UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

For the quarterly period ended September 30, 2023

For the transition period from ___ to ___

Commission file number 1-5837

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address and zip code of principal executive offices)

Registrant’s telephone number, including area code 212 -556-1234

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | |||||||||||||

| Smaller reporting company | Emerging growth company | ||||||||||||||||

If an emerging growth company, indicate by the check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to section 13(a) of the Exchange Act. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

Number of shares of each class of the registrant’s common stock outstanding as of November 3, 2023 (exclusive of treasury shares):

| Class A Common Stock | shares | |||||||

| Class B Common Stock | shares | |||||||

THE NEW YORK TIMES COMPANY

INDEX

| PART I | Financial Information | |||||||||||||||||||

| Item | 1 | Financial Statements | ||||||||||||||||||

Condensed Consolidated Balance Sheets as of September 30, 2023 (unaudited) and December 31, 2022 | ||||||||||||||||||||

| Condensed Consolidated Statements of Operations (unaudited) for the quarters and nine months ended September 30, 2023 and September 25, 2022 | ||||||||||||||||||||

| Condensed Consolidated Statements of Comprehensive Income (unaudited) for the quarters and nine months ended September 30, 2023 and September 25, 2022 | ||||||||||||||||||||

| Condensed Consolidated Statements of Changes In Stockholders’ Equity (unaudited) for the quarters and nine months ended September 30, 2023 and September 25, 2022 | ||||||||||||||||||||

| Condensed Consolidated Statements of Cash Flows (unaudited) for the nine months ended September 30, 2023 and September 25, 2022 | ||||||||||||||||||||

| Notes to the Condensed Consolidated Financial Statements | ||||||||||||||||||||

| Item | 2 | Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||||||||||||||||||

| Item | 3 | Quantitative and Qualitative Disclosures About Market Risk | ||||||||||||||||||

| Item | 4 | Controls and Procedures | ||||||||||||||||||

| PART II | Other Information | |||||||||||||||||||

| Item | 1 | Legal Proceedings | ||||||||||||||||||

| Item | 1A | Risk Factors | ||||||||||||||||||

| Item | 2 | Unregistered Sales of Equity Securities and Use of Proceeds | ||||||||||||||||||

| Item | 5 | Other Information | ||||||||||||||||||

| Item | 6 | Exhibits | ||||||||||||||||||

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

THE NEW YORK TIMES COMPANY

CONDENSED CONSOLIDATED BALANCE SHEETS

(In thousands, except share and per share data)

| September 30, 2023 | December 31, 2022 | |||||||||||||

| (Unaudited) | ||||||||||||||

| Assets | ||||||||||||||

| Current assets | ||||||||||||||

| Cash and cash equivalents | $ | $ | ||||||||||||

| Short-term marketable securities | ||||||||||||||

Accounts receivable (net of allowances of $ | ||||||||||||||

| Prepaid expenses | ||||||||||||||

| Other current assets | ||||||||||||||

| Total current assets | ||||||||||||||

| Other assets | ||||||||||||||

| Long-term marketable securities | ||||||||||||||

Property, plant and equipment (less accumulated depreciation and amortization of $ | ||||||||||||||

| Goodwill | ||||||||||||||

| Intangible assets, net | ||||||||||||||

| Deferred income taxes | ||||||||||||||

| Miscellaneous assets | ||||||||||||||

| Total assets | $ | $ | ||||||||||||

See Notes to Condensed Consolidated Financial Statements.

1

THE NEW YORK TIMES COMPANY

CONDENSED CONSOLIDATED BALANCE SHEETS-(Continued)

(In thousands, except share and per share data)

| September 30, 2023 | December 31, 2022 | |||||||||||||

| (Unaudited) | ||||||||||||||

| Liabilities and stockholders’ equity | ||||||||||||||

| Current liabilities | ||||||||||||||

| Accounts payable | $ | $ | ||||||||||||

| Accrued payroll and other related liabilities | ||||||||||||||

| Unexpired subscriptions revenue | ||||||||||||||

Accrued expenses and other | ||||||||||||||

| Total current liabilities | ||||||||||||||

| Other liabilities | ||||||||||||||

Pension benefits obligation | ||||||||||||||

Postretirement benefits obligation | ||||||||||||||

Other | ||||||||||||||

| Total other liabilities | ||||||||||||||

| Stockholders’ equity | ||||||||||||||

Common stock of $ | ||||||||||||||

Class A – authorized: | ||||||||||||||

Class B – convertible – authorized and issued shares: 2022 – | ||||||||||||||

Additional paid-in capital | ||||||||||||||

Retained earnings | ||||||||||||||

Common stock held in treasury, at cost | ( | ( | ||||||||||||

Accumulated other comprehensive loss, net of income taxes: | ||||||||||||||

Foreign currency translation adjustments | ( | ( | ||||||||||||

Funded status of benefit plans | ( | ( | ||||||||||||

| Net unrealized loss on available-for-sale securities | ( | ( | ||||||||||||

Total accumulated other comprehensive loss, net of income taxes | ( | ( | ||||||||||||

Total New York Times Company stockholders’ equity | ||||||||||||||

Noncontrolling interest | ||||||||||||||

| Total stockholders’ equity | ||||||||||||||

| Total liabilities and stockholders’ equity | $ | $ | ||||||||||||

See Notes to Condensed Consolidated Financial Statements.

2

THE NEW YORK TIMES COMPANY

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

(In thousands, except per share data)

| For the Quarters Ended | For the Nine Months Ended | |||||||||||||||||||||||||

| September 30, 2023 | September 25, 2022 | September 30, 2023 | September 25, 2022 | |||||||||||||||||||||||

| Revenues | ||||||||||||||||||||||||||

| Subscription | $ | $ | $ | $ | ||||||||||||||||||||||

| Advertising | ||||||||||||||||||||||||||

| Other | ||||||||||||||||||||||||||

Total revenues | ||||||||||||||||||||||||||

| Operating costs | ||||||||||||||||||||||||||

| Cost of revenue (excluding depreciation and amortization) | ||||||||||||||||||||||||||

| Sales and marketing | ||||||||||||||||||||||||||

| Product development | ||||||||||||||||||||||||||

| General and administrative | ||||||||||||||||||||||||||

| Depreciation and amortization | ||||||||||||||||||||||||||

| Acquisition-related costs | ||||||||||||||||||||||||||

| Impairment charges | ||||||||||||||||||||||||||

| Multiemployer pension plan liability adjustment | ( | ( | ( | ( | ||||||||||||||||||||||

| Total operating costs | ||||||||||||||||||||||||||

| Operating profit | ||||||||||||||||||||||||||

| Other components of net periodic benefit (income)/costs | ( | ( | ||||||||||||||||||||||||

| Interest income and other, net | ||||||||||||||||||||||||||

| Income before income taxes | ||||||||||||||||||||||||||

| Income tax expense | ||||||||||||||||||||||||||

| Net income | $ | $ | $ | $ | ||||||||||||||||||||||

| Average number of common shares outstanding: | ||||||||||||||||||||||||||

| Basic | ||||||||||||||||||||||||||

| Diluted | ||||||||||||||||||||||||||

| Basic earnings per share attributable to common stockholders | $ | $ | $ | $ | ||||||||||||||||||||||

| Diluted earnings per share attributable to common stockholders | $ | $ | $ | $ | ||||||||||||||||||||||

| Dividends declared per share | $ | $ | $ | $ | ||||||||||||||||||||||

See Notes to Condensed Consolidated Financial Statements.

3

THE NEW YORK TIMES COMPANY

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME/(LOSS)

(Unaudited)

(In thousands)

| For the Quarters Ended | For the Nine Months Ended | |||||||||||||||||||||||||

| September 30, 2023 | September 25, 2022 | September 30, 2023 | September 25, 2022 | |||||||||||||||||||||||

| Net income | $ | $ | $ | $ | ||||||||||||||||||||||

| Other comprehensive income/(loss), before tax: | ||||||||||||||||||||||||||

| Loss on foreign currency translation adjustments | ( | ( | ( | ( | ||||||||||||||||||||||

| Pension and postretirement benefits obligation | ||||||||||||||||||||||||||

| Net unrealized gain/(loss) on available-for-sale securities | ( | ( | ||||||||||||||||||||||||

| Other comprehensive income/(loss), before tax | ( | ( | ||||||||||||||||||||||||

| Income tax expense/(benefit) | ( | ( | ||||||||||||||||||||||||

| Other comprehensive income/(loss), net of tax | ( | ( | ||||||||||||||||||||||||

| Comprehensive income attributable to common stockholders | $ | $ | $ | $ | ||||||||||||||||||||||

See Notes to Condensed Consolidated Financial Statements.

