UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

| | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

or

| | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to |

Commission File Number

National Research Corporation

(Exact name of Registrant as specified in its charter)

| | | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

| | ||

| (Address of principal executive offices) (Zip Code) |

| ( | ||

| (Registrant’s telephone number, including area code) |

Securities registered pursuant to 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of each exchange on which registered |

| | | The |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | | ☒ | |

| Non-accelerated filer | ☐ | Smaller reporting company | | |

| Emerging growth company | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.) Yes

Aggregate market value of the common stock held by non-affiliates of the registrant at June 30, 2022: $

Indicate the number of shares outstanding of each of the issuer’s classes of common stock as of the latest practicable date.

Common Stock, $.001 par value, outstanding as of February 23, 2023:

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 2023 Annual Meeting of Shareholders are incorporated by reference into Part III.

| Page |

||

| Item 1. |

||

| Item 1A. |

||

| Item 1B. |

||

| Item 2. |

||

| Item 3. |

||

| Item 4. |

||

| Item 5. |

||

| Item 6. |

||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

| Item 7A. |

||

| Item 8. |

||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

| Item 9A. |

||

| Item 9B. |

||

| Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

|

| Item 10. |

53 | |

| Item 11. |

53 | |

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters |

|

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

|

| Item 14. |

||

| Item 15. |

||

| Item 16. |

||

i

| Item 1. |

Business |

Special Note Regarding Forward-Looking Statements

Certain matters discussed in this Annual Report on Form 10-K are “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements can generally be identified as such because the context of the statement includes phrases such as National Research Corporation, doing business as NRC Health (“NRC Health,” the “Company,” “we,” “our,” “us” or similar terms), “believes,” “expects,” “may,” “could,” “anticipates,” “estimates,” “plans,” “intends,” or the use of words such as “would,” “will,” “may,” “could,” “goal,” “focus,” or “should,” or other words of similar import. Similarly, statements that describe our future plans, objectives or goals are also forward-looking statements. In this Annual Report on Form 10-K, statements regarding the value and utility of, and market demand for, our service offerings, future opportunities for growth with respect to new and existing clients, our future ability to compete and the types of firms with which we will compete, future consolidation in the healthcare industry, future adequacy of our liquidity sources, future revenue sources, future revenue growth, future revenue estimates used to calculate recurring contract value, the expected impact of economic factors, including inflation, future capital expenditures including, without limitation, our headquarters renovation costs, and the timing, amount, and sources of cash to fund such capital expenditures, future stock repurchases and dividends, the expected impact of pending claims and contingencies, the future outcome of uncertain tax positions, our future use of owned and leased real property, the expected impact of the conflict in Ukraine, and the expected impact of the COVID-19 pandemic, among others, are forward-looking statements. Such forward-looking statements are subject to certain risks and uncertainties which could cause actual results or outcomes to differ materially from those currently anticipated. Factors that could affect actual results or outcomes include, without limitation, the following factors:

| ● |

The possibility of non-renewal of our client service contracts, reductions in services purchased or prices, and failure to retain key clients; |

| ● |

Our ability to compete in our markets, which are highly competitive with new market entrants, and the possibility of increased price pressure and expenses; |

| ● |

The likelihood that the COVID-19 or other pandemic will adversely affect our operations, sales, earnings, financial condition and liquidity; |

| ● |

The likelihood that the ongoing Russian-Ukraine conflict will adversely affect our operations, sales, earnings, financial condition and liquidity; |

| ● |

The effects of an economic downturn; |

| ● |

The impact of consolidation in the healthcare industry; |

| ● |

The impact of federal healthcare reform legislation or other regulatory changes; |

| ● |

Our ability to attract and retain key managers and other personnel; |

| ● |

The possibility that our intellectual property and other proprietary information technology could be copied or independently developed by our competitors; |

| ● |

The possibility for failures or deficiencies in our information technology platform; |

| ● |

The possibility that we or our third-party providers could be subject to cyber-attacks, security breaches or computer viruses; and |

| ● |

The factors set forth under the caption “Risk Factors” in Part I, Item 1A of this Annual Report on Form 10-K and various disclosures in our press releases, stockholder reports, and other filings with the Securities and Exchange Commission. |

Shareholders, potential investors and other readers are urged to consider these and other factors in evaluating the forward-looking statements and are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements included are only made as of the date of this Annual Report on Form 10-K and we undertake no obligation to publicly update such forward-looking statements to reflect subsequent events or circumstances, except as required by the federal securities laws.

General

For more than 40 years, NRC Health has led the charge to humanize healthcare and support organizations in their understanding of each unique individual. NRC Health’s commitment to Human Understanding® helps leading healthcare systems get to know each person they serve not as point-in-time insights, but as an ongoing relationship. Guided by its uniquely empathic heritage, NRC Health’s patient-focused approach, unmatched market research, and emphasis on consumer preferences are transforming the healthcare experience, creating strong outcomes for patients and entire healthcare systems.

Our end-to-end solutions enable our clients to understand what matters most to each person they serve – before, during, after, and beyond clinical encounters – to gain a longitudinal understanding of how life and health intersect, with the goal of developing lasting, trusting relationships. Our ability to measure what matters most and systematically capture, analyze, and deliver insights based on self-reported information from patients, families, and consumers is critical in today’s healthcare market. We believe access to and analysis of our extensive consumer-driven information is increasingly valuable as healthcare providers need to better understand and engage the people they serve to create long-term relationships and build loyalty.

Our expertise includes the efficient capture, transmittal, analysis, and interpretation of critical data elements from millions of healthcare consumers. Using our solutions, our partners gain insights into what people think and feel about their organizations in real-time, allowing them to build on their strengths and implement service recovery with greater speed and personalization. We also provide legacy experience-based solutions and shared intelligence from industry thought leaders and the nation’s largest member network focused on healthcare governance and strategy to member boards and executives.

Our portfolio of subscription-based solutions provides actionable information and analysis to healthcare organizations across a range of mission-critical, constituent-related elements, including patient experience, service recovery, care transitions, employee engagement, reputation management, and brand loyalty. We partner with clients across the continuum of healthcare services and believe this cross-continuum positioning is a unique and an increasingly important capability as evolving payment models drive healthcare providers and payers towards a more collaborative and integrated service model.

We have a broad and diversified client base that is distributed primarily across the United States. Our ten largest clients collectively accounted for 15%, 14%, and 14% of our total revenue in 2022, 2021 and 2020, respectively. Approximately 1%, 2% and 2% of our revenue was derived from foreign customers in 2022, 2021, and 2020, respectively.

We have achieved a market leadership position through our more than 40 years of industry innovation and experience, as well as our long-term, recurring revenue relationships (solutions that are used or required by a client each year) with many of the healthcare industry’s largest organizations. Since our founding in 1981, we have focused on meeting the evolving information needs of the healthcare industry through internal product development, as well as select acquisitions. We are a Delaware corporation headquartered in Lincoln, Nebraska.

