UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

For the fiscal year ended December 26 , 2021

For the transition period from ___ to ___

Commission file number 1-5837

THE NEW YORK TIMES CO MPANY

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||||||||

| (Address and zip code of principal executive offices) | |||||||||||||||||

Registrant’s telephone number, including area code: (212 ) 556-1234

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: Not Applicable

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

☑ | Accelerated filer | ☐ | ||||||||||||

Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by the check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

The aggregate worldwide market value of Class A Common Stock held by non-affiliates, based on the closing price on June 25, 2021, the last business day of the registrant’s most recently completed second quarter, as reported on the New York Stock Exchange, was approximately $7.3 billion. As of such date, non-affiliates held 34,341 shares of Class B Common Stock. There is no active market for such stock.

The number of outstanding shares of each class of the registrant’s common stock as of February 17, 2022 (exclusive of treasury shares) was as follows: 166,751,793 shares of Class A Common Stock and 781,724 shares of Class B Common Stock.

Documents incorporated by reference

| INDEX TO THE NEW YORK TIMES COMPANY 2021 ANNUAL REPORT ON FORM 10-K | ||

| ITEM NO. | ||||||||||||||||||||

Subscribers, Subscriptions and Audience | ||||||||||||||||||||

| Human Capital | ||||||||||||||||||||

| 16 | ||||||||||||||||||||

| PART I | ||

FORWARD-LOOKING STATEMENTS | ||

This Annual Report on Form 10-K, including the sections titled “Item 1 — Business,” “Item 1A — Risk Factors” and “Item 7 — Management’s Discussion and Analysis of Financial Condition and Results of Operations,” contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Terms such as “aim,” “anticipate,” “believe,” “confidence,” “contemplate,” “continue,” “conviction,” “could,” “drive,” “estimate,” “expect,” “forecast,” “future,” “goal,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “opportunity,” “optimistic,” “outlook,” “plan,” “position,” “potential,” “predict,” “project,” “seek,” “should,” “strategy,” “target,” “will,” “would” or similar statements or variations of such words and other similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such terms. Forward-looking statements are based upon our current expectations, estimates and assumptions and involve risks and uncertainties that change over time; actual results could differ materially from those predicted by such forward-looking statements. Factors that we think could, individually or in the aggregate, cause our actual results to differ materially from expected and historical results include those described in “Item 1A — Risk Factors” below, as well as other risks and factors identified from time to time in our Securities and Exchange Commission (“SEC”) filings. You are cautioned not to place undue reliance on any such forward-looking statements, which speak only as of the date they are made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

ITEM 1. BUSINESS | ||

OVERVIEW

The New York Times Company (the “Company”) was incorporated on August 26, 1896, under the laws of the State of New York. The Company and its consolidated subsidiaries are referred to collectively in this Annual Report on Form 10-K as “we,” “our” and “us.”

We are a global media organization focused on creating, collecting and distributing high-quality news and information that helps our audience understand and engage with the world. We believe that The Times’s original, independent and high-quality reporting, storytelling and journalistic excellence across topics and formats set us apart from other news organizations and is at the heart of what makes our journalism worth paying for. The quality of our coverage has been widely recognized with many industry and peer accolades, including 132 Pulitzer Prizes and citations, more than any other news organization.

The Company includes our digital and print products and related businesses, including:

•our core news product, The New York Times (“The Times”), which is available on our mobile applications, on our website (NYTimes.com) and as a printed newspaper, and associated content such as our podcasts;

•our other interest-specific products, including Games, Cooking and Audm (our read-aloud audio service), which are available on mobile applications and websites; Wirecutter, our online review and recommendation product; and, following our acquisition of The Athletic Media Company on February 1, 2022 (as further described below), The Athletic; and

•our related businesses, such as our licensing operations; our commercial printing operations; our live events business; and other products and services under The Times brand.

On February 1, 2022, we completed the acquisition of The Athletic Media Company (“The Athletic”), a global digital subscription-based sports media business that provides national and local coverage of more than 200 clubs and teams in the United States and around the world.

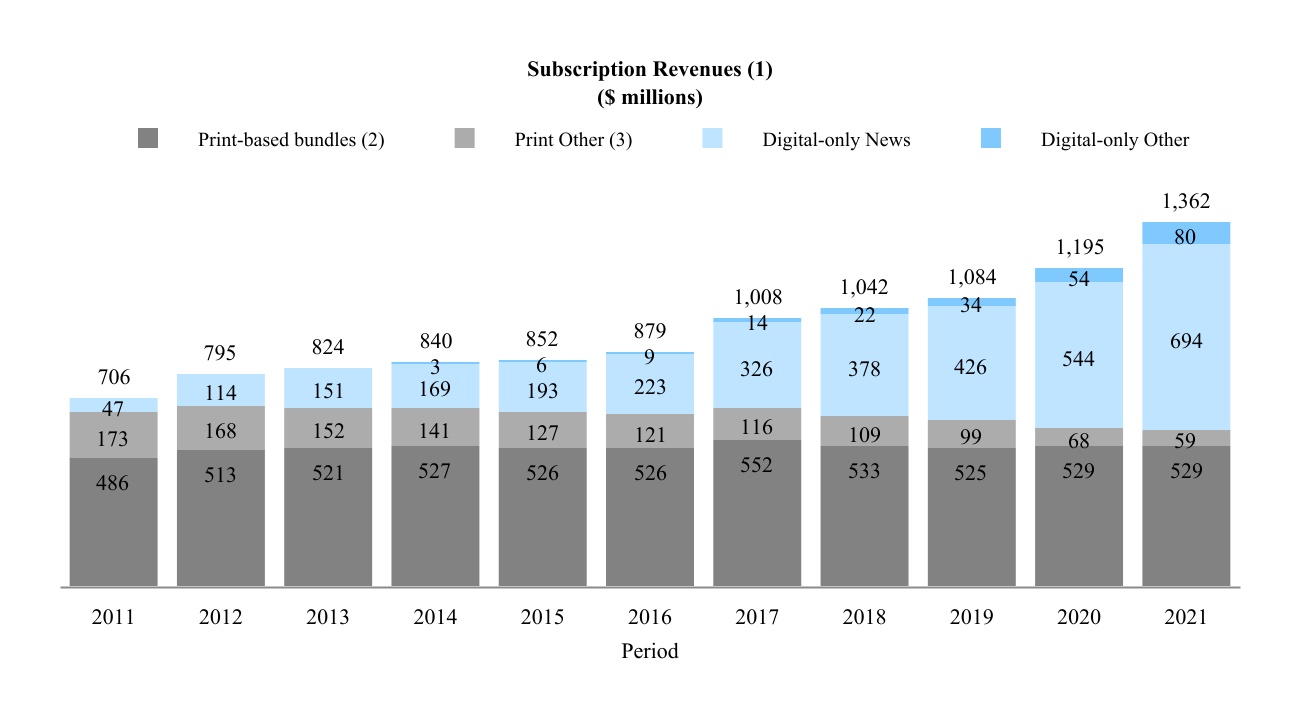

We generate revenues principally from the sale of subscriptions and advertising. Subscription revenues consist of revenues from subscriptions to our digital and print products (which include our news product, as well as our Games, Cooking, Audm and Wirecutter products) and single-copy and bulk sales of our print products. Advertising revenue is derived from the sale of our advertising products and services. Revenue information for the Company appears under “Item 7 — Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

