falseFY00007166340000716634us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-01-012021-12-310000716634us-gaap:AllowanceForCreditLossMember2021-01-012021-12-310000716634us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-01-012020-12-310000716634us-gaap:AllowanceForCreditLossMember2020-01-012020-12-310000716634us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2019-01-012019-12-310000716634us-gaap:AllowanceForCreditLossMember2019-01-012019-12-310000716634us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-12-310000716634us-gaap:AllowanceForCreditLossMember2021-12-310000716634us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-12-310000716634us-gaap:AllowanceForCreditLossMember2020-12-310000716634us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2019-12-310000716634us-gaap:AllowanceForCreditLossMember2019-12-310000716634us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2018-12-310000716634us-gaap:AllowanceForCreditLossMember2018-12-310000716634rdi:TwentyFiveMillionStockRepurchaseProgramMemberus-gaap:NonvotingCommonStockMember2021-12-310000716634rdi:TwoThousandSeventeenStockRepurchasePlanMember2021-12-310000716634rdi:TwoThousandSeventeenStockRepurchasePlanMemberus-gaap:CommonClassAMember2020-03-100000716634rdi:TwoThousandSeventeenStockRepurchasePlanMember2021-01-012021-12-310000716634rdi:TwoThousandSeventeenStockRepurchasePlanMember2020-03-100000716634rdi:TwentyFiveMillionStockRepurchaseProgramMember2019-03-140000716634rdi:TwentyFiveMillionStockRepurchasedTwoMemberus-gaap:NonvotingCommonStockMember2021-04-012021-06-300000716634rdi:TwentyFiveMillionStockRepurchaseProgramMemberus-gaap:NonvotingCommonStockMember2021-01-012021-12-310000716634rdi:TwentyFiveMillionStockRepurchasedTwoMemberus-gaap:NonvotingCommonStockMember2020-04-012021-12-310000716634rdi:TwentyFiveMillionStockRepurchasedThreeMemberus-gaap:NonvotingCommonStockMember2020-03-052020-03-050000716634us-gaap:CommonClassAMemberus-gaap:CommonStockMember2021-01-012021-12-310000716634us-gaap:RetainedEarningsMember2021-12-310000716634us-gaap:ParentMember2021-12-310000716634us-gaap:NoncontrollingInterestMember2021-12-310000716634us-gaap:AdditionalPaidInCapitalMember2021-12-310000716634us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310000716634srt:CumulativeEffectPeriodOfAdoptionAdjustmentMemberus-gaap:AccountingStandardsUpdate201409Memberus-gaap:RetainedEarningsMember2020-12-310000716634srt:CumulativeEffectPeriodOfAdoptionAdjustmentMemberus-gaap:AccountingStandardsUpdate201409Memberus-gaap:ParentMember2020-12-310000716634srt:CumulativeEffectPeriodOfAdoptionAdjustmentMemberus-gaap:AccountingStandardsUpdate201409Memberus-gaap:NoncontrollingInterestMember2020-12-310000716634srt:CumulativeEffectPeriodOfAdoptionAdjustmentMemberus-gaap:AccountingStandardsUpdate201409Member2020-12-310000716634us-gaap:RetainedEarningsMember2020-12-310000716634us-gaap:ParentMember2020-12-310000716634us-gaap:NoncontrollingInterestMember2020-12-310000716634us-gaap:AdditionalPaidInCapitalMember2020-12-310000716634us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310000716634srt:CumulativeEffectPeriodOfAdoptionAdjustmentMemberus-gaap:AccountingStandardsUpdate201409Memberus-gaap:RetainedEarningsMember2019-12-310000716634srt:CumulativeEffectPeriodOfAdoptionAdjustmentMemberus-gaap:AccountingStandardsUpdate201409Memberus-gaap:ParentMember2019-12-310000716634srt:CumulativeEffectPeriodOfAdoptionAdjustmentMemberus-gaap:AccountingStandardsUpdate201409Memberus-gaap:NoncontrollingInterestMember2019-12-310000716634srt:CumulativeEffectPeriodOfAdoptionAdjustmentMemberus-gaap:AccountingStandardsUpdate201409Member2019-12-310000716634us-gaap:TreasuryStockMember2019-12-310000716634us-gaap:RetainedEarningsMember2019-12-310000716634us-gaap:ParentMember2019-12-310000716634us-gaap:NoncontrollingInterestMember2019-12-310000716634us-gaap:AdditionalPaidInCapitalMember2019-12-310000716634us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-310000716634us-gaap:RetainedEarningsMember2018-12-310000716634us-gaap:ParentMember2018-12-310000716634us-gaap:NoncontrollingInterestMember2018-12-310000716634us-gaap:AdditionalPaidInCapitalMember2018-12-310000716634us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-12-3100007166342018-01-012018-12-310000716634us-gaap:CommonClassAMember2018-12-310000716634us-gaap:CommonClassAMember2019-12-310000716634rdi:NonEmployeeDirectorMember2020-12-162020-12-160000716634us-gaap:CommonClassAMember2020-01-012020-12-310000716634us-gaap:CommonClassAMember2019-01-012019-12-310000716634rdi:TwoThousandTwentyStockIncentivePlanMemberus-gaap:CommonClassBMember2020-12-310000716634rdi:NonEmployeeDirectorMemberus-gaap:RestrictedStockUnitsRSUMember2021-12-082021-12-080000716634rdi:NonEmployeeDirectorMemberus-gaap:RestrictedStockUnitsRSUMember2021-08-112021-08-110000716634us-gaap:RestrictedStockUnitsRSUMember2021-04-012021-04-300000716634rdi:NonEmployeeDirectorMemberus-gaap:RestrictedStockUnitsRSUMember2020-12-162020-12-160000716634us-gaap:RestrictedStockUnitsRSUMember2020-03-102020-03-100000716634rdi:AwardDate6Memberus-gaap:RestrictedStockUnitsRSUMember2021-12-310000716634rdi:AwardDate5Memberus-gaap:RestrictedStockUnitsRSUMember2021-12-310000716634rdi:AwardDate4Memberus-gaap:RestrictedStockUnitsRSUMember2021-12-310000716634rdi:AwardDate3Memberus-gaap:RestrictedStockUnitsRSUMember2021-12-310000716634rdi:EmployeesMemberus-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2021-04-012021-04-300000716634us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2021-04-012021-04-300000716634us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2021-01-012021-12-310000716634rdi:NonEmployeeDirectorMemberus-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2020-12-162020-12-160000716634us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2020-12-142020-12-160000716634us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2018-01-012018-09-300000716634rdi:EmployeesMemberus-gaap:RestrictedStockUnitsRSUMember2021-04-012021-04-300000716634rdi:NonEmployeeDirectorMemberus-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMember2020-12-162020-12-160000716634rdi:NonEmployeeDirectorMemberus-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2020-12-162020-12-160000716634us-gaap:RestrictedStockUnitsRSUMember2020-12-142020-12-160000716634rdi:StateCinemaHobartTasmaniaAustraliaMember2021-01-012021-12-310000716634rdi:ShadowViewLandAndFarmingLlcMemberrdi:CoachellaMember2021-03-052021-03-050000716634rdi:EstateOfJamesJ.CotterSr.Memberrdi:CoachellaMember2021-03-052021-03-050000716634rdi:ShadowViewLandAndFarmingLlcMemberrdi:CoachellaMember2021-01-012021-03-310000716634us-gaap:IntersegmentEliminationMemberrdi:RealEstateSegmentMember2021-01-012021-12-310000716634us-gaap:IntersegmentEliminationMemberrdi:RealEstateSegmentMember2020-01-012020-12-310000716634us-gaap:IntersegmentEliminationMemberrdi:RealEstateSegmentMember2019-01-012019-12-310000716634rdi:UnitedStatesBankOfAmericaCreditFacilityMember2021-11-082021-11-080000716634rdi:RevolvingCorporateMarketsLoanFacilityMember2021-06-092021-06-090000716634rdi:UnitedStatesUnionSquareTermLoanMessanineMember2019-08-082019-08-080000716634rdi:SuttonHillCapitalLlcMember2007-06-282007-06-280000716634rdi:RoyalGeorgeTheatreMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMember2021-02-280000716634rdi:AuburnRedyardMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMember2021-01-310000716634rdi:ManukauMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMember2020-12-310000716634rdi:CoachellaMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMember2020-12-310000716634srt:MinimumMemberus-gaap:FurnitureAndFixturesMember2021-01-012021-12-310000716634srt:MinimumMemberus-gaap:BuildingAndBuildingImprovementsMember2021-01-012021-12-310000716634srt:MaximumMemberus-gaap:FurnitureAndFixturesMember2021-01-012021-12-310000716634srt:MaximumMemberus-gaap:BuildingAndBuildingImprovementsMember2021-01-012021-12-310000716634us-gaap:EquipmentMember2021-01-012021-12-310000716634us-gaap:RetainedEarningsMember2021-01-012021-12-310000716634us-gaap:RetainedEarningsMember2019-01-012019-12-310000716634rdi:RoyalGeorgeTheatreMember2021-06-302021-06-300000716634rdi:CoachellaMember2021-03-052021-03-0500007166342020-10-012020-10-010000716634rdi:AllSegmentsMember2021-01-012021-12-310000716634us-gaap:CorporateMember2020-01-012020-12-310000716634rdi:AllSegmentsMember2020-01-012020-12-310000716634us-gaap:CorporateMember2019-01-012019-12-310000716634rdi:AllSegmentsMember2019-01-012019-12-310000716634rdi:SuttonHillPropertiesMemberrdi:SuttonHillCapitalLlcMember2020-10-012020-10-010000716634rdi:SuttonHillPropertiesMember2020-10-012020-10-010000716634us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310000716634us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310000716634us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-01-012019-12-310000716634us-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2021-01-012021-12-310000716634us-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2020-01-012020-12-310000716634rdi:DebtCurrentAndNoncurrentMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310000716634rdi:DebtCurrentAndNoncurrentMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310000716634rdi:DebtCurrentAndNoncurrentMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310000716634rdi:DebtCurrentAndNoncurrentMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2020-12-310000716634rdi:DebtCurrentAndNoncurrentMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2020-12-310000716634rdi:DebtCurrentAndNoncurrentMemberus-gaap:FairValueMeasurementsNonrecurringMember2020-12-310000716634rdi:SuttonHillPropertiesMember2019-01-012019-12-310000716634rdi:ShadowViewLandAndFarmingLlcMember2019-01-012019-12-310000716634rdi:AustraliaCountryCinemasMember2019-01-012019-12-310000716634rdi:SuttonHillPropertiesMemberrdi:UnitedStateCinemasOneTwoThreeTermLoanMember2021-12-310000716634rdi:SuttonHillPropertiesMember2021-12-310000716634rdi:SuttonHillCapitalLlcMember2021-12-310000716634rdi:AustraliaCountryCinemasMember2021-12-310000716634rdi:ShadowViewLandAndFarmingLlcMembersrt:ChiefExecutiveOfficerMember2012-12-310000716634us-gaap:NoncontrollingInterestMember2021-01-012021-12-310000716634us-gaap:NoncontrollingInterestMember2020-01-012020-12-310000716634us-gaap:NoncontrollingInterestMember2019-01-012019-12-3100007166342009-03-310000716634rdi:JamesJ.CotterJr.DerivativeLitigationMember2020-10-012020-10-010000716634rdi:UnitedStatesBankOfAmericaCreditFacilityAmendedMember2021-12-310000716634us-gaap:ScenarioPlanMemberrdi:RevolvingCorporateMarketsLoanFacilityAmendedMember2021-12-290000716634rdi:JindaleeQueenslandMemberrdi:RevolvingCorporateMarketsLoanFacilityMember2021-12-290000716634rdi:RevolvingCorporateMarketsLoanFacilityMember2021-12-290000716634rdi:RevolvingCorporateMarketsLoanFacilityAmendedMember2021-12-290000716634rdi:UnitedStatesUnionSquareTermLoanEmeraldCreekCapitalMember2021-05-070000716634us-gaap:RevolvingCreditFacilityMemberrdi:CorporateLoanFacilityMember2019-03-150000716634rdi:CoreFacilityMemberrdi:CorporateLoanFacilityMember2019-03-150000716634rdi:RevolvingCorporateMarketsLoanFacilityMember2019-03-150000716634rdi:CorporateLoanFacilityMember2019-03-150000716634rdi:UnitedStatesUnionSquareTermLoanSunLifeMember2016-12-290000716634rdi:UnitedStatesUnionSquareTermLoanMessanineMember2016-12-290000716634rdi:UnitedStatesUnionSquareTermLoanFirstMortgageMember2016-12-290000716634rdi:RealEstateRevenueMembersrt:MinimumMember2021-12-310000716634rdi:RealEstateRevenueMembersrt:MaximumMember2021-12-310000716634rdi:VillageEastCinemaMemberrdi:SuttonHillCapitalLlcMember2021-12-310000716634rdi:CinemaMembersrt:MinimumMember2021-12-310000716634rdi:CinemaMembersrt:MaximumMember2021-12-310000716634rdi:VillageEastCinemaMember2021-12-310000716634rdi:VillageEastCinemaMember2021-12-310000716634rdi:LiquorLicensesMember2021-12-310000716634rdi:LiquorLicensesMember2020-12-310000716634rdi:MtGravattCinemaMember2021-01-012021-12-310000716634rdi:RialtoCinemasMember2020-01-012020-12-310000716634rdi:MtGravattCinemaMember2020-01-012020-12-310000716634rdi:RialtoCinemasMember2019-01-012019-12-310000716634rdi:MtGravattCinemaMember2019-01-012019-12-310000716634us-gaap:ForeignCountryMember2021-01-012021-12-310000716634country:US2021-01-012021-12-310000716634us-gaap:ForeignCountryMember2020-01-012020-12-310000716634country:US2020-01-012020-12-310000716634us-gaap:ForeignCountryMember2019-01-012019-12-310000716634country:US2019-01-012019-12-310000716634rdi:NonIncomeproducingPropertiesMember2020-01-012020-12-310000716634rdi:CinemaExhibitionSegmentMember2020-01-012020-12-310000716634rdi:BusinessSegmentCinemaMember2021-01-012021-12-310000716634rdi:BusinessSegmentCinemaMember2020-01-012020-12-310000716634rdi:BusinessSegmentRealEstateMember2021-12-310000716634rdi:BusinessSegmentCinemaMember2021-12-310000716634rdi:BusinessSegmentRealEstateMember2020-12-310000716634rdi:BusinessSegmentCinemaMember2020-12-310000716634rdi:BusinessSegmentRealEstateMember2019-12-310000716634rdi:BusinessSegmentCinemaMember2019-12-310000716634us-gaap:OperatingSegmentsMemberrdi:AllSegmentsMemberrdi:RealEstateSegmentMember2021-01-012021-12-310000716634us-gaap:OperatingSegmentsMemberrdi:AllSegmentsMemberrdi:CinemaExhibitionSegmentMember2021-01-012021-12-310000716634us-gaap:OperatingSegmentsMemberrdi:AllSegmentsMember2021-01-012021-12-310000716634us-gaap:OperatingSegmentsMemberrdi:AllSegmentsMemberrdi:RealEstateSegmentMember2020-01-012020-12-310000716634us-gaap:OperatingSegmentsMemberrdi:AllSegmentsMemberrdi:CinemaExhibitionSegmentMember2020-01-012020-12-310000716634us-gaap:OperatingSegmentsMemberrdi:AllSegmentsMember2020-01-012020-12-310000716634us-gaap:OperatingSegmentsMemberrdi:AllSegmentsMemberrdi:RealEstateSegmentMember2019-01-012019-12-310000716634us-gaap:OperatingSegmentsMemberrdi:AllSegmentsMemberrdi:CinemaExhibitionSegmentMember2019-01-012019-12-310000716634us-gaap:OperatingSegmentsMemberrdi:AllSegmentsMember2019-01-012019-12-310000716634srt:MaximumMemberus-gaap:TradeNamesMember2021-01-012021-12-310000716634us-gaap:OtherIntangibleAssetsMember2021-01-012021-12-310000716634rdi:BeneficialLeasesMember2021-01-012021-12-310000716634us-gaap:TradeNamesMember2021-12-310000716634rdi:BeneficialLeasesMember2021-12-310000716634us-gaap:TradeNamesMember2020-12-310000716634us-gaap:OtherIntangibleAssetsMember2020-12-310000716634rdi:BeneficialLeasesMember2020-12-310000716634us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310000716634us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310000716634us-gaap:FairValueMeasurementsNonrecurringMember2021-12-310000716634us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2020-12-310000716634us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2020-12-310000716634us-gaap:FairValueMeasurementsNonrecurringMember2020-12-310000716634us-gaap:SubordinatedDebtMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310000716634us-gaap:SubordinatedDebtMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310000716634us-gaap:SubordinatedDebtMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310000716634us-gaap:SubordinatedDebtMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2020-12-310000716634us-gaap:SubordinatedDebtMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2020-12-310000716634us-gaap:SubordinatedDebtMemberus-gaap:FairValueMeasurementsNonrecurringMember2020-12-310000716634rdi:TrustPreferredSecuritiesMember2009-04-292009-04-300000716634rdi:RialtoCinemasMember2020-12-310000716634rdi:MtGravattCinemaMember2020-12-310000716634srt:MinimumMember2021-12-310000716634srt:MaximumMember2021-12-310000716634us-gaap:RestrictedStockUnitsRSUMember2021-12-310000716634us-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2020-12-310000716634us-gaap:DesignatedAsHedgingInstrumentMember2020-12-310000716634us-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:InterestExpenseMember2021-01-012021-12-310000716634us-gaap:DesignatedAsHedgingInstrumentMember2021-01-012021-12-310000716634us-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:InterestExpenseMember2020-01-012020-12-310000716634us-gaap:DesignatedAsHedgingInstrumentMember2020-01-012020-12-310000716634us-gaap:InterestRateContractMemberus-gaap:InterestExpenseMember2021-01-012021-12-310000716634us-gaap:InterestRateContractMemberus-gaap:InterestExpenseMember2020-01-012020-12-310000716634rdi:UnfavorableMember2021-12-310000716634rdi:FavorableMember2021-12-310000716634rdi:UnfavorableMember2020-12-310000716634rdi:FavorableMember2020-12-310000716634us-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2021-12-310000716634us-gaap:FairValueMeasurementsRecurringMember2021-12-310000716634us-gaap:DesignatedAsHedgingInstrumentMember2021-12-310000716634us-gaap:FairValueMeasurementsRecurringMember2020-12-310000716634us-gaap:CorporateNonSegmentMember2021-01-012021-12-310000716634us-gaap:CorporateNonSegmentMember2020-01-012020-12-310000716634us-gaap:CorporateNonSegmentMember2019-01-012019-12-310000716634us-gaap:SupplementalEmployeeRetirementPlanDefinedBenefitMember2014-08-2900007166342014-08-290000716634us-gaap:DomesticCountryMember2021-12-310000716634stpr:NJ2021-12-310000716634stpr:HI2021-12-310000716634stpr:CA2021-12-310000716634rdi:NewYorkStateMember2021-12-310000716634rdi:NewYorkCityMember2021-12-310000716634rdi:UnitedStatesUnionSquareTermLoanEmeraldCreekCapitalMember2021-05-072021-05-070000716634rdi:UnitedStatesUnionSquareTermLoanEmeraldCreekCapitalExtensionMember2021-05-072021-05-070000716634rdi:MinettaAndOrpheumTheatresLoanMemberrdi:SantanderBankMember2021-01-012021-12-310000716634rdi:UnitedStatesUnionSquareTermLoanFirstMortgageMember2020-01-242020-01-240000716634rdi:TrustPreferredSecuritiesMember2007-02-042007-02-050000716634rdi:JindaleeQueenslandMemberrdi:RevolvingCorporateMarketsLoanFacilityMember2021-12-292021-12-290000716634rdi:RevolvingCorporateMarketsLoanFacilityMember2021-08-060000716634rdi:UnitedStatesUnionSquareTermLoanFirstMortgageMember2020-12-290000716634rdi:NewZealandCorporateCreditFacilityMember2020-06-290000716634rdi:UnitedStateCinemasOneTwoThreeTermLoanMember2020-03-130000716634rdi:PurchaseMoneyPromissoryNoteMember2019-09-180000716634rdi:RevolvingCorporateMarketsLoanFacilityAmendedMember2019-03-150000716634rdi:BankGuaranteeFacilityMember2019-03-150000716634rdi:NewZealandCorporateCreditFacilityTranchOneMember2018-12-200000716634rdi:UnitedStateCorporateOfficeTermLoanMember2017-06-260000716634rdi:UnitedStateCorporateOfficeTermLoanMember2016-12-130000716634rdi:UnitedStateCinemasOneTwoThreeTermLoanMember2016-08-310000716634srt:MinimumMemberrdi:UnitedStateCorporateOfficeTermLoanMember2021-01-012021-12-310000716634srt:MaximumMemberrdi:UnitedStateCorporateOfficeTermLoanMember2021-01-012021-12-310000716634srt:MinimumMemberrdi:UnitedStateCorporateOfficeTermLoanMember2020-01-012020-12-310000716634srt:MaximumMemberrdi:UnitedStateCorporateOfficeTermLoanMember2020-01-012020-12-310000716634rdi:UnitedStateCorporateOfficeTermLoanMember2017-06-262017-06-260000716634rdi:TrustPreferredSecuritiesMember2009-03-310000716634srt:MinimumMemberrdi:UnitedStatesUnionSquareTermLoanEmeraldCreekCapitalMemberus-gaap:LondonInterbankOfferedRateLIBORMember2021-05-072021-05-070000716634rdi:UnitedStatesUnionSquareTermLoanEmeraldCreekCapitalMemberus-gaap:LondonInterbankOfferedRateLIBORMember2021-05-072021-05-070000716634srt:MinimumMemberrdi:UnitedStatesBankOfAmericaCreditFacilityAmendedMemberus-gaap:EurodollarMember2021-01-012021-12-310000716634srt:MaximumMemberrdi:UnitedStatesBankOfAmericaCreditFacilityAmendedMemberus-gaap:EurodollarMember2021-01-012021-12-310000716634rdi:UnitedStatesBankOfAmericaCreditFacilityMemberus-gaap:EurodollarMember2020-08-072020-08-070000716634rdi:UnitedStatesBankOfAmericaCreditFacilityMember2020-08-072020-08-070000716634rdi:UnitedStatesBankOfAmericaLineOfCreditMemberus-gaap:LondonInterbankOfferedRateLIBORMember2020-03-062020-03-060000716634srt:MinimumMemberrdi:CorporateLoanFacilityMember2019-03-152019-03-150000716634srt:MaximumMemberrdi:CorporateLoanFacilityMember2019-03-152019-03-150000716634rdi:RevolvingCorporateMarketsLoanFacilityMemberrdi:BankBillSwapBidRateMember2019-03-152019-03-150000716634rdi:SuttonHillCapitalLlcMember2007-06-280000716634rdi:RealEstateRevenueMember2021-01-012021-12-310000716634rdi:CinemaMember2021-01-012021-12-310000716634rdi:RealEstateRevenueMember2020-01-012020-12-310000716634rdi:CinemaMember2020-01-012020-12-310000716634rdi:RealEstateRevenueMember2019-01-012019-12-310000716634rdi:CinemaMember2019-01-012019-12-310000716634us-gaap:OperatingSegmentsMemberrdi:ThirdPartyMemberrdi:RealEstateSegmentMember2021-01-012021-12-310000716634us-gaap:OperatingSegmentsMemberrdi:ThirdPartyMemberrdi:CinemaExhibitionSegmentMember2021-01-012021-12-310000716634us-gaap:OperatingSegmentsMemberrdi:ThirdPartyMember2021-01-012021-12-310000716634us-gaap:OperatingSegmentsMemberrdi:RealEstateSegmentMember2021-01-012021-12-310000716634us-gaap:OperatingSegmentsMemberrdi:CinemaExhibitionSegmentMember2021-01-012021-12-310000716634us-gaap:IntersegmentEliminationMemberrdi:CinemaExhibitionSegmentMember2021-01-012021-12-310000716634us-gaap:OperatingSegmentsMember2021-01-012021-12-310000716634us-gaap:IntersegmentEliminationMember2021-01-012021-12-310000716634us-gaap:OperatingSegmentsMemberrdi:ThirdPartyMemberrdi:RealEstateSegmentMember2020-01-012020-12-310000716634us-gaap:OperatingSegmentsMemberrdi:ThirdPartyMemberrdi:CinemaExhibitionSegmentMember2020-01-012020-12-310000716634us-gaap:OperatingSegmentsMemberrdi:ThirdPartyMember2020-01-012020-12-310000716634us-gaap:OperatingSegmentsMemberrdi:RealEstateSegmentMember2020-01-012020-12-310000716634us-gaap:OperatingSegmentsMemberrdi:CinemaExhibitionSegmentMember2020-01-012020-12-310000716634us-gaap:IntersegmentEliminationMemberrdi:CinemaExhibitionSegmentMember2020-01-012020-12-310000716634us-gaap:OperatingSegmentsMember2020-01-012020-12-310000716634us-gaap:IntersegmentEliminationMember2020-01-012020-12-310000716634us-gaap:OperatingSegmentsMemberrdi:ThirdPartyMemberrdi:RealEstateSegmentMember2019-01-012019-12-310000716634us-gaap:OperatingSegmentsMemberrdi:ThirdPartyMemberrdi:CinemaExhibitionSegmentMember2019-01-012019-12-310000716634us-gaap:OperatingSegmentsMemberrdi:ThirdPartyMember2019-01-012019-12-310000716634us-gaap:OperatingSegmentsMemberrdi:RealEstateSegmentMember2019-01-012019-12-310000716634us-gaap:OperatingSegmentsMemberrdi:CinemaExhibitionSegmentMember2019-01-012019-12-310000716634us-gaap:IntersegmentEliminationMemberrdi:CinemaExhibitionSegmentMember2019-01-012019-12-310000716634us-gaap:OperatingSegmentsMember2019-01-012019-12-310000716634us-gaap:IntersegmentEliminationMember2019-01-012019-12-310000716634us-gaap:CommonClassBMemberus-gaap:CommonStockMember2021-12-310000716634us-gaap:CommonClassAMemberus-gaap:CommonStockMember2021-12-310000716634us-gaap:TreasuryStockMember2021-12-310000716634us-gaap:CommonClassBMemberus-gaap:CommonStockMember2020-12-310000716634us-gaap:CommonClassAMemberus-gaap:CommonStockMember2020-12-310000716634us-gaap:TreasuryStockMember2020-12-310000716634us-gaap:CommonClassBMemberus-gaap:CommonStockMember2019-12-310000716634us-gaap:CommonClassAMemberus-gaap:CommonStockMember2019-12-310000716634us-gaap:CommonClassBMemberus-gaap:CommonStockMember2018-12-310000716634us-gaap:CommonClassAMemberus-gaap:CommonStockMember2018-12-310000716634us-gaap:TreasuryStockMember2018-12-310000716634us-gaap:CommonClassBMember2021-12-310000716634us-gaap:CommonClassAMember2021-12-310000716634us-gaap:CommonClassBMember2020-12-310000716634us-gaap:CommonClassAMember2020-12-310000716634rdi:TwoThousandTwentyStockIncentivePlanMemberus-gaap:CommonClassAMember2021-12-310000716634rdi:TwoThousandTwentyStockIncentivePlanMember2020-12-3100007166342021-01-012021-06-3000007166342018-12-310000716634rdi:SuttonHillCapitalLlcMember2015-02-280000716634us-gaap:CorporateMember2021-12-310000716634rdi:RealEstateSegmentMember2021-12-310000716634rdi:CinemaExhibitionSegmentMember2021-12-310000716634rdi:AllCountryMember2021-12-310000716634country:US2021-12-310000716634country:NZ2021-12-310000716634country:AU2021-12-310000716634us-gaap:CorporateMember2020-12-310000716634rdi:RealEstateSegmentMember2020-12-310000716634rdi:CinemaExhibitionSegmentMember2020-12-310000716634rdi:AllCountryMember2020-12-310000716634country:US2020-12-310000716634country:NZ2020-12-310000716634country:AU2020-12-310000716634rdi:ShadowViewLandAndFarmingLlcMember2021-12-310000716634rdi:TrustPreferredSecuritiesMember2009-01-012009-12-310000716634us-gaap:StockOptionMember2021-01-012021-12-310000716634us-gaap:StockOptionMember2020-01-012020-12-310000716634us-gaap:RestrictedStockUnitsRSUMember2020-01-012020-12-310000716634us-gaap:StockOptionMember2019-01-012019-12-310000716634us-gaap:ParentMember2021-01-012021-12-310000716634us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310000716634us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310000716634us-gaap:AccumulatedTranslationAdjustmentMember2021-12-310000716634us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2021-12-310000716634us-gaap:AccumulatedGainLossNetCashFlowHedgeParentMember2021-12-310000716634us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-12-310000716634us-gaap:AccumulatedTranslationAdjustmentMember2020-12-310000716634us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2020-12-310000716634us-gaap:AccumulatedGainLossNetCashFlowHedgeParentMember2020-12-310000716634us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2020-12-310000716634us-gaap:BuildingAndBuildingImprovementsMember2021-12-310000716634us-gaap:BuildingAndBuildingImprovementsMember2020-12-310000716634rdi:VillageEastCinemaMember2020-12-310000716634rdi:Covid19Member2020-12-310000716634rdi:TrustPreferredSecuritiesMember2007-02-050000716634rdi:TrustPreferredSecuritiesMember2019-01-012019-12-310000716634us-gaap:ParentMember2020-01-012020-12-310000716634us-gaap:CommonClassAMemberus-gaap:CommonStockMember2020-01-012020-12-310000716634us-gaap:TreasuryStockMember2020-01-012020-12-310000716634us-gaap:CommonClassAMemberus-gaap:CommonStockMember2019-01-012019-12-310000716634us-gaap:TreasuryStockMember2019-01-012019-12-310000716634rdi:ShareRepurchasedProgramMember2019-09-182019-09-180000716634rdi:PurchaseMoneyPromissoryNoteMember2019-09-182019-09-180000716634rdi:AwardDate6Memberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310000716634rdi:AwardDate5Memberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310000716634rdi:AwardDate4Memberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310000716634rdi:AwardDate3Memberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310000716634rdi:AwardDate2Memberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310000716634rdi:AwardDate1Memberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310000716634us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-3100007166342021-03-050000716634rdi:RoyalGeorgeTheatreMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMember2021-02-012021-02-280000716634rdi:ManukauMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMember2020-12-012020-12-310000716634rdi:CoachellaMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMember2020-12-012020-12-310000716634rdi:InvercargillMember2021-08-300000716634rdi:AuburnRedyardMember2021-06-090000716634rdi:ShadowViewLandAndFarmingLlcMemberrdi:CoachellaMember2021-03-050000716634rdi:ManukauMember2021-03-040000716634rdi:ManukauMember2021-02-230000716634rdi:VillageEastCinemaMember2019-08-280000716634rdi:SuttonHillCapitalsInterestInSuttonHillPropertiesMember2021-12-310000716634us-gaap:LandMember2021-12-310000716634rdi:ConstructionInProgressIncludingCapitalizedInterestMember2021-12-310000716634us-gaap:LandMember2020-12-310000716634rdi:ConstructionInProgressIncludingCapitalizedInterestMember2020-12-310000716634rdi:ShadowViewLandAndFarmingLlcMembersrt:ChiefExecutiveOfficerMember2012-01-012012