Use these links to rapidly review the document

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark one) | ||

ý |

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2011 |

||

o |

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to .

Commission File No.: 000-09273

MOCON, Inc.

(Exact name of registrant as specified in its charter)

| Minnesota (State or other jurisdiction of incorporation or organization) |

41-0903312 (I.R.S. Employer Identification No.) |

|

7500 Mendelssohn Avenue North Minneapolis, Minnesota (Address of principal executive offices) |

55428 (Zip Code) |

Registrant's telephone number, including area code: (763) 493-6370

Securities registered under Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Common Stock, par value $0.10 per share | The NASDAQ Stock Market LLC (NASDAQ Global Market) |

Securities registered under Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES o NO ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES o NO ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ý NO o

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Act). YES o NO ý

The aggregate market value of the registrant's common stock, excluding outstanding shares beneficially owned by directors and executive officers, computed by reference to the price at which the common stock was last sold as of June 30, 2011 (the last business day of the registrant's second quarter) as reported by the Nasdaq Global Market System, was $77,049,164.

As of March 12, 2012, 5,470,898 shares of common stock of the registrant were deemed outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this annual report on Form 10-K incorporates by reference information (to the extent specific sections are referred to herein) from the registrant's Proxy Statement for its 2012 Annual Meeting of Shareholders to be held May 24, 2012.

This annual report on Form 10-K contains or incorporates by reference not only historical information, but also forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are subject to the safe harbor created by those sections. We refer you to the information under the heading "Part I. Item 1. Business—Forward-Looking Statements."

As used in this annual report on Form 10-K, references to "MOCON," the "Company," "we," "our" or "us," unless the context otherwise requires, refer to MOCON, Inc. and our subsidiaries.

All trademarks or trade names referred to in this report are the property of their respective owners.

MOCON, Inc. designs, manufactures, markets and services products, and provides consulting services, primarily in the test and measurement, analytical instrument and services markets. Our products include instruments that detect, measure and monitor gases and other chemical compounds which help our customers improve the quality of their products, as well as develop new products.

Our gas and vapor permeation instruments were first used in the food packaging industry, starting in the 1970s, to measure small amounts of moisture which can adversely affect dry cereals and other food packaging. Today our core business, the detection, measurement and analysis of vapors and gases, serves industries far beyond food packaging. Our products serve markets such as foods, beverages, pharmaceuticals and consumer products, oil and gas exploration and industrial and environmental safety. For example, our newest analyzers measure the parameters necessary to predict the safe shelf life of packaged foods. This effort, together with others, has allowed us to enter the food and beverage safety markets worldwide.

Our principal business strategy is to employ our product development and technological capabilities, manufacturing processes and sales and marketing skills where we can successfully penetrate the market and become a leader in the segment. Our management team continually emphasizes product innovation, product performance, quality improvements, cost reductions and other value-adding activities. We seek growth opportunities through technological and product improvement, by acquiring and developing new products, by acquiring companies or new product lines, or purchasing the rights to existing technologies.

MOCON, Inc. was incorporated as a Minnesota corporation in February 1966, and was initially involved in the commercialization of technology developed for the measurement of water vapor permeating through food packaging materials. Today, the key drivers in the industries we serve are food and beverage product safety and quality, improving workplace safety, supplying testing equipment for oil and gas exploration, and analyzing the quality of air both indoors and outdoors.

Historically, a significant portion of our sales has come from international customers. In recognition of the importance of our international customers, we maintain a physical presence in Europe through our wholly-owned subsidiary, Paul Lippke Handels-GmbH, located in Neuwied, Germany, and in Asia through a sales, service and laboratory facility in Shanghai, China.

Our current plans for growth include continued substantial funding for research and development to foster new product development and to pursue strategic acquisitions and investments where appropriate. In this regard, on March 9, 2012, we entered into an agreement to acquire PBI-Dansensor A/S (Dansensor) for approximately $20,000,000. Dansensor is a manufacturer of specialized instrumentation for Modified Atmosphere Packaging (MAP) of foods, beverages, pharmaceuticals and other perishable items. We currently expect to complete this acquisition on April 2, 2012.

2

Our principal executive offices and worldwide headquarters are located at 7500 Mendelssohn Avenue North, Minneapolis, Minnesota 55428 USA, and our telephone number is (763) 493-6370. Our website address is www.mocon.com. The information contained on our website or connected to our website is not incorporated by reference into this annual report on Form 10-K and should not be considered part of this report.

We make available, free of charge on our website, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission. We also make available, free of charge and through our website, to any shareholder who requests, the charters of our board committees and our Code of Ethics. Requests for copies can be directed to our Chief Financial Officer at the address and phone number above.

Products and Services

We develop, manufacture, market and service test and measurement, analytical and monitoring instruments and systems used to detect, measure and analyze gases and other chemical compounds, as well as providing related consulting services. Please see our consolidated financial statements beginning on page F-1 for financial information concerning our business, including our sales, net income and net assets. Our sales are grouped into four major categories as discussed below.

Permeation Products and Services

Our permeation products consist of systems and services that measure the rate at which various gases and vapors transmit through a variety of materials. These products perform measurements under precise temperature, pressure and relative humidity conditions. The principal market for these products consists of manufacturers of packaging materials, including manufacturers of papers, plastic films, coatings and containers and the users of such packaging materials, such as companies in the food, beverage, pharmaceutical and consumer product industries. Other customers include manufacturers of displays, solar panels, fuel cells, and many other sophisticated materials.

We also provide certain laboratory testing services to companies that have a need for permeation data. These services consist primarily of testing film and package permeation for companies that:

- •

- wish to outsource their testing needs to us;

- •

- are interested in evaluating our instrumentation prior to purchase; or

- •

- have purchased our products but have a need for additional capacity.

Our permeation products and services accounted for approximately 59%, 57% and 57% of our consolidated sales in 2011, 2010 and 2009, respectively. Permeation instruments that we currently manufacture include OX-TRAN® systems for oxygen transmission rates, PERMATRAN-W® systems for water vapor transmission rates, and PERMATRAN-C® systems for carbon dioxide transmission rates. Our AQUATRAN® ultra-high sensitivity, trace moisture permeation analyzer has been increasingly accepted as the standard test instrument of choice in the flat panel, solar cell and electronics industries. Our systems are available in a wide range of options for our customers, including high or low throughput, price, sensitivity and ease of use. They are primarily marketed to research and development departments, as well as production and quality assurance groups.

3

Gas Analyzer Instruments, Sensors and Detectors

Our Baseline-MOCON, Inc. subsidiary located near Boulder, Colorado offers advanced gas analysis and monitoring instrumentation used in applications such as oil and gas exploration, process gas analysis, industrial hygiene and safety, environmental air monitoring and indoor air quality.

In this group, we manufacture and sell two types of gas analyzer instruments: gas chromatographs (GCs) and total hydrocarbon analyzers (THA's). These instruments are typically installed in fixed locations at the monitoring sites and perform their functions of detecting and measuring various hydrocarbons continually or at regular intervals. We also make gas sensors and detectors which are sold to original equipment manufacturers (OEMs) of mobile gas safety equipment.