THE NEW YORK TIMES COMPANY – P. 1

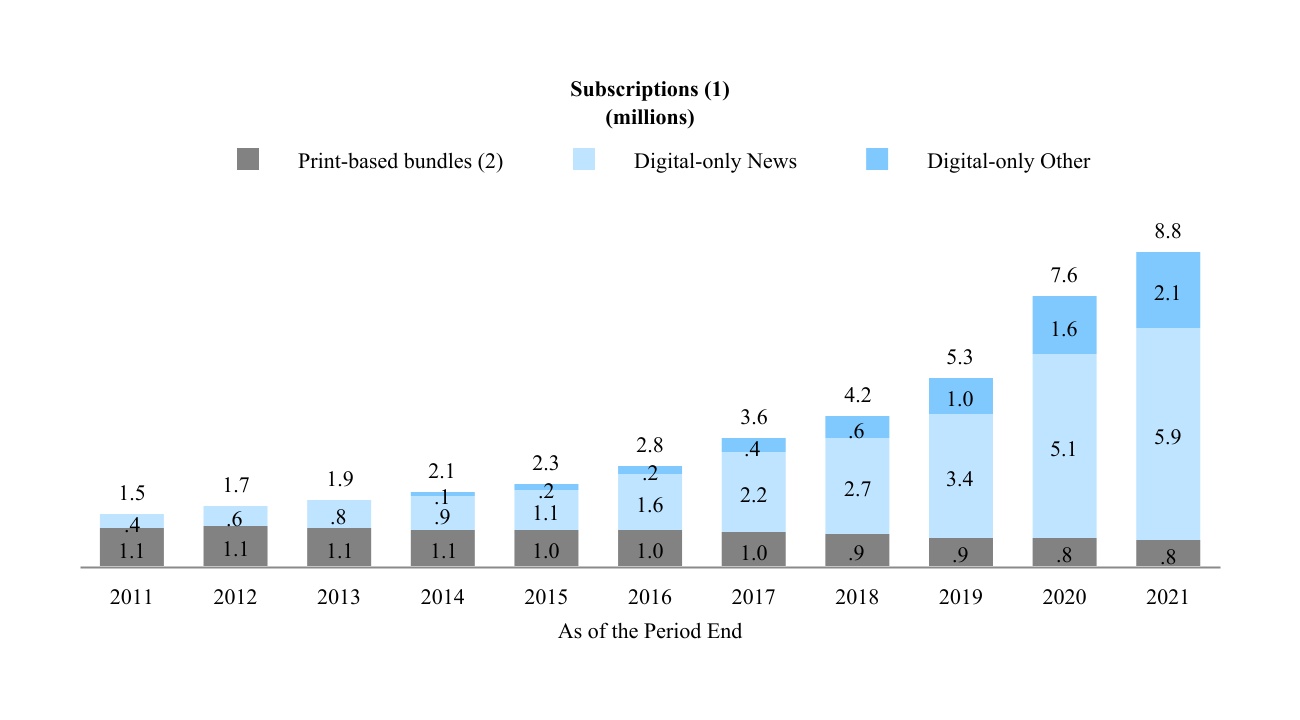

We believe that the significant growth in subscriptions to our products demonstrates the success of our “subscription-first” strategy and the willingness of our readers to pay for high-quality journalism. As of December 26, 2021, approximately 7.6 million subscribers had purchased approximately 8.8 million paid subscriptions across our products, more than at any point in our history. Our non-news products Games and Cooking each crossed one million subscriptions just before the end of 2021.

In early 2019, we established a goal of reaching 10 million subscriptions by 2025, a target we have now surpassed with the acquisition of The Athletic in 2022. In February 2022, we announced a new target: at least 15 million total subscribers by year-end 2027.

During 2021, we continued to make significant investments in our journalism and our digital product experience as well as in the back-end technology and underlying capabilities that allow users to seamlessly move among various devices and products. The Times continued to break stories, produce investigative reports and help our audience understand a wide range of topics, including the coronavirus (Covid-19) pandemic and its many reverberations, the intersection of race and culture in America, and the varied effects of climate change. In addition, we continue to innovate advertising offerings that integrate well with the user experience, including solutions that use proprietary first-party data — rather than third-party data — to generate predictive insights and help inform our clients’ advertising strategies while leveraging our audiences in privacy-forward ways, as well as our audio advertising offerings. We also expanded subscriptions to our non-news products by launching a subscription option to our Wirecutter product during the third quarter of 2021.

In January 2022, we acquired Wordle, a popular digital word game, to join our Games portfolio.

The global Covid-19 pandemic, efforts to contain it and the resulting economic disruptions have impacted and may further impact our business in various ways. See “Item 1A — Risk Factors” and “Item 7 — Management’s Discussion and Analysis of Financial Condition and Results of Operations” for more information.

PRODUCTS

The Company’s principal business consists of distributing content through our digital and print platforms. In addition, we distribute selected content on third-party platforms.

Since 2011, we have charged consumers for content provided on our core news website (NYTimes.com) and mobile applications. Digital subscriptions can be purchased by individual consumers or as part of group education or group corporate subscriptions. Our core news access model generally offers users who have registered free access to a limited number of articles before requiring users to subscribe for access to additional content. We have made the choice at times to suspend limits on registered users’ free access to particularly important coverage.

In addition to subscriptions to our digital news product, we offer an All Digital Access subscription package that includes bundled access to our news website and mobile application, Games, Cooking and Wirecutter products. We also offer standalone subscriptions to our Games, Cooking, Audm and Wirecutter products, and effective February 1, 2022, The Athletic. Our access model for our Games, Cooking and Wirecutter products generally offers users who have registered free access to limited pieces of content before requiring users to subscribe for access to additional content.

Our products also include podcasts, which are distributed both on our digital platforms and on third-party platforms. We generate advertising and licensing revenue from this content.

The Times’s print edition newspaper, published seven days a week in the United States, commenced publication in 1851. The Times also has an international edition that is tailored for global audiences. First published in 2013, the international edition succeeded the International Herald Tribune, a leading daily newspaper that commenced publishing in Paris in 1887. Our print newspapers are sold in the United States and around the world through individual home-delivery subscriptions, bulk subscriptions (primarily by schools and hotels) and single-copy sales. Print home-delivery subscribers are entitled to receive free access to our digital news, Games, Cooking and Wirecutter products.

P. 2 – THE NEW YORK TIMES COMPANY

SUBSCRIBERS, SUBSCRIPTIONS AND AUDIENCE

Our content reaches a broad audience through both digital and print platforms. As of December 26, 2021, approximately 7.6 million subscribers had purchased approximately 8,789,000 paid subscriptions across 236 countries and territories to our digital and print products. As of December 31, 2021, The Athletic, which we acquired on February 1, 2022, had approximately 1.2 million subscribers.

Paid digital-only subscriptions totaled approximately 8,005,000 as of December 26, 2021, an increase of approximately 19% compared with December 27, 2020. This amount includes standalone paid subscriptions to our Games, Cooking, Audm and Wirecutter products. International digital-only news subscriptions represented approximately 18% of our digital-only news subscriptions as of December 26, 2021.

The number of paid digital-only subscriptions also includes estimated group education and group corporate subscriptions (which collectively represent approximately 5% of total paid digital subscriptions to our news products). The numbers of paid group subscriptions and subscribers are derived using the value of the relevant contract and a discounted subscription rate. The actual number of users who have access to our products through group sales is substantially higher.

According to comScore Media Metrix, an online audience measurement service, in 2021, NYTimes.com had a monthly average of approximately 90 million unique visitors in the United States on either desktop/laptop computers or mobile devices. Globally, including the United States, NYTimes.com had a monthly average of approximately 125 million unique visitors on either desktop/laptop computers or mobile devices, according to internal data estimates.

