UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended March 31, 2021

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number: 1-1023

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||||||||

| , | , | ||||||||||||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||||||||

Registrant’s telephone number, including area code: 212 -438-1000

Securities registered pursuant to Section 12(b) of the Act:

| Class | Trading Symbol | Name of Exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Date File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☑ | ☐ | Accelerated filer | ☐ | Non-accelerated filer | Smaller reporting company | Emerging growth company | |||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO ☑

As of April 23, 2021 (latest practicable date), 240.9 million shares of the issuer's classes of common stock (par value $1.00 per share) were outstanding.

1

S&P Global Inc.

INDEX

| Page Number | |||||

Item 6. Exhibits | |||||

2

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Directors of S&P Global Inc.

Results of Review of Interim Financial Statements

We have reviewed the accompanying consolidated balance sheet of S&P Global Inc. (and subsidiaries) (the “Company”) as of March 31, 2021, the related consolidated statements of income, comprehensive income, equity (deficit) and cash flows for the three-month periods ended March 31, 2021 and 2020, and the related notes (collectively referred to as the “consolidated interim financial statements”). Based on our reviews, we are not aware of any material modifications that should be made to the consolidated interim financial statements for them to be in conformity with U.S. generally accepted accounting principles.

We have previously audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the consolidated balance sheet of the Company as of December 31, 2020, the related consolidated statements of income, comprehensive income, equity and cash flows for the year then ended, and the related notes and schedule (not presented herein); and in our report dated February 9, 2021, we expressed an unqualified audit opinion on those consolidated financial statements. In our opinion, the information set forth in the accompanying consolidated balance sheet as of December 31, 2020, is fairly stated, in all material respects, in relation to the consolidated balance sheet from which it has been derived.

Basis for Review Results

These financial statements are the responsibility of the Company's management. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the SEC and the PCAOB. We conducted our review in accordance with the standards of the PCAOB. A review of interim financial statements consists principally of applying analytical procedures and making inquiries of persons responsible for financial and accounting matters. It is substantially less in scope than an audit conducted in accordance with the standards of the PCAOB, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Accordingly, we do not express such an opinion.

/s/ ERNST & YOUNG LLP

New York, New York

April 29, 2021

3

PART I — FINANCIAL INFORMATION

Item 1. Financial Statements

S&P Global Inc.

Consolidated Statements of Income

(Unaudited)

| (in millions, except per share amounts) | Three Months Ended | ||||||||||

| March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| Revenue | $ | $ | |||||||||

| Expenses: | |||||||||||

| Operating-related expenses | |||||||||||

| Selling and general expenses | |||||||||||

| Depreciation | |||||||||||

| Amortization of intangibles | |||||||||||

| Total expenses | |||||||||||

| Gain on dispositions | ( | ( | |||||||||

| Operating profit | |||||||||||

| Other (income) expense, net | ( | ||||||||||

| Interest expense, net | |||||||||||

| Income before taxes on income | |||||||||||

| Provision for taxes on income | |||||||||||

| Net income | |||||||||||

Less: net income attributable to noncontrolling interests | ( | ( | |||||||||

| Net income attributable to S&P Global Inc. | $ | $ | |||||||||

Earnings per share attributable to S&P Global Inc. common shareholders: | |||||||||||

| Net income: | |||||||||||

| Basic | $ | $ | |||||||||

| Diluted | $ | $ | |||||||||

| Weighted-average number of common shares outstanding: | |||||||||||

| Basic | |||||||||||

| Diluted | |||||||||||

| Actual shares outstanding at period end | |||||||||||

See accompanying notes to the unaudited consolidated financial statements.

4

S&P Global Inc.

Consolidated Statements of Comprehensive Income

(Unaudited)

| (in millions) | Three Months Ended | ||||||||||

| March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| Net income | $ | $ | |||||||||

| Other comprehensive income: | |||||||||||

Foreign currency translation adjustments | ( | ( | |||||||||

Income tax effect | ( | ||||||||||

| ( | ( | ||||||||||

Pension and other postretirement benefit plans | |||||||||||

Income tax effect | ( | ( | |||||||||

| Unrealized gain (loss) on cash flow hedges | ( | ||||||||||

Income tax effect | |||||||||||

| ( | |||||||||||

| Comprehensive income | |||||||||||

Less: comprehensive income attributable to nonredeemable noncontrolling interests | ( | ( | |||||||||

Less: comprehensive income attributable to redeemable noncontrolling interests | ( | ( | |||||||||

Comprehensive income attributable to S&P Global Inc. | $ | $ | |||||||||

See accompanying notes to the unaudited consolidated financial statements.

5

S&P Global Inc.

Consolidated Balance Sheets

| (in millions) | March 31, 2021 | December 31, 2020 | |||||||||

| (Unaudited) | |||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash | |||||||||||

Accounts receivable, net of allowance for doubtful accounts: 2021 - $ | |||||||||||

| Prepaid and other current assets | |||||||||||

| Total current assets | |||||||||||

Property and equipment, net of accumulated depreciation: 2021 - $ | |||||||||||

| Right of use assets | |||||||||||

| Goodwill | |||||||||||

| Other intangible assets, net | |||||||||||

| Other non-current assets | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES AND EQUITY | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

Accrued compensation and contributions to retirement plans | |||||||||||

| Income taxes currently payable | |||||||||||

| Unearned revenue | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Long-term debt | |||||||||||

| Lease liabilities — non-current | |||||||||||

| Pension and other postretirement benefits | |||||||||||

| Other non-current liabilities | |||||||||||

| Total liabilities | |||||||||||

| Redeemable noncontrolling interest (Note 8) | |||||||||||

| Commitments and contingencies (Note 12) | |||||||||||

| Equity: | |||||||||||

| Common stock | |||||||||||

| Additional paid-in capital | |||||||||||

| Retained income | |||||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

| Less: common stock in treasury | ( | ( | |||||||||

| Total equity — controlling interests | |||||||||||

| Total equity — noncontrolling interests | |||||||||||

| Total equity | |||||||||||

| Total liabilities and equity | $ | $ | |||||||||

See accompanying notes to the unaudited consolidated financial statements.

6

S&P Global Inc.

Consolidated Statements of Cash Flows

(Unaudited)

| (in millions) | Three Months Ended | ||||||||||

| March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| Operating Activities: | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to cash provided by operating activities: | |||||||||||

| Depreciation | |||||||||||

| Amortization of intangibles | |||||||||||

| Provision for losses on accounts receivable | |||||||||||

| Deferred income taxes | ( | ( | |||||||||

| Stock-based compensation | |||||||||||

| Gain on dispositions | ( | ( | |||||||||

| Other | |||||||||||

| Changes in operating assets and liabilities, net of effect of acquisitions and dispositions: | |||||||||||

| Accounts receivable | |||||||||||

| Prepaid and other current assets | ( | ( | |||||||||

| Accounts payable and accrued expenses | ( | ( | |||||||||

| Unearned revenue | ( | ( | |||||||||

| Other current liabilities | |||||||||||

| Net change in prepaid/accrued income taxes | |||||||||||

| Net change in other assets and liabilities | ( | ( | |||||||||

| Cash provided by operating activities | |||||||||||

| Investing Activities: | |||||||||||

| Capital expenditures | ( | ( | |||||||||

| Acquisitions, net of cash acquired | ( | ( | |||||||||

| Proceeds from disposition | |||||||||||

| Changes in short-term investments | |||||||||||

| Cash used for investing activities | ( | ( | |||||||||

| Financing Activities: | |||||||||||

| Dividends paid to shareholders | ( | ( | |||||||||

| Distributions to noncontrolling interest holders, net | ( | ( | |||||||||

| Repurchase of treasury shares | ( | ||||||||||

| Exercise of stock options | |||||||||||

| Employee withholding tax on share-based payments | ( | ( | |||||||||

| Cash used for financing activities | ( | ( | |||||||||

| Effect of exchange rate changes on cash | ( | ( | |||||||||

| Net change in cash, cash equivalents, and restricted cash | ( | ||||||||||

| Cash, cash equivalents, and restricted cash at beginning of period | |||||||||||

| Cash, cash equivalents, and restricted cash at end of period | $ | $ | |||||||||

See accompanying notes to the unaudited consolidated financial statements.