Human Understanding Solutions

NRC Health recognizes that behind every person is a story. We help our partners get to know each person they serve - their behaviors, preferences, wants, and needs—not as point-in-time insights, but as an ongoing relationship.

With the complexity and demands associated with healthcare delivery today, seeing the whole picture is now more important than ever. The end-to-end Human Understanding solutions are designed to help capture and act on what matters most to patients and their families.

The Human Understanding solutions deliver the capabilities needed to turn strategic aspiration into action in critical focus areas. Each set of capabilities unlocks Human Understanding at the right time and place to improve care, enhance performance, and catalyze growth.

Our digital solutions consist of three primary solution categories which can be implemented both collectively as an enterprise solution or individually to meet specific needs within the organization. The primary solution categories include Marketing, Reputation, and Experience.

Marketing Solutions – Our Marketing solutions are subscription-based services that allow for improved tracking of awareness, perception, and consistency of healthcare brands; real-time assessment of competitive differentiators; and enhanced segmentation tools to evaluate the needs, wants, and behaviors of communities through real-time competitive assessments and enhanced segmentation tools. Market Insights is the largest U.S. healthcare consumer database of its kind, measuring the opinions and behaviors of approximately 300,000 healthcare consumers across the contiguous United States annually. Market Insights is a syndicated survey that provides clients with an independent third-party source of information that is used to understand consumer perception and preferences and optimize marketing strategies. Our Marketing solutions provide clients with on-demand tools to measure brand value and build brand equity in their markets, evaluate and optimize advertising efficacy and consumer recall, and tailor research to obtain the real time voice of customer feedback to support branding and loyalty initiatives.

Experience Solutions – Our Experience solutions are provided on a subscription basis via a cross-continuum multi-mode digital platform that collects and measures data and then delivers business intelligence that our clients utilize to improve patient experience, engagement and loyalty. Patient experience data can also be collected on a periodic basis using Consumer Assessment of Healthcare Providers and Systems (“CAHPS”) compliant mail and telephone survey methods for regulatory compliance purposes and to monitor and measure improvement in CAHPS survey scores. CAHPS survey data can be collected and measured as an integrated service within our digital platform or independently as a legacy service offering. Our Experience solutions provide healthcare systems with the ability to receive and act on customer and employee feedback across all care settings in real-time. Experience solutions include patient experience, workforce engagement, health risk assessments, care transition, and improvement tools. These solutions enable clients to comply with regulatory requirements and to improve their reimbursement under value-based purchasing models. More importantly, our Experience solutions provide quantitative and qualitative real-time feedback, improvement plans, and coaching insights. By illuminating the complete care journey in real time, our clients can ensure each individual receives the care, respect, and experience they deserve. Developing a longitudinal profile of what healthcare customers want and need allows for organizational improvement and increased customer loyalty.

Our Experience solutions also include tools to drive effective communication between healthcare providers and patients in the critical 24-72 hours post discharge using an automated discharge call workflow supported by our digital platform. Through preference-based communications and real-time alerts, these solutions enable organizations to identify and manage high-risk patients to reduce readmissions, increase patient satisfaction and support safe care transitions. Tracking, trending and benchmarking tools isolate the key areas for process improvement allowing organizations to implement changes and reduce future readmissions.

Reputation Solutions – Our Reputation solutions allow healthcare organizations to share a picture of their organization and ensure that timely and relevant content informs better consumer decision-making. Our star ratings tools enable our partners to publish a five-star rating metric and verified patient feedback derived from actual patient survey data to complement their online physician information. Sharing this feedback not only results in better-informed consumer decision-making but also has the ability to drive new patient acquisition and grow online physician reputation. Our reputation monitoring tool alerts our partners to ratings and reviews on third-party websites and provides workflows for response and service recovery. These solutions raise physician awareness of survey results and provide access to improvement resources and educational development opportunities designed to improve the way care is delivered.

The Governance Institute

Our Governance solutions, branded as The Governance Institute (“TGI”), serves not-for-profit health system boards of directors, executives, and physician leadership. TGI’s subscription-based, value-driven membership services are provided through national conferences, publications, advisory services, and an online portal designed to improve the effectiveness of hospital and healthcare systems by continually strengthening their board governance, strategic planning, medical leadership, management performance and customer loyalty. TGI also conducts research studies and tracks industry trends showcasing emerging healthcare trends and best practice solutions of healthcare system boards across the country. TGI thought leadership helps our client board members and executives inform and guide their organization’s strategic priorities in alignment with the rapidly changing healthcare market.

For additional information on our operating segment and our revenue and assets by geographic area, see Note 13, “Segment Information,” to our consolidated financial statements.

Markets

Growth Strategy

We believe that the value proposition of our current solutions, combined with the favorable alignment of our solutions with emerging market demand, positions us to benefit from multiple growth opportunities. We believe that we can accelerate our growth through (1) increasing scope of services and sales of our existing solutions to our existing clients (or cross-selling), (2) winning additional new clients through market share growth in existing market segments, (3) developing and introducing new solutions to new and existing clients, and (4) pursuing acquisitions of, or investments in, firms providing products, solutions or technologies which complement ours.

Increasing contract value with existing clients. Our growth team actively identifies and pursues cross-sell opportunities for clients to add additional solutions in order to accelerate our growth. Organic contract value growth is also realized by the increased scope of solution adoption as the size of client organizations increase from market expansion and consolidation.

Adding new clients. We believe that there is an opportunity to add new clients across all solutions. Our sales organization is actively identifying and engaging new client prospects with a focus on demonstrating the economic value derived from adopting the portfolio of solutions in alignment with the prospect’s strategic objectives.

Adding new solutions. The need for effective solutions in the market segments that we serve is evolving to align with emerging healthcare consumerism trends. The evolving market creates an opportunity for us to introduce new solutions that leverage and extend our existing core competencies. We believe that there is an opportunity to drive sales growth with both existing and new clients, across all of the market segments that we serve, through the introduction of new solutions.

Pursue strategic acquisitions and investments. We have historically complemented our organic growth with strategic acquisitions, having completed eight such transactions over the past nineteen years. These transactions have added new capabilities and access to market segments that are adjacent and complementary to our existing solutions and market segments. We believe that additional strategic acquisition and/or investment opportunities will exist from time to time to complement our organic growth by further expanding our service capabilities, technology offerings and end markets.

We generate the majority of our revenue from the renewal of subscription-based client service agreements, supplemented by sales of additional solutions to existing clients and the addition of new clients. Our sales activities are carried out by our growth team staffed with professional, trained sales associates.

We engage in marketing activities that enhance our brand visibility in the marketplace, generate demand for our solutions and engage existing clients. Strategic campaigns and programs focus on (1) ensuring coverage of prospective clients via targeted advertising and account-based campaigns, (2) elevating client value evidence and success stories to an executive level profile, (3) engaging key stakeholders with content, programming and events and (4) amplifying thought leadership through public and media relations programs that include earning placement in national media and trade publications, securing podium presentations at key industry events and winning awards on behalf of us and our executives.