Our gas analyzer instruments, sensors and detectors are for use in industrial hygiene (detection of hazardous gases in the workplace), hydrocarbon gas analysis for oil and gas exploration, contaminant detection in the manufacture of specialty gases, and environmental monitoring (tracking the release, or the presence, of toxic substances). These substances can include the intentional release of toxic gases by terrorists which would be a homeland security application. Our newest GC offering measures trace levels of contaminants in beverage grade carbon dioxide which is used to carbonate soft drinks, beer and water.

Our gas analyzer instruments, sensors and detectors accounted for approximately 18% of our consolidated sales in each of the years 2011, 2010 and 2009, respectively. We market some of these products under the names BEVALERT®, PETROALERT®, and piD-TECH®.

Package Testing Products and Services

We manufacture and sell two primary products in this group—headspace analyzers and leak detection equipment. Our headspace analyzer products are used to analyze the amount and type of gas present in the headspace of flexible and rigid packages, as applied to gas flushing in modified or controlled atmosphere packaging. The principal market for these products consists of packagers of foods, beverages and pharmaceuticals. Our headspace analyzer products include the PAC CHECK® series of off-line headspace analyzers and the GSA™ series of on-line gas stream analyzers for continuous and intermittent monitoring of modified atmosphere packaging (MAP) and other gas flushing operations.

Our leak detection products detect leaks in sterile medical trays, food pouches, blister packs and a wide range of other sealed packages. We currently manufacture three types of leak detection instruments. The first type is a non-destructive leak detector that senses small amounts of carbon dioxide escaping from a package or tray. The second type of instrument detects leaks and checks for seal integrity by applying and measuring pressure within a package. The third type pulls a vacuum on a package and looks for vacuum or gas flow changes. The principal markets for these products are packagers of sterile medical items, pharmaceuticals and food products.

Our packaging products and services group accounted for 16%, 16% and 18% of our consolidated sales in 2011, 2010 and 2009, respectively. We market these products under the names PAC CHECK®, LIPPKE®, SKYE® and PAC GUARD®.

Other Instruments and Services

Consulting and Analytical Services

We provide consulting and analytical services, on a special project basis, for customers that require custom solutions to unique problems. Services that we typically provide relate to:

- •

- absorption or diffusion of various compounds;

4

- •

- shelf-life concerns;

- •

- flavor or odor identification; or

- •

- other special permeation applications.

The principal markets for our consulting and analytical services consist of manufacturers of foods, beverages, pharmaceuticals, plastics, chemicals, electronics and personal care products.

Gas Chromatography Analyzer Products and Services

We sell various gas chromatographic (GC) instruments and provide services with an emphasis on multidimensional gas chromatography through our Microanalytics Instrumentation Corp. (Microanalytics) subsidiary, which is located near Austin, Texas. A variety of GC specific applications have been developed by Microanalytics, ranging from petroleum and petrochemical purity assay to aroma and off-odor analysis for the food, beverage, packaging and other industries. We integrate GCs and components that we purchase from third parties to form multidimensional GC analyzer systems. These GC analyzers represent state-of-the-art technology in gas chromatographic separations and are used in identifying compounds causing off-odors in various products, in identifying critical aroma compounds, and in high purity analysis of single component matrixes. Our GC analyzer products include the AROMATRAX® systems for odor and aroma analysis and profiling. The principal markets for our GC analyzer products consist of food, beverage, pharmaceutical, petroleum, chemical and petrochemical manufacturers.

Weighing and Pharmaceutical Products and Services

Our weighing products automatically determine the weight of pharmaceutical capsules and tablets and reject those that are out of acceptable limits. Our VERICAP™ high-speed capsule weighing system runs at rates up to 2,000 capsules per minute and can be integrated into a capsule production line in pharmaceutical factories. Our AB™ automatic balance weighing systems are designed for off-line use for both tablets and capsules, and we market these products primarily to the pharmaceutical industry. In addition, we sell tablet inspection systems and blister packaging-related equipment through our Lippke subsidiary, which also sells products of other manufacturers.

Food Safety Products

Our food safety products are designed to automatically detect microbial contamination in food and beverage samples. Using the total viable count (TVC) method, our GreenLight series of instruments perform rapid and precise measurements of bacterial load in raw meats, poultry, seafood, dairy and produce samples. There are three models of the GreenLight instrument available with the Model 930 being released in July 2011.

Our other instruments and services groups accounted for an aggregate of approximately 7%, 9% and 7% of our consolidated sales in each of the years 2011, 2010 and 2009.

Competition

We have several competitors for all of our products and services in both foreign and domestic markets. The principal competitive factors for our products and services are:

- •

- product quality and performance;

- •

- product reliability;

- •

- product support; and

- •

- price.

5

We compete with a variety of companies in each market in which we sell our products. Some of our competitors have greater assets and resources than we do, and some are smaller than we are. To remain competitive, we must continue to invest in research and development, marketing, customer service and support, and manage our operating expenses. We believe that we have strategies in place to develop technological and other advantages that will give us a competitive advantage over our competitors. However, there can be no assurance that we will have sufficient resources to execute these strategies, or that our competitors will not develop new technologies or other advantages which would require us to reduce our prices, result in lost orders or otherwise adversely affect our financial results.

Manufacturing and Supplies

We manufacture products at our locations in Minnesota, Texas, Colorado and Germany. Our manufacturing capabilities include electro-mechanical assembly, testing, integration of components and systems, calibration and validation of systems. Certain components that we use in our products are currently purchased from single source suppliers. Although we maintain an inventory of these components, an interruption or delay in supply from one of these sources could result in delays in our production while we locate an alternative supplier, which in turn could result in a loss of sales and income.

Patents, Trademarks and Other Intellectual Property Rights

We believe that the protection afforded us by our patent rights is important to our business, and we will continue to seek patent protection for our technology and products. We require all of our employees and consultants to assign to us all inventions that are conceived and developed during their employment, except to the extent prohibited by applicable law. To protect our proprietary information, we have entered into confidentiality and non-compete agreements with those of our employees and consultants who have access to sensitive information. We hold both United States and international patents and have U.S. and international patents pending. We currently hold 40 active U.S. patents and 34 foreign patents which will expire during the period from 2012 through 2029, and have another 55 patents pending. We do not believe that the expiration of our patents on their scheduled expiration dates will have a material adverse effect on our business.

We own, have the right to use, or have applied for certain trademarks which protect and identify our products. Our trademarks and service marks include the following registered marks: MOCON®, APCHECK®, AQUATRACE®, AQUATRAN®, AROMATRAN®, AROMATRAX®, BASELINE®, BEVALERT®, CALCARD®, CAL-SMART®, COULOX®, FLO SMART®, GREENLIGHT®, HERSCH®, LIPPKE®, LIQUI-BLOK®, MICROANALYTICS®, MULTICHECK®, OPTECH®, OX-TRAN®, PAC CHECK®, PAC GUARD®, PERMATRAN-C®, PERMATRAN-W®, PETROALERT®, piD-TECH®, QUICK START®, SKYE® and VOC-TRAQ®. Our trademarks and service marks have a life of 5 to 20 years, and are subject to periodic maintenance which may be extended in accordance with applicable law.