7

S&P Global Inc.

Consolidated Statements of Equity (Deficit)

(Unaudited)

| Three Months Ended March 31, 2021 | |||||||||||||||||||||||||||||||||||||||||||||||

| (in millions) | Common Stock $1 par | Additional Paid-in Capital | Retained Income | Accumulated Other Comprehensive Loss | Less: Treasury Stock | Total SPGI Equity | Noncontrolling Interests | Total Equity | |||||||||||||||||||||||||||||||||||||||

| Balance as of December 31, 2020 | $ | $ | $ | ( | $ | $ | $ | 62 | $ | ||||||||||||||||||||||||||||||||||||||

Comprehensive income 1 | ( | ||||||||||||||||||||||||||||||||||||||||||||||

Dividends (Dividend declared per common share — $ | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||

| Employee stock plans | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||

| Change in redemption value of redeemable noncontrolling interest | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||

| Other | |||||||||||||||||||||||||||||||||||||||||||||||

| Balance as of March 31, 2021 | $ | $ | $ | $ | ( | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||

| Three Months Ended March 31, 2020 | |||||||||||||||||||||||||||||||||||||||||||||||

| (in millions) | Common Stock $1 par | Additional Paid-in Capital | Retained Income | Accumulated Other Comprehensive Loss | Less: Treasury Stock | Total SPGI Equity | Noncontrolling Interests | Total Equity | |||||||||||||||||||||||||||||||||||||||

| Balance as of December 31, 2019 | $ | $ | $ | $ | ( | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||

Comprehensive income 1 | ( | ||||||||||||||||||||||||||||||||||||||||||||||

Dividends (Dividend declared per common share — $ | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||

| Share repurchases | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||

Employee stock plans | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||

Change in redemption value of redeemable noncontrolling interest | |||||||||||||||||||||||||||||||||||||||||||||||

| Other | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||

| Balance as of March 31, 2020 | $ | $ | $ | $ | ( | $ | $ | ( | $ | $ | ( | ||||||||||||||||||||||||||||||||||||

1Excludes comprehensive income of $51 million and $49 million for the three months ended March 31, 2021 and 2020, respectively, attributable to our redeemable noncontrolling interest.

See accompanying notes to the unaudited consolidated financial statements.

8

S&P Global Inc.

Notes to the Consolidated Financial Statements

(Unaudited)

1. Nature of Operations and Basis of Presentation

S&P Global Inc. (together with its consolidated subsidiaries, "S&P Global," the “Company,” “we,” “us” or “our”) is a leading provider of transparent and independent ratings, benchmarks, analytics and data to the capital and commodity markets worldwide.

Our operations consist of four reportable segments: S&P Global Ratings ("Ratings"), S&P Global Market Intelligence ("Market Intelligence"), S&P Global Platts ("Platts") and S&P Dow Jones Indices ("Indices").

•Ratings is an independent provider of credit ratings, research, and analytics, offering investors and other market participants information, ratings and benchmarks.

•Market Intelligence is a global provider of multi-asset-class data, research and analytical capabilities, which integrate cross-asset analytics and desktop services.

•Platts is the leading independent provider of information and benchmark prices for the commodity and energy markets.

•Indices is a global index provider that maintains a wide variety of valuation and index benchmarks for investment advisors, wealth managers and institutional investors.

The accompanying unaudited financial statements of the Company have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and notes required by U.S. GAAP for complete financial statements. Therefore, the financial statements included herein should be read in conjunction with the financial statements and notes included in our Form 10-K for the year ended December 31, 2020 (our “Form 10-K”). Certain prior-year amounts have been reclassified to conform with current presentation.

In the opinion of management, all normal recurring adjustments considered necessary for a fair statement of the results of the interim periods have been included. The operating results for the three months ended March 31, 2021 are not necessarily indicative of the results that may be expected for the full year.

Restricted Cash

Restricted cash of $18 million and $14 million included in our consolidated balance sheets as of March 31, 2021 and December 31, 2020, respectively, includes amounts held in escrow accounts in connection with our acquisition of Kensho.

Contract Assets

Contract assets include unbilled amounts from when the Company transfers service to a customer before a customer pays consideration or before payment is due. As of March 31, 2021 and December 31, 2020, contract assets were $16 million and $7 million, respectively, and are included in accounts receivable in our consolidated balance sheets.

Unearned Revenue

We record unearned revenue when cash payments are received in advance of our performance. The decrease in the unearned revenue balance at March 31, 2021 compared to December 31, 2020 is primarily driven by $883 million of revenues recognized that were included in the unearned revenue balance at the beginning of the period, offset by cash payments received in advance of satisfying our performance obligations.

9

Remaining Performance Obligations

Remaining performance obligations represent the transaction price of contracts for work that has not yet been performed. As of March 31, 2021, the aggregate amount of the transaction price allocated to remaining performance obligations was $2.2 billion. We expect to recognize revenue on approximately half and three-quarters of the remaining performance obligations over the next 12 and 24 months, respectively, with the remainder recognized thereafter.

We do not disclose the value of unfulfilled performance obligations for (i) contracts with an original expected length of one year or less and (ii) contracts where revenue is a usage-based royalty promised in exchange for a license of intellectual property.

Costs to Obtain a Contract

We recognize an asset for the incremental costs of obtaining a contract with a customer if we expect the benefit of those costs to be longer than one year. We have determined that the costs associated with certain sales commission programs are incremental to the costs to obtain contracts with customers and therefore meet the criteria to be capitalized. Total capitalized costs to obtain a contract were $124 million and $129 million as of March 31, 2021 and December 31, 2020, respectively, and are included in prepaid and other current assets and other non-current assets on our consolidated balance sheets. The capitalized asset will be amortized over a period consistent with the transfer to the customer of the goods or services to which the asset relates, calculated based on the customer term and the average life of the products and services underlying the contracts which has been determined to be approximately 5 years. The expense is recorded within selling and general expenses.

We expense sales commissions when incurred if the amortization period is one year or less. These costs are recorded within selling and general expenses.

Other (Income) Expense, net

The components of other (income) expense, net for the three months ended March 31 are as follows:

| (in millions) | 2021 | 2020 | |||||||||

| Other components of net periodic benefit cost | $ | ( | $ | ( | |||||||

| Net loss from investments | |||||||||||

| Other (income) expense, net | $ | ( | $ | ||||||||

10

2. Acquisitions and Divestitures

Acquisitions

Merger Agreement

In November of 2020, S&P Global and IHS Markit Ltd ("IHS Markit") entered into a merger agreement, pursuant to which, among other things, a subsidiary of S&P Global will merge with and into IHS Markit, with IHS Markit surviving the merger as a wholly owned subsidiary of S&P Global. Under the terms of the merger agreement, each share of IHS Markit issued and outstanding (other than excluded shares and dissenting shares) will be converted into the right to receive 0.2838 fully paid and nonassessable shares of S&P Global common stock (and, if applicable, cash in lieu of fractional shares, without interest), less any applicable withholding taxes. As of February 28, 2021, IHS Markit had approximately 398.5 million shares outstanding. On March 11, 2021, S&P Global and IHS Markit shareholders voted to approve the merger agreement. Subject to certain closing conditions, the merger is expected to be completed in the second half of 2021.

2021

During the three months ended March 31, 2021, we did not complete any material acquisitions.

2020

In February of 2020, CRISIL, included within our Ratings segment, completed the acquisition of Greenwich Associates LLC ("Greenwich"), a leading provider of proprietary benchmarking data, analytics and qualitative, actionable insights that helps financial services firms worldwide measure and improve business performance. The acquisition will complement CRISIL's existing portfolio of products and expand offerings to new segments across financial services including commercial banks and asset and wealth managers. The acquisition of Greenwich is not material to our consolidated financial statements.

