impairments and gain or loss on disposal of assets, net are excluded because they do not occur in or reflect the ordinary course of our ongoing business operations and are inherently unpredictable in timing and amount, and in the case of impairments, are non-cash amounts, so their exclusion facilitates comparison of historical, current and forecasted financial results.

•Litigation recoveries or charges, net are excluded because they often relate to events that may have occurred in prior or multiple periods, do not occur in or reflect the ordinary course of our business and are inherently unpredictable in timing and amount. During fiscal 2022, we incurred a one-time contingent attorneys' fee of $18 million related to the finalization of the settlement agreement (the “Settlement Agreement”) resulting in the settlement of the vast majority of opioid lawsuits filed by state and local governmental entities. Due to the unique nature and significance of the Settlement Agreement, and the one-time, contingent nature of the fee, this fee was included in litigation recoveries or charges, net. Additionally, during fiscal 2022 our Pharmaceutical segment profit was positively impacted by a $16 million judgment for lost profits. This judgment was the result of an ordinary course intellectual property rights claim and, therefore, is not adjusted in calculating the litigation recoveries or charges, net adjustment. During fiscal 2021, we incurred a tax benefit related to a carryback of a net operating loss. Some pre-tax amounts, which contributed to this loss, relate to litigation charges. As a result, we allocated substantially all of the tax benefit to litigation charges.

•Loss on early extinguishment of debt is excluded because it does not typically occur in the normal course of business and may obscure analysis of trends and financial performance. Additionally, the amount and frequency of this type of charge is not consistent and is significantly impacted by the timing and size of debt extinguishment transactions.

•(Gain)/Loss on sale of equity interest in naviHealth was incurred in connection with the sale of our remaining equity interest in naviHealth in fiscal 2020. The equity interest was retained in connection with the initial sale of our majority interest in naviHealth during fiscal 2019. We exclude this significant gain because gains or losses on investments of this magnitude do not typically occur in the normal course of business and are similar in nature to a gain or loss from a divestiture of a majority interest, which we exclude from non-GAAP results. The gain on the initial sale of our majority interest in naviHealth in fiscal 2019 was also excluded from our non-GAAP measures.

The tax effect for each of the items listed above is determined using the tax rate and other tax attributes applicable to the item and the jurisdiction(s) in which the item is recorded. The gross, tax and net impact of each item are presented with our GAAP to non-GAAP reconciliations.

Definitions

Growth rate calculation: growth rates in this report are determined by dividing the difference between current-period results and prior-period results by prior-period results.

Non-GAAP operating earnings: operating earnings/(loss) excluding (1) LIFO charges/(credits), (2) surgical gown recall costs/(income), (3) state opioid assessment related to prior fiscal years, (4) shareholder cooperation agreement costs, (5) restructuring and employee severance, (6) amortization and other acquisition-related costs, (7) impairments and (gain)/loss on disposal of assets, net and (8) litigation (recoveries)/charges, net.

Non-GAAP earnings before income taxes: earnings/(loss) before income taxes excluding (1) LIFO charges/(credits), (2) surgical gown recall costs/(income), (3) state opioid assessment related to prior fiscal years, (4) shareholder cooperation agreement costs, (5) restructuring and employee severance, (6) amortization and other acquisition-related costs, (7) impairments and (gain)/loss on disposal of assets, net, (8) litigation (recoveries)/charges, net, (9) loss on early extinguishment of debt and (10) (gain)/loss on sale of equity interest in naviHealth.

Non-GAAP net earnings attributable to Cardinal Health, Inc.: net earnings/(loss) attributable to Cardinal Health, Inc. excluding (1) LIFO charges/(credits), (2) surgical gown recall costs/(income), (3) state opioid assessment related to prior fiscal years, (4) shareholder cooperation agreement costs, (5) restructuring and employee severance, (6) amortization and other acquisition-related costs, (7) impairments and (gain)/loss on disposal of assets, net, (8) litigation (recoveries)/charges, net, (9) loss on early extinguishment of debt and (10) (gain)/loss on sale of equity interest in naviHealth, each net of tax.

17 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| Explanation and Reconciliation of Non-GAAP Financial Measures | ||||||||

Non-GAAP effective tax rate: provision for income taxes adjusted for the tax impacts of (1) LIFO charges/(credits), (2) surgical gown recall costs/(income), (3) state opioid assessment related to prior fiscal years, (4) shareholder cooperation agreement costs, (5) restructuring and employee severance, (6) amortization and other acquisition-related costs, (7) impairments and (gain)/loss on disposal of assets, net, (8) litigation (recoveries)/charges, net, (9) loss on early extinguishment of debt and (10) (gain)/loss on sale of equity interest in naviHealth divided by (earnings before income taxes adjusted for the ten items above).