4

THE NEW YORK TIMES COMPANY

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

For the Quarters Ended September 30, 2023 and September 25, 2022

(Unaudited)

(In thousands, except share data)

| Capital Stock - Class A and Class B Common | Additional Paid-in Capital | Retained Earnings | Common Stock Held in Treasury, at Cost | Accumulated Other Comprehensive Loss, Net of Income Taxes | Total New York Times Company Stockholders’ Equity | Non- controlling Interest | Total Stock- holders’ Equity | |||||||||||||||||||

| Balance, June 26, 2022 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | ||||||||||||||||

| Net income | — | — | — | — | — | |||||||||||||||||||||

| Dividends | — | — | ( | — | — | ( | — | ( | ||||||||||||||||||

| Other comprehensive loss | — | — | — | — | ( | ( | — | ( | ||||||||||||||||||

| Issuance of stock-based awards, net of withholding taxes: | ||||||||||||||||||||||||||

Restricted stock units vested – | ( | — | — | — | ( | — | ( | |||||||||||||||||||

Share repurchases – | — | — | — | ( | — | ( | — | ( | ||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | |||||||||||||||||||||

| Balance, September 25, 2022 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | ||||||||||||||||

| Balance, June 30, 2023 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | ||||||||||||||||

| Net income | — | — | — | — | — | |||||||||||||||||||||

| Dividends | — | — | ( | — | — | ( | — | ( | ||||||||||||||||||

| Other comprehensive income | — | — | — | — | — | |||||||||||||||||||||

| Issuance of stock-based awards, net of withholding taxes: | ||||||||||||||||||||||||||

Restricted stock units vested – | ( | — | — | — | ( | — | ( | |||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | |||||||||||||||||||||

| Balance, September 30, 2023 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | ||||||||||||||||

5

THE NEW YORK TIMES COMPANY

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

For the Nine Months Ended September 30, 2023 and September 25, 2022

(Unaudited)

(In thousands, except share data)

| Capital Stock - Class A and Class B Common | Additional Paid-in Capital | Retained Earnings | Common Stock Held in Treasury, at Cost | Accumulated Other Comprehensive Loss, Net of Income Taxes | Total New York Times Company Stockholders’ Equity | Non- controlling Interest | Total Stock- holders’ Equity | |||||||||||||||||||

| Balance, December 26, 2021 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | ||||||||||||||||

| Net income | — | — | — | — | — | |||||||||||||||||||||

| Dividends | — | — | ( | — | — | ( | — | ( | ||||||||||||||||||

| Other comprehensive loss | ( | ( | ( | |||||||||||||||||||||||

| Issuance of stock-based awards, net of withholding taxes: | ||||||||||||||||||||||||||

Stock options – | — | — | — | — | — | |||||||||||||||||||||

Restricted stock units vested – | ( | — | — | — | ( | — | ( | |||||||||||||||||||

Performance-based awards – | ( | — | — | — | ( | — | ( | |||||||||||||||||||

Share repurchases – | — | — | — | ( | — | ( | — | ( | ||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | |||||||||||||||||||||

| Balance, September 25, 2022 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | ||||||||||||||||

| Balance, December 31, 2022 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | ||||||||||||||||

| Net income | — | — | — | — | — | |||||||||||||||||||||

| Dividends | — | — | ( | — | — | ( | — | ( | ||||||||||||||||||

| Other comprehensive income | — | — | — | — | — | |||||||||||||||||||||

| Issuance of stock-based awards, net of withholding taxes: | ||||||||||||||||||||||||||

Restricted stock units vested – | ( | — | — | — | ( | — | ( | |||||||||||||||||||

Performance-based awards – | ( | — | — | — | ( | — | ( | |||||||||||||||||||

Share repurchases – | — | — | — | ( | — | ( | — | ( | ||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | |||||||||||||||||||||

| Balance, September 30, 2023 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | ||||||||||||||||

6

THE NEW YORK TIMES COMPANY

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(In thousands)

| For the Nine Months Ended | ||||||||||||||

| September 30, 2023 | September 25, 2022 | |||||||||||||

| Cash flows from operating activities | ||||||||||||||

| Net income | $ | $ | ||||||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||||||||

| Depreciation and amortization | ||||||||||||||

| Amortization of right of use asset | ||||||||||||||

| Stock-based compensation expense | ||||||||||||||

| Multiemployer pension plan liability adjustment | ( | ( | ||||||||||||

| Impairment charges | ||||||||||||||

| Gain on sale of land | ( | |||||||||||||

| Change in long-term retirement benefit obligations | ( | ( | ||||||||||||

| Contingent consideration fair value adjustment | ||||||||||||||

| Other – net | ||||||||||||||

| Changes in operating assets and liabilities, net of business acquisitions: | ||||||||||||||

| Accounts receivable – net | ||||||||||||||

| Other assets | ( | |||||||||||||

| Accounts payable, accrued payroll and other liabilities | ( | ( | ||||||||||||

| Unexpired subscriptions | ||||||||||||||

| Net cash provided by operating activities | ||||||||||||||

| Cash flows from investing activities | ||||||||||||||

| Purchases of marketable securities | ( | ( | ||||||||||||

| Maturities of marketable securities | ||||||||||||||

| Business acquisitions, net of cash acquired | ( | |||||||||||||

| Sales of investments – net | ( | |||||||||||||

| Capital expenditures | ( | ( | ||||||||||||

| Other – net | ||||||||||||||

| Net cash used in investing activities | ( | ( | ||||||||||||

| Cash flows from financing activities | ||||||||||||||

| Long-term obligations: | ||||||||||||||

| Dividends paid | ( | ( | ||||||||||||

| Payment of contingent consideration | ( | ( | ||||||||||||

| Capital shares: | ||||||||||||||

| Proceeds from stock option exercises | ||||||||||||||

| Repurchases | ( | ( | ||||||||||||

| Share-based compensation tax withholding | ( | ( | ||||||||||||

| Net cash used in financing activities | ( | ( | ||||||||||||

| Net increase/(decrease) in cash, cash equivalents and restricted cash | ( | |||||||||||||

| Effect of exchange rate changes on cash | ( | ( | ||||||||||||

| Cash, cash equivalents and restricted cash at the beginning of the period | ||||||||||||||

| Cash, cash equivalents and restricted cash at the end of the period | $ | $ | ||||||||||||

See Notes to Condensed Consolidated Financial Statements.

7

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

NOTE 1. BASIS OF PRESENTATION

In the opinion of management of The New York Times Company (the “Company”), the Condensed Consolidated Financial Statements present fairly the financial position of the Company as of September 30, 2023, and December 31, 2022, and the results of operations, changes in stockholders’ equity and cash flows of the Company for the periods ended September 30, 2023, and September 25, 2022. The Company and its consolidated subsidiaries are referred to collectively as “we,” “us” or “our.” All adjustments necessary for a fair presentation have been included and are of a normal and recurring nature. All significant intercompany accounts and transactions have been eliminated in consolidation. The financial statements were prepared in accordance with the requirements of the United States Securities and Exchange Commission (“SEC”) for interim reporting. As permitted under those rules, certain notes or other financial information that are normally required by accounting principles generally accepted in the United States of America (“GAAP”) have been condensed or omitted from these interim financial statements. These financial statements, therefore, should be read in conjunction with the Consolidated Financial Statements and related Notes included in our Annual Report on Form 10-K for the year ended December 31, 2022. Due to the seasonal nature of our business, operating results for the interim periods are not necessarily indicative of a full year’s operations. The third quarter of 2023 included an additional day compared with the third quarter of 2022 as a result of the change in the Company’s fiscal year to the calendar year.

The Company has two reportable segments: The New York Times Group (“NYTG”) and The Athletic.

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in our Condensed Consolidated Financial Statements. Actual results could differ from these estimates.

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

As of September 30, 2023, our significant accounting policies, which are detailed in our Annual Report on Form 10-K for the year ended December 31, 2022, have not changed.

NOTE 3. REVENUE

We generate revenues principally from subscriptions and advertising.