In January of 2020, we completed the acquisition of the ESG Ratings Business from RobecoSAM, which includes the widely followed SAM* Corporate Sustainability Assessment, an annual evaluation of companies' sustainability practices. The acquisition will bolster our position as the premier resource for essential environmental, social, and governance ("ESG") insights and product solutions for our customers. Through this acquisition, we will be able to offer our customers even more transparent, robust and comprehensive ESG solutions. The acquisition of the ESG Ratings Business is not material to our consolidated financial statements.

Divestitures

2021

During the three months ended March 31, 2021, we did not complete any dispositions.

During the three months ended March 31, 2021, we recorded a pre-tax gain of $2 million ($2 million after-tax) in Gain on dispositions in the consolidated statements of income related to the sale of Standard & Poor's Investment Advisory Services LLC ("SPIAS"), a business within our Market Intelligence segment, in July of 2019.

2020

In January of 2020, Market Intelligence entered into a strategic alliance to transition S&P Global Market Intelligence's Investor Relations ("IR") webhosting business to Q4 Inc. ("Q4"), a third party provider of investor relations related services. This alliance will integrate Market Intelligence's proprietary data into Q4's portfolio of solutions, enabling further opportunities for commercial collaboration. In connection with transitioning its IR webhosting business to Q4, Market Intelligence made a minority investment in Q4. During the three months ended March 31, 2020, we recorded a pre-tax gain of $7 million ($7 million after-tax) in Gain on dispositions in the consolidated statements of income related to the sale of IR.

11

The operating profit of our businesses that were disposed of for the periods ending March 31, 2021 and 2020 is as follows:

| (in millions) | 2021 | 2020 | |||||||||

Operating profit 1 | $ | $ | |||||||||

1 The three months ended March 31, 2021 excludes a pre-tax gain related to the sale of the SPIAS of $2 million. The three months ended March 31, 2020 excludes a pre-tax gain on the sale of the IR webhosting business of $7 million.

3. Income Taxes

The effective income tax rate was 23.4 % and 21.5 % for the three months ended March 31, 2021 and March 31, 2020, respectively. The increase in the three months ended March 31, 2021 was primarily due to a decrease in the recognition of excess tax benefits associated with share-based payments and an increase in taxes on foreign operations. At the end of each interim period, we estimate the annual effective tax rate and apply that rate to our ordinary quarterly earnings. The tax expense or benefit related to significant unusual or infrequently occurring items that will be separately reported or reported net of their related tax effect, and are individually computed, is recognized in the interim period in which those items occur. In addition, the effect of changes in enacted tax laws or rates or tax status is recognized in the interim period in which the change occurs.

The Company is continuously subject to tax examinations in various jurisdictions. As of March 31, 2021 and December 31, 2020, the total amount of federal, state and local, and foreign unrecognized tax benefits was $126 million and $121 million, respectively, exclusive of interest and penalties. We recognize accrued interest and penalties related to unrecognized tax benefits in interest expense and operating-related expense, respectively. As of March 31, 2021 and December 31, 2020, we had $25 million and $24 million, respectively, of accrued interest and penalties associated with unrecognized tax benefits. Based on the current status of income tax audits, we believe that the total amount of unrecognized tax benefits may decrease by approximately $18 million in the next twelve months as a result of the resolution of local tax examinations.

12

4. Debt

A summary of long-term debt outstanding is as follows:

| (in millions) | March 31, 2021 | December 31, 2020 | |||||||||

| Long-term debt | |||||||||||

1Interest payments are due semiannually on June 15 and December 15, and as of March 31, 2021, the unamortized debt discount and issuance costs total $5 million.

2Interest payments are due semiannually on January 22 and July 22, and as of March 31, 2021, the unamortized debt discount and issuance costs total $5 million.

3Interest payments are due semiannually on June 1 and December 1, and as of March 31, 2021, the unamortized debt discount and issuance costs total $4 million.

4Interest payments are due semiannually on February 15 and August 15, beginning on February 15, 2021, and as of March 31, 2021, the unamortized debt discount and issuance costs total $8 million.

5Interest payments are due semiannually on May 15 and November 15, and as of March 31, 2021, the unamortized debt discount and issuance costs total $3 million.

6Interest payments are due semiannually on May 15 and November 15, and as of March 31, 2021, the unamortized debt discount and issuance costs total $10 million.

7Interest payments are due semiannually on June 1 and December 1, and as of March 31, 2021, the unamortized debt discount and issuance costs total $11 million.

8Interest payments are due semiannually on February 15 and August 15, beginning on February 15, 2021, and as of March 31, 2021, the unamortized debt discount and issuance costs total $19 million.

The fair value of our total debt borrowings was $4.3 billion and $4.6 billion as of March 31, 2021 and December 31, 2020, respectively, and was estimated based on quoted market prices.

On April 26, 2021, we entered into a revolving $1.5 billion five-year credit agreement (our "credit facility") that will terminate on April 26, 2026. This credit facility replaced our revolving $1.2 billion five-year credit facility (our "previous credit facility") that was scheduled to terminate on June 30, 2022. The previous credit facility was canceled immediately after the new credit facility became effective. There were no outstanding borrowings under the previous credit facility when it was replaced.

As of March 31, 2021 and December 31, 2020, we had the ability to borrow a total of $1.2 no

Depending on our corporate credit rating, we paid a commitment fee of 8 to 17.5 basis points for our previous credit facility, whether or not amounts have been borrowed. During the three months ended March 31, 2021, we paid a commitment fee of 10 basis points. The interest rate on borrowings under our previous credit facility was, at our option, calculated using rates that are primarily based on either the prevailing London Inter-Bank Offer Rate, the prime rate determined by the administrative agent or the Federal Funds Rate. For certain borrowings under this previous credit facility, there was also a spread based on our corporate credit rating.

13

5. Derivative Instruments

Our exposure to market risk includes changes in foreign exchange rates and interest rates. We have operations in foreign countries where the functional currency is primarily the local currency. For international operations that are determined to be extensions of the parent company, the U.S. dollar is the functional currency. We typically have naturally hedged positions in most countries from a local currency perspective with offsetting assets and liabilities. As of March 31, 2021 and December 31, 2020, we have entered into foreign exchange forward contracts to mitigate or hedge the effect of adverse fluctuations in foreign exchange rates and cross currency swap contracts to hedge a portion of our net investment in a foreign subsidiary against volatility in foreign exchange rates. During the three months ended March 31, 2021, we entered into a series of interest rate swaps to mitigate or hedge the adverse fluctuations in interest rates on our future debt refinancing. These contracts are recorded at fair value that is based on foreign currency exchange rates and interest rates in active markets; therefore, we classify these derivative contracts within Level 2 of the fair value hierarchy. We do not enter into any derivative financial instruments for speculative purposes.

Undesignated Derivative Instruments

During the three months ended March 31, 2021 and twelve months ended December 31, 2020, we entered into foreign exchange forward contracts in order to mitigate the change in fair value of specific assets and liabilities in the consolidated balance sheet. These forward contracts do not qualify for hedge accounting. As of March 31, 2021 and December 31, 2020, the aggregate notional value of these outstanding forward contracts was $178 million and $460 million, respectively. The changes in fair value of these forward contracts are recorded in prepaid and other assets or other current liabilities in the consolidated balance sheet with their corresponding change in fair value recognized in selling and general expenses in the consolidated statement of income. The amount recorded in other current liabilities as of March 31, 2021 and December 31, 2020 was $1 million and $2 million, respectively. The amount recorded in selling and general expense related to these contracts was a net loss of $6 million and $11 million for three months ended March 31, 2021 and 2020, respectively.