-12-310000716634rdi:JamesCotterAndMichaelFormanMember2021-01-012021-12-310000716634us-gaap:AccumulatedTranslationAdjustmentMember2021-01-012021-12-310000716634us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2021-01-012021-12-310000716634us-gaap:AccumulatedGainLossNetCashFlowHedgeParentMember2021-01-012021-12-310000716634us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-01-012021-12-310000716634rdi:RialtoCinemasMember2021-12-310000716634rdi:MtGravattCinemaMember2021-12-310000716634rdi:RialtoCinemasMember2021-01-012021-12-310000716634rdi:SuttonHillPropertiesMember2021-01-012021-12-310000716634rdi:ShadowViewLandAndFarmingLlcMember2021-01-012021-12-310000716634rdi:AustraliaCountryCinemasMember2021-01-012021-12-310000716634rdi:SuttonHillPropertiesMember2020-01-012020-12-310000716634rdi:ShadowViewLandAndFarmingLlcMember2020-01-012020-12-310000716634rdi:AustraliaCountryCinemasMember2020-01-012020-12-310000716634rdi:EightySixthStreetCinemaMember2021-01-012021-12-310000716634rdi:SuttonHillCapitalLlcMember2020-11-062020-11-060000716634rdi:EightySixthStreetCinemaMember2020-01-012020-12-310000716634rdi:EightySixthStreetCinemaMember2019-01-012019-12-310000716634rdi:UnitedStateCinemasOneTwoThreeMember2016-01-012016-12-310000716634rdi:UnitedStatesUnionSquareLineOfCreditMember2021-12-310000716634rdi:UnitedStatesBankOfAmericaCreditFacilityMember2021-12-310000716634rdi:UnitedStateCorporateOfficeTermLoanMember2021-12-310000716634rdi:UnitedStateCinemasOneTwoThreeTermLoanMember2021-12-310000716634rdi:TrustPreferredSecuritiesMember2021-12-310000716634rdi:PurchaseMoneyPromissoryNoteMember2021-12-310000716634rdi:NewZealandCorporateCreditFacilityMember2021-12-310000716634rdi:NationalAustraliaBankAustralianCorporateTermLoanMember2021-12-310000716634rdi:MinettaAndOrpheumTheatresLoanMember2021-12-310000716634rdi:UnitedStatesUnionSquareLineOfCreditMember2020-12-310000716634rdi:UnitedStatesBankOfAmericaLineOfCreditMember2020-12-310000716634rdi:UnitedStatesBankOfAmericaCreditFacilityMember2020-12-310000716634rdi:UnitedStateCorporateOfficeTermLoanMember2020-12-310000716634rdi:UnitedStateCinemasOneTwoThreeTermLoanMember2020-12-310000716634rdi:TrustPreferredSecuritiesMember2020-12-310000716634rdi:PurchaseMoneyPromissoryNoteMember2020-12-310000716634rdi:NewZealandCorporateCreditFacilityMember2020-12-310000716634rdi:NationalAustraliaBankAustralianCorporateLoanFacilityMember2020-12-310000716634rdi:MinettaAndOrpheumTheatresLoanMember2020-12-310000716634rdi:UnitedStatesBankOfAmericaLineOfCreditMember2020-03-060000716634rdi:NewZealandCorporateCreditFacilityMember2021-08-302021-08-300000716634rdi:NewZealandCorporateCreditFacilityMember2021-05-072021-05-070000716634rdi:NewZealandCorporateCreditFacilityTranchTwoMember2018-12-202018-12-200000716634rdi:NewZealandCorporateCreditFacilityTranchOneMember2018-12-202018-12-200000716634rdi:NewZealandCorporateCreditFacilityTranchOneMember2018-12-192018-12-1900007166342019-12-3100007166342009-12-3100007166342007-02-050000716634rdi:UnitedStateCinemasOneTwoThreeMember2020-01-012020-12-310000716634rdi:UnitedStateCinemasOneTwoThreeMember2019-01-012019-12-310000716634rdi:SuttonHillCapitalLlcMember2021-01-012021-12-310000716634currency:NZDrdi:SpotRateMember2021-01-012021-12-310000716634currency:NZDrdi:AverageRateMember2021-01-012021-12-310000716634currency:AUDrdi:SpotRateMember2021-01-012021-12-310000716634currency:AUDrdi:AverageRateMember2021-01-012021-12-310000716634currency:NZDrdi:SpotRateMember2020-01-012020-12-310000716634currency:NZDrdi:AverageRateMember2020-01-012020-12-310000716634currency:AUDrdi:SpotRateMember2020-01-012020-12-310000716634currency:AUDrdi:AverageRateMember2020-01-012020-12-310000716634currency:NZDrdi:SpotRateMember2019-01-012019-12-310000716634currency:NZDrdi:AverageRateMember2019-01-012019-12-310000716634currency:AUDrdi:SpotRateMember2019-01-012019-12-310000716634currency:AUDrdi:AverageRateMember2019-01-012019-12-310000716634us-gaap:OtherIntangibleAssetsMember2021-12-310000716634rdi:TrustPreferredSecuritiesMember2015-12-310000716634rdi:TrustPreferredSecuritiesMember2008-12-310000716634rdi:TrustPreferredSecuritiesMember2011-12-012011-12-310000716634rdi:TrustPreferredSecuritiesMember2008-12-302008-12-310000716634rdi:RoyalGeorgeTheatreMember2021-01-012021-12-310000716634rdi:ManukauMember2021-01-012021-12-310000716634rdi:InvercargillMember2021-01-012021-12-310000716634rdi:CoachellaMember2021-01-012021-12-310000716634rdi:AuburnRedyardMember2021-01-012021-12-310000716634srt:ChiefExecutiveOfficerMember2021-01-012021-12-310000716634rdi:TrustPreferredSecuritiesMember2012-05-012012-05-010000716634rdi:NewZealandCorporateCreditFacilityMemberrdi:BankBillSwapBidRateMember2020-06-292020-06-290000716634rdi:NewZealandCorporateCreditFacilityTranchOneMemberrdi:BankBillSwapBidRateMember2018-12-202018-12-200000716634rdi:UnitedStatesUnionSquareLineOfCreditMember2021-01-012021-12-310000716634rdi:UnitedStatesBankOfAmericaCreditFacilityMember2021-01-012021-12-310000716634rdi:UnitedStateCorporateOfficeTermLoanMember2021-01-012021-12-310000716634rdi:UnitedStateCinemasOneTwoThreeTermLoanMember2021-01-012021-12-310000716634rdi:PurchaseMoneyPromissoryNoteMember2021-01-012021-12-310000716634rdi:NewZealandCorporateCreditFacilityMember2021-01-012021-12-310000716634rdi:NationalAustraliaBankAustralianCorporateTermLoanMember2021-01-012021-12-310000716634rdi:MinettaAndOrpheumTheatresLoanMember2021-01-012021-12-310000716634rdi:UnitedStateCinemasOneTwoThreeTermLoanMember2020-03-132020-03-130000716634rdi:UnitedStatesUnionSquareLineOfCreditMember2020-01-012020-12-310000716634rdi:UnitedStatesBankOfAmericaLineOfCreditMember2020-01-012020-12-310000716634rdi:UnitedStatesBankOfAmericaCreditFacilityMember2020-01-012020-12-310000716634rdi:UnitedStateCorporateOfficeTermLoanMember2020-01-012020-12-310000716634rdi:UnitedStateCinemasOneTwoThreeTermLoanMember2020-01-012020-12-310000716634rdi:TrustPreferredSecuritiesMember2020-01-012020-12-310000716634rdi:PurchaseMoneyPromissoryNoteMember2020-01-012020-12-310000716634rdi:NewZealandCorporateCreditFacilityMember2020-01-012020-12-310000716634rdi:NationalAustraliaBankAustralianCorporateLoanFacilityMember2020-01-012020-12-310000716634rdi:MinettaAndOrpheumTheatresLoanMember2020-01-012020-12-310000716634rdi:MinettaAndOrpheumTheatresLoanMemberrdi:SantanderBankMember2018-10-122018-10-120000716634rdi:MinettaAndOrpheumTheatresLoanMember2018-10-122018-10-120000716634rdi:TrustPreferredSecuritiesMember2018-10-112018-10-110000716634rdi:UnitedStateCorporateOfficeTermLoanMember2016-12-132016-12-130000716634rdi:UnitedStateCinemasOneTwoThreeTermLoanMemberrdi:SantanderBankMember2016-08-312016-08-310000716634rdi:SuttonHillPropertiesMemberrdi:UnitedStateCinemasOneTwoThreeTermLoanMember2016-08-312016-08-310000716634rdi:UnitedStateCinemasOneTwoThreeTermLoanMember2016-08-312016-08-310000716634rdi:SuttonHillCapitalLlcMember2016-01-012016-12-3100007166342016-01-012016-12-310000716634rdi:TrustPreferredSecuritiesMember2008-01-012008-12-310000716634rdi:TrustPreferredSecuritiesMember2021-01-012021-12-310000716634rdi:InvercargillMember2021-09-300000716634rdi:RoyalGeorgeTheatreMember2021-06-300000716634rdi:AuburnRedyardMember2021-06-300000716634rdi:ManukauMember2021-03-310000716634rdi:CoachellaMember2021-03-310000716634rdi:TrustPreferredSecuritiesMember2018-10-310000716634rdi:JamesJ.CotterJr.LitigationMattersMemberrdi:CotterVotingTrustMemberus-gaap:CommonClassBMember2021-01-012021-12-310000716634rdi:JamesJ.CotterJr.LitigationMattersMemberrdi:CotterTrustMemberus-gaap:CommonClassBMember2021-01-012021-12-310000716634rdi:JamesJ.CotterJr.LitigationMattersMemberrdi:CotterEstateMemberus-gaap:CommonClassBMember2021-01-012021-12-310000716634rdi:JamesJ.CotterJr.LitigationMattersMemberrdi:CotterVotingTrustMemberus-gaap:CommonClassBMember2021-12-310000716634rdi:JamesJ.CotterJr.LitigationMattersMemberrdi:CotterTrustMemberus-gaap:CommonClassBMember2021-12-310000716634rdi:JamesJ.CotterJr.LitigationMattersMemberrdi:CotterEstateMemberus-gaap:CommonClassBMember2021-12-310000716634us-gaap:ParentMember2019-01-012019-12-310000716634us-gaap:AdditionalPaidInCapitalMember2019-01-012019-12-310000716634rdi:StateCinemaHobartTasmaniaAustraliaMember2020-03-310000716634rdi:StateCinemaHobartTasmaniaAustraliaMember2019-12-030000716634rdi:StateCinemaHobartTasmaniaAustraliaMember2019-12-042020-03-310000716634srt:ChiefExecutiveOfficerMember2012-01-012012-12-310000716634rdi:UnitedStateCinemasOneTwoThreeMemberrdi:SuttonHillCapitalLlcMember2021-01-012021-12-310000716634rdi:UnitedStateCinemasOneTwoThreeMember2015-01-012015-01-010000716634country:NZ2021-01-012021-12-310000716634country:AU2021-01-012021-12-310000716634country:NZ2020-01-012020-12-310000716634country:AU2020-01-012020-12-3100007166342020-01-012020-12-3100007166342019-01-012019-12-310000716634rdi:AuburnRedyardMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMember2021-01-012021-01-3100007166342021-12-3100007166342020-12-310000716634us-gaap:CommonClassBMember2021-01-012021-12-310000716634us-gaap:CommonClassAMember2021-01-012021-12-3100007166342020-06-300000716634us-gaap:CommonClassBMember2022-03-150000716634us-gaap:CommonClassAMember2022-03-1500007166342021-01-012021-12-31rdi:segmentiso4217:USDxbrli:sharesrdi:itemxbrli:pureiso4217:NZDiso4217:AUDutr:acreiso4217:USDxbrli:shares