Competition

The healthcare information and market research services industry is highly competitive. We have traditionally competed with healthcare organizations’ internal marketing, market research, and/or quality improvement departments which create their own performance measurement tools, and with relatively small specialty research firms which provide survey-based healthcare market research and/or performance assessment. Our primary competitors among such specialty firms include Press Ganey, which we believe has significantly higher annual revenue than us, and several other organizations that we believe have less annual revenue than us. We also compete with market research firms and technology solutions which provide survey-based, general market research or voice of the customer feedback capabilities and firms that provide services or products that complement healthcare performance assessments such as healthcare software or information systems.

We believe the primary competitive factors within our market include quality of service, timeliness of delivery, unique service capabilities, credibility of provider, industry experience, and price. We believe that our industry leadership position, exclusive focus on the healthcare industry, cross-continuum presence, comprehensive portfolio of solutions and relationships with leading healthcare providers position us to compete in this market.

Although only a few of these competitors have offered specific services that compete directly with our solutions, many of these competitors have substantially greater financial, information gathering, and marketing resources than us and could decide to increase their resource commitments to our market. There are relatively few barriers to entry into our market, and we expect increased competition in our market which could adversely affect our operating results through pricing pressure, increased marketing expenditures, and market share losses, among other factors. There can be no assurance that we will continue to compete successfully against existing or new competitors.

We believe that our competitive strengths include the following:

A leading provider of patient experience solutions for healthcare providers and other healthcare organizations. Our history is based on capturing the voice of the consumer in healthcare markets. Our solutions build on the “Eight Dimensions of Patient-Centered Care,” a philosophy developed by noted patient advocate Harvey Picker, who believed patients’ experiences are integral to quality healthcare. This foundation has been enhanced through our digital platform offering that provides the delivery of data and insights on a real time basis to understand what matters most to each individual. Based on our more than 40 years of experience, we are able to deliver unique and relevant healthcare domain expertise to the clients we serve.

Established client base of leading healthcare organizations. Our client portfolio encompasses a majority of the leading healthcare systems across the United States. Over 270 of the top 400 healthcare systems based on net patient revenue are currently using one or more of our solutions. Our client base provides a unique network effect to share best practices among existing clients and to attract new clients. Our existing client base also provides a significant organic growth opportunity to upsell and cross sell additional solutions.

Highly scalable and visible revenue model. Our solutions are offered primarily through fixed price, subscription-based service agreements. The solutions we provide are also recurring in nature, which enables an ongoing relationship with our clients and favorable retention. This combination of subscription-based revenue, a base of ongoing client renewals and automated platforms creates a highly visible and scalable revenue model.

Comprehensive portfolio of solutions. Our portfolio of subscription-based solutions provides actionable information and analysis to healthcare organizations across a range of mission-critical, constituent-related elements, including patient experience, service recovery, care transitions, employee engagement, reputation management, and brand loyalty. Our end-to-end solutions enable our clients to understand what matters most to each person they serve – before, during, after, and beyond clinical encounters – to gain a longitudinal understanding of each individual. We partner with clients across the continuum of healthcare services and believe this cross-continuum positioning is a unique and an increasingly important capability as evolving payment models drive healthcare providers and payers towards a more collaborative and integrated service model.

Exclusive focus on healthcare. We focus exclusively on healthcare and serving the unique needs of healthcare organizations across the continuum, which we believe gives us a distinct competitive advantage compared to other survey and analytics software providers. Our value proposition incorporates the benefits to clients derived from our deep subject matter expertise that has been built from helping healthcare organizations over the past 40 years. Our platform includes features and capabilities built specifically for healthcare providers, including a library of performance improvement content which can be tailored to the provider based on their specific customer feedback profile.

Experienced senior management team led by our founder. Our senior management team has extensive industry and leadership experience. Michael D. Hays, our Chief Executive Officer and President, founded NRC Health in 1981. Prior to launching the Company, Mr. Hays served as Vice President and as a Director of SRI Research Center, Inc. (now known as the Gallup Organization). Our Chief Financial Officer, Kevin Karas, CPA, has extensive financial experience having served as CFO at two previous companies, along with healthcare experience at Rehab Designs of America, Inc. and NovaCare, Inc. Jona Raasch has served as our Chief Operating Officer for most of the last 31 years and as Chief Executive Officer of the Governance Institute for more than 15 years. Helen Hrdy was appointed as our Chief Growth Officer in 2020. Prior to this position Ms. Hrdy served as our Senior Vice President, Customer Success, for eight years.

Resources

Our success depends in part upon our data collection processes, research methods, data analysis techniques and internal systems, and procedures that we have developed specifically to serve clients in the healthcare industry. We have no patents for most of our intellectual property. Consequently, we rely on a combination of copyright and trade secret laws and associate nondisclosure agreements to protect our systems, survey instruments and procedures. There can be no assurance that the steps we have taken to protect our rights will be adequate to prevent misappropriation of such rights or that third parties will not independently develop functionally equivalent or superior systems or procedures. We believe that our systems and procedures and other proprietary rights do not infringe upon the proprietary rights of third parties. There can be no assurance, however, that third parties will not assert infringement claims against us in the future or that any such claims will not result in protracted and costly litigation, regardless of the merits of such claims or whether we are ultimately successful in defending against such claims.

Government Regulation

According to the Centers for Medicare and Medicaid Services (“CMS”), health expenditures in the United States were approximately $4.3 trillion in 2021, or $12,914 per person. In total, health spending accounted for 18.3% of the nation’s Gross Domestic Product in 2021. Addressing this growing expenditure burden continues to be a major policy priority at both federal and state levels. In addition, increased co-pays and deductibles in healthcare plans have focused even more consumer attention on health spending and affordability. In the public sector, Medicare provides health coverage for individuals aged 65 and older, while Medicaid provides coverage for low-income families and other individuals in need. Both programs are administered by the CMS. With the aging of the U.S. population, Medicare enrollment has increased significantly. In addition, longer life spans and greater prevalence of chronic illnesses among both the Medicare and Medicaid populations have placed tremendous demands on the health care system.

An increasing percentage of Medicare reimbursement and reimbursement from commercial payers has been determined under value payment models, based on factors such as patient readmission rates and provider adherence to certain quality-related protocols. At the same time, many hospitals and other providers are creating new models of care delivery to improve patient experience, reduce cost and provide better clinical outcomes. These new models are based on sharing financial risk and managing the health and behaviors of large populations of patients and consumers. This transformation towards value-based payment models and increased engagement of healthcare consumers is resulting in a greater need for existing healthcare providers to deliver more customer-centric healthcare. At the same time, organizations that have successfully developed effective customer service models and brand loyalty in other industry verticals are entering the healthcare services market.