Net Investment Hedges

During the three months ended March 31, 2021 and twelve months ended December 31, 2020, we entered into cross currency swaps to hedge a portion of our net investment in a certain European subsidiary against volatility in the Euro/U.S. dollar exchange rate. These swaps are designated and qualify as a hedge of a net investment in a foreign subsidiary and are scheduled to mature in 2024, 2029, 2030 As of March 31, 2021 and December 31, 2020, the notional value of our outstanding cross currency swaps designated as a net investment hedge was $1 5 million and $3 million for the three months ended March 31, 2021 and 2020, respectively.

Cash Flow Hedges

Foreign Exchange Forward Contracts

During the three months ended March 31, 2021 and twelve months ended December 31, 2020, we entered into a series of foreign exchange forward contracts to hedge a portion of the Indian rupee, British pound, and Euro exposures through the first quarter of 2023 and the fourth quarter of 2022, respectively.These contracts are intended to offset the impact of movement of exchange rates on future revenue and operating costs and are scheduled to mature within twenty-four months . The changes in the fair value of these contracts are initially reported in accumulated other comprehensive loss in our consolidated balance sheet and are subsequently reclassified into revenue and selling and general expenses in the same period that the hedged transaction affects earnings.

As of March 31, 2021, we estimate that $19 million of pre-tax gain related to foreign exchange forward contracts designated as cash flow hedges recorded in other comprehensive income is expected to be reclassified into earnings within the next twenty-four months.

14

As of March 31, 2021 and December 31, 2020, the aggregate notional value of our outstanding foreign exchange forward contracts designated as cash flow hedges was $491 million and $489 million, respectively.

Interest Rate Swaps

During the three months ended March 31, 2021, we entered into a series of interest rate swaps. These contracts are intended to mitigate or hedge the adverse fluctuations in interest rates on our future debt refinancing and are scheduled to mature beginning in the first quarter of 2027. These interest rate swaps are designated as cash flow hedges. The changes in the fair value of these contracts are initially reported in accumulated other comprehensive loss in our consolidated balance sheet and are subsequently reclassified into Interest expense, net in the same period that the hedged transaction affects earnings.

As of March 31, 2021, we estimate that $2 million of pre-tax gains related to interest rate swaps designated as cash flow hedges recorded in other comprehensive income is expected to be reclassified into earnings within the next twenty-four months.

As of March 31, 2021, the aggregate notional value of our outstanding interest rate swaps designated as cash flow hedges was $2.3 billion.

The following table provides information on the location and fair value amounts of our cash flow hedges and net investment hedges as of March 31, 2021 and December 31, 2020:

| (in millions) | March 31, | December 31, | ||||||||||||

| Balance Sheet Location | 2021 | 2020 | ||||||||||||

| Derivatives designated as cash flow hedges: | ||||||||||||||

| Prepaid and other current assets | Foreign exchange forward contracts | $ | $ | |||||||||||

| Prepaid and other current assets | Interest rate swap contracts | $ | $ | |||||||||||

| Other current liabilities | Foreign exchange forward contracts | $ | $ | |||||||||||

| Derivatives designated as net investment hedges : | ||||||||||||||

| Other non-current liabilities | Cross currency swaps | $ | $ | |||||||||||

The following table provides information on the location and amounts of pre-tax gains (losses) on our cash flow hedges and net investment hedges for the three months ended March 31:

| (in millions) | Gain (Loss) recognized in Accumulated Other Comprehensive Loss (effective portion) | Location of Gain (Loss) reclassified from Accumulated Other Comprehensive Loss into Income (effective portion) | Gain (Loss) reclassified from Accumulated Other Comprehensive Loss into Income (effective portion) | ||||||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||||||||

| Cash flow hedges - designated as hedging instruments | |||||||||||||||||||||||||||||

| Foreign exchange forward contracts | $ | $ | ( | Revenue, Selling and general expenses | $ | $ | ( | ||||||||||||||||||||||

| Interest rate swap contracts | $ | $ | Interest expense, net | $ | $ | ||||||||||||||||||||||||

| Net investment hedges - designated as hedging instruments | |||||||||||||||||||||||||||||

| Cross currency swaps | $ | $ | $ | $ | |||||||||||||||||||||||||

15

| (in millions) | 2021 | 2020 | |||||||||

| Cash Flow Hedges | |||||||||||

| Foreign exchange forward contracts | |||||||||||

| Net unrealized gains (losses) on cash flow hedges, net of taxes, beginning of period | $ | $ | |||||||||

| Change in fair value, net of tax | ( | ||||||||||

| Reclassification into earnings, net of tax | ( | ||||||||||

| Net unrealized gains (losses) on cash flow hedges, net of taxes, end of period | $ | $ | ( | ||||||||

| Interest rate swap contracts | |||||||||||

| Net unrealized gains (losses) on cash flow hedges, net of taxes, beginning of period | $ | $ | |||||||||

| Change in fair value, net of tax | |||||||||||

| Reclassification into earnings, net of tax | |||||||||||

| Net unrealized gains (losses) on cash flow hedges, net of taxes, end of period | $ | $ | |||||||||

| Net Investment Hedges | |||||||||||

| Net unrealized gains (losses) on net investment hedges, net of taxes, beginning of period | $ | ( | $ | ( | |||||||

| Change in fair value, net of tax | |||||||||||

| Reclassification into earnings, net of tax | |||||||||||

| Net unrealized gains (losses) on net investment hedges, net of taxes, end of period | $ | ( | $ | ||||||||

6. Employee Benefits

We maintain a number of active defined contribution retirement plans for our employees. The majority of our defined benefit plans are frozen. As a result, no new employees will be permitted to enter these plans and no additional benefits for current participants in the frozen plans will be accrued.

We also have supplemental benefit plans that provide senior management with supplemental retirement, disability and death benefits. Certain supplemental retirement benefits are based on final monthly earnings. In addition, we sponsor a voluntary 401(k) plan under which we may match employee contributions up to certain levels of compensation as well as profit-sharing plans under which we contribute a percentage of eligible employees' compensation to the employees' accounts.

We also provide certain medical, dental and life insurance benefits for active and retired employees and eligible dependents. The medical and dental plans and supplemental life insurance plan are contributory, while the basic life insurance plan is noncontributory. We currently do not prefund any of these plans.

We recognize the funded status of our retirement and postretirement plans in the consolidated balance sheets, with a corresponding adjustment to accumulated other comprehensive loss, net of taxes. The amounts in accumulated other comprehensive loss represent net unrecognized actuarial losses and unrecognized prior service costs. These amounts will be subsequently recognized as net periodic pension cost pursuant to our accounting policy for amortizing such amounts.

Net periodic benefit cost for our retirement and postretirement plans other than the service cost component are included in other (income) expense, net in our consolidated statements of income.

16

| (in millions) | 2021 | 2020 | |||||||||

| Service cost | $ | $ | |||||||||

| Interest cost | |||||||||||

| Expected return on assets | ( | ( | |||||||||

| Amortization of prior service credit / actuarial loss | |||||||||||

| Net periodic benefit cost | $ | ( | $ | ( | |||||||

Net periodic benefit cost related to our postretirement plans reflected in the table above was not material for the three months ended March 31, 2021 and 2020.

As discussed in our Form 10-K, we changed certain discount rate assumptions for our retirement and postretirement plans and our expected return on assets assumption for our retirement plans which became effective on January 1, 2021. The effect of the assumption changes on retirement and postretirement expense for the three months ended March 31, 2021 did not have a material impact to our financial position, results of operations or cash flows.

In the first three months of 2021, we contributed $3 million to our retirement plans and expect to make additional required contributions of approximately $8 million to our retirement plans during the remainder of the year. We may elect to make additional non-required contributions depending on investment performance or any potential deterioration of our pension plan status in the remaining nine months of 2021.

7. Stock-Based Compensation

We issue stock-based incentive awards to our eligible employees under the 2019 Stock Incentive Plan ("2019 Plan") and to our eligible non-employee Directors under a Director Deferred Stock Ownership Plan. The 2019 Plan permits the granting of incentive stock options, nonqualified stock options, stock appreciation rights, performance stock, restricted stock and other stock-based awards.