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2021 or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______ to ______

Commission File No. 1-8625

READING INTERNATIONAL, INC.

(Exact name of registrant as specified in its charter)

| |

Nevada (State or other jurisdiction of incorporation or organization) 189 Second Avenue, Suite 2S New York New York (Address of principal executive offices) | 95-3885184 (I.R.S. Employer Identification Number) 10003 (Zip Code) |

Registrant’s telephone number, including Area Code: (213) 235-2240

Securities Registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | Trading Symbol | Name of each exchange on which registered |

Class A Nonvoting Common Stock, $0.01 par value | RDI | NASDAQ |

Class B Voting Common Stock, $0.01 par value | RDIB | NASDAQ |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No þ

Indicate by check mark whether registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the preceding 12 months (or for shorter period than the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit post such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer ¨ Accelerated Filer ¨ Non-Accelerated Filer þ Smaller Reporting Company ¨ Emerging Growth Company ¨

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. þ

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date. As of June 30, 2021 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the registrant's voting and non-voting common equity held by non-affiliates based on the closing price on that date as reported by the Nasdaq Stock Market was $124,342,409. As of March 15, 2022, there were 20,314,372 shares of class A non-voting common stock, par value $0.01 per share and 1,680,590 shares of class B voting common stock, par value $0.01 per share, outstanding.

Documents Incorporated by Reference

Certain portions of the registrant’s definitive Proxy Statement for the 2022 annual meeting of the stockholders to be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year ended December 31, 2021 are incorporated by reference into Part III of this Annual Report on Form 10-K.

READING INTERNATIONAL, INC.

ANNUAL REPORT ON FORM 10-K

YEAR ENDED DECEMBER 31, 2021

INDEX

The information in this Annual Report on Form 10-K for the year ended December 31, 2021 ("2021 Form 10-K" or “2021 Annual Report”) contains certain forward-looking statements, including statements related to trends in the Company's business. The Company's actual results may differ materially from the results discussed in the “Cautionary Statement Regarding Forward-Looking Statements”. Factors that might cause such a difference include those discussed in "Item 1 – Our Business," "Item 1A – Risk Factors," and "Item 7 – Management's Discussion and Analysis of Financial Condition and Results of Operations" as well as those discussed elsewhere in this 2021 Form 10-K. |

PART I

Item 1 – Our Business

GENERAL

Reading International, Inc. (“RDI” and collectively with our consolidated subsidiaries and corporate predecessors, our “Company,” “Reading,” “we,” “us,” or “our”) was incorporated in 1999 incident to our reincorporation in the State of Nevada. Our class A non-voting common stock (“Class A Stock”) and class B voting common stock (“Class B Stock”) are listed for trading on the NASDAQ Capital Market (Nasdaq-CM) under the symbols RDI and RDIB, respectively. Our Corporate Headquarters is at 189 Second Avenue, Suite 2S, New York, New York, 10003.

Our corporate website address is www.ReadingRDI.com. We provide, free of charge on our website, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Sections 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we have electronically filed such material with, or furnished it to, the Securities and Exchange Commission (the “SEC”) (www.sec.gov). The contents of our Company website are not incorporated into this report. Our corporate governance charters for our Audit and Conflicts Committee and Compensation and Stock Options Committee are available on our website.

BUSINESS DESCRIPTION

Synergistic Diversification and Branding

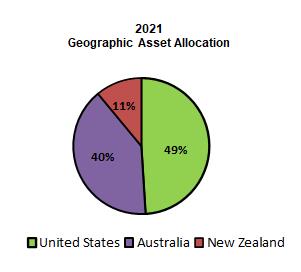

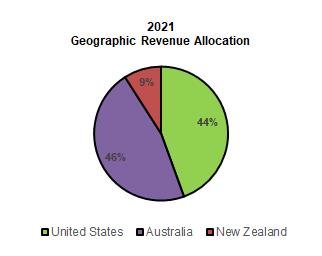

We are an internationally diversified company focused on the development, ownership and operation of entertainment and real property assets in three jurisdictions: (i) United States (“U.S.”), (ii) Australia, and (iii) New Zealand. We group our businesses in two operating segments, which are owned and operated through various operating subsidiaries:

Theatrical Motion Picture Exhibition (“Cinema Exhibition”), through our 63 cinemas.