Subscription revenues consist of revenues from subscriptions to our digital and print products (which include our news product, as well as The Athletic and our Cooking, Games and Wirecutter products), and single-copy and bulk sales of our print products. Subscription revenues are based on both the number of copies of the printed newspaper sold and digital-only subscriptions, and the rates charged to the respective customers.

Advertising revenue is generated principally from advertisers (such as technology, financial and luxury goods companies) promoting products, services or brands on digital platforms in the form of display ads, audio and video, and in print in the form of column-inch ads. Advertising revenue is generated primarily from offerings sold directly to marketers by our advertising sales teams. A smaller proportion of our total advertising revenues is generated through open-market programmatic auctions run by third-party ad exchanges. Advertising revenue is primarily determined by the volume (e.g., impressions), rate and mix of advertisements. Digital advertising includes our core digital advertising business and other digital advertising. Our core digital advertising business includes direct-sold website, mobile application, podcast, email and video advertisements. Direct-sold display advertising, a component of core digital advertising, includes offerings on websites and mobile applications sold directly to marketers by our advertising sales teams. Other digital advertising includes open-market programmatic advertising and creative services fees. Print advertising includes revenue from column-inch ads and classified advertising as well as preprinted advertising, also known as freestanding inserts. NYTG has revenue from all categories discussed above.

8

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

The Athletic has revenue from direct-sold display advertising, podcast, email and video advertisements and open-market programmatic advertising. There is no print advertising revenue generated from The Athletic.

Other revenues primarily consist of revenues from licensing, Wirecutter affiliate referrals, commercial printing, the leasing of floors in the New York headquarters building located at 620 Eighth Avenue, New York, New York (the “Company Headquarters”), television and film, our live events business, retail commerce and our student subscription sponsorship program.

Subscription, advertising and other revenues were as follows:

| For the Quarters Ended | For the Nine Months Ended | |||||||||||||||||||||||||||||||||||||||||||||||||

| (In thousands) | September 30, 2023 | As % of total | September 25, 2022 | As % of total | September 30, 2023 | As % of total | September 25, 2022 | As % of total | ||||||||||||||||||||||||||||||||||||||||||

| Subscription | $ | % | $ | % | $ | % | $ | % | ||||||||||||||||||||||||||||||||||||||||||

| Advertising | % | % | % | % | ||||||||||||||||||||||||||||||||||||||||||||||

Other (1) | % | % | % | % | ||||||||||||||||||||||||||||||||||||||||||||||

Total | $ | % | $ | % | $ | % | $ | % | ||||||||||||||||||||||||||||||||||||||||||

(1) Other revenues include building rental revenue, which is not under the scope of Revenue from Contracts with Customers (Topic 606). Building rental revenue was $6.8 million and $7.3 million for the third quarters of 2023 and 2022, respectively, and $20.5 million and $21.5 million for the first nine months of 2023 and 2022, respectively.

The following table summarizes digital and print subscription revenues, which are components of subscription revenues above, for the third quarters and first nine months ended September 30, 2023, and September 25, 2022:

| For the Quarters Ended | For the Nine Months Ended | |||||||||||||||||||||||||||||||||||||||||||||||||

| (In thousands) | September 30, 2023 | As % of total | September 25, 2022 | As % of total | September 30, 2023 | As % of total | September 25, 2022 | As % of total | ||||||||||||||||||||||||||||||||||||||||||

Digital-only subscription revenues(1) | $ | % | $ | % | $ | % | $ | % | ||||||||||||||||||||||||||||||||||||||||||

Print subscription revenues(2) | % | % | % | % | ||||||||||||||||||||||||||||||||||||||||||||||

| Total subscription revenues | $ | % | $ | % | $ | % | $ | % | ||||||||||||||||||||||||||||||||||||||||||

(1) Includes revenue from bundled and standalone subscriptions to our news product, as well as to The Athletic and to our Cooking, Games and Wirecutter products. | ||||||||||||||||||||||||||||||||||||||||||||||||||

(2) Includes domestic home-delivery subscriptions, which include access to our digital products. Also includes single-copy, NYT International and Other subscription revenues. | ||||||||||||||||||||||||||||||||||||||||||||||||||

The following table summarizes digital and print advertising revenues, which are components of advertising revenues above, for the third quarters and first nine months ended September 30, 2023, and September 25, 2022:

| For the Quarters Ended | For the Nine Months Ended | |||||||||||||||||||||||||||||||||||||||||||||||||

| (In thousands) | September 30, 2023 | As % of total | September 25, 2022 | As % of total | September 30, 2023 | As % of total | September 25, 2022 | As % of total | ||||||||||||||||||||||||||||||||||||||||||

| Advertising revenues: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Digital | $ | % | $ | % | $ | % | $ | % | ||||||||||||||||||||||||||||||||||||||||||

| % | % | % | % | |||||||||||||||||||||||||||||||||||||||||||||||

| Total advertising | $ | % | $ | % | $ | % | $ | % | ||||||||||||||||||||||||||||||||||||||||||

Performance Obligations

We have remaining performance obligations related to digital archive and other licensing and certain advertising contracts. As of September 30, 2023, the aggregate amount of the transaction price allocated to the remaining performance obligations for contracts with a duration greater than one year was approximately $194 million. The Company will recognize this revenue as performance obligations are satisfied. We expect that approximately $23 million, $74 million and $97 million will be recognized in the remainder of 2023, 2024 and thereafter through 2028, respectively.

9

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Unexpired Subscriptions

Payments for subscriptions are typically due upfront and the revenue is recognized ratably over the subscription period. The proceeds are recorded within Unexpired subscriptions revenue in the Condensed Consolidated Balance Sheet. Total unexpired subscriptions as of December 31, 2022, were $155.9 million, of which approximately $149 million was recognized as revenues during the nine months ended September 30, 2023.

Contract Assets

As of September 30, 2023, and December 31, 2022, the Company had $3.7

NOTE 4. MARKETABLE SECURITIES

The Company accounts for its marketable securities as available for sale (“AFS”). Pre-tax net unrealized losses in Accumulated other comprehensive income (“AOCI”) were $5.4 million and $11.4 million as of September 30, 2023, and December 31, 2022, respectively.

The following tables present the amortized cost, gross unrealized gains and losses, and fair market value of our AFS securities as of September 30, 2023, and December 31, 2022:

| September 30, 2023 | ||||||||||||||||||||||||||

| (In thousands) | Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | ||||||||||||||||||||||

| Short-term AFS securities | ||||||||||||||||||||||||||

| Corporate debt securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

| U.S. Treasury securities | ( | |||||||||||||||||||||||||

| U.S. governmental agency securities | ( | |||||||||||||||||||||||||

| Total short-term AFS securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

| Long-term AFS securities | ||||||||||||||||||||||||||

| U.S. Treasury securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

| Corporate debt securities | ( | |||||||||||||||||||||||||

| U.S. governmental agency securities | ( | |||||||||||||||||||||||||

| Total long-term AFS securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

| December 31, 2022 | ||||||||||||||||||||||||||

| (In thousands) | Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | ||||||||||||||||||||||

| Short-term AFS securities | ||||||||||||||||||||||||||

| Corporate debt securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

| U.S. Treasury securities | ( | |||||||||||||||||||||||||

| U.S. governmental agency securities | ( | |||||||||||||||||||||||||

| Municipal securities | ( | |||||||||||||||||||||||||

| Total short-term AFS securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

| Long-term AFS securities | ||||||||||||||||||||||||||

| U.S. Treasury securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

| Corporate debt securities | ( | |||||||||||||||||||||||||

| U.S. governmental agency securities | ( | |||||||||||||||||||||||||

| Total long-term AFS securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

10

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

The following tables represent the AFS securities as of September 30, 2023, and December 31, 2022, that were in an unrealized loss position for which an allowance for credit losses has not been recorded, aggregated by investment category and the length of time that individual securities have been in a continuous unrealized loss position:

| September 30, 2023 | ||||||||||||||||||||||||||||||||||||||

| Less than 12 Months | 12 Months or Greater | Total | ||||||||||||||||||||||||||||||||||||

| (In thousands) | Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | ||||||||||||||||||||||||||||||||

| Short-term AFS securities | ||||||||||||||||||||||||||||||||||||||

| Corporate debt securities | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

| U.S. Treasury securities | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| U.S. governmental agency securities | ( | ( | ||||||||||||||||||||||||||||||||||||

| Total short-term AFS securities | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

| Long-term AFS securities | ||||||||||||||||||||||||||||||||||||||

| U.S. Treasury securities | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| U.S. governmental agency securities | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| Total long-term AFS securities | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

| December 31, 2022 | ||||||||||||||||||||||||||||||||||||||

| Less than 12 Months | 12 Months or Greater | Total | ||||||||||||||||||||||||||||||||||||

| (In thousands) | Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | ||||||||||||||||||||||||||||||||

| Short-term AFS securities | ||||||||||||||||||||||||||||||||||||||

| Corporate debt securities | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

| U.S. Treasury securities | ( | ( | ||||||||||||||||||||||||||||||||||||

| U.S. governmental agency securities | ( | ( | ||||||||||||||||||||||||||||||||||||

| Municipal securities | ( | ( | ||||||||||||||||||||||||||||||||||||

| Total short-term AFS securities | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

| Long-term AFS securities | ||||||||||||||||||||||||||||||||||||||

| U.S. Treasury securities | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| U.S. governmental agency securities | ( | ( | ||||||||||||||||||||||||||||||||||||

| Total long-term AFS securities | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

We assess AFS securities on a quarterly basis or more often if a potential loss-triggering event occurs.