For the three months ended March 31, 2021 and 2020, total stock-based compensation expense primarily related to restricted stock and unit awards was $19 million and $11 million, respectively. Total unrecognized compensation expense related to unvested restricted stock and unit awards as of March 31, 2021 was $73 million, which is expected to be recognized over a weighted average period of 1.6 years.

8. Equity

Stock Repurchases

On January 29, 2020, the Board of Directors approved a share repurchase program authorizing the purchase of 30 million shares (the "2020 Repurchase Program"), which was approximately 12 % of the total shares of our outstanding common stock at that time. On December 4, 2013, the Board of Directors approved a share repurchase program authorizing the purchase of 50 million shares (the "2013 Repurchase Program"), which was approximately 18 % of the total shares of our outstanding common stock at that time.

Our purchased shares may be used for general corporate purposes, including the issuance of shares for stock compensation plans and to offset the dilutive effect of the exercise of employee stock options. As of March 31, 2021, 30 million shares remained available under the 2020 Repurchase Program and 0.8 million shares remained available under the 2013 repurchase program. Our 2020 Repurchase Program and 2013 Repurchase Program have no expiration date and purchases under these programs may be made from time to time on the open market and in private transactions, depending on market conditions.

We have entered into accelerated share repurchase (“ASR”) agreements with financial institutions to initiate share repurchases of our common stock. Under an ASR agreement, we pay a specified amount to the financial institution and receive an initial delivery of shares. This initial delivery of shares represents the minimum number of shares that we may receive under the agreement. Upon settlement of the ASR agreement, the financial institution delivers additional shares. The total number of shares ultimately delivered, and therefore the average price paid per share, is determined at the end of the applicable purchase period of each ASR agreement based on the volume weighted-average share price, less a discount. We account for our ASR agreements as two transactions: a stock purchase transaction and a forward stock purchase contract. The shares delivered under the ASR agreements resulted in a reduction of outstanding shares used to determine our weighted average common shares

17

outstanding for purposes of calculating basic and diluted earnings per share. The repurchased shares are held in Treasury. The forward stock purchase contracts were classified as equity instruments. The ASR agreements were executed under our 2013 Repurchase Program, approved on December 4, 2013.

The terms of each ASR agreement entered for the three months ended March 31, 2020, structured as outlined above, are as follows:

| (in millions, except average price) | ||||||||||||||||||||||||||||||||||||||

| ASR Agreement Initiation Date | ASR Agreement Completion Date | Initial Shares Delivered | Additional Shares Delivered | Total Number of Shares Purchased | Average Price Paid Per Share | Total Cash Utilized | ||||||||||||||||||||||||||||||||

February 11, 2020 1 | July 27, 2020 | $ | $ | |||||||||||||||||||||||||||||||||||

February 11, 2020 2 | July 27, 2020 | $ | $ | |||||||||||||||||||||||||||||||||||

1 The ASR agreement was structured as a capped ASR agreement in which we paid $500 million and received an initial delivery of 1.3 million shares and an additional amount of 0.2 million during the month of February, representing a minimum number of shares of our common stock to be repurchased based on a calculation using a specified capped price per share. We completed the ASR agreement on July 27, 2020 and received an additional 0.2 million shares.

2 The ASR agreement was structured as an uncapped ASR agreement in which we paid $500 million and received an initial delivery of 1.4 million shares, representing 85 % of the $500 million at a price equal to the then market price of the Company. We completed the ASR agreement on July 27, 2020 and received an additional 0.3 million shares.

Additionally, we purchased shares of our common stock in the open market for the three months ended March 31, 2020 as follows:

| (in millions, except average price) | ||||||||||||||||||||

| Total Number of Shares Purchased | Average Price Paid Per Share | Total Cash Utilized | ||||||||||||||||||

| March 31, 2020 | $ | $ | ||||||||||||||||||

During the three months ended March 31, 2021, we did not use cash to repurchase shares. During the three months ended March 31, 2020, we purchased a total of 3.4 million shares for $1,150 million of cash. During the fourth quarter of 2019, we repurchased shares for $3 million, which settled in the first quarter of 2020, resulting in $1,153 million of cash used to repurchase shares.

Redeemable Noncontrolling Interests

The agreement with the minority partners that own 27 % of our S&P Dow Jones Indices LLC joint venture contains redemption features whereby interests held by minority partners are redeemable either (i) at the option of the holder or (ii) upon the occurrence of an event that is not solely within our control. Specifically, under the terms of the operating agreement of S&P Dow Jones Indices LLC, CME Group and CME Group Index Services LLC ("CGIS") has the right at any time to sell, and we are obligated to buy, at least 20 % of their share in S&P Dow Jones Indices LLC. In addition, in the event there is a change of control of the Company, for the 15 days following a change in control, CME Group and CGIS will have the right to put their interest to us at the then fair value of CME Group's and CGIS' minority interest.

If interests were to be redeemed under this agreement, we would generally be required to purchase the interest at fair value on the date of redemption. This interest is presented on the consolidated balance sheets outside of equity under the caption “Redeemable noncontrolling interest” with an initial value based on fair value for the portion attributable to the net assets we acquired, and based on our historical cost for the portion attributable to our S&P Index business. We adjust the redeemable noncontrolling interest each reporting period to its estimated redemption value, but never less than its initial fair value, using both income and market valuation approaches. Our income and market valuation approaches incorporate Level 3 fair value measures for instances when observable inputs are not available. The more significant judgmental assumptions used to estimate the value of the S&P Dow Jones Indices LLC joint venture include an estimated discount rate, a range of assumptions that form the basis of the expected future net cash flows (e.g., the revenue growth rates and operating margins), and a company specific beta. The significant judgmental assumptions used that incorporate market data, including the relative weighting of market observable information and the comparability of that information in our valuation models, are forward-looking and could be affected by future economic and market conditions. Any adjustments to the redemption value will impact retained income.

18

Noncontrolling interests that do not contain such redemption features are presented in equity.

Changes to redeemable noncontrolling interest during the three months ended March 31, 2021 were as follows:

| (in millions) | |||||

| Balance as of December 31, 2020 | $ | ||||

| Net income attributable to redeemable noncontrolling interest | |||||

| Distributions payable to redeemable noncontrolling interest | ( | ||||

| Redemption value adjustment | |||||

Balance as of March 31, 2021 | $ | ||||

Accumulated Other Comprehensive Loss

The following table summarizes the changes in the components of accumulated other comprehensive loss for the three months ended March 31, 2021:

| (in millions) | Foreign Currency Translation Adjustments | Pension and Postretirement Benefit Plans | Unrealized Gain (Loss) on Cash Flow hedges | Accumulated Other Comprehensive Loss | |||||||||||||||||||

| Balance as of December 31, 2020 | $ | ( | $ | ( | $ | $ | ( | ||||||||||||||||

Other comprehensive (loss) income before reclassifications | ( | 1 | ( | ||||||||||||||||||||

Reclassifications from accumulated other comprehensive income (loss) to net earnings | 2 | ( | 3 | ( | |||||||||||||||||||

| Net other comprehensive (loss) income | ( | ( | |||||||||||||||||||||

Balance as of March 31, 2021 | $ | ( | $ | ( | $ | $ | ( | ||||||||||||||||

1Includes an unrealized gain related to our cross currency swaps. See note 5 – Derivative Instruments for additional detail of items recognized in accumulated other comprehensive loss.

2Reflects amortization of net actuarial losses and is net of a tax benefit of $1 million for the three months ended March 31, 2021. See Note 6 — Employee Benefits for additional details of items reclassed from accumulated other comprehensive loss to net earnings.

3See Note 5 — Derivative Instruments for additional details of items reclassified from accumulated other comprehensive loss to net earnings.