Real Estate, including real estate development and the rental or licensing of retail, commercial and live theatre assets comprised, as of the date of this 2021 Annual Report, of approximately 9,730,000 square feet of land and approximately 713,000 square feet of net rentable area.

COVID-19 Impact and Company Response

COVID-19 Impact on our Cinema Business

In March 2020, as a result of the COVID-19 pandemic, all of our cinemas in the United States, Australia, and New Zealand were forced to temporarily close by government mandate, ultimately causing an immediate halt to our cinema income. Since the onset of the pandemic, a majority of our cinemas have reopened (some with occupancy restrictions in place). As of the date of this 2021 Annual Report, all our cinemas are open other than one cinema in the U.S. and one cinema in New Zealand which remain closed due to reasons unrelated to the pandemic.

These pandemic related closures have had a material negative impact on our box office results, cinema attendances and the wider cinema industry in general. In 2021, cinemas have reopened as the pandemic has abated and recent variants have not required widespread cinema closures, but attendance is still below pre-pandemic levels due to a variety of factors, including continuing social distancing requirements, public reticence to participate in group activities, competition from streaming services and until relatively recently, the lack of strong film product. Patrons who have returned are responding well to our expanded food and beverage offerings, as spend per patron continue to strengthen. The industry has, in recent months, experienced a positive shift in box office results with the releases of more traditional blockbuster movies to cinemas, such as Spider-Man: No Way Home, Shang-Chi and the Legend of the Ten Rings, and Eternals. We believe that the performance of these films has provided optimism for the cinema industry.

Notwithstanding the impact of COVID-19, we have expanded our global cinema portfolio. We (i) opened five new cinemas in Australia since the third quarter of 2019, (ii) completed two top-to-bottom renovations in the U.S in 2021, and (iii) have two more cinemas in the pipeline to open in 2022.

COVID-19 Impact on our Real Estate Business

Our real estate business has been less impacted, and virtually all of our tenants are currently paying full rents. As of the date of this 2021 Annual Report, 97% of our tenants in our Australian and New Zealand real estate businesses are currently open for trading (some with trading restrictions in place). STOMP reopened at our Orpheum Theater in New York on July 20, 2021, and Audible, an Amazon company, continues to license our Minetta Lane Theater in New York, and resumed public performances on October 8, 2021. We began receiving rental income from our new Culver City office tenant in October 2020.

With regard to our architectural award winning 44 Union Square redevelopment project, while COVID-19 has severely constrained leasing activity in Manhattan, in January 2022 we secured a long-term lease with a strong credit retailer for the cellar, ground floor, and second floor of the building. Our real estate team continues to work to secure office tenants for the remaining space. Our progress regarding this property is discussed in our Real Estate overview below.

As for our other real estate holdings, subject to capital availability and assuming a return to normalcy, we will once again put emphasis on developing and enhancing the following properties: our Courtenay Central, Cannon Park, and Newmarket Village Entertainment Themed Centers, and our Cinemas 1,2,3 and Philadelphia Viaduct properties.

Management’s Response to the Challenges of COVID-19

In response to lower cash inflows from our cinema businesses, we reviewed our real estate portfolio to identify assets that had not been adversely impacted by the pandemic and which would require material capital investment to generate any material increase in value. These asset monetizations are detailed at Note 5 - Real Estate Transactions to the financial statements. We have used the proceeds from the sale of these properties to pay down debt, to cover operating expenses, to fund limited capital improvements, and to strengthen our liquidity. At December 31, 2021, we had cash and cash equivalents totaling $83.3 million, compared to $26.8 million at December 31, 2020. During 2021, we have reduced our net debt from $285.0 million as of December 31, 2020, to $236.9 million as of December 31, 2021.

In addition to the monetization of certain real estate assets, we implemented a number of measures to reduce our day-to-day cost of operations while improving the safety of our cinemas in the light of the COVID-19 pandemic. These measures include, but are not limited to, terminating U.S. cinema and live theater staff for the period of cinema closures, reducing our utilities and essential operating expenditures to the minimum levels necessary, terminating or deferring non-essential capital expenditure, and reducing corporate-level employment costs. We have enhanced our cleaning protocols and installed partitions and air filtration systems to improve the safety aspects of our cinemas and upgraded our mobile platforms to increase social distancing. Furthermore, we were able to keep our Australia and New Zealand cinema level staff due to government assistance provided in those countries.

We have been able to maintain most of our assets and keep our key personnel in place as we reopen our cinemas. Generally speaking, our lenders and landlords continue to work with us, and we continue in occupancy all of our cinemas and have not lost any cinema assets as a result of the COVID-19 pandemic. We negotiated rent abatements and/or deferrals with our landlords throughout 2020 and 2021, and we continue to discuss further concessions with our landlords. We have a variety of landlords, and these discussions are being progressed on a location-by-location basis. Further, we believe our relationships with our film suppliers continue to be strong.

In Conclusion

In 2021, we have taken a number of significant steps to preserve our liquidity, and we will continue to evaluate our operations as the pandemic continues. We modified our business strategy in order to ensure our long-term viability in a way that would not have a dilutive impact on our stockholders, overleverage our Company, or require that we fire sale assets. In arriving at the determination to rely upon the monetization of certain real estate assets to bridge this gap in cinema cashflow (which has in 2021 produced net proceeds to our Company of $139.4 million) and to reduce our need to make capital expenditures, we considered a variety of alternatives, including the issuance of additional common stock and the issuance of high interest rate “junk” debt. We determined that it would be in the best interests of our Company and our stockholders to not dilute equity by issuing stock in the middle of an unprecedented pandemic and to not mortgage our future with high interest rate debt.

With the development and distribution of a variety of vaccines, and a government focus on reducing or eliminating certain pandemic-related restrictions, we anticipate that the impact of the COVID-19 pandemic on our results of operation will be a passing event in the long-term, and we believe that we will ultimately return to results that resemble those of the pre-pandemic era in the future. However, no assurance can be given that we will achieve these results and, unfortunately, there is still a risk of future global outbreaks of COVID-19 and its associated variants, such as the Delta and Omicron variants. In addition, we may be adversely impacted by long-term social trends and movie release patterns, which are placing greater emphasis on streaming in periods prior to the COVID-19 pandemic.

In short, we have preserved our core business and, while we have monetized on favorable terms certain real estate assets earlier than we had intended, we still hold quality real estate assets in which to invest our time and resources.

OUR COMMERCIAL BRANDS

Set forth below is a brief description of the various brands under which we organize our business operations:

| | | | |

Business Segment / Unit | Our Commercial Brands | Country | Description | Website Link |

Cinema Exhibition / All Countries |

| United States Australia New Zealand | Our Reading Cinemas tradename is derived from our over 185-year history as the “Reading Railroad” featured on the Monopoly® game board. Under this brand, we deliver beyond-the-home entertainment (principally mainstream movies and alternative content and food and beverage) across our three operating jurisdictions. All our cinemas are equipped with the latest, state-of-the-art digital screens, 33 Reading Cinemas feature at least one TITAN LUXE, TITAN XC or IMAX premium auditorium, and 178 of our Reading Cinemas screens feature luxury recliner seating as of December 31, 2021. | Reading Cinemas US Reading Cinemas AU Reading Cinemas NZ |

| United States | In 2021, our Consolidated Theatres celebrated 104 years of providing cinematic entertainment in the state of Hawaii. We are the oldest and largest circuit in Hawaii with nine cinemas on the islands of Oahu and Maui. In 2019, we completed the “Top-To-Bottom” renovation of our Consolidated Theatre in Mililani on Oahu, now featuring 14-screens with recliner seating and a TITAN LUXE screen, a full F&B upgrade, including the sale of beer, wine & spirits, and a lobby re-design. Our Consolidated Theatre at the Kahala Mall underwent a “Top-to-Bottom” renovation and reopened on November 5, 2021, with recliner seating throughout along with a state-of-the-art kitchen and an elevated F&B menu. Our Consolidated Theatre at Kapolei commenced renovation during the second quarter of 2021 and reopened March 3, 2022, with recliner seating in half of the auditoriums and an elevated F&B menu. | Consolidated Theatres |

|

| United States Australia | Several of our cinemas are arthouses or specialty theaters operating under our Angelika brand. These cinemas feature specialty films, such as independent films, international films, and documentaries. Since its opening in 1989, our New York City Angelika Film Center has been and consistently continues to be one of the most popular and influential arthouse cinemas in the U.S., featuring principally independent and foreign films. To date, we have expanded our Angelika Film Center Group to include nine other Angelika Film Centers: two in Dallas, TX, two in the Washington DC area, three in New York, NY, one in Sacramenta, CA and one in San Diego, CA. Each of our Angelika Film Centers also offers a curated food and beverage experience. In early 2021, we announced that our Cinemas 1,2,3, Village East and Tower Theatre cinemas would be operated as Angelika brand cinemas: (i) the Cinemas 1,2,3 by Angelika, (ii) the Village East by Angelika and (iii) the Tower Theatre by Angelika. In December 2019, we acquired the iconic 100-year-old State Cinema in Hobart, Tasmania, Australia, which has been ranked the fifth highest grossing arthouse in Australia for the last decade. The cinema, which features 10 screens, a rooftop cinema and bar, a large café and an independent bookstore, is and has been a major cultural destination in North Hobart for decades. In early 2021, the cinema was also rebranded as State Cinema by Angelika. The State Cinema Bar which serves a range of wines and spirits was rebranded the Angelika Bar in 2020. We continue to look to expand our specialty theater portfolio by looking for more specialty theater sites in the U.S., Australia, and New Zealand. | Angelika Film Center State Cinema |

| | | |

| | | |

| | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

Business Segment / Unit | Our Commercial Brands | Country | Description | Website Link |

|

| United States | Launched in December 2020, Angelika Anywhere, is an art focused streaming platform available in the U.S. and more recently, in Australia. We created Angelika Anywhere to allow us to expand the reach of our “Angelika” based cinema experience beyond the four walls of a conventional brick-and-mortar cinema. Our goal is to offer cinephiles easy and curated access to the type of product that has made our Angelika Film Center the most recognized, dedicated arthouse in North America. | Angelika Anywhere |