As of September 30, 2023, and December 31, 2022, we did not intend to sell and it was not likely that we would be required to sell these investments before recovery of their amortized cost basis, which may be at maturity. Unrealized losses related to these investments are primarily due to interest rate fluctuations as opposed to changes in credit quality. Therefore, as of September 30, 2023, and December 31, 2022, we have recognized no

11

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

NOTE 5. GOODWILL AND INTANGIBLES

Goodwill and Intangibles

The changes in the carrying amount of goodwill as of September 30, 2023, and since December 26, 2021, were as follows:

| (In thousands) | NYTG | The Athletic | Total | |||||||||||||||||

| Balance as of December 26, 2021 | $ | $ | $ | |||||||||||||||||

| Foreign currency translation | ( | ( | ||||||||||||||||||

| Acquisition of The Athletic Media Company | ||||||||||||||||||||

| Measurement period adjustments | ||||||||||||||||||||

| Balance as of December 31, 2022 | ||||||||||||||||||||

| Foreign currency translation | ( | ( | ||||||||||||||||||

| Balance as of September 30, 2023 | $ | $ | $ | |||||||||||||||||

The foreign currency translation line item reflects changes in goodwill resulting from fluctuating exchange rates related to the consolidation of certain international subsidiaries.

| (In thousands) | Gross Book Value | Accumulated Amortization | Net Book Value | Remaining Weighted-Average Useful Life (Years) | ||||||||||||||||||||||

| Trademark | $ | $ | ( | $ | ||||||||||||||||||||||

| Existing subscriber base | ( | |||||||||||||||||||||||||

| Developed technology | ( | |||||||||||||||||||||||||

| Content archive | ( | |||||||||||||||||||||||||

| Total finite-lived intangibles | $ | $ | ( | $ | ||||||||||||||||||||||

Amortization expense for intangible assets included in Depreciation and amortization in our Condensed Consolidated Statements of Operations was $7.3 million and $7.4 million for the third quarters of 2023 and 2022, respectively, and $22.0 million and $19.7 million for the first nine months of 2023 and 2022, respectively. The estimated aggregate amortization expense for the remainder of 2023 and each of the following fiscal years ending December 31 is presented below:

| (In thousands) | ||||||||

| Remainder of 2023 | $ | |||||||

| 2024 | ||||||||

| 2025 | ||||||||

| 2026 | ||||||||

| 2027 | ||||||||

| Thereafter | ||||||||

| Total amortization expense | $ | |||||||

The aggregate carrying amount of intangible assets of $292.8 million, which includes an indefinite-lived intangible of $2.5 million, is included in Intangible assets, net in our Condensed Consolidated Balance Sheet as of September 30, 2023.

12

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

NOTE 6. INVESTMENTS

Non-Marketable Equity Securities

Our non-marketable equity securities are investments in privately held companies/funds without readily determinable market values. Gains and losses on non-marketable securities revalued, sold or impaired are recognized in Interest income and other, net in our Condensed Consolidated Statements of Operations.

As of September 30, 2023, and December 31, 2022, non-marketable equity securities included in Miscellaneous assets in our Condensed Consolidated Balance Sheets had a carrying value of $29.7 million and $29.8 million, respectively.

NOTE 7. OTHER

Capitalized Computer Software Costs

Amortization of capitalized computer software costs included in Depreciation and amortization in our Condensed Consolidated Statements of Operations was $2.1 million and $2.0 million for the third quarters of 2023 and 2022, respectively, and $5.7 million and $5.9 million for the first nine months of 2023 and 2022, respectively.

Interest income and other, net

Interest income and other, net, as shown in the accompanying Condensed Consolidated Statements of Operations, was as follows:

| For the Quarters Ended | For the Nine Months Ended | |||||||||||||||||||||||||

| (In thousands) | September 30, 2023 | September 25, 2022 | September 30, 2023 | September 25, 2022 | ||||||||||||||||||||||

| Interest income | $ | $ | $ | $ | ||||||||||||||||||||||

Gain on the sale of land (1) | ||||||||||||||||||||||||||

| Interest expense | ( | ( | ( | ( | ||||||||||||||||||||||

| Total interest income and other, net | $ | $ | $ | $ | ||||||||||||||||||||||

(1) On December 9, 2020, we entered into an agreement to lease and subsequently sell approximately four acres of land at our printing and distribution facility in College Point, N.Y., subject to certain conditions. The lease commenced on April 11, 2022. At the time of the lease expiration in February 2025, we will sell the parcel to the lessee for approximately $36 million. The transaction is accounted for as a sales-type lease and as a result, we recognized a gain of approximately $34 million (net of commissions) at the time of lease commencement.

Restricted Cash

A reconciliation of cash, cash equivalents and restricted cash as of September 30, 2023, and September 25, 2022, from the Condensed Consolidated Balance Sheets to the Condensed Consolidated Statements of Cash Flows is as follows:

| (In thousands) | September 30, 2023 | September 25, 2022 | ||||||||||||

| Reconciliation of cash, cash equivalents and restricted cash | ||||||||||||||

| Cash and cash equivalents | $ | $ | ||||||||||||

| Restricted cash included within miscellaneous assets | ||||||||||||||

| Total cash, cash equivalents and restricted cash shown in the Condensed Consolidated Statements of Cash Flows | $ | $ | ||||||||||||

Substantially all of the amount included in restricted cash is set aside to collateralize workers’ compensation obligations.

13

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Revolving Credit Facility

On July 27, 2022, the Company entered into an amendment and restatement of its previous credit facility that, among other changes, increased the committed amount to $350.0 million and extended the maturity date to July 27, 2027 (as amended and restated, the “Credit Facility”). Certain of the Company’s domestic subsidiaries have guaranteed the Company’s obligations under the Credit Facility. Borrowings under the Credit Facility bear interest at specified rates based on our utilization and consolidated leverage ratio. The Credit Facility contains various customary affirmative and negative covenants. In addition, the Company is obligated to pay a quarterly unused commitment fee at an annual rate of 0.20 %.

As of September 30, 2023, and December 31, 2022, there were no 0.6

Severance Costs

We recognized $3.1 million and $2.0 million in severance costs for the third quarters of 2023 and 2022, respectively, and $7.6 million and $4.7 million for the first nine months of 2023 and 2022, respectively. These costs are recorded in General and administrative costs in our Condensed Consolidated Statements of Operations.

We had a severance liability of $6.9 million and $4.4 million included in Accrued expenses and other in our Condensed Consolidated Balance Sheets as of September 30, 2023, and December 31, 2022, respectively.

Impairment Charges

In September 2023, we recorded a $2.5 million impairment of our Serial podcast indefinite-lived intangible asset. See Note 5 for more details.

In June 2023, we ceased using certain leased office space in Long Island City, New York. As a result, we recorded non-cash impairment charges of $7.6 million and $5.1 million to the right-of-use assets and fixed assets, respectively. The impairment amount was determined by comparing the fair value of the impacted asset group to its carrying value as of the measurement date, as required by ASC 360, Property, Plant and Equipment. The fair value of the asset group was based on estimated sublease income for the affected property, taking into consideration the time we expect it will take to obtain a sublease tenant and the expected applicable discount rates.