9. Earnings Per Share

19

The calculation of basic and diluted EPS for the three months ended March 31 is as follows:

| (in millions, except per share amounts) | 2021 | 2020 | |||||||||

Amounts attributable to S&P Global Inc. common shareholders: | |||||||||||

| Net income | $ | $ | |||||||||

Basic weighted-average number of common shares outstanding | |||||||||||

| Effect of stock options and other dilutive securities | |||||||||||

Diluted weighted-average number of common shares outstanding | |||||||||||

Earnings per share attributable to S&P Global Inc. common shareholders: | |||||||||||

| Net income: | |||||||||||

| Basic | $ | $ | |||||||||

| Diluted | $ | $ | |||||||||

We have certain stock options and restricted performance shares that are potentially excluded from the computation of diluted EPS. The effect of the potential exercise of stock options is excluded when the average market price of our common stock is lower than the exercise price of the related option during the period or when a net loss exists because the effect would have been antidilutive. Additionally, restricted performance shares are excluded because the necessary vesting conditions had not been met or when a net loss exists. For the three months ended March 31, 2021 and 2020, there were no 0.4

10. Restructuring

We continuously evaluate our cost structure to identify cost savings associated with streamlining our management structure. Our 2020 restructuring plan consisted of a company-wide workforce reduction of approximately 830 positions, and are further detailed below. The charges for the restructuring plans are classified as selling and general expenses within the consolidated statements of income and the reserves are included in other current liabilities in the consolidated balance sheets.

In certain circumstances, reserves are no longer needed because of efficiencies in carrying out the plans or because employees previously identified for separation resigned from the Company and did not receive severance or were reassigned due to circumstances not foreseen when the original plans were initiated. In these cases, we reverse reserves through the consolidated statements of income during the period when it is determined they are no longer needed.

The initial restructuring charge recorded and the ending reserve balance as of March 31, 2021 by segment is as follows:

| 2020 Restructuring Plan | |||||||||||

| (in millions) | Initial Charge Recorded | Ending Reserve Balance | |||||||||

| Ratings | $ | $ | |||||||||

| Market Intelligence | |||||||||||

| Platts | |||||||||||

| Indices | |||||||||||

| Corporate | |||||||||||

| Total | $ | $ | |||||||||

The ending reserve balance for the 2020 restructuring plan was $58 million as of December 31, 2020. For the three months ended March 31, 2021, we have reduced the reserve for the 2020 restructuring plan by $16 million. The reductions primarily related to cash payments for employee severance charges.

20

11. Segment and Related Information

We have four reportable segments: Ratings, Market Intelligence, Platts and Indices. Our Chief Executive Officer is our chief operating decision-maker and evaluates performance of our segments and allocates resources based primarily on operating profit. Segment operating profit does not include Corporate Unallocated, other (income) expense, net, or interest expense, net, as these are amounts that do not affect the operating results of our reportable segments.

A summary of operating results for the three months ended March 31 is as follows:

| Revenue | |||||||||||

| (in millions) | 2021 | 2020 | |||||||||

| Ratings | $ | $ | |||||||||

| Market Intelligence | |||||||||||

| Platts | |||||||||||

| Indices | |||||||||||

Intersegment elimination 1 | ( | ( | |||||||||

| Total revenue | $ | $ | |||||||||

| Operating Profit | |||||||||||

| (in millions) | 2021 | 2020 | |||||||||

Ratings 2 | $ | $ | |||||||||

Market Intelligence 3 | |||||||||||

Platts 4 | |||||||||||

Indices 5 | |||||||||||

| Total reportable segments | |||||||||||

Corporate Unallocated expense6 | ( | ( | |||||||||

| Total operating profit | $ | $ | |||||||||

1Revenue for Ratings and expenses for Market Intelligence include an intersegment royalty charged to Market Intelligence for the rights to use and distribute content and data developed by Ratings.

2 Operating profit for 2021 includes amortization of intangibles from acquisitions of $5 million.

3 Operating profit for 2021 includes a gain on disposition of $2 million, and operating profit for 2020 includes a gain on disposition of $7 million and employee severance charges of $2 million. Additionally, operating profit for 2021 and 2020 includes amortization of intangibles from acquisitions of $16 million and $19 million, respectively.

4 Operating profit for both 2021 and 2020 includes amortization of intangibles from acquisitions of $2

5 Operating profit for both 2021 and 2020 includes amortization of intangibles from acquisitions of $1

6 Corporate Unallocated expense for 2021 includes IHS Markit merger costs of $49 million and Kensho retention related expense of $2 million. Corporate Unallocated expense for 2020 includes employee severance charges of $7 million and Kensho retention related expense of $5 million. Additionally, Corporate Unallocated expense for both 2021 and 2020 includes amortization of intangibles from acquisitions of $7

21

The following table presents our revenue disaggregated by revenue type for the three months ended March 31:

| (in millions) | Ratings | Market Intelligence | Platts | Indices | Intersegment Elimination 1 | Total | |||||||||||||||||||||||||||||

| 2021 | |||||||||||||||||||||||||||||||||||

| Subscription | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Non-subscription / Transaction | |||||||||||||||||||||||||||||||||||

| Non-transaction | ( | ||||||||||||||||||||||||||||||||||

| Asset-linked fees | |||||||||||||||||||||||||||||||||||

| Sales usage-based royalties | |||||||||||||||||||||||||||||||||||

| Total revenue | $ | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||

| Timing of revenue recognition | |||||||||||||||||||||||||||||||||||

Services transferred at a point in time | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

Services transferred over time | ( | ||||||||||||||||||||||||||||||||||

| Total revenue | $ | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||

| (in millions) | Ratings | Market Intelligence | Platts | Indices | Intersegment Elimination 1 | Total | |||||||||||||||||||||||||||||

20202 | |||||||||||||||||||||||||||||||||||

| Subscription | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Non-subscription / Transaction | |||||||||||||||||||||||||||||||||||

| Non-transaction | ( | ||||||||||||||||||||||||||||||||||

| Asset-linked fees | |||||||||||||||||||||||||||||||||||

| Sales usage-based royalties | |||||||||||||||||||||||||||||||||||

| Total revenue | $ | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||

| Timing of revenue recognition | |||||||||||||||||||||||||||||||||||

| Services transferred at a point in time | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Services transferred over time | ( | ||||||||||||||||||||||||||||||||||

| Total revenue | $ | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||

1 Intersegment eliminations primarily consists of a royalty charged to Market Intelligence for the rights to use and distribute content and data developed by Ratings.

2 In the first quarter of 2021, we reevaluated our transaction and non-transaction presentation for Ratings which resulted in a reclassification from transaction revenue to non-transaction revenue of $2 million for the first quarter of 2020.

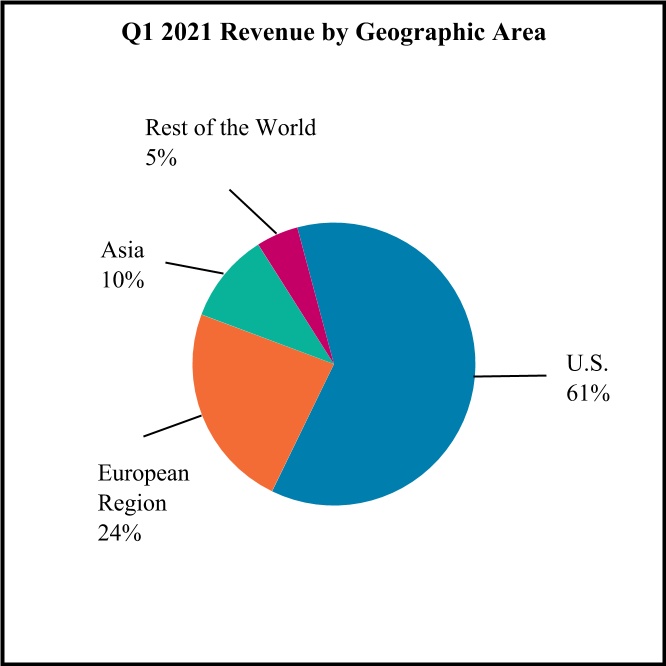

The following provides revenue by geographic region for the three months ended March 31:

| (in millions) | |||||||||||

| 2021 | 2020 | ||||||||||

| U.S. | $ | $ | |||||||||

| European region | |||||||||||

| Asia | |||||||||||

| Rest of the world | |||||||||||

| Total | $ | $ | |||||||||

See Note 2 — Acquisitions and Divestitures and Note 10 — Restructuring for additional actions that impacted the segment operating results.