Real Estate / Leasing |

| United States | Historically known as Tammany Hall, this approximately 73,000 square foot building overlooking Manhattan’s Union Square, has now signed its first tenant who will occupy most of the ground floor, the cellar and the second floor. Hailed as a dramatic pièce de résistance with its first in the city, over 800-piece, glass dome, this building brings the future to New York’s fabled past. In 2021, the building was selected for the following awards: (i) Design Award of Honor in the Renovation, Restoration and Adaptive Re-use category by the Society of American Registered Architects, (ii) 1st Place Addition Award by Retrofit Magazine, (iii) the Architecture + Collaboration Popular Choice Winner by the Architizer A+ Awards and (iv) the Architecture + Collaboration Jury Winner by the Architizer A+ Awards. 44 Union Square is one of a very limited number of locations in Manhattan that will provide major office tenant(s) with a “brandable” site, and the only such location on Union Square. | 44 Union Square |

|

| Australia | Located on 203,000 square feet of land in suburban Brisbane, Newmarket Village is currently comprised of approximately 102,000 square feet of net rentable area, including a Coles Supermarket and 43 other third-party tenants, offering community level F&B, retail, and professional services. At the end of 2017, we completed a major expansion that added a new eight-screen Reading Cinemas with TITAN LUXE, an additional 10,000 square feet of restaurant tenant space and 124 parking spaces. Adjacent to our Newmarket Village, we own a three-level, 22,000 square foot office building. Taken together with the retail components, the center is 92% leased as of December 31, 2021. | Newmarket Village |

|

| Australia | Anchored by our six-screen Reading Cinemas, and 13 other third party tenants offering F&B or other retail offers, Cannon Park is located in Townsville, Australia, and is currently comprised of 408,000 square feet of land and 105,000 square feet of net rentable area. As of December 31, 2021, this property was 87% leased. | Cannon Park Townsville |

|

| Australia | Anchored by our 10-screen Reading Cinemas and five F&B or third-party tenants, The Belmont Common is located in Perth, Australia, and is currently comprised of 103,000 square feet of land and 15,000 square feet of net rentable area. As of December 31, 2021, the lease occupancy rate for this property was 94%. | The Belmont Common |

|

Business Segment / Unit | Our Commercial Brands | Country | Description | Website Link |

|

| New Zealand | Located in the heart of Wellington – New Zealand’s capital city – this center is comprised, on a consolidated basis through various subsidiaries, of 161,000 square feet of land, including two parking lot parcels totaling 84,184 square feet. Courtenay Central is situated proximate to the Te Papa Tongarewa Museum (attracting over 1.5 million visitors annually, pre-COVID), across the street from the site of the new convention center being constructed to handle the demand for such space in Wellington (estimated to open its doors in 2023) and at a major public transit hub. Damage from the 2016 earthquake necessitated demolition of our nine-story parking garage at the site. In January 2019, unrelated seismic issues caused us to close major portions of the existing cinema and retail structure while we reevaluate the center for future redevelopment as an entertainment themed urban center with potentially a major food and grocery component. Wellington continues to be rated as one of the top cities in the world in which to live, and we continue to believe that our assets in Wellington are located in one of the most vibrant areas of New Zealand. | Courtenay Central |

Live Theatre |

| United States | We operate two off-Broadway live theatres in Manhattan under the Liberty Theatres tradename. In 2018, we entered a license with Audible, a subsidiary of Amazon, pursuant to which our Minetta Lane Theatre serves as Audible’s live theatre home in New York City. | Liberty Theatres |

We synergistically bring together cinema-based entertainment and real estate and believe that these two business segments complement one another, as our cinemas have historically provided the steady cash flows that allow us to be opportunistic in acquiring and holding long-term real estate assets (including non-income producing land) and support our real estate development activities. Our real estate allows us to develop an asset base that we believe will stand the test of time and one that can provide financial leverage and, if needed, during times such as the current pandemic, a funding source to reduce dependence on debt and meet operating costs. More specifically, the combination of these two segments provides a variety of business advantages including the following:

Diversification of our Risk Profile and Enhanced Flexibility in meeting our Cash Needs. We believe that our real estate base provides us with the flexibility to raise additional liquidity through one, or a combination of mortgage-based borrowing, sale and leaseback transactions and/or sale. Real-estate backed loans typically allow higher leverage of cash flows than operating loans secured by cinema assets, and the underlying assets themselves provide us a more ready source of liquidity through sale than traditional cinema assets. Strategic asset monetization has formed a key part of our COVID-19 response strategy.

Reduced Pressure to Deliver Cinema Business Growth; to Grow for Growth’s Sake. Pure cinema operators can encounter financial difficulty as demands upon them to produce cinema-based earnings growth tempt them into reinvesting their cash flow into increasingly marginal cinema sites, overpaying for existing cinemas or entering into high-rent leases. While we believe that attractive opportunities to acquire cinema assets and/or to develop high-end specialty type theaters in the future will continue to exist, we do not feel pressure to build or acquire cinemas for the sake of adding units or building gross cinema revenues. This strategy has, over the years, allowed us to acquire cinemas at multiples of trailing theater cash flow below those paid by third parties. We intend to focus our use of cash flow on our real estate development and operating activities, to the extent that attractive cinema opportunities are not available to us or that such funds are not needed for reinvestment to maintain our cinemas in a competitive position. In 2021, we invested approximately $9.6 million in the upgrading and repositioning of our historic cinema assets or adding new cinemas, and approximately $4.2 million in the acquisition or development of our non-cinema real estate assets. The impact of the COVID-19 pandemic on our business has postponed or reprioritized most of our capital expenditures based on assessments of conditions and liquidity requirements.

Enhanced Control over our own Destiny. Some exhibitors are finding their cinemas stranded in dead or dying centers. In our entertainment-themed centers, or “ETCs”, we are better able as exhibitors to control this risk and, as landlords, to realize the benefits of the synergies between entertainment and retail. In our ETCs, we have focused on creating and developing a mix of lifestyle tenancies that, we believe, are less vulnerable to the “Amazon Effect” being felt by traditional centers and that benefit from the foot traffic generated by our cinemas.

The Certainty of Cinema Anchor Tenancies. Cinemas can be used as anchors for larger retail developments such as our ETCs, and our involvement in the cinema business can give us an advantage over other real estate developers or redevelopers who must identify and negotiate with third-party anchor tenants. We have used cinemas to create our own tenant-anchors at our four ETCs.

Flexibility in Property Use. We are always open to the idea of converting an entertainment property to another use, if there is a higher and better use for the property, or to sell individual assets if an attractive opportunity presents itself. Our 44 Union Square property, which is in the lease-up phase of its redevelopment was initially acquired as an entertainment property.

Our hybrid, multi-country strategy emphasizes diversification, and the building of long-term hard asset values. We believe that this business strategy is proving its worth as we have progressed through and are emerging from the current pandemic.

At December 31, 2021, our principal tangible assets included:

interests in 63 cinemas comprising of 515 screens;

fee interests in two live theatres (the Orpheum and Minetta Lane both in Manhattan);

fee interest in our 44 Union Square property, previously used by us as a live theatre venue and for rental to third parties, is in the lease-up phase of its redevelopment for retail and office uses, of which the lower level, ground floor, and second floor of the building is now fully leased to a national retailer;

fee interest in one cinema (the Cinemas 1,2,3) in Manhattan, in which we own a 75% managing member interest in the holding limited liability company;

fee interests in two cinemas in Australia (Bundaberg and Maitland) and three cinemas in New Zealand (Dunedin, Napier and Rotorua);

fee interest in our ETCs in Brisbane (Newmarket Village), Townsville (Cannon Park), Perth (The Belmont Common) and Wellington (Courtenay Central), each of which includes a Reading Cinemas;

fee interest in our administrative office buildings in Culver City, California and Melbourne, Australia. Both buildings also feature one other third-party tenant;

in addition to the fee interests described immediately above, fee ownership of approximately 8.9 million square feet of developed and undeveloped real estate in the United States, Australia and New Zealand; and

cash and cash equivalents, aggregating $83.3 million.

We now present an overview of our business segments.

CINEMA EXHIBITION

Overall

We are dedicated to creating engaging cinema experiences for our guests through hospitality-styled comfort and service, state-of-the-art cinematic presentation, uniquely designed venues, curated film and event programming, and crafted food and beverage options. As discussed previously, we manage our worldwide cinema exhibition business under various brands.