Non-GAAP diluted earnings per share attributable to Cardinal Health, Inc.: non-GAAP net earnings attributable to Cardinal Health, Inc. divided by diluted weighted-average shares outstanding.

18 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| Explanation and Reconciliation of Non-GAAP Financial Measures | ||||||||

GAAP to Non-GAAP Reconciliation

| (in millions, except per common share amounts) | Operating Earnings/(Loss) | Operating Earnings Growth Rate | Earnings/(Loss) Before Income Taxes | Provision for Income Taxes | Net Earnings/(Loss)1 | Net Earnings1 Growth Rate | Diluted EPS1,2 | Diluted EPS1 Growth Rate | ||||||||||||||||||

| Three Months Ended March 31, 2023 | ||||||||||||||||||||||||||

| GAAP | $ | 572 | N.M. | $ | 544 | $ | 197 | $ | 345 | N.M. | $ | 1.34 | N.M. | |||||||||||||

| Restructuring and employee severance | 16 | 16 | 4 | 12 | 0.05 | |||||||||||||||||||||

| Amortization and other acquisition-related costs | 74 | 74 | 19 | 55 | 0.21 | |||||||||||||||||||||

Impairments and (gain)/loss on disposal of assets, net 3 | 20 | 20 | (69) | 89 | 0.35 | |||||||||||||||||||||

| Litigation (recoveries)/charges, net | (76) | (76) | (22) | (54) | (0.21) | |||||||||||||||||||||

| Non-GAAP | $ | 606 | 11 | % | $ | 578 | $ | 129 | $ | 447 | 11 | % | $ | 1.74 | 20 | % | ||||||||||

| Three Months Ended March 31, 2022 | ||||||||||||||||||||||||||

| GAAP | $ | (97) | N.M. | $ | (137) | $ | 1,253 | $ | (1,391) | N.M. | $ | (5.05) | N.M. | |||||||||||||

| Restructuring and employee severance | 31 | 31 | 8 | 23 | 0.08 | |||||||||||||||||||||

| Amortization and other acquisition-related costs | 79 | 79 | 20 | 59 | 0.21 | |||||||||||||||||||||

Impairments and (gain)/loss on disposal of assets, net 3 | 471 | 471 | (1,189) | 1,660 | 6.03 | |||||||||||||||||||||

Litigation (recoveries)/charges, net 4 | 61 | 61 | 10 | 51 | 0.18 | |||||||||||||||||||||

| (Gain)/Loss on sale of equity interest in naviHealth | — | (1) | — | (1) | — | |||||||||||||||||||||

| Non-GAAP | $ | 545 | (21) | % | $ | 504 | $ | 101 | $ | 402 | (11) | % | $ | 1.45 | (5) | % | ||||||||||

| Nine Months Ended March 31, 2023 | ||||||||||||||||||||||||||

GAAP | $ | 590 | N.M. | $ | 517 | $ | 189 | $ | 325 | N.M. | $ | 1.23 | N.M. | |||||||||||||

| State opioid assessment related to prior fiscal years | (6) | (6) | (2) | (4) | 0.02 | |||||||||||||||||||||

| Shareholder cooperation agreement costs | 8 | 8 | 2 | 6 | (0.02) | |||||||||||||||||||||

| Restructuring and employee severance | 62 | 62 | 14 | 48 | 0.18 | |||||||||||||||||||||

| Amortization and other acquisition-related costs | 216 | 216 | 56 | 160 | 0.61 | |||||||||||||||||||||

Impairments and (gain)/loss on disposal of assets, net 3 | 883 | 883 | 138 | 745 | 2.82 | |||||||||||||||||||||

| Litigation (recoveries)/charges, net | (256) | (256) | (98) | (158) | (0.60) | |||||||||||||||||||||

Non-GAAP | $ | 1,497 | (3) | % | $ | 1,424 | $ | 299 | $ | 1,122 | (1) | % | $ | 4.24 | 6 | % | ||||||||||

| Nine Months Ended March 31, 2022 | ||||||||||||||||||||||||||

| GAAP | $ | (632) | N.M. | $ | (741) | $ | 328 | $ | (1,071) | N.M. | $ | (3.82) | N.M. | |||||||||||||

| Surgical gown recall costs/(income) | 1 | 1 | — | 1 | — | |||||||||||||||||||||

| Restructuring and employee severance | 56 | 56 | 14 | 42 | 0.15 | |||||||||||||||||||||

| Amortization and other acquisition-related costs | 237 | 237 | 61 | 176 | 0.63 | |||||||||||||||||||||

Impairments and (gain)/loss on disposal of assets, net 3 | 1,764 | 1,764 | (119) | 1,883 | 6.71 | |||||||||||||||||||||

