Exhibit 10.2

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

| | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended

OR

| | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number

MAUI LAND & PINEAPPLE COMPANY, INC.

(Exact name of registrant as specified in its charter)

| | | |

| (State or other jurisdiction | (IRS Employer | |

| of incorporation or organization) | Identification No.) |

(Address of principal executive offices)

(

(Registrant’s telephone number, including area code)

None

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| | | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| | Smaller reporting company Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

| Class | Outstanding at May 3, 2022 | |

| Common Stock, no par value | |

MAUI LAND & PINEAPPLE COMPANY, INC.

AND SUBSIDIARIES

| Cautionary Note Regarding Forward-Looking Statements | 2 |

| 3 |

|

| Item 1. Condensed Consolidated Financial Statements (Unaudited) |

3 |

| Condensed Consolidated Balance Sheets, March 31, 2022 and December 31, 2021 (Audited) |

3 |

| 4 | |

| 5 | |

| Condensed Consolidated Statements of Cash Flows, Three Months Ended March 31, 2022 and 2021 |

6 |

| Notes to Condensed Consolidated Interim Financial Statements |

7 |

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations |

14 |

| Item 3. Quantitative and Qualitative Disclosures About Market Risk |

17 |

| 17 | |

| 18 | |

| 18 | |

| 18 | |

| 19 | |

| 20 | |

| 21 | |

| Exhibit 3.2 | |

| Exhibit 10.1 | |

| Exhibit 10.2 | |

| Exhibit 10.3 | |

| Exhibit 31.1 |

|

| Exhibit 31.2 |

|

| Exhibit 32.1 |

|

| Exhibit 32.2 |

|

| Exhibit 101 | |

| Exhibit 104 |

Cautionary Note Regarding Forward-Looking Statements

This Quarterly Report on Form 10-Q and other reports filed by us with the U.S. Securities and Exchange Commission contain “forward-looking statements” intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. These statements relate to future events or our future financial performance and are subject to known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to differ materially from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. These statements include all statements included in or incorporated by reference to this Quarterly report on Form 10-Q that are not statements of historical facts, which can generally be identified by words such as “anticipate,” “believe,” “continue” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “project,” “pursue,” “will,” “would,” or the negative or other variations thereof or comparable terminology. We caution you that the foregoing list may not include all of the forward-looking statements made in this Quarterly Report. Actual results could differ materially from those projected in forward-looking statements as a result of the following factors, among others:

| • |

the impacts of the COVID-19 pandemic, including its impacts on us, our operations, or our future financial or operational results; |

| • |

unstable macroeconomic market conditions, including, but not limited to, energy costs, credit markets, interest rates and changes in income and asset values; |

| • |

risks associated with real estate investments generally, and more specifically, demand for real estate and tourism in Hawaii; |

| • |

risks due to joint venture relationships; |

| • |

our ability to complete land development projects within forecasted time and budget expectations, if at all; |

| • |

our ability to obtain required land use entitlements at reasonable costs, if at all; |

| • |

our ability to compete with other developers of real estate in Maui; |

| • |

potential liabilities and obligations under various federal, state and local environmental regulations with respect to the presence of hazardous or toxic substances; |

| • |

changes in weather conditions, the occurrence of natural disasters, or threats of the spread of contagious diseases; |

| • |

our ability to maintain the listing of our common stock on the New York Stock Exchange; |

| • |

our ability to comply with funding requirements of our defined benefit pension plan; |

| • |

our ability to comply with the terms of our indebtedness, including the financial covenants set forth therein, and to extend maturity dates, or refinance such indebtedness, prior to its maturity date; |

| • |

our ability to raise capital through the sale of certain real estate assets; |

| • |

risks related to reference rate reform; |

| • |

availability of capital on terms favorable to us, or at all; and |

| • |

failure to maintain security of internal and customer electronic information. |

Such risks and uncertainties also include those risks and uncertainties discussed in the sections entitled “Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our Annual Report on Form 10-K for the year ended December 31, 2021 (the “2021 Annual Report”) and the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” as well as other factors described from time to time in our reports filed with the SEC. Although we believe our opinions and expectations reflected in the forward-looking statements are reasonable as of the date of this report, we cannot guarantee future results, levels of activity, performance or achievements, and our actual results may differ substantially from the views and expectations set forth in this report. Thus, you should not place undue reliance on any forward-looking statements. New factors emerge from time to time, and it is not possible for us to predict which factors will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Further, any forward-looking statements speak only as of the date made and, except as required by law, we undertake no obligation to publicly revise our forward-looking statements to reflect events or circumstances that arise after the date of this report. We qualify all of our forward-looking statements by these cautionary statements.

Item 1. Condensed Consolidated Financial Statements (Unaudited)

MAUI LAND & PINEAPPLE COMPANY, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

| March 31, 2022 (unaudited) | December 31 2021 (audited) | |||||||

| (in thousands except share data) | ||||||||

| ASSETS | ||||||||

| CURRENT ASSETS | ||||||||

| Cash | $ | $ | ||||||

| Restricted cash | ||||||||

| Accounts receivable, net | ||||||||

| Prepaid expenses and other assets | ||||||||

| Assets held for sale | ||||||||

| Total current assets | ||||||||

| PROPERTY & EQUIPMENT | ||||||||

| Accumulated depreciation | ( | ) | ( | ) | ||||

| Property & equipment, net | ||||||||

| OTHER ASSETS | ||||||||

| Deferred development costs | ||||||||

| Other noncurrent assets | ||||||||

| Total other assets | ||||||||

| TOTAL ASSETS | $ | $ | ||||||

| LIABILITIES & STOCKHOLDERS' EQUITY CURRENT LIABILITIES | ||||||||

| Accounts payable | $ | $ | ||||||

| Payroll and employee benefits | ||||||||

| Accrued retirement benefits, current portion | ||||||||

| Deferred revenue, current portion | ||||||||

| Other current liabilities | ||||||||

| Total current liabilities | ||||||||

| LONG-TERM LIABILITIES | ||||||||

| Accrued retirement benefits, net of current portion | ||||||||

| Deferred revenue, net of current portion | ||||||||

| Deposits | ||||||||

| Other noncurrent liabilities | ||||||||

| Total long-term liabilities | ||||||||

| TOTAL LIABILITIES | ||||||||

| COMMITMENTS AND CONTINGENCIES | ||||||||

| STOCKHOLDERS' EQUITY | ||||||||

| Common stock-- par value, shares authorized, and shares issued and outstanding at March 31, 2022 and December 31, 2021, respectively | ||||||||

| Additional paid-in-capital | ||||||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| Accumulated other comprehensive loss | ( | ) | ( | ) | ||||

| Total stockholders' equity | ||||||||

| TOTAL LIABILITIES & STOCKHOLDERS' EQUITY | $ | $ | ||||||

See Notes to Condensed Consolidated Interim Financial Statements.

MAUI LAND & PINEAPPLE COMPANY, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(UNAUDITED)

| Three Months Ended March 31, | ||||||||

| 2022 | 2021 | |||||||

| (in thousands except per share amounts) | ||||||||

| OPERATING REVENUES | ||||||||

| Real estate | $ | $ | ||||||

| Leasing | ||||||||

| Resort amenities and other | ||||||||

| Total operating revenues | ||||||||

| OPERATING COSTS AND EXPENSES | ||||||||

| Real estate | ||||||||

| Leasing | ||||||||

| Resort amenities and other | ||||||||

| General and administrative | ||||||||

| Share-based compensation | ||||||||

| Depreciation | ||||||||

| Total operating costs and expenses | ||||||||

| OPERATING LOSS | ( | ) | ( | ) | ||||

| Other income | ||||||||

| Pension and other post-retirement expenses | ( | ) | ( | ) | ||||

| Interest expense | ( | ) | ( | ) | ||||

| LOSS FROM CONTINUING OPERATIONS | $ | ( | ) | $ | ( | ) | ||

| Loss from discontinued operations, net | ( | ) | ||||||

| NET LOSS | $ | ( | ) | $ | ( | ) | ||

| Pension, net | ||||||||

| TOTAL COMPREHENSIVE LOSS | $ | ( | ) | $ | ( | ) | ||

| LOSS PER COMMON SHARE-BASIC AND DILUTED | ||||||||

| Loss from Continuing Operations | $ | ( | ) | $ | ( | ) | ||

| Loss from Discontinued Operations | $ | $ | ( | ) | ||||

| Net Loss | $ | ( | ) | $ | ( | ) | ||

See Notes to Condensed Consolidated Interim Financial Statements.