We believe that our current portfolio of solutions is uniquely aligned to address these healthcare market trends and related business opportunity. We provide tools and solutions to capture, interpret and improve the CAHPS data required by CMS as well as real time feedback that enables clients to better understand what matters most to people at key moments in their relationship with a health organization. Our solutions enable our clients to both satisfy patient survey compliance requirements and design experiences to build loyalty and improve the wellbeing of the people and communities they care for.

Human Capital

As of December 31, 2022, we employed a total of 491 associates. None of our associates are represented by a collective bargaining unit. The majority of our associates work remotely. We attract a passionate team of associates who care deeply about making a difference in advancing “Human Understanding” in healthcare. We consider our relationships with our associates to be good.

We are committed to providing a workplace free of harassment or discrimination based on race, color, religion, sex, sexual orientation, gender identity, national origin, genetic information, ancestry, veteran status, or disability. We are an equal opportunity employer committed to inclusion and diversity.

Available Information

More information regarding NRC Health is available on our website at www.nrchealth.com. We are not including the information contained on or available through our website as part of, or incorporating such information by reference into, this Annual Report on Form 10-K. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports are made available to the public at no charge through a link appearing on our website. We provide access to such materials through our website as soon as reasonably practicable after electronically filing such material with, or furnishing it to, the Securities and Exchange Commission. Reports and amendments posted on our website do not include access to exhibits and supplemental schedules electronically filed with the reports or amendments.

| Item 1A. |

Risk Factors |

You should carefully consider each of the risks described below, together with all of the other information contained in this Annual Report on Form 10-K, before making an investment decision with respect to our securities. If any of the following risks develop into actual events, our business, financial condition or results of operations could be materially and adversely affected and you may lose all or part of your investment.

Risks Related to our Business

We depend on contract renewals, including retention of key clients, for a large share of our revenue and our operating results could be adversely affected.

We expect that a substantial portion of our revenue for the foreseeable future will continue to be derived from renewable service contracts. Substantially all contracts are renewable annually at the option of our clients, although contracts with clients under unit-based arrangements generally have no minimum purchase commitments. Client contracts are generally cancelable on short notice without penalty, however we are entitled to payment for services through the cancellation date. To the extent that clients fail to renew or defer their renewals, we anticipate our results may be materially adversely affected. We rely on a limited number of key clients for a substantial portion of our revenue. Our ten largest clients collectively accounted for 15%, 14%, and 14% of our total revenue in 2022, 2021 and 2020, respectively. Our ability to secure renewals depends on, among other things, our ability to gather and analyze performance data in a consistent, high-quality, and timely fashion. In addition, the service needs of our clients are affected by accreditation requirements, enrollment in managed care plans, the level of use of satisfaction measures in healthcare organizations’ overall management and compensation programs, the size of operating budgets, clients’ operating performance, industry and economic conditions, and changes in management or ownership. As these factors are beyond our control, we cannot ensure that we will be able to maintain our renewal rates. Any material decline in renewal rates from existing levels would have an adverse effect on our revenue and a corresponding effect on our operating and net income.

We operate in a highly competitive market and could experience increased price pressure and expenses as a result.

The healthcare information and market research services industry is highly competitive. We have traditionally competed with healthcare organizations’ internal marketing, market research and/or quality improvement departments that create their own performance measurement tools, and with relatively small specialty research firms that provide survey-based healthcare market research and/or performance assessment. Our primary competitors among such specialty firms include Press Ganey, which we believe has significantly higher annual revenue than us, and three or four other firms that we believe have lower annual revenue than us. We also compete with market research firms and technology solutions which provide survey-based, general market research or voice of the customer feedback capabilities and firms that provide services or products that complement healthcare performance assessments, such as healthcare software or information systems. Although only a few of these competitors have offered specific services that compete directly with our services, many of these competitors have substantially greater financial, information gathering, and marketing resources than us and could decide to increase their resource commitments to our market. Furthermore, we do not have a publicly traded group of peers, which makes it difficult to compare and benchmark performance to other similar companies. There are relatively few barriers to entry into our market, and we expect increased competition in our market which could adversely affect our operating results through pricing pressure, increased marketing expenditures, and market share losses, among other factors. There can be no assurance that we will continue to compete successfully against existing or new competitors.

Because our clients are concentrated in the healthcare industry, our revenue and operating results may be adversely affected by changes in regulations, a business downturn or consolidation with respect to the healthcare industry.

Substantially all of our revenue is derived from clients in the healthcare industry. As a result, our business, financial condition and results of operations are influenced by conditions affecting this industry, including changing political, economic, competitive and regulatory influences that may affect the procurement practices and operation of healthcare providers and payers. Future legislative changes, including additional provisions to control healthcare costs, improve healthcare quality and expand access to health insurance, could result in lower reimbursement rates and otherwise change the environment in which providers and payers operate. In addition, large private purchasers of healthcare services are placing increasing cost pressure on providers. Healthcare providers may react to these cost pressures and other uncertainties by curtailing or deferring purchases, including purchases of our services.

Moreover, there has been consolidation of companies in the healthcare industry, a trend which we believe will continue to grow. Consolidation in this industry, including the potential acquisition of certain of our clients, could adversely affect aggregate client budgets for our services, could result in clients performing more marketing, market research and/or quality improvement functions internally or could result in the termination of a client’s relationship with us. The impact of these developments on the healthcare industry is difficult to predict and could have an adverse effect on our revenue and a corresponding effect on our operating and net income.

We could be negatively impacted by the Coronavirus or “COVID-19” pandemic or other outbreaks or pandemics.

The outbreak of COVID-19, and the associated responses, have impacted our business in a variety of ways, including business and travel restrictions, recommended social distancing and other guidelines. During the COVID-19 pandemic or other outbreaks or pandemics, businesses, including our clients, may de-emphasize external business opportunities and restrict in-person meetings while shifting their attention toward addressing COVID-19 or pandemic planning, business disruptions, higher costs, and revenue shortfalls. We rely on third-party service providers and business partners, for services or supplies that are critical to providing our clients’ services. These third parties are also subject to risks and uncertainties related to the COVID-19 pandemic or similar outbreaks, which may interfere with their ability to provide their services in a timely manner and in accordance with the agreed-upon terms or our agreements, which could interfere with our ability to operate our business.

To the extent the COVID-19 pandemic or other similar outbreaks adversely affects the Company’s business, results of operations, financial condition and stock price, it may also have the effect of heightening many of the other risks described in this Part I, Item 1A of this Form 10-K.

We could be negatively impacted by the Russian-Ukraine conflict or similar global events.

The Russian-Ukraine conflict, and any expansion of the Russian-Ukraine conflict, could adversely affect our business and operations. We outsource certain software development services to third parties in the Ukraine. Since the onset of the active Russian-Ukraine conflict, our contractors have been able to continue their work. However, those services could be more negatively impacted in the future.