Marketing and Customers; Distribution Methods

We market our products and services throughout the United States and in over 60 foreign markets. We use a direct sales force of approximately 25 employees and approximately 20 independent sales representatives to market and sell our products and services to end users in the United States, Canada, Germany and China, and use a network of approximately 50 independent sales representatives to market, service and sell our products and services in other foreign countries. To our knowledge, none of our independent sales representatives sell a material amount of product manufactured by any of our competitors.

6

For information concerning our export sales by geographic area, see Note 13 of the notes to consolidated financial statements. We market products and services to research laboratories, production departments and quality control groups in the life science, medical, food, pharmaceutical, plastics, paper, electronics, oil and gas and other industries. One independent representative accounted for approximately 10% of our consolidated sales in 2010, and another independent representative accounted for 6% in 2009. We do not believe that the loss of any single customer would have a material adverse effect on our business or financial performance.

Backlog

As of December 31, 2011, our total backlog was $4,685,976 for all of our products as compared to $6,055,065 and $2,440,794 as of December 31, 2010 and 2009, respectively. The decrease in backlog at the end of 2011 was due primarily to an unprecedented order volume received in the last quarter of 2010, which did not repeat in 2011. We anticipate shipping the majority of the current backlog in 2012.

Research and Development

We are committed to an ongoing engineering program dedicated to innovating new products and improving the quality and performance of our existing products. Our engineering expenses are primarily incurred in connection with the improvement of existing products, cost reduction efforts, and the development of new products that may have additional applications or represent extensions of existing product lines. None of these costs are borne directly by our customers.

We incurred expenses of $2,402,566, $2,135,365 and $1,847,993 during the fiscal years ended December 31, 2011, 2010 and 2009, respectively, for research and development (R&D) of our products. These amounts were approximately 6% to 7% of our consolidated sales for each of those three fiscal years. On an annual basis, we currently intend to spend approximately 6% to 8% of our consolidated sales on R&D in the future.

Working Capital Practices

We strive to maintain a level of inventory that is appropriate given our projected sales. Our standard domestic payment terms are net 30 days and our international payment terms vary but generally range between 30 and 90 days. International sales are, in some cases, transacted pursuant to letters of credit.

Seasonality

Our business is not seasonal in nature.

Employees

As of December 31, 2011, we had approximately 150 full-time employees. Included in this total are approximately 20 scientists and engineers who research and develop potential new products. None of our employees are represented by a labor union, and we consider our employee relations to be satisfactory.

7

Executive Officers of the Registrant

Our executive officers, their ages and their offices held, as of March 12, 2012 are as follows:

| Name | Age | Title | |||

|---|---|---|---|---|---|

Robert L. Demorest |

66 | Chairman of the Board, President and Chief Executive Officer, MOCON, Inc. | |||

Daniel W. Mayer |

61 |

Executive Vice President, MOCON, Inc. |

|||

Darrell B. Lee |

63 |

Vice President, Chief Financial Officer, Treasurer and Secretary, MOCON, Inc. |

|||

Douglas J. Lindemann |

54 |

Vice President and General Manager, MOCON, Inc. |

|||

Robert E. Forsberg |

56 |

President, Baseline-MOCON, Inc. |

|||

There are no family relationships among any of our directors and executive officers. Information regarding the business experience of our executive officers is set forth below.

Mr. Robert L. Demorest has been our President, Chief Executive Officer, and Chairman of the Board since April 2000. Mr. Demorest is also a director of Marten Transport, Ltd., a publicly traded company.

Mr. Daniel W. Mayer has been an Executive Vice President for us since January 1995.

Mr. Darrell B. Lee has been our Chief Financial Officer, Vice President, Treasurer and Secretary for more than five years.

Mr. Douglas J. Lindemann has been a Vice President and General Manager for more than five years.

Mr. Robert E. Forsberg has been the President of Baseline-MOCON, Inc. for more than five years.

Forward-Looking Statements

This Annual Report on Form 10-K contains or incorporates by reference not only historical information, but also forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are subject to the safe harbor created by those sections. In addition, we or others on our behalf may make forward-looking statements from time to time in oral presentations, including telephone conferences and/or web casts open to the public, in press releases or reports, on our website or otherwise. All statements other than statements of historical facts included in this Annual Report on Form 10-K that address activities, events or developments that we expect, believe or anticipate will or may occur in the future are forward-looking statements including, in particular, the statements about our plans, objectives, strategies and prospects regarding, among other things, our financial condition, results of operations, addressable market size estimates and business. We have identified some of these forward-looking statements with words like "believe," "may," "could," "might," "forecast," "possible," "potential," "project," "will," "should," "expect," "intend," "plan," "predict," "anticipate," "estimate," "approximate" or "continue" and other words and terms of similar meaning. These forward-looking statements may be contained in the notes to our consolidated financial statements and elsewhere in this

8

Annual Report on Form 10-K, including under the heading "Management's Discussion and Analysis of Financial Condition and Results of Operations."

Forward-looking statements involve risks and uncertainties. These uncertainties include factors that affect all businesses as well as matters specific to us. The following are some of the uncertainties and factors known to us that could cause our actual results to differ materially from what we have anticipated in our forward-looking statements: successfully competing against our competitors; acceptance, endorsement, and use of our products; technological changes and product obsolescence; our ability to identify acquisition candidates and successfully integrate the operations of those acquisitions into our existing operations; the impact of worldwide economic conditions on our operations; the disruption in global financial markets and the potential impact on the ability of our counterparties to perform their obligations and our ability to obtain future financing; factors impacting the stock market and share price; ability of our manufacturing facilities to meet customer demand; reliance on single source suppliers; loss or impairment of a principal manufacturing facility; regulatory matters; timing and success of new product introductions; adequate protection of our intellectual property rights; product liability claims; and currency and other economic risks inherent in selling our products internationally.

For more information regarding these and other uncertainties and factors that could cause our actual results to differ materially from what we have anticipated in our forward-looking statements or otherwise could materially adversely affect our business, financial condition or operating results, refer to this Annual Report on Form 10-K under Part I, Item 1A, "Risk Factors."

All forward-looking statements included in this Annual Report on Form 10-K are expressly qualified in their entirety by the foregoing cautionary statements. We wish to caution readers not to place undue reliance on any forward-looking statement that speaks only as of the date made and to recognize that forward-looking statements are predictions of future results, which may not occur as anticipated. Actual results could differ materially from those anticipated in the forward-looking statements and from historical results, due to the risks and uncertainties described in this Annual Report on Form 10-K under the heading "Item 1A. Risk Factors" below, as well as others that we may consider immaterial or do not anticipate at this time. Although we believe that the expectations reflected in our forward-looking statements are reasonable, we do not know whether our expectations will prove correct. The expectations reflected in our forward-looking statements can be affected by inaccurate assumptions we might make or by known or unknown risks and uncertainties, including those described below under the heading "Item 1A. Risk Factors." The risks and uncertainties described under the heading "Item 1A. Risk Factors" below are not exclusive and further information concerning us and our business, including factors that potentially could materially affect our financial results or condition, may emerge from time to time. We assume no obligation to update forward-looking statements to reflect actual results or changes in factors or assumptions affecting such forward-looking statements. We advise you, however, to consult any further disclosures we make on related subjects in our quarterly reports on Form 10-Q and current reports on Form 8-K we file with or furnish to the Securities and Exchange Commission.