MAUI LAND & PINEAPPLE COMPANY, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

(UNAUDITED)

For the Three Months Ended March 31, 2022 and 2021

(in thousands)

| Common Stock | Additional Paid in | Accumulated |

Accumulated Other Comprehensive | |||||||||||||||||||||

| Shares | Amount | Capital | Deficit | Loss | Total | |||||||||||||||||||

| Balance, January 1, 2022 | $ | $ | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||

| Share-based compensation | ||||||||||||||||||||||||

| Vested restricted stock issued | ( | ) | - | |||||||||||||||||||||

| Shares canceled to pay tax liability | ( | ) | ( | ) | ( | ) | ||||||||||||||||||

| Other comprehensive income - pension | ||||||||||||||||||||||||

| Net loss | ( | ) | ( | ) | ||||||||||||||||||||

| Balance, March 31, 2022 | $ | $ | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||

| Balance, January 1, 2021 | $ | $ | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||

| Share-based compensation | ||||||||||||||||||||||||

| Vested restricted stock issued | ( | ) | - | |||||||||||||||||||||

| Shares canceled to pay tax liability | ( | ) | ( | ) | ( | ) | ||||||||||||||||||

| Other comprehensive income - pension | ||||||||||||||||||||||||

| Net loss | ( | ) | ( | ) | ||||||||||||||||||||

| Balance, March 31, 2021 | $ | $ | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||

See Notes to Condensed Consolidated Interim Financial Statements.

MAUI LAND & PINEAPPLE COMPANY, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| Three Months Ended March 31, | ||||||||

| 2022 | 2021 | |||||||

| (in thousands) | ||||||||

| NET CASH PROVIDED BY (USED IN) OPERATING ACTIVITIES | $ | $ | ( | ) | ||||

| CASH USED IN INVESTING ACTIVITIES | ||||||||

| Payments for property and deferred development costs | ( | ) | ( | ) | ||||

| CASH FLOWS FROM FINANCING ACTIVITIES | ||||||||

| Proceeds from long-term debt | ||||||||

| Debt and common stock issuance costs and other | ( | ) | ( | ) | ||||

| NET CASH (USED IN) PROVIDED BY FINANCING ACTIVITIES | ( | ) | ||||||

| NET INCREASE (DECREASE) IN CASH | ( | ) | ||||||

| CASH AND RESTRICTED CASH AT BEGINNING OF PERIOD | ||||||||

| CASH AND RESTRICTED CASH AT END OF PERIOD | $ | $ | ||||||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION: | ||||||||

| Cash paid during the period for interest | $ | $ | ||||||

SUPPLEMENTAL SCHEDULE OF NON-CASH FINANCING ACTIVITIES:

| ● | The aggregate value of common stock of the Company issued to certain members of the Company’s management totaled $ |

See Notes to Condensed Consolidated Interim Financial Statements.

MAUI LAND & PINEAPPLE COMPANY, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS

(UNAUDITED)

| 1. | BASIS OF PRESENTATION |

The accompanying unaudited condensed consolidated interim financial statements have been prepared by Maui Land & Pineapple Company, Inc. (together with its subsidiaries, collectively, the “Company”) in conformity with generally accepted accounting principles in the United States (“GAAP”) for interim financial information that are consistent in all material respects with those applied in the Company’s Annual Report on Form 10-K for the year ended December 31, 2021, and pursuant to the instructions to Form 10-Q and Article 8 promulgated by Regulation S-X of the U.S. Securities and Exchange Commission (“SEC”). Accordingly, they do not include all of the information and notes to the annual audited consolidated financial statements required by GAAP for complete financial statements. In the opinion of management, the accompanying unaudited condensed consolidated interim financial statements contain all normal and recurring adjustments necessary to fairly present the Company’s financial position, results of operations and cash flows for the interim periods ended March 31, 2022 and 2021. The unaudited condensed consolidated interim financial statements and notes should be read in conjunction with the annual audited consolidated financial statements and notes thereto included in the Company’s Form 10-K for the year ended December 31, 2021.

| 2. | USE OF ESTIMATES AND RECLASSIFICATIONS |

The Company’s reports for interim periods utilize numerous estimates of general and administrative expenses and other costs for the full year. Future actual amounts may differ from these estimates. Amounts reflected in these condensed consolidated interim statements are not necessarily indicative of results for a full year.

| 3. | RESTRICTED CASH |

Restricted cash of $

| 4. | SHARES – BASIC AND DILUTED |

Basic and diluted weighted-average shares outstanding for the three months ended March 31, 2022 and 2021 were

Basic net loss per common share is computed by dividing net loss by the weighted-average number of common shares outstanding. Diluted net loss per common share is computed similar to basic net loss per common share except that the denominator is increased to include the number of additional common shares that would have been outstanding if the dilutive potential common shares from share-based compensation arrangements had been issued.

| 5. | PROPERTY |

Property at March 31, 2022 and December 31, 2021 consisted of the following:

| March 31, 2022 (unaudited) | December 31, 2021 (audited) | |||||||

| (in thousands) | ||||||||

| Land | $ | $ | ||||||

| Land improvements | ||||||||

| Buildings | ||||||||

| Machinery and equipment | ||||||||

| Total property | ||||||||

| Less accumulated depreciation | ||||||||

| Property & equipment, net | $ | $ | ||||||

Land

Most of the Company’s

Land Improvements

Land improvements are comprised primarily of roads, utilities, and landscaping infrastructure improvements at the Kapalua Resort. Also included is the Company’s potable and non-potable water systems in West Maui. The majority of the Company’s land improvements were constructed and placed in service in the mid-to-late 1970’s or conveyed in 2017. Depreciation expense would be considerably higher if these assets were stated at current replacement cost.

Buildings

Buildings are comprised of restaurant, retail and light industrial spaces located at the Kapalua Resort and Hali’imaile which are used in the Company’s leasing operations. The majority of the buildings were constructed and placed in service in the mid-to-late 1970’s. Depreciation expense would be considerably higher if these assets were stated at current replacement cost.

Machinery and Equipment

Machinery and equipment are mainly comprised of zipline course equipment installed in 2008 at the Kapalua Resort and used in the Company’s leasing operations.

6. ASSETS HELD FOR SALE

Assets held for sale at March 31, 2022 and December 31, 2021 consisted of the following:

| March 31, 2022 (unaudited) | December 31, 2021 (audited) | |||||||

| (in thousands) | ||||||||

| Kapalua Resort, -acre Kapalua Central Resort project | $ | $ | ||||||

| Upcountry Maui, -acre parcel of agricultural land | ||||||||

| $ | $ | |||||||

In December 2021, the Company entered into an agreement to sell the Kapalua Central Resort project for $

In February 2022, the Company entered into an agreement to sell the

The above assets held for sale have not been pledged as collateral under the Credit Facility (as defined in Note 7).

7. LONG-TERM DEBT

Long-term debt is comprised of amounts outstanding under the Company’s $

The terms of the Credit Facility include various representations, warranties, affirmative, negative and financial covenants and events of default customary for financings of this type. Financial covenants include a minimum liquidity (as defined) of $

The outstanding balance of the Credit Facility was as of March 31, 2022. The Company believes it was in compliance with the covenants under the Credit Facility as of March 31, 2022.