Shown in the following table are the number of locations and screens in our theater circuit in each country, by state/territory/region, our cinema brands, and our interest in the underlying asset as of December 31, 2021:

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | State / Territory / | | Location | | Screen | | Interest in Asset

Underlying the Cinema | | |

Country | | Region | | Count | | Count | | Leased | | Owned | | Operating Brands |

United States | | Hawaii | | 9 | | 98 | | 9 | | | | Consolidated Theatres |

| | California | | 7 | | 88 | | 7 | | | | Reading Cinemas, Angelika Film Center |

| | New York | | 3 | | 16 | | 2 | | 1 | | Angelika Film Center |

| | Texas | | 2 | | 13 | | 2 | | | | Angelika Film Center |

| | New Jersey | | 1 | | 12 | | 1 | | | | Reading Cinemas |

| | Virginia | | 1 | | 8 | | 1 | | | | Angelika Film Center |

| | Washington DC | | 1 | | 3 | | 1 | | | | Angelika Film Center |

| | U.S. Total | | 24 | | 238 | | 23 | | 1 | | |

Australia | | Victoria | | 9 | | 62 | | 9 | | | | Reading Cinemas |

| | New South Wales | | 6 | | 44 | | 5 | | 1 | | Reading Cinemas |

| | Queensland | | 6 | | 56 | | 3 | | 3 | | Reading Cinemas, Event Cinemas(1) |

| | Western Australia | | 2 | | 16 | | 1 | | 1 | | Reading Cinemas |

| | South Australia | | 2 | | 15 | | 2 | | | | Reading Cinemas |

| | Tasmania | | 2 | | 14 | | 2 | | | | Reading Cinemas, State Cinema |

| | Australia Total | | 27 | | 207 | | 22 | | 5 | | |

New Zealand | | Wellington | | 3 | | 18 | | 2 | | 1 | | Reading Cinemas |

| | Otago | | 3 | | 15 | | 2 | | 1 | | Reading Cinemas, Rialto Cinemas(2) |

| | Auckland | | 2 | | 15 | | 2 | | | | Reading Cinemas, Rialto Cinemas(2) |

| | Canterbury | | 1 | | 8 | | 1 | | | | Reading Cinemas |

| | Southland | | 1 | | 5 | | 1 | | | | Reading Cinemas |

| | Bay of Plenty | | 1 | | 5 | | | | 1 | | Reading Cinemas |

| | Hawke's Bay | | 1 | | 4 | | | | 1 | | Reading Cinemas |

| | New Zealand Total | | 12 | | 70 | | 8 | | 4 | | |

GRAND TOTAL | | | | 63 | | 515 | | 53 | | 10 | | |

(1)Our Company has a 33.3% unincorporated joint venture interest in a 16-screen cinema located in Mt. Gravatt, Queensland managed by Event Cinemas.

(2)Our Company is a 50% joint venture partner in two New Zealand Rialto cinemas totaling 13 screens. We are responsible for the booking of these cinemas and our joint venture partner, Event Cinemas, manages their day-to-day operations.

We continue to focus on upgrading our existing cinemas and developing new cinema opportunities to provide our customers with premium offerings, including luxury recliner seating, state-of-the-art presentation including sound, lounges, cafés and bar service, and other amenities. Currently, 178 of our auditoriums feature recliner seating (excluding our joint ventures). In addition, 33 of our auditoriums now feature large format TITAN XC, TITAN LUXE, or IMAX screens. Our circuit has been completely converted to digital projection and sound systems. However, in certain of our cinemas we have, as a point of differentiation, retained the ability to show film in the 70MM format preferred by some directors.

Although we operate cinemas in three nations, the general nature of our operations and operating strategies does not vary materially from jurisdiction-to-jurisdiction. In each jurisdiction, our gross receipts are primarily from box office receipts, food and beverage sales, gift card purchases, online ticketing fees, and screen advertising. Our ancillary revenue is created principally from theater rentals (for example, for film festivals and special events), and ancillary programming (such as concerts and sporting events).

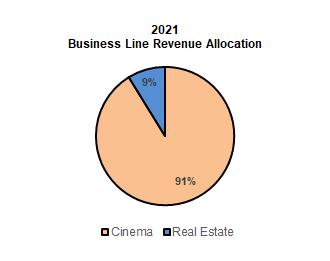

Our cinemas generated approximately 58% of their 2021 revenue from box office receipts. Ticket prices vary by location, and in selected locations we offer reduced rates for senior citizens, children and, in certain markets, military and students.

Showtimes and features are placed in advertisements on our various websites, on internet sites and, in some markets, in limited instances, local newspapers. We are continually increasing our presence in social media, thereby, reducing our dependency on print advertising. Film distributors may also advertise certain feature films in various print, radio and television media, as well as on the internet, and distributors generally pay those costs.

F&B sales accounted for approximately 33% of our total 2021 cinema revenue. Although certain cinemas have licenses for the sale and on-premises consumption of alcoholic beverages, historically F&B products have been primarily popcorn, candy, and soda. This is changing, as more of our theaters are offering expanded food and beverage offerings. One of our strategic focuses is to upgrade our

existing cinemas with expanded F&B offerings consistent with what we believe to be the new position of cinemas in the pathway from content provider to consumer.

Screen advertising and other revenue contribute approximately 8% of our total 2021 cinema revenue. With the exception of certain rights that we have retained to sell to local advertisers, generally speaking, we are not in the screen advertising business and nationally recognized screen-advertising companies’ contract with us for the right to show such advertising on our screens.

Management of Cinemas

With the exception of our three unconsolidated cinemas, we manage our cinemas with executives located in Los Angeles and Manhattan in the U.S., Melbourne, Australia, and Wellington, New Zealand. Our two New Zealand Rialto cinemas are owned by a joint venture in which Reading New Zealand is a 50% joint venture partner. While we assist in the booking of these two cinemas, our joint venture partner, Event Cinemas, manages their day-to-day operations. Our one-third interest in a 16-screen Brisbane cinema is passive in nature. That cinema is being managed by Event Cinemas.

Licensing and Pricing

Film product is available from a variety of sources, ranging from the major film distributors, such as Paramount Pictures, Warner Bros, Disney, Sony Pictures, Universal Pictures and Lionsgate, to a variety of smaller independent film distributors. In Australia and New Zealand, some of those major distributors distribute through local unaffiliated distributors. Worldwide, the major film distributors dominate the market for mainstream conventional films. In the U.S., art and specialty film is distributed through the art and specialty divisions of these major distributors, such as Searchlight Pictures and Sony Pictures Classics, and through independent distributors such as A24 and Neon. Film payment terms are generally based on an agreed-upon percentage of box office receipts that will vary from film-to-film.

Competition

Film is allocated by the applicable distributor among competitive cinemas and in an increasingly material number of situations to streaming services. Accordingly, from time to time, we may be unable to license every film that we desire to play. In the Australian and New Zealand markets, we generally have access to all film product in the market. Due to the COVID-19 pandemic, we have seen a rise in streaming services with greater quantity and quality of films offered. We have also seen certain major distributors skip the traditional theatrical window and go straight to streaming, PVOD or Video on Demand (“VOD”). Furthermore, we have also seen the shortening of theatrical windows as part of the increase in streaming service. For example, in July 2020, AMC announced partnering with Universal to shorten the theatrical window with new movies going to PVOD within three weeks of their debut instead of the typical 75 to 90-day window. In November 2020, Cinemark announced the same. Given the concentration of viewing, and the increasing amount of product being released, the impact of these shortened windows on our revenues is uncertain.

Competition for films may be intense, depending upon the number of cinemas in a particular competitive market. Our ability to obtain top grossing, first run feature films may be adversely impacted by our comparatively small size, and the limited number of screens and markets that we can supply to distributors. Moreover, because of the dramatic consolidation of screens into the hands of a few very large and powerful exhibitors such as AMC, Cineworld, and Cinemark, who between them control over 57% of the North American market, these mega-exhibition companies are in a position to offer distributors access to many more screens in major markets than we can. Also, the major exhibitors have a significant number of markets where they operate without material competition, meaning that the distributors have no alternative exhibitor for their films in these markets. Accordingly, distributors may decide to give preference to these mega-exhibitors when it comes to licensing top-grossing films, rather than deal with independent exhibitors such as ourselves. The situation is different in Australia and New Zealand, where typically every major multiplex cinema has access to all of the film currently in distribution, regardless of the ownership of that multiplex cinema. However, on the reverse side, we have suffered somewhat in these markets from competition from boutique operators, who are able to book top grossing commercial films for limited runs, thus increasing competition for customers wishing to view such top grossing films. We believe it is likely that the power of these major circuits will increase vis-à-vis smaller independent and regional operators with the termination of the so called “Paramount Decree” by the United States District Court at the request of the Department of Justice on August 7, 2020. The order provides for a two-year sunset period on the Paramount Decree’s provisions banning block booking and circuit dealing.

The availability of state-of-the-art technology and/or luxury recliner seating can also be a factor in the preference of one cinema over another. In recent periods, a number of cinemas have opened or reopened featuring luxury recliner seating and/or expanded food and beverage service, including the sale of alcoholic beverages and food served to the seat. Over the last seven years, we have invested in certain cinemas by converting to luxury recliner seating and adding alcoholic beverages to our menus. We are currently working to upgrade the seating and food and beverage offerings (including the offering of alcoholic beverages) at additional existing cinemas. We now offer alcoholic beverages at over half of our worldwide cinemas.

The film exhibition markets in the United States, Australia, and New Zealand are to a certain extent dominated by a limited number of major exhibition companies who have substantial financial resources which could allow them to operate in a more competitive manner