In the United States, The Times had the largest daily and Sunday print circulation of all seven-day newspapers for the six-month period ended September 30, 2021, according to data collected by the Alliance for Audited Media (“AAM”), an independent agency that audits circulation of most U.S. newspapers and magazines.

For the fiscal year ended December 26, 2021, The Times’s average print circulation (which includes paid and qualified circulation of the newspaper in print) was approximately 343,000 for weekday (Monday to Friday) and 820,000 for Sunday. (Under AAM’s reporting guidance, qualified circulation represents copies available for individual consumers that are either non-paid or paid by someone other than the individual, such as copies delivered to schools and colleges and copies purchased by businesses for free distribution.)

Average circulation for the international edition of our newspaper (which includes paid circulation of the newspaper in print and electronic replica editions) for the fiscal years ended December 26, 2021, and December 27, 2020, was approximately 91,100 (estimated) and 104,800, respectively. These figures follow the guidance of Office de Justification de la Diffusion, an agency based in Paris and a member of the International Federation of Audit Bureaux of Circulations that audits the circulation of most newspapers and magazines in France. For 2020, this guidance excludes data from March through June 2020 in the calculation of the annual average. The final 2021 figure will not be available until April 2022.

THE NEW YORK TIMES COMPANY – P. 3

ADVERTISING

We have a comprehensive portfolio of advertising products and services. Advertising revenue is principally from advertisers (such as technology, luxury goods and financial companies) promoting products, services or brands on digital platforms in the form of display ads, audio and video, and in print, in the form of column-inch ads.

The majority of our advertising revenue is derived from offerings sold directly to marketers by our advertising sales teams. A smaller proportion of our total advertising revenues is generated through programmatic auctions run by third-party advertising exchanges.

Digital advertising includes our core digital advertising business and other digital advertising. Our core digital advertising includes direct-sold website, mobile application, podcast, email and video advertisements. Our digital advertising offerings include solutions that use proprietary first-party data — rather than third-party data — to generate predictive insights and help inform our clients’ advertising strategies while leveraging our audiences in privacy-forward ways. Other digital advertising includes advertising revenues generated by open-market programmatic advertising, creative services associated with branded content, advertisements appearing on our Wirecutter product and classified advertising. In 2021, digital advertising represented approximately 62% of our advertising revenues.

At the time of its acquisition, The Athletic had a limited advertising business, consisting primarily of podcast advertising. We expect to develop a broader set of advertising products and services for the site over time.

Print advertising for The Times includes revenue from column-inch ads and classified advertising, including line-ads as well as preprinted advertising, also known as freestanding inserts. Column-inch ads are priced according to established rates, with premiums for color and positioning, and classified advertising is paid for on a per-line basis. The Times newspaper had the largest market share in 2021 in print advertising among a national newspaper set that consists of USA Today, The Wall Street Journal and The Times, according to MediaRadar, an independent agency that measures advertising sales volume. In 2021, print advertising represented approximately 38% of our advertising revenues.

Our business is affected in part by seasonal patterns in advertising, with generally higher advertising volume in the fourth quarter due to holiday advertising.

COMPETITION

We face a market undergoing profound transformation and significant competition in all aspects of our business. We compete for audience, subscribers, and advertising against a wide variety of digital and print media companies, including digital and traditional print content providers, news aggregators, search engines, social media platforms and streaming services, any of which might attract audiences and/or advertisers to their platforms and away from ours. Our news product most directly competes for audience, subscriptions and advertising with other U.S. and global news and information digital and print products, including The Washington Post, The Wall Street Journal, CNN, BBC News, Vox, The Guardian and Financial Times. Our digital news product also competes with customized news feeds, news aggregators and social media products of companies such as Apple, Alphabet, Meta Platforms and Twitter. Our other digital products compete with comparable content providers, as well as other digital media of general interest. In addition, we compete for advertising on digital advertising networks and exchanges with real-time bidding and other programmatic buying channels.

Competition for subscription revenue and audience is generally based upon content breadth, depth, originality, quality and timeliness; product experience; format; price and access model; visibility on search engines and social media platforms and in mobile application stores; and service, while competition for advertising is generally based upon audience levels and demographics, advertising rates, service, targeting capabilities, advertising results and breadth of advertising offerings. We believe that The Times’s original, independent and high-quality reporting, storytelling and journalistic excellence across topics and formats set us apart from others and is at the heart of what makes our journalism worth paying for, and we believe our journalism attracts valuable audiences providing a safe and trusted platform for advertisers’ brands.

P. 4 – THE NEW YORK TIMES COMPANY

OTHER BUSINESSES

We also derive revenue from other businesses, which primarily include:

•The Company’s licensing of our intellectual property. Our licensing division transmits articles, graphics and photographs from The Times and other publications to over 1,500 clients, including newspapers, magazines and websites in over 95 countries and territories worldwide. The licensing division also handles digital archive distribution, which licenses electronic databases to resellers in the business, professional and library markets; magazine licensing; news digests; book development; and rights and permissions. In addition, the Company licenses select content to third-party digital platforms for access by their users. Finally, the Company licenses content for use in, and collaborates with third parties in the development and production of, television and films;

•In addition to advertising and subscription revenue, our Wirecutter product generates affiliate referral revenue (revenue generated by offering direct links to merchants in exchange for a portion of the sale price upon completion of a transaction);

•The Company’s commercial printing operations, which utilize excess capacity at our facility in College Point, N.Y., to print and distribute products for third parties; and

•The Company’s live events business, which hosts physical and virtual live events to connect audiences with our journalists and outside thought leaders, and is monetized through sponsorship and advertising.

PRINT PRODUCTION AND DISTRIBUTION

The Times is currently printed at our production and distribution facility in College Point, N.Y., as well as under contract at 24 remote print sites across the United States. We also utilize excess capacity at our College Point facility for commercial printing and distribution for third parties. The Times is delivered in the New York metropolitan area through a combination of our own drivers and agreements with other newspapers and third-party delivery agents. In other markets in the United States and Canada, The Times is delivered through agreements with other newspapers and third-party delivery agents.

The international edition of The Times is printed under contract at 28 sites throughout the world and is sold in over 85 countries and territories. It is distributed through agreements with other newspapers and third-party delivery agents.

RAW MATERIALS

The primary raw materials we use are newsprint and coated paper, which we purchase from a number of North American and European producers. A significant portion of our newsprint is purchased from Resolute FP US Inc., a subsidiary of Resolute Forest Products Inc., a large global manufacturer of paper, market pulp and wood products.

In 2021 and 2020, we used the following types and quantities of paper:

| (In metric tons) | 2021 | 2020 | ||||||||||||

Newsprint(1) | 63,600 | 71,600 | ||||||||||||

Coated and Supercalendered Paper(2) | 9,800 | 10,200 | ||||||||||||

(1) Newsprint usage includes paper used for commercial printing.

(2) The Times uses a mix of coated and supercalendered paper for The New York Times Magazine, and coated paper for T: The New York

Times Style Magazine.

THE NEW YORK TIMES COMPANY – P. 5

HUMAN CAPITAL

The talented employees who make up our inclusive workplace are vital to the continued success of our mission and business and central to our long-term strategy. In order to attract, develop and maximize the contributions of world-class talent, we are working to create a rewarding employee experience in a variety of ways, including building a more diverse, equitable and inclusive workplace; developing and promoting talent; providing equitable and competitive compensation and benefits (total rewards); and supporting employees’ health, safety and well-being.