8. SHARE-BASED COMPENSATION

The Company’s directors, officers and certain members of management receive a portion of their compensation in restricted shares of the Company’s common stock granted under the Company’s 2017 Equity and Incentive Award Plan (“Equity Plan”). Share-based compensation is valued based on the average of the high and low share price on the date of grant. Shares are issued upon execution of agreements reflecting the grantee’s acceptance of the respective shares subject to the terms and conditions of the Equity Plan. Restricted shares issued under the Equity Plan vest quarterly and have voting and regular dividend rights but cannot be disposed of until such time as they are vested. All unvested restricted shares are forfeited upon the grantee’s termination of directorship or employment from the Company.

Share-based compensation is determined and awarded annually to the Company’s officers and certain members of management based on their achievement of certain predefined performance goals and objectives under the Equity Plan. Such share-based compensation is comprised of an annual incentive paid in shares of common stock and a long-term incentive paid in restricted shares vesting quarterly over a period of years.

Share-based compensation totaled [approximately] $

9. ACCRUED RETIREMENT BENEFITS

Accrued retirement benefits at March 31, 2022 and December 31, 2021 consisted of the following:

| March 31, 2022 (unaudited) | December 31, 2021 (audited) | |||||||

| (in thousands) | ||||||||

| Defined benefit pension plan | $ | $ | ||||||

| Non-qualified retirement plans | ||||||||

| Total | ||||||||

| Less current portion | ||||||||

| Non-current portion of accrued retirement benefits | $ | $ | ||||||

The Company has a defined benefit pension plan which covers substantially all of its former bargaining and non-bargaining full-time, part-time and intermittent employees. In 2011, pension benefits under the plan were frozen. The Company also has an unfunded non-qualified retirement plan covering nine of its former executives. The non-qualified retirement plan was frozen in 2009 and future vesting of additional benefits was discontinued.

The net periodic benefit costs for pension and postretirement benefits for the three months ended March 31, 2022 and 2021 were as follows:

|

Three Months Ended March 31, (unaudited) | ||||||||

| 2022 | 2021 | |||||||

| (in thousands) | ||||||||

| Interest cost | $ | $ | ||||||

| Expected return on plan assets | ( | ) | ( | ) | ||||

| Amortization of net actuarial loss | ||||||||

| Pension and other postretirement expenses | $ | $ | ||||||

10. CONTRACT ASSETS AND LIABILITIES

Receivables from contracts with customers were $

Deferred club membership revenue

The Company manages the operations of the Kapalua Club, a private, non-equity club program providing members special programs, access and other privileges at certain of the amenities within the Kapalua Resort. Deferred revenues from dues received from the private club membership program are recognized on a straight-line basis over year.

Deferred license fee revenue

The Company entered into a trademark license agreement with the owner of the Kapalua Plantation and Bay golf courses, effective April 1, 2020. Under the terms and conditions set forth in the agreement, the licensee is granted a perpetual, terminable on default, transferable, non-exclusive license to use the Company’s trademarks and service marks to promote its golf courses and to sell its licensed products. The Company received a single royalty payment of $

Escrowed deposits

The Company has $

11. INCOME TAXES

The Company uses a recognition threshold and measurement attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. The Company’s provision for income taxes is calculated using the liability method. Deferred income taxes are provided for all temporary differences between the financial statement and income tax basis of assets and liabilities using tax rates enacted by law or regulation. A full valuation allowance was established for deferred income tax assets as of March 31, 2022 and December 31, 2021, respectively.

12. REPORTABLE OPERATING SEGMENTS

The Company’s reportable operating segments are comprised of the discrete business units whose operating results are regularly reviewed by the Company’s Chief Executive Officer – its chief decision maker – in assessing performance and determining the allocation of resources. Reportable operating segments are as follows:

| • | Real Estate includes the planning, entitlement, development and sale of real estate inventory. |

| • | Leasing includes revenues and expenses from real property leasing activities, license fees and royalties for the use of certain of the Company’s trademarks and brand names by third parties, and the cost of maintaining the Company’s real estate assets, including conservation activities. The operating segment also includes the management of ditch, reservoir and well systems that provide non-potable irrigation water to West and Upcountry Maui areas. |

| • | Resort Amenities include a membership program that provides certain benefits and privileges within the Kapalua Resort for its members. |

The Company’s reportable operating segment results are measured based on operating income (loss), exclusive of interest, depreciation, general and administrative, share-based compensation, pension and other postretirement expenses.

Reportable operating segment revenues and income for the three months ended March 31, 2022 and 2021 were as follows:

|

Three Months Ended March 31, (unaudited) | ||||||||

| 2022 | 2021 | |||||||

| (in thousands) | ||||||||

| Operating Segment Revenues | ||||||||

| Real estate | $ | $ | ||||||

| Leasing | ||||||||

| Resort amenities and other | ||||||||

| Total Operating Segment Revenues | $ | $ | ||||||

| Operating Segment Income (Loss) | ||||||||

| Real estate | $ | ( | ) | $ | ( | ) | ||

| Leasing | ||||||||

| Resort amenities and other | ( | ) | ( | ) | ||||

| Total Operating Segment Income | $ | $ | ||||||

13. LEASING ARRANGEMENTS

The Company leases land primarily to agriculture operators and space in commercial buildings, primarily to restaurant and retail tenants through 2048. These operating leases generally provide for minimum rents and, in some cases, licensing fees, percentage rents based on tenant revenues, and reimbursement of common area maintenance and other expenses. Certain leases allow the lessee an option to extend or terminate the agreement. There are no leases allowing a lessee an option to purchase the underlying asset. Total leasing income subject to ASC Topic 842 for the three months ended March 31, 2022 and 2021 were as follows:

| Three Months Ended March 31, (unaudited) | ||||||||

| 2022 | 2021 | |||||||

| (in thousands) | ||||||||

| Minimum rentals | $ | $ | ||||||

| Percentage rentals | ||||||||

| Licensing fees | ||||||||

| Other (primarily common area recoveries) | ||||||||

| Total | $ | $ | ||||||

14. DISCONTINUED OPERATIONS

In December 2019, the Company entered into an Asset Purchase Agreement to sell the Public Utilities Commission (“PUC”) regulated assets of Kapalua Water Company, Ltd. and Kapalua Waste Treatment Company, Ltd. located in the Kapalua Resort. The Company received net proceeds of approximately $

15. COMMITMENTS AND CONTINGENCIES

On December 31, 2018, the State of Hawaii Department of Health (“DOH”) issued a Notice and Finding of Violation and Order (“Order”) for alleged wastewater effluent violations related to the Company’s Upcountry Maui wastewater treatment facility. The facility was built in the 1960’s to serve approximately 200 single-family homes developed for workers in the Company’s former agricultural operations. The facility is made up of two 1.5-acre wastewater stabilization ponds and surrounding disposal leach fields. The Order includes, among other requirements, payment of a $

The DOH agreed to defer the Order without a hearing date while the Company continues working on a previously approved corrective action plan to resolve and remediate the facility’s wastewater effluent issues. Continued testing of wastewater effluent consistently returns results within the allowable ranges. No hearing date has been set as discussions with the DOH are still ongoing to address any other matters regarding the Order. At March, 31 2022 and December 31, 2021, approximately $

There are various other claims and legal actions pending against the Company. The resolution of these other matters is not expected to have a material adverse effect on the Company’s consolidated financial position or results of operations after consultation with legal counsel.

16. FAIR VALUE MEASUREMENTS

GAAP establishes a framework for measuring fair value, and requires certain disclosures about fair value measurements to enable the reader of the unaudited condensed consolidated interim financial statements to assess the inputs used to develop those measurements by establishing a hierarchy for ranking the quality and reliability of the information used to determine fair values. GAAP requires that financial assets and liabilities be classified and disclosed in one of the following three categories:

Level 1: Quoted market prices in active markets for identical assets or liabilities.