Civil unrest, political instability or uncertainty, military activities, utility service breakdowns or broad-based sanctions, should they continue for the long term or escalate, could interrupt our contractors’ ability to provide services and require our associates to perform the services or replace the contractors which could have an adverse effect on our operations and financial performance, including higher volatility in foreign currency exchange rates, increased use of less cost-efficient resources and negative impacts to our business resulting from deteriorating general economic conditions. Further, we cannot predict the impact of the military actions and any heightened military conflict or geopolitical instability that may follow, including additional sanctions or countersanctions, heightened inflation, cyber disruptions or attacks, higher energy costs, and supply chain disruptions.

General economic factors could adversely impact our profitability.

Negative changes in general economic conditions, in the geographic areas in which we operate may reduce our profitability. An economic downturn and inflationary pressures can reduce the demand for our services and result in termination as well as slower client payments or client defaults on receivables. Additionally, in 2022, we experienced increased costs including the costs of labor, contracted services, costs associated with our building improvements and equipment purchases and we expect elevated levels of inflation to continue in 2023. Inflation may increase our costs without a corresponding increase in our contract revenue due to fixed contract arrangements, which could result in decreased margins and profitability.

We face several risks relating to our ability to collect the data on which our business relies.

Our ability to provide timely and accurate performance measurement and improvement services to our clients depends on our ability to collect large quantities of high-quality data through surveys. If survey operations are disrupted and we are unable to process surveys in a timely manner, then our revenue and net income could be negatively impacted. We outsource certain operations and engage third parties to perform work needed to fulfill our client services. For example, we use vendors to perform certain outreach and data collection services related to our survey operations. If any of these vendors cease to operate or fail to adequately perform the contracted services and alternative resources and processes are not utilized in a timely manner, our business could be adversely affected. The loss of any of our key vendors could impair our ability to perform our client services and result in lower revenues and income. It would also be time-consuming and expensive to replace, either directly or through other vendors, the services performed by these vendors, which could adversely impact revenues, expenses and net income. Furthermore, our ability to monitor and direct our vendors’ activities is limited. If their actions and business practices violate policies, regulations or procedures otherwise considered illegal, we could be subject to reputational damage or litigation which would adversely affect our business.

If receptivity to our survey methods by respondents declines, or, for some other reason, their willingness to complete and return surveys declines, or if we, for any reason, cannot rely on the integrity of the data we receive, then our revenue could be adversely affected with a corresponding effect on our operating and net income.

If intellectual property and other proprietary information technology were copied or independently developed by our competitors, our operating results could be negatively affected.

Our success depends in part upon our data collection process, research methods, data analysis techniques, and internal systems and procedures that we have developed specifically to serve clients in the healthcare industry. We do not hold patents for our intellectual property. Consequently, we rely on a combination of copyright, trade secret laws and associate nondisclosure agreements to protect our systems, survey instruments and procedures. We cannot assure you that the steps we have taken to protect our rights will be adequate to prevent misappropriation of such rights, or that third parties will not independently develop functionally equivalent or superior systems or procedures. We believe that our systems and procedures and other proprietary rights do not infringe upon the proprietary rights of third parties. We cannot assure you, however, that third parties will not assert infringement claims against us in the future, or that any such claims will not result in protracted and costly litigation, regardless of the merits of such claims, or whether we are ultimately successful in defending against such claims.

Failures, interruptions or deficiencies in our information technology and communications systems could negatively impact our business and operating results.

Our ability to provide timely and accurate performance measurement and improvement service to our clients is dependent, to a significant extent, upon the technology that we develop internally as well as the efficient and uninterrupted operation of our information technology and communication systems, and those of our external service providers. Investment in the enhancement of existing and development of new information technology processes is costly and affects our ability to successfully serve our clients. The failure or deficiency of the technology we develop could negatively impact the willingness or ability for our clients to use our services and our ability to perform our services. Our failure to anticipate clients’ expectation and needs, adapt to emerging technological trends, or design efficient and effective information technology platforms, could result in lower utilization, loss of customers, damage to customer relationships, reduced revenue and profits, refunds to customers and damage to our reputation. Although we have procedures to monitor the efficacy of our information technology platforms, the procedures may not prevent failures or deficiencies in the information technology platforms we develop, we may not adapt quickly enough and may incur significant costs and delays that could harm our business. Additional costs could be incurred to further develop and improve our information technology platforms.

Our systems and those of our external service providers could be exposed to damage or interruption from fire, natural disasters, energy loss, telecommunication failure, security breach and computer viruses. An operational failure or outage in our information technology and communication systems or those of our external service providers, could result in loss of customers, damage to customer relationships, reduced revenue and profits, refunds of customer charges and damage to our reputation and may result in additional expense to repair or replace damaged equipment and recover data loss resulting from the interruption. Although we have taken steps to prevent system failures and have back-up systems and procedures to prevent or reduce disruptions, such steps may not prevent an interruption of services and our disaster recovery planning may not account for all contingencies. Additionally, our insurance may not adequately compensate us for all losses or failures that may occur. Any one of the above situations could have a material adverse effect on our business, financial condition, results of operations and reputation.

If we or our third-party service providers sustain cyber-attacks or other privacy or data security incidents that result in security breaches that disrupt our operations or result in the unintended dissemination of protected personal information or proprietary or confidential information, we could suffer a loss of revenue and increased costs, exposure to significant liability, reputational harm and other serious negative consequences.

In connection with our client services, we and our third-party service providers receive, process, store and transmit sensitive business information and, in certain circumstances, personal medical information of our clients’ patients, electronically over the internet. We or our third-party service providers may become the target of attempted cyber-attacks and other security threats and may be subject to breaches of the information technology systems we use. Experienced computer programmers and hackers may be able to penetrate our security controls and access, misappropriate or otherwise compromise protected personal information or proprietary or confidential information or that of third-parties, create system disruptions or cause system shutdowns that could negatively affect our operations. They also may be able to develop and deploy viruses, worms, ransomware, and other malicious software programs that attack our systems or otherwise exploit any security vulnerabilities.

In addition, the risk of cyber-attacks has increased in connection with the military conflict between Russia and Ukraine and the resulting geopolitical conflict. In light of those and other geopolitical events, nation-state actors or their supporters may launch retaliatory cyber-attacks, and may attempt to cause supply chain and other third-party service provider disruptions, or take other geopolitically motivated retaliatory actions that may disrupt our business operations, result in data compromise, or both. Nation-state actors have in the past carried out, and may in the future carry out, cyber-attacks to achieve their aims and goals, which may include espionage, information operations, monetary gain, ransomware, disruption, and destruction. In February 2022, the U.S. Cybersecurity and Infrastructure Security Agency issued a “Shields Up” alert for American organizations noting the potential for Russia’s cyber-attacks on Ukrainian government and critical infrastructure organizations to impact organizations both within and beyond the United States, particularly in the wake of sanctions imposed by the United States and its allies. These circumstances increase the likelihood of cyber-attacks and/or security breaches.