NOTE 8. FAIR VALUE MEASUREMENTS

Fair value is the price that would be received upon the sale of an asset or paid upon transfer of a liability in an orderly transaction between market participants at the measurement date. The transaction would be in the principal or most advantageous market for the asset or liability, based on assumptions that a market participant would use in pricing the asset or liability. The fair value hierarchy consists of three levels:

Level 1–quoted prices in active markets for identical assets or liabilities that the reporting entity has the ability to access at the measurement date;

Level 2–inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly; and

Level 3–unobservable inputs for the asset or liability.

14

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Assets/Liabilities Measured and Recorded at Fair Value on a Recurring Basis

The following table summarizes our financial assets and liabilities measured at fair value on a recurring basis as of September 30, 2023, and December 31, 2022:

| (In thousands) | September 30, 2023 | December 31, 2022 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Total | Level 1 | Level 2 | Level 3 | Total | Level 1 | Level 2 | Level 3 | |||||||||||||||||||||||||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||||||||||||||||||||||||||

Short-term AFS securities (1) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Corporate debt securities | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

| U.S Treasury securities | ||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. governmental agency securities | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Municipal securities | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Total short-term AFS securities | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

Long-term AFS securities (1) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Treasury securities | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

| Corporate debt securities | ||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. governmental agency securities | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Total long-term AFS securities | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

| Liabilities: | ||||||||||||||||||||||||||||||||||||||||||||||||||

Deferred compensation (2)(3) | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

Contingent consideration (4) | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

(1) We classified these investments as Level 2 since the fair value is based on market observable inputs for investments with similar terms and maturities.

(2) The deferred compensation liability, included in Other liabilities—other in our Condensed Consolidated Balance Sheets, consists of deferrals under The New York Times Company Deferred Executive Compensation Plan (the “DEC”), a frozen plan that enabled certain eligible executives to elect to defer a portion of their compensation on a pre-tax basis. The deferred amounts are invested at the executives’ option in various mutual funds. The fair value of deferred compensation is based on the mutual fund investments elected by the executives and on quoted prices in active markets for identical assets. Participation in the DEC was frozen effective December 31, 2015.

(3) The Company invests the assets associated with the deferred compensation liability in life insurance products. Our investments in life insurance products are included in Miscellaneous assets in our Condensed Consolidated Balance Sheets, and were $50.6 million as of September 30, 2023, and $48.4 million as of December 31, 2022. The fair value of these assets is measured using the net asset value per share (or its equivalent) and has not been classified in the fair value hierarchy.

(4) The remaining contingent consideration balances (as discussed below) are included in Accrued expenses and other, for the current portion of the liability, and Other non-current liabilities, for the long-term portion of the liability, in our Condensed Consolidated Balance Sheets.

15

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Level 3 Liabilities

The contingent consideration liability is related to the 2020 acquisition of substantially all the assets and certain liabilities of Serial Productions, LLC and represents contingent payments based on the achievement of certain operational targets, as defined in the acquisition agreement, over the five years following the acquisition. The Company estimated the fair value using a probability-weighted discounted cash flow model. The estimate of the fair value of contingent consideration requires subjective assumptions to be made regarding probabilities assigned to operational targets and the discount rate. As the fair value is based on significant unobservable inputs, this is a Level 3 liability.

The following table presents changes in the contingent consideration balances for the third quarters and nine months ended September 30, 2023, and September 25, 2022:

| Quarters Ended | Nine Months Ended | |||||||||||||||||||||||||

| (In thousands) | September 30, 2023 | September 25, 2022 | September 30, 2023 | September 25, 2022 | ||||||||||||||||||||||

Balance at the beginning of the period | $ | $ | $ | $ | ||||||||||||||||||||||

| Payments | ( | ( | ( | |||||||||||||||||||||||

Fair value adjustments (1) | ||||||||||||||||||||||||||

| Contingent consideration at the end of the period | $ | $ | $ | $ | ||||||||||||||||||||||

(1) Fair value adjustments are included in General and administrative costs in our Condensed Consolidated Statements of Operations. | ||||||||||||||||||||||||||

NOTE 9. PENSION AND OTHER POSTRETIREMENT BENEFITS

Pension

Single-Employer Plans

We maintain The New York Times Companies Pension Plan, a frozen single-employer defined benefit pension plan. The Company also jointly sponsors a defined benefit plan with The NewsGuild of New York known as the Guild-Times Adjustable Pension Plan (the “APP”) that continues to accrue active benefits.

We also have a foreign-based pension plan for certain employees (the “foreign plan”). The information for the foreign plan is combined with the information for U.S. non-qualified plans. The benefit obligation of the foreign plan is immaterial to our total benefit obligation.

The components of net periodic pension (income)/cost were as follows:

| For the Quarters Ended | ||||||||||||||||||||||||||||||||||||||

| September 30, 2023 | September 25, 2022 | |||||||||||||||||||||||||||||||||||||

| (In thousands) | Qualified Plans | Non- Qualified Plans | All Plans | Qualified Plans | Non- Qualified Plans | All Plans | ||||||||||||||||||||||||||||||||

| Service cost | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Interest cost | ||||||||||||||||||||||||||||||||||||||

| Expected return on plan assets | ( | ( | ( | ( | ||||||||||||||||||||||||||||||||||

| Amortization of actuarial loss | ||||||||||||||||||||||||||||||||||||||

| Amortization of prior service credit | ( | ( | ( | ( | ||||||||||||||||||||||||||||||||||

| Net periodic pension (income)/cost | $ | ( | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||

16

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

| For the Nine Months Ended | ||||||||||||||||||||||||||||||||||||||

| September 30, 2023 | September 25, 2022 | |||||||||||||||||||||||||||||||||||||

| (In thousands) | Qualified Plans | Non- Qualified Plans | All Plans | Qualified Plans | Non- Qualified Plans | All Plans | ||||||||||||||||||||||||||||||||

| Service cost | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Interest cost | ||||||||||||||||||||||||||||||||||||||

| Expected return on plan assets | ( | ( | ( | ( | ||||||||||||||||||||||||||||||||||

| Amortization of actuarial loss | ||||||||||||||||||||||||||||||||||||||

| Amortization of prior service credit | ( | ( | ( | ( | ||||||||||||||||||||||||||||||||||

| Net periodic pension (income)/cost | $ | ( | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||

During the first nine months of 2023 and 2022, we made pension contributions of $7.7 million and $7.5 million, respectively, to the APP. We expect to make contractual contributions in 2023 of approximately $10 million, which more than satisfy minimum funding requirements.

As part of our strategy to reduce the pension obligations and the resulting impact on our overall financial position, we have offered lump-sum payments to certain former employees participating in both our qualified and non-qualified pension plans. In the third quarter of 2023, the Company extended a voluntary offer to certain former employees who participated in The New York Times Companies Pension Plan to elect immediate lump-sum payments. The election period for this voluntary offer closes on November 14, 2023.

Multiemployer Plans

During the third quarters of 2023 and 2022, we recorded favorable adjustments of $2.3 million and $7.1 million, respectively, related to a reduction to our multiemployer pension plan liability. These adjustments were recorded in Multiemployer pension plan liability adjustment in our Condensed Consolidated Statements of Operations.

Other Postretirement Benefits

The components of net periodic postretirement benefit cost were as follows:

| For the Quarters Ended | For the Nine Months Ended | |||||||||||||||||||||||||

| (In thousands) | September 30, 2023 | September 25, 2022 | September 30, 2023 | September 25, 2022 | ||||||||||||||||||||||

| Service cost | $ | $ | $ | $ | ||||||||||||||||||||||

| Interest cost | ||||||||||||||||||||||||||

| Amortization of actuarial loss | ||||||||||||||||||||||||||

| Amortization of prior service credit | ( | |||||||||||||||||||||||||

| Net periodic postretirement benefit cost | $ | $ | $ | $ | ||||||||||||||||||||||

17

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

NOTE 10. INCOME TAXES

The Company had income tax expense of $16.4 million and $40.2 million in the third quarter and first nine months of 2023, respectively. The Company had income tax expense of $14.2 million and $39.2 million in the third quarter and first nine months of 2022, respectively. The Company’s effective tax rates were 23.4 % and 24.7 % for the third quarter and first nine months of 2023, respectively. The Company’s effective tax rates were 28.0 % and 27.5 % for the third quarter and first nine months of 2022, respectively. The increase in income tax expense in the third quarter and first nine months of 2023 was primarily due to higher income in both periods. The decrease in the effective tax rate in the third quarter and first nine months of 2023 was primarily due to higher federal tax credits for increasing research and development activities in 2023.