Level 2: Observable market based inputs or unobservable inputs that are corroborated by market data.

Level 3: Unobservable inputs that are not corroborated by market data.

The Company considers all cash on hand to be unrestricted cash for the purposes of the unaudited condensed consolidated balance sheets and unaudited condensed consolidated statements of cash flows. The fair value of receivables and payables approximate their carrying value due to the short-term nature of the instruments. The valuation is based on settlements of similar financial instruments all of which are short-term in nature and are generally settled at or near cost.

17. RECENT ACCOUNTING PRONOUNCEMENTS

In June 2016, the FASB issued ASU 2016-13 to update the methodology used to measure current expected credit losses (“CECL”). This ASU apples to financial assets measured at amortized cost, including loans, held-to-maturity debt securities, net investments in leases, and trade accounts receivable as well as certain off-balance sheet exposures, such as loan commitments. This ASU requires consideration of a broader range of reasonable and supportable information to explain credit loss estimates. The guidance must be adopted using a modified retrospective transition method through a cumulative-effect adjustment to retained earnings/(accumulated deficit) in the period of adoption. ASU 2019-10 was subsequently issued delaying the effective date to the first quarter of 2023. The Company is in the process of assessing the impact of the ASU on its consolidated financial statements.

In November 2021, the FASB issued ASU 2021-10 as an update of ASC Topic 832 to increase the transparency of government assistance received by a business entity, including disclosure of the types of transactions, the accounting for those transactions, and the effect of those transactions on its financial statements. The ASU is effective for annual periods beginning after December 15, 2021. The Company is currently evaluating the impact of the ASU on its consolidated financial statements and related disclosures.

Item 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of our unaudited condensed consolidated interim financial condition and results of operations should be read in conjunction with our annual audited consolidated financial statements and related notes included in our Annual Report on Form 10-K for the year ended December 31, 2021 and the unaudited condensed consolidated financial statements and related notes included in this Quarterly Report on Form 10-Q. The following discussion contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those expressed or implied by the forward-looking statements below. Factors that could cause or contribute to those differences in our actual results include, but are not limited to, those discussed below and those discussed elsewhere within this Quarterly Report, particularly in the section entitled “Cautionary Note Regarding Forward-Looking Statements.” Depending upon the context, the terms the “Company,” “we,” “our,” and “us,” refer to either Maui Land & Pineapple Company, Inc. alone, or to Maui Land & Pineapple Company, Inc. and its subsidiaries collectively.

Overview

Maui Land & Pineapple Company, Inc. is a Hawaii corporation and the successor to a business organized in 1909. The Company consists of a landholding and operating parent company, its principal subsidiary, Kapalua Land Company, Ltd. and certain other subsidiaries of the Company.

We own approximately 23,000 acres of land on the island of Maui, Hawaii and develop, sell, and manage residential, resort, commercial, agricultural and industrial real estate through the following business segments:

| • |

Real Estate—Our real estate operations consist of land planning and entitlement, development and sales activities. |

| • |

Leasing—Our leasing operations include commercial, agricultural and industrial land and property leases, licensing of our registered trademarks and trade names, management of ditch, reservoir, and well systems that provide potable and non-potable water in West and Upcountry Maui, and the stewardship of conservation areas. |

| • |

Resort Amenities—We manage the operations of the Kapalua Club, a private, non-equity club program providing our members special programs, access and other privileges at certain amenities at the Kapalua Resort. |

We continue to monitor the effects of the COVID-19 pandemic on us, our customers, and our vendors. While we are not able to accurately predict the magnitude or scope of such impacts at this time, should the existence of the COVID-19 pandemic continue for an extended period, our future business operations, including the results of operations, cash flows and financial position will be significantly affected. Appropriate remote work arrangements continue to be established for our employees in order to maintain our financial reporting systems.

Results of Operations

Three Months Ended March 31, 2022 compared to Three Months Ended March 31, 2021

CONSOLIDATED

| Three Months Ended March 31, (unaudited) |

||||||||

| 2022 |

2021 |

|||||||

| (in thousands) |

||||||||

| Operating revenues |

$ | 2,248 | $ | 2,059 | ||||

| Segment operating costs and expenses |

(1,341 | ) | (1,349 | ) | ||||

| General and administrative |

(756 | ) | (719 | ) | ||||

| Share-based compensation |

(379 | ) | (349 | ) | ||||

| Depreciation |

(274 | ) | (300 | ) | ||||

| Operating loss |

(502 | ) | (658 | ) | ||||

| Other income |

- | 13 | ||||||

| Pension and other postretirement expenses |

(114 | ) | (116 | ) | ||||

| Interest expense |

(2 | ) | (33 | ) | ||||

| Loss from Continuing Operations |

(618 | ) | (794 | ) | ||||

| Loss from Discontinued Operations |

- | (140 | ) | |||||

| Net loss |

$ | (618 | ) | $ | (934 | ) | ||

| Loss from Continuing Operations per Common Share |

$ | (0.03 | ) | $ | (0.04 | ) | ||

| Loss from Discontinuing Operations per Common Share |

$ | - | $ | (0.01 | ) | |||

| Net loss per Common Share |

$ | (0.03 | ) | $ | (0.05 | ) | ||

REAL ESTATE

| Three Months Ended March 31, (unaudited) |

||||||||

| 2022 |

2021 |

|||||||

| (in thousands) |

||||||||

| Operating revenues |

$ | - | $ | - | ||||

| Operating costs and expenses |

(90 | ) | (97 | ) | ||||

| Operating loss |

$ | (90 | ) | $ | (97 | ) | ||

There were no sales of real estate for the three months ended March 31, 2022 and March 31, 2021, respectively.

There were no significant real estate development expenditures in the first three months of 2022 and 2021, respectively.

Real estate development and sales are cyclical and depend on a number of factors. Results for one period are therefore not necessarily indicative of future performance trends in this business segment. Uncertainties associated with COVID-19 may, among other things, reduce demand for real estate and impair prospective purchasers’ ability to obtain financing, which would adversely affect revenues from our real estate operations in future periods.

LEASING

| Three Months Ended March 31, (unaudited) |

||||||||

| 2022 |

2021 |

|||||||

| (in thousands) |

||||||||

| Operating revenues |

$ | 2,031 | $ | 1,801 | ||||

| Operating costs and expenses |

(741 | ) | (840 | ) | ||||

| Operating income |

$ | 1,290 | $ | 961 | ||||

The continued easing of travel restrictions and social distancing guidelines by state and local authorities have contributed to higher passenger volume to the island of Maui during the three months ended March 31, 2022 as compared to the three months ended March 31, 2021. As a result of increased visitor traffic, we collected higher leasing income from our commercial leasing portfolio. Certain leasing income is contingent upon tenant sales exceeding a defined threshold and is recognized as a percentage of sales after those thresholds are achieved. Recognized percentage leasing income was $394,000 and $117,000 for the three months ended March 31, 2022 and 2021, respectively.

The impact of COVID-19 during the three months ended March 31, 2021 adversely affected our tenants’ sales activity and ability to pay rent. Additional reserves of $60,000 were recorded as of March 31, 2021. No provision for doubtful accounts were recorded for the three months ended March 31, 2022.

Our leasing operations face competition from other property owners in Maui and Hawaii.

RESORT AMENITIES AND OTHER

| Three Months Ended March 31, (unaudited) |

||||||||

| 2022 |

2021 |

|||||||

| (in thousands) |

||||||||

| Operating revenues |

$ | 217 | $ | 258 | ||||

| Operating costs and expenses |

(510 | ) | (412 | ) | ||||

| Operating loss |

$ | (293 | ) | $ | (154 | ) | ||

Our Resort Amenities segment includes the operations of the Kapalua Club, a private, non-equity club providing its members special programs, access and other privileges at certain of the amenities at the Kapalua Resort, including a 30,000 square foot full-service spa and a private pool-side dining beach club. The Kapalua Club does not operate any resort amenities and the member dues collected are primarily used to pay contracted fees to provide access for its members to the spa, beach club, golf courses, and other resort amenities.