We were the target of an external cyber-attack in February 2020 (the “February incident”) which resulted in a temporary suspension of our services to clients. One of our third-party service providers was the target of an external cyber-attack in December 2022 which resulted in a temporary suspension of certain services to our clients. In both instances no protected data was compromised or exfiltrated. We, and our service providers, will likely continue to be the target of other attempted cyber-attacks and security threats. Such cyber-attacks may subject us to litigation and regulatory risk, civil and criminal penalties, additional costs and diversion of management attention due to investigation, remediation efforts and engagement of third-party consultants and legal counsel in connection with such incidents, payment of “ransoms” to regain access to our systems and information, loss of clients, damage to client relationships, reduced revenue and profits, refunds of client charges and damage to our reputation, any of which could have a material adverse effect on our business, cash flows, financial condition and results of operations. While we have contingency plans and insurance coverage for potential liabilities of this nature, they may not be sufficient to cover all claims and liabilities and in some cases are subject to deductibles and layers of self-insured retention.

We cannot ensure that we or our third-party service providers will be able to identify, prevent or contain the effects of cyber-attacks or other cybersecurity risks that bypass our security measures or disrupt our information technology systems or business. We have security technologies, processes and procedures in place to protect against cybersecurity risks and security breaches. However, hardware, software or applications we develop or procure from third parties may contain defects in design, manufacturer defects or other problems that could unexpectedly compromise information security. In addition, because the techniques used to obtain unauthorized access, disable or degrade service or sabotage systems change frequently, are becoming increasingly sophisticated, and may not immediately produce signs of intrusion, we may be unable to anticipate these techniques, timely discover or counter them or implement adequate preventative measures.

In addition, we use third-party technology, systems and services for a variety of reasons, including, without limitation, encryption and authentication technology, employee email, content delivery to clients, back-office support, and other functions that in some cases involve processing, storing and transmitting large amounts of data for our business. These third-party providers may also experience security breaches or interruptions to their information technology hardware and software infrastructure and communications systems that could adversely impact us.

Under the Health Insurance Portability and Accountability Act of 1996, as amended by the Health Information Technology for Economic and Clinical Health Act of 2009, or HITECH, implementing regulations promulgated by the U.S. Department of Health and Human Services, or “HHS,” including what are referred to as the “Privacy Rule” and the “Security Rule” (collectively, “HIPAA”), we face potential liability related to the privacy of health information we obtain. We are required through our contracts with our clients and by HIPAA to protect the privacy and security of certain health information and to make certain disclosures to our clients or to the public if this information is unlawfully accessed.

Changes in privacy and information security laws and standards may require that we incur significant expense to ensure compliance due to increased technology investment and operational procedures. Noncompliance with any privacy or security laws and regulations, including, without limitation, HIPPA, or any security breach, cyber-attack or cybersecurity breach, and any incident involving the misappropriation, loss or other unauthorized disclosure or use of, or access to, sensitive or confidential information, whether by us or by one of our third-party service providers, could require us to expend significant resources to continue to modify or enhance our protective measures and to remediate any damage. In addition, this could negatively affect our operations, cause system disruptions, damage our reputation, cause client losses and contract breaches, and could also result in regulatory enforcement actions, material fines and penalties, litigation or other actions that could have a material adverse effect on our business, cash flows, financial condition and results of operations. Even if cyber-attacks or other cybersecurity breaches do not result in noncompliance with privacy or security laws, the perception that such noncompliance may have occurred by our clients or in the news media may have an adverse impact on our stock price and could result in damage to our reputation or loss of clients, which could have a material adverse effect on our business, cash flows, financial condition and results of operations.

Reputational harm could have a material adverse effect on our business, financial condition and results of operations.

Our ability to maintain a positive reputation is critical to selling our services. Our reputation could be adversely impacted by any of the following (whether or not valid): the failure to maintain high ethical and social standards; the failure to perform our client services in a timely manner; violations of laws and regulations; failure to adequately preserve information security; and the failure to maintain an effective system of internal controls or to provide accurate and timely financial information. Damage to our reputation or loss of our clients’ confidence in our services for any of these, or any other reasons, could adversely impact our business, revenues, financial condition, and results of operations, as well as require additional resources to rebuild our reputation.

Our operations are subject to laws and regulations that impose significant compliance costs and create reputational and legal risk.

Due to the nature of the services we offer, we are subject to significant commercial, trade and privacy regulations. We cannot predict the nature, scope or effect of future regulatory requirements to which our operations might be subject or the manner in which existing laws might be administered or interpreted, which could have a material and negative impact on our business and our results of operation. For example, recent years have seen an increase in the development or enforcement of legislation related to healthcare reform, privacy, trade compliance and anti-corruption. Additionally, some of the services we provide include information our clients need to fulfill regulatory reporting requirements. If our services result in errors or omissions in our clients’ regulatory reporting, we may be subject to loss of clients, reputational harm or litigation, each potentially adversely impacting our business. Furthermore, although we maintain a variety of internal policies and controls designed to educate, discourage, prevent and detect violations of such laws, we cannot guarantee that such actions will be effective or sufficient or that individual employees will not engage in inappropriate behavior in breach of our policies. Such conduct, or even an allegation of misbehavior, could result in material adverse reputational harm, costly investigations, severe criminal or civil sanctions, or could disrupt our business, and could negatively affect our results of operations or financial condition.

Our growth strategy includes future acquisitions and/or investments which involve inherent risk.

In order to expand services or technologies to existing clients and increase our client base, we have historically, and may in the future, make strategic business acquisitions and/or investments that we believe complement our business. Acquisitions have inherent risks which may have material adverse effects on our business, financial condition, or results of operations, including, among other things: (1) failure to successfully integrate the purchased operations, technologies, products or services and maintain uniform standard controls, policies and procedures; (2) substantial unanticipated integration costs; (3) loss of key associates including those of the acquired business; (4) diversion of management’s attention from other operations; (5) failure to retain the customers of the acquired business; (6) failure to achieve any projected synergies and performance targets; (7) additional debt and/or assumption of known or unknown liabilities; (8) dilutive issuances of equity securities; and (9) a write-off of goodwill, software development costs, client lists, other intangibles and amortization of expenses. If we fail to successfully complete acquisitions or integrate acquired businesses, we may not achieve projected results and there may be a material adverse effect on our business, financial condition and results of operations.

Risks Related to our Common Stock

Our principal shareholders effectively control the Company.

A majority of our common stock and voting power was historically owned and/or held by Michael D. Hays, our Chief Executive Officer and President. However, over the years Mr. Hays, for estate planning purposes, gifted and/or transferred almost all of his directly owned shares to trusts for the benefit of his family. Currently, the principal holders of shares previously owned by Mr. Hays are the Common Property Trust and the Amandla MK Trust (collectively the “Trusts”).