22

12. Commitments and Contingencies

Leases

We determine whether an arrangement meets the criteria for an operating lease or a finance lease at the inception of the arrangement. We have operating leases for office space and equipment. Our leases have remaining lease terms of 1 year to 12 years, some of which include options to extend the leases for up to 12 years, and some of which include options to terminate the leases within 1 year. We consider these options in determining the lease term used to establish our right of use ("ROU") assets and associated lease liabilities. We sublease certain real estate leases to third parties which mainly consist of operating leases for space within our offices.

Leases with an initial term of 12 months or less are not recorded on the balance sheet; we recognize lease expenses for these leases on a straight line-basis over the lease term in operating-related expenses and selling and general expenses.

Operating lease ROU assets and operating lease liabilities are recognized based on the present value of future minimum lease payments over the lease term at commencement date. Our future minimum based payments used to determine our lease liabilities include minimum based rent payments and escalations. As most of our leases do not provide an implicit rate, we use our estimated incremental borrowing rate based on the information available at commencement date in determining the present value of lease payments.

The following table provides information on the location and amounts of our leases on our consolidated balance sheets as of March 31, 2021 and December 31, 2020:

| (in millions) | March 31, | December 31, | ||||||||||||

| Balance Sheet Location | 2021 | 2020 | ||||||||||||

| Assets | ||||||||||||||

| Right of use assets | Lease right of use assets | $ | $ | |||||||||||

| Liabilities | ||||||||||||||

| Current lease liabilities | ||||||||||||||

| Lease liabilities — non-current | Non-current lease liabilities | |||||||||||||

The components of lease expense for the three months ended March 31 are as follows:

| (in millions) | 2021 | 2020 | |||||||||

| Operating lease cost | $ | $ | |||||||||

| Sublease income | ( | ( | |||||||||

| Total lease cost | $ | $ | |||||||||

Supplemental information related to leases for the three months ended March 31 are as follows:

| (in millions) | 2021 | 2020 | ||||||||||||

| Cash paid for amounts included in the measurement for operating lease liabilities | ||||||||||||||

| Operating cash flows for operating leases | $ | $ | ||||||||||||

| Right of use assets obtained in exchange for lease obligations | ||||||||||||||

| Operating leases | ||||||||||||||

23

Weighted-average remaining lease term and discount rate for our operating leases are as follows:

| March 31, | December 31, | ||||||||||

| 2021 | 2020 | ||||||||||

| Weighted-average remaining lease term (years) | |||||||||||

| Weighted-average discount rate | % | % | |||||||||

Maturities of lease liabilities for our operating leases are as follows:

| (in millions) | |||||

2021 (Excluding the three months ended March 31, 2021) | $ | ||||

| 2022 | |||||

| 2023 | |||||

| 2024 | |||||

| 2025 | |||||

| 2026 and beyond | |||||

| Total undiscounted lease payments | $ | ||||

| Less: Imputed interest | |||||

| Present value of lease liabilities | $ | ||||

Related Party Agreements

In June of 2012, we entered into a license agreement (the "License Agreement") with the holder of S&P Dow Jones Indices LLC noncontrolling interest, CME Group, replacing the 2005 license agreement between Indices and CME Group. Under the terms of the License Agreement, S&P Dow Jones Indices LLC receives a share of the profits from the trading and clearing of CME Group's equity index products. During the three months ended March 31, 2021 and 2020, S&P Dow Jones Indices LLC earned $37 million and $47 million, respectively, of revenue under the terms of the License Agreement. The entire amount of this revenue is included in our consolidated statement of income and the portion related to the 27 % noncontrolling interest is removed in net income attributable to noncontrolling interests.

Legal and Regulatory Matters

In the normal course of business both in the United States and abroad, the Company and its subsidiaries are defendants in a number of legal proceedings and are often the subject of government and regulatory proceedings, investigations and inquiries.

In the second quarter of 2020, Indices, a joint venture with CME Group controlled by the Company, received a “Wells Notice” from the Staff of the SEC stating that the Staff has made a preliminary determination to recommend that the SEC file an enforcement action against Indices. The proposed action would allege violations of federal securities laws with respect to the absence of disclosure of a quality assurance mechanism and the impact of that mechanism on certain volatility related index values published on one business day in 2018. The Staff’s recommendation may involve a civil injunctive action, a cease and desist proceeding, disgorgement, pre-judgment interest and civil money penalties. The Wells Notice is neither a formal allegation nor a finding of wrongdoing. It allows Indices the opportunity to provide its perspective and to address the issues raised by the Staff before any decision is made by the SEC on whether to authorize the commencement of an enforcement proceeding. Indices has been cooperating with the SEC in this matter and intends to continue to do so.

A class action lawsuit was filed in Australia on August 7, 2020 against the Company and a subsidiary of the Company. A separate lawsuit was filed against the Company and a subsidiary of the Company in Australia on February 2, 2021 by two entities within the Basis Capital investment group. The lawsuits both relate to alleged investment losses in collateralized debt obligations rated by Ratings prior to the financial crisis.

We can provide no assurance that we will not be obligated to pay significant amounts in order to resolve these matters on terms deemed acceptable.

From time to time, the Company receives customer complaints, particularly, though not exclusively, in its Ratings and Indices segments. The Company believes it has strong contractual protections in the terms and conditions included in its arrangements

24

with customers. Nonetheless, in the interest of managing customer relationships, the Company from time to time engages in dialogue with such customers in an effort to resolve such complaints, and if such complaints cannot be resolved through dialogue, may face litigation regarding such complaints. The Company does not expect to incur material losses as a result of these matters.

Moreover, various government and self-regulatory agencies frequently make inquiries and conduct investigations into our compliance with applicable laws and regulations, including those related to ratings activities and antitrust matters. For example, as a nationally recognized statistical rating organization registered with the SEC under Section 15E of the Exchange Act, S&P Global Ratings is in ongoing communication with the staff of the SEC regarding compliance with its extensive obligations under the federal securities laws. Although S&P Global seeks to promptly address any compliance issues that it detects or that the staff of the SEC or another regulator raises, there can be no assurance that the SEC or another regulator will not seek remedies against S&P Global for one or more compliance deficiencies. Any of these proceedings, investigations or inquiries could ultimately result in adverse judgments, damages, fines, penalties or activity restrictions, which could adversely impact our consolidated financial condition, cash flows, business or competitive position.

In view of the uncertainty inherent in litigation and government and regulatory enforcement matters, we cannot predict the eventual outcome of such matters or the timing of their resolution, or in most cases reasonably estimate what the eventual judgments, damages, fines, penalties or impact of activity (if any) restrictions may be. As a result, we cannot provide assurance that such outcomes will not have a material adverse effect on our consolidated financial condition, cash flows, business or competitive position. As litigation or the process to resolve pending matters progresses, as the case may be, we will continue to review the latest information available and assess our ability to predict the outcome of such matters and the effects, if any, on our consolidated financial condition, cash flows, business or competitive position, which may require that we record liabilities in the consolidated financial statements in future periods.

13. Recently Issued or Adopted Accounting Standards

In August of 2020, the Financial Accounting Standards Board ("FASB") issued guidance that amends the accounting for convertible instruments and the derivatives scope exception for contracts in an entity's own equity. The guidance was effective on January 1, 2021, and the adoption of this guidance did not have a significant impact on our consolidated financial statements.