The decrease in operating revenues was primarily due to lower membership levels for the three months ended March 31, 2022, compared to the three months ended March 31, 2021.

The increase in operating costs and expenses for the three months ended March 31, 2022, compared to the three months ended March 31, 2021, was primarily due to higher golf course fees charged to the Company.

LIQUIDITY AND CAPITAL RESOURCES

Liquidity

We had cash on hand of $5.8 million and $5.6 million at March 31, 2022 and December 31, 2021, respectively.

At March 31, 2022, the entire $15.0 million revolving Credit Facility was available for borrowing. The Credit Facility, which matures on December 31, 2025, provides for revolving or term loan borrowing options. Interest on revolving loan borrowing is calculated based on the Bank’s prime rate minus 1.125 percentage points. Interest on term loan borrowing is fixed at the Bank’s commercial loan rates with interest rate swap options available. We have pledged approximately 30,000 square feet of commercial leased space in the Kapalua Resort as security for the Credit Facility. Net proceeds from the sale of any collateral are required to be repaid toward outstanding borrowings and will permanently reduce the Credit Facility’s revolving commitment amount. There are no commitment fees on the unused portion of the Credit Facility.

The terms of the Credit Facility include various representations, warranties, affirmative, negative and financial covenants and events of default customary for financings of this type. Financial covenants include a minimum liquidity (as defined) of $2.0 million, a maximum of $45.0 million in total liabilities, and a limitation on new indebtedness.

As of March 31, 2022, we believe we were in compliance with the covenants under the Credit Facility. If economic conditions are negatively impacted by the COVID-19 pandemic in future periods, we expect to borrow under our Credit Facility.

Cash Flows

Net cash flow provided by our operating activities was $2.8 million for the three months ended March 31, 2022. There were no interest payments due for the three months ended March 31, 2022.

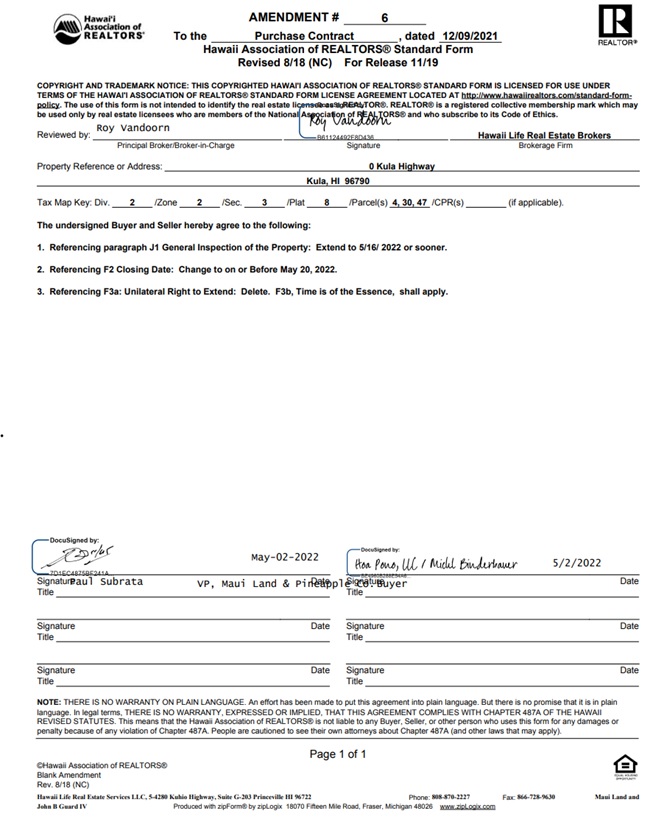

In December 2021, the Company entered into an agreement to sell the Kapalua Central Resort project for $40.0 million. On May 5, 2022, terms of the agreement were amended to extend the diligence period to May 19, 2022 and extend the closing date to two weeks following the expiration of the diligence period. The buyer transferred a non-refundable deposit of $300,000 into escrow on March 31, 2022.

In February 2022, we entered into an agreement to sell a 646-acre parcel located in Upcountry Maui for $9.7 million. Terms of the agreement, subsequently amended in May 2022, include a diligence period ending on May 16, 2022 and a closing date no later than May 20, 2022. A $2.0 million deposit is currently held in escrow.

No contributions are required to be made to our defined benefit pension plan in 2022. During the three months ended March 31, 2021, we made a minimum funding contribution of $553,000 to the plan.

Future Cash Inflows and Outflows

Our business initiatives include investing in our operating infrastructure, continued planning and entitlement efforts on our development projects. This may require borrowing under our Credit Facility or other indebtedness, repayment of which may be dependent on selling of our real estate assets at acceptable prices in condensed timeframes.

Our indebtedness could have the effect of, among other things, increasing our exposure to general adverse economic and industry conditions, limiting our flexibility in planning for, or reacting to, changes in our business and industry, and limiting our ability to borrow additional funds.

Critical Accounting Policies and Estimates

The preparation of the unaudited condensed consolidated interim financial statements in conformity with accounting principles generally accepted in the United States of America requires the use of accounting estimates. Changes in these estimates and assumptions are considered reasonably possible and may have a material effect on the unaudited condensed consolidated interim financial statements and thus actual results could differ from the amounts reported and disclosed herein. Our critical accounting policies that require the use of estimates and assumptions were discussed in detail in our 2021 Annual Report. There have been no significant changes in our critical accounting policies during the three months ended March 31, 2022.

Item 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

We have no material exposure to changes in interest rates related to our borrowing and investing activities used to maintain liquidity and to fund business operations. We have no material exposure to foreign currency risks.

We are subject to potential changes in consumer behavior and regulatory risks through travel and social distancing restrictions due to our location as a vacation destination. Potential deferrals and abatements of tenant lease rents may impact our base and percentage rental income.

Item 4. CONTROLS AND PROCEDURES

Evaluation of Disclosure Controls and Procedures

We maintain disclosure controls and procedures (as such term is defined in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934, as amended) that are designed to ensure that information required to be disclosed in our Exchange Act reports is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms, and that such information is accumulated and communicated to our management, including our Principal Executive Officer and Principal Financial Officer, as appropriate, to allow timely decisions regarding required disclosure.

In designing and evaluating the disclosure controls and procedures, our management recognizes that any controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving the desired control objectives, and our management necessarily was required to apply its judgment in evaluating the cost-benefit relationship of possible controls and procedures.

As required by Rules 13a-15(b) and 15d-15(b) under the Exchange Act, we carried out an evaluation, under the supervision and with the participation of our management, including our Chief Executive Officer and Chief Financial Officer, of the effectiveness of the design and operation of our disclosure controls and procedures as of the end of the fiscal quarter covered by this report. Based upon the foregoing, our Principal Executive Officer and Principal Financial Officer concluded that our disclosure controls and procedures were effective to provide reasonable assurance that information required to be disclosed by us in our Exchange Act reports is recorded, processed, summarized and reported within the time periods specified in applicable SEC rules and forms.

Changes in Internal Controls Over Financial Reporting

There have been no significant changes in our internal controls over financial reporting (as such term is defined in Exchange Act Rule 13a-15(f) or 15d-15(f)) during the three months ended March 31, 2022.

For information related to Item 1. Legal Proceedings, refer to Note 15, Commitments and Contingencies, to our condensed consolidated financial statements included herein.