Building a more diverse, equitable and inclusive workplace

Each year since 2017, we have prepared an in-depth report on diversity and inclusion at The Times to promote accountability over time. Steps to advance our diversity, equity and inclusion goals include:

•Investing in dedicated resources. In 2021, we continued to build out a dedicated team to lead and support our diversity, equity and inclusion initiatives.

•Adopting policies, processes and guidelines to promote an equitable and respectful organizational culture. This includes a rigorous and transparent process for investigating workplace complaints and concerns, as well as ongoing efforts to codify and promote behavioral expectations for employees working at The Times on how to approach their work, and engage with, manage and lead each other.

•Focusing on pay equity. Every two years, including in 2021, we conduct a pay-equity study, an in-depth review of our compensation practices conducted with an outside expert to identify, assess and rectify any inconsistencies in pay. We analyze average differences across race and gender of people performing similar work, taking into account factors that explain legitimate differences in pay, such as tenure and performance, and also perform a thorough analysis of individual pay.

•Investing in diversifying the employee pipeline. We are creating and expanding programs like The New York Times Fellowship Program (a one-year work program for up-and-coming journalists), hosting an annual Student Journalism Institute for journalists of color, and supporting many outside organizations dedicated to increasing diversity in journalism, technology and media.

•Evolving opportunities for identity-based connection. We currently have 13 active employee resource groups providing opportunities for employees with a shared identity to support each other and serving as a forum through which to develop leadership and management skills.

Developing and promoting talent

We recognize the importance of creating opportunities for employees to evolve and succeed, at every level.

Identifying and putting in place effective executive leadership is critically important to our success. Our Board of Directors works with senior management to ensure that strategic plans are in place for both short- and long-term executive succession. The Board conducts an annual detailed review of the Company’s leadership pipeline and succession plans for key senior leadership roles.

We also value ongoing development and continuous learning, and strive to support and provide enriching opportunities to our employees. We have made significant investments to bolster role-based and professional development learning and skill building to further meet the needs of our workforce.

Providing equitable and competitive total rewards

Talent – including our employees and those we seek to hire – is in high demand, particularly journalists and people working in digital product development disciplines.

We offer comprehensive total rewards, which are designed to meet the needs of our current and future employees; support the Company’s strategic goals, mission and values; drive a high-performance culture; and offer competitive and equitable pay. In line with our business goals, our total rewards philosophy links compensation to achieving sustained high performance. Along with the compensation and benefits we provide, our reputation, workplace culture, and focus on equity and inclusion are all factors that help us attract and retain highly skilled people of diverse backgrounds.

P. 6 – THE NEW YORK TIMES COMPANY

Supporting employees’ health, safety and well-being

Our employees’ well-being is vital to our success, and their physical and mental health, safety and work-life balance are a top priority. We have invested in programs that help support their day-to-day wellness needs and goals including, but not limited to: access to licensed professional counselors, health coaching and advocacy services, fitness resources, child and elder care help, and more.

As a result of the Covid-19 pandemic, the vast majority of our employees continue to work remotely. During 2021, we continued and broadened some of the benefits we introduced in the early stages of the pandemic that were designed to support employees during an extended period of working from home, including dependent care relief, office-supply reimbursement, ergonomic resources, and mental health and wellness support. We also continue to evolve our remote and distributed work policies and practices. These include protocols to protect the health and safety of our employees, including those who do not work remotely, such as those who are working in our offices, our journalists in the field and employees working in our College Point, N.Y., printing and distribution facility.

We also continue to adapt to ever-changing workplace and workforce dynamics, and plan to transition to a hybrid work model with employees working both from our offices and remotely. We are focused on building capabilities to support a variety of work styles where individuals, teams, and our business can be successful.

Workforce Demographics

We had approximately 5,000 full-time equivalent employees as of December 26, 2021, which includes more than 2,000 involved in our journalism operation.

Approximately 38% of our full-time equivalent employees were represented by unions as of December 26, 2021. In addition, some of our technology employees are seeking to form a union. The following is a list of collective bargaining agreements covering various categories of the Company’s employees and their corresponding expiration dates. As indicated below, one collective bargaining agreement, under which approximately 26% of our full-time equivalent employees are covered, has expired and negotiations for a new contract are ongoing. Additionally, as indicated below, one collective bargaining agreement, under which less than 1% of our full-time equivalent employees are covered, will expire within one year and we expect negotiations for a new contract to begin in the near future. We cannot predict the timing or the outcome of these negotiations.

| Employee Category | Expiration Date | ||||

NewsGuild of New York (The New York Times) | March 30, 2021 | ||||

| Machinists | March 30, 2022 | ||||

| Mailers | March 30, 2023 | ||||

| Voice Actors | October 31, 2023 | ||||

NewsGuild of New York (Wirecutter) | February 28, 2024 | ||||

| Drivers | March 30, 2025 | ||||

| Typographers | March 30, 2025 | ||||

| Paperhandlers | March 30, 2026 | ||||

| Pressmen | March 30, 2026 | ||||

| Stereotypers | March 30, 2026 | ||||

THE NEW YORK TIMES COMPANY – P. 7

AVAILABLE INFORMATION

We maintain a corporate website at http://www.nytco.com, and we encourage investors and other interested persons to use it as a way of easily finding information about us. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and all amendments to those reports, and the Proxy Statement for our Annual Meeting of Stockholders are made available, free of charge, on this website as soon as reasonably practicable after such reports have been filed with or furnished to the SEC. In addition, we may periodically make announcements or disclose important information for investors on this website, including press releases or news regarding our financial performance and other items that may be material or of interest to our investors. Therefore, we encourage investors, the media, and others interested in our Company to review the information we post on this website. We have included our website addresses throughout this report as inactive textual references only. The information contained on the websites referenced herein is not incorporated into this filing.

P. 8 – THE NEW YORK TIMES COMPANY

ITEM 1A. RISK FACTORS | ||

This section highlights specific risks that could affect us and our businesses. You should carefully consider each of the following risks, as well as the other information included in this Annual Report on Form 10-K. Our business, financial condition, results of operations and/or the price of our publicly traded securities could be materially adversely affected by any or all of these risks, or by other risks or uncertainties not presently known or currently deemed immaterial, that may adversely affect us in the future.

Risks Related to Our Business and Industry

We face a market undergoing profound transformation and significant competition in all aspects of our business.

Our industry is transforming as consumer demand transitions from traditional media — such as print newspapers — to digital, resulting in rapid changes in consumer behavior, advertiser behavior, talent behavior and competitive boundaries. The future structure of our industry remains unpredictable, leading to significant opportunity and uncertainty for our business and our competitors.

We operate in a highly competitive environment. We compete for audience share and subscribers, as well as subscription revenue, advertising revenue, and other revenues such as licensing and affiliate referral revenues. Our competitors include content providers and distributors, as well as news aggregators, search engines and social media platforms. Competition among these companies is robust, and new competitors can quickly emerge.

Our ability to compete effectively depends on many factors both within and beyond our control, including among others:

•our ability to continue delivering a breadth of high-quality journalism and content that is interesting and relevant to our audience;

•our reputation and brand strength relative to those of our competitors;

•the popularity, usefulness, ease of use, performance, reliability and value of our digital products, compared with those of our competitors;

•the sustained engagement of our audience directly with our products;

•our ability to reach new users in the United States and abroad;

•our ability to develop, maintain and monetize our products;

•the pricing of our products and our content access model;

•our marketing and selling efforts, including our ability to differentiate our products and services from those of our competitors;

•our visibility on search engines and social media platforms and in mobile app stores, compared with that of our competitors;

•our ability to attract, retain, and motivate talented employees, including journalists and people working in digital product development disciplines, among others, who are in high demand;

•our ability to provide advertisers with a compelling return on their investments; and

•our ability to manage and grow our business in a cost-effective manner.