Litigation (recoveries)/charges, net 4,5 | 113 | 113 | 19 | 94 | 0.33 | |||||||||||||||||||||

| Loss on early extinguishment of debt | — | 10 | 3 | 7 | 0.03 | |||||||||||||||||||||

| (Gain)/Loss on sale of equity interest in naviHealth | — | (2) | — | (2) | — | |||||||||||||||||||||

| Non-GAAP | $ | 1,540 | (20) | % | $ | 1,438 | $ | 306 | $ | 1,131 | (20) | % | $ | 4.01 | (16) | % | ||||||||||

19 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| Explanation and Reconciliation of Non-GAAP Financial Measures | ||||||||

1 Attributable to Cardinal Health, Inc.

2 For the three and nine months ended March 31, 2022, GAAP diluted EPS and the EPS impact from the GAAP to non-GAAP per share reconciling items are calculated using a weighted average of 275 million and 281 million common shares, respectively, which excludes potentially dilutive securities from the denominator due to their anti-dilutive effects resulting from our GAAP net loss for the periods. For the three and nine months ended March 31, 2022, non-GAAP diluted EPS is calculated using a weighted average of 277 million and 282 million common shares, respectively, which includes potentially dilutive shares.

3 Impairments and (gain)/loss on disposal of assets, net included pre-tax goodwill impairment charges related to the Medical segment of $863 million recorded during the nine months ended March 31, 2023. For fiscal 2023, the estimated net tax benefit related to the impairments is $68 million and is included in the annual effective tax rate. As a result, the amount of tax expense recognized increased approximately by an incremental $74 million during the three months ended March 31, 2023. The incremental interim tax benefit recognized during the nine months ended March 31, 2023 was $66 million and will reverse in the fourth quarter of the fiscal year.

During the three and nine months ended March 31, 2022, impairments and (gain)/loss on disposal of assets, net included pre-tax goodwill impairment charges of $474 million and $1.8 billion, respectively, related to the Medical segment. For fiscal 2022, the estimated net tax benefit related to the impairment was $126 million and was included in the annual effective tax rate. As a result, the amount of tax expense recognized during the three and nine months ended March 31, 2022 increased approximately by an incremental $1.2 billion and $180 million, respectively, and lowered the provision for income taxes during the fourth quarter of fiscal 2022 by approximately $180 million.

4 Litigation (recoveries)/charges, net includes a one-time contingent attorney fee of $18 million recorded during the three and nine months ended March 31, 2022 related to the finalization of the settlement agreement (the "Settlement Agreement") resulting in the settlement of the vast majority of opioid lawsuits filed by state and local governmental entities. Due to the unique nature and significance of the Settlement Agreement, and the one-time, contingent nature of the fee, this related fee was included in litigation (recoveries)/charges, net.

5 Litigation (recoveries)/charges, net for the nine months ended March 31, 2022 does not include a $16 million judgement for lost profits related to an ordinary course intellectual property claim, which positively impacted Pharmaceutical segment profit.

.

The sum of the components and certain computations may reflect rounding adjustments.

We apply varying tax rates depending on the item's nature and tax jurisdiction where it is incurred.

20 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| Other | |||||

Quantitative and Qualitative Disclosures About Market Risk

There have been no material changes in the quantitative and qualitative market risk disclosures included in our 2022 Form 10-K since the end of fiscal 2022 through March 31, 2023.

Controls and Procedures

Evaluation of Disclosure Controls and Procedures

We evaluated, with the participation of our principal executive officer and principal financial officer, the effectiveness of our disclosure controls and procedures (as defined in Rule 13a-15(e) under the Securities Exchange Act of 1934 (the "Exchange Act")) as of March 31, 2023. Based on this evaluation, our principal executive officer and principal financial officer have concluded that as of March 31, 2023, our disclosure controls and procedures were effective to provide reasonable assurance that information required to be disclosed in our reports under the Exchange Act is recorded, processed, summarized, and reported within the time periods specified in the SEC rules and forms and that such information is accumulated and communicated to management as appropriate to allow timely decisions regarding required disclosure.

Changes in Internal Control Over Financial Reporting

There were no changes in our internal control over financial reporting during the quarter ended March 31, 2023 that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

21 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| Other | ||||||||

Legal Proceedings

In addition to the proceeding described below, the legal proceedings described in Note 6 of the "Notes to Condensed Consolidated Financial Statements" are incorporated in this "Legal Proceedings" section by reference.