Beginning in 2022, the Tax Cuts and Jobs Act of 2017 eliminated the option to deduct research and development expenditures immediately in the year incurred and instead requires taxpayers to capitalize and amortize such expenditures over five years. In 2022, our cash from operations decreased approximately $60 million and our net deferred tax assets increased by a similar amount as a result of this legislation. In 2023, we expect a negative impact on our cash from operations of approximately $31 million. The actual impact on 2023 cash from operations will depend on the amount of research and development costs we incur, on whether Congress modifies or repeals this provision, and on whether new guidance and interpretive rules are issued by the U.S. Treasury, among other factors.

On August 16, 2022, the President signed the Inflation Reduction Act of 2022 (the “IRA”) into law. We do not expect the tax-related provisions of the IRA, which are effective beginning in 2023, to have a material impact on our consolidated financial statements.

NOTE 11. EARNINGS PER SHARE

We compute earnings per share based upon the lower of the two-class method or the treasury stock method. The two-class method is an earnings allocation method used when a company’s capital structure includes either two or more classes of common stock or common stock and participating securities. This method determines earnings per share based on dividends declared on common stock and participating securities (i.e., distributed earnings), as well as participation rights of participating securities in any undistributed earnings.

Earnings per share is computed using both basic shares and diluted shares. The difference between basic and diluted shares is that diluted shares include the dilutive effect of the assumed exercise of outstanding securities. Our stock-settled long-term performance awards and restricted stock units could have a significant impact on diluted shares. The difference between basic and diluted shares was approximately 0.8 million and 0.7 million in the third quarter and first nine months of 2023, respectively, and resulted primarily from the dilutive effect of our stock-based awards. The difference between basic and diluted shares was de minimis in the third quarter and first nine months of 2022, respectively.

Securities that could potentially be dilutive are excluded from the computation of diluted earnings per share when a loss from continuing operations exists or when the exercise price exceeds the market value of our Class A Common Stock because their inclusion would result in an anti-dilutive effect on per share amounts.

There were approximately 0.1 1.6 million and 1.1 million restricted stock units excluded from the computation of diluted earnings per share in the third quarter and first nine months of 2022, respectively, because they were anti-dilutive. There were no

NOTE 12. SUPPLEMENTAL STOCKHOLDERS’ EQUITY INFORMATION

Share Repurchases

In February 2022, the Board of Directors approved a $150.0 million Class A share repurchase program that replaced the previous program, which was approved in 2015. In February 2023, in addition to the remaining 2022 authorization, the Board of Directors approved a $250.0 million Class A share repurchase program. The authorizations provide that shares of Class A Common Stock may be purchased from time to time as market conditions warrant, through open-market purchases, privately negotiated transactions or other means, including Rule 10b5-1 trading plans. We expect to repurchase shares to offset the impact of dilution from our equity compensation program and to return capital to our stockholders. There is no expiration date with respect to these authorizations.

As of September 30, 2023, repurchases under these authorizations totaled approximately $148.6 million (excluding commissions) and approximately $251.4 million remained. During the nine months ended September 30, 2023, repurchases under these authorizations totaled approximately $43.6 million (excluding commissions).

18

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Accumulated Other Comprehensive Income

The following table summarizes the changes in AOCI by component as of September 30, 2023:

| (In thousands) | Foreign Currency Translation Adjustments | Funded Status of Benefit Plans | Net Unrealized Loss on Available-For-Sale Securities | Total Accumulated Other Comprehensive Loss | ||||||||||||||||||||||

| Balance as of December 31, 2022 | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

| Other comprehensive income before reclassifications, before tax | ( | |||||||||||||||||||||||||

| Amounts reclassified from accumulated other comprehensive loss, before tax | ||||||||||||||||||||||||||

| Income tax expense | ( | |||||||||||||||||||||||||

| Net current-period other comprehensive income, net of tax | ( | |||||||||||||||||||||||||

| Balance as of September 30, 2023 | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

The following table summarizes the reclassifications from AOCI for the nine months ended September 30, 2023:

(In thousands) Detail about accumulated other comprehensive loss components | Amounts reclassified from accumulated other comprehensive loss | Affects line item in the statement where net income is presented | ||||||||||||

| Funded status of benefit plans: | ||||||||||||||

Amortization of prior service credit (1) | $ | ( | Other components of net periodic benefit (income)/costs | |||||||||||

Amortization of actuarial loss (1) | Other components of net periodic benefit (income)/costs | |||||||||||||

Total reclassification, before tax (2) | ||||||||||||||

| Income tax expense | Income tax expense | |||||||||||||

| Total reclassification, net of tax | $ | |||||||||||||

(1) These AOCI components are included in the computation of net periodic benefit (income)/cost for pension and other postretirement benefits. See Note 9 for more information. | ||||||||||||||

(2) There were no reclassifications relating to noncontrolling interest for the quarter ended September 30, 2023. | ||||||||||||||

Stock-based Compensation Expense

Total stock-based compensation expense included in the Condensed Consolidated Statements of Operations is as follows:

| For the Quarters Ended | For the Nine Months Ended | |||||||||||||||||||||||||

| (In thousands) | September 30, 2023 | September 25, 2022 | September 30, 2023 | September 25, 2022 | ||||||||||||||||||||||

| Cost of revenue | $ | $ | $ | $ | ||||||||||||||||||||||

| Sales and marketing | ||||||||||||||||||||||||||

| Product development | ||||||||||||||||||||||||||

| General and administrative | ||||||||||||||||||||||||||

| Total stock-based compensation expense | $ | $ | $ | $ | ||||||||||||||||||||||

19

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

NOTE 13. SEGMENT INFORMATION

The Company identifies a business as an operating segment if: (i) it engages in business activities from which it may earn revenues and incur expenses; (ii) its operating results are regularly reviewed by the Company’s President and Chief Executive Officer (who is the Company’s Chief Operating Decision Maker) to make decisions about resources to be allocated to the segment and assess its performance; and (iii) it has available discrete financial information.

Since the acquisition of The Athletic in the first quarter of 2022, the Company has had two reportable segments: NYTG and The Athletic. These segments are evaluated regularly by the Company’s Chief Operating Decision Maker in assessing performance and allocating resources. Management uses adjusted operating profit (loss) by segment in assessing performance and allocating resources. Adjusted operating profit is defined as operating profit before depreciation and amortization, severance, multiemployer pension plan withdrawal costs and special items. Adjusted operating profit for NYTG and The Athletic is presented below, along with a reconciliation to consolidated income before taxes. Asset information by segment is not a measure of performance used by the Company’s Chief Operating Decision Maker. Accordingly, we have not disclosed asset information by segment.

Subscription revenues from and expenses associated with our digital subscription package (or “bundle”) are allocated to NYTG and The Athletic. The Athletic was first introduced into our bundle in June 2022. Therefore, The Athletic’s results for the second quarter of 2022 include bundle revenues and expenses for only part of the quarter, whereas the second quarter of 2023 includes bundle revenues and expenses for the entire quarter.

Prior to April 1, 2023, we allocated bundle revenues first to our digital news product based on its standalone list price and then the remaining bundle revenues were allocated to the other products in the bundle, including The Athletic, based on their relative standalone list prices. Starting April 1, 2023, we allocate 10 % of bundle revenues to The Athletic based on management’s view of The Athletic’s relative value to the bundle, which is derived based on analysis of various metrics, and allocate the remaining bundle revenues to NYTG.

Prior to April 1, 2023, we allocated to NYTG and The Athletic direct variable expenses associated with the bundle, which include credit card fees, third party fees and sales taxes, based on a historical actual percentage of these costs to bundle revenues. Starting April 1, 2023, we allocate 10 % of product development, marketing and subscriber servicing expenses (including the direct variable expenses referenced above) associated with the bundle to The Athletic, and the remaining costs are allocated to NYTG, in each case, in line with the revenues allocations.

For comparison purposes, the Company has recast segment results for the quarters following the second quarter of 2022 to reflect the updated allocation methodology. The second quarter of 2022 was not recast as the change was de minimis for that quarter in light of the timing of the introduction of The Athletic to the bundle.