Some of our current and potential competitors have greater resources than we do, which may allow them to compete more effectively than us. In addition, several of the companies that have competing digital news destinations, subscriptions and other products, such as Apple and Alphabet, also control some of the primary environments in which we develop relationships with new users and market and sell subscriptions to our products, and therefore can affect our ability to compete effectively. Some of these companies encourage their large audiences to consume our content within their products, impacting our ability to attract, engage and monetize users directly.

THE NEW YORK TIMES COMPANY – P. 9

Our ability to grow the size and profitability of our subscriber base depends on many factors, both within and beyond our control, and a failure to do so could adversely affect our results of operations and business.

Revenue from subscriptions to our digital and print products makes up a majority of our total revenue. Our future growth and profitability depend upon our ability to retain, grow and effectively monetize our audience and digital subscriber base in the United States and abroad. We have invested and will continue to invest significant resources in our efforts to do so, but there is no assurance that we will be able to successfully grow our subscriber base in line with our expectations, or that we will be able to do so without taking steps such as adjusting our pricing or incurring subscription acquisition costs that could adversely affect our subscription revenues, margin and/or profitability.

Our ability to attract and grow our digital subscriber base depends on the size of our audience and its sustained engagement directly with our products, including the breadth, depth and frequency of use. The size and engagement of our audience is dependent on many factors both within and beyond our control, including significant news events, user sentiment about the quality of our content and products in comparison to our competitors, the free access we provide to our content, and our ability to successfully manage changes implemented by search engines that affect the visibility of our content, among other factors. If users become less engaged with our products, they may be less likely to subscribe.

We have set a goal to reach 15 million subscribers by the end of 2027 (from approximately 7.6 million as of year-end 2021) based on our historical performance, as well as internal and external research on the market of adults globally who are paying — or are willing to pay — for English-language news, sports information, puzzles, recipes, expert shopping advice and/or podcasting. The actual size and speed of development of this market, as well as our ability to penetrate this market to grow our subscriber base, are uncertain. Consumers’ willingness to subscribe to our products may depend on a variety of factors, including subscriber engagement, our subscription and pricing model, our ability to adapt to varied and changing consumer expectations, general economic conditions and their potential impact on consumer discretionary spending, and our marketing expenditures and effectiveness, as well as other factors within and outside our control. We may also face additional challenges in expanding our subscriber base to new audiences within and outside of the United States, which is part of our strategy, and the growth of our business could be harmed if our expansion efforts do not succeed. For example, although we have a significant number of users outside of the United States, we could be at a disadvantage compared with local and multinational competitors who may devote more resources to local or regional coverage than we do. Additionally, with our acquisition of The Athletic, we will need to appeal to a new and different subscriber base that currently has modest overlap with the subscriber base of our other products. Our continued expansion will depend on our ability to adapt, on a cost-effective basis, our content, products, pricing and marketing for global audiences. This will include adapting to differences in content preferences; product-feature preferences; culture; language; and market dynamics such as user behavior, spending capability and payment processing systems. As we grow larger and increase our subscriber base, we expect it will become increasingly difficult to maintain our rate of growth.

We must also manage the rate at which subscribers cancel their subscriptions to our products — what we refer to as our “churn.” Subscription cancellations are caused by many and varied reasons, including subscribers’ perception that they do not engage with our content sufficiently, the end of promotional pricing or in response to increases or other adjustments we may implement from time to time in our subscription pricing, changes in local credit card regulations and broader consumer protection regulations, and the expiration of subscribers’ credit cards; they may also be facilitated by the rollout of certain new account management features like the ability to cancel a subscription online. As we adjust our access model to encourage users who may spend less time with our products to subscribe, new subscriber cohorts may not retain at the same rate as prior cohorts of subscribers.

The future growth of our business and profitability also depend on our ability to successfully monetize our subscriber relationships and maintain attractive unit economics. We are investing in efforts to encourage subscribers to use and pay for multiple products, primarily through our multi-product package (“bundle”), but there can be no assurance that such efforts will be successful. We have also implemented and may continue to implement changes in our pricing model, such as price increases, that could have an adverse impact on our ability to attract, engage and retain subscribers.

Print subscriptions continue to decline as the media industry has transitioned from being primarily print-focused to digital and we do not expect this trend to reverse. As print subscriptions fall, we may be unable to slow the resulting print revenue declines with revenue from home-delivery price increases. In addition, if we are unable to

P. 10 – THE NEW YORK TIMES COMPANY

offset and ultimately replace continued print subscription revenue declines with other sources of revenue, such as digital subscriptions, our operating results will be adversely affected.

Our ability to manage and grow the size and profitability of our subscriber base is dependent on metrics that are subject to inherent challenges in measurement.

We rely on certain metrics, such as subscriptions, subscribers, average revenue per subscriber and registered users, which we use to evaluate growth trends, measure our performance and make strategic decisions. These metrics are calculated using internal company data as well as information we receive from our business affiliates, and are subject to inherent challenges in measurement. For example, there may be individuals who have multiple Times subscriptions or registrations, which we treat as multiple subscribers or registrations, as well as single subscriptions and registrations that are used by more than one person. Accordingly, the calculations of our subscribers and registered users may not reflect the actual number of people using our products. The accuracy of our metrics also depends on accurate reporting by third parties such as Apple and Alphabet, as some of our subscribers purchase their subscriptions through these intermediaries. Inaccuracies in these metrics may affect our understanding of certain details of our business, which could result in incorrect business decisions and/or affect our longer-term strategies. In addition, as our tools for measuring these metrics evolve, the methodologies for tracking may change over time, which could result in unexpected changes to our metrics. Real or perceived material inaccuracies in these metrics could harm our reputation, subject us to legal or regulatory actions and/or adversely affect our operating and financial results.

Our success depends on our ability to improve and scale our technical and data infrastructure and respond and adapt to changes in technology and consumer behavior.

Our ability to attract and retain our users is dependent upon the reliable performance and increasing capabilities of our products and our underlying technical and data infrastructure. As we invest in our array of products and our digital business grows in size, scope and complexity, we must continue to invest in maintaining, integrating, improving and scaling our technical infrastructure. Our failure to do so effectively, or any significant disruption in our service, could damage our reputation, result in a potential loss or ineffective monetization of users, and adversely affect our financial results.

The continuing rapid evolution of technology in the media industry and changes in the preferences and expectations of consumers also pose a number of challenges that could adversely affect our revenues and competitive position. For example, among others:

•we may be unable to maintain or update our technology infrastructure quickly enough and in a way that meets market and consumer demands;

•we may fail to successfully manage changes implemented by social media platforms, search engines, news aggregators, mobile app stores and device manufacturers, including those that encourage user engagement with our content in their environments rather than directing users to our products, and those affecting how our content and applications are discovered, prioritized, displayed and monetized;

•the consumption of our content on delivery platforms of third parties may lead to limitations on monetization of our products, the loss of control over distribution of our content and of a direct relationship with our audience, and lower engagement and subscription rates;

•consumers may increasingly use technology that decreases our ability to enforce limits on the free access we provide to our content and/or obtain useful information with respect to the behavior of users who engage with our products; and

•we may fail to successfully adapt our digital products to meet changing consumer preferences and expectations regarding privacy and security.