As of February 23, 2022, approximately 41.1% of our outstanding common stock was owned by the Trusts and approximately 50.8% of our outstanding common stock was held by the Trusts and other entities owned or controlled by members of Mr. Hays’ family. As a result, the Trusts and these other entities have the power to indirectly control decisions such as whether to issue additional shares or declare and pay dividends and can control matters requiring shareholder approval, including the election of directors and the approval of significant corporate matters such as change of control transactions. The effects of such influence could be to delay or prevent a change of control of the Company unless the terms are approved by the Trusts and these other entities.

The market price of our common stock may be volatile and shareholders may be unable to resell shares at or above the price at which the shares were acquired.

The market price and trading volume of our common stock has historically been and may continue to be highly volatile, and investors in our common stock may experience a decrease in the value of their shares, including decreases that are in response to factors beyond our control, including, but not limited to:

| ● |

Variations in our financial performance and that of similar companies; |

|

| ● |

Regulatory and other developments that may impact the demand for our services; |

|

| ● |

Reaction to our press releases, public announcements and filings with the Securities and Exchange Commission; |

|

| ● |

Client, market and industry perception of our services and performance; |

|

| ● |

Actions of our competitors; |

|

| ● |

Changes in earnings estimates or recommendations by analysts who follow our stock; |

|

| ● |

Loss of key personnel; |

|

| ● |

Investor, management team or large stockholder sales of our stock; |

|

| ● |

Changes in accounting principles; and |

|

| ● |

Variations in general market, economic and political conditions or financial markets. |

Any of these factors, among others, may result in changes in the trading volume and/or market price of our common stock. Following periods of volatility in the market price of securities, shareholders have often filed securities class-action lawsuits. Our involvement in a class-action lawsuit would result in substantial legal fees and divert our senior management’s attention from operating our business, which could harm our business and net income.

General Risk Factors

Our operating results may fluctuate and this may cause our stock price to decline.

Our overall operating results may fluctuate as a result of a variety of factors, including the size and timing of orders from clients, client demand for our services (which, in turn, is affected by factors such as accreditation requirements, enrollment in managed care plans, operating budgets and clients’ operating performance), the hiring and training of additional staff, expense increases, and industry and general economic conditions. Because a significant portion of our overhead is fixed in the short-term, particularly some costs associated with owning and occupying our building and full-time personnel expenses, our results of operations may be materially adversely affected in any particular period if revenue falls below our expectations. These factors, among others, make it possible that in some future period our operating results may be below the expectations of securities analysts and investors which would have a material adverse effect on the market price of our common stock.

Our business and operating results could be adversely affected if we are unable to attract or retain key managers and other personnel.

Our future performance may depend, to a significant extent, upon the efforts and ability of our key personnel who have expertise in gathering, interpreting and marketing survey-based performance information for healthcare markets. Although client relationships are managed at many levels within our company, the loss of the services of Michael D. Hays, our Chief Executive Officer and President, or one or more of our other senior managers, could have a material adverse effect, at least in the short to medium term, on most significant aspects of our business, including strategic planning, product development, and sales and customer relations. Our success will also depend on our ability to hire, train and retain skilled personnel in all areas of our business. Competition for qualified personnel in our industry is intense, and many of the companies that compete with us for qualified personnel have substantially greater financial and other resources than us. Furthermore, we expect competition for qualified personnel to become more intense as competition in our industry increases. We cannot assure you that we will be able to recruit, retain and motivate a sufficient number of qualified personnel to compete successfully.

Like many other companies, we experienced higher attrition rates the last two years. We may incur higher costs to attract, train and retain these associates. Attrition in our sales and service areas can also impact our ability to retain and attract new business. We may need to develop or adapt to new ways of doing business that challenge our leadership, our associate training, our human resources, and our business practices, and we cannot assure you that we will be successful in doing so. The short and long-term costs associated with these potential changes are difficult to quantify.

Failure to comply with public company regulations could adversely impact our profitability.

As a public company, we are subject to the reporting requirements of the Securities Exchange Act of 1934, the Sarbanes-Oxley Act of 2002, the Dodd-Frank Act Wall Street Reform and Consumer Protection Act, the listing requirements of NASDAQ and other applicable securities rules and regulations. Additionally, laws, regulations and standards relating to corporate governance and public disclosure are subject to varying interpretations and continue to develop and change. If we misinterpret or fail to comply with these rules and regulations, our legal and financial compliance costs and net income may be adversely affected.

| Item 1B. |

Unresolved Staff Comments |

We have no unresolved staff comments to report pursuant to this item.

| Item 2. |

Properties |

Our headquarters is located in an owned office building in Lincoln, Nebraska, of which 62,000 square feet have been used for operations. Our credit facilities are secured by this property and our other assets. We are currently renovating the building and expect renovations to complete in 2024. In February 2021, we began leasing 19,300 square feet of space in Lincoln, Nebraska for our mail survey processing operations that were previously housed at our headquarters.

We are leasing 4,000 square feet of office space in Markham, Ontario through February 2024, which we vacated as of October 2022. In addition, we lease 1,000 square feet of office space in Bethel, Connecticut. We are subleasing as a sublessor 4,300 square feet of office space in Seattle, Washington. We were leasing 300 square feet of office space in Atlanta, Georgia on a month-to-month lease which we ended in February 2023.

| Item 3. |

Legal Proceedings |

From time to time, we are involved in certain claims and litigation arising in the normal course of business. Management assesses the probability of loss for such contingencies and recognizes a liability when a loss is probable and estimable. For additional information, see Note 1, under the heading “Commitments and Contingencies,” to our consolidated financial statements. Regardless of the final outcome, any legal proceedings, claims, inquiries and investigations, however, can impose a significant burden on management and employees, may include costly defense and settlement costs, and could cause harm to our reputation and brand, and other factors.

| Item 4. |

Mine Safety Disclosures |

Not applicable.

| Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

We have one class of outstanding capital stock, which is our Common Stock, par value $.001 per share (“Common Stock”). Our Common Stock trades on the NASDAQ Global Select Market under the symbol “NRC”.

Cash dividends in the aggregate amount of $20.9 million, $12.2 million and $5.3 million were declared in 2022, 2021 and 2020 respectively. The payment and amount of future dividends, if any, is at the discretion of our Board of Directors and will depend on our future earnings, financial condition, general business conditions, alternative uses of our earnings and cash and other factors.

On February 14, 2023, there were approximately 10 shareholders of record and approximately 13,661 beneficial owners of our Common Stock.

In February 2006 and subsequently amended in May 2013, our Board of Directors authorized the repurchase of up to 2,250,000 shares of Common Stock in the open market or in privately negotiated transactions under a stock repurchase program (the “2006 Program”). In 2022, we repurchased all the remaining shares authorized for repurchase under the 2006 Program. In May 2022, our Board of Directors approved a new stock repurchase authorization of 2,500,000 shares of Common Stock (the “2022 Program”).