9

The following are significant factors known to us that could have material adverse effects on our business, financial condition or operating results and should be considered carefully in connection with any evaluation of an investment in our common stock. Additionally, the following risk factors could cause our actual results to materially differ from those reflected in any forward-looking statements.

If economic conditions decline, companies may reduce their capital spending which could adversely affect our business, operating results and financial condition.

The Company's operations and performance depend significantly on worldwide economic conditions. Uncertainty about global economic conditions poses a risk as consumers and businesses postpone spending in response to tighter credit, unemployment, negative financial news and/or declines in income or asset values, which could have a material negative effect on demand for the Company's products and services. Our customers include pharmaceutical, food, medical and chemical companies, laboratories, government agencies and public and private research institutions. The capital spending of these entities can have a significant effect on the demand for our products. Decreases in capital spending by any of these customer groups could have a material adverse effect on our sales, business and results of operations.

Further, our customers' and independent representatives' ability to borrow money from their existing lenders or to obtain credit from other sources to purchase our products may be impaired. Although we maintain allowances for doubtful accounts for estimated losses resulting from the inability of our customers to make required payments and such losses have historically been within our expectations and the provisions established, we cannot guarantee that we will continue to experience the same loss rates that we have in the past, especially given the current turmoil in the worldwide economy. A significant change in the liquidity or financial condition of our customers could cause unfavorable trends in our receivable collections and additional allowances may be required, which could adversely affect our operating results. If investors have concerns that our business, operating results and financial condition will be negatively impacted by a worldwide economic downturn, our stock price could decrease.

If we fail to complete the acquisition of PBI-Dansensor (Dansensor), if we complete our planned acquisition of Dansensor and the financial performance of this company falls below expectations or if we fail to effectively integrate Dansensor with the rest of our organization, our operating results could be negatively impacted.

On March 9, 2012, we signed an acquisition agreement to acquire Dansensor for approximately $20,000,000. Dansensor is a manufacturer of specialized instrumentation for Modified Atmosphere Packaging (MAP) of foods, beverages, pharmaceuticals, and other perishable items. While we expect to complete this acquisition on or about April 2, 2012, the closing is subject to various conditions and if the conditions are not met, then we may not complete this acquisition and we will have spent substantial funds on pursuing this acquisition for which we will not receive any benefit.

If we do complete this acquisition, it will be the largest acquisition we have completed in our history. We made this acquisition based on the financial and strategic benefits of the acquisition that we expect to realize. Realizing these benefits could come with risks, which may include:

- •

- diversion of our management's attention from our core businesses;

- •

- difficulties in assimilating the operations and products of Dansensor and difficulties in realizing projected

efficiencies, cost savings and revenue synergies;

- •

- potential loss of key employees or customers of Dansensor or adverse effects on existing business relationships with suppliers and customers;

10

- •

- the indebtedness we will incur in connection with the indebtedness could in turn restrict our ability to access additional

capital when needed or to pursue other important elements of our business strategy; and

- •

- unexpected and undisclosed, contingent or other liabilities or problems.

If we fail to successfully integrate Dansensor, if the acquisition fails to meet our expectations or if there are events or changes in circumstances that adversely affect the value of this acquisition, then any intangibles or long-lived assets resulting from the acquisition of Dansensor may be deemed "impaired". If there are events or changes in circumstances that might adversely affect the value of Dansensor, we must assess whether the amount of this acquisition reflected on the balance sheet exceeds its fair value. Any write-down will reduce our reported net income and could possibly have a negative effect on our stock price.

In connection with the expected acquisition of Dansensor, we intend to enter into a credit agreement with Wells Fargo Bank. We expect the credit agreement will contain certain financial covenants, including financial covenants that require us to maintain a financial ratio that is impacted by the dividends we pay. We also expect that the credit agreement will contain certain operating covenants, including operating covenants that restrict future acquisitions that we can complete. If we are unable to meet the financial, operating or other covenants under the loan agreement and cannot negotiate waivers or amendments of the covenants, we may not be able to pay dividends or could be in default under the loan agreement, which would give Wells Fargo Bank a range of remedies, including declaring all outstanding debt to be due and payable and foreclosing on the assets securing the loan agreement.

At the same time we entered into the acquisition agreement to acquire Dansensor, we executed a commitment letter with Wells Fargo Bank. This commitment letter contemplates we will enter into a credit agreement that provides for a combination of a secured revolving credit line for $5.0 million and secured term debt for $3.5 million, each with a maturity of four years. The loan agreement will require us to maintain certain financial ratios, one of which is affected by the amount of dividends we pay. We may be required to reduce, or eliminate, the amount of dividends we pay to maintain this ratio. Although we currently believe that we will be able to pay dividends consistent with past practice without falling below the applicable ratio, there can be no guarantee that this will be the case. We believe that the price of our common stock would be negatively impacted if we reduced or eliminated our dividend payments.

In addition, we expect to be subject to certain operating covenants in the loan agreement which could limit our ability to conduct our business and respond to changing economic and business conditions and may place us at a competitive disadvantage relative to other companies that are subject to fewer restrictions. For example, pursuing acquisitions has been a part of our growth strategy. Under the loan agreement, we are restricted from doing certain acquisitions. Therefore, transactions that we may view as important opportunities such as acquisitions, will be subject to the consent of Wells Fargo Bank, which consent may be withheld or granted subject to conditions specified at the time. We also expect to be prohibited from repurchasing shares of our common stock without the consent of Wells Fargo Bank.

Under the loan agreement, we will grant to Wells Fargo a lien on all of our assets other than the shares of Dansensor we expect to acquire. We expect that the loan agreement will contain customary events of default, including, among others, the failure to comply with certain covenants or other agreements. We expect that upon the occurrence and during the continuation of an event of default, amounts due under the loan agreement could be accelerated by Wells Fargo Bank and Wells Fargo Bank could foreclose on our assets, which could have a material adverse effect on us.

11

In connection with the expected acquisition of Dansensor, we will enter into a financing agreement with the seller, PBI Holding A/S. Our obligations under the seller financing agreement will be secured by the shares of Dansensor that we acquire. If we fail to pay amounts due under the seller financing agreement on time or violate any of the provisions of this seller financing agreement, PBI Holding will have a range of remedies, including declaring all outstanding debt to be due and payable under the seller financing agreement and foreclosing on the shares of Dansensor.