Potential risks and uncertainties include, among other things, those factors discussed in the sections entitled “Business,” “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our 2021 Annual Report and the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Quarterly Report on Form 10-Q. Readers should carefully review those risks and the risks and uncertainties disclosed in other documents we file from time to time with the SEC. We undertake no obligation to publicly release the results of any revisions to any forward-looking statements to reflect anticipated or unanticipated events or circumstances occurring after the date of such statements. During the three months ended March 31, 2022, there were no material changes to the risks and uncertainties described in Part I, Item 1A, “Risk Factors,” of our Annual Report on Form 10-K for the year ended December 31, 2021.

| * |

Filed herewith |

| ** |

The certifications attached as Exhibit 32.1 and 32.2 accompany this Quarterly Report on Form 10-Q pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, shall not be deemed “filed” by the registrant for purposes of Section 18 of the Exchange Act, and shall not be incorporated by reference into any of the registrant’s filings under the Securities Act or the Exchange Act, whether made before or after the date of this Quarterly Report, irrespective of any general incorporation language contained in any such filing. |

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

| MAUI LAND & PINEAPPLE COMPANY, INC. |

||

| May 10, 2022 |

/s/ Wade K. Kodama |

|

| Date |

Wade K. Kodama |

|

| Chief Financial Officer |

||

| (Principal Financial Officer) |

| 3.2* | Amended By-Laws of Maui Land & Pineapple Company, Inc. (as of April 22, 2013). |

| 10.1* |

Amendment No. 1 to Purchase and Sale Agreement and Escrow Instructions, by and between the Maui Land & Pineapple Company, Inc. and Fakhry LLC, dated March, 29, 2022. |

| 10.2* |

Amendment No. 6 to the Purchase Contract and Counter Offer, by and among Maui Land & Pineapple Company, Inc., Mr. Michl Binderbauer, and Mr. Hong, Liang, dated May 2, 2022. |

| 10.3* |

Amendment No. 2 to Purchase and Sale Agreement and Escrow Instructions, by and between Maui Land & Pineapple Company, Inc. and Fakhry LLC, dated May, 5, 2022. |

| 31.1* |

Certification of Principal Executive Officer pursuant to Rule 13a-14(a) under the Securities Exchange Act of 1934, adopted pursuant to Section 302 of the Sarbanes-Oxley Act of 2002, as amended. |

| 31.2* |

Certification of Principal Financial Officer pursuant to Rule 13a-14(a) under the Securities Exchange Act of 1934, adopted pursuant to Section 302 of the Sarbanes-Oxley Act of 2002, as amended. |

| 32.1** |

Certification of Principal Executive Officer pursuant to 18 U.S.C. Section 1350, adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, as amended. |

| 32.2** |

Certification of Principal Financial Officer pursuant to18 U.S.C. Section 1350, adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, as amended. |

| 101.INS* |

Inline XBRL Instance Document |

| 101.SCH* |

Inline XBRL Taxonomy Extension Schema Document |

| 101.CAL* |

Inline XBRL Taxonomy Extension Calculation Document |

| 101.DEF* |

Inline XBRL Taxonomy Extension Definition Linkbase |

| 101.LAB* |

Inline XBRL Taxonomy Extension Labels Linkbase Document |

| 101.PRE* |

Inline XBRL Taxonomy Extension Presentation Link Document |

| 104* |

Cover Page Interactive Data File (formatted as Inline XBRL and contained in Exhibit 101 |

| * |

Filed herewith |

| ** |

The certifications attached as Exhibit 32.1 and 32.2 accompany this Quarterly Report on Form 10-Q pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, shall not be deemed “filed” by the registrant for purposes of Section 18 of the Exchange Act, and shall not be incorporated by reference into any of the registrant’s filings under the Securities Act or the Exchange Act, whether made before or after the date of this Quarterly Report, irrespective of any general incorporation language contained in any such filing. |

Exhibit 3.2

AMENDED BYLAWS

OF

MAUI LAND & PINEAPPLE COMPANY, INC.

(AS OF APRIL 22, 2013)

ARTICLE I

PRINCIPAL OFFICE; SEAL

SECTION 1. Principal Office. The principal office of the Company shall be in Kahului, Maui, Hawaii; there may be such subordinate or branch offices in such place or places within Hawaii or elsewhere as may be considered necessary or requisite by the Board of Directors to transact the business of the corporation, such subordinate or branch offices to be in charge of such person or persons as may be appointed by the Board of Directors.

SECTION 2. Seal. The corporation shall have a corporate seal (and one or more duplicates thereof) of such form and device as the Board of Directors shall determine.

ARTICLE II

STOCKHOLDERS

SECTION 1. Annual Meetings. The annual meeting of the stockholders of the corporation shall be held on such day during the first six months following the end of the fiscal year of the corporation or calendar year if the same be used as the accounting period of the corporation as the Board of Directors or the President may determine. The annual meeting shall be a general meeting and at such meeting any business within the powers of the corporation may be transacted without special notice of such business, except as may be required by law, by the Articles of Association, or by these Bylaws (including without limitation Section 7 of this Article II). To the extent permitted by law, meetings of stockholders may be held at such place within or without the State of Hawaii.

SECTION 2. Special Meetings. Special meetings of the stockholders may be held at any time. Such meetings shall be held upon the call of the President or of any two directors or of the holders of not less than one-fourth of the capital stock of the Company issued and outstanding and entitled to vote at such special meeting. At any special meeting, only such business shall be transacted as is specified in the notice given of such meeting.

SECTION 3. Notices of Meetings. Notices of every meeting of stockholders, whether annual or special, shall state the place, day and hour of the meeting, whether it is annual or special, and in the case of any meeting shall state briefly the business proposed to be transacted thereat. Such notice shall be given by mailing a written or printed copy thereof, postage prepaid, in the case of an annual meeting at least twenty days before the date assigned for the meeting, and in the case of a special meeting at least twenty days before the date assigned for the meeting, to each stockholder entitled to vote at such meeting at his address as it appears on the transfer books of the corporation. Upon notice being given in accordance with the provisions hereof, the failure of any stockholder to receive actual notice of any meeting shall not in any way invalidate the meeting or the proceedings thereat.

SECTION 4. Quorum. At all meetings of stockholders the presence in person or by proxy of stockholders owning a majority of all of the shares of stock issued and outstanding and entitled to vote at said meeting shall constitute a quorum, and the action of the holders of a majority of the shares of stock present or represented at any meeting at which a quorum is present shall be valid and binding upon the corporation and its stockholders, except as otherwise provided by law, by the Articles of Association or by these Bylaws. Once a quorum is established at a meeting, it shall not be broken by the absence or withdrawal of one or more stockholders before the meeting is adjourned.

SECTION 5. Voting, Proxies.

(a) At any meeting of the stockholders, each stockholder, except where otherwise provided by the clauses and terms applicable to the stock held by such stockholder, shall be entitled to vote in person or by proxy and shall have one vote for each share of voting stock registered in his name at the close of business on the day preceding the date of such meeting or on such record date as may be fixed by the Board of Directors. In the case of an adjourned meeting, unless otherwise provided by the Board of Directors, the record date for the purpose of voting at such adjourned meeting shall be the day preceding the date of the adjourned meeting. When voting stock is transferred into the name of a pledgee under a pledge agreement, the pledgor shall have the right to vote such stock unless prior to the meeting the pledgee or his authorized representative shall file with the Secretary written authorization from the pledgor authorizing such pledgee to vote such stock. An executor, administrator, guardian or trustee may vote stock of the corporation held by him in such capacity at all meetings, in person or by proxy, whether or not such stock shall have been transferred into his name on the books of the corporation, but if such stock shall not have been so transferred he shall, if requested as a prerequisite to so voting, file with the Secretary a certified copy of his letters of appointment as such executor, administrator or guardian, or evidence of his appointment or authority as such trustee. If there be two or more executors, administrators, guardians or trustees, all or a majority of them may vote the stock in person or by proxy. Stock held in the names of two or more persons as tenants in common or joint tenants may be voted by any one of them unless protested by the other or others. The survivor(s) of a joint tenancy or tenants by the entirety may vote such stock without the necessity of indicating such survivorship.