In January of 2020, the FASB intended to clarify the interaction of the accounting for equity securities under Accounting Standards Codification ("ASC") 321, investments accounted for under the equity method of accounting under ASC 323, and the accounting for certain forward contracts and purchased options accounted for under ASC 815. The guidance clarifies how to account for the transition into and out of the equity method of accounting when considering observable transactions under the measurement alternative. The guidance was effective on January 1, 2021, and the adoption of this guidance did not have a significant impact on our consolidated financial statements.

In December of 2019, the FASB issued guidance to simplify the accounting for income taxes, which eliminates certain exceptions to the general principles of Topic 740. The guidance is effective for reporting periods after December 15, 2020. Our adoption of this guidance on January 1, 2021 did not have a significant impact on our consolidated financial statements.

25

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations (Unaudited)

The following Management's Discussion and Analysis (“MD&A”) provides a narrative of the results of operations and financial condition of S&P Global Inc. (together with its consolidated subsidiaries, "S&P Global," the “Company,” “we,” “us” or “our”) for the three months ended March 31, 2021. The MD&A should be read in conjunction with the consolidated financial statements, accompanying notes and MD&A included in our Form 10-K for the year ended December 31, 2020 (our “Form 10-K”), which have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). The MD&A includes the following sections:

•Overview

•Results of Operations — Comparing the Three Months Ended March 31, 2021 and 2020

•Liquidity and Capital Resources

•Reconciliation of Non-GAAP Financial Information

•Critical Accounting Estimates

•Recently Issued or Adopted Accounting Standards

•Forward-Looking Statements

OVERVIEW

We are a leading provider of transparent and independent ratings, benchmarks, analytics and data to the capital and commodity markets worldwide. The capital markets include asset managers, investment banks, commercial banks, insurance companies, exchanges, trading firms and issuers; and the commodity markets include producers, traders and intermediaries within energy, petrochemicals, metals and agriculture.

Our operations consist of four reportable segments: S&P Global Ratings ("Ratings"), S&P Global Market Intelligence ("Market Intelligence"), S&P Global Platts ("Platts") and S&P Dow Jones Indices ("Indices").

•Ratings is an independent provider of credit ratings, research, and analytics, offering investors and other market participants information, ratings and benchmarks.

•Market Intelligence is a global provider of multi-asset-class data, research and analytical capabilities, which integrate cross-asset analytics and desktop services.

•Platts is the leading independent provider of information and benchmark prices for the commodity and energy markets.

•Indices is a global index provider maintaining a wide variety of valuation and index benchmarks for investment advisors, wealth managers and institutional investors.

Key results for the three months ended March 31 are as follows:

| (in millions, except per share amounts) | 2021 | 2020 | % Change 1 | ||||||||||||||

| Revenue | $ | 2,016 | $ | 1,786 | 13% | ||||||||||||

Operating profit 2 | $ | 1,081 | $ | 912 | 19% | ||||||||||||

| Operating margin % | 54 | % | 51 | % | |||||||||||||

| Diluted earnings per share from net income | $ | 3.12 | $ | 2.62 | 19% | ||||||||||||

1 % changes in the tables throughout the MD&A are calculated off of the actual number, not the rounded number presented.

2 2021 includes IHS Markit merger costs of $49 million, Kensho retention related expense of $2 million and a gain on disposition of $2 million. 2020 includes employee severance charges of $9 million, a gain on disposition of $7 million and Kensho retention related expense of $5 million. 2021 and 2020 also includes amortization of intangibles from acquisitions of $31 million and $29 million, respectively.

Revenue increased 13% driven by increases at all of our reportable segments. Revenue growth at Ratings was mainly driven by an increase in transaction revenue due to higher corporate bond ratings revenue, an increase in bank loan ratings revenue and higher structured finance revenues. Revenue growth at Market Intelligence was driven by subscription revenue growth in Credit Risk Solutions, Data Management Solutions and Market Intelligence Desktop products. Revenue growth at Indices was due to higher average levels of assets under management ("AUM") for ETFs and mutual funds, partially offset by lower exchange-

26

traded derivative revenue. The revenue increase at Platts was primarily due to continued demand for market data and market insights products. Foreign exchange rates had a favorable impact of 1 percentage point.

Operating profit increased 19%, with a favorable impact from foreign exchange rates of 2 percentage points. Excluding the unfavorable impact of IHS Markit merger costs in 2021 of 4 percentage points and a higher gain on dispositions in 2020 of 1 percentage point, partially offset by higher employee severance charges in 2020 of 1 percentage point, operating profit increased 23%. The increase was primarily due to revenue growth at all of our reportable segments combined with a decrease in travel and entertainment expenses from non-essential travel restrictions in response to the 2019 novel coronavirus ("COVID-19"), partially offset by higher compensation costs driven by annual merit increases and additional headcount.

We are closely monitoring the impact of the outbreak of COVID-19 on all aspects of our business. While COVID-19 did not have a material adverse effect on our reported results for the three months ended March 31, 2021, we are unable to predict the ultimate impact that it may have on our business, future results of operations, financial position or cash flows.

Our Strategy

We are a leading provider of transparent and independent ratings, benchmarks, analytics and data to the capital and commodity markets worldwide. Our purpose is to provide the intelligence that is essential for companies, governments and individuals to make decisions with conviction. We seek to deliver on this purpose in line with our core values of integrity, excellence and relevance.

In 2018, we announced the launch of Powering the Markets of the Future to provide a framework for our forward-looking business strategy. Through this framework, we seek to deliver an exceptional, differentiated customer experience by enhancing our foundational capabilities, evolving and growing our core businesses, and pursuing growth via adjacencies. In 2021, we will strive to deliver on our strategic priorities in the following key areas:

Finance

•Meeting or exceeding revenue growth and EBITA margin targets with particular focus on accelerating growth in the greater Asia Pacific region;

•Funding organic opportunities and pursuing disciplined acquisitions, investments and partnerships to support our key growth areas;

•Taking a lead role in the market regarding ESG disclosures and achieving our stated environmental sustainability targets; and

•Executing against Integration Management Office ("IMO") and regulatory milestones; building trust and team cohesion with IHS Markit (NYSE:INFO) colleagues; laying groundwork to set proforma organization up for successful realization of our synergy and strategic goals.

Customer

•Continuing to deliver our key initiatives to the market and building them through a customer-first lens;

•Prioritizing customer preferences, while enhancing and adjusting the delivery of our products across multiple channels such as feeds and APIs; and delivering on S&P Global Platform initiatives;

•Incorporating a customer perspective in all divisions and functions, including the reimagining of our customer's work environments and how best to serve them; pursuing partnerships to meet customers where they are; and

•Nurturing and protecting the core franchise, while growing brand equity with the appropriate investments.

Operations

•Improving end-user productivity and experience by providing our employees with the tools and processes to better serve our customers;

27

•Reimagining our work environment by continuing to standardize our technology and encouraging employee participation in the reshaping of where we work, how we work and how we serve;

•Advancing our risk culture by maturing risk management & compliance processes and our cyber security posture; and

•Utilizing our innovation teams and latest technology to maintain our commitment to advancing our shared data processes and technical capabilities.

People

•Continuing to foster a people first environment, while maintaining existing levels of engagement;

•Encouraging career mobility through career coaching, while attracting and retaining the best people; and

•Improving diverse representation through talent acquisition, advancement and retention, while continuing to raise awareness of racial education.

There can be no assurance that we will achieve success in implementing any one or more of these strategies as a variety of factors could unfavorably impact operating results, including prolonged difficulties in the global credit markets and a change in the regulatory environment affecting our businesses. See Item 1A, Risk Factors in this Form 10-Q and our most recently filed Annual Report on Form 10-K.

28

RESULTS OF OPERATIONS — COMPARING THE THREE MONTHS ENDED MARCH 31, 2021 AND 2020

Consolidated Review

| (in millions) | 2021 | 2020 | % Change | ||||||||||||||