If we close on the acquisition of Dansensor, we will enter into a loan agreement with PBI Holding, the seller of Dansensor, that will require us to pay approximately $6,600,000, plus interest, to PBI Holding over a four year period. To secure the performance of our obligations under this seller financing agreement, we will pledge the shares of Dansensor to PBI Holding. The seller financing agreement will prevent us from taking certain restructuring activities with respect to Dansensor until the loan to the seller is paid off, which could delay our ability to realize some expected synergies with Dansensor. If we default on our obligations under the seller financing agreement and are unable to obtain a waiver from PBI Holding, amounts due under the seller financing agreement could be accelerated by PBI Holding and they could foreclose on our shares of Dansensor, which could have a material adverse effect on us.

Some of the markets in which we operate have experienced minimal growth in recent years, and our ability to increase our sales will depend in part on our ability to develop new products, develop new applications for our existing products or acquire complementary businesses and product lines.

We have identified a number of strategies that we believe will allow us to grow our business and increase our sales in markets experiencing minimal growth, including developing new products and technologies, entering new markets such as food safety, capitalizing on our relationship with Luxcel Biosciences Limited, developing new applications for our technologies, acquiring complementary businesses and product lines, and strengthening our sales force. However, we can make no assurance that we will be able to successfully implement these strategies, or that these strategies will result in the growth of our business or an increase in our sales. Acquisitions that we may find attractive may be subject to the consent of Wells Fargo Bank under the loan agreement we intend to execute with them.

If we fail to attract and retain qualified managerial and technical personnel, we may fail to remain competitive.

Our future success depends, in significant part, upon the continued service and performance of our senior management and other key personnel. We rely on knowledgeable, experienced and skilled technical personnel, particularly engineers, scientists and service personnel, to design, assemble, sell and service our products. The loss of the services of our management team, some of whom have significant experience in our industry, and other key personnel could impair our ability to effectively manage our company and to carry out our business plan. Our inability to attract or retain qualified personnel could have a significant negative effect and thereby materially harm our business and financial condition.

If future operating results of Luxcel Biosciences Limited (Luxcel) do not meet our expectations, there is the possibility that our investment in this affiliated company could be deemed to be impaired, and thus a potential write-down may be warranted.

In January 2010, we acquired a minority equity interest in Luxcel for €2,500,000 (approximately $3,625,000). This investment is carried on our consolidated balance sheet at historical cost, adjusted only for currency fluctuations. We periodically assess this equity investment for impairment. If there are events or changes in circumstances that might adversely affect the value of this investment, we must assess whether the amount of this investment reflected on the balance sheet exceeds its fair value. Any write-down will reduce our reported net income and could possibly have a negative effect on our stock price.

12

We face risks of technological changes that may render our products obsolete.

The markets for our products and services are characterized by technological change and evolving industry standards. As a result of such changes and evolving standards, our products may become noncompetitive or obsolete and we may have to develop new products in order to maintain or increase our sales. New product introductions that are responsive to these factors require significant planning, design, development and testing at the technological, product and manufacturing process levels, and we may not be able to timely develop new products. In addition, industry acceptance of new technologies that we may develop may be slow due to, among other things, existing regulations or standards written specifically for older technologies and general unfamiliarity of users with new technologies. As a result, any new products that we may develop may not generate any meaningful sales or profits for us for a number of years, if at all.

A significant portion of our sales are generated from foreign countries and selling in foreign countries entails a number of risks which could result in a decrease in our sales or an increase in our operating expenses.

Sales outside the United States accounted for approximately 56% of our sales in each of the three years 2011, 2010, and 2009. We expect that foreign sales will continue to account for a significant portion of our revenues in the future, and the percentage of sales outside the United States will increase following our planned acquisition of Dansensor. Sales to customers in foreign countries are subject to a number of risks including, among others:

- •

- agreements may be difficult to enforce;

- •

- receivables may be difficult to collect;

- •

- certain regions may experience political unrest and conflict and economic instability;

- •

- foreign customers may have longer payment cycles;

- •

- the countries into which we sell may impose tariffs or adopt other restrictions on foreign trade;

- •

- currency fluctuations could reduce reported profitability in future periods;

- •

- fluctuations in exchange rates may affect product demand;

- •

- legal and regulatory requirements may be difficult to monitor and comply with, especially if inconsistent with U.S. laws

and regulations;

- •

- customizing products for foreign countries and managing and staffing international operations may lead to increased costs;

and

- •

- protection of intellectual property in foreign countries may be more difficult to enforce.

If any of these risks were to materialize, our sales into foreign countries could decline, or our operating costs could increase, which would adversely affect our financial results.

Fluctuations in foreign currency exchange rates could result in declines in our reported net sales and net earnings.

Because the functional currency of our foreign operations is the applicable local currency, we are exposed to foreign currency exchange rate risk arising from transactions in the normal course of business, such as sales to third party customers and purchases from suppliers denominated in foreign currencies. Our reported net sales and net earnings are subject to fluctuations in foreign exchange rates. Because our products are manufactured or sourced primarily from the United States, a stronger U.S. dollar generally has a negative impact on results from operations outside the United States while a weaker dollar generally has a positive effect. Our primary exchange rate exposure is with the euro. We generally do not use hedging activities to minimize the volatility associated with foreign currency exchange rate changes. If we do use such activities in the future, they also involve some risk.

13

Some of our competitors have greater resources than we do, which may provide our competitors with an advantage in the development and marketing of new products.

We currently encounter, and expect to continue to encounter, competition in the sale of our products. We believe that the principal competitive factors affecting the market for our products include product quality and performance, price, reliability and customer service. Our competitors include large multinational corporations. Some of our competitors have substantially greater financial, marketing and other resources than we do. As a result, they may be able to adapt more quickly to new or emerging technologies and changes in customer requirements, or to devote greater resources to the promotion and sale of their products than we can. In addition, competition could increase if new companies enter the market or if existing competitors expand their product lines or intensify efforts within existing product lines. Our current products, products under development and our ability to discover new technologies may be insufficient to enable us to compete effectively with our competitors.

Our reliance upon patents, domestic trademark laws, trade secrets and contractual provisions to protect our proprietary rights may not be sufficient to protect our intellectual property from others who may sell similar products.

We hold patents relating to various aspects of our products and believe that proprietary technical know-how is critical to many of our products. Proprietary rights relating to our products are protected from unauthorized use by third parties only to the extent that they are covered by valid and enforceable patents or are maintained in confidence as trade secrets. We cannot be certain that we will be issued any patents from any pending or future patent applications owned by or licensed to us or that the claims allowed under any issued patents will be sufficiently broad to protect our technology. In the absence of patent protection, we may be vulnerable to competitors who attempt to copy our products or gain access to our trade secrets and proprietary know-how. Our competitors may initiate litigation to challenge the validity of our patents, or they may use their resources to design comparable products that do not infringe our patents. We may incur substantial costs if our competitors initiate litigation to challenge the validity of our patents or if we initiate any proceedings to protect our proprietary rights. If the outcome of any such litigation is unfavorable to us, it could have a material adverse effect on our business and results of operations. There may also be pending or issued patents held by parties not affiliated with us that relate to our products or technologies and we may need to acquire licenses to any such patents to continue selling some or all of our products. If we are required to obtain any such license in order to be able to continue to sell some or all of our products, we may not be able to do so on terms that are favorable to us, if at all.