(b) The instrument appointing a proxy shall be in writing, signed by the appointer or his duly authorized agent in handwriting or by rubber stamp, and filed with the Secretary. A proxy that is regular on its face and apparently executed by the stockholder entitled to vote (including a proxy with an illegible signature) shall be presumed to be authentic and genuine, unless the corporation shall receive evidence to the contrary. Proxies for stock owned by two or more persons named as tenants in common or as joint tenants shall be valid if signed by one or two persons. Proxies for stock in the name of corporations, partnerships, nominees or brokers shall be valid if signed with the name of the corporation, partnership, nominee or broker, either in handwriting or by rubber stamp and without requiring the signature of an officer or agent. Minor variations between signatures and the name of the appointer as it appears upon the stock books of the corporation or, in the case of a corporation, failure to affix the corporate seal, shall not invalidate the proxy. If a proxy is appointed by cable, telegram, telex, radiogram or other electronic message, the typewritten signature of the appointer shall be sufficient for a valid proxy. A proxy executed by a third party as agent or attorney-in-fact for a stockholder shall be presumed valid unless the corporation should receive evidence to the contrary. A proxy executed by a married woman shall be presumed to be authentic and genuine if the corporation's record of stock ownership shows such stock in her maiden name and if there is a connecting feature in the execution and signature. Unless expressly limited by its terms, every instrument appointing a proxy shall continue in full force and effect until a written revocation thereof shall be filed with the Secretary.

(c) Stockholders shall have no right to elect directors by cumulative voting.

SECTION 6. Adjournment. Any meeting of stockholders, whether annual or special, and whether a quorum be present or not, may be adjourned from time to time by the Chairman thereof with the consent of the holders of a majority of all of the shares of stock present or represented at such meeting and entitled to vote thereat without notice other than the announcement at such meeting. At any such adjourned meeting at which a quorum shall be present, any business may be transacted that might have been transacted at the original meeting as originally called and noticed.

SECTION 7. Action at Meetings of Stockholders. No business may be transacted at an annual meeting of stockholders other than business that is either (a) specified in the notice of meeting (or any supplement thereto) given by or at the direction of the Board of Directors; (b) otherwise properly brought before the annual meeting by or at the direction of the Board of Directors; or (c) otherwise properly brought before the annual meeting by any stockholder of the corporation (i) who is a stockholder of record on the date of the giving of the notice provided for in this Section 7 and on the record date for the determination of stockholders entitled to vote at such annual meeting and (ii) who complies with the notice procedures set forth in this Section 7.

In addition to any other applicable requirements for business properly to be brought before an annual meeting by a stockholder, such stockholder must have given timely notice thereof in proper written form to the Chairman of the Board, if any, the President or the Secretary of the corporation.

To be timely, a stockholder's notice must be delivered to or mailed and received at the principal executive offices of the corporation not less than ninety (90) days nor more than one hundred twenty (120) days prior to the anniversary date of the immediately preceding annual meeting of stockholders; provided, however, that in the event that the annual meeting is called for a date that is not within thirty (30) days before or after such anniversary date, notice by the stockholder in order to be timely must be so received not later than the close of business on the tenth (10th) day following the day on which the notice of the annual meeting is first mailed by the corporation or on which the corporation makes public disclosure of the date of the annual meeting, whichever first occurs; and provided further that, in the case of the 1999 annual meeting of stockholders, any such notice shall be timely if received by the close of business on the later of (i) the tenth (10th) day following the date on which the corporation's proxy statement for the 1999 annual meeting is first mailed to stockholders or (ii) April 12, 1999.

To be in proper written form, a stockholder's notice must set forth as to each matter such stockholder proposes to bring before the annual meeting (i) a brief description of the business desired to be brought before the annual meeting and the reasons for conducting such business at the annual meeting, (ii) the name and record address of such stockholder, (iii) the class or series and number of shares of capital stock of the corporation that are owned by such stockholder (x) beneficially and (y) of record, (iv) a description of all arrangements or understandings between such stockholder and any other person or persons (including their names) in connection with the proposal of such business by such stockholder and any material interest of such stockholder in such business and (v) a representation that such stockholder intends to appear in person or by proxy at the annual meeting to bring such business before the meeting.

No business shall be conducted at the annual meeting of stockholders except business brought before the annual meeting in accordance with the procedures set forth in this Section 7, provided, however, that once business has been brought properly before the annual meeting in accordance with such procedures, nothing in this Section 7 shall be deemed to preclude discussion by any stockholder of any such business.

The business transacted at any special meeting of stockholders shall be confined to the business stated in the notice of meeting.

Notwithstanding the foregoing provisions of this Section 7, a stockholder also shall comply with all applicable requirements of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), and the rules and regulations promulgated thereunder, with respect to the matters set forth in this Section 7. Nothing in this Section 7 shall be deemed to affect any rights of stockholders to request inclusion of proposals in the corporation's proxy statement pursuant to Rule 14a-8 under the Exchange Act.

ARTICLE III

BOARD OF DIRECTORS

SECTION 1. Number and Term of Office; Qualifications.

(a) The Board of Directors shall consist of five (5) members. Each director shall hold office until the next annual meeting and thereafter until his successor is duly elected or appointed and qualified.

(b) To the extent required by law, not less than one member of the Board of Directors shall be a resident of the State of Hawaii. Whenever for any reason not less than one member of the Board of Directors is a resident of the State of Hawaii, the Board shall have no power to act in any manner, except the power to act under Section 6 of this Article to have at least one member as a resident of the State of Hawaii.

(c) The Board of Directors may, at any meeting, appoint one or more "Directors Emeritus" in recognition of the past contributions of such persons or their spouses to the corporation or for other appropriate reasons. A Director Emeritus will be eligible to attend all meetings of the Board of Directors, to have his or her expenses paid and to receive meeting fees (though not any annual retainer), but shall not be eligible to vote and shall not be counted as part of the quorum at any such meeting.

(d) Only persons who are nominated in accordance with the following procedures shall be eligible for election as directors of the corporation. Nominations of persons for election to the Board of Directors may be made at any annual meeting of stockholders or at any special meeting of stockholders called for the purpose of electing directors (a) by or on behalf of the Board of Directors or (b) by any stockholder of the corporation (i) who is a stockholder of record on the date of the giving of the notice provided for in this Section 1(d) and on the record date for the determination of stockholders entitled to vote at such meeting and (ii) who complies with the notice procedures set forth in this Section 1(d).

In addition to any other applicable requirements for a nomination to be made by a stockholder, such stockholder must have given timely notice thereof in proper written form to the Chairman of the Board, if any, the President or the Secretary of the corporation.

To be timely, a stockholder's notice must be delivered to or mailed and received at the principal executive offices of the corporation (i) in the case of an annual meeting, not less than ninety (90) days nor more than one hundred twenty (120) days prior to the anniversary date of the immediately preceding annual meeting of stockholders, provided, however, that in the event the annual meeting is called for a date that is not within thirty (30) days before or after such anniversary date, notice by the stockholder in order to be timely must be so received not later than the close of business on the tenth (10th) day following the day on which the notice of the annual meeting is first mailed by the corporation or on which the corporation makes public disclosure of the date of the annual meeting, whichever first occurs; and (ii) in the case of a special meeting of stockholders called for the purpose of electing directors, not later than the close of business on the tenth (10th) day following the day on which a notice of the date of the special meeting is first mailed by the corporation or on which the corporation makes public disclosure of the date of the special meeting, whichever first occurs. Notwithstanding the preceding sentence, a stockholder's notice concerning nominations of directors to be elected at the 1999 annual meeting shall be timely if received by the close of business on the later of (i) the tenth day following the date on which the corporation's proxy statement for the 1999 annual meeting is first mailed to stockholders or (ii) April 12, 1999.