The results of The Athletic have been included in our Condensed Consolidated Financial Statements beginning February 1, 2022, the date of the acquisition. Results for the first nine months of 2022 included The Athletic for approximately eight months, while results for the first nine months of 2023 included The Athletic for the full nine months.

20

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

The following tables present segment information:

| For the Quarters Ended | For the Nine Months Ended | |||||||||||||||||||||||||||||||||||||

| (In thousands) | September 30, 2023 | September 25, 2022 (1) | % Change | September 30, 2023 | September 25, 2022 (1) | % Change | ||||||||||||||||||||||||||||||||

| Revenues | ||||||||||||||||||||||||||||||||||||||

| NYTG | $ | $ | % | $ | $ | % | ||||||||||||||||||||||||||||||||

| The Athletic | % | % | ||||||||||||||||||||||||||||||||||||

| Total revenues | $ | $ | % | $ | $ | % | ||||||||||||||||||||||||||||||||

| Adjusted operating profit (loss) | ||||||||||||||||||||||||||||||||||||||

| NYTG | $ | $ | % | $ | $ | % | ||||||||||||||||||||||||||||||||

| The Athletic | ( | ( | ( | % | ( | ( | ( | % | ||||||||||||||||||||||||||||||

| Total adjusted operating profit | $ | $ | % | $ | $ | % | ||||||||||||||||||||||||||||||||

| Less: | ||||||||||||||||||||||||||||||||||||||

| Other components of net periodic benefit costs | ( | * | ( | * | ||||||||||||||||||||||||||||||||||

| Depreciation and amortization | ( | % | % | |||||||||||||||||||||||||||||||||||

| Severance | % | % | ||||||||||||||||||||||||||||||||||||

| Multiemployer pension plan withdrawal costs | % | % | ||||||||||||||||||||||||||||||||||||

| Acquisition-related costs | — | * | ||||||||||||||||||||||||||||||||||||

| Impairment charges | * | * | ||||||||||||||||||||||||||||||||||||

| Multiemployer pension plan liability adjustment | ( | ( | ( | % | ( | ( | ( | % | ||||||||||||||||||||||||||||||

| Add: | ||||||||||||||||||||||||||||||||||||||

| Interest income and other, net | * | ( | % | |||||||||||||||||||||||||||||||||||

| Income before income taxes | $ | $ | % | $ | $ | % | ||||||||||||||||||||||||||||||||

(1) Recast to reflect updated bundle allocation methodology. | ||||||||||||||||||||||||||||||||||||||

| * Represents a change equal to or in excess of 100% or not meaningful. | ||||||||||||||||||||||||||||||||||||||

21

THE NEW YORK TIMES COMPANY

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

| Revenues detail by segment | ||||||||||||||||||||||||||||||||||||||

| For the Quarters Ended | For the Nine Months Ended | |||||||||||||||||||||||||||||||||||||

| (In thousands) | September 30, 2023 | September 25, 2022 (1) | % Change | September 30, 2023 | September 25, 2022 (1) | % Change | ||||||||||||||||||||||||||||||||

| NYTG | ||||||||||||||||||||||||||||||||||||||

| Subscription | $ | $ | % | $ | $ | % | ||||||||||||||||||||||||||||||||

| Advertising | % | ( | % | |||||||||||||||||||||||||||||||||||

| Other | % | % | ||||||||||||||||||||||||||||||||||||

| Total | $ | $ | % | $ | $ | % | ||||||||||||||||||||||||||||||||

| The Athletic | ||||||||||||||||||||||||||||||||||||||

| Subscription | $ | $ | % | $ | $ | % | ||||||||||||||||||||||||||||||||

| Advertising | * | * | ||||||||||||||||||||||||||||||||||||

| Other | * | * | ||||||||||||||||||||||||||||||||||||

| Total | $ | $ | % | $ | $ | % | ||||||||||||||||||||||||||||||||

| The New York Times Company | ||||||||||||||||||||||||||||||||||||||

| Subscription | $ | $ | % | $ | $ | % | ||||||||||||||||||||||||||||||||

| Advertising | % | ( | % | |||||||||||||||||||||||||||||||||||

| Other | % | % | ||||||||||||||||||||||||||||||||||||

| Total | $ | $ | % | $ | $ | % | ||||||||||||||||||||||||||||||||

(1) Recast to reflect updated bundle allocation methodology. | ||||||||||||||||||||||||||||||||||||||

| * Represents a change equal to or in excess of 100% or not meaningful. | ||||||||||||||||||||||||||||||||||||||

NOTE 14. CONTINGENT LIABILITIES

Legal Proceedings

We are involved in various legal actions incidental to our business that are now pending against us. These actions generally have damage claims that are greatly in excess of the payments, if any, that we would be required to pay if we lost or settled the cases. We record a liability for legal claims when a loss is probable and the amount can be reasonably estimated. Although the Company cannot predict the outcome of these matters, no amount of loss in excess of recorded amounts as of September 30, 2023, is believed to be reasonably possible.

NOTE 15. SUBSEQUENT EVENTS

22

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

EXECUTIVE OVERVIEW

We are a global media organization focused on creating, collecting and distributing high-quality news and information that helps our audience understand and engage with the world. We believe that our original, independent and high-quality reporting, storytelling and journalistic excellence set us apart from other news organizations and are at the heart of what makes our journalism worth paying for.

We generate revenues principally from the sale of subscriptions and advertising. Subscription revenues consist of revenues from standalone subscriptions to our digital products, our digital subscription package (or “bundle”) and subscriptions to and single-copy and bulk sales of our print products. Advertising revenue is derived from the sale of our advertising products and services. Other revenues primarily consist of revenues from licensing, Wirecutter affiliate referrals, commercial printing, the leasing of floors in our headquarters (the “Company Headquarters”), television and film, our live events business, retail commerce and our student subscription sponsorship program.

Our main operating costs are employee-related costs.

Beginning with the third quarter of 2023, we have updated our presentation of total operating costs to include operating items that are outside the ordinary course of our operations (“special items”). These items have been previously presented separate from operating costs and included in operating profit. We recast operating costs for the prior periods in order to present comparable financial results. There was no change to consolidated operating profit, net income or cash flows as a result of this change.

In the accompanying analysis of financial information, we present certain information derived from our consolidated financial information but not presented in our financial statements prepared in accordance with generally accepted accounting principles in the United States of America (“GAAP”). We are presenting in this report supplemental non-GAAP financial performance measures that exclude depreciation, amortization, severance, non-operating retirement costs, and certain identified special items, as applicable. In addition, we present our free cash flow, defined as net cash provided by operating activities less capital expenditures. These non-GAAP financial measures should not be considered in isolation from or as a substitute for the related GAAP measures and should be read in conjunction with financial information presented on a GAAP basis. For further information and reconciliations of these non-GAAP measures to the most directly comparable GAAP measures, see “— Results of Operations — Non-GAAP Financial Measures.”

The third quarter of 2023 included an additional day compared with the third quarter of 2022 as a result of the change in the Company’s fiscal year to the calendar year.

The Company has two reportable segments: The New York Times Group (“NYTG”) and The Athletic.

The results of The Athletic have been included in our Condensed Consolidated Financial Statements beginning February 1, 2022, the date of the acquisition. Results for the first nine months of 2022 included The Athletic for approximately eight months, while results for the first nine months of 2023 included The Athletic for the full nine months.

23

Industry Trends, Economic Conditions, Challenges and Risks

We operate in a highly competitive environment that is subject to rapid change. Companies shaping our competitive environment include information providers and distributors, as well as news aggregators, search engines and social media platforms. Competition among these companies is robust, and new competitors can quickly emerge. We have designed our strategy to take advantage of both the challenges and opportunities presented by this period of transformation in our industry.

We and the companies with which we do business are subject to risks and uncertainties caused by factors beyond our control, including economic, public health and geopolitical conditions. These include economic weakness, uncertainty and volatility, including the potential for a recession; a competitive labor market and evolving workforce expectations, including for unionized employees; inflation; supply chain disruptions; rising interest rates; and political and sociopolitical uncertainties and conflicts. These factors may result in declines and/or volatility in our results.

We believe the macroeconomic environment has had and may continue to have an adverse impact on both digital and print advertising spending.

We are experiencing a competitive labor market and pressure on compensation and benefit costs for certain employees, mainly in technology roles. In addition, although we have not seen a significant impact from inflation on our recent financial results to date, if inflation remains at current levels, or increases, for an extended period, our employee-related costs are likely to increase. Our printing and distribution costs also have been impacted and may be further impacted by inflation and higher costs, including those associated with raw materials, delivery costs and/or utilities.