In addition, we rely on trade secrets and proprietary know-how that we seek to protect, in part, by confidentiality agreements with our collaborators, employees and consultants. These agreements may be breached and we may not have adequate remedies for any such breach. Even if these confidentiality agreements are not breached, our trade secrets may otherwise become known or be independently developed by competitors.

We rely on our management information systems for inventory management, distribution, accounting, and other functions. If our information systems fail to adequately perform these functions or if we experience an interruption in their operation, our business and results of operations could be adversely affected.

The efficient operation of our business depends on our management information systems. We rely on our management information systems to effectively manage accounting and financial functions, order entry, order fulfillment and inventory replenishment. The failure of our management information systems to perform could disrupt our business and could result in decreased sales, increased overhead costs, excess inventory and product shortages, causing our business and results of operations to suffer. In addition, our management information systems are vulnerable to damage or interruption from natural or man-made disasters, terrorist attacks, computer viruses or hackers, power loss, or other

14

computer systems, internet, telecommunications or data network failures. Any such interruption could adversely affect our business and results of operations.

We may encounter difficulties as we upgrade and evolve the capabilities of our computer systems, which could adversely impact our abilities to accomplish anticipated future cost savings and better serve our customers.

We are currently in the process of implementing a new enterprise resource planning (ERP) system which includes a major upgrade of the software used to run a number of the key processes critical to our business. If the new system does not function according to our expectations, it could adversely impact our results of operations and hinder our ability to adequately serve our customers.

The market price of our common stock has fluctuated significantly in the past and will likely continue to do so in the future and any broad market fluctuations may materially adversely affect the market price of our common stock.

The market price of our common stock has been volatile in the past, ranging from a high sales price of $17.67 and a low sales price of $11.97 during 2011, and several factors could cause the price to fluctuate substantially in the future. These factors include:

- •

- announcements of new products by us or our competitors;

- •

- quarterly fluctuations in our financial results;

- •

- merger and acquisition activity in our industry segment;

- •

- customer contract awards;

- •

- a change to the rates at which we have historically paid dividends, which could be impacted by our loan agreement with

Wells Fargo Bank;

- •

- developments in regulation; and

- •

- general economic and political conditions in the various markets where our products are sold.

In addition, the stock prices of instrumentation companies have experienced significant price and volume fluctuations that often have been unrelated to the operating performance of such companies. This market volatility may adversely affect the market price of our common stock.

Complying with securities laws and regulations is costly for us.

Changing laws, regulations and standards relating to corporate governance and public disclosure, including regulations promulgated by the SEC and Nasdaq, are creating particular challenges for smaller publicly-held companies like us. We are committed to maintaining high standards of corporate governance and public disclosure. As a result, our efforts to comply with evolving laws, regulations and standards have resulted in, and are likely to continue to result in, increased general and administrative expenses and a diversion of management time and attention from revenue-generating activities to compliance activities.

If we experience any increase in the cost of raw materials or supplies, we may experience a decrease in profit margins.

In the past, the overall cost of the materials that we purchase has not risen much more than the rate of inflation. We believe that the price of our products and the prices of our competitors' products is a significant factor affecting our customers' buying decisions and consequently, we may not be able to pass along any cost increases in raw materials and supplies in the form of price increases or sustain profit margins that we have achieved in prior years.

15

We have spent significant resources to develop new products in the food and beverage safety and packaging industries, and we have thus far only realized minimal revenues from these products.

Over the past two years we began to market our newest BevAlert system and OpTech-O2 analyzer. We believe that there are significant addressable markets for both of these products and while we believe both of these products are superior in many respects to other similar products being sold by our competitors, each one is new to the marketplace and may not gain the market acceptance necessary to allow us to capitalize on what we believe will be an increasing demand in the food and beverage industries for safety testing and monitoring products. While we have realized increasing sales of our BevAlert system and modest sales to date of our OpTech-O2 analyzer, there can be no assurance that sales of these products will continue. In August 2010, we introduced the GreenLight food safety test instrument which determines the presence or absence of bacteria in food products or ingredients. While we believe this product represents a dramatic improvement over existing technology being used in the food industry, we have not realized significant revenues to date.

If we are not able to successfully market these products, we will not recover the significant research and development and other expenses we have incurred to bring these products to market.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

We lease an aggregate of 74,175 square feet of office, engineering, laboratory and production space in Minnesota, Texas, Germany and China. We believe that all of our facilities are generally adequate for their present operations and that suitable space is readily available if any of our leases are not extended.

In March 2010, we signed a 15-year lease for a property which replaced our former Minneapolis headquarters and operations center. The new lease commenced July 1, 2010 and is for a location consisting of approximately 60,000 square feet of space, also in Minneapolis, Minnesota. This space is leased until October 2025.

Microanalytics' operations occupy approximately 5,100 square feet of space in the metropolitan area of Austin, Texas. This space is leased until February 2013.

Lippke's operations are located in Neuwied, Germany, and occupy approximately 8,075 square feet. This space is leased until July 2018.

The MOCON (Shanghai) Trading Co., Ltd. operations are located in Shanghai, China, and occupy approximately 1,000 square feet. This space is leased until December 2012.

In addition to our leased facilities described above, we own approximately two acres of land and a building located near Boulder, Colorado that consists of approximately 9,300 square feet of office and production space in which our Baseline-MOCON, Inc. subsidiary conducts its operations.

There are no material pending legal, governmental, administrative or other proceedings to which we are a party or of which any of our property is the subject.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

16

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information and Dividends

Our common stock is quoted on the Nasdaq Global Market System under the symbol MOCO. The following table sets forth, for the fiscal periods indicated, the high and low sales prices for our common stock as reported by the Nasdaq Global Market System. These quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not necessarily represent actual transactions. The following table also sets forth, for the fiscal periods indicated, the amount of cash dividends declared on our common stock:

| |

2011 | 2010 | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Fiscal Period

|

High | Low | Dividend | High | Low | Dividend | |||||||||||||

1st Quarter |

$ | 14.77 | $ | 11.97 | $ | 0.100 | $ | 11.10 | $ | 9.00 | $ | 0.095 | |||||||

2nd Quarter |

$ | 15.49 | $ | 13.91 | $ | 0.100 | 12.60 | 10.00 | 0.095 | ||||||||||

3rd Quarter |

$ | 17.67 | $ | 12.20 | $ | 0.100 | 12.90 | 10.02 | 0.095 | ||||||||||

4th Quarter |

$ | 17.00 | $ | 13.76 | $ | 0.100 | 13.85 | 11.85 | 0.095 | ||||||||||

We have paid quarterly cash dividends without interruption or decline since 1988. Cash dividends paid in 2011, 2010 and 2009 totaled $2,104,739, $1,952,872 and $1,958,750, respectively. Our Board of Directors monitors and evaluates our dividend practice quarterly, and the Board may elect at any time to increase, decrease or not pay a dividend on our common stock based upon our financial condition, results of operations, cash requirements and future prospects and other factors deemed relevant by the Board. Under the loan agreement we expect to sign with Wells Fargo Bank, we will be required to maintain certain financial ratios. One of these ratios will be impacted by the amount of dividends we pay. If paying dividends at our historical rate were to cause us to be out of compliance with this ratio, or otherwise cause us to be in breach of our covenants under our loan agreement with Wells Fargo Bank, we may be required to reduce or eliminate dividends until such time as we are able to repay our loan, regain compliance with the financial ratios and other covenants in the loan agreement, or negotiate a waiver or amendment with Wells Fargo Bank.