To be in proper written form, a stockholder's notice must set forth (i) as to each person whom the stockholder proposes to nominate for election as a director (a) the name, age, business address and residence address of the person, (b) the principal occupation or employment of the person, (c) the class or series and number of shares of capital stock of the corporation that are owned by the person (x) beneficially and (y) of record, and (d) any other information relating to the person that would be required to be disclosed in a proxy statement or other filings required to be made in connection with solicitations of proxies for election of directors pursuant to Section 14 of the Exchange Act and the rules and regulations promulgated thereunder; and (ii) as to the stockholder giving the notice (a) the name and record address of such stockholder, (b) the class or series and number of shares of capital stock of the corporation that are owned by such stockholder (x) beneficially and (y) of record, (c) a description of all arrangements or understandings between such stockholder and each proposed nominee and any other person or persons (including their names) pursuant to which the nomination(s) are to be made by such stockholder, (d) a representation that such stockholder intends to appear in person or by proxy at the meeting to nominate the persons named in its notice and (e) any other information relating to such stockholder that would be required to be disclosed in a proxy statement or other filings required to be made in connection with solicitations of proxies for election of directors pursuant to Section 14 of the Exchange Act and the rules and regulations promulgated thereunder. Such notice must be accompanied by a written consent of each proposed nominee to being named as a nominee and to serve as a director if elected.

No person shall be eligible for election as a director of the corporation unless nominated in accordance with the procedures set forth in this Section 1(d), and unless such person satisfies (if applicable) the requirements of Section 1(e) of this Article III.

(e) No person shall be eligible for election as a director if his or her election would cause the Company to have insufficient "independent directors" within the meaning of Section 121 of the Company Guide of the American Stock Exchange (or any successor provision) to meet the requirements of that Section (or any successor provision).

SECTION 2. Removal of Directors. Any director may be removed from office with or without cause at any time and another person may be elected in his place to serve for the remainder of his term at any special meeting of stockholders called for that purpose by the affirmative vote of the holders of a majority of all of the shares of capital stock of the corporation outstanding and entitled to vote. In case any vacancy so created shall not be filled by the stockholders at such meeting, such vacancy shall be filled by the Board of Directors.

SECTION 3. Chairman. The Board may appoint from among its members a Chairman who shall preside at all meetings and serve during the pleasure of the Board.

SECTION 4. Registration, Meetings, Notice.

(a) Each director shall, upon election to such office, register with the corporation his mailing address.

(b) The Board of Directors shall, without any notice being given, hold a meeting for the purpose of organization as soon as may be practicable after each annual meeting of stockholders.

(c) The Board of Directors may in its discretion schedule regular meetings of the Board to be held at a stated time and place and no notice, written or otherwise, of such meeting shall be required. The Board of Directors may in its discretion alter the time and place for such regular meetings from time to time.

(d) Special meetings of the Board of Directors may be called by the Chairman of the Board of Directors or, in the absence of the Chairman or if no Chairman shall have been appointed, at the call of the President and, in any case, at the call of any two directors.

(e) The Secretary shall give notice of every special meeting of the Board of Directors orally or by cabling or delivering a copy of the same to each director at his registered mailing address not less than forty-eight hours prior to any such meeting. Such notice shall constitute full legal notice of any special meeting, whether actually received or not and whether any director concerned resides in Honolulu or not. No special meeting and no business transacted at any such meeting shall be invalidated or in any way affected by the failure of any director to receive actual notice of any such meeting.

(f) Any director may expressly, in writing or otherwise, waive notice of any meeting. At any meeting, the presence of a director shall be equivalent to the waiver of the giving of notice of said meeting to said director.

(g) To the extent permitted by law, any action required or permitted to be taken at any meeting of the directors or of a committee of the directors may be taken without a meeting if all of the directors or all of the members of the committee, as the case may be, sign a written consent or written consents setting forth the action taken or to be taken at any time before or after the intended effective date of such action. Such consent or consents shall be filed with the minutes of directors' meetings or committee meetings, as the case may be, and shall have the same effect as a unanimous vote.

(h) To the extent permitted by law, members of the Board of Directors or of a committee of the Board of Directors may participate in a meeting of such Board or committee by means of conference telephone or similar communications equipment by means of which all persons participating in the meeting can hear each other, and participating in a meeting pursuant to this section shall constitute presence in person at such meeting.

SECTION 5. Quorum, Adjournment. A majority of the Board of Directors shall constitute a quorum for the transaction of any business. Any act or business must receive the approval of a majority of such quorum unless otherwise provided by law, the Articles of Association or these Bylaws. A quorum, once established, shall not be broken by the absence or withdrawal of one or more directors before the meeting is adjourned. The Chairman or a majority of the directors present may adjourn the meeting from time to time without further notice.

SECTION 6. Permanent Vacancies. If any permanent vacancy shall occur in the Board of Directors through death, resignation, removal or other cause, the remaining director or directors, whether or not a majority of the whole Board, by the affirmative vote of a majority of the remaining director or directors, may elect a successor director to hold office for the unexpired portion of the term of the director whose place shall be vacant.

SECTION 7. Temporary Vacancies, Substitute Directors. If any temporary vacancy shall occur in the Board of Directors through the absence of any director from the State of Hawaii or the sickness or disability of any director, the remaining director or directors, whether constituting a majority or a minority of the whole Board, may by the affirmative vote of a majority of such remaining director or directors appoint some person as a substitute director who shall be a director during such absence, sickness or disability and until such director shall return to duty or the office of such director shall become permanently vacant. The determination of the Board of Directors, as shown on the minutes, of the fact of such absence, sickness or disability shall be conclusive as to all persons and to the corporation.

SECTION 8. Expenses and Fees. By resolution of the Board of Directors, expenses of attendance, if any, and a director's fee in such amount as the Board of Directors shall from time to time determine, may be allowed for attendance at each meeting of the Board and of each meeting of any committee created by the Board, provided that nothing herein contained shall be construed to preclude any director from serving the corporation in any other capacity and receiving compensation therefor.

SECTION 9. Executive Committee. The Board of Directors, by vote of a majority of the Board, may at its discretion appoint or elect an Executive Committee of not less than two members from its own number who shall have charge of the management of the business and affairs of the corporation in the interim between meetings of the Board of Directors and may exercise all powers of that body during such interim, but shall at all times be subject to any instructions issued by the Board of Directors. The Executive Committee may make its own rules of procedure. The Board of Directors, by vote of a majority of the Board, may at its discretion appoint or elect from its own number one or more alternate members of the Executive Committee who may be alternates for designated members of the Executive Committee or alternates at large or both. Any alternate member of the Executive Committee who is an alternate for a designated member shall be and act as a member of the Executive Committee at any meeting from which the designated member is absent and any alternate at large shall be and act as a member of the Committee at any meeting from which any member of the Committee for whom an alternate has not been designated may be absent.

Such Executive Committee shall make a report of its acts and transactions at the next meeting of the Board of Directors. Vacancies occurring in such Committee or among the alternates for members of such Committee may be filled only by vote of the majority of the Board of Directors, but shall only be filled by a director of the corporation. The acts of the majority of the Executive Committee of the Board shall be effective in all respects as the acts of such Committee and such Committee may act by a writing signed by all of its members, other than alternates, without a meeting being held.

SECTION 10. Audit Committee. The Chairman of the Board of Directors shall have the power, subject to confirmation by the affirmative vote of the majority of the whole Board, to appoint an Audit Committee of not less than three members, one of whom must be a member of the Board of Directors. The Audit Committee shall serve as an independent check on the reliability of the Company's financial controls and its financial reporting, and shall review the work of the independent auditors. The Audit Committee may make its own rules of procedure and shall report to the Board of Directors.