The media industry has transitioned from being primarily print-focused to digital, resulting in secular declines in both print subscription and print advertising revenues, and we do not expect this trend to reverse.

We actively monitor industry trends, economic conditions, challenges and risks to remain flexible and to optimize and evolve our business as appropriate; however, the full impact they will have on our business, operations and financial results is uncertain and will depend on numerous factors and future developments. The risks related to our business are further described in the section titled “Item 1A — Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2022.

24

RESULTS OF OPERATIONS

The following table presents our consolidated financial results:

| For the Quarters Ended | For the Nine Months Ended | |||||||||||||||||||||||||||||||||||||

| (In thousands) | September 30, 2023 | September 25, 2022 | % Change | September 30, 2023 | September 25, 2022 | % Change | ||||||||||||||||||||||||||||||||

| Revenues | ||||||||||||||||||||||||||||||||||||||

| Subscription | $ | 418,577 | $ | 382,672 | 9.4 | % | $ | 1,225,709 | $ | 1,138,270 | 7.7 | % | ||||||||||||||||||||||||||

| Advertising | 117,113 | 110,467 | 6.0 | % | 341,124 | 344,116 | (0.9) | % | ||||||||||||||||||||||||||||||

| Other | 62,655 | 54,541 | 14.9 | % | 183,104 | 158,399 | 15.6 | % | ||||||||||||||||||||||||||||||

Total revenues | 598,345 | 547,680 | 9.3 | % | 1,749,937 | 1,640,785 | 6.7 | % | ||||||||||||||||||||||||||||||

| Operating costs | ||||||||||||||||||||||||||||||||||||||

| Cost of revenue (excluding depreciation and amortization) | 311,135 | 294,856 | 5.5 | % | 927,910 | 876,804 | 5.8 | % | ||||||||||||||||||||||||||||||

| Sales and marketing | 62,635 | 64,732 | (3.2) | % | 191,910 | 205,089 | (6.4) | % | ||||||||||||||||||||||||||||||

| Product development | 57,433 | 50,474 | 13.8 | % | 170,542 | 148,729 | 14.7 | % | ||||||||||||||||||||||||||||||

| General and administrative | 81,870 | 71,970 | 13.8 | % | 235,194 | 212,468 | 10.7 | % | ||||||||||||||||||||||||||||||

| Depreciation and amortization | 21,475 | 21,760 | (1.3) | % | 64,173 | 61,150 | 4.9 | % | ||||||||||||||||||||||||||||||

| Acquisition-related costs | — | — | — | — | 34,712 | * | ||||||||||||||||||||||||||||||||

| Impairment charges | 2,503 | — | * | 15,239 | — | * | ||||||||||||||||||||||||||||||||

| Multiemployer pension plan liability adjustment | (2,273) | (7,127) | (68.1) | % | (2,273) | (7,127) | (68.1) | % | ||||||||||||||||||||||||||||||

Total operating costs (1) | 534,778 | 496,665 | 7.7 | % | 1,602,695 | 1,531,825 | 4.6 | % | ||||||||||||||||||||||||||||||

| Operating profit | 63,567 | 51,015 | 24.6 | % | 147,242 | 108,960 | 35.1 | % | ||||||||||||||||||||||||||||||

| Other components of net periodic benefit (income)/costs | (684) | 1,757 | * | (2,053) | 4,903 | * | ||||||||||||||||||||||||||||||||

| Interest income and other, net | 5,736 | 1,579 | * | 13,426 | 38,258 | (64.9) | % | |||||||||||||||||||||||||||||||

| Income before income taxes | 69,987 | 50,837 | 37.7 | % | 162,721 | 142,315 | 14.3 | % | ||||||||||||||||||||||||||||||

| Income tax expense | 16,372 | 14,220 | 15.1 | % | 40,211 | 39,196 | 2.6 | % | ||||||||||||||||||||||||||||||

| Net income | $ | 53,615 | $ | 36,617 | 46.4 | % | $ | 122,510 | $ | 103,119 | 18.8 | % | ||||||||||||||||||||||||||

(1) Third quarter and nine months of 2022 were recast to conform to the current presentation of total operating costs. See Executive Overview for more details. | ||||||||||||||||||||||||||||||||||||||

| * Represents a change equal to or in excess of 100% or not meaningful. | ||||||||||||||||||||||||||||||||||||||

25

Revenues

Subscription Revenues

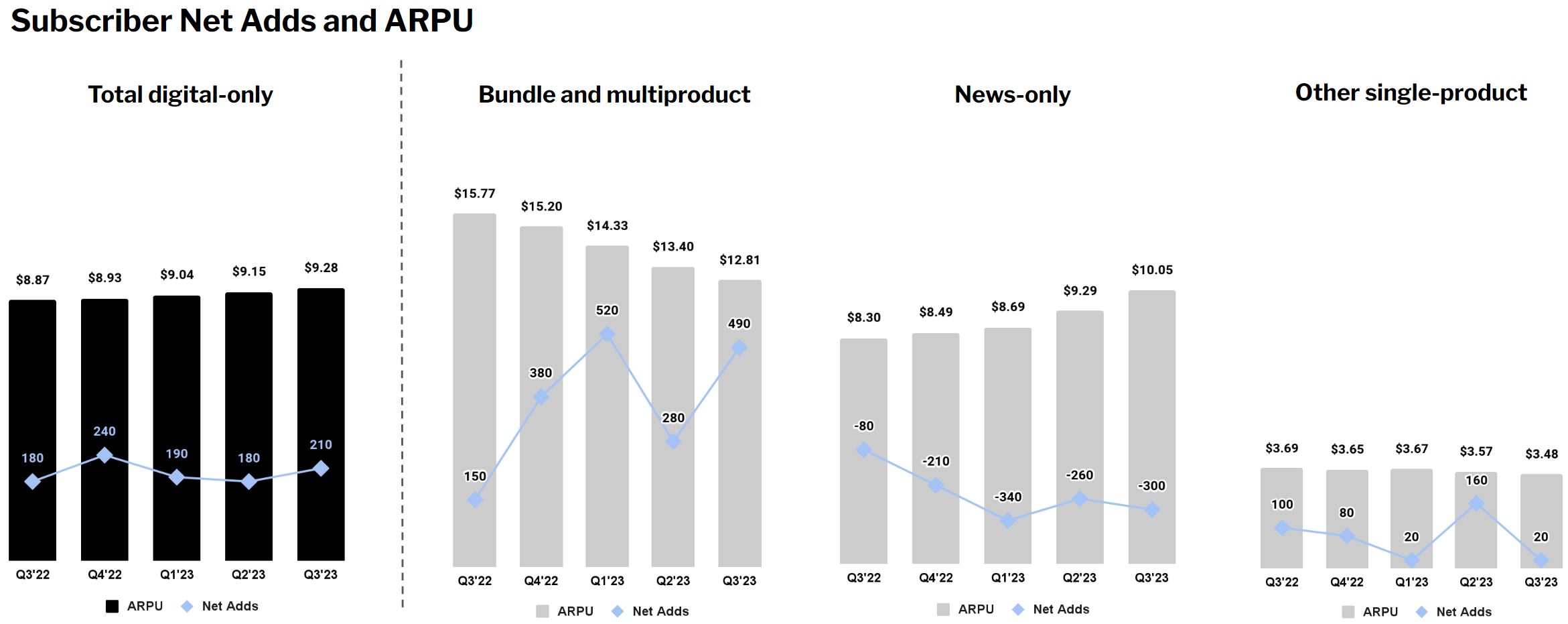

Subscription revenues consist of revenues from subscriptions to our digital and print products (which include our news product, as well as The Athletic and our Cooking, Games and Wirecutter products), and single-copy and bulk sales of our print products (which represent less than 5% of these revenues). Subscription revenues are based on both the number of copies of the printed newspaper sold and digital-only subscriptions, and the rates charged to the respective customers.

We offer a bundle that includes access to our digital news product, as well as The Athletic and our Cooking, Games and Wirecutter products. Our subscriptions also include standalone digital subscriptions to our digital news product, as well as to The Athletic, and to our Cooking, Games and Wirecutter products. Access to our new Audio product, which we launched in the second quarter of 2023, is included in bundle subscriptions and subscriptions to our digital and print news products.