For information concerning securities authorized for issuance under equity compensation plans, please see Part III—Item 12.

Holders

As of March 12, 2012, there were approximately 250 holders of record and approximately 3,600 beneficial holders of our common stock.

Issuer Repurchases of Equity Securities

Other than the withholding of 2,327 shares of our common stock in connection with the cashless net exercise of stock options to pay the exercise price of such options, we did not repurchase any shares of our common stock or other equity securities of MOCON registered pursuant to Section 12 of the Securities Exchange Act of 1934, as amended, during the fourth quarter ended December 31, 2011. We currently are not authorized by our Board of Directors to make repurchases of our common stock.

Recent Sales of Unregistered Securities

During the fourth quarter and year ended December 31, 2011, we did not issue or sell any shares of our common stock or other equity securities of MOCON without registration under the Securities Act of 1933, as amended.

17

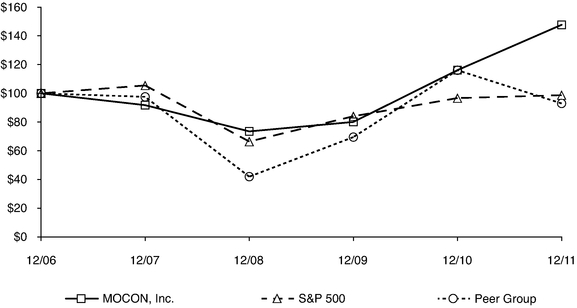

Stock Performance Graph

The following graph compares the cumulative shareholder return on MOCON's common stock to the S&P 500 Index and a peer group consisting of five companies with a market capitalization similar to MOCON. The peer companies were selected from the scientific and technical instruments industry within the technology sector. The graph compares the performance for the last five fiscal years, assuming an investment of $100 on December 31, 2006, including the reinvestment of all dividends. The peer group consists of the following companies: eMagin Corp., Transcat, Inc., Sypris Solutions, Inc., Dynasil Corporation of America and CyberOptics Corp. We picked these five companies because they operate in the same technology sector that we do and have a market capitalization similar to ours.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among MOCON, Inc., the S&P 500 Index, and a Peer Group

*$100 invested on 12/31/06 in stock or index, included reinvestment of dividends.

Fiscal year ending December 31.

| |

12/06 | 12/07 | 12/08 | 12/09 | 12/10 | 12/11 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

MOCON, Inc. |

100.00 | 91.78 | 73.50 | 80.09 | 116.15 | 147.71 | |||||||||||||

S&P 500 |

100.00 | 105.49 | 66.46 | 84.05 | 96.71 | 98.75 | |||||||||||||

Peer Group |

100.00 | 97.56 | 42.00 | 69.54 | 116.09 | 92.97 | |||||||||||||

18

ITEM 6. SELECTED FINANCIAL DATA

| |

Years Ended December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||

| |

(in thousands, except per share data) |

|||||||||||||||

CONSOLIDATED STATEMENT OF INCOME DATA: |

||||||||||||||||

Sales |

$ | 37,361 | $ | 31,549 | $ | 26,638 | $ | 29,696 | $ | 27,397 | ||||||

Net income |

5,451 | 4,518 | 2,910 | 4,059 | 3,805 | |||||||||||

Net income per common share: |

||||||||||||||||

Basic |

1.02 | 0.87 | 0.54 | 0.73 | 0.69 | |||||||||||

Diluted |

0.98 | 0.84 | 0.53 | 0.72 | 0.67 | |||||||||||

Cash dividends declared per share |

0.40 | 0.38 | 0.36 | 0.34 | 0.315 | |||||||||||

| |

As of December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||

| |

(in thousands) |

|||||||||||||||

CONSOLIDATED BALANCE SHEET DATA: |

||||||||||||||||

Current assets |

$ | 23,357 | $ | 19,399 | $ | 23,706 | $ | 22,357 | $ | 21,306 | ||||||

Total assets |

39,705 | 34,339 | 30,327 | 32,953 | 29,673 | |||||||||||

Current liabilities |

6,140 | 5,632 | 4,088 | 4,464 | 3,949 | |||||||||||

Noncurrent liabilities |

325 | 298 | 257 | 271 | 339 | |||||||||||

Stockholders' equity |

33,240 | 28,409 | 25,982 | 28,218 | 25,385 | |||||||||||

19

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

This Management's Discussion and Analysis provides material historical and prospective disclosures intended to enable investors and other users to assess our financial condition and results of operations. Statements that are not historical are forward-looking and involve risks and uncertainties including those discussed under the heading "Item 1A. Risk Factors" and elsewhere in this Annual Report on Form 10-K. For more information, see "Part I Item 1 Business—Forward-Looking Statements" of this Annual Report on Form 10-K. The following discussion of the results of the operations and financial condition of MOCON should be read in conjunction with our consolidated financial statements and the related notes thereto included elsewhere in this Annual Report on Form 10-K.

Overview

MOCON, Inc. designs, manufactures, markets and services products and provides consulting services primarily in the measurement and analytical instrument and services markets. Our products include instruments that detect, measure and monitor gases and chemical compounds. We continually seek growth opportunities through technological and product improvement, by acquiring and developing new products, and by acquiring synergistic companies or rights to technologies.

We have three primary operating locations in the United States—Minnesota, Colorado and Texas—and foreign operations in Germany and China. We use a mix of direct sales force and independent sales representatives to market our products and services in the United States, Canada, Germany and China and use a network of independent sales representatives to market and service our products and services in other foreign countries.

Historically, a significant portion of our sales has come from international customers. In recognition of the importance of our international business, we maintain a physical presence in Europe through our wholly-owned subsidiary located in Neuwied, Germany, and in Asia through a sales, service, and laboratory facility in Shanghai, China.

Our current plans for growth include substantial funding for research and development to foster new product development together with strategic acquisitions where appropriate. To that end, on March 9, 2012, we signed an agreement to acquire PBI-Dansensor, as more fully described earlier in this report.

Significant Transactions and Financial Trends

Throughout these financial sections, you will read about significant transactions or events that materially contribute to, or reduce our earnings, and materially affect our financial results and financial position. In 2011, we experienced a significant increase in sales and net income as all three major product categories recognized higher revenues. The largest increase came in our permeation products and services group due to the emphasis being placed on sustainable packaging materials as the marketplace becomes increasingly sensitive to environmental impact issues. In 2010, we experienced a significant increase in sales and net income as global economic conditions improved. We believe that the increase in 2010 was primarily due to pent-up demand, a large order from the Chinese government and the extension of Federal tax incentives for domestic purchases of capital equipment.