The table below summarizes repurchases of Common Stock during the three-month period ended December 31, 2022.

| Period |

Total Number of Shares Purchased |

Average Price Paid per Share |

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs(1) |

Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs(1) |

||||||||||||

| Oct 1 – Oct 31, 2022 |

— | — | — | 1,987,517 | ||||||||||||

| Nov 1 – Nov 30, 2022 |

51,083 | 36.69 | 51,083 | 1,936,434 | ||||||||||||

| Dec 1 – Dec 31, 2022 |

11,990 | 36.96 | 11,990 | 1,924,444 | ||||||||||||

| Total |

63,073 | 63,073 | ||||||||||||||

| (1) |

Shares were repurchased pursuant to the 2022 program. |

See Item 12 in Part III of this Annual Report on Form 10-K for certain information concerning shares of our Common Stock authorized for issuance under our equity compensation plans.

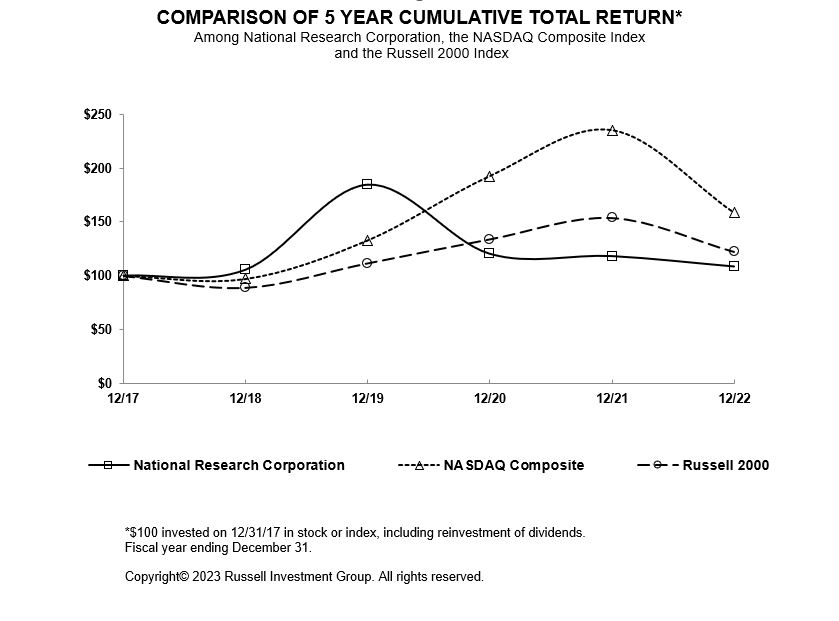

The following graph compares the cumulative 5-year total return provided shareholders on our Common Stock relative to the cumulative total returns of the NASDAQ Composite Index and the Russell 2000 Index. Because of the uniqueness of our markets and products and lack of publicly traded peers, we do not believe that a combination of peer issuers can be selected on an industry or line-of-business basis to provide a meaningful basis for comparing shareholder return. Accordingly, the Russell 2000 Index, which is comprised of issuers with generally similar market capitalizations to that of the Company, is included in the graph as permitted by applicable regulations. An investment of $100 (with reinvestment of all dividends) is assumed to have been made in our Common Stock and in each of the indexes on December 31, 2017, and our relative performance is tracked through December 31, 2022.

The stock price performance included in this graph is not necessarily indicative of future stock price performance.

| 12/17 |

12/18 |

12/19 |

12/20 |

12/21 |

12/22 |

|||||||||||||||||||

| National Research Corporation Common Stock (1) |

100.00 | 105.36 | 184.87 | 120.42 | 118.22 | 108.51 | ||||||||||||||||||

| NASDAQ Composite |

100.00 | 97.16 | 132.81 | 192.47 | 235.15 | 158.65 | ||||||||||||||||||

| Russell 2000 |

100.00 | 88.99 | 111.70 | 134.00 | 153.85 | 122.41 | ||||||||||||||||||

(1)Prior to a recapitalization that took place in 2018, our Common Stock was referred to as Class A Common Stock.

| Item 6. |

[Reserved] |

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following discussion and analysis provides a summary of significant factors relevant to our financial performance and condition. It should be read in conjunction with the consolidated financial statements and accompanying notes included in Part II, Item 8 of this Form 10-K. This section of this Form 10-K generally discusses 2022 and 2021 items and year-to-year comparisons between 2022 and 2021. Discussions of 2020 items and year-to-year comparisons between 2021 and 2020 are not included in this Form 10-K, and can be found in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II, Item 7 of the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2021.

Overview

Our purpose is to humanize healthcare and support organizations in their understanding of each unique individual. Our commitment to Human Understanding® helps leading healthcare systems get to know each person they serve not as point-in-time insights, but as an ongoing relationship. Our end-to-end solutions enable our clients to understand what matters most to each person they serve – before, during, after, and beyond clinical encounters – to gain a longitudinal understanding of how life and health intersect, with the goal of developing lasting, trusting relationships. Our ability to measure what matters most and systematically capture, analyze, and deliver insights based on self-reported information from patients, families, and consumers is critical in today’s healthcare market. We believe access to and analysis of our extensive consumer-driven information is increasingly valuable as healthcare providers need to better understand and engage the people they serve to create long-term relationships and build loyalty.

Our portfolio of subscription-based solutions provides actionable information and analysis to healthcare organizations across a range of mission-critical, constituent-related elements, including patient experience, service recovery, care transitions, employee engagement, reputation management, and brand loyalty. We partner with clients across the continuum of healthcare services and believe this cross-continuum positioning is a unique and an increasingly important capability as evolving payment models drive healthcare providers and payers towards a more collaborative and integrated service model.

The outbreak of COVID-19, and the associated responses, have impacted our business in a variety of ways. Many businesses, including many of our clients, have de-emphasized external business opportunities and restricted in-person meetings while shifting their attention toward addressing COVID-19 planning, business disruptions, higher costs, and revenue shortfalls. The on-going impacts of the COVID-19 pandemic and associated impacts on our business, including the impact on our revenue, expenses, and cash flows, cannot be predicted at this time.

Critical Accounting Policies and Estimates

The preparation of financial statements requires management to make estimates and assumptions that affect amounts reported therein. The following areas are considered critical accounting estimates because they involve significant judgments or assumptions, involve complex or uncertain matters or they are susceptible to change and the impact could be material to our financial condition or operating results:

| ● |

Revenue recognition; and |

|

| ● |

Valuation of goodwill and identifiable intangible assets. |

Revenue Recognition

We derive a majority of our revenue from annually renewable subscription-based service agreements with our customers. Such agreements are generally cancelable on short or no notice without penalty. We also derive revenue from fixed, non-subscription arrangements. Our revenue recognition policy requires management to estimate, among other factors, the future contract consideration we expect to receive under variable consideration subscription arrangements as well as future total estimated contract costs over the contract term with respect to fixed, non-subscription arrangements. If management made different judgments and estimates, then the amount and timing of revenue for any period could differ from the reported revenue. See Notes 1 and 3 to our consolidated financial statements for a description of our revenue recognition policies.

Valuation of Goodwill and Identifiable Intangible Assets