We continue to invest significant resources to mitigate these potential risks and to build, maintain and evolve our products, data and technology infrastructure. These investments may adversely impact our operating results in the near term and there can be no assurance as to our ability to use new and existing technologies to distinguish our products and services from those of our competitors, develop in a timely manner compelling new products and services that engage users, or sufficiently improve and scale our technical infrastructure and prevent disruptions in our service. If we are not successful in adapting our technical and data infrastructure and responding to changes in technology and consumer behavior, our business, financial condition and prospects may be adversely affected.

THE NEW YORK TIMES COMPANY – P. 11

Our advertising revenues are affected by numerous factors, including economic conditions, market dynamics, evolving digital advertising trends and the evolution of our strategy.

We derive substantial revenues from the sale of advertising in our products. Advertising spending is sensitive to overall economic conditions, and our advertising revenues could be adversely affected if advertisers respond to weak or uneven economic conditions by reducing their budgets or shifting spending patterns or priorities, or if they are forced to consolidate or cease operations. Worldwide economic conditions in the aftermath of the Covid-19 pandemic, including supply chain disruptions and inflationary pressures, may materially adversely affect our advertising revenues.

As the digital advertising market continues to evolve, our ability to compete successfully for advertising budgets will depend on, among other things, our ability to engage and grow digital audiences, collect and leverage data, and demonstrate the value of our advertising and the effectiveness of our products to advertisers. In determining whether to buy advertising with us, our advertisers consider the demand for our products, demographics of our audience, advertising rates, results observed by advertisers, breadth and perceived effectiveness of advertising offerings and alternative advertising options.

Large digital platforms, such as Meta Platforms, Alphabet and Amazon, which have greater audience reach, audience data and targeting capabilities than we do, command a large share of the digital display advertising market, and we anticipate that this will continue. The remaining market is subject to significant competition among publishers and other content providers, and audience fragmentation. These dynamics have affected, and will likely continue to affect, our ability to attract and retain advertisers and to maintain or increase our advertising rates.

Additionally, digital advertising networks and exchanges with real-time bidding and other programmatic buying channels that allow advertisers to buy audiences at scale also play a significant role in the marketplace and represent another competitive threat. They have caused and may continue to cause further downward pricing pressure and the loss of a direct relationship with marketers, especially during periods of economic downturn.

The evolving standards for delivery of digital advertising, as well as the development and implementation of technology, regulations, policies and practices that adversely affect our ability to deliver, target or measure the effectiveness of advertising (such as blocking the display of advertising, the phase-out of browser support for third-party cookies and of mobile operating systems for advertising identifiers), may also adversely affect our advertising revenues if we are unable to develop effective solutions to mitigate their impact.

Additionally, our digital advertising offerings also now include products that use proprietary first-party data — rather than third-party data — to generate predictive insights and help inform our clients’ advertising strategies. Our ability to quickly and effectively evolve these products; the volume, quality, and price of competitive products; and continued changes to industry regulation all have the potential to impact the success of this strategy.

We have also taken further steps intended to improve our users’ experiences and retain and grow our subscriber base. For example, in order to improve users’ experiences, we ceased presenting open-market programmatic advertising in our iOS and Android mobile applications. While these changes may result in long-term benefits for our advertising revenue, they have reduced and may further reduce the inventory for some of our digital advertising products and may otherwise impact advertising revenues.

Our digital advertising operations also rely on a small number of significant technologies (particularly Alphabet’s ad manager) which, if interrupted or meaningfully changed, or if the providers leverage their power to alter the economic structure, could have an adverse impact on our advertising revenues, operating costs and/or operating results.

Although print advertising revenue continues to represent a significant portion of our total advertising revenue (approximately 38% of our total advertising revenues in 2021), the overall proportion continues to decline and we do not expect this trend to reverse. This trend was further accelerated by the impact of the Covid-19 pandemic and efforts to contain it on some of our traditional print advertisers, such as entertainment and retail. A further decline in the economic prospects of these and other advertisers could alter current or prospective advertisers’ spending priorities or result in consolidation or closures across various industries, which may reduce the Company’s print and overall advertising revenue.

P. 12 – THE NEW YORK TIMES COMPANY

Our brand and reputation are key assets of the Company. Negative perceptions or publicity could adversely affect our business, financial condition and results of operations.

We believe The New York Times brand is a powerful and trusted brand with an excellent reputation for high-quality independent journalism and content, and this brand is a key element of our business. Our brand might be damaged by incidents that erode consumer trust (such as negative publicity), a perception that our journalism is unreliable or a decline in the perceived value of independent journalism or general trust in the media, which may be in part as a result of changing political and cultural environments in the United States and abroad or active campaigns by domestic and international political and commercial actors. We may introduce new products or services that users do not like and that may negatively affect our brand. We also may fail to provide adequate customer service, which could erode confidence in our brand. Our brand and reputation could also be adversely impacted by negative claims or publicity regarding the Company or its operations, products, employees, practices (including social and environmental practices) or business affiliates (including advertisers); as well as our potential inability to adequately respond to such negative claims or publicity, even if such claims are untrue. Our reputation could also be damaged by failures of third-party vendors we rely on in many contexts. We are investing in defining and enhancing our brand. These investments are considerable and may not be successful. To the extent our brand and reputation are damaged, our ability to attract and retain readers, subscribers, advertisers and/or employees could be adversely affected, which could in turn have an adverse impact on our business, revenues and operating results.

The continuing impact of the Covid-19 pandemic is difficult to predict and creates considerable uncertainty for our business.

The global Covid-19 pandemic continues to have widespread, rapidly evolving, and unpredictable impacts on global society, economies, financial markets and business practices. The pandemic, efforts to contain it, and the resulting disruptions have impacted our business in various ways. There is substantial uncertainty as to the nature and degree of the continued effects of the pandemic over time.

For example, during 2020 we experienced significant growth in the number of subscriptions to our digital news and other products, which we believe was attributable in part to an increase in traffic given the news environment and as a result of the pandemic. The rate of digital subscription growth moderated in 2021, although it was our second-best year for net subscription additions, and we do not expect the 2020 growth rate to be indicative of results for future periods. The growth in subscriptions to our products during the pandemic may also in part reflect changes in how our users spend their time during the pandemic, and our ability to attract and retain subscribers may continue to be impacted by patterns of behavior influenced by the course of the pandemic. In addition, revenues from the single-copy and bulk sales of our print newspaper have been, and we expect will continue to be, adversely affected as a result of continued increased levels of remote working and reductions in travel.

The worldwide economic slowdown caused by the pandemic led to a significant decline in our advertising revenues in 2020 as advertisers reduced their spending. While we experienced significantly increased demand for advertising in 2021, particularly with respect to digital advertising as the broader advertising market recovered, there is no assurance that this recovery will be sustained, and developments related to the pandemic such as global supply chain disruptions and labor shortages, among others, could adversely impact our advertising revenues in the future if our advertisers were to reduce their advertising spend as a result. We expect reduced print advertising spending by businesses that continue to be negatively impacted by the pandemic, along with secular trends, to continue to adversely affect our print advertising revenues, and some of our print advertising revenues may not return to pre-pandemic levels. In addition, the pandemic and attempts to contain it have resulted in the postponement and cancellation of live events, and while this impact moderated in 2021, this continues to adversely affect our revenues from live events and related services.

As a result of the ongoing pandemic, we altered certain aspects of our operations and the vast majority of our employees continue to work remotely. Remote work may heighten operational risk (including cybersecurity risk), result in a decline in productivity or otherwise negatively affect our ability to manage the business. In addition, if a significant portion of our workforce is unable to work due to illness, power outages, connectivity issues or other causes that impact our employees’ ability to work remotely, our operations may be negatively impacted. We will continue to actively monitor these other comparable issues raised by the pandemic and may take further actions that alter our business operations as may be required or that we determine are appropriate. It is not clear what effects any such alterations or modifications may have on our business and financial results.