Between June 2019 and January 2020, three purported shareholders filed actions on behalf of Cardinal Health, Inc. in the U.S. District Court for the Southern District of Ohio against certain current and former members of our Board of Directors alleging that the defendants breached their fiduciary duties by failing to effectively monitor Cardinal Health's distribution of controlled substances and approving certain payments of executive compensation. In January, 2020, the court consolidated these derivative cases under the caption In re Cardinal Health, Inc. Derivative Litigation and in March 2020, plaintiffs filed an amended complaint.

In December 2021, the parties reached an agreement in principle to settle this matter and in October 2022, the court entered an order approving the settlement and dismissing the case. This settlement does not include any admission of liability. Under the settlement, in December 2022, Cardinal Health's director and officer liability insurance carriers, on behalf of the defendants, paid Cardinal Health $124 million, less approximately $31 million in attorneys' fees and expenses awarded by the court to plaintiffs' counsel.

22 | Cardinal Health | Q3 Fiscal 2023 Form 10-Q | |||||||

| Other | |||||

Risk Factors

You should carefully consider the information in this Form 10-Q, including the Risk Factors below, and the risk factors discussed in "Risk Factors" and other risks discussed in our 2022 Form 10-K, our Form 10-Q for the quarter ended December 31, 2022 and September 30, 2022, and our other filings with the SEC since June 30, 2022. These risks could materially and adversely affect our results of operations, financial condition, liquidity, and cash flows. Our business also could be affected by risks that we are not presently aware of or that we currently consider immaterial to our operations.

Our business could be affected by activist shareholders.

In September 2022, we entered into a Cooperation Agreement (the "Cooperation Agreement") with Elliott Associates, L.P. and Elliott International, L.P. (together, "Elliott") under which our Board of Directors, among other things, (1) appointed four new independent directors, including a representative from Elliott , and (2) formed an advisory Business Review Committee of the Board, which is tasked with undertaking a comprehensive review of our strategy, portfolio, capital-allocation framework and operations. In May 2023, we extended the term of the Cooperation Agreement until the later of July 15, 2024 or until Elliott's representative ceases to serve on, or resigns from, our Board of Directors.

The Cooperation Agreement may create unintended consequences, such as creating uncertainty about our management, operations or future strategic direction, which could result in the loss of future business opportunities or negatively impact our ability to attract and retain qualified talent. Additionally, implementing any actions recommended by the Business Review Committee and the Board may be costly and time-consuming, may be disruptive to our ongoing business operations and may ultimately be unsuccessful.

It is possible that activist shareholders may, among other things, attempt to effect additional changes and exert influence over our Board of Directors and management or initiate a proxy contest, which may disrupt our operations by diverting the attention of management and the Board and be costly and time-consuming. Any such proxy contests, actions or requests, or the mere public presence of activist shareholders, may cause the market price for our shares to experience volatility, which could be significant.

We could be subject to adverse changes in the tax laws or additional challenges to our tax positions.

We are a large multinational corporation with operations in the United States and many foreign countries. As a result, we are subject to the tax laws of many jurisdictions.

From time to time, proposals are made in the United States and other jurisdictions in which we operate that could adversely affect our tax positions, effective tax rate or tax payments. Specific initiatives that may impact us include possible increases in U.S. or foreign corporate income tax rates or other changes in tax law to raise revenue, the repeal of the LIFO (last-in, first-out) method of inventory accounting for income tax purposes, the establishment or increase in taxation at the U.S. state level on the basis of gross revenues, recommendations of the base erosion and profit shifting project undertaken by the Organization for Economic Cooperation and Development and the European Commission’s investigation

into illegal state aid. In August 2022, the U.S. federal government enacted the Inflation Reduction Act, which imposed a 15 percent corporate minimum tax on certain large corporations and a 1 percent tax on share repurchases after December 31, 2022. These provisions may adversely impact our financial position and results of operations.

Additionally, in connection with the accruals taken in connection with opioid-related lawsuits in fiscal years 2021 and 2020, we recorded net tax benefits of $228 million and $488 million, respectively, reflecting our current assessment of the estimated future deductibility of the amount that may be paid. We have made reasonable estimates and recorded amounts based on management's judgment and our current understanding of the U.S. Tax Cuts and Jobs Act ("Tax Act"); however, these estimates require significant judgment, and it is possible that they could be subject to challenges by the U.S. Internal Revenue Service ("IRS").

The U.S. tax law governing deductibility was changed by the Tax Act. The taxing authorities could challenge our interpretation of the Tax Act or the estimates and assumptions used to assess the future deductibility of these benefits, or tax law could change again. We also regularly review these estimates and assumptions from time to time and adjust our accruals based on our review, resulting in changes in our tax provision/(benefit). The actual amount of tax benefit related to uncertain tax positions may differ materially from these estimates. See Note 7 of the "Notes to Condensed Consolidated Financial Statements" for more information regarding these matters.