Our international sales have historically accounted for a significant portion of our revenues, and we expect our international sales, as a percentage of total sales, to increase as a result of our planned acquisition of PBI-Dansensor.

20

Our research and development costs were approximately 6% of our consolidated sales in 2011, and 7% of our consolidated sales in both 2010 and 2009. On an annual basis, we intend to spend approximately 6% to 8% of our sales on research and development in the future.

While these items are important in understanding and evaluating our financial results, certain trends, such as our international sales accounting for a significant portion of our revenues, and other transactions or events such as those discussed later in this Management's Discussion and Analysis, may also have a material impact on our financial results.

Critical Accounting Policies

Our significant accounting policies are described in Note 1 to our consolidated financial statements included in Item 8 of this Annual Report on Form 10-K. This Management's Discussion and Analysis of Financial Condition and Results of Operations is based upon our consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these consolidated financial statements requires management to make estimates and judgments that affect the reported amount of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities. The Securities and Exchange Commission has defined a company's most critical accounting policies as those that are most important to the portrayal of its financial condition and results of operations, and which require the company to make its most difficult and subjective judgments, often as a result of the need to make estimates of matters that are inherently uncertain. Based on this definition, we have identified the following critical accounting policies. Although we believe that our estimates and assumptions are reasonable, they are based upon information available when they are made. Actual results may differ significantly from these estimates under different assumptions or conditions.

Revenue Recognition

We recognize revenue when it is realized or realizable and earned. We consider revenue realized or realizable when persuasive evidence of an arrangement exists, the product has been shipped or the services have been provided to the customer, title and risk of loss of products has passed to the customer, the sales price is fixed or determinable, and collectability is reasonably assured. Our terms are FOB shipping point with no right of return, except in rare cases, and customer acceptance of our products is not required. The revenue recognition policy does not differ among the various product lines, the marketing venues, or various geographic destinations. We do not have distributors who stock our equipment. We do not offer rebates, price protection, or other similar incentives, and discounts when offered are recorded as a reduction in revenue. We record revenue net of sales tax charged to the customer.

Revenue for preventive maintenance agreements is recognized on a per visit basis and extended warranties on a straight-line basis over the life of the contracts.

In the first quarter 2010, we adopted ASC Topic 605 related to recognizing revenue from shipments with multiple element arrangements. This guidance provides that the overall arrangement fee will be allocated to each element (both delivered and undelivered items) based on their relative selling price, as demonstrated by vendor-specific objective evidence (VSOE) or third-party evidence (TPE). Where VSOE or TPE is not available, revenue will be allocated using an estimated selling price. This adoption did not have a material impact on our consolidated financial statements.

Allowance for Doubtful Accounts and Sales Returns

Our allowance for doubtful accounts and sales returns is for accounts receivable balances that are estimated to be uncollectible as well as anticipated sales returns. The reserve is based on a number of factors, including: (1) an analysis of customer accounts and (2) our historical experience with accounts

21

receivable write-offs and sales returns. The analysis includes the age of the receivable, the financial condition of a customer or industry and general economic conditions. We believe our financial results could be materially different if historical trends are not predictive of future results or if economic conditions worsened for our customers. In the event we determined that a smaller or larger allowance for doubtful accounts is appropriate, we would record a credit or charge to selling, general and administrative expense in the period that we made such a determination. As of December 31, 2011 and 2010, we had $150,921 and $183,291, respectively, reserved against our accounts receivable for doubtful accounts and sales returns.

Accrual for Excess and Obsolete Inventories

We perform an analysis to identify excess and obsolete inventory. We record a charge to cost of sales for amounts identified. Our analysis includes inventory levels, the nature of the components and their inherent risk of obsolescence, and the on-hand quantities relative to the sales history of that component. We believe that our financial results could be materially different if historical trends are not predictive of future results or if demand for our products decreased because of economic or competitive conditions or otherwise. As of December 31, 2011 and 2010, we had $364,591 and $320,195, respectively, accrued for excess and obsolete inventories.

Recoverability of Long-Lived Assets

We assess the recoverability of intangibles and other long-lived assets periodically whenever events or changes in circumstances indicate that expected future undiscounted cash flows might not be sufficient to support the carrying amount of an asset. We deem an asset to be impaired if a forecast of undiscounted future operating cash flows is less than an asset's carrying amount. If an asset is determined to be impaired, the loss is measured as the amount by which the carrying value of the asset exceeds its fair value. Changes in our business strategies, changes in the economic environment in which we operate, competitive conditions, and other factors could result in future impairment charges. We did not record any long-lived asset impairment charges in 2011 or 2010.

Goodwill

We assess the recoverability of goodwill on our annual measurement date or whenever events or changes in circumstances indicate that expected future undiscounted cash flows might not be sufficient to support the carrying amount of an asset. Goodwill is considered to be impaired if it is determined that the carrying amount of the reporting unit exceeds its fair value. Assessing the impairment of goodwill requires us to make judgments regarding the fair value of the net assets of our reporting units and the allocation of the carrying amount of shared assets to the reporting units. Our annual assessment included comparison of the carrying amount of the net assets of a reporting unit, including goodwill, to the fair value of the reporting unit. A significant change in our market capitalization or in the carrying amount of net assets of a reporting unit could result in an impairment charge in future periods. We did not record any goodwill impairment as the fair values of our reporting units substantially exceeded their carrying values.

Accrued Product Warranties

Our products are generally covered by a warranty, with warranty periods ranging from ninety days to one year from the date of sale. Estimated warranty costs are accrued in the same period in which the related revenue is recognized, based on anticipated parts and labor costs, utilizing historical experience. Additional warranty reserves are also accrued for major rework campaigns. We periodically assess the adequacy of our warranty reserves based on changes in these factors and record any necessary adjustments if actual claim experience indicates that adjustments are necessary. Although we believe the likelihood to be relatively low, warranty claims experience could be materially different

22

from actual results due to manufacturing changes that could impact product quality, a change in our warranty policy in response to industry trends, as yet unrecognized defects in products sold, or other factors. As of December 31, 2011 and 2010, we had $205,506 and $217,819, respectively, accrued for future estimated warranty claims.

Income Taxes

In the preparation of our consolidated financial statements, management is required to estimate income taxes in each of the jurisdictions in which we operate. This process involves estimating actual current tax exposures together with assessing temporary differences resulting from differing treatment of items for tax and accounting purposes. These differences result in deferred tax assets and liabilities, which are included in our Consolidated Balance Sheets.

Management reviews the deferred tax assets for recoverability on a quarterly basis and assesses the need for valuation allowances. These deferred tax assets are evaluated by considering historical levels of income, estimates of future taxable income streams and the impact of tax planning strategies. A valuation allowance is recorded to reduce deferred tax assets when it is determined that it is more likely than not that we would not be able to realize all or part of our deferred tax assets. At December 31, 2011 and 2010, we provided a valuation allowance in the amounts of $51,000 and $318,000, respectively, against our net deferred tax assets.