THE NEW YORK TIMES COMPANY – P. 13

The Times newspaper is printed at our production and distribution facility in College Point, N.Y., as well as under contract at remote print sites, and significant operational disruptions at these facilities, or at our newsprint suppliers or print and distribution partners, could adversely affect our operating results. If a significant percentage of our College Point employees were unable to work as a result of the pandemic or because of vaccination mandates, our ability to print and distribute the newspaper and other commercial print products in the New York area could be negatively affected. To the extent our newsprint suppliers or print and distribution partners are further affected by financial pressures, labor shortages, supply chain issues or other circumstances relating to Covid-19 that lead to reduced operations or consolidations or closures of print sites and/or distribution routes, this could lead to an increase in costs to print and distribute our newspapers and/or a decrease in revenues if printing and distribution are disrupted.

The future impact that the Covid-19 pandemic will have on our business, operations and financial results is uncertain and will depend on numerous evolving factors and future developments that we are not able to reliably predict or mitigate, including the extent of variants and resurgences; the effect of ongoing vaccination and mitigation efforts; the impact of the pandemic on economic conditions and the companies with which we do business, including our advertisers; governmental, business and other’s actions in response to the pandemic; and changes in consumer behavior as a result of the pandemic, among many other factors. It is also possible that the Covid-19 pandemic may accelerate or worsen the other risks discussed in this section.

The international scope of our business exposes us to economic, geopolitical and other risks inherent in foreign operations.

We have news bureaus and other offices around the world, and our digital and print products are generally offered globally. We are focused on further expanding the international scope of our business and face the inherent risks associated with doing business abroad, including:

•government policies and regulations that restrict our products and operations, including censorship or other restrictions on access to our content and products; the expulsion of journalists or other employees; or other restrictive or retaliatory actions or behavior;

•effectively managing and staffing foreign operations, including complying with local laws and regulations in each different jurisdiction;

•providing for the safety and security of our journalists and other employees and affiliates;

•potential economic, legal, political or social uncertainty and volatility in local or global market conditions or catastrophic events (e.g., a natural disaster, an act of terrorism, a pandemic (such as the Covid-19 pandemic), epidemic or outbreak of a disease or severe weather) that could adversely affect the companies with which we do business, cause changes in discretionary spending, restrict our journalists’ travel or otherwise adversely impact our operations and business;

•navigating local customs and practices;

•protecting and enforcing our intellectual property and other rights under varying legal regimes;

•complying with international laws and regulations, including those governing intellectual property, libel and defamation, labor and employment, tax, payment processing, consumer privacy and the collection, use, retention, sharing and security of consumer and staff data;

•restrictions on the ability of U.S. companies to do business in foreign countries, including restrictions on foreign ownership, foreign investment or repatriation of funds;

•higher-than-anticipated costs of entry; and

•currency exchange rate fluctuations.

Adverse developments in any of these areas could have an adverse impact on our business, financial condition and results of operations. For example, we may incur increased costs necessary to comply with existing and newly adopted laws and regulations or penalties for any failure to comply.

P. 14 – THE NEW YORK TIMES COMPANY

Attracting and maintaining a talented and diverse workforce, which is vital to our success, is increasingly challenging and costly; failure to do so could have a negative impact on our competitive position, reputation, business, financial condition and results of operations.

Our ability to attract, develop and maximize the contributions of world-class talent, and to create the conditions for our people to do their best work, is vital to the continued success of our mission and business and central to our long-term strategy. Talent is in high demand, particularly journalists and people working in digital product development disciplines. Our employees and individuals we seek to hire are highly sought after by our competitors and other companies, some of which have greater resources than we have and may offer compensation packages that are perceived to be better than ours. As a result, we may not be able to retain our existing employees or hire new employees quickly enough to meet our needs.

Our continued ability to attract and retain highly skilled talent from diverse backgrounds for all areas of our organization depends on many factors, including our reputation; workplace culture; progress with respect to diversity, equity and inclusion efforts; and the compensation and benefits we provide. Employee-related costs are our main operating costs, and these costs have increased in recent years as we have invested in our business and competed for talent, and may further increase. Stock-based compensation is an increasing component of our overall compensation costs, and if the perceived value of our equity awards relative to our competitors declines, including as a result of volatility or declines in the market price of our Class A common stock or changes in perception about our future prospects, that may adversely affect our ability to recruit and retain talent. We must also continue to adapt to ever-changing workplace and workforce dynamics and other changes in the business and cultural landscape. We plan to transition to a hybrid work model, with employees working both from our offices and remotely, which may challenge our corporate culture, make us undesirable to talent that prefers different working arrangements, pressure our operations and introduce additional costs as we invest in our offices and technological improvements to support hybrid work. Failing to adapt effectively to these changes or to otherwise meet workforce expectations could impact our ability to compete effectively (including for talent) or have an adverse impact on our corporate culture or operations. Effective succession planning is also important to our long-term success, and a failure to effectively ensure the transfer of knowledge and train and integrate new employees could hinder our strategic planning and execution. If we are unable to attract and maintain a talented and diverse workforce, it would negatively disrupt our operations and our ability to complete ongoing projects; would impact our competitive position and reputation; and could adversely affect our business, financial condition or results of operations.

A significant number of our employees are unionized, and our business and results of operations could be adversely affected if labor agreements were to further restrict our ability to maximize the efficiency of our operations.

Approximately 38% of our full-time equivalent employees were represented by unions as of December 26, 2021, including certain employees at Wirecutter who formed a union in 2019. As a result, we are required to negotiate the wages, benefits and other terms and conditions of employment with many of our employees collectively. In addition, some of our technology employees are seeking to form a union. Our business and results could be adversely affected if future labor negotiations or contracts were to further restrict our ability to maximize the efficiency of our operations, or if a larger percentage of our employees were to unionize. If we are unable to negotiate labor contracts on reasonable terms, or if we were to experience significant labor unrest or other business interruptions in connection with labor negotiations or otherwise, our ability to produce and deliver our products could be impaired. Labor unrest or campaigns by labor organizations have resulted in and may continue to result in negative publicity, which can adversely impact our reputation and our ability to recruit, retain and motivate talent, as well as divert management’s attention and resources. In addition, our ability to make adjustments to control compensation and benefits costs, change our strategy or otherwise adapt to changing business needs may be further limited by the terms and duration of our collective bargaining agreements.

Adverse results from litigation or governmental investigations can impact our business practices and operating results.

From time to time, we are party to litigation, including matters relating to alleged libel or defamation and employment-related matters, as well as regulatory, environmental and other proceedings with governmental authorities and administrative agencies. See Note 18 of the Notes to the Consolidated Financial Statements regarding certain matters. Adverse outcomes in lawsuits or investigations could result in significant monetary damages or injunctive relief that could adversely affect our results of operations or financial condition as well as our ability to conduct our business as it is presently being conducted. In addition, regardless of merit or outcome, such proceedings

THE NEW YORK TIMES COMPANY – P. 15

can have an adverse impact on the Company as a result of legal costs, diversion of management and other personnel, harm to our reputation, and other factors.

Risks Related to Acquisitions, Divestitures and Investments

We incurred substantial costs in our recent acquisitions of The Athletic, and our future investments in connection with the acquisition may prove costlier than we anticipate. As a result, we may not realize the expected benefits as and when we have forecasted or at all.

We completed the acquisition of The Athletic, a global digital subscription-based sports media business, on February 1, 2022 for an all-cash price of approximately $550 million, subject to customary closing adjustments. We also incurred significant non-recurring expenses in connection with this acquisition, including legal, accounting, financial advisory, integration planning and other expenses. We intend to invest additional amounts in an effort to scale The Athletic’s subscriptions business, build its advertising business and make The Athletic, which operated at a loss prior to the acquisition, accretive to our overall profitability.

In addition, while we intend to operate The Athletic as a standalone product, we expect that it will still require significant attention and resources from our management team and others working on the transition. This will include the implementation of public company policies and procedures, including effective internal control over financial reporting and disclosure controls and procedures, legal standards and compliance and information security practices. Devoting resources to this integration of The Athletic into the Company means that these resources will be redeployed to varying degrees from their normal day-to-day activities. This could impair our effectiveness and efficiency and may have an adverse impact on our financial condition or results of operations.

The success of The Athletic acquisition will depend, in part, on our ability to apply our subscription, advertising, marketing and operational expertise to help scale their growth in a profitable, efficient and effective manner. We may not be able to manage The Athletic successfully, or doing so may be costlier than we anticipate, and we may experience difficulty in realizing the expected benefits of this acquisition. Potential difficulties that may be encountered may include the loss of key employees, unknown liabilities, unforeseen expenses and/or other complexities associated with the integration.

We may fail to meet our publicly announced guidance about the impact of The Athletic on our business and future operating results, which would cause our stock price to decline.

Our publicly announced guidance and expectations with respect to the impact of The Athletic acquisition on our revenue growth and operating results are based on forecasts prepared by our management. Forecasts are based upon a number of assumptions and estimates that are inherently subject to significant business, economic and competitive uncertainties and contingencies relating to our business, many of which are beyond our control and/or are based upon specific assumptions with respect to future business decisions, which may change. While all guidance is necessarily speculative in nature, guidance relating to the anticipated results of operations of a recently acquired business is inherently more speculative in nature than other guidance as management will, necessarily, be less familiar with the business, procedures and operations of the recently acquired business. It is possible that some or all of our assumptions regarding The Athletic underlying any guidance furnished by us may turn out not to be correct and actual results may vary significantly from our guidance.

Our business will be impacted by risks applicable to The Athletic.

While we intend to operate The Athletic as a standalone product, its results will be consolidated with ours and accordingly, from the completion of the acquisition, our results are subject to risks and uncertainties affecting its business. These risks include many of the risks outlined elsewhere in these risk factors, as well as others. In our review of The Athletic in connection with the acquisition, we may have failed to identify or fully prepare for all of the problems, liabilities or other shortcomings or challenges facing the business, including issues related to intellectual property, privacy, data protection, information security practices, regulatory compliance practices and tax and employment practices. To the extent unexpected liabilities arise, our recourse to the former owners of The Athletic will be limited and our remedies under customary representation and warranty insurance we obtained in connection with the acquisition may not be adequate to offset such liabilities. As a result, any such liabilities, if significant, could have a material adverse effect on us.

P. 16 – THE NEW YORK TIMES COMPANY

Investments we make in new and existing products and services expose us to risks and challenges that could adversely affect our operations and profitability.

We have invested and expect to continue to invest significant resources to enhance and expand our existing products and services and to acquire and develop new products and services. These investments have included, in addition to The Athletic, among others: enhancements to our core news product and other products (including Games, Cooking, Audm and Wirecutter); investments in various audio, film and television and children’s product initiatives; and investments in our commercial printing and other ancillary operations. These efforts present numerous risks and challenges, including the need for us to appeal to new audiences, develop additional expertise in certain areas, overcome technological and operational challenges and effectively allocate capital resources; new and/or increased costs (including marketing costs and costs to recruit, integrate and retain talented employees); risks associated with strategic relationships such as content licensing; new competitors (some of which may have more resources and experience in certain areas); and additional legal and regulatory risks from expansion into new areas. As a result of these and other risks and challenges, growth into new areas may divert internal resources and the attention of our management and other personnel, including journalists and product and technology specialists.

Although we believe we have a strong and well-established reputation as a global media company, our ability to market our products effectively, and to gain and maintain an audience, particularly for some of our new digital products, is not certain, and if they are not favorably received, our brand may be adversely affected. Even if our new products and services, or enhancements to existing products and services, are favorably received, they may not advance our business strategy as expected, may result in unanticipated costs or liabilities and may fall short of expected return on investment targets or fail to generate sufficient revenue to justify our investments, which could adversely affect our business, results of operations and financial condition.

Acquisitions, divestitures, investments and other transactions could adversely affect our costs, revenues, profitability and financial position.

In order to position our business to take advantage of growth opportunities, we intend to continue to engage in discussions, evaluate opportunities and enter into agreements for possible additional acquisitions, divestitures, investments and other transactions. We may also consider the acquisition of, or investment in, specific properties, businesses or technologies that fall outside our traditional lines of business and diversify our portfolio, including those that may operate in new and developing industries, if we deem such properties sufficiently attractive.

Acquisitions may involve significant risks and uncertainties, including:

•difficulties in integrating acquired businesses (including cultural challenges associated with transitioning employees from the acquired company into our organization);

•failure to identify in advance liabilities, deficiencies, or other claims;

•diversion of management attention from other business concerns or resources;

•use of resources that are needed in other parts of our business;

•possible dilution of our brand or harm to our reputation;

•the potential loss of key employees;

•risks associated with new strategic relationships;

•risks associated with integrating financial reporting, internal control and information technology systems; and

•other unanticipated problems and liabilities.

Competition for certain types of acquisitions is significant. We may not be able to find suitable acquisition candidates, and we may not be able to complete acquisitions or other strategic transactions on favorable terms, or at all. Even if successfully negotiated, closed and integrated, certain acquisitions or investments may prove not to advance our business strategy, may cause us to incur unanticipated costs or liabilities, may result in write-offs of impaired assets, and may fall short of expected return on investment targets, which could adversely affect our business, results of operations and financial condition.

THE NEW YORK TIMES COMPANY – P. 17

In addition, we have divested and may in the future divest certain assets or businesses that no longer fit with our strategic direction or growth targets. Divestitures involve significant risks and uncertainties that could adversely affect our business, results of operations and financial condition. These include, among others, the inability to find potential buyers on favorable terms, disruption to our business and/or diversion of management attention from other business concerns, loss of key employees and possible retention of certain liabilities related to the divested business.

Finally, we have made investments in companies, and we may make similar investments in the future. Investments in these businesses subject us to the operating and financial risks of these businesses and to the risk that we do not have sole control over the operations of these businesses. Our investments are generally illiquid and the absence of a market may inhibit our ability to dispose of them. In addition, if the book value of an investment were to exceed its fair value, we would be required to recognize an impairment charge related to the investment.

Risks Related to Our Operating Costs

The nature of significant portions of our expenses may limit our operating flexibility and could adversely affect our results of operations.

Our main operating costs are employee-related costs, and these costs have increased in recent years as we have invested in our business and competed for talent that is in high demand, and may further increase. Employee-related costs generally do not decrease proportionately with revenues. In addition, our ability to make short-term adjustments to manage our costs or to make changes to our business strategy may be limited by certain of our collective bargaining agreements. If we were unable to implement cost-control efforts or reduce our operating costs sufficiently in response to a decline in our revenues, our profitability will be adversely affected.

The size and volatility of our pension plan obligations may adversely affect our operations, financial condition and liquidity.